Inference for the panel ARMA–GARCH model when both and are large111The codes for the numerical analysis are accessible at https://github.com/subingGitHub/Codes-for-panel-ARMA-GARCH-model.

Abstract. We propose a panel ARMA–GARCH model to capture the dynamics of large panel data with individuals over time periods. For this model, we provide a two-step estimation procedure to estimate the ARMA parameters and GARCH parameters stepwisely. Under some regular conditions, we show that all of the proposed estimators are asymptotically normal with the convergence rate , and they have the asymptotic biases when both and diverge to infinity at the same rate. Particularly, we find that the asymptotic biases result from the fixed effect, estimation effect, and unobservable initial values. To correct the biases, we further propose the bias-corrected version of estimators by using either the analytical asymptotics or jackknife method. Our asymptotic results are based on a new central limit theorem for the linear-quadratic form in the martingale difference sequence, when the weight matrix is uniformly bounded in row and column. Simulations and one real example are given to demonstrate the usefulness of our panel ARMA–GARCH model.

Keywords: ARMA specification; Asymptotic bias; Central limit theorem; Fixed effects; GARCH specification; Large dynamic panel; Linear-quadratic form; Two-step estimation

1 Introduction

The dynamic panel model is a valuable statistical tool for analyzing panel data and investigating the dynamic relationships between variables, making it useful in various fields such as economics, finance, and social sciences. See Baltagi (2021) and Hsiao (2022) for its surveys. Let be a pair of observations for individual unit at time point , where and . Here, is the number of cross-sectional units and is the number of time periods. To describe a first-order autoregressive (AR(1)) structure of as well as a linear relationship between and the -dimensional vector of exogenous variables , the benchmark dynamic panel model is defined as

| (1.1) |

for and , where is the unobservable fixed effect to characterize the individual heterogeneity, is a -dimensional vector of unknown parameters, is an unknown scalar parameter, and is the model disturbance. Notably, not only helps to mitigate issues related to omitted variable bias and endogeneity, but also holds practical significance. For example, if is the return of asset at time , represents the excess return of this asset over different risk factors , and investors have a preference for larger values of . In this context, the statistical inference of is practically useful.

Although the presence of is crucial, it causes the well-known incidental parameter problem (Neyman and Scott, 1948), making the estimation of model (1.1) challenging. To solve this problem, researchers have explored two strands of literature. The first strand focuses on the least square (LS) estimator (also known as within estimator) of and by concentrating out . When is fixed, Nickell (1981) reveals that the LS estimator is biased. When both and diverge to infinity at the same rate, the asymptotic bias of LS estimator appears and it can be corrected by the analytical asymptotics method in Hahn and Kuersteiner (2002) or the Jackknife method in Hahn and Newey (2004) and Dhaene and Jochmans (2015). Unlike the LS estimation method, the estimation method in the second strand removes by adopting the first difference (FD) treatment. This leads to the FD-based generalized method of moments (FD-GMM) estimator in Arellano (1991) and the FD-based maximum likelihood (FD-ML) estimator in Hsiao et al. (2002). Despite FD-GMM and FD-ML estimators of and being consistent for fixed and large , they are highly model specific and not applicable for estimating . In addition, Alvarez and Arellano (2003) illustrates that similar to the LS estimator, the FD-GMM estimator also suffers an asymptotic bias when both and diverge to infinity at the same rate.

Needless to say, model (1.1) is inadequate to capture the higher-order serial correlation as well as conditional heteroskedasticity of . To remedy this deficiency, we propose a panel autoregressive moving-average (ARMA) model with fixed effects and generalized autoregressive conditional heteroskedasticity (GARCH) disturbances to study , where all of share the same ARMA and GARCH parameters cross-sectionally, but remain the unobservable fixed effects in both panel ARMA and panel GARCH specifications. In short, our proposed model is termed as the panel ARMA–GARCH model. Clearly, the panel ARMA specification is applied to characterize the higher-order serial correlation of , and the existence of MA part could avoid the use of a large AR specification. The panel GARCH specification inspired by Engle (1982) and Bollerslev (1986) is introduced to depict the conditional heteroskedasticity, which is a prevalent phenomenon in financial and economic data. Although the ARMA–GARCH is a benchmark specification for studying the time series data (Francq and Zakoïan, 2004; Zhu and Ling, 2011), it has not been well explored in the dynamic panel framework. When has the higher-order AR structure, a few works in Hansen (2007), Lee (2012), and Lee et al. (2018) study the estimation of dynamic panel model. However, their estimation methods neither incorporate the MA specification for nor account for the GARCH disturbances. Till now, the only formal attempt for studying the panel GARCH specification is made by Pakel et al. (2011). However, the estimation method in Pakel et al. (2011) has two major limitations. First, it only works for the small case with , since it does not investigate the asymptotic bias of estimator when both and diverge to infinity at the same rate. Second, it assumes the zero-mean of , so how the estimation of fixed effects and ARMA parameters affects that of GARCH specification is unclear.

This paper is motivated to comprehensively study the estimation of the panel ARMA–GARCH model. Our contributions to the literature are summarized as follows:

First, we propose a two-step estimation for the panel ARMA–GARCH model. To be specific, we estimate the panel ARMA specification by using the LS estimation method at step one. Based on the residuals from the step one, we then estimate the panel GARCH specification by adopting the variance-targeting quasi-maximum likelihood (VT-QML) estimation method (Francq et al., 2011) at step two. Under some regularity conditions, we prove that both LS estimator of ARMA parameters and VT-QML estimator of GARCH parameters are asymptotically normal with the convergence rate , and they have the asymptotic biases when both and diverge to infinity at the same rate. Particularly, we illustrate that the existence of fixed effects and unobservable initial values produces the asymptotic biases in both LS and VT-QML estimators, and the latter estimator also suffers from the asymptotic bias caused by the first-step estimation effect. Moreover, we apply either the analytical asymptotics or jackknife method to correct the bias, and establish the related asymptotics for the bias-corrected estimators. For the fixed effects in both ARMA and GARCH specifications, we show that their estimators are asymptotically normal with the convergence rate , so their statistical inference can be implemented in a straightforward manner.

Second, we provide a new tool to study the convergence rate and central limit theorem (CLT) for the linear-quadratic form , where is a vector of random variables, and and are non-stochastic weight matrix and vector, respectively. When is an independent and identically distributed (i.i.d.) or martingale difference sequence, Whittle (1964), Giraitis and Taqqu (1997, 1998), and Hsing and Wu (2004) establish the CLT for the quadratic form (i.e., ) under the assumption that is a function of , while this assumption on is further relaxed by Wu and Shao (2007) and Giraitis et al. (2017). When is an i.i.d. sequence, Kelejian and Prucha (2001) provides the CLT for the linear-quadratic form under a weaker assumption that is uniformly bounded in row and column. However, all of the aforementioned results of CLT are invalid for deriving the asymptotics of our proposed estimators. In this paper, under the assumption that is uniformly bounded in row and column, we derive the CLT for the linear-quadratic form under general conditions on , which allow to be block-independent with certain temporal dependence (that is, the martingale difference structure) within the block. Our new results on the linear-quadratic form are interesting in their own rights and could be useful for many other studies.

