defi short = DeFi, long = decentralized finance \DeclareAcronymtvl short = TVL, long = total value locked \DeclareAcronymtvr short = TVR, long = total value redeemable \DeclareAcronymlp short = LP, long = liquidity provider \DeclareAcronymcdp short = CDP, long = collateralized debt position \DeclareAcronymamm short = AMM, long = automated market maker \DeclareAcronymdex short = DEX, long = decentralized exchange \DeclareAcronymncb short = NCB, long = non-crypto-backed \DeclareAcronymltv short = LTV, long = loan-to-value ratio \DeclareAcronymtrafi short = TradFi, long = traditional finance \DeclareAcronymp2p short = P2P, long = peer-to-peer \DeclareAcronympos short = PoS, long = proof-of-stake \DeclareAcronymeth short = ETH, long = Ether \DeclareAcronymiou short = IOU, long = I-owe-you \DeclareAcronymplf short = PLF, long = protocols for loanable funds \DeclareAcronymaum short = AUM, long = assets under management \DeclareAcronymabs short = ABS, long = asset-backed securities \DeclareAcronymcdo short = CDO, long = collateralized debt obligation \DeclareAcronymapr short = APR, long = annual percentage rate \DeclareAcronymnft short = NFT, long = non-fungible token

Piercing the Veil of TVL: DeFi Reappraised

Abstract.

\Acftvl is widely used to measure the size and popularity of protocols and the broader ecosystem in \acfdefi. However, the prevalent \acstvl calculation framework suffers from a “double counting” issue that results in an inflated metric. We find existing methodologies addressing double counting either inconsistent or flawed. To mitigate the double counting issue, we formalize the \acstvl framework and propose a new framework, \acftvr, designed to accurately assess the true value within individual \acsdefi protocol and \acsdefi systems. The formalization of \acstvl indicates that decentralized financial contagion propagates through derivative tokens across the complex network of \acsdefi protocols and escalates liquidations and stablecoin depegging during market turmoils. By mirroring the concept of money multiplier in \acftrafi, we construct the \acsdefi multiplier to quantify the double counting in \acstvl. Our empirical analysis demonstrates a notable enhancement in the performance of \acstvr relative to \acstvl. Specifically, during the peak of DeFi activity on December 2, 2021, the discrepancy between \acstvl and \acstvr widened to $139.87 billion, resulting in a TVL-to-TVR ratio of approximately 2. We further show that \acstvr is a more stable metric than \acstvl, especially during market turmoils. For instance, a 25% decrease in the price of \acfeth results in an overestimation of the \acsdefi market value by more than $1 billion when measuring using \acstvl as opposed to \acstvr. Overall, our findings suggest that \acstvr provides a more reliable and stable metric compared to the traditional \acstvl calculation.

1. Introduction

An important notion within the emerging \acdefi sector is the \acftvl, which refers to the cumulative value of crypto assets deposited by users in a \acdefi protocol or a \acdefi ecosystem (Gogol et al., 2023). Analogous to the concept of \acaum in \actrafi (Werner et al., 2022), TVL represents a similar measure of assets pooled for investment. However, unlike \actrafi, where assets are managed by financial advisors or wealth managers, \acdefi operates through a network of interconnected smart contracts, enabling investors to directly engage with these contracts to achieve their investment objectives. \actvl stands as a crucial metric for gauging both the size and popularity of the \acdefi ecosystem. Moreover, it provides insights into the confidence investors have in various \acdefi protocols, acting as a comprehensive indicator of market activity. This metric effectively captures the evolving dynamics within the \acdefi landscape, serving as a vital barometer for understanding shifts in investor behavior and protocol performance. According to DeFiLlama (DefiLlama, 2023), the \actvl stands at approximately $175.39 bn on March 19, 2024. This represents an impressive 211-fold increase compared to the \actvl four years prior, illustrating the rapid growth and escalating popularity of the \acdefi sector.

However, the present methodologies of computing \actvl in the DeFi domain grapple with a challenge known as “double counting” (Chandler, 2020). Double counting is the problem whereby the value of (certain) underlying cumulative crypto assets locked in \acdefi products is counted more than once. Double counting occurs as a result of the rapid increase in derivative tokens and complex financial instruments, obscuring the true value held within the \acdefi ecosystem and potentially leading to confusion among investors. Additionally, the approaches to calculating \actvl in the \acdefi arena are not only non-uniform but also frequently lack clarity. This results in various platforms providing \actvl statistics for distinct \acdefi protocols, each using their own specific calculation methods (DefiLlama, 2023; Token Terminal, 2023; Purdy, 2020; L2BEAT, 2023). The calculation methods employed by these platforms, along with any potential biases in their data, are often not transparently disclosed. This absence of standardization and transparency impedes the accurate determination of a \acdefi system’s actual usage and value contained. Consequently, the financial metrics and figures reported up to this point lack the ability to convey an unequivocal and objective truth about the underlying value or performance. This ambiguity underscores the need for more reliable and transparent measurement methods in the field.

The problem of double counting poses a significant financial risk. For example, this issue exacerbates the potential for exaggerated declines in the inflated \actvl during market downturns. This is primarily manifested via a downward spiral in the endogenous prices and quantities of derivative tokens within \acplf, ultimately leading to increased liquidation events. Such distortions can lead to unwarranted panic among investors, as the perceived value may decrease more dramatically than actual market conditions warrant. This phenomenon not only undermines the financial stability of the \acdefi ecosystem but also introduces significant risks. These include the potential for rapid capital withdrawal and loss of confidence by investors, which could further affect the overall cryptocurrency and \actrafi markets.

To overcome these challenges, we propose a novel metric termed \actvr, designed to eliminate double counting. Establishing such a metric is vital for accurately assessing the true underlying crypto asset value locked in DeFi products.

In addition, our research quantifies risk within the traditional \actvl framework and introduces indicators for DeFi risk monitoring. This includes metrics akin to the money multiplier used in monetary economics. Our formalization of \acstvl demonstrates that financial instability in the sector can spread through the \acsdefi network via derivative tokens. This process exacerbates liquidations and causes stablecoins to deviate from their pegs during periods of market turmoil. Our balance sheet approach applied to the inter-\acsdefi network provides evidence of the complex interconnections between instruments and their contributions to the emergence of financial contagion. We finally extend our debate by linking our analysis in \acdefi to the the causes and mechanisms of traditional financial contagion in the inter-bank network such as the propagation of subprime mortgage crisis.

In this work, we: (1) provide in-depth anatomy of the double counting problem under the \actvl framework, (2) identify drawback in existing methodologies addressing double counting, (3) propose TVR: an enhanced measurement framework to address the double counting problem, (4) conduct an empirical analysis to accurately assess the total value locked in the DeFi system and evaluate the magnitude of double counting involved, (5) measure the risk of financial contagion under the traditional \actvl framework, (6) propose a metric to quantify the double counting.

Overall, our contribution to the current literature on \actvl can be summarized as follows:

-

(1)

\ac

tvl formalization and \acdefi accounting framework establishment: We employ accounting concepts to model operations in \acdefi and formalize the \actvl, quantifying the extent of double counting.

-

(2)

Revealing the origin of double counting: Based on the \acdefi accounting framework and \actvl formalization, we heuristically explain the mechanism of double counting under the \actvl framework.

-

(3)

Identifying drawback in existing methodologies addressing double counting: We find existing methodologies addressing double counting either inconsistent or flawed.

-

(4)

Establishing a double-counting-free measurement framework: We introduce an enhanced measurement framework, the \actvr, to evaluate the actual value locked within a \acdefi system and avoid double counting. We present the algorithm for \actvr, a more efficient and user-friendly framework to address the double counting problem compared to the input-output framework in economics. By decomposing \actvl of all \acdefi protocols and calculating \actvr, we find a substantial amount of double counting within the \acdefi system, with a maximum of $139.87 billion with a \actvl-\actvr ratio around 2. We track the evolution of token composition in \actvr over time.

-

(5)

Quantifying financial contagion risk comparatively under the traditional \actvl and the new \actvr frameworks: Based on the system of six representative \acdefi protocols, we uncover the financial contagion risk stemming from double counting within the traditional \actvl framework. Our findings reveal that \actvl exhibits greater sensitivity to market downturns in comparison to \actvr, highlighting \actvr as a more stable metric. A 25% drop in \acfeth price leads to a significant divergence, resulting in approximately a $1 billion greater decrease in \acstvl compared to \acstvr.

-

(6)

Quantifying double counting and documenting its correlation with macroeconomy and crypto market: We are also the first to build the \acdefi money multiplier based on \actvr and \actvl in parallel to the \actrafi macroeconomic money multiplier to quantify the double counting. We document that the \acdefi money multiplier is positively correlated with crypto market indicators and negatively correlated with macroeconomic indicators.

2. Background and Terminologies

2.1. Ethereum and \acfpos

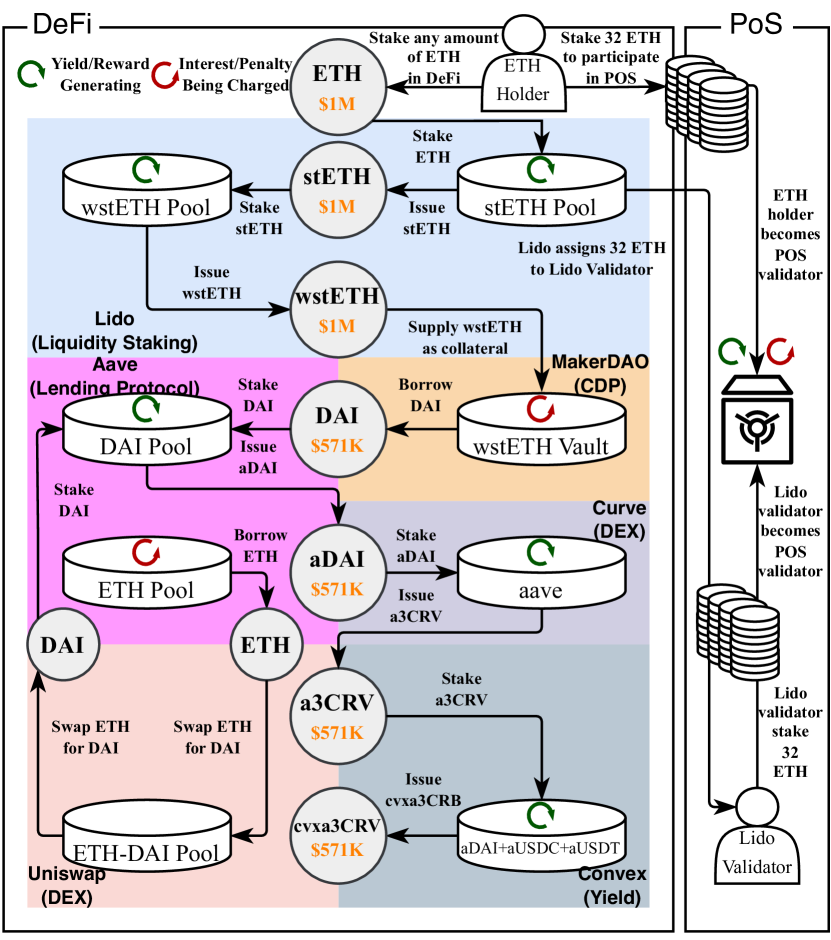

Ethereum is the blockchain powering thousands of decentralized applications. \acpos is Ethereum’s current consensus mechanism (ethereum.org, 2024). Under the \acpos mechanism, a holder of \aceth (Ethereum’s native currency) can lock 32 \aceth into a deposit contract and participate as a validator in block attestation. While keeping online and utilizing blockchain knowledge, a validator receives a reward for successful attestation; conversely, unsuccessful attestation results in a penalty for the validator, as shown in the \acpos part in Figure 1.

2.2. Decentralized Finance (DeFi) and DeFi Protocols

defi is an ecosystem of (\acdefi) protocols operating autonomously through smart contracts run on blockchains. \acdefi protocols are decentralized applications with financial utilities. Many \acdefi protocols, such as asset exchanges and lending platforms, draw inspiration from and mirror traditional centralized finance systems (Xu et al., 2023; Werner et al., 2022; Qin et al., 2021). For our study, we select Lido, MakerDAO, Aave V2, Uniswap V2, Curve, and Convex (see Figure 1). These protocols have the highest \actvl and, as of today, represent approximately the 68% of the total \actvl (DefiLlama, 2023). These six protocols can be classified into \acplf and non-\acplf.

