Specific Wasserstein divergence between continuous martingales

Abstract.

Defining a divergence between the laws of continuous martingales is a delicate task, owing to the fact that these laws tend to be singular to each other. An important idea, put forward by N. Gantert in [31], is to instead consider a scaling limit of the relative entropy between such continuous martingales sampled over a finite time grid. This gives rise to the concept of specific relative entropy. In order to develop a general theory of divergences between continuous martingales, it is only natural to replace the role of the relative entropy in this construction by a different notion of discrepancy between finite dimensional probability distributions. In the present work we take a first step in this direction, taking a power of the Wasserstein distance instead of the relative entropy. We call the newly obtained scaling limit the specific -Wasserstein divergence.

In our first main result we prove that the specific -Wasserstein divergence is well-defined, and exhibit an explicit expression for it in terms of the quadratic variations of the martingales involved. This is obtained under vastly weaker assumptions than the corresponding results for the specific relative entropy. Next we illustrate the usefulness of the concept, by considering the problem of optimizing the specific -Wasserstein divergence over the set of win-martingales. In our second main result we characterize the solution of this optimization problem for all and, somewhat surprisingly, we single out the case as the one with the best probabilistic properties. For instance, the optimal martingale in this case is very explicit and can be connected, through a space transformation, to the solution of a variant of the Schrödinger problem.

Key words and phrases:

Entropy, win-martingale, martingale optimal transport, Wasserstein distance, Schrödinger problem.1. Introduction

The aim of this paper is to introduce a novel notion of divergence between continuous martingales, and thereafter to fully study and solve divergence optimization problems over the set of win martingales (used as models for prediction markets [3]).

Identifying two real-valued continuous martingales as probability measures on the continuous path space

a natural choice for divergence would be the relative entropy

or its generalization, the -divergence . This naive approach leads to an immediate difficulty, namely, that the laws of continuous martingales tend to be singular to each other and hence have a trivial divergence in the above sense. As an example, the reader can consider to be respectively the laws of Brownian motion and two times the Brownian motion, and check that these measures are concentrated on disjoint sets.

A natural approach to circumvent this difficulty is to rather discretize the martingales in time, compare them at the discrete-time level, and then consider a (scaling) limit in which the time mesh-size goes to zero. This approach was introduced by Gantert in [31], and more recently refined by Föllmer in [28], leading to the notion of specific relative entropy between continuous martingales. The key in that construction is to use the conventional relative entropy when comparing the laws of the time-discretized martingales. In this article we introduce and study the specific Wasserstein divergence, obtained by considering a power of the Wasserstein distance instead of the relative entropy in the aforementioned scaling limit. This is hence a first step towards a general theory of divergences between continuous martingales.

1.1. Specific Wasserstein divergence

Denote throughout by the space of probability measures on a Polish space .

Given a function which only vanishes on the diagonal, we may interpret as the discrepancy between and . Inductively, after having defined , a discrepancy functional between elements in , then a natural choice for a discrepancy functional between elements in is given by

| (1.1) |

where is the projection of on the first coordinates, , is the conditional law of the -th marginal given the previous trajectory , with similar notations for and .

If now , a natural choice for a discrepancy functional between and is to take

assuming that the limit exists and that a universal scaling sequence has been found. Here and throughout we use the notation for the push-forward (i.e., image measure) of under the map

and likewise for .

We remark that (1.1) is akin to the time consistency property in the theory of dynamic risk measures (see Remark 2.4 below), and is very natural given the temporal structure of processes like martingales. Taking to be the relative entropy , the construction described so far gives rise (with ) to the specific relative entropy. Thus the specific relative entropy can be understood as the rate of increase of the relative entropy as the number of marginals taken into account increases.

In this paper, we will be concerned with the case

where is the celebrated Wasserstein- distance and is any positive real number. We call the resulting object the specific -Wasserstein divergence (though sometimes we omit to mention the parameter ), and denote it by . Moreover, we will only be concerned with continuous martingale laws throughout. As a side note, we remark that taking a different Wasserstein distance than would change very little the results in this paper.

We proceed to describe our first main result: Suppose is the law of a continuous martingale starting wlog. at 0 and admitting an absolutely continuous quadratic variation with density denoted by . Suppose that is the law of standard Brownian motion. In Theorem 2.9 we obtain the existence of the specific Wasserstein divergence together with its explicit formula

In fact, in Theorem 2.9 we can allow the law to be more general than the Wiener measure, e.g. it can come from the law of a martingale diffusion with a well-behaved volatility coefficient. One notable aspect of this result is that the assumptions needed are vastly weaker than the ones needed for the corresponding result in the case of the specific relative entropy. In particular, we can handle the situation where is the constant martingale (i.e., a Brownian motion with zero volatility), and more generally, certain cases where and may be singular to each other for every . We consider this result a first step towards building a general theory of divergences between continuous martingales, since unlike the case of the specific relative entropy, the construction here gives a whole family of divergences.

Related to the above main result, we recover in Proposition 2.16 a functional inequality by Föllmer [28] concerning (in our terminology) the specific Wasserstein divergence, specific relative entropy, and an adapted Wasserstein distance. Our proof method is based on Theorem 2.9 and different from the original approach by this author.

1.2. Optimization over win-martingales

The main application of the concept of specific Wasserstein divergence that we want to put forward in this paper, concerns a problem of optimization over the set of win-martingales. A continuous time martingale over time is called a win-martingale if it starts with a deterministic position and ends up at time 1 on either or . In other words, it transports at time to at time . Such martingales have been proposed as models of prediction markets (cf. [3]) and optimization problems over the set of win-martingales were proposed by Aldous [2].

