Statistical algorithms for low-frequency diffusion data: a PDE approach

Abstract

We consider the problem of making nonparametric inference in multi-dimensional diffusion models from low-frequency data. Statistical analysis in this setting is notoriously challenging due to the intractability of the likelihood and its gradient, and computational methods have thus far largely resorted to expensive simulation-based techniques. In this article, we propose a new computational approach which is motivated by PDE theory and is built around the characterisation of the transition densities as solutions of the associated heat (Fokker-Planck) equation. Employing optimal regularity results from the theory of parabolic PDEs, we prove a novel characterisation for the gradient of the likelihood. Using these developments, for the nonlinear inverse problem of recovering the diffusivity (in divergence form models), we then show that the numerical evaluation of the likelihood and its gradient can be reduced to standard elliptic eigenvalue problems, solvable by powerful finite element methods. This enables the efficient implementation of a large class of statistical algorithms, including (i) preconditioned Crank-Nicolson and Langevin-type methods for posterior sampling, and (ii) gradient-based descent optimisation schemes to compute maximum likelihood and maximum-a-posteriori estimates. We showcase the effectiveness of these methods via extensive simulation studies in a nonparametric Bayesian model with Gaussian process priors. Interestingly, the optimisation schemes provided satisfactory numerical recovery while exhibiting rapid convergence towards stationary points despite the problem nonlinearity; thus our approach may lead to significant computational speed-ups. The reproducible code is available online at https://github.com/MattGiord/LF-Diffusion.

keywords:

[class=MSC]keywords:

and

1 Introduction

‘Diffusions’ are mathematical models used ubiquitously across the sciences and in applications. They describe the stochastic time-evolution of a large variety of phenomena, including heat conduction [9], chemical reactions [61], cellular dynamics [19] and financial markets [68]. See the monograph [5] for further examples and references. In many situations, the ‘drift’ and ‘diffusivity’ parameters of a stochastic process are not precisely known, and have to be estimated from discrete-time observations of a particle trajectory

| (1.1) |

for some ‘observation distance’ . This is the central inferential problem considered in the present article. Due to their unorthodox likelihood structure, which is implicitly determined by the transition probabilities of , discrete diffusion data have posed formidable difficulties for statistical analysis. While remarkable progresses have recently been made in deriving theoretical recovery guarantees, devising efficient computational algorithms remains a significant challenge – see below for more discussion.

Here, we shall study these issues in a representative nonparametric model for diffusion inside a bounded, insulated, and inhomogeneous medium; possible extensions will be discussed below. Taking, throughout, the diffusion domain to be a subset , , such a system is macroscopically described by the (Fokker-Planck) parabolic partial differential equation (PDE), which we shall refer to as the ‘heat equation’,

| (1.2) |

encapsulating the changes over time in the substance density at each location [34, Chapter 11]. Above, and denote, respectively, the divergence and gradient operators, is the inward-pointing unit normal vector with associated normal derivative , and is a ‘conductivity’ function modelling the spatially-varying intensity at which diffusion occurs throughout the inhomogeneous medium. At the microscopic level, the discretely trajectory of a diffusing particle, started inside , evolves according to the associated stochastic differential equation (SDE),

| (1.3) |

where is a standard -dimensional Brownian motion and the term models reflection of the particle at the boundary via the local time process ; see [71] for details. The connection between the SDE (1.3) and the PDE (1.2) will play a key role throughout this paper.

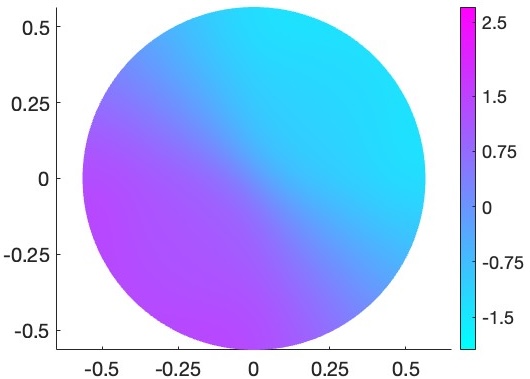

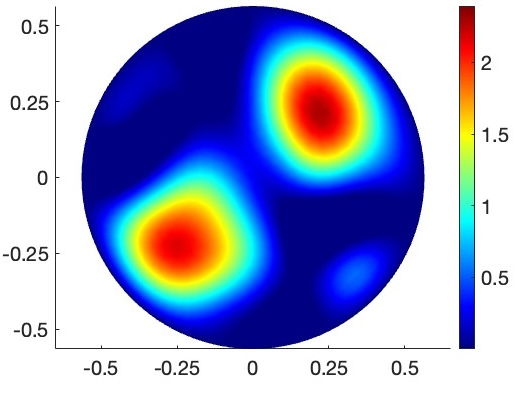

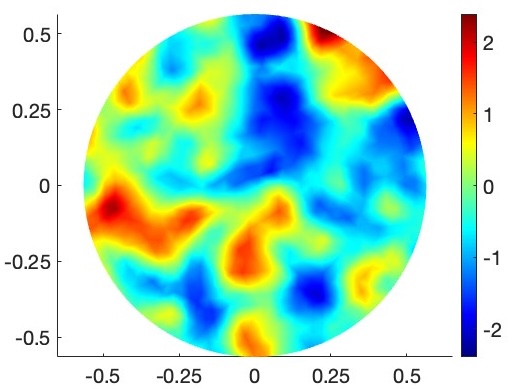

The statistical reconstruction task consists of determining nonparametrically (i.e. within some infinite-dimensional function class) from the discrete measurements (1.1) separated by a (fixed) time lag . Often times, because of the characteristics of the data collection process, cannot be reduced under a certain non-zero threshold – in the statistical literature, this is referred to as the ‘low-frequency’ regime, which is the main setting our PDE techniques will be targeted at. An illustration of the problem with synthetic data is provided in Figure 1. For example, [50, Chapter 1] describes a filtering problem in weather forecasting where measurements are inputted in a large scale dynamical system every few hours; see also [42] for a similar situation in system biology. Other possible approaches based on stochastic analysis which are typically only available with ‘high-frequency’ or continuous-time measurements of will not be pursued here; more discussion can be found below.

Related ‘parameter identification’ problems for the conductivity in diffusion equations have been widely studied in the inverse problem literature, largely in applications where observations of a steady-state system are available in the form of (possibly noisy) point evaluations of the solution of a time-independent elliptic PDE. Among the many contributions, we refer to [20, 46, 51, 75, 1] for models with boundary measurements in the context of the famous ‘Caldéron problem’, and to [64, 32, 70, 57, 37] for interior measurements schemes connected to the ‘Darcy’s flow’ model.

1.1 Challenges

In the present setting, the invariant distribution of the diffusion process in (1.3) can be shown to coincide with the uniform distribution on [10, Chapter 1.11.3], and therefore to be non-informative about the conductivity . Similarly, in the low-frequency regime, many commonly used sample statistics (such as the ‘sample quadratic variation’) cannot be employed to validly estimate [39, Section 1.2.3]. Instead, the problem must rather be approached using the information contained in the transition densities , namely the probability density functions of the conditional laws , and the resulting likelihood function

| (1.4) |

However, apart from certain special cases, the transition densities of diffusion processes, including those of model (1.3), are generally not available in closed form, making the likelihood for low-frequency observations analytically intractable. This is the central issue posing a huge challenge to the design, implementation and theoretical analysis of statistical algorithms.

In such context, a large part of the existing parametric and nonparametric methods relies on computational strategies that involve sophisticated (and often computationally onerous) missing data techniques, whereby the unobserved continuous trajectory between the data points is treated as a latent variable and inputted via simulation schemes for diffusion bridges, enabling the approximation of the likelihood for low-frequency observations by the more tractable one relative to continuous-time measurements. This approach was first pioneered, in general diffusion models, by Pedersen [60] to construct simulated maximum likelihood estimators, and by Roberts and Stramer [65], Elerian et al. [31] and Eraker [33] to implement Bayesian inference with data-augmentation. See [30, 27, 14, 40, 13, 47, 59, 15, 77, 67] and the many references therein.

1.2 Main contributions

In this paper, we adopt a novel PDE perspective to address the computational challenges arising in the nonparametric diffusion statistical model (1.3) with low-frequency observations. Our main contributions are as follows.

-

•

We derive theoretical PDE formulae for likelihoods and gradients which are concretely computable via standard finite element methods for elliptic PDEs.

-

•

We formulate several novel algorithms for posterior sampling and optimisation.

-

•

We implement and numerically demonstrate the efficacy of the algorithms for computing maximum-a-posteriori, maximum likelihood and posterior mean estimates, as well as for posterior sampling.

Let us briefly expand on these points. In Section 2, building on the characterisation of the transition densities appearing in (1.4) as the fundamental solutions of the heat equation (1.2), we first show how the computation of can be reduced to a corresponding time-independent eigenvalue problem for the elliptic (self-adjoint) infinitesimal generator. This will later lead to a simple likelihood evaluation routine, cf. (2.10), that does not require any data-augmentation step. Building on such PDE characterisation, the main theoretical result of this article, Theorem 2.1, is then derived. In particular, we prove a ‘closed-form’ expression for the gradient of the likelihood, by characterising the Frechét derivatives of the maps , for fixed. These are obtained using perturbation arguments for parabolic PDEs and the so-called ‘variation-of-constants’ principle [49, Chapter 4], building on the regularisation step developed by Wang [81] to deal with the singular behavior of the transition densities relative to vanishing time instants. The full argument is fairly technical; it is presented in Appendix A. Again using the self-adjointness of the generator and numerical methods for elliptic PDEs, we then propose an efficient strategy to numerically evaluate the likelihood gradient, which can serve as the building block for the implementation of gradient-based statistical algorithms.

Section 3 details the statistical procedures which we derive from the above theoretical developments. Our results enable a large algorithmic toolbox of common likelihood-based computational techniques – in particular, we pursue both gradient-free (preconditioned Crank-Nicolson, pCN) and gradient-based (unadjusted Langevin, ULA) algorithms for posterior sampling, as well as gradient descent methods. These schemes allow to obtain numerical approximations for posterior mean and maximum a posteriori (MAP) estimates, posterior quantiles for uncertainty quantification, as well as (penalised) maximum likelihood type estimators. The detailed description of the algorithms can be found in Sections 3.2-3.4.

In several simulation studies, presented in Section 4, we apply the above methods to a representative nonparametric Bayesian model with truncated Gaussian series priors. In the large data limit , these priors have recently been shown by Nickl [53] to lead to consistent inference of the data-generating ‘ground truth’ conductivity – but in principle, our numerical methods are also applicable to any other prior distribution, too. Interestingly, [53] undertook a similar PDE-based point of view to prove the injectivity of the nonlinear map from the conductivity to the transition densities, providing the first statistical guarantees for nonparametric Bayesian procedures with multi-dimensional low-frequency diffusion data.

1.3 Related literature and discussion

In the seminal paper [39] by Gobet et al., spectral methods (related to the ones pursued here) were used to obtain minimax-optimal nonparametric estimators in one-dimensional diffusion models. However, it seems challenging to apply their approach to the present multi-dimensional setting, where the elliptic generator defines a genuine PDE. Analogous ideas also underpin the parametric estimators built by Kessler and Sørensen [44] using certain spectral martingale estimating functions. We also mention the works by Aït-Sahalia [3, 4] which (in a parametric setting) derive closed-form likelihood approximations via Hermite polynomials along with resulting approximate maximum likelihood estimators. In contrast to our work, calculations of gradients are not considered there; moreover, the expansions on the eigenbasis of the self-adjoint generator of (1.3) considered here lead to rapidly (i.e. exponentially) decaying remainders terms.

Let us briefly discuss future directions of research which may build on the present work. A first important avenue would be the extension of the developed methodology beyond the (divergence form) diffusion model (1.2)-(1.3). Natural generalisations would e.g. encompass anisotropic diffusions with matrix-valued conductivities, as well as models for diffusion in a ‘potential energy field’; see Section 5 for further discussion. Secondly, our calculations, combined with the results in [53], may also pave the way to proving ‘gradient stability’ properties in the sense of [58]; further see [17], [6] and [52, Chapter 3]. Using the program put forth in [58], a rigorous investigation of the complexity of the employed sampling and optimisation algorithms can then be carried out, with the goal of deriving bounds for the computational cost that scale polynomially with respect to the discretisation dimension and the sample size.

Another interesting question concerns the relationship between the observation time lag , the ‘numerical stability’ of the proposed methodology, and the ‘statistical information’ contained in the sample. While, algorithmically, lower frequency samples imply better spectral approximations of the likelihood and its gradient, higher sampling frequencies allow to capture finer characteristics of the observed process. For very-high frequency or continuous data, likelihood evaluations become tractable via Girsanov’s theorem. Understanding the more detailed ‘phase transitions’ between the different regimes will inform which methods to employ in practice. Recent work has shown that nonparametric Bayesian procedures based on Gaussian priors can achieve optimal statistical convergence rates in the model (1.3) with ‘high-frequency’ observations (where for some ) [43] and with continuous-time observations [78, 62, 80, 55, 38].

