Eigenvector overlaps in large sample covariance matrices and nonlinear shrinkage estimators

Nanyang Technological University )

Abstract

Consider a data matrix of size , where the columns are independent observations from a random vector with zero mean and population covariance . Let and denote the left and right singular vectors of , respectively. This study investigates the eigenvector/singular vector overlaps , and , where are general deterministic matrices with bounded operator norms. We establish the convergence in probability of these eigenvector overlaps toward their deterministic counterparts with explicit convergence rates, when the dimension scales proportionally with the sample size . Building on these findings, we offer a more precise characterization of the loss for Ledoit and Wolf’s nonlinear shrinkage estimators of the population covariance .

1 Introduction

The estimation of covariance matrices or precision matrices is a fundamental problem in the field of multivariate statistics that continues to garner significant attention. This seemingly straightforward problem holds substantial importance across a multitude of domains such as finance, genomics, signal processing, and many others, due to its wide-ranging downstream applications.

Consider a -dimensional random vector with a zero mean. The nonnegative-definite population covariance matrix of interest is defined as . Let be the data matrix where are independent observations from the random vector . It is well understood that when the number of variables is commensurate with the sample size , the sample covariance matrix

| (1.1) |

has limited efficiency when estimating and can lead to erroneous conclusions. This curse of dimensionality has spurred a plethora of efforts over the past two decades to develop robust, efficient, and scalable methods for covariance estimation in high-dimensional settings. For a comprehensive review of recent advances in this topic, we recommend [9, 22, 25, 38] and the references therein.

In the absence of any prior knowledge about the structure of the population covariance, the class of shrinkage estimators developed by Ledoit and Wolf [29, 34] is one of the most widely recognized and commonly employed method due to their proven capability to reduce estimation error. The key characteristic of shrinkage estimators is their rotational invariance, which essentially means that these estimators are derived by retaining the eigenvectors of the sample covariance matrix while manipulating the eigenvalues. Specifically, suppose that the singular value decomposition (SVD) of and the spectral decomposition of are respectively given by

| (1.2) |

where and denote the left and right singular vectors of , respectively. Here the singular values of and the eigenvalues of are ordered as

Then, a rotationally invariant estimator (RIE) of admits the form

with the shrunk eigenvalues typically dependent on . The concept of shrinking the eigenvalues of sample covariance matrices dates back to the pioneering works by Stein [43, 44]. Within this framework, the task of covariance estimation boils down to the identification of an optimal , such that the resulting RIE is optimal with respect to (w.r.t.) some specified criterion.

In the high-dimensional regime (), a remarkable breakthrough in this line of research was the introduction of the linear shrinkage estimator by Ledoit and Wolf [27]. In this context, is derived through a (data-dependent) linear transformation of the sample eigenvalues . Subsequently, Ledoit and Wolf continued to excavate the potential of shrinkage methods by investigating the more flexible approach of nonlinear shrinkage of sample eigenvalues [28, 29, 30, 31, 32]. The introduction of these nonlinear shrinkage estimators coincided with significant advancements in random matrix theory (RMT), resulting in an additional level of performance improvement. One can refer to the systematic review provided in [34] for more details about this trajectory and extensive pointers to the literature.

To motivate our research about eigenvector overlaps in large sample covariance matrices, let us quickly revisit Ledoit and Wolf’s approach of constructing nonlinear shrinkage estimators. The first step involves selecting an appropriate loss function to quantify the estimation error. One can derive the minimizer of the optimization problem

| (1.3) |

That is, we operate within the class of RIEs and target at the optimal estimator that minimizes estimation error. For illustration, we consider the Frobenius loss , where denotes the Frobenius norm. In this situation, by elementary matrix algebra, one can easily show that the minimizer of (1.3) is given by the oracle shrinkages

| (1.4) |

i.e., the overlaps of sample eigenvectors w.r.t the population covariance. Consequently, the finite-sample optimal “estimator” is given by

with defined in (1.4). However, the “estimator” is not practically feasible since the shrunk eigenvalues involve the unknown population covariance . This explains why these values are termed “oracle”. Nevertheless, it signifies considerable progress as the problem has now been transformed from estimating parameters in the full population covariance matrix to the more amenable task of estimating eigenvector overlaps. This paves the way for the application of high-dimensional asymptotic results from RMT.

In the high-dimensional regime where is proportional to , Marčenko and Pastur’s groundbreaking work [36] established the weak convergence of , namely the empirical spectral distribution (ESD) of the sample covariance , to a certain limiting spectral distribution (LSD). Ledoit and Péché [26] extended this result by demonstrating the weak convergence of , i.e., the empirical spectral measure weighted by eigenvector overlaps. Specifically, it has been established that the Radon-Nikodym derivative of the weak limit of this weighted measure w.r.t. the Marčenko-Pastur law is given by for . Here represents the Stieltjes transform of the Marčenko-Pastur law. Refer to (2.3) below for its formal definition. This development gave rise to the introduction of the transitional shrinkages

| (1.5) |

The nonlinear shrinkage estimator based on the transitional estimates in (1.5) is still infeasible in practice due to its reliance on , the Stieltjes transform of the LSD. However, a practical estimator can be derived from these transitional quantities upon employing a consistent estimator of ,

| (1.6) |

In the early implementations by Ledoit and Wolf [29, 30, 32], the estimation of was accomplished through an indirect approach that involves a large dimensional optimization problem [33] to recover the spectrum of . However, due to the lack of an analytical solution for this optimization problem, implementing these numerical strategies is cumbersome and typically demands a considerable amount of computational time. In their follow-up work [28], Ledoit and Wolf devised a computationally more tractable implementation by integrating the kernel estimator of LSD developed in [23]. More recently, Benaych-Georges [5] suggested an even more direct approach, approximating by with some . Here, represents the Stieltjes transform of the ESD, which can be readily computed from the sample eigenvalues . This strategy has also been adopted in the algorithm developed in [6] for estimating cross-covariance matrices.

Both approaches in [28] and [5] result in effective and robust implementations of nonlinear shrinkage estimators. In [28], by drawing comparisons with the finite-sample optimal estimator , the practical performance of the algorithmic estimator

has been extensively validated through Monte Carlo simulations. Regarding the theoretical efficacy of , Ledoit and Wolf [28, 30] demonstrated that, under some technical assumptions,

| (1.7) |

Essentially, this means that asymptotically, the algorithmic implementation is equally effective as its oracle counterpart when minimizing the loss.

However, note that the evaluation of the loss incurred when estimating (1.4) with (1.6),

| (1.8) |

is still absent in the literature. From the perspective of practitioners, a quantitative evaluation of the loss (1.8) offers compelling justifications to employ as a feasible substitute for the oracle estimator . Moreover, an explicit convergence rate in terms of for (1.8) could provide theoretical supports for the fast convergence, in terms of loss, of towards as depicted in [28, Figure 4]. It is even more challenging to investigate each individual eigenvector overlaps

| (1.9) |

In view of the above this article focuses on the asymptotic behavior of the eigenvector overlaps within the context of large sample covariance matrices. We highlight that the results we establish are considerably more general than merely the convergence of the loss (1.8). Actually, we are able to quantify, in the high-dimensional regime, the convergence of each eigenvector overlap towards their corresponding deterministic counterparts. This even yields a satisfactory control, in terms of the operator norm, over the difference between and ,

More specifically, our main result covers the overlaps of the left/right singular vectors of the data matrix w.r.t. arbitrary deterministic matrices with bounded operator norms,

| (1.10) |

where the matrices are of compatible sizes. This level of flexibility in choosing the deterministic matrix enables us to manage various nonlinear shrinkage estimators induced by different loss functions [30, 32], extending our analysis beyond the Frobenius loss .

The methodology of this article, from a theoretical perspective, is inspired by the work of [12], which investigated eigenvector overlaps in the context of additively deformed non-Hermitian i.i.d. matrices. The research [12] is part of a broader effort led by Cipolloni, Erdős, Schröder, and their collaborators, focusing on the overlaps of singular vectors/eigenvectors in large random matrix ensembles. A pivotal aspect of this line of research is the development of the so-called multi-resolvent local law, which serves as a potent theoretical tool for inferring asymptotic properties of eigenvector overlaps. This ambitious project initially focused on resolving the eigenstate thermalization hypothesis (ETH) for the most fundamental prototype in RMT, the Wigner matrices [10, 13, 14, 15, 16]. Subsequently, the scope expanded to encompass random matrix ensembles involving full-rank deformation, including deformed non-Hermitian i.i.d. matrices [12], deformed Wigner matrices [11], and general Wigner-type matrices [20].

