Optimal Bias-Correction and Valid Inference in High-Dimensional Ridge Regression: A Closed-Form Solution

Ridge regression is an indispensable tool in big data econometrics but suffers from bias issues affecting both statistical efficiency and scalability. We introduce an iterative strategy to correct the bias effectively when the dimension is less than the sample size . For , our method optimally reduces the bias to a level unachievable through linear transformations of the response. We employ a Ridge-Screening (RS) method to handle the remaining bias when , creating a reduced model suitable for bias-correction. Under certain conditions, the selected model nests the true one, making RS a novel variable selection approach. We establish the asymptotic properties and valid inferences of our de-biased ridge estimators for both and , where and may grow towards infinity, along with the number of iterations. Our method is validated using simulated and real-world data examples, providing a closed-form solution to bias challenges in ridge regression inferences.

Keywords: Ridge Regression, Bias Correction, High-Dimension, Ridge Screening, Inference, Bias-Variance Trade-off

Regularization theory was one of the first signs of the existence of intelligent inference.—Vladimir N. Vapnik (p.9, Vapnik (2013))

1 Introduction

Ridge regression, or more formally -regularization estimation, is a fundamental tool in econometrics, statistics, and machine learning with applications in various fields of science, technology, engineering, mathematics, medicine, social sciences, and humanities. The idea of -regularization appeared in the early 1940s for the stability of inverse problems; see Tikhonov (1943). It was first introduced to data analysis by Hoerl (1959) and later formulated in Hoerl and Kennard (1970b, a) for providing a robust solution to some of the persistent challenges encountered in traditional linear regression techniques; see Hoerl (1985) for a nice review. Emerging as a fundamental technique in predictive modeling, ridge regression addresses issues such as multicollinearity and overfitting, which commonly afflict predictive models dealing with high-dimensional data. Since its inception, ridge regression’s practical adoption persists due to its superior performance over the least-squares estimator in various scenarios, evident in applications across neuroscience, chemistry, biology, and economics; see Leonard et al. (2023), Zahrt et al. (2019), Otwinowski and Plotkin (2014), Giannone et al. (2021), and Abadie and Kasy (2019), among others, underscoring its empirical effectiveness. From a shrinkage perspective, the ridge estimator also dominates the least-squares solutions in the sense that its mean-squared errors (MSEs) can be smaller, which provides a reasonable explanation on the empirical effectiveness of ridge estimators. See Theobald (1974), Athey and Imbens (2019), Hastie (2020), Hansen (2022a), and a comprehensive introduction to ridge regression in van Wieringen (2023).

The ridge estimator offers a closed-form expression that simplifies both theoretical and empirical analyses. It aligns with the dense modeling techniques of Giannone et al. (2021), which acknowledge the potential significance of all explanatory variables for prediction. Empirical studies, such as those in Giannone et al. (2021), indicate that dense models generally tend to outperform the sparse ones in out-of-sample economic prediction performance. Similarly, Abadie and Kasy (2019) find that the ridge estimators dominate the lasso and the pre-testing estimators in terms of the risks when the effects of different predictors on the dependent variable are “smoothly distributed”. These results suggest that ridge estimators indeed constitute a crucial tool in econometric modeling and economic forecasting, especially in the big data era.

However, as highlighted in Section 2.8 of Athey and Imbens (2019), constructing valid confidence intervals remains a challenge for many regularized methods, including ridge regression, even in asymptotic settings. This long-standing challenge in ridge-type regression involves at least two critical aspects within a linear regression framework: (a) performing hypothesis tests on specific linear combinations of the regression coefficients using the ridge estimators; and (b) deriving confidence or prediction intervals based on the ridge estimators in empirical applications. The primary reason for these challenges is that the inherent bias of ridge estimators poses significant challenges, compromising both statistical efficiency and scalability across various applications. To date, the feasibility of conducting statistical inferences and hypothesis testing on ridge-type estimators without imposing additional structural constraints remains largely unexplored in the literature. This complexity arises from the ridge estimator’s intrinsic bias, which complicates direct statistical inferences despite its elegant closed-form expression. As a result, research addressing the inference challenges of ridge regression in high-dimensional settings is limited, leading to its widespread application across disciplines without comprehensive theoretical investigations.

To the best of our knowledge, there are only a few works in the literature concerning the bias and inference of ridge estimators under different scenarios. Under a sparse structure, Shao and Deng (2012) proposed a threshold ridge regression method and proved its consistency. The method therein actually estimates the projected coefficient vector rather than the true one in the linear model. Dobriban and Wager (2018) derived the limit of the predictive risk of ridge regression and regularized discriminant analysis in a dense random effects model. Bühlmann (2013) proposed to use the lasso to correct the bias of ridge estimators. However, the estimation depends on the existence of an initial estimator which needs to be accurate enough. Zhang and Politis (2022) adopted a similar approach as that in Shao and Deng (2012) and proposed a threshold ridge regression and a bootstrap method to make inferences. However, the method therein still estimates the projected coefficient vector rather than estimating the true one, and the remaining bias may not be asymptotically negligible in general.

In this paper, we introduce a systematic approach tailored specifically for mitigating the bias in ridge-type estimators for high-dimensional linear regression models. Leveraging the closed-form expression of the ridge estimators, the bias term can also be established in an analytic form. Although the bias term involves the true parameters which are unknown in practice, we found that replacing the true parameters with the ridge estimators turns out to be an effective way to mitigate the bias. Therefore, the proposed method employs an iterative bias-correction strategy, and the bias can be reduced substantially when the number of iterations is sufficiently large. Notably, it achieves complete bias correction if the covariate dimension is smaller than the sample size , and can reduce considerable bias if surpasses . We show that our bias-correction method is an optimal one in the sense that the bias can be completely corrected (asymptotically) when with a sufficient number of the proposed bias-correction iterations, and the remaining bias of the de-biased ridge estimator when is unattainable through any linear transformations of the response vector.

To further combat the remaining bias in the de-biased ridge estimators when , we introduce a novel ridge-screening (RS) method for covariate selection prior to applying our bias correction procedure. The RS approach constructs a restricted model that inherently encompasses the true model as a subset. This is based on the assumption that only a subset of the covariates holds significance in the linear model. Specifically, we postulate that the number of significant covariates should be less than the sample size, which can appropriately diverge relative to the dimension and sample size . Crucially, we demonstrate that under certain mild conditions, the true model is inherently nested within the selected one, establishing RS as a novel variable selection approach that offers independent value beyond bias correction. Leveraging this restricted model, our bias-correction procedure can be further applied to the restricted model and effectively rectifies the bias in the resulting ridge estimators

The derivation of the methodology and theory is mainly based on a fixed design, which is similar to the setting in Hansen (2022b), and the results throughout this paper are valid for random regressors by conditioning on the design matrix. This paper rigorously establishes the asymptotic properties and provides valid inferences of our estimators for both and under some relaxed and intuitive conditions. Furthermore, we delve into the bias-variance trade-off of our de-biased ridge estimators, examining its relationship with the number of iterations in the bias-correction procedure. To validate our methodology, we provide empirical evidence using both simulated and real-world data. The prediction intervals constructed by the proposed method are indeed satisfactory for forecasting the U.S. macroeconomic series using factor-augmented regression. Moreover, the RS method can further enhance the coverage rates of these prediction intervals. These empirical validations highlight the practical efficacy and adaptability of our approach across a wide range of high-dimensional regression settings.

The contributions of this paper are multi-fold. First, the proposed bias-correction method is simple and easy to implement. In fact, the proposed approach is a systematic procedure and the resulting de-biased estimator has a closed-form expression. Second, the optimality of the proposed bias-correction procedure consists of two aspects: (a) it achieves complete bias correction when the covariate dimension is smaller than the sample size ; and (b) the remaining bias of the de-biased ridge estimator in the scenario when is unattainable through any linear transformations of the response vector. These results distinguish our work from the existing ones that only part of the bias can be corrected in most of the aforementioned literature. Third, we also propose a novel variable selection procedure, namely the ridge-screening (RS) method, which screens out some insignificant variables based on the de-biased ridge estimator due to its optimality. Fourth, we also establish the asymptotic properties of the de-biased ridge estimators in both scenarios when and , and it is shown that the de-biased ridge estimators are asymptotically normal, which provides valid inference methods for the ridge estimators. Fifth, we develop a procedure to construct confidence and prediction intervals in ridge regressions using our proposed de-biased estimators and associated inference methods. Finally, we establish the bias-variance trade-off of our proposed approach both theoretically and through validation with simulated data. It’s important to note that, unlike the scenario described in Section 2.8 of Athey and Imbens (2019) where many inference approaches for regularized machine learning methods compromise predictive performance, our proposed procedure focuses on correcting the bias and rendering the estimators suitable for inferences, without adversely affecting their predictive performance.

We highlight that the asymptotic framework adopted in this paper is slightly different from traditional approaches in the literature. Typically, in conventional frameworks, the asymptotic properties are established when the dimension and/or the sample size are approaching infinity. However, in our study, most of the asymptotic results are derived under a different scenario that the number of iterations in the bias-correction procedure tends towards infinity for any given configuration of the dimension and the sample size . This configuration can be sufficiently large to encompass the framework of big data analysis. One of the primary motivations behind this choice is to demonstrate the validity of our proposed procedure by explicitly providing the exact bias and covariance terms of the de-biased estimators in this paper. This approach is also reasonable because it reflects common scenarios encountered in practical data analysis, where datasets often have fixed dimensions and sample sizes. Without this setting, the dimensions of the bias and covariance terms of the de-biased estimators would expand to infinity if we considered and approaching infinity, making them challenging to formulate and describe theoretically. Moreover, our asymptotic results remain valid as and approach infinity. This holds true so long as we initially allow the number of iterations to increase towards infinity at a moderate rate. In this asymptotic manner, we can symbolically retain the forms of the bias and covariance terms for a growing configuration of . Therefore, it’s important to emphasize that our chosen asymptotic framework does not undermine the validity of the proposed bias-correction procedures.

