Decentralization of Ethereum’s Builder Market

Abstract.

Blockchains protect an ecosystem worth more than $500bn with their strong security properties derived from the principle of decentralization. Is today’s blockchain really decentralized? In this paper, we empirically studied one of the least decentralized parts of Ethereum—the most used blockchain system in practice—and shed light on the decentralization issue from a new perspective.

To avoid centralization caused by Maximal Extractable Value (MEV), Ethereum adopts a novel mechanism that produces blocks through a builder market. After two years in operation, however, the builder market has evolved to a highly centralized one with three builders producing more than 90% of blocks. Why does the builder market centralize, given that it is permissionless and anyone can join? Moreover, what are the security implications of a centralized builder market to MEV-Boost auctions? Through a rigorous empirical study of the builder market’s core mechanism, MEV-Boost auctions, we answered these two questions using a large-scale auction dataset we curated since 2022.

Unlike previous works that focus on who wins the auctions, we focus on why they win, to shed light on the openness, competitiveness, and efficiency of MEV-Boost auctions. We show the access barriers around private order flows constitute a significant entry barrier to the builder market. A new builder needs to pay up to 1.4 ETH to access this private order flow, a significant amount considering their low initial profits. By computing the true value of bids, we investigated the inequality in block-building capabilities among builders and the competitiveness and efficiency of the MEV-Boost auctions. We observed that top, middle, and tail builders have significantly varying capabilities in extracting MEV, and the inequality worsens when MEV increases. 88% of the MEV-Boost auctions we studied were competitive, yet uncompetitive auctions still resulted in a total loss of 221.09 ETH for the proposers, which is 0.98% of their total gain. Meanwhile, only about 79% of the MEV-Boost auctions were efficient, and over half of the inefficient auctions were caused by block subsidization. Our findings also help identify directions for improving the decentralization of builder markets.

1. Introduction

At the core of any decentralized blockchain, a key assumption underpinning their strong security properties (integrity, availability, censorship resistance, incentive compatibility, etc) is “decentralization”, that the system is run by a large number of independent participants (Nakamoto, 2008; Eyal and Sirer, 2018; Schwarz-Schilling et al., 2022; Wahrstätter et al., 2023a; Bahrani et al., 2024; Roughgarden, 2020). It is community consensus that one of the greatest threats to decentralization is Maximal Extractable Value (MEV) (Daian et al., 2020), profits that protocol participants, hereafter referred to as validators, can reap by manipulating the ordering of transactions. MEV can lead to centralization because it disproportionally benefits well-resourced validators compared to “regular” ones, as extracting MEV requires significant capital, intelligence, and computational resources, which regular validators may not have (Bahrani et al., 2024; Ethereum Foundation, 2024b; Pai and Resnick, 2023; Buterin, 2021b, a).

In an effort to level the playground for validators, the Ethereum community proposed Proposer111A proposer is a validator chosen as the leader in a round of consensus to add a new block to the blockchain.-Builder Separation (PBS) (Ethereum Foundation, 2024b). The idea is to outsource the task of building profitable blocks to specialized entities called block builders. In the current implementation called MEV-Boost (Flashbots, 2024), the proposer runs an auction among builders and adds the block with the highest bid to the blockchain. MEV-Boost is permissionless for builders so any builder can join the auction. Ideally, builders compete with each other in auctions, and the auctioneer—the proposer—collects a significant portion of MEV in auction revenue without doing much work, eliminating the competitive advantage of sophisticated validators over regular ones.

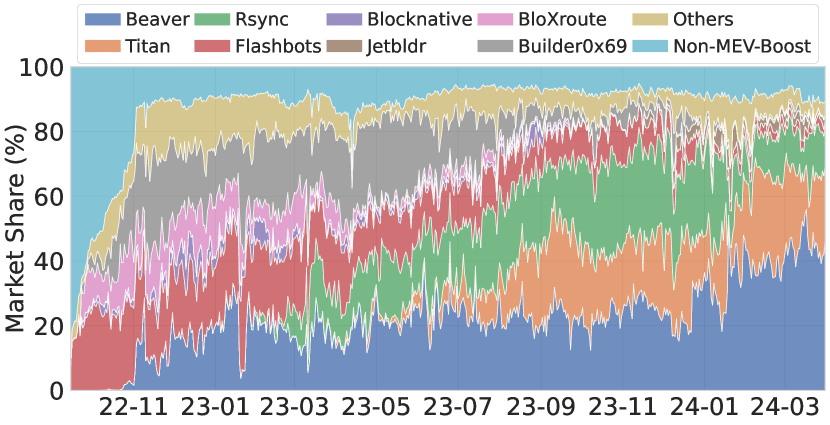

Does PBS achieve its goal? The answer is rather unclear. As shown in Fig. 1, the current market share is highly concentrated, with over 90% of the blocks produced through MEV-Boost being built by just three builders. However, the current concentration does not necessarily defeat the purpose of PBS for two reasons: first, builder markets may evolve and new builders may join and disrupt the concentration; second, centralization does not imply a lack of competition—it only takes a few non-colluding bidders to make the auction competitive and efficient.

Thus, while previous works (Flashbots, 2024; Wahrstätter, 2024; Labs, 2024; Heimbach et al., 2023; Wahrstätter et al., 2023b; Yang et al., 2022; Thiery, 2023) point out the centralization issue, they did not answer two key questions: First, how open is the builder market to new builders? Second, despite the centralization, are MEV auctions actually competitive and efficient? (We leave technical definitions to future sections, but intuitively, an auction is competitive if the winner outbids the second-best bidder; an auction is efficient if the bidder with the highest valuation wins.)

In this paper, we answer these questions through a rigorous empirical study of historical MEV auctions. The key ingredient of our study is a large-scale auction dataset we curated since 2022: we collected 5.57 billion partial bids222Partial and full bids are to be defined in Sec. 3.1 of 3,810,630 auctions from September 2022 to March 2024; in addition, in collaboration with ultra sound relay (Money, 2023), we obtained full bids for a total of 147,926 auctions from April 2023 to August 2023.

Auction data gives us direct visibility into the openness, competitiveness, and efficiency of MEV-Boost auctions. For example, historical bids allow us to “simulate” past auctions assuming a different set of transactions were available to builders, allowing us to discern the importance of different transactions. Another example is that we can compute the true value of each bid (i.e., the actual worth of the block to a builder, which is usually higher than what they bid) from transactions. The competitiveness and efficiency of an auction follow directly from a comparison between the true values and bid values. This is in contrast to, say, eBay auctions, where the true value of an item is subjective and cannot be retroactively computed from data.

Now we present an overview of methods and findings.

| Finding 1: Private order flows contribute to 60% of the MEV in over 50% of the blocks in MEV-Boost. |

|---|

| Finding 2: To access private order flows, new builders need to pay up to 1.4 ETH to enter the market. |

| Finding 3: The inequality in block building is highest among tail builders, followed by middle and least among top builders, and it worsens when MEV increases. |

| Finding 4: 88.84% of the MEV-Boost auctions are competitive, with proposers’ losses from uncompetitive auctions amounting to 0.98% of total gains. |

| Finding 5: 79.74% of the MEV-Boost auctions are efficient, and 51.4% of the inefficient auctions are caused by block subsidization. |

1.1. Openness of the Builder Market

First, we investigate the reasons behind centralization by quantifying the market entry barrier for a new builder. One such barrier could be the ability to build effective MEV extraction algorithms, but we investigated a perhaps more basic barrier: the ability to access profitable transactions. Recall that MEV extraction is about manipulating the ordering of transactions, so having access to “extractable” transactions is the basis of any extraction algorithm.

As we will present in Sec. 4, private order flows (Kilbourn, 2022)—the transactions that bypass the public mempool—contribute an increasing portion to builder income. This means that it would be difficult for a builder to win the auction without access to private order flows. Moreover, not all private order flows are equally profitable for builders, so the ability to access “good” private order flows forms a barrier to entering the builder market.

Using the auction dataset, we identified the providers of profitable transactions, quantified their importance to the builders, and investigated their accessibility to new builders.

Identifying pivotal private order flow providers. In today’s MEV ecosystem (to be presented in Sec. 2.2), private order flows come from various private order flow providers. Different providers impose different access barriers to their private order flows. Some providers (such as MEV-Share (Flashbots, 2024) and MEV Blocker (MEV Blocker, 2023)) have relatively clear criteria a builder must satisfy to access their flows. Still, some providers (e.g., most searchers) are almost completely opaque to the public. To identify important providers, we define the pivotal level of a provider as the percentage of MEV-Boost auctions in which the winner would have lost had transactions from were not available. As we will show in Sec. 4.1, we identified five pivotal providers whose pivotal level exceeds 50% over a period longer than two weeks. That is, if a builder cannot access the flows from any of these providers, it will lose the majority of the auctions during the period of our study.

The good news is that two of these pivotal providers are MEV Blocker (MEV Blocker, 2023) and MEV-Share (Flashbots, 2024), which are open to builders who meet a relatively clear set of criteria. The bad news is that satisfying the requirements set by MEV Blocker and MEV-Share is non-trivial for new builders, which we discuss next.

Quantifying the market entrance barrier. Typically, providers share private order flows to reputable builders with a certain market share (Sec. 4.2). However, this presents a chicken-and-egg problem for new builders: to gain market shares, they need private order flows to win the auction, but starting out new, they do not have market share and thus cannot access private order flows. To navigate this dilemma, new builders resort to subsidization (Flashbots, 2024): bidding higher than their actual profits in MEV-Boost auctions, to establish the required market shares. Therefore a new builder needs to have enough capital to keep subsidizing until reaching a certain market share. To understand the significance of this entry barrier, we compute the minimal cost of subsidization required to maintain a 1% market share, which is the requirement of MEV Blocker. Specifically, we first calculate the minimal subsidy a builder needs to win an MEV-Boost auction without private order flows; then, we sum up the minimum subsidies over 1% of total auctions per day as the daily cost.

