Predictive Decision Synthesis for Portfolios: Betting on Better Models

Abstract

We discuss and develop Bayesian dynamic modelling and predictive decision synthesis for portfolio analysis. The context involves model uncertainty with a set of candidate models for financial time series with main foci in sequential learning, forecasting, and recursive decisions for portfolio reinvestments. The foundational perspective of Bayesian predictive decision synthesis (BPDS) defines novel, operational analysis and resulting predictive and decision outcomes. A detailed case study of BPDS in financial forecasting of international exchange rate time series and portfolio rebalancing, with resulting BPDS-based decision outcomes compared to traditional Bayesian analysis, exemplifies and highlights the practical advances achievable under the expanded, subjective Bayesian approach that BPDS defines.

Keywords:

Bayesian predictive decision synthesis, dynamic models, financial forecasting, FX portfolios, model uncertainty, multivariate volatility, portfolio decisions, target portfolios, TV–VAR models1 Introduction

Portfolio optimization is a major area of application and success of Bayesian decision analysis, going back at least to Markowitz (1952) and arguably earlier (de Finetti, 1940; Markowitz, 2006; Rubinstein, 2006). More recent Bayesian literature has emphasized financial time series modelling and forecasting to link with portfolio decision analysis (e.g. Quintana and West, 1987; West and Harrison, 1989, chap. 15; West and Harrison, 1997, chap. 16; Aguilar and West, 2000; Karlsson, 2013; Zhao et al, 2016; Gruber and West, 2016 and 2017; Prado et al, 2021, chap. 10), along with continuing concern for customizing utility specifications to guide Bayesian portfolio selection (e.g. Irie and West, 2019, and references therein)

Here we explicitly address portfolio decision goals when multiple forecasting models are to be explored and combined. Accounting for model uncertainty in pure forecasting is routine (e.g. West and Harrison, 1997; Jacobson and Karlsson, 2004; Andersson and Karlsson, 2008; Cheng et al, 2012; Aye et al, 2015; Wang et al, 2016; Steel, 2020; Lavine et al, 2021; Wang et al, 2023; Bernaciak and Griffin, 2024), but decision goals are not generally incorporated in these statistical approaches. In portfolio analysis, the main goal of forecasting asset returns is selecting desirable portfolios; we argue that this should be a key focus in combining relevant forecasting models. Recent Bayesian “goal-focused” methods aim to incorporate specific prediction goals beyond those of traditional Bayesian model averaging (e.g. Eklund and Karlsson, 2007; Pettenuzzo and Ravazzolo, 2016; Lavine et al, 2021; Loaiza-Maya et al, 2021; West, 2020; McAlinn, 2021; Bernaciak and Griffin, 2024). However, this literature rarely addresses explicit decision goals. A related literature concerns combining portfolio rules (e.g. Kan and Zhou, 2007; Demiguel et al, 2009; Tu and Zhou, 2011; Füss et al, 2024), though without explicit consideration of forecasting models.

Bayesian Predictive Decision Synthesis (BPDS), introduced in Tallman and West (2023), closes these gaps. BPDS is a fully Bayesian, theoretically founded framework to evaluate, compare, and combine sets of candidate models based on both their anticipated and historical decision outcomes as well as pure predictive performance and validity. We develop BPDS here in the setting of financial forecasting for portfolio decisions. BPDS is an expansion of Bayesian Predictive Synthesis (BPS) (McAlinn and West, 2019; McAlinn et al, 2020; McAlinn, 2021; Johnson and West, 2023), with explicit incorporation of the decision context and goals. BPDS aims to more highly weight models and outcomes that are better-performing in both recommended (Bayesian decision-theoretic) optimal decisions and more traditional statistical forecasting accuracy metrics. The context of sequential portfolio decision analysis is a canonical setting for the development and exploitation of BPDS for improved predictive decision-making in the central practical context of model uncertainty.

2 Bayesian Predictive Decision Synthesis

2.1 Model Uncertainty and Portfolio Decisions

Quantities of interest and relevant notation are defined as follows, indexed by time and implicitly representing the process of sequential analysis as time progresses. This is a standard setting of Bayesian model uncertainty analysis, indexed by time. We use the standard notation that represents all information and data accrued up to and including time , the point at which a decision is to be made to target some outcome at time . Relevant quantities include:

-

•

A forecast outcome vector . Examples are the time daily returns on assets, representing the percent change in price from time to time , or a set of returns over a multi-period path ahead from times to for some portfolio horizon

-

•

An explicit, decision problem targeting the outcome at time , in this case selecting a set of portfolio weightings on the assets.

-

•

A set of models , , such as a set of dynamic regression models for the asset return vector with different predictors across models, or other distinct model forms.

-

•

Initial model probabilities , such as from traditional Bayesian model averaging (BMA) based on prior data and information, and/or from historical performance in goal-focused forecasting such as Bayesian adaptive variable selection (AVS: Lavine et al, 2021, a special case of BPS)– or related methods (e.g. Loaiza-Maya et al, 2021).

-

•

Predictive densities provided by each model , . For example, a one-step predictive for that day’s FX returns, or a multi-step predictive for daily returns over the next days.

-

•

Model applies decision analysis with its utility function to evaluate the model-specific, optimal portfolio for time . This would be the optimal portfolio decision if the decision-maker restricted the analysis only to include and its associated utility function.

Faced with this model uncertainty question, the decision-maker aims to synthesize information across models to forecast and decide on a final portfolio weight vector under whatever overall utility function is chosen. This is then repeated sequentially over time.

2.2 BPDS

In the above setting, BPDS has the following ingredients. This follows and extends the main methodological developments from the BPDS theory in Tallman and West (2023).

Initial Mixture and Baseline Model

BPDS requires a “baseline” predictive density based on a notional additional model and a corresponding baseline optimal decision The baseline serves as an over-dispersed “safe haven” model whose predictions more heavily favor regions of the outcome space than are less well-supported by the initial mixture of the models. The initial probabilities are extended and renormalized to include a non-zero – an initially “small” probability on representing the concern that “all (initial ) models are wrong”, i.e., the issue of model set incompleteness.

We thus have the density defined over models and outcomes jointly. The margin for , simply is the called the initial mixture.

This framework reduces to the traditional (sequential, dynamic) Bayesian model uncertainty analysis when and if the other are appropriately based on historical data (West and Harrison, 1997, Sect. 12.2). In that special case, the initial mixture is simply that based on standard BMA.

BPDS Model Probabilities and Densities

BPDS modifies the initial density to an updated BPDS density where the are positive, model and outcome-dependent weights. That is,

| (1) |

with normalizing over both outcomes and models, i.e.,

| (2) |

The implied margin for is the BPDS mixture

| (3) |

where, for each model

| (4) |

The are BPDS model predictive densities, the are BPDS model probabilities, and the mixture is the BPDS predictive density.

Portfolio BPDS Scores and Relaxed Entropic Tilting

BPDS model weights are generally and uniquely defined as

| (5) |

with ingredients discussed below. The model-specific optimal portfolio vectors play critical roles in these BPDS model weightings.

First, is a vector of scores depending on outcome and the optimal portfolio under . Here is generated by optimizing whatever utility function is chosen for the decision analysis under . The elements of are realized values of utility functions at the optimal portfolio were to be the actual outcome. These utility functions are chosen so that higher scores are desirable. This allows for scoring models based on multiple metrics, expanding to multi-criteria decision analysis. Restrictions on score functions depend on the context and models involved. An example of a class of relevant score functions is given in the following section.

Second, is a BPDS tilting vector that defines relative weights and the directional impact of changes in score elements. Larger values in lead to more appreciable BPDS weightings, while recovers the prior mixture. The term tilting relates to the Bayesian decision-theoretic foundation and derivation of eqn. (5) which is based on relaxed entropic tilting (RET: see Tallman and West, 2022; 2023, section 3; West, 2023, sect. 2.3).

The specification of references expected scores. Taking expectations over jointly, the initial model has initial expected score High scores are desirable. The RET framework aims to achieve scores higher than initial, asking for the BPDS distribution to have expected score at least for some non-negative vector with at least one positive element. With this constraint, RET chooses to minimize the the Küllback-Leibler (KL) divergence of from , yielding two key results: (i) is defined in eqn. (1) with weighting function precisely as in eqn. (5); (ii) achieves exactly the expected score improvement bound specified by , i.e., The RET theory shows that any feasible choice of corresponds to a unique . The decision-maker has the liberty to choose in each specific portfolio context; various choices are explored in the portfolio examples below.

3 Risk : Return Score Functions for Portfolios

The section temporarily drops the time index from the notation, for clarity. Thus is a vector of asset returns, and a vector score on using model-specific portfolio vector were to be the observed outcome.

3.1 Utility Theory, Bivariate Scores and Risk Tolerance

Consider score dimensions and the class of vector scores where with portfolio return and a chosen target portfolio return .

