The PEAL Method: a mathematical framework to streamline securitization structuring

Abstract

Securitization is a financial process where the cash flows of income-generating assets are sold to institutional investors as securities, liquidating illiquid assets. This practice presents persistent challenges due to the absence of a comprehensive mathematical framework for structuring asset-backed securities. While existing literature provides technical analysis of credit risk modeling, there remains a need for a definitive framework detailing the allocation of the inbound cash flows to the outbound positions. To fill this gap, we introduce the PEAL Method: a 10-step mathematical framework to streamline the securitization structuring across all time periods.

The PEAL Method offers a rigorous and versatile approach, allowing practitioners to structure various types of securitizations, including those with complex vertical positions. By employing standardized equations, it facilitates the delineation of payment priorities and enhances risk characterization for both the asset and the liability sides throughout the securitization life cycle.

In addition to its technical contributions, the PEAL Method aims to elevate industry standards by addressing longstanding challenges in securitization. By providing detailed information to investors and enabling transparent risk profile comparisons, it promotes market transparency and enables stronger regulatory oversight.

In summary, the PEAL Method represents a significant advancement in securitization literature, offering a standardized framework for precision and efficiency in structuring transactions. Its adoption has the potential to drive innovation and enhance risk management practices in the securitization market.

1 Unboxing securitizations

1.1 Introduction

Securitization is a financial process where the cash flows of income-generating assets are sold to institutional investors as securities, liquidating illiquid assets. Despite securitization modelling complexity, the literature addressing the requisite mathematical modeling is sparse. While there are a few notable exceptions - such as the two excellent books describing in detail the issues encountered in structuring asset-backed securities (Bluhm and Overbeck, 2006; Bluhm et al., 2010) - a comprehensive mathematical framework describing how the inbound cash flows are allocated to the outbound positions is lacking. This paper introduces the PEAL Method, a 10-step mathematical framework designed to streamline securitization structuring while encompassing a comprehensive analysis across all time periods. It offers a standardized mathematical approach adaptable to various scenarios, ensuring compliance with regulations and enabling transparent risk assessment for both the asset and the liability sides. Inspired by Queuing Theory, which elucidates queuing system dynamics, we present securitization as a mathematical study akin to optimizing queuing processes. By establishing a link between inbound and outbound cash flows in 10 steps, our method aims to enhance efficiency and affordability in structuring securitizations, ultimately fostering transparency and regulatory compliance.

1.2 Securitization definition

European Regulation No 2402/2017 (Reg 2402), Article 2(1), defines securitization as a \saytransaction or scheme, whereby the credit risk associated with an exposure or a pool of exposures (Exposures) \sayis tranched, having all of the following characteristics: (a) payments [to the securitization positions (Positions, see definition in Sec. 7.1)] \sayin the transaction or scheme are dependent upon the performance of the Exposures; \say(b) the subordination of tranches determines the distribution of losses during the ongoing life of the transaction or scheme; (c) the transaction or scheme does not create exposures which possess all of the characteristics listed in Article 147(8) of Regulation No 575/2013.

Article 2(1)(a) requires that the payments toward the Positions be dependent upon the performance of the Exposures. Therefore a scheme or transaction is not considered a securitization if the Exposures ongoing losses are always zero . In fact, if this were the case, there would be no credit risk to \saytranche, and thus the letter (b) requirement would not be satisfied. Whilst it is necessary the presence of potential losses, it is not sufficient per sé. Article 2(1)(b) additionally requires to \saytranche the credit risk in such a way that the losses be allocated to the different Positions so as to reflect the subordination of tranches continuously during their ongoing life.

Thus, Reg 2402 defines securitization in mathematical terms: in order to classify a scheme or transaction as a securitization, both the Exposures’ ongoing losses and the Positions’ cash flows must be calculated and jointly analyzed. To our best knowledge, there is no prior paper that has defined a clear relationship between these two elements. Indeed, we aspire to fill this gap, identifying the main inbound and outbound building-blocks needed to structure a securitization and providing a conceptual and mathematical definition of each element individually and in correlation to the others.

This paper111Unless otherwise defined all terms of this paper have the same meaning of Reg 2402. introduces the PEAL Method222PEAL stands for (P)ositions, (E)vents recovery, (A)ssets, and (L)osses and represents the name of the macro building-blocks that are at the basis of the Securitization Theory. that, correlating the inbound to the outbound cash flows, opens up the securitization black-box and enables more sophisticated and robust statistical analyses. Our mathematical approach leaves less room for possible arrangers’ misjudgments, all while easing the Public Authorities supervision.