The sample covariance matrices examined in this article are subjected to a multiplicative deformation induced by the population covariance , which aligns our work with the studies [11, 12, 20]. This intrinsic anisotropy within the underlying random matrix ensembles forces the deterministic counterpart of to be energy-dependent, meaning it relies on both the observable and the location of . Consequently, these deformed ensembles pose a significantly more complex technical challenge compared to Wigner matrices, where asymptotically concentrates around the normalized trace of regardless of the index .

The situation is further complicated by the sparsity of eigenvalues near the edges of LSD. In fact, the studies [11, 12, 20] have predominantly concentrated on developing asymptotic results for the overlap of bulk eigenvectors, i.e., those corresponding to eigenvalues located in the bulk of the asymptotic spectrum. Essentially, this excludes eigenvectors associated with edge eigenvalues (e.g., with ). In this article, we venture into this challenging edge regime by conducting a meticulous analysis on resolvent chains involving spectral parameters close to the edges. Importantly, this rigorous effort leads to a nontrivial convergence rate for the overlap of edge eigenvectors, and significantly enhances our analysis of the nonlinear shrinkage estimators.

Finally, let us mention that apart from [5, 26], there are two additional research directions in the field of RMT concerning the asymptotic behavior of eigenvectors of large sample covariance matrices. Both directions focus on linear functionals of eigenvectors, i.e. with deterministic . One direction, represented by [1, 39, 40, 41, 45, 46], investigates the global behavior of eigenvectors by examining the LSD weighted by . In the presence of an additional finite-rank deformation, another direction, represented by [3, 8, 37], analyzes the almost sure limit and fluctuation of the spiked eigenvectors. Overall speaking, compared with the extensive literature on eigenvalues, there are relatively few works dedicated to eigenvectors. Furthermore, we highlight that for a general non-null , the analysis of individual eigenvectors of sample covariance matrices is notably scarce in the literature, and this article makes a progress in alleviating this situation.

To summarize, this article makes two key contributions. Firstly, we give more precise characterizations of the loss functions for estimating the population covariance matrix including the one from the algorithmic approximation of the oracle estimates for Ledoit-Wolf’s nonlinear shrinkage estimators in the high-dimensional regime. Secondly, we establish the convergence of overlaps for all individual left and right singular vectors of the data matrix, except for those in the null space, toward their respective deterministic counterparts with convergence rates.

The structure of this article is organized as follows. Section 2 presents the main result regarding the convergence of eigenvector overlaps. Section 3 characterizes the convergence rate of the loss functions of nonlinear shrinkage estimators. Section 4 is dedicated to our primary technical result, namely the multi-resolvent local laws for sample covariance matrices. Here, a crucial concept, the regularity of observables in resolvent chains, is introduced. In Section 4.3 we demonstrate how this powerful technical result is utilized to establish the main results discussed in Section 1. The subsequent sections delve into the proof of the multi-resolvent local laws, with a detailed organization provided at the beginning of Section 5.

Notations.

Throughout this article, we regard as the fundamental parameter and take . To streamline notation, we frequently suppress the dependence on from the notations, bearing in mind that all quantities that are not explicitly constant may depend on the asymptotic parameter . Given the -dependent nonnegative quantities and , we write if for some -independent constant . Here may implicitly depend on other quantities that are explicitly -independent (e.g., used in our assumptions below). We also write if both and hold.

We adopt the following notion of high probability bounds from [19] to systematize statements of the form “ is bounded with high probability by up to small powers of ”. For two families of nonnegative random variables parameterized by and ,

we say is stochastically dominated by , uniformly in , if for all (small) and (large) ,

| (1.11) |

In this case, we write . If is complex with , we also write . We refer to [7, Lemma 3.4] for the basic properties of .

Let be a class of square matrices indexed by . We define the normalized trace . It is worth noting that the normalization constant is given by the index rather that the dimension of . We also use to denote the standard inner product of two vectors of the same dimension. We consistently use to denote the Euclidean norm of the vector and to refer to the operator norm of w.r.t. the Euclidean norm. Finally, given positive integers , we let and abbreviate .

Acknowledgement.

The authors would like to express their sincere gratitude to Oliver Ledoit for bringing to our attention the importance of quantifying the convergence of the loss (1.8).

2 Singular vector/eigenvector overlaps

This section is to present our main results concerning the singular vector overlaps for the data matrix . First, the three singular vector overlaps in (1.10) can be unified as follows. Let

| (2.1) |

We can define . Then, constitute an orthonormal basis of and correspond to the eigenvectors of the self-adjoint dilation of ,

| (2.2) |

Here we also make the convention that

Now with the ’s, it suffices to target the overlaps for general deterministic matrices . Informally speaking, the main theoretical result of this article states that, in the high-dimensional regime, under certain regularity condition on the spectrum of ,

where the deterministic coefficients can be computed from the LSD for the ’s (or the ’s). The formal statement is presented in Theorem 2.2. Before that, we need to rigorously formulate the technical assumptions and recall some fundamental results from RMT that are necessary for a coherent presentation.

For the assumptions presented subsequently, we adopt the convention that represents a constant (independent of ) that can be chosen arbitrarily small.

Assumption 1 (High-dimension regime).

Suppose uniformly for all .

Assumption 2 (Data generating process).

We assume that , the matrix of observations, is generated according to , where the entries of are independent real random variables with and . Furthermore, we assume that there exist constants , for any , such that .

With Assumption 2, the sample covariance matrix can be expressed as . The remaining assumptions pertain to the LSD of . Assume that the eigenvalues of are given by

We make the following two basic assumptions to avoid problem degeneration.

Assumption 3 (Boundedness of ).

.

Assumption 4 (Anti-concentration at ).

.

Our next two assumptions concern the regularity of LSD of , and therefore require a more technical discussion. Before detailing these assumptions, let us gather several elementary results concerning the LSD of and its Stieltjes transform. Most of the subsequent statements, as well as their proofs, can be founded in [4, 24, 42].

For each , there exists a unique satisfying the self-consistent equation

| (2.3) |

Moreover, is the Stieltjes transform of a probability measure supported in ,

By slight abuse of terminology, we refer to the measure as the limiting spectral distribution (LSD) of . Rigorously speaking, represents LSD of the Gram matrix since almost surely, the Lévy-Prokhorov metric between and , the ESD of , converges to zero as . The measure possesses a continuous density on . In fact, by [42, Theorem 1.1], one can extend the definition of down to the real axis by setting

Then, the density of is given by . When there is no ambiguity, we also use to denote the density of . The following lemma characterizes the support of and can be found in [24, Lemma 2.6]. Note that .

Lemma 2.1.

Here we use to denote the number of bulk components of . Note that both and the edges may depend on via . We are now ready to state our assumptions on the regularity of the spectrum of , which essentially preclude pathological behaviors of the LSD . These regularity conditions have been previously discussed in various works on high-dimensional sample covariance matrices. The version we present here takes the same form as in [24]. For a more detailed explanation of the rationale behind these assumptions, we refer readers to [24] and the references therein.

We acknowledge a potential critique of Assumption 5 regarding its exclusion of spiked eigenvalues in the spectrum of . However, we anticipate that, through a straightforward perturbation argument, most estimates on eigenvector overlaps and the loss of shrinkage estimators presented in this article remain valid for non-spiked sample eigenvectors within a spiked population model. We have refrained from incorporating spiked eigenvalues due to the methodological differences in deriving shrinkage for such cases, which warrant an independent treatment. Interested readers can refer to the work of Donoho, Gavish and Johnstone [17] for a detailed exploration of shrinkage methods in the context of spiked population models.

Assumption 5 (Edge regularity).

Assume that the following holds for all ,

Assumption 6 (Bulk regularity).

Given any , there exists a constant such that

We note that Assumption 5 constrains to be bounded by some constant depending only on . Here the two assumptions are formulated in terms of . We mention that one can readily rephrase them using the LSD of the singular values of , or equivalently, the eigenvalues of . Actually, we find it convenient to introduce

where the probability measure can be related to via

In this article, we interchangeably use the LSDs and (and their Stieltjes transform and ). The choice of which one to use depends on the context.