2.2.1. \acplf

Protocols for Loanable Funds (\acplf) are \acdefi protocol that allow users to supply and borrow cryptocurrency under overcollaterization mechanism. The overcollaterization mechanism in PLF necessitates users to pledge increased collateral to borrow a reduced amount of debt, capped at a maximum dollar value equal to the \acltv times the debt value. This mechanism ensures the overall solvency of the platform. If a user’s account collateral-to-debt ratio falls below one, the liquidation may be triggered, resulting in a fixed portion of the collateral being wiped out (Qin et al., 2021; MakerDAO, 2022a; Aave, 2022, 2023). In certain \acpplf, as the health ratio drops to various thresholds, the proportion of liquidated collateral varies. In the case of Aave V3, there are two thresholds for liquidation. If the account’s collateral-to-debt ratio is below 1, half of the collateral can be liquidated in a single liquidation. If the ratio drops below 0.95, the entire collateral can be liquidated in a single process (Aave, 2023). \acplf includes \accdp such as MakerDAO (orange block in Figure 1) and lending protocols (purple block). Unlike lending protocols, which allow borrowing of any cryptocurrency, users in \accdp can only generate noncustodial stablecoins (CoinMarketCap, 2024). The collateralization model in DeFi’s CDP mirrors a tranche system, where stablecoins represent senior debt and users resemble buyers of the junior tranche in a CDO, as seen in TraFi (Klages-Mundt and Minca, 2022). Stablecoins are a cryptocurrency designed to offer the stability of money to function effectively, aiming to provide price stability relative to a specific reference point, often the USD (Moin et al., 2020).

2.2.2. Non-\acplf

Applying the method of exclusion, liquidity staking, \acdex, and yield aggregator fall into the category of non-PLF. Liquidity staking protocols allow users to earn rewards by staking any amount of tokens, while also offering a tradable and liquid receipt for their staked position. The liquidity staking protocol Lido (blue block in Figure 1) accepts any amount of ETH from ETH holders, and in exchange issues liquid receipt tokens (stETH and wstETH) that can be further used in other \acdefi protocol. At the same time, Lido allocates ETH to selected knowledgeable Lido validators in order for them to participate in block attestation in the Ethereum blockchain. Rewards and penalties for block attestation are distributed among staking users, the Lido protocol, and Lido validators. \acpdex such as Uniswap (purple block) and Curve (dark blue) are the \acdefi protocol that allows users to provide liquidity and swap assets (Xu et al., 2023). Yield platforms such as Convex (grey block) are protocols that reward users for staking or providing liquidity on their platform.

2.2.3. \acdefi token, liquidity pool, and \acdefi composability

defi tokens are cryptocurrencies that provide users access to the \acdefi system. The liquidity pool operates as the functional unit within the \acdefi protocol, operating as a smart contract to facilitate users in supplying, borrowing, or swapping \acdefi tokens. \acdefi composability refers to the capability of multiple \acdefi protocols to seamlessly communicate with each other, enabling \acdefi tokens to be chained and integrated to create new \acdefi tokens and financial services. Incentivizing users to contribute liquidity to \acdefi protocols and sustain the functionality of liquidity pools, many protocols provide interest rewards to users staking tokens in these pools. In contrast to \acpos mentioned in §2.1 where validators cannot utilize locked \aceth, several \acdefi protocols allow \acplp to get receipt tokens (e.g. wstETH from Lido in Figure 1) which holds the same notional value of the locked tokens (e.g. stETH staked in Lido). To increase liquidity and achieve other functionality, users can take these new tokens and stake them into other protocols (e.g. MakerDAO). Given the additivity of interest and composability across different protocols, \acdefi users commonly repeat this process multiple times among several protocols to maximize rewards, as depicted in Figure 1. Additionally, \acdefi staking has the advantage of not demanding a minimum deposit or block attestation knowledge compared to \acpos, making it more appealing for user participation.

2.2.4. \acdefi protocol metrics, double counting, and \acdefi tracing website

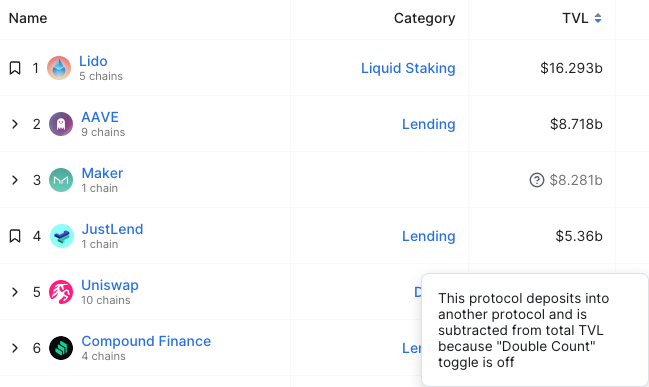

To assess the size and popularity of \acdefi protocols, metrics such as \actvl, protocol revenue, and protocol users are utilized, with \actvl being the most influential and widely used. However, the \actvl calculation method faces the known problem of double counting (Chandler, 2020). DeFiLlama (one the few tracing services which aggregates tokens breakdown of almost all \acdefi protocols to compute the \actvl) tries to accounts for double counting by excluding protocols categorized under liquidity staking or those feeding tokens into other protocols. DeFiLlama has the “double count” toggle in its \actvl dashboard to let users decide whether to filter out the double counting by removing the \actvl of protocols that deposit into another protocol from the total \actvl of single chain or all chains, as shown in Figure 2. As we will show in §3.3, this approach is both rudimentary and imprecise.

2.3. Total Value Locked (TVL)

According to (Binance Academy, 2023; Gogol et al., 2023), we offer the following definition along with a mathematical expression (cf. Equation 1) for the term \actvl.

Definition 0 (Total Value Locked).

Total Value Locked is defined as the total value of assets staked by users in a \acdefi protocol or \acdefi ecosystem at a specific moment.

| (1) |

where: is the total \actvl of the \acdefi ecosystem at time ; and are respectively the set of all \acdefi protocols at time and the set of all tokens in protocol at time ; is the \actvl of protocol at time ; is the dollar price of token at time ; and is the quantity of the token locked in the protocol at time .

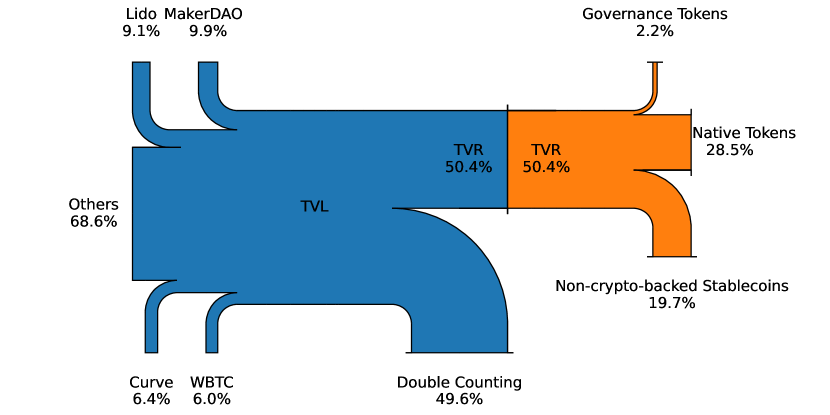

As shown in Table 1, the disclosure of \actvl counting methodologies is currently inconsistent across the \acdefi data providers. Each of them offers varying levels of disclosure about their methodologies, with often inconsistent practices among them. Furthermore, only two of them attempt to tackle the issue of double counting. In Figure 1, the TVL is the sum of all orange numbers, totaling 4.7474 million—4.7474 times the initial ETH value deposited.

| \acdefi Tracing Website | Protocols Coverage | TVL-related Information | ||||||

| Number | \Actvl Presented | Overall Methodology | Protocol-specific Methodology | Toke Price Sources | Constituent Protocols | Code | Double Counting Solution | |

| (DeFiLlama, 2023) | 3,570 | ● | ● | ● | ● | ● | ● | ● |

| (L2BEAT, 2023) | 47 | ● | ● | ○ | ○ | ● | ● | ○ |

| (DappRadar, 2022) | 4,126 | ● | ○ | ○ | ○ | ● | ○ | ○ |

| (Stelareum, 2023) | 309 | ● | ○ | ○ | ○ | ● | ○ | ○ |

| (DeFi Pulse, 2022) | N/A | ○ | ● | ○ | ○ | ○ | ○ | ● |

3. TVL Double Counting Analysis

In this section, we explain the double counting problem using a balance-sheet approach. A balance sheet provides a concise overview of an entity’s assets, liabilities, and equities. We apply this traditional accounting framework to \acdefi platforms.

3.1. Balance Sheet of DeFi Protocols

For each specific protocol, we use a balance-sheet approach to consolidate double-entry bookkeeping and describe its financial condition. The aggregate value locked can be regarded as a significant element on the asset side of a \acdefi protocol’s balance sheet (Deloitte, 2023a). In the context of a \acdefi system, we apply the principles of consolidated balance sheets to depict its financial status on an aggregated basis. By leveraging the principle of non-duplication used in consolidated balance sheet accounting (whereby, accounting entries that are recorded as assets in one company and as liabilities in another are eliminated, before aggregating all remaining items) (Deloitte, 2023b), we can effectively eliminate instances of double counting within a \acdefi system.

3.2. The Anatomy of Double Counting Problem

| Assets | $000 | $000 |

| Value Locked - stETH | 1,000 | 1,000 |

| Total Assets | 1,000 | 1,000 |

| Liabilities | $000 | $000 |

| Payables - wstETH | 1,000 | 1,000 |

| Total Liabilities | 1,000 | 1,000 |

| Assets | $000 | $000 |

| Value Locked - wstETH | - | 1,000 |

| Receivables - DAI | - | 571 |

| Total Assets | - | $1,571 |

| Liabilities | $000 | $000 |

| Payables - wstETH | - | 1,000 |

| New Money - DAI | - | 571 |

| Total Liabilities | - | 1,571 |

| $000 | $000 | |

| Total Value Locked | 1,000 | 2,000 |

| Assets | $000 | $000 |

| Value Locked | 1,000 | 1,000 |

| Receivables | - | 571 |

| Total Assets | 1,000 | 1,571 |

| Liabilities | $000 | $000 |

| Payables | 1,000 | 1,571 |

| Total Liabilities | 1,000 | 1,571 |

Double counting problem occurs when the value locked in multiple protocols within a \acdefi system is double-counted in the \actvl calculation due to composability. The composability enables \acdefi users to achieve sophisticated operations within the \acdefi system (c.f. Figure 1), making the double counting problem non-trivial. For illustration purpose, we describe two common operations that lead to double counting.

3.2.1. Wrapping

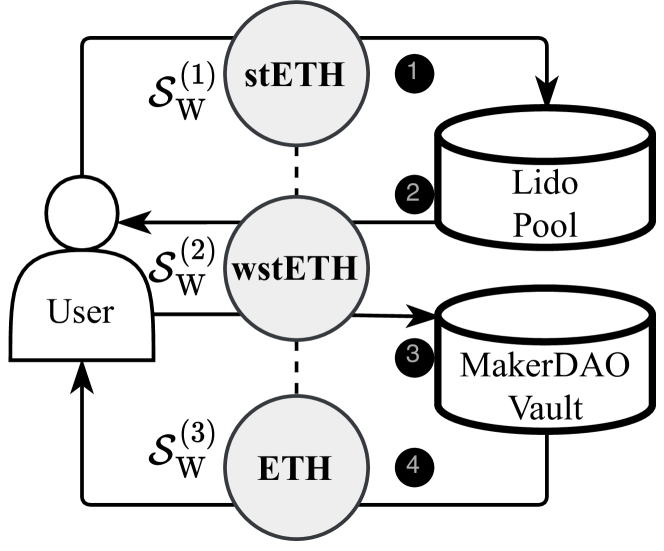

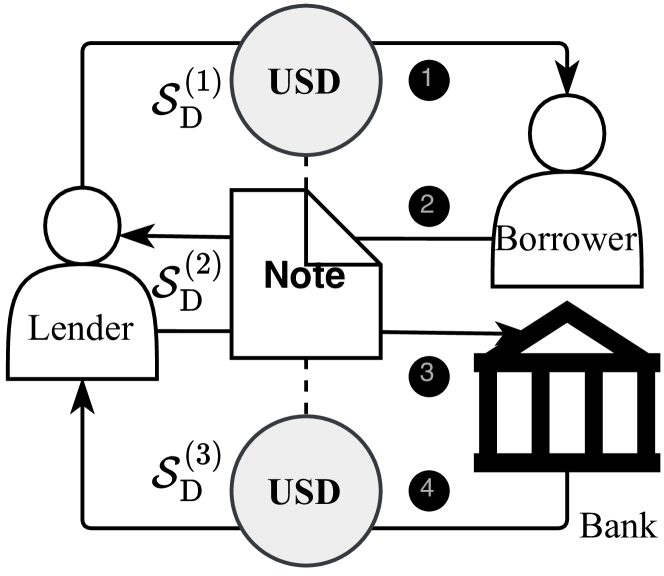

3(a) depicts a scenario where an investor initially supplies $1m in stETH to Lido (step 1), which is then converted into $1m of wstETH (step 2). Subsequently, the investor deposits this wstETH into MakerDAO (step 3) and borrows up to $571k in DAI (step 4), based on the \actvl of the wstETH low fee vault at the time of this paper. The financial flows generated by the wrapping in \acdefi can be related to the rehypothecation process in \actrafi, illustrated in 3(c). The promissory hypothecation enables lenders who provide loans to borrowers (step 1) and issue a promissory note (step 2) to pledge the promissory note (step 3) and borrow money from the bank (step 4) (Andolfatto et al., 2017).