These bivariate scores are motivated by the classic, bounded-above risk-averse exponential utility function for return given by for some risk tolerance level parameter . A second-order Taylor series approximation around gives with quadratic function and This is a very accurate approximation across ranges of that correspond to realistic models for return prediction in portfolio analyses, especially for daily returns. Up to constants, essentially reduces to the Markowitz function , maximized at . Were we to consider BPDS based on only a univariate score, then is faithful to this natural utility function and theoretical considerations. This has the contextual interpretation of as a chosen level of risk tolerance. The implied BPDS weight function would then be .

In contrast, choosing the suggested and more general bivariate score allows flexibility in addressing risk tolerance. This leads to which agrees with the univariate case above if/when and ; this defines a maximizing target return at this level of risk tolerance. Hence the bivariate score allows more flexibility in the role of the return/risk elements and their impact on the BPDS analysis while overlaying and replicating the classical exponential utility-based example as a special case. Operationally, it also yields the direct interpretation of as the implied level of risk tolerance.

3.2 Bivariate Scores and Tilting Vectors

In this section, we step aside from the mixture context to focus on generating portfolio-relevant insights from RET applied to a single model. This aids in understanding the roles of implied tilting vectors in the portfolio context and the relation to risk tolerance, among other details.

For this, consider predictions from any initial model such that the implied return has mean , where can be positive or negative, and variance We highlight aspects of the implied distribution of the bivariate score involving excess return and practical implications for BPDS analysis.

Distributions of Scores

Whatever the distribution of and the score vector under may be, knowing only and implies To explore the distribution of further, useful insights arise in assuming a normal approximation to .

With daily returns on FX and stock indices, and are typically of the order of 0.01 or less; this is relevant in exploring score uncertainty via the variance matrix . Were to be normal, then it is easy to show that Hence, is more uncertain than if . With practical levels of small % returns, this is very likely, and is typically much smaller than . That is, we expect to be much more uncertain about the first score element than the second.

While the two score elements are deterministically related, their joint distribution is not wholly degenerate since knowing does not precisely determine . In fact, the covariance is easily be shown to be . The implied score correlation is then where Note that: (i) has the sign of and depends only on the expected excess return in standardized units; (ii) is a decreasing function of and is an increasing function of ; (iii) over the range to , the correlation decreases from roughly 0.8 to ; (iv) for any given the absolute value is an increasing function of ; (v) for any given , the value is a decreasing function of .

RET Distribution and Tilting Vector in the Normal Example

Suppose that is normal. For a given tilting vector and any the resulting RET distribution is then also normal with easily computed moments. The implied on the return alone is then normal with moments that are easily shown to be

Hence the expected score under has elements

| (6) | ||||

These equations are easily solved for as a function of to give analytic evaluation of the tilting vector. This can be shown to give

With and it follows that as is desirable. Then eqn. (6) leads to or where has, as noted earlier, interpretation in terms of risk tolerance. We also easily have that

| (7) |

Some examples below choose so that , i.e., in the above. In that case, eqn. (7) reduces to the simple form This special case leads to , i.e., the two score dimensions are uncorrelated.

The above expressions for relate to our earlier comment about the bivariate score allowing the analysis to more flexibly reflect actual attitudes to risk through the direct specification of expected target scores any choice of which directly determines risk tolerance. Some examples follow.

Examples: Tilting Vectors and Risk Tolerance

Numerical examples highlight the relationships between taget expected scores and the implied tilting vector and associated risk tolerance

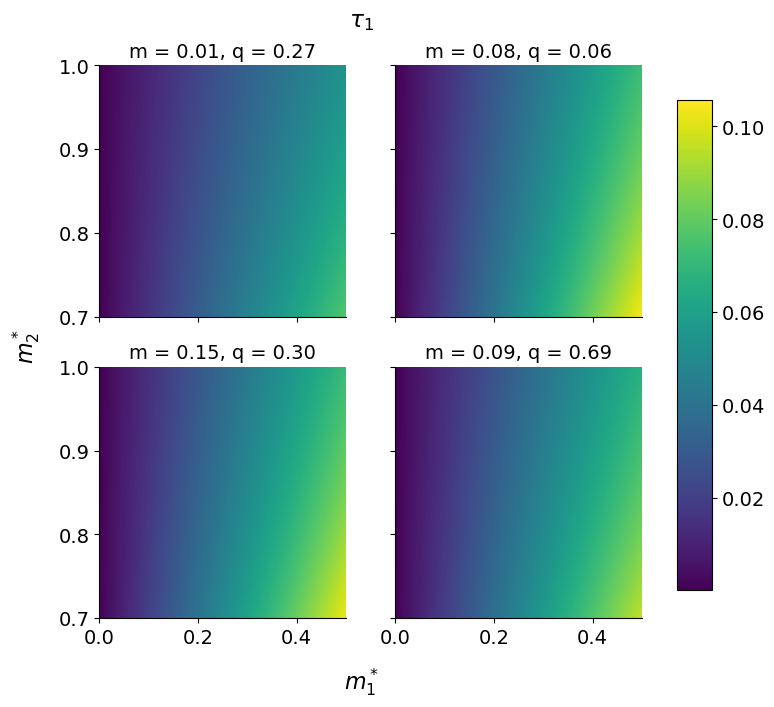

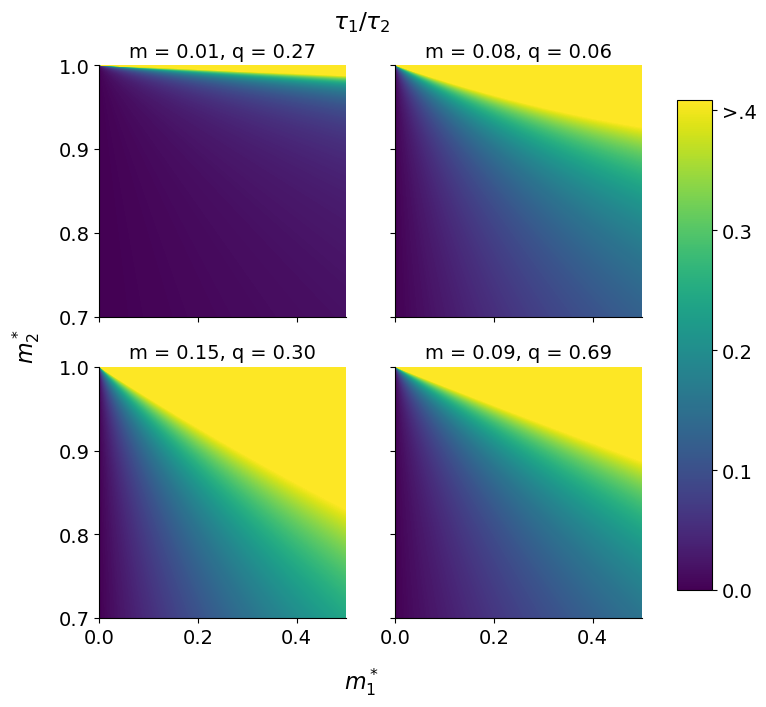

Specifying target expected scores under can be simply addressed through utilizing percent improvements over the initial expectations under Figures 1, 2 and 3 display values of , and for a few practical values of and and against different levels of percent target improvements in each of the score dimensions; the percent levels are denoted by and , where is the percent improvement in expected return over and is the percent improvement in . The general lack of correlation between the two score dimensions is due to the lack of prior score correlation. Then, the risk tolerance level may become large for small values of and large values of , indicating that these values should be carefully set to properly constrain risk.

4 Case Study: Data, Models and Portfolio Construction

4.1 Setting and Data

The study involves an extension of the example applying BPDS to portfolio analysis in Tallman and West (2023), with more recent data, adapted models, and an in-depth investigation of the BPDS hyperparameters used.