2 Likelihood and gradient computation via PDEs

Throughout, let , , be a non-empty, open, bounded and convex set with smooth boundary . It is well-known that for any twice continuously differentiable and strictly positive , , and any given starting point the SDE (1.3) has a unique path-wise solution , constituting a continuous-time Markov diffusion process reflected at the boundary (since and are Lipschitz); see [71]. In view of these regularity assumptions, for some we maintain

| (2.1) |

as the parameter space. Recall the low-frequency observations from (1.1) with measurement distance , which we shall keep fixed throughout.

2.1 Parabolic PDE characterisations

The Markov property of implies that the likelihood of any factorises as a product of the (symmetric) transition densities ; cf. (1.4). These characterise the conditional laws

| (2.2) |

and more generally the transition operator

| (2.3) |

acting on square-integrable test functions . The semigroup is known to play the role of the ‘solution operator’ for the heat equation (1.2); thus the transition densities also constitute the fundamental solution to (1.2). Informally, this means that for fixed, the map solves (1.2) with Dirac initial condition,

| (2.4) |

Here, we denoted by the elliptic divergence form operator

a notation that we will use throughout. The operator , with domain given by the set of functions in the Sobolev space with zero Neumann boundary conditions,

constitutes the infinitesimal generator of the process (1.3). While the transition density functions are not available in closed form, their characterisation through (2.4) implies a convenient spectral expansion in terms of the eigenpairs of the generator , cf. (2.9), which we will use below for evaluating the likelihood .

A more intricate question is whether the gradient of the likelihood function also satisfies a PDE characterisation which can be exploited for computational purposes. The key challenge is thus to understand the perturbations of the nonlinear map , which turns out to provide insight into the preceding question – this is the content of Theorem 2.1. To understand the intuition behind the theorem, let us fix some perturbation such that . Then, subtracting the PDE (2.4) for and for yields immediately that the difference solves (again, informally)

which is another instance of the heat equation, now with an inhomogeneity and with zero initial conditions. A natural candidate for the linearisation (in ) of the right hand side is , and thus in turn provides a natural candidate for the linearisation of the transition densities. Here, we have written to informally denote the linear ‘solution operator’ to an inhomogeneous heat equation with zero initial condition, which under suitable regularity conditions is given by the variation-of-constants formula – see e.g. Chapter 4 of [49].

Making the above argument rigorous is technically delicate due to the singularity of and of the source term for , which makes the standard parabolic regularity theory (e.g. from [49]) not directly applicable. Thus, one needs to clarify in which sense the above PDEs hold, and whether existence and uniqueness can be guaranteed suitably for to be well-specified. Generalising a regularisation technique developed in [81] (in a related one-dimensional model), we accomplish this in the ensuing theorem for dimensions , proving a variation-of-constants representation for the linearisation of . For and fixed, define the operator

where is given by (2.1). Note that depends nonlinearly on .

Theorem 2.1.

Suppose that , that and fix any . Then, the Fréchet derivate of at is given by the following linear operator

| (2.5) |

More specifically, for any and , there exist and such that for any with and ,

| (2.6) |

Here, can be chosen independently of and , as above.

The preceding theorem states that the map is Fréchet differentiable with respect to , with derivative at identified by the linear operator (2.5). In particular, this is implied by the remainder estimate (2.6), which holds uniformly for and in balls of the Hölder space . The proof of the result can be found in Appendix A. Note that our derivative is obtained ‘pointwise’ in , thus rigorously providing a gradient formula for conditional on any data rather than just in ‘quadratic mean’, a weaker regularity condition in terms of which several key results from asymptotic frequentist statistical theory [79] are formulated. Differentiability in quadratic mean is, in particular, implied by Theorem 2.1.

In fact, by the same proof techniques that we employ for Theorem 2.1, one can show that the Frechét derivative is Hölder continuous (with respect to the operator norm). Such regularity statements for gradients are essential for understanding the discretisation error incurred by the algorithms constructed below, and thus may be important for future work. The proof is presented in Section 6.1.

Theorem 2.2.

Assume the setting of Theorem 2.1 and let . Then, there is some (independent of ) and some such that for all with , as well as ,

2.2 Reduction to elliptic eigenvalue problems

By the divergence theorem, e.g. [26, p. 171], if then

which shows that is self-adjoint with respect to the inner product of . By a suitable application of the spectral theorem (e.g. [72, p. 582]), we deduce the existence of an orthonormal system of eigenfunctions and of associated (negative) eigenvalues such that

| (2.7) |

We will take throughout the increasing ordering , . Then it holds that is constant with corresponding eigenvalue , independently of . For notational convenience, we shall take , so that . Also, by ellipticity, the first non-zero eigenvalue satisfies the ‘spectral gap’ estimate for some constant only depending on and . The eigenvalues diverge following Weyl’s asymptotics as , with multiplicative constants only depending on , and . These facts follow similarly to the arguments for the Neumann-Laplacian (here corresponding to the case ) developed in [72, p. 403f], in view of the boundedness and the boundedness away from zero of . For details, see [53, Section 3].

Using such a spectral analysis of the generator, we can represent the action of the transition operator from (2.3) on any ‘initial condition’ by

| (2.8) |

Accordingly, the transition densities (2.2), which form the integral kernels of , satisfy

| (2.9) |

We conclude that for any , if we have numerical access to the eigenpairs , the likelihood may be evaluated using the spectral formula

| (2.10) |

Upon closer inspection, we can also derive a spectral representation of the Frechét derivatives from Theorem 2.1. Indeed, since the transition density functions and the transition operators can be expanded with respect to the same eigenpairs of , we obtain a convenient double series expansion of the integrand in (2.5). This further allows to separate the spatial and time dependency, leading to a closed form expression for the integration in time, which avoids potential numerical instability caused by the singular behaviour of the integrand for . In summary, the following spectral characterisation of the linear operator is obtained; see Section 6.2 for the proof.

2.3 Numerical PDE methods

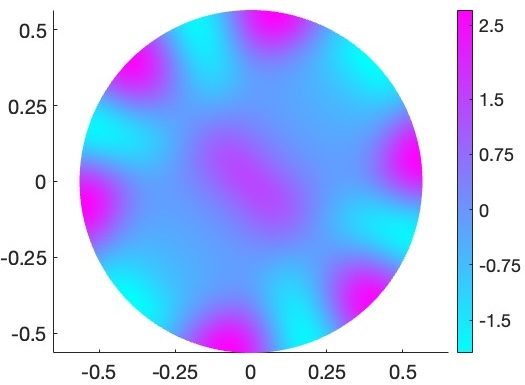

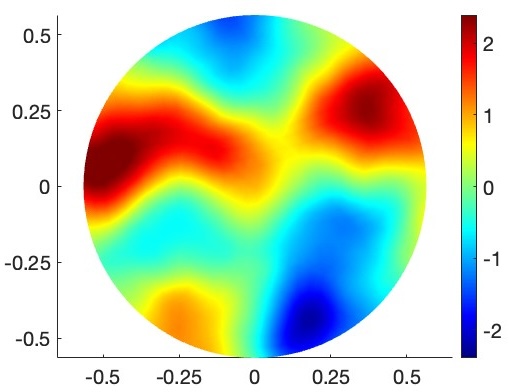

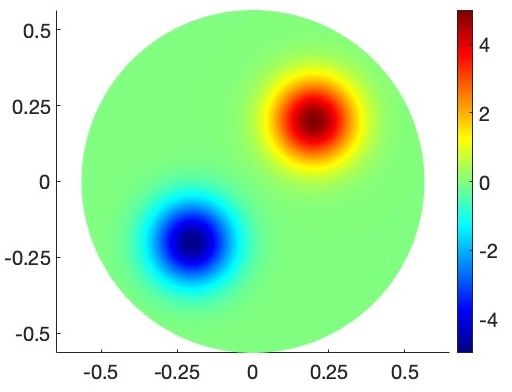

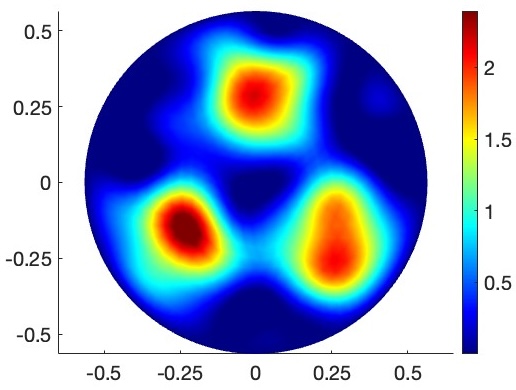

While the eigenpairs are generally not available in closed form, the elliptic eigenvalue problem (2.7) has been widely investigated in the literature on numerical techniques for PDEs, with foundational work by Vainikko [76] and later landmark contributions in [18, 21, 28, 7, 45] among the others. We further refer to the monograph [8] and to the recent survey article [16] for overviews. Specifically, the problem can be tackled with efficient and reliable Galerkin methods (e.g., of finite element type), returning approximations of the first non-constant eigenfunctions; see Figure 2 for an illustration. The superscript is used as a proxy for the parameter governing the reconstruction quality of the employed numerical method, in the sense that smaller values of yield smaller approximations errors, with convergence when (cf. Remark 2.4 below). For example, in standard finite element methods based on piece-wise polynomial functions defined over a triangular mesh covering the domain, is typically chosen to be an upper bound for the side length of the mesh elements.

Based on such numerical techniques, the computation of the transition density functions and the likelihood via the spectral characterisations (2.9) and (2.10) respectively can be concretely performed by replacing the eigenpairs with their approximations, and by truncating the series at level , resulting in the simple routines

| (2.12) |

| (2.13) |

This is the likelihood approximation that we will employ in Section 3.2 for the implementation of posterior sampling via the pCN method [22].

Turning to the gradient, for any fixed direction , the Frechét derivative can be efficiently computed according to the formula from Corollary 2.3, analogously truncating the double series at some level , and replacing the eigenpairs with their numerical approximations. For a stable computation of the two internal series, since for eigenvalues with multiplicities finite element methods generally return distinct approximations that differ by small amounts, the conditions and should be replaced by the requirements and , respectively, for a sufficiently small threshold to be specified by the user. This results in the derivatives evaluation routine

| (2.14) |

which will serve as a basis for the implementation of gradient-based statistical algorithms. In particular, upon discretising the parameter space , the log-likelihood gradient can be derived from an application of the chain rule and the above derivative formulae, wherein the directions are identified by the ‘coordinates’ in the chosen discretisation scheme – see Section 3.1 below for details.

Remark 2.4 (Numerical approximation errors).

The numerical routines (2.13) and (2.14) entails two sources of approximation errors, arising, respectively, from the numerical solution of the elliptic eigenvalue problem (2.7) and the truncation of the series appearing in (2.10) and (2.11). For the latter, explicit error bounds readily follow from Weyl’s asymptotics, the available estimates for the norm of the eigenfunctions, and since is fixed. For instance, by Corollary 1 in [53], provided that lies in a Sobolev space of sufficient smoothness , the series term of the numerical likelihood formula (2.13) satisfies, for arbitrarily small and for constants only depending on , and ,

for all large enough and all , whereupon the tails of the series in (2.10) are seen to decay exponentially. Thus, depending on the application at hand and the magnitude of the time lag between consecutive observations, a relatively low truncation level in (2.13) may be expected to yield the desired accuracy level.

Concerning the numerical solution of the elliptic eigenvalue problem (2.7), there is a wide literature developing error analyses for a variety of finite element methods; see [16] and references therein. Among these, well-known results for the widespread approach based on piece-wise polynomial approximating functions over a triangulation of the domain, combined with the norm estimates in Corollary 1 in [53], assuming again that for some , yield the error bound for the eigenvalues

| (2.15) |

with constants only depending on , and , and where is the (user-specified) maximal side length for the elements in the triangular mesh, cf. [7, Section 10.3]. Analogous bounds also holds for the approximation errors in Sobolev norms of the eigenfunctions. Note that the estimate (2.15) deteriorates as the index grows, due to the more pronounced oscillatory behaviour that the eigenfunctions tend to exhibit at higher frequencies. However, as observed earlier, in the presence of a fixed time lag , only a small number of eigenpairs are generally needed to approximate the series in (2.10) and (2.14) with high accuracy, so that we may expect the overall error resulting from the numerical solution of the eigenvalue problem (2.7) by finite element methods to be small even for a relatively coarse triangular mesh.

Remark 2.5 (Computational cost).

The numerical approximation of the eigenpairs underpinning the proposed computational approach can be performed via the off-the-shelf PDE solvers implemented in many mathematical and statistical software. Since, in light of Remark 2.4, only a small number of eigenpairs is needed in practice, such step is generally computationally inexpensive, at least for applications in low dimensional domains (including the relevant physical cases ). For reference, the approximation of the first eigenpairs associated to the conductivity function displayed in Figure 1 (left) required around seconds on a MacBook Pro with M1 processor, using the finite element method implemented in MATLAB R2023a Partial Differential Equation Toolbox, based on a discretisation of the domain with an unstructured triangular mesh comprising 1981 nodes. Since the routines (2.13) and (2.14) only require a single numerical solution of the eigenvalue problem (2.7), and only further involves exponentiation, products and sums, we then obtain an overall comparable computational cost, with no additional bottlenecks. In fact, for the numerical likelihood formula (2.13), since handling a larger number of observations only implies a linear growth in the number of product terms, the proposed approach results to be extremely scalable with respect to the sample size.

