A Revisit of the Optimal Excess-of-Loss Contract

Abstract

It is well-known that Excess-of-Loss reinsurance has more marketability than Stop-Loss reinsurance, though Stop-Loss reinsurance is the most prominent setting discussed in the optimal (re)insurance design literature. We point out that optimal reinsurance policy under Stop-Loss leads to a zero insolvency probability, which motivates our paper. We provide a remedy to this peculiar property of the optimal Stop-Loss reinsurance contract by investigating the optimal Excess-of-Loss reinsurance contract instead. We also provide estimators for the optimal Excess-of-Loss and Stop-Loss contracts and investigate their statistical properties under many premium principle assumptions and various risk preferences, which according to our knowledge, have never been investigated in the literature. Simulated data and real-life data are used to illustrate our main theoretical findings.

Keywords and phrases: Risk analysis, Optimal Insurance, Nonparametric Estimation.

1 Introduction

1.1 Literature Review

Risk transfer is an effective risk management exercise and consists of transferring liabilities from one or multiple risk holders (known as insurance buyer(s)) to another or multiple insurance carriers (known as insurance seller(s)). Finding the optimal contact between (amongst) two (or more than two) parties has received a huge amount of attention in the literature of actuarial science. A simple Google Scholar search on April 23, 2024 with the keywords “optimal insurance” and “risk transfer” resulted in 2,830,000 and 5,810,000, respectively research outputs. This is not surprising since the optimality of such risk management exercise goes beyond understanding insurance liabilities. This paper aims to contribute to the problem of optimal insurance contract of insurance liabilities, which has a very specific trait that is not shared with other sector-specific liabilities (e.g., financial liabilities) in the sense that the insurance liabilities do not have a liquid market so that their value is market-based valuation. Cost-of-Capital (CoC) approach is a practical methodology for evaluating insurance liabilities, which are based on the cost of meeting the local capital requirements to hold such liabilities in that territory. In other words, CoC is a regulatory-based methodology that is used within the insurance sector.

The optimal risk transfer problem is often understood in the optimal insurance literature as how an insurer and reinsurer would share the aggregate liability between the two insurance players so that the risk position of the insurer is optimized; the optimization from the reinsurer’s point of view is also possible. One may view the problem from both the insurer’s and reinsurer’s point of view, a case in which the analysis becomes a Pareto optimal insurance contract problem that is a long-standing strand of research established in economic theory with ramifications in insurance and risk literature, but also in the wider operations research field; an insurance perspective could be found in Ruschendorf (2013) and references therein. Other equilibrium concepts are possible; for example, Boonen and Ghossoub (2023) investigates the Bowley equilibrium with risk sharing and optimal reinsurance formulations, and focus on the common traits of Bowley optimality and Pareto efficiency under fairly general preferences. Bespoke conditions could be imposed on the optimal (re)insurance contract besides the usual absence of moral hazard; one interesting setting is the so called Vajda condition that is discussed in Boonen and Jiang (2022).

Depending on the risk preferences, the optimal reinsurance literature is quite rich; e.g., Cai et al. (2008) and Cai and Tan (2007) consider Value-at-Risk (VaR) and Expected Shortfall (ES) buyer’s preferences, while quantile risk and expectile preferences are investigated in Asimit, Badescu and Verdonck (2013), and Cai and Weng (2016), respectively; Balbás, Balbás and Heras (2009) investigates some general risk preferences. The optimal contract from the buyer’s point of view in the presence of the seller’s counterparty default risk is discussed in Chen (2024), Chi and Tan (2021), Cai, Lemieux, and Liu (2014), Asimit, Badescu and Cheung (2013), and Bernard and Ludkovski (2012). Regulatory considerations are discussed for example in Asimit, Chi, and Hu (2015) and Bernard and Tian (2009). Robust formulations are investigated for example in Asimit, Hu and Xie (2019), Asimit et al. (2017), Balbás, Balbás and Heras (2011), Boonen and Jiang (2024) and Gollier (2014), while Cai, Li and Mao (2023) provides a theoretical perspective to robust decision-making when preferences are ordered by distorsion risk measures which are considered in our paper and many other papers in the optimal (re)insurance literature. Non-standard settings are considered in the literature; e.g., Bäuerle and Glauner (2018) investigates the optimal transfer in an insurance network from an economic point of view, while Asimit et al. (2016) studies Solvency II capital efficiency through risk transfers within an insurance group.

The optimal insurance problem under expected utility settings is often defined without making any assumption regarding the seller’s premium principle. When risk preferences are ordered by risk measures, then premium principle assumptions are required. Kaluszka (2001) studies the mean-variance premium principle, Asimit, Badescu and Verdonck (2013) investigate quantile risk premium principles, and Chi and Tan (2013) consider general premium principles, though many other papers rely on certain premium principle assumptions that are specific to the buyer’s risk preferences.

1.2 Background and Problem Definition

Throughout this paper, the insurance field is represented by , an atomless probability space, endowed with , the set of all non-negative real-valued random variables on this probability space. Let , , be the set of random variables with finite moment, and be the set of bounded random variables. A risk measure is a function that maps an element of to a (extended) real number, i.e. . We recall below some properties for a generic risk measure and generic random variable – with cumulative distribution function (cdf) , survival distribution function , and generalized left-continuous inverse – representing the future loss of a financial asset or insurance liability.

These properties are well-known in the literature and an extensive introduction to risk measures can be found in Föllmer and Schied (2011). Two well-known risk measures are Value-at-Risk (VaR) and Expected Shortfall (ES), defined as

where and is the risk level. It is evident that the two risk measures are homogeneous of order and translation invariant, and ES is convex.

We are now ready to provide the mathematical formulation of the problem of interest. Suppose that an insurer has insured a large number of policies with independent and identically distributed non-negative losses for with cdf .

We consider now that the reinsurance premium is calculated by the expected value principle. Thus, the total cost for this portfolio of policies after buying Excess-of-Loss (EoL) reinsurance becomes

| (1) |

where is the loading factor. A practical question is to find the optimal retention for by minimizing the buyer’s risk when its perception of risk is modeled by some given risk measures such as VaR and ES. To better appreciate our study, we first point out an issue with the Stop-loss (SL) optimal reinsurance (SL is EoL with ) in Cai and Tan (2007), where the total cost is studied; that is, the optimal retention is found via minimizing or , which leads to the following optimal retention

| (2) |

Now, if then

implying no high risk to the buyer, which is mathematically explained by the truncated buyer’s liability . The same issue remains if one replaces by , i.e., considering the SL for the total loss instead of one loss in Cai and Tan (2007). However, when the number of policies is large enough, will not have such a truncation issue to cause a severely distorted risk level for optimal retention, and thus, the optimal EoL (with ) retention would not share the same counter-intuitive property as SL (when ). Specifically, under the EoL approach, becomes , the “correct” level, as long as is sufficiently large. Numerical and theoretical justifications of this assertion are leveraged to Section 1 of the supplementary material. Furthermore, the SL optimal retention in (2) is not an explicit function of the risk level . This is also counter-intuitive as the SL optimal retention may remain constant while , which implies the insurance company’s level of risk aversion, increases. Conversely, we will show in the real data analysis (see Section 5) that the EoL optimal retention decreases as increases.

To derive the optimal retention, it is necessary to know the distribution function of , which is well-known to be challenging. This motivates us to define approximately optimal retention by using a normal distribution to approximate the distribution of when is large enough.

Before outlining our main contributions, we would like to differentiate the EoL and SL contracts, which are compared in this paper. Note that EoL has more marketability than SL as the latter is prohibitively expensive to buyers since the deductible is applied to the annual aggregate loss and not to the individual claims (as for EoL). There are other negative traits of SL that are not shared with EoL. For example, the loss development of an insurance claim is the process of a claim from reporting until the claim is fully settled, which takes a significant amount of time for many lines of business such as personal accident insurance, medical malpractice insurance, workers compensation, liability claims, etc.; the lag is even larger for long-tail lines of coverage where arbitrage or court proceedings are more likely to occur. Long lags are big impediments to activate SL contracts since the deductible is applied to the aggregate loss, which is known when all claims from that year are fully settled and that may require many years; this is not the case to EoL where each claim is shared between the buyer and seller.

