From Linear to Linearizable Optimization: A Novel Framework with Applications to Stationary and Non-stationary DR-submodular Optimization

Abstract

This paper introduces the notion of upper linearizable/quadratizable functions, a class that extends concavity and DR-submodularity in various settings, including monotone and non-monotone cases over different convex sets. A general meta-algorithm is devised to convert algorithms for linear/quadratic maximization into ones that optimize upper quadratizable functions, offering a unified approach to tackling concave and DR-submodular optimization problems. The paper extends these results to multiple feedback settings, facilitating conversions between semi-bandit/first-order feedback and bandit/zeroth-order feedback, as well as between first/zeroth-order feedback and semi-bandit/bandit feedback. Leveraging this framework, new algorithms are derived using existing results as base algorithms for convex optimization, improving upon state-of-the-art results in various cases. Dynamic and adaptive regret guarantees are obtained for DR-submodular maximization, marking the first algorithms to achieve such guarantees in these settings. Notably, the paper achieves these advancements with fewer assumptions compared to existing state-of-the-art results, underscoring its broad applicability and theoretical contributions to non-convex optimization.

1 Introduction

Overview: The prominence of optimizing continuous adversarial -weakly up-concave functions (with DR-submodular and concave functions as special cases) has surged in recent years, marking a crucial subset within the realm of non-convex optimization challenges, particularly in the forefront of machine learning and statistics. This problem has numerous real-world applications, such as revenue maximization, mean-field inference, recommendation systems [4, 19, 29, 11, 23, 17, 25]. This problem is modeled as a repeated game between an optimizer and an adversary. In each round, the optimizer selects an action, and the adversary chooses a -weakly up-concave reward function. Depending on the scenario, the optimizer can then query this reward function either at any arbitrary point within the domain (called full information feedback) or specifically at the chosen action (called semi-bandit/bandit feedback), where the feedback can be noisy/deterministic. The performance metric of the algorithm is measured with multiple regret notions - static adversarial regret, dynamic regret, and adaptive regret. The algorithms for the problem are separated into the ones that use a projection operator to project the point to the closest point in the domain, and the projection-free methods that replace the projection with an alternative such as Linear Optimization Oracles (LOO) or Separation Oracles (SO). This interactive framework introduces a range of significant challenges, influenced by the characteristics of the up-concave function (monotone/non-monotone), the constraints imposed, the nature of the queries, projection-free/projection-based algorithms, and the different regret definitions.

| Set | Feedback | Reference | Appx. | # of queries | ||||

| Monotone | Full Information | stoch. | [45] | |||||

| [34] | ||||||||

| Corollary 6-c | ||||||||

| Semi-bandit | stoch. | [34] | - | |||||

| Corollary 6-c | - | |||||||

| Full Information | stoch. | [34] | ||||||

| Corollary 6-c | - | |||||||

| Bandit | det. | [38] | - | |||||

| [47] | - | |||||||

| stoch. | [34] | - | ||||||

| Corollary 6-c | - | |||||||

| general | Full Information | stoch. | [34] | |||||

| Semi-bandit | stoch. | [7] | - | |||||

| [34] | - | |||||||

| Corollary 6-b | - | |||||||

| Full Information | stoch. | [34] | ||||||

| Bandit | stoch. | [34] | - | |||||

| Corollary 6-b | - | |||||||

| Non-Monotone | general | Full Information | stoch. | [34] | ||||

| [47] | ||||||||

| Corollary 6-d | ||||||||

| Semi-bandit | stoch. | [34] | - | |||||

| Corollary 6-d | - | |||||||

| Full Information | stoch. | [34] | ||||||

| Corollary 6-d | ||||||||

| Bandit | det. | [47] | - | |||||

| stoch. | [34] | - | ||||||

| Corollary 6-d | - | |||||||

This table compares different static regret results for the online up-concave maximization. The logarithmic terms in regret are ignored. Here . Our algorithm is projection-free and use a separation oracle. The rows marked with use gradient ascent, requiring potentially computationally expensive projections. Note that the result of [38], marked by , uses a convex optimization subroutine in each iteration, which could potentially be more expensive than projection and therefore not considered a projection-free result. It is also the only existing result, in all the tables, that outperforms ours.

All results assume that functions are Lipschitz. Except for our results on monotone functions over general convex sets, all results also assume differentiability. All previous results assume that functions are DR-submodular, while we only require up-concavity. Results of [34] and [38] also assume functions are smooth, i.e., their gradients are Lipschitz.

In this paper, we present a comprehensive approach to solving adversarial up-concave optimization problems, encompassing different feedback types (including bandit, semi-bandit and full-information feedback), characteristics of the up-concave function and constraint region, projection-free/projection-based algorithms, and regret definitions. While the problem has been studied in many special cases, the main contribution of this work is a framework that is based on a novel notion of the function class being upper linearizable (or upper quadratizable). We design a meta-algorithm that converts certain algorithms designed for online linear maximization to algorithms capable of handling upper linearizable function classes. This allows us to reduce the problem of up-concave maximization in three different settings to online linear maximization and obtain corresponding regret bounds. In particular, our results include monotone -weakly up-concave functions over general convex set, monotone -weakly up-concave functions over convex sets containing the origin and non-monotone up-concave functions. While the above result is for first order feedback, we then derive multiple results that increase the applicability of the above results. We extend the applicability of and algorithm introduced in [33] to our setting which allows us to convert algorithms for first-order/semi-bandit feedback into algorithms for zeroth-order/bandit feedback. We also design a meta-algorithm that allows us to convert algorithms that require full-information feedback into algorithms that only require semi-bandit/bandit feedback.

We demonstrate the usefulness of results through two applications as described in the following. In the first application, we use the SO-OGD Algorithm in [16] as the base algorithm for online linear optimization, which is a projection-free algorithm. Using this, we first obtain the adaptive regret (and therefore also static regret) guarantees for the three setups of DR-submodular (or more generally, up-concave) optimization with semi-bandit feedback/first order feedback in the respective cases. Then, the meta-algorithms for conversion of first-order/semi-bandit to zeroth-order/bandit are used to get result with zeroth-order/bandit feedback. In the cases where the algorithms are full-information and not (semi-)bandit, we use another meta-algorithm to obtain algorithms in (semi-)bandit feedback setting. In the next application, we use the “Improved Ader” algorithm of [42] which is a projection based algorithm providing dynamic regret guarantees for the convex optimization. Afterwards, the same approach as above are used to obtain the results in the three scenarios of up-concave optimization with first-order feedback.

Technical Novelty: The main technical novelties in this work are as follows.

-

1.

This paper proposes a novel framework and novel notion of quadratizable functions and relates the algorithms and regret guarantees for optimization of linear functions to that for quadratizable functions. The key novelty is that while the relation to linearization has been studied for convex optimization, we find that the relation is more general.