1.3 Securitization: asset-side basic variables

Let the asset-side of a securitization be composed of portfolios, and let each portfolio have a number of Exposures . Each of the Exposures of portfolio is amortized over months, that are pooled together into the securitization at month (where and ). By exploiting these definitions, let a securitization be Basic when all the portfolios are structured at the same initial time . On the other hand, let a securitization be Rolling when at least one of the portfolios is structured at a time . We indicate by

| (1) |

the total number of Exposures generating inbound cash flows. If

| (2) |

is the duration of each portfolio , then the Exposures maximum duration is

| (3) |

We assume that the time when Exposures are pooled together is

| (4) |

where is the origin of our timeline that, when not differently specified, is . Then for each Exposure we define the installments as

| (5) |

where and are the quota capital and interest of the Exposure amortization schedule. We assume that and be zero outside the time interval where they are defined, i.e for or . Notice that with , the first installment is due at the beginning of the subsequent period . Then, the total capital due by Exposure is

| (6) |

and the outstanding capital of Exposure is

| (7) |

while the total securitization capital is

| (8) |

The total interest due by Exposure is

| (9) |

and the outstanding interest of Exposure is

| (10) |

while the total securitization interest is

| (11) |

We can then define the total securitization outstanding balance as

| (12) |

We call a securitization \sayIslamic when the total interest of any Exposure () is always , and \sayEuropean otherwise. Independently if the securitization were to be Basic or Rolling, Islamic or European, the equations in this paper would hold true.

1.4 Securitization: liability-side basic variables

Let a securitization liability-side be composed of Positions (see definition in Sec. 7). Each of the Positions is amortized over months. All Positions start their amortization period at the same time , and their maximum duration is

| (13) |

where and . Indeed, because there is a mismatch between the inbound and the outbound cash flow lifespan, often : for example, it might happen that the securitization Positions’ lifespan be years while some Exposures might pay installments for years. Currently, most practitioners would discount the extra 2-years Exposures’ cash flows from year -th back to year -th implicitly assuming that the securitization will be able to sell those extra cash flows to interested -rd parties when the time come. This approach is not consistent with a pure cash-flow method, that requires to consider only cash flows that will certainly materialize within the Position maximum duration . Therefore, for the purpose of this paper, any inbound cash flow obtained after will not be considered in computing the Positions’ outbound cash flows (i.e. ).

1.5 Inputs, Events, Scenarios & Clusters definition

We define as a Base Input any initial parameter to compute the inbound cash flows defined at the time of structuring. We call the set of those unique Base Inputs. We define an Event to be any action or situation that might affect, in positive or negative, the Base Inputs at a certain time . We call the set of those unique Events List of Events or LE. An Event of the LE () may affect each Exposure at a certain time , where . Let us recall that the Kronecker delta symbol is defined as

| (14) |

while the Heaviside theta symbol is defined as

| (15) |

Thus, if any Event of the List of Event affects the performance of the Exposure from (or at) happening at time , then allows us to account for the impact of spot Events, while allows us to account for continuous Events whose impact extends from time on. In the following, to simplify the notation we indicate in formulas with when it does not give rise to ambiguities.

We define a Scenario as a combination of the possible Events affecting the Base Inputs of all the Exposures . We define the Base Scenario as the unique Scenario that is unaffected by any Event. The inbound cash flows computed in the Base Scenario can be considered as the initial estimated \saybudget at the time of structuring of the securitization. The inbound cash flows computed in any other Scenarios will diverge from the Base Scenario for a certain amount: if it is positive it is a gain while if it is negative it is a loss. In all other Scenarios, the probability of each Event affecting each Base Input of any Exposure differs according to their respective risk profile. In every Scenario, each Exposure can be affected over time by one or more elements of the List of Events. Due to the combinatorial explosion problem, it is impossible to use a brute force approach to enumerate the total number of Scenarios underlying the securitization (or even only the number of Scenarios of portfolio ). Thus, it is necessary to use a sampling approach like the Monte Carlo Method. The reason is simple: if we consider only IF an element of the List of the Events materializes, the number of potential Scenarios depends on the number of elements ; such quantity grows exponentially with the number of Exposures composing the portfolios as