Given a fixed initial position and , our aim is to optimize the specific Wasserstein divergence among all continuous win-martingales started at and admitting an absolutely continuous quadratic variation, whereby denotes the constant martingale. More specifically, we maximize for and minimize for . These optimization problems are related to the one in [7], wherein the specific relative entropy with respect to standard Brownian motion is minimized over this set of martingales. Similarly to this reference, we employ first order conditions to characterize in Proposition 3.3, via ordinary differential equations, the (Markovian) volatility coefficient of a candidate optimal martingale. Then, in Section 4, the optimality of the candidate is verified by making use of the associated HJB equation and stochastic analysis arguments. Hence we obtain semi-explicit solutions for a whole family of continuous-time martingale optimal transport problems (which cannot be transformed into an Skorokhod Embedding Problem), usually considered a difficult task.

We identify two cases where the solution to our problem is fully explicit. One is for , where the solution is a so-called Bass martingale (see [8, 10]). As this object is well studied we do not explore this case in any detail. The fully novel case is . In this setting the unique optimal win martingale solves the SDE

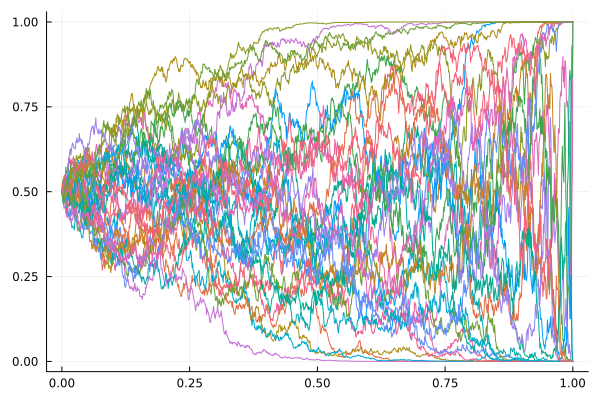

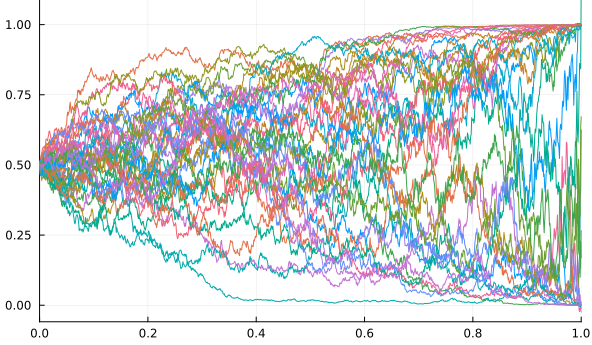

In order to provide some intuition, we provide some numerical simulations of the Bass martingale and . The reader may notice that the former tends to explore the space relatively faster than the latter. Indeed Lemma 3.6 below justifies that for each moment of time , the distribution of the Bass martingale is greater than that of in the sense of convex order.

If we stretch the time-index set from to in a natural way, the time-changed martingale admits the more amenable form

with a suitable Brownian motion. In this form, it can be readily interpreted in terms of filtering theory. Indeed, is precisely the conditional probability of the drift being equal to for a Brownian motion with an unobservable drift which can be either 0 or 1. Moreover the marginal distributions of and are fully explicit and simple to describe. This is in stark contrast to the situation in [7].

If we then perform a change of space-scale

so that the resulting process has unit volatility coefficient, it turns out that this process satisfies the SDE

This process can also be interpreted in a number of interesting ways. For instance the marginal laws of are a mixture between the marginal laws of a drifted Brownian motion with drift .

More interestingly, we have the following result, where we denote by the law of the Brownian bridge from 0 at time 0 to at time , and we define :

For every , the law restricted to converges as to the law of restricted to .

This result, which we formalize in Theorem 5.4, says that is precisely the law of Brownian motion conditioned on the event as . In other words, is a solution (more precisely, a limit of solutions) to the celebrated Schrödinger problem (see [43]). To the authors’ best knowledge, this is the first instance that a solution to a continuous martingale transport problem has been naturally connected to the solution of a likewise continuous Schrödinger problem.

1.3. Connections to the literature

The specific relative entropy was introduced and interpreted as a rate function by Gantert [31]. More recently [12] obtained an explicit formula for this quantity (between time-homogeneous Markov martingales), and Föllmer [28] extended Gantert’s results and established a Talagrand-type inequality between semimartingale laws using this object. In [7] the specific relative entropy was used to solve an open question by Aldous (see [33] for an alternative point of view and solution).

The adapted Wasserstein distance, appearing in the aforementioned Talagrand-type inequality by Föllmer, is a metric between stochastic processes that incorporates their temporal structure; see [6, 9, 13, 42] among others.

Win-martingales have been proposed as models for prediction markets (cf. [3]), and optimization problems over the set of win-martingales were proposed by Aldous [2] in connection to the aforementioned open question. Such optimization problems are particular instances of martingale optimal transport, a subject that has been extensively studied in the recent years. Following [36, 16, 22, 30] martingale versions of the classical transport problem (see e.g. [57, 58, 52, 27] for recent monographs) are often considered due to applications in mathematical finance but admit further applications, e.g. to the Skorokhod problem [15, 19]. In analogy to classical optimal transport, necessary and sufficient conditions for optimality have been established for martingale transport (MOT) problems in discrete time ([18, 20]) but not so much is known for the continuous time problem. Notable exceptions are [38, 55, 8, 10, 7, 33, 45, 34].

The Schrödinger problem has its origin in [53, 54]. In a nutshell, it asks for the most likely evolution for a large system of particles given initial and terminal configurations. By they theory of large deviation, this amounts to an entropy minimization problem. If the initial configuration is a point mass and the particles are Markovian, its solution is a Markov bridge [44]. We refer to Léonard’s survey [43] for a historical account and to the more contemporary articles [4, 21, 23, 24, 49] for recent contributions.