As mentioned earlier, the behavior of eigenvector overlaps in our context is influenced by the positions of their corresponding eigenvalues. Hence, we introduce the concept of classical locations , which serve as the deterministic counterpart of the singular values . These classical locations can be defined as quantiles of as follows,

| (2.4) |

A profound result in RMT is the so-call singular value/eigenvalue rigidity. Essentially, with high probability, the singular values (reps. the eigenvalues ) are closed to their classical locations (resp. ) with a precision depending on . The details are presented in Proposition 4.3. To streamline the presentation, we also define the classical number of eigenvalues in the -th bulk component through

| (2.5) |

We note that it has been proved in [24, Lemma A.1] that for all . Now we can relabel the spectral components as follows,

| (2.6) |

The eigenvalues and the singular vectors can be defined in exactly the same way. Finally, let us introduce the main theoretical tool of this article, the resolvent (Green function),

| (2.7) |

The single-resolvent local law (see Proposition 4.2 below) asserts that whenever , the resolvent becomes asymptotically deterministic in the weak operator sense as . The deterministic surrogate is given by

| (2.8) |

Here we use to denote the top-left block of . Similar to , the function , and thus , also have a continuous extension to the real line from the upper half plane,

We are now prepared to rigorously present the main theoretical result of this article.

Theorem 2.2 (Eigenvector overlaps).

Corollary 2.3 (Singular vector overlaps).

Remark 2.4 (Convergence rate).

To gain insight into the convergence rate provided on the r.h.s. of (2.9) and (2.10), let us consider the simplest case where , meaning that contains only one bulk component. In this scenario, for , (2.10a) simplifies to

In the bulk regime where , this aligns with the convergence rate established in [12] for overlap of bulk singular vectors (in the context of a different random matrix ensemble). We anticipate this rate to be optimal, up to the arbitrary small prefactor introduced by the definition of .

This convergence rate gradually degrades when transitioning to the edge regime . Particularly, for eigenvectors corresponding to the largest eigenvalues, i.e., with , the convergence rate we obtain reduces to . While this still provides a nontrivial quantification of the convergence of edge eigenvector overlaps toward their deterministic counterparts, which is sufficient for our statistical motivation, we acknowledge the possibility of improving upon this rate to , as demonstrated for bulk eigenvectors. Considering the scope and length of this article, we defer this exploration to future work.

Remark 2.5 (Relationship with Ledoit and Péché’s result).

The quantiles strictly locate within the interior of , ensuring the strict positivity of the density in (2.9) and (2.10a). The maps and , up to a common factor, correspond to the asymptotic density of the measures and , respectively. In essence, precisely represents the Radon-Nikodym derivative as described in [26].

The concentration bound (2.10a) can be interpreted as a local refinement of Ledoit and Péché’s conclusion [26] regarding the weak convergence of . This is somewhat reminiscent of how the eigenvalue rigidity estimates refine the weak convergence of the ESD. Both the rigidity estimates and the concentration of eigenvector overlaps (first established in [21] and [13] respectively, in the context of Wigner matrices) suggest that, in the realm of RMT, we can generally expect more than mere global convergence; to some extent, finer control over each individual spectral component is achievable.

Remark 2.6 (Energy dependency).

The energy dependency of the deterministic counterparts of the eigenvector overlaps only manifests in the estimate (2.10a) and is absent from (2.10b) and (2.10c). This is consistent with the structure of as outlined in (2.8): the anisotropy is confined to its upper-left block. In fact, in the null case where , this anisotropy vanishes, and (2.10a) becomes energy independent,

We remark that the estimate (2.10b) on right singular vectors closely resembles the corresponding estimates regarding eigenvectors of Wigner matrices [10, 13]. Moreover, we observe that the overlaps of right singular vectors of the matrix share the same asymptotic limit as those of the undeformed matrix . Consequently, we can conclude that, up to the first-order behavior, the left multiplicative deformation has no impact on the overlaps of right singular vectors. However, whether this deformation affects higher-order behaviors of , such as fluctuation, requires further investigation.

Finally, let us underline the distinctive pattern exhibited by (2.10c) compared to its counterpart [12, Equation (2.8c)] for additively deformed i.i.d. square matrices. For the undeformed matrix with Gaussian entries, the estimate (2.10c) can be easily derived from the independence between the left and right eigenvectors. This result is anticipated to hold for with a general entry distribution due to universality. Our estimate (2.10c) suggests that the left multiplicative deformation maintains this weak correlation between the ’s and the ’s. Contrastingly, an additive deformation as in [12], would disrupt this weak correlation, causing the overlap to concentrate around a nonzero deterministic quantity.

3 Ledoit-Wolf’s nonlinear shrinkage estimators

In this section, we utilize the estimate (2.10a) to conduct a finite-sample analysis of Ledoit-Wolf’s nonlinear shrinkage estimators. We mention that our results regarding eigenvector overlaps, as presented in Section 2, do not cover those eigenvectors in the null space of . Therefore, to facilitate discussion, we introduce the following additional assumption to ensure the invertibility of . The investigation of eigenvectors in null space of is deferred to future work.

Assumption 7 (Invertibility of ).

Suppose and uniformly for all .

Note that Assumption 7 automatically implies Assumptions 1 and 4. However, for simplicity, we still state the subsequent result under Assumptions 1-7. With Assumption 7, it is not difficult to verify that the relabelling introduced in (2.6) satisfies . As per the regularity of the leftmost edge of ensured by Assumption 5, as well as the eigenvalue rigidity estimate (4.8), this implies that , the smallest eigenvalue of , is bounded below by some positive constant with high probability. Also note that now the estimate (2.10a) encompasses all the eigenvectors of .

The derivation of Ledoit-Wolf’s nonlinear shrinkage estimators has been previously outlined. The transition from the finite-sample optimal yet infeasible shrinkage (1.4) to the practical algorithmic one (1.6) hinges on the deterministic counterparts of eigenvector overlaps as described in (2.10a). Actually, by setting and utilizing (2.3), it is straightforward to verify that the formula of the transitional shrinkage introduced in (1.5) aligns with this Radon-Nikodym derivative in (2.10a). The only difference is that, in (1.5) the classical eigenvalue locations are replaced by their empirical counterparts , whose impact is amenable due to eigenvalue rigidity (4.8).

It is worth noting that this strategy extends beyond the Frobenius loss and can be applied to various loss functions with statistical backgrounds, as explored by Ledoit and Wolf [30, 32]. Hence, besides the Frobenius loss, we also discuss another representative loss function, the so-called inverse Frobenius loss , which essentially represents the Frobenius loss for estimating the precision matrix . The corresponding formulas for the finite-sample optimal, transitional and algorithmic shrinkages under are detailed in Table 1. In this case, the transitional shrinkages are derived by setting in (2.10a).

| Loss function | Frobenius | Inverse Frobenius |

|---|---|---|

| Formula of loss | ||

| Optimal | ||

| Transitional | ||

| Algorithmic |

For a rigorous investigation of these algorithmic shrinkage estimators, it is necessary to clarify how , the Stieltjes transform of the LSD, is estimated. A natural estimator of is its empirical counterpart, the Stieltjes transform of the ESD of ,

| (3.1) |

Note that we have let . However, directly setting is not viable due to the singularity of at . As previously discussed, currently there exist two computationally efficient solutions for this issue. One strategy, proposed by [28], involves the use of a kernel to smooth the ESD, thereby enabling the evaluation of its Stieltjes transform at . Another approach, suggested by [5], incorporates an additional imaginary part for the spectral parameter to mitigate this singularity,

| (3.2) |

In this article we adopt the latter approach for analysis, as it is more transparent from the perspective of RMT. Another motivation for this selection is to circumvent the introduction of additional notations caused by kernel smoothing, which could potentially complicate the work. Nevertheless, we emphasis that this choice is not particularly significant, as the finite-sample analysis in this article can be straightforwardly adapted to analyze the shrinkage estimators implemented in [28]. In fact, the most formidable aspect of the analysis lies in quantifying the loss from the finite-sample optimal shrinkages to the transitional ones, which is addressed by our main estimate (2.10a). Conversely, the loss from the transitional shrinkages to the algorithmic ones is relatively manageable in viewing of existing tools [23, 24].

Algorithm 1 below outlines the entire estimation process, where we operate under the Frobenius loss. Its adaption to the inverse Frobenius Loss is straightforward using Table 1 and (3.2). Note that in Algorithm 1 we have locally adapted the scale parameters to ensure that the resulting estimator fulfills the scale-equivariant property discussed in [28].