-

2.

We show that the class of quadratizable function optimization is general, and includes not only concave, but up-concave optimization in several cases. For some of the cases, this proof uses a generalization of the idea of boosting ([45, 47]) which was proposed for DR-submodular maximization, as mentioned in Corollaries 2 and 3.

- 3.

-

4.

We note the generality of the above results in this paper. Our results are general in the following three aspects:

a) In this work, we improve results for projection-free static regret guarantees for DR-submodular optimization in all considered cases and obtain the first results for dynamic and adaptive regret. Moreover, these guarantees follow from existing algorithms for the linear optimization, using only the statement of the regret bounds and simple properties of the algorithms.

b) We consider 3 classes of DR-submodular functions in this work. However, to extend these results to another function class, all one needs to do is to (i) prove that the function class is quadratizable; and (ii) provide an unbiased estimator of (as described in Equation 1).

c) We consider 2 different feedback types in offline setting (first/zero order) and 4 types of feedback in the online setting (first/zero order and full-information/trivial query). Converting results between different cases is obtained through meta-algorithms and guarantees for the meta-algorithms which only relies on high level properties of the base algorithms (See Theorems 6, 7 and 8)

Key contributions: The key contributions in this work are summarized as follows.

-

1.

This paper formulates the notion of upper quadratizable functions, which is a class that generalizes the notion of concavity and also DR-submodularity in several settings. In particular, we demonstrate the the following function classes are upper quadratizable: (i) monotone -weakly -strongly DR-submodular functions with curvature over general convex sets, (ii) monotone -weakly DR-submodular functions over convex sets containing the origin, and (iii) non-monotone DR-submodular optimization over general convex sets.

-

2.

We provide a general meta-algorithm that converts algorithms for linear/quadratic maximization to algorithms that maximize upper quadratizable functions. This results is a unified approach to maximize both concave functions and DR-submodular functions in several settings.

-

3.

While the above provides results for semi-bandit feedback (for monotone DR-submodular optimization over general convex sets) and first-order feedback (for monotone DR-submodular optimization over convex sets containing the origin, and non-monotone DR-submodular optimization over general convex sets), the results could be extended to more general feedback settings. Two meta algorithms are provided that relate semi-bandit/first-order feedback to bandit/zeroth order feedback; and that relate first/zeroth order feedback to semi-bandit/bandit feedback. Together they allow us to obtain results in 4 feedback settings (first/zero order full-information and semi-bandit/bandit). We also discuss a meta-algorithm to convert online results to offline guarantees.

-

4.

The above framework is applied using different algorithms as the base algorithms for linear optimization. SO-OGD [16] is a projection-free algorithm using separation oracles that provides adaptive regret guarantees for online convex optimization. We use our framework to obtain 10 projection-free algorithms that cover all 12 cases in Table 1. We improve the regret guarantees for the previous SOTA projection-free algorithms in all the cases. If we also allow comparisons with the algorithms that are not projection-free, we still improve the SOTA results in 3 cases and match the SOTA in 8 cases.

-

5.

Using our framework, we convert online results using SO-OGD to offline results to obtain 6 projection free algorithms described in Table 2. We improve the regret guarantees for the previous SOTA projection-free algorithms in all the cases. If we also allow comparisons with the algorithms that are not projection-free, we still improve the SOTA results in 3 cases and match the SOTA in the remaining 3 cases.

-

6.

We use our framework to convert the adaptive regret guarantees of SO-OGD to obtain projection-free algorithms with adaptive regret bounds that cover all cases in Table 3. Our results are first algorithms with adaptive regret guarantee for online DR-submodular maximization.

-

7.

“Improved Ader” [42] is an algorithm providing dynamic regret guarantees for online convex optimization. We use our framework to obtain 6 algorithms which provide the dynamic regret guarantees as shown in Table 3. Our results are first algorithms with dynamic regret guarantee for online DR-submodular maximization.

-

8.

For monotone -weakly functions with bounded curvature over general convex sets, we improve the approximation ratio (See Lemma 1).

-

9.

As mentioned in the descriptions of the tables, in all cases considered, whenever there is another existing result, we obtain our results using fewer assumptions than the existing SOTA.

2 Problem Setup and Definitions

For a set , we define its affine hull to be the set of for all in and . The relative interior of is defined as For any , we define the path length Given and , we say a differentiable function is -strongly -weakly up-concave if it is -strongly -weakly concave along positive directions. Specifically if, for all in , we have

This table compares the different results for the number of oracle calls (complexity) within the constraint set for up-concave maximization with stochastic feedback. Here and .

[19], [45] and [47] use gradient ascent, requiring potentially computationally expensive projections.

All previous results assume that functions are differentiable, DR-submodular, Lipschitz and smooth (i.e., their gradients are Lipschitz). Result of [18] also requires the function Hessians to be Lipschitz. It also requires the density of the stochastic oracle to be known and the log of density to be 4 times differentiable with bounded 4th derivatives. We only require the functions to be up-concave, differentiable and Lipschitz, expect for results on monotone functions over general convex sets where we do not need differentiability.

We say is a -strongly -weakly up-super-gradient of if for all in , the above holds with instead of . We say is -strongly -weakly up-concave if it is continuous and it has a -strongly -weakly up-super-gradient. When it is clear from the context, we simply refer to as an up-super-gradient for . When and the above inequality holds for all , we say is -strongly concave. A differentiable function is called -weakly continuous DR-submodular if for all , we have . It follows that any -weakly continuous DR-submodular functions is -weakly up-concave. We refer to Appendix B for more details.

Given a continuous monotone function , its curvature is defined as the smallest number such that for all and such that 111 In the literature, the curvature is often defined for differentiable functions. When is differentiable, we have . We define the curvature of a function class as the supremum of the curvature of functions in .

Online optimization problems can be formalized as a repeated game between an agent and an adversary. The game lasts for rounds on a convex domain where and are known to both players. In -th round, the agent chooses an action from an action set , then the adversary chooses a loss function and a query oracle for the function . Then, for , the agent chooses a points and receives the output of the query oracle. The precise definition of agent is given in Appendix B, with the query oracle being any of stochastic/deterministic first/zeroth order or semi-bandit/bandit.

