High-dimensional copula-based Wasserstein dependence.

Abstract

We generalize -Wasserstein dependence coefficients to measure dependence between a finite number of random vectors. This generalization includes theoretical properties, and in particular focuses on an interpretation of maximal dependence and an asymptotic normality result for a proposed semi-parametric estimator under a Gaussian copula assumption. In addition, we discuss general axioms for dependence measures between multiple random vectors, other plausible normalizations, and various examples. Afterwards, we look into plug-in estimators based on penalized empirical covariance matrices in order to deal with high dimensionality issues and take possible marginal independencies into account by inducing (block) sparsity. The latter ideas are investigated via a simulation study, considering other dependence coefficients as well. We illustrate the use of the developed methods in two real data applications.

keywords:

Copula , Normal scores rank correlation , Regularization , Sparsity , Wasserstein dependence2020 MSC: Primary 62Axx, 62Hxx; Secondary 62Exx, 62Gxx.

1 Introduction

A prominent line of research in statistics considers measuring dependence between groups of variables. In case of two groups, greatly celebrated is the canonical correlation analysis of [27] relying on the Pearson correlation coefficient. To step away from the assumption of Gaussianity, concordance measures as studied in, e.g., [22, 37, 42] among many others, are also used for quantifying general monotonic associations between two random vectors in [23]. In [26], measures of association computed from collapsed random variables are used to measure the dependence between random vectors. Fundamental is copula theory (e.g., [38, 43]), allowing to split multivariate distributions into marginal distributions on the one hand, and a dependence structure described by the copula on the other hand. Especially when the marginals are continuous, the preference often goes to copula-based dependence measures since then, by Sklar’s theorem [43], the copula is unique, and hence margin-free dependence can unequivocally be quantified.

Statistical independence between random vectors holds if and only if the true underlying copula is the product of the marginal copulas (where a one dimensional copula is basically a uniform distribution on ), yielding zero dependence. However, the dependence measures mentioned above do not detect all types of departure from independence, meaning that they might vanish while the independence product copula is misspecified. Since the work of [44], there has been a growing interest for dependence measures that completely characterize independence. Some recent developments are, e.g., the Hoeffding’s Phi-Square measure of [35], the -dependence measures of [11] (of which the Hellinger correlation [20] and essential dependence [51] are particular cases), the coefficient of Chatterjee [8, 2, 18, 1], and the -Wasserstein coefficients of [36].

The aim of this article is to elaborate further on the optimal transport measures of [36]. First, the focus will be on extending their dependence coefficients from two to finitely many random vectors. We do this from a copula point of view. This includes generalizing the results of [36], and also verifying the axioms stated in [11] (see also A). Some additional examples, focusing on, e.g., the impact of the normalization, are provided as well. Afterwards, we dive into the Bures-Wasserstein dependence making a Gaussian copula assumption. This yields dependence measures that are attractive, and more amenable for estimation. The results are a far from straightforward extension of results of [36] to the case of a finite number of random vectors, and require significant mathematical care.

The proposed semi-parametric estimation approach of the Bures-Wasserstein coefficients relies on the sample matrix of normal scores rank correlations (see, e.g., [24]). Since we extend the theory to a general finite amount of groups of variables, high dimensional cases with a large number of variables compared to the sample size are of study interest as well. Acclaimed penalization techniques are known to significantly improve (inverse) covariance matrix estimation (see, e.g., [29] and references therein). We utilize these ideas in our Gaussian copula context in order to correct for high dimensionality bias and possibly enforce sparsity at the individual level or group level to take plausible marginal independencies into account.

The outline of this paper is the following. Section 2 explains how optimal transport theory is combined with copula theory in order to arrive at a dependence measure between multiple groups of random variables that completely characterizes independence and is invariant with respect to the univariate marginal distributions. The verification of the properties postulated in [11] for such dependence measures is also part of this section. The Gaussian copula approach is discussed in Section 3, with special attention to the meaning of maximal dependence, and asymptotic normality of the proposed semi-parametric estimator. Afterwards, different regularization techniques for Gaussian copula covariance matrices are discussed in Section 4. Next to an empirical illustration of the asymptotic normality result, simulations are performed in Section 5 to investigate the performance of these regularization techniques on various dependence coefficients for random vectors. Two real data applications are discussed in Section 6. All proofs are deferred to the Appendix. Any experiments reported can be reproduced via the source code available at https://github.com/StevenDeKeyser98/VecDep. Additional figures are included in the Supplementary Material.

2 General -Wasserstein dependence

We consider a -dimensional random vector defined on consisting of marginal random vectors for having continuous univariate marginal random variables for . The numbers are such that , and denotes the -dimensional Lebesgue measure defined on , the Borel sigma-algebra on . Let be a probability measure. Our aim is to measure the dependence between . For and the set of Borel probability measures on , the random vector is assigned a copula probability law having corresponding marginal copula laws of for . Note that in case , the law is that of a uniform distribution on . We denote for the set of measures such that

for all and . This is a natural generalization of the set of coupling measures. Obviously, . Quantifying the intensity of relation between can be done by measuring the difference between and the product measure . We use the -Wasserstein distance, whose square is, for certain measures given by

| (1) |

The interpretation of the metric (1) is optimal transport, see, e.g., [39]. It is the minimal effort (cost) required to transform the mass of into the mass of , i.e., for every transport an infinitesimal amount of mass from to at a distance cost of . Aggregating the mass that leaves gives and the total mass that reaches equals . For certain non-degenerate (i.e. not Dirac delta distributions) reference laws for , we now define

where the second identity is known to be true (see, e.g., [39]). We call a subset -compact if every sequence in the metric space has a convergent subsequence with limit in . Lemma 1 gives the main properties of . Proofs of Lemma 1, and all other theoretical results of Section 2, can be found in B.

Lemma 1.

It holds that

-

(a)

-

(b)

-

(c)

If either for all or is absolutely continuous (with respect to ) for all , then implies

-

(d)

The set is -compact in and the mapping is continuous.

Its interpretation, together with its mathematical properties, make an appealing measure of dependence between random vectors . In what follows, we assume that is absolutely continuous for , and let be a compact set such that . General axioms for dependence measures between multiple random vectors are formulated in [11], see also A. Lemma 1 offers aid in proving them here, see Proposition 1.

Proposition 1.

Consider Axioms (A1)-(A8) given in A, and a normalized version of given by

| (2) |

Then, satisfies (A1)-(A3) and (A5)-(A7). Axioms (A4) and (A8) are satisfied by the non-normalized version .

The supremum in (2) is attained when is -compact (e.g., ) because of (d) in Lemma 1. It represents the case of maximal dependence, which characterization (and hence the overall behaviour of (2)), largely depends on . There is still freedom in choosing the normalization by picking the set . It might impose additional constraints (in addition to having marginals ) on the that characterizes maximal dependence (for example should be in the same copula family as ). Strictly speaking, we can have a different for every copula , even if the marginals are the same.

Regarding axioms (A4) and (A8), we make the following remark.

Remark 1.

While (2) does not satisfy axiom (A4) in general (that is for every possible choice of ), there might still be some specific choices for such that (A4) is satisfied. We illustrate this further in Example 1.

Also, when considering uniformly as , axiom (A8) can be satisfied by (2) under some extra constraints. The numerator converges if is chosen such that is continuous (considering the uniform metric on the space of copulas). In Section 3, we see that this holds in the class of Gaussian copulas when taking .

We now arrive at a natural generalization of the Wasserstein dependence coefficients of [36], which come from (2) with two particular choices of reference measures.

Definition 1.

For , let denote the measure of an -variate Gaussian copula with identity correlation matrix (i.e., the -variate independence copula). For with and for , where is -compact and non-degenerate for , define

If the context is clear, we just write for , or also to emphasize that we are measuring the dependence between random vectors (having joint copula ).

Let us consider an example illustrating that does not necessarily satisfy Axiom (A4) in general.

Example 1.

Consider a random vector having a trivariate Gaussian copula with correlation matrix

Let be the marginal copula measure of for , which in this case is in fact the Lebesgue measure corresponding to a distribution. The product measure is the three dimensional independence copula, being equal to the trivariate Gaussian copula with identity correlation matrix . Also note that is independent of . One can quickly check that (using (3), see further)

The remaining question is what to pick for , i.e., which quantity do we put in the denominator and defines the maximal amount of dependence. Well, if , we should find the squared -Wasserstein distance between the independence copula and any other trivariate distribution having and as marginals, that is every possible trivariate copula. This is, as far as we are concerned, an open problem. However, in this context, it is reasonable to restrict to the Gaussian copula family. Doing so, one has

where stands for the comonotonicity copula measure, i.e., the limit of an equicorrelated (, where and ) Gaussian copula with correlation tending to . With this choice of , can never reach the maximum dependence, since

Another way to put it, is that

where is computed in a similar way, also restricting the couplings to Gaussian ones. We thus see that, when adding an independent component into consideration, the dependence has decreased and hence axiom (A4) is definitely not fulfilled. Taking a look at , it is maybe more tempting to have maximal dependence when and restrict further to only those that are Gaussian and furthermore satisfy for all . Then, it is quickly seen that

and hence , in harmony with axiom (A4). So, for actual computation, it is better to restrict to the Gaussian copula family, and if some additional information is given (like zeroes in the correlation matrix), incorporating this in can lead to a more interpretative dependence quantification.