The rest of the paper is organized as follows: Section 2 introduces the ridge estimation and its bias-correction procedure in scenarios when and , where a ridge-screening method is also introduced for variable selection. Following this, Section 2 also presents the inference methodologies for the proposed de-biased estimators. Section 3 examines the proposed approach’s finite-sample performance via Monte-Carlo simulations. Section 4 provides an empirical application of the proposed method, and Section 5 offers conclusive insights. All proofs and derivations for the asymptotic results are available in an online Appendix.

Notation: We use the following notation. For a vector , is the -norm and is the -norm. denotes the identity matrix. For a matrix , its operator norm is , where denotes the largest eigenvalue of a matrix, and is the square root of the minimum non-zero eigenvalue of . denotes the absolute value of elementwisely. The superscript ′ denotes the transpose of a vector or matrix. We also use the notation to denote and or and have the same order.

2 Models and Methodology

2.1 High-dimensional Linear Regression

Let be a given sample of centered observable data. We consider the problem of estimating a -dimensional vector from the following linear model:

| (1) |

where is a scalar response variable, is a -dimensional covariate vector, and is a random error term with mean zero and finite variance. Similar to the setting in Hansen (2022b) and Ch. 29 of Hansen (2022a), we treat the design matrix consisting of covariates as a fixed one. But the estimation results throughout the paper remain valid for random regressors by conditioning on the design matrix data . Note that Model (1) can be expressed in vector form

| (2) |

where is an -dimensional response vector, and is an -dimensional vector of errors with and , where is a diagonal matrix with positive and bounded diagonal elements. If and is an invertible matrix, the least-squares estimator for is

| (3) |

Note that the least-squares estimator is only well-defined if exists. In a high-dimensional setting, if the columns of the design matrix are linearly dependent, for example, this is obviously true when , this collinearity among the columns implies that is singular, rendering an invalid estimator. To make the least-squares estimator in (3) a well-defined quantity, we modify the definition in (3) as

| (4) |

where is the Moore-Penrose generalized inverse. It is not hard to see that the estimator in (4) reduces to the one in (3) if and is invertible. Therefore, we will denote the estimator in (4) as the least-squares solution throughout this article.

2.2 Ridge Regression

The ridge regression estimator was first proposed by Hoerl (1959); see the review article of Hoerl (1985). It essentially comprises of an ad-hoc fix to resolve the singularity issue of in the presence of many covariates. Suppose is invertible for a given , the ridge estimator is defined as

| (5) |

which simply replaces by with a tuning parameter in the least-squares estimator of (3). From a regression point of view, the ridge estimator can be obtained in the following way. Let and be the augmented data, the ridge estimator is a solution to the following optimization problem:

| (6) |

From the expression of the ridge estimator for a given , it is not hard to see that

and

which is the componentwise regression estimator if each covariate is standardized. Therefore, a large would reduce the variance of the estimator, but the bias may increase as grows.

In this paper, we only focus on a given and investigate the bias-correction and inference issues for . For the purpose of comparisons with the proposed approach, we first specify the initial bias of the ridge estimator of (5) in the following theorem.

Theorem 1.

Remark 1.

The condition for the result in Theorem 1 to hold is the same as that for linear regression models. If the design matrix is random with either independent and identically distributed () or weakly dependent columns, we require , and then, the bias of the ridge estimator conditioning on and a given is

which is the same as that in (7). See also Ch. 29.6 in Hansen (2022a) for details.

From Theorem 1, the bias of the ridge estimator depends on the unknown true parameter . Therefore, it is fundamentally challenging to make any statistical inference on the ridge estimator or to construct any confidence or prediction intervals involving the ridge estimator. Consequently, it is important to seek an effective way to correct or reduce the bias of a ridge estimator.

In the next section, we will tackle this issue by proposing an iterative procedure to reduce the bias of the ridge estimators.

2.3 Bias-Correction

The discussion in this section is divided into two key parts depending on whether is invertible or singular. For simplicity, in line with the setting in Wang and Leng (2016), we assume that is invertible when and singular when throughout this article111An alternative framework is to consider the scenarios that and , a common setting in random matrix theory, which is also helpful in establishing the asymptotic results if we further allow later.. This assumption is well-justified as we consider a fixed design matrix in this paper and naturally maintains its invertibility when . Furthermore, in extreme cases where highly correlated variables are present within (in a random sense), we may implement specific transformations based on prior knowledge or statistical methods such as the hierarchical clustering or the -means algorithm to mitigate these correlations prior to conducting ridge regression; see the discussion in Section 4.1.2 of Fan and Lv (2008). Consequently, we only focus on the bias-correction issue in this paper and rule out the case when some covariates in are highly correlated.

Note that the ridge estimator in (5) can be written as

| (8) |

The bias-correction procedure is based on this expression and (7) in Theorem 1. The rationale for the procedure is as follows. Since in the bias term of (7) is unknown, we first replace it by defined in (5) and construct a first-step de-biased ridge estimator as

| (9) |

Plugging from (8) into (9), we obtain:

| (10) |

Consequently, the bias term of is

| (11) |

It’s apparent that the -norm of the bias term produced by is smaller than that of the initial bias in Theorem 1 under mild conditions, implying that the bias has been partially corrected by . To see this, we conduct a singular-value decomposition on or a spectral decomposition on , and the effectiveness of the bias-correction approach depends on two observations: (a) the eigenvalues of are positive and strictly less than one; and (b) the eigenvalues of becomes smaller in the de-biased estimator of (10) compared to those of in .

Following the first step, we replace the unknown vector in (11) by the ridge estimator again, leading us to construct a second-step de-biased estimator:

| (12) |

By a similar argument, the bias term of is

| (13) |

where the eigenvalues of are even smaller compared to those of in . Consequently, we can show that the -norm of the bias is smaller than that of under the same framework. We continue this procedure and denote

| (14) |

as a de-biased estimator at the -th step, where we define for . To characterize the effect of the bias correction, we make an assumption on the singular-value decomposition (SVD) of first.

Assumption 1.

For , is invertible and the SVD of is , where and with for .

Assumption 1 is intuitive for a fixed design with a large and fixed configuration of . For example, the eigenvalues of are of order if the entries of are independent copies of a random variable with zero mean, unit variance, and finite fourth moment if ; see the Bai-Yin’s law in Bai and Yin (1993). Consequently, the eigenvalues of are strictly less than one, which ensures that our iterative procedure can substantially reduce the bias. In fact, we have the following theorem on the de-biased ridge estimator in (14).

Theorem 2.

Remark 2.

(i) We observe that the assumptions required for Theorem 2 are quite minimal. We only need the fundamental assumptions inherent to linear regression models, ensuring that the bias term can be asymptotically eliminated with a sufficient number of iterations.

(ii) The requirement for the -norm of to be finite stems from the expectation of the response having a limited number of significant covariates in linear regression models. Without this restriction, as the number of covariates grows, each coefficient’s contribution might become sufficiently small, allowing the response’s variance to remain finite. It’s important to highlight that the condition for the number of iterations can still be met even if at a polynomial rate. This is because decays exponentially, given that for . Thus, the number of iterations can be selected to scale logarithmically with the dimension .

(iii) As discussed in the Introduction section, the asymptotic results in Theorem 2 are established for any given

as

. This approach is also reasonable because it reflects common scenarios encountered in practical data analysis, where datasets often have fixed dimensions and sample sizes.

As a matter of fact, if Assumption 1 holds for increasing and with , the results remain applicable when first, followed by

. In addition, under the framework in Bai and Yin (1993) that , the asymptotic results hold simultaneously as if and the penalty parameter because still hold in this setting.

(iv) Although the convergence in Theorem 1 is based on a given , it can be readily shown that

implying that the convergence to zero is uniformly for a range of . Similar argument also applies to the asymptotic results in Theorem 3-5 below.

Theorem 2 implies that we can completely correct the bias term incurred by the ridge estimator if so long as we conduct a sufficient number of iterations. This result is particularly useful for empirical data analysis when and are given.

To investigate the performance of the de-biased estimator when under which is a singular matrix, we first perform a singular-value-decomposition on . Suppose the true rank of is , where we can simply set since we deal with a given and fixed configuration of without including highly correlated covariates. However, the results in Theorem 3 still hold for . By abuse of notation, there exist semi-orthogonal matrices and , and a diagonal matrix with such that

| (16) |

Since is symmetric and invertible, there also exists an orthogonal complement matrix of such that

| (17) |

We formulate the above description in Assumption 2 below.

Assumption 2.

Then, we have the following theorem.

Theorem 3.

Remark 3.

(i) The requirement for the number of iterations is the same as that in Theorem 2, and therefore, we omit the illustrations to save space.

(ii) The bias term in Theorem 3 corroborates the assertion in Shao and Deng (2012) that ridge regression primarily estimates

rather than .

(iii) Similar to Theorem 2, the asymptotic results in Theorem 3 are established for any given configuration of as , because we can explicitly specify the bias term for fixed and . If we additionally allow , the result in Theorem 3 can be reformulated as

so long as and for , where is the rank of .

(iv) It’s possible that the rank of is in the case of . In such situations, we can obtain similar results as those outlined in Theorem 3. The approach to handling this scenario is similar to that for , and therefore, we omit further discussion on this and focus on the previously mentioned setting.

A key insight from Theorem 3 is that there is a remaining bias term that cannot be corrected by the proposed method. This is understandable since the projection of on the singular directions is not captured in Model (2) according to the singular-value-decomposition of in (16). If the vector belongs to the space spanned by the columns of , there will be no need to correct the bias since . Otherwise, it is challenging to make such a correction for the bias in Theorem 3. As a matter of fact, we have the following theorem regarding the bias term in Theorem 3.

Theorem 4.

Under the conditions in Theorem 3, there is no linear transformation matrix such that .

We focus on linear transformations of the data in Theorem 4 because the least-squares estimator and the ridge estimator are all linear combinations of the data . Theorem 4 indicates that the remaining bias term is unattainable through any linear transformation of the data , showing that the proposed approach does its best to correct the bias. The results in Theorems 2–4 also indicate that our bias-correction method is an optimal one for any given .