| (16) |

On the other hand, for the PEAL Method, it is not only relevant IF an Exposure is affected by an Event, but also WHEN: the impact on its performance can be sensibly different if an Event happens at time or at . Therefore, the probability of the Scenario’s cash flows depends on the probability of each Event impacting over time each Exposure composing that Scenario. Thus, the number of Scenarios for a securitization composed of portfolios, each with Exposures with the same amortization period and the same number of Events is

| (17) |

Thus, for example for a securitization composed of just one portfolio , with Exposures, with an average between and months and a LE composed of only 3 elements (), the total number of Scenarios range between and , that is well above the total estimated number of atoms in the universe (i.e. ). Therefore, direct enumeration of all possible Scenarios is out of reach and it becomes mandatory to use an indirect approach for the computations, like the Monte Carlo Method.

Finally, we define a Cluster as a set of homogeneous Exposures with the same risk profile: thus, we consider each portfolio to correspond to a single Cluster. For example, let a securitization originate from a single portfolio whose Exposures can be described by two different probability density functions (PDF): since the portfolio is described by two different Clusters, we consider them as two separate portfolios, and thus .

2 The PEAL Method to structure a securitization

After having defined in Sec. 1.2 the cases under which a transaction or a scheme must be considered a securitization, this Section introduces the PEAL Method structuring process. In abstract terms, a securitization has a balance sheet similar to the one of a traditional company: on the asset side there are the Exposures that generate inbound cash flows, and on the liability side there are the Positions to whom the securitization, at certain conditions, has the obligation to pay outbound cash flows. Such outbound payments must follow a univocal and unambiguous order, such that it must always be possible to describe it as a deterministic algorithm333Notice that a strict usage of a deterministic algorithm to describe payments’ priority removes ambiguities on who must be paid first and avoids litigations.. Equity is often negligible, thus we will not consider it in the modelling.

To date, the established structuring practice for the asset side often uses a macro-approach that entails that the total inbound cash flows be impacted by the negative Events historical loss averages. Thus, on the liability side, the documentation provided to investors - commonly known as investment memorandum - only shows the average Scenario without any data related to any risk metric of the Positions, especially to time-dependent metrics, that would allow investors and supervisory authorities to be continuously updated on the evolution of the Positions’ performances. Indeed, such metrics are nowadays almost impossible to calculate with the current macro-approach.

The PEAL Method, by considering on the asset side the statistical properties of every single Exposure in different Scenarios , adopts a micro-approach for calculating the securitization risk analysis on the liability side. This is analogous to the development of statistical mechanics, an area of physics that, by studying the behavior of large groups of microscopic components (atoms, molecules) has allowed to explain the laws of classical thermodynamics, which studies the relationships among macroscopic quantities characterizing materials like temperature, pressure, and heat capacity. It is worth noting that there is an exponential number of micro-states in statistical mechanics, which contributes to the complexity of the system. At the same time, such complexity enables better characterization of the fluctuations of the system. On the same footing, this paper considers the statistical dynamics of the exponential number of possible outcomes to better characterize the ongoing Positions’ risk profiles and time Features.

2.1 Structuring a securitization

In the PEAL framework a Structuring Method is a set of mathematical rules to build a robust process where the total inbound cash flows are allocated as outbound cash flows among the different Positions respecting Reg 2402 provisions. All Structuring Methods follow the same 10-steps process. There are 4 Steps to characterize the asset side:

-

•

Step 1: select the Exposures Type;

-

•

Step 2: select the LE and generate the Scenarios ; 444The set must be a representative statistical sample of all the possible Scenarios .

-

•

Step 3: compute the basic inbound building-blocks (BIB);

-

•

Step 4: compute the composite inbound building-blocks (CIB).

Then there are 4 Steps to characterize the liability side:

-

•

Step 5: select the number of X Cost and Y Note Positions;

-

•

Step 6: design the Positions to absorb the Tranches;

-

•

Step 7: dimension the Gross Cost (GC) and Gross Notes (GN);

-

•

Step 8: compute the Net Cost (NC) and Net Notes (NN).

Finally, there are 2 Steps to optimize the securitization Structuring Methods:

-

•

Step 9: compute the relevant Features;

-

•

Step 10: optimize the chosen Features.

In the next 10 Sections, we describe each of the above steps more in detail.