3 Applications to statistical algorithms

We now turn to the problem of estimating the conductivity function from the low-frequency diffusion data . Leveraging the novel approach developed in Section 2, we gain direct access to the large algorithmic toolbox of likelihood-based nonparametric statistical inference, overcoming the need of computationally expensive data-augmentation techniques [65, 14, 59, 77, 67]. For illustration, we shall consider below, within a representative Bayesian model, instances of:

-

•

Gradient-free Metropolis-Hastings MCMC algorithms for posterior sampling;

-

•

Gradient-based posterior sampling methods of Langevin type;

-

•

Gradient-based optimisation techniques for the computation of the MAP estimates (i.e. penalised MLE).

3.1 A nonparametric Bayesian approach with Gaussian priors

We shall focus on nonparametric Bayesian procedures with prior distributions arising from Gaussian processes. These are among the most universally used priors on function spaces in applications, e.g. [63, 70, 52], [36, Chapter 7] and [35, Chapter 11], and in the estimation problem at hand they have recently been shown by Nickl [53] to lead to ‘asymptotically consistent’ posteriors that concentrate around the ground truth as the sample size increases. For concreteness, let us follow in this section the prior construction of [53]; more general classes will be considered in Appendix C.

3.1.1 Parametrisation

In order to incorporate the point-wise lower bound required in the definition (2.1) of the parameter space , we model any as

| (3.1) |

for some real-valued and for some smooth and strictly increasing link function (e.g. the standard choice ). Under such bijective reparametrisation, we regard as the unknown functional parameter to be estimated and discretise it by

| (3.2) |

where , , are the (smooth) non-constant eigenfunctions of the standard Neumann-Laplacian with associated (strictly positive) eigenvalues , solving (2.7) with , cf. [72, p. 403f]. Correspondingly, we write .

3.1.2 Prior and posterior

We assign to in (3.1) a truncated Gaussian series prior by endowing the vector of Fourier coefficients in (3.2) with the diagonal multivariate Gaussian prior

| (3.3) |

In the following we will, in slight abuse of notation, interchangeably write for the prior (3.3) on as well as for the resulting push-forward priors on and . By Bayes’ formula (e.g., [35, p. 7]), the posterior distribution of has probability density function (with respect to the Lebesgue measure of )

| (3.4) |

where is the log-likelihood of , that is

| (3.5) |

Remark 3.1 (-regular Gaussian priors).

For fixed , the prior (3.3) induces a multivariate Gaussian distribution on the -dimensional linear space spanned by the eigenfunctions . For , the prior converges towards an infinite-dimensional ‘-regular’ Gaussian probability measure with RKHS included into the Sobolev space , e.g. arguing as in the proof of Lemma 2.3 in [38], using Proposition 2 in [53] and the results in Section 11.4.5 of [35]. In fact, Theorem 10 in [53] gives a precise growth condition on as a power of the sample size that leads, under certain additional regularity conditions, to rates of contraction for the associated posterior distribution.

3.1.3 Gradients of log-posterior densities

A careful application of Theorem 2.1 and of the chain rule to the maps , , implies the differentiability of the posterior density (3.4) (and of its logarithm). We identify the resulting formula for the gradient in the next proposition.

Proposition 3.2.

In view of the developments presented in Section 2, the concrete implementation of the above characterisation of the partial derivatives can be approached by replacing the transition densities and the Frechét derivatives with their numerical counterparts and defined as after (2.12) and (2.14) respectively. This results in the gradient evaluation routine , where

| (3.7) |

For the latter, we note that a single solution via finite element methods of the elliptic eigenvalue problem (2.7) with is required across all the partial derivatives, whereupon the exponential coefficients appearing in (2.14) can also be calculated before the specification of the directions . Thus, overall, the numerical gradient formula (3.7) is only marginally computationally more expensive than the efficient likelihood evaluation routine (2.13).

3.2 Posterior inference via the pCN algorithm

To perform inference based on the posterior density (3.4), we begin by considering the class of ‘zeroth-order’ Metropolis-Hasting MCMC sampling methods, whose implementation in the present setting is readily enabled by the numerical likelihood formula (2.13). We focus here on the widespread pCN algorithm [22]. Given the low-frequency diffusion data (1.1) and under the prior construction (3.3), the algorithm generates a -valued Markov chain by repeating the following steps, given some initialisation point ,

-

1.

Draw a prior sample and for a given ‘stepsize’ define the ‘proposal’ .

- 2.

The first step only involves the straightforward task of drawing a sample from the diagonal multivariate Gaussian prior . The second step requires the evaluation of the proposal likelihood , which is achieved through the routine (2.13). Apart from the latter, all the operations involved within the two steps are elementary; therefore the computational complexity of each pCN iteration is largely driven by the cost of evaluating the numerical likelihood formula (2.13). One can thus expect generally modest computation times, cf. Remark 2.5. An excellent scalability with respect to the sample size is also obtained.

The proposals and acceptance probabilities prescribed by the pCN algorithm are of Metropolis-Hastings type, e.g. Proposition 1.2.2 in [52], so that the generated Markov chain can be shown to be reversible and to have invariant probability measure equal to the posterior distribution , cf. [73]. The posterior mean estimator is then numerically evaluated through the Monte Carlo average for some large , typically after discarding an initial ‘burnin’ batch of iterates in order to account for the convergence from the initialisation point towards equilibrium. Similarly, the posterior quantiles can be approximated by the empirical quantiles of the MCMC samples. The corresponding posterior mean estimator of the unknown functional parameter is given by

| (3.9) |

As argued in [22], the pCN algorithm leads to well-defined MCMC methods in function spaces whose performance has certain robustness properties with respect to the discretisation dimension (here, the truncation level ), in that its acceptance probabilities do not deteriorate under a discretisation refinement.

3.3 Posterior inference via the unadjusted Langevin algorithm

In alternative to the pCN algorithm laid out above, the results of Section 2 can also be used to build a variety of gradient-based iterative methods, which, through the incorporation of the resulting geometric information on the likelihood surface, may achieve potentially significant improvements in the efficiency of exploration of the parameter space.

Here, we shall consider approximate sampling from the posterior density (3.4) via MCMC algorithms of Langevin type, arising from the discretisation of the Langevin SDE

| (3.10) |

where is a standard -dimensional Brownian motion, and is as after (3.6). The solution to (3.10) is well-known to have stationary distribution equal to the posterior , as the latter can be shown to be invariant with respect to the associated infinitesimal generator, cf. p. 45-47 in [10].

Among the posterior sampling methods based on the SDE (3.10), let us focus on the unadjusted Langevin algorithm (ULA) which is obtained by an Euler-Maruyama discretisation. Specifically, for a stepsize , the ULA generates an -valued Markov chain via

| (3.11) |

whereby the characteristics of are approximated by their empirical analogues relative to a sufficiently high number of ULA samples (e.g. as in (3.9) for the posterior mean).

From (3.11), it is seen that the central operation underlying each step of the ULA is the computation of the gradient of the log-posterior density for the current state of the chain. In the problem at hand, this task can be efficiently (and scalably) performed in concrete via the evaluation routine (3.7).

Employing the proposed computational approach, further gradient-based MCMC methods can similarly be implemented. For example, in the popular Metropolis-adjusted Langevin Algorithm the ULA updates (3.11) are used to construct the proposals within a Metropolis-Hastings architecture, and are subject to an accept-reject step similar to the one specified for the pCN algorithm in (3.8), leading to similar dimension-robustness properties. We refer to [66, Section 1.4] and [22, Section 4.3] for more details and references.

3.4 MAP estimation via gradient descent

Lastly, it is also of interest to consider optimisation techniques. In particular, given the posterior density in (3.4), the associated MAP estimator is defined as any element

| (3.12) |

In fact, identifying, through the parametrisation (3.2), conductivities with the corresponding coefficient vectors , the MAP estimator is seen to be a discretisation of the penalised MLE

where is the likelihood in (1.4), and where the Sobolev norm penalty corresponds to the limit of the RKHS norm for the truncated Gaussian series prior (3.3) when , cf. Remark 3.1.

A standard approach to solve the optimisation problem (3.12) is the gradient-descent algorithm, prescribing the iteration of

| (3.13) |

The MAP estimator is then concretely computed through the output of the step, for some typically chosen according to a suitable convergence criterion. The associated MAP estimator of the reparametrised functional coefficient is approximated by

Similarly to the ULA for posterior sampling described in Section 3.3, the single gradient evaluation required at each iteration of the gradient descent algorithm (3.13) can be tackled via the efficient routine (3.7).

Remark 3.3 (Multimodality of the posterior).

In view of the nonlinear dependence of the transition densities on the conductivity function , cf. (2.9), the log-likelihood and the log-posterior density are generally non-concave and potentially multimodal. This can indeed be seen in our numerical experiments; see Appendix C. Thus, while gradient-based iterative schemes may be able to compute global maximisers under specific conditions and ‘warm starts’ (see e.g. [32, Chapter 11], [58]), in general one should only expect to reach convergence towards a local optimum. The global convergence behaviour of gradient-based schemes in SDE models is a highly challenging topic for future research.

On the other hand, compared to MCMC algorithms, optimisation methods are generally computationally attractive, in that they typically require only a small fraction of the number of iterations. In our simulation studies, the MAP estimates also yielded satisfactory reconstructions; see Section 4.5. We further note that, in the present setting, the latter could also be used in conjunction with the posterior samplers described in Section 3.2 and 3.3 as a fast-to-compute initialisation point, reducing the associated burnin times.

4 Numerical experiments

| 500 | 1000 | 2500 | 5000 | 10000 | 50000 | |

| .4846 | .3953 | .3532 | .3343 | .3188 | .2097 | |

We tested the proposed computational approach in extensive simulation studies, using the ‘non-parametric’ Bayesian model introduced in Section 3.1. Here, we present part of the results, while deferring further examinations to Appendix C. All the numerical experiments were carried out on a MacBook Pro with M1 processor (and 8GB RAM), to which the reported computation times refer. All the required finite element computations for elliptic eigenvalue problems were performed using MATLAB Partial Differential Equation Toolbox (R2023a release), based on a triangulation of the domain comprising 1981 nodes (with maximal side length ).