Third, our panel ARMA–GARCH model paves a new way to study the high-dimensional time series. In the literature, the majority of work focuses on the estimation of high-dimensional vector AR model under certain regularity constraints; see, for example, the sparsity constraint in Basu and Michailidis (2015), Kock and Callot (2015), and Wu and Wu (2016), the banded constraint in Guo et al. (2016), the network constraint in Zhu et al. (2017), and the low rank constraint in Basu et al. (2019) and Wang et al. (2022). See also Wilms et al. (2023) for the exploration of high-dimensional vector ARMA model under sparsity constraint. Our panel ARMA specification essentially poses a panel constraint that all ARMA parameters are the same cross-sectionally. This panel constraint not only allows us to pool all information available in the panel, but also enables us to derive the asymptotic normality of LS estimator. Note that when diverges to infinity, so far only Zhu et al. (2017) establishes the asymptotic normality of model estimator, however, it neither accounts for the fixed effects nor considers the MA structure and GARCH disturbances. Compared with all of above studies on the high-dimensional time series models, our asymptotic normality result allows for more general martingale difference disturbances in the panel ARMA specification, thereby expanding the potential scope of applications for practitioners. Analogously, our panel GARCH specification also has a panel constraint that all GARCH parameters are the same cross-sectionally, as made by Pakel et al. (2011). When diverges to infinity, so far there is no theoretical development for the high-dimensional GARCH model. Our asymptotic normality result of the VT-QML estimator fills this gap for the first time in the literature. Owing to the panel structure in GARCH specification, the asymptotic normality of the VT-QML estimator works for the case of moderate (say, e.g., ), as demonstrated by our simulation studies. This overcomes a shortcoming of the classical GARCH models, which typically require a very large to get accurate estimates. From a practical viewpoint, how to deal with the moderate case is important for studying many low-frequency real data.

The remaining paper is organized as follows. Section 2 introduces the panel ARMA-GARCH model and its two-step estimation method. Section 3 provides some general theoretical results for the linear-quadratic form. Section 4 establishes the asymptotics of all proposed estimators and their corrected versions. Simulations are given in Section 5. A real application is presented in Section 6. Concluding remarks are offered in Section 7. Technical proofs and some additional simulations are deferred into the supplementary materials.

Throughout the paper, is the one-dimensional Euclidean space, is the identity matrix, and is the -dimensional vector of ones. For a matrix , is its transpose, is its trace, is its -norm, and is its inverse when . For a random variable , is its -norm for . A sequence of matrices is uniformly bounded in row (or column) if (or ). A sequence of random variables is uniformly -bounded if . Moreover, denotes a generic bounded constant, denotes a sequence of random variables converging to zero (bounded) in probability, “” denotes convergence in probability, and “” denotes convergence in distribution.

2 The model and its estimation method

2.1 The panel ARMA–GARCH model

Given a panel of observations , our panel ARMA–GARCH model is defined as

| (2.1a) | ||||

| (2.1b) | ||||

for and , where and are the unobservable fixed effects, is a -dimensional vector of unknown parameters, and are the ARMA parameters, and are the GARCH parameters, and is a sequence of i.i.d. errors with mean zero and variance one. Here, we assume , , and to ensure , where is the conditional variance of given the -field generated by . Clearly, the panel ARMA–GARCH model contains two parts: the panel ARMA specification with orders and in (2.1a) and the panel GARCH specification with orders and in (2.1b), where the panel ARMA specification nests the dynamic panel specification in (1.1), and the panel GARCH specification is the same as that in Pakel et al. (2011).

It is worth noting that the panel ARMA–GARCH model serves as a bridge, connecting the dynamic panel literature with the high-dimensional time series literature. Compared with the high-dimensional ARMA or GARCH model, the panel ARMA–GARCH model has a crucial panel constraint that all of share the same ARMA and GARCH parameters cross-sectionally. This panel constraint is common in the dynamic panel literature. It allows us to use the entire panel observations to estimate these shared parameters, so the resulting estimators can have the asymptotic normality with the convergence rate . Like most of dynamic panel models, the panel ARMA–GARCH model also inherits their another common feature that the dynamics of only depends on their own lagged values but not on the lagged values of other . This cross-sectional independence feature is not often assumed in the high-dimensional ARMA or GARCH model, although it could help to avoid over-parameterization, improve prediction, and match an empirical finding that relies more on its own past than it does on the past of other (Engle and Kroner, 1995). To capture the cross-section dependence, we could follow the common way to add the spatial or network structure in the panel ARMA–GARCH model as done in Zhu et al. (2017), Kuersteiner and Prucha (2020), and Zhou, et al. (2020). It appears that our estimation method and related technical treatments can be extended to these spatial and network cases, which are not investigated in detail for ease of exposition.

2.2 The two-step estimation method

Due to the presence of and , the estimation of our panel ARMA–GARCH model has the incidental parameter problem. To solve this problem, we design a two-step estimation method to estimate panel ARMA specification and panel GARCH specification stepwisely.

In the first step, we estimate the panel ARMA specification in (2.1a) by using the LS estimation method. Let be the parameter vector in (2.1a) and be its true value, where is the parameter space of , , with , , and , and and are defined analogously. For , its parametric form is defined iteratively by . By construction, we have . However, is computationally infeasible due to some unobservable initial values. Therefore, we have to consider (i.e., the computationally feasible version of ) defined iteratively by for and , with the initial values . Let with . Then, satisfies the following equation:

| (2.2) |

where with , with , , and and are two invertible matrices defined by

Clearly, is the computationally feasible version of , where with .

From (2.2), we know that has the form

| (2.3) |

Then, our objective function for the LS estimation is defined as . By solving the equations , the solution of for any given is

| (2.4) |

where . Furthermore, by replacing with in , we get the concentrated objective function , where . Based on , we define the LS estimator of as follows:

| (2.5) |

where and . Substituting with in (2.4), we obtain , which is the LS estimator of . In sum, our LS estimator of is , where .

In the second step, we estimate the panel GARCH specification in (2.1b) by using the variance-targeting (VT) method (Francq et al., 2011). Let be the parameter vector in (2.1b) and be its true value, where , , with and , and and are defined analogously. To facilitate the VT method, we assume , which implies that (Bollerslev, 1986). Then, we have , so we can re-parameterize (2.1b) as

| (2.6) |

For in (2.6), it has the parametric form defined iteratively by

| (2.7) |

for . Clearly, . By assuming in (2.6), the log-likelihood function of (ignoring constants) is

| (2.8) |

where . As and are unobservable, we have to consider (i.e., the computationally feasible version of ) defined by

where (i.e., the computationally feasible version of ) is defined iteratively by

with the initial values and . Here, is the residual computed from with , and is a given constant.

