Estimation and Inference for

Three-Dimensional Panel Data Models

††An earlier version of this paper has been circulated and submitted to working paper series under the title “Multi-Level Panel Data Models: Estimation and Empirical Analysis”, which is available at https://ideas.repec.org/p/msh/ebswps/2022-4.html.

Gao and Peng would like to acknowledge the Australian Research Council Discovery Projects Program for its financial support under Grant Numbers: DP200102769 & DP210100476. Liu’s research is financially supported by the National Natural Science Foundation of China under Grant No. 72203114.∗University of North Texas, United States. †Monash University, Australia. ♯Nankai University, China.

Guohua Feng∗, Jiti Gao†, Fei Liu♯ and Bin Peng†

Hierarchical panel data models have recently garnered significant attention. This study contributes to the relevant literature by introducing a novel three-dimensional (3D) hierarchical panel data model, which integrates panel regression with three sets of latent factor structures: one set of global factors and two sets of local factors. Instead of aggregating latent factors from various nodes, as seen in the literature of distributed principal component analysis (PCA), we propose an estimation approach capable of recovering the parameters of interest and disentangling latent factors at different levels and across different dimensions. We establish an asymptotic theory and provide a bootstrap procedure to obtain inference for the parameters of interest while accommodating various types of cross-sectional dependence and time series autocorrelation. Finally, we demonstrate the applicability of our framework by examining productivity convergence in manufacturing industries worldwide.

Keywords: Asymptotic Theory, Bias Correction, Dependent Wild Bootstrap, Hierarchical Model

JEL classification: C23, O10, L60

1 Introduction

In the past three decades or so, panel data research has undergone significant advancements, leveraging its capacity to extract richer insights from both cross-sectional and time dimensions. Within this domain, a notable strand of research (Bai, 2009; Fan et al., 2016) has garnered increasing attention, with a particular focus on addressing cross-sectional dependence (CSD) in large and settings by accounting for correlations among observations across different entities within a panel. Specifically, strong CSD is often addressed through a factor structure approach involving the estimation of a low-rank representation, while weak CSD poses inference challenges related to estimating the asymptotic covariance matrix. Additionally, accounting for time series autocorrelation (TSA) is essential when analyzing data with a temporal dimension. To tackle both CSD and TSA jointly, various methods have been proposed in the relevant literature. For instance, Gonçalves (2011) suggests using the moving block bootstrap method, Bai et al. (2020) employ a thresholding method in conjunction with a heteroskedasticity and autocorrelation-consistent (HAC) covariance matrix estimator, and Gao et al. (2023) consider a dependent wild bootstrap procedure, extending the time series approach of Shao (2010) to a high-dimensional time series framework.

Recent developments in panel data research, especially in contexts where observations exhibit hierarchical structures, have led to the emergence of the relevant literature on hierarchical panel data models (Matyas et al., 2017; Chen et al., 2022; Jin et al., 2023; Zhang et al., 2023). This evolution reflects the recognition of the necessity to extend beyond traditional panel data models to capture dependencies at multiple levels of aggregation, such as individuals nested within groups or regions nested within countries. Consequently, the literature on hierarchical panel data models builds upon and extends methodologies developed in the cross-sectional dependence literature to accommodate these hierarchical structures, ultimately enabling researchers to more accurately model and analyze complex panel datasets.

Another pertinent literature is regression with incidental parameters, a concept pioneered by Neyman and Scott (1948). Lancaster (2000) commends their seminal paper as a remarkable contribution, widely acknowledged for its influence within the statistical community. To see the challenges posed by incidental parameters in the context of 3 dimensional (3D) panels, we present the following table outlining the potential incidental parameters across different data structures:

While a 3D panel involves only one additional layer, it significantly increases complexity. To the best of our knowledge, no prior studies have attempted to integrate all potential specifications of incidental parameters into a single regression model. Hence, a unified framework is needed. Fortunately, incidental parameters can be integrated using a factor structure. For example, all four conceivable scenarios of a 2D panel can fit within a structure such as . This approach offers valuable insights into addressing the challenge of 3D panel data modeling.

With the above challenges in mind, the primary objective of this study is to contribute to the literature on hierarchical panel data models by introducing a panel data regression model with three sets of latent factor structures: one set of global factors and two sets of local factors. Compared with pure factor models, this model is capable of estimating the coefficient of a particular observed independent variable while accounting for both commonalities and individual differences across entities. In addition, in comparison with panel data regression models with only one or two sets of factors, the proposed model and estimation theory is capable to model dependencies that exist at multiple levels of aggregation. This model finds applications in various contexts. For example, in the context of modeling economic convergence, the latent global factors represent economic events affecting the growth of all countries and industries, while the two local factors represent events affecting specific countries or industries, respectively. In the context of modeling international trade, the latent global factors represent factors affecting the trade of all countries, while the two local factors represent events affecting importing or exporting countries, respectively.

To better understand the 3D factor structure, suppose that we have two groups of individuals:

(1.1)

where and are two positive integers, and for any positive integer . In the literature of modeling empirical growth (e.g., Rodrik, 2013), represents industries, and denotes countries; in the context of bilateral trade (e.g., Chen et al., 2022), and respectively represent importing countries and exporting countries; in the stochastic actor-oriented models (e.g., Koskinen and Snijders, 2023), refers to social groups and refers to individuals within each group; etc. In addition, we let denote a set of outcome variables:

(1.2)

which is indexed by both and , and also varies over each time period . The definition of should be self-evident in the aforementioned studies, so we omit these details here. Throughout this paper, we assume that each layer of information is influenced by distinct factors, enabling us to extract essential insights through careful data processing. While akin to the concept of distributed PCA (Fan et al., 2019), our approach diverges in that we aim to disentangle factors layer by layer and across different blocks within each layer, rather than consolidating factors from disparate nodes.

For a clearer grasp of the 3D factor structure, we visually represent the three sets of latent factors (, , and ) in Figure 1, utilizing empirical growth data as a demonstration.

Figure 1: Different Factors of the Hierarchy

Specifically, , and represent , , and vectors respectively, denoting the global, country-specific, and industry-specific factors or shocks driving . Here, , , and are non-negative fixed integers, subject to the constraint:

(1.3)

where is a fixed positive constant. This condition implies that , , and can potentially be 0. In an extreme scenario, if behaves entirely randomly like an idiosyncratic error, then for all pairs. Figure 1 illustrates that influences every industry and country, while each country-specific (or industry-specific) shock can also impact a specific subset of countries or industries. Mathematically, for all , Figure 1 reveals the following mapping:

(1.4)

where , , and are factor loadings indicating how each factor influences at each time period . Figure 1, along with the restriction (1.3) and the mapping (1.4), together entail the following observations:

1.

Figure 1, the restriction (1.3), and the mapping (1.4) encompass all possible combinations of incidental parameters.

2.

The global shock (if exists) affects all countries and industries, while the country and industry shocks ( and ) respectively impact a specific subset of countries or industries.

3.

From the a signal-to-noise ratio point of view, can be recovered by aggregating all available information, whereas and can be identified block by block.

4.

The dimensions and exhibit symmetry, despite potential differences in the values of and .

Finally, to accommodate potential endogeneity, we posit that the unobservable factors exert influence on regressors, subject to less restrictive conditions (refer to Remark 2.1 and Assumption 1 for more details). Further elaboration on this aspect will be provided when detailing the model setup and associated conditions in Section 2. Our objective is twofold: to estimate the coefficients of these endogenous regressors and to discern factors across various levels or blocks of the hierarchy.

Concluding this section, we summarize our contributions as follows. In addition to the introduction of a panel data regression model featuring three sets of latent factor structures, this study also provides additional contributions in the following areas:

1.

We propose an estimation method to recover the parameters of interest and unobservable factors across levels and blocks of the hierarchy, and establish its asymptotic properties.

2.

The unified hierarchy structure in a 3D framework covers the total 64 possibilities of incidental parameters which have been the center of a wide range of applications since Neyman and Scott (1948).

3.

We provide a bootstrap procedure to obtain inferences for the parameters of interest, accommodating various types of cross-sectional dependence (CSD) and time series autocorrelation (TSA) within the data generating process of the hierarchy.

4.

To validate our theoretical findings, we conduct extensive simulations and analyze real data examples. In the empirical study, we specifically utilize data from manufacturing industries at the ISIC two-digit level to examine the twin hypotheses of conditional and unconditional convergence for manufacturing industries across countries.

The rest of the paper is organized as follows. Section 2 presents our model and methodology. An asymptotic theory is established accordingly for each step involved in different estimation procedures. Section 3 conducts extensive numerical studies to examine the theoretical findings. Specifically, Section 3.1 examines the theoretical findings using extensive simulations, while Section 3.2 uses a set of data from manufacturing industries at the ISIC two-digit level to examine the twin hypotheses of conditional and unconditional-convergence for manufacturing industries across countries. Section 4 concludes. Key assumptions with their justifications are given in Appendix A. In the online supplementary Appendix B, Appendix B.2 provides two detailed numerical implementations; Appendix B.3 includes the necessary preliminary lemmas; Appendix B.4 presents the detailed proofs; some additional estimation results of the empirical study are reported in Appendix B.1.