Except for some families like normal distributions, computing the Wasserstein distance is very involved and tools and theory for statistical inference are still scarce. The authors of [36] give an overview of the literature so far, concluding that additional theory is still needed, and propose a quasi-Gaussian (based on covariance matrices) approach instead. We assume that the copula of is Gaussian.

3 A Gaussian copula approach

In this section, we assume a Gaussian copula model for , elaborate more on maximal dependence, and discuss statistical inference within this framework.

3.1 The Bures-Wasserstein distance

The main incentive is the well-known formula for the squared -Wasserstein distance between Gaussian distributions, say with covariance matrices and , becoming the so-called squared Bures-Wasserstein distance (see, e.g., [45]) between and :

| (3) |

were tr stands for the trace of a matrix. We denote by the set of symmetric matrices, the set of positive semi-definite ones and the set of positive definite ones. Let again and consider for . We also define the set

as the set of all covariance matrices of random vectors such that the covariance matrix of , being , remains fixed for all and

| (4) |

with a matrix of zeroes, as the covariance matrix when the are all independent.

Consider now a random vector having a Gaussian copula with covariance matrix

| (5) |

This means that (5) is the usual covariance matrix of the random vector , with and for and , where is the marginal distribution of and the univariate standard normal quantile function. Measuring the dependence between can be done by utilizing the -Wasserstein dependence coefficients of Definition 1, now taking for .

Definition 2.

For with , with for and a -compact set with , define

where is the matrix given in (4). If the context is clear, we also write or for .

If the true copula is indeed Gaussian, the adequacy of the Bures-Wasserstein dependence remains, and we obtain something way more easy to handle. In order to make them fully practically usable, that is to say suitably attractive for estimation, we ought to find explicit expressions for the suprema in the denominator of the dependence measures. When and , the authors of [36] found elegant solutions to this problem, which we generalize to general .

3.2 Maximal Bures-Wasserstein dependence

We need the definition of majorization of two vectors and its behaviour under convex functions, as studied in [33].

Definition 3.

For two vectors , we say that majorizes , denoted as , if

where are the components of in decreasing order, and similarly for .

When and are the vectors of eigenvalues of two correlation matrices, being majorized by means that the proportion of the total variance explained by the first principal components is larger for the correlation matrix with eigenvalues , for any , than for the correlation matrix with eigenvalues . Fixing covariance matrices with , the goal is now to find whose ordered eigenvalues majorize those of any matrix . Together with Lemma 2 (see Proposition 3.C.1 in [33]), this will enable us to characterize maximal dependence between random vectors in terms of covariance matrices.

Lemma 2.

If is convex, with an interval, then

for all .

Since the -Wasserstein dependence coefficients satisfy axiom (A1), we can assume that without loss of generality. Suppose that

| (6) |

is the eigendecomposition of , i.e., with the diagonal matrix with ordered eigenvalues on the diagonal (counting multiplicities), and an orthogonal matrix containing the corresponding eigenvectors for . The proof of Proposition 2, and all other theoretical results of Section 3, are provided in C.

Proposition 2.

Let have eigendecomposition (6) for . Define the matrix as

| (7) |

with and , and off-diagonal blocks

where

the upper left block of for (denoting for the matrix of zeroes). If we define for , the eigenvalues of are

| (8) |

Furthermore, for any with eigenvalues , it holds that

Example 2 gives the matrix for some specific cases.

Example 2.

Some expressions for in case can be found in [36]. If with for all , the matrix is obviously given by , a matrix full of ones. Consider next for , i.e., bivariate random vectors, with covariance matrix of given by

Assuming , one can check that of in (7) for and is given by

| (9) |

The result is similar in case or up to some signs (orthogonal transformations, to which is invariant). The principal components of are

corresponding to the eigenvalues respectively, with

and

A quick check then verifies that if has correlation matrix with blocks (9), it holds that for all and , i.e., all first principal components are perfectly correlated and all second principal components as well.

Proposition 3 states that the matrix in (7) maximizes the intensity of dependence, i.e., when taking for fixed marginal covariance matrices .

A general interpretation of is given in Remark 2. .

Remark 2.

Assuming again that , the matrix in (7) is the covariance matrix of

where such that for all we have , and in addition for all , , i.e., and have the first components in common for all . The correlation matrix of the principal components of is

with as in Proposition 2. Hence, if has a Gaussian copula with covariance matrix , then for the -th principal components of and are perfectly correlated for all . This is the interpretation of maximal dependence for the Bures-Wasserstein dependence measures.

In the upcoming section, we also assume that .

3.3 Statistical inference

In practice, we have an i.i.d. sample for from , where for is a sample from for . A natural estimator for the Gaussian copula covariance matrix is known as the matrix of sample normal scores rank correlation coefficients (see, e.g., [24]),

| (10) |

defined by computing normal scores

obtained through the empirical cdf for and . The quantity is calculated as the conventional Pearson correlation of the bivariate scores and by observing that

which holds because for and is the rank of in the sample .

A next natural step in estimating is to plug in for the unknown . Define the map by for , where is the diagonal matrix containing the diagonal of , and let be the Frobenius norm. Fréchet differentiability of the mapping

on suffices in order for the delta method to transform an asymptotic normality result for into an asymptotic normality result for . We first highlight some notation. We assume , the matrix is again defined by (7) based on the eigendecompositions as in (6), and is the matrix in (4). Further, let

| (11) |

be the projection matrix onto the coordinates, satisfying . Partition the matrix as

| (12) |

with for and defining . Based on these partitions, further define

| (13) |

for with . Finally, we will need the matrices

| (14) |

with and

| (15) |

Theorem 1 formally states an asymptotic normality result for the estimator .

Theorem 1.

Let have a Gaussian copula with correlation matrix with such that has distinct eigenvalues, and let be given by (10) based on which the plug-in estimator is constructed. Then for , it holds that

as , with asymptotic variance

where is the diagonal matrix consisting of the diagonal of , and

with

| (16) |

and

| (17) |

Remark 3.

When , it holds that and for . The higher-order delta method can however still provide a weak convergence result for . A detailed study of this is research in progress.

We look at another example, which is also studied in [12], but in the context of -dependence measures.

Example 3.

Consider a four dimensional random vector having a Gaussian copula with covariance matrix

| (18) |

Then one can check that (recall also Example 2 for finding the matrix )

| (19) |

and

| (20) |

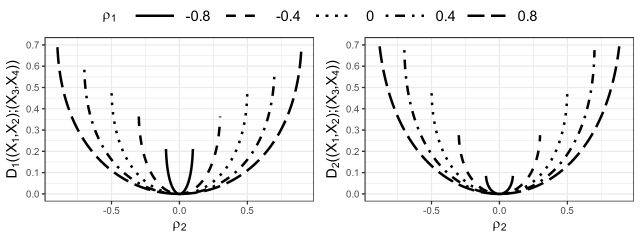

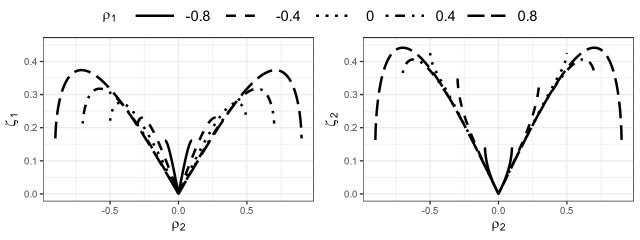

Fig. 1 shows how (19) and (20) depend on for different values of . Clearly, independence holds if and only if , as it should. When , the second principal component of is perfectly correlated with the second principal component of , where is the marginal distribution of for , see also [12]. This causes the -dependence measures studied in [12] to reach their maximum value, because a singularity is attained. In particular, taking for instance and , all (normalized) -dependence measures equal , while and .

The reason for and still being small, is that is pretty small and, recalling Remark 2, not both first and second principal components of and are perfectly correlated, only one of them is. Only when and thus also , we have . Maximal Bures-Wasserstein dependence is not attainable for the family (18) if , because it imposes additional restrictions on the correlations (i.e., not every element in is a member of (18)). Picking a set for a normalization that adjusts according to these restrictions, would lead to more cases of maximal dependence.