Like , the presence of in causes the incidental parameter problem, but we cannot concentrate out since the equation does not deliver a closed-form solution of . To circumvent this deficiency, we simply estimate by

in view of the fact that is the second moment of . After replacing with in , we further estimate by the VT-QML estimator

| (2.9) |

where and . Based on and , we now estimate by

To sum up, our VT-QML estimator of is , where .

We should highlight that the classical QML estimation method estimates the ARMA–GARCH model jointly instead of stepwisely (Francq and Zakoïan, 2004). Here, our main reason to use the two-step estimation method is to tackle the incidental parameter problem, so that can be concentrated out at step one and can be re-parameterized out at step two. Clearly, the joint estimation method does not allow us to achieve this goal.

3 The asymptotics of linear-quadratic form

To establish the asymptotic theory of our proposed estimators, we need some new asymptotics for the following linear-quadratic form:

| (3.1) |

where is an -dimensional vector of variables with , is an non-stochastic block weight matrix with -th block , and is an -dimensional non-stochastic weight vector with . Note that the elements of and are allowed to depend on and , and we have suppressed their subscripts and for ease of presentation.

When and , the linear-quadratic form reduces to the quadratic form . Under the assumption that is a function of , Whittle (1964), Giraitis and Taqqu (1997, 1998), and Hsing and Wu (2004) derive the CLT for the quadratic form , where is an i.i.d. or martingale difference sequence. However, the above assumption on is restrictive. For example, it rules out the quadratic form with , which can appear in our objective function (through ) in (2.5) and has to be tackled. Wu and Shao (2007) relieves this assumption by posing the assumption for any given and some other assumptions on , which remain inapplicable to the quadratic form with . Giraitis et al. (2017) provides some assumptions about the Euclidean and spectral norms of matrix , which is difficult to check for matrices appearing in our proofs for the proposed estimators.

When and , Kelejian and Prucha (2001) establishes the CLT for the linear-quadratic form , provided that is uniformly bounded in row and column and is an i.i.d. sequence. Although the condition of is desirable, the proof technique in Kelejian and Prucha (2001) is not transferable to the case of , under which there is temporal dependence in each .

Below, we provide the asymptotics for the linear-quadratic form , based on the following general conditions on , , and in (3.1).

Condition 1.

(i) and . (ii) .

Condition 2.

(i) is an independent sequence. (ii) For each , is a strictly stationary and uncorrelated sequence, and is -bounded for some with . (iii) For each , the following moment conditions hold:

where , , , and .

We offer some remarks on the above two conditions. Condition 1(i) requires that is uniformly bounded in row and column, and Condition 1(ii) holds when elements in are uniformly bounded. This condition is similar to the one in Kelejian and Prucha (2001), and it does not need to assume that is a function of . Condition 2(i)–(ii) assume that are i.i.d. across and strictly stationary in for each , and they are also uncorrelated for each . These settings are common in dynamic panel models (see Hahn and Kuersteiner (2002)), and if each is viewed as a block of , they essentially allow to be block-independent with certain temporal dependence within the block. Meanwhile, the stationarity and -boundedness condition in Condition 2(ii) ensures the existence of , , , and in Condition 2(iii). The moment conditions in Condition 2(iii) are regular and they are satisfied if Conditions 1–2(ii) hold,

| (3.2) |

The sufficient conditions in (3.2) are mild, and they hold for many time series specifications. For example, when follows the GARCH specification with a finite fourth moment for each , the conditions in (3.2) are valid, since and for some (Francq and Zakoïan, 2019). It is worth noting that our Condition 2(iii) is different from the high-order cumulative summability conditions on for each in Hahn and Kuersteiner (2002), and it is easy to check as demonstrated above. For the validity of high-order cumulative summability conditions, some mixing conditions are generally needed but they can be difficult to verify for many time series specifications.

To present the asymptotics of , we first give the formulas of its mean and variance:

where , , , and , , , and are defined as in Condition 2. Next, we show the convergence rate of is .

Moreover, to establish the CLT of , we need the condition below:

Condition 3.

(i) For each , is ergodic and a martingale difference sequence with respect to the filtration , where is a -field generated by .

(ii) Either the conditional variance for all , or the matrix satisfies (a) ; (b) with any ; and (c) as .

Condition 3 poses some regular conditions on for each . Specifically, Condition 3(i) holds when has the GARCH specification. Condition 3(ii) is made to handle , which is a non-martingale difference sequence with respect to . When is an i.i.d. sequence across , we have for all , so Condition 3(ii) holds. In general, when has certain temporal dependence structure such as GARCH, for all . Then, we can verify Condition 3(ii) by checking these matrix assumptions in parts (a)–(c), which hold in our following theoretical analysis for the proposed estimators. For similar matrix assumptions, one can refer to Wu and Shao (2007) and Giraitis et al. (2017). Now, we give the CLT for .

Since the presence of exogenous variables in (2.2) can make stochastic in our theoretical analysis, we further give a corollary to allow for the exogenous .

4 The asymptotics of all proposed estimators

4.1 The technical assumptions

Let be an -dimensional vector of unknown parameters with the true value in (2.1a)–(2.1b), where is the parameter space of , and . Denote , , , and . To derive the asymptotics of our proposed estimators, we make the following assumptions:

Assumption 4.1.

(i) is compact and is an interior point of .

(ii) For each , both and have no common root with and ; moreover, and when , , and .

(iii) For each , and have no common root with , and .

Assumption 4.2.

(i) are non-stochastic and uniformly bounded in and . Or, they are strictly exogenous, independent across and , strictly stationary in for each , and -bounded for some .

(ii) are i.i.d. variables with mean zero and variance one, and they are uniformly -bounded for some .

Assumption 4.3.

, where .

Assumption 4.1 ensures the stationarity, invertibility, and identifiability of the ARMA–GARCH model for each individual (see, e.g., Brockwell and Davis (2002) and Francq and Zakoïan (2019)). Particularly, the condition of is consistent with the finite second moment of (i.e., ), and it ensures the applicability of the VT technique. Assumption 4.2 provides some regular conditions for the exogenous variables and model errors. The temporal independence assumption for the exogenous variable is made to ease our theoretical analysis, and it can be generalized into certain martingale difference or mixing assumptions. Assumption 4.3 is common for dynamic panel models; see, for example, Hahn and Kuersteiner (2002), Alvarez and Arellano (2003), and many others. It states that our asymptotic analysis below is for the case when both and diverge to infinity at the same rate.

4.2 The asymptotics for the panel ARMA specification

4.2.1 The asymptotics of and

Denote and . Then, we re-write

where , , and and are defined in the same way as and , respectively, with replaced by . From the proof in the supplementary materials,

| (4.1) |

where the first item leads to the asymptotic normality of , the second item is negligible, and the last two items cause the asymptotic bias of . Similarly, from the proof in the supplementary materials, we can show

| (4.2) |

where the third item contributes to the asymptotic variance of , and the rest three items are negligible.