-

(1)

Set with ;

Compute the Stieltjes transform ;

Calculate the shrunk eigenvalue ;

We are now in a position to present our main statistical finding concerning the finite-sample performance of nonlinear shrinkage estimators.

Theorem 3.1 (Nonlinear shrinkage estimators).

Let be some -dependent scale parameter satisfying , where is a small constant. Suppose that is the nonlinear shrinkage estimator obtained from Algorithm 1. Recall the relabelling introduced in (2.6). Then, under Assumptions 1-7, we have the entrywise bound

| (3.3) |

where , and . Consequently, in terms of the loss function, we have

| (3.4) |

In addition, if is the estimator derived by adapting Algorithm 1 to the inverse Frobenius loss (defined in Table 1), then the estimates (3.3) and (3.4) also hold for .

Considering the r.h.s. of the bound (3.4) on the loss, a favorable choice for the scale parameter is . With this choice, we have the following corollary of Theorem 3.1.

Corollary 3.2 (Nonlinear shrinkage estimators with ).

It should be emphasized that Theorem 3.1 and Corollary 3.2 are not intended to justify the convergence of toward the population covariance . Actually, according to [30, Theorem 4.2], the loss is typically of a constant order. In other words, within the class of RIEs, even the finite-sample optimal estimator is incapable of achieving consistency without additional structural assumptions on . The primary contribution of Theorem 3.1 and Corollary 3.2 lies in quantifying the loss incurred when employing as a feasible surrogate for . Fortunately, with an appropriate choice of the scale parameter , it is found that this loss is dominated by the rate of , which is sufficiently rapid to convince the practitioners to adopt the algorithmic estimator as an approximation of .

As highlighted, our approach actually yields a more general entrywise estimate (3.5) that goes beyond just assessing the loss. This entrywise estimate even implies the convergence of toward in terms of the operator norm. However, it should be noted that, akin to Theorem 2.2, we do not seek for the optimal convergence rate for those indices corresponding to the eigenvalues near the spectral edges. Consequently, there is potential to enhance this rate for the edge regime, thus refining the resulting convergence rate of .

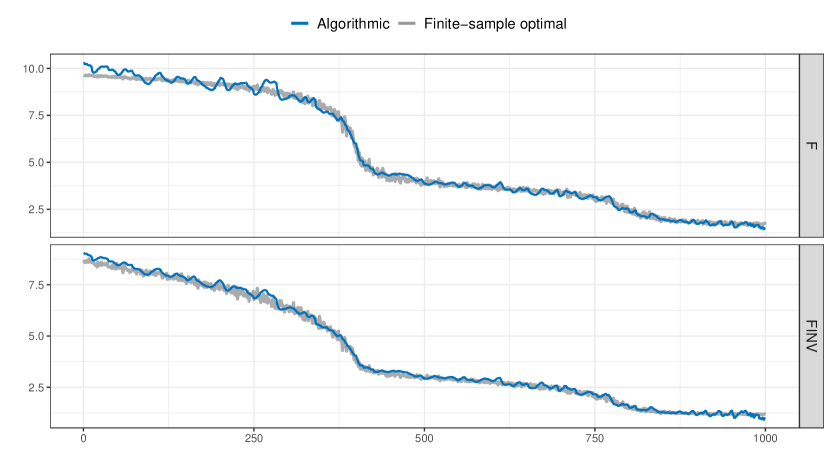

The entrywise convergence (3.5) is depited in Figure 1, where the finite-sample optimal shrinkages (resp. ) and their algorithmic counterparts (resp. ) are juxtaposed. These values are computed from a sample covariance matrix. In this Monte Carlo simulation, we allocate of the population eigenvalues as , as , and as , a configuration notably discussed and analyzed in detail by [2]. Refer to [28] for a comprehensive simulation study on the loss of nonlinear shrinkage estimators under this population covariance setting. For the simulation corresponding to Figure 1, a sample size of is used, the scale parameter is set as , and is generated from i.i.d. normal variables of zero mean and variance . The simulation results confirm our theoretical findings: an entrywise alignment of the algorithmic shrinkages with the finite-sample optimal ones is observed.

Remark 3.3 (Probabilistic bounds).

As previously clarified, the notation is used to signify that “ is bounded with high probability by up to small powers of ”. Nevertheless, it would be beneficial to further elaborate on this notation in (3.5) and (3.6), and to rephrase these bounds in a way that statisticians are more accustomed to.

Firstly, we remark that the entrywise bound in (3.5) is uniform across indices and . As the cardinality of the corresponding index set is bounded by powers of , a simple union bound allows the interchange of with the supremum over indices in (1.11), without degrading the probability tail. Specifically, for arbitrary (small) and (large) , we have

for all sufficiently large .

Similarly, one can use the definition (1.11) to explicitly formulate the probabilistic bounds on and . Here we would like to mention the compatibility of with . Specifically, if satisfies , and is a deterministic control parameter with , where is some large constant, then implies . See e.g. [7, Lemma 7.1]. Consequently, the first bound in (3.6) implies that, for arbitrary (small) , we have

for all sufficiently large .

Remark 3.4 (Loss functions).

As previously noted, Ledoit and Wolf [30, 32] have explored various loss functions with statistical background. Notably, both the inverse Stein loss and the minimum variance loss yield the same finite-sample optimal shrinkages as the Frobenius loss. Consequently, the analysis of estimators derived from these loss functions is fundamentally similar, with the exception of using a different formula when evaluating the loss. Overall speaking, this evaluation is not difficult to achieve by leveraging the entrywise bound (3.5).

4 Multi-resolvent local laws

4.1 Single resolvent local laws and matrix Dyson equation

This section provides a concise overview of the single resolvent local laws for sample covariance matrices [4, 24] and the matrix Dyson equation [18]. For a more comprehensive introduction to these topics, readers are encouraged to explore the works cited and the references therein.

The spectral parameter we consider always falls into the fundamental domain

| (4.1) |

where is some sufficiently small constant (depending only on ). Throughout this article, we reserve for the spectral parameter of the functions , and , and for the spectral parameter of . It is worth noting that for any , one can uniquely revert from its square through , where the square root is selected to have a branch cut along the negative real line. Consequently, functions of can effortlessly be regarded as functions of , and vice versa. Throughout the subsequent discussion, we will frequently utilize this one-to-one correspondence without further explanation.

Thanks to Assumption 5, the following comparison holds uniformly for and ,

| (4.2) |

We denote the distance of to the real line and the closest spectral edge as

| (4.3) |

The following lemma summarizes some basic estimates regarding the Stieltjes transform , specifically ensuring the boundedness of the deterministic approximation .

Lemma 4.1 (Basic properties of ).

| For sufficiently small (depending only on ), the following estimates hold uniformly for , | |||

| (4.4a) | |||

| In addition, we have that follows from | |||

| (4.4b) | |||

Apart from the apparent comparison between and , the estimates in Lemma 4.1 have already been established in [4, 24] in terms of . Specifically, the estimate for can be proved as in [4, Theorem 3.1]. The estimates for and have been established in [24, Lemma A.4] near the edge and in [24, Lemma A.6] in the bulk.

According to (4.4a), it is possible for the “density” to be much smaller than if and . This low-density regime presents challenges for theoretical analysis, as many parts of our proof require a lower bound on . Consequently, for most of the results presented in this paper, we need to exclude this regime and focus on the spectral parameters from

| (4.5) |

Note that this definition guarantees uniformly for .

Notations.

Let us make some notational conventions before proceeding. We frequently identify the matrices and with their natural embeddings in , i.e.

We also introduce the matrices

| (4.6) |

When there is no ambiguity, we use the abbreviations and .

We often use the letter to represent indices within , while reserve for indices within (or , depending on the specific context). Hence, summation over (resp. ) without further specification should be interpreted as (resp. ). Continuing with this convention, we denote the canonical bases of and as and , respectively. These two set of vectors can also be identified with their natural embeddings in , so that their union constitutes the canonical bases of .

We now present the single resolvent local laws for sample covariance matrices, both in averaged and isotropic form, established in [24, Theorem 3.6].

Proposition 4.2 (Single resolvent local laws).

As a standard corollary of the single resolvent local laws, we have the following rigidity result, obtained in [24, Theorem 3.12], which offers large deviation bounds on the locations of individual singular values/eigenvalues.

