1 Introduction

Mean field games (MFG) theory has been introduced in [29, 32] (see [12, 15] for a comprehensive introduction) as a tool to study games with infinitely many agents and it is particularly suitable to model economic problems for market competition. While in the first formulation of the theory the influence of the mass of agents on the single player occurs only through the spatial distribution, a subsequent development, known as mean field games of controls, considers the case in which the agent also reacts to decisions, i.e. optimal controls, of the other agents (see [10, 14, 19, 30]). In this latter framework, a very interesting problem, first proposed in [26, 27] and then widely studied in literature, is the one known as Cournot mean field games of controls, a model for the production of an exhaustible resource by a continuum of producers.

To introduce the Cournot model, we start describing the control problem solved by the representative agent. The state variable represents the inventory level. The dynamics of the agent, a producer, is given by the reflected stochastic differential equation

|

|

|

(1) |

where is the local time at and is the control variable which gives the instantaneous rate of production. For , letting

the value function is

|

|

|

(2) |

where is the discount factor, is the price, , with , the production cost. Given the function which describes the distribution of the agents at time , assume that

-

•

In equilibrium, all agents are using the same policy, which we denote by , but they are heterogeneous in their inventories ;

-

•

Each agent is infinitesimally small, i.e. the producers influence the market price only through the average production ;

-

•

Each agent is a price taker, taking as given the price from its “belief”, hence the in Eq. 2 is only over .

Then, the Nash equilibria can be characterized by the MFG of controls system (cfr. [26, Proposition 3.1, p. 26]):

|

|

|

(3) |

where . is the price function. Eq. 3 (i) is the backward in time Hamilton-Jacobi-Bellman (HJB) equation characterizing the value function for a representative agent (producer) at time and inventory state ; (ii) is a forward in time Fokker-Planck-Kolmogorov equation (FPK) which governs the evolution of the probability distribution driven by the optimal control ; (iii) is a fixed point equation characterizing the optimal policy for the single producer at time and inventory level . Note that the coupling term in (i) depends not only on the distribution of the agents , but also on the optimal rate of production . This is a difficulty at the core of MFG of controls. The Cournot model in our paper has additional structure motivated by economic intuitions, making it more trackable than general MFG of controls.

Given the boundary conditions for and in the MFG system, the operator defining the FPK equation is the adjoint of the infinitesimal generator of the stochastic process Eq. 1, in the sense that,

|

|

|

(4) |

From (i) and (iii) in system (3), the equation for the optimal policy can be reformulated more explicitly as

|

|

|

(5) |

Therefore is characterized as a recursive competitive equilibrium.

Throughout the paper we will be also using the notation for the Hamiltonian:

|

|

|

(6) |

We denote the flux at and aggregate production at , respectively by:

|

|

|

(7) |

Following [26, 27], the price function is determined according to a rule of supply/demand equilibrium on the market, where the demand is given by a function , monotonically decreasing w.r.t. the -variable.

Hence for any aggregate production at time , designated by ,

|

|

|

(8) |

and we recall from (3) (i) and from Eq. 7 that

Two typical examples of demand and price functions are given by (see [27]):

|

|

|

(9) |

|

|

|

(10) |

In both of these examples, stands for a global wealth factor and for the growth of demand in the economy. In Eq. 9 the constant is exogenous and represents the price of a substitute. The demand in Eq. 10 satisfies constant elasticity of substitution (CES), where a high stands for a low price of substitution.

The model previously described was proposed in [26, 27] and discussed also in [15]. Theoretical analysis was developed in [21, 23, 24, 22, 25], but mainly in the case of a linear price function. Even though nonlinear price functions have been considered by some of these works, they had different economic interpretations and assumptions, see Remark 2.3 for more details. Numerical simulations of Cournot MFG of controls have been considered in [27] and then in [16] and [35].