By (4.1)–(4.2) and an additional technical assumption below, we can obtain the asymptotics of in Theorem 4.1.

Assumption 4.4.

Both and exist, and is non-singular, where

Theorem 4.1.

Remark 1.

Remark 2.

For saving space, the explicit formulas of , , , and are given in Section B.1 of the supplementary materials. Then, under the conditions in Theorem 4.1, we can consistently estimate , , and by their plug-in counterparts , , and , respectively.

From Theorem 4.1, we find that when , is -consistent and asymptotically centered normal; when (i.e., both and diverge to infinity at the same rate), is still -consistent but asymptotically non-centered normal with mean .

Notably, the terms and reflect the influence of the fixed effects and unobservable initial values on the asymptotic bias of , respectively. If (i.e., (2.1a) is a panel AR() model), we can show that ; therefore, as expected, there is no asymptotic bias resulting from the unobservable initial values in this case. Particularly, if and (i.e., (2.1a) is a panel AR(1) model), our asymptotic normality result in Theorem 4.1 is consistent to that in Hahn and Kuersteiner (2002). Unlike Hahn and Kuersteiner (2002) requiring to be a mixing sequence, our technical treatment of Theorem 4.1 works for a more general model and allows to be the martingale difference sequence.

Let be the -th entry of . The following theorem shows that is -consistent and asymptotically normal without any asymptotic bias.

4.2.2 Bias correction of

From Theorem 4.1, we find that has some asymptotic biases when . To achieve a better finite sample performance than , we consider the following analytical bias correction estimator

| (4.3) |

where and in Remark 2 are the plug-in estimators of and , respectively. Although is expected to have a nice finite sample performance, the calculation of and could become tedious when the orders of the panel ARMA specification are large. Hence, to avoid this computational issue, we follow the idea of Dhaene and Jochmans (2015) to propose the half-panel Jackknife bias correction estimator

| (4.4) |

where and are defined in the same way as , based on the observations for and those for , respectively. Note that the equation (4.4) can be re-written as . Thus, is actually an estimator for the asymptotic bias, and its calculation does not rely on the explicit formulas of the asymptotic bias. The asymptotic normality of and is given as follows:

The above theorem shows that both and are -consistent and asymptotically centered normal. Thus, they could have a better finite sample performance than in terms of bias (see the numerical evidence in Section 5 below).

4.3 The asymptotics for the panel GARCH specification

4.3.1 The asymptotics of and

The objective function in (2.9) involves the unobservable initial values, the estimated fixed effect , and the residual which is further based on the ARMA parameter estimator and the estimated fixed effect . To account for their impact on the asymptotics of , we define and recursively by

where

Here, with and being the lag operator, and can be re-written as . Note that similar to in (2.4), is the solution of by solving the equations .

Denote . First, by letting , we re-write

| (4.5) |

where captures the effect of unobservable initial values in ARMA and GARCH specifications, and is defined in the same way as with and replaced by and , respectively. Second, by letting , we re-write

| (4.6) |

where reflects the effect of the estimation of by , and is defined in the same way as with and replaced by and , respectively. Third, by letting with , we re-write

| (4.7) |

where considers the effect of the estimation of by , and is defined in the same way as with and replaced by and , respectively. Finally, we re-write

| (4.8) |

where gives the effect of the estimation of by , and is defined in the same way as with and replaced by and , respectively.

Now, denote

where is defined in the supplementary materials and it is zero if is systematic about zero. By (4.5)–(4.8) and the proof in the supplementary materials, we have

| (4.9) |

In (4.9), the first item (resulting from , , , and ) gives the asymptotic normality of , the second item (resulting from , , , and ) causes the asymptotic bias of , and the last item is negligible.

Denote . Similar to (4.9), from the proof in the supplementary materials, we can obtain

| (4.10) |

where

In (4.10), the first item contributes to the asymptotic variance of , and the second item is negligible.

Remark 3.

For saving the space, we give the explicit formulas of , , , , , and in Section B.2 of the supplementary materials. Then, under the conditions of Theorem 4.4, we can consistently estimate , , and by their plug-in counterparts , , and , respectively. For , we show that in Section C.3 of the supplementary materials, but we are unable to provide its explicit formula due to the non-linearity of GARCH specification with some non-zero parameters . Consequently, we cannot offer a consistent estimator of .

The results of Theorem 4.4 are new to the literature, and they demonstrate that has a similar asymptotic behavior as in Theorem 4.1. However, it is worth noting that the asymptotic bias of consists of three parts: , , and . Specifically, the first part comes from the estimated fixed effects and , the second part stems from the bias of estimated ARMA parameter vector , and the third part results from the unobservable initial values in both panel ARMA and panel GARCH specifications. Particularly, if and (i.e., follows a panel AR–ARCH model), we can show that , so the third part of the asymptotic bias of disappears.

Finally, we give a theorem to show that and are -consistent and asymptotically normal without any asymptotic bias.

4.3.2 Bias correction of

Since the asymptotic bias in Theorem 4.4 is caused by that of , we can exclude this asymptotic bias by constructing an alternative VT-QML estimator , which is formed in the same way as with replaced by its bias-corrected counterpart or . Unfortunately, the remaining asymptotic biases in Theorem 4.4 cannot be eliminated by this analytical method, as their explicit formulas are unavailable; see the discussions in Remark 3 above. To deal with this problem, we follow Section 4.2 to consider the half-panel Jackknife bias correction estimator

| (4.11) |

where and are defined in the same way as , but only involving observations during and , respectively. Now, we give the asymptotic normality of below:

The above theorem demonstrates that is -consistent and asymptotically centered normal. Thus, it could have a better finite sample performance than in terms of bias, as shown by our simulation studies in the next section.

5 Simulations

In this section, we examine the finite sample performance of the estimators and in (2.5) and (2.9), together with their analytical bias correction estimator in (4.3), and Jackknife bias correction estimators and in (4.4) and (4.11).

Specifically, we generate 1000 replications of the sample size from the following panel ARMA()–GARCH() model:

| (5.1) | ||||

where , , , , , , , , and , , , and are independent. For each replication, we compute all of considered estimators , , , , and . Based on the results from 1000 replications, Tables 1, 2, and 3 report the sample bias, the sample standard deviations (SD), and the ratio of SD over the average estimated asymptotic standard deviations (AD) of all considered estimators, respectively. Here, since the sample size is too small to provide reliable estimation results for GARCH parameters, the related results are excluded. From Tables 1–3, we can have the following findings:

-

(i)

For each given , the biases of and decrease with the value of . In contrast, for each given , the biases of and do not have a clear decreasing trend when the value of increases. This observation matches our theoretical results in Theorems 4.1 and 4.4 that the asymptotic bias of or has the order which is irrespective of the value of . Moreover, the bias-corrected estimators and (or ) have much smaller biases than (or ), especially when the value of is small. This is consistent with our asymptotic analysis in Theorems 4.3 and 4.6. In addition, compared with , has slightly smaller biases when is small, but this mild advantage disappears when is large.