An adversary is a set of realized adversaries , where each maps to where and is a query oracle for . Adversaries can be oblivious ( are constant and independent of ), weakly adaptive ( are independent of ), or fully adaptive (no restrictions). We use to denote the set of all possible realized adversaries with deterministic -th order oracles. If the oracle is instead stochastic and bounded by , we use to denote such an adversary. Finally, we use and to denote all oblivious realized adversaries with -th order deterministic and stochastic oracles, respectively. In order to handle different notions of regret with the same approach, for an agent , adversary , compact set , approximation coefficient and , we define regret as

where the expectation in the definition of the regret is over the randomness of the algorithm and the query oracle. We use the notation when is a singleton. We may drop when it is equal to 1. When , we often assume that the functions are non-negative. Static adversarial regret or simply adversarial regret corresponds to , and . When , and contains only a single element then it is referred to as the dynamic regret [50, 42]. Adaptive regret is defined as [22]. We drop , and when the statement is independent of their value or their value is clear from the context.

| Set | Feedback | Reference | Appx. | regret type | |||

| Monotone | Full Information | Corollary 7-c | dynamic | ||||

| Corollary 6-c | adaptive | ||||||

| Semi-bandit | Corollary 6-c | adaptive | |||||

| Full Information | Corollary 7-c | dynamic | |||||

| Corollary 6-c | adaptive | ||||||

| Bandit | Corollary 6-c | adaptive | |||||

| general | Semi-bandit | Corollary 7-b | dynamic | ||||

| Corollary 6-b | adaptive | ||||||

| Bandit | Corollary 7-b | dynamic | |||||

| Corollary 6-b | adaptive | ||||||

| Non-Monotone | general | Full Information | Corollary 7-d | dynamic | |||

| Corollary 6-d | adaptive | ||||||

| Semi-bandit | Corollary 6-d | adaptive | |||||

| Full Information | Corollary 7-d | dynamic | |||||

| Corollary 6-d | adaptive | ||||||

| Bandit | Corollary 6-d | adaptive | |||||

This table includes different results for non-stationary up-concave maximization, while no prior results exist in this setup to the best of our knowledge. The results for adaptive regret are projection-free and use a separation oracle while results for dynamic regret use convex projection.

3 Formulation of Upper-Quadratizable Functions and Regret Relation to that of Quadratic Functions

Let be a convex set, be a function class over . We say the function class is upper quadratizable if there are maps and and constants , and such that

| (1) |

As a special case, when , we say is upper linearizable. We use the notation to denote the class of functions for all and . Similarly, for any , we use the notation to denote the class of functions for all , and . A similar notion of lower-quadratizable/linearizable may be similarly defined for minimization problems such as convex minimization 222 We say is lower-quadratizable if .

We say an algorithm is a first order query algorithm for if, given a point and a first order query oracle for , it returns (a possibly unbiased estimate of) . We say is bounded by if the output of is always within the ball and we call it trivial if it simply returns the output of the query oracle at .

Recall that an online agent is composed of action function and query function . Informally, given an online algorithm with semi-bandit feedback, we may think of as the online algorithm with and . As a special case, when and is trivial, we have .

Theorem 1.

Let be algorithm for online optimization with semi-bandit feedback. Also let be function class over that is quadratizable with and maps and , let be a query algorithm for and let . Then the following are true.

-

1.

If returns the exact value of , then we have .

-

2.

On the other hand, if returns an unbiased estimate of and the output of is bounded by , then we have .

4 Up-concave function optimization is upper-quadratizable function optimization

In this section, we study three classes of up-concave functions and show that they are upper-quadratizable. We further use this property to obtain meta-algorithms that convert algorithms for quadratic optimization into algorithms for up-concave maximization.

4.1 Monotone up-concave optimization over general convex sets

For differentiable DR-submodular functions, the following lemma is proven for the case in Lemma 2 in [12] and for the case in [19], (Inequality 7.5 in the arXiv version). See Appendix D for proof.

Lemma 1.

Let be a non-negative monotone -strongly -weakly up-concave function with curvature bounded by . Then, for all , we have

where is an up-super-gradient for .

Here we show that any semi-bandit feedback online linear optimization algorithm for fully adaptive adversary is also an online up-concave optimization algorithm.

Theorem 2.

Let be a convex set, let , , and let be algorithm for online optimization with semi-bandit feedback. Also let be a function class over where every is the restriction of a monotone -strongly -weakly up-concave function curvature bounded by defined over to the set . Then we have

Theorem 3.

Under assumptions of Theorem 2, if we further assume that is -Lipschitz for some and , then we have

4.2 Monotone up-concave optimization over convex sets containing the origin

The following lemma is proven for differentiable DR-submodular functions in Theorem 2 and Proposition 1 of [45]. The proof works for general up-concave functions as well. We include a proof in Appendix E for completeness.

Lemma 2.

Let be a non-negative monotone -weakly up-concave differentiable function and let be the function defined by

Then is differentiable and, if the random variable is defined by the law

| (2) |

then we have . Moreover, we have

Theorem 4.

Let be a convex set containing the origin, let and let be algorithm for online optimization with semi-bandit feedback. Also let be a function class over where every is the restriction of a monotone -weakly up-concave function defined over to the set . Assume is differentiable and -Lipschitz for some . Then, for any , we have

where .

4.3 Non-monotone up-concave optimization over general convex sets

The following lemma is proven for differentiable DR-submodular functions in Corollary 2, Theorem 4 and Proposition 2 of [47]. The arguments works for general up-concave functions as well. We include a proof in Appendix F for completeness.

Lemma 3.

Let be a non-negative continuous up-concave differentiable function and let . Define as the function

Then is differentiable and, if the random variable is defined by the law

| (3) |

then we have . Moreover, we have

Theorem 5.

Let be a convex set, , and be algorithm for online optimization with semi-bandit feedback. Also let be a function class over where every is the restriction of an up-concave function defined over to the set . Assume is differentiable and -Lipschitz for some . Then, for any , we have

where .

5 Meta algorithms for other feedback cases

In this section, we study several meta-algorithms that allow us to convert between different feedback types and also convert results from the online setting to the offline setting.

First order/semi-bandit to zeroth order/bandit feedback: In this section we discuss meta-algorithms that convert algorithms designed for first order feedback into algorithms that can handle zeroth order feedback. These algorithms and results are generalization of similar results in [33] to the case where .

We choose a point and a real number such that . Then, for any shrinking parameter , we define . For a function defined on a convex set , its -smoothed version is given as

where , for any , is the linear space that is a translation of the affine hull of and is sampled uniformly at random from the -dimensional ball . Thus, the function value is obtained by “averaging” over a sliced ball of radius around . For a function class over , we use to denote . We will drop the subscript when there is no ambiguity (See Appendix G for the description of the algorithms and the proof.).

Theorem 6.

Let be an -Lipschitz function class over a convex set and choose and as described above and let . Let be a compact set and let . Assume is an algorithm for online optimization with first order feedback. Then, if where is described by Algorithm 5 and , we have

On the other hand, if we assume that is semi-bandit, then the same regret bounds hold with , where is described by Algorithm 6.