Before proceeding further, it is convenient to introduce some notations that will be repeatedly used throughout the article. Vectors and matrices are always written in bold font. For a matrix , and denote the Frobenius norm and the spectral norm of , respectively, and stands for the transpose of . Provided that has full column rank, let with . For two block wise matrices and , provided is well defined, we let define the block wise Hadamard product, i.e., . Also, we let return a diagoal matrix with and on the main diagonal. For a vector , let define the norm. For two scalars and , , . For two random variables and , stands for and . represents the conventional indicator function, and “” and “” stand for convergence in probability and convergence in distribution respectively. and stand for the expectation and probability induced by the bootstrap procedure.

2 Model & Methodology

In this section, we will introduce our panel data regression model featuring three sets of latent factor structures, outline a method for estimating the model, and establish its asymptotic properties. Before delving into the specifics of our model, we wish to emphasize two crucial points. Firstly, our main focus is on regressing on a vector , where is fixed. Secondly, as discussed in the introduction, we hypothesize that the unobservable factors impact the regressors to address potential endogeneity. With this consideration, our panel data regression model with three sets of latent factor structures is formulated as follows:

(2.1)

where and every quantity on the right hand side of (2.1) are unknown, and with can all be large. Our goal is to infer , and to recover the spaces spanned by the three sets of unobservable factors. For the time being, we assume that , ’s and ’s are known, and we will address their estimation in Section 2.3. The setup connects with the existing works, such as Ando and Bai (2017) and Jin et al. (2023), by addressing many challenges of the relevant literature within one framework.

We now rewrite the main equation (i.e., the upper equation) of (2.1) in vector form as follows:

(2.2)

where

Remark 2.1.

We refrain from expressing in matrix form at this stage, as we aim to minimize constraints on , and as much as possible. These parameters may even exhibit characteristics akin to weak factor loadings, as observed in Uematsu and Yamagata (2023). If the focus is about the structure of only, and we refer interested readers to Jin et al. (2023) for a comprehensive investigation on the factor structure without regressors.

According to (2.1) and (2.2), it is reasonable to assume that for

(2.4)

has full column rank. Otherwise, one can always reorganize the unobservable factors to achieve a representation with full column rank.

Remark 2.2.

If is observable, we can immediately rewrite (2.2) as

(2.5)

which enables consistent estimation for using the OLS method. For the case with unobservable , a very intuitive idea following a typical two dimensional panel data approach (such as Ando and Bai, 2017) is to consider an objective function in the following form:

(2.6)

where each is a generic matrix satisfying . One would hope to obtain the estimates of and by combining the quantity of (2.6) over . However, the restriction simply cannot be fulfilled practically. To illustrate this, suppose we consider a fixed . Then allow us to generate a set of . Once moving on to a different , will generate another set of . In general, and are not necessarily the same unless (1): ; and (2): and are generated from two orthogonal spaces from the perspective of vector multiplication. However, it rules out the most common restriction, such as .

To tackle the problem raised in Remark 2.2, we put our thoughts in a nutshell below. For simplicity, suppose that as

(2.7)

which does not lose any generality, as it is only a matter of rotating matrices in view of the factor structure admitting the following expression:

(2.8)

in which . Lemme B.2 of the online supplement shows the feasibility of (2.7) when taking over . By (2.7), simple algebra shows that

(2.9)

in which the representation automatically separates , , and , and also serves as a projection matrix asymptotically. Thus, (2.9) sheds light on how to recover , , and within a single framework. We are now ready to proceed.

2.1 Estimation Procedure

We start by introducing a set of new symbols. Let , , and be some generic matrices each sharing the same dimensions with , , and respectively. We define

(2.10)

Similar to and , we define and Also, let be a generic matrix with dimensions matching .

Using these symbols, we introduce the following objective function:

(2.11)

where , and the following conditions hold:

(2.12)

Remark 2.3.

The first three conditions of (2.12) are standard in the literature. The last condition essentially requires and . Rather than labeling it as a constraint, it merely dictates the sequence of calculations when minimizing .

Consider as an example. Minimizing with respect to is equivalent to maximizing the following quantity:

(2.13)

where the equality holds because of . Equation (2.13) implies that in order to obtain the estimates of and , one should project out the estimate of firstly, which is automatically taken into account in view of (2.11) and (2.13).

Having explained the above points, we outline our estimation procedure below.

Step 1

Perform the following optimization:

(2.14)

where and . Here, (2.14) can be decomposed as follows:

1.

where ;

2.

, where includes the largest eigenvalues of , and

3.

For , , where includes the largest eigenvalues of , and

4.

For , , where includes the largest eigenvalues of , and

Step 2

Finally, update the estimate of by

(2.15)

where .

The detailed numerical implementation in provided in Appendix B.2. In the next subsection, we propose the above estimation procedure, and establish the corresponding asymptotic properties.

2.2 Asymptotic Properties

For the sake of space, we present the assumptions along with their relevant discussions in Appendix A. First we show the overall consistency of the proposed approach.

The establishment of Lemma 2.1 does not require an excessive number of conditions for the variables involved in (2.1). It shows that we can recover as a whole. As expected, the global factor can be estimated firstly by putting everything together.

As shown in (1.4) and (2.13), in order to recover and , we need to divide the data into different blocks as presented in the estimation procedure, so ’s are automatically partitioned into blocks accordingly. As a consequence, we can no longer use the overall consistency of derived in Lemma 2.1. To proceed, we further impose Assumption 2, and summarize the results associated with and in Lemma 2.2 below.

Lemma 2.2 justifies the validity of our approach across all blocks involved in Step 1. With this, we have successfully recovered all key components of model (2.2), thus concluding our examination of Step 1 in the estimation procedure.

Now, we proceed to Step 2, where we delve into inferring .

Theorem 2.1.

Suppose that Assumptions 1 and 2 hold. In addition, let . As , for

where , and .

Theorem 2.1 offers an asymptotic distribution associated with each . To conduct practical inference, it’s essential to consider the time series correlation present in the term . Therefore, we adopt the dependent wild bootstrap procedure (DWB) of Shao (2010), and provide the following procedure for .

Bootstrap Procedure:

(i).

Let be an

-dependent time series for each bootstrap draw, and let the components of satisfy that

where , is a constant and defined in Assumption 2, and is a symmetric kernel defined on satisfying that and for .

(ii).

For , construct a new set of dependent

variables by , where . Accordingly, the new estimate of is obtained using

(iii).

We repeat the above procedure times.

Theorem 2.2.

Let the conditions of Theorem 2.1 hold. Assume further that and , where , , and is defined in Assumption 2.

As , for

Theorem 2.2 provides a procedure to recover the asymptotic distribution for each given . It is worth mentioning that the DWB method is initially introduced in Shao (2010) in the context of time series analysis, wherein a comprehensive comparison between the DWB and some existing bootstrap methods can be found.

2.3 Selection of the Numbers of Factors

To conclude our theoretical investigation, we provide a procedure to select the numbers of factors. For notational simplicity, we define and Thus, our goal is to estimate , , and .

First, we emphasize that we can still get consistent estimation of by prescribing a to be the numbers of global, country and industry factors. As long as , the estimation procedure of Section 2.1, and the results developed in Section 2.2 still hold true. In connection with the estimation procedure of Section 2.1, we provide the following steps to estimate firstly, and then estimate the elements of and sequentially.

Step 1*

Prescribe a to be the numbers of global, country and industry factors, and implement the estimation procedure of Section 2.1 to obtain .

Step 2*

Using , we calculate as in Section 2.1, and estimate the number of global factors as follows:

(2.16)

where , is a mock eigenvalue, and stands for the largest eigenvalue of . Record the eigenvectors corresponding to the largest eigenvalues in .

Step 3*

Having obtained and , we sequentially estimate ’s and ’s as follows:

(2.17)

where are mock eigenvalues, and and stand for the -th largest eigenvalues of and respectively.

The estimators in (2.16) and (Step 3*) can be considered as extensions of Lam and Yao (2012). However, as pointed out by Lam and Yao (2012), it remains unresolved to bound the ratio associated with the eigenvalues which converge to 0 from below. To bypass this unresolved issue, we introduce a data driven tuning parameter . The idea is that although it is challenging to study a ratio with a denominator converging to 0, we can discard this ratio and construct a V-shape curve by employing the indicator function in (2.16) and (Step 3*), respectively.

Up to this point, we have successfully recovered all the unknown quantities as mentioned in the beginning of Section 2. In the next section, we examine the above theoretical results using extensive simulations.

Remark 2.4.

