Dominance between combinations of infinite-mean Pareto random variables

Abstract

We study stochastic dominance between portfolios of independent and identically distributed (iid) extremely heavy-tailed (i.e., infinite-mean) Pareto random variables. With the notion of majorization order, we show that a more diversified portfolio of iid extremely heavy-tailed Pareto random variables is larger in the sense of first-order stochastic dominance. This result is further generalized for Pareto random variables caused by triggering events, random variables with tails being Pareto, bounded Pareto random variables, and positively dependent Pareto random variables. These results provide an important implication in investment: Diversification of extremely heavy-tailed Pareto profits uniformly increases investors’ profitability, leading to a diversification benefit. Remarkably, different from the finite-mean setting, such a diversification benefit does not depend on the decision maker’s risk aversion.

Keywords: Pareto distributions; portfolio diversification; first-order stochastic dominance; majorization order.

1 Introduction

Pareto distributions are ubiquitous for modeling heavy-tailed phenomena in diverse fields; see Andriani and McKelvey, (2007) for over 80 applications of Pareto distributions. Their applications in economics, finance, and insurance can be found in, e.g., Arnold, (2015), McNeil et al., (2015) and Ibragimov et al., (2015). In practice, many large profits or losses modelled by Pareto distributions exhibit extremely heavy tails, leading to infinite first moments. Examples include financial returns from some technological innovations (Silverberg and Verspagen, , 2007), catastrophic losses (Ibragimov et al., 2009; Hofert and Wüthrich, , 2012), and operational losses (Moscadelli, , 2004). A list of empirical examples of infinite-mean Pareto models is summarized by Chen et al. (2024b).

Diversification is a fundamental concept in finance and economics, pioneered by Markowitz (1952). At a high level, when it comes to decision making in portfolio selection, it is commonly agreed that risk-averse agents (in the sense of Rothschild and Stiglitz (1970)) would prefer more diversification, whereas risk-seeking agents do not like diversification; e.g., Samuelson, (1967) and Fama and Miller, (1972). Such results are typically formulated for finite-mean models of investment payoffs, but for infinite-mean models, notions of risk aversion and risk seeking, which rely on expected utility functions, may not behave well and can be difficult to interpret. Intriguing or even counter-intuitive results may be obtained for infinite-mean models, as recently studied by Chen et al. (2024a).

This paper focuses on the portfolio diversification of extremely heavy-tailed, i.e., infinite-mean, Pareto random variables. For two random variables and , we say that is smaller than in first-order stochastic dominance, denoted by , if for all . First-order stochastic dominance is the strongest commonly used stochastic dominance ordering. For iid extremely heavy-tailed Pareto random variables and a nonnegative vector , Chen et al. (2024a) showed

| (1) |

Intuitively, (1) suggests that a diversified portfolio of iid extremely heavy-tailed Pareto random variables has a larger tail probability than a non-diversified portfolio. If represent profits, then any decision maker consistent with will choose the diversified portfolio represented by over the non-diversified one represented by . The situation will be completely flipped if represent losses; the non-diversified portfolio is now preferred. Therefore, whether agents are risk-averse or not does not matter for the decision, but whether the infinite-mean random variables represent gains or losses matters.

There is a clear limitation of (1): It only allows for the comparison of a general portfolio with a completely non-diversified portfolio. To understand decisions in portfolio selection, one needs to compare a portfolio with another one, possibly also diversified, but to a lesser extent. This problem was not addressed by the results of Chen et al. (2024a). Thus, we answer the following question in this paper: What is the stochastic dominance relation between two different diversified portfolios of iid extremely heavy-tailed Pareto random variables?

Let and be the exposure vectors of the two portfolios such that is smaller than in majorization order (see Section 2 for the definition of majorization order). This implies that the two vectors have equal total exposures (i.e., ), making it fair to compare the two portfolios. Moreover, the components of a smaller vector in majorization order are less “spread out”; that is, the components of are closer to each other than those of . Therefore, it is natural to consider the portfolio with exposure vector as more diversified than that with exposure vector . One of our main results, presented in Section 2, is the following inequality

| (2) |

Inequality (2), in the sense of the strongest form of risk comparison, shows that a more diversified portfolio of iid extremely heavy-tailed Pareto random variables leads to a larger tail probability. Note that (2) includes (1) as a special case.