The main contributions of this paper are twofold. First, we point out that optimal reinsurance policy under SL – one of the most prominent settings discussed in the literature – leads to zero insolvency probability for VaR-based regulatory environments as is the case for EU and UK insurance companies where capital requirements are designed on the 1/200 event basis over a one-year time horizon. This peculiar property of the optimal SL reinsurance contract is the main motivation of our paper and we show that a remedy is possible if one investigates the optimal EoL reinsurance contract instead. Second, we provide estimators to the optimal EoL/SL deductible and investigate their statistical properties under many premium principle assumptions and various risk preferences, which, according to our knowledge, have never been investigated in the literature.

The paper is organized as follows: EoL risk model is considered under the risk measure in Section 2 for various premium principles, which are further generalized in Section 3 when the risk preferences are ordered by distortion risk measures. Some simulation studies are provided in Section 4, while real data analysis is employed in Section 5.

2 Approximately optimal retention for VaR

In this section, we consider the total cost of under the risk measure. Later, we will generalize the result to distortion risk measures in Section 3. Because VaR is translation invariant, we have

| (3) |

Define

For large , it follows from the Central Limit Theorem that

| (4) |

where is the cdf of a standard normal random variable. Therefore, instead of minimizing to obtain the optimal retention , we propose to ignore the term in (4) to approximate the right hand side of (3), i.e., minimizing

| (5) |

whose solution is called an approximately optimal retention.

The structure of this section is as follows: Section 2.1 identifies the optimal retention by assuming a constant loading factor under the expected value principle, while a decreasing loading factor is considered in Section 2.2; the standard deviation and Sharpe ratio principles are explored in Sections 2.3 and 2.4 by assuming a decreasing loading factor.

2.1 Constant Loading Factor

We now solve (5) with a constant loading factor . In this case, the optimal retention turns out to be a solution to

| (6) |

The next result stated as Theorem 1 shows that (6) admits a unique solution under some very mild regularity conditions. Recall that we allow in Theorem 1, which means that the event of having no claim is not a null set.

Theorem 1.

Assume , has the support (i.e., ) or , and is continuous on . When the support is , we further assume , which is always true when is large enough. Then, there exists a unique approximately optimal retention such that

Proof.

Note that , , and , and in turn,

Hence, solving for is equivalent to solving for . That is, we only need to show that there is a unique solution for .

Since and for all , and

we conclude that is negative, zero, and positive for , , and , respectively, where happens and only happens on , which is ensured by the conditions that the right endpoint of is infinity, is continuous on , and . That is,

| (8) |

Note that

Thus, and . The latter, (2.1) and (8), and the fact that conclude that has a unique solution on . The proof is now complete. ∎

2.2 Decreasing Loading Factor

Note that diverges to infinity as , which is not surprising since a constant for any implies that the seller does not include the diversification effect in its premium calculation, case in which the seller would not be incentivized to participate in such reinsurance contract. Therefore, it would be more practical to adjust/reduce the loading factor as gets large so that the reinsurance premium becomes more realistic. To estimate and study its asymptotic properties, we consider instead a bounded approximated optimal retention by assuming such that

| (9) |

where may depend on the retention . In this case, is the unique solution to and converges to the unique solution to

To estimate this solution nonparametrically, we solve the following equation

| (10) |

where

| (11) |

Let denote this solution, which is an estimator for . Let denote the covariance matrix of , where , and define

| (12) |

which estimate the first-order derivatives, and , respectively. The asymptotic properties of are given in Theorem 2.

Proof.

For simplicity, the proof uses and for and , respectively. Then

| (13) |

when

| (14) |

It follows from (13) that

implying that

i.e.,

where

Hence,

which implies our main result since are consistent estimators of , respectively. The proof is now complete. ∎

2.3 Standard Deviation Premium Principle

We extend the analysis in Section 2.2 by assuming a decreasing loading factor and the standard deviation principle. Specifically, a particular choice of is assumed in (5) as

| (15) |

which depends on both and and satisfies (9), where

Hence, the total cost for the insurer becomes

and the optimal retention should minimize

Once again, we seek for that minimizes (16) below as we ignore the terms:

| (16) |

The existence of the approximately optimal retention is shown in Theorem 3 below.

Theorem 3.

Assume has the support (i.e., ) or , is continuous on , and

| (17) |

If , we further assume that

| (18) |

Then, there exists at least one solution of and an approximately optimal retention is its smallest solution, which is a local minimum of .

Proof.

Because

and

| (19) |

it follows from (18) in Theorem 3 that

| (20) |

By (17), we have

| (21) |

implying that

| (22) |

Hence, it follows from (20) and (22) that there exists at least one solution of for , and let be the smallest solution. Then, there exists such that for , for , and , implying that is a local minimum of for . The proof is now complete. ∎

To estimate the optimal retention nonparametrically, we minimize the following function for :

| (23) |

where and are given by (11),

| (24) |

Denote and as the minimizers of in (16) and in (23), respectively. Put , and let be the covariance matrix of . Define

| (25) |

to estimate and on top of and which are defined in (12). We further denote as the empirical survival function of and as any consistent estimator of the density function for , e.g., a kernel density estimation. The asymptotic properties of the approximately optimal retention are provided in Theorem 4.

Theorem 4.

Proof.

For notational convenience, we write and for and , respectively. Then

| (26) |

when . Expansion of yields

| (27) | ||||

where

We also have

The latter together with (26) and (27) imply that

where and

Hence, the theorem follows as , and are consistent estimators of , and , respectively. The proof is now complete. ∎

2.4 Sharpe Ratio Premium Principle

We now recast the results in Section 2.3 by assuming the Sharpe Ratio premium principle

| (28) |

leading to the total cost for the insurer as

In this case, the loading factor becomes

which is decreasing in and satisfies (9). As before, the optimal retention minimizes

and we seek for that minimizes (29) below by ignoring the terms:

| (29) |

The existence of the approximately optimal retention is shown in Theorem 5 below.

Theorem 5.

Assume has the support (i.e., ) or , is continuous on , and

| (30) |

If , we further assume that

| (31) |

Then, there exists at least one solution of and an approximately optimal retention is its smallest solution, which is a local minimum of .

Proof.

To estimate the optimal retention nonparametrically, we minimize the following function for :

| (34) |

Denote and as the minimizers of in (29) and in (34), respectively. The asymptotic properties of the approximately optimal retention are provided in Theorem 6.

Theorem 6.

Proof.

Since the proof is similar to that for Theorem 4, we omit the details. ∎

Remark 1.

Another choice of the reinsurance premium beyond the Sharpe Ratio may also seem natural. That is, we could use the Standard Deviation to determine the reinsurance premium as follows:

However, the resulting objective function has a positive derivative at , which often leads to a trivial approximately optimal retention being either zero or infinity. Therefore, we do not discuss this setting in the paper as the optimal retention is trivial.

3 Generalization to distortion risk measures

We show now that our results in Section 2 can be naturally extended to optimal reinsurance problems under general distortion risk measures. A large class of quantile-based risk measures is the distorted class, for which Definition 1 is needed.

Definition 1.

A distortion function is a non-decreasing function such that and .

Yarri’s dual theory of choice under risk – e.g., see Yaari (1987) – postulates that the risk preferences of a nonrisk neutral decision maker could be modeled by an expectation concerning a reweighed or distorted probability measure, where the distortion function is as in Definition 1. We are ready to define a distortion risk measure, which is given as Definition 2.

Definition 2.

Let be a non-negative random variable and be a distortion function. The Choquet integral

| (35) |

is called a distortion risk measure, where on .

Note that is a distortion function since is a distortion function. Further, is an expectation with respect to a reweighed probability measure, namely ; that is, is a Lebesgue-Stieljes integral. It is not difficult to see that VaR and ES are distortion risk measures with distortion functions and , respectively for all . Other examples are i) Dual-power with , ii) Gini with , iii) Proportional hazard transform (PHT) with , and iv) Wang transform with .

The results in Section 2 could be generalized to the class of distortion risk measures through Lemma 1 after verifying some robustness conditions. Note that the case in which the risk preferences are ordered by ES is a special case of our main results in this section.

Lemma 1.

Let follow the standard normal distribution . We have

Proof.