Full information to trivial query: In this section, we discuss a meta-algorithm that converts algorithms that require full-information feedback into algorithms that have a trivial query oracle. In particular, it converts algorithms that require first-order full-information feedback into semi-bandit algorithms and algorithms that require zeroth-order full-information feedback into bandit algorithms.

Here we assume that does not depend on the observations in the current round. If the number of queries is not constant for each time-step, we simply assume that queries extra points and then discards them, so that we obtain an algorithm that queries exactly points at each time-step, where does not depend on . We say a function class is closed under convex combination if for any and any with , we have .

Theorem 7.

Let be an online optimization algorithm with full-information feedback and with queries at each time-step where does not depend on the observations in the current round and . Then, for any -Lipschitz function class that is closed under convex combination and any , and , let , , and let and denote the horizon of the adversary. Then, we have

Online to Offline: An offline optimization problem can be though of as an instance of online optimization where the adversary picks the same function and query oracle at each round. Moreover, instead of regret, the performance of the algorithm is measured by sample complexity, i.e., the minimum number of queries required so that the expected error from the -approximation of the optimal value is less than . Conversions of online algorithms to offline are referred to online-to-batch techniques and are well-known in the literature (See [37]). A simple approach is to simply run the online algorithm and if the actions chosen by the algorithm are , return for with probability . We use to denote the meta-algorithm that uses this approach to convert online algorithms to offline algorithms. The following theorem is a corollary which we include for completion (See Appendix I for the proof.).

Theorem 8.

Let be an online algorithm that queries no more than times per time-step that obtains an -regret bound of over an oblivious adversary . Then the sample complexity of over is .

6 Applications

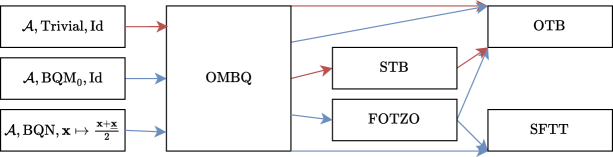

Figure 1 captures the applications that are mentioned in Tables 1, 2 and 3. The exact statements are stated in Corollaries 6, 7 and 6 in the Appendix. To obtain a result from the graph, let be one of SO-OGA or IA and select a directed path that has the following properties.

-

•

The path starts at one of the three nodes on the left.

-

•

The path must be at least of length 1 and the edges must be the same color.

-

•

If is IA, the path should not contain or .

For example, if and the path starts at the middle node on the left, then passes through , , , we get

which is a projection-free algorithm (using separation oracles) with bandit feedback for monotone up-concave functions over convex sets that contain the origin. As mentioned in Table 3 and Corollary 6-(c), the adaptive regret of this algorithm is of order . Note that the text written in the three nodes on the left correspond to the inputs of the meta-algorithm . Also note that the color red corresponds to the setting where is a trivial query algorithm which means that the output of is semi-bandit.

7 Conclusions

In this work, we have presented a comprehensive framework for addressing optimization problems involving upper quadratizable functions, encompassing both concave and DR-submodular functions across various settings and feedback types. Our contributions include the formulation of upper quadratizable functions as a generalized class, the development of meta-algorithms for algorithmic conversions, and the derivation of new projection-free algorithms with improved regret guarantees. By extending existing techniques from linear/quadratic optimization to upper quadratizable functions, we have significantly advanced the state-of-the-art in non-convex optimization.

Moreover, our results offer insights into the fundamental properties of optimization problems, shedding light on the connections between different function classes and algorithmic approaches. The versatility of our framework allows for seamless transitions between different feedback settings, enabling practitioners to tailor algorithms to specific application requirements. Furthermore, our results in dynamic and adaptive regret guarantees for DR-submodular maximization represent significant milestones in the field, opening up new avenues for research and application.

References

- [1] Omar Besbes, Yonatan Gur, and Assaf Zeevi. Non-stationary stochastic optimization. Operations Research, 63(5):1227–1244, 2015.

- [2] An Bian, Kfir Levy, Andreas Krause, and Joachim M Buhmann. Continuous DR-submodular maximization: Structure and algorithms. In Advances in Neural Information Processing Systems, 2017.

- [3] Andrew An Bian, Baharan Mirzasoleiman, Joachim Buhmann, and Andreas Krause. Guaranteed Non-convex Optimization: Submodular Maximization over Continuous Domains. In Proceedings of the 20th International Conference on Artificial Intelligence and Statistics, April 2017.

- [4] Yatao Bian, Joachim Buhmann, and Andreas Krause. Optimal continuous DR-submodular maximization and applications to provable mean field inference. In Proceedings of the 36th International Conference on Machine Learning, June 2019.

- [5] Gruia Calinescu, Chandra Chekuri, Martin Pál, and Jan Vondrák. Maximizing a monotone submodular function subject to a matroid constraint. SIAM Journal on Computing, 40(6):1740–1766, 2011.

- [6] Lin Chen, Christopher Harshaw, Hamed Hassani, and Amin Karbasi. Projection-free online optimization with stochastic gradient: From convexity to submodularity. In Proceedings of the 35th International Conference on Machine Learning, July 2018.

- [7] Lin Chen, Hamed Hassani, and Amin Karbasi. Online continuous submodular maximization. In Proceedings of the Twenty-First International Conference on Artificial Intelligence and Statistics, April 2018.

- [8] Lin Chen, Mingrui Zhang, and Amin Karbasi. Projection-free bandit convex optimization. In Proceedings of the Twenty-Second International Conference on Artificial Intelligence and Statistics, pages 2047–2056. PMLR, 2019.

- [9] Shengminjie Chen, Donglei Du, Wenguo Yang, Dachuan Xu, and Suixiang Gao. Continuous non-monotone DR-submodular maximization with down-closed convex constraint. arXiv preprint arXiv:2307.09616, July 2023.

- [10] Amit Daniely, Alon Gonen, and Shai Shalev-Shwartz. Strongly adaptive online learning. In Proceedings of the 32nd International Conference on Machine Learning, pages 1405–1411. PMLR, 2015.

- [11] Josip Djolonga and Andreas Krause. From map to marginals: Variational inference in Bayesian submodular models. Advances in Neural Information Processing Systems, 2014.

- [12] Maryam Fazel and Omid Sadeghi. Fast first-order methods for monotone strongly dr-submodular maximization. In SIAM Conference on Applied and Computational Discrete Algorithms (ACDA23), 2023.

- [13] Yuval Filmus and Justin Ward. A tight combinatorial algorithm for submodular maximization subject to a matroid constraint. In 2012 IEEE 53rd Annual Symposium on Foundations of Computer Science, pages 659–668, 2012.

- [14] Abraham D Flaxman, Adam Tauman Kalai, and H Brendan McMahan. Online convex optimization in the bandit setting: gradient descent without a gradient. In Proceedings of the sixteenth annual ACM-SIAM symposium on Discrete algorithms, pages 385–394, 2005.