2.4 Ridge Screening

To further address the uncorrectable bias term identified in Theorem 3 and ensure valid statistical inferences when , additional structures must be imposed on the parameters or covariates. Without these additional structures, as demonstrated in Theorem 4, the bias-correction becomes challenging. In the subsequent analysis, we will use or to denote a generic constant, the specific value of which may vary across different contexts.

In this section, we propose a ridge-screening approach to select the significant variables in Model (2). It is feasible for both scenarios when and . Therefore, it can also be treated as a new variable selection approach especially useful in a high-dimensional setting, which is of independent interest to statisticians, econometricians, and data scientists. We only focus on the scenario when and is singular in such a situation. Note that the reason for the remaining bias term in Theorem 3 that cannot be corrected is that some projection directions of the coefficients are not captured in Model (2). For example, this is the case when some parameters in are redundant if certain covariates in are strongly correlated. Therefore, it is reasonable to make an assumption that some covariates in are not useful in the linear regression (2), and hence, they can be dropped first before establishing valid ridge estimators. To embrace the sparsity assumption in high-dimensional data analysis, we assume the true parameter vector belongs to the following submodel class

| (18) |

where we assume its cardinality . It is obvious that we require , which is the rank of defined in Assumption 2. This cardinality assumption is natural and it reflects the idea that many coefficient parameters are relatively small among the -dimensional vector . We treat them as zero elements only for ease of exploitation. According to the results in Theorem 2 and Theorem 3, we can see that

| (19) |

as for a given .

It is intuitive to expect that the components of corresponding to positions in the submodel will be greater than those at positions in , the complement set of . This is due to the following reason: Assuming the number of nonzero elements in is finite or relatively small compared to , then the -norm of the -dimensional dense vector is also of finite or relatively small order. Consequently, the magnitude of each projected coordinate in is of a smaller order compared to the nonzero elements in on average. Therefore, we propose a Ridge-Screening (RS) method that selects the submodel class

| (20) |

where and we use a different penalty to distinguish it from the one utilized in the subsequent step. The ranking method to derive the submodel in (20) is similar to the approach presented in Section 2.2 of Fan and Lv (2008). However, the method in Fan and Lv (2008) is based on marginal correlations between the response and the features, while (20) is a utilization of a de-biased estimator, which is more proximate to the true parameter than the conventional ridge estimator in Eq. (5) of Fan and Lv (2008). Furthermore, our methodology is not constrained by a specific choice of , and it can be chosen by an information criterion or a cross-validation method as discussed at the end of Section 2.4.

In practice, we may select in (20) through cross-validation along with because the actual design matrix with columns of covariates is no longer singular in such cases. Additionally, we can show that the model with covariates asymptotically encompasses the submodel in (18) under mild conditions, i.e., the true submodel in (18) is nested within the one with covariates.

Now, we restrict the design matrix to the submodel class and denote the restricted design as , and the new ridge estimator is

| (21) |

where , and can be different from the used in the ridge screening approach in (20). When and are optimally selected using the method outlined at the end of Section 2.4 below, we can set because it is optimal for the restricted ridge estimator with a given set of significant variables. We observe that the eigenvalues of are strictly greater than zero for a given configuration of . This essentially reduces the scenario to the case when in Section 2.3. Consequently, we can employ the bias-correction procedure detailed in Section 2.3 over iterations to obtain a de-biased estimator:

| (22) |

To establish the asymptotic properties of the RS method and the de-biased estimator for the restricted one in (22), we make a few intuitive assumptions first.

Assumption 3.

The nonzero singular values of in (16) are of order and the penalty parameters .

Assumption 4.

For any submatrix of with dimension , all the eigenvalues of , denoted as for , are of order .

Assumption 5.

For defined in (18), for some , and the magnitude of the -th projected coordinate for , and , where is the number of nonzero elements in .

Assumption 6.

Assume is a sub-Gaussian random variable in the sense that

for any which is a finite positive constant.

Assumptions 3-4 are natural conditions about the orders of the singular values of and , and the penalty parameter (or ) is comparable to the magnitude of (or ). Similar to the illustrations for Assumption 1, the magnitude in Assumption 3-4 can be easily verified if the entries of are independent copies of a random variable with zero mean, unit variance, and finite fourth moment under the setting ; see Bai and Yin (1993). In fact, the orders specified in Assumptions 3-4 are only employed to establish the validity of the ridge-screening method in Theorem 5 below, and they are not the only ones capable of achieving this, so long as the rates can be properly controlled in the proof of Theorem 5. For any fixed which can be large, the efficacy of the bias-correction method and the inference methods in Section 2.5 below remain valid so long as the nonzero singular values and the penalty parameters are strictly greater than zero. Assumption 5 indicates that the minimum nonzero element in cannot be too small, and the norm of the -th projected coordinate is bounded by the magnitude of its original coordinate (up to a small constant). This is actually a reasonable and intuitive assumption. For instance, in Assumption 5, if (at most) because there are only nonzero elements in , then , but it is a -dimensional vector, meaning that the magnitude of each is of order on average. We may postulate that in such a case and Assumption 5 is even slightly weaker than this situation as we can allow that the projected coordinate to be of the same order as that of the original one. Assumption 6 is a general condition that includes Gaussian distributions as a special case.

We have the following theorem regarding the de-biased estimator in (22) after the ridge-screening.

Theorem 5.

Let Assumptions 1-6 hold.

(i) Assuming the true parameter belongs to the submodel in (18). If , the number of iterations in the first stage satisfies , and , the number of selected elements in (20), satisfies that when , and

we have

where we use in the sense that may contain more parameters than .

(ii) Conditioning on the event of , for a properly chosen , the bias of the de-biased and restricted ridge estimator is

| (23) |

where is the true value of restricted on the submodel . That is, consists of the nonzero elements in and some zero ones associated with their original indexes in . If the number of iterations satisfies , we have

Remark 4.

(i) Theorem 5 implies that the ridge-screening method is applicable in both and scenarios. Remarkably, there’s no need to specify , which is the number of nonzero elements in the true . For , we can simply set as Assumption 2 and choose variables which consists of all the covariates. For , we may choose under the assumption that and in an asymptotic sense, which is reasonable because is often small and we can adopt in the setting of random matrix theory.

(ii) Theorem 5 establishes that our proposed method from Section 2.3 can completely correct the bias of the restricted ridge estimators, which is particularly helpful when . This, in conjunction with the results of Theorem 2, confirms the versatility of our bias-correction approaches in addressing both scenarios where and .

(iii) For , our discoveries from Theorems 4-5 underscore the significance of initially reducing all covariates to significant ones, where . This reduction, combined with the proposed bias-correction procedure for the restricted ridge estimators, enables subsequent valid statistical inferences using the de-biased ridge estimators, as detailed in Section 2.5 below.

To conclude this subsection, we provide a summary of the pseudo-code for the proposed bias-correction procedures in Algorithm 1 and Algorithm 2, corresponding to the scenarios of and , respectively. For the convergence criterion in Algorithm 1, we can choose a small threshold , say , and the convergence of the algorithm is determined by checking whether the following inequality hold:

| (24) |

It’s important to note that the convergence is guaranteed because the sequence converges, as demonstrated in the proof of Theorem 2 in the Appendix. Additionally, we emphasize that the number of iterations is typically not large, as only a logarithmic order of the dimension is required to ensure convergence, as discussed in Remark 2.

Finally, we briefly discuss the methods for selecting the unknown parameters in Algorithms 1-2 of the proposed approaches. Firstly, the sole unknown parameter in Algorithm 1 is . Throughout this paper, we assume to be given, as our focus is mainly on the bias-correction issue for ridge estimators. Empirically, one can employ the widely-accepted information criteria (e.g., AIC or BIC) or utilize cross-validation methods to determine an appropriate . For a comprehensive understanding, readers are referred to Section 1.8 of van Wieringen (2023). Secondly, in the ridge-screening method of Algorithm 2 when , the parameters are unknown. Here, one can employ the aforementioned information criteria or cross-validation methods, as discussed in Sections 1.8.1-1.8.3 of van Wieringen (2023), to simultaneously determine . This can be achieved by selecting a candidate for and then determining the optimal such that the pair minimizes the information criterion or yields the best prediction performance on test sets using the restricted ridge estimator . The final choice of can be determined by evaluating the performance across each grid point of the penalty parameters. After identifying the significant variables through the RS method, the parameter used in bias-correction is equal to , as represents the optimal choice for the associated . Given that these methods are well-established in the literature, we omit further details here to save space.

Input: Design matrix , response vector , and penalty ;

Output: A de-biased ridge estimator .

Input: Design matrix , response vector , and penalty parameters ;

Output: A de-biased ridge estimator .

2.5 Inference

In this section, we briefly introduce the inference method for the de-biased ridge estimators in Sections 2.3 and 2.4. The following theorem can be derived immediately based on the proofs of Theorem 2 and Theorem 5.

Theorem 6.

Assume , where is a diagonal covaraince matrix.

(i) If and is invertible. Under Assumption 1, we have

where denotes the exact distribution, , and

Furthermore, for any given configuration of with , we have

where is the asymptotic limit of .

(ii) Under Assumptions 2-6 and a true model in (18) when . Suppose is sufficiently large in the ridge-screening such that the event holds. Then the estimator in (22) has the following limiting distribution

where , and

Furthermore, for any given configuration of with , we have

where is the asymptotic limit of .

Remark 5.

(i) The Assumption of can be relaxed to is a martingale difference sequence with finite variances, and the results in Theorem 6 still hold if we make use of martingale central limit theorems in Hall and Heyde (2014) as under Assumptions 3-4.

(ii) Equation (14) and Theorem 6 indicate that

| (25) |

and

| (26) |

for and , respectively, where denotes approximate equivalence in distribution for sufficiently large and a given configuration of . Therefore, we can make use of the approximations in (5) and (5) to make statistical inference.

(iii) Under the assumption that and the nonzero singular values of are of order , we can easily show that the variance terms in (5) and (5) are of order . Consequently,

implying that our de-biased estimators are convergent with standard rate .

