Gradient descent for unbounded convex functions

on Hadamard manifolds

and its applications to scaling problems

Abstract

In this paper, we study asymptotic behaviors of continuous-time and discrete-time gradient flows of a “lower-unbounded” convex function on a Hadamard manifold , particularly, their convergence properties to the boundary at infinity of . We establish a duality theorem that the infimum of the gradient-norm of over is equal to the supremum of the negative of the recession function of over the boundary , provided the infimum is positive. Further, the infimum and the supremum are obtained by the limits of the gradient flows of , Our results feature convex-optimization ingredients of the moment-weight inequality for reductive group actions by Georgoulas, Robbin, and Salamon, and are applied to noncommutative optimization by Bürgisser et al. FOCS 2019. We show that the gradient descent of the Kempf-Ness function for an unstable orbit converges to a 1-parameter subgroup in the Hilbert-Mumford criterion, and the associated moment-map sequence converges to the mimimum-norm point of the moment polytope. We show further refinements for operator scaling—the left-right action on a matrix tuple . We characterize the gradient-flow limit of operator scaling via a vector-space generalization of the classical Dulmage-Mendelsohn decomposition of a bipartite graph. Also, for a special case of , we reveal that this limit determines the Kronecker canonical form of matrix pencils .

Keywords: Hadamard manifold, geodesically-convex optimization, gradient flow, matrix scaling, geometric programming, Hilbert-Mumford criterion, Kempf-Ness theorem, moment map, moment polytope, operator scaling, Dulmage-Mendelsohn decomposition, Kronecker canonical form, matrix pencil.

MSC-classifications: 90C25, 53C35

1 Introduction

In convex optimization, it is usually assumed that the objective function is bounded below. The performance of a minimization algorithm is evaluated by convergence behavior to the minimum of . The present paper addresses convergence behavior of a minimization algorithm for a “lower-unbounded” convex function , i.e., . This may look meaningless, because the trajectory of the algorithm diverges to the infinity, and goes to . The meta question of the paper is:

What can we gain from such a divergent sequence?

Let us formalize our setting and mention its background. Let be a Hadamard manifold—a simply-connected complete Riemannian manifold with nonpositive curvature, and let be a differentiable (geodesically-)convex function. We consider the following unconstrained convex optimization on :

| (1.1) |

Such a problem setting is significant in the recent progress on operator scaling [24] and generalizations; see [1, 9, 10, 19, 20, 21, 28]. In the classical matrix scaling [44], the scalability is equivalent to the boundedness of (1.1) for some . Further, it is also equivalent to the perfect matching condition of the associated bipartite graph. Hayashi, Hirai, and Sakabe [26] studies the asymptotic behavior of the Sinkhorn algorithm for unscalable (unbounded) case, and revealed that a combinatorial certificate (Hall blocker) of unscalability can be identified from the divergent behavior of the algorithm. Although a Hall blocker is easily obtained by a network-flow algorithm, finding the corresponding certificate (shrunk subspace) in the operator scaling setting is possible but quite difficult; see [25, 31, 32]. A recent work by Franks, Soma, and Goemans [17] modifies the operator Sinkhorn algorithm—alternating minimization algorithm for a convex function on a Hadamard manifold of positive definite matrices—to obtain a shrunk subspace in polynomial time, although it is still rather complicated. The matrix and operator scaling problems are generalized to a class of convex optimization involved with reductive group actions, called noncommutative optimization [10], which asks to minimize the Kempf-Ness function associated with an orbit of the action. This is formulated as convex optimization on a Hadamard manifold, specifically, a symmetric space of nonpositive curvature. It is lower-unbounded if and only if the orbit is unstable, where a -parameter subgroup in the famous Hilbert-Mumford criterion is an unbounded certificate that generalizes a Hall blocker and shrunk subspace. As mentioned in [10], the design of polynomial-time algorithms for several noncommutative optimizations, such as (un)stability determination, moment-polytope membership, and orbit-closure intersection, is a great challenge, and will bring fruitful applications to broader areas of mathematical sciences. Many of them involve the (un)bounded determination of Kempf-Ness functions, though our current knowledge on such problems is only limited.

Motivated by these considerations, we study the minimization of lower-unbounded convex functions on Hadamard manifolds. Even in the Euclidean setting , there are few works (see e.g., [3, 39]) on such study. We focus on asymptotic behavior of the most simplest algorithm—gradient descent. Accompanied with this, we also consider its continuous version—gradient flow, that is, a trajectory produced by differential equation .

The contribution and organization of this paper are summarized as follows. We begin with a general study on asymptotic behavior of the gradient flow/descent for an unbounded convex function on . As in the Euclidean setting, the recession function (asymptotic slope) of (see [27, 33]) is a basic tool analyzing the unboundenss, which is a function defined on the boundary at infinity of . Intuitively, the boundary is the set of all directions from an arbitrary fixed point , and represents the slope of along the direction at infinity. A Hadamard manifold admits a compactification , where the resulting topology is called the cone topology. These notions and related manifold terminologies are summarized in Section 2.

We focus on the convergence properties, with respect to the cone topology, of the gradient flow/descent for an unbounded convex function . In Section 3, under the sufficient condition of unboundedness, we establish in Theorem 3.1 that the gradient flow converges to a point of boundary with providing the following min-max (inf-sup) relation:

| (1.2) |

The limit is the unique minimizer of over , and is a certificate of the unboundedness. Further, we also show in Theorem 3.7 that the same result holds for the sequence obtained by the gradient descent applied to an -smooth convex function with step-size . These are the core results of the paper that drives the subsequent arguments.

Even Euclidean setting , the convergence results on the gradient flow/descent seem new, and brings an interesting ramification (Theorem 3.14): both and converges to the minimum-norm point of the gradient space (that is convex). This means that the gradient descent is interpreted as a minimum-norm point algorithm in the gradient space. Other interesting connections and implications to Hessian Riemannian gradient flow [2] and geometric programming are also mentioned.

In Section 4, we mention applications. In Section 4.1, we deal with the norm-minimization in a reductive group action on a complex vector (projective) space. As mentioned, this is the minimization of the Kempf-Ness function of an orbit. Then, the gradient descent in this case is nothing but the first-order algorithm in [10]. Applying our results, we show that for the unstable case the trajectory of the first-order algorithm converges, in cone topology, to the unique minimizer of , that produces a -parameter subgroup in the Hilbert-Mumford criterion. Further, the spectre of the moment-map ( transported gradient of ) along the trajectory converges to the minimum-norm point of the moment polytope . For the gradient-flow setting, we reveal the connection to the theory of the moment-weight inequality for reductive group actions, developed by Georgoulas, Robbin, and Salamon [22] building upon the earlier work of GIT by Kempf, Kirwan, Mumford, Ness and a recent work by Chen and Sun [13, Section 4]. Specifically, the weak duality in (1.2) becomes the moment-weight inequality, and the strong duality via the gradient flow can explain important parts of their theory. It may be fair to say that our results in Section 3 extract and discretize convex-optimization ingredients of their theory.

In Section 4.2, we focus on the left-right action on a matrix tuple , that corresponds to the operator scaling problem. In this setting, the middle equality in (1.2) is interpreted as a duality theorem for the scalability limitation (Theorem 4.19), which sharpens Gurvits’ characterization in an inf-sup form. We then study the limit of the gradient flow/descent of the Kempf-Ness function . Our focus is in the unscalable case, whereas the scalable case was studied in detail by Kwok, Lau, Ramachandran [36]. We show in Theorems 4.22 and 4.24 that the minimum-norm point of the moment polytope and the limit of the gradient flow/descent are characterized by a certain simultaneous block-triagularization of , which is a vector-space generalization of the classical Dulmage-Mendelsohn decomposition [15] of a bipartite graph. More specifically, the sequence of (normalized) scaling tuples along the gradient flow/descent converges to a block-diagonal matrix modulo the left-right unitary group action, where the block structure is determined by our generalized DM-decomposition. This answers the gradient-flow/descent variant of an open question by Garg and Oliveria [21, Section 6] for asking the behavior of the operator Sinkhorn algorithm for unscalable instances. Finding this block-structure itself is significant. We partially eliminate the unitary indeterminacy from , and exploit a convergence sequence to a coarse block-triangular structure (Theorems 4.25 and 4.26). This leads to a construction of a shrunk subspace (a certificate of unscalability) by the simple gradient descent with the help of the rounding of Franks, Soma, and Goemans [17].