3 Step 1: Select the Type of Exposures

Let a group of Exposures that exhibit similar characteristics be defined as a Type. The 1st Step of any Structuring Method is to select, for each portfolio , the Type of Exposures (TE). The following is a non-exhaustive list of the eleven most used Types in Italy to date:

-

1.

Corporate Loan (CL): loan provided to a company;

-

2.

Mortgages Loan (ML): loan with an immovable asset as collateral;

-

3.

Auto Loan (AL): loan with a car or truck as collateral;

-

4.

Student Loan (SL): loan provided to a student for education;

-

5.

Credit Card Loan (CC): money borrowed per credit card expenses;

-

6.

Cessione Quinto Pensione (QP): pension-backed loan;

-

7.

Cessione Quinto Salario (QS): salary-backed loan;

-

8.

Real Estate (RE): property-generating income (e.g. lands, buildings);

-

9.

Energy Estate (EE): equipment producing clean energy;

-

10.

Exotic Asset (EA): perishable assets (e.g. wine, reggiano parmesan);

-

11.

Negative Event Exposures (NE): any loan that is affected by a negative Event by the time of structuring (so-called unlikely-to-pay or non-performing-exposures).

Notice that, although it is mathematically possible to structure a securitization composed of portfolios with heterogeneous Types, European supervisory authorities have forbidden this provision in Reg 2402. Thus, to date all portfolios composing an European securitization must be homogeneous in Type. Notice that Clusters further refine the definition of Types: in fact, the Exposures of the same Cluster not only have the same Type but also the same risk profile. Thus, a securitization based on Auto Loans with ratings A and B, would consist of portfolios (Clusters) with the same Type.

4 Step 2: Select the LE & generate the Scenarios

The 2nd Step of any Structuring Method is to select, for each portfolio , the List of Events () that best describe the selected Type of Exposures, used to compute the Clusters. Some of the most relevant Events that might affect each Type of Exposure are listed in Table 1 in Appendix A. Consider that any Structuring Method might use only a subset of the List of Events in Table 1. As an example, if the List of Events were just: prepayments (\saype) and defaults (\sayde), then the . Once selected the , the arranger must generate the relative Scenarios via Monte Carlo, respecting the Clusters’ risk profile distributions and correlations.

5 Step 3: Basic inbound building-blocks (BIB)

As will be further explained in this Section, the inbound cash flows can be allocated to 3 basic mutually exclusive and commonly exhaustive building-blocks (the Basic Inbound building-Blocks or BIB) that allow designing uniquely the securitization asset-side: the assets (A), the losses (L); and the events recovery (E). The 3rd Step of any Structuring Method is to compute the BIB. See Sec. 11.1 for the definition of Full-Performing, Performing, Non-Performing, and Super-Performing Exposures.

5.1 Asset building-block (A)

Let the inbound cash flows of the Exposures in the Base Scenario be defined as Gross Asset . Exploiting this definition, the Base Scenario inbound cash flows of an Exposure is

| (18) |

while the overall securitization Base Scenario inbound cash flows is

| (19) |

Then, the Scenario inbound cash flows of a Performing Exposure is

| (20) |

while the overall securitization Scenario inbound cash flows is

| (21) |

that is the Asset building-block. Notice that is any Event of the List of Events , affecting in a particular Scenario the Exposure ; and is the Heaviside function as explained in Sec. 1.5. There exist Events that may impact only the capital at time or only the interest at time . Considering that the is the same as multiplying the cash flows for , where is the first occurrence in each Scenario of any Event. We can then simplify Equation (20) to

| (22) |

5.2 Loss building-block (L)

Let the Scenario inbound cash flows of Non-Performing & Super-Performing Exposures be defined as the Losses building-block . Exploiting this definition, the Scenario inbound cash flows of a Non-Performing or Super-Performing Exposure is

| (23) |

then Scenario total losses are

| (24) |

When in a particular Cluster all the () Events affecting the Exposures of the portfolios are MECE, the previous Equation (24) becomes

| (25) |

where . Then, the Scenario cumulative Loss is

| (26) |

Exploiting definition is possible to establish a liability-independent metric to compute the asset-side losses. Indeed, any Financial Institution, given the same assets inputs and with comparable risk models, would get an equivalent distribution, despite substantially different Waterfall Configurations, and thus different payment priorities (see definition in Sec. 8).

