Partial Identification of Heteroskedastic Structural VARs:

Theory and Bayesian Inference

Abstract

We consider structural vector autoregressions identified through stochastic volatility. Our focus is on whether a particular structural shock is identified by heteroskedasticity without the need to impose any sign or exclusion restrictions. Three contributions emerge from our exercise: (i) a set of conditions under which the matrix containing structural parameters is partially or globally unique; (ii) a statistical procedure to assess the validity of the conditions mentioned above; and (iii) a shrinkage prior distribution for conditional variances centred on a hypothesis of homoskedasticity. Such a prior ensures that the evidence for identifying a structural shock comes only from the data and is not favoured by the prior. We illustrate our new methods using a U.S. fiscal structural model.

keywords:

Identification Through Heteroskedasticity , Stochastic Volatility , Non-centred Parameterisation , Shrinkage Prior , Normal Product Distribution , Tax Shocks JEL classification: C11, C12, C32, E621 Introduction

This paper considers the partial identification of a structural shock in a multivariate setup that is in line with the definition by Rubio-Ramírez et al. (2010). This definition states that a structural shock is identified when the parameters of its corresponding equation within a system are globally identified, that is, up to being sign–normalised as in Waggoner and Zha (2003b). Partial identification is essential in empirical analyses using Structural Vector Autoregressions (SVARs) and focusing on fewer shocks than there are variables in the model. For example, it is often the case that one is interested in the identification of a specific shock, such as a monetary or a fiscal policy shock. Moreover, partial identification becomes even more important in larger systems of variables that, on the one hand, improve the forecasting performance of the model, resulting in more realistic impulse responses but, on the other one, increase the number of shocks that are not necessarily of interest or difficult to interpret (see Carriero et al., 2019).

In our approach, the source of partial identification is conditional heteroskedasticity that offers the potential to identify all the parameters of a given equation up to a sign following the seminal developments proposed by Rigobon (2003). We choose a specific model for conditional variances, namely Stochastic Volatility (SV) as proposed by Cogley and Sargent (2005), and in line with the identification ideas put forth by recent studies, such as Lewis (2021) and Bertsche and Braun (2022). Not only does this choice offer a flexible approach to address identification, but it also has been shown to be a key extension of homoskedastic SVARs that leads to improved forecasting performance (see, e.g., Clark and Ravazzolo, 2015; Chan and Eisenstat, 2018).

The main contribution of this paper is a general condition for the partial identification of a structural shock via heteroskedasticity. This condition states that a structural shock is identified up to sign if the sequence of its conditional variances is distinct from and not proportional to those for all other shocks. Our condition covers both conditional and unconditional heteroskedasticity and most of the heteroskedastic models used in empirical studies. It is expressed explicitly in terms of conditional variances, simplifying the proof and granting a straightforward interpretation. In these respects, it stands out from the existing conditions on which we provide more details in Section 2. We further show that a shock having such a unique sequence of (conditional) variances leads to globally identified impulse response functions.

Importantly, the conditions for partial identification that we derive can be verified. In this regard, a second contribution of this paper is the development of a Savage-Dickey Density Ratio (SDDR) for the hypothesis of homoskedasticity that extends the procedure by Chan (2018) for univariate SV models to multivariate structural models and generalising it. This is achieved by proposing a new prior distribution for the parameter that is associated with changes in the latent log volatilities. Notably, such a parameter plays a key role in our framework as it allows us to verify if a particular shock of interest can be identified through heteroskedasticity. For convenience, we refer to it as volatility of the log-volatility parameter hereafter. The prior for this parameter is centred at the hypothesis of homoskedasticity and follows a hierarchical structure determining the level of shrinkage and ensuring the verification to be based on less arbitrary choices. Given the flexibility of our setup, we provide conditions under which the analysis using the SDDR is feasible. Our verification procedure generalises that by Lütkepohl and Woźniak (2020) to SVARs with a more flexible process for conditional volatility, namely the SV model. Notably, our approach verifies the conditions assumed to hold for the identification test proposed by Lewis (2021).

A third contribution of this paper is the provision of a detailed analysis of the marginal prior distribution of the conditional variances implied by the normality of the SV process innovations, our new prior for the volatility of the log-volatility parameter, and the non-centred SV process parameterisation proposed by Kastner and Frühwirth-Schnatter (2014) that we adapt to the SVAR context. We show that the marginal prior for conditional variances is centred around the hypothesis of homoskedasticity and exhibits strong shrinkage towards it while maintaining heavy tails. These features are essential for SVAR models with identification via heteroskedasticity to be verified for two reasons. First, they standardise the SVAR model facilitating the identification and estimation of conditional variances and the structural matrix. Secondly, this setup requires the evidence in favour of heteroskedasticity to come from the data. We also point out a problem of a standard prior setup for the SV model in heteroskedastic SVARs used by Cogley and Sargent (2005) and more recently by Chan et al. (2024).

Estimation is conducted using a Gibbs sampler that implements optimal techniques such as the structural matrix sampler by Waggoner and Zha (2003a), autoregressive slope row-by-row sampling by Chan et al. (2024), auxiliary mixture by Omori et al. (2007), and the ancillarity-sufficiency interweaving strategy by Kastner and Frühwirth-Schnatter (2014) granting efficient simulation smoothing when the heteroskedasticity is uncertain. All estimation procedures are accessible via the R package bsvars by Woźniak (2024a, b) implementing our algorithms in compiled code using C++, which speeds up the computations by orders of magnitude. Additionally, the package offers a wide range of structural and predictive analyses using heteroskedastic SVARs.

We illustrate our methods by studying the sources of identification of unanticipated tax shocks using a structural model by Mertens and Ravn (2014). We find evidence for identification via heteroskedasticity in an extended sample covering the period until 2023. In a recent paper, Lewis (2021) also considers identification via time-varying volatility to estimate the effects of unanticipated tax changes for Mertens and Ravn’s data. However, he uses a frequentist approach and, hence, his methods differ fundamentally from those developed in the following.

Our paper is closely related to a number of studies that pursue identification through heteroskedasticity using different techniques. For example, Lütkepohl and Milunovich (2016) investigate identification by testing a heteroskedastic rank defined as the number of independent heteroskedastic processes following a Generalised Autoregressive Conditional Heteroskedasticity (GARCH) model. Lanne and Luoto (2021) propose a test for the validity of moment conditions based on kurtosis of the structural shocks that are in line with their non-normality or heteroskedasticity. Lewis (2021) proposes a test based on the autocorrelation of the reduced-form residuals that assumes non-proportional changes in volatilities of the structural shocks. Lütkepohl et al. (2021) propose a test for identification through heteroskedasticity for a two-regime volatility model when the timing of the change is known. Finally, Lütkepohl and Woźniak (2020) develop th SDDR to verify identification via Markov-switching heteroskedasticity in a model with an arbitrary number of regimes.

The remainder of this paper is as follows. Section 2 introduces the SVAR model and the identification results, with proofs relegated to the appendix. Section 3 parametrises the conditional heteroskedasticity using the SV model while the underlying priors for the volatility process are presented in Section 4. The SDDR for the verification of the identification via heteroskedasticity is introduced in Section 5. The priors and estimation of the remaining groups of parameters is scrutinised in Section 6 and the appendix, respectively. Finally, we illustrate our methodology by investigating identification of unanticipated tax shocks in Section 7.

Notation

We use the following notation: denotes the available data, is the identity matrix of order , and are a matrix of zeros and a vector of ones of the indicated dimensions, respectively, the operator puts the vector provided as its argument on the main diagonal of a diagonal matrix of the order corresponding to the dimension of the vector, an indicator function takes the value of 1 if the condition provided as the argument holds and 0 otherwise, denotes the Kronecker product of matrices. defines the set with all elements of the set which are not in the set . denotes the gamma function, and denotes the modified Bessel function of the second kind. The following notation is used for statistical distributions: stands for a univariate normal and for the -variate normal distribution. stands for a univariate normal product while for the univariate log normal product distribution (to be defined in Section 4). The gamma distribution is denoted by , the inverted gamma 2 by , and the uniform distribution by . Unless specified otherwise, goes from 1 to , goes from 1 to , and goes from 1 to .

2 Partial identification in heteroskedastic SVARs

In this section we establish results for partial identification of structural parameters that are applicable within a broad class of heteroskedastic SVAR models. Some theoretical results in this section can be interpreted as general matrix results and thus extendable to different modeling frameworks. Similarly general identification results can be found in Lewis (2021). These, however, are based on moments formulated in such a way so as to become testable in a frequentist setup. In contrast, we state our conditions so as to facilitate Bayesian analysis. To make notation less cumbersome, Theorem 1, Corollary 1 and Corollary 2 are presented using SVAR-consistent notation.

2.1 Model

We begin by describing two common representations for SVAR models. Consider first the following reduced-form equation:

| (1) |

where is an -dimensional vector of observable time series variables, , , are autoregressive coefficient matrices, is a vector containing deterministic terms such as the intercept, trend variables, or dummies, is the corresponding matrix of coefficients, and is an -dimensional, zero-mean, serially uncorrelated error term.

The structural equations introduce a linear relationship between the reduced-form innovations, , and the structural shocks, , via the contemporaneous effects matrix ,

| (2) |

where the structural shocks are additionally contemporaneously uncorrelated. Depending on the model used, the time-varying covariances, , or conditional covariances, , of are denoted by , where the are the unconditional or conditional variances. We also consider an alternative structural form of the model:

| (3) |

where is a nonsingular structural matrix that represents the impact effects of the structural errors on the observed variables. In other words, represents the zero-horizon impulse responses.