To our knowledge, there has not been a complete analysis of the model in [26, 27] for nonlinear price functions. Under natural assumptions on , which in particular include the ones defined in Eqs. 9 and 10, we prove existence and uniqueness of the classical solution to system (3). Existence is obtained by proving the global convergence of the smoothed policy iteration (SPI) algorithm, an iterative learning procedure introduced in [37] for solving MFG systems. This method is similar to fictitious play (see [13] and [35]) as a learning algorithm, but the agent only evaluates a policy (which amounts to solving a linear problem) and then performs a greedy update. The convergence analysis of (SPI) for Cournot MFG of controls, even though highly based on the theoretical apparatus developed in [37], faces essential difficulties and contains differences due to the recursive characterization of the optimal policy, see (iii) in system (3). To our knowledge there has not been theoretical convergence analysis of iterative algorithms in this general setting for Cournot MFG of controls.

Dealing with the numerical resolution of MFG systems by finite difference method typically requires using some iterative algorithms, e.g. fixed point [3, 5], Newton method [2, 1], fictitious play [13, 28, 33, 35], policy iteration [8, 11, 34] or smoothed policy iteration [37]. See e.g. [4, 33] and the references therein for more details. In particular, [35] considered convergence rate of a fictitious play algorithm for solving an MFG of controls, similar to our Cournot model but with only linear price function and periodic boundary conditions. [3] considered numerical solution of a Cucker-Smale type MFG of controls with periodic or Neumann boundary conditions. Fictitious play type iterative computation has been considered in [18, 38] for one shot Cournot games with a finite number of agents. Based on a finite difference discretization of (SPI), we define an efficient numerical method for the resolution of system (3). While developing the numerical scheme, special attention is paid to preserving the adjoint structure of the MFG system and to the consistency of the flux boundary condition for the FPK equation.