- [15] Dan Garber and Ben Kretzu. Improved regret bounds for projection-free bandit convex optimization. In Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics, pages 2196–2206. PMLR, 2020.

- [16] Dan Garber and Ben Kretzu. New projection-free algorithms for online convex optimization with adaptive regret guarantees. In Proceedings of Thirty Fifth Conference on Learning Theory, pages 2326–2359. PMLR, 2022.

- [17] Shuyang Gu, Chuangen Gao, Jun Huang, and Weili Wu. Profit maximization in social networks and non-monotone DR-submodular maximization. Theoretical Computer Science, 957:113847, 2023.

- [18] Hamed Hassani, Amin Karbasi, Aryan Mokhtari, and Zebang Shen. Stochastic conditional gradient++: (non)convex minimization and continuous submodular maximization. SIAM Journal on Optimization, 30(4):3315–3344, 2020.

- [19] Hamed Hassani, Mahdi Soltanolkotabi, and Amin Karbasi. Gradient methods for submodular maximization. In Advances in Neural Information Processing Systems, 2017.

- [20] Elad Hazan and Satyen Kale. Projection-free online learning. In Proceedings of the 29th International Coference on International Conference on Machine Learning, ICML’12, pages 1843–1850. Omnipress, 2012.

- [21] Elad Hazan and Edgar Minasyan. Faster projection-free online learning. In Proceedings of Thirty Third Conference on Learning Theory, pages 1877–1893. PMLR, 2020.

- [22] Elad Hazan and C. Seshadhri. Efficient learning algorithms for changing environments. In Proceedings of the 26th Annual International Conference on Machine Learning, ICML ’09, pages 393–400. Association for Computing Machinery, 2009.

- [23] Shinji Ito and Ryohei Fujimaki. Large-scale price optimization via network flow. Advances in Neural Information Processing Systems, 2016.

- [24] Duksang Lee, Nam Ho-Nguyen, and Dabeen Lee. Non-smooth, h\”older-smooth, and robust submodular maximization. arXiv preprint arXiv:2210.06061, 2023.

- [25] Yuanyuan Li, Yuezhou Liu, Lili Su, Edmund Yeh, and Stratis Ioannidis. Experimental design networks: A paradigm for serving heterogeneous learners under networking constraints. IEEE/ACM Transactions on Networking, 2023.

- [26] Yucheng Liao, Yuanyu Wan, Chang Yao, and Mingli Song. Improved Projection-free Online Continuous Submodular Maximization. arXiv preprint arXiv:2305.18442, May 2023.

- [27] Zhou Lu, Nataly Brukhim, Paula Gradu, and Elad Hazan. Projection-free adaptive regret with membership oracles. In Proceedings of The 34th International Conference on Algorithmic Learning Theory, pages 1055–1073. PMLR, 2023.

- [28] Zakaria Mhammedi. Efficient projection-free online convex optimization with membership oracle. In Proceedings of Thirty Fifth Conference on Learning Theory, pages 5314–5390. PMLR, 2022.

- [29] Siddharth Mitra, Moran Feldman, and Amin Karbasi. Submodular+ concave. Advances in Neural Information Processing Systems, 2021.

- [30] Aryan Mokhtari, Hamed Hassani, and Amin Karbasi. Stochastic conditional gradient methods: From convex minimization to submodular maximization. The Journal of Machine Learning Research, 21(1):4232–4280, 2020.

- [31] Loay Mualem and Moran Feldman. Resolving the approximability of offline and online non-monotone DR-submodular maximization over general convex sets. In Proceedings of The 26th International Conference on Artificial Intelligence and Statistics, April 2023.

- [32] Rad Niazadeh, Negin Golrezaei, Joshua Wang, Fransisca Susan, and Ashwinkumar Badanidiyuru. Online learning via offline greedy algorithms: Applications in market design and optimization. Management Science, 69(7):3797–3817, July 2023.

- [33] Mohammad Pedramfar and Vaneet Aggarwal. A generalized approach to online convex optimization. arXiv preprint arXiv:2402.08621, 2024.

- [34] Mohammad Pedramfar, Yididiya Y. Nadew, Christopher John Quinn, and Vaneet Aggarwal. Unified projection-free algorithms for adversarial DR-submodular optimization. In The Twelfth International Conference on Learning Representations, 2024.

- [35] Mohammad Pedramfar, Christopher Quinn, and Vaneet Aggarwal. A unified approach for maximizing continuous -weakly DR-submodular functions. optimization-online preprint optimization-online:25915, 2024.

- [36] Mohammad Pedramfar, Christopher John Quinn, and Vaneet Aggarwal. A unified approach for maximizing continuous DR-submodular functions. In Thirty-seventh Conference on Neural Information Processing Systems, 2023.

- [37] Shai Shalev-Shwartz. Online learning and online convex optimization. Foundations and Trends® in Machine Learning, 4(2):107–194, 2012.

- [38] Zongqi Wan, Jialin Zhang, Wei Chen, Xiaoming Sun, and Zhijie Zhang. Bandit multi-linear dr-submodular maximization and its applications on adversarial submodular bandits. In International Conference on Machine Learning, 2023.

- [39] Yibo Wang, Wenhao Yang, Wei Jiang, Shiyin Lu, Bing Wang, Haihong Tang, Yuanyu Wan, and Lijun Zhang. Non-stationary projection-free online learning with dynamic and adaptive regret guarantees. Proceedings of the AAAI Conference on Artificial Intelligence, 38(14):15671–15679, 2024.

- [40] Bryan Wilder. Equilibrium computation and robust optimization in zero sum games with submodular structure. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 32, 2018.

- [41] Jiahao Xie, Zebang Shen, Chao Zhang, Boyu Wang, and Hui Qian. Efficient projection-free online methods with stochastic recursive gradient. Proceedings of the AAAI Conference on Artificial Intelligence, 34(4):6446–6453, 2020.

- [42] Lijun Zhang, Shiyin Lu, and Zhi-Hua Zhou. Adaptive online learning in dynamic environments. In Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc., 2018.

- [43] Lijun Zhang, Tianbao Yang, jin, and Zhi-Hua Zhou. Dynamic regret of strongly adaptive methods. In Proceedings of the 35th International Conference on Machine Learning, pages 5882–5891. PMLR, 2018.

- [44] Mingrui Zhang, Lin Chen, Hamed Hassani, and Amin Karbasi. Online continuous submodular maximization: From full-information to bandit feedback. In Advances in Neural Information Processing Systems, volume 32, 2019.

- [45] Qixin Zhang, Zengde Deng, Zaiyi Chen, Haoyuan Hu, and Yu Yang. Stochastic continuous submodular maximization: Boosting via non-oblivious function. In Proceedings of the 39th International Conference on Machine Learning, 2022.