It follows from the Central Limit Theorem that

As and is integrable, we have is -uniformly integrable.***For a distortion function , a set of random variables is called -uniformly integrable if By Theorem 4 of Wang et al. (2020), translation invariance and homogeneity of of order 1,

Therefore, instead of minimizing to define the optimal retention , we seek an approximately optimal retention by minimizing

| (36) |

Similar to Theorem 1, we can show the unique solution after replacing in Theorem 1 with . Further, we can estimate this unique approximately optimal retention and derive its asymptotic normal limit. Specifically, we have a generalized result below following a proof similar to that of Theorem 1, which is given as Theorem 7 that needs the following notation.

Theorem 7.

Assume , has the support (i.e., ) or , and is continuous on . When the support is , we further assume , which is always true when is large enough. Then, there exists a unique approximately optimal retention such that

4 Simulation studies

We conduct two simulation studies in this section. Section 4.1 assesses the validity of substituting the actual VaR of total cost as specified in (3) with the normal-approximated VaR outlined in (5); this assessment is conducted under the four loading factor rules delineated in Sections 2.1–2.4. Section 4.2 empirically examines the statistical properties of the optimal retention estimators introduced in Theorems 2, 4, and 6.

4.1 Examining validity of approximately optimal retention

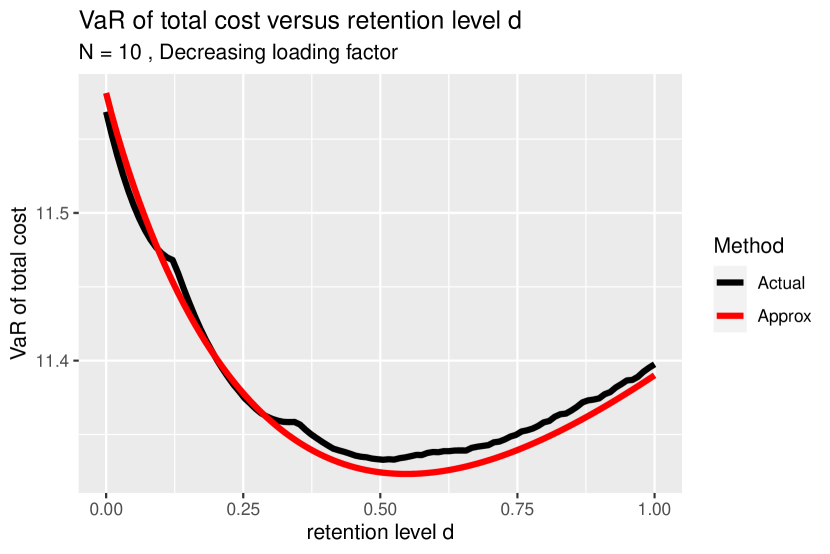