4.1 Data generation

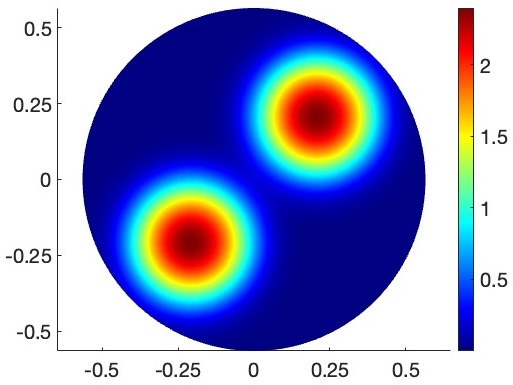

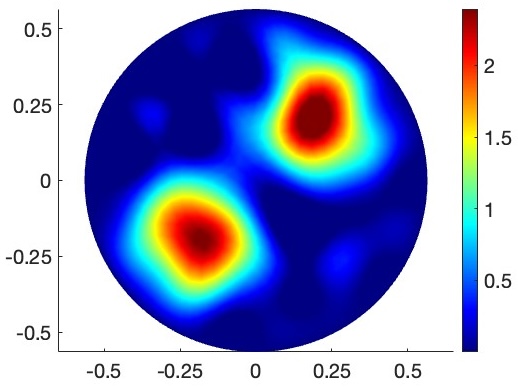

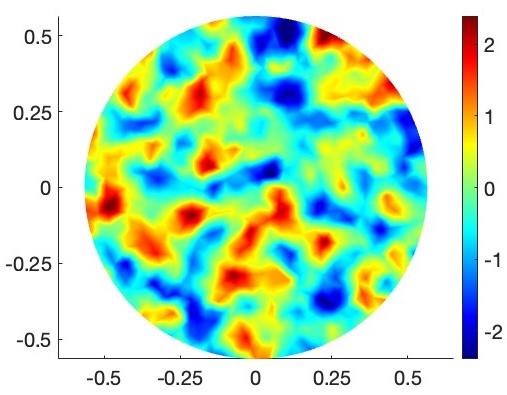

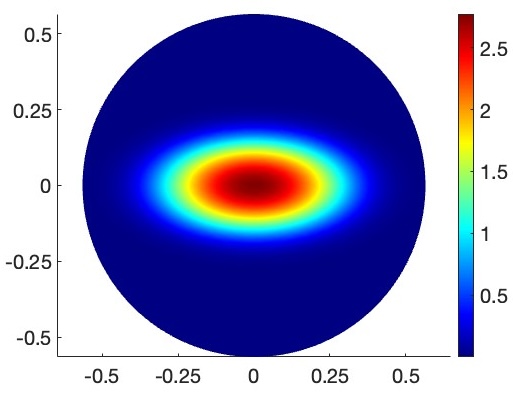

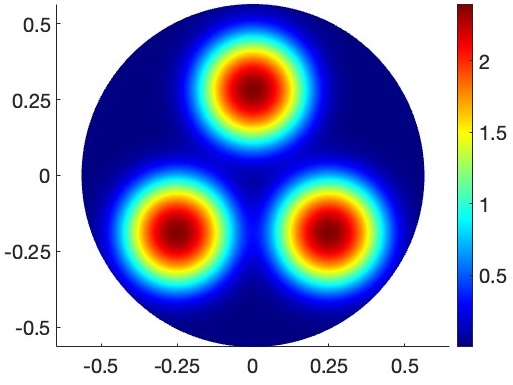

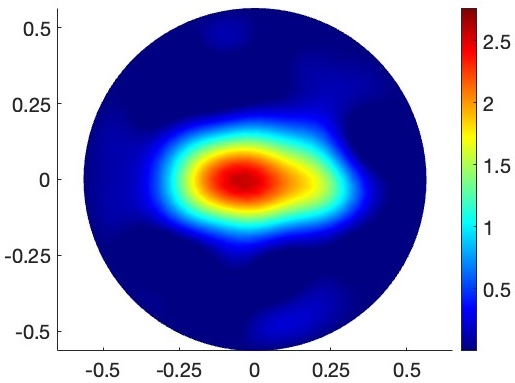

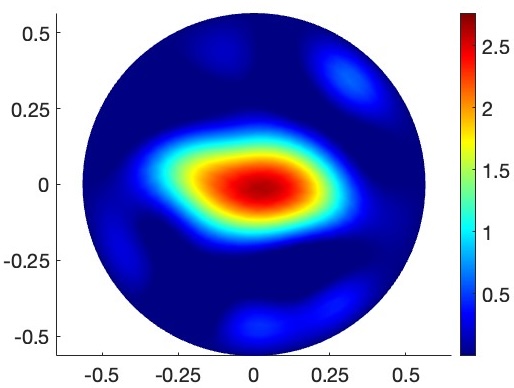

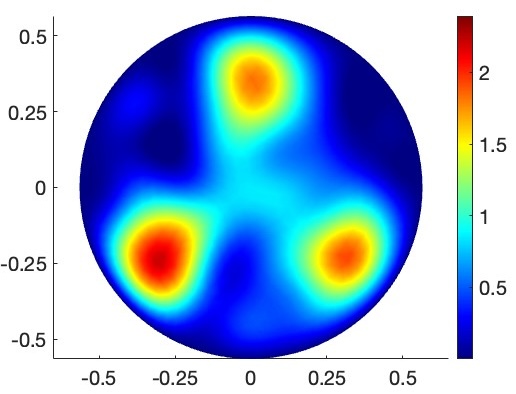

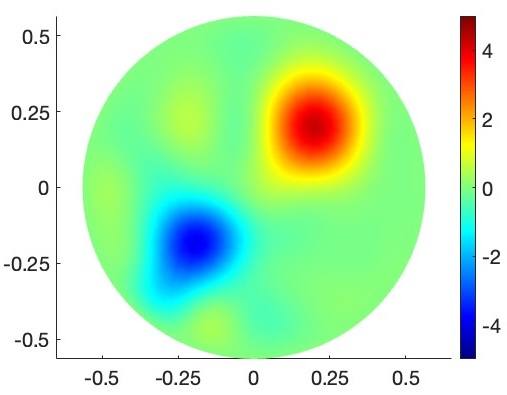

Throughout, we used the unit area disk as the working domain, and took the true conductivity function to be , cf. Figure 1 (left). The trajectory of the diffusion process (1.3) was simulated via the Euler-Maruyama scheme, generating the sequence of ‘continuous-time’ states by the iteration

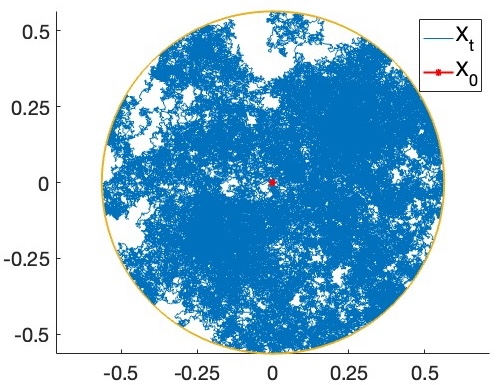

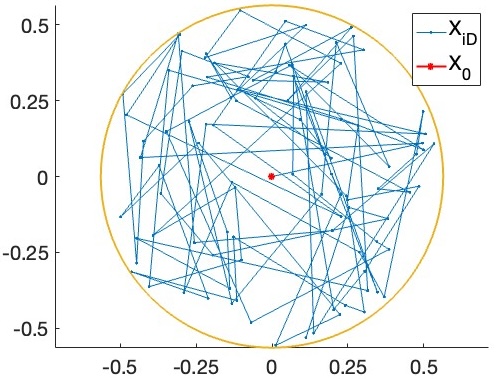

suitably modified to incorporate (elastic) reflections at the boundary; see Figure 1 (centre). We set the initial condition at the origin, specified the time stepsize by , and repeated the scheme for times, giving the overall time horizon . From the simulated trajectory, discrete observations were then sampled with time lags according to , cf. Figure1 (right). Note that , resulting in a realistic representation of the scenario with low-frequency data.

4.2 Parameterisation and prior specification

Across the experiments, we used the truncated Gaussian series priors from (3.3), with the same truncation level , regularity and variability . Moreover, we used the parameterisation of conductivities given by (3.1)-(3.2), with link function and . The -norm of the reparameterised ground truth is , while the -approximation error resulting from ‘projecting’ onto the linear space spanned by the eigenfunction equals , leading to a ‘benchmark’ relative error of .

4.3 Results for the pCN algorithm

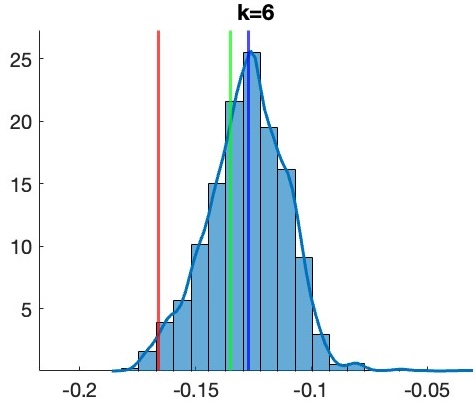

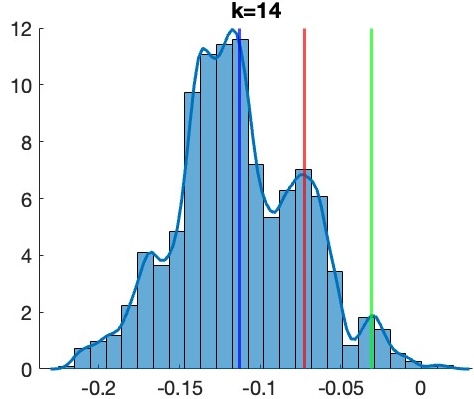

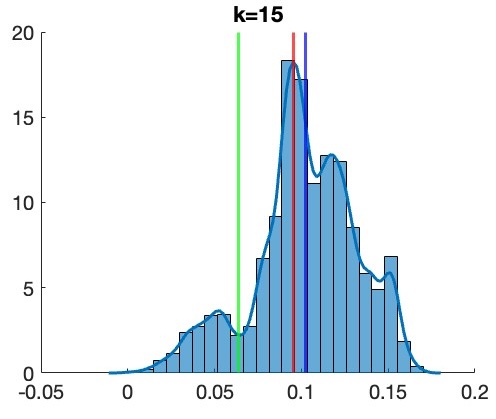

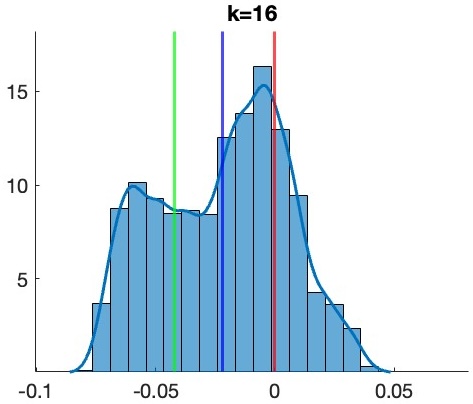

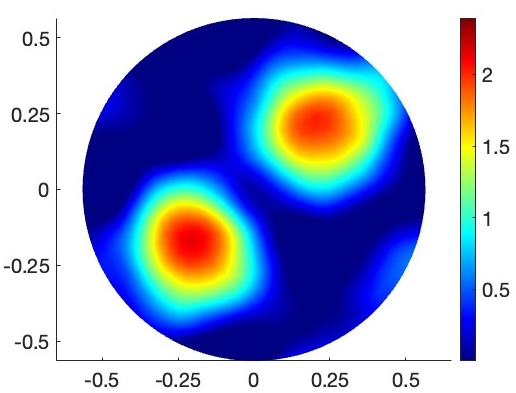

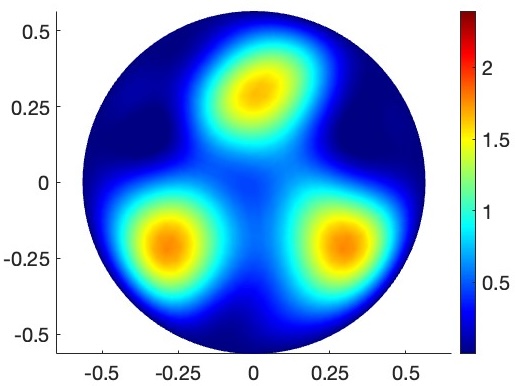

We begin by presenting the results for the pCN algorithm from Section 3.2. The Monte Carlo approximations for the posterior mean estimators of are plotted in Figure 3, with increasing sample sizes . As expected from the posterior consistency result of [53], they show a progressive improvement in the quality of reconstruction. Table 1 reports the obtained -estimation errors for the posterior mean estimates.