- [46] Qixin Zhang, Zengde Deng, Zaiyi Chen, Kuangqi Zhou, Haoyuan Hu, and Yu Yang. Online learning for non-monotone DR-submodular maximization: From full information to bandit feedback. In Proceedings of The 26th International Conference on Artificial Intelligence and Statistics, April 2023.

- [47] Qixin Zhang, Zongqi Wan, Zengde Deng, Zaiyi Chen, Xiaoming Sun, Jialin Zhang, and Yu Yang. Boosting gradient ascent for continuous DR-submodular maximization. arXiv preprint arXiv:2401.08330, 2024.

- [48] Peng Zhao, Guanghui Wang, Lijun Zhang, and Zhi-Hua Zhou. Bandit convex optimization in non-stationary environments. Journal of Machine Learning Research, 22(125):1–45, 2021.

- [49] Peng Zhao, Yu-Jie Zhang, Lijun Zhang, and Zhi-Hua Zhou. Dynamic regret of convex and smooth functions. In Advances in Neural Information Processing Systems, volume 33, pages 12510–12520, 2020.

- [50] Martin Zinkevich. Online convex programming and generalized infinitesimal gradient ascent. In Proceedings of the 20th international conference on machine learning (icml-03), pages 928–936, 2003.

Appendix A Related works

DR-submodular maximization

Two of the main methods for continuous DR-submodular maximization are Frank-Wolfe type methods and Boosting based methods. This division is based on how the approximation coefficient appears in the proof.

In Frank-Wolfe type algorithms, the approximation coefficient appears by specific choices of the Frank-Wolfe update rules. (See Lemma 8 in [34]) The specific choices of the update rules for different settings have been proposed in [3, 2, 31, 36, 9]. The momentum technique of [30] has been used to convert algorithms designed for deterministic feedback to stochastic feedback setting. [18] proposed a Frank-Wolfe variant with access to a stochastic gradient oracle with known distribution. Frank-Wolfe type algorithms been adapted to the online setting using Meta-Frank-Wolfe [7, 8] or using Blackwell approachablity [32]. Later [44] used a Meta-Frank-Wolfe with random permutation technique to obtain full-information results that only require a single query per function and also bandit results. This was extended to another settings by [46] and generalized to many different settings with improved regret bounds by [34].

Another approach, referred to as boosting, is to construct an alternative function such that maximization of this function results in approximate maximization of the original function. Given this definition, we may consider the result of [19, 7, 12] as the first boosting based results. However, in these cases (i.e., the case of monotone DR-submodular functions over general convex sets), the alternative function is identical to the original function. The term boosting in this context was first used in [45] for monotone functions over convex sets containing the origin, based on ideas presented in [13, 29]. This idea was used later in [38, 26] in bandit and projection-free full-information settings. Finally, in [47] a boosting based method was introduced for non-monotone functions over general convex sets.

Up-concave maximization

Not all continuous DR-submodular functions are concave and not all concave functions are continuous DR-submodular. [29] considers functions that are the sum of a concave and a continuous DR-submodular function. It is well-known that continuous DR-submodular functions are concave along positive directions [5, 3]. Based on this idea, [40] defined an up-concave function as a function that is concave along positive directions. Up-concave maximization has been considered in the offline setting before, e.g. [24], but not in online setting. In this work, we focus on up-concave maximization which is a generalization of DR-submodular maximization.

Projection-free optimization

In the past decade, numerous projection-free online convex optimization algorithms have emerged to tackle the computational limitations of their projection-based counterparts [20, 6, 41, 8, 21, 15, 28, 16]. In the context of DR-submodular maximization, the Frank-Wolfe type methods discussed above are projection-free.

Non-stationary regret

Dynamic regret was first analyzed in [50] for first order deterministic feedback. Later [42] obtained the lower bound and optimal algorithm in this setting. This was later expanded to bandit setting in [48]. Adaptive regret was first analyzed in [22] and the first optimal algorithm for projection-free adaptive regret was proposed in [16]. We refer to [22, 1, 10, 43, 42, 49, 48, 27, 39, 16] and references therein for more details.

Optimization by quadratization

The framework discussed here for analyzing online algorithms is based on the convex optimization framework introduced in [33]. We extend the framework to allows us to work with -regret.Moreover, [33] also demonstrates that algorithms that are designed for quadratic/linear optimization with fully adaptive adversary obtain a similar regret in the convex setting. In this paper we introduce the notion of quadratizable functions generalizes this idea beyond convex functions to all quadratizable functions. (see Theorem 1) This allows us to integrate the boosting method with our framework to obtain various meta-algorithms for continuous DR-submodular maximization.

Appendix B Problem Setup in Detail

In this section, we further expand on the description in Section 2.

A function class is a set of real-valued functions. Given a set , a function class over is a subset of all real-valued functions on . A set is called a convex set if for all and , we have . For any , we define the path length

A real-valued differentiable function is called concave if , for all . More generally, given and , we say a real-valued differentiable function is -strongly -weakly concave if

for all .

We say a differentiable function is -strongly -weakly up-concave if it is -strongly -weakly concave along positive directions. Specifically if, for all in , we have

This notion could be generalized in the following manner. We say is a -strongly -weakly up-super-gradient of if for all in , we have

Then we say is -strongly -weakly up-concave if it is continuous and it has a -strongly -weakly up-super-gradient. When it is clear from the context, we simply refer to as an up-super-gradient for . When and the above inequality holds for all , we say is -strongly concave.

A differentiable function is called continuous DR-submodular if for all , we have . More generally, we say is -weakly continuous DR-submodular if for all , we have . It follows that any -weakly continuous DR-submodular functions is -weakly up-concave.

Given a continuous monotone function , its curvature is defined as the smallest number such that

for all and such that . 333 In the literature, the curvature is often defined for differentiable functions. When is differentiable, we have We define the curvature of a function class as the supremum of the curvature of functions in .

Online optimization problems can be formalized as a repeated game between an agent and an adversary. The game lasts for rounds on a convex domain where and are known to both players. In -th round, the agent chooses an action from an action set , then the adversary chooses a loss function and a query oracle for the function . Then, for , the agent chooses a points and receives the output of the query oracle.

To be more precise, an agent consists of a tuple , where is a probability space that captures all the randomness of . We assume that, before the first action, the agent samples . The next element in the tuple, is a sequence of functions such that that maps the history to where we use to denote range of the query oracle. The last element in the tuple, , is the query policy. For each and , is a function that, given previous actions and observations, either selects a point , i.e., query, or signals that the query policy at this time-step is terminated. We may drop as one of the inputs of the above functions when there is no ambiguity. We say the agent query function is trivial if and for all . In this case, we simplify the notation and use the notation to denote the agent action functions and assume that the domain of is .