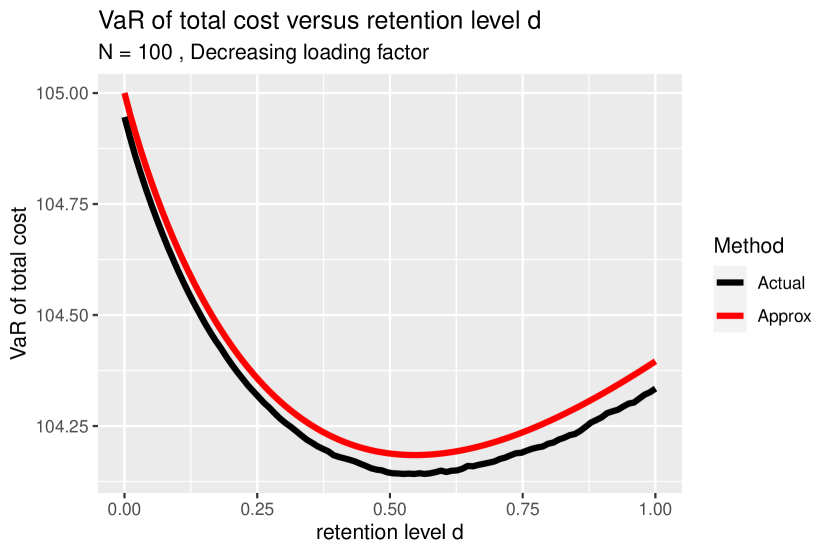

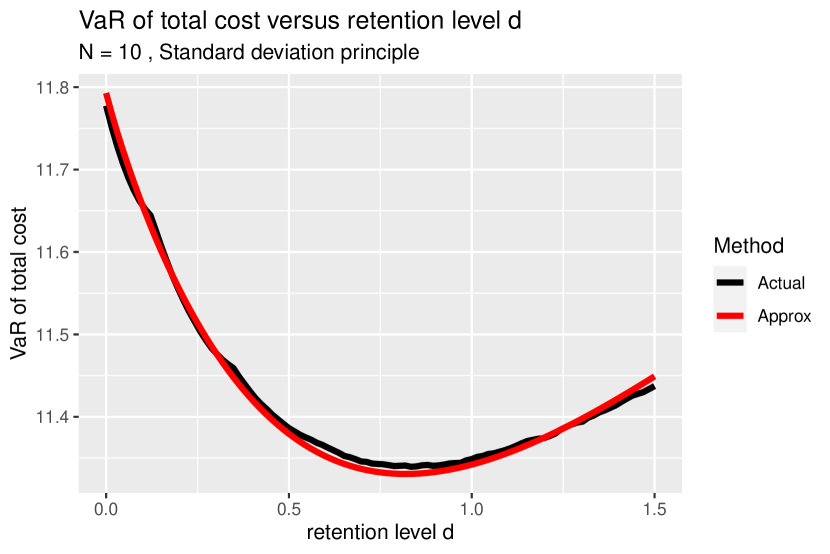

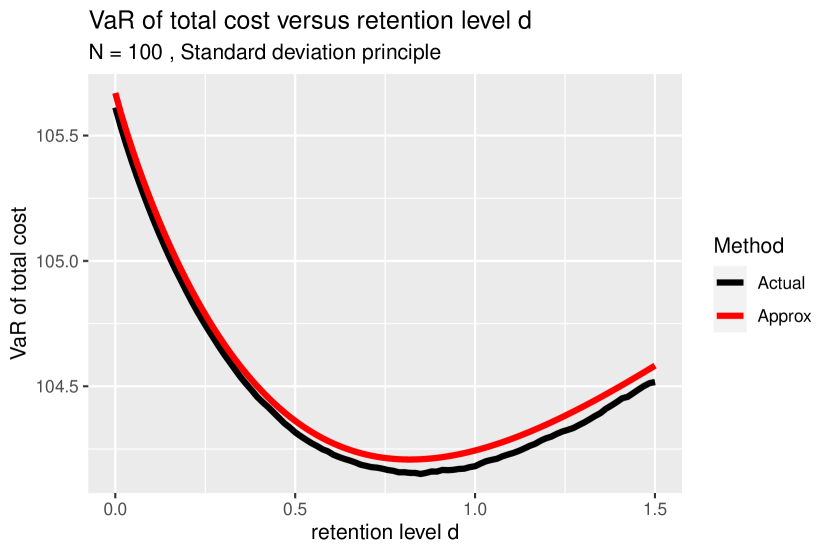

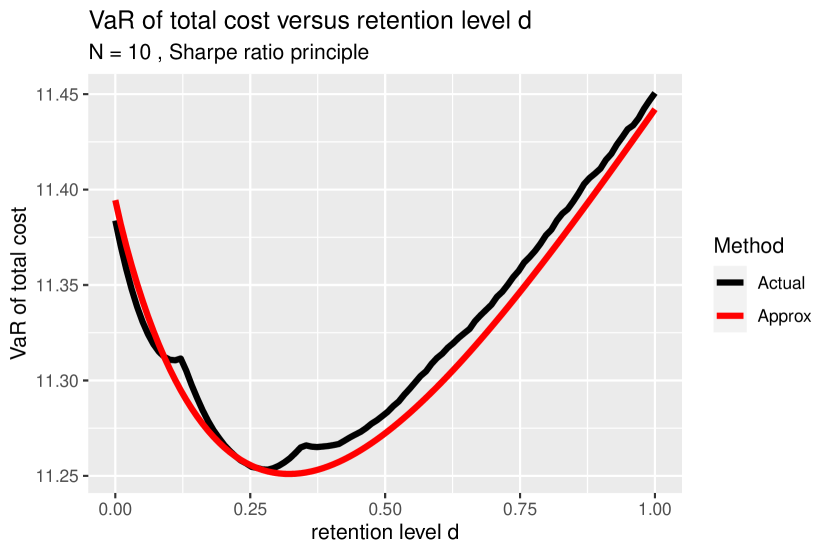

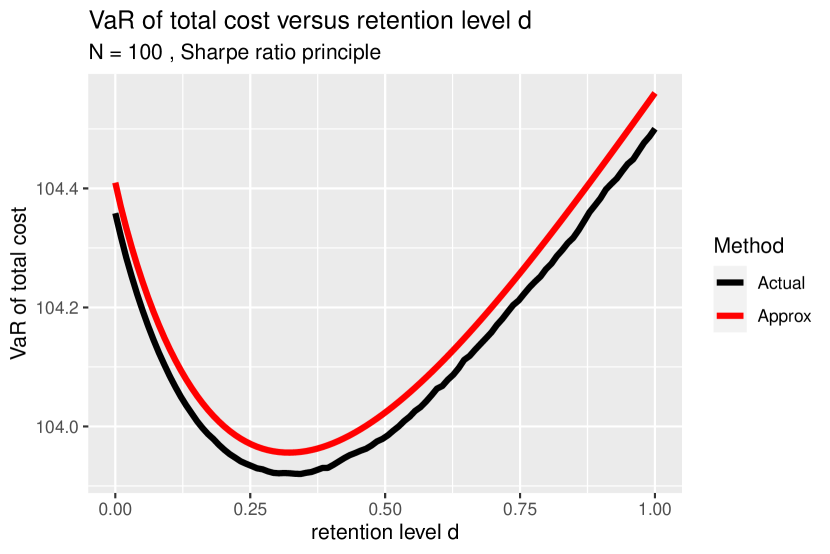

We generate samples of from a Pareto (type-II) distribution with a probability density function given by , where the shape parameter and the scale parameter , such that . We set the risk level at and consider sample sizes of , , and . In this analysis, we examine all four loading factor rules by setting for the constant loading factor, choosing for the decreasing loading factor, and for the remaining two rules.

We compute the true VaR of the total cost using (3), where and are approximated through simulated samples. For example, we have with iid sampled from a Pareto distribution for and . We also compute the normal-approximated VaR of total cost in (5) by numerical integration.

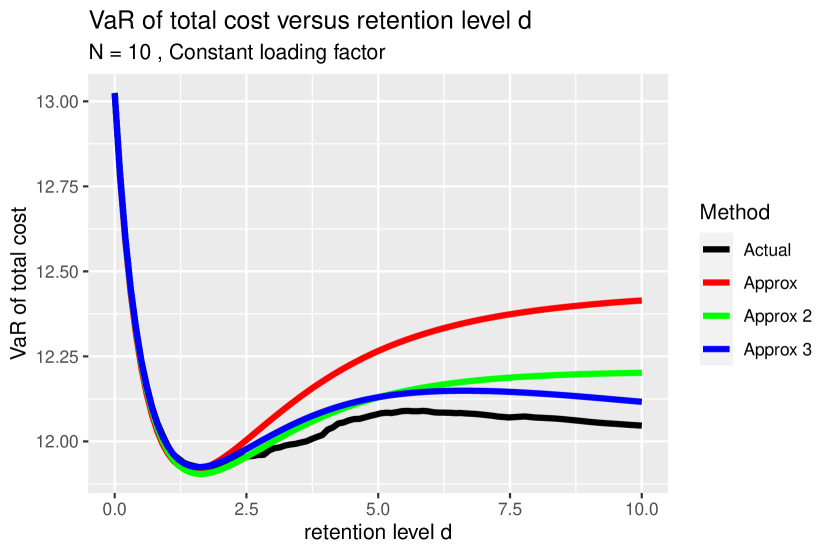

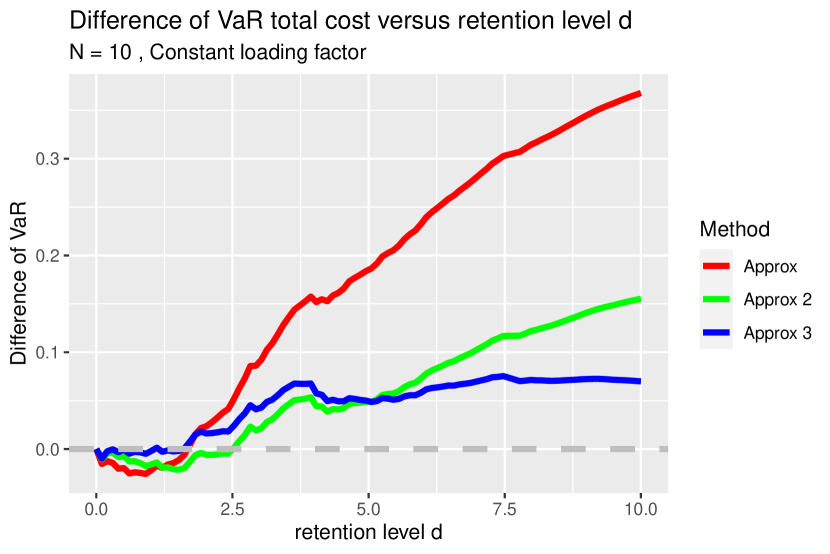

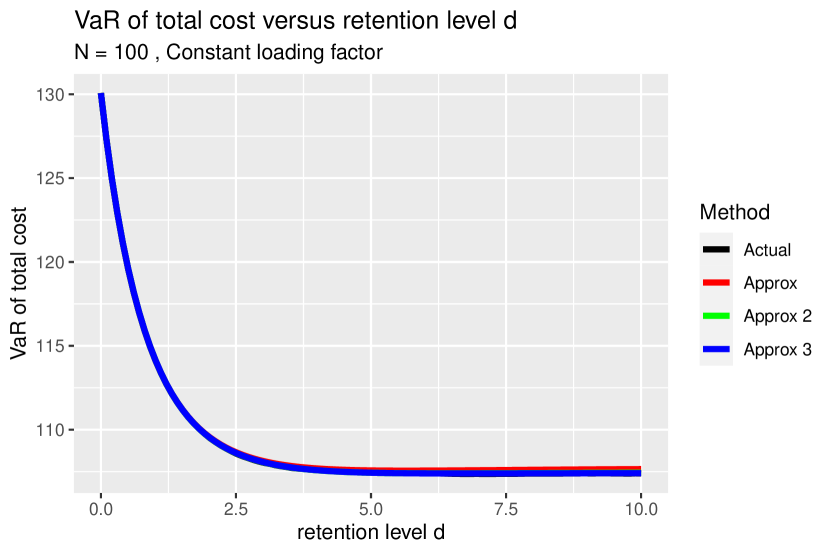

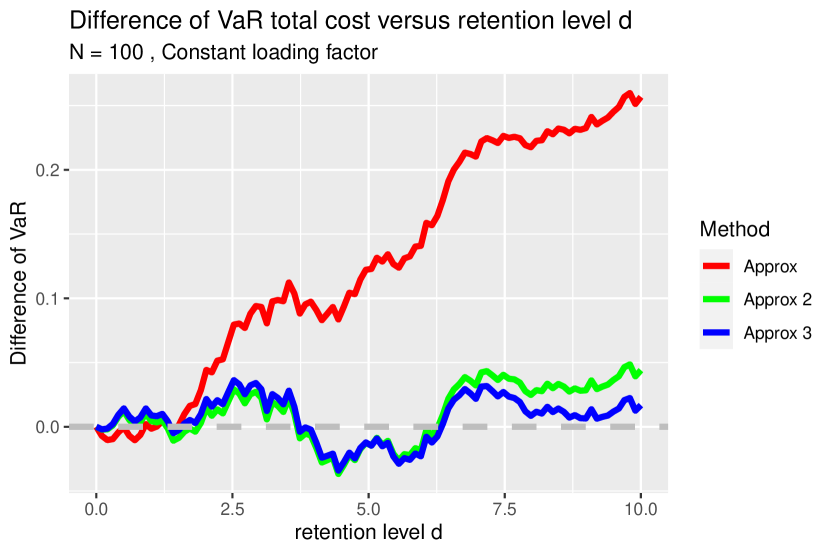

Figure 1 (left panel) and Figure 2 plot (red curves) and (black curves) as a function of for and under the four loading factor rules. We note that approximates closely to under all loading factor rules. For all loading factor rules except for the constant loading factor, we observe an optimal retention that minimizes the VaR of the total cost. Conversely, for the constant loading factor, both and become flat as increases, especially when is large. Hence, it is difficult to identify by solely observing the plots.