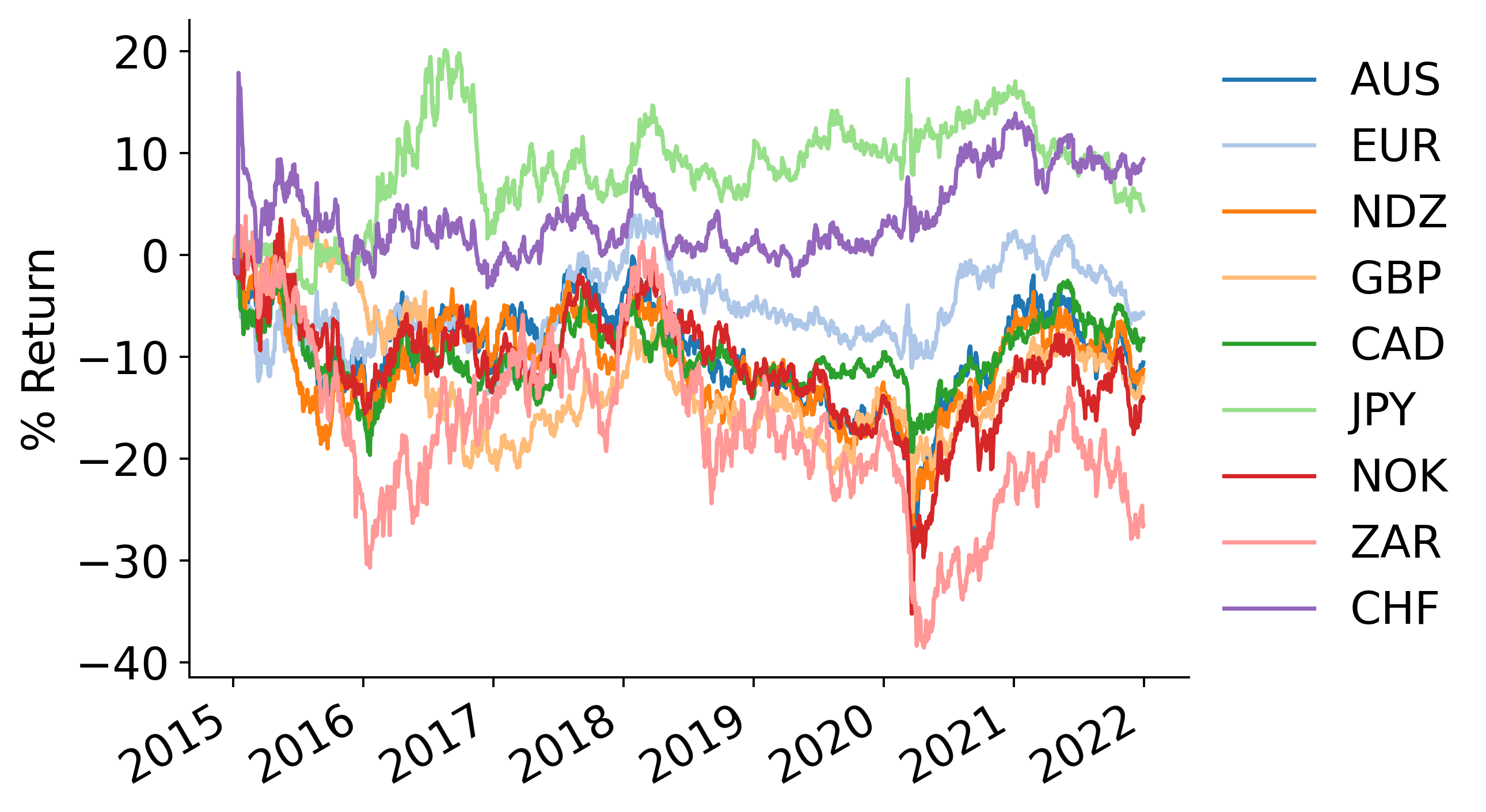

The data set includes daily returns for currencies beginning in January 2001 and ending in December 2021. The motivation for this asset set is to ensure model performance is not anchored in the performance of the market indices used in Tallman and West (2023), with the goal of providing additional value beyond the market return. The FX assets are noted in Table 1 with cumulative returns over the time period in Figure 4.

| Ticker | Currency | Ticker | Currency | |

|---|---|---|---|---|

| AUD | Australian Dollar | JPY | Japanese Yen | |

| EUR | Euro | NOK | Norwegian Krone | |

| NZD | New Zealand Dollar | ZAR | South African Rand | |

| GBP | UK Pound Sterling | CHF | Swiss Franc | |

| CAD | Canadian Dollar |

4.2 Models and Model-Specific Portfolios

The are time-varying vector autoregressive (TV–VAR) models applied to log FX prices. Details of these standard models are in Tallman and West (2023, Appendix) with full theory in Prado et al (2021, sect. 10.8). On day each model predicts the vector where is the vector of asset prices on day . These transform to returns via .

The dataset is divided into 3 time periods. The period to the beginning of 2015 is used to fit a large set of models, the next 4 years (2015-2018 inclusive) is used to select a subset of “better-performing models”, and the final 3 years (2019-2021 inclusive) defines a hold-out data test period. The larger initial set contains models of AR order , reflecting potential day momentum effects in FX prices. In each model, each univariate series is predicted by all values of with differing coefficients for each asset. These coefficients evolve over time as multivariate random walks; each model uses a state evolution discount factor to govern the degree of these changes. The model set is further expanded with a range of possible discount factors governing the evolution of the time-varying volatility matrix in each model (Aguilar and West, 2000; Irie and West, 2019; Prado et al, 2021, chaps. 9 & 10). Discount factor values define differing degrees of change in levels of volatility of each of the assets over time, as well as– critically for portfolio analysis– in the inter-dependencies among the assets as represented by time-varying covariances, with smaller values allowing for more adaptation. This gives 9 different model parameter combinations.

In each TV–VAR model , standard Bayesian forward-filtering analysis applies, and forecasting for daily portfolio rebalancing uses Monte Carlo samples of the predictive distributions for log-prices mapped to the mean vector and covariance matrix on the percent return scale. Model-specific decisions use standard Markowitz mean-variance optimization: these minimize predicted portfolio variances among sum-to-one portfolios with daily expected returns constrained to specified target levels (e.g. Prado et al, 2021, sect. 10.4.7). The initial set of BPDS model/decision pairs is completed by the use of 3 different benchmark targets coupled with each of the 9 TV–VAR models. The actual target return for each model on any day is where is the mean vector of predicted returns. This adaptive return target helps down-weight desired returns when the predictions favor small values; this helps to prevent large portfolio positions that would result from using the benchmark target. It also ensures that a portfolio that will lose money is never targeted in expectation. On each day, the resulting optimized portfolio weight vector is thus a vector of asset weights that has two constraints: they sum to one, i.e., , and they have the specified target for the expected return that day.

4.3 Selection of Models for BPDS Analysis

From the initial set of 27 models, a greedy strategy is used to select a subset of “good” models from analysis over the initial time period 2015-2018. This is to reduce cross-model dependencies in the resulting smaller set and to focus on some of the potentially more useful predictive and decision models. This is done sequentially, reducing from the full model set at each step. At each step: (i) consider the set of remaining models that have historical daily returns whose empirical correlation with those of each of the models already selected are lower than a defined correlation bar taken as 0.95; (i) among these, identify the model with the highest realized 1-day portfolio Sharpe ratio (SR– computed as realized daily mean return divided by realized daily return standard deviation over the historical data, multiplied to transform to the annual scale); (iii) add this model to the selected set until there are no models left with a positive Sharpe ratio or small enough correlation.

As the models share the same mathematical foundation, there is a high level of cross-model dependence in the initial set so a rather high correlation bar is used to yield several models in the selected set. The bar at 0.95 led to selected models with variability in the defining model order and volatility matrix discount factor parameters. This suffices for our study; the goal is not necessarily to create an optimal model set that will lead to the highest returns, but rather a well-performing model set for demonstrating aspects and benefits of BPDS in portfolio decisions.