Also, in Section 4.3, for a special case of , we reveal that our DM-decomposition of coarsens and determines the well-known Kronecker canonical form of matrix pencils . The Kronecker form plays important roles in the systems analysis by a differential-algebraic equation (DAE) . Its computation has been studied for a long time in the literature of numerical computation; see e.g., [14, 45]. Our convergence result (Theorem 4.30) suggests a new iterative method for determining the Kronecker structure, which is based on the simple gradient descent and is conceptually different from the existing ones.

These results may be positioned as attempts of detecting, by algorithms in , hidden structures in the boundary at infinity, which has been little studied so far. We hope that our attempts lead to more serious studies from computational complexity perspective. Particularly, it is an important future direction to improve the present convergence-type results of the gradient descent to the ones having explicit iteration complexity.

2 Preliminaries

Let and denote the sets of real and nonnegative real numbers, respectively. We often add to and the infinity elements , where the topology and ordering are extended in the natural way. Let denote the set of complex numbers , where denotes the complex conjugate and denotes the real part . The same notation is used for a complex vector with as . For a matrix over , let denote the transpose conjugate. For sets and of row indices and column indices, let denote the submatrix of with row indices in and column indices in . For two matrices (of possibly different sizes), let denote the block-diagonal matrix of block-diangonals in order. For a vector , let denote the diagonal matrix with .

The general linear group and special linear group over are simply denoted by and , respectively. The unitary group and special unitary group are denoted by and , respectively. For a finite dimensional vector space over , let denote the group of linear isomorphisms on .

For a positive integer , let . For , let be defined as if and otherwise. If , then is simply written as .

Sequences and are simply denoted by and , respectively.

2.1 Riemannian geometry

We will utilize standard terminologies and notation on Riemannian geometry; see e.g., [42]. See also a recent book [7] for optimization perspective. We assume sufficient differentiability for manifolds, and functions, maps, and vector/tensor fields on them. Let be a Riemannian manifold. For , let denote the tangent space of at , where denotes the Riemannian metric at and denotes the associated norm. Let and denote the unit sphere and ball in , respectively. The angle of two vectors is defined as . The product of two Riemannian manifolds is viewed as a Riemannian manifold by setting .

For a path and , let denote the tangent vector of at . The length of the path is defined by . The distance between is the infimum of the length of a path connecting and . We consider the Levi-Civita connection associated with the Riemannian metric. The connection determines a parallel transport along any path with , where . By using the parallel transport, the covariant derivative of a vector field by is given by , where is a path with and .

In this paper, any manifold is assumed complete. That is, the metric space are complete. Then the distance is always attained by a geodesic—a path satisfying for . By a unit-speed geodesic ray we mean a geodesic with (and then for all ). For and , there is a unique geodesic with and . By the completeness of , the map is defined on . This gives rise to a surjective map , called the exponential map.

For a map , where is another manifold, let denote the differential of at . The differential of a function is given by , where is a path with and . The gradient of is then defined via

The covariant differentiation of the gradient vector field gives rise to the Hessian :

The Hessian is a symmetric operator in the sense that .

Complex projective space.

We will consider the complex projective space as a Riemannian manifold. Let be an -dimensional vector space over . The complex projective space over is a quotient manifold by the equivalent relation for some nonzero . The image of by is denoted by . A Riemannian structure on is given by the Fubini-Study form as follows. Let be a Hermitian inner product on . Regard as a -dimensional Euclidean space by the real inner product . This induces a Riemannian structure on the sphere , where we set . Then is viewed as the Riemannian quotient of by isometry for . The resulting metric on is called the Fubini-Study metric. See e.g., [7, Chapter 9] for Riemannian quotient manifolds.

2.2 Hadamard manifolds

A Hadamard manifold is simply-connected complete Riemannian manifold having nonpositive sectional curvature everywhere; see [42, V.4]. For any two points in , a geodesic connecting them is uniquely determined (up to an affine rescaling). The exponential map is a diffeomorphism from to . The parallel transport from to along the geodesic is simply written as .

In this paper, the boundary at infinity and the cone topology on play partiularly important roles; see [42, V.4.2] for a quick introduction for these notions. Two unit-speed geodesic rays are called asymptotic if for some constant . The asymptotic relation is an equivalence relation on the set of all unit-speed geodesic rays. Let denote the set of equivalence classes for all rays. Let us fix an arbitrary point . Any unit vector defines an asymptotic class of unit-speed geodesic ray . This correspondence is a bijection between and , and induces a topology on that is isomorphic to sphere . In fact, this topology is independent of the choice of . Further, the topologies on and on are extended to as follows. Since is a diffeomorphism, it holds , where is an equivalence relation or . With , we obtain compact Hausdorff space (isomorphic to ). This topology on is called the cone topology. Then, a sequence in converges to if and only if

-

•

, and

-

•

the sequence in determined by converges to , where the asymptotic class of geodesic is equal to .

The angle of two points is defined as , where and are the representatives of and , respectively, at . The angle defines a metric on , which induces a different topology. By using the angle metric on , we can define a metric on the Euclidean cone of the boundary by . This space is viewed as the space of asymptotic classes of (not necessarily unit-speed) geodesic rays. It is identified with , though the metric space has a different topology from and is not necessarily a manifold. The metric space is known as a Hadamard space—a complete geodesic metric space satisfying the CAT(0)-inequality [8]. It is uniquely geodesic, and its convexity is defined along geodesics. The unit ball around the origin is a convex set, where the origin is the image of point with . Observe that can be identified with for any .

Manifold of positive definite matrices and symmetric space.

A representative example of Hadamard manifolds is the space of positive definite Hermitian matrices; see [8, II. 10]. The tangent space at is identified with the vector space of Hermitian matrices, and the Riemannian metric is given by . In this case, several manifold notions are explicitly written; see, e.g., [28, Section 5.2]. The exponential map at is given by , where is the matrix exponential. Particularly, any geodesic issuing from is of form for some Hermitian matrix with , where is the Frobenious norm. An explicit formula of the geodesic parallel transport is also known. We will use one special case: .

Any totally geodesic subspace of is also a Hadamard manifold. Here a submanifold is said to be totally geodesic if every geodesic in is also geodesic in . It is known that for a Lie group defined by polynomials and satisfying , submanifold is a totally geodesic subspace. Such a group is called a reductive algebraic group, and is known as a symmetric space (of nonpositive curvature). A particular case we will face is: and , where tangent space at is given by . It is known that the boundary at infinity of the symmetric space becomes spherical building, and the associated cone becomes a Euclidean building; see e.g., [8, II. 10]. We will consider convex functions on these spaces in Section 4.

2.3 Convex functions

In Hadamard manifold , by the uniqueness of geodesics, convexity is naturally introduced. A function is said to be convex if for every geodesic one dimensional function is convex. This condition is equivalent to . From , the convexity of is equivalent to the positive semidefiniteness of the Hessian :

for all . We also consider the Lipschitz condition for gradient vector field . A function is said to be -smooth with if

for all , . That is, the operator norm is bounded by for all .