We then numerically calculate the actual and approximately optimal retentions and , and the results are displayed in Table 1. Recall that the approximation order of in (5) is . For all loading factor rules other than the constant loading factor, the actual optimal retention , which minimizes the true VaR of total cost , yields similar values as the approximately optimal retention , which minimizes the approximated VaR of total cost . Also, the relative difference generally reduces as increases. Furthermore, does not change substantially as changes. As a result, the approximate optimal retention approach for VaR works well under these three loading factor rules.

| Loading factor rule | Approx. order | Actual | Approx. | Diff. (%) | |

|---|---|---|---|---|---|

| Constant loading factor | 10 | 1.8549 | 1.4856 | -19.91 | |

| Constant loading factor | 10 | 1.8549 | 1.6276 | -12.25 | |

| Constant loading factor | 10 | 1.8549 | 1.5921 | -14.17 | |

| Constant loading factor | 25 | 3.4442 | 2.6838 | -22.08 | |

| Constant loading factor | 25 | 3.4442 | 2.9634 | -13.96 | |

| Constant loading factor | 25 | 3.4442 | 2.9969 | -12.99 | |

| Constant loading factor | 100 | 7.1241 | 5.6581 | -20.58 | |

| Constant loading factor | 100 | 7.1241 | 6.3361 | -11.06 | |

| Constant loading factor | 100 | 7.1241 | 6.6660 | -6.43 | |

| Decreasing loading factor | 10 | 0.5034 | 0.5472 | 8.70 | |

| Decreasing loading factor | 25 | 0.5835 | 0.5472 | -6.21 | |

| Decreasing loading factor | 100 | 0.5472 | 0.5472 | 0.02 | |

| Standard deviation principle | 10 | 0.7847 | 0.8189 | 4.36 | |

| Standard deviation principle | 25 | 0.8187 | 0.8189 | 0.03 | |

| Standard deviation principle | 100 | 0.8499 | 0.8189 | -3.64 | |

| Sharpe ratio principle | 10 | 0.2797 | 0.3218 | 15.06 | |

| Sharpe ratio principle | 25 | 0.3149 | 0.3218 | 2.18 | |

| Sharpe ratio principle | 100 | 0.3203 | 0.3218 | 0.45 |

For the constant loading factor, while the optimal retention exists despite the flatness of the curves in the left panels of Figure 1, there are noticeable discrepancies between and for a given , especially when is large. Hence, the normal approximation with order is not sufficiently accurate in determining the optimal retention under this loading factor rule. One may address this issue by employing Edgeworth expansion to improve the approximation precision. Denote and as the Edgeworth approximated VaRs with orders and , respectively; see Section 2 of the supplementary material for more details. We now add (green curves) and (blue curves) to the left panels of Figure 1 and the approximation errors (green curves) and (blue curves) to the right panels. We numerically calculate the optimal retention that minimizes the approximated VaRs and , and the results are added to Table 1. From the right panel, it is apparent that the approximation errors of VaR, especially for the higher-order Edgeworth expansions (blue curves), are significantly reduced compared to the normal approximations. The discrepancies between and are also significantly reduced by employing higher-order approximation methods. In a nutshell, the use of a constant loading factor needs a higher order Edgeworth expansion for the approximately optimal retention when is large.

4.2 Verifying statistical properties of nonparametric approach

We adopt the same simulation setup as in Section 4.1 except assessing larger sample sizes of and . The computational complexity associated with such large sample sizes is given by the fact the direct estimation of the true VaR of the total cost is unfeasible without resorting to the normal approximation technique. In each simulation run, we compute the nonparametric estimation of the approximately optimal retention, which is under the decreasing loading factor, under the standard deviation principle, or under the Sharpe ratio principle. To obtain an -vector of estimated optimal retentions, which is for each of the three loading factor rules, we repeat the simulation runs times. Additionally, through numerical integration, we compute the “true” approximately optimal retention, denoted as under the decreasing loading factor, under the standard deviation principle, or under the Sharpe ratio principle. We calculate the sample mean of and compare it with the true approximately optimal retention to evaluate the bias of the proposed nonparametric estimation approach.

| Mean optimal retention | Std. Error optimal retention | |||||

| True | Estimated | Bias (%) | Theoretical | Empirical | Diff. (%) | |

| Decreasing loading factor | ||||||

| 0.5472 | 0.5478 | 0.10 | 0.0392 | 0.0392 | -0.05 | |

| 0.5472 | 0.5478 | 0.11 | 0.0196 | 0.0201 | 2.57 | |

| 0.5472 | 0.5474 | 0.04 | 0.0088 | 0.0087 | -0.24 | |

| Standard deviation principle | ||||||

| 0.8189 | 0.8185 | -0.05 | 0.1115 | 0.1199 | 7.54 | |

| 0.8189 | 0.8187 | -0.03 | 0.0577 | 0.0594 | 2.98 | |

| 0.8189 | 0.8191 | 0.02 | 0.0263 | 0.0262 | -0.22 | |

| Sharpe ratio principle | ||||||

| 0.3218 | 0.3259 | 1.29 | 0.0442 | 0.0468 | 5.85 | |

| 0.3218 | 0.3233 | 0.46 | 0.0229 | 0.0235 | 2.64 | |

| 0.3218 | 0.3220 | 0.07 | 0.0104 | 0.0105 | 1.73 | |

Utilizing the results from Theorems 2, 4 and 6, we compute the theoretical standard error of the optimal retention estimators, represented as, for example, under the decreasing loading factor, and compare it with the sample standard deviation of to assess the validity of the theoretical results. Note that for the computation of standard errors under Theorems 4 and 6, we utilize the kernel density estimator with a Gaussian kernel function and a bandwidth of 0.1. While alternative kernel functions and bandwidths are possible, we have observed that they exert negligible influence on the computed standard errors, hence we do not delve into further details regarding these alternatives. Table 2 summarizes the findings across various and loading factor rules. Our observations indicate minimal estimation biases of the nonparametrically estimated optimal retention in all scenarios, and in turn, we empirically confirm the consistency of the proposed nonparametric estimators. Moreover, the empirical standard deviations of our estimators closely align with the theoretical standard errors across all cases, which provides empirical validation to the asymptotic properties outlined in Theorems 2, 4 and 6. Additionally, as becomes large, we note a decline in the relative bias of the estimated optimal retention, as well as the relative difference between the theoretical and empirical standard errors, consistent with the asymptotic theories.