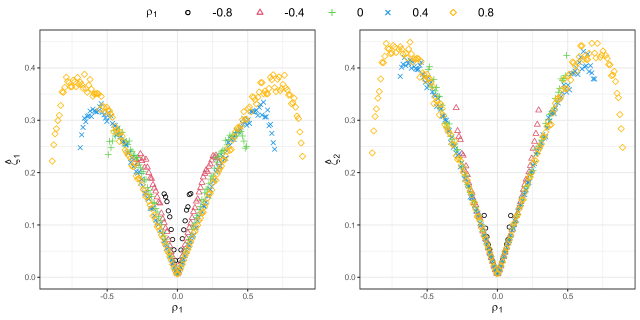

Fig. 2 depicts the asymptotic standard deviation of for as given in Theorem 1 for this specific example. We mainly observe increasing behaviour when the strength of dependence increases. However, in some cases where and get close to satisfying , we see the asymptotic standard deviation going down. For example, if , the asymptotic standard deviation is maximal () at , after which it converges to for . When keeping fixed and letting , the dependence attains a local maximum, which it cannot transcend, resulting in (slightly) lower asymptotic variance. This behaviour was also noticed in the same example in [12] for their (normalized) -dependence measures, whose asymptotic variance tends to zero when , because the singularity forces them to reach their global maximum. For the optimal transport dependence coefficients, the global maximum is only attained when , in which case the asymptotic variance also tends to zero.

4 A Gaussian copula approach: regularized estimation

Empirical covariance matrices are known to approach singularity when the dimension is close to the sample size. The estimator does not require an inverted covariance matrix, but it inquires about eigenvalue dispersion, and this tends to be biased when using the empirical covariance matrix, see, e.g., [31]. Typically, estimates of large eigenvalues tend to be biased upwards, and estimates of small eigenvalues tend to be biased downwards. Increasing dimensionality aggravates this, but penalization techniques can be used to restrain. We briefly discuss ridge regularization, as in [50], but now in a Gaussian copula context.

Of course, the ridge estimator will not completely shrink elements of the empirical covariance matrix to zero. However, the task might be to find a likely estimate for which multiple variables are marginally independent, i.e., a sparse estimate of the covariance matrix having zero entries. For this purpose, we look at a Gaussian copula formulation of the penalization ideas discussed in [29]. Finally, penalties can also be applied to groups of elements instead of just individual elements. A group lasso penalty, for instance, enables to shrink entire blocks of the covariance matrix to zero.

In Section 4.1, we discuss penalization methods for the Gaussian copula covariance matrix in case remains fixed with the sample size. Afterwards, in Section 4.2, we briefly touch upon the case where depends on .

4.1 Fixed dimension

Denote for the maximum likelihood estimator of a model, and the correlation matrix corresponding to (recall that is the diagonal matrix containing the diagonal of ). By adding a certain penalty, say to the Gaussian log-likelihood, where is a certain penalty parameter depending on , a general penalized optimization problem for estimating (under the constraint of positive definiteness ), is given by

| (21) |

and corresponding correlation matrix . However, the core of this paper is that we merely assume a Gaussian copula. Hence, instead of making use of , we compute , being the (block) matrix of sample normal scores rank covariances with entries for (similar block notation as in (10)). The main difference is that we do not have true Gaussian scores, but only non-parametrically estimated Gaussian scores . The copula formulation of (21) becomes

| (22) |

where we use the additional subscript in to indicate that we are in the copula context. A genuine Gaussian copula correlation matrix is then .

We go deeper into three choices for the penalty :

-

–

the ridge penalty , where

-

–

(adaptive) lasso-type penalties , where is the ’th element of the ’th block of (similar block notation as in (10)), is a weight (e.g., zero when in order to not shrink diagonal elements, or larger for smaller preliminary estimated entries in order to shrink these more) and is a certain penalty function depending on

-

–

group lasso-type penalties , where is the Frobenius matrix norm, a matrix with ones as off-diagonal elements and zeroes on the diagonal (in order to avoid shrinking the variances), and a certain penalty function depending on .

The ridge penalty is different from the other ones (and will also be considered separately in the simulations in Section 5) in the sense that it only focuses on improving the estimation of the Gaussian copula covariance matrix (and corresponding dependence coefficients) when is large compared to , and not on a sparsity assumption. Asymptotic properties are centred around consistency. Having is definitely manageable for ridge penalization. For the latter two penalties, the set defined as , where is the vector of upper diagonal elements of and , is of crucial importance. Indeed, next to consistency, we hope that for , where , with , a property called sparsistency. Having leads to degeneracy of the lasso-type estimators, which is why we restrict ourselves to in the simulations.

Example 4 shows that the sparsity of (which is obviously preserved by ), i.e., the entries belonging to , can manifest itself in different forms, calling for different shrinkage penalties.

Example 4.

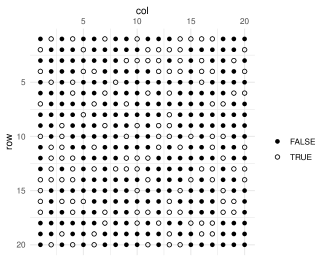

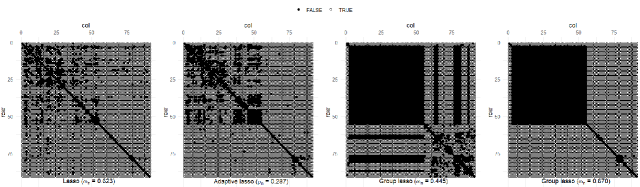

A covariance graph is a graphical model that represents variables as nodes and marginal dependencies as edges (similar to a Markov random field representing conditional dependencies), see, e.g., Section 1 of [4] for several references. Marginal independencies correspond to individual zeroes in the correlation matrix and many different sparsity patterns can occur. The first plot of Fig. 3 shows the sparsity structure of a correlation matrix of a random covariance graph for a total of variables, where of the elements equal zero, corresponding to the TRUE entries. A penalty of the form allows reflecting these marginal independencies in the estimated correlation matrix, and could result in a better plug-in estimator for our dependence measures.

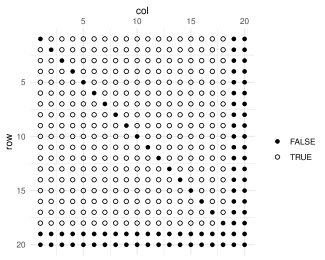

Next, imagine a person answering a total of twenty questions in the form of seven short questionnaires , all consisting of three questions, except for , which only contains two. The interest is in the relationship between the answers of the different questionnaires. Furthermore, assume that are on completely different topics, and all three questions are each time self-contained. Only the very last two questions contained in are related to each other, and to the other questions in the first six questionnaires as well. Then, it can be expected that only the blocks for and are different from zero (and the diagonal of , of course), i.e., has a sparsity pattern as visualized in the second plot of Fig. 3, where of the elements equal zero. Such a pattern calls for a penalty, enabling shrinkage of entire blocks, and possibly more accurate estimation of the Gaussian copula dependence coefficients compared to using the matrix of normal scores rank correlations , or a penalty.

We shall now elaborate more on the theoretical properties and computational aspects of the estimators and given in (22) corresponding to the three types of penalties and .

Ridge regularization

Warton [50] extensively studies the estimator , i.e., the estimator (21) under the assumption of a normal distribution, with penalty term for and . His Theorem 1 tells us that

where is the corresponding maximum penalized likelihood estimator. The value of is picked through -fold cross-validation with the normal likelihood as objective function. If is an eigenvalue of , then is an eigenvalue of , i.e., all eigenvalues smaller than one are expanded, and all eigenvalues larger than one are shrunk towards one (recall the discrepancy of biased eigenvalue dispersion of the non-regularized empirical covariance matrix), at a pace that increases as decreases. Furthermore, the value of tends to one in probability if , and there is zero probability that (no regularization) if does not have full rank, i.e., is guaranteed to be non-singular, even if (see Theorem 2 and Theorem 3 in [50]). In our Gaussian copula context, we suggest the estimator

| (23) |

and the same -fold cross-validation procedure for selecting , but now based on an estimated Gaussian sample. Heuristically (we do not go into detail here), the asymptotic properties of carry over to , since we know that (see, e.g., the proof of Theorem 1) for .

Regularized estimation and sparsity

Concentrating on the fully Gaussian setting, the general penalization criterion is considered in [29]. Typically, one takes if and otherwise in order to avoid penalization of the diagonal elements, which do not vanish. Another possibility is , where is a preliminary estimate for with corresponding correlation and a certain threshold value, i.e., we only shrink those elements that have a sufficiently small preliminary estimated correlation, and the amount of shrinkage is proportional to the size of the preliminary estimated covariance. This is an idea similar to the adaptive lasso of [13] and used in, e.g., [16]. A similar problem often arises when estimation of the precision matrix (inverse covariance matrix) is of interest, think of graphical models for example (see, e.g., [29] for some specific references). It is usually solved by first performing a local linear approximation to the penalty function (see, e.g., [52] in case of a precision matrix):

with a current estimated entry of in step . Hence, should be taken as (typically, one iteration already suffices for satisfactory results)

| (24) |

which is a weighted covariance graphical lasso problem with weights

We can summarize the values in a block matrix (again similar as in (10)), allowing us to rewrite (24) as

| (25) |

where is the -norm of the vector of all elements contained in , and stands for elementwise multiplication. As illustrated in [4], the optimization (25) consists of a convex part , and a concave part , making the entire problem non-convex (big difference with the precision matrix case, where graphical lasso is convex), i.e., convergence to a global minimum is not guaranteed. Also, when , the solution to (25) will be degenerate because is not full rank. The authors of [4] suggest to use for some in such cases, where is chosen such that, e.g., the resulting matrix has condition number equal to . Still, they encounter difficulties of estimation when . For this reason, we restrict ourselves to in the simulations.