We next introduce an important tool for studying unboundedness of a convex function. Let us fix . The recession function (asymptotic slope) [27, 33] is defined by

| (2.1) |

where is independent of ; if and are asymptotic, then [35, Lemma 2.10]. The recession function is naturally extended to by allowing to any vector in . If , then and matches the recession function in Euclidean convex analysis; see [41, Section 8] and [29, Section 3.2]. As in the Euclidean case, and the following properties hold:

| (2.2) |

The second property is included in [33, Lemma 3.2 (vi)]. Moreover, it is known [27] that is a positively homogeneous convex function on Hadamard space .

In particular, both and are sufficient conditions for unboundedness of . In fact, they are equivalent.

Proposition 2.1 ([33, Lemma 3.2 (iii), Lemma 3.4]; see also [27]).

-

(1)

if and only if .

-

(2)

If , then there uniquely exists with .

The existence in (2) follows from lower-semicontinuity of on the compact space with respect to the cone topology. The uniqueness of in (2) can be seen from positively homogeneous convexity of on , as in the Euclidean case.111If , then by convexity, it holds for the midpoint of and in , and by it holds .

As a sharpening of the easier part (the only-if part) in (1), we here mention the following weak duality between the gradient-norm and the recession function.

Lemma 2.2 (Weak duality).

Proof.

For and , it holds

∎

In Section 3, we show, via the gradient flow of , that the equality (strong duality) always holds. This technique may be viewed as a refinement of the proof of the if-part in Proposition 2.1 (1) in [33], in which a limit of the gradient flow of constructs with . A similar gradient-flow approach can be found in [13, 22, 46] for the setting of GIT; see Section 4.1.

3 Asymptotic behavior of gradient flow

3.1 Continuous-time gradient flow

Let be a convex function. Consider the following differential equation—the gradient flow of ,

| (3.1) |

It is clear that the trajectory is going to minimize ; see Lemma 3.2 (1) below. In fact, if a minimizer of exists, then converges to a minimizer. This convergence is known for a general setting of Hadamard spaces; see e.g., [4, Theorem 5.1.16] and [37, Theorem 2.41]. Our focus is the case where is unbounded below, particularly the case where the minimum gradient-norm is positive. We establish the following convergence of an unbounded gradient flow and the strong duality between the gradient-norm and the recession function.

Theorem 3.1.

Suppose that . Let be the solution of (3.1).

-

(1)

converges to the minimum gradient norm , and

-

(2)

converges, in cone topology, to the unique minimizer of over ,

where the following equality holds

| (3.2) |

We should mention related results. In a general setting of a Hadamard space , Caprace and Lytchak [12, Proposition 4.2] showed that the gradient-flow curve of a Lipschitz convex function with converges to a point in the boundary of . Their proof relies on a very general result of Karlsson and Margulis [34, Theorem 2.1] for semi-contraction semigroups in uniformly convex spaces. Here it is well-known that the gradient-flow semigroup satisfies the (semi-)contraction property:

| (3.3) |

where is the solution of (3.1) with initial point . If the velocity of escape

| (3.4) |

is positive, then [34, Theorem 2.1] is applicable for the convergence of in ; Caprace and Lytchak actually showed that implies . Although a more effort can deduce, from this convergence result, the whole statement of Theorem 3.1, we take a different approach which relies on neither [34] nor contraction property (3.3). As mentioned after Lemma 2.2, our proof is partly inspired by an idea in [33] but directly establishes the relation (3.2). An advantage of this approach is to adapt to the discrete setting in Section 3.2.

We start with the following well-known properties of gradient flows.

Lemma 3.2.

-

(1)

The solution of (3.1) is defined on .

-

(2)

is nonincreasing.

-

(3)

is nonincreasing.

We describe a proof since the intermediate equations will be used.

Proof.

(2) follows from

(3) follows from

(1). Suppose that is defined on for finite . The length of curve is given by

where the inequality follows from (3). This means that the curve belongs to the closed ball of radius with center . Then, is connected to the solution of (3.1) with initial point . Thus the solution of (3.1) is defined on . ∎

Proof of Theorem 3.1.

Let . First, we note

| (3.5) | |||

| (3.6) |

Then it holds . Otherwise, has an accumulation point in and by (3.5), contradicting .

Define via For , by convexity of along geodesic from to , it holds

From this, we have

where the second inequality follows from (3.5) and (3.6), the third from the Cauchy–Schwartz inequality for and , and the fourth from Lemma 3.2 (3).

Choose any convergence subsequence with and . Then it holds

For , we have Then, by weak duality (Lemma 2.2),

Thus the equality holds. Since the minimum of over uniquely exists (Proposition 2.1 (2)), it must hold . Any convergence subsequence of converges to . Since is compact, itself converges to . ∎

Even if , the strong duality holds (since ):

Corollary 3.3.

The velocity of escape (3.4) coincides with the minimum gradient-norm.

Proposition 3.4.

Suppose that . Then it holds

Proof.

For , it holds . Hence

On the other hand, we have

where is the unit speed geodesic from to . Thus it holds

For arbitrary large , can be arbitrary close to . Hence we have

∎

We next consider the “convergence” of gradient . Since the space varies, the convergence concept of is less obvious. In our intuition, and would have opposite directions in limit. The following partially justifies this intuition.

Proposition 3.5.

Suppose that . Let denote the representative of the unique minimizer of over . Then it holds

Question 3.6.

Does hold ?

We will see in Section 4 that this property holds for the Kempf-Ness function and has important consequences.

Proof of Proposition 3.5.

Let be the unit-speed geodesic from to . Let . Then, by [42, Chapter III, Proposition 4.8 (1)], it holds Therefore, we have

| (3.7) |

On the other hand, by Proposition 3.4, it holds , where the inequality is a general property. Thus the equality holds in (3.7). Necessarily we have

| (3.8) |

By , we have . With parallel transport and , we have the claim. ∎

3.2 Discrete-time gradient flow (gradient descent)

Next we consider the discrete version. Suppose that is an -smooth convex function. Consider the following sequence:

| (3.9) |

This is nothing but the trajectory generated by the gradient descent with initial point and step-size ; we remark in Remark 3.12 another type of discrete gradient flow. The convergence/accumulation of to a minimizer of can be shown under several reasonable assumptions; see e.g., [7, Theorem 11.29]. For an unbounded case, as in the continuous setting, we establish the following.

Theorem 3.7.

Suppose that . Let be the sequence in (3.9).

-

(1)

converges to the minimum gradient norm , and

-

(2)

converges, in cone topology, to the unique minimizer of .

Hence the following holds

| (3.10) |

Our original attempt proving this was to establish the contraction property

| (3.11) |

for the semigroup of (3.9), and to apply the approach of [12, 34]. But we could not do it, and do not know whether (3.11) is true. Note that (3.11) is true in Euclidean space ; see e.g., [43, Example 1].

The proof goes a way analogous to Theorem 3.1. Corresponding to Lemma 3.2, the following properties hold.

Lemma 3.8.

-

(1)

.

-

(2)

.

Contrary to the well-known inequality (see [7, (11.15)]), our inequality (1) seems less well-known; see Remark 3.13 for further discussion.

Proof.

(2). Let . Then we have

where we use since is a geodesic. Since is invariant under parallel transport, the operator norm of is equal to that of . By convexity and -smoothness, all eigenvalues of belong to . Hence we have

(1).

By squaring this, we have , particularly,

| (3.12) |

From convexity, it holds

∎

Proof of Theorem 3.7.

Let . For , we have

| (3.13) | |||||

| (3.14) |

where the first inequality follows from Lemma 3.8 (1) and the second from the triangle inequality. Then holds (as before).

We show the limiting behavior of the decrement of the function-value, the change of gradients, and the velocity of escape.

Proposition 3.9.

Suppose that .

-

(1)

.

-

(2)

.

-

(3)

.

Proof.