Proposition 4.3 (Singular value/eigenvalue rigidity).

Although Proposition 4.2 is stated for spectral parameters with positive real parts, its extension to parameters with negative real parts is straightforward thanks to the chiral symmetry

| (4.9) |

The approach employed in [24] to establish Proposition 4.2 is essentially grounded in the Schur complement formula. Here, we opt for the approach of cumulant expansion (reduced to Stein’s lemma when dealing with Gaussian variables), which offers greater adaptability for deriving multi-resolvent local laws. The cumulant expansion formula presented here can be derived through a slight modification of [35, Proposition 3.1].

Lemma 4.4 (Cumulant expansion formula).

Let be fixed and . Supposed is a centered real random variable with finite moments to order . Denote the -th cumulant of by . Then, we have the expansion

| (4.10) |

assuming that all expectations on the r.h.s. exist. The remainder term satisfies, for any ,

To apply the cumulant expansion formula (4.10) to the resolvent , we start by representing the self-adjoint dilation as a sum of independent rank- matrices,

Given any differentiable , we define its derivative w.r.t. as

In particular, we have

| (4.11) |

Definition 4.5 (Second-order renormalization).

Let . Following [13], we define the second-order renormalization of , denoted with an underline, as

| (4.12) |

The summation in (4.12) essentially corresponds to the second-order term in the cumulant expansion formula (4.10). Particularly, when the ’s are Gaussian variables, we have . Therefore, by concentration and universality, it is reasonable to expect that this summation captures the leading term of , and in a certain sense, collects the terms that are subleading to this term.

Utilizing (4.11) and , we have by definition

| (4.13) |

where we introduced the linear operator on matrices,

| (4.14) |

Note that we can decompose , with

| (4.15a) | ||||

| (4.15b) | ||||

The motivation behind this decomposition is that, given any , the image is block-diagonal, whereas is block-off-diagonal. In the context of this paper, for terms involving , the primary contribution is typically captured by the part involving , whereas the contribution from the part involving is negligible up to the leading order. This is not surprising since the prefactor in (4.15b) inherently diminishes the importance of .

Now, referring to (4.13) and the preceding discussion, it is reasonable to expect that , the deterministic approximation of , satisfies the following so-called matrix Dyson equation (MDE)

| (4.16) |

This is exactly the case for defined in (2.8). Actually, utilizing the self-consistent equation (2.3), we know that can also be characterized as the unique solution to

| (4.17) |

4.2 Multi-resolvent local laws with regular matrices

As previously mentioned, the key technical result of this paper, leading to Theorem 2.2, is the multi-resolvent local laws, which extend Proposition 4.2 to chains of resolvents and deterministic matrices. For our purposes, we primarily focus on resolvent chains of length or ,

| (4.18) |

where are deterministic matrices. Here we also abbreviate . For what follows, we frequently use such abbreviations to streamline notation when there are multiple spectral parameters. Similar to the single resolvent local laws, we can identify certain deterministic matrices, dependent on the spectral parameters as well as the matrices , that asymptotically serve as the deterministic approximation (in weak operator sense) of these resolvent chains. Let us denote the deterministic approximations for the two resolvent chains in (4.18) respectively by

whose definitions are to be clear in (4.22) below. As highlighted in [12, 16], these deterministic approximations cannot be directly obtained by substituting the ’s with the ’s in (4.18). Instead, they can be derived from the so-called recursive Dyson equations, for which we refer to the derivations in Section 6 as well as [12, Appendix D].

To this end, we introduce the two-body stability operator

| (4.19) |

We also define as the inverse operator of . In other words,

| (4.20) |

Note that notations can be interpreted analogously. Using (4.15a), one can easily verify that for generic matrices and . Consequently, the two operators and can be related through

| (4.21) |

where and are general matrices with compatible dimensions.

Definition 4.6 (Deterministic approximations).

Given deterministic matrices and spectral parameters , we set , and define

| (4.22a) | ||||

| (4.22b) | ||||

Here the identities in (4.22) directly follow from (4.19) and (4.20). In fact, we have

Alternatively, the equivalence between the definitions in (4.22) can be obtained by expanding different resolvents in the chain. For more details, see [12, Appendix D] , where the reader can also find how to generalize Definition 4.6 to accommodate chains involving more than three resolvents.

We proceed to derive an explicit formula for the operator defined in (4.20). Given spectral parameters , we define the divided difference

| (4.23) |

and introduce the quantities (with indicating “top” and referring to “bottom”)

| (4.24a) | ||||

| (4.24b) | ||||

Now let be a deterministic matrix. We denote its top-left diagonal block by and bottom-right diagonal block by , i.e.

Set . Utilizing (4.15a) and (4.20), we have

| (4.25) |

Multiplying both sides of (4.25) by and , respectively, and taking the normalize trace, we obtain

Solving these equations leads to

Plugging this back into (4.25) yields

| (4.26) | ||||

Now we would like to conduct a stability analysis of the operator in the local regime so as to motivate the introduction of regular observables in Definition 4.8 below. Specifically, our goal is to obtain an asymptotic estimate of for and with . In viewing of (4.26) and Lemma 4.1, the most trivial estimate is that

| (4.27) |

The magnitude of is significantly influenced by whether the two parameters lie in the same half-plane. To this end, for , we let

The next lemma offers several estimates of the divided difference that are crucial for subsequent analysis, and its proof is presented in Section 7.1.

Lemma 4.7 (Divided difference).

| By letting sufficiently small (depending only on ), we have the following estimates uniformly for with , | ||||

| (4.28a) | ||||

| (4.28b) | ||||

| Moreover, for with , we have | ||||

| (4.28c) | ||||

For what follows, we consistently assume that is chosen to be sufficiently small, dependent only on , such that the estimates in Lemmas 4.1 and 4.7 hold.

The upper bound in (4.28b) is indeed tight, as evident by setting . Suppose we are given with . Let us abbreviate and . Now, with Lemmas 4.1 and 4.7, it is apparent that the estimate (4.27) yields

Suppose, for simplicity, that . Then, this upper bound is essentially of order in the bulk, gradually transitioning to as we approach the edges.

Conversely, the trivial bound (4.27) greatly improves if , the numerator of the fraction in the second line of (4.26) is sufficiently small to counterbalance the singularity induced by the denominator. This prompts us to examine the regular observables defined as follows.

Definition 4.8 (Regular observables).

Let . We introduce the control parameter

| (4.29) |

Let be a deterministic matrix, with its diagonal block given by and , respectively. We say that is -regular if , and

| (4.30) |

Lemma 4.9 (Basic properties of regular observables).

We have the following statements regarding the regular observables as defined in Definition 4.8. For statements (i)-(iv), we assume that and is -regular.

-

(i)

is -regular for .

-

(ii)

are -regular.

-

(iii)

is -regular.

-

(iv)

for .

-

(v)

Among the four constraints listed in (4.30), the two constraints with are implied by either of the two constraints with .

The proof of Lemma 4.9 is provided in Section 7.2. Now, one can compare the bound obtained in Lemma 4.9 (iv) with the trivial bound in (4.27). Note that Definition 4.8 is actually formulated for a sequence of matrices . Therefore, there should be no ambiguity in the use of the asymptotic notation . Moreover, in the global regime , the condition (4.30) plays no role, as in this case we have according to Lemma 4.7.

Compared with the regular observables given in [12, Definition 3.1], our definition is adapted to moderately tolerate the deviation of from zero. This adaption offers greater flexibility and accommodates the edge regime, thereby significantly enhancing our proof.

The next lemma provides bounds on the deterministic approximations defined in (4.22) when the matrices are regular. It is a straightforward corollary of (4.26) and Lemma 4.7.

Lemma 4.10 (Bounds on the deterministic approximations).

Let and for , let be -regular as per Definition 4.8. Then, we have

| (4.31) |

The multi-resolvent local laws in this article are formulated for resolvent chains with regular matrices. For such resolvent chains, not only does the magnitude of the deterministic approximation decrease significantly (as depicted in Lemma 4.10), but so does the corresponding approximation error. Let us first clarify the concept of regularity in resolvent chains.

Definition 4.11 (Regular observables in resolvent chains).

Consider one of the two expressions

for some fixed length , where and are deterministic matrices. For any , we call regular (w.r.t. its surrounding parameters) if it is -regular as per Definition 4.8. In case of the first expression above (i.e. in averaged form), the indices are understood cyclically modulo (i.e. ).