Our analysis highlights a non-trivial cost for new builders to establish a reputation through subsidization—they need to invest up to 1.4 ETH to subsidize their blocks and secure a minimal 1% market share during the period of our study. The cost is comparable to or even higher than the profits of small builders (Flashbots, 2024).

Trust barriers result in access barriers. An important takeaway is that siloes of private order flows stem from the lack of a fair exchange mechanism between providers and builders. In the current design, builders are at an advantage and malicious builders can harm providers by, e.g., sandwich attacks (Zhou et al., 2021) and imitation attacks (Qin et al., 2023). Therefore, providers only share their order flows with reputable builders, even though such reputation-based protection is pretty weak. As entry barriers arise from the trust crisis, reducing or eliminating these trust barriers is essential for making the builder market more decentralized. We discuss several ideas in Sec. 7.2.

1.2. Competitiveness and Efficiency

The first question focuses on the evolution of builder markets. In the second question, we focus on the status quo and study the implications of a centralized builder market as we have today.

MEV-Boost auction adopts an open-bid, ascending price auction akin to an English auction (Besanko et al., 2009), with a 12-second deadline. English auctions have appealing features: ideally, assuming bidders do not collude and can react to each other instantaneously, the bidders who can extract most MEV will win (efficiency), paying at least the MEV extracted by the second-highest bidder (competitiveness).

However, given the small number of builders in today’s builder market, it is unclear if MEV-Boost auctions indeed induce the desired dynamics. We investigate whether the apparent centralization of the builder market indeed leads to inadequate competition and a loss of efficiency.

True values in MEV-Boost auctions. In MEV-Boost auctions, for a block , a bid value (BV) is the amount the builder is willing to pay for to be added to the blockchain. The total revenue gained by the bidder from is the true value (TV). Rational bidders would bid lower than the true value to get a non-zero profit. The true value of a block can computed from transactions in .

Inequality in block building capabilities. We first compare the true values across different builders for the same auction to understand the variations in builders’ abilities to extract values. A builder who consistently demonstrates a superior ability to extract value could dominate the market. We used the quartile coefficient of dispersion (QCD) (Wikipedia, 2022) to quantify the inequality of true values across builders. Our results in Sec. 5.1 reveal significant differences in the block-building capabilities of top, middle, and tail builders. The inequality worsens as the MEV of a slot increases, possibly because significant MEV opportunities are more likely to be shared with only a limited number of builders. Fortunately, the inequality among top builders is not significant, which supports the premise of competitiveness and efficiency.

More than 88% of auctions are competitive. Using the true values, we propose two metrics, competitive index (CI) and efficient index (EI), to quantify whether an auction is competitive or efficient, respectively (see Sec. 5.2 for details.) Our results reveal that approximately 88.84% of the MEV-Boost auctions we analyzed were competitive. However, we also found that the auctions tend to be less competitive when the MEV of a slot increases. As discussed previously, the main concern is that a lack of competition can cause loss to proposers. We therefore quantify the loss for proposers. Our study shows that 16,498 of the 147,926 MEV-Boost auctions were uncompetitive, where proposers incurred total losses amounting to 221.09 ETH, which is 0.98% of the total gains of the proposers.

Only 79% of auctions are efficient. An interesting finding is that more than 20% of MEV-Boost auctions are inefficient and the auctions tend to be inefficient when the MEV in an MEV-Boost auction is low. Further analysis reveals that over half of the inefficient auctions are caused by block subsidization. The winners of these inefficient auctions overbid to win, although they do not have the highest true value. Moreover, block subsidization is more common when the extractable value is small, because the cost will be relatively low. Although this may not benefit the overall welfare, it is advantageous for proposers as they earn more than expected.

Suggestions for future developments. Since many identified issues stem from trust concerns, future developments should aim to design mechanisms that reduce or eliminate the reliance on trust. Possible directions include community supervision (Flashbots, 2023a) and the use of Trusted Execution Environments (TEEs) (Costan and Devadas, 2016) to ensure the integrity and confidentiality of private order flows (Flashbots, 2024c). Another idea is to implement a reliable leakage detection mechanism for private order flows, which we briefly discuss in Sec. 7.2. Such mechanisms would encourage private order flow providers to distribute their flows across multiple builders, thus increasing the equality of the builders’ ability to extract value.

Contribution

To the best of our knowledge, we are the first to use the rich auction data to analyze the decentralization of Ethereum’s builder market, while most previous works are limited to on-chain data. Our dataset of the true values of 147,926 MEV-Boost auctions from April to August 2023 may be of independent interest. Our dataset of 5.57 billion partial bids since 2022 is the largest-scale known to us.

We characterized the efficacy of PBS in terms of being open to new builders and inducing competitive and efficient auctions. Our key findings are highlighted in Tab. 1, which we summarize below.

-

•

Sec. 4: Private order flows contribute to more than 60% of the MEV in over 50% of blocks every day since July 2023. We identified five pivotal private order flow providers that had a significant and sustained impact on the winners of more than half of the MEV-Boost auctions. Two of them are MEV Blocker and MEV-Share.

-

•

Sec. 4.2: Private order flow providers impose market share requirements on builders, which costs new builders up to 1.4 ETH in subsidy to enter the market during the period of our study.

-

•

Sec. 5.1: The QCD shows a significant inequality in builders’ abilities to extract value across top, middle, and tail builders, but the inequality among the top builders is not significant.

-

•

Sec. 5.2: We find that 88.84% of the 147,926 MEV-Boost auctions are competitive. However, proposers incur losses of 221.09 ETH from the uncompetitive auctions, representing 0.98% of their total gain. These losses can still threaten the stable separation between proposers and builders.

-

•

Sec. 5.2: 79.74% of the MEV-Boost auctions in our study are efficient. A significant factor contributing to inefficiency is block subsidization, where winners overbid to secure the auctions, possibly driven by the need to meet market share requirements.

Besides contributing to the literature on MEV mitigation, our work also contributes to the Economics literature on the analysis of MEV-Boost auctions. Currently, there is only limited auction theoretic analysis that considers the complexity of real-world MEV auctions (Gupta et al., 2023; Pai and Resnick, 2023; Wu et al., 2024). The findings in this paper can serve as empirical evidence for future theoretic analysis of MEV-Boost auctions.

2. Background

2.1. MEV-Boost Auctions

MEV. Miner/Maximal Extractable Value (MEV) (Daian et al., 2020) refers to the profit that privileged players (e.g., validators) can earn by including, excluding, and reordering the transactions. MEV poses a threat to decentralization, as explained in the introduction. There are two schools of thought on mitigating the negative impacts of MEV. The first one is referred to as MEV democratization (Flashbots, 2022b), the main idea of which is to facilitate MEV extraction and level the playground. MEV-Boost (Flashbots, 2024), to be introduced below, is the primary example. Another approach is to enforce certain ordering policies (e.g., FIFO) to prevent order manipulation, such as (Kelkar et al., 2020, 2023). We focus on MEV-Boost because it is widely used.

PoS Ethereum. Before introducing background on MEV-Boost auctions, we first cover the relevant concepts in Ethereum’s Proof of Stake-based consensus protocol called Gasper (Buterin et al., 2020). Participants of Gasper are called validators. Each validator must deposit 32 ETH as collateral (Ethereum Foundation, 2024a). Time is divided into 12-second intervals called slots. This results in 7,200 slots in Ethereum per day. During each slot, a single validator, referred to as the proposer, proposes a block, while other validators vote for the proposed block if it extends the chain head in their local view.

Proposer-builder separation (PBS) and MEV-Boost. Proposer-builder separation (PBS) can be conceptually viewed as a sidecar to the core consensus protocol (although some proposals are more tightly coupled with consensus) to allow the proposer to outsource the job of building blocks to builders.

MEV-Boost (Flashbots, 2024) is the current incarnation of the PBS idea. About 90% of all blocks on Ethereum are built by MEV-Boost (Wahrstätter, 2024). The basic idea is to auction off the right to propose a block to the builder who bids the highest in an open-bid ascending price auction (contributors, 2024). Because builders and proposers are mutually untrusted, the auction is facilitated by a (trusted) third party called a relay (Flashbots, 2022a). Here are the high-level steps (we refer readers to (Flashbots, 2024) for details):

-

•

Builders submit bids to relays throughout the slot. For the purpose of this paper, we denote a bid with that consists of a block , a bid value to be paid to the proposed if the block is proposed, and the builder’s public key. Bids are signed by the builder but we omit the signature for clarity. Relays verify that indeed pays the proposer at least .

-

•

Relays expose a public API that publishes partial bids in the form of . includes parent hash, gas limit, gas used, etc. Partial bids do not include block content.

-

•

The proposer selects a block hash , typically the one with the highest , and sends the relay a signature on . This signature is a promise to propose in the consensus protocol (if it proposes another block, this signature is evidence of equivocation and will cause the proposer to be penalized (Buterin et al., 2020).) After verifying the signature, the relay returns to the proposer.

Two additional remarks. First, relays are trusted entities, but anyone can run a relay (currently there are ten (EthStaker Community, 2024)), and builders and proposers can connect to the relays they trust. Second, winning bids are recorded on-chain, and losing bids are discarded after the auction. We collected and archived the historical bids over time to enable this study, as we will detail in Sec. 3.

2.2. MEV Supply Chain

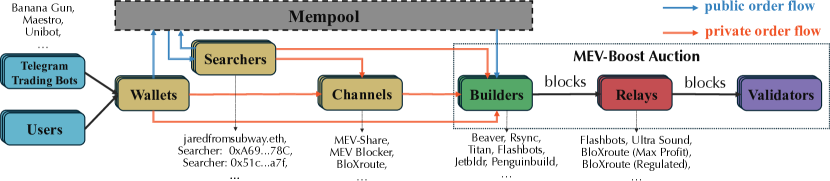

The ecosystem around discovering and extracting MEV forms an MEV supply chain, as depicted in Fig. 2. Builders, relays, and proposers (validators) have been introduced above. Now we introduce the “upstream” of builders.