(iv) In practice, it is often assumed that the error term is homoskedastic with , which simplifies the inference.

Consequently, for sufficiently large and , a consistent estimator for can be obtained as:

depending on whether or . Then, the variance terms in (5) and (5) can be estimated from the data.

Hence, by correcting the bias, we can proceed to make statistical inferences and construct confidence intervals using distributions in (5) and (5) without the need to identify the sparse structure in Model (1). This is possible because all biases can be approximated by the data, and the covariance terms in the limiting distributions are of full rank, and they can be estimated from the available data.

2.6 Time Series Ridge Regression

In this section, we briefly illustrate the feasibility of the proposed bias-correction method in time series ridge regression. In particular, we consider the following Auto-Regressive (AR) model:

| (27) |

where is the covariate vector consisting of the lagged variables of , and is the associated parameter vector. We restrict our consideration to cases where . It’s uncommon to encounter situations where the number of lagged regressors in autoregressive (AR) models exceeds the sample size. In practical datasets, instances of AR models with orders surpassing, for instance, , are quite rare.

Let , , and , then, Model (27) can be expressed as

| (28) |

where we assume for simplicity. For a proper , the de-biased estimator in (14) can be written as

For weakly stationary time series sequence , the ergodic theorem guarantees that

Suppose the covariance matrix admits a similar spectral decomposition as in Assumption 1 above, and the the magnitude of the penalty satisfies as that in Assumption 3, we can show that

For large , it follows that

| (29) |

and

| (30) |

Equation (29) suggests that the bias-correction procedure remains applicable to time series regression with weakly dependent regressors. Additionally, Equation (30) confirms that the asymptotic distribution from Theorem 6(i) holds true for time series data as well.

2.7 Constructions of Confidence and Prediction Intervals

In this section, we explore methods for constructing confidence and prediction intervals based on ridge regression. For simplicity, we assume to facilitate the illustrations.

We begin by outlining the construction of confidence intervals for the mean response with a given covariate when . Note that in a ridge regression, then, by (5) in Remark 5(ii) with a sufficiently large , we have

| (31) |

where

In practice, we may replace in by , which is estimated from the data as that in Remark 5(iv), and we denote the estimated variance in (31) by . Denote the critical value of a standard normal distribution such that its tail probability is , then, the -confidence interval for is , where

| (32) |

and

| (33) |

Next, we discuss the way to construct prediction intervals for a future value with a new covariate . According to Ch. 2 of Montgomery et al. (2012), by a similar argument as that for the confidence intervals, we can construct the -prediction intervals of the future value as , where

| (34) |

and

| (35) |

The values presented in (32)-(35) are directly estimated from the data. Consequently, we are equipped to construct valid confidence and prediction intervals in ridge regression employing our proposed bias-correction techniques. Analogously, confidence and prediction intervals can also be established for models utilizing de-biased ridge estimators post ridge-screening when . For instance, the -prediction interval of the future value produced by the restricted ridge estimator is with

| (36) |

and

| (37) |

where is the -dimensional sub-vector of the new covariate selected by the ridge-screening method.

2.8 Bias-Variance Trade-off

The bias-variance trade-off is a fundamental concept in machine learning and statistics. It refers to the delicate balance between two sources of error in a predictive model. It is a way of analyzing a learning algorithm’s expected errors. Therefore, it would be interesting if we can derive the bias-variance trade-off of our de-biased estimators as we increase the number of iterations.

In this section, we study the MSE of the de-biased ridge estimator in the -th iteration for with a given . The analysis of the scenario where is similar, and hence, we only derive it for the case when . The MSE of the -th de-biased ridge estimator is defined as

| (38) |

For simplicity, we assume . By Assumption 1 and Theorem 6(i),

| (39) |

where with

By a similar argument, we can show that

| (40) |

where with

As the number of iterations increases, we can readily see that the bias term in (2.8) decreases while the variance term in (2.8) increases. Therefore, it is interesting to see whether there is a bias-variance trade-off in the proposed bias-correction procedure.

In the following theorem, we provide some sufficient conditions under which we have a bias-variance trade-off in the proposed method.

Theorem 7.

Let Assumption 1 hold and where .

(i) If and for and some , then, as the number of iterations increases, the MSE of will initially decrease to its minimum value and subsequently rise to a stable level. In particular, the minimum of the MSE can be achieved at the -th iteration for some , where

and is the largest integer that does not exceed .

(ii) If for , then, as the number of iterations increases, the MSE of will decrease to a stable level.

Remark 6.

(i) Theorem 7 indicates there exists a bias-variance trade-off in the proposed bias-correction procedure under certain conditions. That is, if the design matrix and the penalty meet the criteria outlined in Theorem 7(i), the MSE of the de-biased estimators can attain a minimum value by balancing the bias and variance terms as the number of iterations , or equivalently, the "model complexity", increases.

(ii) Theorem 7(ii) suggests the possibility of a monotonically decreasing MSE as the number of iterations increases. This phenomenon arises because the increase in the variance term is not comparable to the decrease in the bias term. Consequently, this finding is intriguing as it indicates the potential for a de-biased estimator to achieve an even smaller MSE than classical ridge estimators.

(iii) We highlight that the conditions specified in Theorem 7(ii) can be easily satisfied under certain scenarios. For instance, assuming as detailed in Assumption 3, and or depending on whether is a sparse or dense vector with bounded elements (given that each entry in is of order , it becomes evident that is at least of order , which can exceed . Similarly, the condition in Theorem 7(i) can also be satisfied if is of a smaller rate. We omit the details to save space.

The simulation results presented in Section 3 further corroborate our findings.

From Theorem 2 in Theobald (1974), the MSE of the classical ridge estimator can be smaller than that of the least-squares estimator for certain properly chosen . In our framework, we observe a similar paradigm concerning the number of iterations , as described in the following corollary

Corollary 1.

Under the conditions outlined in Theorem 7, there exists an iteration number such that

suggesting that the proposed de-biased estimators can further minimize the MSEs while also correcting a portion of the bias compared to classical ridge estimators.

3 Monte Carlo Simulations

In this section, we conduct Monte-Carlo experiments to illustrate the proposed procedure. We consider two scenarios where and and study the effect of the bias-correction procedure and the approximation of the asymptotic normalities established in Section 2.5.

Example 1. In this example, we consider the data-generating process in (2) for different settings of with . For each configuration of , we set the seed number in R software as (1234) and first generate an matrix , where its elements are drawn independently from a Uniform distribution . We then perform a singular-value decomposition on and obtain its left and right singular vectors and , then we let . The first elements of are generated from independently, and the remaining elements are from . In each replication, the noise is generated from multivariate normal distribution . We consider the scenarios where , , , and . The choices of are , , , and . 1000 replications are used in each setting throughout the experiments.

In Table 1, we report the estimation errors of the ridge estimators and the de-biased ones. For each configuration of , we define the empirical mean squared errors (MSEs) as

| (41) |

and

| (42) |

where and are the ridge estimators and the de-biased one with iterations in the -th replication, respectively. The standard errors and are estimated via

| (43) |

In other words, we evaluate the estimations of the standard errors by the ridge estimators and the de-biased ones.

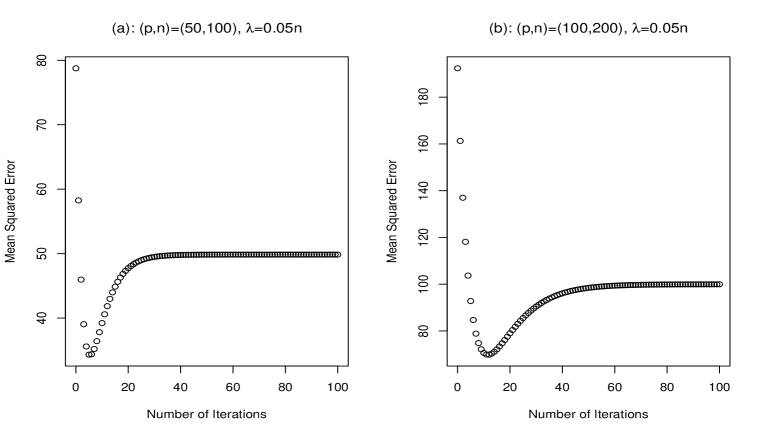

For each setting in Table 1, we see that the MSE first decreases as the number of iterations increases, and then increases as we use more iterations to correction the bias terms. This is understandable because it is in line with the bias-variance trade-off in the machine learning literature. See, for example, Hastie et al. (2009). Specifically, we plot the MSEs for and with in Figure 1, where we can clearly see that the MSEs can achieve a minimum point as we increase the number of iterations, or equivalently, the model complexity, and the MSE will further increase as we try to completely correct the biases. Finally, the MSE becomes stable, which is consistent with our asymptotic theory. Moreover, the standard error estimated using the debiased ridge estimator is closer to the true one (unity), showing the effectiveness of our bias-correction procedure.