In Section 3, we generalize (2) into several models that can be more relevant in different settings. In particular, in Theorem 2, extremely heavy-tailed Pareto random variables are assumed to be caused by triggering events, which usually happen with small probabilities. Proposition 3 considers iid random variables whose tails follow an extremely heavy-tailed Pareto distribution. Proposition 5 studies extremely heavy-tailed Pareto distributions with an upper bound. Theorem 3 deals with extremely heavy-tailed Pareto random variables that are positively dependent and modelled by a Clayton copula.

The implications of (2) in investment decisions are discussed in Section 4. As expected, for agents making investments whose profits are iid extremely heavy-tailed Pareto random variables, diversification uniformly improves their preferences as long as the preferences are monotone and well-defined. In particular, they do not need to be risk averse. As such improvements are strict, the optimal investment strategy is to assign an equal weight to each investment in the portfolio. This strategy, known as the rule, is also optimal for risk-averse expected utility agents if the profits have finite mean. On the other hand, if the random variables represent losses, then the optimal decision is the opposite, as implied by (1). Section 5 concludes the paper.

There are some studies on the diversification of extremely heavy-tailed random variables (see, e.g., Embrechts et al., (2002) and Ibragimov, (2009)), and most of their findings concern how diversification affects the spreadness of portfolios and thus are different from (2). Although (1) is a special case of (2), our technical results are quite different from those of Chen et al. (2024a). First, the results in the latter paper do not address the comparison between diversified portfolios with different weight vectors, and thus they are weaker than ours when formulated with the same dependence assumption. Our proofs are distinct from Chen et al. (2024a) and rely on analysis of majorization order and probabilistic inequalities. On the other hand, Chen et al. (2024a) showed (1) under some form of negative dependence. It remains unclear whether our main results can be generalized to accommodate negative dependence, due to distinct mathematical techniques used in the proofs. Instead, we establish a result under a specific form of positive dependence in Section 3.4. Another related result is obtained by Ibragimov, (2005), which implies that (2) holds for iid positive one-sided stable random variables with infinite mean. The techniques of Ibragimov, (2005) rely on properties of stable distributions, which are very different from ours, as Pareto distributions do not belong to that class.

We conclude this section by fixing some notation. Throughout, random variables are defined on an atomless probability space . Denote by the set of all positive integers and the set of non-negative real numbers. For , write . For vectors and , their dot product is . For , denote by . For , write , , and . We write for . For a random variable with distribution , its quantile is defined as

In this paper, terms like “increasing” and “decreasing” are in the non-strict sense.

2 Diversification of iid Pareto random variables

2.1 Majorization order

For , the Pareto distribution is specified by the cumulative distribution function

The parameter is a scale parameter (i.e., for , we have ) and is the tail parameter. The mean of is infinite if and only if . Clearly, it suffices to consider the distribution which we write as . We say that the distribution is extremely heavy-tailed if , and it is moderately heavy-tailed if . A profit or loss that follows a distribution will be referred to as Pareto profit or Pareto loss, respectively.

We recall the notions of -transform and majorization order from Marshall et al. (2011).

Definition 1.

Let and be two vectors in .

-

(i)

is a -transform of if for some and with ,

(3) and for .

-

(ii)

is dominated by in majorization order, denoted by , if and

where and represent the th smallest order statistics of and , respectively. We write if and .

The lemma below will be used to establish our main result.

Lemma 1.

(Marshall et al., 2011, Section 1.A.3) For , if and only if can be obtained from by a finite number of -transforms.

Clearly, for with , the components of are less “spread out” than those of . For instance,

Therefore, if and are the exposure vectors of two portfolios, the portfolio with exposure vector is considered to be more diversified than the one with exposure vector .

2.2 Main result

For , denote its increasing rearrangement by . For random variables and , we write if for all satisfying , and this will be referred to as strict stochastic dominance.111This condition is stronger than a different notion of strict stochastic dominance defined by and . In the following lemma, we first compare portfolios of two independent extremely heavy-tailed Pareto random variables with possibly different tail parameters.

Lemma 2.

Let be a vector of independent components with for where . For satisfying , we have . Moreover, if , then .

Proof.