Table 2 shows the balance sheets of Lido and MakerDAO, and the consolidated balance sheet of the \acdefi system consists of Lido and MakerDAO. In , the value of the DeFi system is $1m, where represents a NCB stablecoin (see See Table 4 for a comprehensive list of notations). However, if we deposit the receipt token wstETH from Lido into MakerDAO to issue another receipt token DAI, the \actvl will be $2m under the traditional TVL measurement. The balance sheets are expanded and the \actvl is double-counted due to the existence of wstETH. In the consolidated balance sheet, the \actvl is adjusted to $1m after eliminating the value associated with the wstETH.

3.2.2. Leveraging

| Assets | $000 | $000 |

| Value Locked - DAI | 2,000 | 2,900 |

| Receivables - dETH | 900 | 900 |

| Total Assets | 2,900 | 3,800 |

| Liabilities | $000 | $000 |

| Payables - aDAI | 2,000 | 2,900 |

| Payables - aETH | 900 | 900 |

| Total Liabilities | 2,000 | 3,800 |

| Assets | $000 | $000 |

| Value Locked - ETH | 1,800 | 900 |

| Value Locked - DAI | 1,800 | 2,700 |

| Total Assets | 3,600 | 3,600 |

| Liabilities | $000 | $000 |

| Payables - ETH-DAI-LP | 3,600 | 3,600 |

| Total Liabilities | 3,600 | 3,600 |

| $000 | $000 | |

| Total Value Locked | 5,600 | 6,500 |

| Assets | $000 | $000 |

| Value Locked | 5,600 | 5,600 |

| Total Assets | 5,600 | 5,600 |

| Liabilities | $000 | $000 |

| Payables | 5,600 | 5,600 |

| Total Liabilities | 5,600 | 5,600 |

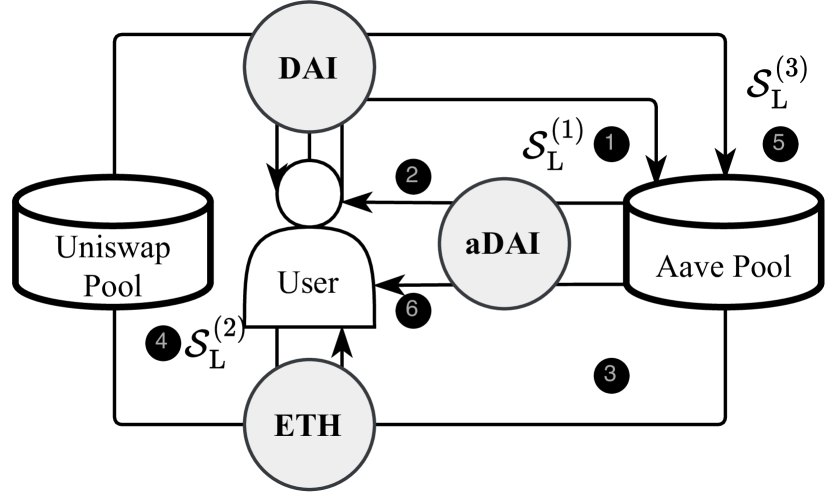

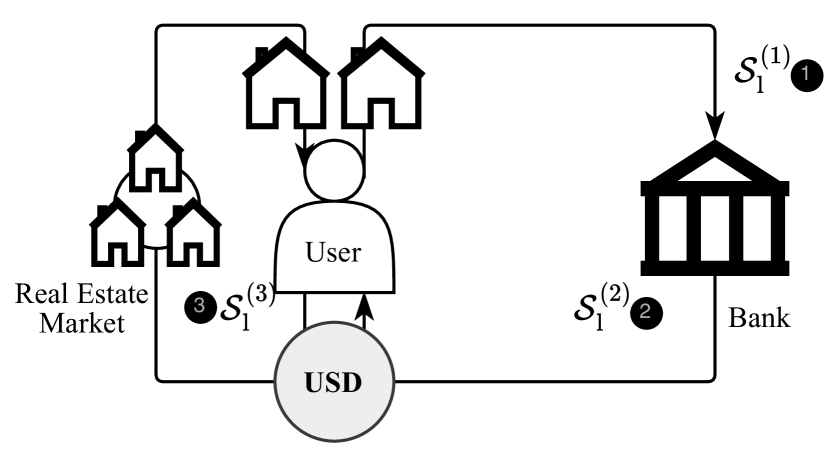

As illustrated in 3(d), the leveraging operation in \acdefi can be related to the leveraging process in \actrafi. In \actrafi, the investor can use her house as collateral (step 1) to borrow cash (step 2) and then use cash to buy another house (step 3). In the scenario of 3(b), we assume that liquidity providers have already supplied $900k ETH to Aave and $1.8m ETH along with $1.8m DAI to Uniswap to facilitate swaps and borrowing. Initially, Aave has $900k ETH in assets and $900k worth of aETH in liabilities, while Uniswap holds $1.8m ETH and $1.8m DAI in assets and $1.8m worth of ETH-DAI LP tokens in liabilities. An investor provides $2m DAI (step 1) as collateral to borrow $900k \aceth (step 3) in Aave, swaps the borrowed $900k \aceth to $900k DAI (step 4) in Uniswap, and then deposits $900k DAI (step 5) from Uniswap in the Aave to issue the receipt token aDAI (step 6).

Table 3 shows the balance sheets of Aave and Uniswap, and the consolidated balance sheet of the \acdefi system consisting of Aave and Uniswap. In , the value of the DeFi system is $5.6m. However, if the user borrows $900k \aceth, swaps the \aceth into DAI, and deposits the DAI into Aave, the \actvl will be $6.5m under the traditional \actvl measurement. This \actvl is also double-counted because it includes DAI. In the consolidated balance sheet, the \actvl is adjusted to $5.6m after eliminating the value associated with DAI.

3.3. Limitations in Existing Methodologies Addressing Double Counting

Some \acdefi tracking websites strive to mitigate the issue of double counting, yet they may not be able to eradicate it entirely. The methodology put forward by DeFiLlama, as elaborated in §2.2.4, encounters limitations due to the varying degrees of double counting across different protocols. Thus, simply excluding a particular category of protocols does not suffice to address the problem of double counting comprehensively. This is further illustrated through the example of 3(a), highlighting MakerDAO and Aave, where double counting is evidenced through a balance-sheet analysis, as shown in Table 2. Despite we show the occurrence of double counting within Aave, DeFiLlama accounts for Aave’s \actvl (see Figure 2).

4. Enhanced measurement framework

In the following section, we formalize the \actvl to show the risk under the traditional \actvl framework and introduce our new measurement framework called \acftvr to accurately assess the value within the \acdefi ecosystem.

4.1. \acdefi Token Classification

To formalize \actvl and derive \actvr, we initially classify \acdefi tokens into plain tokens and derivative tokens , which can be represented as . See Table 4 for a comprehensive list of notations. We provide the following definitions for the plain and underlying tokens:

| Notation | Definition |

| \acdefi token classification | |

| Set of staked \acdefi tokens. | |

| Set of plain tokens | |

| Set of derivative tokens | |

| Set of governance tokens such as MKR | |

| Set of native tokens such as \aceth | |

| Set of \acncb stablecoins such as USDT | |

| Set of crypto-backed stablecoins | |

| \actvl formalization | |

| \actvl of a \acdefi system at time | |

| \actvl of a \acdefi protocol at time | |

| Set of \acdefi protocols at time | |

| Set of \acplf at time | |

| Set of non-\acplf at time | |

| Set of token staked in protocol at time | |

| Price of token at time | |

| Quantity of token staked in the \acdefi system at time | |

| Endogenous derivative token price formalization | |

| Derivative token ; | |

| Underlying token of derivative token | |

| Ultimate underlying token of derivative token | |

| Set of the underlying tokens of derivative token | |

| The ratio between underlying token quantity and derivative token quantity | |

| Short-term depegging of derivative token price due to secondary market’s demand and supply dynamics at time | |

| The pegged value of crypto-backed stablecoin at time set by the \accdp | |

| The ratio of total collateral value to total debt value in a \accdp at time | |

| Endogenous token quantity in \acplf formalization | |

| Close factor for a specific threshold in a \acplf, the proportion of collateral wiped out in the liquidation | |

| Threshold for the health factor subjected to different close factors | |

| The liquidation threshold for a collateral, a percentage at which a position is defined as undercollateralized | |

| The health ratio computed from the \acplf user’s collateral value in USD multiplied by the current liquidation threshold for each of the user’s outstanding assets at time , divided by the user’s borrow value in USD | |

| The profitability ratio of an account in a liquidation, computed from the total collateral value in USD divided by the total debt value in USD | |

| Set of token borrowed | |

| \actvr formalization | |

| Total payables in the balance sheet of account at time | |

| Total receivables in the balance sheet of account at time | |

| Money multiplier | |

| \acdefi money multiplier computed from \actvl divided by \actvr | |

| \actrafi money multiplier computed from M2 divided by M0 | |

| Sticky price consumer price index less food and energy at time | |

| Federal fund effective rate at time | |

| S&P Cryptocurrency Broad Digital Market Index at time | |

| Ethereum gas price at time | |

| Ether price at time | |

Definition 0 (Plain Token).

A \acdefi token without underlying tokens.

Definition 0 (Derivative Token).

A \acdefi receipt token or \aciou token generated in a given ratio by locking a designated quantity of its underlying tokens into the smart contract of the protocol to represent the ownership of underlying tokens for future redemption.

In the example used in Figure 1, \aceth is a plain token that is initially deposited in the system and has no underlying token. Instead, other tokens (stETH, wstETH, DAI, aDAI, a3CRV, and cvxa3CRV) are derivative tokens with underlying tokens.

According to Definition 4.1, we can further classify plain tokens into governance tokens , native tokens , and \acncb tokens , which can be expressed as . Native tokens, encompassing both layer 1 and layer 2 tokens, along with governance tokens, serve as representative units of value within the blockchain and \acdefi projects and have no underlying token, respectively (CoinMarketCap, 2023a, b, c). \Acncb stablecoins refer to stablecoins that are not backed by other cryptocurrencies.

4.2. Formalizing TVL

4.2.1. \actvl formula from the classification

Based on the classification of derivative tokens and plain tokens in §4.1, we can compute the \actvl by summing the total value of plain tokens and derivative tokens locked in the system:

| (2) |

4.2.2. Endogenous derivative token price

Derivative tokens have endogenous prices determined by the underlying token prices. According to Definition 4.2, the relationship between the quantity of issued derivative tokens and their locked underlying tokens is defined by a specific ratio. The price of the derivative token is also pegged in a specified ratio, with fluctuations influenced by the secondary market’s demand and supply dynamics.

For derivative tokens that are not crypto-backed stablecoins generated by the \accdp, the following relationship exists between the price of the derivative token and the price of all its underlying tokens:

| (3) |

where . The temporary depegging is exogenous, being associated with the token’s supply and demand dynamics as well as liquidity factors. For example, stETH depegged in 2022 due to the selling pressure from Celsius and market illiquidity (Medium, 2022). For crypto-backed stablecoins generated by the \accdp, the relationship is different due to the overcollaterization mechanism. The overcollaterization mechanism requires that \accdp users should keep the collateral value higher than the debt value to a certain extent, ensuring the overall solvency of the system. Otherwise, the liquidation of the user account will be triggered, wiping out the user’s collateral. The relationship between the crypto-backed stablecoin and its underlying tokens is as follows:

| (4) |

where . Appendix C shows a detailed explanation of the derivative token pegging mechanism that supports Equation 3 and Equation 4.

defi composability allows the underlying token of a derivative token to serve as the derivative token of another token, as illustrated in Figure 1 and 3(a). We can derive the derivative token price function in terms of its ultimate underlying token, which belongs to the category of plain tokens:

| (5) |

where and is the function composition operator.

4.2.3. Endogenous token quantity in \acplf

Tokens staked in a \acplf, including \acpcdp such as MakerDAO or lending protocols such as Aave, have a token quantity determined by the token price due to the liquidation mechanism. The quantity of tokens staked in a \acplf is equal to the summation of the quantity of this token across all accounts. A drop in collateral price results in a reduction of the account’s health ratio, leading to different scenarios: (1) When the health ratio of an account, denoted as , is greater than or equal to 1, the account is deemed safe, and the quantity of collateral in the account remains unchanged, represented by . (2) When the health ratio of an account falls below 1, the user may face liquidation, prompting the smart contract to transfer varying proportions of collateral and sell it off. Additionally, when the profitability ratio of an account, represented by , is greater than or equal to 1, it indicates that the total collateral value is sufficient to cover the total debt value. In this scenario, the liquidation is deemed profitable for liquidators, leading to a successful liquidation. As stated in §2.2.1, health ratios falling below distinct thresholds will result in different proportions of collateral being subject to liquidation. (3) If the profitability ratio of an account, denoted as , is less than 1, the liquidation is considered unprofitable for liquidators, rendering the liquidation unviable and the quantity of collateral in the account unchanged, represented by . For plain tokens staked in the \acplf, the token quantity can be expressed in Equation 6.

| (6) |

The quantity of derivative tokens locked in the \acplf can be influenced by the price of their ultimate underlying tokens due to the endogenous derivative price. When derivative tokens are staked in the \acplf account as collateral, the health factor of the account can be expressed as a function of their underlying token prices according to §4.2.2. Since the health factor is the condition of Equation 6, the quantity of derivative tokens locked in the \acplf can also be the function of its ultimate underlying token prices .