| (50,100) | 78.8 | 58.3 | 34.3 | 39.2 | 47.7 | 49.8 | 49.9 | 1.29 | 1.19 |

| (50,400) | 105.3 | 95.9 | 67.9 | 48.4 | 35.6 | 42.9 | 49.3 | 1.11 | 1.06 |

| (100,200) | 192.4 | 161.3 | 92.8 | 70.6 | 79.0 | 98.5 | 100.0 | 1.47 | 1.23 |

| (100,500) | 217.4 | 201.4 | 151.2 | 111.4 | 76.7 | 79.0 | 96.3 | 1.15 | 1.05 |

| (50,100) | 92.6 | 77.6 | 44.8 | 34.5 | 39.2 | 49.1 | 49.8 | 1.34 | 1.19 |

| (50,400) | 110.4 | 105.2 | 87.2 | 70.3 | 49.4 | 35.1 | 42.9 | 1.12 | 1.05 |

| (100,200) | 210.5 | 191.5 | 135.5 | 96.4 | 70.9 | 85.7 | 98.5 | 1.50 | 1.23 |

| (100,500) | 210.4 | 217.2 | 186.5 | 155.8 | 113.8 | 71.6 | 79.0 | 1.16 | 1.03 |

| (50,100) | 104.6 | 98.1 | 76.8 | 58.6 | 40.2 | 36.7 | 46.4 | 1.39 | 1.18 |

| (50,400) | 114.1 | 112.2 | 105.1 | 97.1 | 83.2 | 55.8 | 37.9 | 1.12 | 1.04 |

| (100,200) | 224.3 | 217.1 | 191.0 | 163.9 | 124.3 | 75.4 | 74.1 | 1.52 | 1.20 |

| (100,500) | 231.9 | 228.8 | 217.1 | 203.5 | 179.5 | 127.6 | 85.3 | 1.16 | 1.03 |

| (50,100) | 107.3 | 103.2 | 88.6 | 74.0 | 54.1 | 34.7 | 39.2 | 1.40 | 1.14 |

| (50,400) | 114.9 | 113.7 | 109.3 | 104.1 | 94.6 | 72.3 | 50.3 | 1.12 | 1.05 |

| (100,200) | 227.2 | 222.8 | 206.0 | 187.3 | 156.1 | 99.8 | 71.2 | 1.53 | 1.20 |

| (100,500) | 233.1 | 231.3 | 224.1 | 215.4 | 199.4 | 159.8 | 115.9 | 1.16 | 1.06 |

Furthermore, we study the consistency of the de-biased estimators using our proposed method. For simplicity, we investigate the averaging estimation errors (AEEs) of the ridge estimators and the de-biased ones, which are defined, respectively, as

| (44) |

and

| (45) |

where the ones in the -norm are the empirical versions of the biases. The AEEs are reported in Table 2. From Table 2, we can see a decreasing pattern for each as the number of iterations increases, implying that our de-biased estimators are consistent to the true parameters for sufficiently large .

| (50,100) | 1.24 | 1.01 | 0.50 | 0.20 | 0.04 | 0.03 | 0.03 |

| (50,400) | 1.45 | 1.38 | 1.14 | 0.89 | 0.55 | 0.13 | 0.03 |

| (100,200) | 1.38 | 1.26 | 0.86 | 0.53 | 0.21 | 0.03 | 0.03 |

| (100,500) | 1.47 | 1.42 | 1.21 | 1.00 | 0.67 | 0.21 | 0.04 |

| (50,100) | 1.36 | 1.23 | 0.84 | 0.52 | 0.20 | 0.03 | 0.03 |

| (50,400) | 1.49 | 1.45 | 1.31 | 1.16 | 0.91 | 0.44 | 0.13 |

| (100,200) | 1.45 | 1.38 | 1.14 | 0.89 | 0.55 | 0.13 | 0.03 |

| (100,500) | 1.50 | 1.47 | 1.36 | 1.23 | 1.01 | 0.56 | 0.21 |

| (50,100) | 1.45 | 1.40 | 1.23 | 1.04 | 0.75 | 0.28 | 0.05 |

| (50,400) | 1.51 | 1.50 | 1.45 | 1.39 | 1.28 | 1.00 | 0.66 |

| (100,200) | 1.50 | 1.47 | 1.38 | 1.27 | 1.08 | 0.66 | 0.29 |

| (100,500) | 1.52 | 1.51 | 1.47 | 1.42 | 1.33 | 1.09 | 0.78 |

| (50,100) | 1.47 | 1.44 | 1.33 | 1.20 | 0.98 | 0.54 | 0.20 |

| (50,400) | 1.52 | 1.51 | 1.48 | 1.44 | 1.37 | 1.18 | 0.92 |

| (100,200) | 1.51 | 1.49 | 1.43 | 1.36 | 1.24 | 0.92 | 0.56 |

| (100,500) | 1.53 | 1.52 | 1.49 | 1.47 | 1.41 | 1.25 | 1.02 |

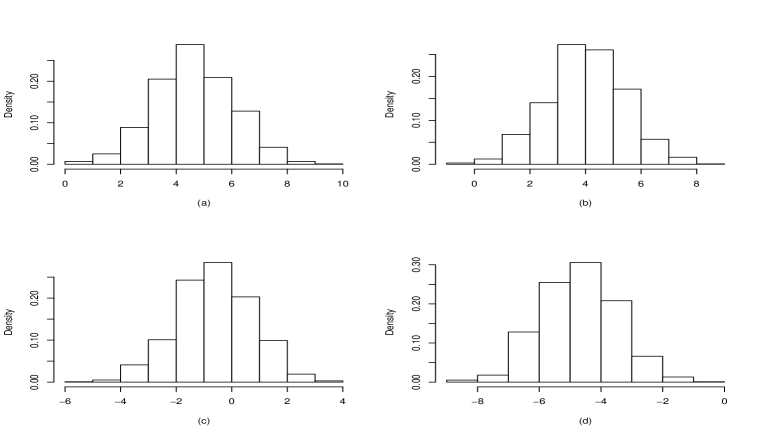

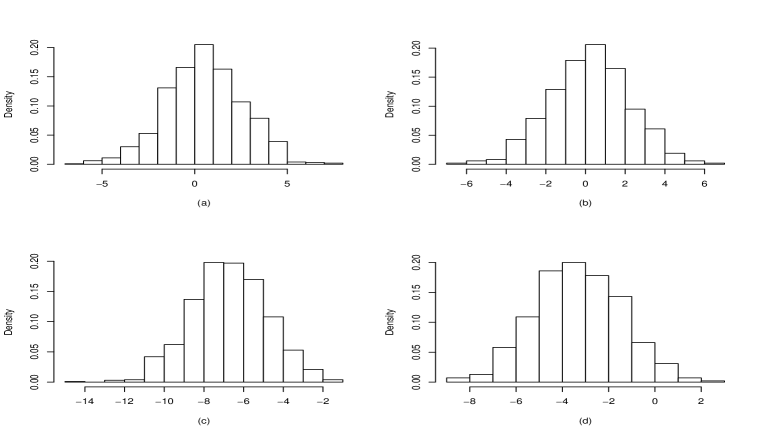

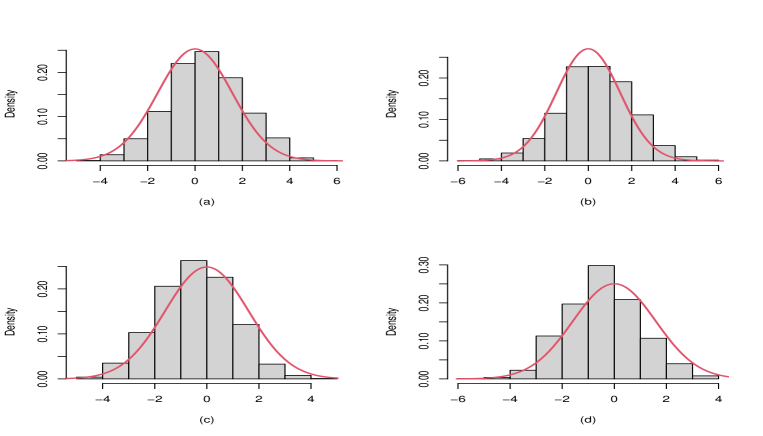

Finally, we investigate the performance of the inference approach based on the de-biased estimators in Theorem 6 for . For simplicity, we only consider the case when and , and we can produce similar results for other settings. Let be the -th standard unit vector of ,

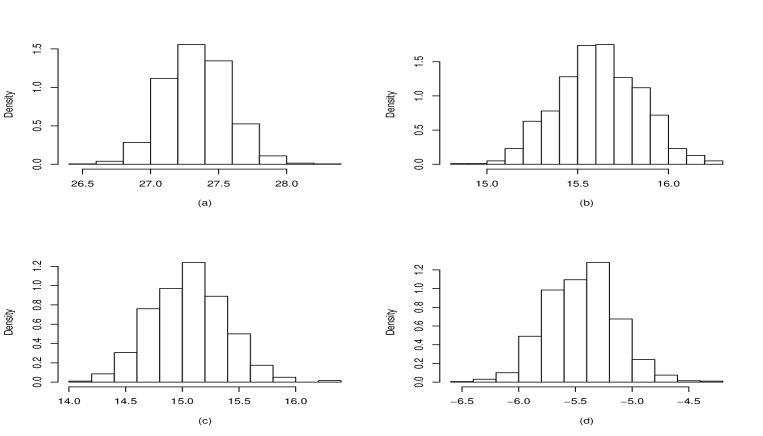

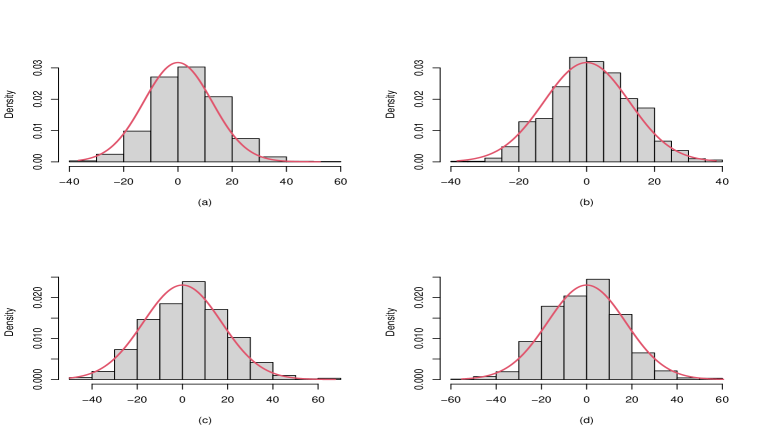

where is an -dimensional vector of zeros. Figure 2 presents the histograms of , , , and obtained from 1000 experiments. From Figure 2, we see that the biases of the empirical means in all the histogram plots are significantly large and diverges from zero, implying that the traditional ridge estimators are not appropriate to make statistical inferences without the information of the bias terms. In contrast, we plot the empirical histograms of the de-biased counterparts in Figure 3 under the same setting. From Figure 3, we see that the finite sample performance is quite satisfactory, and the bias effect of the de-biased estimators is very small. In addition, the curve of the normal distribution in Theorem 6(i) is added to the corresponding histograms, where the standard error term is estimated from the data as that in Remark 5(iv) and Table 1. From these curves, we can further confirm that our inference method is valid for the de-biased ridge estimators, indicating that valid inferences based on the ridge estimators with our bias-correction method can be made in practice.