Using a majorize approach, they propose in [4] to solve convex approximations to the original problem in an iterative way. Next to sparsity, their algorithm achieves positive definiteness. Another optimization technique for solving (25) is developed in [49], who uses coordinate descent, resulting in a faster and more stable algorithm. We use this algorithm as it is implemented in [16].

Under a set of typical assumptions, consistency and sparsistency results for the estimator are given in [29]. One of their main conclusions is the preference for non-convex penalty functions such as the scad penalty of [14]:

where . We take because of the arguments given in [14]. Such penalties shrink less entries that are large in magnitude, and as such reduce the bias. Moreover, a strong theoretical upper bound on the tuning parameter , as is needed for, e.g., the lasso penalty (being the limit of for ) in order to guarantee consistency, is not needed, yielding better sparsity properties. So, also in case of sparse covariance matrix estimation, the scad has the oracle property in the sense of [14] (zeroes are asymptotically estimated as zero, and estimated non-zeroes are asymptotically normal).

So far, we have been assuming a multivariate normal model, while the core of this paper is that we merely assume a semi-parametric normal copula model, i.e., within reach is the estimator , and not . As mentioned in [15], who use the term sparse M-estimator, “such estimation problems have benefited from a very limited attention so far”, and “the large sample analysis amply differs from the fully parametric viewpoint”. Recall the sets and introduced for the property of sparsistency. Define also

| (26) |

where denotes the derivative of with respect to , evaluated in , and similarly for the second derivative. The sequence is related to the asymptotic bias of the penalized estimator, and equals for the lasso penalty. Theorem 2 states the consistency and sparsistency of the estimator .

Theorem 2.

Proof.

The conditions (27) and (28) are satisfied by, e.g., the lasso and scad penalty. The condition in (27) is a smoothing condition on the penalty function, and (28) guarantees sparsity in the estimates. However, note that the condition for cannot be fulfilled by the lasso since then . Hence, Theorem 2 does not guarantee sparsistency of the lasso estimator.

Regularized estimation and group sparsity

Recall the second plot in Fig. 3 of Example 4, where entire groups of variables are independent of each other, and/or have no dependence within, resulting in a correlation sparsity pattern with entire zero blocks. A penalty of the form , where is the Frobenius norm and a matrix with ones as off-diagonal elements and zeroes on the diagonal in order to avoid shrinkage of the variances, might lead to an estimator that incorporates this sparsity structure. The non-differentiability of at allows to simultaneously shrink all entries of a certain block, and hence performs a group selection. For actually computing , a local linear approximation of can again be performed, which will boil down to a similar problem as finding in case of the lasso penalty . So, let us assume from now on that . The ideas explained in [49], which we use for numerically finding , can in general not be used for finding , because some of the arguments do not apply to the Frobenius norm. Nevertheless, the problem

| (29) |

has a solution in the form of an elementwise soft thresholding operation. Denoting for the ’th element of the ’th block of , similarly for , and further

it is known that (similar to, e.g., Proposition 1 in [6])

Hence, we can numerically compute by using ideas similar to the optimization approach of [4], i.e., by majorizing by its tangent plane and using generalized gradient descent steps, which comes down to iteratively solving (convex) problems of the form (29). For the actual implementation, we used to code available in [5], and fine-tuned it such that it can also cope with a group lasso penalty. Regarding the asymptotic properties, it is intuitively clear that a result similar to Theorem 2 will hold, with sparsistency formulated at the level of blocks instead of individual elements. For asymptotic properties in case of truly independent copies, we refer to Section 3 of [6].

4.2 Dimension depending on the sample size

So far, we have been assuming that the total dimension of the random vector remains fixed with . When for depending on , of primary interest might be the behaviour of the empirical Gaussian copula covariance matrix given in (10). Proposition 4 (see D for a proof) tells us how the dimension influences the consistency of the estimator in max norm .

Proposition 4.

Let be a sequence of dimensions depending on , and corresponding Gaussian copula covariance matrices. Assume that , where denotes the maximum eigenvalue, and let be the estimator given in (10) with . Then, it holds that

for .

So, Proposition 4 ensures that is a consistent estimator as long as as , i.e., as long as we are not in an ultra-high dimensional setting. In the context of the penalization techniques, one can also assume that depends on . For the ridge regularization, this will lead to inconsistencies in high-dimensional settings, see Section 3.1 in [50] (basically because sample eigenvalues are known to be inconsistent when ). Regarding the penalties, Theorem H.1. in [15] states that

where , and under the additional conditions (next to those of Theorem 2) that and for . Hence, is allowed to increase with , but consistency requires . If, in addition (see Theorem H.2. in [15]), and for , true zeroes are asymptotically identified with probability one (but there might still be some false positives).

5 Simulation study

The aim of this section is to empirically study the finite sample performance of the (non-)regularized plug-in estimators for the Gaussian copula based dependence coefficients and discussed in Section 3. The finite-sample distribution of the estimator of Section 3, is investigated in Section 5.1, and the regularized estimators are considered in Section 5.2.

5.1 Finite-sample performance of the estimator of Section 3

Theorem 1 gives an asymptotic normality result with explicit asymptotic variance for the estimator for , with the matrix of sample normal scores rank correlations given in (10). Let now be the plug-in estimator of the asymptotic standard deviation obtained by replacing with . By simulating a sample from a certain multivariate distribution having a Gaussian copula, we can compute a realization of the actual sampling distribution of the studentized estimator , and several replications can be used to represent characteristics of the entire distribution, which should approximately (for large ) be a standard normal one according to Theorem 1.

We consider four settings which we can generate samples from:

-

1.

Setting 1: , with standard normal marginals and a Gaussian copula having an autoregressive AR(1) correlation matrix with (i.e., the ’th element of equals ).

-

2.

Setting 2: as Setting 1, but now with marginals

-

(a)

a distribution with degrees of freedom for

-

(b)

an exponential distribution with mean for

-

(c)

a beta distribution with parameters and for

-

(d)

an -distribution with degrees of freedom and for .

-

(a)

-

3.

Setting 3: similar to Setting 1, but with .

-

4.

Setting 4: , with standard normal marginals and a Gaussian copula having an equicorrelated correlation matrix with .

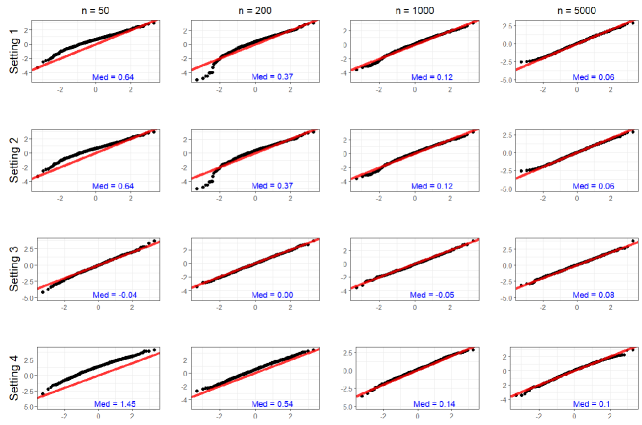

Each time, we draw samples of sizes and make standard normal Q–Q plots to assess the goodness-of-fit with a standard normal distribution. See Fig. 4 for the results in case of . Similar plots are obtained for . In each setting, there is a qualitative fit with the standard normal distribution for larger sample sizes. Changing the marginals has no influence (Setting 1 versus Setting 2). Small correlations (Settings 1 and 2), yield a more pronounced lack-of-fit than higher correlations (Setting 3). Increasing the total dimension to (Setting 4) results in a large positive bias for small sample sizes, calling for regularization techniques.

Next, in Fig. 2, asymptotic standard deviations and were shown in the context of Example 3. Generating samples from, e.g., a multivariate normal distribution with mean zero and covariance matrix given in (18), we obtain estimates , whose sample standard deviation multiplied with , say , can be seen as an approximation for when is large. Fig. 5 depicts for different values of and in case and . We see the same patterns popping up as in Fig. 2, illustrating the asymptotic variance formula given in Theorem 1 empirically in this particular setting.

5.2 Penalization techniques

We now turn our attention to the different covariance matrix penalization techniques discussed in Section 4. We start with illustrating ridge regularization, in particular the improvements it gives in plug-in estimation of Gaussian copula based dependence coefficients between multiple random vectors. We do this for increasing values of , possibly larger than . Recall that the ridge estimator is rather easy to compute, and there are no additional difficulties when . This study thus also allows for an impression on how the dependence coefficients behave with increasing . Afterwards, we go to sparsity inducing (group)-lasso type methods, and investigate for two fixed values of and different sample sizes (with ) their ability of recovering marginal independencies (interpretability) on the one hand, and whether this improves the estimation of the dependence coefficients (accuracy) on the other hand.