5.3 Event recovery building-block (E)

Let the spot inbound cash flows mitigating negative or deriving by positive Events in the Scenario be defined as the event recovery building-block . For example, in Corporate Loans Type if the List of Events where , then the Exposure event recovery would be the sum of \sayspot recoveries such as the prepayments and the recovery of collateral as

| (27) |

while the total inbound event recovery in Scenario would be

| (28) |

5.4 Disambiguating spot vs non-spot cash flows

In the previous Sections we have explained that non-spot555Non-Spot: cash flows different from zero more than once in different time . inbound cash flows shall be described by the Gross Assets , the Assets and the Losses . On the other hand, the spot666Spot: cash flows different from zero just at one specific time . inbound cash flows shall be described by the event recovery .

For example, if we consider the Corporate Loans Type of Exposures we know from Table 1 that the main Events that apply are 777Events: prepayments, defaults, return to life, and variation of the euribor. Thus, an Exposure is expected to prepay voluntarily at time if it is affected by the prepayment Event : whilst the negative effect impacts the Assets , the positive prepayment cash flow is spot at time and thus shall be absorbed by the event recovery building-block as . The same approach can be used for the default Event , so the positive recovery of collateral cash flow is spot at time and thus shall be absorbed by the event recovery building-block as . On the other hand, if an Exposure that has defaulted at time , is affected by the \sayreturn-to-life Event at a time such that , then and will have the form:

| (29) |

where \sayreactivates the cash flows after the recovery time .

The same dynamic applies to the Euribor Event , where we expect the Euribor to change overtime versus its Base Input, and thus we need to account for the change of installment for each Exposure whose interest is dependant on the change of euribor. A positive or negative variation of the euribor from its Base Input value/function changes the Exposure total installment and therefore we can consider that the impact of the Euribor Event is non-spot and thus shall be accounted in . Notice that if the new is lower than the Base Input , the . On the other hand, if the new is higher than the Base Input , the . Lastly, it is important to remember that a change in euribor shall not be immediately reflected in a change in the payments toward Positions: indeed, an increase in euribor is likely to increase the probability of default, and a decrease in euribor is likely to trigger an increase of prepayments, with respect to the default and the prepayment distribution values that were expected initially. Further analyses on the implication of the Euribor Event against the excess losses deriving from changes versus the Base Inputs shall be done.

The disambiguation logic applied in the previous example for Corporate Loans can be applied to any Event in any Type of Exposure. When deciding whether an inbound cash flow shall be allocated to Gross Assets , Assets or Events recovery , always consider if its cash flows are indeed spot or non-spot, and allocate accordingly the relative cash flows to the proper inbound building-block.

6 Step 4: Composite inbound building-blocks (CIB)

As will be further explained in this Section, the basic inbound building-blocks can be used to compute different composite inbound building-blocks (CIBs). The 4th Step of any Structuring Method is to compute all the following CIB:

6.1 Optimization inbound building-block

Notice that, in calculating all the following composite inbound building-blocks, we will introduce a new block that is dimensioned at the end of the structuring process, in the optimization phase of Step 10 (see Sec. 12). This \saynew block represents an inbound cash flow paid by a 3rd-party, often una-tantum at time , as a lump sum that is neither reimbursed nor remunerated (e.g. the upfront payment provided to cover the first agents’ expenses in Negative Event Exposures) and will be called or . In the first structuring cycle, such amount shall be considered null (), and only in the optimization phase the arranger will have the choice to dimension . To date, we define the Base Scenario initial endowment inbound cash flows as and the Scenario initial endowment inbound cash flows . Normally, the difference between these two amount is always zero, but there might exist theoretical situations where () and () due to unexpected situations like the bankruptcy of the trustee hosting the cash flows or the default of the bonds in which the cash reserve is invested. In some cases, the difference might be due to a delay in the upfront payment by the 3-rd party.

6.2 Total Inbound Cash Flows (ICF)

We define the Base Scenario total inbound cash flows as

| (30) |

considering that in the Base Scenario then

| (31) |

that represents the maximum initial endowment given the Base Inputs.

6.3 Total Available Funds (TAF)

We define the inbound cash flows that can be allocated at any time as an outbound cash flows to the Positions in any Scenario as total available funds as

| (32) |

6.4 Total Loss (TL)

We define the sum of Scenario Losses and the difference between the Base Scenario and the Scenario optimization inbound block plus the Super Senior Embedded Position (see definition in Sec. 7.3) as Total Loss

| (33) |

where the is Equation (31), the is Equation (32), the is Equation (28), the is the Total Net Loss of Equation (35), and is Equation (45).