Without loss of generality, assume that and is a -transform of . Write and . As is a -transform of , we have . Let for . Then, there exist such that for . For the first statement on stochastic dominance, it suffices to show that, for ,

| (4) |

We first derive the distribution function of . For any ,

Similarly, we have

Let . For , define

To prove (4), we need to show for any . It suffices to show that is increasing in . The derivative of is

Thus, it suffices to prove

Since , we need to show that for . Note that by . Thus,

This means that is decreasing, and hence for . It is clear that ) is strictly increasing in for . Hence, the strict inequality in the second assertion of the lemma is obtained. ∎

Now, using Lemmas 1 and 2 and the fact that first-order stochastic dominance is closed under convolution (e.g., Theorem 1.A.3 (b) of Shaked and Shanthikumar (2007)), we obtain the following theorem for independent extremely heavy-tailed Pareto random variables.

Theorem 1.

Let be a vector of independent components with for all where . For satisfying , we have . Moreover, if , then . In particular, if , we have when and when .

Proof.

By Lemma 1 in Ma (1998), there exists a finite number of vectors , which is an increasing rearrangement of , , such that

where is a -transform of for each . Hence, it suffices to show that holds for being a -transform of . Suppose that and such that . Take as in (3) such that is a -transform of . By Lemma 2, we have . As first-order stochastic dominance is closed under convolutions and for , we obtain

Moreover, let and

for which the density function is denoted by . For , we have

where the inequality follows from the strictness statement in Lemma 2, i.e., . ∎

Note that Pareto distributions with smaller tail indices are larger in first-order stochastic dominance. In the case that the Pareto random variables have non-identical tail indices, Theorem 1 means that if we shift exposures from extremely heavy-tailed Pareto random variables with larger tail indices to those with smaller tail indices, the portfolio gets larger in first-order stochastic dominance.

For the rest of the paper, we will mainly focus on the case of identically distributed Pareto random variables, to get concise results and to separate the effect of diversification from the effect of marginal distributions.

Theorem 1 shows that a portfolio of iid extremely heavy-tailed Pareto random variables with a smaller exposure vector in majorization order is larger in first-order stochastic dominance. This implies a diversification benefit: A more diversified portfolio of iid extremely heavy-tailed Pareto profits is strictly preferred; the strictness of the diversification benefit is crucial for the optimal investment decisions of agents (see Section 4). Several generalizations of Theorem 1 are studied in Section 3.

2.3 Further discussions

We first present a simple corollary on comparing iid portfolios with different sizes. Write for . By noting that

the following result directly follows from Theorem 1.

Corollary 1.

For , let be a vector of iid random variables with . For with , we have .

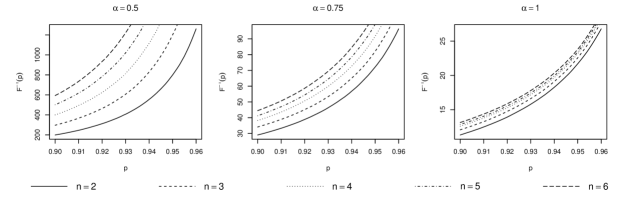

Corollary 1 means that the more components in a portfolio of iid extremely heavy-tailed Pareto profits, the more benefit we have from diversification. For , , and iid random variables , denote by the distribution function of . We plot for in Figure 1. The difference between the curves for different becomes more pronounced as becomes smaller, i.e., the tail of the Pareto random variables becomes heavier.

The assumption of an extremely heavy tail is necessary for Theorem 1 in the iid case, which is made clear by the following proposition, with its proof provided in the appendix.

Proposition 1.

Suppose that such that , and is a vector of iid random variables with finite mean. The inequality cannot hold unless is degenerate.

Proposition 1 suggests that first-order stochastic dominance is not able to compare portfolios of iid finite-mean random variables. A more suitable notion of stochastic dominance in this case is second-order stochastic dominance. For two random variables and , is smaller than in second-order stochastic dominance, denoted by , if for all increasing and concave functions , provided that the expectations exist. The relation means that is “less variable” than . The following result directly follows from Theorem 3.A.35 of Shaked and Shanthikumar (2007).

Proposition 2.

Let be a vector of iid Pareto random variables with tail parameter . For satisfying , we have .

Proposition 2 means that diversification of iid Pareto random variables with finite mean makes the portfolio less “spread out”, and thus less risky in the sense of Rothschild and Stiglitz (1970). This observation is distinct from Theorem 1, which suggests that diversification makes a portfolio “larger” if the Pareto random variables are extremely heavy-tailed. Implications of Theorem 1 and Proposition 2 for investors are discussed in Section 4.