2.2 Identification

It is well known that the structural matrices or are not identified without additional restrictions. Below, we state the general conditions for partial identification of some of the parameters of these matrices as the following matrix result.

Theorem 1.

Let , , be a sequence of positive definite matrices and a sequence of diagonal matrices with . Suppose there exists a nonsingular matrix such that

| (4) |

Let be a possibly infinite dimensional vector. Then the column of is unique up to sign if .

Proof.

Theorem 1 has obvious implications for models set up as in (3). It implies that, if the component of has a sequence of variances which is different from the variance sequence of any other component of , the column of will be identified up to a sign. The theorem generalizes identification results for some special volatility models that have been used in the literature on identification through heteroskedasticity (see, e.g., Kilian and Lütkepohl, 2017, Chapter 14). For example, it is easy to see that identification results for volatility models based on a finite number of volatility regimes as considered by Rigobon (2003), Rigobon and Sack (2003), Lanne and Lütkepohl (2008), Lanne et al. (2010), Netšunajev (2013), Herwartz and Lütkepohl (2014), Woźniak and Droumaguet (2015), Lütkepohl and Velinov (2016), Lütkepohl and Netšunajev (2017) are special cases of Theorem 1.

As we will consider SV models in the following, it is important to mention that Theorem 1 applies for such models. In this context, SV models have also been proposed by Lewis (2021) and Bertsche and Braun (2022). In such cases, the conditional covariance matrices of the reduced form errors for model (3) are given by

where is a diagonal matrix. If the vary stochastically, as in SV dynamics, they will not be proportional with probability 1 and, hence, satisfy the conditions for identification of Theorem 1. So if any one of the structural errors has changing conditional variances, it will be identified, even if all the other components have constant conditional variance. We will use that insight in our Bayesian analysis of the SV model. It may be worth noting, however, that Theorem 1 also implies that a single shock may be homoskedastic and still be identified in case all other shocks are heteroskedastic. This discussion also shows that Theorem 1 generalises results for full identification in Sentana and Fiorentini (2001), Lewis (2021), and Bertsche and Braun (2022) to the case of partial identification.

As we will consider the structural form setup (2), it is useful to know that Theorem 1 implies that a single row of is identified if the corresponding error term has a variance vector which is different from the variance vectors of all other equations. More precisely, Theorem 1 implies the following result:

Corollary 1.

Let , , , and , , be as in Theorem 1. Suppose there exists a nonsingular matrix such that

| (5) |

Then the row of is unique up to sign if .

Proof.

– See A.2. ∎

Note that the vectors contain value one for the variance in period 0. This specific parameterisation gives the elements of vector the interpretation of variances relative to the variances for . We are using relative variances in our theorem and corollary because it makes it easier to state the result, is in line with our standardisation of the structural model, and also leads directly to the verification procedure discussed in Section 5.

The corollary generalises Theorem 1 of Lütkepohl and Woźniak (2020). It provides a general result on identification of a single equation through heteroskedasticity. It shows that a structural shock and, hence, the corresponding structural equation is identified if the sequence of variances is distinct from the variance sequences of any of the other shocks.

2.3 Impulse responses

Structural impulse responses are computed from the reduced-form impulse responses , , which are obtained by the following recursions from the -order reduced-form VAR slope coefficients:

| (6) |

where for (Lütkepohl, 2005, Section 2.1.2). The structural impulse responses are the elements of the matrices , . Thus, for computing them, the structural matrices or are needed. In particular, if just one shock is identified through heteroskedasticity, the following result formalises the implications of Corollary 1 for impulse response analysis:

Corollary 2.

If the row of is identified and, hence, unique in model (2), then the column of is unique and the structural impulse responses can be obtained by right-multiplying the matrices by the column of .

Proof.

See A.3. ∎

We present theoretical results for impulse responses based on the SVAR in (2) since this is the specification used for the empirical application in this paper. However, it is straightforward to verify that – for the SVAR setup in (3) – if just one shock is uniquely identified and the corresponding column of the matrix is given, then all the responses to the shock are uniquely obtained by right-multiplying the matrices by the column of .

3 SVAR model with stochastic volatility

Our empirical model is the SVAR model corresponding to equation (2), that is, the specification with the structural matrix . The model below supplements this specification with the assumption of conditionally normally distributed and heteroskedastic error terms with conditional variances following the SV process. Conditional heteroskedasticity has been proven an essential extension of SVARs facilitating the model identification (e.g., Bertsche and Braun (2022)).

We make an additional assumption for the structural shocks from equation (2) to be jointly conditionally normally distributed, given the past observations of vector , with zero means and conditional variances :

| (7) |

The joint normality and a diagonal covariance matrix imply conditional independence between the structural shocks.

In our setting, the conditional variances are specified by an SV process that is expressed in its non-centred parametrisation where the structural shocks are decomposed into conditional standard deviations and a standardised normal error term:

| (8) | ||||

| (9) |

The conditional variances are defined as the exponent of the volatility of the log-volatility parameter, , and the latent log-volatility term, :

| (10) |

where follows a zero-mean stationary autoregressive process of order one with autoregressive parameter and standardised normal shocks, :

| (11) | ||||

| (12) |

We further assume that implying that . This non-centred parameterisation of state-space models was introduced by Frühwirth-Schnatter and Wagner (2010) and adapted for the SV model by Kastner and Frühwirth-Schnatter (2014) and Chan (2018).

Such a model specification ensures that the specification of the conditional variances is in line with that from Theorem 1. Note that, given equations (11) and (12), the initial condition is equal to the unconditional expected value of that is equal to 0. This, however, does not fix the unconditional expected value of the conditional variances that depends on and . Therefore, we will standardise the system in a different way. Our standardisation uses a non-centred SV specification and a prior that shrinks the model towards homoskedasticity, as explained in Section 4.

The non-centred specification implies a centred specification via the one-to-one relationships , , and . Then equations (10), (11), and (12) can be rewritten respectively as:

| (13) | ||||

| (14) | ||||

| (15) |

These one-to-one relationships might suggest that these two specifications are equivalent. However, complementing them with commonly used prior distributions for the parameters and reveals essential differences. Our choice of the non-centred parameterisation of the SV process for SVARs identified via heteroskedasticity is motivated by (i) its potential to provide the standardisation of the model, (ii) the feasibility of specifying a prior distribution for the conditional variances that is centred at a point corresponding to homoskedasticity of the structural shocks, and (iii) the possibility to verify the homoskedasticity hypothesis for each of the shocks, which helps to assess partial identification of the system. The latter is essential to determine which shocks are identified through heteroskedasticity. All of these features can be understood by the analysis of the prior distribution for the parameters and the implied prior for the conditional variances that we analyse in Section 4.

4 The prior for stochastic volatility

We propose a novel prior specification for the SV process and its parameters that is suitable for the SVAR models in the context of identification through heteroskedasticity. It is based on the model equations (8)–(12). Our objectives for setting this prior are that (i) the implied prior for the conditional variances is centred around a homoskedastic process, (ii) it provides a controlled level of shrinkage towards the hypothesis of homoskedasticity of the structural shocks, (iii) it supports the standardisation of the system at a point where for all and (and, hence, the shock is homoskedastic), (iv) it leads to an efficient Gibbs sampler for the estimation of the model, and (v) it facilitates a reliable verification of the partial identification through heteroskedasticity using the SDDR.

By centring at and shrinking the prior for the conditional variances towards the hypothesis of homoskedasticity we address the critique of Bayesian SVARs identified through heteroskedasticity by Lewis (2021) and Bertsche and Braun (2022). They argue that the conventional priors enable the identification via the implied non-normality of residuals irrespectively of whether the structural shocks are heteroskedastic or not. Note that this feature is shared by the corresponding frequentist models that assume the normality of the SV equation innovations. Our priors proposed in the following let the data decide on whether particular shocks are homo- or heteroskedastic. As a consequence, in our setup, it is the data that decides on the partial or full identification of the SVAR system via heteroskedasticity. At the same time, our priors facilitate the estimation of a parametric model when it is partially identified and perform a valid verification of the identification using SDDRs.

This section first states the prior for the latent process and the parameters of the SV process. Then, it analyses the properties of the implied priors for the conditional variances and their logarithms. Finally, it discusses how partial identification of the SVAR model can be verified in our setup.

4.1 Priors for the SV process parameters

In order to state the prior distribution for we define a vector , and a matrix with ones on the main diagonal, with on the first subdiagonal, and with zeros elsewhere.

The prior for the latent process is determined by equations (11) and (12) which imply the following conditionally multivariate normal distribution, given parameter :

| (16) |

The remaining parameters of the SV process include – the essential parameter of the non-centred parameterisation responsible for the variance of the log-conditional variances, – the latent process’ autoregressive parameter, and – the prior variance of . These parameters follow a hierarchical prior structure, including normal, uniform, and truncated gamma distributions, respectively:

| (17) | ||||

| (18) | ||||

| (19) |

This original specification is our proposal for the prior distributions of the SV process for structural shocks of the SVAR models in the context of identification through heteroskedasticity. It is complemented by three restrictions:

| (20) | ||||

| (21) | ||||

| (22) |

Under the first restriction, the latent SV process has no unit roots and is stationary. Note that restrictions (20) and (21) result in the bounds for as presented in the uniform prior for from expression (18). Similarly, the truncation of the gamma prior for results from the restriction (21). The last restriction from inequality (22) determines the marginal prior for and makes it particularly suitable for our setup, as explained below. We show that under restrictions (20) and (21), all our objectives regarding centring and shrinking of the prior for the conditional variances are met, whereas, under the last one, the SDDR for the verification of the partial identification provides reliable results and is free of arbitrary choices.