A query oracle is a function that provides the observation to the agent. Formally, a query oracle for a function is a map defined on such that for each , the is a random variable taking value in the observation space . The query oracle is called a stochastic value oracle or stochastic zeroth order oracle if and . Similarly, it is called a stochastic up-super-gradient oracle or stochastic first order oracle if and is a up-super-gradient of at . In all cases, if the random variable takes a single value with probability one, we refer to it as a deterministic oracle. Note that, given a function, there is at most a single deterministic gradient oracle, but there may be many deterministic up-super-gradient oracles. We will use to denote the deterministic gradient oracle. We say an oracle is bounded by if its output is always within the Euclidean ball of radius centered at the origin. We say the agent takes semi-bandit feedback if the oracle is first-order and the agent query function is trivial. Similarly, it takes bandit feedback if the oracle is zeroth-order and the agent query function is trivial444This is a slight generalization of the common use of the term bandit feedback. Usually, bandit feedback refers to the case where the oracle is a deterministic zeroth-order oracle and the agent query function is trivial.. If the agent query function is non-trivial, then we say the agent requires full-information feedback.

An adversary is a set such that each element , referred to as a realized adversary, is a sequence of functions where each maps a tuple to a tuple where and is a query oracle for . We say an adversary is oblivious if for any realization , all functions are constant, i.e., they are independent of . In this case, a realized adversary may be simply represented by a sequence of functions and a sequence of query oracles for these functions. We say an adversary is a weakly adaptive adversary if each function described above does not depend on and therefore may be represented as a map defined on . In this work we also consider adversaries that are fully adaptive, i.e., adversaries with no restriction. Clearly any oblivious adversary is a weakly adaptive adversary and any weakly adaptive adversary is a fully adaptive adversary. Given a function class and , we use to denote the set of all possible realized adversaries with deterministic -th order oracles. If the oracle is instead stochastic and bounded by , we use to denote such an adversary. Finally, we use and to denote all oblivious realized adversaries with -th order deterministic and stochastic oracles, respectively.

In order to handle different notions of regret with the same approach, for an agent , adversary , compact set , approximation coefficient and , we define regret as

where the expectation in the definition of the regret is over the randomness of the algorithm and the query oracle. We use the notation when is a singleton. We may drop when it is equal to 1. When , we often assume that the functions are non-negative.

Static adversarial regret or simply adversarial regret corresponds to , and . When , and contains only a single element then it is referred to as the dynamic regret [50, 42]. Adaptive regret, is defined as [22]. We drop , and when the statement is independent of their value or their value is clear from the context.

Appendix C Proof of Theorem 1

The proof is similar to the proof of Theorems 2 and 5 in [33].

Proof.

Deterministic oracle:

We first consider the case where is a deterministic query oracle for . Let denote the output of at time-step . For any realization , we define to be the tuple where

and . Note that each is a deterministic function of and therefore . Since the algorithm uses semi-bandit feedback, the sequence of random vectors chosen by is identical between the game with and . Therefore, according to definition of quadratizable functions, for any , we have

Therefore, we have

| (4) |

Hence

Stochastic oracle:

Next we consider the case where is a stochastic query oracle for .

Let capture all sources of randomness in the query oracles of , i.e., for any choice of , the query oracle is deterministic. Hence for any and realized adversary , we may consider as an object similar to an adversary with a deterministic oracle. However, note that does not satisfy the unbiasedness condition of the oracle, i.e., the returned value of the oracle is not necessarily the gradient of the function at that point. Recall that maps a tuple to a tuple of and a stochastic query oracle for . We will use to denote the expectation with respect to the randomness of query oracle and to denote the expectation conditioned on the history and the action of the agent. Similarly, let denote the expectation with respect to the randomness of the agent. Let be the random variable denoting the output of at time-step and let

Similar to the deterministic case, for any realization and any , we define to be the pair where

We also define . Note that a specific choice of is necessary to make sure that the function returned by is a deterministic function of and not a random variable and therefore belongs to .

Since the algorithm uses (semi-)bandit feedback, given a specific value of , the sequence of random vectors chosen by is identical between the game with and . Therefore, for any , we have

where the first inequality follows from the fact that is up-quadratizable and . Therefore we have

Since is oblivious, the sequence is not affected by the randomness of query oracles or the agent. Therefore we have

where the second inequality follows from Jensen’s inequality. Hence we have

Appendix D Proof of Lemma 1

Proof.

We have . Therefore, following the definition of curvature, we have

Since is non-negative, this implies that

| (5) | ||||

On the other hand, according to the definition, we have

Therefore, using Inequality 5 and the fact that , we see that

where we used and

in the last equality. The claim now follows from multiply both sides by . ∎

Appendix E Proof of Lemma 2

Proof.

Clearly we have . For any , the integrand in the definition of is a continuous non-negative function of that is bounded by

Therefore is well-defined on . Moreover, we have555Note that we do not require the gradient to be defined everywhere for this equality to hold. It is sufficient for to exist at Lebesgue almost every point on every line segment. This is satisfied when the 1-dimensional Hausdorff measure of the set is zero.

It follows that is differentiable everywhere and . To prove the last claim, first we note that

On the other hand, using monotonicity and up-concavity of , we have

where we used in the last equality. Therefore

Appendix F Proof of Lemma 3

We start by stating a useful lemma from the literature.

Lemma 4 (Lemma 2.2 of [31]).

For any two vectors and any continuously differentiable non-negative DR-submodular function we have

Proof of Lemma 3.

Clearly we have . For any , the integrand in the definition of is a continuous function of that is bounded by

Therefore is well-defined on . Moreover, we have 666Similar to Lemma 2, we do not require the gradient to be defined everywhere for this equality to hold. It is sufficient for to exist at Lebesgue almost every point on every line segment. This is satisfied when the 1-dimensional Hausdorff measure of the set is zero.

It follows that is differentiable everywhere and .

Next we bound . We have

For the first term, we have

which implies that

| (7) |

Appendix G Proof of Theorem 6

The algorithms are special cases of Algorithms 2 and 3 in [33] where the shrinking parameter and the smoothing parameter are equal. We include a description of the algorithms for completion.

The proof of Theorem 6 is similar to the proof of Theorems 6 and 7 in [33]. The only difference being that we prove the result for -regret instead of regret. We include a proof for completion.

Proof.