Wallet. Users use wallets to interact with blockchains. A user communicates her intent (e.g., transferring cryptocurrency) to the wallet, which generates the transaction to fulfill the user’s intent and sends it to the network. MEV may be generated during this process, e.g., when the user transaction creates an arbitrage opportunity. While the wallet is typically controlled by the users, it can also be managed by a third party, such as Telegram trading bots (Intelligence, 2024). These bots are automated programs integrated with the Telegram app (Telegram, 2024), automatically conducting cryptocurrency trades on behalf of users. Users’ transactions eventually reach builders or proposers, either through the peer-to-peer network (the mempool) or through third-party services called private channels.

Mempool. Mempool is a temporary storage of pending transactions before they are added to the blockchain. All transactions stored in the mempool are publicly visible.

Channel. A private channel, or channel for short, connects users directly with builders, bypassing the mempool. Channels receive transactions from users and then, forward them to the builders specified by the users, offering privacy and atomicity guarantees. E.g., a user can send a bundle (list) of transactions and request them not to be unbundled. Examples include MEV-Share (Flashbots, 2024), MEV Blocker (MEV Blocker, 2023), BloXroute (bloXroute Labs, 2024), etc.

Searcher. Searchers are a special type of users. They run (typically proprietary) algorithms to construct profitable transaction sequences (bundles) based on the pending transactions and the blockchain state. Same as regular users, searchers may submit transactions to mempool or channels. In addition, most builders have public APIs that allow searchers to submit bundles directly. Some searchers may prefer channels for the privacy and atomicity benefits. A search is said to integrate with a builder if it sends almost all of its orders to that builder exclusively. For example, searcher 0xA69b… is considered an integrated searcher of Beaver Builder because Beaver Builder includes the majority of its transactions.

Some channels, such as MEV-Share and MEV Blocker, allow searchers to read pending transactions in the channel and extract MEV from them, provided that such extraction should not harm users (e.g., only backrunning is allowed).

Private order flow. Order flow refers to a source of transactions that may carry extractable value and can be categorized into two categories: public order flow, originating from the public mempool, and private order flow, sent directly by users or searchers without being broadcast to the public mempool. The entities that can provide private order flows to the builders are referred to as private order flow providers, which includes searchers, channels, users, and Telegram trading bots as shown in Fig. 2.

2.3. Model and Assumptions.

Accounts and states. We follow the model of (Babel et al., 2023a, b). We use to denote the space of all possible accounts. For example, in Ethereum, both user-owned and contract-owned accounts are represented by 160-bit identifiers. For , denotes the balance of all tokens held in account , and specifies the balance of token . For simplicity, is used to denote the balance of the primary token (e.g., ETH in Ethereum).

Transaction and block. A transaction is a string whose execution changes the system’s state. A block is an ordered sequence of transactions. Executing transactions in a block transforms an initial state into a new state , represented by .

Extracted value (EV). The extracted value of a block in state for a participant is the changes of ’s balances after executing . Assuming controls a set of accounts , the extracted value of for is:

| (1) |

where .

Builder’s income. We assume a builder ’s income from building a block is , or for short since the builder identity is usually encoded in the block. We compute EV following a similar approach as that in MEV analysis tools (EigenPhi, 2023; Flashbots, 2023b) and previous works (Heimbach et al., 2023; Thiery, 2023). Specifically, can be computed as the sum of the transaction priority fees (Ethereum, 2024) and direct transfers (Flashbots, 2024a) to the builder’s addresses minus the refund to other addresses. We also refer to the builder’s income from a block (or a set of transactions in a block) as the value of the block (or the set of transactions).

Note that is a lower bound of the builder’s actual income from because the builder may own accounts out of in Equation 1, or even receive payments off-chain. We discuss the implications in Sec. 7.

3. Dataset

We created two auction datasets to study the decentralization of the builder market: a dataset of partial bids from September 2022 to March 2024, and a dataset of full bids from April to August 2023. The full bids are obtained from the ultra sound relay (Money, 2023). Recall from Sec. 2.1 that a bid consists of a block and a bid value and a partial bid consists of where includes parent hash, gas limit, gas used, etc.

To support analysis, we also collected on-chain data, including blocks and transactions on Ethereum, as well as miscellaneous data, which will be detailed below. Tab. 2 summarizes the datasets.

| Dataset | Content | # of entries | Source |

| On-chain | blocks | 4,019,895 | Reth node |

| transactions | 606,484,921 | ||

| Auction | blocks produced by MEV-Boost | 3,517,851 | relay API |

| partial bids | 5,577,318,196 | relay API | |

| full bids from ultra sound | 164,700,566 | ultra sound relay | |

| Misc. | builder public keys | 191 | see Sec. 3.1 |

| builder addresses | 125 | ||

| searcher addresses | 2,069 | ||

| private transactions | 49,081,209 | ||

| transaction sources | 33,010,466 |

3.1. Data Collection and Validation

On-chain data. We run an Ethereum execution client Reth (paradigmxyz, 2024) along with a consensus client Lighthouse (Prime, 2024) to collect blocks and transactions from September 15, 2022, to March 31, 2024. The on-chain dataset includes 4,019,895 blocks and 606,484,921 transactions.

Data from relay APIs. We connected to all 13 known relays333three relays were inactive during the period of our study and collected the following information from their public APIs: 1) the winning bid including the final block sent to the proposer; and 2) partial bids for blocks that did not win the auction. Recall that partial bids do not include the block body. We collected 3,517,851 winning bids and 5,577,318,196 partial bids from September 15, 2022, to March 31, 2024, in a total of 3,810,630 auctions. We use winning bids to identify blocks produced through MEV-Boost. We use partial bids to quantify the importance of private order flow providers in Sec. 4.

To validate the completeness of the data collected from relay APIs, we compared the winning bids we collected with three public datasets (Network, 2023; Wahrstätter, 2023; DataAlways, 2024). Our dataset includes 5,382 more winning bids than other datasets combined. Upon comparison with on-chain blocks, we find they are all included on Ethereum, thereby indicating a high level of completeness.

Full bids from the ultra sound relay . From the ultra sound relay (Money, 2023), we obtained the full bids in 147,926 historical auctions that took place between April and August 2023. Since the data volume is large (we record roughly 200 GB data per day), our dataset samples one week of each month: April 9-15, May 1-7, June 1-7, July 1-7, and August 1-7, 2023. The dataset consists of 164,700,566 full bids (block, bid value, and builder public key). We use full bids in Sec. 5 to quantify the competitiveness and efficacy of MEV-Boost auctions.

The original data from relays includes bids submitted after the deadline because of network latency. We removed them as we are only interested in the bids before the auction ends. On April 18, 2023, MEV-Boost introduced bid cancellation that allows a bidder to cancel a previous bid by submitting a lower one. However, proposers can query bids before they are canceled and store them locally (Ethereum Research, 2023), effectively bypassing cancellation. Therefore we do not take cancellation into consideration.

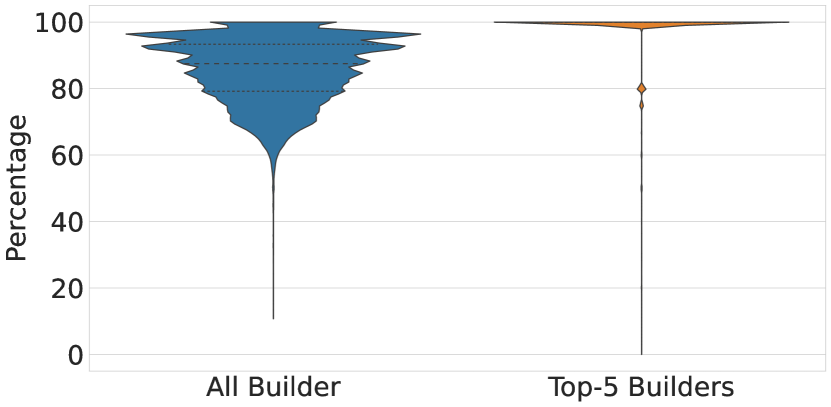

Not all builders connect to the ultra sound relay, so we need to validate that the full bids from ultra sound relay cover a significant subset of all builders. We compute the percentage of the builders that submit to ultra sound relay over all known builders. The set of all known builders is a union of all builders that appeared in our datasets, including winning bids, partial bids, and bids from the ultra sound relay. As shown in Fig. 10, bids from the ultra sound relay covered more than 80% of the builders in over 75% of the MEV-Boost auctions during our study period. Moreover, the top-5 builders by market share (Flashbots, Beaver, Rsync, Builder0x69, and Titan) almost always submitted to ultra sound relay.

Miscellaneous data. In practice, builders are known by their common names (e.g., flashbots builder), but a builder may use multiple public keys to sign bids and use multiple addresses to receive and make payments. We collect builders’ public keys to attribute bids to builders. We collect builder’s addresses to calculate the true value of bids. We use private transaction hashes to identify private order flows and use the searchers’ addresses and sources of transactions to identify the private order flow providers in Sec. 4.

-

•

Builder public keys: We collect public keys controlled by each builder combining two data sources. First, some builders publish their public keys in official documents or code repositories. For example, Titan builder has disclosed 12 public keys in its official document (Builder, 2024). Second, some builders leave distinct marks in their blocks’ “extra field”. For example, Flashbots builder uses the mark ‘‘Illuminate Democratize Distribute’’. Given that such marks are unauthenticated and susceptible to impersonation, we ignore them unless they are used more than 100 times in the bids by the same builder public key.

-

•

Builder addresses: We collect the builder addresses from the blocks’ last transactions combined with the public dataset (Etherscan, 2024). Similarly, to validate their completeness, we manually cross-check them with related works (Heimbach et al., 2024, 2023), and the results show that our dataset includes 113 more builder addresses, which is the most complete so far.

- •

-

•

Private transaction hashes: We use data from Mempool Guru (Yang et al., 2022) to label transactions that bypassed the public mempool as private. We believe these labels have already been cross-validated since the private transactions are collected by seven distributed nodes.

-

•

Transaction sources: we are interested in where a transaction originates from and which part of the MEV supply chain it has traversed through.

We identified transactions originated from Telegram trading bots, including Maestro (Maestro, 2023a), Banana Gun (Banana Gun, 2023), and Unibot (Unibot X, 2023), by searching for transactions that interacted with their official smart contracts.