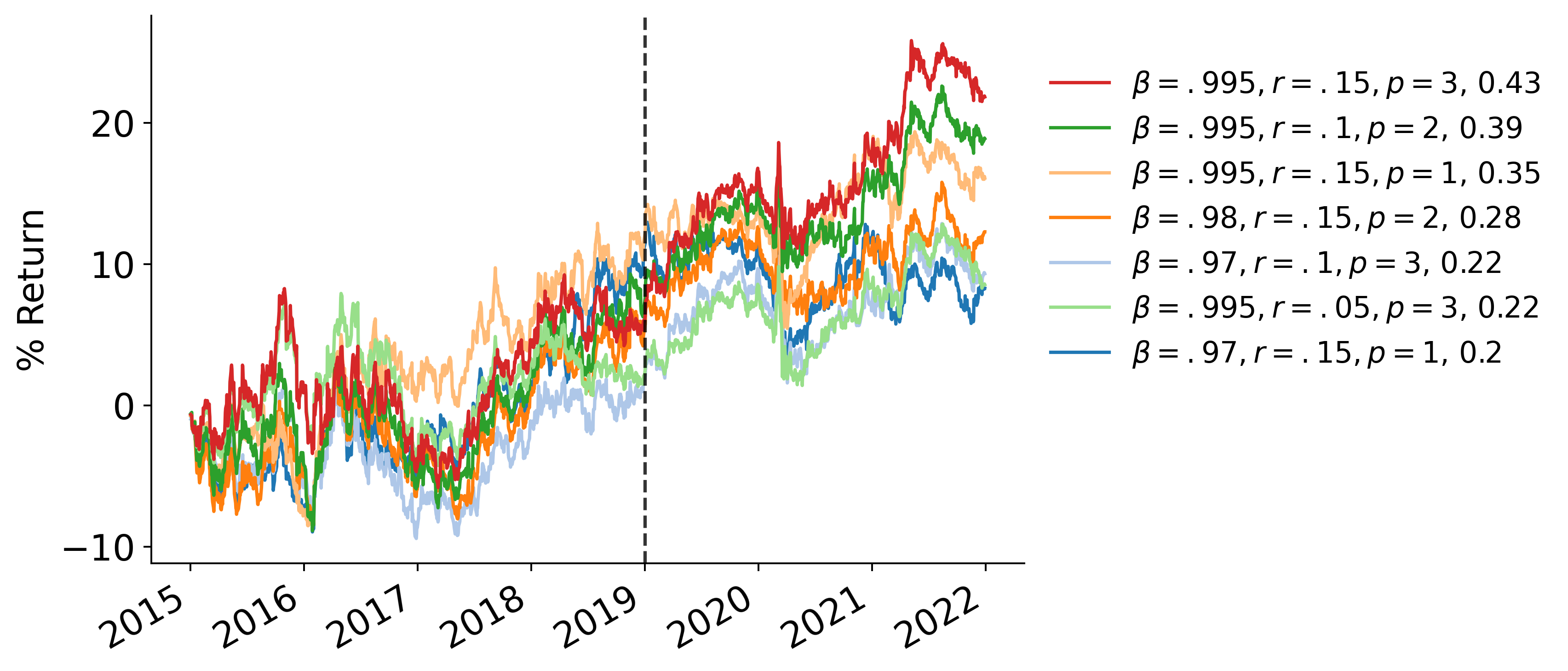

One relevant detail to note is that the returns for January 15th, 2015 were removed from the analysis. That was the day the Swiss Franc (CHF) was decoupled from the Euro, which resulted in an immediate gain of nearly 30% relative to the US dollar. This led to extreme returns across all models, and greatly down-weighted the impact of performance throughout the rest of the test period. To avoid biasing model selection on this single-day event, this day is ignored in the analysis. The selected models, their Sharpe ratios, and maximum return correlations with other selected models over 2015-2018 are shown in Table 2. Cumulative returns and Sharpe ratios from portfolios under each of these models over the entire period are shown in Figure 5.

| SR | SR | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.995 | 0.15 | 1 | 0.41 | 0.89 | 0.98 | 0.15 | 2 | 0.20 | 0.95 | |

| 0.97 | 0.15 | 1 | 0.40 | 0.89 | 0.995 | 0.05 | 3 | 0.11 | 0.95 | |

| 0.995 | 0.1 | 2 | 0.25 | 0.95 | 0.97 | 0.1 | 3 | 0.10 | 0.92 | |

| 0.995 | 0.15 | 3 | 0.22 | 0.95 |

5 Initial BPDS Analysis

5.1 Portfolio Setting: Forecast Horizon and Portfolio Targets

The initial example replicates the set-up of the portfolio example in Tallman and West (2023) but with the new data set and expanded model set. The score function is , with further relevant details discussed in Section 2 above. The in the first dimension is dropped for simplicity and ease of specification for the target score improvement in terms of a percentage. As is just a constant with respect to and , this does not change any previous results and has no effect on the resulting analysis. Note that, unlike the settings in Tallman and West (2023), now depends on , selected such that , a dynamic target based on the specified targets in the underlying models. This does not affect the mechanics of the BPDS methodology; it simply ensures that BPDS is more adaptive to exploit the fact that the model targets are now changing over time. Several BPDS specifications are evaluated to help understand how BPDS is applied and to explore robustness.

One main variant explored is the portfolio forecast horizon. With this motivation, results from evaluating both and day ahead portfolios are included. The 1-day portfolios are the portfolios introduced previously, calculated using the predicted next-day returns. The 5-day portfolios are made by fitting each TV–VAR model to daily returns, as in the 1-day case, but then forecasting asset returns 5 days into the future. This gives predictions where now is redefined as . The moments of this distribution are then used to define 5-day ahead portfolios with the same sum-to-one constraint along with the revised target expected return in as where is the mean forecast vector 5-days ahead. Though calculated using a 5-day portfolio, these portfolios will still be updated each day; a given portfolio will only be held for a single day before rebalancing. The interest in 5-day ahead analyses is partly contextual in that such portfolios can have better risk profiles and smaller movements in portfolio weights. Also, models might be more easily differentiated, as single-day forecasts tend to be more similar across models while the longer horizon can show more distinctions.

Further explorations consider ranges of chosen percent target score improvements, with BPDS target expected scores set as the element-wise product vector , where and for all combinations of and . The initial probabilities are set using discounted BMA probabilities (Zhao et al, 2016); that is, at each . The discount factor provides discounting of historical model weights between days and hence– relative to standard BMA which has – analysis avoids the eventual degeneration of model probabilities. The BPDS portfolio is calculated using Markowitz optimization, just as in each of the models, but now with a target return of with risk tolerance . This is the value of that maximizes , the weighted sum of the score function utilizing BPDS weighting vector . We additionally restrict the tilting vector such that so that the portfolio target can be at most doubled; this is in order to obviate large values earlier seen in Figure 3, and is enforced in the computations to evaluate at each time point.

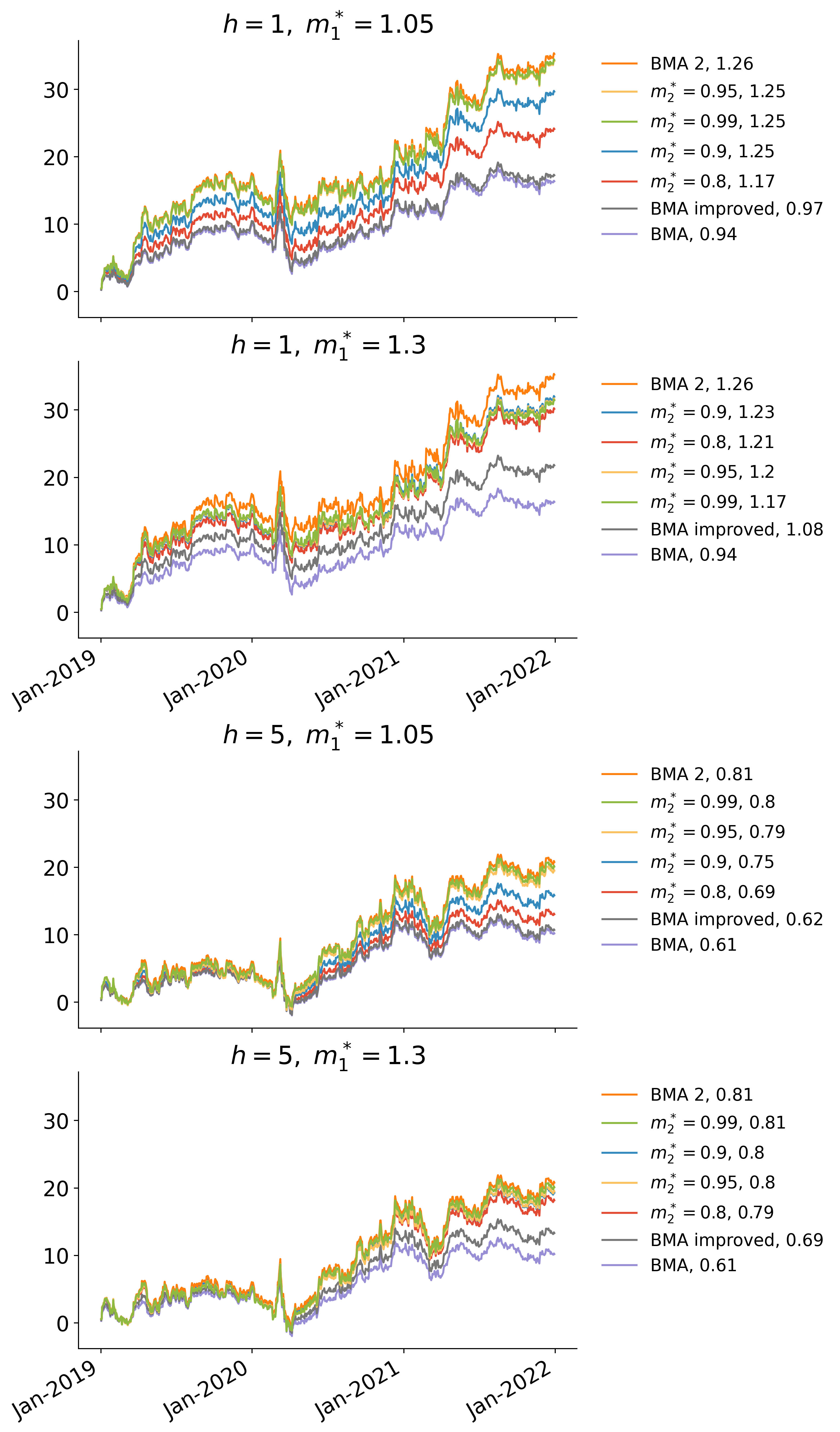

5.2 Some Summary Results

Comparative results involving cumulative returns and Sharpe ratios are seen in Figure 6. Additional comparisons come from the standard BMA analysis (, for all , and target return ). Then, in an effort to advantage BMA through a modified specification of the portfolio setup, we added extensions for potential improvements on BMA using target returns and , labelled as “improved BMA” and “BMA 2” respectively. These connect to the fact that is the desired percent return score improvement in BPDS, and is the upper bound on which defines the target return for BPDS.