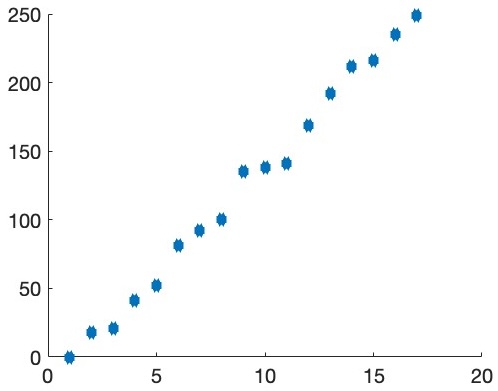

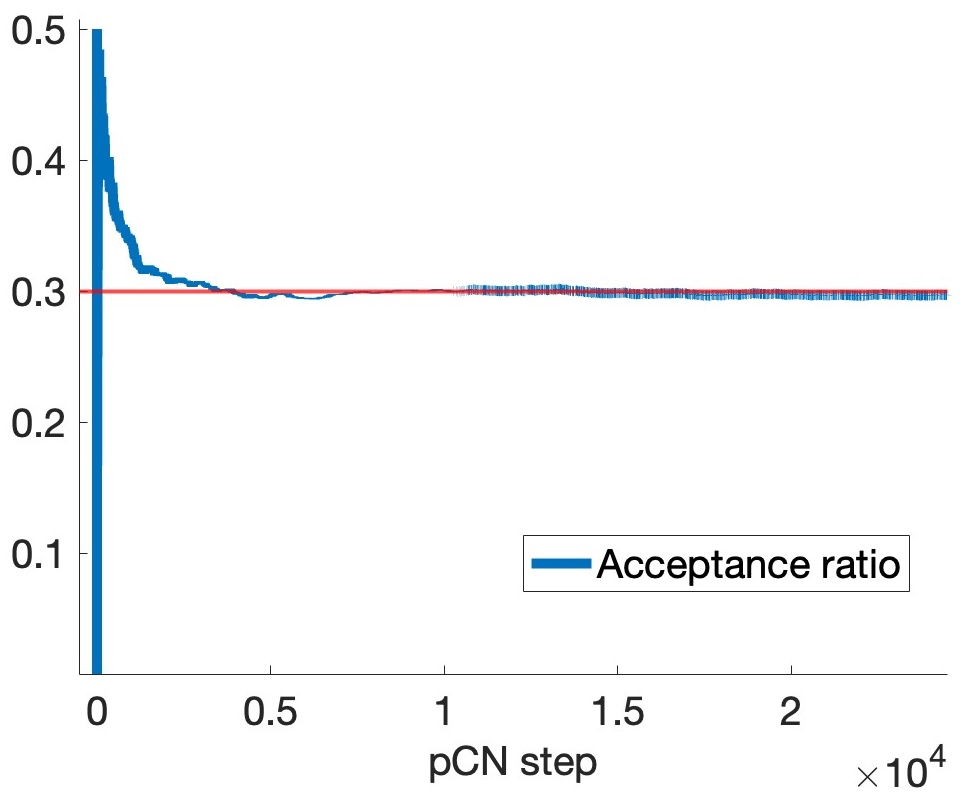

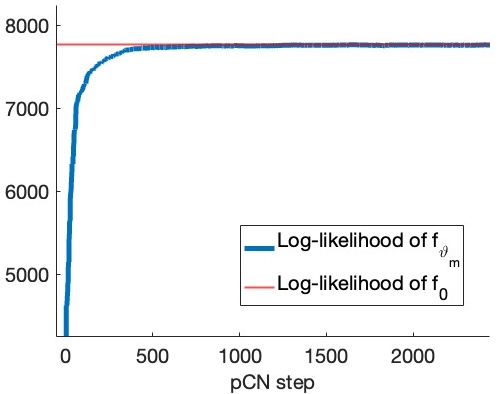

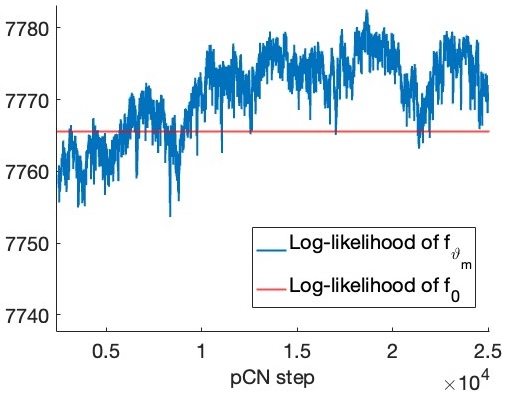

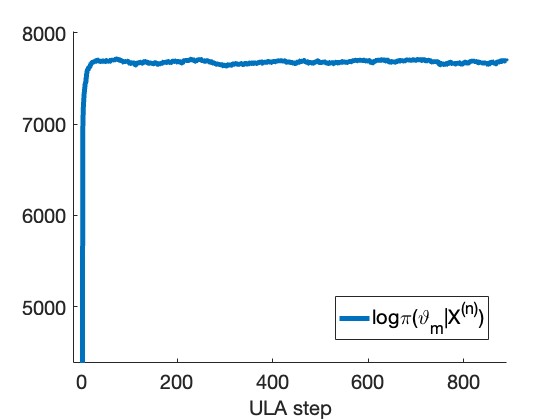

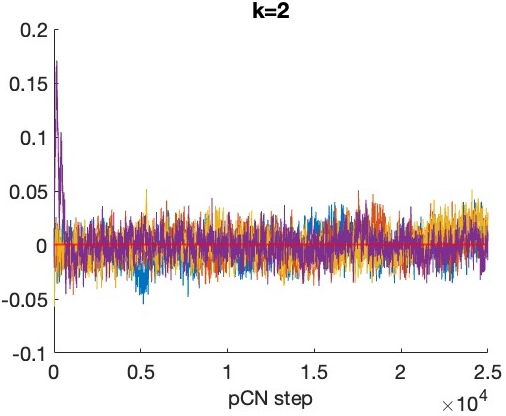

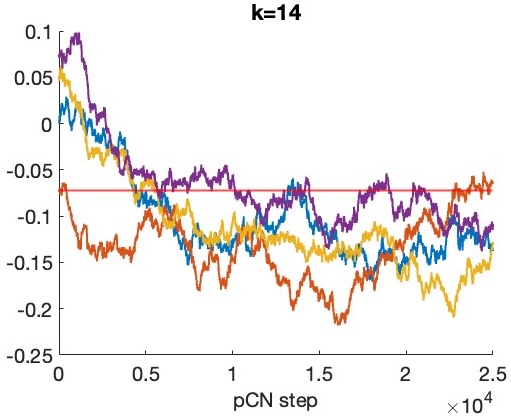

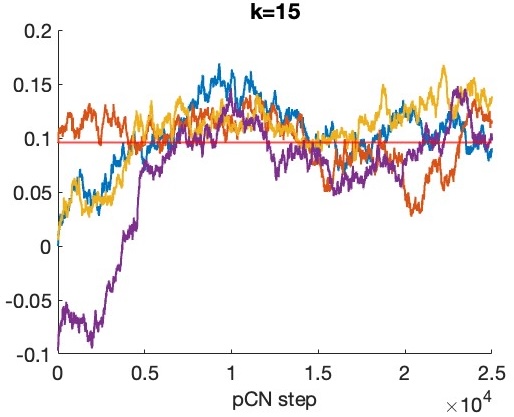

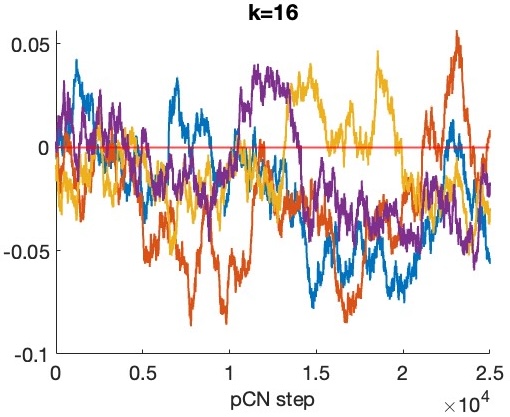

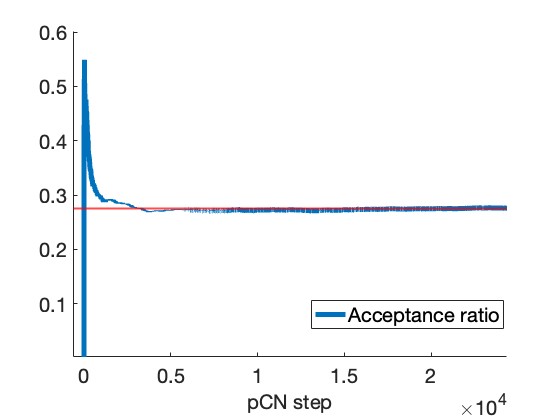

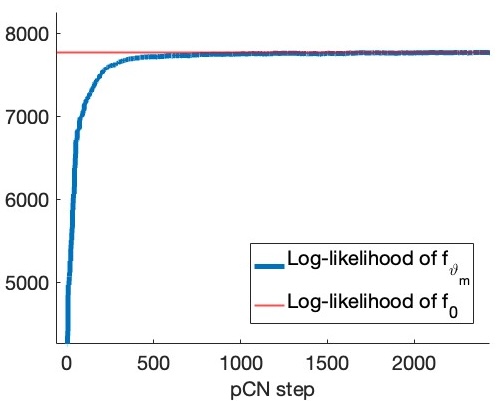

The stepsize in the pCN algorithm was chosen (depending on the sample size) amongst , to achieve acceptance probabilities of around after the burnin phase, cf. Figure 4 (left). Each run of the posterior sampler was initialised at the ‘cold start’ and was terminated after iterations, discarding the first 2500 ones as the burnin. During such burnin phases, the generated chains were observed to effectively move from their starting points towards the region where the posterior concentrates. This is visualised, for , in Figure 4 (centre and right) via the trace-plot of the associated log-likelihood values, which rapidly increase towards and then oscillate around the log-likelihood of the ground truth.

For each pCN step, the evaluation of the likelihood ratios to compute the acceptance probabilities (3.8) was carried out via the routine (2.13). The truncation level for the series in (2.13) was chosen adaptively across the iterations so to include all the approximate eigenvalues , after which the exponentially decaying coefficients in (2.13) satisfy for all . For the run with sample size , the chain steps took approximately 56 minutes, with an average computation time of .13 seconds per iteration.

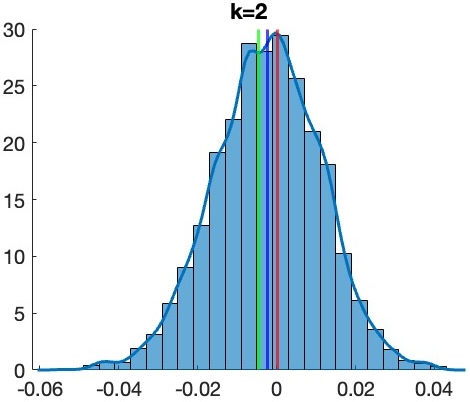

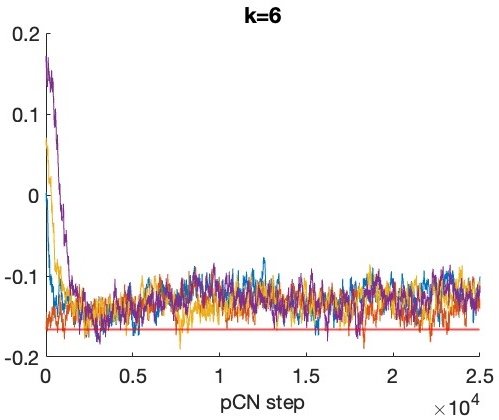

Further details on the results obtained via the pCN algorithm are provided in Appendix C, including chain trace-plots and the resulting approximate marginal posterior distributions of the Fourier coefficients . Additional numerical experiments will also be discussed, investigating the role of the initialisation point, the implementation of other classes of Gaussian priors, and the recovery of different ground truths.

4.4 Results for the ULA

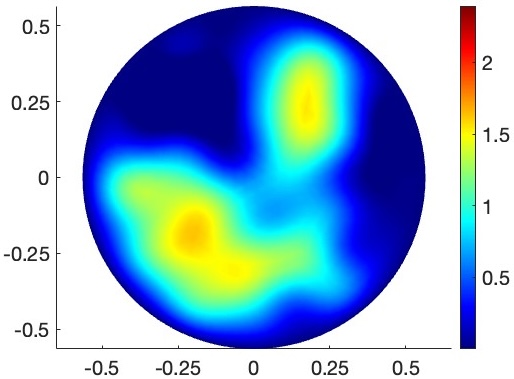

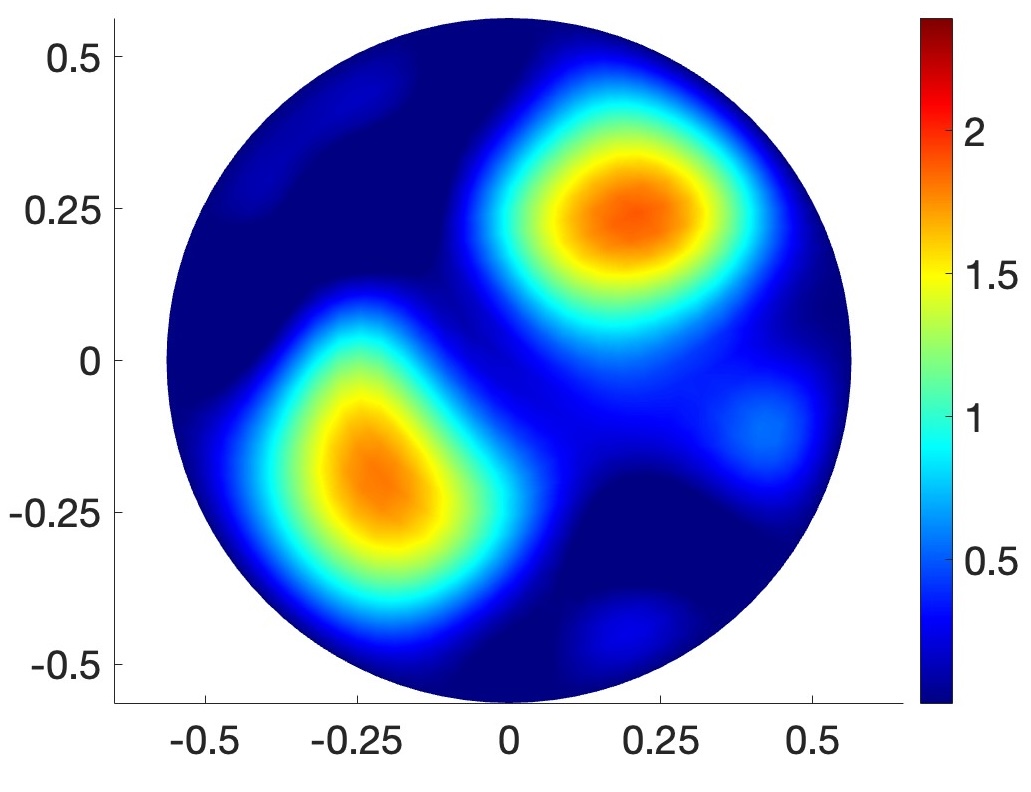

Based on the same domain, ground truth, synthetic data set , with , and prior specification used in Section 4.3, we next considered posterior sampling via the ULA, cf. Section 3.3. Figure 5 (left) shows the resulting (Monte Carlo approximations to the) posterior mean estimate of the reparametrised conductivity function . The corresponding -estimation error was , yielding a relative error of .

A total of iterations of the ULA were used, with stepsize and initialisation point . Compared to the pCN method, through the incorporation of the gradient, the ULA chain was observed to move very efficiently towards the regions of higher posterior probability, which is visualised in Figure 5 (right) by the rapid increase and subsequent stabilisation of the log-posterior density. Accordingly, a shorter burnin of 250 samples was employed. Within each iteration of the ULA, the required gradient evaluation was performed through the routine (3.7). The computational parameters (including the choice of the truncation level ) for the finite element method were specified exactly as for the pCN method in the previous section. The runtime of the ULA was around 90 minutes, with an average computation time of .54 seconds per iteration.