We are now ready to present our the main technical achievement of this article. The multi-resolvent local laws we develop are applicable to spectral parameters within the domain

| (4.32) |

Theorem 4.12 (Local laws with regular matrices).

Fix arbitrary (small) . Under Assumptions 1-6, we have the following local laws uniformly in , deterministic vectors with , and deterministic matrices , that are regular w.r.t. their surrounding parameters.

-

(i)

Averaged law with one regular matrix:

(4.33a) -

(ii)

Isotropic law with one regular matrix:

(4.33b) -

(iii)

Averaged law with two regular matrices:

(4.33c) -

(iv)

Isotropic law with two regular matrices:

(4.33d)

The key estimate driving our theoretical result on eigenvector overlaps is (4.33c), with the other three estimates being byproducts obtained during the derivation of this primary estimate. It is worth noting that all the estimates in (4.33) provide nontrivial error bounds, considering the typical order of the deterministic approximations outlined in Lemma 4.10. The prefactors and in the error bounds of (4.33c) and (4.33d) suggest that these rates may not be optimal. However, we refrain from optimizing over these rates as (4.33c) is already sufficient for our intended application.

4.3 Proof of the main results

In this section, we provide the proof of our main results, Theorems 2.2 and 3.1, utilizing the averaged law with two regular matrices (4.33c). Prior to that, let us introduce the notion of one-point regularization, which projects an arbitrary matrix with bounded norm into the class of regular matrices. It is worth noting that there are multiple ways to regularize a matrix, and the choice is not unique. Here, we utilize (4.34) since it aligns well with our proof.

Lemma 4.13 (One-point regularization).

Let be a deterministic matrix with . Suppose its top-left and bottom-right diagonal blocks are given by and , respectively. For , we define the one-point regularization of w.r.t. as

| (4.34) |

Equivalently, we can write

| (4.35) |

Suppose such that . Then, is -regular.

Without loss of generality, in the proofs of Theorems 2.2 and 3.1, we assume that , meaning contains only one bulk component and the classical number of eigenvalues in this component is given by . The extension to the case of multiple bulk components is straightforward and thus omitted.

Proof of Theorem 2.2.

Fix arbitrary (small) and (large) . Let . Recalling the classical locations defined in (2.4), we introduce the spectral parameters

where the scales are specified as

By the rigidity estimates in Proposition 4.3, we have with probability at least ,

| (4.36) |

Given any deterministic with , let be its one-point regularization w.r.t. as defined in (4.34). Thanks to Lemma 4.13 and Lemma 4.9 (i), (ii), we know that both and are -regular, where and . Therefore, by utilizing the averaged law with two regular matrices (4.33c) in Theorem 4.12, along with the bound from Lemma 4.10, we have

Since , the above bound readily implies, with probability at least ,

On the other hand, whenever the rigidity estimate (4.36) holds, we have

In other words, we have established, with probability at least ,

Now, it remains to reduce the l.h.s. of the preceding inequality to the l.h.s. of (2.9). Utilizing the definition of one-point regularization in (4.35), along with and , we have

Here for the coefficient we can employ the equations (7.12a) and (7.12c) below to get

where we also used the estimates in Lemmas 4.1 and 4.7 in the last step. We mention that although the equations/estimates for and we employ here are originally stated for with , their validity remains intact as . Summarizing the three equations above concludes the proof. ∎

Proof of Theorem 3.1.

As mentioned, we assume to simplify the presentation. Additionally, note that this proof is conducted under the additional Assumption 7, which implies when . Algorithm 1 and Theorem 3.1 are formulated using the spectral parameters and the Stieltjes transform . However, for the sake of notation simplicity, we opt to formulate this proof in terms of and the Stieltjes transform

Importantly, this switch in spectral parameters does not alter the essence of the argument. Moreover, according to the eigenvalue rigidity estimate (4.8), it suffice to work with the high-probability event where the singular values adhere closely to their classical locations,

In particular, for a sufficiently large constant , we have uniformly across and . Consequently, we can, without loss of generality, suppose that .

Now, regarding the entrywise estimate (3.3), we need to prove

| (4.37) |

By setting in (2.10a), we obtain

where we utilized computed from (4.17). This corresponds to the first fraction on the r.h.s. of (4.37). Next, we leverage the estimates from Lemmas 4.1 and 4.7 to obtain

Here, using the triangle inequality, we have

On the one hand, by incorporating the definition of the classical locations along with the square root behavior of the density of the LSD around its edges111See e.g. [4, Theorem 3.1]. Alternatively, we can derive this square root behavior by of by letting in the estimate of as given by (4.4a)., it is not difficult to verify that

On the other hand, by eigenvalue rigidity and the range of we have

Combining these estimates together yields the second fraction on the r.h.s. of (4.37),

| (4.38) |

Finally, we employ the single resolvent local law (4.7) to obtain

where the supremum is taken over with . The estimate above corresponds to the last fraction on the r.h.s. of (4.37). By combining these estimates, we conclude the proof of (4.37).

To prove (3.4), let us recall that the partial order is preserved under summation over a set whose cardinality bounded by powers of ,

Here, the summation over the first fraction can be dominated by

Similarly, for the summation over the second fraction, we can control it by

This completes the proof of (3.4) for the Frobenius loss. Regarding the adaption to the inverse Frobenius loss, the argument remains essentially the same, except that we need to employ the estimate for eigenvector overlaps of the form . To derive the deterministic counterpart in (2.10a) for , we utilize (4.17) again to obtain

which implies that

Note that the ’s serve as the classical location for the eigenvalues . Hence, the formula above illustrates how the transitional shrinkages are obtained. ∎

5 Self-improving inequalities

For the subsequent sections, we delve into the proof of Theorem 4.12. Our methodology for proving the multi-resolvent local laws draws inspiration from [12]. The overarching strategy hinges on deriving a system of self-improving inequalities (Proposition 5.4) that encapsulate the errors in approximating the resolvent chains with their deterministic counterparts. The term “self-improving” implies that these inequalities can be iterated a certain number of times (see Lemma 5.5) to attain the desired error bound. The primary distinction in the analysis of this article, compared to that in [12], lies in the inclusion of the intricate edge regime, where the Stieltjes transform loses its Lipschitz continuity. Our analysis heavily rely on the -Hölder continuity of near the spectral edges, as demonstrated by Lemma 4.7. This reliance is evident in the proofs of Lemmas 6.3 and 6.4 concerning the coefficients introduced by regularization of certain matrices. It is worth noting that while the arguments in this article are complicated by the inclusion of the edge regime, the overall proof remains concise, thanks to our flexible definition of regular observables, which circumvents redundant steps of regularization that contribute less to the overall argument.

We organize the proof as follows. Before delving into details, Section 5.1 introduces several definitions and lemmas that are utilized throughout the proof. In Section 5.2, we present Proposition 5.4, which establishes the system of self-improving inequalities as mentioned above. Leveraging this result, we deduce the multi-resolvent local laws with regular matrices through iteration. The subsequent sections are dedicated to deriving Proposition 5.4. A key element of this derivation is Proposition 5.6, which represents errors in approximating the resolvent chains with their deterministic counterparts as second-order renormalization, up to negligible terms. The proof of this result, which involves considerable effort, is addressed in Section 6. Section 5.3 presents the derivation of the self-improving inequalities by incorporating this representation with the cumulant expansion formula (4.10). The contributions from second and higher cumulants in this expansion are quantified in Section 5.4 and 5.5, respectively. Finally, most proofs of the technical lemmas are consolidated in Section 7 to maintain the coherence of the main argument.

5.1 Preliminaries

To streamline the notations, we employ to represent the errors incurred in approximating the resolvent chains with their deterministic counterparts,

| (5.1a) | ||||

| (5.1b) | ||||

| (5.1c) | ||||

For , we introduce the normalized differences

| (5.2a) | ||||

| (5.2b) | ||||

where we used the short hand notation . We also introduce the following control parameters concerning the uncentralized forms of resolvent chains containing regular matrices, ,

| (5.3a) | ||||

| (5.3b) | ||||

Recall the definitions of the spectral domains and as defined in (4.5) and (4.32), respectively. Due to our utilization of Cauchy’s integral formula (5.5) below, when handling spectral parameters within a specific domain, we might have to rely on estimates for those parameters from a slightly broader domain. As our estimates are refined through iteration, we need to introduce a sequence of nested domains that progressively approach our target domain .