Finally we mention the work of Lacker [41], extended e.g. in [11, 26], wherein the idea of considering a scaling limit of problems in ever higher dimension is also considered. This is more related to a large deviations principle for a particle system whose size goes to infinity, rather than to our framework of a single process that we examine at ever finer resolution.

2. Specific Wasserstein divergence between martingales

2.1. Specific Wasserstein divergence

For Borel probability measures on a metric space we define their -Wasserstein distance

whereby and stands for the set of probability measures on with first marginal and second marginal . See [57, Chapter 7] for background. In case is Euclidean space we will always take to be the metric associated to the Euclidean norm.

In order to define a time-consistent divergence on , with the aforementioned one-dimensional Wasserstein distance as a building block, we proceed inductively. We shall employ the following notation throughout: If , then for and . Likewise if , then is the law of under and we denote . We write for the conditional law of under given the information of , and use the convention .

We fix and define:

Definition 2.1.

Suppose , then . For , supposing that are such that is well-defined -a.s. for each , then we define inductively

Unravelling the induction, we clearly have the equivalent expression

Remark 2.2.

In the definition of , the assumption that is well-defined -a.s. is necessary to integrate with respect to . One sufficient condition for this is that for any . Another sufficient condition is when is the law of a discrete-time Markov process which is uniquely defined by transition kernels which are defined everywhere.

Remark 2.3.

For , thanks to the convexity of , it follows that is also convex in . To see this, take wlog. and two probability distribution . Letting , it can be seen that has the disintegration

and hence

In the computation above, the crucial point is the convexity of , or more precisely, of . This is also the case for with , with denoting the -Wasserstein distance111Defined very much as , but with as the integrand and a power outside of the integral. . In order to keep the convexity of for any we choose in this work throughout, but we could have easily considered instead of .

Remark 2.4.

In this article, we are interested in the divergence between the distributions of two continuous martingales taking real values. Hence we consider the classical Wiener space

equipped with its natural Borel -algebra. We will denote throughout by the canonical process

and by its quadratic variation process. Since we will only be dealing with martingale laws, we do not need to refer to a reference measure in order to define the quadratic variation; see Remark 2.10 for more details.

Inspired by [31], we define the specific Wasserstein divergence as a scaling limit of the finite dimensional discrepancy . For any and , we denote by

the law projected on the time-grid .

Definition 2.5.

For any , we define the specific -Wasserstein divergence as

if is well-defined for all large enough . Otherwise we set it to .

As the following lemma shows, if denotes the law of Brownian motion started at with instantaneous variance / volatility , then we have

and hence

Importantly, this suggests that the scaling factor is the right one for our purposes.

We will need the following invariance property of the divergences :

Lemma 2.6.

Taking we have the following identity for any

Proof.

Note that can also be considered as a map from to when restricted to the first -coordinates, and hence is defined as . Since is a bijection, it can be seen that

and therefore due to the translation invariant property of Wasserstein distance,

Now by change of measure,

and our claim follows by induction. ∎

We will now fix a particular choice of martingale measure, , playing the role of a reference measure. The reader can think of as the law of Brownian motion, however the precise assumption that we need is as follows:

Assumptions 2.7.

Admit the existence of a jointly measurable function , such that is Lipschitz uniformly in and . We denote by the law of the solution of the SDE starting from , and if is fixed from the context we simply write .

Under Assumption 2.7, the conditional law is simply the distribution of where

In this case, is well-defined for any , and for any the divergence is well-defined .

Definition 2.8.

We denote by the set of continuous martingale laws with an absolutely continuous quadratic variation. The density of the quadratic variation will be denoted by .

Inspired by the developments on the particular case of the specific relative entropy [31, 12], we have our first main result:

Theorem 2.9.

Suppose with . Suppose that satisfies Assumption 2.7 with bounded volatility coefficient . Then the limit inferior in the definition of is an actual limit, and we have

If both are time-homogeneous with Lipschitz and uniformly positive bounded volatility (i.e., is Lipschitz and there exists a with for all ), then we have the -a.s. limit

| (2.1) | ||||

Proof.

Step 1: Let us first consider the case . With some abuse of notation, we denote by the conditional distribution of -th marginal of given the first coordinates. Then we obtain that

Taking , where , it can be seen that

and is only dependent on . Also we take for . Then by martingale convergence theorem and the continuity of , -a.s.

We approximate and by Gaussian distributions and ,

and then . Supposing that

| (2.2) |

it can be seen that

The last equality follows from martingale convergence, the dominated convergence theorem and the fact that , -a.s.

Step 2: It remains to verify (2.1), and we claim that

| (2.3) |

Thanks to the martingale representation theorem, on an extended filtered probability space , there exists a Brownian motion and an adapted process such that and , - Now is the law

while can be represented by the distribution

Therefore

| (2.4) |

provides a natural coupling between and , and hence using we get the upper bound

Integrating the above inequality over , one gets that

where we use BDG and Jensen’s inequalities. Therefore, we obtain that

| (2.5) |

Due to the martingale convergence theorem, with respect to norm, and hence is uniformly integrable. Therefore, it can be easily seen that in . As a result, the right hand side converges to as , and thus we verify (2.3).

Similarly, according to BDG and Jensen’s inequalities, it can be seen that

| (2.6) |

where is a constant depending on . In the same way,

Therefore, applying the inequality for , we get that

| (2.7) | ||||

Thanks to Hölder’s inequality, the first term on the right is bounded by

We have a similar estimate for the second term on the right, and hence due to (2.3) and (2.6), we conclude that

By the same reasoning, one can show that

and thus we verify (2.1).

Step 3: Now let us prove the result for . Thanks to the same coupling as in (2.4), we get that

where in the last inequality we use the concavity of over . Summing the above inequality over , and making use of

we obtain that

where the right hand side converges to since . Then by the same argument as in the case , we conclude the result.