Two channels, MEV Blocker and MEV-Share publish data (Protocol, 2024; Flashbots, 2024b) about transactions submitted to them. Specifically, transactions submitted to MEV Blocker are publicly available on Dune (Protocol, 2024), from which we extracted 14,901,303 transaction hashes that fall within our study’s range. We obtained 13,992,371 transactions submitted to MEV-Share from the public Flashbots dataset (Flashbots, 2024b). These transaction labels are sourced from their official datasets and we view them as ground truth.

4. Openess of the builder market

The builder market is technically open to everyone, but the barrier to accessing profitable private order flows (Sec. 2.2) forms an implicit access barrier.

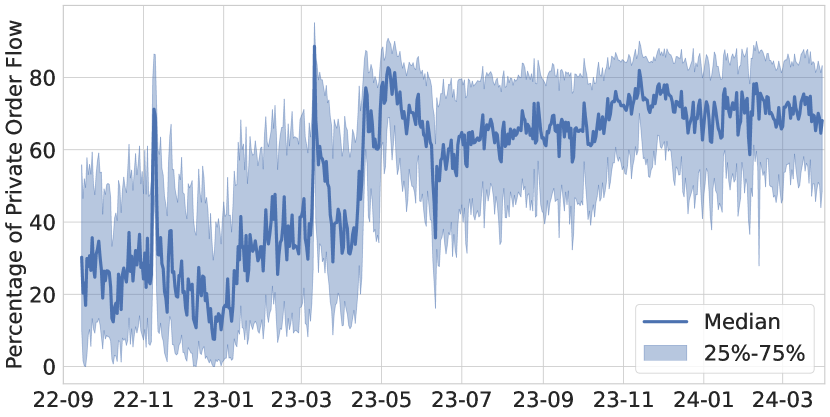

To illustrate the importance of private order flow to the success of builders, Fig. 3 plots the fraction of builder income from private order flows. Currently, approximately 60% of the block value comes from private order flows.

Finding I: The private order flow is crucial for builders to win the MEV-Boost auction because it contributes to more than 60% of the block value in over 50% of blocks.

Where can new builders get private order flows? The entities who provide (or sell) private order flows to builders are called private order flow providers. Different providers impose different access barriers to their private order flows. Some providers are open to new builders who satisfy certain requirements (such as MEV Blocker or MEV-Share), while some (e.g., most searchers) are almost completely opaque to the public.

To understand if the builder market is open to new builders, we first identify important “pivotal” providers and then quantify the cost for a new builder to access private order flows from representative pivotal providers.

4.1. Pivotal Private Order Flow Providers

Prominent private order flow providers are listed in Tab. 6. Based on their roles in the MEV supply chain (see Fig. 2), we categorize them into three types: searcher, Telegram trading bot, and channel.

We now present our method to quantify the importance of individual providers. An existing approach (Lu, 2024; Lu, Angela and Sui, Danning and Durnford, Jaden, 2024) is to compute the contribution of each provider to the builders’ income (Sec. 2.3) during a specific period. However, this approach only considers the magnitude of impact but neglects the duration (in terms of time or the number of auctions). For example, a single private transaction, such as one444 0xf0464b01d962f714eee9d4392b2494524d0e10ce3eb3723873afd1346b8b06e4 transferring 457.55 ETH to the builder as a tip, could contribute significantly to the builder’s income, but this provider may only influence the MEV-Boost auction in a single slot. Thus, we assess the significance of a provider as the number of auctions for which they played an important role; in particular, we focus on the providers that can affect half of the MEV-Boost auctions in over two weeks. This captures their sustained impact on the system.

We define a provider as pivotal for an instance of MEV-Boost auction if removing ’s transactions from the winning block causes the winner to lose the auction. Intuitively, had the winner not accessed ’s order flow, the winner might lose.555Note that the winner may or may not actually lose as it may be able to find an alternative pivotal provider, but this does not invalidate the fact that is pivotal. We identify pivotal providers in a given auction as follows: for each winning bid, we identify the providers of private order flow within the block and subsequently calculate the revised true value excluding each provider’s contribution. If the recalculated true value drops below the next highest bid (from the partial bids dataset Sec. 3.1), the involved private order flow provider is considered pivotal. Note that there can be multiple pivotal providers for an auction.

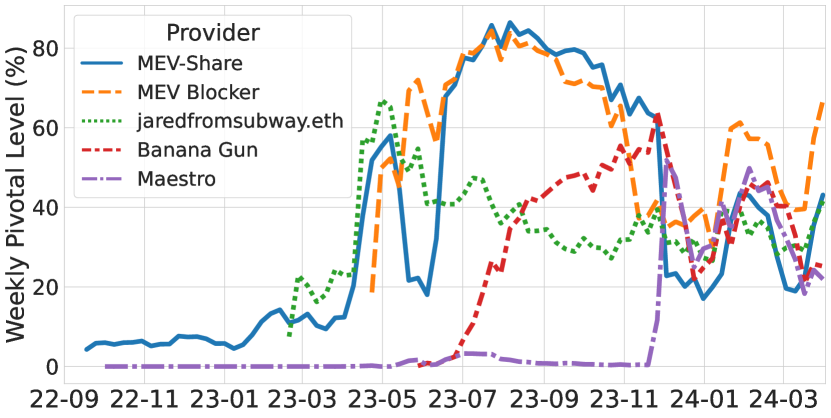

For each pivotal provider, we compute the fraction of auctions in which it is pivotal. We call this metric the pivotal level, a number from 0 to 1. Fig. 4 plots the pivotal level of the top-5 providers.

We can make a few observations from Fig. 4. First, a particular searcher, jaredfromsubway.eth, has been gaining prominence since February 2023 and reached its peak significance in May 2023. During this period, the winners of more than 70% of the MEV-Boost auctions would have failed had they not received order flow from jaredfromsubway.eth. Its influence has gradually decreased since then but still remains pivotal in 20%-40% of auctions since Nov 2023. Besides, the order flow from Telegram trading bots has become vital for builders with the rise of such bots. For instance, Banana Gun is pivotal in about 40% of the MEV-Boost auctions in September 2023.

Second, we can observe a positive trend from Fig. 4 that MEV Share and MEV Blocker have been increasingly pivotal since May 2023. These two providers positively impact decentralization because they have relatively clear requirements for accessing their order flows (the requirements of different providers will be discussed in Sec. 4.2).

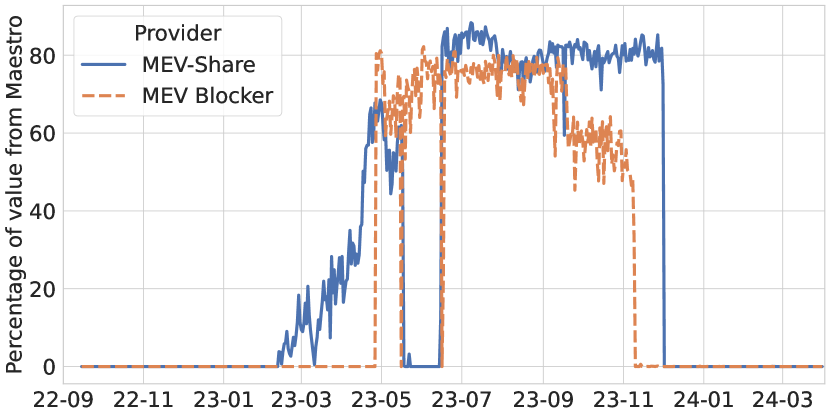

Third, we observe a notable downtrend in the pivotal level of MEV-Share and MEV Blocker starting from November 2023, accompanied by an uptrend in Maestro, a popular Telegram trading bot (Maestro, 2023a), beginning in December 2023. This is because Maestro used to be an important upstream of MEV-Share and MEV Blocker but stopped in November 2023, causing the pivotal levels of MEV-Share and MEV Blocker to drop significantly.

Although platforms like MEV-Share and MEV Blocker positively affect decentralization, the incentives of their upstream providers may not be aligned. For example, Mastro may prefer to send flows to builders directly for a better price than what MEV-Share and MEV Blocker can offer. It is alarming to see that upstream providers can significantly swing the significance of platforms.

Finding II: We identified five pivotal providers (MEV-Share, MEV Blocker, jaredfromsubway.eth, Banana Gun, Maestro) who had a sustained influence on the outcome of more than half of MEV-Boost auctions. A positive trend towards decentralization is observed as the pivotal level of the searcher jaredfromsubway.eth decreased, while the pivotal level of MEV-Share and MEV Blocker increased. However, their reliance on upstream providers like Maestro is alarming.

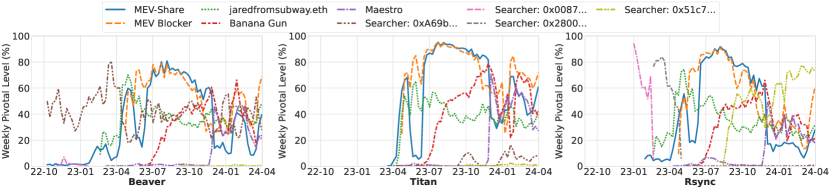

Builder-specific Pivotal Level. We compute each provider’s builder-specific pivotal level to understand the relationship between providers and builders. For a given provider , its pivotal level specific to builder is the pivotal level of the MEV-Boost auctions where is the winner.

Fig. 5 plots selected providers’ builder-specific pivotal levels for the top-3 builders, ranked based on their weekly market share in April 2024. We include providers whose weekly pivotal levels exceed 25% for any of the three builders over two months to illustrate these builder-specific pivotal levels. We note a clear variation in the importance of providers for different builders. For example, the significance of MEV Blocker and Banana Gun to Titan Builder is greater than they are to other builders. Furthermore, we observe that some providers have a pivotal level exceeding 50% only with specific builders, suggesting a possible collaborative relationship. The searcher 0xA69b… consistently influences over 50% of the MEV-Boost auctions won by Beaver Builder, while the searchers 0x0087…, 0x2800…, and 0x51c7… successively affect those won by Rsync Builder. These pivotal providers are all integrated searchers of the corresponding builders that have been identified in previous works (Heimbach et al., 2024; Gupta et al., 2023). This observation corroborates findings from previous studies (Heimbach et al., 2024; Gupta et al., 2023; Thiery, 2023), confirming that the order flows from integrated searchers are crucial to those builders.