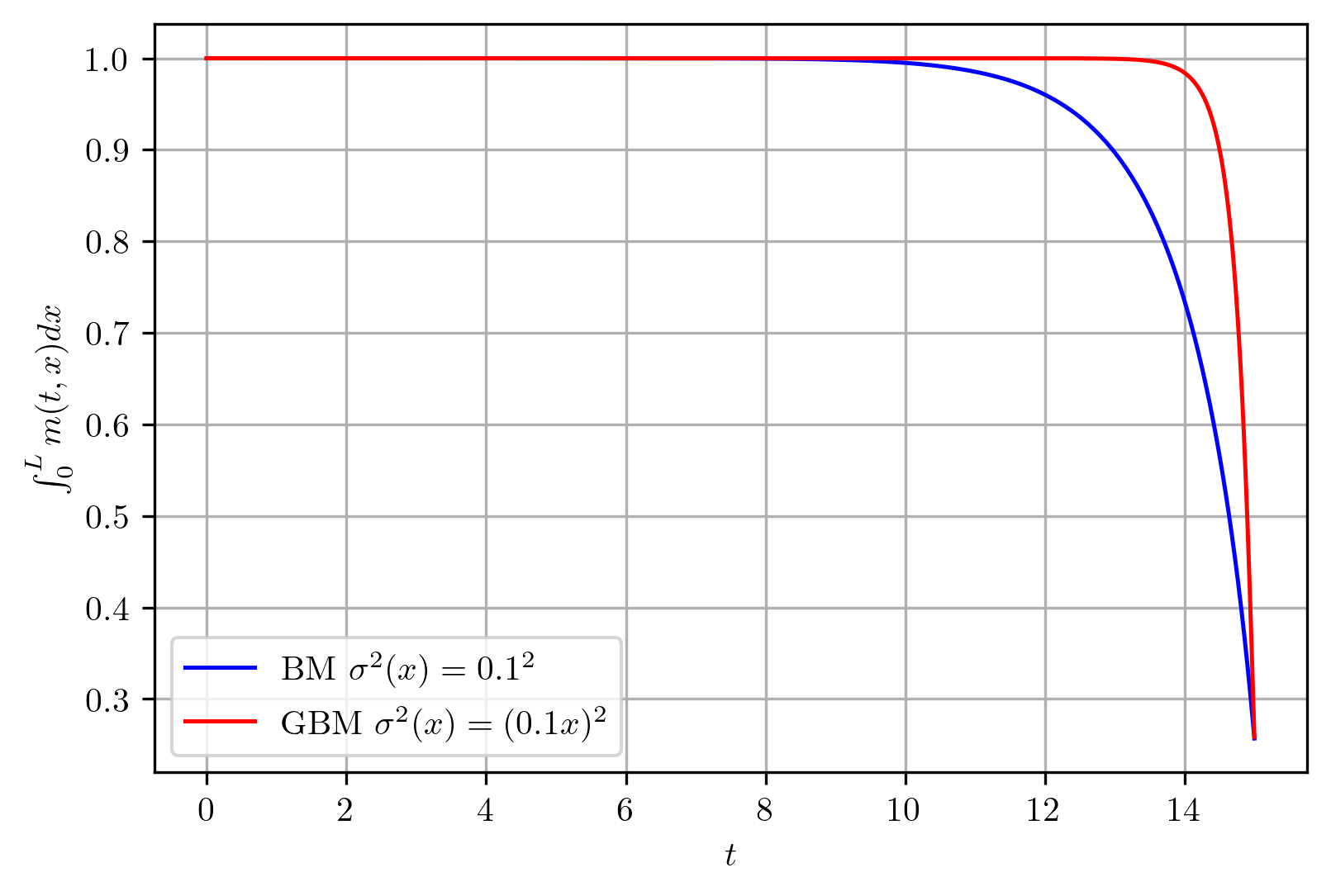

We observe that, in contrast to [27] where the Cournot MFG of controls was considered on the interval , we study the problem on the bounded interval and we impose a Neumann boundary condition for and the dual flux boundary condition for at . Moreover in [27], the dynamics of the agent is given by a geometric Brownian motion (GBM), hence the diffusion coefficient may degenerate at . We assume in the theoretical analysis. However, our numerical experiments show that the method performs well in models with GBM diffusions. We plan to consider the theoretical aspects of the degenerate diffusion in the future. We conclude observing that our analytical and numerical method can be extended to consider a wide range of competitive equilibrium models.

2 Assumptions and preliminary results

We first introduce some functional spaces. For any , and are the usual Lebesgue spaces. Given a Banach space , is the vector-valued Lebesgue spaces.

We denote with the space of all functions on , such that and the norm

|

|

|

is finite. The dual space of is denoted by . We denote by the space of functions such that are all in , endowed with the norm

|

|

|

We also denote by the Banach space of function such that the norm (cfr. [31] p.6)

|

|

|

Let be the space of continuous functions in and the space of functions in and once continuously differentiable w.r.t. . For , and denote the spaces of Hölder continuous functions in , endowed with the norms

|

|

|

(11) |

|

|

|

(12) |

|

|

|

(13) |

As we will make strong assumptions on the regularity of the initial and boundary conditions, we only need Sobolev spaces with . Throughout the paper we use for an arbitrary constant such that . It is know from [31, Corollary pp. 342-343] that

|

|

|

(14) |

We make the following standing assumptions:

Assumption 2.1.

We assume:

-

(A2.1.1)

is , , and .

-

(A2.1.2)

is and

|

|

|

-

(A2.1.3)

The price function is for both variables. for all . There exists , being for both variables, such that for all . Moreover, there exist , such that

|

|

|

-

(A2.1.4)

The viscosity coefficient is and non degenerate, i.e. .

We first consider some results related to the FPK equation with Robin boundary conditions (see [5, 7, 17] for related results). Given the initial-boundary value problem

|

|

|

(17) |

We give the following definition of weak solution (see [31, Chapter V, section 1]).

Definition 2.4.

A function is said to be a bounded weak solution to Eq. 17 if , and

|

|

|

for any and any function such that , , .

Lemma 2.5.

Suppose satisfies (A2.1.1) and .

Then, there exists a unique solution to Eq. 17 satisfying , . In addition, , for all .

Let , , be the solution to Eq. 17 corresponding to and set

. Then

|

|

|

where is a constant depending only on , , and .

Proof.

The existence and uniqueness of a weak solution

|

|

|

is standard from energy estimates (cfr. [11]). From [7, Proposition 2.2], there exists a constant which depends only on , , and such that

|

|

|

Therefore, is a bounded weak solution in the sense of Definition 2.4 and follows from [31, Chapter V, Theorem 1.1]. One can use duality method to show as in [20, Proposition 4.3], while in follows from (A2.1.1) and Harnack inequality (cf. [36, Theorem 6.27]) and [5, Proof of Theorem 2.2]. It is clear that satisfies

|

|

|

Then, by standard energy estimates (cfr. [11]), we obtain the result.