To conclude this section, we note that practically it is not guaranteed that each country (or industry) has the same number of individuals, so it brings certain unbalanceness to the data set. Formally, , we may have , which is exactly the same as our empirical study of Section 3.2. After carefully checking the proofs, we can see that as long as and , all the aforementioned results are still valid with certain modifications.

3 Numerical Studies

In this section, we conduct extensive numerical studies to examine the theoretical findings. Specifically, Section 3.1 examines the theoretical findings using extensive simulations, while Section 3.2 uses a set of data from manufacturing industries at the ISIC two-digit level to examine the twin hypotheses of conditional and unconditional-convergence for manufacturing industries across countries.

3.1 Simulation

In this subsection, we provide simulation studies, and the main data generating process (DGP) follows (2.1). In what follows, we provide details about each component involved.

To capture heterogeneity of the coefficients, we generate them by for , which implies . For factors and loadings, we first generate the numbers of factors. Specifically, we let , and let and be randomly selected from the set with equal probability attached to each possible outcome. The design is to show that we allow and to be 0, which is meaningful for practical analysis. Therefore, for each generated dataset, only is fixed. The values of and vary at each simulation replication.

Sequentially, we generate factors and loadings, and let them be independently drawn from some normal distributions: , if , if , , if , if , , if , if , where , , , and stand for the columns of , , and respectively. We note that normal distributions are not really necessary here, as the choice of some other distributions doesn’t affect the finite-sample performance. To present the main steps for the simulation and save the space, we do not further explore alternative options.

We generate residuals as follows:

where , with , and

in which is the element of , and . Based on the above DGP, we have weak serial correlation and cross-sectional dependence among .

Finally, we assemble ’s and ’s as in (2.1). For each dataset, we carefully calculate all the unknown quantities following the numerical implementation of Appendix B.2.

To evaluate the performance of our proposed method, we repeat the above procedure times, and define several criteria. For notational simplicity, the subindex k always stands for the corresponding quantities obtained at the replication in what follows. That said, we use root mean square errors (RMSE) to measure our estimates about , , , and :

(3.1)

where we let if , and similarly, we let , , , and if , , , and respectively. For the purpose of comparison, we estimate , , and by assuming that , , and are known, and calculate , , , and as in (3.1).

To evaluate the estimation about the numbers of factors, we define the following rates:

(3.2)

Apparently, , , and measure the percentages of correctly identifying the numbers of global, country and industry factors; , , and measure the percentages of under estimation; , , and measure the percentages of over estimation.

Finally, we evaluate the coverage rates (CR) of the bootstrap procedure. For ,

(3.3)

where stands for the element of , stands for the 95% confidence interval obtained from the bootstrap draws associated with , and and respectively stand for the elements of and obtained at the simulation replication.

We summarize results in Tables 1, 2, and 3. As and are symmetric in a sense, we alter and only in the following tables, while keeping for simplicity. We now discuss each table in details. In Table 1, as expected, as either or increases, we have improved probability of correctly identifying , , and . Even for the case , we are still able to identify different numbers of factors with probabilities greater than 70%. In Table 2, as expected, , , , and outperform , , , and respectively. However, the differences are not very significant, and gradually vanish as the sample size increases. This is not surprising, as we have better probabilities to identify different types of factors with large sample size. As a result, it is less likely to have misspecified factor structures as the sample size increases. Table 3 reports the coverage rates of the bootstrap procedure. Overall, the numbers are very close to the nominal rate 95%, and even for . To conclude, as explained in Remark 2.2, we emphasize that the above results show our method works well for the case with .

Table 1: Selection of Factor Numbers

60

60

60

0.702

0.000

0.298

0.709

0.219

0.072

0.764

0.165

0.071

120

0.956

0.000

0.044

0.902

0.063

0.035

0.941

0.029

0.029

180

0.990

0.000

0.010

0.937

0.036

0.026

0.973

0.008

0.019

120

60

0.716

0.000

0.284

0.703

0.219

0.077

0.768

0.212

0.020

120

0.946

0.000

0.054

0.887

0.072

0.042

0.954

0.043

0.003

180

1.000

0.000

0.000

0.937

0.033

0.030

1.000

0.000

0.000

Table 2: Root Mean Square Errors

60

60

60

0.270

0.207

0.694

0.332

0.335

0.582

0.842

0.587

120

0.210

0.169

0.574

0.261

0.236

0.268

0.619

0.352

180

0.191

0.159

0.533

0.233

0.209

0.189

0.559

0.283

120

60

0.277

0.197

0.726

0.298

0.310

0.569

0.872

0.558

120

0.224

0.165

0.617

0.225

0.230

0.284

0.664

0.309

180

0.201

0.154

0.566

0.195

0.203

0.154

0.584

0.196

Table 3: Coverage Rates

CR

60

60

60

0.958

120

0.930

180

0.948

120

60

0.989

120

0.943

180

0.950

3.2 An Empirical Study

The analysis of economic and productivity convergence stands as a compelling area of inquiry within economics, offering an ideal application for our hierarchical panel data model as outlined in Section 2. Specifically, starting with the seminal study by Baumol (1986), numerous studies have been devoted to testing whether income or productivity of poorer economies are converging to those of richer economies. As Durlauf (2003) puts it, “Few issues in empirical growth economics have received as much attention as the question of whether countries exhibit convergence”. A main technique employed by these studies is “cross-country growth regressions”, where aggregate- or industry-level cross-country data are used to regress the average growth rates of per capita income (or labour productivity) over a long period on the initial level of income per capita (or labour productivity) and some additional control variables111In this study we follow Rodrik (2013) and define labour productivity of an industry as the industry’s real value added divided by its number of employees. As is well known, the value added of an industry, also referred to as gross domestic product (GDP)-by-industry, is the contribution of a private industry or government sector to overall GDP (The U.S. Bureau of Economic Analysis, 2006, available at https://www.bea.gov/help/faq/184). The definitions of labour productivity and value added, therefore, imply that an industry’s labour productivity can be considered as the industry’s “GDP per capita”, which in turn implies that neoclassical growth models predict not only conditional convergence in GDP per capita among economies but also industry-level convergence in labour productivity among economies.. A negative and significant coefficient on the initial conditions is taken to be evident in favour of -convergence. For excellent surveys of cross-country convergence studies, see Durlauf (2003) for example. Despite the increasing availability of disaggregated data at industry level, the hierarchical structure of these data, to the best of our knowledge, has rarely been explored.

3.2.1 Data

We begin our empirical analysis by introducing the data. For labor productivity (or real value added per employee), we follow Rodrik (2013) and use the dataset of UNIDO’s INDSTAT2, which provides data on value added (in nominal U.S dollars) and employment for 23 manufacturing industries at the ISIC two-digit level for a large number of countries. With this dataset, real value added can be computed by deflating the nominal value added by the US producer price index, and labor productivity can then be obtained by further dividing real value added by employment (i.e., number of employees). Growth in labor productivity is then measured as percentage change in labor productivity.

Our control variables include a wide range of factors that have been found to be important for assessing convergence. These include human capital (as measured by school enrollment), investment price, trade openness and terms of trade, institutions (measured by civil liberties), and government consumption share. We refer interested readers to Sala-I-Martin et al. (2004) for detailed definitions of a wide range of variables. A summary of the dataset is given in Table B.1 and Table B.2 of the online supplement. It should be noted that since geographical factors are usually time-invariant, they will be captured by the factor structures and thus are not included in the control variables. When measuring dependent and independent variables, we follow Salimans (2012), and treat them differently. Specifically, the dependent variable is measured as a five-year moving average of economic growth, while all explanatory variables are measured at the beginning of each five year period. Due to data availability, our sample starts at 1963 and ends at 2018. For the same reason, the number of countries varies across industries.

3.2.2 Estimation Results

We now investigate conditional convergence for the manufacturing industries, which can be done by estimating equation (2.2) where all components (i.e., initial productivity, control variables and three types of factors) are included. The factor selection is achieved using the method that is described in Section 2.3.

For the global factor, we identify one factor that affects the growth in labour productivity of each country in every manufacturing industry and it accounts for 22.50% of the variations in . Panels A and B of Table A.1 present the estimated numbers of industry and country factors. As evident from the table, the number of factors varies among industries and countries, ranging from 1 to 10. These factors collectively explain 56.65% of ’s variations. Overall, the factor structure can account for approximately 80% of the variations in , indicating a superior goodness of fit for our model.