Lemma 5.1 (Nested spectral domains).

Fix some (small) and let be some sufficiently small constant depending only on . Given arbitrary (large) , there exists a sequence of nested spectral domains , , such that

and the following statements hold for every ,

-

(i)

is formed by the union of disjoint convex polygons.

-

(ii)

whenever .

-

(iii)

for all , where the domain is understood as and the constant is -independent.

There are various approaches to construct the spectral domains to fulfill the conditions outlined in Lemma 5.1. However, the specific construction of these domains is not essential for subsequent discussions. Therefore, we refrain from providing a formal proof for Lemma 5.1. Nevertheless, for visual clarity and reader comprehension, we depict one possible construction of the ’s in Figure 2 along with a brief description of their formation. We also remark that the motivation behind imposing requirement (iii) is clarified in (7.20). For what follows, we fix some sufficiently large and consistently refer to , , as a sequence of spectral domains that satisfy the requirements specified in Lemma 5.1.

The subsequent two identities are utilized to simplify the analysis of resolvent chains involving by reducing them to shorter ones.

Lemma 5.2.

Let with . We have the resolvent identity

| (5.4) |

Moreover, by Cauchy’s integral formula, for with we have

| (5.5) |

where the boundary is oriented counter-clockwise.

Next, let us make some conventions for statements regarding stochastic domination. Consider a family of nonnegative random variables, . Throughout the proof, we reserve the letter to denote regular matrices, while use to refer to generic deterministic matrices. Let be some deterministic control parameter depending only on and . For the sake of brevity, we consistently use streamlined statements like

to indicate that is stochastically dominated by , uniformly for spectral parameters , deterministic matrices regular in the sense of Definition 4.11, as well as generic deterministic matrices and vectors with bounded norms. We even omit the mention of when the spectral domain is evident from the context.

With the notations introduced above, our objective, the local laws presented in Theorem 4.12, can be rephrased as follows,

The following inductive hypothesis is frequently employed in our proof,

| (5.6) |

where are deterministic control parameters depending only on and . In light of Lemma 4.10, it is not difficult to see that if we introduce

| (5.7) |

then we have the following bounds provided (5.6),

| (5.8) |

As will be demonstrated later, our application of the cumulant expansion formula (4.10) frequently involves resolvent chains containing more than two regular matrices. To avoid directly dealing with these quantities, we rely on the following reduction lemma, which simplifies the analysis of these longer resolvent chains to shorter ones, albeit with the inclusion of a prefactor (powers of ) that is manageable for our purposes. Its proof is presented in Section 7.4.

Lemma 5.3 (Reduction inequalities).

Suppose we have (5.6). By introducing the control parameters

| (5.9) |

we have the following bounds

| (5.10) |

Moreover, if the matrices below are regular w.r.t. their surrounding spectral parameters, then we also have the following bounds uniformly in ,

| (5.11) |

5.2 Self-improving inequalities: proof of Theorem 4.12

We are now in a position to present the system of self-improving inequalities that leads to our multi-resolvent local laws (4.33). It is worth noting that the resolvent chains involving more than two regular matrices have already been processed by Lemma 5.3. Consequently, the inequalities in (5.12) below do not involve control parameters with indices larger than .

However, as previously mentioned, the reduction inequalities in Lemma 5.3 are unable to accurately capture the magnitude of the forms and . The large prefactor in (5.9) ultimately leads to the non-optimal convergence rate in the local laws (4.33c) and (4.33d). In the context of Wigner matrices [14, 15], this issue is circumvented by extending the derivation of self-improving inequalities to , and using refined estimates of and to achieve the optimal estimate for and . We could have adopted this strategy to enhance our estimates in Proposition 5.4 and Theorem 4.12. However, considering the complexity of our regularization compared to Wigner matrices, implementing such a strategy would significantly lengthen the arguments. Given the scope and focus of this article, we defer this technical improvement to future research.

Proposition 5.4 (Self-improving inequalities).

Given (5.6), we have the following uniformly in ,

| (5.12a) | ||||

| (5.12b) | ||||

| (5.12c) | ||||

| (5.12d) | ||||

The following simple argument is repeatedly utilized in the proof of Theorem 4.12 and can be found in [12, Lemma 4.11].

Lemma 5.5 (Iteration).

Fix some every (small) and (large) . Suppose that is a family of nonnegative random variables satisfying on , and for every fixed ,

where are deterministic control parameters. Then, there exists some such that the following holds: for every fixed ,

We are now ready for the proof of our multi-resolvent local laws with regular observables.

Proof of Theorem 4.12.

We can initiate the iteration procedure with the following trivial estimate that directly follows from ,

Summing up the inequalities (5.12a) and (5.12b) yields,

Therefore, by employing Lemma 5.5, we find that for some sufficiently large ,

| (5.13) |

Plugging (5.13) into (5.12c), we arrive at

By leveraging Lemma 5.5 again, we obtain the following estimate,

| (5.14) |

Finally, inserting (5.13) and (5.14) into (5.12d), we conclude with

This, according to Lemma 5.5, implies that uniformly in Now the proof completes upon plugging this estimate back into (5.13) and (5.14). ∎

5.3 Cumulant expansion: proof of Proposition 5.4

The remainder of Section 5 is dedicated to deriving the self-improving inequalities (5.12). As mentioned, the argument hinges on the cumulant expansion formula (4.10) in conjunction with the following proposition, which expresses the centralized forms of resolvent chains as fully underlined terms. One can compare Proposition 5.6 with its counterpart in [12]. The primary difference is that here we require the regularity of instead of itself. This distinction arises from the anisotropic nature of the operator in our context.

Proposition 5.6 (Representation as fully underlined).

Given (5.6), there exists a deterministic matrix that depends linearly on , such that is -regular and

| (5.15a) | ||||

| (5.15b) | ||||

| (5.15c) | ||||

| (5.15d) | ||||

where the error terms are controlled by the parameters

| (5.16a) | ||||

| (5.16b) | ||||

| (5.16c) | ||||

| (5.16d) | ||||

The proof of Proposition 5.6 is detailed in Section 6. Here, let us focus on the proof of Proposition 5.4. The following identity is useful when dealing with the second-order contribution that arises in cumulant expansion. For generic matrices , we have

Furthermore, we remark that it suffices to derive the self-improving inequalities (5.4) under the assumption that the regular matrices and the vectors appear are all real.

Derivation of (5.12a): By definition of the second-order renormalization (4.12), we have

Therefore, for arbitrary fixed , we can leverage (4.10) and (5.15a) to get

where the summation is taken over nonnegative integers and multisets of natural numbers . We use to denote the cardinality of and define . Note that here the second-order contribution from cumulant expansion comprises two parts. The leading part has been offset due to the fully underlined term, while the subleading part is encapsulated by the quantity

| (5.17) |

Here, we opt not to list all the terms, as the omitted terms can be controlled in a similar manner to the listed representative terms. On the other hand, for the contribution stemming from higher-order cumulants, we used the notation

| (5.18) |

Strictly speaking, the summation over and should have an upper limit and we should include a remainder term as in (4.10). However, by choosing this upper limit to be sufficiently large, while depending only (e.g., ), one can easily prove that the corresponding remainder term is dominated by . In other words, this additional error term has no significant impact on our argument. Therefore, we omit this technical detail from the equations above.

The quantities and are estimated in Lemmas 5.7 and 5.8 below. By employing the estimates (5.25a) and (5.26a), we obtain

Utilizing Young’s inequalities, we therefore arrive at

which concludes the proof of (5.12a) since is arbitrary.

Derivation of (5.12b): The derivation of the remaining three self-improving inequalities follows the same procedure as that for (5.12a). Therefore, we only highlight the definitions that are necessary for subsequent discussion in Sections 5.4 and 5.5. Referring to (4.12), we have

Hence, we can apply the cumulant expansion formula (4.10) and the representation (6.2) to get

The quantity related to second-order contribution is given by

| (5.19) | ||||

The quantity associated with higher-order cumulants is defined as

| (5.20) |

We obtain the self-improving inequality (5.12b) by utilizing the estimates (5.25b) and (5.26b).

Derivation of (5.12c): Again, we employ (4.10) and (6.2) to get

where we introduced

| (5.21) | ||||

as well as

| (5.22) |

This time, we employ (5.25c) and (5.26c) to conclude the derivation.