BPDS is able to achieve superior cumulative returns and Sharpe ratios compared to BMA and “improved BMA”, across all settings of . The 5-day portfolios improve over BMA comparisons but generally see relatively lackluster results compared to the 1-day portfolios. This is mainly due to the use of initial BMA-based weights. BMA focuses wholly on 1-step ahead predictive accuracy, so the initial probabilities used here in BPDS generally favour models based on predictive performance at this short-term horizon. This represents a disconnect in BPDS when focused on 5-day portfolios. A relevant extension would be weighting models using 5-day forecast accuracy/likelihood weightings. Then, there is no obvious pattern of improvement across different values of and , partly due to the restriction placed on that emphasizes control on the risk:reward behavior regardless of the target setting and drives most of the results.

BPDS outcomes are generally close to those of BMA 2, but do not empirically improve upon the latter in this first set of comparisons. This indicates that most of the performance gains come from the target increase and that the tilting and variation in the target increase are not as helpful. However, note that the methodology for setting the score improvement here is rather simplistic, using a grid of percent improvements. In particular, this does not consider the underlying distribution of the score function which implies, for example, that a 10% decrease in variance could be a fairly large jump, whereas a 5% increase in the target return itself is a fairly small improvement. This observation is key to the methodological extension in the next section that explicitly involves consideration of aspects of the predictive distributions for scores in setting the BPDS targets– and yields substantial advances in BPDS performance and dominance over the BMA extensions.

6 Practicable Portfolio BPDS: Structured Score Targets

6.1 Score Standardization and Eigenscore Targets

Recent use of BPDS in economic applications in Chernis et al (2024) introduced target expected score specifications that reflect the importance of relative scales and dependencies among the elements of each under the initial distribution at each time . We have discussed aspects of this above in Section 3.2 and revisit it here. A key point is to exploit aspects of the distribution of scores to guide choices of relevant targets that are not wildly inconsistent with the distribution. This aids in avoiding overly aggressive or inconsistent targets such as those highlighted in the naive score targets used in the previous section.

At each time write and for the mean vector and variance matrix of under . With eigendecomposition where with positive elements, the eigenscore is a standardized score vector with zero mean vector and identity variance matrix. Specified shifts in each dimension of the standardized score vector are now on the same scale and so directly comparable, while the orthogonality implies that there will be limited interaction between them in the ensuing BPDS analysis. Hence it is natural and intuitive to define BPDS analysis based on the specification of standardized expected scores that then map back to the original score scale. That is, with a specified target vector on the standardized scale the implied target score on the original scale is

We know from Section 3.2 that is typically close to diagonal (and exactly diagonal in some cases) with a much larger variance on the first score element than the second. That is, or exactly and . Hence (or exactly ) So, with comparable values of the two standardized score targets, the fact that implies a much greater– and undesirable– increase of the target expected return (first element of ) than the risk (second element of ). Further insights come from theoretical results in Tallman and West (2023, sect. 3.4) that define approximate expressions for when specified target scores are “small deviations” from In the current setting that theory leads to This shows that, for given and knowing , there is much greater shrinkage towards zero of than of This implies that a much larger improvement is needed in the return dimension to achieve a similar level of tilting as in the risk dimension.

An initial use of the standardization concept in this setting explores for some small defining equal increments in each score dimension. To assess relevant values of we begin with a focus on the target excess return itself. Set for some such that , so that represents the percent target increase over the initial expected return. Equating this to yields the (small) The implication for the target for the risk element of the score vector is that This target score strategy is now used in FX reanalysis.

6.2 FX Portfolio Analysis Revisited

Example Analysis with Eigenscores

The analysis of Section 5 is repeated, now setting BPDS score targets with the eigenscore strategy. We compare results under a range of percent improvements on the expected return. Note that in this setting there is the result that the implied risk tolerance level . As a result, the BPDS target return improvement will generally be constant across and any improvements for two different values of will be the result of the tilting and not due to different increases in the BPDS target return.