Remark 1 (Generalized Pareto distributions).

As a pillar of the Extreme Value Theory, the Pickands-Balkema-de Haan Theorem (Balkema and de Haan, , 1974; Pickands, , 1975) states that the generalized Pareto distributions are the only possible non-degenerate limiting distributions of the excess of random variables beyond a high threshold. The generalized Pareto distribution for is defined as

where ( corresponds to an exponential distribution) and ; see Embrechts et al. (1997). If , then does not have finite mean. As a generalized Pareto distribution for can be converted to by a location-scale transform, Theorem 1 can be equivalently stated for the generalized Pareto distribution with .

Remark 2 (Extremely heavy-tailed Pareto sum).

We say an extremely heavy-tailed Pareto sum is a random variable where , , are independent, , , and . Let be a vector of iid extremely heavy-tailed Pareto sum random variables, and satisfy . Then . This can be shown by applying Theorem 1 (ii) to iid copies of each and using the fact that convolution preserves first-order stochastic dominance.

Remark 3.

Let and be independent with such that . For such that , it is natural to consider whether the following statement is true

| (5) |

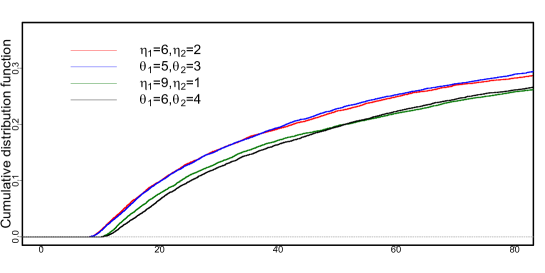

Fix and . In Figure 2, we plot the empirical distribution functions of and for two cases: and . Based on our numerical result, (5) does not seem to hold, although we do not have a proof.

3 Extensions of Theorem 1

In this section, to further understand how diversification works for extremely heavy-tailed Pareto random variables, we generalize Theorem 1 to several models. Specifically, in Section 3.1, we study Pareto random variables caused by events with a low probability of occurrence. Section 3.2 considers non-negative random variables whose tail region follows a Pareto distribution. A result regarding Pareto distributions with an upper bound is given in Section 3.3. Finally, Section 3.4 examines the case of positively dependent Pareto random variables using a stochastic representation of Pareto distributions.

3.1 Triggering event

Extremely heavy-tailed phenomenons are often triggered by events with very small probabilities of occurrence. For instance, profits from technology breakthroughs and losses caused by severe catastrophes can be extremely heavy-tailed. In this context, it is natural to model the outcome of a rare event as where is a Pareto random variable and is the triggering event independent of (i.e., given the occurrence of event , the outcome has a Pareto distribution). Let be iid Pareto random variables with , and be the respective triggering events of such that are independent of . Let .

If , then represent different outcomes caused by the same triggering event. For satisfying , we obtain from Theorem 1 the following stochastic inequality:

The theorem below shows that the above inequality also holds for any events with an equal probability of occurrence and an arbitrary dependence.

Theorem 2.

Let be iid random variables with , and be events with equal probability, which are independent of . Suppose that , . For satisfying , we have .

Proof.

We assume without losing generality. Below, we first show the case that . For , let , where . It suffices to show that is increasing in . Let . If , for all . If , . If , we have

As , . Then, if , we have

Take such that . Using the fact that , it is clear that if . If ,

Hence, is increasing on if . If , we have

By Lemma 2, it is clear that is strictly increasing on if . Hence, we have the result for .

Next, we show the result for . By Lemma 1, it suffices to show that holds for being a -transform of . Write and . Take such that and is a -transform of . For , let . For , we write

It is clear that

By Theorem 1, we have

Note that

Then

For , let denote the density of . For , we have

The above inequality is obtained by applying the result for on mutually exclusive events. Hence, we have the result for . ∎

3.2 Pareto tails

In practice, random variables may not follow Pareto distributions in their entire support, whereas they have power-like distributions beyond some high thresholds (implied by the Pickands-Balkema-de Haan Theorem; see, e.g., Theorem 3.4.13 (b) in Embrechts et al. (1997)). Therefore, it is practically useful to assume that a random variable has a Pareto distribution only in the tail region. For , we say that has a Pareto() distribution beyond if for and .

Proposition 3.