Derivation of (5.12d): Finally, we have

where we introduced

| (5.23) | ||||

as well as

| (5.24) |

The derivation is completed by applying (5.25d) and (5.26d).

As previously mentioned, the following two lemmas provide control over the intermediate quantities that arise in the derivation of the self-improving inequalities. Their proofs are presented in Section 5.4 and Section 5.5, respectively.

Lemma 5.7.

Given the inductive hypothesis (5.6), we have the following uniformly in ,

| (5.25a) | ||||

| (5.25b) | ||||

| (5.25c) | ||||

| (5.25d) | ||||

Lemma 5.8.

Given the inductive hypothesis (5.6), we have the following uniformly in ,

| (5.26a) | ||||

| (5.26b) | ||||

| (5.26c) | ||||

| (5.26d) | ||||

5.4 Second-order contribution: proof of Lemma 5.7

Let us begin with the two estimates concerning the averaged forms, (5.25a) and (5.25c). Recall the -regularity of as specified in Proposition 5.6. Upon examining the resolvent chains in (5.17) and (5.21), we observe that all the deterministic matrices are regular w.r.t. their surrounding spectral parameters expect for the matrix that we place at the end of the chains. Therefore, we can utilize the spectral decomposition of and then apply the isotropic estimates, which yields

where we used the definition of in (5.9).

Moving forward, let us consider the estimate (5.25b). We can utilize (5.11) for the first factor in the first line and second factor in the second line of (5.19). It turns out that

It remains to demonstrate the estimate (5.25d). For the three representative terms outlined in (5.23), we utilize (5.11) to control their second factor due to the presence of the non-regular matrix . Specifically, the first line of (5.23) can be controlled by

While the second line of (5.23) is dominated by

Finally, for the third line of (5.23), we can estimate it with

Summarizing the three estimates above concludes the proof of (5.25d).

5.5 Higher-order contribution: proof of Lemma 5.8

This section is devoted to the proof of Lemma 5.8. As , we have the following trivial bounds

Plugging these bounds into the definition of and in (5.18) and (5.22), we obtain

which establishes the averaged bounds (5.26a) and (5.26c) when . Similarly, for the isotropic forms defined in (5.20) and (5.24), we can apply the elementary bounds

It follows that

In conclusion, we still need to demonstrate the averaged bounds (5.26a) and (5.26c) when , and the isotropic bounds (5.26b) and (5.26d) when . In these cases, we must handle the summation more delicately instead of estimating it simply with . Specifically, we rely on the following lemma.

Lemma 5.9.

We informally refer to the isotropic forms of the type as off-diagonal resolvent entries. Lemma 5.9 refines the trivial estimate for the summation over these off-diagonal resolvent entries with regular matrices by a factor of , at the expense of introducing control parameters indexed by . We could have provide an analogous estimate for the summation over . However, the suboptimal control of through reduction inequalities offsets our expected gain. Essentially, in our context, extending Lemma 5.9 to off-diagonal entries with two regular matrices does not yield significant improvement.

The proof of Lemma 5.9 is provided in Section 7.4. For the subsequent discussion, we frequently utilize Lemma 5.9 alongside with the Cauchy-Schwarz inequality. For instance, we have

Proof of (5.26a) and (5.26c) for with : In this case, the first factor of the summands in (5.18) and (5.22) must contain at least one off-diagonal resolvent entry. Consequently, we can leverage Lemma 5.9 to obtain

Proof of (5.26a) and (5.26c) for : In this case, at least one off-diagonal resolvent entry is present in the second factor of the summands in (5.26a) and (5.26c). It turns out that

The estimates (5.26a) and (5.26c) are obtained by taking the square root of the preceding bounds.

Proof of (5.26b) and (5.26d) for : In this case, we have . Hence, applying Lemma 5.9 yields

Note that we have .

Proof of (5.26b) and (5.26d) for : Essentially, in this case we must have and . In addition, we have . Therefore, we can apply Lemma 5.9 to both the two factors of the terms in (5.20) and (5.24), resulting in

Since , the factor appearing at the end of the estimate for can, at most, weaken the bound in square bracket by .

6 Representation as fully underlined

This section is devoted to the proof of Proposition 5.6. Here, we present several technical lemmas that are instrumental in deriving the representations in (5.15). Readers can navigate directly to the actual proof and refer back to these lemmas when they are utilized.

The following lemma introduces the concept of “pre-regularizing” a matrix. The motivation behind this operation is to ensure that the product of the pre-regularized matrix and becomes regularized in the sense of Definition 4.8.

Lemma 6.1 (One-point pre-regularization).

Let be a deterministic matrix with . Suppose its top-left and bottom-right diagonal blocks are given by and , respectively. For , we define the one-point pre-regularization of w.r.t. as

| (6.1) |

Equivalently, we can write

| (6.2) |

Suppose such that . Then, is -regular.

Given , we introduce the deterministic block-diagonal matrices

| (6.3) |

Explicitly, by the MDE (4.16) or the self-consistent equation (4.17), we have

| (6.4a) | ||||

| (6.4b) | ||||

Moreover, recalling our definition of in (4.20) and in (4.22a), it is straightforward to verify

| (6.5) |

In the proof of Proposition 5.6, the regularization of the matrices is required. Given the explicit formulas for in (6.4), this essentially translates to the regularization of . Here, one might consider employing the one-point regularization defined in (4.34). However, this proves to be infeasible as it fails to guarantee the lower estimate stated in Lemma 6.4 below. Therefore, we are compelled to consider the following two-point regularization instead. The coefficient given in (6.7) below is somehow artificial. Readers can find the intuition behind this definition in the proof of Lemma 6.4.

Lemma 6.2 (Two-point regularization).

Given any two spectral parameters , we define the two-point regularization of w.r.t. as follows (note that the order of matters):

| (6.6) |

where the coefficient is given by

| (6.7) |

The matrix is -regular.

Now, with (6.6), we can define the two-point regularization of w.r.t. as

| (6.8) |

The proofs of Lemmas 6.1 and 6.2 are provided in Section 7.2. Here, we summarize how these two lemmas are utilized in this section. Let and set for some deterministic . The following two decompositions are crucial in deriving the representations in (5.15),

| (6.9a) | ||||

| (6.9b) | ||||

where the coefficients in (6.9a) are given by (6.2), while the coefficients in (6.9b) are defined through (6.8). Although one can explicitly write down the formula for using (6.4) and (6.7), we refrain from doing so as this explicit form is not relevant to our proof.

We have the following two estimates concerning the coefficients in (6.9), the proofs of which are postponed to Section 7.3. Recall that the operator has been defined in (4.20).

Lemma 6.3.

Let and suppose that the deterministic matrix is -regular. Then, for and defined in (6.3), we have

| (6.10) |

where we abbreviate .

Lemma 6.4.

Let , and set as in (6.6). Then, with , we have

| (6.11) |

Finally, we present the following lemma, crucial for controlling resolvent chains involving . The proof of this lemma can be found in Section 7.4.

Lemma 6.5.

Let , and assume that is regular w.r.t. its surrounding spectral parameters. Then, we have the following estimates,

| (6.12a) | ||||

| (6.12b) | ||||

| (6.12c) | ||||

6.1 Averaged law with one regular matrix

In this section, we derive the representation (5.15a). Combining the expression (4.13) for and the MDE (4.16), we obtain the following expansion of ,

| (6.13) |

Let be -regularized and abbreviate and . Multiplying both sides of (6.13) by and taking the normalized trace yields

Recalling (4.19) and (4.21), we thus arrive at

Next, we apply the decomposition (6.9a) of to the three terms in the r.h.s. of the preceding equation with . Let us abbreviate when there is no ambiguity. This step leads to

| (6.14) | ||||

Note that Lemma 6.1 ensures the -regularity of . Therefore, the last two terms in first line of (6.14) can be controlled as follows,

We proceed to rewrite the term with angular brackets in the second line of (6.14). Let be defined as in (6.3) and recall from (6.5). We have

where we utilized (4.13) and in the first step, the MDE (4.16) in the second step, and (4.21) in the last step. Plugging this back into (6.14), we obtain

Now, we can apply the decomposition (6.9b) of to the r.h.s and end up with

| (6.15) | ||||

where we abbreviate and implicitly used that .

Leveraging Lemma 6.3, the coefficients preceding in the second line of (6.15) can be controlled by . With the single resolvent average law (4.7), we conclude that

| (6.16) |