Example 2. In this example, we consider the scenario where . The seed number used in this example is the same as that in Example 1. Each row of the design matrix is generated independently from multivariate standard normal distribution . For each configuration of , the first elements in are generated from , the th to the th element are from , and the remaining ones are zeros. In other words, we consider the sparse vector with in (18). The dimensions and the sample sizes are , and , and we consider , , and in each replication for any given . For simplicity, we choose in the ridge screening of (20) with iterations. replications are used for each configuration of throughout the experiments.

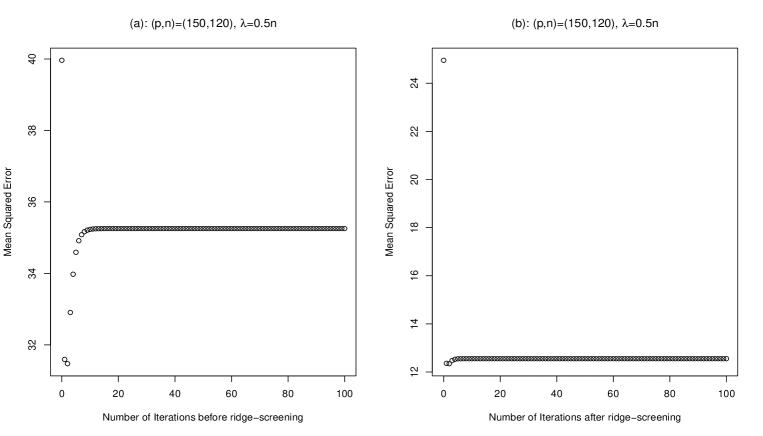

In Table 3, we report the empirical MSEs of the ridge estimators and the de-biased ones before applying the ridge-screening method, and those after the ridge-screening with iterations in the first stage of bias-corrections. Specifically, the upper panel in Table 3 for each presents the MSEs of the ridge estimators and the de-biased ones using 100 iterations without applying the ridge-screening approach. We see that the MSEs of the de-biased estimators become quite stable as we increase the number of iterations, which is consistent with our findings that there is a term that cannot be corrected from the data. In addition, the estimated standard errors are not close to unity, which is the true one in the experiments. In the lower panel of Table 3 for each , we apply the ridge-screening approach with and sort out the largest components of , and then obtain the restricted ridge estimators. We further apply the bias-correction approach and the de-biased estimators are obtained in another iterations. From the lower panels of Table 3 for each , we see that the bias of the de-biased estimators decreases sharply to a relatively stable value for each configuration of , which is understandable since the selected model consists of more parameters than those in the true one. In addition, the estimation errors are significantly smaller than those without the ridge-screening approach, and the estimated standard errors after bias correction are closer to the true one than the methods without using the ridge-screening and the bias-correction approaches. We also note that the estimated standard errors are still larger than the true one (unity) when after the ridge-screening, but they are much closer to the true ones than all the ones produced by the original ridge estimators. In addition, this can be optimized by choosing more appropriate tuning parameter (e.g. or ) such that the estimated standard errors are close to one. Furthermore, we also note that there is also a bias-variance trade-off in the MSEs of the de-biased estimators with or without the ridge-screening. Figure 4 plots the the empirical MSEs of the de-biased ridge estimators for different number of iterations for and , where (a) plots the MSEs of the de-baised ridge estimators before applying the ridge-screening method, and (b) provides the MSEs of the de-biased ridge estimators after the ridge-screening. We can clearly see that there is an optimal number of iteration that minimizes the MSE, which is in line with our asymptotic results in Theorem 7.

We also study the performance of the proposed ridge-screening method in Table 4, where the empirical probability (EP) is calculated by

| (46) |

where is the recovery in the -th experiment and is the cardinality of the set . We can see from Table 4 that our method provides satisfactory performance in variable selections333The comparison results with other variable selection approaches, such as the LASSO, are not provided in this experiment due to the empirical probability of correct recoveries by the proposed RS method being in all settings of Table 4..

| (before ridge-screening) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| (150,120) | 30.64 | 26.70 | 28.64 | 28.73 | 28.73 | 28.73 | 28.73 | 1.66 | 2.14 |

| (150,140) | 14.84 | 10.87 | 11.67 | 11.68 | 11.68 | 11.68 | 11.68 | 2.00 | 2.07 |

| (220,180) | 50.10 | 45.30 | 46.08 | 46.12 | 46.12 | 46.12 | 46.12 | 1.75 | 2.24 |

| (220,200) | 30.90 | 24.09 | 25.02 | 25.04 | 25.04 | 25.04 | 25.04 | 1.82 | 2.03 |

| , (after ridge-screening) | |||||||||

| (150,120) | 11.34 | 5.44 | 5.50 | 5.50 | 5.50 | 5.50 | 5.50 | 1.37 | 0.84 |

| (150,140) | 8.95 | 5.52 | 5.62 | 5.62 | 5.62 | 5.62 | 5.62 | 1.25 | 0.82 |

| (220,180) | 10.89 | 3.51 | 3.48 | 3.48 | 3.48 | 3.48 | 3.48 | 1.58 | 0.91 |

| (220,200) | 8.49 | 3.40 | 3.45 | 3.45 | 3.45 | 3.45 | 3.45 | 1.50 | 0.90 |

| (before ridge-screening) | |||||||||

| (150,120) | 39.96 | 31.59 | 34.59 | 35.23 | 35.25 | 35.25 | 35.25 | 2.48 | 3.46 |

| (150,140) | 23.83 | 15.88 | 18.09 | 18.39 | 18.39 | 18.39 | 18.39 | 2.33 | 3.10 |

| (220,180) | 60.94 | 51.27 | 52.98 | 53.43 | 53.45 | 53.45 | 53.45 | 2.63 | 3.68 |

| (220,200) | 45.13 | 32.61 | 35.01 | 35.45 | 35.46 | 35.46 | 35.46 | 2.86 | 3.62 |

| , (after ridge-screening) | |||||||||

| (150,120) | 24.95 | 12.36 | 12.55 | 12.55 | 12.55 | 12.55 | 12.55 | 2.60 | 1.31 |

| (150,140) | 17.94 | 9.56 | 10.04 | 10.05 | 10.05 | 10.05 | 10.05 | 2.39 | 1.21 |

| (220,180) | 31.66 | 13.39 | 12.73 | 12.73 | 12.73 | 12.73 | 12.73 | 3.01 | 1.44 |

| (220,200) | 24.13 | 9.39 | 9.51 | 9.51 | 9.51 | 9.51 | 9.51 | 3.00 | 1.30 |

| (before ridge-screening) | |||||||||

| (150,120) | 53.47 | 40.79 | 44.04 | 47.60 | 48.03 | 48.04 | 48.04 | 3.89 | 5.72 |

| (150,140) | 36.98 | 24.48 | 29.14 | 31.97 | 32.23 | 32.23 | 32.23 | 3.90 | 5.35 |

| (220,180) | 76.32 | 61.94 | 64.70 | 68.21 | 68.59 | 68.60 | 68.60 | 4.15 | 6.17 |

| (220,200) | 64.95 | 46.37 | 50.70 | 54.71 | 55.11 | 55.11 | 55.11 | 4.63 | 6.53 |

| , (after ridge-screening) | |||||||||

| (150,120) | 44.82 | 27.37 | 26.15 | 26.49 | 26.50 | 26.50 | 26.50 | 4.23 | 2.75 |

| (150,140) | 31.97 | 17.88 | 18.98 | 19.42 | 19.43 | 19.43 | 19.43 | 4.22 | 2.53 |

| (220,180) | 59.55 | 35.56 | 32.39 | 32.55 | 32.56 | 32.56 | 32.56 | 4.80 | 2.86 |

| (220,200) | 51.11 | 26.92 | 25.79 | 26.20 | 26.21 | 26.21 | 26.21 | 5.14 | 2.93 |

| EP | (150,200) | (150,140) | (220,180) | (220,200) |

| 100% | 100% | 100% | 100% | |

| EP | (150,200) | (150,140) | (220,180) | (220,200) |

| 100% | 100% | 100% | 100% | |

| EP | (150,200) | (150,140) | (220,180) | (220,200) |

| 100% | 100% | 100% | 100% | |

Similar to the experiments in Example 1, we present the empirical averaging estimation errors (AEEs) in Table 5. The settings of , , , , and are the same as those in Table 3. From Table 5, we see that the averaging estimation errors before ridge-screening are also quite stable as we increase the number of iterations which is similar to the findings in Table 3. After we apply the ridge-screening approach to the de-biased estimators in the upper panel of Table 5 with for each , the bias terms (in the lower panel for each ) decrease substantially from the ones before, and they also decrease to stable values as we increase the number of iterations in the second-stage bias correction. Notably, the bias terms are all significantly smaller than those in the upper panel without the ridge-screening procedure. This is in agreement with our theoretical results in Theorem 5 and Theorem 7.