Let be a vector of iid random variables beyond with . For satisfying , we have for .

Proof.

We assume that without losing generality. Below, we show the case that . For , let where . It suffices to show that is increasing as increases. Denote by the probability measure of and . We have

For , let

Fix and . For , let

Taking the second derivative of , we have

Therefore, is concave, which implies that is increasing on . Hence, is increasing on .

In the realm of insurance, excess-of-loss reinsurance is frequently used, i.e., only losses beyond some high threshold are covered. Proposition 3 leads to the following corollary.

Corollary 2.

Let be iid random variables with , and satisfy .

-

(i)

Let where . Then . Moreover, if , then .

-

(ii)

Let where . Then . Moreover, if , then .

Proof.

The statement (i) is a special case of Proposition 3, and (ii) is obtained from (i) by shifting locations of the random variables in (i). ∎

For the end of this subsection, we have the following Proposition 4 regarding the case of different marginals.

Proposition 4.

Let be a vector with independent components such that for , where such that . Consider where , and satisfying . Then . Moreover, if , then for .

Proof.

We assume that without losing generality. Below, we show the case that . For , let where . It suffices to show that is increasing as increases. If , for all . If , we have

For , let

Taking the derivative of , and noting that for and , we have

where the last inequality follows from the fact that the function is increasing in . Therefore, is strictly increasing on .

3.3 Bounded Pareto random variables

Next, we consider random variables modeled by extremely heavy-tailed Pareto distributions with an upper bound. For , let , where are iid Pareto random variables with . For satisfying , by Proposition 1, does not hold. However, the following proposition shows that the tail probability of still dominates that of if the upper bound is large enough.

Proposition 5.

Fix such that and with . Let . Let be iid random variables with and with . Then for .

Proof.

Let . If there is at least one with , then . Thus, for ,we have

Let . As Hence, we also have . By Theorem 1, we have the desired result. ∎

Proposition 5 implies that if the upper bound is large enough (e.g., the total wealth in an economy), a more diversified portfolio of extremely heavy-tailed Pareto random variables can dominate a less diversified one in the sense of tail probability in a large region.

3.4 Positive dependence

So far, all results require independence among the components of . Chen et al. (2024a) obtained results also under a notion of negative dependence. Our techniques for proving Theorem 1 do not generalize to negative dependence, but we are able to obtain some results under a specific form of positive dependence. See, e.g., Puccetti and Wang (2015) for concepts of positive and negative dependence, including comonotonicity, which we will mention in passing below.

We consider the case that Pareto random variables are positively dependent via a common shock. Let , , denote the distribution function of a gamma random variable with density for . Note that a Pareto random variable , , has the following stochastic representation

where and are independent (see, e.g., Lemma 1 of Sarabia et al., (2016)).

Let and , , be independent. Consider a multivariate Pareto distribution with parameter , denoted by , of which the associated random vector has the stochastic representation below

| (6) |

Clearly, are positively dependent as they are all affected by the common shock ; if , for (see p. 155 of Sarabia et al., (2016)). The distribution of is the Type II multivariate Pareto distribution; see Arnold, (2015). The survival copula 222Joint distributions of uniform random variables over are known as copulas; see Nelsen (2006) for an introduction. associated with is the Clayton copula with parameter , given by

The Clayton copula approaches independence as goes to and it approaches comonotonicity as goes to .

Theorem 3.

Let with and . For satisfying , we have .

Remark 4 (Feller-Pareto distribution).

Remark 5 (Mixture dependence).

Let the components of be identically distributed Pareto random variables with tail parameter . It is clear that the inequality holds if are comonotonic (i.e., perfectly positively dependent). Therefore, by Theorems 1 and 3, also holds if the dependence structure (i.e., copula) of is a mixture of independence, comonotonicity, and the Clayton copula with parameter .

4 Investment implications

Suppose that an agent needs to decide on several investments whose profits are iid Pareto random variables. Let be the set of all random variables. The agent is equipped with a preference function where is a set of random variables representing profits. The agent prefers over if and only if . For the rest of our discussions, we make minimal assumptions of monotonicity on in the following two forms.

-

(a)

Weak monotonicity: for if .

-

(b)

Mild monotonicity: is weakly monotone and if .