(3). By the triangle inequality, it holds . Hence

On the other hand, for arbitrary , we have

where the first inequality follows from Lemma 3.8 (2), the second from (1), and the third from the convexity of , and is the unit speed geodesic from to . Thus for arbitrary , it holds

For arbitrary large , can be arbitrary close to . Hence we have

∎

For convergence of , the same property of Proposition 3.5 holds:

Proposition 3.10.

Suppose that . Let denote the representative of the unique minimizer of over . Then it holds

Question 3.11.

Does hold ?

Proof of Proposition 3.10.

Let . We first show

| (3.16) |

Indeed, by the triangle inequality and Theorem 3.7 (1), we have . On the other hand, by Proposition 3.9 (3), it holds , where the inequality is true for an arbitrary sequence.

Consider the geodesic triangle of vertices . Let denote the unit-speed geodesic from to . Let denote the angle at vertex of this triangle. Then

By the law of cosines in CAT(0) space (see e.g., [8, II.1.9 (2)]), we have

Take in this inquality. By , , (seen from Proposition 3.9(3)), and (3.16), we have , and By Proposition 3.9 (2), it holds and

By taking parallel transport and , we have the claim. ∎

Remark 3.12.

Another type of discrete gradient flow, well-studied in the literature of nonpositively-curved space (see [4, 37, 40]), is defind via the resolvent map ,

| (3.17) |

where is a positive parameter. Let be a sequence of positive reals (satisfying and ). Then a discrete analogue (the proximal point method) of gradient flow is as follows:

| (3.18) |

For our manifold case, it can be written as an implicit difference scheme:

| (3.19) |

Several nice (convergence) properties are known for the sequence of (3.18). For example, contraction property (3.11) holds for the semigroup of (3.18); see [4, Theorem 2.2.23]. On the other hand, solving (3.17) is a nontrivial task from algorithmic point of view

Remark 3.13.

3.3 Euclidean specialization

Here we present refinements of the above results for Euclidean setting . As far as our knowledge, the convergence results on discrete/continuous gradient flows seem new even in the Euclidean case, which are further sharpened as follows. In the Euclidean space , the tangent space is also identified with for every , where the inner product is given by . Notice that the parallel transport for any path is the identity map. Let be a convex function. We assume the -smoothness of when the discrete gradient flow (3.9) is considered. The gradient and Hessian are obtained by and , respectively. Let be the Legendre-Fenchel conjugate of :

Then it holds that

| (3.20) |

Note that the duality relation (Corollary 3.3) can be seen from this expression; see the proof of Theorem 3.14 below. In particular, the closure of the gradient space is convex, and both and converge to the point in having the minimum norm, which is uniquely determined.

Theorem 3.14.

Let denote the minimum-norm point of .

-

(1)

converges to , and converges to .

-

(2)

converges to , and converges to .

Proof.

It suffices to show the claims for and . The unique minimizer of over the unit sphere is written as . Indeed, consider the unit normal vector of supporting hyperplane at , which is written as . Then . ∎

Since , the expected convergences in Questions 3.6 and 3.11 hold in this case. We end this section with other interesting aspects.

Hessian Riemannian gradient flow.

Here we point out that the convergence of to the minimum-norm point can also be explained via the theory of Hessian Riemannian gradient flow by Alvarez, Bolte, and Brahic [2]. Suppose for simplicity that Hessian is nonsingular for every . Consider continuous gradient flow , and let . One more derivative yields

From , we have the following differential equation obeyed by :

| (3.21) |

In fact, this can also be viewed as a gradient flow on a Riemannian manifold as follows. Define a Riemannian metric on an open convex set by

| (3.22) |

In this metric, the gradient of is given by . Then the differential equation (3.21) becomes the gradient flow of the squared-norm function :

| (3.23) |

This is a particular instance of a Hessian Riemannian gradient flow in [2]. Then, by [2, Proposition 4.4], the solution of (3.23) minimizes over in limit . which proves .

It may be interesting to develop a discrete version of Hessian Riemannian gradient flow that can explain the convergence of . Also, developing a manifold analogy, by possibly using the space in [27], may be an interesting direction. Related to this issue, in Section 4.1, we will consider a similar gradient flow (Kirwan’s flow) in the complex projective space.

Matrix scaling and geometric programming.

The matrix scaling problem [44] is: For a given nonnegative matrix , find positive diagonal matrices (scaling matrices) such that and . This scalability condition is represented as for the following convex function

| (3.24) |

Required scaling matrices are obtained by , for having small gradient norm . Particularly, such a point is obtained by minimizing . Sinkhorn algorithm [44]—the standard algorithm for matrix scaling—is viewed as alternating minimization of .

For motivating combinatorial optimization application, Hayashi, Hirai, and Sakabe [26] studied asymptotic behavior of the Sinkhorn algorithm in the unscalable case (), and revealed remarkable convergence properties: Both gradient ( row and column marginal of ) and the scaled matrix become oscillating between two accumulation points in limit, which is characterized by a canonical block-triangular form of , knowns as (an extended version of) the DM-decomposition [15]; see also [38, Section 2.2.3].

Our results reveal analogous asymptotic behavior of the gradient descent for unscalable matrix scaling. The matrix-scaling optimization for (3.24) falls into a more general class of convex optimization, called geometric programming, to which our results are applicable. The geometric programming asks to minimize a function of the following form:

| (3.25) |

where and for . It is well-known (see e.g.,[11]) that

-

•

is -smooth convex with , and

-

•

.

Therefore, with , by the gradient descent (3.9) applied to (3.24), the gradient sequence converges to the minimum-norm point of . The point and the limit of (in the projective space) are again characterized via the DM-decomposition of . They will be explained for a more general setting of operator scaling in Section 4.2.

Apart from the matrix scaling application, it is a notable fact that the gradient descent (3.9) applied to (3.25) is viewed as a minimum-norm point algorithm for , which is seemingly new and interesting in its own right. Further convergence/complexity analysis of this algorithm is left to future work.

4 Applications

4.1 Norm-minimization in reductive group actions

We consider the formulation of noncommutative optimization in [10]; see also [28]. Let be a connected reductive algebraic group over . Specifically, it is closed under complex conjugate and is defined by a finite set of polynomials. Its Lie algebra is the complexification of the Lie algebra of a maximal compact subgroup as , where . The inner product on is defined by . Let be a finite dimensional vector space over . Let be a rational representation, where denotes its Lie algebra representation: . Consider a -invariant Hermitian inner product and the associated norm on . The norm-minimization problem over the orbit of is given by

| (4.1) |

It turned out (e.g., [10]) that this optimization problem and relatives have numerous, sometimes unexpected, applications and connections in various fields of mathematical sciences. The most fundamental problem is to ask whether the infimum is zero, i.e., the origin is in an orbit closure . This is the (semi-)stability problem in geometric invariant theory (GIT). The representation gives rise to a Hamiltonian action on complex projective space by . The corresponding (modified) moment map is given by

| (4.2) |

where the moment map is formally given by ; see [22, Lemma 8.2]. The following theorem is fundamental:

Theorem 4.1 (Kempf-Ness theorem, Hilbert-Mumford criterion; see [22, Theorem 8.5 (i), Theorem 12.4]).

For , the following conditions are equivalent:

-

(i)

.

-

(ii)

.

-

(iii)

There is a 1-parameter subgroup of such that .

The orbit in this situation is called unstable. Accordingly, we call the 1-parameter subgroup in (iii) an unstable 1-PSG.

The unstability corresponds to the lower-unboundedness of the Kempf-Ness function . Since is -invariance, the Kempf-Ness function is viewed as a function on the symmetric space . With by and , we may consider the Kempf-Ness function as the following function on Hadamard manifold :

| (4.3) |

Then is an -smooth convex function such that the transported gradient of provides the moment map :

Lemma 4.2 ([10]).

-

(1)

is -smooth convex, where is the maximum of the norm of a weight for .

-

(2)

.