4.5 Results for the MAP estimator (via gradient descent)

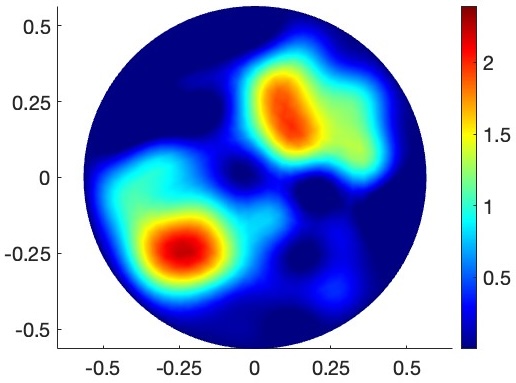

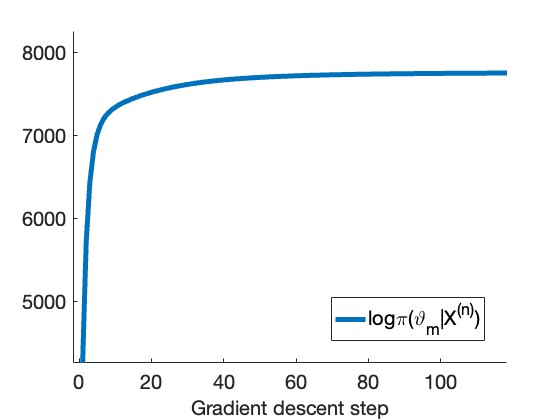

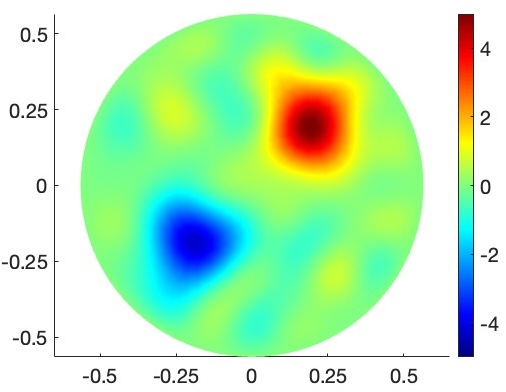

We conclude by presenting the numerical recovery results for the optimisation methods described in Section 3.4. The MAP estimate arising from the same prior (and dataset) employed in Sections 4.3 and 4.4 is shown in Figure 6 (left), with associated -estimation error equal to (and relative error of ).

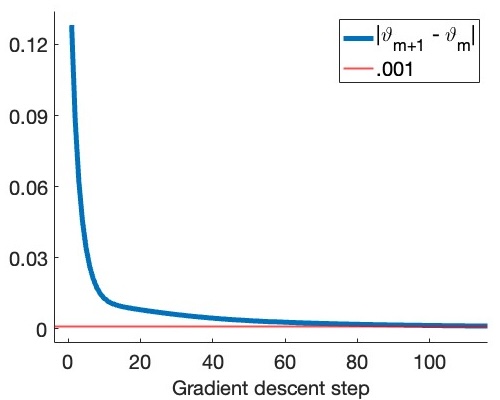

The MAP estimate was computed via the gradient descent algorithm, initialised at and run, with stepsize , until the verification of the convergence criterion . In total, iterations were necessary to achieve convergence; see Figure 6 (centre). See Figure 6 (right) for the trace-plot of the log-posterior density along the steps of the scheme, which exhibits a rapid increase over the initial iterations, similarly to the ULA. The required evaluation of the log-posterior density gradient was performed exactly as outlined in Section 4.4, resulting in an overall computation time of around 1 minute.

Interestingly, the obtained MAP estimate appears to be visually close in shape to the posterior means calculated via the pCN algorithm and the ULA, with a relatively comparable estimation error. This is despite the multimodality of the posterior and the consequent convergence of the gradient descent towards a local maximum; furhter see Appendix C.

5 Summary and further discussion

In this article, we have developed novel approaches to statistical inference with discrete observations from a class of stochastic diffusion models. Using the PDE characterisation of the transition density functions as fundamental solutions of certain divergence-form heat equations, we have employed abstract parabolic PDE arguments to derive a novel closed-form expression for gradients of likelihoods. Leveraging spectral theory for the elliptic generators, we have then derived powerful series representations for the likelihood and its gradient. Computationally, we have argued (and demonstrated through simulation studies) that these developments lead to reliable and efficient numerical routines based on finite element methods for elliptic eigenvalue problems, that can be used as the basis for the construction of gradient-free and gradient-based statistical methods. This has been illustrated through the implementation and empirical investigation of some commonly used MCMC algorithms and optimisation techniques for nonparametric Bayesian inference with Gaussian priors.

While our work provides novel theoretical and methodological contributions to the challenging problem of inference with low-frequency diffusion data, it also raises several interesting open research questions. Let us conclude by expanding upon two important ones.

5.1 Extensions to models with a potential energy field

The scope of the present investigation has been focused on diffusion processes in isolated media, governed by eq. (1.2) and (1.3). Extensions to models beyond these is of primary interest and a natural avenue for future research. In particular, many of the ideas developed here can be generalised to the important case where the diffusing particles are immersed within a (spatially-varying) ‘potential energy’ field and thus are subject to a ‘displacement force’ directed towards the local minima of , identified by the gradient vector field . This results in an SDE with additional drift component,

| (5.1) |

with associated (Gibbs-type) invariant probability density function and infinitesimal generator

| (5.2) |

As the latter is again in divergence form, and hence self-adjoint with respect to the inner product of , conditional inference on the conductivity function given any may then be pursued with minimal modifications to the approach developed in Section 2. In fact, in the realistic scenario of being also unknown, we envision decomposing the problem by obtaining a preliminary estimate of the invariant probability density function (for instance via standard linear kernel density estimators; see e.g. [39, 56, 29, 24, 38]). Based on , the statistical analysis on can then be performed by replacing the generator in (5.2) with a plug-in estimate . Alternatively, a joint Bayesian model can be considered by endowing the additional drift component in (5.1) with a prior distribution (such as those employed in [38]), which would then require to modify our MCMC algorithms to be of ‘Gibbs’ type. These generalisations are, however, beyond the scope of the present work.

5.2 Bounds on the computational complexity via gradient stability

Another important issue concerns the computational complexity of the employed posterior sampling and optimisation algorithms, going beyond the qualitative invariance properties discussed in Sections 3.2 and 3.3. A recent line of work initiated by Nickl and Wang in [58] has shown that polynomial-time bounds on the iteration complexity of MCMC methods may be obtained under ‘local convexity’ properties for the (negative) log-likelihood near the ground truth, quantified via a stability estimate for the log-likelihood gradient (i.e. a lower bound for its minimal eigenvalue), jointly with regularity properties of the associated Hessian matrix.

In the present setting, this program can indeed be pursued, albeit under a considerable amount of technical work. In particular, one may approach the verification of the key gradient stability condition using the characterisation of the Frechét derivatives in (2.5) and (2.11). Similarly, our ‘bootstrap’ PDE arguments also provide a blueprint for deriving the required higher-order regularity properties for the log-likelihood.

6 Proofs of Theorem 2.2, Corollary 2.3 and Proposition 3.2

In order to achieve a self-contained exposition, we deferred the proof of our main result, Theorem 2.1, to Appendix A. We here present the proofs of Theorem 2.2, Corollary 2.3 and Proposition 3.2.

6.1 Proof of Theorem 2.2

We will use throughout notation and facts from the proof of Theorem 2.1, which can be found in Appendix A. Let , and let with . For some regularisation parameter which will be chosen below in dependence on , let and be ‘regularised Frechét derivatives’ defined as in (A.16) below, and make the decomposition

We estimate each of the terms separately. Our goal is to show that for some ,

Arguing like in the estimates for term in the proof of Theorem 2.1, there exists some constant (specifically, chosen as in (A.17) below) such that

It remains to estimate term . To this end, we define the function by

where we have used the previous notation (despite potentially taking nonpositive values). By inspection of the definition of , we have that . The function satisfies the PDE

Using Theorem A.1 and the Sobolev embedding (holding since ), we obtain that for any ,

where the spaces and are defined in (A.7) below. Noting that the difference equals the term defined in (A.14), we now choose small enough – like in the Lemmas A.2 and A.3 below – to obtain that

where . By our choice of it is ensured that .

The term can be treated similarly. Using Theorem B.1,

The last expression is almost identical to the right hand side of the PDE (A.3) satisfied by , except with in place of . Following the exact same argument as in the proof of Lemma A.2, it can be shown that . Overall, we have obtained that .

Finally, choose ; upon combining all the preceding estimates, this yields

which concludes the proof upon choosing . ∎

6.2 Proof of Corollary 2.3

For and satisfying the assumptions of Corollary 2.3, recall the expression of the Frechét derivative from Theorem 2.1,

By the spectral representations (2.8) and (2.9) for the transition operators and density functions, we can then write the above integrand as, for any fixed and , recalling that (independently of ),

| (6.1) |

Now,

and since by Green’s first identity (e.g. [34, Section C.2]), recalling that ,

we have

Replaced into (6.1), this gives

and finally

where

∎

6.3 Proof of Proposition 3.2

For fixed , denote for convenience

| (6.2) |

The proof then clearly follows if we show that is continuously differentiable and that for ,

| (6.3) |

where is the linear operator defined as in (2.5) with . Recalling the notation , , the map in (6.2) is seen to be the result of the composition

where

The linear function is smooth (in the Frechét sense), with for all . Further, it is easy to see that in view of the regularity of , the function also is smooth, with Frechét derivative given by the linear operator

Theorem 2.1 and Theorem 2.2 together imply that is continuously differentiable. The differentiability of is then obtained the chain rule, e.g. [34, Section E.4]. In particular, with the element of the standard basis of ,

This concludes the derivation of (6.3) and the proof of the proposition.

[Acknowledgments] The authors would like to thank Richard Nickl and Markus Reiß for several helpful discussions.

M. G. gratefully acknowledges the support of MUR - Prin 2022 - Grant no. 2022CLTYP4, funded by the European Union – Next Generation EU, and the affiliation to the ”de Castro” Statistics Initiative, Collegio Carlo Alberto, Torino. S. W. gratefully acknowledges the support of the Air Force Office of Scientific Research Multidisciplinary University Research Initiative (MURI) project ANSRE.

References

- [1] {barticle}[author] \bauthor\bsnmAbraham, \bfnmK.\binitsK. and \bauthor\bsnmNickl, \bfnmR.\binitsR. (\byear2019). \btitleOn statistical Caldéron problems. \bjournalMathematical Statistics and Learning \bvolume2 \bpages165–216. \endbibitem

- [2] {barticle}[author] \bauthor\bsnmAgmon, \bfnmS.\binitsS., \bauthor\bsnmDouglis, \bfnmA.\binitsA. and \bauthor\bsnmNirenberg, \bfnmL.\binitsL. (\byear1964). \btitleEstimates near the boundary for solutions of elliptic partial differential equations satisfying general boundary conditions II. \bjournalCommunications on Pure and Applied Mathematics \bvolume17 \bpages35-92. \endbibitem

- [3] {barticle}[author] \bauthor\bsnmAït-Sahalia, \bfnmYacine\binitsY. (\byear2002). \btitleMaximum likelihood estimation of discretely sampled diffusions: a closed-form approximation approach. \bjournalEconometrica \bvolume70 \bpages223–262. \endbibitem

- [4] {barticle}[author] \bauthor\bsnmAït-Sahalia, \bfnmYacine\binitsY. (\byear2008). \btitleClosed-form likelihood expansions for multivariate diffusions. \bjournalThe Annals of Statistics \bvolume36 \bpages906–937. \endbibitem

- [5] {bbook}[author] \bauthor\bsnmAllen, \bfnmE.\binitsE. (\byear2007). \btitleModeling with Itô stochastic differential equations. \bseriesMathematical Modelling: Theory and Applications \bvolume22. \bpublisherSpringer, Dordrecht. \endbibitem

- [6] {barticle}[author] \bauthor\bsnmAltmeyer, \bfnmRandolf\binitsR. (\byear2022). \btitlePolynomial time guarantees for sampling based posterior inference in high-dimensional generalised linear models. \bjournalarXiv preprint arXiv:2208.13296. \endbibitem

- [7] {barticle}[author] \bauthor\bsnmBabuška, \bfnmIvo\binitsI. and \bauthor\bsnmOsborn, \bfnmJohn E\binitsJ. E. (\byear1989). \btitleFinite element-Galerkin approximation of the eigenvalues and eigenvectors of selfadjoint problems. \bjournalMathematics of computation \bvolume52 \bpages275–297. \endbibitem

- [8] {bincollection}[author] \bauthor\bsnmBabuška, \bfnmI.\binitsI. and \bauthor\bsnmOsborn, \bfnmJ.\binitsJ. (\byear1991). \btitleEigenvalue problems. In \bbooktitleFinite Element Methods (Part 1). \bseriesHandbook of Numerical Analysis \bvolume2 \bpages641-787. \bpublisherElsevier. \endbibitem

- [9] {binbook}[author] \bauthor\bsnmBaehr, \bfnmHans Dieter\binitsH. D. and \bauthor\bsnmStephan, \bfnmKarl\binitsK. (\byear1998). \btitleHeat conduction and mass diffusion In \bbooktitleHeat and Mass Transfer \bpages105–250. \bpublisherSpringer Berlin Heidelberg, \baddressBerlin, Heidelberg. \endbibitem

- [10] {bbook}[author] \bauthor\bsnmBakry, \bfnmDominique\binitsD., \bauthor\bsnmGentil, \bfnmIvan\binitsI. and \bauthor\bsnmLedoux, \bfnmMichel\binitsM. (\byear2014). \btitleAnalysis and geometry of Markov diffusion operators \bvolume348. \bpublisherSpringer, Cham. \endbibitem

- [11] {barticle}[author] \bauthor\bsnmBandeira, \bfnmAfonso S\binitsA. S., \bauthor\bsnmMaillard, \bfnmAntoine\binitsA., \bauthor\bsnmNickl, \bfnmRichard\binitsR. and \bauthor\bsnmWang, \bfnmSven\binitsS. (\byear2023). \btitleOn free energy barriers in Gaussian priors and failure of cold start MCMC for high-dimensional unimodal distributions. \bjournalPhilosophical Transactions of the Royal Society A \bvolume381 \bpages20220150. \endbibitem