-

(ii)

The values of SD for all considered estimators become smaller when the value of either or increases, and they are nearly unchanged to the bias correction implementation. This supports our theoretical results in Theorems 4.1, 4.3–4.4, and 4.6 that all estimators are -consistent and the formula of their asymptotic variance remains the same, irrespective of the bias correction implementation.

-

(iii)

The values of SD/AD are close to one for all considered estimators, except the GARCH parameter estimators and in the case of . This finding is not unexpected, since the experience in the literature shows that it is more hard to estimate than . It is worth noting that for classical GARCH models, a sample size as small as 100 cannot deliver accurate GARCH parameter estimators with reliable standard errors. Hence, although the estimators of are less satisfactory for , our findings are still encouraging, since they indicate that the asymptotic normality of our considered estimators in Theorems 4.1 and 4.4 holds even when the value of is around 100. Clearly, the panel structure of our model leads to the advantage of our estimators in dealing with moderate samples.

Overall, the above simulation results demonstrate that , , and perform better than their competitors in terms of bias, and their asymptotic normality holds even when is as small as 100. In the supplementary materials, some additional simulation results for model (5.1) with student distributed errors are also provided, and they give us a similar conclusion as above.

| Bias | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 50 | 20 | 0.008 | 0.001 | 0.003 | 0.008 | 0.001 | 0.005 | 0.033 | 0.003 | 0.023 | —– | —– | —– | —– |

| 50 | 0.003 | 0.000 | 0.001 | 0.004 | 0.001 | 0.001 | 0.012 | 0.000 | 0.005 | 0.055 | 0.001 | 0.135 | 0.024 | |

| 100 | 0.001 | 0.001 | 0.001 | 0.002 | 0.000 | 0.001 | 0.005 | 0.001 | 0.003 | 0.025 | 0.000 | 0.053 | 0.022 | |

| 200 | 0.001 | 0.000 | 0.000 | 0.001 | 0.000 | 0.000 | 0.003 | 0.000 | 0.001 | 0.013 | 0.001 | 0.023 | 0.006 | |

| 300 | 0.001 | 0.000 | 0.000 | 0.001 | 0.000 | 0.000 | 0.001 | 0.001 | 0.001 | 0.008 | 0.000 | 0.016 | 0.002 | |

| 100 | 20 | 0.008 | 0.002 | 0.003 | 0.008 | 0.001 | 0.005 | 0.032 | 0.004 | 0.023 | —– | —– | —– | —– |

| 50 | 0.004 | 0.001 | 0.001 | 0.004 | 0.000 | 0.001 | 0.011 | 0.001 | 0.006 | 0.054 | 0.003 | 0.130 | 0.047 | |

| 100 | 0.002 | 0.000 | 0.000 | 0.002 | 0.000 | 0.001 | 0.005 | 0.000 | 0.003 | 0.026 | 0.000 | 0.053 | 0.021 | |

| 200 | 0.000 | 0.001 | 0.001 | 0.001 | 0.000 | 0.000 | 0.003 | 0.000 | 0.001 | 0.013 | 0.001 | 0.022 | 0.008 | |

| 300 | 0.000 | 0.001 | 0.001 | 0.001 | 0.000 | 0.000 | 0.002 | 0.000 | 0.001 | 0.008 | 0.001 | 0.016 | 0.002 | |

| SD | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 50 | 20 | 0.046 | 0.046 | 0.049 | 0.016 | 0.016 | 0.018 | 0.044 | 0.041 | 0.048 | —– | —– | —– | —– |

| 50 | 0.028 | 0.028 | 0.028 | 0.010 | 0.010 | 0.010 | 0.027 | 0.027 | 0.029 | 0.028 | 0.035 | 0.101 | 0.157 | |

| 100 | 0.020 | 0.020 | 0.020 | 0.007 | 0.007 | 0.007 | 0.019 | 0.019 | 0.019 | 0.020 | 0.022 | 0.063 | 0.076 | |

| 200 | 0.015 | 0.014 | 0.015 | 0.005 | 0.005 | 0.005 | 0.013 | 0.012 | 0.013 | 0.014 | 0.015 | 0.044 | 0.048 | |

| 300 | 0.012 | 0.012 | 0.012 | 0.004 | 0.004 | 0.004 | 0.010 | 0.010 | 0.010 | 0.012 | 0.013 | 0.035 | 0.037 | |

| 100 | 20 | 0.032 | 0.032 | 0.035 | 0.012 | 0.012 | 0.013 | 0.032 | 0.030 | 0.035 | —– | —– | —– | —– |

| 50 | 0.020 | 0.020 | 0.021 | 0.007 | 0.007 | 0.007 | 0.019 | 0.018 | 0.020 | 0.020 | 0.024 | 0.073 | 0.114 | |

| 100 | 0.015 | 0.015 | 0.015 | 0.005 | 0.005 | 0.005 | 0.013 | 0.013 | 0.014 | 0.014 | 0.015 | 0.045 | 0.052 | |

| 200 | 0.010 | 0.010 | 0.010 | 0.004 | 0.004 | 0.004 | 0.009 | 0.009 | 0.009 | 0.010 | 0.011 | 0.031 | 0.033 | |

| 300 | 0.008 | 0.008 | 0.008 | 0.003 | 0.003 | 0.003 | 0.007 | 0.007 | 0.007 | 0.008 | 0.009 | 0.025 | 0.026 | |

| SD/AD | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 50 | 20 | 1.025 | 1.021 | 1.106 | 1.017 | 1.018 | 1.153 | 0.920 | 0.866 | 1.020 | —– | —– | —– | —– |

| 50 | 0.998 | 0.997 | 1.010 | 1.001 | 1.001 | 1.043 | 1.022 | 1.003 | 1.083 | 1.022 | 1.279 | 0.737 | 1.976 | |

| 100 | 0.986 | 0.986 | 0.991 | 0.993 | 0.993 | 0.999 | 1.017 | 1.009 | 1.046 | 0.968 | 1.079 | 0.856 | 1.332 | |

| 200 | 1.034 | 1.034 | 1.045 | 0.955 | 0.955 | 0.981 | 0.967 | 0.963 | 0.988 | 0.973 | 1.048 | 0.950 | 1.163 | |

| 300 | 1.010 | 1.010 | 1.015 | 1.001 | 1.001 | 1.004 | 0.958 | 0.955 | 0.968 | 1.000 | 1.047 | 0.975 | 1.089 | |

| 100 | 20 | 1.032 | 1.028 | 1.107 | 1.040 | 1.045 | 1.152 | 0.943 | 0.887 | 1.052 | —– | —– | —– | —– |

| 50 | 1.020 | 1.019 | 1.047 | 1.011 | 1.012 | 1.058 | 0.981 | 0.962 | 1.029 | 1.030 | 1.239 | 0.773 | 2.128 | |

| 100 | 1.041 | 1.041 | 1.044 | 1.012 | 1.012 | 1.030 | 1.003 | 0.994 | 1.036 | 0.956 | 1.076 | 0.875 | 1.287 | |

| 200 | 1.022 | 1.022 | 1.021 | 1.047 | 1.047 | 1.044 | 0.959 | 0.954 | 0.973 | 1.004 | 1.066 | 0.949 | 1.142 | |

| 300 | 1.011 | 1.011 | 1.013 | 0.996 | 0.996 | 0.986 | 0.975 | 0.972 | 0.979 | 0.988 | 1.038 | 0.980 | 1.098 | |