Ridge regularization

As explained in Section 4, the ridge estimator of the Gaussian copula correlation matrix tries to cope with biased eigenvalue dispersion of the empirical correlation matrix which aggravates when is large compared to . Moreover, it is easy to implement (with a straightforward cross-validation procedure for selecting the penalty parameter ), and guarantees a positive definite outcome. One can expect that the performance of the estimator is better than the performance of when is large compared to . To demonstrate this, we consider the following two designs:

-

1.

Design 1: We let and with , e.g., if , we are measuring the dependence between random vectors of dimension

-

2.

Design 2: We let and with , e.g., if , we are measuring the dependence between random vectors of dimension .

In each design, we generate samples of sizes from a distribution (but, assume unknown marginals), where is the correlation matrix of an process with , and compute the empirical mean squared error of and .

The penalty parameter is determined by -fold cross-validation (as described by equation (4) in [50]) on a grid of equidistant elements in . In addition, we do the same for two Gaussian copula-based -dependence measures discussed in [12], known as the (normalized) mutual information and Hellinger distance, respectively given by

| (30) |

where is given in (4), and denotes the determinant. Note that the dependence coefficients in (30) depend on products of eigenvalues (they are based on divergences of copula densities), while and depend on sums of eigenvalues (arising from the Bures-Wasserstein distance).

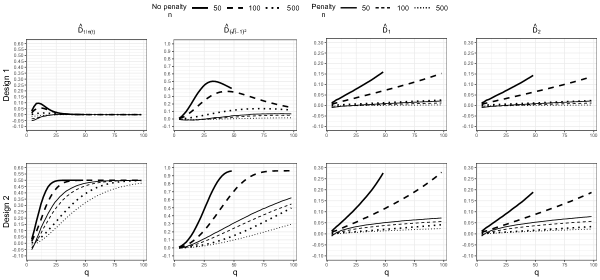

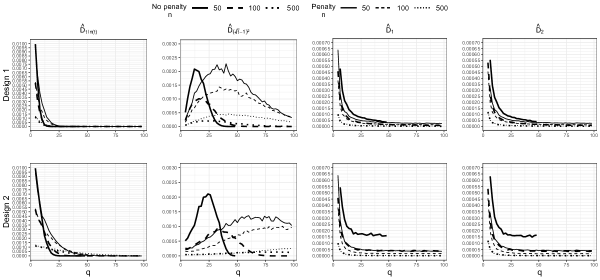

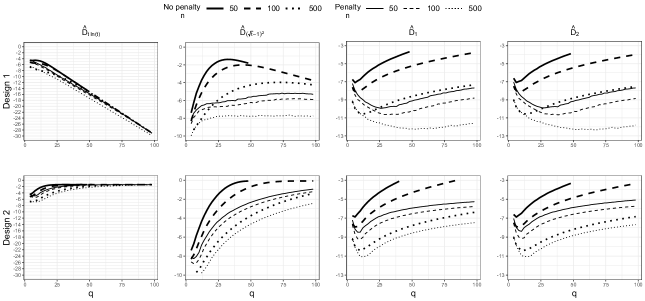

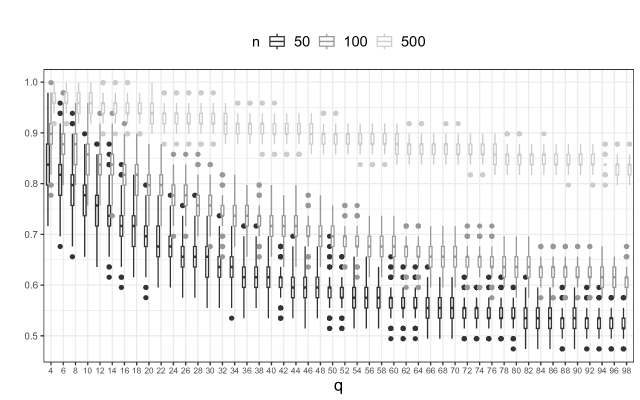

Fig. 6 shows plots of the logarithm of the Monte Carlo mean squared error of (penalty) and (no penalty) for the four dependence measures for each sample size in both designs as a function of . In all cases, we see vast improvements when using ridge regularization, especially when is small compared to (note that when and , the estimators are not defined because of singularity of . Fig. 7 shows boxplots of the selected values for the penalization parameter . We clearly see compatibility with the theoretical property that tends to one in probability when , and higher dimensions require a larger correction of the eigenvalue dispersion, i.e., a smaller .

Finally, Fig. 6 also indicates that it would be interesting to study the behaviour of the dependence coefficients when , which can happen in multiple ways. In the first design for example, remains fixed for all , but . Because -dependence measures satisfy Axiom (A4) of A (see, e.g., [12]), we know that when , which is probably why the mean squared error of first increases and afterwards decreases/becomes constant (in particular, the variance tends to when , and the bias decreases/becomes constant, see Fig. S1 and S2 of the Supplementary Material for plots of the bias and variance). Regarding the optimal transport dependence measures and , we expect them (based on our simulations) to converge to when , probably because the strong normalization (denominator) grows faster than the numerator does. We see the variance of decreasing in , and the biases increasing in .

In the second design, remains fixed, but . The optimal transport measures seem (in our simulations) to converge to zero again, while the -dependence measures remain constant. We leave a formal study of the behaviour of these dependence coefficients when for further research.

(Adaptive/Group) lasso-type estimation

Recall the two different sparsity patterns discussed in Example 4 for a correlation matrix. By performing lasso-type estimation, we hope to recover zero entries (interpretability) on the one hand, and improve accuracy on the other hand. In particular, for the latter, we desire better performance of the plug-in estimator than of the non-penalized estimator , where is a certain correlation matrix based dependence coefficient.

For the simulation, we consider the following correlation structures

-

1.

Scenario 1: We take with , and having the non-block sparse correlation structure given in the left plot of Fig. 3, with zeroes.

- 2.

-

3.

Scenario 3: We take with , and such that there is only dependence with and within , yielding a block sparse correlation structure, with zeroes.

Each time, we generate samples from a distribution (marginals are again assumed to be unknown), and compute the no penalty, lasso, adaptive lasso (of [16] with and tuning parameter ), scad, and group lasso estimator for . The considered sample sizes are for Scenarios 1 and 2, and for Scenario 3. Based on the replications, we report on the average true positive rate (TPR), which we want to be close to one, and false positive rate (FPR), which we want to be close to zero. We also compute the empirical root mean squared error of (where is the estimated correlation matrix in question), and empirical mean squared error of , with the mutual information , Hellinger distance , or one of the optimal transport dependence measures or .

For tuning (or in case of the adaptive lasso), we use the BIC criterion (see, e.g., [17] for the case of a precision matrix in Gaussian graphical models):

| (31) |

where is the estimated candidate covariance matrix using the penalty parameter . We want to maximize (31) in . We do this over an equidistant grid of values in . The number stands for the degrees of freedom, and is estimated for the (adaptive) lasso and scad by the number of non-zero entries in , not taking the elements under the diagonal into account. For the group lasso, the degrees of freedom can be estimated in a similar spirit as equation (23) in [9]:

where is the ’th block of , similarly for , and is a matrix with ones as off-diagonal elements and zeroes on the diagonal. The results are summarized in Table 1.

In Scenario 1 (, no block sparsity, zeroes), there is no group sparsity, which results in low TPR (and also low FPR, since only few entries get shrunk to zero) for the group lasso estimator. The other penalization techniques are, as expected, preferred for recovering zeroes. Clearly, any type of considered penalization yields more accurate estimation of in Frobenius norm than in case no penalty is used. However, this does not necessarily imply better estimation of the dependence coefficients, especially for lasso and scad. For good estimation of these, it is important not to lose sight of the non-zero entries, which is why the adaptive lasso performs really well. Note that the mutual information is estimated very well in the non-penalized case, but this is mainly due to the fact that the true value equals , which is very close to one, being an effect of the dimension (recall also Fig. 6). All non-penalized mutual information estimates are close to one because of a relatively large , yielding low estimation error.

In Scenario 2 (, block sparsity, zeroes), all penalization techniques perform well in identifying zeroes. For obtaining both high TPR and low FPR, the group lasso performs slightly better than lasso and scad. Also, when the focus is on estimating , penalization is clearly beneficial, and the group lasso outperforms the other techniques. Regarding the dependence coefficients, we see that, for the optimal transport measures, lasso and scad give improvement compared to using no penalty, especially for smaller sample sizes. The error of the -dependence

| Scenario 1 (, no block sparsity, zeroes) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| n | TPR | FPR | |||||||

| \hdashline | |||||||||

| no penalty | |||||||||

| \hdashline | |||||||||

| lasso | |||||||||

| \hdashline | |||||||||

| adaptive lasso | |||||||||

| \hdashline | |||||||||

| scad | |||||||||

| \hdashline | |||||||||

| group lasso | |||||||||

| Scenario 2 (, block sparsity, zeroes) | |||||||||

| n | TPR | FPR | |||||||

| \hdashline | |||||||||

| no penalty | |||||||||

| \hdashline | |||||||||

| lasso | |||||||||

| \hdashline | |||||||||

| adaptive lasso | |||||||||

| \hdashline | |||||||||

| scad | |||||||||

| \hdashline | |||||||||

| group lasso | |||||||||

| Scenario 3 (, block sparsity, zeroes) | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| n | TPR | FPR | |||||||

| \hdashline no penalty | |||||||||

| \hdashline lasso | |||||||||

| \hdashline adaptive lasso | |||||||||

| \hdashline scad | |||||||||

| \hdashline group lasso | |||||||||

estimates is rather low in case no penalty is used, which is again an effect of the dimension. Aside from this, the group lasso or the adaptive lasso (especially for larger sample sizes) gives the lowest error.