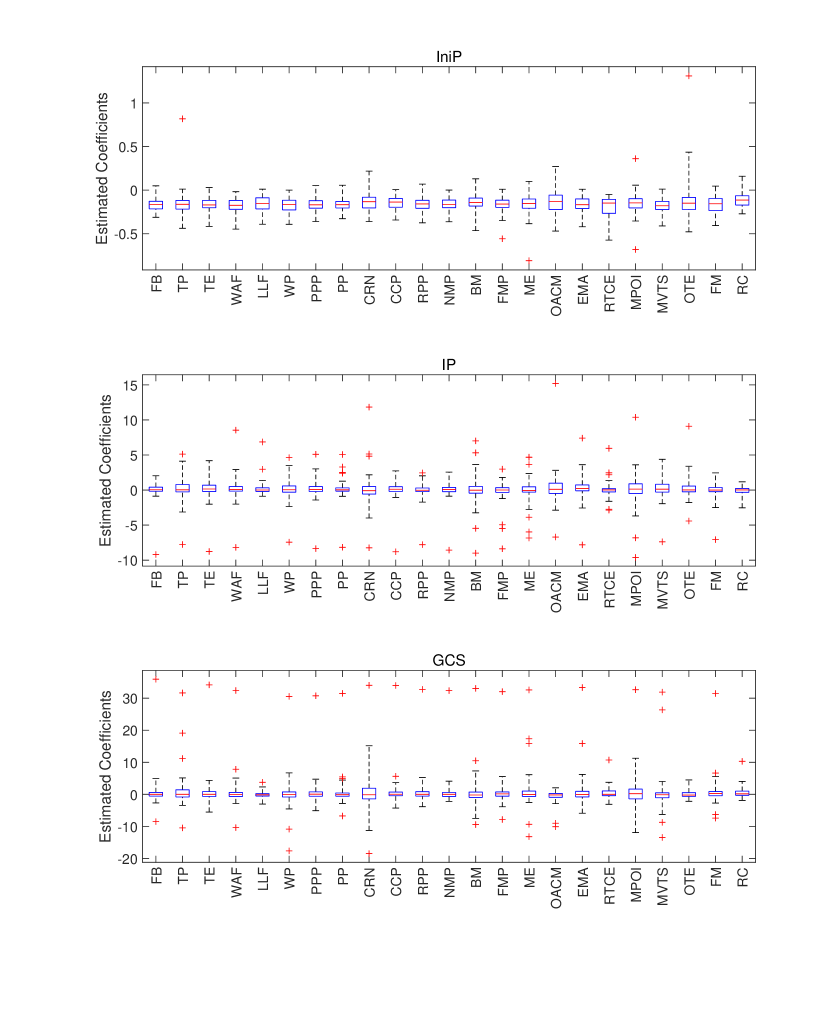

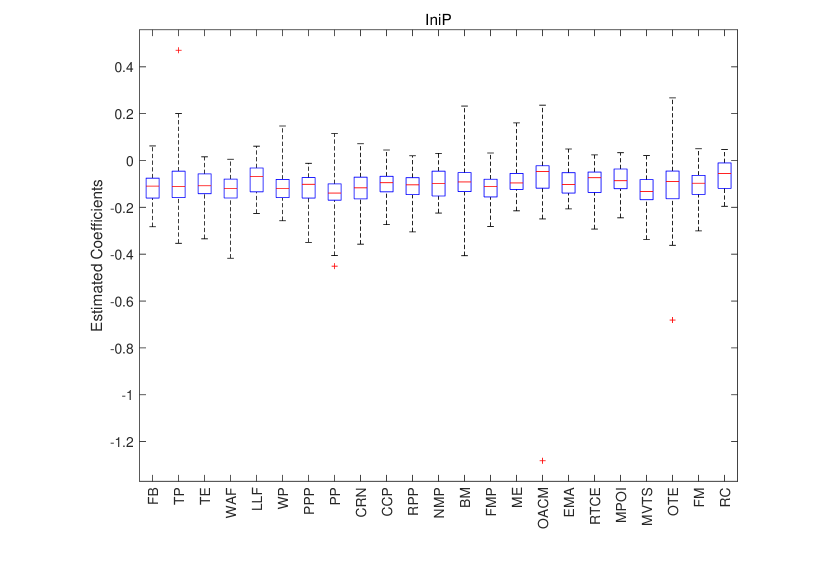

For the sake of space, Figures B.1 and B.2 of the online supplement provide the boxplots of country-specific estimated coefficients for each explanatory variable across 23 industries. To illustrate the average magnitudes of the partial effects from the initial productivity and the control variables, we calculate the the means of estimated regression coefficients along with their 95% confidence intervals. The results are reported in Panel A of Table A.2. The estimated average of partial effects for initial productivity is -0.157 and highly significant with a 95% confidence interval of (-0.161, -0.152). This suggests that when country characteristics are controlled, initial labour productivity, on average, is negatively related to the subsequent rate of growth in labour productivity. In other words, conditional convergence in labour productivity exists for the manufacturing industry as a whole. This finding is in line with that of Rodrik (2013) who, by applying a fixed effects panel data model to the UNIDO’s INDSTAT dataset, also finds conditional convergence in labour productivity for the total manufacturing industry. It is also consistent with the income convergence literature (Sala-I-Martin et al., 2004) that finds that once country characteristics are controlled for, the coefficient on initial income becomes negative and statistically significant. To show the disparity in conditional convergence of productivity among countries, we present the country-specific estimated partial effects for initial productivity within the food and beverages industry in Table A.3 as an example. Despite the consistent negative estimates across all countries, there exists significant divergence in their magnitudes. For instance, coefficients for some countries such as Albania, Croatia, and Malawi exceed -0.25, whereas the effects are substantially lower in others like Pakistan and Peru, or even insignificant as in Jordan and Syria. This finding demonstrates the importance of employing heterogeneous panel data in the examination of productivity convergence. Moreover, such country-specific variations are also present in the estimates for other industries as well as the estimated partial effects for control variables. Due to the page constraints, the corresponding results are omitted here.

In order to confirm our results regarding conditional convergence in labour productivity, we conduct two robustness checks. First, we re-estimate the model for the following three subperiods: 1973-2018, 1983-2018 and 1993-2018. The results are provided in Panels B-D in Table A.2, respectively. It is evident that the estimated average of partial effects for initial productivity remain negative and statistically significant, confirming the conditional convergence of productivity on the average level. Secondly, we follow Rodrik (2013) and exclude OCED countries from our sample of countries. The results, which are presented in Panel E of Table A.2, show that our findings of conditional convergence is very robust to the exclusion of OECD countries. Specifically, the estimated average coefficient of initial productivity is -0.160 with a 95% confidence interval of (-0.164 -0.155).

To summarize this section, we have examined the hypothesis of the conditional convergence of productivity for manufacturing industries across countries. The empirical results presented in this section suggest that there is strong and consistent evidence of convergence once factors that affect steady-state levels of labour productivity are controlled for. As comparison, we also examine the unconditional convergence of productivity by excluding the control variables. Due to the page constraint, we provide the estimation results and discussion on such issue in the online supplement.

4 Conclusion

The hierarchy of large datasets has garnered considerable attention recently (e.g., Chen et al., 2022, Jin et al., 2023, Zhang et al., 2023, along with numerous real data examples collected in Matyas et al., 2017). In this study, we contribute to the literature by proposing a panel data regression model with three sets of latent factor structures, which, to the best of our knowledge, has not been extensively explored in the existing literature. Rather than consolidating factors from various nodes, as seen in the literature of distributed PCA (Fan et al., 2019), we propose an estimation method to recover the parameters of interest by peeling off factors layer by layer and across different blocks within certain layers. We establish estimation theory and asymptotic properties accordingly. Additionally, we present a bootstrap procedure to infer the parameters of interest, allowing for different types of cross-sectional dependence (CSD) and time-series autocorrelation (TSA) in the data generating process (DGP). Finally, we validate our theoretical findings using extensive simulated and real data examples. In our empirical study, we utilize data from manufacturing industries at the ISIC two-digit level to examine the twin hypotheses of conditional and unconditional convergence for manufacturing industries across countries.

References

(1)

Ando and Bai (2017)

Ando, T. and Bai, J. (2017),

‘Clustering huge number of financial time series: A panel data approach with

high-dimensional predictors and factor structures’, Journal of the

American Statistical Association112(519), 1182–1198.

Bai (2009)

Bai, J. (2009), ‘Panel data models with

interactive fixed effects’, Econometrica77(4), 1229–1279.

Bai et al. (2020)

Bai, J., Choi, S. H. and Liao, Y. (2020), ‘Standard errors for panel data models with unknown

clusters’, Journal of Econometrics p. forthcoming.

Baumol (1986)

Baumol, W. J. (1986), ‘Productivity growth,

convergence, and welfare: What the long-run data show’, American

Economic Review76(5), 1072–1085.

Bernard and Jones (1996)

Bernard, A. and Jones, C. (1996),

‘Productivity across industries and countries: Time series theory and

evidence’, Review of Economics and Statistics78(1), 135–46.

Bosq (2012)

Bosq, D. (2012), Nonparametric

Statistics for Stochastic Processes: Estimation and Prediction, Lecture

Notes in Statistics, Springer New York.

Caselli and Coleman II (2001)

Caselli, F. and Coleman II, W. J. (2001), ‘The U.S. structural transformation and regional

convergence: A reinterpretation’, Journal of Political Economy109(3), 584–616.

Chen et al. (2022)

Chen, R., Yang, D. and Zhang, C.-H. (2022), ‘Factor models for high-dimensional tensor time

series’, Journal of the American Statistical Association117(537), 94–116.