4.2.4. \actvl as a function of ultimate underlying tokens price

According to §4.2.2 and §4.2.3, we can further split the \actvl into the following four categories: dollar amount of plain tokens in non-\acplf (), plain tokens in a \acplf (), derivative tokens in non-\acplf (), and derivative tokens in a \acplf (). Therefore, we can further derive the following function of \actvl in terms of ultimate underlying tokens from Equation 2:

| (7) |

4.2.5. Metrics inflation and decentralized financial contagion

The existence of derivative tokens not only inflates the actual value locked by \acdefi users but also serves as the channel for the spread of decentralized financial contagion. The value of derivative tokens in Equation 7 represents the market worth of tokens created through the wrapping process illustrated in 3(a), leading to double counting. Furthermore, due to the endogeneity discussed in §4.2.2 and §4.2.3, the value of derivative tokens will also contribute to the \actvl decrease, liquidations, and the depegging of crypto-backed stablecoins when the market experiences downturn, amplifying the impact of price declines of their underlying tokens several times over the value of plain tokens and making the \actvl sensitive to the change of plain token price.

4.3. Total Value Redeemable (TVR)

To address the double counting problem discussed in §3.2 and avoid incorporating the risk of decentralized financial contagion discussed in §4.2.5, we introduce the metric \actvr.

4.3.1. Definition and formalization of \actvr

We offer the following definition along with mathematical expressions (cf. Equation 8) for the term \actvr:

Definition 0 (Total Value Redeemable).

Total Value Redeemable is defined as the token value that can be ultimately redeemed from a \acdefi protocol or a \acdefi ecosystem.

We can express the \actvr of the whole \acdefi ecosystem as follows:

| (8) |

Compared to \actvl, \actvr removes the derivative token value and only includes the plain token value to eliminate the double counting problem. The exclusion of inflated values also decreases the complexity of the interplay within the \acdefi system, mitigating the high sensitivity of the metric concerning the ultimate underlying tokens.

When evaluating the \actvr for an individual protocol, aggregating the total value of plain tokens is not applicable anymore since there is no inter-protocol wrapping illustrated in 3(a) when focusing solely on a single protocol. However, a naive summation of the token value deposited in the protocol, as done in the traditional \actvl framework, is also inappropriate. This is because leveraging (see 3(b)) and intra-protocol wrapping (a variant of 3(a)) could also lead to the double counting and inflate the protocol’s \actvl as explained in §3.2.

To avoid intra-protocol double counting, we can employ the notations in the account-perspective balance sheet to accurately evaluate the redeemable value of the individual protocol. We chose Lido as the case study to illustrate intra-protocol wrapping and Aave to show leveraging because they represent the largest protocols where these instances of double counting could occur. 5(a) shows the account-perspective balance sheets of the Lido user in the intra-protocol wrapping scenario. In this scenario, a user deposits 1,000 USD \aceth to receive 1,000 USD in stETH in state . Subsequently, the user deposits 1,000 USD in stETH to generate 1,000 wstETH in state . From the user’s standpoint, irrespective of the frequency of intra-protocol token wrapping, the total value of receivables remains constant at $1 million in this scenario. 5(b) shows the account-perspective balance sheets of the Aave user in the leveraging scenario, as illustrated in 3(b). When users take leverage to expand both protocol’s (see 3(a)) and their account’s balance sheet, the total value of payables indicates the extent to which receivables are inflated, which is $900,000 in the scenario. Calculating the difference between the total value of receivables and the actual receivables helps offset this inflation. Therefore, the \actvr of an individual \acdefi protocol at time can be expressed as follows:

| (9) |

| Assets | $000 | $000 |

| Receivables - stETH | 1,000 | 0 |

| Receivables - wstETH | - | 1,000 |

| Total Assets | 1,000 | 1,000 |

| Liabilities | $000 | $000 |

| Total Liabilities | 0 | 0 |

| Net Positions | $000 | $000 |

| Initial Deposit Value - ETH | 1,000 | 1,000 |

| Total Net Positions | 1,000 | 1,000 |

| Total Liabilities and Net Positions | 1,000 | 1,000 |

| Assets | $000 | $000 | $000 |

| Cash - DAI | 2,000 | 0 | 0 |

| Cash - ETH | - | 900 | 0 |

| Receivables - aDAI | - | 2,000 | 2,000 |

| Receivables - aETH | - | - | 900 |

| Total Assets | 2,000 | 2,900 | 2,900 |

| Liabilities | $000 | $000 | $000 |

| Payables - dETH | - | 900 | 900 |

| Total Liabilities | 0 | 0 | 0 |

| Net Positions | $000 | $000 | $000 |

| Initial Deposit Value - DAI | 2,000 | 2,000 | 2,000 |

| Total Net Positions | 2,000 | 2,000 | 2,000 |

| Total Liabilities and Net Positions | 2,000 | 2,900 | 2,900 |

4.3.2. \actvr Algorithm

We propose the algorithm for the \actvr measurement framework. To optimize time complexity, we integrate a hash set to filter plain token values among the breakdowns of protocol tokens for \actvr calculation. First, we insert all plain tokens into the hash set. Then, we fetch on-chain token breakdowns of all protocols at this moment. Next, we check whether the token is in the hash table. If the token is in the hash table, its value will be added to the \actvr.

Input: Protocol list , ETH price decline in percentage , and on-chain data ;

Output: , ;

5. Data Collection

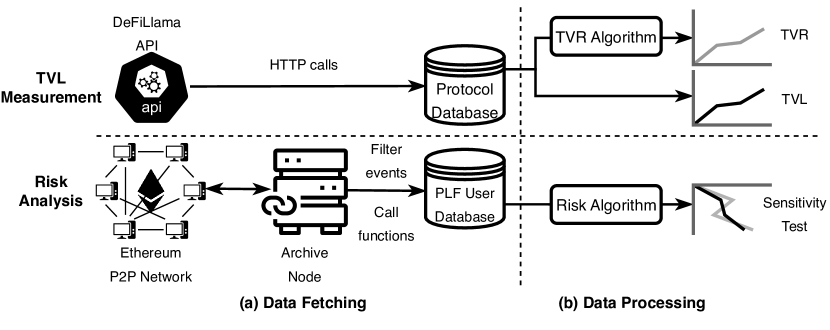

The data pipeline setup is outlined in Figure 4. The data pipeline constitutes two components: \actvl measurement and risk analysis. We crawl the tokens breakdown data and adjust \actvl () from 1st January 2021 to 1st March 2024 using DeFiLlama API. DeFiLlama offers the most comprehensive universe of DeFi protocols of all blockchains compared to all other DeFi-tracing websites, as illustrated Table 1. is DeFiLlama’s improved metric aimed at mitigating the double counting problem and is regarded as flawless in §3.3. We then aggregate the tokens breakdown of each protocol to obtain the \actvl per protocol per day (). Furthermore, we sum up the across all protocols over time to get the total \actvl over time () and the total \actvr () over time using the \actvr filter.

For the risk analysis, we retrieve the data by crawling blockchain states (e.g. MakerDAO vaults data) and blockchain events (e.g. Aave deposit events) from an Ethereum archive node, on a dual AMD Epyc 7F32 with 128 GB DDR4 ECC RAM, 2 240G Intel SSD and 2 16 TB Seagate EXOS in Raid 1 configuration. An Ethereum archive node stores not only the blockchain data but also the chain state at every historical block, supporting efficient historical state query. As of the latest information available, establishing an Ethereum archive node requires disk space ranging from 3 TB to 12 TB. Our sample of risk analysis constitutes six leading \acdefi protocols with the highest \actvl within each respective \acdefi protocol category, as shown in Figure 1. Table 6 shows the statistics of accounts in sensitivity tests in MakerDAO and Aave on three representative dates.

| PLF | Maximum TVL (2021-12-02) | LUNA collapse (2022-05-09) | FTX collapse (2022-11-08) |

| MakerDAO | 27,051 | 28,220 | 29,711 |

| Aave | 21,336 | 30,859 | 47,957 |

6. Empirical Measurement Results

6.1. \Actvl, Adjusted \actvl, and \actvr

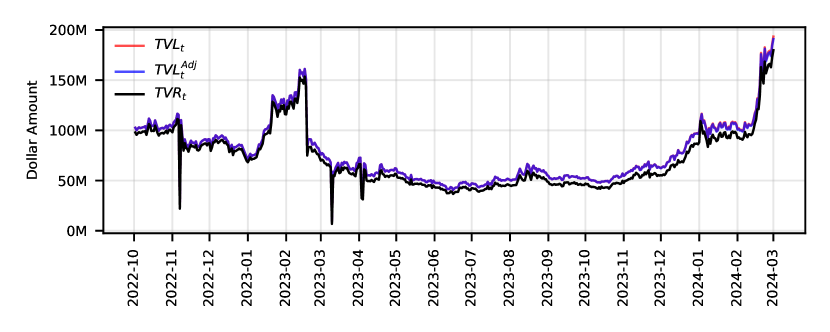

To apply the \actvr framework, we retrieve \actvl data from DeFillama from June 1st 2019 to March 1st 2024. DeFiLlama provides raw \actvl data subjected to the double counting and adjusted \actvl using its methodology to address the double counting problem. We build the \actvr from DeFiLlama \actvl subjected to double counting using our measurement methodology.

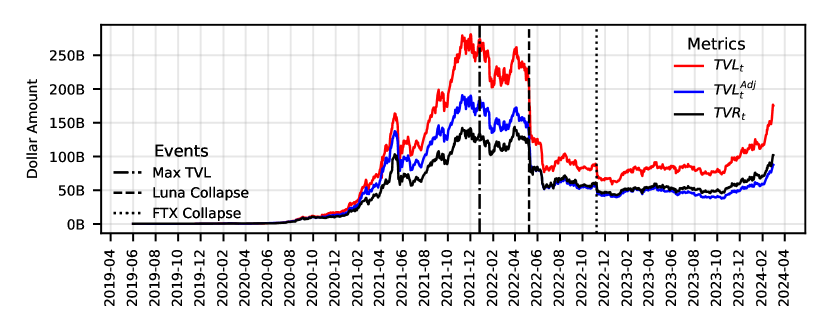

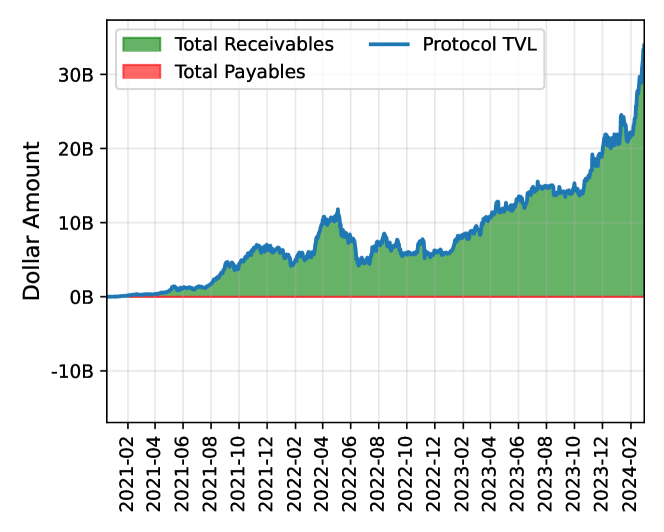

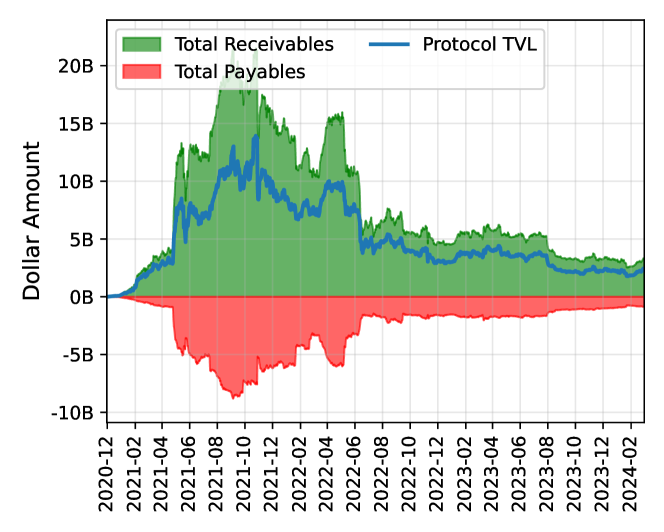

Figure 5 shows the all-chain DeFiLlama \actvl subjected to the double counting (), DeFiLlama adjusted \actvl (), and \actvr () over time. Our empirical measurement reveals the level of double counting within the DeFi ecosystem, with \acstvl-\acstvr discrepancies reaching up to $139.87 bn, and a TVL-TVR ratio of around 2 when the \acstvl reached its all-time high. Moreover, there is a distinction between DeFiLlama’s adjusted \actvl and the \actvr due to differences in methodology. Before June 2022, the \actvr exceeds DeFiLlama’s adjusted \actvl because the token value deposited of removed protocols under DeFiLlama’s methodology is lower than the actual value that needs to be removed within the \actvr framework. Conversely, after June 2022, the \actvr falls below DeFiLlama’s adjusted \actvl because the token value deposited of protocols removed by DeFiLlama is higher than the actual value that needs to be removed within the \actvr framework. In both scenarios, the inaccurate valuation of double-counted removals according to DeFiLlama’s methodology is highlighted, as demonstrated in §3.3. However, all three metrics follow a similar trend, encompassing the surge during the \acdefi summer, a period marked by increased investor participation in the \acdefi market, as well as the sharp decline in Luna collapse on May 9, 2022 and FTX collapse on November 8, 2022.