∎

Corollary 2.6.

Under the assumptions of Lemma 2.5, for all , .

Proof.

Since and for all , then . Integrating on the FPK equation

|

|

|

Using the boundary conditions , and , we obtain

|

|

|

We now consider some preliminary results for the MFG system (3). Define the space

|

|

|

(18) |

we call a triple a weak solution to the Cournot MFG of controls system (3) if (i) and (ii) are satisfied in the sense of distributions and (iii) is satisfied pointwise.

∎

Lemma 2.7.

Suppose is a weak solution to system (3). Then and

. In addition,

|

|

|

(19) |

|

|

|

(20) |

Proof.

It is clear from (A2.1.2) that for all . From the HJB equation in system (3) obviously

|

|

|

hence

|

|

|

The weak parabolic maximum principle implies that . Since for all we obtain for all . From Eq. 20, . Recall that is a convex function, hence the Hamiltonian

|

|

|

It follows from standard estimates for quasilinear parabolic equations, e.g. [31, Chapter 5, Theorem 6.3], that and . The derivative of w.r.t in the sense of distributions is

|

|

|

where denotes an indicator function. We can differentiate the HJB equation (3) (i), with being a weak solution to

|

|

|

From , it is clear that is bounded in . It is easy to see from (or by using energy estimates) that . From , and , we can use the parabolic maximum principle for weak solutions (cfr. [31, Chapter 3, Theorem 7.2, p. 188]) and obtain for all . From and Eq. 5 we obtain Eq. 19.

Next, we show Eq. 20 by a contradiction argument. Suppose at some time . Then from we have

|

|

|

With Eq. 5, we can then obtain for all . This implies

|

|

|

This is a contradiction as we have assumed for all in (A2.1.3).

∎

The following result is crucial for proving uniqueness of the solution to system (3) and convergence of learning algorithms. It is analogous to [13, Lemma 2.7] and [37, Lemma 2.8]. Here, since the admissible set of controls is compact( cf. Remark 2.9) we give a modified proof. The novelty in the proof is that we consider separately the case when the constraints on are binding.

Lemma 2.10.

Let ,

|

|

|

then for all such that ,

|

|

|

(21) |

Proof.

We have:

|

|

|

If , then , hence Eq. 21. If , then ,

|

|

|

If , then and , hence ,

|

|

|

Therefore,

|

|

|

∎

4 Learning algorithm and existence of the solution

We introduce the smoothed policy iteration algorithm ((SPI) in short), motivated by the algorithm (SPI1) introduced in [37]. As we have shown that system (3) has at most one solution in Theorem 3.1, we prove the global convergence of the algorithm and this shows the existence of solution to the system.

Given , iterate for each :

-

(i)

Generate the distribution from the smoothed policy. Solve

|

|

|

(26) |

-

(ii)

Price update. Set

|

|

|

(27) |

-

(iii)

Policy evaluation. Solve

|

|

|

(28) |

-

(iv)

Policy update.

|

|

|

(29) |

-

(v)

Policy smoothing

|

|

|

(30) |

Unless otherwise specified, we use the following learning rates for Eq. 30.

Assumption 4.1.

for all .

Step (v) policy smoothing Eq. 30 can be reformulated as

|

|

|

(31) |

To speed up the convergence, one puts increasingly larger weights on more recent observations of , cfr. [18, p. 191] and [37, Remark 3.1].

Lemma 4.3.

For each , there exists a unique solution , with

and with and ,

to the system Eq. 26-Eq. 28 such that

|

|

|

(32) |

where is independent of .

Proof.

From , we also have . Then Eq. 32 holds by using Lemma 2.5 and standard parabolic estimates.

∎

Lemma 4.4.

There exists a constant , such that for all ,

|

|

|

|

(33) |

|

|

|

|

Proof.

We denote

|

|

|

It is clear from Eqs. 29 and 30

|

|

|

(34) |

From

|

|

|

and Lemma 2.5, it follows that . Then it is easy to see from (A2.1.3)

|

|

|

From

|

|

|

|

(35) |

|

|

|

|

|

|

|

|

and Eq. 34, we get

from the standard parabolic estimates. Then, from Sobolev embedding Eq. 14, Eq. 11 and Eq. 12, we obtain . From Eq. 29,

|

|

|

|

|

|

|

|

∎

The following Lemma plays a pivotal role in the convergence analysis of Fictitious Play for mean field games. Its proof can be found in [13, Lemma 2.7].