Step 4: Finally, we prove (2.1) for the case and the argument for is the same. It is sufficient to estimate and apply Borel-Cantelli. Without loss of generality, we assume both and are nonnegative. For each and , we have

where in the last inequality we use the fact that . For the first term on the right, it follows from the definition of that

where we use boundedness and Lipschitz property of . Together with the inequality

we get the estimate

Remark 2.10.

Remark 2.11.

Taking to be a non-negative constant, say , Theorem 2.9 says

as promised in the introduction. Particularly natural are the choices , corresponding to standard Brownian motion, and , corresponding to the constant martingale.

Remark 2.12.

Let us discuss in detail how Theorem 2.9 relates to the literature. The only precursor that we are aware of is the case of the specific relative entropy. In that case, that a scaling limit of relative entropies is greater or equal than an explicit function of the quadratic variation, was already obtained by Gantert in [31, Satz 1.3] and subsequently refined in recent times by Föllmer in [28]. That equality can occur in that case, was obtained under strong assumptions in [12]. Compared to these results, we obtained the equality in Theorem 2.9 under assumptions that are vastly weaker. This is possible because controlling the error caused by approximating conditional distributions of over short time-intervals, by Gaussians measures with the same mean and variance, is significantly more demanding in the case of the relative entropy.

2.2. Relation between specific relative entropy and adapted Wasserstein distance

Let us provide the definition of specific relative entropy and adapted Wasserstein distance.

Definition 2.13.

Let be the relative entropy defined via with . Then the specific relative entropy is defined as the limit

With our methodology of defining divergences between processes in the introduction, is exactly equal to the limit of with . Suppose are martingale measures with volatility respectively. Then some strong conditions [12] obtains explicit formula

while in general the l.h.s. is the greater one ([31, Satz 1.3]).

Definition 2.14 (Bicausal coupling).

Let , be two probability distributions over . Then a probability measure is said to be a bicausal coupling between and if222We denote by the canonical process on .

-

(1)

, for all .

-

(2)

Causal from to : under , for all .

-

(3)

Causal from to : under , for all .

We denote the set of all bicausal couplings between and by .

The concept of bicausal coupling is a natural extension of coupling between probability distribution to the framework of stochastic processes, in which the filtration is a crucial component. See [42, 1] and the references therein for more on this concept. With this notion, one can define the so-called adapted Wasserstein distance between stochastic processes, which has been used in stability analysis for various stochastic optimization problems [51, 50, 9, 1, 5, 14].

Definition 2.15 ().

Letting be two distributions of martingales, define

With these ingredients we can state a chain of (in)equalities recently derived by Föllmer in [28]. Our proof method, based on time discretization, differs from that author’s approach.

Proposition 2.16.

Suppose and with . Then we have the (in)equalities

Proof.

To prove the first equality, it suffices to show that

Suppose . Thanks to the bicausal condition, is a martingale with respect to the filtration under . Then due to the martingale representation theorem, there exists two independent Brownian motions (perhaps in an enlarged probability space) such that

with constraints , -a.e. Then by Itô’s isometry,

where we use Cauchy-Schwartz in the last inequality. Moreover, it is clear that the equality is obtained when , , and .

Let us now prove the second inequality involving specific relative entropy invoking the well-known Talagrand inequality for standard Gaussian distribution [32, Theorem 1.5]

Recall that is the projection of on the time-grid , and the conditional distribution of the -th marginal of given the first coordinates. Then it is straightforward that

Letting and using Theorem 2.9, we get that .

∎

3. Optimal win-martingales

Win-martingales appear naturally as (idealized) models for prediction markets (cf. [3]). A win-martingale is supposed to track the probability of an event happening at time . Hence they are supposed to start with a known value in and terminate distributed as a Bernoulli random variable.

Optimization problems over the set of win-martingales were proposed by Aldous [2], and two such problems were solved in [7, 33].

3.1. Specific Wasserstein divergence optimization over win martingales

Given in convex order, martingale optimal transport problems in continuous-time often take the form:

| (3.1) |

where denotes the set of continuous martingale laws with an absolutely continuous quadratic variation, stands for the canonical process, and for the density of its quadratic variation. Martingale optimal transport problem is a variant of optimal transport in mathematical finance and is an essential tool for robust pricing and hedging; see e.g. [17, 25, 45, 34].

In this paper, we consider optimization problems among an important subclass of martingales, the so-called win-martingales. We write for the set of laws of continuous martingales with time-index set which have absolutely continuous quadratic variation and start in . The subset of win-martingales consist of those martingales in which terminate in either or . It is clear that the terminal distribution of such win-martingales is Bernoulli(.

Let . In (3.1), taking , , and , the martingale optimal transport problem can be interpreted as a specific Wasserstein divergence optimization problem. We are interested in solving for all333Except for the case , which is trivial in that every feasible martingale is optimal. :

| (3.2) |

whereby we recall that stands for the constant martingale (see Remark 2.11).

First we observe that the maximization problem is trivial in the case of (and the same for the minimization problem when ) as the following example reveals. Therefore when referring to , we solve the minimization problem if and the maximization problem if .

Example 3.1.

Fix , , and take an arbitrary . We construct a sequence of which is the distribution of

where is a continuous time process with distribution . Then it can be easily seen by Jensen’s inequality

and hence

3.2. Ansatz for the optimizer

In this subsection, we propose a candidate optimizer, and verify that it is indeed the unique optimizer in the next section. The key ingredient is a first order condition for MOT obtained in [7] but that we recall here for the convenience of the reader:

Lemma 3.2.

[First order condition for MOT on the line] Consider the MOT problem (3.1), and suppose that is differentiable in its last variable, that is an optimizer, and that

is a continuous -semimartingale. Then is a martingale under .