4.2 Implied priors for conditional variances and their logarithms

The SV process equations (8)–(12), the prior distributions for their parameters (16)–(19), and the restrictions (20)–(22) imply prior distributions for the interpretable sequences of random variables like conditional variances and their logarithms. The following definitions will simplify the subsequent discussion of these priors.

Definition 1.

(Normal product distribution)

Let and denote two independent zero-mean normally distributed random variables with variances and respectively. Then, a random variable follows the normal product distribution with zero mean and variance , denoted by , with density function given by: .

The normal product distribution is known in the statistical literature. We state it here to clarify our notation. However, the following distribution is new and its density function is obtained by change of variables.

Definition 2.

(Log normal product distribution)

Let a random variable follow the normal product distribution with variance . Then, a random variable follows the log normal product distribution, denoted by , with density given by: .

We are now ready to state the implied marginal priors for the volatilities in Proposition 1:

Proposition 1.

(Marginal distributions of conditional volatilities)

Given the prior specification from equations (8)–(12) and (16)–(22), the marginal priors for the latent process , log-conditional variances , and conditional variances are given by the following normal, normal product, and log normal product distributions:

- (a)

-

,

- (b)

-

,

- (c)

-

,

with the corresponding limiting distributions:

- (d)

-

,

- (e)

-

,

- (f)

-

.

Proof.

(a) The result is based on the properties of a normal compound distribution that facilitates the integration of , where the joint distribution under the integral is constructed from the conditional distributions , and using . (b) The result is obtained directly by applying Definition 1, the result (a) and the prior in expression (17). Points (c)–(f) are obtained as a straightforward consequence of the first two results. ∎

4.3 Non-centred and centred SV representations

In order to understand our prior setup it is essential to understand the properties of the implied prior distributions and compare them to a conventional prior for SV processes. Our proposed normal prior for the parameter from equation (17) implies the following gamma prior for the conditional variance of the SV process in its centred parameterisation with expected value :

| (23) |

However, the conventional conjugate prior for a variance parameter belongs to the family of inverted-gamma distributions. We state this conventional prior for the sake of comparison to our proposal. Let the conventional prior for in the centred parameterisation have the expected value equal to and be specified as:

| (24) |

where denotes the inverted-gamma 2 distribution (see Bauwens et al., 1999, Appendix A). The alternative prior specifications from equations (23) and (24) illustrate how our approach is different from the conventional take on SV models. Our gamma prior for the volatility of the log-volatility parameter in equation (23) implies strong shrinkage towards the homoskedasticity (see Chan, 2018). Furthermore, the prior from equation (23) shows that our specification can be equivalently presented as the SV process in its centred parameterisation and with a gamma prior for the variance of the latent process.

4.4 Properties of the prior for conditional variances

At the beginning of the current section, we stated the objectives for our prior setup. Below we provide more insights into how these objectives are embedded in our priors and why that matters.

The first objective was to centre the prior for conditional variances around the hypothesis of homoskedasticity. As long as the prior expected values of the log-conditional variances following the normal product distribution are 0 for all , that is, centred at the homoskedastic process, the expected values of the conditional variances following the log normal product distribution are not simply equal to 1, of course. However, the log normal product distribution has a pole at value 1. Property 1 establishes when this distribution has a single mode at this point.

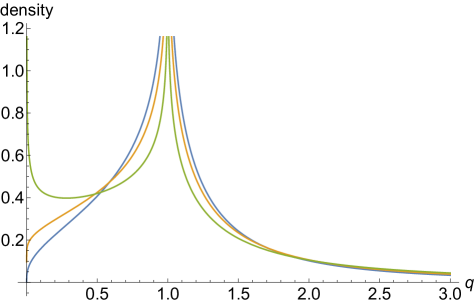

Property 1.

(Single pole of log normal product distribution at point 1)

The log normal product distribution from Definition 2 has a single pole at point 1 iff . In this case, the value of the density function approaches 0 when the argument goes to 0. When , this density function differs from 0 and goes to infinity when goes to 0.

Note: the blue, orange, and green lines correspond to the densities for the values of the scale parameter, , equal to 0.8, 1, and 1.5 respectively.

We illustrate Property 1 in Figure 1. First, note that the condition for a single pole for the distribution of conditional variances for all was stated in expression (21) and, consequently, defined our prior. Secondly, the single pole of the log normal product distribution implies a strong concentration of the prior probability mass at the point corresponding to the pole. This point is implying homoskedasticity of the structural shocks. This extreme concentration of probability mass to the point of unbounded probability density function supports our claim that at the prior mode, the SVAR model is not identified through heteroskedasticity. Still, the distribution is proper and allows a strong signal from the data to push the posterior probability mass towards heteroskedasticity. Finally, note that the inequality restriction is imposed on the parameter of the limiting log normal product distribution, , to ensure it holds for all .

The second objective was to shrink the prior for conditional variances towards homoskedasticity. It is also obtained by imposing the restriction from Property 1 in inequality (21). This objective cannot be obtained without this restriction. The second pole at point 0 distributes probability mass over the interval from zero to 1 more evenly. In effect, the posterior estimates are either pushed towards very small values when they are shrunk towards 0 or take practically any value on the real scale. Additionally, our hierarchical prior exhibits the same shrinkage properties for the log-conditional volatilities as analysed in other contexts by Bitto and Frühwirth-Schnatter (2019) and Cadonna et al. (2020). These properties include the extreme concentration of the prior mass at the point of homoskedasticity and heavy tails, allowing to accommodate the signals of heteroskedasticity from the data.

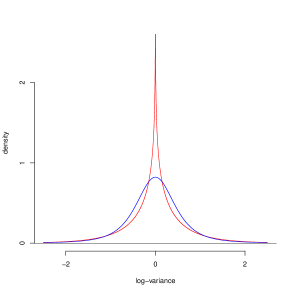

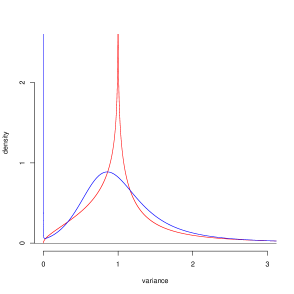

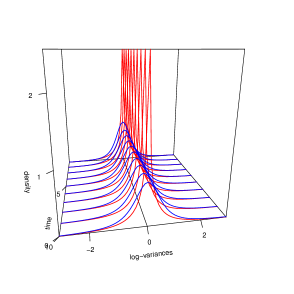

| (a) marginal prior for a log-variance | (b) marginal prior for a variance |

|

|

| (c) prior for log-variances over time | (d) prior for variances over time |

|

|

Note: red corresponds to our non-centred and blue to the centred parameterisation of the Stochastic Volatility process.

The latter remark leads to the third objective of specifying the prior so that the SVAR model is standardised. The conventional standardisations of the model in the frequentist approach rely either on setting the diagonal elements of the matrix to 1 or the unconditional expected value of the conditional variances, , to value 1. Both of these solutions complicate the derivation of an efficient Bayesian estimation algorithm and might require cumbersome treatment of the local identification of the model. Our property relies on the appropriate centring and shrinking of the prior that results in standardised posterior output.

All of these features are clearly visible in Figure 2 that juxtaposes our prior distribution with a conventional setup. These figures present in red our prior distribution for the non-centred parameterisation with the restrictions (20)–(22), and in blue a conventional prior for the SV process in its centred parameterisation. In both setups here we apply a uniform prior for on the interval , and the unrestricted inverse gamma prior for as in expression (24).

Figure 2 (a) presents the marginal limiting prior for log-conditional variances for two cases: (i) our proposed prior is plotted in red where the hyper-parameters were integrated out according to with respect to the priors for and as in equations (18)–(21); (ii) a conventional prior is plotted in blue where the marginalisation is performed with respect to parameters and following the unrestricted prior described in the paragraph above. Our proposal is based on the normal product distribution, and the marginal prior inherits its properties, including the pole at zero, strong shrinkage towards the prior mean, and heavy tails. The conventional prior is Student-t distributed, not exhibiting that strong concentration of the prior probability mass around homoskedasticity.

Figure 2 (b) presents a similarly obtained marginal limiting prior distribution of the conditional variances and reveals major differences in the prior specifications. Firstly, note that our prior plotted in red has a single pole at value 1, and exhibits strong shrinkage towards this point. The conventional prior that is log distributed has a mode at point 1 and a pole at point 0. The pole arises from the marginalisation of the log distribution with respect to parameters and and is described in Property 2.

Property 2.