5 Real Data analysis

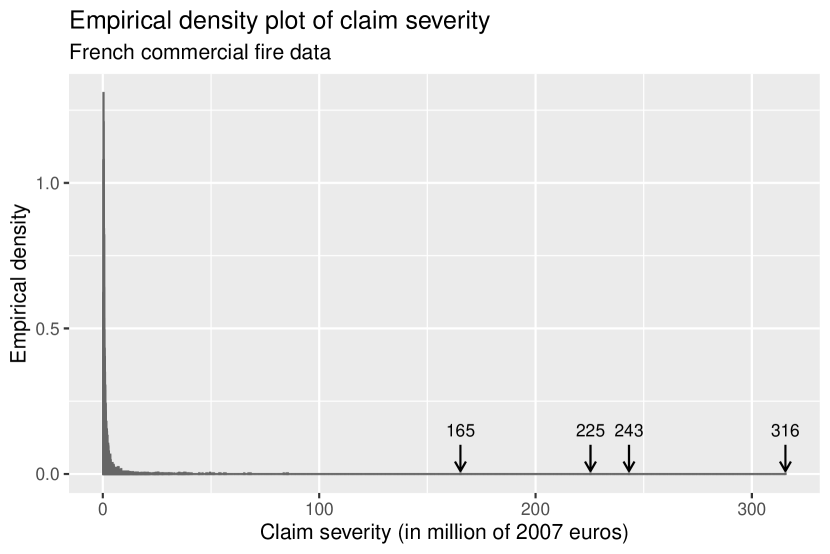

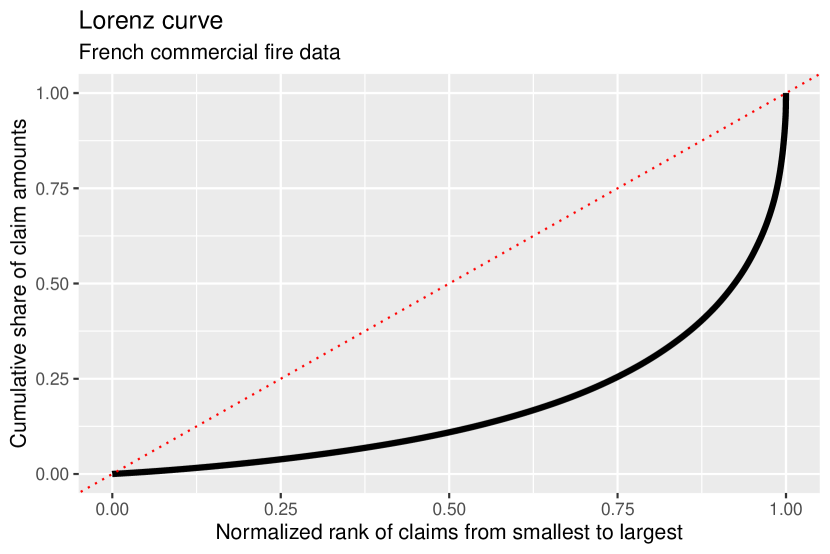

We analyze the frecomfire dataset, which consists of 9,613 commercial fire losses located in France, spanning from 1982 to 1996. This dataset is publicly accessible via the R package CASdatasets. The left panel of Figure 3 displays the empirical density of claim severities, with each claim expressed in million euros (at the 2007 value). The distribution of claim sizes exhibits significant right-skewness, as evidenced by several extreme losses indicated by arrows. In the right panel of Figure 3, the Lorenz curve illustrates the cumulative share of claim amounts against the cumulative normalized rank of claims. A substantial deviation of the Lorenz curve from the equality line indicates considerable disparities between large and small claims. The pronounced gap between the Lorenz curve and the equality line reflects the wide dispersion of claim amounts. Notably, the median, mean, and maximum loss amounts are 0.7633, 1.9811, and 315.54, respectively, with the 20 largest loss comprising more than 10% of the total loss. The heavy-tailed nature of the claim distribution, coupled with several exceptionally large losses, highlights the importance for insurance companies to transfer individual losses, rather than aggregate liabilities, to reinsurers. This motivates the analysis of EoL reinsurance, rather than SL reinsurance, as explored, for instance, by Cai and Tan (2007).

Our primary objective is to investigate the variations in nonparametric estimates of the approximately optimal retention across various effective loading factors and risk levels under three loading factor rules: decreasing loading factor, standard deviation principle, and Sharpe ratio principle. It is important to highlight that we assess the effective loading factors by using expressions such as (15) under the standard deviation principle, rather than relying on the nominal loading factors like in (15) so that we ensure equitable comparisons among the three loading factor rules.

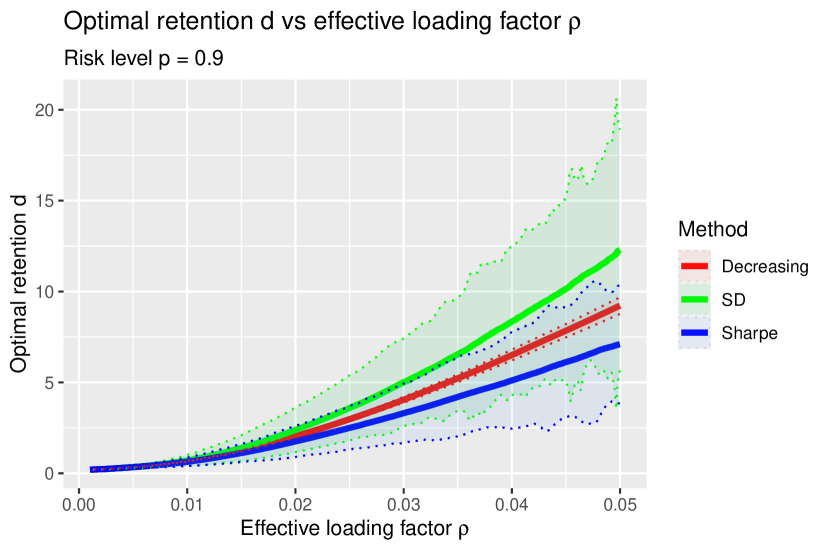

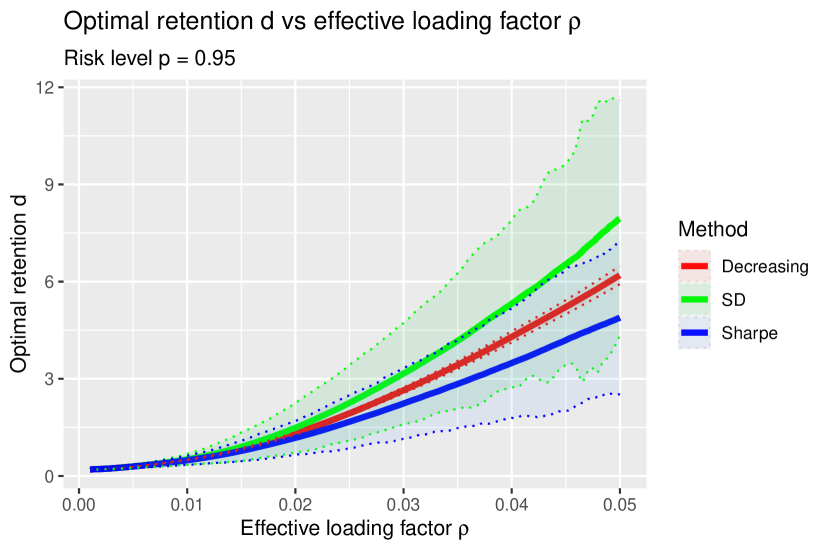

Figure 4 displays the optimal retention as a function of the effective loading factor , with fixed values of (left panel) or (right panel) under each of the three loading factor rules, accompanied by corresponding 95% confidence intervals determined based on Theorems 2, 4 and 6. Across all loading factor rules, it is evident that the optimal retention level increases with for any fixed . This observation is intuitive, as a higher implies a greater cost for risk transfer, thereby incentivizing insurers to retain losses up to a higher level. Furthermore, it is observed that the standard deviation loading factor principle yields the highest optimal retention for any fixed and , followed by the decreasing loading factor, and finally the Sharpe ratio principle. This trend can be rationalized by considering that the standard deviation of the excess loss decreases as increases. Consequently, the effective loading factor under the standard deviation principle diminishes with increasing , encouraging insurers to select a higher retention level to mitigate reinsurance costs. Additionally, the confidence bands under the standard deviation and Sharpe ratio principles are notably wider than those under the decreasing loading factor. This discrepancy arises because the loading factor under either principle, which is contingent on the second moment of the excess loss, may be heavily influenced by extreme losses, leading to increased standard errors. Conversely, the normal-approximated VaR of the total cost relies solely on the excess loss up to its first moment under the decreasing loading factor, resulting in decreased sensitivity of the estimated optimal retention to extreme losses.