In Scenario 3 (, block sparsity, zeroes), the group lasso is again desirable for exploiting the sparsity structure, and even achieves zero FPR. For accurate estimation of in Frobenius norm, the group lasso also performs best. Most accurate estimation of dependence (except for the mutual information, where no penalty performs best because the true value is again very close to one) is obtained by the group lasso when , and by the adaptive lasso when is large compared to .

In conclusion, when the true correlation matrix is sparse, interpretability can be enhanced by using a penalty that is able to completely shrink entries to zero. The group lasso is preferred for obtaining both good TPR and FPR when this sparsity is at the block level (Scenarios 2 and 3), and also performs well in estimating dependence in such cases, particularly when is rather small. The true is estimated more accurately (compared to using no penalty) in Frobenius norm when using any penalty and in any scenario, but this does not necessarily result in better estimation of dependence. Especially when there are still quite some non-zeroes (Scenario 1), but also when is rather large, adaptive lasso is recommended for good accuracy of the estimated dependence coefficients. The -dependence measures are estimated with rather low error when using no penalty, but this is because they attain their upper bound of rather quickly when the dimension increases.

6 Real data applications

In Section 6.1, we look into an application of optimal transport dependence measures between possibly more than two random vectors to sensory analysis. In Section 6.2, we illustrate how these measures, together with the considered penalization techniques, can be useful in finding clusters among speech signal attributes used for detecting Parkinson’s disease.

6.1 Application to sensory analysis

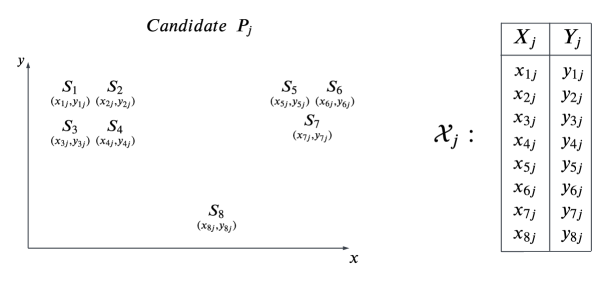

Consider a caterer who wants to sell eight different smoothies, say , on an event, and is looking for three employees willing to take up this job. A total of people, say , show up for this job opportunity, all equally qualified, and the caterer is looking for a fair way to pick three candidates. Every candidate is asked to taste each of the eight smoothies, and is given a sheet of paper in order to position the different smoothies, knowing that the closer certain smoothies are to each other, the more similar they are considered by the individual. For example, according to candidate in Fig. 8, the smoothies and are similar, but quite different from the similarly tasting smoothies and , and none of them resembles .

As such, the caterer acquires datasets, say for , containing the smoothies as rows and the - coordinates on the sheet of paper for person , denoted as a random vector , as columns, representing the smoothie similarities of each candidate. So, the dataset contains a sample from of size eight, denoted as for . The data is available in the R package SensoMineR ([30]). The criterion based on which three employees are picked consists of finding the three individuals that have the least similar spatial configurations, meaning three very diversified tastes (in the hope of not selling only a few smoothies because of prepossessed preferences by the sellers).

Typically, see, e.g., [32], the similarity between two configurations is measured by the RV coefficient

| (32) |

and for three configurations one can take, e.g., the average of all pairwise RV coefficients. Yet, pairwise coefficients feel unnatural and it would be better to compute a trivariate vector similarity. Note that (32) is actually the RV coefficient between two random vectors and of size two having joint, empirical covariance matrix

and we get a similar (larger) block covariance matrix in when taking individuals into account.

Since not restricted to two random vectors anymore, one can also opt for an (estimated) optimal transport dependence coefficient or between three vectors of size two for measuring the similarity between three individual spatial configurations. Note that the dispersion of the coordinates might differ among the individuals (some might use the entire sheet, while others only use the right corner), but since we use the normal scores rank correlations, we do not need any centering or scaling of the data. Pairwise scatterplots of the normal scores of the - coordinates of the people are shown in Fig. S3 of the Supplementary Material, indicating that dependencies are mainly correlation based, i.e., a Gaussian copula model is suitable for modelling the dependencies. When zooming in on candidates and , we get the pairwise scatterplots given in Fig. 9. From this, we expect for example that candidates and have quite independent smoothies preferences, while candidates and have rather strong correlations between their coordinates.

| two based on | two based on | three based on | three based on | ||||

|---|---|---|---|---|---|---|---|

| \cdashline1-2 \cdashline3-4 \cdashline5-6 \cdashline7-8 | |||||||

| ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ | ⋮ |

We denote and for the estimated similarity between two candidates or three candidates for . Recall that these are actually dependencies between and random vectors of size respectively, i.e., with , or with respectively, estimated based on a sample of size .

Table 2 shows the two strongest and two weakest couples or triplets according to or . The caterer will definitely hire candidate and . In [32], they cluster the candidates using the clustatis method, bringing forward three classes of individuals, see their Fig. 5. We see that belongs to class , while belongs to class and to class , also indicating their diversified smoothie similarity pattern. The optimal transport dependence measures give an unequivocal ordering of patterns based on similarities that go beyond two random vectors.

Note that we can also switch the role of the smoothies and the individuals, i.e., construct datasets in , and similarly look at the dependence between smoothies. Doing so, both and agree that and are the least similar among all possible triplets. They are respectively called Casino_PBC, Innocent_SB and Carrefour_SB, and the biplots (based on various sensometrics methods) in Fig. 2. of [32] indeed also reveal angels between these smoothies that are close to . So, and would be a good choice if the caterer wanted to limit his smoothie supply to three flavours that still have a satisfactory amount of diversity.

candidates and of the smoothies dataset.

6.2 Clustering dysphonia measures

In a second real data application, we study the LSVT voice rehabilitation dataset of [47], freely accessible at the UCI Machine Learning Repository (https://archive.ics.uci.edu/dataset/282/lsvt+voice+rehabilitation). Parkinson’s disease frequently leads to vocal impairment, the extent of which can be assessed using sustained vowel phonations. In particular, the sustained vowel “ahh…” (denoted as /a/) is typically studied. Next, dysphonia measures are used to extract clinically useful information from speech signals. The dataset consists of such measurements on phonations. As mentioned in Section C of [47], several of these dysphonia measures are similar (algorithmic variations of the same basic ideas), e.g., there are many jitter (a measure of cycle-to-cycle variation in frequency) and shimmer (a measure of cycle-to-cycle variation in amplitude) variants. Hence, there is a large amount of redundancy among the attributes, which could worsen the performance of supervised learning (like, e.g., a classifier as studied in [47]), and some kind of preliminary feature selection is recommended.

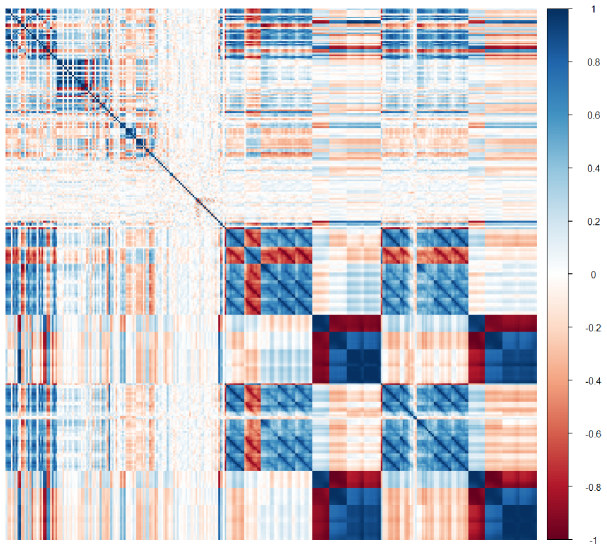

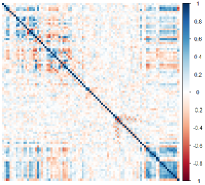

There are indeed many dysphonia measures that exhibit a (very) strong sample normal scores rank correlation, see Fig. S4 of the Supplementary Material. In order to eliminate strong detrimental redundancies (that closely approach singularity), we iteratively search (pairwise) for attributes that have a normal scores rank correlation larger than in absolute value, and each time discard one of them. Remaining are dysphonia measures, whose (non-singular) sample normal scores rank correlation matrix is given in the left panel of Fig. S5 of the Supplementary Material.