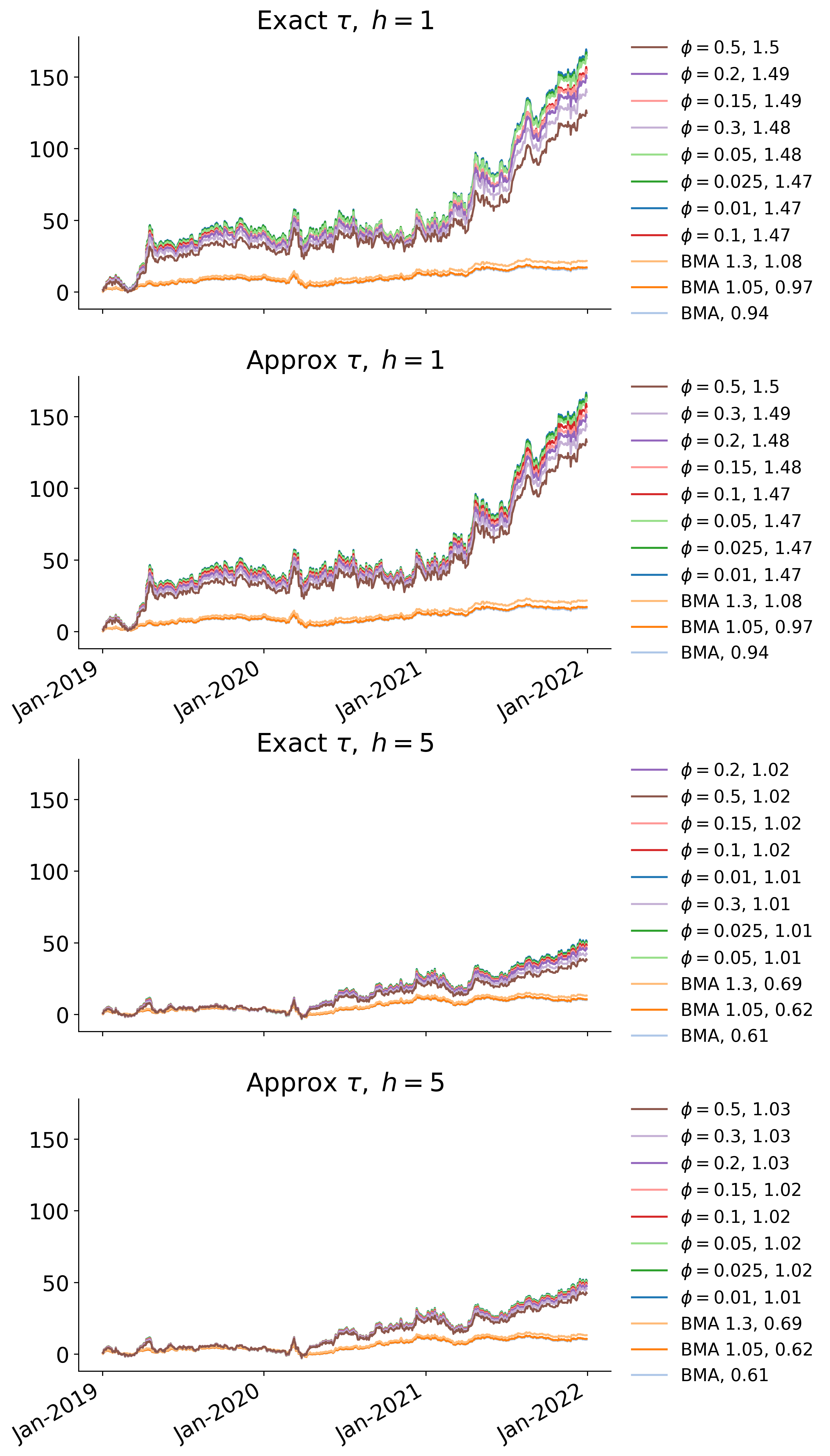

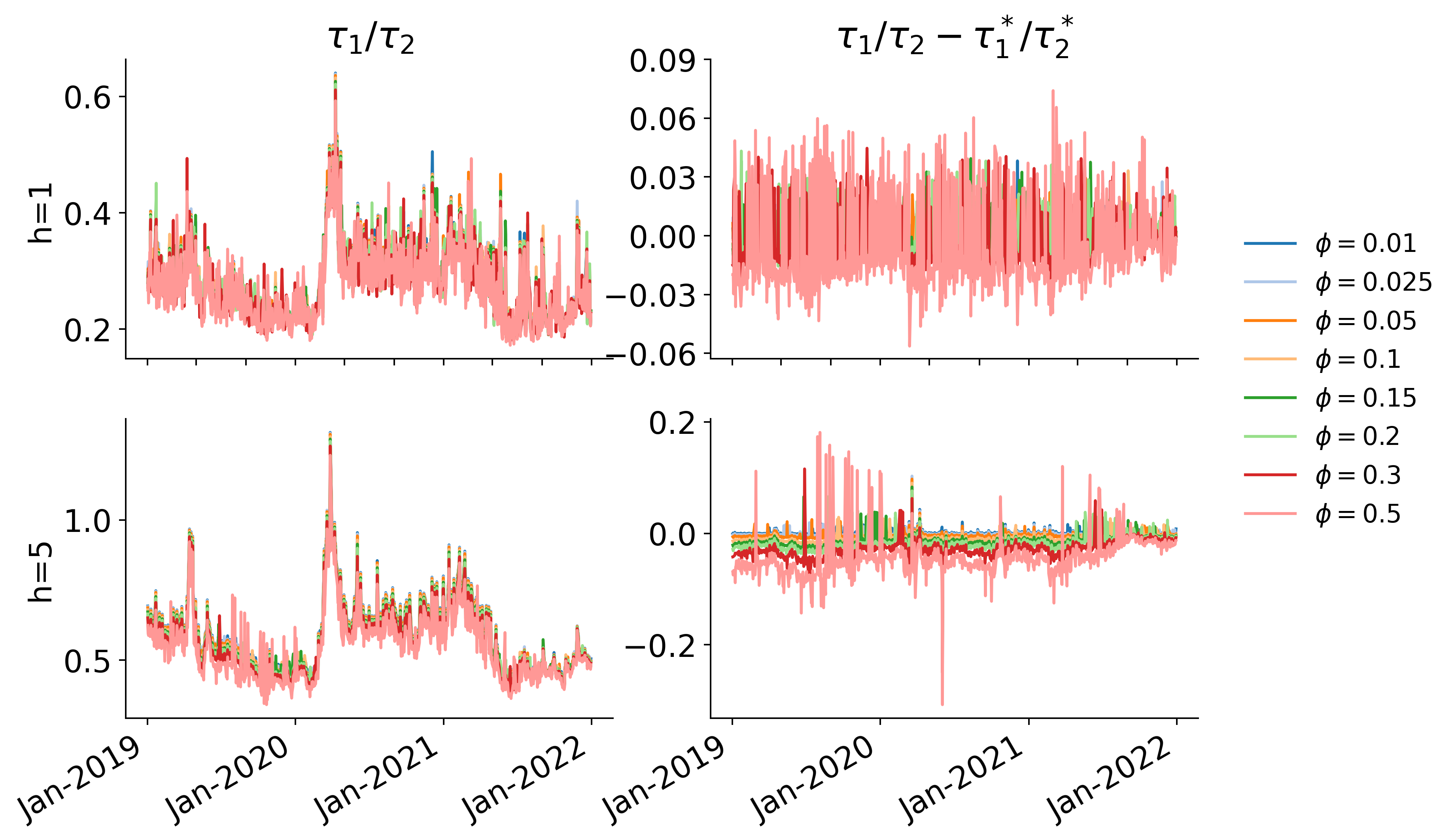

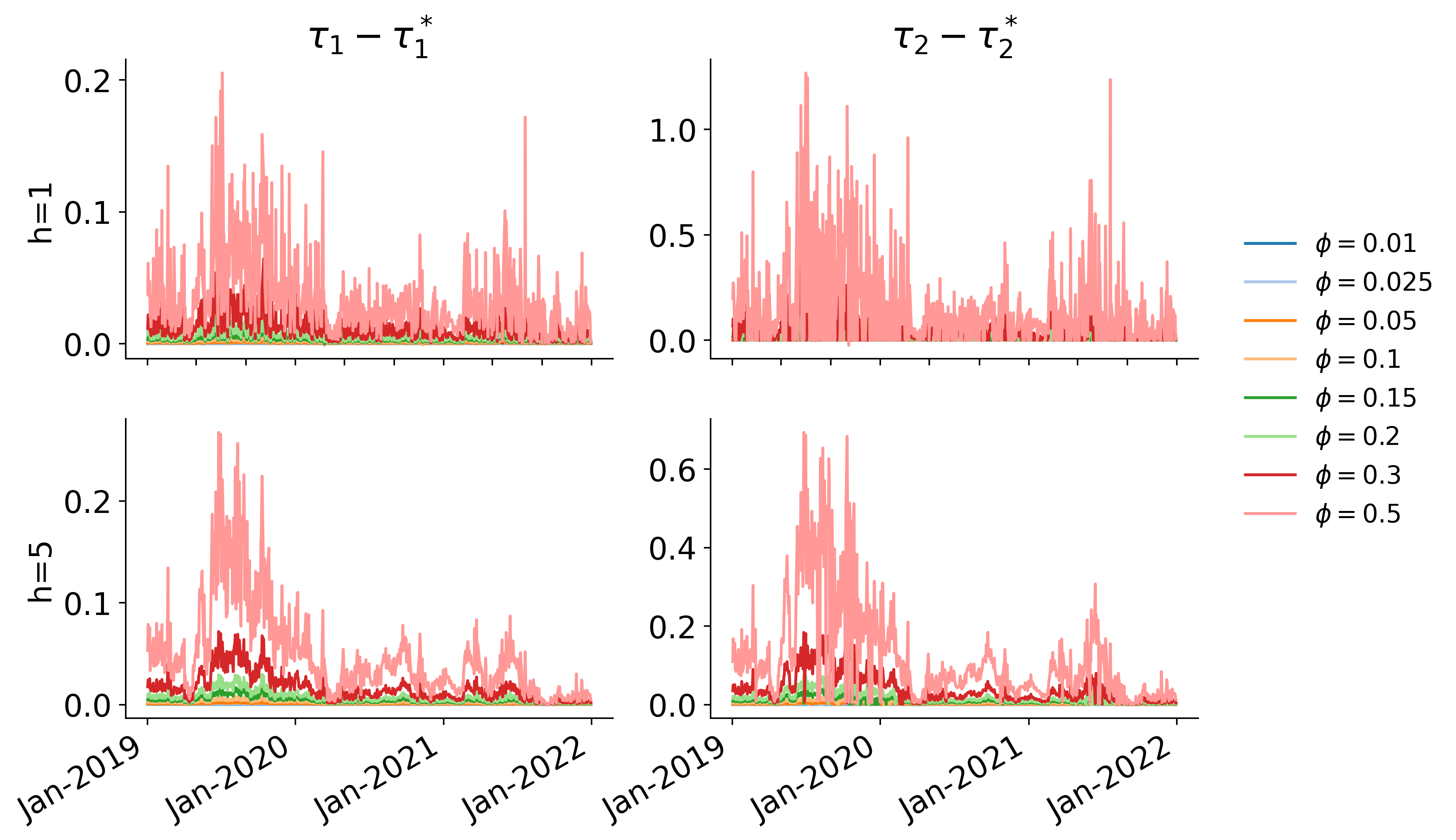

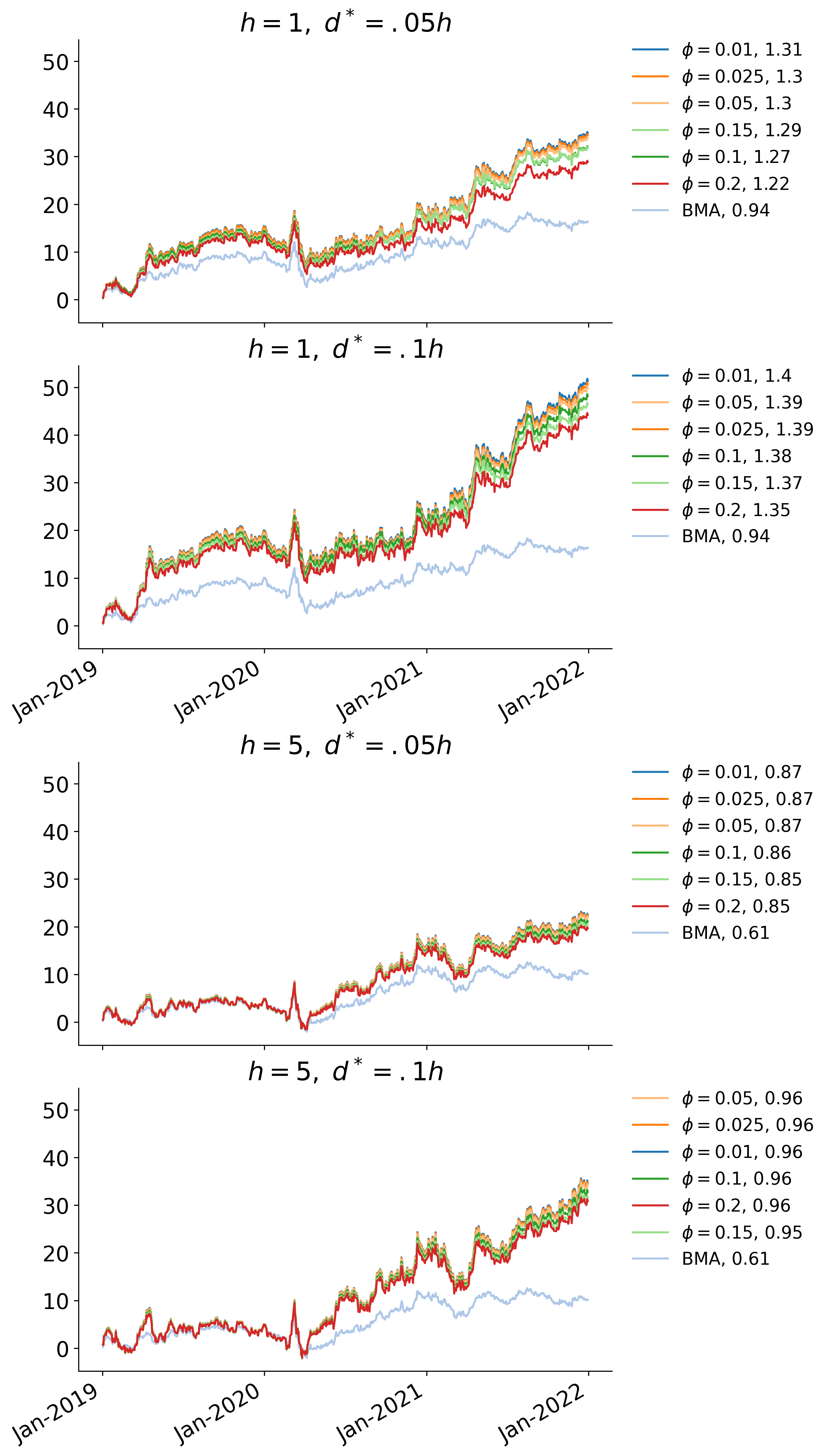

The analysis is repeated for all . Cumulative returns and Sharpe ratios are shown in Figure 7. Results are shown from analysis using the approximation as well as from exact calculations; this aids in empirical investigation of the accuracy of the approximation. Resulting differences in and between the approximate and exact analyses are in Figures 9 and 9.

Portfolio results under all BPDS specifications far exceed those under BMA and the improved BMA approaches, using either the exact or approximate calculations of . The 1-day portfolios have superior results in terms of both returns and Sharpe ratios, again mainly due to the lack of connection between the initial weights and the BPDS score in the 5-day case. There are some small differences between the exact and approximate versions for larger values of . This is expected as higher correspond to higher values of , and the theoretical approximation is for “small ”. The high increases in returns are partly explained by Figure 9; the return target is drastically increased, leading to a target of a nearly 0.35% daily return. This aggression in terms of seeking high returns leads to the extreme returns seen in Figure 7. Since the Sharpe ratios are normalized, this BPDS specification can be realistically compared with BMA despite the difference in return scales, and the results demonstrate realistic and marked improvements using BPDS.

Repeat Analysis using Modified Target Scores

The above results are very positive in terms of BPDS improving decision outcomes. However, the large values of risk tolerance generated overly optimistic return targets. Knowing that in this setting, and that this ratio cannot be changed by altering , a modified choice of standardized target score is suggested to address this. This simple modification replaces the standardized target with for a chosen constant . This factor represents and induces differences in the degrees of tilting in the return and risk dimension of the score. In particular, a value naturally acts to increase the role of the risk score element and hence can balance an overly optimistic/aggressive return target driving the first element. Some numerical examples below explore this. In these examples, is chosen based on the initial test data analysis; its value is determined so that the average over the test time period of generated values of is equal to , a chosen average threshold on the risk tolerance measure.

The examples here are based on choices and , linked to the and day horizons for portfolio targets. This implies that, on average over the initial test data set, the return target increase will be less than either or for the 1-day portfolio. This will lead to a more practically reasonable target compared to the aggressive daily target in the analysis of the previous section, an analysis in which the tolerance was unconstrained. This leads to and respectively when , and and when . Portfolio outcomes shown here are based on analyses using the exact calculation of ; the approximate values are now used only as starting points for the optimization to evaluate . Realized cumulative returns and Sharpe ratios are shown in Figure 10.

Realized cumulative returns are now on a much more practically reasonable scale, while still maintaining a nice risk-adjusted return. All BPDS specifications for the 1-day portfolios are seen to substantially improve over BMA relative to the initial exploration in Section 5. Note also that the empirical cumulative returns under the 5-day strategy are more comparable with those under the 1-day strategy than in the earlier, unconstrained analysis. That said, there is still room for improvement in the multi-day strategies as they are here still using initial model probabilities based on variants of BMA-based weights. As noted earlier, the latter are wholly based on 1-step forecast accuracy. This is a main question in terms of future development of more appropriate initial model weightings, among which will be to adapt prior goal-focused scoring approaches to refine the specification of the initial (Lavine et al, 2021; Loaiza-Maya et al, 2021).