| (before ridge-screening) | |||||||

|---|---|---|---|---|---|---|---|

| (150,120) | 0.44 | 0.41 | 0.42 | 0.42 | 0.42 | 0.42 | 0.42 |

| (150,140) | 0.30 | 0.24 | 0.25 | 0.25 | 0.25 | 0.25 | 0.25 |

| (220,180) | 0.47 | 0.44 | 0.44 | 0.44 | 0.44 | 0.44 | 0.44 |

| (220,200) | 0.37 | 0.32 | 0.32 | 0.32 | 0.32 | 0.32 | 0.32 |

| , (after ridge-screening) | |||||||

| (150,120) | 0.26 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 | 0.17 |

| (150,140) | 0.22 | 0.16 | 0.16 | 0.16 | 0.16 | 0.16 | 0.16 |

| (220,180) | 0.21 | 0.11 | 0.11 | 0.11 | 0.11 | 0.11 | 0.11 |

| (220,200) | 0.19 | 0.11 | 0.11 | 0.11 | 0.11 | 0.11 | 0.11 |

| (before ridge-screening) | |||||||

| (150,120) | 0.51 | 0.45 | 0.47 | 0.47 | 0.47 | 0.47 | 0.47 |

| (150,140) | 0.39 | 0.31 | 0.33 | 0.33 | 0.33 | 0.33 | 0.33 |

| (220,180) | 0.52 | 0.48 | 0.48 | 0.48 | 0.48 | 0.48 | 0.48 |

| (220,200) | 0.45 | 0.38 | 0.39 | 0.39 | 0.39 | 0.39 | 0.39 |

| , (after ridge-screening) | |||||||

| (150,120) | 0.40 | 0.27 | 0.27 | 0.27 | 0.27 | 0.27 | 0.27 |

| (150,140) | 0.34 | 0.24 | 0.24 | 0.25 | 0.25 | 0.25 | 0.25 |

| (220,180) | 0.37 | 0.24 | 0.23 | 0.23 | 0.23 | 0.23 | 0.23 |

| (220,200) | 0.33 | 0.20 | 0.20 | 0.20 | 0.20 | 0.20 | 0.20 |

| (before ridge-screening) | |||||||

| (150,120) | 0.60 | 0.52 | 0.53 | 0.56 | 0.56 | 0.56 | 0.56 |

| (150,140) | 0.50 | 0.40 | 0.43 | 0.45 | 0.45 | 0.45 | 0.45 |

| (220,180) | 0.59 | 0.53 | 0.54 | 0.55 | 0.55 | 0.55 | 0.55 |

| (220,200) | 0.54 | 0.46 | 0.47 | 0.49 | 0.49 | 0.49 | 0.49 |

| , (after ridge-screening) | |||||||

| (150,120) | 0.54 | 0.42 | 0.41 | 0.41 | 0.41 | 0.41 | 0.41 |

| (150,140) | 0.46 | 0.34 | 0.35 | 0.35 | 0.35 | 0.35 | 0.35 |

| (220,180) | 0.52 | 0.40 | 0.38 | 0.38 | 0.38 | 0.38 | 0.38 |

| (220,200) | 0.48 | 0.34 | 0.33 | 0.33 | 0.33 | 0.33 | 0.33 |

Finally, we study the performance of the inference method in Theorem 6(ii). We only consider the case when , , and , and we can produce similar results for other settings. Define

We plot the empirical histograms of , , , and in Figure 5, from which it is observed that most of the estimators are not centered around zero. Subsequently, we apply the bias-correction procedure to the original ridge estimators, and the empirical histograms of the bias-corrected estimators are presented in Figure 6 as compared to Figure 5. From Figure 6, it can be seen that while some estimators become more centered around zero (e.g., (a) and (b)) due to the bias-correction procedure, the validity of inference without ridge-screening cannot be assured, as (c) and (d) still exhibit significant biases.

Furthermore, we apply the ridge-screening approach to the de-biased estimators depicted in Figure 6, subsequently obtaining restricted ridge estimators along with their de-biased counterparts. Figure 7 showcases the empirical histograms of: (a) ; (b) ; (c) ; and (d) , where is a -dimensional vector with as its sub-vector and the remaining elements are set to zero. Similar to the curves in Figure 3, the density curve in Figure 7 is plotted based on the limiting distribution specified in Theorem 6(ii). From Figure 7, it is evident that the de-biased restricted ridge estimators predominantly cluster around zero. The density curves for the corresponding estimators are quite satisfactory, suggesting the validity of the proposed inference approach.

4 Empirical Application

In this section, we apply the proposed method to forecast the U.S. macroeconomic series and study the out-of-sample prediction intervals using ridge regression. We consider the widely used macroeconomic variables studied by Stock and Watson (2002a), McCracken and Ng (2016), Giannone et al. (2021), and Gao and Tsay (2022, 2023), among many others. The data are obtained from the FRED-MD data base which are maintained by St. Louis Fed. See https://research.stlouisfed.org/econ/mccracken/fred-databases/. There are 127 variables in the online data set, and we remove 4 of them because of missing values therein. Consequently, we consider the 123 macro variables spanning from July 1962 to December 2019 as all the series have no missing values during this period, which is the same as the setting in Gao and Tsay (2023). The detailed variables and transformation codes to ensure the stationarity of each macro variable are provided in Table IA.I of Gao and Tsay (2023). The sample size is .

Similar to Stock and Watson (2002b), Bai and Ng (2006), and Cheng and Hansen (2015), we adopt the following factor-augmented regression model:

| (47) |

where consists of 122 macroeconomic variables, is the remaining target one, and is an -dimensional latent factor process which can be estimated by applying Principal Component Analysis (PCA) to . We set and , and apply the ridge regression to estimate the parameters and for and with estimated factors. Hence, the number of covariates in the ridge regression is . We focus on the prediction of the consumer price index: all (CPI-All), which is an important index related to the inflation. See also Stock and Watson (2002a) and Gao and Tsay (2022) for similar studies.

First, we set which contains 16 candidates for the penalty parameter. We split the sample into two subsamples, where the first one consists of the first of the data for modeling and the second subsample of the remaining of the data for out-of-sample prediction. We adopt the rolling-window scheme as that in Gao and Tsay (2023), that is, we train the factors and the forecasting coefficients using the first subsample to predict the next target data point. Then we repeat the above procedure after moving the next available observation of predictors and target CPI-All variable from the second subsample to the first one to obtain the next prediction. This rolling-window scheme is terminated when there is no more observation to compute the forecasting error. We choose the optimal penalty in the ridge estimator such that the out-of-sample mean-squared forecast errors (MSFEs) achieve a minimum value. Thus, this setting is in line with the advocated models combining regularized estimation and data-driven selection of regularization parameters in Abadie and Kasy (2019). In this experiment, we find that the optimal penalty for and for .

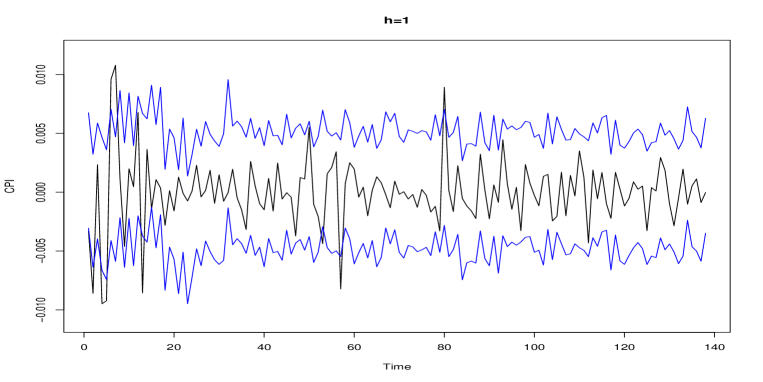

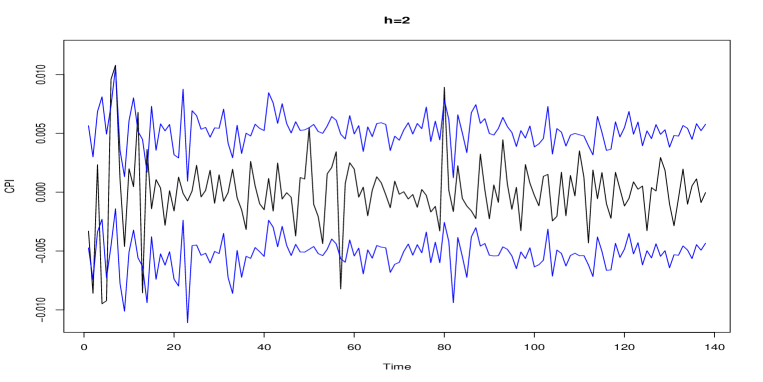

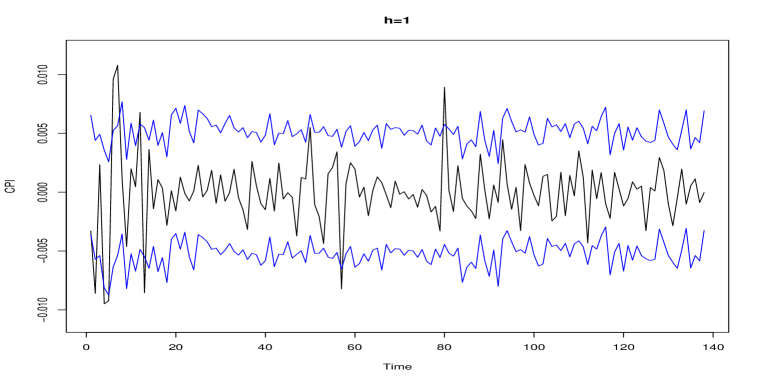

Next, for each configuration of and , we execute Algorithm 1. We observe that the bias-correction procedure terminates within 3 to 5 iterations when setting in equation (24). For simplicity, we opt for in the bias-correction, a choice deemed sufficiently large. Following the guidelines provided in Section 2.7, we compute pointwise prediction intervals for the data points in the testing set. The standard errors for each prediction are determined using the method described in Remark 5(iv). We present the pointwise prediction intervals for both 1-step ahead and 2-step ahead forecasts in Figure 8 and Figure 9, respectively. It is evident that the majority of the true observations fall within these prediction intervals. Additionally, we evaluate the coverage rates of the prediction intervals across the 138 points in the testing set. We find a consistent coverage rate of for both the 1-step and 2-step ahead forecasts, indicating that the prediction intervals perform effectively in this empirical example.