The second property (2) is implicit in [10] and follows from and . In particular, for the Kempf-Ness function , the unboundedness and the positivity of the minimum gradient-norm are equivalent. Applying Corollary 3.3, we have:

Theorem 4.3.

. If , then is an unstable 1-PSG.

Proof.

As seen below, this is a part of the theory of moment-weight inequality [22], in which the recession function is essentially Mumford’s numerical invariant, called the -weight; see Lemma 4.11 below.

Bürgisser et al. [10] applies the gradient descent (the first-order algorithm) to :

| (4.4) |

where . For the semi-stable case (), they showed its iteration complexity to compute and to find with . For unstable case (), our result (Theorem 3.7) implies that the gradient descent constructs an unstable -PSG in limit, where an unstable -PSG is said to maximum if it is obtained as the minimizer of over .

Theorem 4.4.

Suppose that . Let be the sequence of (4.4), and let be the sequence defined by . Then converges to the unique minimizer of over , where is the maximum unstable -PSG.

Unfortunately, since is not necessarily (upper-semi)continuous, this theorem does not imply the algorithmic statement: is an unstable -PSG for some large . Therefore, we need a certain rounding idea to obtain an unstable -PSG from . We see in the next Section 4.2 that such a rounding is possible for the left-right action.

We also consider the convergence of the moment map (transported gradient). Let denote a positive Weyl chamber: It is a convex cone with the property that for any there is a unique point with for some . The moment polytope is defined as the closure of the image of :

The convexity theorem by Guillemin and Sternberg [23] says that it is a convex polytope.

Theorem 4.5 (Convexity theorem [23]).

is a convex polytope.

| (4.5) |

we have the convergence of the moment-map spectre along the gradient-descent trajectory:

Theorem 4.6.

converges to the minimum norm point of .

Remark 4.7.

Suppose that the convergence in Question 3.11 is true. Then converges to , where and is the unique minimizer of over . On the other hand, is the limit of the sequence determined by by Theorem 3.7 and Proposition 3.9 (3). Choose so that . Then the analogue of Theorem 3.14 holds:

We see in Theorem 4.6 below that it is true for the continuous setting.

Moment-weight inequality and gradient flow of moment-map squared.

Clearly, via Theorem 3.1, the above results (Theorems 4.4 and 4.6) hold for the continuous-time gradient flow:

| (4.6) |

Our consideration for this case falls into the theory of moment-weight inequality by Georgoulas, Robbin, and Salamon [22], which builds upon the earlier work of GIT by Kempf, Kirwan, Mumford, Ness, and a recent work by Chen and Sun [13]. Here we briefly summarize the relation by deducing an important part of the theory from our results in Section 3.1. We use notation for the action on . According to [22, Chapter 3], consider the gradient flow (Kirwan’s flow) of the squared-norm of the moment-map on :

| (4.7) |

This is a gradient flow of a real analytic function on a compact manifold . By a standard argument of Lojasiewics gradient inequality, the limit of exists.

Theorem 4.8 (Convergence Theorem [22, Theorem 3.3]).

The limit exists.

Further, the limit attains the infinum of the momemt-map norm over the orbit in .

Theorem 4.9 (Moment-limit theorem [22, Theorem 6.4]).

Let be the solution of (4.7), and let . Then it holds

| (4.8) |

This is a variant of [22, Theorem 4.1 (ii)], and the proof is also similar; we give it in Appendix. In particular, Theorem 4.6 can be understood as a discrete version of the moment-limit theorem, though we do not know whether converges.

We next explain the moment-weight inequality. The (restriction of) -weight is defined by

| (4.9) |

The -weight is nothing but the recession function of .

Lemma 4.11 (See [22, Lemma 5.2]).

.

Proof.

. ∎

We now state a main part of moment-weight inequality (for linear actions).

Theorem 4.12 (Moment-weight inequality [22, Theorems 6.7, 10.1, 10.2, 10.4]).

From our convex-optimization perspective, the moment-weight inequality (4.10) is explained by the weak duality (Lemma 2.2). The equality case is explained by the strong duality (Theorem 3.1), the gradient-flow construction of the unique minimizer of , and the formula of the velocity of escape (Proposition 3.4).

We also describe the limit of the moment map , which is a sharpening of [22, (10.9) in Theorem 10.4], and an analogue of Theorem 3.14 (1).

Theorem 4.13 (Limit of moment map).

Suppose that . It holds . In particular, for , it holds

Proof.

In particular, the convergence in Question 3.6 holds in this case. We finally state one important uniqueness property of minimizers of the moment-map norm over , which seems not follow from our approach directly.

Theorem 4.14 (Second Ness uniqueness theorem [22, Theorem 6.5]).

For , if , then .

In the next subsection, we characterize such minimizers in the left-right action.

4.2 Operator scaling and its gradient-flow limit

Let be an -tuple of matrix over . Let , be nonnegative vectors with the same sum , where are arranged as

| (4.11) |

The operator scaling problem, originally introduced by Gurvits [24] for and extended by Franks [16] for general , is to ask: For a given accuracy , find such that

| (4.12) |

where the norm is the Frobenius norm. A matrix tuple is said to be (approximately) -scalable if for every positive there are satisfying (4.12). If some satisfy (4.12) for , then is called exactly -scalable, and is called a -scaling of . The operator scaling is a quantum generalization of the matrix scaling, and turned out to have rich applications; see [16, 19, 20, 21]. For simplicity, we assume that the left and right common kernels of are both trivial: and .

In the view of the previous section, the operator scaling problem can be viewed as the moment polytope membership of the left-right action defined by

| (4.13) |

where . A maximal compact subgroup is given as , and the -invariant Hermitian product on is given by . From , we see that the moment map is given by

| (4.14) |

A positive Weyl chamber is taken as the set of diagonal matrices with satisfying (4.11) and , and is regarded as a subset of . Then the moment polytope consists of vectors of eigenvalues of over (the closure of the -orbit of ). Comparing (4.14) with (4.12), we have:

Lemma 4.15.

is -scalable if and only if belongs to , where .

We consider the operator scaling problem of the most basic case: . Then, it holds

| (4.15) |

Accordingly, Kempf-Ness theorem with Hilbert-Mumford criterion (Theorem 4.1) links with the -scaling problem, and is sharpened as follows: Let denote the family of pairs of vector subspaces , such that for all , , .

Theorem 4.16 (Charaterization of scalability [24]).

The following are equivalent:

-

(i)

.

-

(ii)

is -scalable.

-

(iii)

For all , it holds .

A vector-space pair violating (iii) actually gives rise to an unstable -PSG as follows: Choose and such that the first rows of span and the first rows of span , where . Then one can see that is an unstable -PSG.

Further, the strictly inequality in (iii) brings the exact scalability:

Theorem 4.17 (Exact scalability [24]).

If for all other than and , then is exactly -scalable.

The exact case corresponds to the existence of with . By Lemma 4.2 (2), this is the case where the Kempf-Ness function has an optimum a point of zero gradient. Then, Theorem 4.17 can be deduced from a general property (2.2) of the recession function (given in (4.18) below). Here the Kempf-Ness function is written as

| (4.16) |

Lemma 4.18 ([10]).

is -smooth convex.

Now Theorem 4.4 (Corollary 3.3, or moment-weight inequality (Theorem 4.12)) sharpens (ii) (iii) of Theorem 4.16 in the following min-max (inf-sup) form:

Theorem 4.19 (Duality theorem for scalability limit).

| (4.17) |

where the infimum in LHS is taken over all , with and the supremum in RHS is taken over all , , , with and .

Proof.

It suffices to show that is equal to the objective function of RHS in (4.17). Here is written as for , , with . Then we have

| (4.18) | |||||

where we used in the last equality. ∎

Consider the continuous-time and discrete-time gradient flows of :

| (4.19) | |||

| (4.20) |

where we let by Lemma 4.18. We study asymptotic behavior of (4.19) and (4.20). In the rest of this section, we are going to characterize:

-

(A)

The limit of the minimum-norm point of .