Durlauf (2003)

Durlauf, S. N. (2003), ‘The convergence

hypothesis after 10 years’, Revista Economica de Castilla-La Mancha2, 55–74.

Fan et al. (2016)

Fan, J., Liao, Y. and Wang, W. (2016), ‘Projected principal component analysis in factor models’, Annals of

Statistics44(1), 219–254.

Fan et al. (2019)

Fan, J., Wang, D., Wang, K. and Zhu, Z. (2019), ‘Distributed estimation of principal eigenspaces’,

Annals of Statistics47(6), 3009 – 3031.

Gao (2007)

Gao, J. (2007), Nonlinear Time Series:

Semiparametric and Nonparametric Methods, Chapman and Hall.

Gao et al. (2023)

Gao, J., Peng, B. and Yan, Y. (2023), ‘Higher-order expansions and inference for panel data models’, Journal

of the American Statistical Association0(0), 1–12.

Golub and Van Loan (2013)

Golub, G. H. and Van Loan, C. F. (2013), Matrix Computations (4th Edition), The Johns

Hopkins University Press.

Gonçalves (2011)

Gonçalves, S. (2011), ‘The moving blocks

bootstrap for panel linear regression models with individual fixed effects’,

Econometric Theory27(5), 1048–1082.

Hansen (1992)

Hansen, B. E. (1992), ‘Consistent covariance

matrix estimation for dependent heterogeneous processes’, Econometrica60(4), 967–972.

Koskinen and Snijders (2023)

Koskinen, J. and Snijders, T. A. B. (2023), ‘Multilevel longitudinal analysis of social

networks’, Journal of the Royal Statistical Society Series A:

Statistics in Society186(3), 376–400.

Lam and Yao (2012)

Lam, C. and Yao, Q. (2012), ‘Factor

modeling for high-dimensional time series: Inference for the number of

factors’, Annals of Statistics40(2), 694–726.

Lancaster (2000)

Lancaster, T. (2000), ‘The incidental

parameter problem since 1948’, Journal of Econometrics95(2), 391–413.

Lu et al. (2021)

Lu, X., Miao, K. and Su, L. (2021),

‘Determination of different types of fixed effects in three-dimensional

panels’, Econometrics Reviews40(9), 867–898.

Mankiw et al. (1992)

Mankiw, N. G., Romer, D. and Weil, D. N. (1992), ‘A contribution to the empirics of economic growth’,

Quarterly Journal of Economics107(2), 407–437.

Matyas et al. (2017)

Matyas et al. (2017), The Econometrics

of Multi-dimensional Panels: Theory and Applications, Springer, Chamg.

McLeish (1975)

McLeish, D. L. (1975), ‘A maximal inequality

and dependent strong laws’, Annals of probability3(5), 829–839.

Moon and Weidner (2015)

Moon, H. R. and Weidner, M. (2015),

‘Linear regression for panel with unknown number of factors as interactive

fixed effects’, Econometrica83(4), 1543–1579.

Neyman and Scott (1948)

Neyman, J. and Scott, E. L. (1948),

‘Consistent estimates based on partially consistent observations’, Econometrica16(1), 1–32.

Rodrik (2013)

Rodrik, D. (2013), ‘Unconditional convergence

in manufacturing’, Quarterly Journal of Economics128(1), 165–204.

Sala-I-Martin et al. (2004)

Sala-I-Martin, X., Doppelhofer, G. and Miller, R. I. (2004), ‘Determinants of long-term growth: A bayesian

averaging of classical estimates (bace) approach’, American Economic

Review94(4), 813–835.

Salimans (2012)

Salimans, T. (2012), ‘Variable selection and

functional form uncertainty in cross-country growth regressions’, Journal of Econometrics171(2), 267–280.

Shao and Yu (1996)

Shao, Q.-M. and Yu, H. (1996), ‘Weak

convergence for weighted empirical processes of dependent sequences’, Annals of Probability24(4), 2098–2127.

Shao (2010)

Shao, X. (2010), ‘The dependent wild

bootstrap’, Journal of the American Statistical Association105(489), 218–235.

Uematsu and Yamagata (2023)

Uematsu, Y. and Yamagata, T. (2023),

‘Inference in sparsity-induced weak factor models’, Journal of Business

& Economic Statistics41(1), 126–139.

Zhang et al. (2023)

Zhang, B., Pan, G., Yao, Q. and Zhou, W. (2023), ‘Factor modeling for clustering high-dimensional time

series’, Journal of the American Statistical Association0(0), 1–12.

Appendix A

In the following, we first provide a few notations which will be repeatedly used in Assumptions and theoretical development of the paper. Key assumptions with their justifications will follow.

Notations:

Operation: ;

Parameters: and ;

Regressors: and ;

Errors: , , , and

Loadings: , , , , and ;

Some matrices: , and .

Assumption 1.

1.

For the error components, the followings hold:

(a)

, and ;

(b)

, and .

2.

For the loadings, the followings hold:

(a)

in which

(b)

in which

(c)

in which

3.

For the factors, the followings hold:

(a)

;

(b)

and .

4.

For the regressors, the followings hold:

(a)

,

(b)

.

5.

Suppose with probability approaching 1, where , , , and .

Assumption 1 imposes a set of regular conditions. All of the conditions involving , and can be easily justified in the same fashion as in Lemma B.2. However, as we cannot define some type of mixing condition along the dimension or , so we state them as they are via a set of high level assumptions. Assumption 1.1 is well discussed in the Appendix of Moon and Weidner (2015). Assumption 1.2 regulates the behavior of factor loadings, while Assumption 1.3 imposes assumption on the factors. As explained under (2.4), Assumption 1.3.(a) is only a matter of rotating matrix, which can be easily fulfilled in practice. For example, let all of , and be independently generated from multivariate standard normal distribution. As explained in Remark 2.1, Assumption 1.4 actually does not impose too many conditions on variables used to generate . For instance, one may have weak factor signal through the factor loadings associated with . If that is the case, one definitely cannot use to collect factors without any special treatment. That is why we offer the current estimation approach in Section 2. Assumption 1.5 is an identification condition, which is similar to Assumption A of Bai (2009).

Assumption 2.

1.

Suppose that are independent of the other variables, and and , and for , are strictly -mixing process with the -mixing coefficient

satisfying with and , where and are the -algebras generated by and , respectively. Finally, there exits such that .

2.

.

The mixing condition of Assumption 2.1 is necessary to derive Lemma B.2, which is then further required to derive Lemma 2.2 and the asymptotic distribution. The requirements about ’s impose conditions on the existence of some moments of , which can be easily fulfilled, e.g., follows a normal distribution. Assumption 2.2 is standard.

Table A.1: Estimation of industry- and country-specific factors.

Panels A and B present the estimated numbers of industry-specific and country-specific factors, respectively, along with the total proportion of variance explained by these two groups of factors. The sample period is from 1963 to 2018.

Panel A

Panel B

Industry

No. of Factors

Country

No. of Factors

Country

No. of Factors

Country

No. of Factors

FB

4

ALB

1

GTM

1

PAK

5

TP

5

ARM

5

HND

5

PAN

2

TE

1

AZE

1

HRV

4

PER

5

WAF

1

BDI

3

IND

5

PHL

5

LLF

1

BEN

5

IRN

5

POL

4

WP

1

BFA

1

JAM

1

PRY

5

PPP

5

BGD

2

JOR

3

RUS

5

PP

5

BGR

5

KAZ

5

SDN

1

CRN

8

BLR

1

KEN

1

SEN

6

CCP

5

BRA

5

KGZ

5

SLV

2

RPP

3

BWA

1

KHM

1

SYR

4

NMP

1

CAF

1

LAO

5

THA

1

BM

10

CIV

1

LBN

2

TTO

2

FMP

1

CMR

5

LKA

5

TUN

1

ME

4

COL

3

MDA

1

TUR

1

OACM

8

DOM

3

MDG

3

TZA

5

EMA

5

DZA

6

MEX

5

UGA

4

RTCE

4

ECU

1

MNG

9

UKR

5

MPOI

2

EGY

1

MOZ

5

URY

1

MVTS

8

ETH

2

MWI

5

VEN

5

OTE

1

GAB

5

MYS

2

YEM

4

FM

1

GEO

1

NIC

4

ZAF

5

RC

8

GHA

3

NPL

3

ZWE

6

GMB

7

OMN

5

% of Var()

56.65%

Table A.2: The means of estimated coefficients.

Panels A-D report the means of estimated regression coefficients and their 95% confidence intervals for different samples periods. Panel E provides the estimation results for the sample without including OECD countries.