The two assumptions are satisfied by all commonly used preference models. As a classic example, the expected utility model in decision analysis, denoted by , is defined as

where the utility function is measurable, and typically assumed to be increasing. Here, for to be well-defined, it can be infinite. Clearly, is weakly monotone and is mildly monotone if is strictly increasing. An expected utility agent is risk averse if is concave, in the sense of Rothschild and Stiglitz (1970). The following result shows that risk-averse expected utility agents always prefer a more diversified portfolio of iid Pareto profits, regardless of the tail parameter .

Proposition 6.

Let be a vector of iid Pareto random variables and be an increasing and concave function. For satisfying , we have .

Proof.

Let be the tail parameter of the iid Pareto random variables. As has nonnegative components, and are always well-defined. If , the result directly follows from Theorem 1 as is weakly monotone. If , we have by Proposition 2. Through the definition of second-order stochastic dominance, as is increasing and concave, we have the desired result. ∎

For an expected utility decision maker, we can observe a sharp contrast between finite-mean and infinite-mean models. Consider a decision maker with preference function . For a random vector , we say that pro-diversification holds if for all satisfying . Intuitively, this means that the decision maker likes more diversification.

Theorem 4.

Consider an expected utility decision maker with a utility function .

-

(i)

Pro-diversification holds for all iid with finite mean if and only if is concave.

-

(ii)

Pro-diversification holds for all iid with two-point marginals if and only if is concave.

-

(iii)

Pro-diversification holds for all iid with marginals for if is increasing.

Proof.

If is concave, then by Theorem 3.A.35 of Shaked and Shanthikumar (2007), if for all iid with finite mean, and thus pro-diversification holds. This shows the “if” direction of (i). Suppose that pro-diversification holds for , where each of and takes values with probability. We have , yielding , which implies concavity by Sierpiński’s Theorem on mid-point concavity. This shows the “only if” direction of (ii). The “only if” direction of (i) and the “if” direction of (ii) are implied by the above two shown directions. Statement (iii) follows directly from Theorem 1. ∎

Theorem 4 clarifies the fact that pro-diversification for finite-mean models is a result of risk aversion, but for infinite-mean Pareto models it is not related to risk aversion. As far as we are aware, this observation is new to the literature. Infinite-mean Pareto distributions can be used to model profits from technological innovations (Silverberg and Verspagen, (2007)). Our result can explain the widely observed diversified investment in many start-up firms by venture capital firms, which are, intuitively, not necessarily risk averse.

Other useful preference models are risk measures in the sense of Artzner et al. (1999) and Föllmer and Schied (2016). Almost all distortion risk measures are mildly monotone; see Proposition A.1 of Chen et al. (2024b) for the precise statement.

The rest of this section focuses on extremely heavy-tailed Pareto random variables. Note that some preference models may give value in the presence of extremely heavy tailedness and are thus not useful in this case; Chen et al. (2024b) listed some useful decision models in evaluating infinite-mean random variables.

A mapping on is Schur-concave (resp. Schur-convex) if (resp. ) for . We speak of strict Schur-concavity by replacing both inequalities above as strict inequalities. From now on, is assumed to contain the convex cone of Pareto random variables with . As implied by Theorem 1, a more diversified portfolio of iid extremely heavy-tailed Pareto random variables is more likely to be large. The following result directly follows from Theorem 1.

Proposition 7.

Let be a vector of iid random variables with and . The mapping on is Schur-concave if is weakly monotone, and it is strictly Schur-concave if is mildly monotone.

For , let be the th column vector of the identity matrix. The above result says that, for any weakly monotone risk measure , and such that and ,

The above inequalities are strict if is mildly monotone and . We emphasize the importance of the strict inequalities to decision makers below.

Suppose that an agent wants to allocate their exposures onto to maximize their preference. The agent faces a total position where the function represents a penalty and it is Schur-convex. The agent has one of the following optimization problems:

-

(p1)

maximize subject to and with given ,

-

(p2)

maximize subject to .

The following proposition follows from the strictness statement of Theorem 1.

Proposition 8.

Let be mildly monotone and . Then the maximizer to (p1) is , and the set of maximizers to (p2) is in .