Suppose that the optimizers of are Markov diffusions with volatility function . Applying Lemma 3.2 to our case , being an optimizer implies that is a martingale, and hence due to Itô’s formula we get an equality

| (3.3) |

which is then equivalent to

where we take . This is precisely the porous media equation, and its explicit solutions can be found by separation of variables according to [56, Chapter 4]. This observation motivates us to consider of the form . The first order condition of being martingale yields that

which implies that Denoting , we get that an autonomous ODE

| (3.4) |

Solving (3.4) with boundary conditions , we obtain the following result

Proposition 3.3.

Fix . With the boundary condition , (3.3) has a nonnegative solution such that for

where is a unique positive constant (in particular , ). Furthermore we have that if , that if , and that only at .

Proof.

It is sufficient to solve (3.4). Multiplying (3.4) by and integrating w.r.t. , in the case that we obtain a new equation

Thanks to the boundary condition , we could guess that for all and hence .

In the case that , and therefore at . Noting that , we choose so that

where we change the variable . Since is finite, there exists a unique so that the above equality holds, and in the case of one can easily get . Therefore, we obtain that

which implicitly provides a solution to (3.4) over , and we can extend the solution symmetrically to .

In the case that , , and by a similar argument the solution is implicitly given by

where and is the unique positive solution of

If we have instead

Solving , we get , and therefore

where is the unique positive solution of

In the end, noticing that and , we obtain the results by direct computation.

∎

So for every , we have a candidate win martingale

| (3.5) | ||||

where is the unique solution in Proposition 3.3 for the given parameter . Applying [40, Theorem 5.5.7] to the time-scaled martingale with , the above SDE admits a unique weak solution on . Observe that, for , if then also for all since . In particular then we have a.s. Hence the martingale is bounded in for every and in particular exists a.s. and in . Thus and , hence also

and in particular a.s. We conclude that the event is negligible since on this event .

Let us also take . According to (3.3), is a local martingale. Due to Proposition 3.3, is uniformly bounded over and hence is a true martingale for any .

We summarize the discussion above:

Lemma 3.4.

is well-defined on the whole interval , it is a continuous martingale bounded in every , and it satisfies a.s. (implying that ). Furthermore, the process is also a martingale on .

Remark 3.5.

Let us discuss some explicit solutions, end how these compare to each other. As we discuss in detail in Section 5, one can verify that satisfies (3.3) and Proposition 3.3 with , which gives rise to the SDE

In the case of , the volatility function given by Proposition 3.3 yields a win martingale , which is a particular case of a so-called Bass martingale [8, 10]. Indeed, these authors consider the problem of maximizing over martingales satisfying initial and terminal distributional constraints. Explicitly, with the cdf of the centred Gaussian with variance .

At the end of this section, we justify a claim in the introduction: At each moment of time , the distribution of the Bass martingale , is more spread out in space than the distribution of . Actually, we can say more. Recalling the Aldous martingale defined in [7] through the SDE

we prove that

| (3.6) |

The Aldous martingale is characterized by the fact that , and this can be obtained as the formal limit of (3.3) as . Hence it can be considered as a limiting optimal win-martingale in our context. We proceed to justify (3.6).

A few computation yields that the volatility function of is bounded from above by that of , i.e., over . Then thanks to [37, Theorem 2.1], the first inequality follows. In the following lemma, we prove the second inequality:

Lemma 3.6.

For , it holds that

It follows that is dominated by in the convex order for any , .

Proof.

Recall that and for some functions . It suffices to show that for . By Proposition 3.3, we obtain derivatives of

Equivalently, consider and as inverse functions of and ,

Notice that , and thus the domain of is contained in that of . Therefore in order to show for fixed , it is equivalent to prove that for fixed . Given the explicit derivatives above, it can be easily verified that for . Since , we conclude , which together with [37, Theorem 2.1] completes the proof.

∎

4. Verification of optimality

In this section, we verify that the candidate martingale is the optimizer for in (3.1) (maximizer for and minimizer for ). Associated to the martingale we define its cost

| (4.1) |

where the second equality is due to Lemma 3.4 and Fubini’s theorem.

Lemma 4.1.

For ( ), is the unique maximizer (minimizer ) of the function

Proof.

We only prove the result for the case , and the argument for is similar. Due to (3.4) and , it can be seen that

As is regular, local maximums are obtained at either boundaries or stationary points. Then the first order condition yields that

Solving the equality above, we get the stationary point Noticing that , , , obtains its unique maximizer at .

∎

With the result above, we can now verify that the function satisfies the HJB equation of optimization problem (3.1) strictly before time .

Lemma 4.2.

On , we have that for ,

and in the case that ,

Proof.

Before implementing the verification argument. We would like to mention that the proof for is subtler than for .

Let us introduce the value function of the minimization problem

where denotes the set of distributions of continuous win-martingales over time that starts with at time . Similarly as in Example 3.1, by Jensen’s inequality we have as for . Therefore the terminal condition of value function at is irregular. It implies that the natural terminal condition for its HJB equation

is given by

Although it is degenerate parabolic, little is known, to the authors’ knowledge, due to the irregular boundary condition.

To carry out the verification argument, we want to show that for any feasible martingale with volatility , the process is a sub-martingale. Since is uniformly bounded for , it is a sub-martingale before time as shown in Lemma 4.3. So it reduces to the question whether as for all admissible martingales . The answer is affirmative due to the estimate in Lemma 4.4.

In the rest of this section, we first provide two technical lemmas for the case , and then prove the main result in both cases.

Lemma 4.3.

Fix . Let be feasible for our minimization problem (started from at time 0), and denote by the square root of the density of its quadratic variation. Then the process

is a submartingale on .

Proof.

By Lemma 4.2 we have

from which, thanks to Itô formula, the local submartingale property of follows. The local martingale part of is given by the stochastic integration

Thanks to Proposition 3.3, is uniformly bounded over for and hence is square-integrable over . Therefore the stochastic integral is indeed a martingale and it concludes the result. ∎

Lemma 4.4.