6 Empirical analysis

In this section, we use our panel ARMA–GARCH model to study the dynamics of Producer Price Indices (PPI) growth in domestic market for 31 different countries (see Table 4 below for their names) over 120 months spanning from 2011.06 to 2021.06. To investigate how other economic indicators affect the PPI, we also consider the Consumer Price Index (CPI) growth based on Energy or Food (CPI-E or CPI-F) and Industrial Production (IP) growth in Manufacturing or Construction (IP-M or IP-C) as four exogenous variables. The data of all of these economic indicators are accessible from Organization for Economic Co-operation and Development (OECD) at https://www.oecd.org/.

Let , , , , and denote the log difference of PPI, CPI-E, CPI-F, IP-M, and IP-C growths of country at month , respectively, where the last four exogenous variables are demeaned for a better interpretation on . Based on these variables, we fit the PPI panel data via a panel ARMA()–GARCH() model in (2.1a)–(2.1b), where . After using the backward elimination procedure to remove those insignificant variables at the 5% level, we obtain the following fitted ARMA()–GARCH() model:

| (6.1) | ||||

where the estimates are computed by the Jackknife bias-correction method, and the standard deviations of all estimates are given in parentheses. From this fitted model, we find that PPI has clear serial correlation and GARCH effect from the significance of the ARMA and GARCH parameters, respectively; moreover, we find that two variables CPI-E and IP-M have considerable positive influences on PPI, whereas the eliminated variables CPI-F and IP-C have no significant impact on PPI.

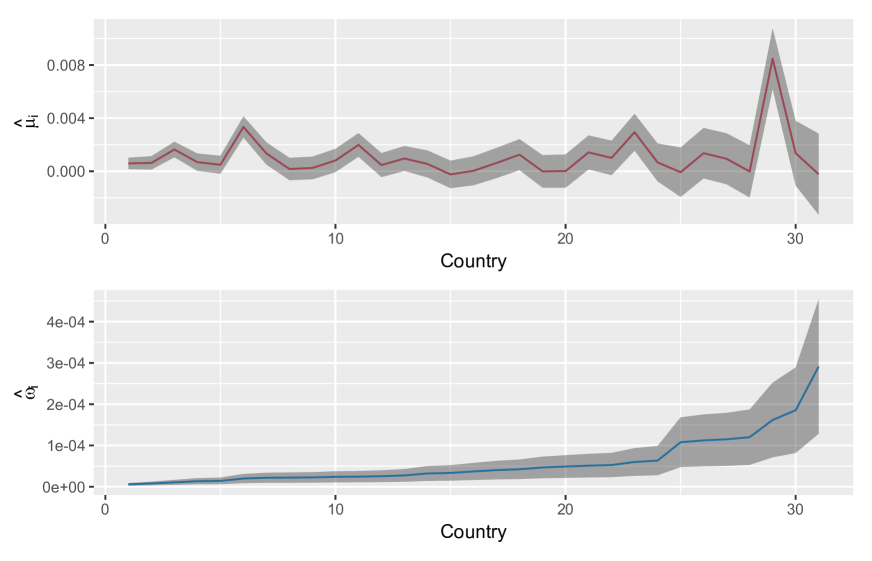

Next, we examine the individual heterogeneity in both mean and variance by plotting the estimated individual effects and with confidence intervals in Figure 1. Note that for each country , the value of (divided by ) represents the mean of due to the zero mean of and , while that of represents the variance of . For ease of interpretation, we align 31 countries in a way such that the values of are in ascending order, as shown in Figure 1. From this figure, we observe the clear individual heterogeneity in both mean and variance. Specifically, we find that (i) except Countries ‘15’, ‘19’, ‘25’, ‘28’, and ‘31’ (Korea, Portugal, Israel, Lithuania, and Greece), all the values of are positive, although some of them are not significantly different from zero; (ii) Countries ‘6’, ‘23’, and ‘29’ (South Africa, Mexico, and Turkiye) have spiked values of , giving a sign of severe inflation in these three countries; and (iii) Countries ‘29’, ‘30’, and ‘31’ (Turkiye, Hungary, and Greece) have much larger values of than other countries, indicating that these three countries could have a higher risk of undergoing hyperinflation or hyperdeflation.

Finally, we assess the out-of-sample forecast performance of model (6.1). For this purpose, we use the following rolling window procedure: first, do the estimation based on the data of the latest 96 months to fit model (6.1) and apply the fitted model to forecast the future as well as its two-sided 95% confidence interval one month ahead; then repeat the foregoing procedure until the end of the sample has been reached. Based on the fitted model, the point forecast of is computed in a conventional way, and the 95% interval forecast of is computed by using the filtered historical simulation method (Barone-Adesi et al., 1998). To see how the bias correction method affects the forecast performance, we compute the fitted model (6.1) by using , , and , leading to the so-called Methods I, IA, and IJ, respectively. As a comparison, we also consider Method II, which fits each based on the univariate ARMA()–GARCH() model

| (6.2) | ||||

where all of unknown parameters above are estimated equation by equation.