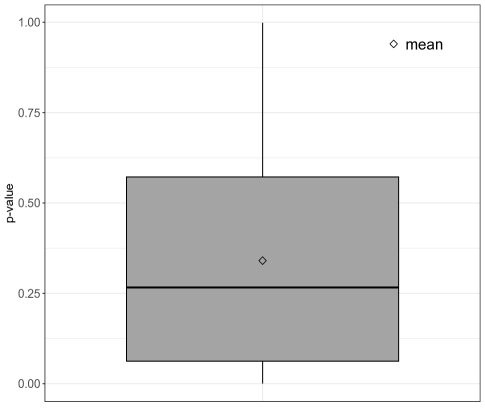

For testing the adequacy of a Gaussian copula for modelling (at least pairwise) dependencies, we consider the test based on the statistic given in equation (2) of [21], where we test the null hypothesis that the copula between a pair of dysphonia measures is Gaussian, and compute the -value based on bootstrap samples. In Fig. 10, a boxplot of -values of pairwise (that is between all pairs of variables) goodness-of-fit tests is shown. Based on the boxplot, we see that is it reasonable to assume (at least pairwise) Gaussian dependencies.

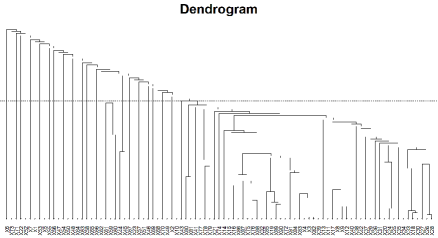

We still have quite a large amount of attributes compared to the sample size of , and we still see some quite large correlations between several first and last dysphonia measures (right upper corner of left panel in Fig. S5), so further feature selection is desired. With this objective in mind, we decide to cluster the remaining attributes in order to get an idea about how they can be divided into properly separated groups that have rather strong similarity within.

In particular, we opt for agglomerative hierarchical variable clustering based on similarity measures (see, e.g., [19] and references within for a survey), where the main task is to measure the similarity, say (or alternatively dissimilarity), between two groups of variables and . Denote for the dysphonia measures, which are initially considered to be clusters on their own. In the first step, the two variables and (for certain with ) that exhibit the largest similarity according to , i.e., taking and , are merged together forming one single cluster. Next, all similarities between the current clusters are again computed, and the two clusters showing the largest similarity are merged. One keeps repeating this until only one big cluster (composed of all the attributes) remains, yielding a total of partitions of the attribute space. In general, the main task is thus to compute (for and )

| (33) |

for certain mutually exclusive . Typically, one specifies a certain (estimated) bivariate dependence coefficient and a certain link function (overlooking multivariate dependence structures) for computing (33), or (estimated) multivariate concordance measures (between univariate random variables) have also been studied (see, e.g., [19]). We decide to take for (33), and as such measure the similarity between clusters (in spite of possible similarity within), which feels more natural and does not require a link function. This is taken to be , where is the ridge penalized estimated Gaussian copula correlation matrix (23), keeping in mind that the total dimension in (33) might be large compared to . The tuning parameter is again determined by a -fold cross-validation search on a grid of equidistant elements in .

We obtain partitions, and one of these should be picked as preferable clustering of the attributes. Since not restricted to two groups, we can also use for measuring the similarity between clusters comprising a specific partition. This in fact measures how separated the obtained clusters of that particular partition are, i.e., it is a measure of redundancy among the clusters of attributes, which we want to be rather small. The dendrogram of the clustering procedure and redundancy as a function of the number of clusters (for each of the obtained partitions) are shown in Fig. 11. Based on this, we decide to look deeper into the cluster partition (where the dotted line cuts the dendrogram), since the redundancy is minimal here (in particular, ). Next, we rearrange the attributes such that dysphonia measures that belong to the same cluster follow each other in the dataset, and the cluster dimensions are

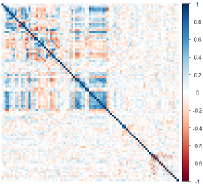

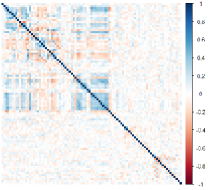

i.e., there is a big cluster of size , two smaller clusters of size and , and clusters of size . The sample normal scores rank correlation matrix after rearrangement, estimated without a penalty and with a ridge penalty are respectively given in the middle and right panel of Fig. S5 in the Supplementary Material.

Denote now the clusters as random vectors . We already know that when using ridge penalization (), which is already way closer to than when using no penalization (then ). Moreover, the rationale behind variable clustering is that clusters are truly separated, i.e., there is (block) sparsity in the Gaussian copula correlation matrix at levels corresponding to attributes belonging to different clusters.

Therefore, we also consider lasso, adaptive lasso, and group lasso estimation of the Gaussian copula correlation matrix. For the lasso and group lasso, we search for an optimal on an equidistant grid of values in , and for the adaptive lasso, we search for an optimal on an equidistant grid of values in , each time aiming to maximize the BIC (31).

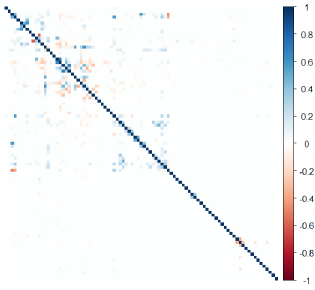

The first panel in Fig. 12 shows the sparse structure of the estimated normal scores rank correlation matrix of the clustered attributes when using the lasso. To a certain extent, we recognize the diagonal blocks corresponding to the within cluster correlations, and observe many zeroes between attributes belonging to different clusters. The estimated inter-cluster dependence equals . Using the adaptive lasso (second panel), we get , and a group lasso estimator (third panel) results in . Note that the group lasso estimator did not shrink any of the diagonal blocks, reflecting the stronger intra-cluster similarities. In the fourth panel of Fig. 12, we visualize a group lasso estimate with a larger penalty parameter (not determined through BIC). When forcing more sparsity by increasing , we see more off-diagonal blocks (and not diagonal blocks) getting shrunk, and this leads to . More detailed images are given in Fig. S6 of the Supplementary Material.

Further feature selection can now be done via replacing each cluster by a single (or maybe multiple) attribute that represents the cluster well (e.g., the attribute within the cluster that has largest similarity with the cluster).

7 Discussion

In this paper, we proposed to use the -Wasserstein distance between the joint copula measure and the product of the marginal copula measures for quantifying dependence between a finite, arbitrary amount of random vectors. The obtained dependence coefficients satisfy several desirable properties and especially have the powerful theoretical quality of detecting any departure from independence. Examples illustrate that the choice of normalization strongly influences the overall dependence quantification. Whether or not one can explicitly calculate the infimum for the optimal transport map and/or the supremum required for the normalization, depends on the specific form of the copula, and a great deal of interesting work remains to be done (also when no explicit copula can be assumed, i.e., when nonparametric estimators need to be considered).

A Gaussian copula approach yields explicit formulas with a clear interpretation. Using the sample matrix of normal scores rank correlation coefficients results in an easily computable plug-in estimator for which we obtained an asymptotic normality result with explicit asymptotic variance in arbitrary dimensions. Expectedly, higher dimensions aggravate the finite sample estimation performance. To cope with this, we studied rank-invariant penalization techniques for estimating the Gaussian copula correlation matrix, leading to estimators that are able to improve accuracy on the one hand, and enhance interpretability by detecting marginal independencies on the other hand. Such estimation challenges have enjoyed rather little attention, and further research would definitely be worthwhile.

Another interesting theoretical challenge is to study the optimal transport (and others as well) dependence coefficients when the dimension grows unboundedly. In the Gaussian copula context, random matrix theory could definitely be useful, and, as also touched upon in our simulations, various behaviours can be expected depending on the nature of the dependence measure, the normalization, whether letting for some , or . Keeping the dimension fixed, our simulations illustrated the asymptotic normality result and the benefits of using penalization techniques when the sample size is rather small and/or when (group) sparsity is pursued.

Finally, in a first real data application, we illustrated the use of the dependence coefficients in evaluating and comparing (possibly more than two) consumer products or similarities in sensory analysis. Alongside, on a second real dataset containing expressions on sustained vowel phonations, we demonstrated how attributes can be hierarchically clustered via multivariate similarities between random vectors (despite similarities within), disposing of traditional link functions. Ridge penalization is preferred when the number of attributes is large compared to the sample size, and (group)-lasso type penalties can be used to reflect the homogeneity and separation of a partition of, in general , groups of variables.

Acknowledgments. The authors thank Dr Gilles Mordant, Georg-August-Universität Göttingen, for scientific discussions during the startup phase of this research. The authors gratefully acknowledge support from the Research Fund KU Leuven [C16/20/002 project].

Appendix A Axioms for dependence measures between random vectors

In [11], a list of axioms is stated for a dependence measure . Up to some minor differences (small corrections and simplifications), the axioms are given as follows.