5 Conclusion

We show that a more diversified portfolio (i.e., the exposure vector is smaller in majorization order) of iid extremely heavy-tailed Pareto random variables is greater than a less diversified one in the sense of first-order stochastic dominance (Theorem 1). This result is generalized to several cases: (i) Pareto random variables are caused by triggering events (Theorem 2); (ii) tail region of random variables are Pareto (Proposition 3); (iii) Pareto random variables are bounded (Proposition 5); (iv) Pareto random variables are positively dependent (Theorem 3). The implications of Theorem 1 for monotone agents making investment decisions are discussed in Section 4, showing that in our setting, preference for portfolio diversification does not necessarily require the decision maker to be risk averse, in sharp contrast to the case of finite-mean models.

Although our main result is generalized to several classes of models, all techniques rely heavily on the specific power form of the Pareto distribution functions, and they do not seem to easily generalize to other infinite-mean distributions. Extension beyond the models in the current paper requires separate future research.

Appendix A Appendices

A.1 Proof of Proposition 1

Proof of Proposition 1.

Write and . Since and , we have that and are identically distributed.

Let be the first component of . If has finite variance, denoted by , then by using , we have . Since , this implies .

In case does not have finite second moment, we can use a strictly convex function given by . Since for , the two expectations and are finite and equal. In view of Lemma 1, it suffices to consider the case that is a -transform of . In this case, since , there exist such that and and . Note that

where . For all distinct, due to strict convexity of , we have

Moreover, we have

Using the equality in expectation and independence between , we know that and cannot take distinct values, and they must be degenerate. ∎

A.2 Feller-Pareto random variables

For , , and , a random variable is called a Feller-Pareto random variable if it has the following stochastic representation,

where and , , are independent. We write . Note that if ; we refer to Arnold, (2015) for distributional properties of the Feller-Pareto family.

The class of Fell-Pareto distributions is very general and it includes Pareto distribution Type I (), Pareto distribution Type II (), Pareto distribution Type III (), and Pareto distribution Type IV (). Clearly, Pareto distributions Type I, II, and III are contained in the class of Pareto distributions Type IV with distribution function

The Feller-Pareto family also includes distributions that are distinctly non-Paretian in their tails; see, e.g., (3.2.17) of Arnold, (2015). For our study, as first-order stochastic dominance is location invariant, it suffices to consider the case and and we write .

Let and , , be independent. Define a random vector via the stochastic representation below

| (A.1) |

Then follows a multivariate Feller-Pareto distribution, denoted by , with common margins . Clearly, are positively dependent as they are all affected by the common shock . Similar to , includes special cases of multivariate Pareto distributions, from Type I to IV; the parameters are chosen analogously to the univariate case.

Theorem A.1.

Suppose that satisfy . Let , and . Then .

Proof.

We write where and are independent. Let . For , we have

where , . Next, we show is concave. Assume for simplicity. Taking the second derivative of , we get

As , and hence is concave. For two random variables and , we say is smaller than in the convex order, denoted by , if for all convex functions provided that the expectations exist. By Theorem 3.A.35 of Shaked and Shanthikumar (2007), since are iid, By the concavity of ,

The proof is done. ∎

Funding

T. Hu would like to acknowledge financial support from National Natural Science Foundation of China (No. 72332007, 12371476). R. Wang is supported by the Natural Sciences and Engineering Council of Canada (RGPIN-2024-03728; CRC-2022-00141). Z. Zou is supported by the Postdoctoral Fellowship Program of CPSF (GZC20232556).

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Andriani and McKelvey, (2007) Andriani, P. and McKelvey, B. (2007). Beyond Gaussian averages: Redirecting international business and management research toward extreme events and power laws. Journal of International Business Studies, 38(7):1212–1230.

- Arnold, (2015) Arnold, B. C. (2015). Pareto Distributions. Second Edition. CRC Press, New York.

- Artzner et al. (1999) Artzner, P., Delbaen, F., Eber, J.-M. and Heath, D. (1999). Coherent measures of risk. Mathematical Finance, 9(3):203–228.

- Balkema and de Haan, (1974) Balkema, A. and de Haan, L. (1974). Residual life time at great age. Annals of Probability, 2(5):792–804.

- Chen et al. (2024a) Chen, Y., Embrechts, P. and Wang, R. (2024a). An unexpected stochastic dominance: Pareto distributions, dependence, and diversification. Operations Research, forthcoming.

- Chen et al. (2024b) Chen, Y., Embrechts, P. and Wang, R. (2024b). Risk exchange under infinite-mean Pareto models. arXiv:2403.20171.

- Cont et al. (2010) Cont, R., Deguest, R. and Scandolo, G. (2010). Robustness and sensitivity analysis of risk measurement procedures. Quantitative Finance, 10(6):593–606.