-

(B)

The limit of in cone topology the unique minimizer of .

-

(C)

The limit of in the mininizer of moment-map norm over (modulo action).

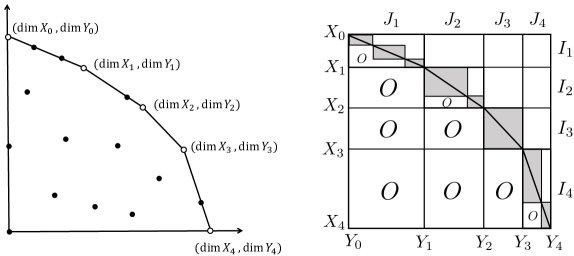

We show that these are characterized by a certain simultaneous block-triangular form of . This block-triangular form is a vector-space generalization of the classical Dulmage-Mendelsohn decomposition [15] (DM-decomposition for short) for a bipartite graph and its associated matrix. We introduce our generalized DM-decomposition in a way analogous to [26, Section 3] for the classical setting, where the essential idea of the construction can be partly found in Ito, Iwata, and Murota [30]. Recall the family defined before Theorem 4.16. Define a map by

Consider the convex hull ; see the left of Figure 1.

Let denote the subset of such that is an extreme point of not equal to .

Lemma 4.20.

For , if and , then and . In particular, is injective on .

Proof.

We may suppose that and are equal or on an adjacent pair of extreme points. Observe . By the dimension identity of vector spaces, it holds

| (4.21) |

This implies that and . Otherwise, or goes beyond , which contradicts . ∎

Therefore, can be arranged as

| (4.22) |

For each , let denote the subset consisting of such that belongs to the edge between and .

Lemma 4.21.

If , then . In particular, is a modular lattice with respect to the partial order , where the minimum and maximum elements are given by and , respectively.

For each , consider a maximal chain (flag) of :

where the length of the chain is uniquely determined by Jordan-Dedekind chain condition. The union is a maximal chain of the whole lattice , and is called a DM-flag. Its subset is called the coarse DM-flag, which is uniquely determined by . From a DM-flag, we obtain a simuletanous block triangular form of as follows. Consider including, as row vectors, a basis of for each . Similarly, consider including, as row vectors, a basis of for each . Suppose that they are positioned in the latter rows for and first rows for . Then, the matrices are simultaneously block-triangularized, as in the right of Figure 1. We call a DM-decomposition222The classical DM-decomposition restricts to coordinate subspaces and to the sublattice of the coordinate subspaces maximizing , where are chosen as permutation matrices. In this setting, a block-triangular form obtained by using the maximal chain of the whole was considered by N. Tomizawa (unpublished) in the development of principal partitions in 1970’s; see [26, Section 3]. So our decomposition may be called a DMT-decomposition, more precisely. of . When (resp. ) is restricted to span only (resp. ), it is called a coarse DM-decomposition of .

For abuse of notation, , , , and also denote the index sets of the corresponding rows and columns of . Define ordered partitions of , of and their refinements , by

| (4.23) | |||

| (4.24) |

Let denote the matrix tuple of block-diagonal matrices obtained from by replacing each (upper) off-diagonal block with zero block. We call a diagonalized DM-decomposition of . A diagonalized version of a coarse DM-decomposition is defined analogously.

Let and . By convexity of , it holds

| (4.25) |

Define by

| (4.26) |

where the constant is defined by

| (4.27) |

We see from (4.25), (4.26), (4.27) that belongs to the positive Weyl chamber:

| (4.28) |

Also we observe that

| (4.29) |

Define by

| (4.30) |

where is a unitary matrix having a basis of in the last rows and is a unitary matrix having a basis of in the first rows. By using these notions, we give solutions of (A) and (B):

Theorem 4.22.

Suppose that is not -scalable.

-

(1)

is the minimum norm point of , and

-

(2)

is the unique minimizer of over , where it holds

| (4.31) |

Proof.

We first show (4.31). From the definitions of and , we have

By the last equation in (4.28), we have

On the other hand, is a coarse DM-decomposition. By (4.29), the maximum in (4.18) is attained by the index of any nonzero element in any diagonal block, and is equal to . Then .

Thus, to complete the proof, it suffices to show . ∎

Proposition 4.23.

Let be a diagonalized DM-decomposition of .

-

(1)

is exactly -scalable.

-

(2)

.

In particular, it holds .

Proof.

(1). We first show:

Claim.

is exactly -scalable.

Proof of Claim.

We can assume that is already equal to a DM-decomposition , where all , are coordinate subspaces. Suppose indirectly that is not exactly -scalable. Then, by Theorems 4.16 and 4.17, there is nontrivial such that . Then belongs to . However, goes beyond or lies on the interior of the segment between and . The former case is obviously impossible. The latter case is also impossible due to the maximality of chain in . ∎

For each , we can choose scaling matrices to make an exact -scaling, where . Then, for , , the scaling is a desired -scaling.

(2). Let be a DM-decomposition of , where . For , define and by

Then we see

where converges to zero for . This implies that . Since admits an exact -scaling and , we have . ∎

Now the sequence of the scaled matrix along the gradient flow/descent accumulates to the -orbit of a diagonalized DM-decomposition , providing a solution of (C):

Theorem 4.24.

Let be a diagonalized DM-decomposition of , and let be a -scaling of .

-

(1)

converges to a point in .

-

(2)

accumulates to points in .

Proof.

It holds . Thus attains the infimum of over , which is also the limit of and . By second Ness uniqueness theorem (Theorem 4.14), we have the claim. ∎

In particular, and converge/accumulate to for a -scaling , , . Although is also a diagonalized DM-decomposition of , it is not clear how to remove the unitary indeterminacy and to extract the DM-structure of . This is possible for the coarse DM-structure as follows:

Theorem 4.25.

Let be the solution of (4.19). Decompose and , where and are unitary matrices, and and are nondecreaing and nonincreasing vectors, respectively.

-

(1)

.

-

(2)

accumulates to coarse DM-decompositions.

-

(3)

accumulates to diagonalized coarse DM-decompositions, which are -scalings.

Proof.

We are going to show that becomes block-diagonalized along the coarse DM-structure in limit. We first note

| (4.32) |

where we used for the first equality, and (4.31) for the second. For any index with , by (1) and (4.29), it holds , and hence

| (4.33) |

Namely, all upper triangular blocks of converge to zero. From the fact that becomes -scalings in limit, all lower triangular blocks necessarily converge to zero, implying (3):

This convergence can be seen from the following observation on a block-triangular matrix:

and imply .

By (4.33) and for with , all lower-triangular blocks of must converge to zero, implying (2). ∎

For the discrete setting, we only give a weaker, but still meaningful, result as follows:

Theorem 4.26.

Let be the solution of (4.20). Decompose and , where and are unitary matrices, and and are nondecreaing and nonincreasing vectors, respectively.

-

(1)

.

-

(2)

accumulates to coarse DM-decompositions. The convergence is linear in the following sense: There are , such that for all , it holds

Proof.

(2). By Theorems 3.7 and 4.22 and Proposition 3.9 (1), it holds

| (4.34) |

where the second equality follows from a well-known argument of Cesáro mean.

Since we have

Suppose that is in a lower-triangular block. By (1) and (4.34), converges to positive value . Therefore, for some and , it holds for all . Then for all . ∎

The same property (3) in Theorem 4.25 for is expected to hold by our numerical experiment but could not be proved due to the lack of the convergence guarantee of . We end this subsection with some implications of these results.

On finding an unstable 1-PSG.