4.2. Quantifying the Access Barrier

Pivotal providers have different degrees of openness to builders: searchers are generally not accessible, and platforms like MEV Share and MEV Blocker are more open, although they also set up certain barriers. In this section, we present more details about the access barrier set up by providers.

Searchers. Since searchers are operated by anonymous entities without any public communication channels, there is no public statement about which builders may access their flows. Existing studies indicate that searchers tend to send their order flow to the top builders (Titan, 2023) or share it exclusively with vertically integrated builders (Titan, 2023; Thiery, 2023; Gupta et al., 2023).

Telegram trading bots. The requirements for Telegram trading bots, in terms of sending order flow to builders, depend on whether they utilize channels like MEV Blocker (Maestro, 2023b; Labs, 2023). If so, their requirements are aligned with those of these channels. Banana Gun does not utilize these channels, nor does it explicitly state the requirements for builders.

Channels. Since channels are public-facing services, we were able to extract their access requirements from the documentation and/or through their communication channels. The requirements of each provider are summarized in Tab. 6.

The channels impose various requirements on a builder’s reputation. Market share—the percentage of blocks built by a given builder—is a metric most relay providers use to evaluate builders’ reputations. Intuitively, a builder with a high market share, seen as reputable, is less likely to compromise private order flows as doing so will forgo their future revenue. MeowRPC (Meow RPC, 2024) sends the order flow to trusted builders with high market share. Similarly, MEV-Share (Flashbots, 2024) requires that a builder possesses a competitive market share. MEV Blocker (MEV Blocker, 2023) requires that a builder must maintain at least 1% market share over one week.

The cost of establishing minimal market share. New builders face a “chicken and egg” problem as they need access to private order flows to win auctions and gain market share, but the private order flow providers only serve builders with a decent market share. In practice, builders pay out of pocket to overbid in MEV Boost auctions, a practice known as block subsidization. This represents a capital entry barrier for new builders, which we are able to quantify using the auction dataset.

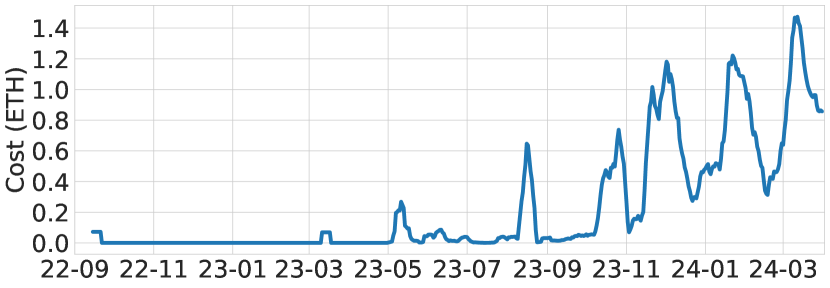

We compute the minimal subsidy needed to establish a 1% market share for one week (which is the requirement of MEV Blocker (MEV Blocker, 2023)) by replaying historical auctions with an added new builder who can only access the public order flow. We relegate the details to Sec. C.4.

The result is plotted in Fig. 6. Initially, this cost was nearly zero before May 2023, but it has steadily increased, surpassing 1.4 ETH by March 2024. It is important to recognize that the costs derived from this method only represent the lower bound. Predicting the minimum cost of winning a MEV-Boost auction is challenging, so builders need to pay more to ensure victory. Furthermore, builders may subsidize more blocks than required, as it is also difficult to precisely achieve a 1% market share. In reality, the subsidies new builders need to provide are substantially higher. For example, tbuilder (Tbuilder, 2024), a new builder in the builder market, subsidized 6.8 ETH in total for 645 blocks in the week before March 21, 2024 (Flashbots, 2024).

Finding III: The private order flow providers impose reputation requirements on the builders, which are usually evaluated based on market share. The minimum entry cost for new builders required to establish a required market share increases over time.

4.3. Trust Crisis and Centralization

Our findings highlight a trust issue in today’s MEV supply chain: the lack of trustworthy fair exchange mechanisms between parties creates order flow silos and harms decentralization.

Private order flow providers are at a disadvantage when interacting with builders and must trust builders not to unbundle the transactions. As a result, providers rely on an informal reputation system for self-protection, but it is not hard to see that reputation mechanisms are easily bypassed, as blockchain is fundamentally anonymous. Once a reputable builder receives the bundle from the searcher, the builder can create a Sybil and cheat the searcher (e.g., by unbundling the transaction bundle) under the new name.

While such an attack has not been reported in practice, it is noteworthy that builders occasionally unbundle searcher’s bundles. For example, the f1b builder unbundled a bundle from the searcher jaredfromsubway.eth at block height 18476515. Although the searcher was compensated afterward, this incident underscores the fragile security foundation of the trust chain in the MEV-Boost auction. We also noticed that one anonymous builder666public key: 0xad5ce1019364de39…35af575554a7aa6f might be the Sybil of a reputable builder because this builder’s blocks included order flows from sources that are only accessible by reputable builders.

The malicious actors within the trust chain pose a dual threat. On the one hand, security concerns deter searchers from submitting their bundles to multiple builders, further entrenching private order flow as a barrier to entry for new builders. On the other hand, integrating the roles of searcher and builder offers a potential mitigation to the security issue. Integrated searcher-builder has other structural advantages (Gupta et al., 2023; Pai and Resnick, 2023) (such as low latency) that may be unfair to regular builders.

In Sec. 7.2, we discuss directions to bridge the trust gap between searchers and builders.

Finding IV: The requirements for builders stem from the barrier of trust, as illustrated by the hidden trust crisis confirmed through real-world examples. Lowering or removing trust requirements in the MEV-Boost auction can facilitate decentralization.

5. Competition and Efficiency in the MEV-Boost auctions

Sec. 4 focuses on the evolution of builder market. In this section, we focus on the status quo and study the implications of a centralized builder market as we have today. First, we investigate the (in)equality of builders’ block-building capability, measured by the true values of builders’ bids in MEV-Boost auctions. Then, we quantify the competitiveness and efficiency of historical MEV Boost auctions. These two studies complement each other. The former evaluates whether today’s builder market has the potential to be competitive, while the latter evaluates whether the current mechanism in fact induces the desired outcomes. Our study includes some MEV-Boost auctions, the highest bids of which are not included on Ethereum due to network latency. However, we do not omit them since the auctions themselves are still meaningful.

5.1. Inequality in Block-building Capacity

A primary metric to evaluate a builder’s block-building capacity is the MEV it extracts over time. In MEV Boost auctions, this quantity is captured by the true values of the builder’s bids.

In the context of auctions generally, the true value of the item being auctioned refers to its actual worth to the bidder. Recall that in MEV-Boost auctions (Sec. 2), a builder submits a block (a list of transactions) and a bid value that the builder is willing to pay to the proposer if is proposed. The true value of , denoted , is typically higher than . One can think of as the builder’s revenue and as the cost. The difference is the profit pocketed by the builder, which we call extracted value (EV) — i.e., is the difference of the builder’s ETH balance after executing transactions in . For example, suppose executing yields a net profit of ETH after paying ETH in bid value in the auction, then the true value (the revenue) is ETH.

To compute of a given block , we follow the standard approach in open source MEV analysis tools (EigenPhi, 2023; Flashbots, 2023b) and previous works (Heimbach et al., 2023; Thiery, 2023), though we built our own analysis toolchain and optimized its performance to handle the large volume of auction data. We compute using a modified Rust Ethereum execution client (Reth (paradigmxyz, 2024)) to execute transactions in and compute the net ETH balance changes of the bidder’s addresses. Most builders’ addresses are well-known partly because they need to build up a reputation. We cross-validated it with other sources to ensure that our dataset was the most complete one to date (see Sec. 3.1 for details.) Then, with bid value from the auction dataset, the true value is the sum of and .

In every slot , bidders can submit multiple bids throughout the duration of the slot. We use to denote the highest bid value from bidder in slot , and the corresponding true value.

Quantifying the inequality of block-building capacities. We compare the highest true values of different builders in the same slot to understand the differences in builders’ ability to extract values. If a builder consistently has the highest true value, then she can potentially dominate the builder market. On the contrary, if many builders have similar true values, then it is plausible that a properly designed market could avoid a monopoly.

To quantify the disparity of block-building capacity, we compute the quartile coefficient of dispersion (QCD) (Wikipedia, 2022) of the highest true values in a given slot. Specifically, suppose the true values of different builders in slot are . Let and representing the first and third quartiles of (i.e., 25% and 75% percentiles). The QCD of slot is

QCD is a real value in . A larger QCD indicates greater dispersion (the intuition is that in a dataset with big dispersion, is much larger than , thus approaches ). Since it uses quartiles, QCD has the benefit of being robust to outliers (Wikipedia, 2022).

We now present the result given by QCD, noting that other metrics lead to a similar conclusion (see Sec. D.1).