Fix . Let us introduce

Then there exist two positive constants such that

| (4.2) |

Proof.

Given any feasible martingale starting from at time , we have by Jensen’s inequality that

Thanks to Doob’s martingale inequality and BDG inequality, the last term on the right is bounded from below by

where is some positive constant. Therefore due to the definition of value function, we obtain the last inequality of (4.2).

We can now carry on the verification argument, showing the optimality of :

Theorem 4.5.

For , the unique optimizer of (3.1) is .

Proof.

Step 1: . Given any feasible martingale (started from at time ), denote by the square root of the density of its quadratic variation. Due to Lemma 4.2,

and therefore is a local super-martingale. Since it is also nonnegative, thanks to Fatou’s lemma is a true super-martingale. Therefore we conclude that

Step 2: . Let be any feasible martingale that starts from at time and . Invoking Lemma 4.4, we get that

which indicates that . According to Lemma 4.3, for any we have

and hence we conclude the result by letting .

Step 3: Uniqueness. We close this theorem by showing the uniqueness of optimizers to Problem (3.1): As the previous proofs show, the only way for to be optimal is by making

be equal to zero. By Lemma 4.1 this is only achieved by .

∎

Remark 4.6.

In the case of , we observe that the optimal win martingale is also the unique solution of the maximization problem

where denotes the set of laws of continuous martingale over time which have absolutely continuous quadratic variation and start at at time . Compared with (3.1), this problem relaxes the constraint of the terminal distribution being , by allowing early termination before time in case the martingale tries to leave the interval , and otherwise permitting an arbitrary distribution at time .

Indeed, by a standard argument, it can be verified that the value function is the unique bounded viscosity solution of its corresponding HJB equation

which is solved by the value of the optimal win martingale . Therefore the same argument as in Theorem 4.5 completes our claim.

Actually, this maximization problem is an analogue of [33], i.e., we take as the objective function instead of the cost considered in [33]. Moreover given the logarithm as objective function, results of [33] imply that allowing early termination makes the optimization problem different. Precisely, the maximizer of

is different from that of

In contrast, as justified above, when the objective function is , our win martingale is optimal no matter if possible early termination is allowed or not.

The verification argument of this section follows the lines of the corresponding argument in [7]. We stress here some differences: Due to the different choice of cost functionals, the candidate value function in [7] tends to near the boundary and in our framework () explodes near terminal time . Therefore in order to finish the verification argument, [7] estimated with uniformly for all admissible martingales , while we make use of a uniform estimate of for .

5. The intriguing case of

In this section, we discuss an intriguing case when . Recall that in the case , and hence according to Theorem 4.5 the SDE

is the unique maximizer of

Remark 5.1.

Now we scale time so that instead of we work on . Defining we find that

| (5.1) |

where is a Brownian motion on . In the following, we will give two interpretations of through the lenses of the Schrödinger problem and filtering theory.

5.1. Connection with the Schrödinger problem

Let and define with as above. Then according to Itô’s formula, solves the SDE

and the drift process is a martingale. The latter is the first order condition of the Schrödinger problem of entropy minimization w.r.t. Wiener measure subject to fixed initial and terminal distributions; see [4, Proposition 3.2] with the potential function . We can in fact justify that the law of is precisely the law of Brownian motion conditioned to as . This is, to the best of our knowledge, the first time that a natural connection between continuous-time MOT and the Schrödinger problem appears. By contrast, the works [35] in continuous-time, and [48, 47] in discrete-time, also deal with martingale transport and so-called Schrödinger bridges, but the connection between the two subjects is forced by design.

Lemma 5.2.

Let be the unique strong solution with of the SDE

where is a Brownian motion started likewise at . Then for we have

Proof.

We denote by the canonical process and by the probability measure so that is a Brownian motion started at . Let

Since , and , we also have by Ito’s formula

where we used that . By Girsanov theorem and the uniqueness of the SDE for , we have that the law of is equal to the law of under , where . ∎

Remark 5.3.

It follows from this lemma that, if , then

i.e. that has the same marginal laws as the simple mixture of two Brownian motions with drifts . This connection had already been observed in [46]. We can readily get the explicit density of (and ) from this.

For simplicity of presentation we assume here that , corresponding to the case . Fixing and , we consider the law of the Brownian bridge starting at at time and finishing at at time with equal probabilities. On this law is absolutely continuous w.r.t. Wiener measure started at , which we have denoted . In fact, if is the density of w.r.t. restricted to , i.e. , then where after a few calculations we find

| (5.2) |

Indeed, one can justify that

from which (5.2) follows. Hence, if we send , we obtain

According to Lemma 5.2 this is precisely the density of w.r.t. . In words:

The law of is the limit, as , of the law at time of Brownian motion conditioned to be at time .

In fact more is true. We first compute

and remember that is the drift of under . Indeed, since is a martingale under , we have

and hence where .

Therefore by Girsanov’s theorem is a Brownian motion under , i.e., the drift of is given by . We notice that this drift converges to as , which is precisely the drift of under the law of . In this sense we can say, as already mentioned in the introduction, that

On every fixed interval , the law of restricted to converges as to the law of restricted to .

More precisely, we prove the following:

Theorem 5.4.

Fix . Let us denote the law of and restricted to by and respectively. Then we have as . As a corollary, converges to in total variation.

Proof.