There is some– though relatively limited– variation in empirical returns as is varied, again due almost wholly to differences in resulting tilting. Small values of are empirically preferable in terms of Sharpe ratios, contrasting with the results from the naive analysis of the previous section. This again demonstrates the importance and value of “small” changes in BPDS target score relative to initial predictions.

Exploration of realized characteristics of portfolio decisions is naturally tied to the time period chosen and displayed. The cumulative return trajectories and Sharpe ratios shown in Figure 10 are for the full 3-year test period. While not a main point in terms of developing and illustrating the BPDS methodology, it is of contextual interest to look at outcomes over different time periods. Our choice of 2019-2021 inclusive is contextually interesting due to the major differences in economic and market behavior over these years, and some insights are generated by looking at year-specific results. As a snap-shot, Table 3 lists realized Sharpe ratios for each specific year under the 1-day portfolio strategy. The main points to note are (i) the year-to-year differences, with 2020 being a stand-out in terms of relatively poor outcomes across models, and (ii) the strong consistency in Sharpe ratios within each year as varies to define different BPDS targets.

As already emphasized, the empirical returns under BPDS as shown in Figure 10 are substantially superior under any of the BPDS variants relative to BMA. That the Sharpe ratios per year under BMA are relatively competitive is due to the fact that BPDS spreads the model probabilities more than BMA each time point, and always has some probability on the over-diffuse baseline to address the model-set incompleteness question. Hence BPDS will almost surely define heavier-tailed forecast distributions for that lead to higher uncertainties on portfolios than under BMA. The latter will typically underestimate uncertainties as it concentrates quickly around one of the initial models. This helps in interpreting the realized Sharpe ratios that represent just one aspect of “performance”, and that is balanced by the realized return outcomes under BPDS as shown in Figure 10 to emphasize this point in this case study. Here, under BPDS the appropriately increased levels of uncertainty are balanced by substantially increased realized returns. Additional metrics highlighting differences between the strategies– including purely predictive comparisons in the full space of returns defined by models for – will be of interest in further comparisons.

| 2019 | 2020 | 2021 | 2019 | 2020 | 2021 | |

|---|---|---|---|---|---|---|

| 2.21 | 0.21 | 1.98 | 2.14 | 0.16 | 2.34 | |

| 2.21 | 0.21 | 1.97 | 2.14 | 0.15 | 2.33 | |

| 2.19 | 0.22 | 1.97 | 2.14 | 0.16 | 2.33 | |

| 2.21 | 0.21 | 1.89 | 2.14 | 0.18 | 2.29 | |

| 2.20 | 0.26 | 1.90 | 2.12 | 0.16 | 2.28 | |

| 2.21 | 0.13 | 1.84 | 2.16 | 0.14 | 2.24 | |

| BMA | 2.17 | 0.23 | 0.88 | 2.17 | 0.23 | 0.88 |

7 Summary Comments

BPDS is a foundational framework that enables the integration of expected and historical decision outcomes in predictive model uncertainty settings. As exemplified here, BPDS can potentially improve realized decision outcomes and thus serve as an important tool for portfolio managers for model combination, calibration, and evaluation. The case study developed in this paper demonstrates the potential for BPDS to improve the trade-off between risk and reward in portfolio analysis. It also provides additional methodology for understanding relevant score functions and setting target scores in the portfolio setting. The results further confirm and expand on the positive results originally reported in Tallman and West (2023). The focused development of customized BPDS target scores, and the practical results in terms of desirable portfolio characteristics, demonstrate the importance of incorporating information about the underlying score distribution, and of the contextual interpretation of the elements of the score vector. The examples show the potential for BPDS to improve on current Bayesian model averaging methods in portfolio analysis, with the prospects for more adaptive portfolios that have better resulting portfolio outcomes.