(Prior for conditional variances in a centred SV model)

Consider a centred SV model from equations (13)–(15) with the inverted-gamma 2 prior for the volatility of the log-volatility parameter as in equation (24) that, for the sake of generality, is stated as:

| (25) |

Then,

- (a)

-

the log-volatilities, , follow a Student-t marginal prior distribution (see Bauwens et al., 1999),

- (b)

-

the conditional variances, , follow a marginal prior distribution (see Hogg and Klugman, 1983),

- (c)

-

the prior distribution stated in (b) has a pole at point 0, unless goes to infinity (see Callealta Barroso et al., 2020, for points (c)–(e)),

- (d)

-

the prior distribution stated in (b) has a second mode – a local maximum – at point iff ,

- (e)

-

the prior distribution stated in (b) has a median at point 1 only if goes to infinity.

Property 2 shows that the unrestricted centred SV parameterisation is highly problematic in SVAR applications. With unconstrained volatility of the log-volatility parameter, it does not ensure even the standardisation of the system about value . Moreover, with any finite values of the shape hyper-parameter, , the pole at point 0 provides heavy local shrinkage towards a point in which the model is singular as it exhibits zero conditional variances of the structural shocks. In this context, our proposal satisfying all the stated objectives robustly leads to reliable posterior estimates and inferences.

Finally, Figures 2 (c) and 2 (d) present the shape of the priors for conditional variances and their logarithms in a dynamic setting for the first ten sample periods. These distributions inherit the properties from the marginal limiting distributions. All these arguments indicate the adequacy of our prior setup that includes an appropriate hierarchy and the restrictions that provide necessary features and interpretations in the context of priors for the volatility process of structural shocks for the SVAR model partially identified through heteroskedasticity.

5 Bayesian assessment of identification conditions

The assessment of the identification conditions is a challenging task for heteroskedastic SVARs because it often relies on the estimated parameters of a model that is potentially not identified (see the points made by Lewis (2021) and by Lütkepohl et al. (2021)). We follow Lütkepohl and Woźniak (2020) and complement the setup of our model with a Savage-Dickey Density Ratio by Verdinelli and Wasserman (1995) for the verification of the identification conditions from Theorem 1. More precisely, we verify the heteroskedasticity of each structural shock by seeking evidence against the homoskedasticity restriction

| (26) |

If this condition holds, the latent volatility equation becomes deterministic with and for all , that is, the latent process is homoskedastic for a given . This restriction is verified for each , that is, for each structural shock. The results allow us to make statements regarding the identification of the SVAR model through heteroskedasticity and answer whether the system is fully or partially identified. Recall that, by Theorem 1, each shock with nonzero is identified through heteroskedasticity. The SDDR is particularly suitable for the verification of the identification conditions because it relies on the estimation outcome of one general model and does not require the estimation of restricted models.

In order to verify the restriction from equation (26) using the SDDR, we adapt the ideas presented by Frühwirth-Schnatter and Wagner (2010) for state space models and applied to SV models by Chan (2018). More specifically, we extend the heteroskedasticity verification procedure using SDDR by Chan (2018) for investigating the hypothesis (26) for the structural shocks of SVAR models. Several features make our procedure reliable. Firstly, it is embedded in the SV hierarchical prior structure that is suitable for the volatility process in the context of identification through heteroskedasticity. Secondly, we extend the normal prior distribution for , as in equation (17), proposed by Chan (2018) by a hierarchical prior for its variance as in equation (19). In contrast, Chan (2018) simply fixes this prior variance. Our specification allows the subsequent estimation of making the prior and the inference using the SDDR less dependent on arbitrary choices. Moreover, based on the results provided by Bitto and Frühwirth-Schnatter (2019) and Cadonna et al. (2020), the marginal prior for , based on a gamma scale mixture of normal distributions, combines the extreme shrinkage towards the hypothesis of homoskedasticity and heavy tails allowing the data to provide the signal of heteroskedasticity that informs posterior inference. An additional property that is necessary for the SDDR to provide reliable outcomes is the bounded density function for the marginal prior for that we discuss below. Finally, our estimation algorithm for the SV parameters uses the ancillarity-sufficiency interweaving strategy by Kastner and Frühwirth-Schnatter (2014) that is the optimal solution making the MCMC algorithm efficient when it is unknown whether the process is homo- or heteroskedastic. Therefore, we provide the setup that is numerically efficient, sufficiently flexible to exploit the information from data, and suitable for partial identification verification of the SVARs identified through heteroskedasticity.

Our SDDR is defined by the ratio of the marginal posterior of ordinate to the marginal prior ordinate for this parameter both evaluated at point 0:

| (27) |

Small values of the SDDR provide evidence against the restriction . In turn, the posterior probability mass being more concentrated around the restriction than the prior probability mass is evidence in favor of the restriction. The analysis of the SDDR in equation (27) reveals that Property 3 establishing the bounded marginal prior for is essential. If this density is unbounded at point , then it is impossible for the data to provide evidence for heteroskedasticity, as the denominator of the SDDRs is equal to infinity and the SDDR itself goes to zero. Additionally, extending the prior by Chan (2018) allows our verification procedure to let the data speak about the heteroskedasticity of structural shocks.

In order to present the result of bounded marginal prior for , we first redefine the prior from equation (19) as:

| (28) |

and provide the density of the marginal prior for .

Proposition 2.

(Density of marginal prior for )

Proof.

The integration proceeds by recognising the constant and kernel and applies to the latter which is facilitated using the normalising constant of the generalised inverse Gaussian distribution provided by Barndorff-Nielsen (1997). ∎

Below, we state that the existence of the upper bound for the density from equation (29) at point 0 depends on the value of hyper-parameter by providing results on the following limit:

Property 3.

(Upper bound of the marginal prior density for ) (See Cadonna et al., 2020, Theorem 2).

| (32) |

Therefore, the marginal prior density function for parameter is bounded from above iff the restriction, , from equation (22) holds. Consequently, we set the hyper-parameter which reduces the gamma prior to an exponential distribution and the Bayesian Lasso prior considered by Belmonte et al. (2014) for state-space models. However, other choices are possible and are best reviewed by Cadonna et al. (2020).

We further set the hyper-parameter . This choice implies that practically the whole prior probability mass of lays within the interval . Therefore, instead of imposing a strict restriction leading to a hard-to-sample-from truncated full conditional posterior distribution for , we impose the restriction via an appropriate prior specification. As we explain in C, we first sample from the generalised inverse Gaussian distribution whose value will be within the interval with a probability close to one thanks to our prior setup. Subsequently, is sampled from the truncated normal distribution given the most recent draw of to fix the truncation set.

The SDDR can be easily computed as long as the densities of the full conditional posterior and the prior distributions are of a known analytical form. In C, we show that, given the data, the latent volatilities processes involved in our model and the parameters of the SVAR equation, the parameters can be independently sampled from the univariate normal full conditional posterior distributions with the mean and variance specified in equations (56)–(58). Then, the numerator of the SDDR can be computed using a sample of draws from the posterior distribution by applying the marginal density ordinate estimator proposed by Gelfand and Smith (1990):

| (33) |

where denotes the density function of a normal distribution, whereas and denote the values of the mean and variance in which the place of the parameters of the model are replaced by their draws from the posterior.

6 Prior distribution for the SVAR parameters

Our objectives for setting the joint prior distribution for the structural matrix and the autoregressive slope parameters collected in the matrix are that (i) it is conditionally conjugate, and thus, facilitates the derivation of an efficient Gibbs sampler for the estimation of the parameters, (ii) it is a reference prior that does not distort the shape of the likelihood function due to the local identification of the model as defined by Rubio-Ramírez et al. (2010), (iii) it can be interpreted as a Minnesota prior proposed by Doan et al. (1984), and (iv) it enjoys the flexibility of the hierarchical prior specification thanks to which the essential hyper-parameters responsible for the level of shrinkage are estimated as argued by Giannone et al. (2015).

All these objectives are met when the prior for the structural matrix is set to the generalised-normal distribution proposed by Waggoner and Zha (2003a) and multivariate normal for the autoregressive parameters. Let and denote the th row of the matrices and , respectively. Then the prior distribution for matrix is proportional to

| (34) |

The parameters of this distribution are further assumed to be equation invariant. That feature makes this distribution the reference prior, which means that it is invariant to the rotations of the structural system up to permutation and sign change of its rows (see Woźniak and Droumaguet, 2015). The scale matrix of the distribution in (34) is set to , where is a hyper-parameter, and the shape parameter is set to , which makes the marginal prior distribution for the rows of the -variate normal distribution with the zero mean and covariance .

The prior distribution for each row of matrix is multivariate normal, sharing features of the Minnesota prior. Therefore, the prior mean of is equal to , where is a diagonal matrix with zeros and ones on the diagonal depending on whether the corresponding variables in are stationary or unit-root nonstationary. The matrix is fixed at if all variables in are unit-root non-stationary or at if they are stationary. The covariances of the rows of are given by diagonal matrices with scalar hyper-parameters and, where , and denotes a vector containing the reciprocal of integer values from 1 to . This matrix provides the increasing level of shrinkage with increasing lag order of the autoregressive slope parameters, incorporating the ideas of the Minnesota prior of Doan et al. (1984). Furthermore, the prior variances of the parameters corresponding to the deterministic terms are equal to , reflecting a popular view that the shrinkage should be relatively weaker for these parameters.

Extending the prior by Giannone et al. (2015), the levels of shrinkage of the autoregressive and structural matrices follow a 3-level global-local hierarchical prior on the equation-specific shrinkage parameters and :

| (35) | ||||

| (36) |

We set and to values 10, 10, 100, and 1 respectively to make the marginal prior for the elements of quite dispersed, and and all equal to 10, which facilitates relatively strong shrinkage for the autoregressive parameters in matrix that gets updated, nevertheless. Providing sufficient flexibility on this 3-level hierarchical prior distribution was essential for a robust shape of the estimated impulse responses.