Equation 9 shows the total receivables, total payables, and \actvr of Lido and Aave V2 in the Ethereum. The green area represents the value of total receivables, while the red area denotes the value of total payables. The protocol \actvl is calculated according to the Equation 9.

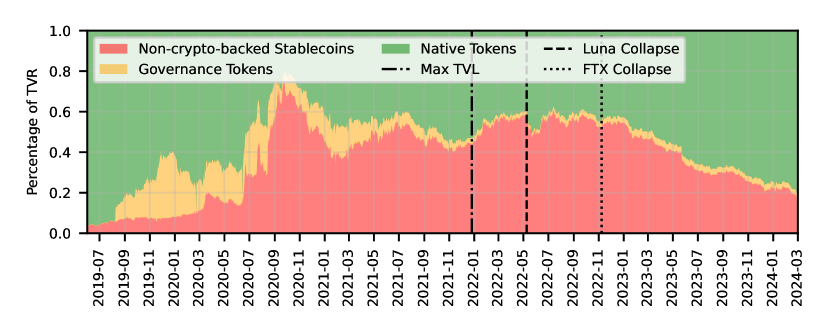

6.2. \Actvr Decomposition

Figure 9 depicts the time series plot of the decomposition of \actvr across all chains. We observe that native tokens dominate across all periods, but their percentage decreases before February 2022. The \acncb stablecoins surge before October 2020. The percentage of governance tokens experiences a rapid increase before January 2021 and began to decline thereafter. All three types of tokens exhibit stability after February 2022, with \acncb tokens and native tokens almost equally distributed. The stability corresponds to the stable period after the LUNA crash and before the FTX collapse in \actvl shown by Figure 5. After the FTX collapse, the proportion of native tokens rises, while the proportion of \acncb stablecoins declines.

6.3. Risk Analysis

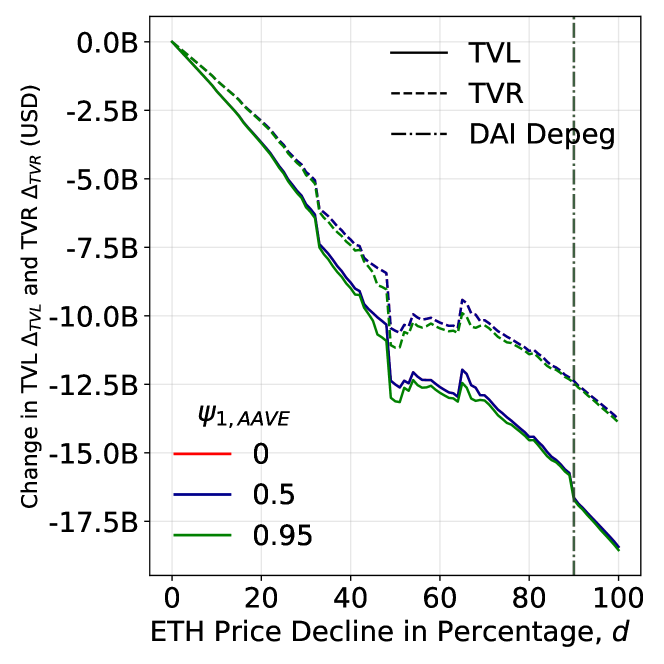

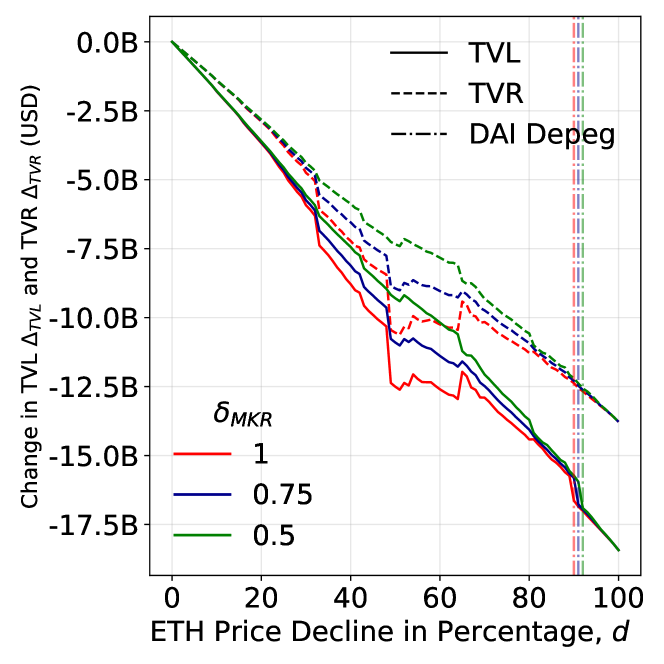

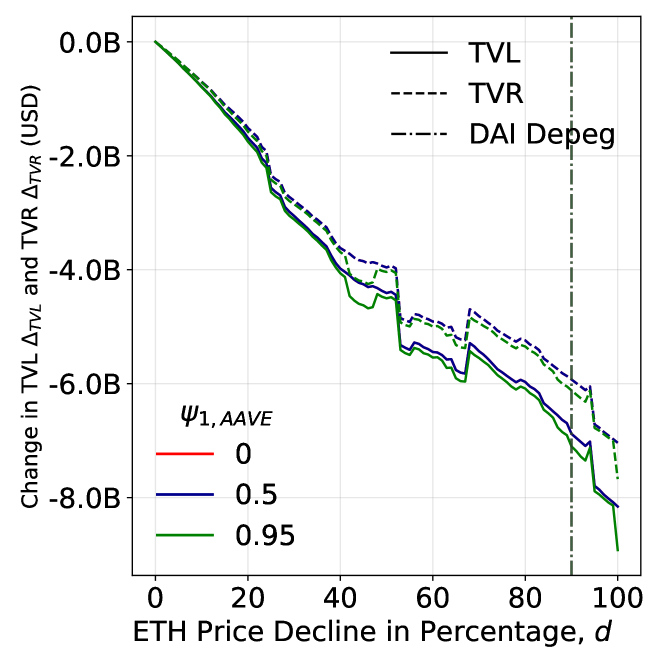

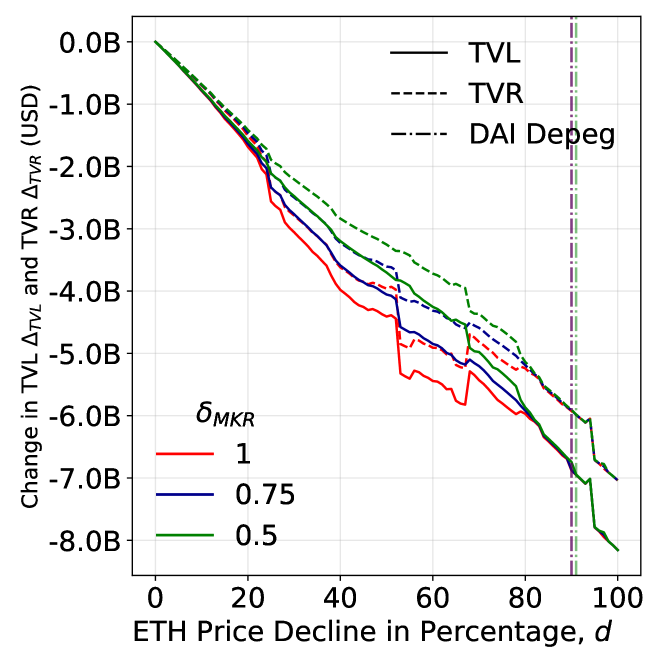

To examine the financial contagion risk derived from the existence of derivative tokens, as discussed in §4.2.5, we conduct comparative sensitivity tests for the change in \actvl and \actvr in terms of the ETH price decline according to Equation 7. For tractability, we assume that in each liquidation, only one rational liquidator will participate, liquidate the maximum amount of collateral possible, and seize borrowed assets based on their share of the user’s total debt. Leveraging on the data for the six leading \acdefi protocols in Figure 1, these tests are conducted on three representative dates, considering different sets of parameters. In Table 7, we set the default value of certain parameters and discuss the plausibility of selected values for risk-specific parameters via the reference of documentation. We detail how we implement the sensitivity test in Algorithm 1.

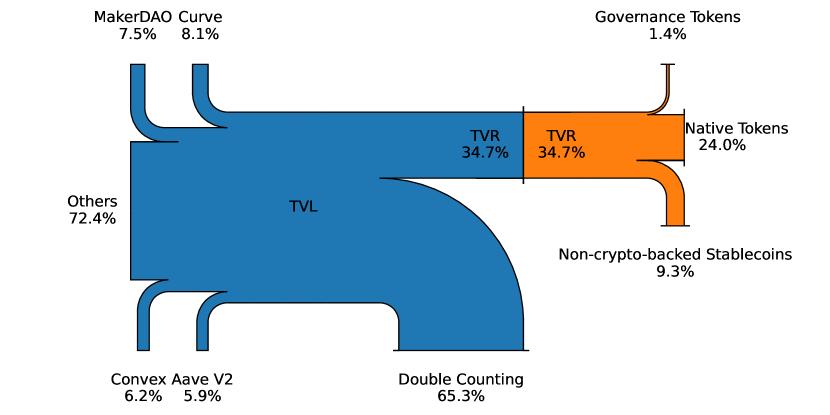

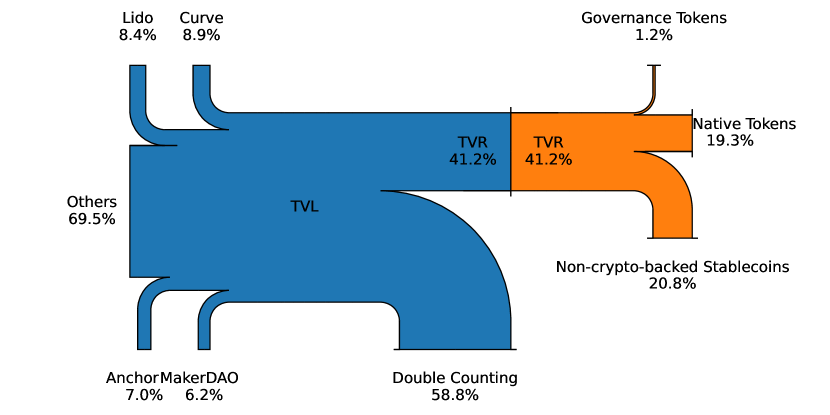

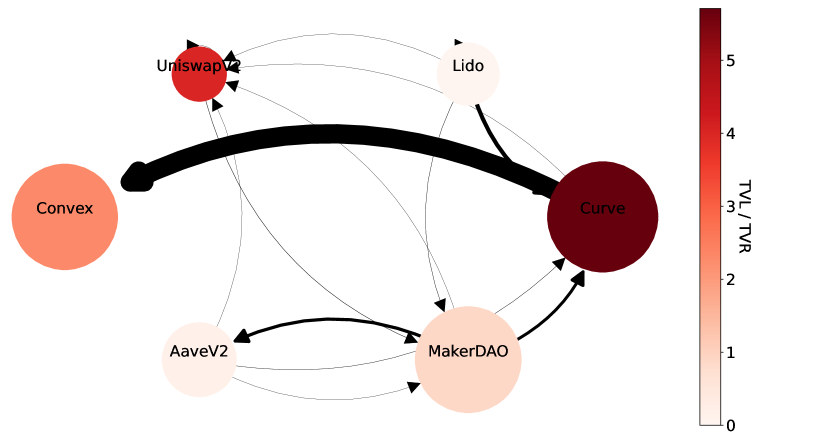

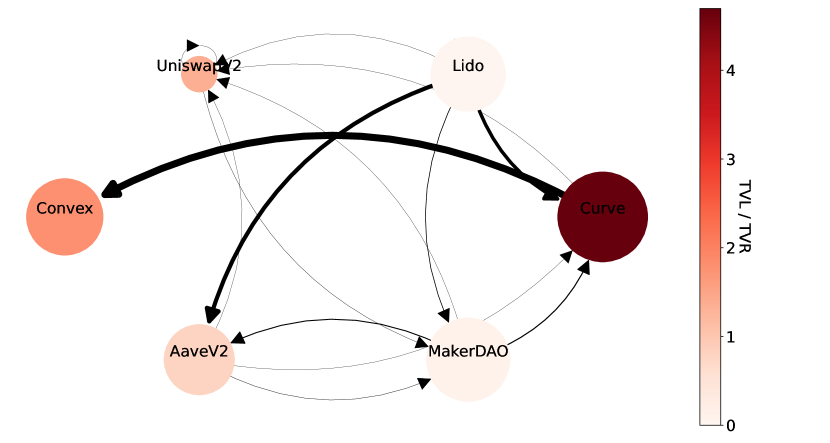

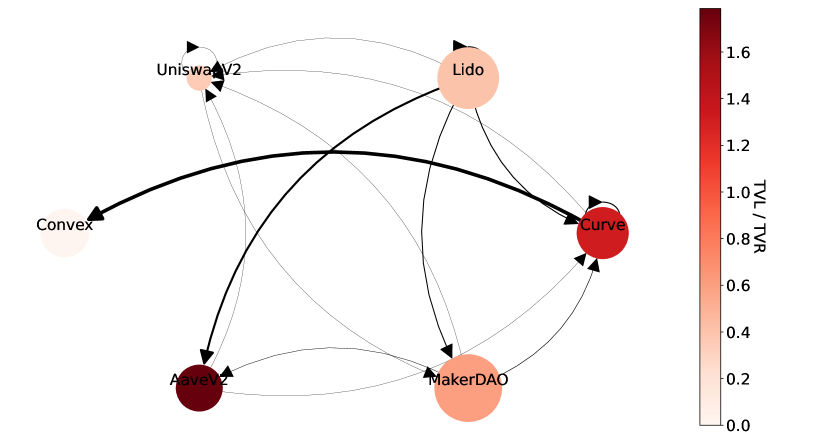

Figure 8 shows the double counting that happened among the six leading protocols. We observe that from the point when \actvl reaches the maximum value until the collapse of LUNA and FTX, the \actvl of protocols, excluding Lido, contracts. Additionally, the overall wrapping effect diminishes. These observations align with the overall \acdefi system dynamics illustrated in Figure 5. Since almost all \aclp tokens generated from the curve can be staked in convex, the wrapping effect between the Curve and the Convex is significant.