| RMSE | p-value of | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Country | I | IA | IJ | II | I | IA | IJ | II | |

| 1 | Germany | 0.347 | 0.325 | 0.320 | 0.341 | 0.629 | 0.629 | 0.629 | 0.003 |

| 2 | Slovenia | 0.469 | 0.470 | 0.461 | 0.486 | 0.001 | 0.005 | 0.005 | 0.000 |

| 3 | Costa Rica | 0.403 | 0.368 | 0.359 | 0.374 | 1.000 | 1.000 | 1.000 | 1.000 |

| 4 | UK | 0.352 | 0.345 | 0.346 | 0.345 | 0.945 | 0.945 | 0.945 | 0.945 |

| 5 | Italy | 0.485 | 0.449 | 0.442 | 0.593 | 0.202 | 0.190 | 0.190 | 0.012 |

| 6 | South Africa | 0.396 | 0.393 | 0.396 | 0.500 | 0.945 | 0.945 | 0.945 | 0.629 |

| 7 | Latvia | 0.702 | 0.657 | 0.642 | 0.822 | 0.016 | 0.202 | 0.202 | 0.000 |

| 8 | Japan | 0.570 | 0.567 | 0.567 | 0.578 | 0.210 | 0.629 | 0.629 | 0.629 |

| 9 | France | 0.586 | 0.576 | 0.575 | 0.586 | 0.629 | 0.945 | 0.945 | 0.945 |

| 10 | Denmark | 0.501 | 0.497 | 0.498 | 0.541 | 0.030 | 0.047 | 0.047 | 0.030 |

| 11 | Colombia | 0.509 | 0.502 | 0.501 | 0.507 | 0.945 | 0.945 | 0.945 | 0.945 |

| 12 | Czechia | 0.584 | 0.591 | 0.587 | 0.540 | 0.629 | 0.629 | 0.629 | 0.042 |

| 13 | Poland | 0.679 | 0.646 | 0.633 | 0.730 | 0.629 | 0.629 | 0.629 | 0.000 |

| 14 | Finland | 0.969 | 0.958 | 0.956 | 0.991 | 0.021 | 0.021 | 0.021 | 0.000 |

| 15 | Korea | 0.716 | 0.682 | 0.664 | 0.532 | 0.210 | 0.210 | 0.210 | 0.210 |

| 16 | Ireland | 0.410 | 0.445 | 0.448 | 0.452 | 0.307 | 0.307 | 0.307 | 0.945 |

| 17 | Spain | 0.913 | 0.873 | 0.868 | 0.857 | 0.629 | 0.629 | 0.629 | 0.202 |

| 18 | Estonia | 0.704 | 0.680 | 0.665 | 0.929 | 0.210 | 0.210 | 0.210 | 0.210 |

| 19 | Portugal | 0.737 | 0.712 | 0.711 | 0.686 | 0.042 | 0.210 | 0.210 | 0.210 |

| 20 | Slovak Republic | 0.755 | 0.713 | 0.709 | 0.857 | 0.629 | 0.629 | 0.629 | 0.210 |

| 21 | Norway | 0.813 | 0.817 | 0.829 | 0.888 | 0.629 | 0.629 | 0.629 | 0.210 |

| 22 | Sweden | 0.809 | 0.792 | 0.796 | 0.828 | 0.629 | 0.210 | 0.210 | 0.210 |

| 23 | Mexico | 1.026 | 1.016 | 1.023 | 0.996 | 0.945 | 0.945 | 0.945 | 0.945 |

| 24 | Netherlands | 0.925 | 0.885 | 0.875 | 0.964 | 0.210 | 0.210 | 0.210 | 0.629 |

| 25 | Israel | 1.286 | 1.269 | 1.271 | 1.296 | 0.629 | 0.629 | 0.629 | 0.629 |

| 26 | Luxembourg | 1.096 | 1.068 | 1.072 | 1.129 | 0.047 | 0.047 | 0.047 | 0.047 |

| 27 | Belgium | 1.486 | 1.437 | 1.432 | 2.234 | 0.629 | 0.629 | 0.629 | 0.202 |

| 28 | Lithuania | 1.586 | 1.537 | 1.519 | 1.589 | 0.089 | 0.089 | 0.089 | 0.021 |

| 29 | Turkiye | 1.317 | 1.234 | 1.188 | 1.106 | 1.000 | 1.000 | 1.000 | 1.000 |

| 30 | Hungary | 2.493 | 2.508 | 2.533 | 2.554 | 0.089 | 0.089 | 0.089 | 0.945 |

| 31 | Greece | 2.079 | 2.062 | 2.055 | 2.081 | 0.945 | 0.945 | 0.945 | 0.945 |

-

•

Note: For each country, the smallest RMSE and the largest p-value of (including ties) are highlighted in shadow.

For each country , Table 4 reports its values of root mean squared error (RMSE) for point forecasts and its p-values of conditional coverage test (Christoffersen, 1998) for 95% interval forecasts, across four different methods. From this table, we find that in terms of the minimized RMSE for point forecasts, (i) Method IJ performs best, since it has a smaller RMSE than Methods I, IA, and II in 26, 21, and 26 countries, respectively; (ii) Method IA has the second best performance, with a smaller RMSE than Methods I and II in 26 and 24 countries, respectively; (iii) although Method I performs worse than Methods IJ and IA, it still outperforms Method II with a smaller RMSE in 20 countries; (iv) Method II performs worst, as it has the smallest RMSE in only 7 countries (including ties). Moreover, in terms of the maximized p-value of for interval forecasts, we find that Methods IA and IJ have the same performance, and they slightly outperform Method I with a larger p-value of in 6 countries; meanwhile, all of Methods I, IA, and IJ perform much better than Method II, which delivers invalid interval forecasts in 9 countries with the p-value of less than 5%.

Overall, our findings from Table 4 imply that model (6.1) produces much better point and interval forecasts than model (6.2), and the former should be used with the bias correction to improve the forecast performance. The advantage of model (6.1) over model (6.2) is probably caused by the fact that the estimators , , and for model (6.1) are -consistent due to its panel structure, whereas the estimators for model (6.2) are only -consistent and they thus are less reliable for smaller value of .

7 Conclusion

In this paper, we propose a new panel ARMA–GARCH model. This model captures the serial correlation in mean via a panel ARMA specification, the conditional heteroskedasticity in variance via a panel GARCH specification, and the individual heterogeneity in both mean and variance via the unobservable fixed effects. Using the concentration and VT treatments to solve the incidental parameter problem, we construct the LS estimator for the panel ARMA specification and the VT-QML estimator for the panel GARCH specification stepwisely. When both and diverge to infinity at the same rate, we establish the asymptotic normality of both LS and VT-QML estimators, which have asymptotic biases of order if . Specifically, we find that the presence of fixed effects and unobservable initial values leads to asymptotic biases of both LS and VT-QML estimators, and the VT-QML estimator even has the asymptotic bias caused by the estimation of panel ARMA specification. To correct the biases, we further propose the bias-corrected LS and VT-QML estimators by using either the analytical asymptotics or jackknife method. Simulations and one real example are given to illustrate the importance of the panel ARMA–GARCH model. As an important theoretical development, we provide a new CLT for the linear-quadratic form in the martingale difference sequence, when the weight matrix is uniformly bounded in row and column. This CLT facilitates our technical proofs for the proposed LS and VT-QML estimators, and it could be useful for studying the estimation of complex models with time effects, spatial effects, or other cross-section effects in the future.

References

- Alvarez and Arellano (2003) Alvarez, J. and Arellano, M. (2003). The time series and cross-section asymptotics of dynamic panel data estimators. Econometrica 71, 1121–1159.

- Arellano (1991) Arellano, M. and Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies 58, 277–297.