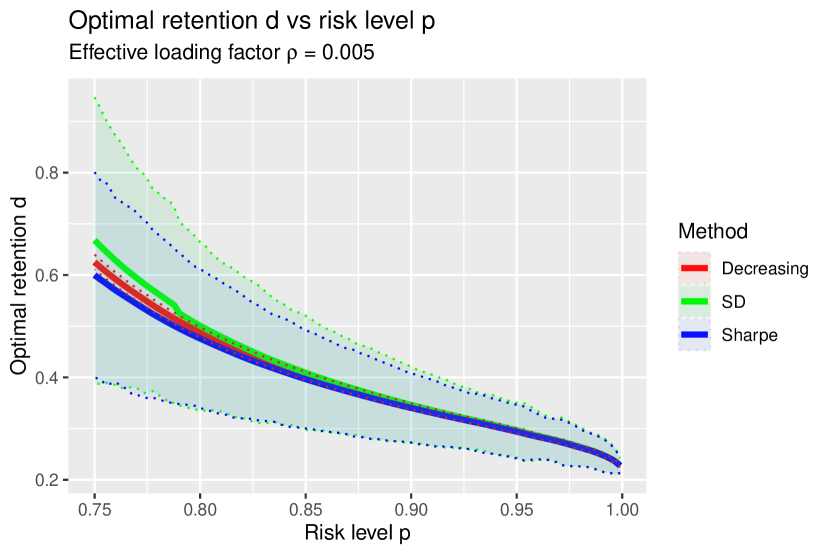

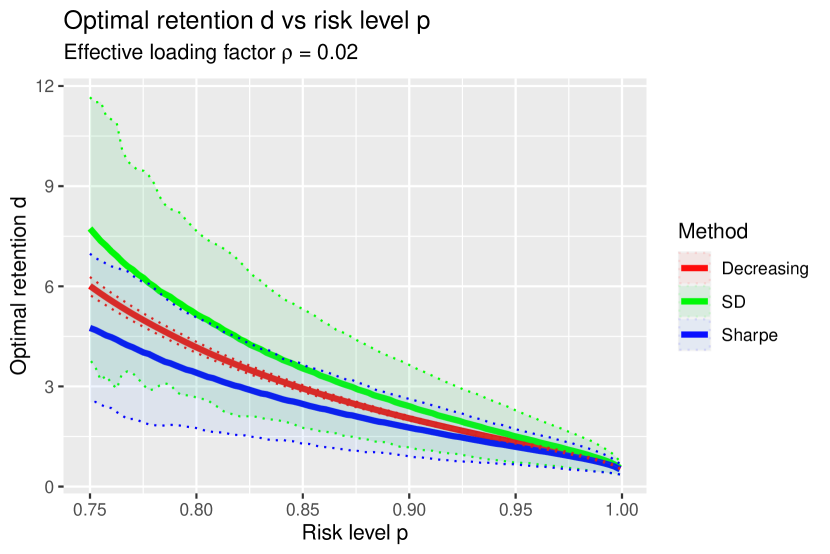

Figure 5 illustrates the optimal retention versus the risk level , with fixed values of (left panel) or (right panel) under the three loading factor rules, accompanied by 95% confidence intervals. Across all loading factor rules, it is observed that the optimal retention decreases as increases. This outcome is logical, as a higher risk level signifies insurers’ greater aversion to risk, thereby reducing their inclination to retain extreme losses by opting for a smaller retention level. Notably, our proposed method addresses the counterintuitive finding of Cai and Tan (2007) that the optimal retention remains unchanged as varies.

References

-

Asimit, A.V., Badescu, A.M. and Cheung, K.C. (2013). Optimal reinsurance in the presence of counterparty default risk. Insurance: Mathematics and Economics, 53(3),690–697.

-

Asimit, A.V., Badescu, A.M., Haberman, S. and Kim, E.-.S. (2016). Efficient risk allocation within a non-life insurance group under Solvency II Regime. Insurance: Mathematics and Economics, 66, 69–76.

-

Asimit, A.V., Badescu, A.M. and Verdonck, T. (2013). Optimal risk transfer under quantile-based risk measures. Insurance: Mathematics and Economics, 53(1), 252–265.

-

Asimit, A.V., Bignozzi, V., Cheung, K.C., Hu, J. and Kim, E.-.S. (2017). Robust and Pareto optimality of insurance contracts. European Journal of Operational Research, 262(2), 720–732.

-

Asimit, A.V., Chi, Y. and Hu, J. (2015). Optimal non-life reinsurance under Solvency II Regime. Insurance: Mathematics and Economics, 65, 227–237.

-

Asimit, A.V., Hu, J. and Xie, Y. (2019). Optimal robust insurance with a finite uncertainty set. Insurance: Mathematics and Economics, 87, 67–81.

-

Balbás, A., Balbás, B. and Heras, A. (2009). Optimal reinsurance with general risk measures. Insurance: Mathematics and Economics 44, 374–384.

-

Balbás, A., Balbás, B. and Heras, A. (2011). Stable solutions for optimal reinsurance problems involving risk measures. European Journal of Operational Research, 214(3), 796–804.

-

Bäuerle, N., and Glauner, A. (2018). Optimal risk allocation in reinsurance networks. Insurance: Mathematics and Economics, 82, 37-47.

-

Bernard, C. and Ludkovski, M. (2012). Impact of counterparty risk on the reinsurance market. North American Actuarial Journal 16(1), 87–111.

-

Bernard, C., and Tian, W. (2009). Optimal reinsurance arrangements under tail risk measures. Journal of Risk and Insurance 76, 709–725.

-

Boonen, T. J., and Ghossoub, M. (2023). Bowley vs. Pareto optima in reinsurance contracting. European Journal of Operational Research, 307(1), 382-391.

-

Boonen, T. J. and Jiang, W. (2022). A marginal indemnity function approach to optimal reinsurance under the Vajda condition. European Journal of Operational Research, 303(2), 928–944.

-

Boonen, T. J. and Jiang, W. (2024). Robust insurance design with distortion risk measures. European Journal of Operational Research, Forthcoming.

-

Cai, J., Lemieux, C., and Liu F. (2014) Optimal reinsurance with regulatory initial capital and default risk. Insurance: Mathematics and Economics 57, 13–24.

-

Cai, J., Li, J. Y. M. and Mao, T. (2023). Distributionally robust optimization under distorted expectations. Operations Research, Forthcoming.

-

Cai, J. and Tan, K.S. (2007). Optimal retention for a stop-loss reinsurance under the VaR and CTE risk measures. Astin Bulletin 37, 93–112.

-

Cai, J., Tan, K. S., Weng, C. and Zhang, Y. (2008). Optimal reinsurance under VaR and CTE risk measures. Insurance: Mathematics and Economics 43, 185–196.

-

Cai, J., and Weng C. (2016). Optimal reinsurance with expectile. Scandinavian Actuarial Journal (7), 624–645.

-

Chen, Y. (2024). Optimal insurance with counterparty and additive background risk. ASTIN Bulletin: The Journal of the IAA, 1-22.

-

Chi, Y. and Tan, K. S. (2021). Optimal incentive-compatible insurance with background risk. ASTIN Bulletin: The Journal of the IAA, 51(2), 661–688.

-

Chi, Y. and Tan, K. S. (2013). Optimal reinsurance with general premium principles. Insurance: Mathematics and Economics 52, 180–189.

-

Denneberg, D. (1994a). Non-additive measure and integral. Kluwer Academic Publishers, Dordrecht.

-

Denneberg, D. (1994b). Conditioning (updating) non-additive measures. Annals of Operations Research, 52, 21–42.

-

Embrechts, P. and Hofert, M. (2013). A note on generalized inverses, Mathematical Methods of Operations Research, 77, 423–432.

-

Föllmer, H. and Schied, A. (2011). Stochastic Finance: An Introduction in Discrete Time, Third ed., Walter de Gruyter.

-

Gollier, C. (2014). Optimal insurance design of ambiguous risks. Economic Theory 57, 555–576.

-

Kaluszka, M. (2001). Optimal reinsurance under mean-variance premium principles. Insurance: Mathematics and Economics 28, 61–67.

-

Rüschendorf, L. (2013). Mathematical Risk Analysis: Dependence, Risk Bounds, Optimal Allocations and Portfolios. Springer.

-

Wang, R., Wei, Y. and Willmot, G. E. (2020). Characterization, robustness and aggregation of signed Choquet integrals. Mathematics of Operations Research, 45(3), 993–1015.

-

Yaari, M. E. (1987). The dual theory of choice under risk. Econometrica: Journal of the Econometric Society, 95–115.