-

(A1)

For every permutation of : : and for every permu- tation of , : .

-

(A2)

.

-

(A3)

if and only if are mutually independent.

-

(A4)

with equality if and only if is independent of .

-

(A5)

is well-defined for any -dimensional random vector (even if there is a singular part in the distribution of ).

-

(A6)

is a function of solely the copula of (which is equivalent to being invariant under strictly increasing transformations of any of the components of ).

-

(A7)

Let be a strictly decreasing, continuous transformation for a fixed and a fixed . Then

where .

-

(A8)

Let be a sequence of -dimensional random vectors with corresponding copulas , then

if uniformly, where denotes the copula of .

Appendix B Proofs of theoretical results of Section 2

B.1 Proof of Lemma 1

For (a), let with be a random vector with distribution and let with be a random vector with distribution , as marginal distribution of an arbitrary coupling of , and having marginals itself. Then, the distribution of is a coupling of and for all such that

| (34) |

Taking the infimum over all couplings yields the result. Part (b) follows immediately from the definition.

Regarding (c), if for all , we have , making the statement trivial since defines a metric. Suppose now that is absolutely continuous for all and . The latter means that, working further on the proof of (a), there exists a minimizing the left-hand side of (34), and with equality instead of inequality. Hence, the -Wasserstein distance between and is obtained at the coupling distribution of coming from , for all . However, Brenier’s theorem (see, e.g., Theorem 2.12 in [48]) tells us that, since is absolutely continuous, this optimum is uniquely and deterministically attained, i.e., (denoting for the gradient) there must exist convex functions such that almost surely for all . Since are independent, this implies that are independent and thus .

We next prove statement (d). The -compactness of follows from the well-known result that if is -convergent, then it is also weakly convergent (see, e.g., [10]) and the limit will again be in as the marginals remain fixed. Finally, let us consider a fixed and arbitrary . Take an arbitrary such that , where we pick such that with . We also denote . It holds that

where we used that because of the triangle inequality (recall that defines a metric). This finishes the proof of statement (d). ∎

B.2 Proof of Proposition 1

We start with proving (A4) for . Suppose we consider an additional random vector having copula measure , an additional absolutely continuous reference measure , and let be the copula measure of . If we first assume that is independent of , we have and hence

such that the Wasserstein dependence measure remains unchanged when adding into consideration. In general, suppose that is an optimal transport map from to , as joint distribution of with and , i.e.,

where the inequality follows from the definition of the Wasserstein distance. If this inequality is an equality, it must hold that

from which

Because of the absolute continuity of the , the latter implies (using Brenier’s theorem) that there exists such that almost surely, while the former means that there exist such that almost surely for all . Since is independent of , this shows that is independent of , i.e., and thus independent from .

The fact that satisfies (A1)-(A3),(A5),(A6) follows from basic properties of copulas and Lemma 1.

In the context of property (A7), assume without loss of generality that gets transformed to for a strictly decreasing transformation and let be the copula distribution of with . Then, with and . Suppose now that is an optimal transport map from to , as joint distribution of , i.e.,

Consider then , which clearly is a coupling of and , as joint distribution of with and . Moreover, putting , we have

by simply doing a substitution . Following a reversed reasoning, we also obtain and hence . Similarly, we can show that where is the copula distribution of and hence conclude (A7).

Finally, for (A8), we want that if uniformly for , it is true that

| (35) |

as . Note that if uniformly, we also have as for every (Helly-Bray theorem). Since convergence in distribution together with convergence of the first two moments implies -convergence, equation (35) is proven by using similar arguments as for (d) of Lemma 1. ∎

Appendix C Proofs of theoretical results of Section 3

C.1 Proof of Proposition 2

The first step of the proof consists of showing that the eigenvalues of are indeed given by (8). Therefore, already note that because of the orthogonality of the matrix

denoting for a matrix of zeroes, the eigenvalues of are the same as those of

| (36) |

which we can find explicitly. Let be the -th canonical unit (column) vector in and put . For ease of notation, we also write if . We now list the eigenvalues and eigenvectors of the matrix .

-

1.

For all and all , the vector

(37) denoting for a column vector of zeroes, is an eigenvector of with eigenvalue

(38)

Indeed, when fixing a certain and , the -th block row of (36) for , multiplied with (37) equals

since , as . If for , we multiply the -th block row of (36) with (37), we obtain

since , as . Hence, for every , the -th block element (in ) of the matrix multiplication of with the vector (37), is equal to (38) multiplied with the vector (37). This shows what was desired, and delivers eigenvalues.

-

1.

For all , the vector

(39) is an eigenvector with eigenvalue

Indeed, following the previous result, it is straightforward to see that for , the multiplication of the -th block row of with the vector (39) equals , as , while the last block row leads to . This gives an additional amount of eigenvalues, resulting in an intermediate total of eigenvalues.

-

1.

For all and all , the vector

(40) is an eigenvector with eigenvalue .

Indeed, when fixing a certain and , the -th block row of (36) for multiplied with (40) equals

since . For , we get

since , as . For , we get

since , as . Finally, for , we obtain

since , and we come by eigenvalues, resulting in the desired total of eigenvalues. These are indeed given by

Next, we need to show that for an arbitrary with eigenvalues , it holds that

| (41) |

For this, we first introduce some notation. We know that must be of the form

with . Based on this, define the matrices

where , for all . We will approach as a block matrix consisting of four blocks. Note that and . Further, put

Then, by applying Theorem 1 in [46] to for an arbitrary and also to , we can pick any satisfying

and integers

that, defined as such, will guarantee that

| (42) |

Notice that (42) describes a total of inequalities. We will now prove (41) by making an adequate choice for the and corresponding indices . In particular, when considering a fixed and fixed , take

Then, concerning the ’ th and ’ th inequality of (42), we see that if , we have

| (43) |

and,

| (44) |

Since , we see that (43) and (44) are equal. If on the other hand , we get

| (45) |

and,

| (46) |

Again because , we have equality between (45) and (46). We thus have shown so far that the second term on the right side of the ’ th inequality of (42) equals the term on the left side of the ’ th inequality. Now, concerning the ’ th and ’ th inequality for , we must have either both or both , or meaning . In the first case, it holds that

and

| (48) |

Since and (by construction, hence they also have the same eigenvalues), we see that (C.1) is equal to (48). For the second case, i.e., both , we have

| (49) | ||||

and

| (50) |

For the same reasons as in the previous case, we clearly see that (49) and (50) are the same expressions. Finally, if ,

| (51) | ||||

and,

| (52) |

Since and , we also have equality between (51) and (52). All together, we have proven that the second term on the right hand side of the ’ th inequality of (42) is equal to the term on the left hand side of the ’ th inequality for all . Hence (42) can be reduced to

| (53) |

Moreover, since by choice for all if , or for all and for all if , and for all , we definitely have

| (54) |

The inequality in (54) is an equality if there are eigenvalues equal to zero. If for example and , this means that eigenvalues should be zero, which is the case for the matrix . Combining (53) with (54) and realizing that the eigenvalues are the same as the eigenvalues , since , finishes the proof. ∎

C.2 Proof of Proposition 3

Consider an arbitrary having ordered eigenvalues . Then, by definition of the Bures-Wasserstein distance (3),

| (55) |

Notice that the function is convex for . By Proposition 2, we know that the eigenvalues of majorize those of . From Lemma 2, it follows that (55) is maximal if . Secondly, we have

Recall that is the eigendecomposition of for , and for we have . Hence, we get

which is of the same form as , but with and replaced by and . Applying Proposition 2 with instead of for , it follows that the eigenvalues of an arbitrary matrix in are majorized by those of the matrix . Hence,

| (56) |

with the eigenvalues of . The fact that (56) is maximal if now follows from the convexity of the function on and Lemma 2. ∎

C.3 Additional lemmas and proof of Theorem 1

Lemma 3.

Proof.

Define the map via being the diagonal matrix whose diagonal is equal to the eigenvalues (counting multiplicities) of in decreasing order. Then, we have for . Also define the map

where the Frobenius norm is naturally defined for a certain through . Using Lemma 3 of [36], it is then quickly seen that the Fréchet derivative of at in the direction of a certain is , with the diagonal matrix containing the diagonal of . Consider now (recalling that )

with the eigenvalues of in decreasing order for and , and putting for . We see that , also putting for . The Fréchet derivative of at in the direction of equals , where satisfies

| (57) |

Defining for all and , as well as for , it is obvious that the eigenvalues of are . Moreover, since we assumed that the eigenvalues are distinct over , it will hold, for small enough, that are in decreasing order again over . Hence, using our definition of , we see that (57) becomes

| (58) |

From expression (58), we observe that is nothing more than the total derivative of the function

at evaluated in . Computing the Jacobian matrix of , we find

By the chain rule, we have just shown that

where is the diagonal block of . Using the notations (11), (12) and (13), we can further simplify the above expression into

where we used that for square matrices , the cyclic permutation property of the trace operator, the fact that and finally the identity for matrices . ∎