- [12] {barticle}[author] \bauthor\bsnmBeskos, \bfnmA.\binitsA., \bauthor\bsnmGirolami, \bfnmM.\binitsM., \bauthor\bsnmLan, \bfnmS.\binitsS., \bauthor\bsnmFarrell, \bfnmP. E.\binitsP. E. and \bauthor\bsnmStuart, \bfnmA. M.\binitsA. M. (\byear2017). \btitleGeometric MCMC for infinite-dimensional inverse problems. \bjournalJournal of Computational Physics \bvolume335 \bpages327-351. \endbibitem

- [13] {barticle}[author] \bauthor\bsnmbeskos, \bfnmAlexandros\binitsA., \bauthor\bsnmpapaspiliopoulos, \bfnmOmiros\binitsO. and \bauthor\bsnmroberts, \bfnmGareth\binitsG. (\byear2009). \btitleMonte carlo maximum likelihood estimation for discretely observed diffusion processes. \bjournalAnnals of statistics \bvolume37 \bpages223–245. \endbibitem

- [14] {barticle}[author] \bauthor\bsnmBeskos, \bfnmAlexandros\binitsA., \bauthor\bsnmPapaspiliopoulos, \bfnmOmiros\binitsO., \bauthor\bsnmRoberts, \bfnmGareth O\binitsG. O. and \bauthor\bsnmFearnhead, \bfnmPaul\binitsP. (\byear2006). \btitleExact and computationally efficient likelihood-based estimation for discretely observed diffusion processes (with discussion). \bjournalJournal of the Royal Statistical Society Series B: Statistical Methodology \bvolume68 \bpages333–382. \endbibitem

- [15] {barticle}[author] \bauthor\bsnmBladt, \bfnmMogens\binitsM., \bauthor\bsnmFinch, \bfnmSamuel\binitsS. and \bauthor\bsnmSørensen, \bfnmMichael\binitsM. (\byear2016). \btitleSimulation of multivariate diffusion bridges. \bjournalJournal of the Royal Statistical Society Series B: Statistical Methodology \bvolume78 \bpages343–369. \endbibitem

- [16] {barticle}[author] \bauthor\bsnmBoffi, \bfnmDaniele\binitsD. (\byear2010). \btitleFinite element approximation of eigenvalue problems. \bjournalActa numerica \bvolume19 \bpages1–120. \endbibitem

- [17] {barticle}[author] \bauthor\bsnmBohr, \bfnmJan\binitsJ. and \bauthor\bsnmNickl, \bfnmRichard\binitsR. (\byear2021). \btitleOn log-concave approximations of high-dimensional posterior measures and stability properties in non-linear inverse problems. \bjournalarXiv e-prints arXiv:2105.07835. \endbibitem

- [18] {barticle}[author] \bauthor\bsnmBramble, \bfnmJames H\binitsJ. H. and \bauthor\bsnmOsborn, \bfnmJE\binitsJ. (\byear1973). \btitleRate of convergence estimates for nonselfadjoint eigenvalue approximations. \bjournalMathematics of computation \bvolume27 \bpages525–549. \endbibitem

- [19] {barticle}[author] \bauthor\bsnmBriane, \bfnmVincent\binitsV., \bauthor\bsnmVimond, \bfnmMyriam\binitsM. and \bauthor\bsnmKervrann, \bfnmCharles\binitsC. (\byear2020). \btitleAn overview of diffusion models for intracellular dynamics analysis. \bjournalBriefings in Bioinformatics \bvolume21 \bpages1136–1150. \endbibitem

- [20] {bincollection}[author] \bauthor\bsnmCalderón, \bfnmAlberto-P.\binitsA.-P. (\byear1980). \btitleOn an inverse boundary value problem. In \bbooktitleSeminar on Numerical Analysis and its Applications to Continuum Physics (Rio de Janeiro, 1980) \bpages65–73. \bpublisherSoc. Brasil. Mat., Rio de Janeiro. \endbibitem

- [21] {barticle}[author] \bauthor\bsnmChatelin, \bfnmFrançoise\binitsF. (\byear1973). \btitleConvergence of approximation methods to compute eigenelements of linear operations. \bjournalSIAM Journal on Numerical Analysis \bvolume10 \bpages939–948. \endbibitem

- [22] {barticle}[author] \bauthor\bsnmCotter, \bfnmS. L.\binitsS. L., \bauthor\bsnmRoberts, \bfnmG. O.\binitsG. O., \bauthor\bsnmStuart, \bfnmA. M.\binitsA. M. and \bauthor\bsnmWhite, \bfnmD.\binitsD. (\byear2013). \btitleMCMC Methods for Functions: Modifying Old Algorithms to Make Them Faster. \bjournalStatistical Science \bvolume28 \bpages424-446. \endbibitem

- [23] {barticle}[author] \bauthor\bsnmCui, \bfnmTiangang\binitsT., \bauthor\bsnmLaw, \bfnmKody J. H.\binitsK. J. H. and \bauthor\bsnmMarzouk, \bfnmYoussef M.\binitsY. M. (\byear2016). \btitleDimension-independent likelihood-informed MCMC. \bjournalJ. Comput. Phys. \bvolume304 \bpages109–137. \endbibitem

- [24] {barticle}[author] \bauthor\bsnmDalalyan, \bfnmArnak\binitsA. and \bauthor\bsnmReiß, \bfnmMarkus\binitsM. (\byear2007). \btitleAsymptotic statistical equivalence for ergodic diffusions: the multidimensional case. \bjournalProbability theory and related fields \bvolume137 \bpages25–47. \endbibitem

- [25] {barticle}[author] \bauthor\bsnmDaners, \bfnmDaniel\binitsD. (\byear2000). \btitleHeat kernel estimates for operators with boundary conditions. \bjournalMathematische Nachrichten \bvolume217 \bpages13–41. \endbibitem

- [26] {bbook}[author] \bauthor\bsnmDavies, \bfnmE Brian\binitsE. B. (\byear1995). \btitleSpectral theory and differential operators \bvolume42. \bpublisherCambridge University Press. \endbibitem

- [27] {barticle}[author] \bauthor\bsnmDelyon, \bfnmBernard\binitsB. and \bauthor\bsnmHu, \bfnmYing\binitsY. (\byear2006). \btitleSimulation of conditioned diffusion and application to parameter estimation. \bjournalStochastic Processes and their Applications \bvolume116 \bpages1660–1675. \endbibitem

- [28] {barticle}[author] \bauthor\bsnmDescloux, \bfnmJean\binitsJ., \bauthor\bsnmNassif, \bfnmNabil\binitsN. and \bauthor\bsnmRappaz, \bfnmJacques\binitsJ. (\byear1978). \btitleOn spectral approximation. Part 1. The problem of convergence. \bjournalRAIRO. Analyse numérique \bvolume12 \bpages97–112. \endbibitem

- [29] {binproceedings}[author] \bauthor\bsnmDexheimer, \bfnmNiklas\binitsN., \bauthor\bsnmStrauch, \bfnmClaudia\binitsC. and \bauthor\bsnmTrottner, \bfnmLukas\binitsL. (\byear2022). \btitleAdaptive invariant density estimation for continuous-time mixing Markov processes under sup-norm risk. In \bbooktitleAnnales de l’Institut Henri Poincare (B) Probabilites et statistiques \bvolume58 \bpages2029–2064. \bpublisherInstitut Henri Poincaré. \endbibitem

- [30] {barticle}[author] \bauthor\bsnmDurham, \bfnmGarland B\binitsG. B. and \bauthor\bsnmGallant, \bfnmA Ronald\binitsA. R. (\byear2002). \btitleNumerical techniques for maximum likelihood estimation of continuous-time diffusion processes. \bjournalJournal of Business & Economic Statistics \bvolume20 \bpages297–338. \endbibitem

- [31] {barticle}[author] \bauthor\bsnmElerian, \bfnmOla\binitsO., \bauthor\bsnmChib, \bfnmSiddhartha\binitsS. and \bauthor\bsnmShephard, \bfnmNeil\binitsN. (\byear2001). \btitleLikelihood inference for discretely observed nonlinear diffusions. \bjournalEconometrica \bvolume69 \bpages959–993. \endbibitem

- [32] {bbook}[author] \bauthor\bsnmEngl, \bfnmHeinz W.\binitsH. W., \bauthor\bsnmHanke, \bfnmMartin\binitsM. and \bauthor\bsnmNeubauer, \bfnmAndreas\binitsA. (\byear1996). \btitleRegularization of inverse problems. \bseriesMathematics and its Applications \bvolume375. \bpublisherKluwer, Dordrecht. \endbibitem

- [33] {barticle}[author] \bauthor\bsnmEraker, \bfnmBjørn\binitsB. (\byear2001). \btitleMCMC analysis of diffusion models with application to finance. \bjournalJournal of Business & Economic Statistics \bvolume19 \bpages177–191. \endbibitem

- [34] {bbook}[author] \bauthor\bsnmEvans, \bfnmLawrence C.\binitsL. C. (\byear2010). \btitlePartial differential equations, \beditionSecond ed. \bpublisherAmerican Math. Soc. \endbibitem

- [35] {bbook}[author] \bauthor\bsnmGhosal, \bfnmSubhashis\binitsS. and \bauthor\bparticlevan der \bsnmVaart, \bfnmAad W.\binitsA. W. (\byear2017). \btitleFundamentals of Nonparametric Bayesian Inference. \bpublisherCambridge University Press, New York. \endbibitem

- [36] {bbook}[author] \bauthor\bsnmGiné, \bfnmEvarist\binitsE. and \bauthor\bsnmNickl, \bfnmRichard\binitsR. (\byear2016). \btitleMathematical foundations of infinite-dimensional statistical models. \bpublisherCambridge University Press, New York. \endbibitem

- [37] {barticle}[author] \bauthor\bsnmGiordano, \bfnmMatteo\binitsM. and \bauthor\bsnmNickl, \bfnmRichard\binitsR. (\byear2020). \btitleConsistency of Bayesian inference with Gaussian process priors in an elliptic inverse problem. \bjournalInverse Problems, to appear. \endbibitem

- [38] {barticle}[author] \bauthor\bsnmGiordano, \bfnmMatteo\binitsM. and \bauthor\bsnmRay, \bfnmKolyan\binitsK. (\byear2022). \btitleNonparametric Bayesian inference for reversible multidimensional diffusions. \bjournalThe Annals of Statistics \bvolume50 \bpages2872–2898. \endbibitem

- [39] {barticle}[author] \bauthor\bsnmGobet, \bfnmEmmanuel\binitsE., \bauthor\bsnmHoffmann, \bfnmMarc\binitsM. and \bauthor\bsnmReiß, \bfnmMarkus\binitsM. (\byear2004). \btitleNonparametric estimation of scalar diffusions based on low frequency data. \bjournalThe Annals of Statistics \bvolume32 \bpages2223 – 2253. \endbibitem

- [40] {barticle}[author] \bauthor\bsnmGolightly, \bfnmAndrew\binitsA. and \bauthor\bsnmWilkinson, \bfnmDarren J\binitsD. J. (\byear2008). \btitleBayesian inference for nonlinear multivariate diffusion models observed with error. \bjournalComputational Statistics & Data Analysis \bvolume52 \bpages1674–1693. \endbibitem

- [41] {barticle}[author] \bauthor\bsnmGraham, \bfnmIvan G\binitsI. G., \bauthor\bsnmKuo, \bfnmFrances Y\binitsF. Y., \bauthor\bsnmNichols, \bfnmJames A\binitsJ. A., \bauthor\bsnmScheichl, \bfnmRobert\binitsR., \bauthor\bsnmSchwab, \bfnmCh\binitsC. and \bauthor\bsnmSloan, \bfnmIan H\binitsI. H. (\byear2015). \btitleQuasi-Monte Carlo finite element methods for elliptic PDEs with lognormal random coefficients. \bjournalNumerische Mathematik \bvolume131 \bpages329–368. \endbibitem

- [42] {barticle}[author] \bauthor\bsnmHeckert, \bfnmAlec\binitsA., \bauthor\bsnmDahal, \bfnmLiza\binitsL., \bauthor\bsnmTjian, \bfnmRobert\binitsR. and \bauthor\bsnmDarzacq, \bfnmXavier\binitsX. (\byear2022). \btitleRecovering mixtures of fast-diffusing states from short single-particle trajectories. \bjournalElife \bvolume11 \bpagese70169. \endbibitem

- [43] {barticle}[author] \bauthor\bsnmHoffmann, \bfnmMarc\binitsM. and \bauthor\bsnmRay, \bfnmKolyan\binitsK. (\byear2022). \btitleBayesian estimation in a multidimensional diffusion model with high frequency data. \bjournalarXiv preprint arXiv:2211.12267. \endbibitem

- [44] {barticle}[author] \bauthor\bsnmKessler, \bfnmMathieu\binitsM. and \bauthor\bsnmSørensen, \bfnmMichael\binitsM. (\byear1999). \btitleEstimating equations based on eigenfunctions for a discretely observed diffusion process. \bjournalBernoulli \bpages299–314. \endbibitem

- [45] {barticle}[author] \bauthor\bsnmKnyazev, \bfnmAndrew V\binitsA. V. and \bauthor\bsnmOsborn, \bfnmJohn E\binitsJ. E. (\byear2006). \btitleNew a priori FEM error estimates for eigenvalues. \bjournalSIAM journal on numerical analysis \bvolume43 \bpages2647–2667. \endbibitem