Supplementary materials for “A Revisit of the Optimal Excess-of-Loss Contract”

1 Numerical study: Comparing EoL and SL approaches

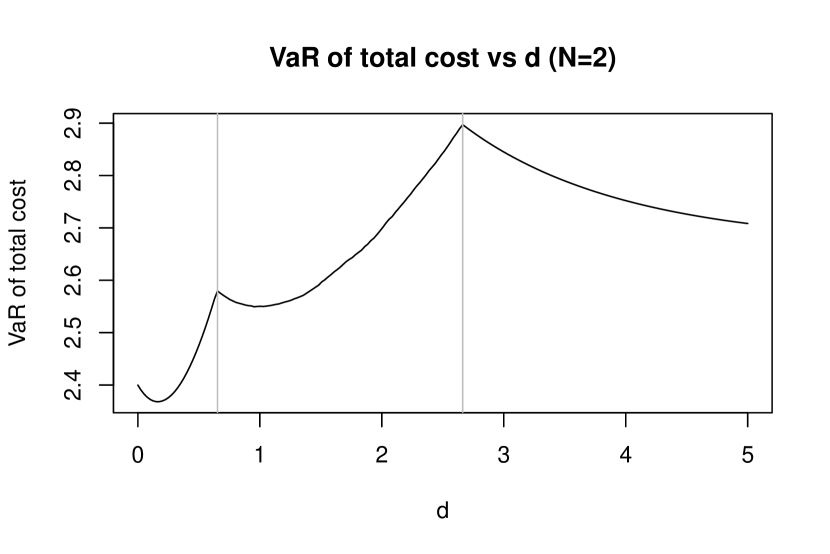

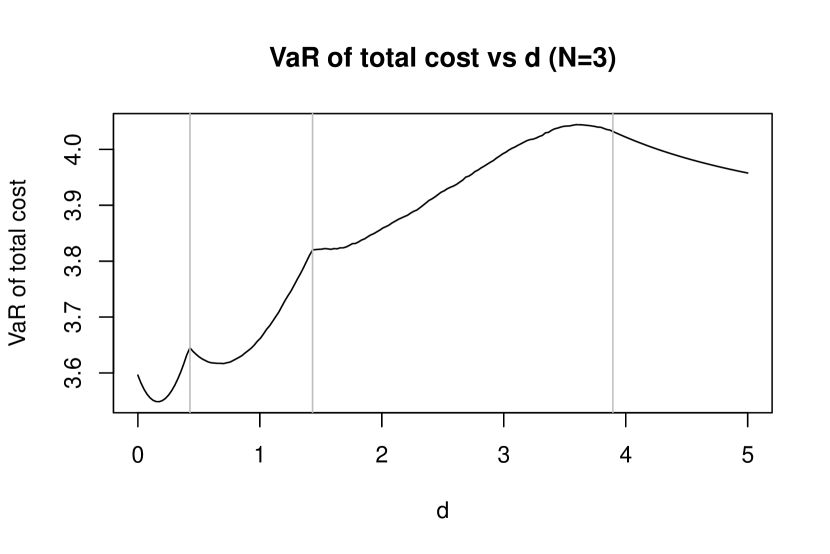

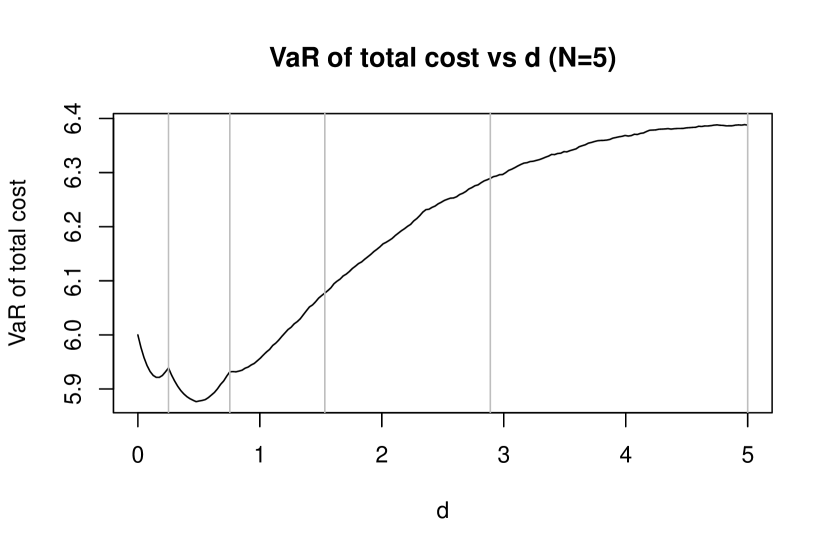

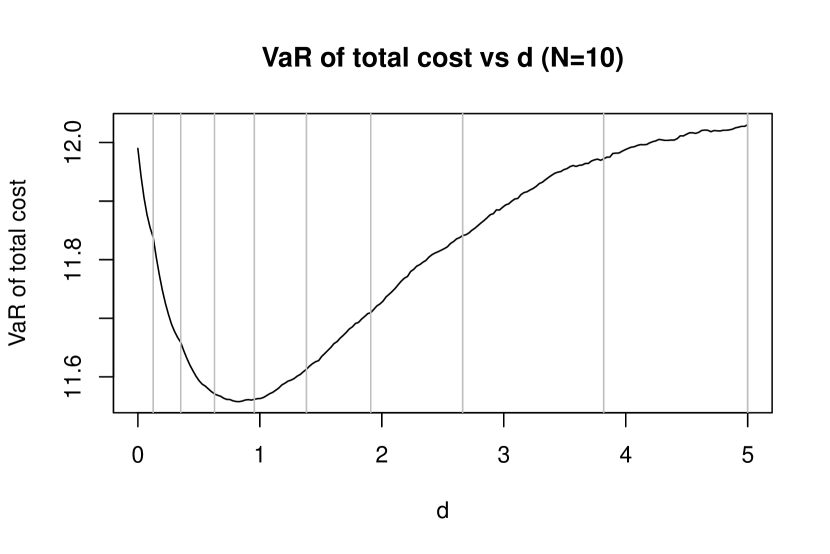

In this section, we substantiate the assertions presented in Section 1.2 of the manuscript regarding the comparison between the EoL and SL approaches. This is accomplished through a numerical investigation with a small supported by theoretical reasoning. We simulate from a Pareto (type-II) distribution with pdf with shape parameter and scale parameter , such that the mean is . We choose for the risk level, for the loading factor, and consider . We first compute the true VaR of the total cost using (3), where and are approximated, respectively, by the empirical -VaR and expectation of and from simulated samples. For example, we compute with iid sampled from the Pareto distribution for and .

Figure 6 plots as a function of for various . We note that is piecewise differentiable except for turning points, which are illustrated by the gray dotted vertical lines added in Figure 6. In addition, if we denote the -th turning point as for , we observe that ; indeed, the density function of exhibits jump points at integer multiples of , causing the turning points.

We then numerically calculate , i.e., minimize over , and compute the probability for various . An interesting series of observations is further noted.

First, the calculated value of is 0.1633, 0.1643, 0.5025, 0.8779, respectively, for . This coincides with the analysis in Theorem 1 that the optimal retention increases with if is fixed.

Second, the calculated probability is 0, 0, 0.25 and 0.25, respectively, for . As is large enough, the probability will be exactly 0.25, and otherwise, the probability will be exactly zero.

Third, we observe from the figure that if and if . Indeed, one can justify it theoretically as follows. From the definition of , if , we have

Since , is upper bounded by and hence , we have and hence . If , we have , and the distribution function of is continuous on . Hence, by the basic definition of quantile. Therefore, we conclude that the VaR of the total cost with the optimal retention is appropriate if and only if the optimal retention is above the first turning point.

Fourth, one can also show that if and only if . With a larger , this condition is more likely to hold. With , i.e., the SL approach following Cai and Tan (2007), we have given , and hence , meaning that the condition never holds.

Overall, while under the SL approach, we empirically and theoretically show that , the correct level, for sufficiently large under the EoL approach. Hence, the EoL optimal retention would not inherit the same counter-intuitive property as the SL optimal retention.

2 Approximating VaR of total cost by Edgeworth expansion

To address the issue of insufficient accuracy outlined by Section 4.1 under the constant loading factor rule, we employ Edgeworth expansion to improve the approximation precision from (4) in the manuscript to obtain and . Suppose that are iid random variables with zero mean, unit variance, and . Then, standard Edgeworth expansion yields

| (37) |

where , . Here, and are the moment quantities, and , and are the Hermite polynomials. From (37) and (3), one can apply the Cornish-Fisher expansion and write

| (38) | ||||

where and

with

We alternatively propose to compute the approximate optimal retention by minimizing

| (39) |

or

| (40) | |||

where the error terms underlying and are, respectively, and .