Finally, we investigate the effectiveness of the ridge-screening (RS) approach in out-of-sample predictions. We take the 1-step ahead prediction as an example. For each , which is the same as our previous candidate set, we adopt and vary from to in (20), that is, we select the largest to variables based on their magnitudes from the set and compute their corresponding out-of-sample forecast errors. By minimizing the out-of-sample MSFEs, we determined that the optimal parameters are . This implies that the submodel, consisting of covariates corresponding to the largest 31 elements in , yields the smallest out-of-sample MSFEs. Consequently, we chose for the subsequent bias-correction procedure in the restricted ridge estimators, conducting it with iterations. Figure 10 displays the out-of-sample prediction intervals based on the selected submodel and the corresponding restricted ridge estimators for . Interestingly, we observe that some observations not covered by the prediction intervals in Figure 8 are encompassed by the new intervals in Figure 10. The coverage rate of these prediction intervals stands at , surpassing the achieved by the previous approach without ridge-screening. This suggests that the ridge-screening method enhances the performance of the prediction intervals.

5 Conclusion

A fundamental question in ridge regression revolves around the possibility of correcting the bias term using available data, alongside ensuring the validity of statistical inferences without affecting the predictive performance of the original ridge estimator. This paper tackles these long-standing challenges by introducing a straightforward and readily implementable iterative procedure, along with a ridge-screening method. In cases where the dimension is smaller than the sample size , our procedure effectively corrects the bias term under very mild assumptions. However, when and the projection matrix becomes singular, we propose a ridge-screening approach to eliminate coefficients that are relatively insignificant compared to others. We then specifically focus on the restricted model, which retains a sufficient number of parameters to encapsulate most of the information regarding the response vector. Our bias-correction procedure can be further applied to the restricted model, enabling the correction of the bias. Moreover, the ridge-screening method offers a novel approach to variable selection, which is of independent interest beyond bias correction. We derive the limiting distributions of the de-biased estimators, facilitating the making of statistical inferences. Simulated and real data examples are used to corroborate the effectiveness and validity of our proposed methodology. The proposed inference solution for ridge regression serves as an illustrative example addressing the inference challenges of regularized machine learning methods outlined in Section 2.8 of Athey and Imbens (2019) without adversely affecting the predictive performance.

References

- (1)

- Abadie and Kasy (2019) Abadie, A., and M. Kasy (2019): “Choosing among regularized estimators in empirical economics: The risk of machine learning,” Review of Economics and Statistics, 101(5), 743–762.

- Athey and Imbens (2019) Athey, S., and G. W. Imbens (2019): “Machine learning methods that economists should know about,” Annual Review of Economics, 11, 685–725.

- Bai and Ng (2006) Bai, J., and S. Ng (2006): “Confidence intervals for diffusion index forecasts and inference with factor-augmented regressions,” Econometrica, 74(4), 1133–1150.

- Bai and Yin (1993) Bai, Z., and Y. Yin (1993): “Limit of the Smallest Eigenvalue of a Large Dimensional Sample Covariance,” Annals of Probability, 21(3), 1275–1294.

- Bühlmann (2013) Bühlmann, P. (2013): “Statistical significance in high-dimensional linear models,” Bernoulli, 19(4), 1212–1242.

- Cheng and Hansen (2015) Cheng, X., and B. E. Hansen (2015): “Forecasting with factor-augmented regression: A frequentist model averaging approach,” Journal of Econometrics, 186(2), 280–293.

- Dobriban and Wager (2018) Dobriban, E., and S. Wager (2018): “High-dimensional asymptotics of prediction: Ridge regression and classification,” The Annals of Statistics, 46(1), 247–279.

- Fan and Lv (2008) Fan, J., and J. Lv (2008): “Sure independence screening for ultrahigh dimensional feature space,” Journal of the Royal Statistical Society Series B: Statistical Methodology (with discussion), 70(5), 849–911.

- Gao and Tsay (2022) Gao, Z., and R. S. Tsay (2022): “Modeling high-dimensional time series: A factor model with dynamically dependent factors and diverging eigenvalues,” Journal of the American Statistical Association, 117(539), 1398–1414.

- Gao and Tsay (2023) (2023): “Supervised Dynamic PCA: Linear Dynamic Forecasting with Many Predictors,” arXiv preprint arXiv:2307.07689.

- Giannone et al. (2021) Giannone, D., M. Lenza, and G. E. Primiceri (2021): “Economic predictions with big data: The illusion of sparsity,” Econometrica, 89(5), 2409–2437.

- Hall and Heyde (2014) Hall, P., and C. C. Heyde (2014): Martingale limit theory and its application. Academic press.

- Hansen (2022a) Hansen, B. E. (2022a): Econometrics. Princeton University Press.

- Hansen (2022b) (2022b): “A modern Gauss–Markov theorem,” Econometrica, 90(3), 1283–1294.

- Hastie (2020) Hastie, T. (2020): “Ridge regularization: An essential concept in data science,” Technometrics, 62(4), 426–433.

- Hastie et al. (2009) Hastie, T., R. Tibshirani, and J. H. Friedman (2009): The elements of statistical learning: data mining, inference, and prediction, vol. 2. Springer.

- Hoerl (1959) Hoerl, A. E. (1959): “Optimum solution of many variables equations,” Chemical Engineering Progress, 55(11), 69–78.

- Hoerl and Kennard (1970a) Hoerl, A. E., and R. W. Kennard (1970a): “Ridge regression: applications to nonorthogonal problems,” Technometrics, pp. 69–82.

- Hoerl and Kennard (1970b) (1970b): “Ridge regression: Biased estimation for nonorthogonal problems,” Technometrics, 12, 55–67.

- Hoerl (1985) Hoerl, R. W. (1985): “Ridge analysis 25 years later,” The American Statistician, 39(3), 186–192.

- Leonard et al. (2023) Leonard, M. K., L. Gwilliams, K. K. Sellers, J. E. Chung, D. Xu, G. Mischler, N. Mesgarani, M. Welkenhuysen, B. Dutta, and E. F. Chang (2023): “Large-scale single-neuron speech sound encoding across the depth of human cortex,” Nature, pp. 1–10.

- McCracken and Ng (2016) McCracken, M. W., and S. Ng (2016): “FRED-MD: A monthly database for macroeconomic research,” Journal of Business & Economic Statistics, 34(4), 574–589.

- Montgomery et al. (2012) Montgomery, D. C., E. A. Peck, and G. G. Vining (2012): Introduction to linear regression analysis (5th ed.). John Wiley & Sons.

- Otwinowski and Plotkin (2014) Otwinowski, J., and J. B. Plotkin (2014): “Inferring fitness landscapes by regression produces biased estimates of epistasis,” Proceedings of the National Academy of Sciences, 111(22), E2301–E2309.

- Shao and Deng (2012) Shao, J., and X. Deng (2012): “Estimation in high-dimensional linear models with deterministic design matrices,” The Annals of Statistics, 40(2), 812–831.

- Stock and Watson (2002a) Stock, J. H., and M. Watson (2002a): “Macroeconomic Forecasting Using Diffusion Indexes,” Journal of Business & Economic Statistics, 20, 147–162.

- Stock and Watson (2002b) Stock, J. H., and M. W. Watson (2002b): “Forecasting Using Principal Components From a Large Number of Predictors,” Journal of the American Statistical Association, 97(460), 1167–1179.

- Theobald (1974) Theobald, C. M. (1974): “Generalizations of mean square error applied to ridge regression,” Journal of the Royal Statistical Society Series B: Statistical Methodology, 36(1), 103–106.

- Tikhonov (1943) Tikhonov, A. N. (1943): “On the stability of inverse problems,” Doklady Akademii Nauk SSSR, 39(5), 195–198.

- van Wieringen (2023) van Wieringen, W. N. (2023): “Lecture notes on ridge regression,” arXiv preprint arXiv:1509.09169, v8.

- Vapnik (2013) Vapnik, V. N. (2013): The nature of statistical learning theory. Springer science & business media.

- Wang and Leng (2016) Wang, X., and C. Leng (2016): “High dimensional ordinary least squares projection for screening variables,” Journal of the Royal Statistical Society Series B: Statistical Methodology, 78(3), 589–611.

- Zahrt et al. (2019) Zahrt, A. F., J. J. Henle, B. T. Rose, Y. Wang, W. T. Darrow, and S. E. Denmark (2019): “Prediction of higher-selectivity catalysts by computer-driven workflow and machine learning,” Science, 363(6424), eaau5631.

- Zhang and Politis (2022) Zhang, Y., and D. N. Politis (2022): “Ridge regression revisited: Debiasing, thresholding and bootstrap,” The Annals of Statistics, 50(3), 1401–1422.

Online Appendix: Proofs of the Theorems

We will use or to denote a generic constant the value of which may change at different places.

Proof of Theorem 1. To see the bias of the ridge estimator, it follows from (2) that

| (A.1) |

Conditioning on , by the assumption that , it follows immediately that

This completes the proof.

Proof of Theorem 2. By (A.1) and an elementary argument, can be written as

| (A.2) |

Then, it follows that

When and is invertible, by Assumption 1, the singular-value decomposition of is

Then, it is not hard to see that

and

Note that, for , each diagonal element in is

at a rate of exponential decay. Therefore, for any given configuration of with , if the number of iteration satisfies with , we can show that

As a matter of fact, the aforementioned result applies to any given and fixed . Furthermore, when considering the scenario where both and tend towards infinity in an asymptotic framework, it is not hard to see that the above convergence also holds under the condition that in relation to the sample size within an asymptotic setting. This completes the proof.

Proof of Theorem 3. Note that

When , by Assumption 2, the singular-value decomposition of is

Then,

| (A.3) |

By a similar argument as that in the proof of Theorem 2, the first term in (Online Appendix: Proofs of the Theorems) vanishes as . Hence,

If we further allow , under a similar setting in the proof of Theorem 2 above, we can show that

which is discussed in Remark 3(iii). This completes the proof.

Proof of Theorem 4. We prove it by contradiction. Suppose is singular and there exists a transformation matrix such that

| (A.4) |

In other words, the remaining bias term in Theorem 3 can be corrected by . (A.4) implies that

| (A.5) |

Since a -dimensional space can be spanned by the columns of , there exist vectors and such that

We only talk about the case when and since either or will lead the bias term to be zero, implying that we do not need to correct it. We plug it into (A.5) and obtain

| (A.6) |