7 An empirical illustration: Verifying identification of tax shocks

When heteroskedasticity is used for identification in SVAR analysis, the shocks are distinguished by their variances or conditional variances. This approach provides distinct shocks without economic labels and requires some additional information to label the shocks. Such information is sometimes available in the form of specific shapes of the impulse responses associated with a shock or a specific sign pattern of the impact effects of the shocks.

To illustrate the methods developed in the previous sections, we will consider a fiscal SVAR model in which the unanticipated tax shock has been identified in different conventional ways. These alternative identification strategies include, for example, Blanchard and Perotti (2002) (henceforth BP) who use restrictions on the short-run effects of the shocks and the instantaneous interactions of the variables to identify their shocks, and by Mountford and Uhlig (2009) using sign restrictions. Moreover, Mertens and Ravn (2014) (henceforth MR), as revised by Ramey (2016), use an external instrument, a narrative measure of the tax shock proposed by Romer and Romer (2010). Finally, Lewis (2021) (henceforth LE) uses heteroskedasticity and, hence, an approach in that respect similar to ours. He uses quite different frequentist estimation and inference methods, however, and he also needs more restrictive assumptions regarding the heteroskedasticity of the shocks. Specifically, he assumes non-proportional changes in the conditional variances of the structural shocks. We use the MR model as our benchmark to illustrate the use of our methodology for identifying the tax shock via heteroskedasticity, and the narrative measure by Romer and Romer (2010) to ensure a correct labelling of the shocks.

7.1 A simple fiscal SVAR

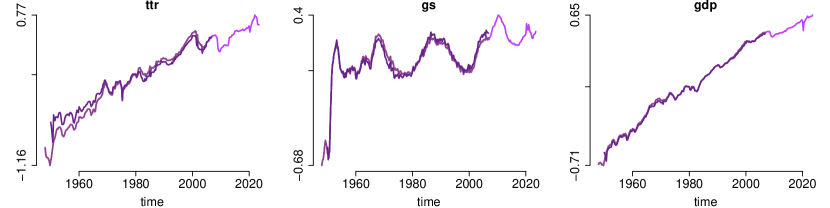

MR specify a three variable fiscal system including total tax revenue, denoted by , government spendings, , and gross domestic product, , and they express all the quarterly variables in real, log, per person terms. We will also consider these three variables and investigate whether the tax shock can be identified by our methodology.

In order to investigate identification through heteroskedasticity in this fiscal system, we use three alternative samples of different length and partly different values even for overlapping periods. They are plotted in Figure 3, where it can be seen that the series are different but similar in overlapping periods. The shortest sample, hereafter MR-sample, uses the data from MR and LE that is downloaded directly from Karl Merten’s website111The spreadsheet is available at: https://karelmertenscom.files.wordpress.com/2017/09/jme2014_data.xls. Following the data construction described by MR, total tax revenue, government spendings, and gross domestic product, as well as the GDP deflator are taken from NIPA Tables number 3.2, 3.9.5, 1.1.5, and 1.1.9, respectively, provided by the U.S. Bureau of Economic Analysis (2024c, d, a, b), and the population variable is provided by Francis and Ramey (2009). This data spans the period 1950Q1 to 2006Q4.

Note: The figure plots three series for three samples: the 2023-sample plotted in light pink includes observations from 1948Q1 to 2023Q3 (), the 2006-sample plotted in darker pink is as the 2023-sample but finishes in 2006Q4 (), the MR-sample, plotted in purple, spans the period from 1950Q1 to 2006Q4 (). The plotted series are standardised by subtracting from each series its first observation in 1980.

We extend the sample to the latest available observations in 2023Q3 with modifications in the population variable that is replaced by one matching Francis and Ramey’s definition and provided by the U.S. Bureau of Labor Statistics (2024). Based on these variables we form two samples, both of which contain longer time series than MR and start in 1948Q1. One of these samples, hereafter the 2023-sample, finishes in 2023Q3, and the other one, hereafter the 2006-sample, terminates in 2006Q4. Following MR, we use a VAR(4) model with a constant term, a linear and a quadratic trend, and a dummy for 1975Q2 as deterministic terms.

7.2 Verifying identification via heteroskedasticity

We base our structural analysis on the model (2). Hence, we have to sample from the posterior of the structural matrix which is not identified without further restrictions if the shocks are not heteroskedastic. Even if the shocks are identified, the row ordering and row signs may change in different drawings from the posterior without taking special precautions to prevent that from happening. We therefore follow LE and reorder the rows and adjust their signs such that each draw has the minimum distance to the benchmark matrix computed from the estimates of the structural parameters from BP to begin with and call this the BP–ordering. More detail on this procedure is provided in D. Hence, the shocks can be labelled along the lines of BP as an unanticipated tax shock (), a government spending shock (), and an additional shock () capturing unexpected changes in not caused by tax or spending shocks. We will label our shocks accordingly although it is, of course, not clear from the outset that the shocks can actually be identified by heteroskedasticity and, thus, we may not get identified shocks with our methodology. If we get identified shocks, they may differ from those in BP or MR in which case our labels may not be meaningful. We will later return to this issue.

| 2023-sample | 2006-sample | MR-sample | ||||

|---|---|---|---|---|---|---|

| -21.38 | [4.69] | -1.51 | [0.18] | 0.32 | [0.05] | |

| -4.62 | [0.79] | -1.32 | [0.15] | 0.23 | [0.05] | |

| -63.39 | [6.43] | 0.50 | [0.03] | 0.39 | [0.03] | |

Note: The table reports the log of the Bayes Factors estimated via the log of SDDRs from equation (27) together with numerical standard errors (NSEs) provided in parentheses. Negative values provide evidence against homoskedasticity. Bold font numbers represent cases in which the evidence for heteroskedasticity is positive (values greater than 3 in absolute terms) or strong (greater than 20) on the scale of Kass and Raftery (1995). The NSEs are computed based on 30 subsamples of the original MCMC draws.

The next step in our analysis is to assess whether there are shocks that are identified through heteroskedasticity. Our main tool for that purpose is the SDDR from equation (27). The SDDR values computed for each of the three shocks individually using our three data samples are reported in Table 1. For the 2023-sample, the evidence for heteroskedasticity of all three structural shocks is strong according to the scale proposed by Kass and Raftery (1995). The values of the log Bayes factors shown in the table mean that the posterior mass in favour of heteroskedasticity exceeds 99% for all the shocks. This result provides overwhelming evidence for the identification of all three shocks via heteroskedasticity in the 2023-sample and is robust to many variations in the model prior specification. These variations include perturbations of the hyper-parameters that need to be fixed in our setup. We checked the conclusions for three values of each scale and shape of the prior distribution for , as well as for three alternative setups for the hyper-parameters for each of the matrices and . Each of these alternative setups included cases of stronger and weaker shrinkage than in our benchmark prior specification.

The evidence for the structural shocks to be identified through heteroskedasticity is much weaker in the 2006-sample. Moreover, the log Bayes factors estimated by the log-SDDRs for the MR-sample are even positive, implying that the posterior mass for homoskedasticity is greater than that for heteroskedasticity. The log-SDDRs are negative for the last two shocks in the 2006-sample that includes eight more observations than the MR-sample from the volatile late 1940s. More specifically, in the 2006-sample, the posterior probability of a heteroskedastic shock is 82%. Obviously, in this case the evidence for identification through heteroskedasticity of the first shock is limited and it is even more limited for the other shocks. These findings are also robust to the perturbations in the values of the prior hyper-parameters.

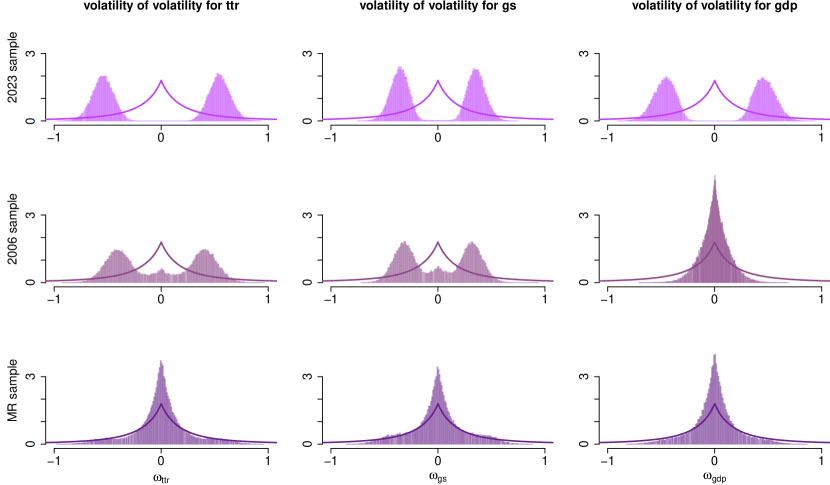

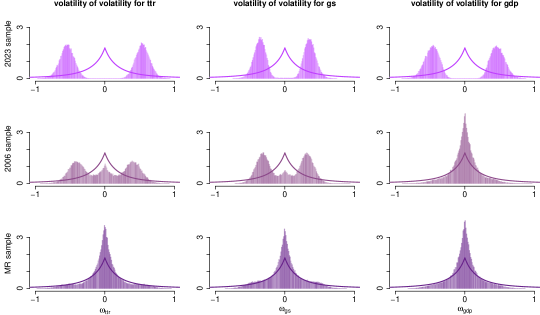

In Figure 4 we further illustrate how the SDDRs work by plotting the marginal prior versus the marginal posterior densities of the volatility of the log-volatility parameter associated with our three samples. Based on the information from these plots, the SDDRs from equation (27) can be approximated by the ratio of the marginal posterior ordinate at zero to that of the marginal prior density. The figures for the 2023-sample exhibit posterior mass concentrated away from the origin, providing evidence against homoskedasticity. Instead, the posterior mass for the 2006- and MR-samples is concentrated about the hypothesis of homoskedasticity, often more than the prior, thus favouring homoskedasticity. Figure 4 features the marginal prior densities of the volatility of the parameters and highlights their essential characteristics discussed in Section 5, such as their high concentration about the origin, fat tails, boundedness from above, and flexibility provided by a hierarchical specification, extending the normal prior with fixed variance used by Chan (2018).