According to the discussion above, and are distributions of SDEs

where , are Brownian motions under and respectively. Then according to Girsanov’s theorem,

and hence

Noting that is bounded, is square integrable under , so an application of the dominated convergence theorem completes the first claim. The second claim follows by Pinsker’s inequality. ∎

Now we are ready to explain the connection to the classical Schödinger problem. A simple version of the latter is as follows: Given , the Schödinger problem looks for minimizers of

Recall the tensorization property of relative entropy , i.e., where is the disintegration w.r.t. the time marginal and is the conditioning law of Brownian motion that ends up with at time . Hence in the case that , the minimizer of corresponding Schödinger problem is uniquely given by for . Therefore the conditioning of Brownian motion is akin to the classical Schrödinger problem, and this points to an intriguing connection between martingale optimal transport and Schrödinger problems. Indeed taking and , then is the limit of solutions as . Another way to stress this is to recall that the drift of , namely , is a martingale, and recalling that this would be precisely the first order optimality condition for the optimizer of the Schrödinger problem.

5.2. and a filtering problem

Recall that fulfills

for and . In fact can be interpreted from the lens of filtering theory as we now explain.

Let denote Wiener measure, i.e. the law of Brownian motion, while is the law of Brownian motion with drift 1. Now denote on . In other words this is the law of a process that can be either Brownian motion without drift or with drift equal to 1, depending on an independent random variable. Finally denote by the canonical process on , and its filtration. Then the stochastic process

satisfies the SDE of , i.e. is equal in law to . Indeed, Girsanov theorem shows that

So with . A few computations show that and . Thus

where for the second equality we used that , where is some Brownian motion adapted to under . Indeed, this follows from the fact that , valid for , which shows that is a martingale in the aforementioned filtration.

References

- [1] B. Acciaio, J. Backhoff-Veraguas, and A. Zalashko. Causal optimal transport and its links to enlargement of filtrations and continuous-time stochastic optimization. Stochastic Processes and their Applications, 130(5):2918–2953, 2020.

- [2] D. Aldous. What is the max-entropy win-probability martingale? https://www.stat.berkeley.edu/aldous/Research/OP/maxentmg.html.

- [3] D. J. Aldous. Using prediction market data to illustrate undergraduate probability. Amer. Math. Monthly, 120(7):583–593, 2013.

- [4] J. Backhoff, G. Conforti, I. Gentil, and C. Léonard. The mean field Schrödinger problem: ergodic behavior, entropy estimates and functional inequalities. Probability Theory and Related Fields, 178(1):475–530, 2020.

- [5] J. Backhoff-Veraguas, D. Bartl, M. Beiglböck, and M. Eder. Adapted Wasserstein distances and stability in mathematical finance. Finance Stoch., 24(3):601–632, 2020.

- [6] J. Backhoff-Veraguas, D. Bartl, B. Mathias, and E. Manu. Adapted Wasserstein distances and stability in mathematical finance. Finance and Stochastics, 24(3):601–632, 2020.

- [7] J. Backhoff-Veraguas and M. Beiglböck. The most exciting game. Electronic Communications in Probability, 29(none):1 – 12, 2024.

- [8] J. Backhoff-Veraguas, M. Beiglböck, M. Huesmann, and S. Källblad. Martingale Benamou–Brenier. The Annals of Probability, 48(5):2258–2289, 2020.

- [9] J. Backhoff-Veraguas, M. Beiglbock, Y. Lin, and A. Zalashko. Causal transport in discrete time and applications. SIAM Journal on Optimization, 27(4):2528–2562, 2017.

- [10] J. Backhoff-Veraguas, M. Beiglböck, W. Schachermayer, and B. Tschiderer. The structure of martingale BenamouBrenier in . arXiv:2306.11019, June 2023.

- [11] J. Backhoff-Veraguas, D. Lacker, and L. Tangpi. Nonexponential Sanov and Schilder theorems on Wiener space: BSDEs, Schrödinger problems and control. Ann. Appl. Probab., 30(3):1321–1367, 2020.

- [12] J. Backhoff-Veraguas and C. Unterberger. On the specific relative entropy between martingale diffusions on the line. Electron. Commun. Probab., 28:Paper No. 37, 12, 2023.

- [13] D. Bartl, M. Beiglböck, and G. Pammer. The Wasserstein space of stochastic processes. arXiv:2104.14245, Apr. 2021.

- [14] D. Bartl and J. Wiesel. Sensitivity of multiperiod optimization problems with respect to the adapted wasserstein distance. SIAM Journal on Financial Mathematics, 14(2):704–720, 2023.

- [15] M. Beiglböck, A. Cox, and M. Huesmann. Optimal transport and Skorokhod embedding. Invent. Math., 208(2):327–400, 2017.

- [16] M. Beiglböck, P. Henry-Labordère, and F. Penkner. Model-independent bounds for option prices: A mass transport approach. Finance Stoch., 17(3):477–501, 2013.

- [17] M. Beiglböck and N. Juillet. On a problem of optimal transport under marginal martingale constraints. Ann. Probab., 44(1):42–106, 2016.

- [18] M. Beiglböck and N. Juillet. Shadow couplings. Trans. Amer. Math. Soc., 374(7):4973–5002, 2021.

- [19] M. Beiglböck, M. Nutz, and F. Stebegg. Fine properties of the optimal Skorokhod embedding problem. J. Eur. Math. Soc. (JEMS), 24(4):1389–1429, 2022.

- [20] M. Beiglböck, M. Nutz, and N. Touzi. Complete duality for martingale optimal transport on the line. Ann. Probab., 45(5):3038–3074, 2017.

- [21] J.-D. Benamou, G. Carlier, S. Di Marino, and L. Nenna. An entropy minimization approach to second-order variational mean-field games. Math. Models Methods Appl. Sci., 29(8):1553–1583, 2019.

- [22] B. Bouchard and M. Nutz. Arbitrage and duality in nondominated discrete-time models. Ann. Appl. Probab., 25(2):823–859, 2015.

- [23] Y. Chen, T. T. Georgiou, and M. Pavon. On the relation between optimal transport and Schrödinger bridges: a stochastic control viewpoint. J. Optim. Theory Appl., 169(2):671–691, 2016.