Suppose that is not -scalable. Consider mapped to the extreme point of with the property that it maximizes among all extreme points maximizing . The subspace pair violates (iii) in Theorem 4.16 and is a special certificate of unscalability, which is called dominant [17]. By Theorem 4.26 (2), after a large number of iterations, the last rows of and the first rows of become bases of an -approximate dominant subspace in the sense that for all and all unit vectors . Franks, Soma, and Goemans [17] established a procedure to round such an -approximate dominant subspace into the exact dominant subspace , where is a polynomial and is the bit-complexity of . Hence, if we would establish global linear convergence in (2), a polynomial number of iterations of the gradient descent (4.20) would suffice to recover the dominant subspace and an unstable 1-PSG.

Matrix scaling case.

An matrix is viewed as a matrix tuple . Consider the left-right action to , in which the group is restricted to the subgroup consisting of diagonal matrices. The corresponding scaling problem is nothing but the matrix scaling problem of nonnegative matrix ; see Section 3.3. The above results are also applicable to this setting. Indeed, the gradient is a pair of diagonal matrices. The trajectory of the gradient flow/descent is also diagonal in , and equal to the one for the geometric programming objective (3.24) in matrix scaling. Then, all subspaces are coordinate subspaces. Hence a DM-decomposition is obtained by row and column permutations, and is equivalent to the original (extended) DM-decomposition of . In Theorem 4.26, unitary matrices are permutation matrices, and all lower-triangular blocks become zero blocks after finitely many iterations. In particular, the expected convergence in Theorem 4.26 is true. This convergence property is almost the same as the one for Sinkhorn algorithm. Indeed, [26] showed that ths limit (Sinkhorn limit) oscillates between the -scaling and -scaling of .

On the limit of operator Sinkhorn algorithm.

This suggests an expectation of limiting behavior of the operator Sinkhorn algorithm (Gurvits’ algorithm), the standard algorithm for the operator scaling problem. The operator Sinkhorn algorithm is viewed as alternating minimization of , where each step scales with and with alternatively. When it is applied to the -scaling , the resulting scaling sequence oscillates between a -scaling and -scaling of . With the view of Theorem 4.24 and the matrix scaling case above, it is reasonable to conjecture that it oscillates between orbits and , where (resp. ) is a -scaling (resp. -scaling) of .

4.3 Kronecker form of a matrix pencil

Finally we discuss a special case of , i.e., . In this case, is naturally identified with matrix pencil , where is an indeterminate. Here we reveal a connection to the Kronecker canonical form of , and suggest a new numerical method for finding the Kronecker structure based on the gradient descent.

The pencil is called regular if and for some . Otherwise, the pencil is called singular. For simplicity, we assume (again) that and . The Kronecker form is a canonical form of a (singular) pencil under transformations for and . The standard reference of the Kronecker form is [18, Chapter XII]; see also [38, Section 5.1.3] for its importance on system analysis. For a positive integer , define matrix by

Theorem 4.27 (Kronecker form; [18, Chapter XII]).

There are such that

| (4.35) |

where is a regular pencil, and , are positive integers determined as follows:

-

•

is the minimum degree of a polynomial vector in that is linearly independent from over .

-

•

is the minimum degree of a polynomial vector in that is linearly independent from over .

The indices , called the minimal indices, are uniquely determined. If and is singular, then the Kronecker form has a zero block with sum of row and column sizes greater than . Therefore, by Theorem 4.16, we have:

Corollary 4.28.

A pencil is regular if and only if and is -scalable.

We point out a further connection that the Kronecker form in the arrangement of (4.35) is viewed as almost a DM-decomposition in our sence. Let denote the number of diagonal blocks of in (4.35). For , let and denote the row and column index sets, respectively, of the -th diagonal block of . Define by the vector subspace spanned by the rows of of indices in . Similarly, define by the vector subspace spanned by the rows of having indices in . We let (and . Suppose that exists and is an upper-triangular matrix. Let denote the vector space spanned by the rows of having the last indices in , and let denote the vector space spanned by the rows of having the first indices in . Let and , where is the direct sum. Consider all indices with , and suppose that they are ordered as .

Proposition 4.29.

-

(1)

is the coarse DM-flag of .

-

(2)

Suppose that is an upper-triangular pencil. Then the union of and is a DM-flag of .

Proof.

(1). Suppose that consists of for , arranged as in (4.22). We show for . Consider the convex hull of and for all . Then belongs to , and the maximal faces of are composed of the line segments connecting points from to with bending points .

We show by the induction on the number of diagonal blocks. Consider the base case where the Kronecker form consists of a single block. It suffices to show . Suppose that is an regular pencil . By regularity, there is no with (otherwise is singular over ). This means no point in beyond the line segment between and . Therefore, we have . Suppose that . Suppose to the contrary that there is with . By basis change, we may assume that

where is the zero matrix for . By and , is a pencil of row and columns with . Then contains a polynomial vector with degree at most ; use Cramer’s formula to see this. Necessarily also has such a polynomial vector. This is a contradiction to Theorem 4.27 (). The case is similar.

Consider a general case of . We can choose such that , , and the line segment between and meets with only at . Consider and . By the construction and (4.21), one of and is outside of . Suppose that . Consider submatrix , that is also a Kronecker form with a smaller number of blocks. From , , and , it necessarily holds . However, this is a contradiction to the inductive assumption. The case is similar; consider sub-Kronecker form .

(2). Observe that all integer points in the maximal faces of are obtained by the images of and . This implies that is a maximal chain of . ∎

The matrix pencil corresponding to a coarse DM-decomposition is particularly called a coarse Kronecker triangular form. This is a refinement of a quasi-Kronecker triangular form in [6] and generalized Schur form in [14, 45] if are unitary and is triangular.

Theorem 4.30 (Convergence to a coarse Kronecker triangular form).

A coarse Kronecker triangular form is enough for determining the structure of the Kronecker form. Indeed, each (non-square) rectangular diagonal block is a or matrix for some integers , from which all minimal indices , can be identified.

The above theorem suggests an iterative method for determining the minimal indices of a singular pencil, which is based on the simple gradient descent and is conceptually different from the existing algorithms, e.g., [14, 45]. It is an interesting future direction to develop a numerically stable algorithm based on our results.

Acknowledgments

We thank Shin-ichi Ohta, Harold Nieuwboer, and Michael Walter for discussion, We also thank Taihei Oki and Tasuku Soma for comments and Shun Sato for suggesting [43]. The first author was supported by JSPS KAKENHI Grant Number JP21K19759.

References

- [1] Z. Allen-Zhu, A. Garg, Y. Li, R. Oliveira, and A. Wigderson. Operator scaling via geodesically convex optimization, invariant theory and polynomial identity testing. In Proceedings of the 50th Annual ACM SIGACT Symposium on Theory of Computing, STOC 2018, pages 172–181. ACM, 2018.

- [2] F. Alvarez, J. Bolte, and O. Brahic. Hessian Riemannian gradient flows in convex programming. SIAM J. Control Optim., 43(2):477–501, 2004.

- [3] A. Auslender. How to deal with the unbounded in optimization: theory and algorithms. Math. Programming, 79(1-3):3–18, 1997.

- [4] M. Bačák. Convex Analysis and Optimization in Hadamard Spaces. De Gruyter, Berlin, 2014.

- [5] A. Beck. First-Order Methods in Optimization. Society for Industrial and Applied Mathematics, Philadelphia, PA, 2017.

- [6] T. Berger and S. Trenn. The quasi-Kronecker form for matrix pencils. SIAM J. Matrix Anal. Appl., 33(2):336–368, 2012.

- [7] N. Boumal. An Introduction to Optimization on Smooth Manifolds. Cambridge University Press, Cambridge, 2023.

- [8] M. R. Bridson and A. Haefliger. Metric Spaces of Non-Positive Curvature. Springer-Verlag, Berlin, 1999.