Lemma 4.5.

Consider a sequence of positive real numbers such that . Then we have .

In addition, if there is a constant such that , then .

Next, we state the convergence result.

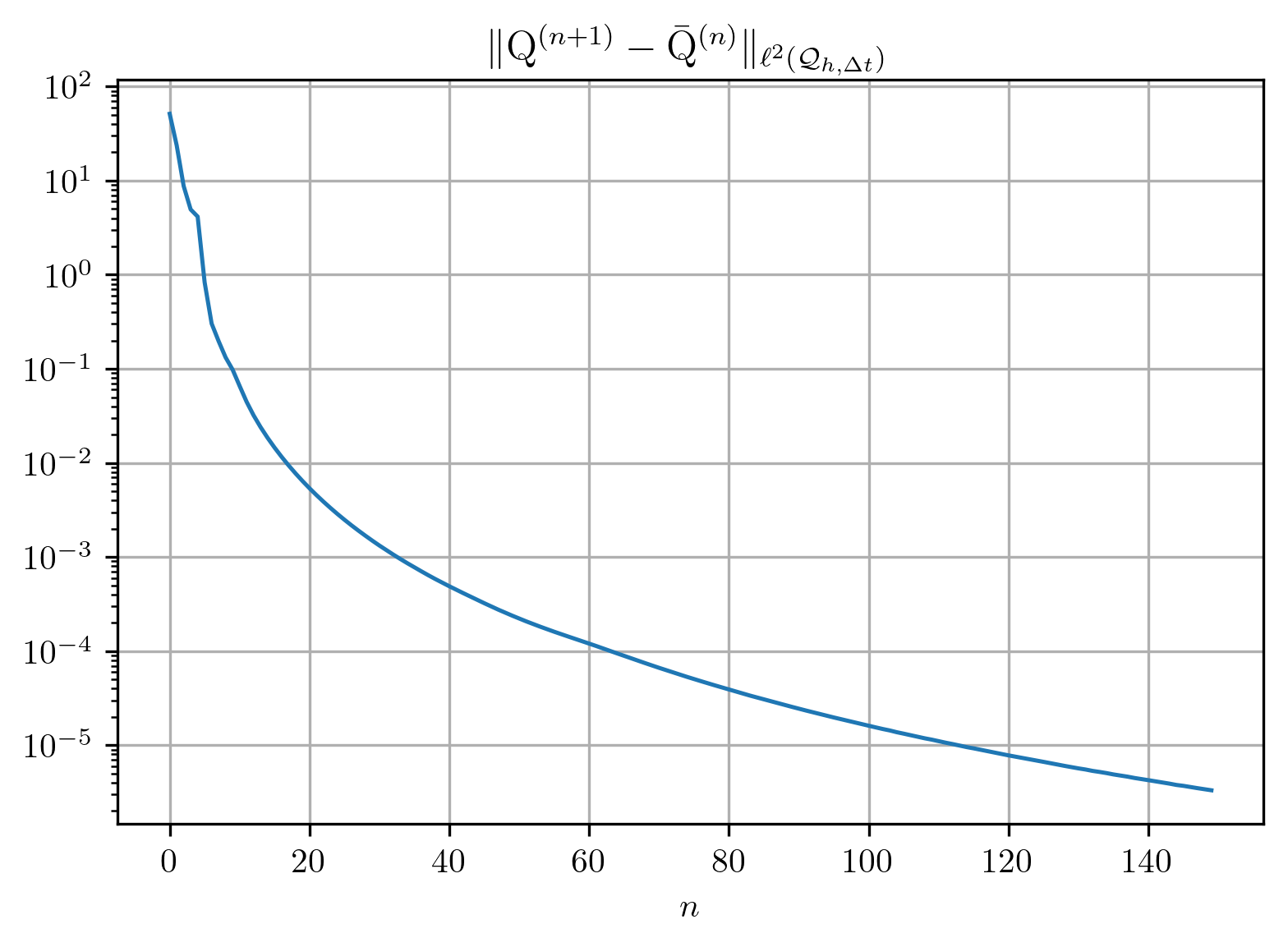