In Figure 10, we show how and change with . curves and curves with the default parameter setting are plotted in the red lines, which are compared with curves and curves with different parameter. Irrespective of parameter values, the curve is always convex due to the existence of liquidation mechanism in \acpplf and more sensitive to than the curve due to the existence of double counting, which aligns with the reasoning in §4.2.5.

| Parameters | Reference | Value | ||

| Maximum TVL (2021-12-02) | LUNA collapse (2022-05-09) | FTX collapse (2022-11-08) | ||

| CoinGecko | $4075.03 | $2249.89 | $1334.29 | |

| (Aave, 2022) | 0.5 | 0.5 | 0.5 | |

| (MakerDAO, 2022a) | 1 | 1 | 1 | |

| (Aave, 2022) | 0 | 0 | 0 | |

Next, we discuss how the value setting of other parameters in Equation 6 affects and .

-

(1)

Close factor : As shown in Figure 10, ceteris paribus, higher leads to greater drop in and . This is true for both and . The drop in under is greater than since the MakerDAO’s \actvl is higher than Aave V2’s \actvl.

-

(2)

Liquidation threshold . In Aave V2, corresponds to the close factor , which means that all collateral will be wiped out during the liquidation when the health factor of an account reaches . As shown in Figure 10, ceteris paribus, higher leads to earlier drop in and .

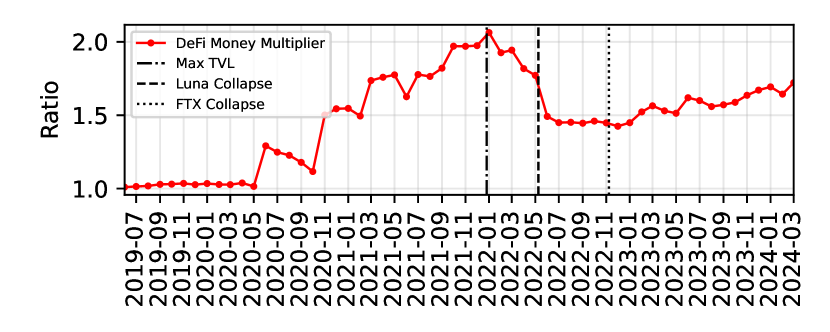

6.4. DeFi Money Multiplier

Similar to traditional finance, investors can take leverage in \acdefi. \actvr shares similarities with M0, the monetary base in economics, encompassing cash and bank deposits—representing the value directly withdrawable from the system. In comparison, \actvl can be likened to M2, which includes M0 plus checking deposits and other short-term deposits.

The M2 to M0 ratio, akin to the traditional “money multiplier”, characterizes the proportion of investor deposits that can be utilized by the bank (FRED, 2023). Drawing a parallel, we can divide \actvl by \actvr to compute the \acdefi money multiplier:

| (10) |

This ratio mirrors the double counting and wrapping effects within the \acdefi ecosystem, similar to the traditional finance concept of the money multiplier. Figure 11 plots the \acdefi money multiplier.

Table 9 shows the Spearman’s rank correlation coefficients (Spearman, 1904) between the \acdefi money multiplier (), key macroeconomic indicators in the US, and representative crypto market indicators. The observed positive correlation between the \acdefi money multiplier and cryptocurrency market indicators such as S&P Cryptocurrency Broad Digital Market Index (), Ethereum gas price (), and Ether price () is significant. During bullish periods in the cryptocurrency market, investors exhibit a propensity for increased investment in \acdefi, concurrently opting for leveraged positions. The \acdefi money multiplier is significantly negatively correlated with the \actrafi money multiplier (), showing the substitution effect between the \actrafi market and \acdefi. As a robustness test, we also calculate Spearman’s rank correlation coefficients (Spearman, 1904) between the natural logarithmic return of these indicators to make variables stationary.

The \acdefi money multiplier, derived from the \actvr and \actvl, affords a discerning perspective on the prevalence of double counting and the wrapping effect within the decentralized finance \acdefi realm. This metric assumes significance not only for investors navigating the intricacies of \acdefi but also for policymakers seeking to comprehend and address systemic risks within this decentralized financial ecosystem.

| Macroeconomic / TradFi indicators | Cryptocurrency / DeFi indicators | |||||||

| 1.00∗∗∗ | 0.71∗∗∗ | -0.19 | 0.06 | -0.01 | 0.28∗ | 0.07 | 0.25 | |

| 0.71∗∗∗ | 1.00∗∗∗ | -0.43∗∗∗ | 0.22 | -0.33∗ | -0.05 | -0.22 | -0.05 | |

| -0.19 | -0.43∗∗∗ | 1.00∗∗∗ | -0.15 | 0.09 | -0.21 | -0.19 | -0.18 | |

| 0.06 | 0.22 | -0.15 | 1.00∗∗∗ | -0.36∗∗ | -0.66∗∗∗ | -0.70∗∗∗ | -0.76∗∗∗ | |

| -0.01 | -0.33∗ | 0.09 | -0.36∗∗ | 1.00∗∗∗ | 0.64∗∗∗ | 0.65∗∗∗ | 0.55∗∗∗ | |

| 0.28∗ | -0.05 | -0.21 | -0.66∗∗∗ | 0.64∗∗∗ | 1.00∗∗∗ | 0.95∗∗∗ | 0.91∗∗∗ | |

| 0.07 | -0.22 | -0.19 | -0.70∗∗∗ | 0.65∗∗∗ | 0.95∗∗∗ | 1.00∗∗∗ | 0.91∗∗∗ | |

| 0.25 | -0.05 | -0.18 | -0.76∗∗∗ | 0.55∗∗∗ | 0.91∗∗∗ | 0.91∗∗∗ | 1.00∗∗∗ | |

| Macroeconomic / TradFi indicators | Cryptocurrency / DeFi indicators | |||||||

| 1.00∗∗∗ | 0.30∗ | -0.11 | 0.40∗∗ | -0.03 | 0.06 | 0.04 | -0.01 | |

| 0.30∗ | 1.00∗∗∗ | -0.26 | 0.69∗∗∗ | -0.08 | 0.09 | 0.07 | -0.16 | |

| -0.11 | -0.26 | 1.00∗∗∗ | -0.25 | -0.09 | -0.17 | -0.25 | 0.02 | |

| 0.40∗∗ | 0.69∗∗∗ | -0.25 | 1.00∗∗∗ | -0.04 | -0.05 | -0.06 | -0.08 | |

| -0.03 | -0.08 | -0.09 | -0.04 | 1.00∗∗∗ | 0.56∗∗∗ | 0.49∗∗∗ | 0.08 | |

| 0.06 | 0.09 | -0.17 | -0.05 | 0.56∗∗∗ | 1.00∗∗∗ | 0.88∗∗∗ | 0.17 | |

| 0.04 | 0.07 | -0.25 | -0.06 | 0.49∗∗∗ | 0.88∗∗∗ | 1.00∗∗∗ | 0.33∗ | |

| -0.01 | -0.16 | 0.02 | -0.08 | 0.08 | 0.17 | 0.33∗ | 1.00∗∗∗ | |

7. Related Work

7.1. Total Value Locked

Chiu et al. (2023) leverage on a standard theoretical production-network model to assess the value added and service outputs across various DeFi sectors. Saengchote (2021) examines the flow of a stablecoin between protocols, offering indicative evidence of DeFi yield-chasing behavior, shedding light on the true implications of DeFi total value locked. \actvl is a fundamental element in assessing the valuation of \acdefi protocols (Kumar et al., 2022; Şoiman et al., 2023). Stepanova et al. (2021) investigate the evolution of \actvl. \actvl can work as a valuable tool for monitoring market dynamics and assessing the risk of bubbles in the digital financial landscape (Maouchi et al., 2022).

7.2. Double Counting

Double counting is also common in macroeconomics and the carbon market. The input-output framework that is used to avoid double-counting is well-known in economics (Koopman et al., 2008, 2013, 2014). Double counting, leading to poor emissions accounting, has the potential to undermine carbon markets. Schneider et al. (2019) emphasize the pivotal role of addressing double counting in achieving the goals of the Paris Agreement and identify key elements for a robust resolution that ensures environmental effectiveness and enables cost-effective mitigation.

7.3. Risks in \acdefi

Many researchers study the liquidation risks, financial stability risks, and fragility in the \acdefi lending market (Qin et al., 2021; Chiu et al., 2022; Darlin et al., 2022). Bekemeier (2021) examines the systemic risk in \acdefi. Qin et al. (2022) quantify the on-chain leverage risk in \acdefi. Nadler et al. (2023) introduce a fully decentralized insurance protocol based on smart contracts to allow risk transfer in \acdefi. Tzinas and Zindros (2023) study the principal-agent problem in the context of liquid staking, which leads to unexpected risks due to delegation.

7.4. Financial Contagion

Financial contagion is the transmission of market disturbances, typically negative, across borders on an international scale or between banks domestically (Bavister and Squirrell, 2000). Debates persist regarding the underlying causes of financial contagion. (Longstaff, 2010) empirically investigate the pricing dynamics of subprime asset-backed \acpcdo and their contagion impact on other markets. (Allen and Gale, 2000) and (Lagunoff and Schreft, 2001) investigate financial contagion arising from financial links among financial intermediaries. (Kaminsky and Reinhart, 2000) document that interconnected trade relations and shared exposure to a common creditor can explain previous clusters of crises, including not only the debt crises of the early 1980s and 1990s but also the historical trend of contagion. (Kiyotaki and Moore, 2002), (Kaminsky et al., 2003), (King and Wadhwani, 1990), (Calvo, 2004), and others, outline mechanisms where negative shocks in one market signify the arrival of economic news directly impacting collateral values or cash flows associated with securities in other markets. In this scenario, contagion can be seen as the transmission of information from more-liquid or swiftly price-discovering markets to others. (Vayanos, 2004), (Acharya and Pedersen, 2005), (Longstaff, 2010), and additional researchers suggest that a significant negative shock in one market could lead to an elevation in the risk premium in other markets. In this scenario, contagion arises as adverse returns in the distressed market influence subsequent returns in other markets through a time-varying risk premium.

8. Discussion

Despite the valuable contributions made, this paper acknowledges certain limitations.

8.1. Granularity

One notable area for potential expansion involves extending the concepts of \actvr and \actvl beyond the protocol level to the smart contract level. Within the \acdefi ecosystem, there exist not only protocols built on smart contracts but also isolated token contracts that could play a role in generating derivative tokens. A direction for future studies could involve broadening the scope of \actvl and \actvr. Researchers might consider encompassing the aggregation of all \acdefi smart contracts. This approach would provide a more comprehensive understanding of the total value and risk within the \acdefi landscape, offering insights into the broader implications of these metrics.

8.2. Subjectivity

This paper acknowledges the subjective nature of \actvr measurement, highlighting the absence of a clear method for automating it. Careful manual processing is essential for distinguishing between plain and derivative tokens. Variation in lists of plain tokens may result in different \actvr. Due to resource constraints, this paper opts to retrieve the plain token list from CoinMarketCap rather than label it. Future research could explore automation techniques for distinguishing plain and derivative tokens.