- Embrechts et al. (1997) Embrechts, P., Klüppelberg, C. and Mikosch, T. (1997). Modelling Extremal Events for Insurance and Finance. Springer, Heidelberg.

- Embrechts et al., (2002) Embrechts, P., McNeil, A. and Straumann, D. (2002). Correlation and dependence in risk management: properties and pitfalls. In Risk Management: Value at Risk and Beyond (Eds: Dempster), pp. 176–223, Cambridge University Press.

- Fama and Miller, (1972) Fama, E. F. and Miller, M. H. (1972). The Theory of Finance. Dryden Press, Hinsdale.

- Filipović and Svindland, (2012) Filipović, D. and Svindland, G. (2012). The canonical model space for law-invariant convex risk measures is . Mathematical Finance, 22(3):585–589.

- Föllmer and Schied (2016) Föllmer, H. and Schied, A. (2016). Stochastic Finance: An Introduction in Discrete Time. Fourth Edition. Walter de Gruyter, Berlin.

- Hofert and Wüthrich, (2012) Hofert, M. and Wüthrich, M. V. (2012). Statistical review of nuclear power accidents. Asia-Pacific Journal of Risk and Insurance, 7(1), Article 1.

- Ibragimov, (2005) Ibragimov, R. (2005). New majorization theory in economics and martingale convergence results in econometrics. Ph.D. Dissertation, Yale University, New Haven, CT.

- Ibragimov, (2009) Ibragimov, R. (2009). Portfolio diversification and value at risk under thick-tailedness. Quantitative Finance, 9(5):565–580.

- Ibragimov et al., (2015) Ibragimov, M., Ibragimov, R. and Walden, J. (2015). Heavy-Tailed Distributions and Robustness in Economics and Finance. Springer Cham.

- Ibragimov et al. (2009) Ibragimov, R., Jaffee, D. and Walden, J. (2009). Non-diversification traps in markets for catastrophic risk. Review of Financial Studies, 22(3):959–993.

- Ma (1998) Ma, C. (1998). On peakedness of distributions of convex combinations. Journal of Statistical Planning and Inference, 70(1):51-56.

- Markowitz (1952) Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1):77–91.

- Marshall et al. (2011) Marshall, A. W., Olkin, I. and Arnold, B. (2011). Inequalities: Theory of Majorization and Its Applications, 2nd edition. Springer, New York.

- McNeil et al., (2015) McNeil, A. J., Frey, R. and Embrechts, P. (2015). Quantitative Risk Management: Concepts, Techniques and Tools. Revised edition. Princeton University Press.

- Moscadelli, (2004) Moscadelli, M. (2004). The modelling of operational risk: Experience with the analysis of the data collected by the Basel committee. Technical Report 517. SSRN:557214.

- Nelsen (2006) Nelsen, R. (2006). An Introduction to Copulas. Second Edition. Springer, New York.

- Pickands, (1975) Pickands, J. (1975). Statistical inference using extreme order statistics. Annals of Statistics, 3(1):119–131.

- Puccetti and Wang (2015) Puccetti, G. and Wang R. (2015). Extremal dependence concepts. Statistical Science, 30(4):485–517.

- Rothschild and Stiglitz (1970) Rothschild, M. and Stiglitz, J. E. (1970). Increasing risk: I. A definition. Journal of Economic Theory, 2(3):225–243.

- Samuelson, (1967) Samuelson, P. A. (1967). General proof that diversification pays. Journal of Financial and Quantitative Analysis, 2(1):1–13.

- Sarabia et al., (2016) Sarabia, J. M., Gómez-Déniz, E., Prieto, F. and Jordá, V. (2016). Risk aggregation in multivariate dependent Pareto distributions. Insurance: Mathematics and Economics, 71:154–163.

- Shaked and Shanthikumar (2007) Shaked, M. and Shanthikumar, J. G. (2007). Stochastic Orders. Springer, New York.

- Silverberg and Verspagen, (2007) Silverberg, G. and Verspagen, B. (2007). The size distribution of innovations revisited: An application of extreme value statistics to citation and value measures of patent significance. Journal of Econometrics, 139(2):318–339.

- Yaari (1987) Yaari, M. E. (1987). The dual theory of choice under risk. Econometrica, 55(1):95–115.