Variable

CI

Panel A (1963-2018)

IniP

-0.157

(-0.161, -0.152)

IP

0.108

(0.044, 0.158)

GCS

0.461

(0.350, 0.601)

Open

0.391

(0.253, 0.506)

SSE

0.368

(0.292, 0.442)

CL

0.015

(0.008, 0.021)

Panel B (1973-2018)

IniP

-0.170

(-0.175, -0.165)

IP

0.103

(0.025, 0.172)

GCS

0.306

(0.154, 0.468)

Open

0.525

(0.344, 0.678)

SSE

0.281

(0.190, 0.367)

CL

0.006

(-0.001, 0.012)

Panel C (1983-2018)

IniP

-0.173

(-0.178, -0.166)

IP

0.105

(0.031, 0.193)

GCS

-0.053

(-0.229, 0.149)

Open

-0.198

(-0.391, 0.012)

SSE

0.022

(-0.096, 0.157)

CL

0.026

(0.016, 0.037)

Panel D (1993-2018)

IniP

-0.145

(-0.205, -0.127)

IP

0.118

(-0.235, 0.492)

GCS

0.743

(-0.381, 1.666)

Open

-0.812

(-1.729, -0.134)

SSE

-0.020

(-0.392, 0.306)

CL

-0.010

(-0.024, 0.048)

Panel E (1963-2018, excluding OECD)

IniP

-0.160

(-0.164, -0.155)

IP

0.168

(0.068, 0.250)

GCS

0.345

(0.170, 0.554)

Open

0.484

(0.297, 0.643)

SSE

0.303

(0.209, 0.399)

CL

0.012

(0.003, 0.019)

Table A.3: Estimated coefficients for IniP in the food and beverages industry.

The three-letter ISO 3166-1 alpha-3 codes are used as the abbreviations for countries. For each country in the food and beverages industry, the estimated coefficient for IniP and its confidence interval are reported. The sample period is from 1963 to 2018.

Country

CI

Country

CI

Country

CI

ALB

-0.267

(-0.326, -0.209)

GTM

-0.132

(-0.188, -0.079)

PAK

-0.124

(-0.223, -0.025)

ARM

-0.191

(-0.251, -0.120)

HND

-0.156

(-0.228, -0.077)

PAN

-0.213

(-0.324, -0.101)

AZE

-0.215

(-0.246, -0.181)

HRV

-0.311

(-0.597, -0.040)

PER

-0.092

(-0.151, -0.036)

BDI

-0.165

(-0.242, -0.097)

IND

-0.196

(-0.306, -0.071)

PHL

-0.215

(-0.304, -0.137)

BEN

-0.130

(-0.219, -0.038)

IRN

-0.130

(-0.229, -0.050)

POL

-0.127

(-0.180, -0.073)

BFA

-0.168

(-0.223, -0.114)

JAM

-0.192

(-0.276, -0.122)

PRY

-0.139

(-0.254, -0.019)

BGD

-0.133

(-0.237, -0.035)

JOR

0.006

(-0.027, 0.044)

RUS

-0.136

(-0.234, -0.043)

BGR

-0.150

(-0.237, -0.044)

KAZ

-0.233

(-0.288, -0.180)

SDN

-0.244

(-0.387, -0.110)

BLR

-0.079

(-0.190, 0.022)

KEN

-0.160

(-0.223, -0.098)

SEN

-0.231

(-0.350, -0.111)

BRA

-0.165

(-0.274, -0.064)

KGZ

-0.258

(-0.373, -0.152)

SLV

-0.063

(-0.124, 0.007)

BWA

-0.123

(-0.199, -0.040)

KHM

-0.220

(-0.358, -0.073)

SYR

-0.003

(-0.201, 0.198)

CAF

-0.079

(-0.156, -0.006)

LAO

-0.150

(-0.283, 0.007)

THA

0.049

(-0.093, 0.186)

CIV

-0.215

(-0.356, -0.066)

LBN

0.026

(-0.041, 0.089)

TTO

-0.096

(-0.199, 0.012)

CMR

-0.196

(-0.279, -0.114)

LKA

-0.138

(-0.255, -0.032)

TUN

-0.148

(-0.266, -0.017)

COL

-0.203

(-0.257, -0.142)

MDA

-0.144

(-0.216, -0.062)

TUR

-0.214

(-0.361, -0.045)

DOM

-0.262

(-0.340, -0.169)

MDG

-0.188

(-0.257, -0.110)

TZA

-0.163

(-0.237, -0.082)

DZA

-0.143

(-0.200, -0.093)

MEX

-0.181

(-0.276, -0.069)

UGA

-0.154

(-0.324, 0.004)

ECU

-0.167

(-0.303, -0.024)

MNG

-0.213

(-0.284, -0.149)

UKR

-0.241

(-0.385, -0.081)

EGY

-0.128

(-0.222, -0.026)

MOZ

-0.234

(-0.355, -0.112)

URY

-0.228

(-0.310, -0.143)

ETH

-0.167

(-0.256, -0.074)

MWI

-0.289

(-0.411, -0.153)

VEN

-0.160

(-0.264, -0.059)

GAB

-0.234

(-0.309, -0.157)

MYS

-0.187

(-0.279, -0.085)

YEM

-0.206

(-0.298, -0.112)

GEO

-0.039

(-0.114, 0.042)

NIC

-0.273

(-0.419, -0.123)

ZAF

-0.244

(-0.397, -0.102)

GHA

-0.028

(-0.354, 0.323)

NPL

-0.133

(-0.196, -0.074 )

ZWE

-0.003

(-0.124, 0.108)

GMB

-0.121

(-0.261, 0.008)

OMN

-0.094

(-0.190, 0.003)

Online Supplementary Appendix B to

“Estimation and Inference for Three-Dimensional Panel Data Models”

Guohua Feng∗, Jiti Gao†, Fei Liu♯ and Bin Peng†

∗University of North Texas, †Monash University and ♯Nankai University

Appendix B

Appendix B is organized as follows. Additional estimation results of the empirical study are reported in Appendix B.1; Appendix B.2 provides two detailed numerical implementations; Appendix B.3 includes the necessary preliminary lemmas; Appendix B.4 presents the detailed proofs.

B.1 Additional empirical results

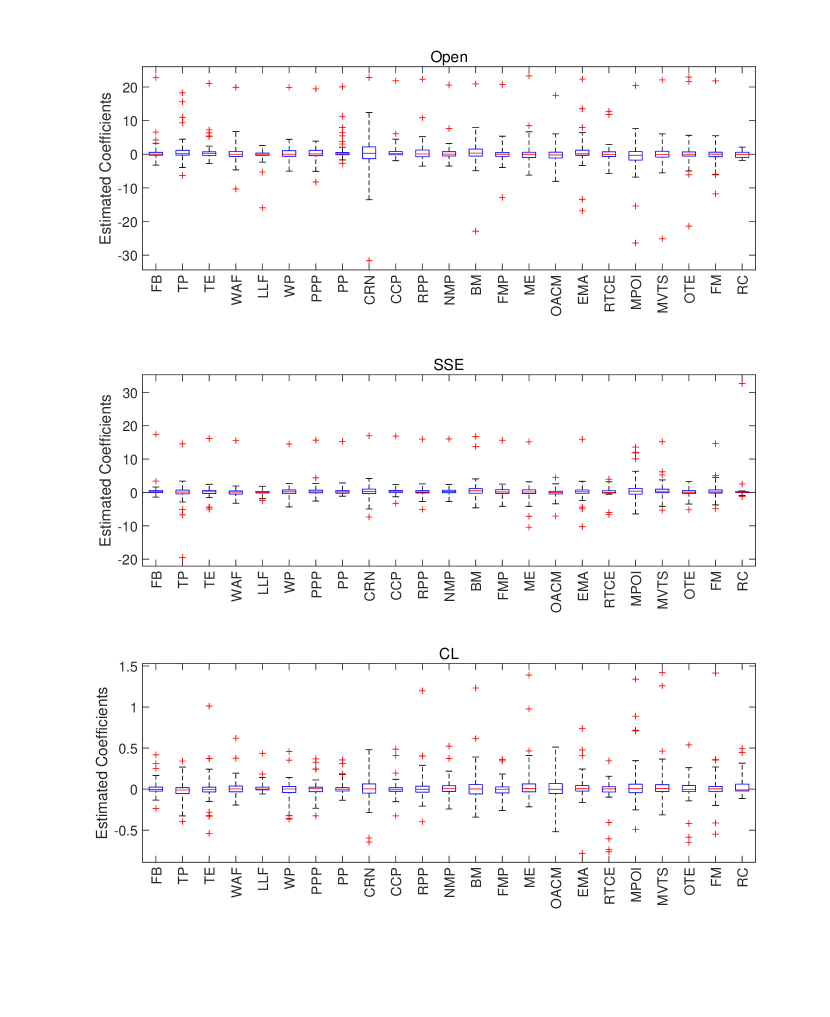

We first present some omitted empirical results for conditional convergence, which are Tables B.1 and B.2, and Figures B.1 and B.2. Figures B.1 and B.2 provide the boxplots of country-specific estimated coefficients for each explanatory variable across 23 industries. As shown in Figure B.1, the majority of the estimated coefficients associated with initial productivity exhibit values below zero, with a limited number of exceptions, while their distribution varies across industries. For the control variables, the estimated coefficients are distributed around zero and they exhibit more evident heterogeneity in different industries.