9. Conclusion

This paper empirically analyzes how double counting arises in the traditional \actvl framework. We introduce an enhanced measurement framework, the \actvr, to evaluate the actual value locked within a \acdefi system and mitigate double counting. By decomposing \actvl of all \acdefi protocols and calculating \actvr, we find a substantial amount of double counting within the \acdefi system, with a maximum of 182.15 billion with a \actvl-\actvr ratio around 3. We track the evolution of token composition in \actvr over time. Additionally, we uncover the escalating crash risk stemming from double counting within the traditional \actvl framework, employing the systems of two prominent protocols. We highlight the pronounced sensitivity of \actvl to token prices when double counting exists, showing that \actvr is a more stable metric when compared to \actvl. We propose the \acdefi money multiplier, drawing parallels with the \actrafi macroeconomic money multiplier. The \acdefi multiplier utilizes both \actvr and \actvl to quantify double counting. We document that the \acdefi money multiplier is positively correlated with crypto market indicators and negatively correlated with macroeconomic indicators.

References

- (1)

- Aave (2022) Aave. 2022. Liquidations - Aave V2. https://docs.aave.com/developers/v/2.0/guides/liquidations#calculating-profitability-vs-gas-cost

- Aave (2023) Aave. 2023. Liquidations - Aave V3. https://docs.aave.com/developers/guides/liquidations

- Acharya and Pedersen (2005) Viral V. Acharya and Lasse Heje Pedersen. 2005. Asset pricing with liquidity risk. Journal of Financial Economics 77, 2 (8 2005), 375–410. https://doi.org/10.1016/J.JFINECO.2004.06.007

- Allen and Gale (2000) Franklin Allen and Douglas Gale. 2000. Financial Contagion. https://doi.org/10.1086/262109 108, 1 (2000), 1–33. https://doi.org/10.1086/262109

- Andolfatto et al. (2017) David Andolfatto, Fernando M. Martin, and Shengxing Zhang. 2017. Rehypothecation and liquidity. European Economic Review 100 (11 2017), 488–505. https://doi.org/10.1016/J.EUROECOREV.2017.09.010

- Baird et al. (2018) Leemon Baird, Mance Harmon, and Paul Madsen. 2018. Hedera: A Public Hashgraph Network & Governing Council. (2018).

- Bavister and Squirrell (2000) Barry D. Bavister and Jayne M. Squirrell. 2000. Contagion: Understanding How It Spreads. The World Bank Research Observer 15, 2 (8 2000), 177–197. https://doi.org/10.1093/WBRO/15.2.177

- Bekemeier (2021) Felix Bekemeier. 2021. Deceptive Assurance? A onceptual View on Systemic Risk in Decentralized Finance (DeFi). ACM International Conference Proceeding Series (12 2021), 76–87. https://doi.org/10.1145/3510487.3510499

- Binance Academy (2023) Binance Academy. 2023. Total Value Locked (TVL). https://academy.binance.com/en/glossary/total-value-locked-tvl

- Calvo (2004) Guillermo A. Calvo. 2004. Contagion in Emerging Markets: When Wall Street is a Carrier. Latin American Economic Crises (2004), 81–91. https://doi.org/10.1057/9781403943859{_}5

- Chandler (2020) Simon Chandler. 2020. DeFi’s ‘Total Value Locked In’ Metric Is A Crooked Mirror. https://cryptonews.com/exclusives/defi-s-total-value-locked-in-metric-is-a-crooked-mirror-7694.htm

- Chiu et al. (2022) Jonathan Chiu, Ozdenoren Emre, Kathy Yuan, and Shengxing Zhang. 2022. On the Inherent Fragility of DeFi Lending. (2022). https://g20.org/wp-content/uploads/2022/02/FSB-Report-on-Assessment-of-Risks-to-Financial-

- Chiu et al. (2023) Jonathan Chiu, Thorsten V. Koeppl, Hanna Yu, and Shengxing Zhang. 2023. Understanding Defi Through the Lens of a Production-Network Model. SSRN Electronic Journal (6 2023). https://doi.org/10.2139/SSRN.4487615

- CoinMarketCap (2023a) CoinMarketCap. 2023a. Top Governance Tokens by Market Capitalization. https://coinmarketcap.com/view/governance/

- CoinMarketCap (2023b) CoinMarketCap. 2023b. Top Layer 1 Tokens by Market Capitalization. https://coinmarketcap.com/view/layer-1/

- CoinMarketCap (2023c) CoinMarketCap. 2023c. Top Layer 2 Tokens by Market Capitalization. https://coinmarketcap.com/view/layer-2/

- CoinMarketCap (2024) CoinMarketCap. 2024. Collateralized Debt Position (CDP) Definition. https://coinmarketcap.com/academy/glossary/collateralized-debt-position-cdp

- DappRadar (2022) DappRadar. 2022. DeFi Rankings. https://docs.dappradar.com/rankings/defi-rankings

- Darlin et al. (2022) Michael Darlin, Georgios Palaiokrassas, and Leandros Tassiulas. 2022. Debt-Financed Collateral and Stability Risks in the DeFi Ecosystem. 2022 4th Conference on Blockchain Research and Applications for Innovative Networks and Services, BRAINS 2022 (2022), 5–12. https://doi.org/10.1109/BRAINS55737.2022.9909090

- DeFi Pulse (2022) DeFi Pulse. 2022. Total Value Locked (TVL). https://docs.defipulse.com/methodology/tvl

- DefiLlama (2023) DefiLlama. 2023. DeFi Dashboard. https://defillama.com/

- DeFiLlama (2023) DeFiLlama. 2023. DefiLlama and our methodology. https://docs.llama.fi/list-your-project/readme

- Deloitte (2023a) Deloitte. 2023a. IAS 1 — Presentation of Financial Statements. https://www.iasplus.com/en/standards/ias/ias1

- Deloitte (2023b) Deloitte. 2023b. IFRS 10 — Consolidated Financial Statements. https://www.iasplus.com/en/standards/ifrs/ifrs10

- ethereum.org (2024) ethereum.org. 2024. Proof-of-stake (PoS). https://ethereum.org/developers/docs/consensus-mechanisms/pos

- FRED (2023) FRED. 2023. The monetary multiplier and bank reserves. https://fredblog.stlouisfed.org/2023/07/the-monetary-multiplier-and-bank-reserves/

- Gogol et al. (2023) Krzysztof Gogol, Christian Killer, Malte Schlosser, Thomas Bocek, and Burkhard Stiller. 2023. SoK: Decentralized Finance (DeFi)-Fundamentals, Taxonomy and Risks. Authorea Preprints (6 2023). https://doi.org/10.22541/AU.168568220.09436681/V1

- Irving (1912) Fisher Irving. 1912. Elementary Principles of Economics. 69 pages.

- Kaminsky and Reinhart (2000) Graciela L. Kaminsky and Carmen M. Reinhart. 2000. On crises, contagion, and confusion. Journal of International Economics 51, 1 (6 2000), 145–168. https://doi.org/10.1016/S0022-1996(99)00040-9

- Kaminsky et al. (2003) Graciela L. Kaminsky, Carmen M. Reinhart, and Carlos A. Végh. 2003. The Unholy Trinity of Financial Contagion. Journal of Economic Perspectives 17, 4 (9 2003), 51–74. https://doi.org/10.1257/089533003772034899

- King and Wadhwani (1990) Mervyn A. King and Sushil Wadhwani. 1990. Transmission of Volatility between Stock Markets. The Review of Financial Studies 3, 1 (1 1990), 5–33. https://doi.org/10.1093/RFS/3.1.5

- Kiyotaki and Moore (2002) Nobuhiro Kiyotaki and John Moore. 2002. Evil Is the Root of All Money. American Economic Review 92, 2 (5 2002), 62–66. https://doi.org/10.1257/000282802320189014

- Klages-Mundt and Minca (2022) Ariah Klages-Mundt and Andreea Minca. 2022. While stability lasts: A stochastic model of noncustodial stablecoins. Mathematical Finance 32, 4 (10 2022), 943–981. https://doi.org/10.1111/MAFI.12357

- Koopman et al. (2013) Robert Koopman, Marinos Tsigas, Zhi Wang, and Xin Li. 2013. CGE experiments based on the GTAP database and two TiVA-based databases. https://ageconsearch.umn.edu/record/332369

- Koopman et al. (2008) Robert Koopman, Zhi Wang, and Shang-Jin Wei. 2008. How Much of Chinese Exports is Really Made In China? Assessing Domestic Value-Added When Processing Trade is Pervasive. (6 2008). https://doi.org/10.3386/W14109

- Koopman et al. (2014) Robert Koopman, Zhi Wang, and Shang Jin Wei. 2014. Tracing Value-Added and Double Counting in Gross Exports. American Economic Review 104, 2 (2 2014), 459–94. https://doi.org/10.1257/AER.104.2.459

- Kumar et al. (2022) Aviral Kumar, Tu Le, Marwa Elnahass, Dominik Metelski, and Janusz Sobieraj. 2022. Decentralized Finance (DeFi) Projects: A Study of Key Performance Indicators in Terms of DeFi Protocols’ Valuations. International Journal of Financial Studies 2022, Vol. 10, Page 108 10, 4 (11 2022), 108. https://doi.org/10.3390/IJFS10040108

- L2BEAT (2023) L2BEAT. 2023. Frequently Asked Questions. https://l2beat.com/faq

- Lagunoff and Schreft (2001) Roger Lagunoff and Stacey L. Schreft. 2001. A Model of Financial Fragility. Journal of Economic Theory 99, 1-2 (7 2001), 220–264. https://doi.org/10.1006/JETH.2000.2733

- Longstaff (2010) Francis A. Longstaff. 2010. The subprime credit crisis and contagion in financial markets. Journal of Financial Economics 97, 3 (9 2010), 436–450. https://doi.org/10.1016/J.JFINECO.2010.01.002

- MakerDAO (2022a) MakerDAO. 2022a. Liquidation 2.0 Module. https://docs.makerdao.com/smart-contract-modules/dog-and-clipper-detailed-documentation

- MakerDAO (2022b) MakerDAO. 2022b. Peg Stability. https://manual.makerdao.com/module-index/module-psm

- Maouchi et al. (2022) Youcef Maouchi, Lanouar Charfeddine, and Ghassen El Montasser. 2022. Understanding digital bubbles amidst the COVID-19 pandemic: Evidence from DeFi and NFTs. Finance Research Letters 47 (6 2022), 102584. https://doi.org/10.1016/J.FRL.2021.102584

- Medium (2022) Medium. 2022. stETH Depegging: What are the Consequences? https://medium.com/huobi-research/steth-depegging-what-are-the-consequences-20b4b7327b0c

- Moin et al. (2020) Amani Moin, Kevin Sekniqi, and Emin Gun Sirer. 2020. SoK: A Classification Framework for Stablecoin Designs. Lecture Notes in Computer Science (including subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics) 12059 LNCS (2020), 174–197. https://doi.org/10.1007/978-3-030-51280-4{_}11/FIGURES/7

- Nadler et al. (2023) Matthias Nadler, Felix Bekemeier, and Fabian Schar. 2023. DeFi Risk Transfer: Towards A Fully Decentralized Insurance Protocol. 2023 IEEE International Conference on Blockchain and Cryptocurrency, ICBC 2023 (2023). https://doi.org/10.1109/ICBC56567.2023.10174937

- Purdy (2020) Jack Purdy. 2020. How to interpret Total Value Locked (TVL) in DeFi. https://messari.io/report/how-to-interpret-total-value-locked-tvl-in-defi

- Qin et al. (2021) Kaihua Qin, Liyi Zhou, Pablo Gamito, Philipp Jovanovic, and Arthur Gervais. 2021. An empirical study of DeFi liquidations: Incentives, risks, and instabilities. Proceedings of the ACM SIGCOMM Internet Measurement Conference, IMC (11 2021), 336–350. https://doi.org/10.1145/3487552.3487811

- Saengchote (2021) Kanis Saengchote. 2021. Where do DeFi Stablecoins Go? A Closer Look at What DeFi Composability Really Means. SSRN Electronic Journal (7 2021). https://doi.org/10.2139/SSRN.3893487

- Schneider et al. (2019) Lambert Schneider, Maosheng Duan, Robert Stavins, Kelley Kizzier, Derik Broekhoff, Frank Jotzo, Harald Winkler, Michael Lazarus, Andrew Howard, and Christina Hood. 2019. Double counting and the Paris Agreement rulebook. Science 366, 6462 (10 2019), 180–183. https://doi.org/10.1126/SCIENCE.AAY8750

- Şoiman et al. (2023) Florentina Şoiman, Jean Guillaume Dumas, and Sonia Jimenez-Garces. 2023. What drives DeFi market returns? Journal of International Financial Markets, Institutions and Money 85 (6 2023), 101786. https://doi.org/10.1016/J.INTFIN.2023.101786

- Spearman (1904) C. Spearman. 1904. The Proof and Measurement of Association between Two Things. The American Journal of Psychology 15, 1 (1 1904), 72. https://doi.org/10.2307/1412159

- Stelareum (2023) Stelareum. 2023. Total Value Locked (TVL) in DeFi protocols. https://www.stelareum.io/en/defi-tvl.html

- Stepanova and Eriņš (2021) Viktorija Stepanova and Ingars Eriņš. 2021. Review of Decentralized Finance Applications and Their Total Value Locked. TEM Journal 10, 1 (2021), 327–333.