Note: The marginal prior density is estimated by numerical integration as in Gelfand and Smith (1990) using a grid of points from -1.1 to 1.1. They are the same for all samples and shocks. The marginal posterior densities are approximated using histograms. The ratio of these densities at point zero approximates the SDDR in equation (27). Posterior mass less concentrated than the prior mass about zero provides evidence against homoskedasticity.

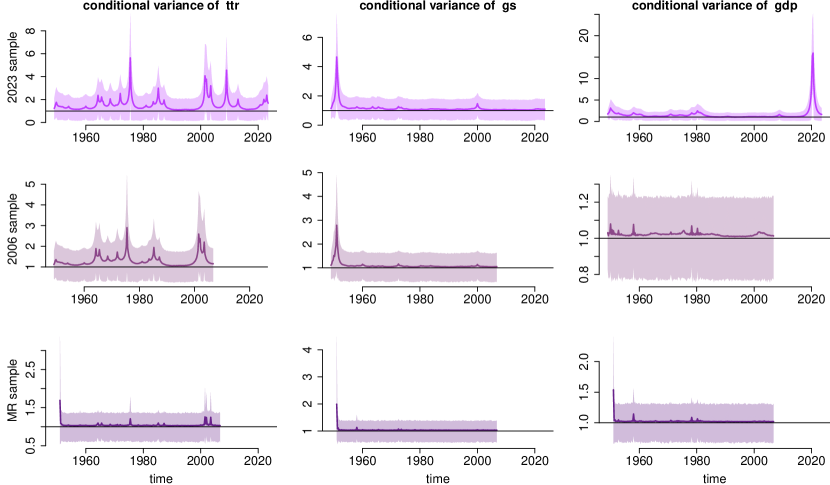

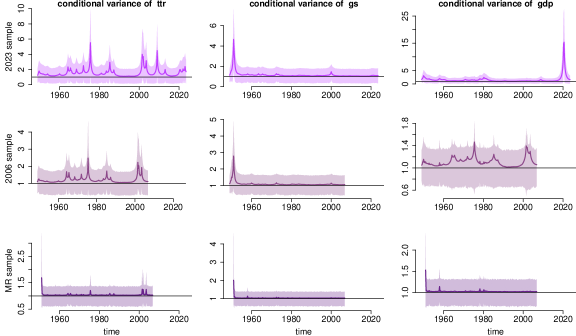

Finally, we analyse the sequences of conditional variances of the structural shocks that are required to be clearly distinct for partial identification of the shocks to hold according to Theorem 1. We plot their posterior means together with 90% highest posterior density (HPD) intervals in Figure 5. The conditional variances are visibly time varying for the 2023-sample. The conditional variances of the first shock are significantly different from 1 in six periods in that sample including the mid 70s and mid 80s, individual quarters in 2001, 2002, and 2003, as well as in the first quarter of 2009. The variances of the second shock are different from 1 in the first quarter of 1951 only, while those of the third shock have HPD intervals not including 1 in 1950, and in quarters 2 and 3 of 2020. The distinctive occurrence times of high volatility periods for the three shocks provide strong evidence for them to be different in these sequences, further supporting the identification via heteroskedasticity in this sample.

Note: The figures plot time-varying conditional variances of the structural shocks. The lines report the posterior mean and the shaded areas 90% HPD intervals. The variances in the first row clearly exhibit non-proportional changes across time. The horizontal black line is set at the value of 1 around which the prior is centred.

The conditional variances in the 2006-sample are to some extent similar to those from the 2023-sample until 2006. However, at all times the 90% HPD intervals include the value of 1. This is caused by a weaker signal provided from the data in the shorter sample regarding time-varying volatility, which undermines the evidence for identification in the framework of our model. In the MR-sample, the evidence for conditional variances that support identification is even weaker. Thus, the bottom line is that, in the 2023-sample, the shocks are clearly identified through heteroskedasticity, while the evidence for identification through heteroskedasticity is weaker in the 2006-sample and no such evidence is found in the MR-sample.

7.3 Checking alternative ordering rules

One may wonder how much our results depend on the BP–ordering of our draws from the posterior of . Therefore, we have repeated our sampling using the estimates obtained by MR to order the rows of the drawings (see D). The results of the SDDRs based on the MR–ordering are presented in Table 2(a). They paint a similar picture as the results in Table 1. The evidence for shocks identified through heteroskedasticity is overwhelming in the 2023-sample. It is weaker for the 2006-sample and hardly existent in the MR-sample.

| 2023-sample | 2006-sample | MR-sample | ||||

|---|---|---|---|---|---|---|

| (a) MR–ordering | ||||||

| -21.38 | [4.97] | -0.92 | [0.14] | 0.32 | [0.05] | |

| -4.62 | [0.79] | -1.27 | [0.13] | 0.24 | [0.04] | |

| -32.46 | [8.16] | 0.38 | [0.04] | 0.38 | [0.03] | |

| (a) PM–ordering | ||||||

| -21.38 | [4.7] | -1.47 | [0.2] | 0.27 | [0.05] | |

| -4.62 | [0.79] | -1.31 | [0.14] | 0.52 | [0.03] | |

| -63.39 | [6.43] | 0.35 | [0.03] | -0.04 | [0.07] | |

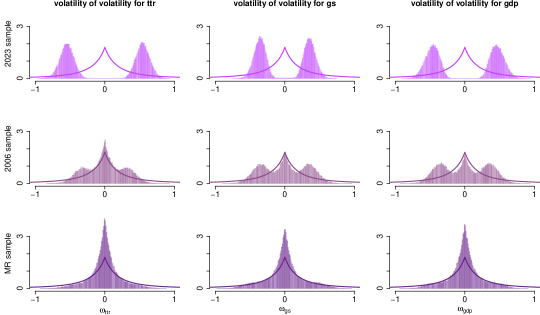

In Figure 6(a) we show the marginal prior and posterior densities of the parameter. The picture is very similar to that in Figure 4. In other words, the posterior in the 2023-sample has considerable mass away from the origin and, hence, strongly supports identified shocks, while the situation is much less clear for the 2006-sample and, for the MR-sample, where identification is clearly not supported because the prior and posterior densities are both centred at zero and have considerable density mass in the neighbourhood of zero.

| (a) MR–ordering |

|

| (b) PM–ordering |

|

Note: The note to Figure 4 applies.

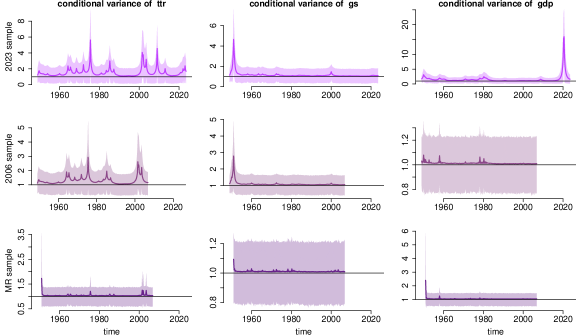

Finally, we show the conditional variances based on the MR–ordering in Figure 7(a). Comparing that figure to Figure 5, it can be seen that the conditional variances are again very similar to those in the latter figure. Thus, the choice of for standardizing the posterior draws is of limited importance. At least, if there is sufficient conditional heteroskedasticity to ensure identification of the shocks, whether we use the BP– or the MR–ordering for the drawings is not important.

| (a) MR–ordering |

|

| (b) PM–ordering |

|

Note: The note to Figure 5 applies.

We emphasize, however, that some kind of standardisation of the drawings is necessary even if the shocks are all well identified because the structure of the model is invariant to changing the order and sign of the shocks. As long as the standardisation ensures a unique ordering and sign of the shocks, it should have little impact on the samples from the posterior distributions if the shocks are well identified. Therefore, given that for the 2023-sample we can expect to identify all three shocks through heteroskedasticity, we have also used a target matrix for this sample which is not based on a set of estimates from some alternative identification scheme. Instead, we have used a selected posterior mode as the benchmark matrix and call it the PM–ordering (see D for details).

In this case, it is not clear a priori that the ordering of the shocks will be the same as for the BP– and MR–orderings. As the shocks are distinguished by their conditional variances, we consider the conditional variances and order them such that they look similar to those based on the BP– and MR–orderings. In this case, the three distinct variance patterns allow for easily matching them with the shocks from the BP– and MR–orderings such that we can easily label the shocks correspondingly. We present the resulting conditional variances in Figure 7(b).