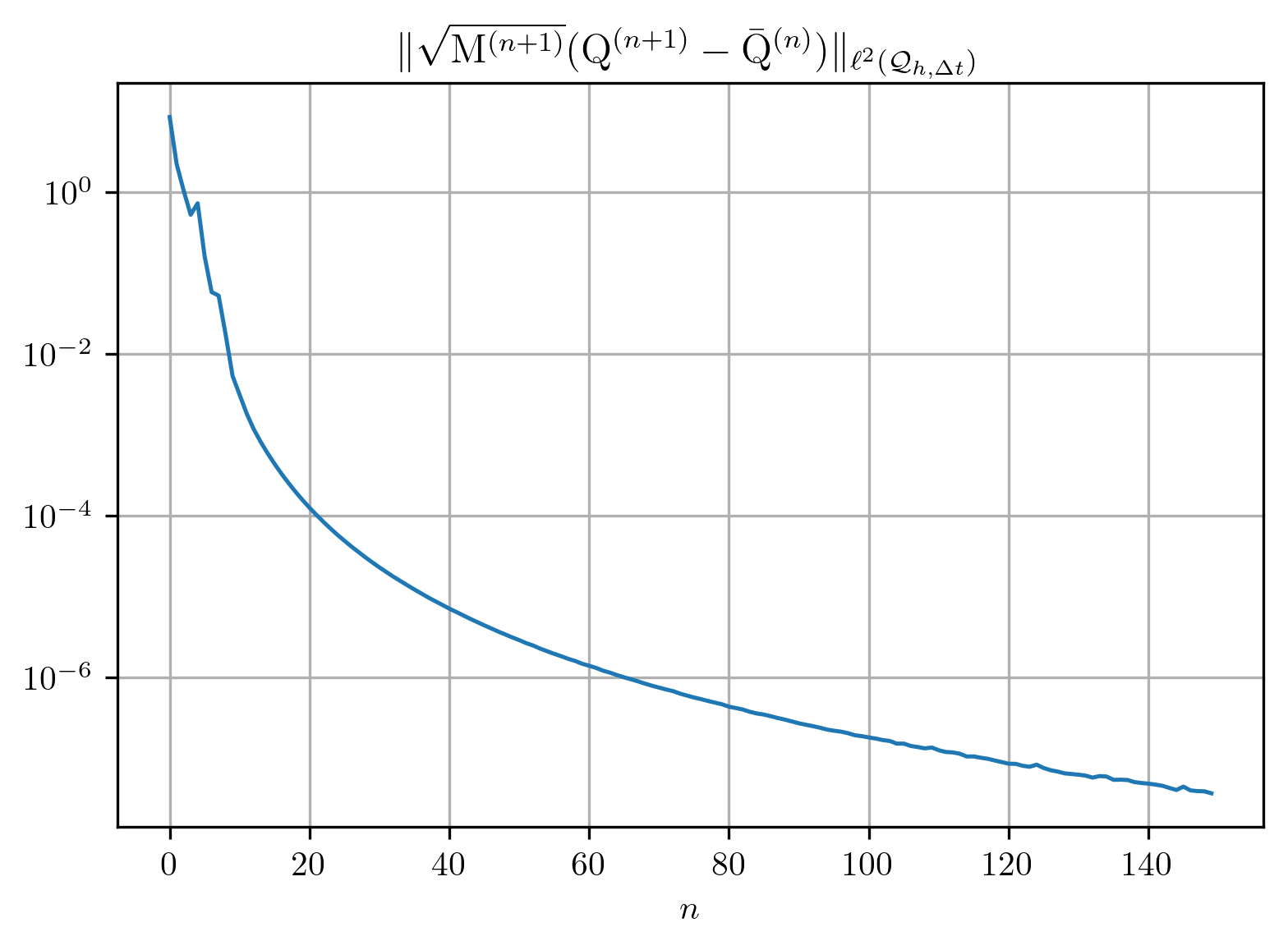

Theorem 4.6.

Under the assumptions (A2.1.1), (A2.1.2), (A2.1.3) and assumption 4.1, the family , , given by the algorithm (SPI) converges to the unique weak solution of the second order MFG system (3).