- [9] P. Bürgisser, C. Franks, A. Garg, R. Oliveira, M. Walter, and A. Wigderson. Efficient algorithms for tensor scaling, quantum marginals, and moment polytopes. In 59th IEEE Annual Symposium on Foundations of Computer Science, FOCS 2018, pages 883–897, 2018.

- [10] P. Bürgisser, C. Franks, A. Garg, R. Oliveira, M. Walter, and A. Wigderson. Towards a theory of non-commutative optimization: geodesic 1st and 2nd order methods for moment maps and polytopes. In 60th IEEE Annual Symposium on Foundations of Computer Science, FOCS 2019, pages 845–861, 2019.

- [11] P. Bürgisser, Y. Li, H. Nieuwboer, and M. Walter. Interior-point methods for unconstrained geometric programming and scaling problems. arXiv:2008.12110, 2020.

- [12] P.-E. Caprace and A. Lytchak. At infinity of finite-dimensional CAT(0) spaces. Math. Ann., 346(1):1–21, 2010.

- [13] X. Chen and S. Sun. Calabi flow, geodesic rays, and uniqueness of constant scalar curvature Kähler metrics. Ann. of Math. (2), 180(2):407–454, 2014.

- [14] J. Demmel and B. K\aragström. The generalized Schur decomposition of an arbitrary pencil : robust software with error bounds and applications. I. Theory and algorithms. ACM Trans. Math. Software, 19(2):160–174, 1993.

- [15] A. L. Dulmage and N. S. Mendelsohn. Coverings of bipartite graphs. Canadian J. Math., 10:517–534, 1958.

- [16] C. Franks. Operator scaling with specified marginals. In Proceedings of the 50th Annual ACM SIGACT Symposium on Theory of Computing (STOC), pages 190–203. ACM, New York, 2018.

- [17] C. Franks, T. Soma, and M. X. Goemans. Shrunk subspaces via operator Sinkhorn iteration. In Proceedings of the 2023 Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), pages 1655–1668. SIAM, Philadelphia, PA, 2023.

- [18] F. R. Gantmacher. The Theory of Matrices. Vols. 1, 2. Chelsea Publishing Co., New York, 1959.

- [19] A. Garg, L. Gurvits, R. Oliveira, and A. Wigderson. Algorithmic and optimization aspects of Brascamp-Lieb inequalities, via operator scaling. Geom. Funct. Anal., 28(1):100–145, 2018.

- [20] A. Garg, L. Gurvits, R. Oliveira, and A. Wigderson. Operator scaling: theory and applications. Found. Comput. Math., 20(2):223–290, 2020.

- [21] A. Garg and R. Oliveira. Recent progress on scaling algorithms and applications. Bull. Eur. Assoc. Theor. Comput. Sci. EATCS, (125):14–49, 2018.

- [22] V. Georgoulas, J. W. Robbin, and D. A. Salamon. The Moment-Weight Inequality and the Hilbert-Mumford Criterion—GIT from the Differential Geometric Viewpoint, volume 2297 of Lecture Notes in Mathematics. Springer, Cham, 2021.

- [23] V. Guillemin and S. Sternberg. Convexity properties of the moment mapping. II. Invent. Math., 77(3):533–546, 1984.

- [24] L. Gurvits. Classical complexity and quantum entanglement. J. Comput. System Sci., 69(3):448–484, 2004.

- [25] M. Hamada and H. Hirai. Computing the nc-rank via discrete convex optimization on spaces. SIAM J. Appl. Algebra Geom., 5(3):455–478, 2021.

- [26] K. Hayashi, H. Hirai, and K. Sakabe. Finding Hall blockers by matrix scaling. Mathematics of Operations Research. to appear.

- [27] H. Hirai. Convex analysis on Hadamard spaces and scaling problems. Foundation of Computational Mathematics. to appear.

- [28] H. Hirai, H. Nieuwboer, and M. Walter. Interior-point methods on manifolds: theory and applications. In 64th IEEE Annual Symposium on Foundations of Computer Science, FOCS 2023, pages 2021–2030. IEEE, 2023.

- [29] J.-B. Hiriart-Urruty and C. Lemaréchal. Fundamentals of Convex Analysis. Springer-Verlag, Berlin, 2001.

- [30] H. Ito, S. Iwata, and K. Murota. Block-triangularizations of partitioned matrices under similarity/equivalence transformations. SIAM J. Matrix Anal. Appl., 15(4):1226–1255, 1994.

- [31] G. Ivanyos, Y. Qiao, and K. V. Subrahmanyam. Non-commutative Edmonds’ problem and matrix semi-invariants. Comput. Complex., 26(3):717–763, 2017.

- [32] G. Ivanyos, Y. Qiao, and K. V. Subrahmanyam. Constructive non-commutative rank computation is in deterministic polynomial time. Comput. Complex., 27(4):561–593, 2018.

- [33] M. Kapovich, B. Leeb, and J. Millson. Convex functions on symmetric spaces, side lengths of polygons and the stability inequalities for weighted configurations at infinity. J. Differential Geom., 81(2):297–354, 2009.

- [34] A. Karlsson and G. A. Margulis. A multiplicative ergodic theorem and nonpositively curved spaces. Comm. Math. Phys., 208(1):107–123, 1999.

- [35] B. Kleiner and B. Leeb. Rigidity of invariant convex sets in symmetric spaces. Invent. Math., 163(3):657–676, 2006.

- [36] T. C. Kwok, L. C. Lau, and A. Ramachandran. Spectral analysis of matrix scaling and operator scaling. SIAM J. Comput., 50(3):1034–1102, 2021.

- [37] U. F. Mayer. Gradient flows on nonpositively curved metric spaces and harmonic maps. Comm. Anal. Geom., 6(2):199–253, 1998.

- [38] K. Murota. Matrices and Matroids for Systems Analysis. Springer-Verlag, Berlin, 2000.

- [39] W. T. Obuchowska. On the minimizing trajectory of convex functions with unbounded level sets. Comput. Optim. Appl., 27(1):37–52, 2004.

- [40] S. Ohta and M. Pálfia. Discrete-time gradient flows and law of large numbers in Alexandrov spaces. Calc. Var. Partial Differential Equations, 54(2):1591–1610, 2015.

- [41] R. T. Rockafellar. Convex Analysis. Princeton University Press, Princeton, NJ, 1970.

- [42] T. Sakai. Riemannian Geometry. American Mathematical Society, Providence, RI, 1996.

- [43] J. M. Sanz Serna and K. C. Zygalakis. Contractivity of Runge-Kutta methods for convex gradient systems. SIAM J. Numer. Anal., 58(4):2079–2092, 2020.

- [44] R. Sinkhorn. A relationship between arbitrary positive matrices and doubly stochastic matrices. Ann. Math. Statist., 35:876–879, 1964.

- [45] P. Van Dooren. The computation of Kronecker’s canonical form of a singular pencil. Linear Algebra Appl., 27:103–140, 1979.

- [46] C. T. Woodward. Moment maps and geometric invariant theory. arXiv:0912.1132, 2011.

Appendix A Proof of Proposition 4.10

Identify with tangent space of at , and define the right-invariant Riemannian metric on by for . Here we consider the following version of the Kempf-Ness function :

| (A.1) |

Lemma A.1.

-

(1)

.

-

(2)

; see [22, Theorem 4.1(i)].

-

(3)

Proof.

(1) is obvious. (2). For , it holds

(3). For , it holds

∎

Lemma A.2 (see [22, Theorem 4.1(ii)]).

For , define map by . Then it holds

Proof.

The infinitesimal action of at is denoted by . By definition of the moment map, for , , and , it holds

where is the complex structure and is the symplectic form on . By taking , it holds

In particular, . On the other hand, it holds

Letting and , we have the claim. ∎

Lemma A.3.

For , define map by . Then it holds

Proof.

Thus, for the solution of (4.6), satisfies