We have also computed SDDRs and the conditional variances of the three shocks, using the PM–ordering of the drawings from the posterior. The results are shown in Table 2(b). They strongly support that all three shocks are identified through heteroskedasticity in the 2023-sample. In fact, the SDDR values in Table 2(b) are identical to the corresponding values for the 2023-sample in Table 1. Additionally, the robustness of heteroskedasticity and identification verification to various ordering rules is confirmed by the plots of marginal posterior and prior distributions of the volatility of the log-volatility parameter for the PM–ordering in Figure 6 (b) closely resembling other reported figures of this parameter. Thus, as long as some fixed ordering is used to standardise the drawings from the posterior of , it does not affect the posterior of the conditional variances and, hence, the identification of the shocks.

7.4 The effects of tax shocks

Thus far, we have documented partial identification via heteroskedasticity of the tax shock in two of our samples. As the MR-sample does not support identification through heteroskedasticity of any of the shocks, we do not consider the MR-sample in the following. There is strong evidence for identification in the 2023-sample and much weaker in the 2006-sample. Subsequently we investigate how this reduced level of empirical support for identification affects the impulse responses of the tax shocks on . Given that our identification results are robust with respect to different orderings of the posterior drawings, we now focus on the PM-ordering.

Given that heteroskedasticity provides three identified shocks, we begin by investigating which one of them is the tax shock. The properties of the conditional variances of the first shock in the PM–ordering closely resemble those of the tax shock in the BP– and MR–orderings. This fact makes it more likely that the first shock in the PM–ordering is the tax shock as well. We investigate this further and report the correlations between the structural shocks from our estimated models and PM–orderings and the narrative measure of the unanticipated tax shock by Romer and Romer (2010) in Table 3. The results show that the first shock in our models is the most correlated with the narrative measure. This correlation exceeds 0.22 for all the models reported in the table. It is much higher than for the second shock for which the values are -0.022 for the 2023-sample and 0.117 for the 2006-sample. They are still higher than for the third shock for which they are less than -0.15 for both samples. Therefore, irrespectively of the empirical support for identification across both samples, the first shock can be labeled the tax shock. The correlations for this shock have similar values as the tax shocks estimated by BP, MR, and LE, according to our reproductions of findings from other papers reported in the last three columns of Table 3.

| 2023-sample | 2006-sample | BP results | MR results | LE results | |

|---|---|---|---|---|---|

| 0.224 | 0.264 | 0.277 | 0.298 | 0.233 | |

| -0.022 | 0.030 | ||||

| -0.154 | -0.170 |

Note: The table reports sample correlations between the narrative measure of tax shocks proposed by Romer and Romer (2010) and used by MR. It indicates that our first shock is the most correlated with the instrument, which validates its labeling as the tax shock. The results in columns 2023-sample and 2006-sample are based on our posterior estimations where we used the posterior mean of the shocks as their estimator. The results in columns BP results, MR results, and LE results are based on our reproduction of the results from MR and LE using the authors’ computer code and data.

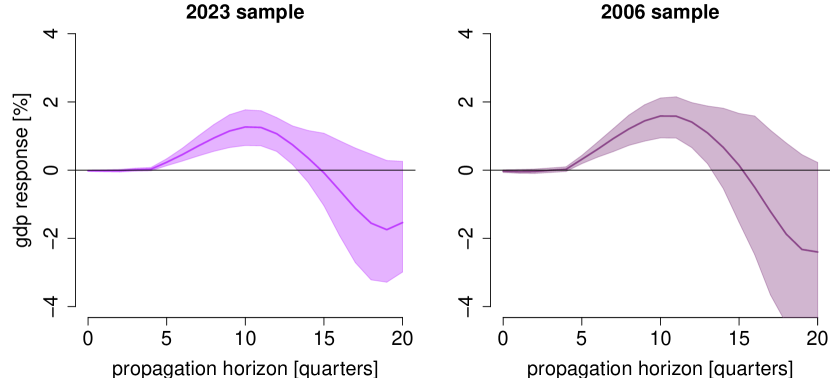

As our first shock in the PM–ordering can be called the tax shock using its correlation with a narrative measure, we investigate its dynamic effects on , a focal relationship in the other studies. In Figure 8 we report the corresponding impulse responses coming from our estimates for both samples. Following MR and LE, they represent responses to a tax shock that reduces by one percent of in the last quarter of 2006. They share three common features, namely, (i) no effect on impact and for the first four quarters followed by (ii) an increase in reaching a peak around 1.27 percent ten quarters after the impact, and (iii) becoming statistically insignificant after around three years. For the two samples they differ by the width of the 68% HDP intervals that are smaller for the 2023-sample and wider for the 2006-sample. This increase in width is driven by both the larger sample size of the 2023-sample and the reduced level of empirical support for identification of the tax shock in the 2006-sample.

Note: The figure reports impulse responses of to a negative tax shock lowering by one percent of value in the last quarter of 2006. The lines report the posterior medians and the shaded areas the 68% HPD point-wise intervals.

Note: The figure reports impulse responses of to a negative tax shock lowering by one percent of value in the last quarter of 2006. In the 2023-sample plot, the line reports the posterior median and the shaded area reports the 95% HPD point-wise interval for the PM–ordering. In the remaining plots, the lines report the maximum likelihood estimator and the shaded areas–the 95% point-wise confidence intervals.

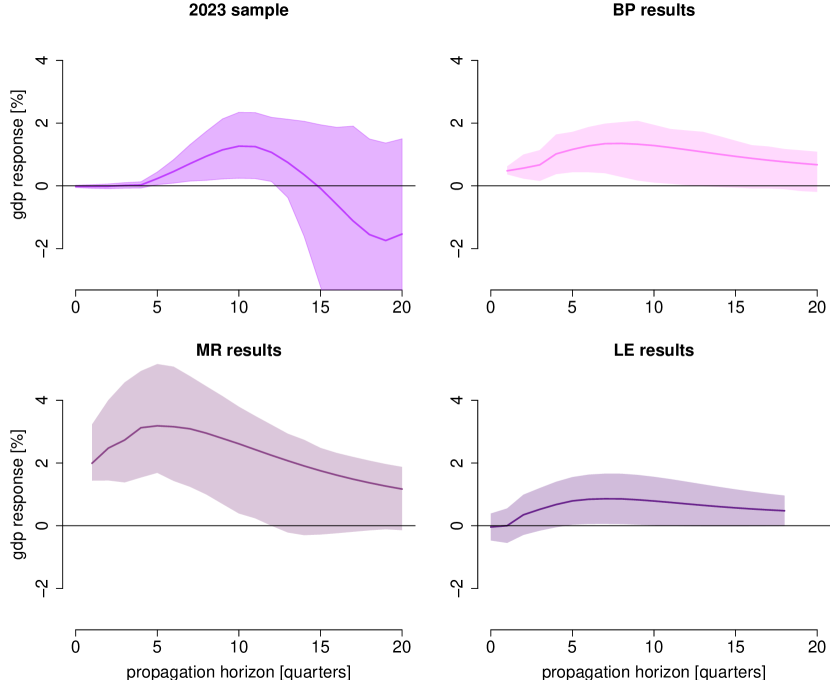

Nevertheless, the impulse response estimates from the 2023- and 2006-samples are quite similar to each other. We further compare them to the impulse responses reported in BP222Our BP results are based on the BP model estimated by MR., MR, and LE for the MR-sample, that is, the original data used by these authors. Figure 9 reports our estimates for the 2023-sample with 95% HDP intervals with the results from the BP, MR, and LE models reporting the maximum likelihood estimates with the 95% confidence intervals. Our results share two features with other estimates, namely, the peak is reached in the mid-horizons, and the statistical significance lost around three years after the impact. Additionally, our peak response is similar to those in BP and LE, whereas MR obtain a larger peak. However, only the impulse responses reported by LE are statistically insignificant on impact and in the following four quarters as in our estimates, while those by BP and MR are positive and significant also on impact. Nevertheless, the conclusions from our estimates do not deviate far from those established in the literature and are obtained by identification via heteroskedasticity and shock labelling using narrative measures only.

8 Conclusions

In this paper, we provided general conditions for the identification of a structural shock via heteroskedasticity in multivariate dynamic structural models. These conditions are applicable to a wide range of heteroskedastic and conditionally heteroskedastic structural vector autoregressions and can also be used if only a subset of the shocks can be identified through heteroskedasticity. We also proposed flexible and easy to compute Savage-Dickey density ratios to verify the identification conditions. This was facilitated by specifying new priors for time-varying conditional variances of the structural shocks. Such priors are flexible due to a hierarchical specification and ensure the standardisation using a specification centred at homoskedastic structural shocks. As a result, shock identification is indicated by the data and not implied by the prior.

These methods were illustrated by investigating whether the shocks in a system of fiscal variables are identified via heteroskedasticity. Identification is not confirmed for one of our samples but is supported when a longer sample period is used.

Our model is flexible and applicable to a wide range of time series in empirical macroeconomic and financial applications, which is facilitated by the code being available in an R package bsvars by Woźniak (2024a, b). Additionally, an important extension in which the structural matrix and the volatility of the log-volatility parameters change over time with a Markov process was recently proposed by Camehl and Woźniak (2024). That model facilitates verification through heteroskedasticity within Markov regimes.