Proof.

Step 1. Let

|

|

|

(36) |

Our aim is to apply Lemma 4.5 to the previous sequence. We have

|

|

|

|

(37) |

Set

|

|

|

|

(38) |

|

|

|

|

From Lemma 2.10, setting in Eq. 21, we have

|

|

|

(39) |

Hence, by using Eq. 39 in Eq. 37, we obtain

|

|

|

(40) |

From Eq. 30, we have

|

|

|

(41) |

By convexity, we get

|

|

|

and therefore

|

|

|

Hence, as from Lemma 2.5, we get

|

|

|

|

(42) |

|

|

|

|

Moreover, as

|

|

|

we get

|

|

|

|

(43) |

|

|

|

|

|

|

|

|

Exploiting Eq. 41, Eq. 42 and Eq. 43 we get, with defined as in Eq. 38,

|

|

|

|

|

|

|

|

|

|

|

|

Denote by the Eq. 28 for and the Eq. 28 for . We have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Therefore

|

|

|

|

|

|

|

|

Multiplying both sides of the previous identity by , and integrating on ,

|

|

|

|

(44) |

|

|

|

|

|

|

|

|

|

|

|

|

By integration by parts,

|

|

|

|

|

|

|

|

Moreover for all ,

|

|

|

|

|

|

|

|

and, for as in (A2.1.3),

|

|

|

Replacing the previous estimates in Eq. 44, we obtain

|

|

|

|

(45) |

|

|

|

|

|

|

|

|

By Eq. 40 and Eq. 45, noticing the telescoping sum, we obtain

|

|

|

|

(46) |

|

|

|

|

|

|

|

|

From Lemma 4.3, we have that the right hand side of Eq. 46 is bounded for any , therefore

. From Lemma 4.3 and Lemma 4.4, we have that . Then we obtain from Lemma 4.5.

Step 2. Since and for all , it follows that

|

|

|

(47) |

Recall that is defined by Eq. 26 and denote by the solution to

|

|

|

which corresponds to the density obtained when using policy instead of .

It follows then from Lemma 2.5 and Eq. 47 that . Since

|

|

|

using the fact that and we obtain

|

|

|

As we have assume in (A2.1.3) that is w.r.t both variables, we obtain

|

|

|

(48) |

For each , . We can extract a subsequence which converges weak in and strongly in , since is a compact domain. We denote by a cluster point of , then from Eq. 47 it is also a cluster point of . With Eq. 48, the fixed point equation (iii) in system (3) is satisfied, i.e. is a solution to system (3). From Theorem 3.1, the solution to the system (3) is unique in , therefore all subsequences converge to the same limit.

∎

Next we show that if is a solution to system (3), then is actually a classical solution to (3) (i). While the bootstrap argument of showing a solution in is a classical solution is rather straight forward for mean field games even in the absence of monotonicity conditions (cfr. [37]), it is much more delicate for mean field games of controls. A crucial assumption is the monotonicity of w.r.t. in (A2.1.3). We first show that is Hölder continuous in time.

Lemma 4.7.

Under assumptions (A2.1.1), (A2.1.2) and (A2.1.3) and suppose is the weak solution to system (3). Then , where is defined as in Eq. 7. Moreover, .

Proof.

Let , and . We denote by using Eq. 7 and (iii) in (3):

|

|

|

|

|

|

|

|

|

|

|

First, we assume and we estimate .

Recall that ,

|

|

|

|

(49) |

|

|

|

|

|

|

|

|

|

|

|

|

Since by assumption, (from Assumption (A2.1.3)). Hence

|

|

|

We observe that

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

Therefore

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

implies by 14 and Eq. 12. From and , cf. Lemma 2.5, it follows . Therefore, from Eq. 49 we obtain

|

|

|

Second, we assume . Then we can follow the same reasoning to obtain . From (A2.1.3), the price is for the -variable. Since

|

|

|

we can conclude .

∎

Theorem 4.8.

Suppose is a solution to system (3), then

|

|

|

Proof.

It follows from Theorem 4.6 that . From Lemma 4.7 and Eq. 5 we then obtain . We have . By Schauder estimate, .

∎