- Baltagi (2021) Baltagi, B. H. (2021). Econometric Analysis of Panel Data. Chichester: John Wiley Sons.

- Barone-Adesi et al. (1998) Barone-Adesi, G., Bourgoin, F., and Giannopoulos, K. (1998). Don’t look back. Risk 11, 100–103.

- Basu et al. (2019) Basu, S., Li, X., and Michailidis, G. (2019). Low rank and structured modeling of high-dimensional vector autoregressions. IEEE Transactions on Signal Processing 67, 1207–1222.

- Basu and Michailidis (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series models. The Annals of Statistics 43, 1535–1567.

- Bollerslev (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31, 307–327.

- Brockwell and Davis (2002) Brockwell, P. J. and Davis, R. A. (2002). Introduction to Time Series and Forecasting, New York: Springer.

- Christoffersen (1998) Christoffersen, P. F. (1998). Evaluating interval forecasts. International Economic Review 39, 841–862.

- Dhaene and Jochmans (2015) Dhaene, G. and Jochmans, K. (2015). Split-panel jackknife estimation of fixed-effect models. The Review of Economic Studies 82, 991–1030.

- Engle (1982) Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 50, 987–1007.

- Engle and Kroner (1995) Engle, R. F. and Kroner, K. F. (1995). Multivariate simultaneous generalized ARCH. Econometric Theory 11, 122–150.

- Francq et al. (2011) Francq, C., Horváth, L., and Zakoïan, J. M. (2011). Merits and drawbacks of variance targeting in GARCH models. Journal of Financial Econometrics 9, 619–656.

- Francq and Zakoïan (2004) Francq, C. and Zakoïan, J. M. (2004). Maximum likelihood estimation of pure GARCH and ARMA-GARCH processes. Bernoulli 10, 605–637.

- Francq and Zakoïan (2019) Francq, C. and Zakoïan, J. M. (2019). GARCH Models: Structure, Statistical Inference and Financial Applications. Hoboken: John Wiley Sons.

- Giraitis et al. (2017) Giraitis, L., Taniguchi, M., and Taqqu, M. S. (2017). Asymptotic normality of quadratic forms of martingale differences. Statistical Inference for Stochastic Processes 20, 315–327.

- Giraitis and Taqqu (1997) Giraitis, L. and Taqqu, M. S. (1997). Limit theorems for bivariate Appell polynomials. Part I: Central limit theorems. Probability Theory and Related Fields 107, 359–381.

- Giraitis and Taqqu (1998) Giraitis, L. and Taqqu, M. S. (1998). Central limit theorems for quadratic forms with time-domain conditions. The Annals of Probability 26, 377–398.

- Guo et al. (2016) Guo, S., Wang, Y., and Yao, Q. (2016). High-dimensional and banded vector autoregressions. Biometrika 103, 889–903.

- Hahn and Kuersteiner (2002) Hahn, J. and Kuersteiner, G. (2002). Asymptotically unbiased inference for a dynamic panel model with fixed effects when both and are large. Econometrica 70, 1639–1657.

- Hahn and Newey (2004) Hahn, J. and Newey, W. (2004). Jackknife and analytical bias reduction for nonlinear panel models. Econometrica 72, 1295–1319.

- Hansen (2007) Hansen, C. B. (2007). Generalized least squares inference in panel and multilevel models with serial correlation and fixed effects. Journal of Econometrics 140, 670–694.

- Hsiao (2022) Hsiao, C. (2022). Analysis of Panel Data. New York: Cambridge University Press.

- Hsiao et al. (2002) Hsiao, C., Pesaran, M. H., and Tahmiscioglu, A. K. (2002). Maximum likelihood estimation of fixed effects dynamic panel data models covering short time periods. Journal of Econometrics 109, 107–150.

- Hsing and Wu (2004) Hsing, T. and Wu, W. B. (2004). On weighted U-statistics for stationary processes. The Annals of Probability 32, 1600–1631.

- Kelejian and Prucha (2001) Kelejian, H. H. and Prucha, I. R. (2001). On the asymptotic distribution of the Moran I test statistic with applications. Journal of Econometrics 104, 219–257.

- Kuersteiner and Prucha (2020) Kuersteiner, G. M., and Prucha, I. R. (2020). Dynamic spatial panel models: Networks, common shocks, and sequential exogeneity. Econometrica 88, 2109–2146.

- Kock and Callot (2015) Kock, A. B. and Callot, L. (2015). Oracle inequalities for high dimensional vector autoregressions. Journal of Econometrics 186, 325–344.

- Lee (2012) Lee, Y. (2012). Bias in dynamic panel models under time series misspecification. Journal of Econometrics 169, 54–60.

- Lee et al. (2018) Lee, Y. J., Okui, R., and Shintani, M. (2018). Asymptotic inference for dynamic panel estimators of infinite order autoregressive processes. Journal of Econometrics 204, 147–158.

- Neyman and Scott (1948) Neyman, J. and Scott, E. L. (1948). Consistent estimates based on partially consistent observations. Econometrica 16, 1–32.

- Nickell (1981) Nickell, S. (1981). Biases in dynamic models with fixed effects. Econometrica 49, 1417–1426.

- Pakel et al. (2011) Pakel, C., Shephard, N., and Sheppard, K. (2011). Nuisance parameters, composite likelihoods and a panel of GARCH models. Statistica Sinica 21, 307–329.

- Wang et al. (2022) Wang, D., Zheng, Y., Lian, H., and Li, G. (2022) High-dimensional vector autoregressive time series modeling via tensor decomposition. Journal of the American Statistical Association 117, 1338–1356.

- Whittle (1964) Whittle, P. (1964). On the convergence to normality of quadratic forms of independent variables. Theory of Probability and Its Applications 9, 103–108.

- Wilms et al. (2023) Wilms, I., Basu, S., Bien, J., and Matteson, D. S. (2023). Sparse identification and estimation of large-scale vector autoregressive moving averages. Journal of the American Statistical Association 118, 571–582.

- Wu and Shao (2007) Wu, W. B. and Shao, X. (2007). A limit theorem for quadratic forms and its applications. Econometric Theory 23, 930–951.

- Wu and Wu (2016) Wu, W. B. and Wu, Y. N. (2016). Performance bounds for parameter estimates of high-dimensional linear models with correlated errors. Electronic Journal of Statistics 10, 352–379.

- Zhou, et al. (2020) Zhou, J., Li, D., Pan, R., and Wang, H. (2020). Network GARCH model. Statistica Sinica 30, 1723–1740.

- Zhu and Ling (2011) Zhu, K. and Ling, S. (2011). Global self-weighted and local quasi-maximum exponential likelihood estimators for ARMA-GARCH/IGARCH models. The Annals of Statistics 39, 2131–2163.

- Zhu et al. (2017) Zhu, X., Pan, R., Li, G., Liu, Y., and Wang, H. (2017). Network vector autoregression. The Annals of Statistics 45, 1096–1123.