Next, we examine the unconditional convergence of labour productivity by excluding the control variables that are employed in Section 3.2. We re-estimate the numbers of factors using the method proposed in Section 2.3 and report the results for industry- and country-specific factors in Table B.3. The values are ranging from 1 to 9 for different industries and countries. In total, the industry- and country-specific factors can account for 65.77% of ’s variations. In addition, we identify one global factor that can explains 27.88% of the variations in . For the estimated coefficients for initial productivity, we present their distributions for each industry in Figure B.3. As can be seen from this figure, most estimated effects of initial productivity on the subsequent growth of productivity are negative and these manufacturing industries exhibit evident difference in the distributions. Furthermore, we calculate the average value of initial productivity’s effects using different samples in Table B.4. The results also indicate a negative relationship between the initial productivity and the subsequent growth rate, which is robust to various sample selections. Additionally, we report the country-specific estimates and the associated 95% confidence intervals for the initial productivity in the food and beverages industry in Table B.4. It is evident to see that the estimated effects are significant and negative for most countries.

To summarize, we can confirm that both unconditional and conditional convergences of productivity exist for most countries after controlling unrecoverable heterogeneity properly.

B.2 Numerical Implementation

In this appendix, we provide two numerical implementations. The first one is about the steps used to calculate simulation results, while the second one is specifically about the procedure of Section 2.2.

1. Implementation about Simulation

1.

We prescribe for instance. Let , , and to obtain as in the second implementation of this section.

2.

Once receiving , we calculate , , and as in Section 2.3.

3.

Using the estimates , , and , we obtain the estimate of again as in the second implementation of this section, i.e., an updated . Simultaneously, we also obtain the estimates , and which serve as the estimated , and respectively.

4.

With all estimates in hand, we implement the DWB procedure as in Section 2.2 to calculate the coverage rates for all ’s. For simplicity, we adopt the Bartlett kernel, i.e., if , and let the bandwidth be .

Randomly generate each element of from standard normal distribution, and conduct SVD decomposition to update and ensure . Generate the elements of and from standard normal distribution, and update and via SVD decomposition for and .

Repeat steps (2)-(4) until reaching some convergence, say, , where and stands for the value of obtained in the replication.

B.3 Preliminary Lemmas

We present some preliminary lemmas below, of which Lemmas B.1, B.2, and B.3 are some generic results.

Lemma B.1.

Suppose that , and is strictly -mixing process with the -mixing coefficient

satisfying for some and , where and are the -algebras generated by and , respectively. Then we have

where is a constant and .

Lemma B.2.

Suppose that , and for , is strictly -mixing process with the -mixing coefficient

satisfying with and , where and are the -algebras generated by and , respectively. Then we have for any given , there exists such that

Lemma B.2 infers, even for the case or (for this lemma only, and are generic notations and could be different from those in the main model), we are still able to achieve under rather minor conditions. Notably, Lemma B.2 does not impose any restrictions on dimension and on the tail behaviour of , so it permits to be correlated cross-sectionally and to have heavy tail behaviour.

Lemma B.3.

Suppose that and are symmetric matrices and that , where is and is , is an orthogonal matrix such that is an invariant subspace for . Decompose and as and . Let . If and , then there exists a matrix with , such that the columns of define an orthonormal basis for a subspace that is invariant for .

where is the principal diagonal of , includes the eigenvectors corresponding to , is the principal diagonal of , includes the eigenvectors corresponding to .

Let

Apparently, we have and in view of Assumption 1.1 and Assumption 1.3.

Similar to the study of and by noting and being symmetric, we can obtain that

(B.8)

According to (B.2), (B.3), (B.5), (B.7) and (B.8), we finally obtain that

(3). Write

(B.9)

In what follows, we consider the terms on the right hand side of (B.9) one by one. By Assumption 1.1, we immediately obtain that

(B.10)

Next, we consider .

(B.11)

where the first inequality follows from the fact that due to ’s being fixed parameters, and the second inequality follows from Assumptions 1.1 and 1.4.

We then consider .

(B.12)

where is defined in Appendix A, the first inequality follows from Assumptions 1.1 and 1.4 and the fact that due to ’s being fixed parameters.

Similar to the study for and by noting and being symmetric, we obtain that

(1). Recall that we have defined a few notations in Assumption 1. Write

Also note, that

where , , is defined in (2.4), and the second equality follows from Lemma B.3.4.

We now start our investigation, and consider

and note that the term

vanishes automatically when taking difference. Thus, using Lemma B.3, we immediately obtain that

(B.14)

We now focus on the right hand side of (B.14), and consider the following two cases:

where is a large positive constant. Note that for Case 1, using Lemma B.4 and Assumption 1, equation (B.14) can further be simplified as follows:

(B.15)

where , and the second equality follows from Assumption 1.2. Following the development on page 1265 of Bai(2009) and using (B.15) and Assumption 1.2, it is easy to see that if we show that Case 2 does not hold, which is exactly what we are about to do.

where and are defined in the same fashion as that on page 1265 of Bai(2009), is a positive constant by Assumption 1. Apparently, Case 2 cannot hold by comparing the right hand sides of (B.14) and (B.16). The proof of the first result is now completed.

where the first inequality follows from the triangle inequality and the fact that , and the second inequality follows from Assumption 1.4.

For , write

where the second inequality follows from Cauchy-Schwarz inequality, and third inequality follows from the development for and Assumptions 1.2-1.4. Similarly, we obtain that

For , write

where the third inequality follows from the development of and the following development:

(1). Note that we can have the following expansion:

Our goal is to prove Suppose that there exits some such that .

For the term , we write

where the first inequality follows from by the second result of Lemma 2.1, and the second result follows from the fourth condition of (2.12) and (B.20).

Next, suppose that is a scalar for simplicity for now only. Then write

where the last equality follows from Lemma B.2 and Assumption 2 straightaway. Thus,

Therefore, if , we conclude that

Thus, it infers

We now show it violates the first result of Lemma 2.1 and (2.14). In view of Lemma 2.1 and Assumption 1.4, we can always replace and with and to achieve

where is obtained by replacing and with and . Thus, the result follows.

(2)-(3). Note that by construction, and are symmetric, so we only need to prove one. Without loss of generality, we consider Step 1.d.

For , write

where the definitions of to should be obvious.

For , write

(B.21)

where the first inequality follows from the triangle inequality and the fact that , and the second inequality follows from Assumption 1.4.

For , write

where the second inequality follows from Cauchy-Schwarz inequality, and third inequality follows from the development for and Assumptions 1.1 and 1.2.

Similar to the development of , we obtain that

For , write

where the second inequality follows from Assumptions 1.3, 1.4 and 2.2. Similarly, we obtain that

Similar to the development of and noting that by Lemma 2.1 and Assumption 1.3, we obtain that

For , using the development similar to those for , we can write

where the second inequality follows from Assumptions 1.1 and 1.4. Similarly, we can obtain

For , write

where the second equality follows from Assumption 1.2, and the last step follows from (B.20).

For , write

where we have used (B.20) and Assumptions 1.2, 1.3, and 2.2.

Similar to the development of , we can obtain that

Similar to the development of and by noting using Assumption 1.3 and (B.20), we can also obtain that

For , we write

where the second equality follows Assumption 1.2 and (B.20).

Similar to the development of , we obtain that

Similar to the development of and invoking Assumption 2.2, we get

By the development similar to and invoking Assumption 2.2, we obtain that

Similar to the development of and by noting , we obtain that

We first note that in what follows, we shall repeatedly expand as in Lemma 2.1 and Lemma 2.2. Therefore, if we can show the terms involved in expansions are , then they are negligible. The reason is that we can repeatedly expand , so the term eventually will have a power .

We start with , and consider

(B.23)

where ’s are defined in the proof of Lemma 2.1, , and the definitions of should be obvious. First, we show that

(B.24)

Take as an example without loss of generality. Note that

(B.25)

where and . Then we can write

where the first inequality follows from (B.25) and Assumption 1, and the second inequality follows from by the third result of Lemma 2.2. The rest terms involved in can be proved similarly, so we omit the details. Thus, (B.24) is proved.

For , write

where the second inequality follows from the development of .

For , it is easy to show that

following the development of and .

Similar to and , we know that

Similar to the development of to , it is easy to know that

Therefore,

in view of the condition in the body of this theorem.

Next, we consider .

(B.26)

where , and the definitions of should be obvious. In what follows, we consider these terms one by one.

Similar to the development of to , we have

For to , it is easy to know that

by the development of to .