There are various potential future directions for applying BPDS in finance. One is in expanding the set of score functions to include other relevant metrics, such as portfolio churn or skewness/kurtosis of the return distribution, and of course other features of portfolio “paths” over multiple forecast horizons (e.g. Irie and West, 2019; Tallman, 2024). Further investigation of the questions related to setting BPDS target scores is also relevant, especially towards improved understanding of how small changes in the target score lead to changes in the resulting decisions. It is also of interest to consider utilizing initial weights that are customized and potentially more relevant than those based on simple, following prior literature on formal Bayesian model weighting based on historical outcomes with respect to specific predictive and decision goals (e.g. Eklund and Karlsson, 2007; Lavine et al, 2021; Bernaciak and Griffin, 2024; Chernis et al, 2024, and references therein).

Acknowledgements

The research reported here was performed while Emily Tallman was a PhD student in Statistical Science at Duke University. Tallman’s research was partially supported by the U.S. National Science Foundation through NSF Graduate Research Fellowship Program grant DGE 2139754. Any opinions, findings, and conclusions or recommendations expressed in this material are those of the authors and do not necessarily reflect the views of the National Science Foundation.

References

- Aguilar and West (2000) Aguilar O, West M (2000) Bayesian dynamic factor models and portfolio allocation. Journal of Business and Economic Statistics 18:338–357

- Andersson and Karlsson (2008) Andersson MK, Karlsson S (2008) Bayesian forecast combination for VAR models. In: Chib S, Griffiths W, Koop G, Terrell D (eds) Bayesian Econometrics, Advances in Econometrics, vol 23, Emerald Group Publishing Limited, pp 501–524

- Aye et al (2015) Aye G, Gupta R, Hammoudeh S, Kim WJ (2015) Forecasting the price of gold using dynamic model averaging. International Review of Financial Analysis 41:257–266

- Bernaciak and Griffin (2024) Bernaciak D, Griffin JE (2024) A loss discounting framework for model averaging and selection in time series models. International Journal of Forecasting DOI 10.1016/j.ijforecast.2024.03.001

- Cheng et al (2012) Cheng C, Xu W, Wang J (2012) A comparison of ensemble methods in financial market prediction. In: 2012 Fifth International Joint Conference on Computational Sciences and Optimization, Curran Associates, Inc., pp 755–759

- Chernis et al (2024) Chernis T, Koop G, Tallman E, West M (2024) Decision synthesis in monetary policy. Under review at: Journal of Business & Economic Statistics ArXiv:xxxx.xxxxx

- Demiguel et al (2009) Demiguel V, Garlappi L, Uppal R (2009) Optimal versus naive diversification: How inefficient is the portfolio strategy? Review of Financial Studies 22:1915–1953

- Eklund and Karlsson (2007) Eklund J, Karlsson S (2007) Forecast combination and model averaging using predictive measures. Econometric Reviews 26:329–363

- de Finetti (1940) de Finetti B (1940) The problem of ‘full-risk insurances’. Journal of Investment Management 4:19–34, 2006 translation by Luca Barone

- Füss et al (2024) Füss R, Glück T, Koeppel C, Miebs F (2024) An averaging framework for minimum-variance portfolios: Optimal rules for combining portfolio weights. Swiss Finance Institute Research Paper 24-10, Swiss Finance Institute

- Gruber and West (2016) Gruber LF, West M (2016) GPU-accelerated Bayesian learning and forecasting in simultaneous graphical dynamic linear models. Bayesian Analysis 11:125–149

- Gruber and West (2017) Gruber LF, West M (2017) Bayesian forecasting and scalable multivariate volatility analysis using simultaneous graphical dynamic linear models. Econometrics and Statistics 3:3–22

- Irie and West (2019) Irie K, West M (2019) Bayesian emulation for multi-step optimization in decision problems. Bayesian Analysis 14:137–160

- Jacobson and Karlsson (2004) Jacobson T, Karlsson S (2004) Finding good predictors for inflation: A Bayesian model averaging approach. Journal of Forecasting 23:479–496

- Johnson and West (2023) Johnson MC, West M (2023) Bayesian predictive synthesis with outcome-dependent pools. Submitted for publication ArXiv:1803.01984

- Kan and Zhou (2007) Kan R, Zhou G (2007) Optimal portfolio choice with parameter uncertainty. The Journal of Financial and Quantitative Analysis 42:621–656

- Karlsson (2013) Karlsson S (2013) Forecasting with Bayesian vector autoregression. In: Elliott G, Timmermann A (eds) Handbook of Economic Forecasting, Handbook of Economic Forecasting, vol 2, Elsevier, pp 791–897

- Lavine et al (2021) Lavine I, Lindon M, West M (2021) Adaptive variable selection for sequential prediction in multivariate dynamic models. Bayesian Analysis 16:1059–1083

- Loaiza-Maya et al (2021) Loaiza-Maya R, Martin GM, Frazier DT (2021) Focused Bayesian prediction. Journal of Applied Econometrics 36:517–543

- Markowitz (1952) Markowitz H (1952) Portfolio selection. The Journal of Finance 7:77–91

- Markowitz (2006) Markowitz H (2006) De Finetti scoops Markowitz. Journal of Investment Management 4:5–18

- McAlinn (2021) McAlinn K (2021) Mixed-frequency Bayesian predictive synthesis for economic nowcasting. Journal of the Royal Statistical Society (Ser C) 70:1143–1163

- McAlinn and West (2019) McAlinn K, West M (2019) Dynamic Bayesian predictive synthesis in time series forecasting. Journal of Econometrics 210:155–169

- McAlinn et al (2020) McAlinn K, Aastveit KA, Nakajima J, West M (2020) Multivariate Bayesian predictive synthesis in macroeconomic forecasting. Journal of the American Statistical Association 115:1092–1110

- Pettenuzzo and Ravazzolo (2016) Pettenuzzo D, Ravazzolo F (2016) Optimal portfolio choice under decision-based model combinations. Journal of Applied Econometrics 31:1312–1332

- Prado et al (2021) Prado R, Ferreira MAR, West M (2021) Time Series: Modeling, Computation and Inference, 2nd edn. Chapman & Hall/CRC Press

- Quintana and West (1987) Quintana JM, West M (1987) An analysis of international exchange rates using multivariate DLMs. The Statistician (now: Journal of the Royal Statistical Society, Ser D) 36:275–281

- Rubinstein (2006) Rubinstein M (2006) Bruno de Finetti and mean-variance portfolio selection. Journal of Investment Management 4:3–4

- Steel (2020) Steel MFJ (2020) Model averaging and its use in economics. Journal of Economic Literature 58:644–719

- Tallman (2024) Tallman E (2024) Bayesian Predictive Decision Synthesis: Methodology and Applications. PhD thesis, Duke University, stat.duke.edu/alumni/alumni-lists-theses/phd-year

- Tallman and West (2022) Tallman E, West M (2022) On entropic tilting and predictive conditioning. Technical Report, Department of Statistical Science, Duke University arXiv2207.10013

- Tallman and West (2023) Tallman E, West M (2023) Bayesian predictive decision synthesis. Journal of the Royal Statistical Society (Ser B) 86:340–363

- Tu and Zhou (2011) Tu J, Zhou G (2011) Markowitz meets Talmud: A combination of sophisticated and naive diversification strategies. Journal of Financial Economics 99:204–215

- Wang et al (2023) Wang X, Hyndman RJ, Li F, Kang Y (2023) Forecast combinations: An over 50-year review. International Journal of Forecasting 39:1518–1547

- Wang et al (2016) Wang Y, Ma F, Wei Y, Wu C (2016) Forecasting realized volatility in a changing world: A dynamic model averaging approach. Journal of Banking and Finance 64:136–149

- West (2020) West M (2020) Bayesian forecasting of multivariate time series: Scalability, structure uncertainty and decisions (with discussion). Annals of the Institute of Statistical Mathematics 72:1–44

- West (2023) West M (2023) Perspectives on constrained forecasting. Bayesian Analysis DOI 10.1214/23-BA1379

- West and Harrison (1989) West M, Harrison PJ (1989) Bayesian Forecasting and Dynamic Models, 1st edn. Springer

- West and Harrison (1997) West M, Harrison PJ (1997) Bayesian Forecasting and Dynamic Models, 2nd edn. Springer

- Zhao et al (2016) Zhao ZY, Xie M, West M (2016) Dynamic dependence networks: Financial time series forecasting & portfolio decisions (with discussion). Applied Stochastic Models in Business and Industry 32:311–339