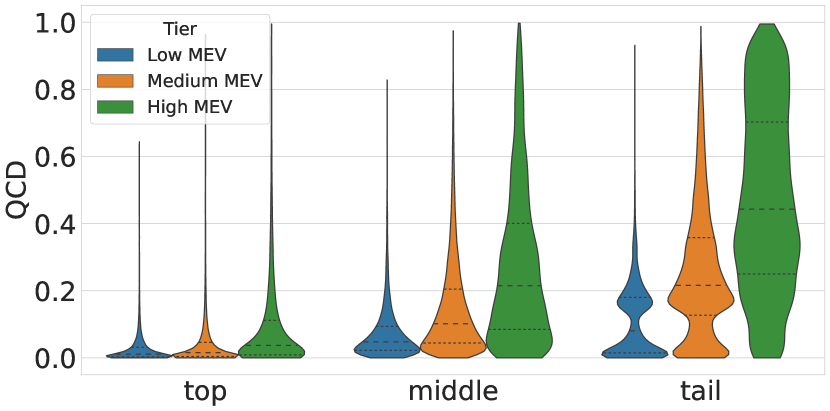

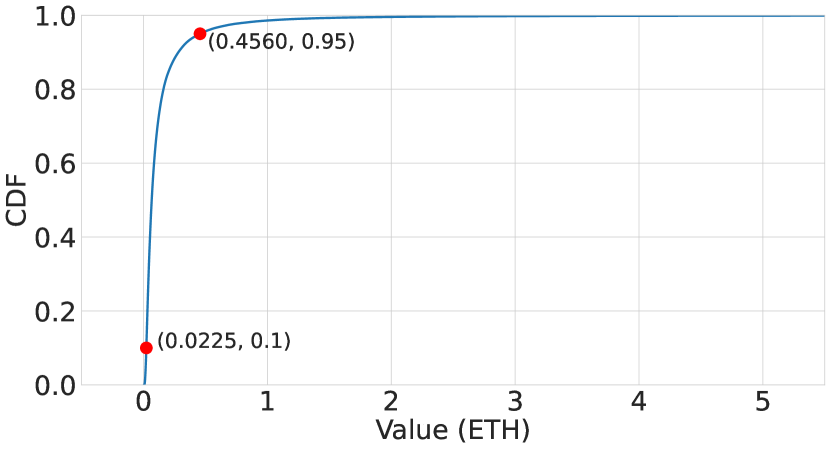

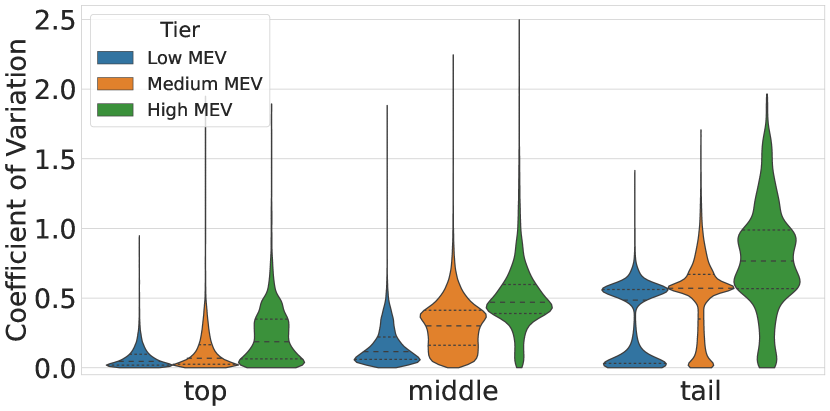

Evaluation results. We categorize the builders into three groups based on their market share from April to August 2023: top builders (top 5), middle builders (6-15), and tail builders (16-25). To understand how the magnitude of MEV in a slot affects the block-building capability, we categorize every slot into one of three tiers according to the final winning bid (as a proxy to the significance of the MEV opportunity in that slot): low MEV (below 0.0225 ETH, the 10th percentile of the winning bid values), high MEV (above 0.4586 ETH, 95th percentile) and medium MEV in between.

In Fig. 7, we plot the distribution of the QCD for MEV-Boost auctions from April 2023 to August 2023 for different builder groups and MEV tiers. (We sample the first week of each month. See Sec. 3.1 for details.) It reveals two trends. In each MEV tier, there is a clear increase in inequality (a high QCD means high inequality) from the top to the middle and then to the tail. That is, top builders have comparable block-building capabilities, but middle and tail builders have significantly different capabilities. This might be good news: top builders having similar abilities means they can meaningfully compete, which is positive for the decentralization of builder market.

Second, the inequality worsens as the MEV tier increases. One possible reason is that private order flow providers may tend to give significant MEV opportunities to select builders due to the trust barrier.

Finding V: The inequality in block building is lowest among top builders, higher among middle builders, and most pronounced among tail builders, and the inequality worsens as a slot’s MEV increases.

5.2. Quantifying Competitiveness and Efficiency

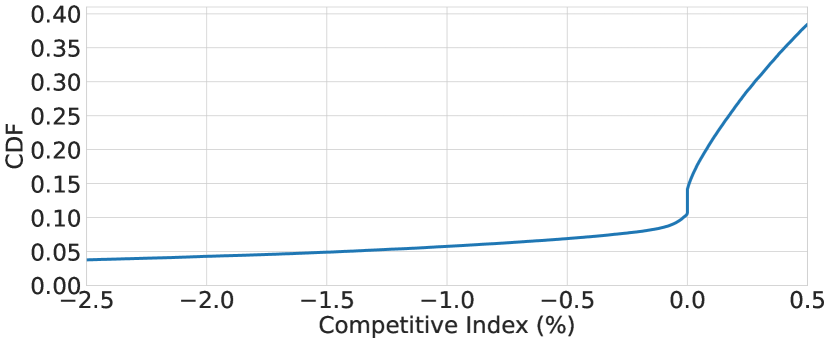

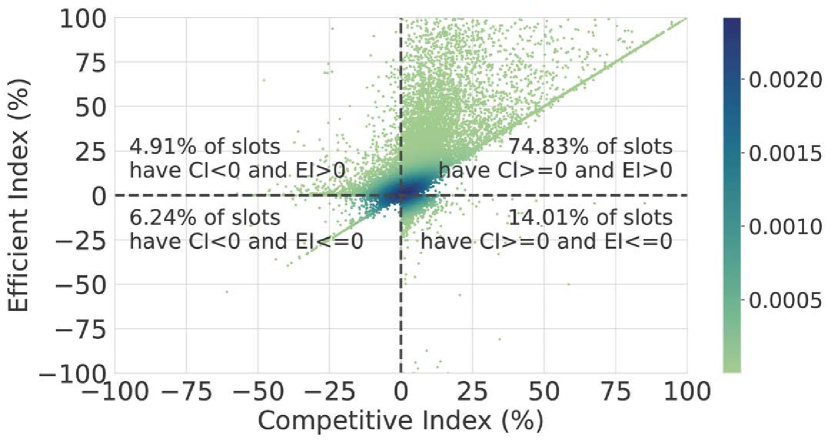

The previous section shows that top-5 builders have comparable true values in most cases. Ideally, revenue from MEV-Boost auctions should be near optimal due to competition. However, whether real-world auctions induce such near-perfect competition is complicated by several confounding factors: builders may not be able to respond to bids due to network latency, they may collude implicitly or explicitly, or they may have incentives to overbid (e.g., to gain market share). In this section, we quantify the competitiveness and efficiency of the MEV-Boost auctions using what we call competitive index (CI) and efficient index (EI).

Competitive index. In a given slot , suppose builders are ordered by their true value from high to low, i.e., , is the bid value of the winner and is the corresponding true value, the competitive index of slot , is defined as:

Namely, measures the relative difference between the winning bid and the second-highest true value. indicates that the winning bid value is not less than the second-highest true value, satisfying the definition of a competitive auction. Conversely, means that the competition is insufficient.

Efficient index. Same as above, the efficient index, , is defined as:

indicates that the winner has the highest true value, whereas implies that the bidder with the highest true value lost the auction.

Fig. 8 shows the distribution of the calculated CI and EI across all MEV-Boost auctions in the ultra sound relay dataset. Notably, 74.83% of the auctions are both competitive and efficient: the winner possesses the highest true value and bids higher than or equal to the second-highest true value. 88.84% (sum of the areas with ) of the auctions are competitive, yet only 79.74% (sum of the areas with ) are efficient.

5.2.1. Implications of uncompetitive auctions

We first note Fig. 8 shows a somewhat strict definition of competitiveness (i.e., ). In reality, builders may bid slightly lower than their true value to ensure profits. Therefore, it is reasonable to relax and consider an auction with to be competitive for a small . We call this notion -competitive. As shown in Fig. 14, when we consider or , the percentage of uncompetitive auctions reduces to about 6% and 5%, respectively. That is, under the slightly relaxed definition, approximately 95% auctions were competitive.

Quantifying proposers’ losses. The concern with uncompetitive auctions lies in the potential loss to validators. If such losses are significant, top validators might be motivated to operate their own builders. Furthermore, vertical integration between top proposers and builders could adversely impact the decentralization of the validators (Bahrani et al., 2024). Thus, quantifying the exact loss validators incur due to insufficient competition is crucial.

For each uncompetitive auction, we consider the second-highest true value as the ideal winning bid value and calculate the difference between this ideal value and the actual winning bid value. This difference represents the loss a validator incurs, which they would have received had the auction been competitive.

| Time | #Slots | #Slots w/ CI ¡ 0 (%) | Profits (ETH) | Losses (ETH) (%) |

|---|---|---|---|---|

| April 9-15 | 28,376 | 1,437 (5.06%) | 2,711.32 | 47.17 (2.02%) |

| May 1-7 | 30,279 | 8,449 (27.90%) | 9,367.50 | 118.50 (1.36%) |

| June 1-7 | 35,414 | 3,137 (8.86%) | 4,346.51 | 24.72 (0.62%) |

| July 1-7 | 36,032 | 2,051 (5.69%) | 3,945.67 | 18.41 (0.48%) |

| August 1-7 | 17,825 | 1,424 (7.99%) | 2,171.07 | 12.29 (0.58%) |

As shown in Tab. 3, we note that the total losses caused by uncompetitive auctions amount to 221.09 ETH in our study, which represents 0.98% of the total gains of proposers, with an average loss of 0.0134 ETH per uncompetitive auction.

The losses are particularly significant during May 1-7, 2023, when a total of 118.50 ETH was lost due to insufficient competition, which is 1.27% of their total gain. These losses may closely correlate with MEV opportunities, given that proposers’ total profits were also notably high during this period. Consequently, even though the losses seem to decrease, this reduction should not be interpreted as an indicator of increasingly intense competition. The concern regarding potential centralization persists, given that the losses experienced by validators have not been fully mitigated.

Finding VI: About 11% of the MEV-Boost auctions in our study are uncompetitive, resulting in total losses of 221.09 ETH for the proposers. These losses represent 0.98% of the total gains of proposers.