Regret bound for :

Note that any realized adversary may be represented as a sequence of functions and a corresponding sequence of query oracles . For such realized adversary , we define to be the realized adversary corresponding to with the stochastic gradient oracles

| (8) |

where is a random vector, taking its values uniformly from , for any and . Since is a stochastic value oracle for , according to Remark 4 in [36], is an unbiased estimator of . 777When using a spherical estimator, it was shown in [14] that is differentiable even when is not. When using a sliced spherical estimator as we do here, differentiability of is not proved in [36]. However, their proof is based on the proof for the spherical case and therefore the results carry forward to show that is differentiable. Hence we have . Using Equation 8 and the definition of the Algorithm 6, we see that the responses of the queries are the same between the game and . It follows that the sequence of actions in corresponds to the sequence of actions in .

Let and . We have

| (9) |

According to Lemma 3 in [36], we have . By using Lipschitz property for the pair , we see that

| (10) |

On the other hand, we have

| (Lemma 3 in [36]) | ||||

| (Definition of ) | ||||

| (Lipschitz) | ||||

Therefore, using Equation 9, we see that

Therefore, we have

Regret bound for :

The proof of the bounds for this case is similar to the previous case. As before, we see that the responses of the queries are the same between the game and . It follows from the description of Algorithm 5 that the sequence of actions in corresponds to the same sequence of actions in .

Let and . We have

| (11) |

To obtain the same bound as before, instead of Inequality G, we have

The rest of the proof follows verbatim. ∎

Corollary 4.

Under the assumptions of Theorem 6, if we have and , then we have

Appendix H Proof of Theorem 7

Proof.

Given a realized adversary , we may define to be the realized adversary constructed by averaging each block of length . Specifically, if the functions chosen by are , the functions chosen by are for . Note that, for any and , we have and if each is differentiable at , then . If the query oracles selected by are , then for any we define the query oracle as the algorithm that first selects an integer with uniform probability and then returns the output of . It follows that is a query oracle for . It is clear from the description of Algorithm 4 that, when the adversary is , the output returned to the base algorithm corresponds to . We have . Hence

Therefore

Remark 1.

Note that in the above proof, we did not need to assume that the query oracles are bounded. Specifically, what we require is that the set of query oracles to be closed under convex combinations. This holds when all query oracles are bounded by , but it also holds under many other assumptions, e.g., if we assume all query oracles variances are bounded by some .

Corollary 5.

Under the assumptions of Theorem 7, if we have , and , then we have

As a special case, when , then we have

Proof.

We have

Appendix I Proof of Theorem 8

Proof.

Since requires queries per time-step, it requires a total of queries. The expected error is bounded by the regret divided by time. Hence we have after queries. Therefore, the total number of queries to keep the error bounded by is . ∎

Appendix J Projection-free adptive regret

The SO-OGD algorithm in [16] is a deterministic algorithm with semi-bandit feedback, designed for online convex optimization with a deterministic gradient oracle. Here we assume that the separation oracle is deterministic.

Here we use the notation , and described in Section 5.

Note that here we use a maximization version of the algorithm, which we denote by SO-OGA. Here denotes projection into the convex set . The original version, which is designed for minimization, uses the update rule in Algorithm 7 instead.

Lemma 5.

Algorithm 8 stops after at most iterations and returns such that , we have .

Proof.

We first note that this algorithm is invariant under translations. Hence it is sufficient to prove the result when .

Let denote the following separation oracle. If or , then returns the same output as . Otherwise, it returns where is the output of . To prove that this is indeed a separation oracle, we only need to consider the case where . We know that is a vector such that

Since is an orthogonal projection, we have

for all , which implies that is a separation oracle.

Now we see that Algorithm 8 is an instance of Algorithm 6 in [16] applied to the initial point using the separation oracle . Hence we may use Lemma 13 in [16] directly to see that Algorithm 8 stops after at most iterations and returns such that , we have Since is the projection of over , we see that Algorithm 8 stops after at most

steps and

In the following, we use the notation

to denote the adaptive regret.

Theorem 9.

Let be a class of linear functions over such that for all and let . Fix such that and set . Then we have

Proof.

Since the algorithm is deterministic, according to Theorem 1 in [33], it is sufficient to prove this regret bound against the oblivious adversary .

Note that this algorithm is invariant under translations. Hence it is sufficient to prove the result when . If , then we have and we may use Theorem 14 from [16] to obtain the desired result for the oblivious adversary . On the other hand, the assumption is only used in the proof of Lemma 13 in [16]. Here we use Lemma 5 instead which does not require this assumption. ∎

The following corollary is an immediate consequence of the above theorem and Theorems 2, 3, 4, 5, 8 and Corollaries 4 and 5.

Corollary 6.

Let SO-OGA denote the algorithm described above. Then the following are true.

-

a)

Under the assumptions of Theorem 2, we have:

- b)

-

c)

Under the assumptions of Theorem 4, we have:

where . Note that is a first order full-information algorithm that requires a single query per time-step. If we also assume is bounded by and , then

where

-

d)

Under the assumptions of Theorem 5, we have:

where . Note that is a first order full-information algorithm that requires a single query per time-step. If we also assume is bounded by and , then

where

Appendix K Dynamic regret

Improved Ader (IA) algorithm [42] is a deterministic algorithm with semi-bandit feedback, designed for online convex optimization with a deterministic gradient oracle.

In Algorithm 10, denotes projection into the convex set . Note that here we used the maximization version of this algorithm. The original version, which is designed for minimization, uses the update rule in Algorithm 10 instead.

Theorem 10.

Let be a class of linear functions over such that for all and let . Set where and . Then for any comparator sequence , we have

Proof.

If we use the oblivious adversary instead, this theorem is simply a restatement of the special case (i.e. when the functions are linear) of Theorem 4 in [42]. 888We note that although Theorem 4 in [42] assumes that the convex set contains the origin, this assumption is not really needed. In fact, for any arbitrary convex set, we may first translate it to contain the origin, apply Theorem 4 and then translate it back to obtain the results for the original convex set. Since the algorithm is deterministic, according to Theorem 1 in [33], the regret bound remains unchanged when we replace with . ∎

The following corollary is an immediate consequence of the above theorem and Theorems 2, 3, 4, 5, and Corollary 4.

Note that we do not use the meta-algorithm since Improved Ader is designed for non-stationary regret and does not offer any advantages in the offline case. On the other hand, we do not use the meta-algorithm in this case since Theorem 7 is only for the setting where the comparator is and does not allow us to convert bounds for dynamic regret.

Corollary 7.

Let IA denote “Improved Ader” described above. Then the following are true.

-

a)

Under the assumptions of Theorem 2, if is -Lipschitz, we have:

- b)

-

c)

Under the assumptions of Theorem 4, we have:

where . Note that is a first order full-information algorithm that requires a single query per time-step. If we also assume is bounded by and , then

where .

-

d)

Under the assumptions of Theorem 5, we have:

where . Note that is a first order full-information algorithm that requires a single query per time-step. If we also assume is bounded by and , then

where .