For , write

Therefore, the investigation of reduces to the study of , which infers that

For and , following the development similar to and , it is easy to know that

For to , invoking (B.25) and following the development for to , it is easy to know that

Thus, we can conclude that

Further, by noting and are symmetric, we immediately obtain that

Thus, when driving the asymptotic distribution, we only need to focus on the following term

which in connection with (B.25) infers that we just need to focus on

By standard large block and small block technique (cf., Gao, 2007), we immediately obtain that for ,

where . In connection with the fact that for ,

the proof is now completed.

Proof of Theorem 2.2:

In the following proofs, we denote and as the expectation and variance conditional on the observed sample, respectively. and denote the norms associated with : and , for any random variable and any positive number . Additionally, let and be the sigma field generated by and the expectation conditional on , respectively.

Write

(B.27)

We then investigate the terms on the right hand side of (B.27) one by one. For the first term, using analogous arguments in the proof of Theorem 2.1, we can obtain

In what follows, we show that can generate the bootstrap distribution. We first show . Note that

(B.28)

For the first term on the right-hand side of (B.28), it is clear to see that . For the second term,

(B.29)

where is a positive integer that satisfies and .

For the first term, by the Davydov’s inequality for -mixing processes (see Bosq, 2012, pp. 19-20) and Assumption 2,

(B.30)

In addition, by the Lipschitz continuity of on , it is clear to see that the first term in (B.29) has the order of

.

Assumption 2 ensures that and have the same limit as and . Therefore, the second term in (B.29) is also negligible. Then, we proceed to study the order of . Define as

(B.31)

Simple algebra indicates . Then, the following result holds for :

Moreover, by McLeish’s inequality for -mixing processes (see Lemma 2.1 of McLeish, 1975) and Assumption 2,

for any positive integer . Together with Lemma A of Hansen(1992), it gives

where and . It follows that

which immediately yields . Therefore, we obtain

Analogously, for ,

In summary of these results, we have

(B.32)

Since is -dependent time series, we can follow the Theorem 3.1 of Shao(2010) and adopt the large-block and small-block argument to prove the central limit theorem for conditional on the observed sample. Define and as the lengths for the large and small blocks and such that and they satisfy .

For , we define a series of variables for the large and small blocks, respectively:

Moreover, we define to contain the reminder terms.

Without loss of generality, we assume . Then, it is clear to see that are independent conditional on the observed data, as are . Therefore,

Under the condition , we have . Analogously, we can show that .

In what follows, we establish the asymptotic normality of (conditional on the observed sample) using the Lindeberg CLT. Similarly to (B.32), we can also show that .

For any , we have

(B.33)

Without loss of generality, we now use the Rosenthal inequality to study the order of . Noteworthily, Rosenthal inequality is designed for the independent random variables. Therefore, we consider the following decomposition for : ,

where

By this definition, it is clear to see that the elements involved in are independent conditional on the observed sample. Directly applying the triangle inequality and Rosenthal inequality sequentially, we obtain

which implies that . In summary of the results that we have established, the Lindeberg condition can be satisfied and

Additionally, using analogous arguments to those in the proof of Theorem 2.1, we can readily obtain that and the second and third terms in (B.27) are asymptotically negligible. Therefore, we are ready to complete the proof of Theorem 2.2.

This concludes the proof of the first result of this lemma.

(2). To investigate the second result, we start the proof by introducing some notations. We denote as a matrix such that , where is an rotation matrix. The matrices , , , and correspond to , , , and of Lemma B.3. Thus, the counterpart of the matrix becomes

in which

(B.37)

Moreover, is an orthonormal basis for a subspace that is invariant for . In addition, note that

By Lemma B.5, for , which are larger than with a probability approaching one. Thus, for we can conclude that

For , by Lemma B.5, , which is less than with a probability approaching one. Thus,

for by construction. In addition, for , it is straightforward to obtain that

using the facts that and . Thus, we are ready to conclude that .

Step 2. Note that and are symmetric. Thus, without loss of generality, we consider two cases: (i) there is at least one in , and (ii) there is at least one in . Note that case (i) does not rule out the possibility that other estimated numbers of factors may be larger than the true value. Similarly, case (ii) does not rule out the possibility that other estimated numbers of factors may be less than the true value. If we can rule out both cases with a probability approaching one, then .

We now consider case (i), and suppose that . By Lemma B.6, we can show that

By replacing of with , we find another , which yields a smaller value for the objective function considered in (Step 3*) with a probability approaching one. However, this is contradictory to the definition of .

Next, we consider case (ii), and suppose that . Again, Lemma B.6 yields that

By replacing of with , we find another , which yields a smaller value for the objective function considered in (Step 3*) with a probability approaching one. However, it is contradictory to the definition of . Based on the above development, we conclude that .

In view of Steps 1 and 2, the proof is now completed.

Table B.1: Summary statistics of the dataset. This table provides the means and standard deviations for the dependent variable and regressors. The sample period is from 1963 to 2018.

Variable Name

Abbreviation

Mean

Std

Growth in Labor productivity

GLP

0.038

0.483

Initial productivity

IniP

7.919

2.678

Investment price

IP

0.278

0.213

Government consumption share

GCS

0.207

0.120

Openness measure

Open

-0.029

0.119

Secondary school enrolment

SSE

0.534

0.313

Civil liberties

CL

4.353

1.797

Table B.2: The number of countries for each industry.

The dataset comprises 23 manufacturing industries at the 2-digit level of the International Standard Industrial Classification of All Economic Activities (ISIC). The sample period is from 1963 to 2018.

Industry Name

Abbreviation

No. of countries

Food and beverages

FB

71

Tobacco products

TP

65

Textiles

TE

71

Wearing apparel, fur

WAF

69

Leather, leather products and footwear

LLF

53

Wood products (excl. furniture)

WP

71

Paper and paper products

PPP

68

Printing and publishing

PP

70

Coke, refined petroleum products, nuclear fuel

CRN

61

Chemicals and chemical products

CCP

71

Rubber and plastics products

RPP

69

Non-metallic mineral products

NMP

70

Basic metals

BM

68

Fabricated metal products

FMP

70

Machinery and equipment n.e.c.

ME

67

Office, accounting and computing machinery

OACM

42

Electrical machinery and apparatus

EMA

68

Radio, television and communication equipment

RTCE

31

Medical, precision and optical instruments

MPOI

54

Motor vehicles, trailers, semi-trailers

MVTS

68

Other transport equipment

OTE

46

Furniture, manufacturing n.e.c.

FM

71

Recycling

RC

23

Table B.3: Estimation of industry- and country-specific factors (without control variables).

Panels A and B of this table present the estimated numbers of industry-specific and country-specific factors, respectively, along with the total proportion of variance explained by these two groups of factors. The sample period is from 1963 to 2018.

Panel A

Panel B

Industry

No. of Factors

Country

No. of Factors

Country

No. of Factors

Country

No. of Factors

FB

1

ALB

1

GTM

1

PAK

1

TP

5

ARM

8

HND

4

PAN

2

TE

1

AZE

2

HRV

3

PER

3

WAF

4

BDI

3

IND

1

PHL

1

LLF

1

BEN

2

IRN

1

POL

4

WP

2

BFA

1

JAM

1

PRY

5

PPP

5

BGD

2

JOR

4

RUS

1

PP

3

BGR

1

KAZ

3

SDN

1

CRN

8

BLR

1

KEN

2

SEN

6

CCP

1

BRA

4

KGZ

3

SLV

2

RPP

3

BWA

1

KHM

5

SYR

6

NMP

1

CAF

1

LAO

1

THA

1

BM

9

CIV

1

LBN

2

TTO

2

FMP

2

CMR

5

LKA

5

TUN

1

ME

4

COL

1

MDA

2

TUR

1

OACM

8

DOM

6

MDG

4

TZA

3

EMA

5

DZA

1

MEX

2

UGA

5

RTCE

4

ECU

1

MNG

5

UKR

5

MPOI

2

EGY

2

MOZ

2

URY

1

MVTS

9

ETH

2

MWI

3

VEN

5

OTE

1

GAB

2

MYS

2

YEM

5

FM

1

GEO

1

NIC

6

ZAF

2

RC

7

GHA

4

NPL

3

ZWE

3

GMB

1

OMN

5

% of Var()

65.77%

Table B.4: The means of estimated coefficients.

Sample

Variable

CI

1963-2018

IniP

-0.107

(-0.109, -0.101)

1973-2018

IniP

-0.119

(-0.121, -0.113)

1983-2018

IniP

-0.141

(-0.143, -0.133)

1993-2018

IniP

-0.154

(-0.162, -0.141)

1963-2018, excluding OECD

IniP

-0.109

(-0.111, -0.103)

Table B.5: Estimated coefficients for IniP in the food and beverages industry (without control variables).

In this table, the three-letter ISO 3166-1 alpha-3 codes are used as the abbreviations for countries. For each country in the food and beverages industry, the estimated coefficient for IniP and its confidence interval (CI) are reported. The sample period is from 1963 to 2018.

Country

CI

Country

CI

Country

CI

ALB

-0.257

(-0.326, -0.191)

GTM

-0.096