- [46] {barticle}[author] \bauthor\bsnmKohn, \bfnmRobert\binitsR. and \bauthor\bsnmVogelius, \bfnmMichael\binitsM. (\byear1984). \btitleDetermining conductivity by boundary measurements. \bjournalCommunications on pure and applied mathematics \bvolume37 \bpages289–298. \endbibitem

- [47] {barticle}[author] \bauthor\bsnmLin, \bfnmMing\binitsM., \bauthor\bsnmChen, \bfnmRong\binitsR. and \bauthor\bsnmMykland, \bfnmPer\binitsP. (\byear2010). \btitleOn generating Monte Carlo samples of continuous diffusion bridges. \bjournalJournal of the American Statistical Association \bvolume105 \bpages820–838. \endbibitem

- [48] {bbook}[author] \bauthor\bsnmLions, \bfnmJean-Louis\binitsJ.-L. and \bauthor\bsnmMagenes, \bfnmEnrico\binitsE. (\byear1972). \btitleNon-homogeneous boundary value problems and applications. Vol. I. \bpublisherSpringer-Verlag, New York-Heidelberg. \endbibitem

- [49] {bbook}[author] \bauthor\bsnmLunardi, \bfnmAlessandra\binitsA. (\byear1995). \btitleAnalytic Semigroups and Optimal Regularity for Parabolic Problems. \bpublisherBirkhäuser. \endbibitem

- [50] {bbook}[author] \bauthor\bsnmMajda, \bfnmAndrew J\binitsA. J. and \bauthor\bsnmHarlim, \bfnmJohn\binitsJ. (\byear2012). \btitleFiltering complex turbulent systems. \bpublisherCambridge University Press. \endbibitem

- [51] {barticle}[author] \bauthor\bsnmNachman, \bfnmAdrian I\binitsA. I. (\byear1988). \btitleReconstructions from boundary measurements. \bjournalAnnals of Mathematics \bvolume128 \bpages531–576. \endbibitem

- [52] {bbook}[author] \bauthor\bsnmNickl, \bfnmR.\binitsR. (\byear2023). \btitleBayesian Non-linear Statistical Inverse Problems. \bseriesZurich Lectures in Advanced Mathematics. \bpublisherEMS Press. \endbibitem

- [53] {barticle}[author] \bauthor\bsnmNickl, \bfnmRichard\binitsR. (\byearto appear). \btitleInference for diffusions from low frequency measurements. \bjournalThe Annals of Statistics. \endbibitem

- [54] {binproceedings}[author] \bauthor\bsnmNickl, \bfnmRichard\binitsR. and \bauthor\bsnmPaternain, \bfnmGabriel P\binitsG. P. (\byear2022). \btitleOn some information-theoretic aspects of non-linear statistical inverse problems. In \bbooktitleProc. Int. Cong. Math \bvolume7 \bpages5516–5538. \endbibitem

- [55] {barticle}[author] \bauthor\bsnmNickl, \bfnmRichard\binitsR. and \bauthor\bsnmRay, \bfnmKolyan\binitsK. (\byear2020). \btitleNonparametric statistical inference for drift vector fields of multi-dimensional diffusions. \bjournalAnn. Statist. \bvolume48 \bpages1383–1408. \endbibitem

- [56] {barticle}[author] \bauthor\bsnmNickl, \bfnmRichard\binitsR. and \bauthor\bsnmSöhl, \bfnmJakob\binitsJ. (\byear2017). \btitleNonparametric Bayesian posterior contraction rates for discretely observed scalar diffusions. \bjournalAnn. Statist. \bvolume45 \bpages1664-1693. \endbibitem

- [57] {barticle}[author] \bauthor\bsnmNickl, \bfnmRichard\binitsR., \bauthor\bparticlevan de \bsnmGeer, \bfnmSara\binitsS. and \bauthor\bsnmWang, \bfnmSven\binitsS. (\byear2020). \btitleConvergence rates for penalized least squares estimators in PDE constrained regression problems. \bjournalSIAM/ASA Journal on Uncertainty Quantification \bvolume8 \bpages374–413. \endbibitem

- [58] {barticle}[author] \bauthor\bsnmNickl, \bfnmRichard\binitsR. and \bauthor\bsnmWang, \bfnmSven\binitsS. (\byear2024). \btitleOn polynomial-time computation of high-dimensional posterior measures by Langevin-type algorithms. \bjournalJournal of the European Mathematical Society \bvolume26 \bpages1031-1112. \endbibitem

- [59] {barticle}[author] \bauthor\bsnmPapaspiliopoulos, \bfnmOmiros\binitsO., \bauthor\bsnmRoberts, \bfnmGareth O\binitsG. O. and \bauthor\bsnmStramer, \bfnmOsnat\binitsO. (\byear2013). \btitleData augmentation for diffusions. \bjournalJournal of Computational and Graphical Statistics \bvolume22 \bpages665–688. \endbibitem

- [60] {barticle}[author] \bauthor\bsnmPedersen, \bfnmAsger Roer\binitsA. R. (\byear1995). \btitleConsistency and asymptotic normality of an approximate maximum likelihood estimator for discretely observed diffusion processes. \bjournalBernoulli \bpages257–279. \endbibitem

- [61] {barticle}[author] \bauthor\bsnmPeletier, \bfnmMark A.\binitsM. A., \bauthor\bsnmSavaré, \bfnmGiuseppe\binitsG. and \bauthor\bsnmVeneroni, \bfnmMarco\binitsM. (\byear2012). \btitleChemical Reactions as -Limit of Diffusion. \bjournalSIAM Review \bvolume54 \bpages327–352. \endbibitem

- [62] {barticle}[author] \bauthor\bsnmPokern, \bfnmY.\binitsY., \bauthor\bsnmStuart, \bfnmA. M.\binitsA. M. and \bauthor\bparticlevan \bsnmZanten, \bfnmJ. H.\binitsJ. H. (\byear2013). \btitlePosterior consistency via precision operators for Bayesian nonparametric drift estimation in SDEs. \bjournalStochastic Process. Appl. \bvolume123 \bpages603-628. \endbibitem

- [63] {bbook}[author] \bauthor\bsnmRasmussen, \bfnmCarl Edward\binitsC. E. and \bauthor\bsnmWilliams, \bfnmChristopher\binitsC. (\byear2006). \btitleGaussian processes for machine learning \bvolume2. \bpublisherMIT press Cambridge, MA. \endbibitem

- [64] {barticle}[author] \bauthor\bsnmRichter, \bfnmGerard R.\binitsG. R. (\byear1981). \btitleAn inverse problem for the steady state diffusion equation. \bjournalSIAM J. Appl. Math. \bvolume41 \bpages210–221. \endbibitem

- [65] {barticle}[author] \bauthor\bsnmRoberts, \bfnmGareth O\binitsG. O. and \bauthor\bsnmStramer, \bfnmOsnat\binitsO. (\byear2001). \btitleOn inference for partially observed nonlinear diffusion models using the Metropolis–Hastings algorithm. \bjournalBiometrika \bvolume88 \bpages603–621. \endbibitem

- [66] {barticle}[author] \bauthor\bsnmRoberts, \bfnmGareth O.\binitsG. O. and \bauthor\bsnmTweedie, \bfnmRichard L.\binitsR. L. (\byear1996). \btitleExponential convergence of Langevin distributions and their discrete approximations. \bjournalBernoulli \bvolume2 \bpages341–363. \endbibitem

- [67] {barticle}[author] \bauthor\bsnmSCHAUER, \bfnmMORITZ\binitsM., \bauthor\bsnmVAN DER MEULEN, \bfnmFRANK\binitsF. and \bauthor\bsnmVAN ZANTEN, \bfnmHARRY\binitsH. (\byear2017). \btitleGuided proposals for simulating multi-dimensional diffusion bridges. \bjournalBernoulli \bvolume23 \bpages2917–2950. \endbibitem

- [68] {bbook}[author] \bauthor\bsnmShreve, \bfnmSteven E.\binitsS. E. (\byear2004). \btitleStochastic calculus for finance. II. \bseriesSpringer Finance. \bpublisherSpringer-Verlag, New York \bnoteContinuous-time models. \endbibitem

- [69] {barticle}[author] \bauthor\bsnmSprungk, \bfnmBjörn\binitsB., \bauthor\bsnmWeissmann, \bfnmSimon\binitsS. and \bauthor\bsnmZech, \bfnmJakob\binitsJ. (\byear2023). \btitleMetropolis-adjusted interacting particle sampling. \bjournalarXiv preprint arXiv:2312.13889. \endbibitem

- [70] {barticle}[author] \bauthor\bsnmStuart, \bfnmA. M.\binitsA. M. (\byear2010). \btitleInverse problems: a Bayesian perspective. \bjournalActa Numer. \bvolume19 \bpages451–559. \endbibitem

- [71] {barticle}[author] \bauthor\bsnmTanaka, \bfnmHiroshi\binitsH. (\byear1979). \btitleStochastic differential equations with reflecting boundary condition in convex regions. \bjournalHiroshima Math. J. \bvolume9 \bpages163–177. \endbibitem

- [72] {bbook}[author] \bauthor\bsnmTaylor, \bfnmMichael E.\binitsM. E. (\byear2011). \btitlePartial differential equations I. Basic theory. \bpublisherSpringer, New York. \endbibitem

- [73] {barticle}[author] \bauthor\bsnmTierney, \bfnmLuke\binitsL. (\byear1998). \btitleA note on Metropolis-Hastings kernels for general state spaces. \bjournalAnnals of applied probability \bpages1–9. \endbibitem

- [74] {bbook}[author] \bauthor\bsnmTriebel, \bfnmHans\binitsH. (\byear1978). \btitleInterpolation theory, function spaces, differential operators. \bseriesNorth-Holland Mathematical Library \bvolume18. \bpublisherNorth-Holland, New York. \endbibitem

- [75] {barticle}[author] \bauthor\bsnmUhlmann, \bfnmGunther\binitsG. (\byear2009). \btitleElectrical impedance tomography and Calderón’s problem. \bjournalInverse problems \bvolume25 \bpages123011. \endbibitem

- [76] {barticle}[author] \bauthor\bsnmVainikko, \bfnmG. M.\binitsG. M. (\byear1964). \btitleAsymptotic error bounds for projection methods in the eigenvalue problem. \bjournalŽ. Vyčisl. Mat i Mat. Fiz. \bvolume4 \bpages405–425. \endbibitem

- [77] {barticle}[author] \bauthor\bparticlevan der \bsnmMeulen, \bfnmFrank\binitsF. and \bauthor\bsnmSchauer, \bfnmMoritz\binitsM. (\byear2017). \btitleBayesian estimation of discretely observed multi-dimensional diffusion processes using guided proposals. \bjournalElectronic Journal of Statistics \bvolume11 \bpages2358–2396. \endbibitem

- [78] {barticle}[author] \bauthor\bparticleVan der \bsnmMeulen, \bfnmFH\binitsF., \bauthor\bsnmVan Der Vaart, \bfnmAad W\binitsA. W. and \bauthor\bsnmVan Zanten, \bfnmJH2265666\binitsJ. (\byear2006). \btitleConvergence rates of posterior distributions for Brownian semimartingale models. \bjournalBernoulli \bvolume12 \bpages863–888. \endbibitem

- [79] {bbook}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmAad\binitsA. \btitleAsymptotic statistics. \bpublisherCambridge University Press, Cambridge. \endbibitem

- [80] {barticle}[author] \bauthor\bparticlevan \bsnmWaaij, \bfnmJan\binitsJ. and \bauthor\bparticlevan \bsnmZanten, \bfnmHarry\binitsH. (\byear2016). \btitleGaussian process methods for one-dimensional diffusions: Optimal rates and adaptation. \bjournalElectronic Journal of Statistics \bvolume10 \bpages628–645. \endbibitem

- [81] {barticle}[author] \bauthor\bsnmWang, \bfnmSven\binitsS. (\byear2019). \btitleThe nonparametric LAN expansion for discretely observed diffusions. \bjournalElectron. J. Stat. \bvolume13 \bpages1329–1358. \endbibitem

Appendix A Proof of Theorem 2.1

Given some fixed constant , recall the definition of the parameter space in (2.1), and the notation for the infinitesimal generator of , with domain

equipped with the -norm. Moreover, let , and respectively denote the transition densities and the transition semigroup of the reflected Brownian motion on ,

| (A.1) |

A.1 Proof strategy

In order to prove the gradient characterisation stated in Theorem 2.1, we first introduce a sequence of regularised transition densities that are shown to satisfy certain parabolic PDEs whose initial conditions become singular as (Section A.2). For each fixed , we then use the regularity theory for parabolic PDEs (reviewed in Section A.3) to estimate the differences between the regularised transition densities (Section A.4). Using a recursive argument, higher order differences can also be controlled (Section A.5). Finally, the result is obtained by employing a careful limiting argument to let the regularisation parameter (Section A.6).

A.2 Regularised transition densities

For any conductivity function , we define a regularised version of the transition density by

It will be helpful to regard these as functions from to for some , where is fixed and the space variable is . To this end, we introduce the notation

By standard parabolic PDE theory (see [49, Proposition 4.1.2]), it is clear that uniquely solves the initial value problem