- [24] G. Conforti. A second order equation for Schrödinger bridges with applications to the hot gas experiment and entropic transportation cost. Probab. Theory Related Fields, 174(1-2):1–47, 2019.

- [25] Y. Dolinsky and H. M. Soner. Martingale optimal transport and robust hedging in continuous time. Probab. Theory Related Fields, 160(1-2):391–427, 2014.

- [26] S. Eckstein. Extended laplace principle for empirical measures of a markov chain. Advances in Applied Probability, 51(1):136–167, 2019.

- [27] A. Figalli and F. Glaudo. An invitation to optimal transport, Wasserstein distances, and gradient flows. EMS Textbooks in Mathematics. EMS Press, Berlin, 2021.

- [28] H. Föllmer. Optimal couplings on Wiener space and an extension of Talagrand’s transport inequality. In Stochastic analysis, filtering, and stochastic optimization, pages 147–175. Springer, Cham, [2022] ©2022.

- [29] H. Föllmer and I. Penner. Convex risk measures and the dynamics of their penalty functions. Statistics & Risk Modeling, 24(1):61–96, 2006.

- [30] A. Galichon, P. Henry-Labordère, and N. Touzi. A stochastic control approach to no-arbitrage bounds given marginals, with an application to lookback options. Ann. Appl. Probab., 24(1):312–336, 2014.

- [31] N. Gantert. Einige grosse Abweichungen der Brownschen Bewegung. Bonner mathematische Schriften. Mathematischen Institut der Universität, 1991.

- [32] N. Gozlan and C. Léonard. Transport inequalities. A survey. Markov Process. Related Fields, 16(4):635–736, 2010.

- [33] G. Guo, S. D. Howison, D. Possamaï, and C. Reisinger. Randomness and early termination: what makes a game exciting? arXiv:2306.07133, June 2023.

- [34] I. Guo and G. Loeper. Path dependent optimal transport and model calibration on exotic derivatives. The Annals of Applied Probability, 31(3):1232–1263, 2021.

- [35] P. Henry-Labordere. From (martingale) Schrödinger bridges to a new class of stochastic volatility model. Available at SSRN 3353270, 2019.

- [36] D. Hobson and A. Neuberger. Robust bounds for forward start options. Math. Finance, 22(1):31–56, 2012.

- [37] D. G. Hobson. Volatility misspecification, option pricing and superreplication via coupling. Annals of Applied Probability, pages 193–205, 1998.

- [38] M. Huesmann and D. Trevisan. A Benamou–Brenier formulation of martingale optimal transport. Bernoulli, 25(4A):2729 – 2757, 2019.

- [39] R. L. Karandikar. On pathwise stochastic integration. Stochastic Processes and their applications, 57(1):11–18, 1995.

- [40] I. Karatzas and S. E. Shreve. Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991.

- [41] D. Lacker. A non-exponential extension of Sanov’s theorem via convex duality. Advances in Applied Probability, 52(1):61–101, 2020.

- [42] R. Lassalle. Causal transport plans and their Monge–Kantorovich problems. Stochastic Analysis and Applications, 36(3):452–484, 2018.

- [43] C. Léonard. A survey of the Schrödinger problem and some of its connections with optimal transport. Discrete Contin. Dyn. Syst., 34(4):1533–1574, 2014.

- [44] C. Léonard, S. Rœ lly, and J.-C. Zambrini. Reciprocal processes. A measure-theoretical point of view. Probab. Surv., 11:237–269, 2014.

- [45] G. Loeper. Option pricing with linear market impact and nonlinear Black–Scholes equations. The Annals of Applied Probability, 28(5):2664–2726, 2018.

- [46] M. Montero. Merge of two oppositely biased Wiener processes. arXiv e-prints, page arXiv:2303.18088, Mar. 2023.

- [47] M. Nutz and J. Wiesel. On the martingale Schrödinger bridge between two distributions. arXiv preprint arXiv:2401.05209, 2024.

- [48] M. Nutz, J. Wiesel, and L. Zhao. Martingale Schrödinger bridges and optimal semistatic portfolios. Finance and Stochastics, 27(1):233–254, 2023.

- [49] S. Pal and T.-K. L. Wong. Multiplicative Schrödinger problem and the Dirichlet transport. Probab. Theory Related Fields, 178(1-2):613–654, 2020.

- [50] G. Pflug. Version-independence and nested distributions in multistage stochastic optimization. SIAM Journal on Optimization, 20(3):1406–1420, 2009.

- [51] G. Pflug and A. Pichler. A distance for multistage stochastic optimization models. SIAM Journal on Optimization, 22(1):1–23, 2012.

- [52] F. Santambrogio. Optimal transport for applied mathematicians, volume 87 of Progress in Nonlinear Differential Equations and their Applications. Birkhäuser Cham, 2015. Calculus of variations, PDEs, and modeling.

- [53] E. Schrödinger. Über die umkehrung der naturgesetze. Sitzungsberichte der Preussischen Akademie der Wissenschaften. Physikalisch-mathematische Klasse, 1931.

- [54] E. Schrödinger. Sur la théorie relativiste de l’électron et l’interprétation de la mécanique quantique. Ann. Inst. H. Poincaré, 2(4):269–310, 1932.

- [55] X. Tan and N. Touzi. Optimal transportation under controlled stochastic dynamics. The annals of probability, pages 3201–3240, 2013.

- [56] J. L. Vázquez. The porous medium equation. Oxford Mathematical Monographs. The Clarendon Press, Oxford University Press, Oxford, 2007. Mathematical theory.

- [57] C. Villani. Topics in optimal transportation. Number 58. American Mathematical Soc., 2003.

- [58] C. Villani. Optimal transport: old and new, volume 338. Springer Science & Business Media, 2008.