5.2.2. Reasons of inefficiency

20.26% of MEV-Boost auctions were not efficient. Further investigation is required to understand why. In an inefficient auction, the builder with the highest true value does not win the auction. There are two possible reasons. First, block subsidization allows a builder to win the auction without possessing the highest true value. Second, builders may “shade” their bids (bid shading means strategically placing bids slightly below one’s true value); if the builder with the highest true value “shades too much,” it will lose.

We analyzed the underlying reasons for all inefficient auctions. In 51.5% of cases, winners win the auctions due to subsidization. In 52.6% of cases, the builder with the highest true value shaded too much. It is important to note that auctions may exhibit inefficiency for multiple reasons. For instance, the winner may subsidize her bid while simultaneously, the builder with the highest true value shades. Thus, the cumulative percentage exceeds 100%.

It is important to note that inefficiency does not necessarily disadvantage the validators. In fact, in inefficient scenarios involving subsidization, validators may receive more value.

Finding VII: MEV-Boost auctions are generally competitive, yet their efficiency falls short of expectations. Further analysis reveals that 51.5% of inefficiencies are caused by subsidization, which, interestingly, does not disadvantage proposers but leads to increased earnings for them in such scenarios.

5.2.3. MEV’s implication on auction outcomes

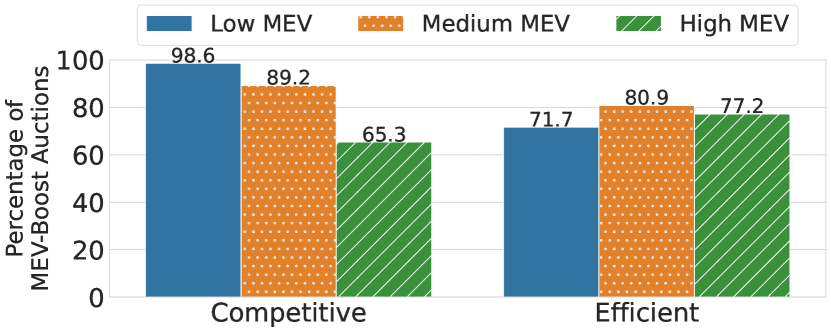

To further understand how the magnitude of MEV in a slot affects the competitiveness and efficiency of the auction, we follow the same methodology and categorize the auctions into three tiers: low MEV, medium MEV, and high MEV. The ratio of competitive and efficient auctions in each tier is shown in Fig. 9.

We note that competitiveness decreases as the MEV of a slot increases, which is consistent with the finding in Sec. 5.1 about the inequality of block-building capabilities in high-MEV slots.

The trend of efficiency is less expected. First, only 71.7% of the auctions within the low MEV tier are efficient. This can be attributed to the generally low overall bid values, rendering the auction outcomes vulnerable to alterations from minor subsidies. Second, while auctions tend to be more efficient in the medium MEV tier, we also observe that efficiencies worsen in the high MEV tier: only 77.2% of these auctions are efficient, and about 90% of inefficient cases result from bid shading, where the builders with the highest true values place their bids much lower than their true values.

Finding VIII: The competitiveness of MEV-Boost auctions deteriorates as a slot’s MEV increases. Efficiency may decline due to block subsidization in the low MEV tier and bid shading in the high MEV tier.

6. Related Work

Empirical study on Ethereum’s builder market. Several previous works studied the centralization of the builder market shares. An early exploration by Yang et al. (Yang et al., 2022) analyzed the market share of relays and builders. Their findings indicated a centralization of Ethereum’s builder market, with Flashbots and builder0x69 accounting for over 53% of the market share between September 15th, 2022, and November 30th, 2022. Similar studies on the builder market conducted by (Wahrstätter et al., 2023b; Heimbach et al., 2023) also confirmed the centralization in the builder market. Their observations were based on the market share and the distribution of total profits generated within the PBS ecosystem. Moreover, several online dashboards (Wahrstätter, 2024; Labs, 2024; Bitfly, 2024; Flashbots, 2024) offer a dynamic view of the ecosystem’s trends by presenting real-time PBS analytics. However, these studies do not quantify the causes of centralization or the security implications of a centralized builder market.

Private order flow. Many studies also discuss the importance of private order flows, particularly focusing on private order flows from integrated searchers. Thiery (Thiery, 2023) counted the total number of transactions, along with their values, from June 1 to July 15, 2023. He found that private order flows account for only 30% of the transactions yet represent 80% of the total value paid to builders. Our study highlights a similar result: in over 50% of blocks, private order flows account for more than 60% of the block value. Gupta et al. (Gupta et al., 2023) confirmed that builders are more likely to win the MEV auction when their integrated searchers can provide high-value exclusive order flow by effectively exploiting arbitrage between a centralized exchange (CEX) and a decentralized exchange (DEX). The dashboard by Winnie (Xiao, 2024) and the study by Titan (Titan, 2023) analyzed the vertical integration between searchers and builders through the quantity and value of transactions sent from searchers to builders. Heimbach et al. (Heimbach et al., 2024) observed that during their study, Beaver Builder received a total of 1,941.1 ETH in transaction fees but paid proposers 6,620.94 ETH. This large gap suggests that Beaver Builder might have received significant off-chain profits from its integrated searchers. These studies show that three integrated builders (Beaver, Rsync, and Manta) gain a significant advantage in order flow from their integrated searchers. Our study made the same observation and further quantified the pivotal level.

Strategic behaviors in MEV-Boost auctions. The strategies used by different entities in the MEV-Boost auctions and their potential impacts have attracted significant interest from researchers. The strategic behaviors of proposers were first studied by (Schwarz-Schilling et al., 2023; Wahrstätter et al., 2023b) focusing on the timing game where proposers strategically delay block proposals to maximize their profits. Öz et al. (Öz et al., 2023) further conducted an agent-based simulation to analyze how waiting games affect consensus stability, finding that a delay strategy can be profitable and not degrade consensus if sufficiently many validators adopt it. A recent study (Always, 2024) empirically investigated timing games in the wild and how block proposal delays affect the block fork rate. The results indicate that three validator sets–P2P, Kiln, and Attestant, that are known or suspected of playing timing games–did not delay their block proposals enough to cause their blocks to be forked. Wu et al. (Wu et al., 2024) proposed a game-theoretic model for MEV-Boost auctions, using simulations to examine various builders’ bidding strategies, including naive, adaptive, last-minute, and bluff bidding. Their results highlighted the importance of latency and exclusive order flow in the effectiveness of bidding strategies. Pai et al. (Pai and Resnick, 2023) analyzed the latency advantage of searcher-builder integration in adjusting bidding values. The strategies discussed in these papers highlight the potential factors that can make MEV-Boost auctions uncompetitive or inefficient, while our paper quantifies these uncompetitive and inefficient auctions.

Causes and implications of centralized builder market. A provider may exclusively share its order flow with a single builder. Previous works such as (Kilbourn, 2022; Frontier, 2023; Gupta et al., 2023) pointed out that exclusive order flows have potential centralizing effects on the builder market, because builders with exclusive order flows are more likely to win MEV-Boost auctions, thus gaining further advantages in receiving order flows from non-integrated searchers and in winning order flow auctions. The decentralization of Ethereum’s builder market not only benefits itself but also positively impacts the decentralization of validators. A recent study showed that heterogeneity among validators in building blocks may lead to centralization; however, a decentralized and competitive builder market can encourage validator decentralization (Bahrani et al., 2024). We complement these theoretical analyses with empirical studies to analyze potential problems caused by the current centralized builder market.

Blockchain decentralization metrics. Nakamoto coefficient was proposed to describe the minimum number of entities required to disrupt the blockchain’s subsystem (Srinivasan and Lee, 2017). Other metrics, such as the Gini coefficient (Dorfman, 1979), Shannon entropy (Lin, 1991), and Herfindahl–Hirschman index (Rhoades, 1993), have also been utilized to measure decentralization (or the lack of it) in staking distribution (Grandjean et al., 2023; Kwon et al., 2019), mining power (Lin et al., 2021; Wu et al., 2019; Kwon et al., 2019), and block building (Heimbach et al., 2023). An SoK paper (Zhang et al., 2022) comprehensively summarized the existing works on blockchain centralization; however, none explored decentralization from the perspective of entry barriers or auctions.

7. Discussion

7.1. Limitations of Our Approach and Data

True value. We compute the true values of bids using a similar approach as that in MEV analysis tools (EigenPhi, 2023; Flashbots, 2023b) and previous works (Heimbach et al., 2023; Thiery, 2023). This approach has a few limitations. First, it relies on the knowledge of the set of addresses controlled by each builder. Most builders use well-known addresses to receive payments from searchers and make payments to proposers, but it is possible that some builders use less publicized addresses. We cross-validated our builder address dataset with other sources to ensure completeness (see Sec. 3.1), but if we missed a builder’s address, the computation of extracted value (and hence true value) would be inaccurate. Secondly, this approach neglects off-chain profits, such as off-chain payments received from searchers. Off-chain payments are more likely to happen between integrated builder-searcher pairs. We might underestimate the true value of a block due to unknown off-chain payments, which could lead to the misclassification of an efficient auction as inefficient due to subsidization. However, in our study, we did not observe any excessively large subsidies. Furthermore, underestimating the winner’s true value does not affect our assessment of competitiveness. We might misclassify an uncompetitive auction as competitive if we underestimate the second-highest true value. However, such underestimation should be uncommon, as we observe that most builders bid around our computed true value. It would be irrational for builders not to bid higher to win the auction if they actually have a higher true value.

Missing pivotal providers. Our results in Sec. 4.1 might omit some pivotal providers since the providers we can identify are a subset of all providers. For example, BloXroute (a widely used channel) does not publish the list of transactions they processed. Thus, we can’t evaluate its pivotal level. This limitation is common in existing studies (Lu, 2024; Lu, Angela and Sui, Danning and Durnford, Jaden, 2024). However, there will not be false positives (classification of a non-pivotal provider as pivotal) because we identify a given transaction’s provider based either on the official dataset from MEV-Share and MEV Blocker or on the specific searchers’ addresses (see Sec. 3). Thus, the significance of each provider will only be underestimated rather than overestimated.