- Token Terminal (2023) Token Terminal. 2023. GMV data. https://tokenterminal.com/docs/our-metrics/gmv-data#total-value-locked-tvl

- Tzinas and Zindros (2023) Apostolos Tzinas and Dionysis Zindros. 2023. The Principal–Agent Problem in Liquid Staking. Cryptology ePrint Archive (2023).

- Ultron (2023) Ultron. 2023. Ultron Whitepaper. (2023).

- Vayanos (2004) Dimitri Vayanos. 2004. Flight to Quality, Flight to Liquidity, and the Pricing of Risk. (2 2004). https://doi.org/10.3386/W10327

- Wang et al. (2022) Zhipeng Wang, Kaihua Qin, Duc Vu Minh, and Arthur Gervais. 2022. Speculative Multipliers on DeFi: Quantifying On-Chain Leverage Risks. In Financial Cryptography and Data Security. Vol. 13411 LNCS. Springer Science and Business Media Deutschland GmbH, 38–56. https://doi.org/10.1007/978-3-031-18283-9{_}3

- Werner et al. (2022) Sam Werner, Daniel Perez, Lewis Gudgeon, Ariah Klages-Mundt, Dominik Harz, and William Knottenbelt. 2022. SoK: Decentralized Finance (DeFi). Proceedings of the 4th ACM Conference on Advances in Financial Technologies (9 2022), 30–46. https://doi.org/10.1145/3558535.3559780

- Xu et al. (2023) Jiahua Xu, Krzysztof Paruch, Simon Cousaert, and Yebo Feng. 2023. SoK: Decentralized Exchanges (DEX) with Automated Market Maker (AMM) Protocols. Comput. Surveys 55, 11 (2 2023). https://doi.org/10.1145/3570639

APPENDIX

Appendix A Ethics

This work does not raise any ethical issues

Appendix B DeFi Bookkeeping

We model value transfers of common transactions in \acdefi protocols via the double-entry bookkeeping in the traditional accounting framework. The double-entry booking keeping has two equal journal entries known as debit (Dr.) and credit (Cr.), which represent a transfer of value to and from that account, respectively (Irving, 1912). The credit side should be indented.

| Protocol | Transaction | Definition | Journal Entry | Quantity | Amount | Type | Example Transaction |

| MakerDAO | Borrowing. | User supplies tokens T with dollar price as collateral to mint stablecoins S with dollar price . | Dr. Receivables – S Dr. Value Locked – T Cr. New Money – S Cr. Payables – T | Assets Assets Liabilities Liabilities | 0x959…0adb | ||

| MakerDAO | Stability fee accrual. | Debt accrues when its dollar price is . | Dr. Receivables – S Cr. Unrealized Gain – S | Assets Equities | - | ||

| MakerDAO | Repayment and collateral withdrawal. | User repays stablecoins S with dollar price and withdraws collateral T with dollar price . | Dr. New Money – S Dr. Payables – T Cr. Receivables – S Cr. Value Locked – T | Liabilities Liabilities Assets Assets | 0x284…701e | ||

| MakerDAO | Collateral price appreciation. | collateral experiences price appreciation . | Dr. Value Locked – T Cr. Payables – T | Assets Liabilities | - | ||

| MakerDAO | Collateral price depreciation. | collateral experiences price depreciation . | Dr. Payables – T Cr. Value Locked – T | Liabilities Assets | - | ||

| MakerDAO | Liquidation penalty. | A liquidation penalty applies to the initial debt and accrual stability fee when the collateral-to-debt ratio of the user’s vault is lower than the liquidation ratio. | Dr. Receivables – Cr. Unrealized Gain – | Assets Equities | - | ||

| MakerDAO | Liquidation settlement. | The liquidator wins in the debt auction, sells collateral with dollar price , and repays debt , liquidation penalty and stability fee with dollar price of the liquidated vault. | Dr. New Money – S Dr. Unrealized Gain – S Dr. Payables – T Cr. Receivables – S Cr. Value Locked – T | Liabilities Equities Liabilities Assets Assets | 0x4d0…cbb4 | ||

| Aave | Supplying. | User supplies tokens T with dollar price as collateral to issue aToken A with dollar price | Dr. Value Locked – T Cr. Payables – A | Assets Liabilities | 0xd49…8a04 | ||

| Aave | Borrowing. | A user borrows tokens B with dollar price in a lending protocol to receive debt tokens D with dollar price . | Dr. Receivables – D Cr. Value Locked – B | Assets Assets | 0xf7d…a661 | ||

| Aave | Debt interest accrual. | Debt token accrues when its dollar price is , representing debt accruals when its dollar price is | Dr. Receivables – D Cr. Unrealized Gain – B | Assets Equities | - | ||

| Aave | Repayment. | A user repays tokens B with dollar price to burn debt tokens D with dollar price . | Dr. Value Locked – B Cr. Receivables – D | Assets Assets | 0x95e…f410 | ||

| Aave | Collateral price appreciation. | collateral experiences price appreciation . | Dr. Value Locked – T Cr. Payables – T | Assets Liabilities | - | ||

| Aave | Collateral price depreciation. | collateral experiences price depreciation . | Dr. Payables – T Cr. Value Locked – T | Liabilities Assets | - | ||

| Aave | Liquidation settlement. | When the health factor of an Aave user is lower than one, the liquidator will trigger the liquidation. The liquidator repays token B with dollar price to receive collateral token T, where is the close factor and is the liquidation bonus. The accrual interest is realized via minting atoken. | Dr. Value Locked – B Dr. Unrealized Gain – B Dr. Payables – A Cr. Receivables – D Cr. Realized Gain – A Cr. Value Locked – T | Assets Equities Liabilities Assets Equities Assets | 0x682…7459 |

Appendix C Derivative Token Pegging Mechanism

For derivative tokens that are not crypto-backed stablecoins generated by the \accdp, In cases where the pegged value of the derivative token deviates from the market value, it becomes subject to the arbitrage processes outlined in Arbitrager’s Strategy 1 for values above the market and Arbitrager’s Strategy 2 for values below the market.

For crypto-backed stablecoins generated by the \accdp, the stablecoin value is pegged to the value of fiat currency through two mechanisms if the total debt value is above the total collateral value . Crypto-backed stablecoins utilize \accdp User’s Strategies 3 and 4 for pegging. To enhance liquidity and pegging stability, some \acpcdp employ a pool between crypto-backed and non-crypto-backed stablecoins (e.g., MakerDAO’s peg stability module (MakerDAO, 2022b)), which allows swapping between the two stablecoins. This setup enables Arbitrager’s Strategies 1 and 2 to facilitate the pegging. If the total debt value is below the total collateral value, the crypto-backed stablecoins will depeg, with their price equal to the pegged value times the ratio between the total collateral value and debt value.

| Arbitrager’s Strategy 1 or |

| 1: Buy derivative tokens at price from the market using (scalar depends on the budget). |

| 2: Burn derivative tokens to redeem all underlying tokens in the given ratio in the liquidity pool. |

| 3: Sell all underlying tokens to get dollar and increase derivative token price . |

| 4: Earn profit and repeat steps 1 to 5 until , i.e. . |

| Arbitrager’s Strategy 2 or |

| 1: Buy all its underlying tokens in the given ratio from the market using (scalar depends on the budget). |

| 2: Lock all underlying tokens in the given ratio to issue derivative token in the liquidity pool. |

| 3: Sell derivative token to get dollar and reduce derivative token price . |

| 4: Earn profit and repeat steps 1 to 5 until , i.e. . |

| Vault Owner’s Strategy 1 |

| 1: Buy crypto-backed stablecoin at price from the market, with the total cost being the dollar amount of debt . |

| 2: Repay debt to unlock all collateral from the \accdp. |

| 3: Save a cost of to unlock all collateral and increase crypto-backed stablecoin price by decreasing its supply. |

| Vault Owner’s Strategy 1 |

| 1: Observe that crypto-backed stablecoin price in the market is higher than its peg value , i.e. . |

| 2: Supply more collateral to increase the collateral-to-debt ratio to decrease the probability of liquidation. |

| 3: Decrease crypto-backed stablecoin price by increasing its supply. |

Appendix D Esoteric Blockchain Analysis

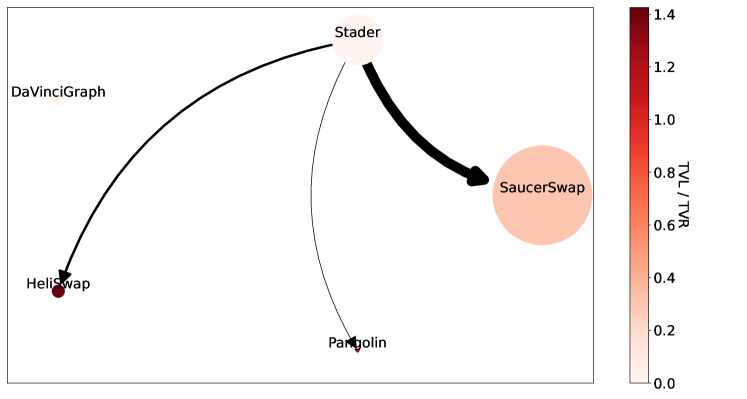

To gain a broader understanding of the double-counting issue, we analyze two esoteric blockchains: Hedera ranked 42nd in \actvl and Ultron ranked 21st in \actvl. Our findings indicate that blockchains with limited infrastructure feature simpler token-wrapping networks, which leads to less double counting. Additionally, we observe that the DeFiLlama framework addressing the double counting might deflate the true value redeemable of an esoteric blockchain.

D.1. Hedera

Hedera is a public hashgraph blockchain and governing body tailored to meet the requirements of mainstream markets (Baird et al., 2018). Figure 12 shows the token wrapping network of Hedera at the end of the sample period. Hedera only has eight DeFi protocols, with three projects having zero TVL and being shut down. Among the other six protocols, only one liquidity staking protocol named Stader can generate receipt tokens that can be subsequently deposited into other protocols. Compared to the networks in Ethereum mentioned in §6.3, Hedera has a simpler token-wrapping network, thus experiencing less double counting under the \actvl framework. Figure 13 shows the \actvl and \actvr of Hedera.

D.2. Ultron

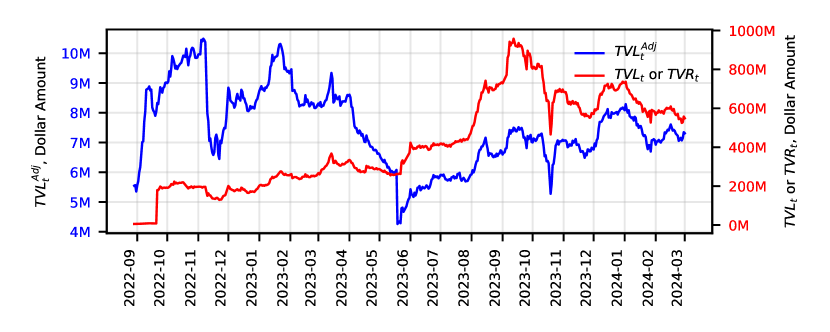

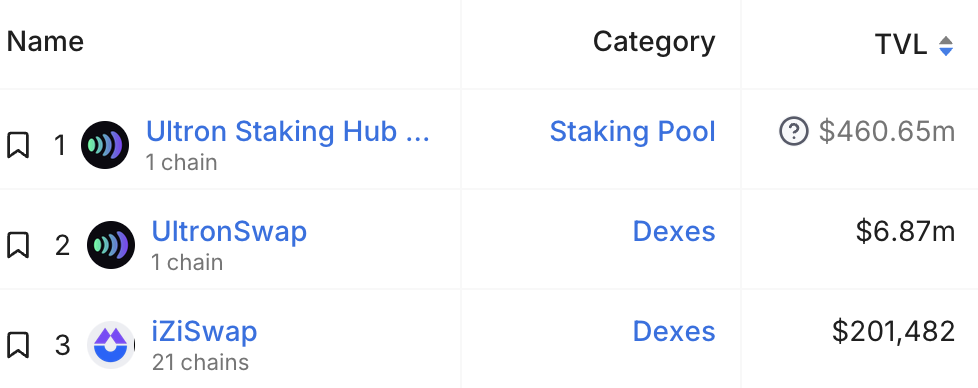

Ultron is an esoteric layer 1 blockchain (Ultron, 2023) with three \acdefi protocols in its ecosystem. The Ultron Staking Hub NFT, created by the Ultron Foundation, serves as a digital asset growth instrument allowing users to earn daily \acapr returns in Ultron native tokens. Each user can mint \acpnft and stake them on the protocol for 5 years with a vesting schedule. All liquidity is securely locked within a staking smart contract and can be claimed at specific timelines. UltronSwap and iZiSwap are two \acpdex on Ultron.

Ultron does not involve wrapping or leverage. \Acpnft minted by Ultron Staking Hub NFT and \aclp tokens generated by two \acpdex cannot be further deposited into other protocols. Therefore, Ultron is not subject to the double counting problem under the \actvr framework. However, DeFiLlama removes the TVL of the Ultron Staking Hub NFT protocol from Ultron’s \actvl excluding double counting, as this protocol falls under the category of protocols that deposit into another protocol. DeFiLlama’s methodology is inaccurate as demonstrated in §3.3, making the DeFillama-adjusted TVL of Ultron significantly lower than its \actvr as shown in Figure 14.