References

- Barndorff-Nielsen (1997) Barndorff-Nielsen, O.E., 1997. Normal inverse gaussian distributions and stochastic volatility modelling. Scandinavian Journal of statistics 24, 1–13.

- Bauwens et al. (1999) Bauwens, L., Lubrano, M., Richard, J., 1999. Bayesian inference in dynamic econometric models. Oxford University Press, USA.

- Belmonte et al. (2014) Belmonte, M.A., Koop, G., Korobilis, D., 2014. Hierarchical Shrinkage in Time-Varying Parameter Models: Hierarchical Shrinkage in Time-Varying Parameter Models. Journal of Forecasting 33, 80–94. doi:10.1002/for.2276.

- Bertsche and Braun (2022) Bertsche, D., Braun, R., 2022. Identification of Structural Vector Autoregressions by Stochastic Volatility. Journal of Business & Economic Statistics 40, 328–341. doi:10.1080/07350015.2020.1813588.

- Bitto and Frühwirth-Schnatter (2019) Bitto, A., Frühwirth-Schnatter, S., 2019. Achieving shrinkage in a time-varying parameter model framework. Journal of Econometrics 210, 75–97.

- Blanchard and Perotti (2002) Blanchard, O., Perotti, R., 2002. An Empirical Characterization of the Dynamic Effects of Changes in Government Spending and Taxes on Output. The Quarterly Journal of Economics 117, 1329–1368. doi:10.1162/003355302320935043.

- Cadonna et al. (2020) Cadonna, A., Frühwirth-Schnatter, S., Knaus, P., 2020. Triple the gamma unifying shrinkage prior for variance and variable selection in sparse state space and tvp models. Econometrics 8, 20.

- Callealta Barroso et al. (2020) Callealta Barroso, F.J., García-Pérez, C., Prieto-Alaiz, M., 2020. Modelling income distribution using the log Student’s t distribution: New evidence for European Union countries. Economic Modelling 89, 512–522. doi:10.1016/j.econmod.2019.11.021.

- Camehl and Woźniak (2024) Camehl, A., Woźniak, T., 2024. Time-varying identification of monetary policy shocks. arXiv preprint arXiv:2311.05883 .

- Carriero et al. (2019) Carriero, A., Clark, T.E., Marcellino, M., 2019. Large Bayesian vector autoregressions with stochastic volatility and non-conjugate priors. Journal of Econometrics 212, 137–154. doi:10.1016/j.jeconom.2019.04.024.

- Chan and Jeliazkov (2009) Chan, J., Jeliazkov, I., 2009. Efficient Simulation and Integrated Likelihood Estimation in State Space Models. International Journal of Mathematical Modelling and Numerical Optimisation 1, 101–120.

- Chan and Eisenstat (2018) Chan, J.C., Eisenstat, E., 2018. Bayesian model comparison for time-varying parameter vars with stochastic volatility. Journal of Applied Econometrics 33, 509–532.

- Chan (2018) Chan, J.C.C., 2018. Specification tests for time-varying parameter models with stochastic volatility. Econometric Reviews 37, 807–823. doi:10.1080/07474938.2016.1167948.

- Chan et al. (2024) Chan, J.C.C., Koop, G., Yu, X., 2024. Large order-invariant bayesian vars with stochastic volatility. Journal of Business & Economic Statistics 42, 825–837. doi:10.1080/07350015.2023.2252039.

- Clark and Ravazzolo (2015) Clark, T.E., Ravazzolo, F., 2015. Macroeconomic Forecasting Performance Under Alternative Specification of Time-Varying Volatility. Journal of Applied Econometrics 30, 551–575.

- Cogley and Sargent (2005) Cogley, T., Sargent, T.J., 2005. Drifts and volatilities: Monetary policies and outcomes in the post WWII US. Review of Economic Dynamics 8, 262–302.

- Doan et al. (1984) Doan, T., Litterman, R.B., Sims, C.A., 1984. Forecasting and Conditional Projection Using Realistic Prior Distributions. Econometric Reviews 3, 37–41.

- Eddelbuettel (2013) Eddelbuettel, D., 2013. Seamless R and C++ Integration with Rcpp. Springer, New York, NY.

- Eddelbuettel et al. (2011) Eddelbuettel, D., François, R., Allaire, J., Ushey, K., Kou, Q., Russel, N., Chambers, J., Bates, D., 2011. Rcpp: Seamless r and c++ integration. Journal of statistical software 40, 1–18.

- Eddelbuettel and Sanderson (2014) Eddelbuettel, D., Sanderson, C., 2014. RcppArmadillo: Accelerating R with high-performance C++ linear algebra. Computational Statistics & Data Analysis 71, 1054–1063.

- Francis and Ramey (2009) Francis, N., Ramey, V.A., 2009. Measures of per capita hours and their implications for the technology-hours debate. Journal of Money, credit and Banking 41, 1071–1097.

- Frühwirth-Schnatter and Wagner (2010) Frühwirth-Schnatter, S., Wagner, H., 2010. Stochastic model specification search for Gaussian and partial non-Gaussian state space models. Journal of Econometrics 154, 85–100.

- Gelfand and Smith (1990) Gelfand, A.E., Smith, A.F.M., 1990. Sampling-Based Approaches to Calculating Marginal Densities. Journal of the American Statistical Association 85, 398–409. doi:10.2307/2289776.

- Giannone et al. (2015) Giannone, D., Lenza, M., Primiceri, G.E., 2015. Prior selection for vector autoregressions. Review of Economics and Statistics 97, 436–451.

- Herwartz and Lütkepohl (2014) Herwartz, H., Lütkepohl, H., 2014. Structural vector autoregressions with Markov switching: Combining conventional with statistical identification of shocks. Journal of Econometrics 183, 104–116.

- Hogg and Klugman (1983) Hogg, R.V., Klugman, S.A., 1983. On the estimation of long tailed skewed distributions with actuarial applications. Journal of Econometrics 23, 91–102. doi:10.1016/0304-4076(83)90077-5.

- Hörmann and Leydold (2014) Hörmann, W., Leydold, J., 2014. Generating generalized inverse gaussian random variates. Statistics and Computing 24, 547–557.

- Hosszejni and Kastner (2021) Hosszejni, D., Kastner, G., 2021. Modeling Univariate and Multivariate Stochastic Volatility in R with stochvol and factorstochvol. Journal of Statistical Software 100.

- Jarociński (2024) Jarociński, M., 2024. Estimating the fed’s unconventional policy shocks. Journal of Monetary Economics .

- Kass and Raftery (1995) Kass, R.E., Raftery, A.E., 1995. Bayes Factors. Journal of the American Statistical Association 90, 773–795. doi:10.1080/01621459.1995.10476572.

- Kastner and Frühwirth-Schnatter (2014) Kastner, G., Frühwirth-Schnatter, S., 2014. Ancillarity-sufficiency interweaving strategy (asis) for boosting mcmc estimation of stochastic volatility models. Computational Statistics & Data Analysis 76, 408–423.

- Kilian and Lütkepohl (2017) Kilian, L., Lütkepohl, H., 2017. Structural Vector Autoregressive Analysis. Cambridge University Press, Cambridge.

- Lanne and Luoto (2021) Lanne, M., Luoto, J., 2021. Gmm estimation of non-gaussian structural vector autoregression. Journal of Business & Economic Statistics 39, 69–81. doi:10.1080/07350015.2019.1629940.

- Lanne and Lütkepohl (2008) Lanne, M., Lütkepohl, H., 2008. Identifying monetary policy shocks via changes in volatility. Journal of Money, Credit and Banking 40, 1131–1149.

- Lanne et al. (2010) Lanne, M., Lütkepohl, H., Maciejowska, K., 2010. Structural vector autoregressions with Markov switching. Journal of Economic Dynamics and Control 34, 121–131.

- Lewis (2021) Lewis, D.J., 2021. Identifying Shocks via Time-Varying Volatility. The Review of Economic Studies 88, 3086–3124. doi:10.1093/restud/rdab009.

- Leydold and Hörmann (2017) Leydold, J., Hörmann, W., 2017. GIGrvg: Random Variate Generator for the GIG Distribution. URL: https://CRAN.R-project.org/package=GIGrvg. r package version 0.5.

- Lütkepohl (2005) Lütkepohl, H., 2005. New Introduction to Multiple Time Series Analysis. Springer-Verlag, Berlin.

- Lütkepohl et al. (2021) Lütkepohl, H., Meitz, M., Netšunajev, A., Saikkonen, P., 2021. Testing identification via heteroskedasticity in structural vector autoregressive models. The Econometrics Journal 24, 1–22.

- Lütkepohl and Milunovich (2016) Lütkepohl, H., Milunovich, G., 2016. Testing for identification in SVAR-GARCH models. Journal of Economic Dynamics and Control 73, 241–258.

- Lütkepohl and Netšunajev (2017) Lütkepohl, H., Netšunajev, A., 2017. Structural vector autoregressions with smooth transition in variances. Journal of Economic Dynamics and Control 84, 43–57.

- Lütkepohl and Velinov (2016) Lütkepohl, H., Velinov, A., 2016. Structural vector autoregressions: Checking identifying long-run restrictions via heteroskedasticity. Journal of Economic Surveys 30, 377–392.