Our auction dataset might miss partial bids since they are self-reported by relays. Recall that we used the second-highest bid value in an MEV-Boost auction as the threshold to determine a pivotal provider. Therefore, underestimating the second-highest bid value might also lead us to underestimate the significance of each provider.

7.2. Future Works

Based on the findings, we now outline directions to enhance the decentralization of builder markets. These directions present interesting technical challenges that we leave for future work.

Several issues we identified boil down to the lack of a trustworthy mechanism to facilitate fair exchanges between private order flow providers and builders. In today’s ecosystem builders are at an advantage. To protect themselves, private order flow providers resort to reputation-based solutions such as requiring a minimal market share, which creates siloes.

One approach is building platforms to facilitate the said fair exchange. For example, MEV-Share is one such platform between searchers and builders. To receive order flows from MEV-Share, builders must agree to the Fair Market Principles set force by the community (Flashbots, 2023a). Should builders fail to adhere to these principles, they will be either removed from or flagged by the community.

However, in its current form, MEV-Share is a trusted party. One direction being explored (e.g., by SUAVE (Flashbots, 2024c)) is to use Trusted Execution Environments (TEEs) to run block-building algorithms without leaking private order flows to the builders, but standard challenges such as side channels and covert channels (Salles et al., 2023) apply.

Another unsolved problem is how to reliably detect private order flow leakage across builders. Currently, after receiving private orders, a builder can leak the orders to another builder (potentially a Sybil), bypassing any reputation or economic penalty. One idea is to embed watermarks in order flows to enable tracking. Watermarks must be invisible to the adversary and not interfere with transaction execution. Designing a secure watermarking scheme against a practical adversary model is an interesting future direction.

A reliable leakage detection mechanism (e.g., watermarking) will open up the design space of reputation systems. For example, one possibility is to ask builders to deposit a certain amount of collateral to access private order flows, and order flow leakage will be penalized economically.

8. Conclusion

In this paper, we characterized the efficacy of PBS by evaluating its openness to new builders and assessing the competitiveness and efficiency of the auctions. Our study identifies a significant entry barrier in the builder market: private order flow. We further quantify the barrier costs—a new builder must pay up to 1.4 ETH to access this flow. Given this barrier, it is not surprising that we observed varying capabilities among builders in extracting MEV, with inequalities among top, middle, and tail builders worsening as MEV increases. Our study shows that 88% of the MEV-Boost auctions were competitive, while 79% were efficient. The proposers’ losses due to uncompetitive auctions are 0.98% of their total gain. Based on these insights, we propose suggestions for future developments to mitigate the trust crisis in the MEV-Boost auctions and facilitate the decentralization of Ethereum’s builder market.

Acknowledgements

This work is partially supported by an Ethereum Foundation Grant. We thank ultra sound relay for sharing the full bid dataset. We also thank the teams of BloXroute, Merkle, MeowRPC, MEV Blocker, Flashbots, and Blocknative for answering our questions about access requirements. We are grateful for the valuable discussions with Thomas Thiery and Barnabé Monnot.

References

- (1)

- Always (2024) Data Always. 2024. Latency is Money: Timing Games. https://hackmd.io/@dataalways/latency-is-money. Accessed: 2024-04-20.

- Babel et al. (2023a) Kushal Babel, Philip Daian, Mahimna Kelkar, and Ari Juels. 2023a. Clockwork finance: Automated analysis of economic security in smart contracts. In 2023 IEEE Symposium on Security and Privacy (SP). IEEE, 2499–2516.

- Babel et al. (2023b) Kushal Babel, Mojan Javaheripi, Yan Ji, Mahimna Kelkar, Farinaz Koushanfar, and Ari Juels. 2023b. Lanturn: Measuring economic security of smart contracts through adaptive learning. In Proceedings of the 2023 ACM SIGSAC Conference on Computer and Communications Security (CCS). 1212–1226.

- Bahrani et al. (2024) Maryam Bahrani, Pranav Garimidi, and Tim Roughgarden. 2024. Centralization in block building and proposer-builder separation. arXiv preprint arXiv:2401.12120 (2024).

- Banana Gun (2023) Banana Gun. 2023. Trade Crypto the Banana Way. https://bananagun.io/. Accessed: 2024-03-28.

- Besanko et al. (2009) David Besanko, David Dranove, Mark Shanley, and Scott Schaefer. 2009. Economics of strategy. John Wiley & Sons.

- Bitfly (2024) Bitfly. 2024. Relay Overview - Open Source Ethereum Blockchain Explorer. https://beaconcha.in/relays Accessed: 2024-02-26.

- Blocknative (2024) Blocknative. 2024. Transaction Boost: MEV Protection. https://www.blocknative.com/mev-protection. Accessed: 2024-03-03.

- bloXroute Labs (2024) bloXroute Labs. 2024. Introduction to BackrunMe. https://docs.bloxroute.com/introduction/backrunme. Accessed: 2024-03-03.

- Builder (2024) Titan Builder. 2024. Builder Public Keys. https://docs.titanbuilder.xyz/builder-public-keys. Accessed: 2024-03-21.

- Buterin (2021a) Vitalik Buterin. 2021a. Endgame. https://vitalik.eth.limo/general/2021/12/06/endgame.html. Accessed: 2024-03-25.

- Buterin (2021b) Vitalik Buterin. 2021b. Proposer/block builder separation-friendly fee market designs. https://ethresear.ch/t/proposer-block-builder-separation-friendly-fee-market-designs/9725. Accessed: 2024-04-29.

- Buterin et al. (2020) Vitalik Buterin, Diego Hernandez, Thor Kamphefner, Khiem Pham, Zhi Qiao, Danny Ryan, Juhyeok Sin, Ying Wang, and Yan X Zhang. 2020. Combining GHOST and casper. arXiv preprint arXiv:2003.03052 (2020).

- contributors (2024) Wikipedia contributors. 2024. English auction. https://en.wikipedia.org/wiki/English_auction. Accessed: 2024-04-28.

- Costan and Devadas (2016) Victor Costan and Srinivas Devadas. 2016. Intel SGX explained. Cryptology ePrint Archive (2016).

- Daian et al. (2020) Philip Daian, Steven Goldfeder, Tyler Kell, Yunqi Li, Xueyuan Zhao, Iddo Bentov, Lorenz Breidenbach, and Ari Juels. 2020. Flash boys 2.0: Frontrunning in decentralized exchanges, miner extractable value, and consensus instability. In 2020 IEEE symposium on security and privacy (SP). IEEE, 910–927.

- DataAlways (2024) DataAlways. 2024. Public domain Ethereum MEV-Boost winning bid data. https://github.com/dataalways/mevboost-data. Accessed: 2024-04-13.

- Dorfman (1979) Robert Dorfman. 1979. A formula for the Gini coefficient. The review of economics and statistics (1979), 146–149.

- EigenPhi (2023) EigenPhi. 2023. Wisdom of DeFi. https://eigenphi.io/. Accessed: 2023-04-16.

- Ethereum (2024) Ethereum. 2024. Gas and fees — ethereum.org. https://ethereum.org/en/developers/docs/gas/. Accessed: 2024-04-23.

- Ethereum Foundation (2024a) Ethereum Foundation. 2024a. How to stake your ETH. https://ethereum.org/en/staking/. Accessed: 2024-04-07.

- Ethereum Foundation (2024b) Ethereum Foundation. 2024b. Proposer Builder Separation (PBS) - Ethereum Roadmap. https://ethereum.org/en/roadmap/pbs/. Accessed: 2024-03-25.

- Ethereum Research (2023) Ethereum Research. 2023. Bid cancellations considered harmful. https://ethresear.ch/t/bid-cancellations-considered-harmful/15500. Accessed: 2023-04-16.

- Etherscan (2024) Etherscan. 2024. MEV Bot Accounts. https://etherscan.io/accounts/label/mev-bot. Accessed: 2024-03-21.

- Etherscan (2024) Etherscan. 2024. MEV Builder Accounts. https://etherscan.io/accounts/label/mev-builder. Accessed: 2023-04-26.

- EthStaker Community (2024) EthStaker Community. 2024. MEV Relay List. https://ethstaker.cc/mev-relay-list. Accessed: 2024-04-26.

- Eyal and Sirer (2018) Ittay Eyal and Emin Gün Sirer. 2018. Majority is not enough: Bitcoin mining is vulnerable. Commun. ACM 61, 7 (2018), 95–102.

- Flashbots (2022a) Flashbots. 2022a. MEV-Boost Relay for Ethereum proposer/builder separation (PBS). https://github.com/flashbots/mev-boost-relay. Accessed: 2024-04-07.

- Flashbots (2022b) Flashbots. 2022b. MEV for the Next Trillion, It’s Time to Get Serious. https://writings.flashbots.net/mev-for-the-next-trillion. Accessed: 2024-04-25.

- Flashbots (2023a) Flashbots. 2023a. Decentralized Orderflow Working Group. https://github.com/flashbots/dowg. Accessed: 2024-04-02.

- Flashbots (2023b) Flashbots. 2023b. mev-inspect-py: an MEV inspector for Ethereum. https://github.com/flashbots/mev-inspect-py. Accessed: 2023-04-16.

- Flashbots (2024a) Flashbots. 2024a. coinbase.transfer() — Flashbots Docs. https://docs.flashbots.net/flashbots-auction/advanced/coinbase-payment. Accessed: 2024-04-09.

- Flashbots (2024b) Flashbots. 2024b. Flashbots Data. https://flashbots-data.s3.us-east-2.amazonaws.com/index.html. Accessed: 2024-03-21.

- Flashbots (2024c) Flashbots. 2024c. The Future of MEV is SUAVE. https://writings.flashbots.net/the-future-of-mev-is-suave. Accessed: 2024-03-25.

- Flashbots (2024) Flashbots. 2024. Introduction to MEV-Boost. https://docs.flashbots.net/flashbots-mev-boost/introduction. Accessed: 2024-04-26.