Notice that the Super Senior Embedded Position components are either additional expenses (see Excessive Costs or Cost of Recovery in Sec. 7.3) or reduced outbound cash flows for the Positions (see Excess Recovery in Section 7.3) that reduce the total available funds . Therefore, shall be treated as \sayadditional losses and shall be added to the total loss to provide a clear picture of the securitization ongoing riskiness to the institutional investors and the public authorities. Finally, it is worth noticing that, by default, the Losses are always \saysmooth whilst the Total Losses , absorbing the spot inbound cash flows, can have loss spikes. As shown in Sec. 6.6, by computing the Tranching on the distribution both of the and of the it is possible to understand what percentage of risk depends on the non-spot functions and what percentage from the spot functions.

6.5 Total Net Loss (TNL)

We define the difference between the Scenario losses and the Scenario events recovery as the net loss

| (34) |

Then, we define the difference between the Scenario total losses and the Scenario events recovery as the total net loss

| (35) |

When relevant, prefer the total loss over the total net loss to compute the Features, as a more robust metric to compare risk profiles across securitizations.

6.6 Total Loss Tranching

This Section is divided in 2 parts: in Sec. 6.6.1 we define the concept of first, second and complementary loss tranches from a regulatory perspective; and in Sec. 6.6.2 we explain how to compute the significant margin within the First Loss Tranche.

6.6.1 Tranching definition

As previously stated, Reg 2402, Article 2(1)(b), explains that in a securitization the subordination of tranches determines the distribution of losses during the ongoing life of the transaction scheme. From this article we can infer two things: (i) the risk is segmented in more than one tranche; (ii) the tranches shall be evaluated on an \sayongoing basis. In this paper, we will consider 3 types of tranches: the first loss tranche (FLT), the second loss tranche (SLT), and the complementary loss tranche (CLT).

Reg 2402, Article 2(18), defines the first loss tranche as \saythe most subordinated tranche in a securitization that is the first tranche to bear losses incurred on the exposures and thereby provides protection to the second loss and, where relevant, higher ranking tranches. What we can deduce from Article 2(18) is that in a securitization there must be at least two Positions () absorbing the different tranches. Therefore, each tranche must be covered by at least one Position, and each Position can \sayabsorb risk from more than one tranche. In addition, European Capital Requirement Regulation No 575/2013 consolidated version of January 2024 (CRR), Article 244(1)(a), explains that an \sayoriginator institution of a traditional securitization may exclude underlying exposures from its calculation of risk-weighted exposure amounts if [] significant credit risk associated with the underlying exposures has been transferred to third parties. Article 244(2)(b) explains that \saysignificant credit risk shall be considered as transferred if \saythe originator can demonstrate that the exposure value of the first loss tranche exceeds a reasoned estimate of the expected loss of the underlying exposure by a substantial margin. Thus the CRR links the to the Exposure expected loss (EL or ) plus a substantial margin (). The CRR does neither provide further details on which distribution to compute the nor on how to compute the \saysubstantial margin. For the purpose of this paper, as distribution we will use the total net loss , whilst for how to asses weather or not there exist we recommend to see next Section (6.6.2). Putting aside for a moment the \saysignificant margin, the computation of the is as follows

| (36) |

where

| (37) |

where is the mean with respect to the total net losses .

Whilst for the there is an indication on how to compute it, for what concerns the second loss tranche , to the best of our knowledge, there is no jurisprudence. After having interviewed tens of practitioners, we believe that the most used method to compute the SLT – a measure of the Unexpected Loss – is the expected shortfall888The \sayexpected shortfall is also known as \sayconditional value at risk (Rockafellar and Uryasev, 2000), or \saysuper quantile (Rockafellar and Royset, 2010). or \sayvalue at risk (VaR). Thus the SLT is the mean of the total net losses , restricted to the values exceeding a certain quantile, minus the first loss tranche as

| (38) |

where

| (39) |

is the value at risk and

| (40) |

is cumulative distribution function at quantile.

Finally, we define the as the difference between the total inbound cash flows and the other tranches as

| (41) |

Notice that the covers extreme losses like the one that materializes in the theoretical scenario where all Exposures turn Non-Performing at and all . In this theoretical Scenario, as Equation (35) shows, being the then the total net loss is equal to the inbound cash flows . The complementary loss tranche is normally the tranche that is covered by the very first Positions, like the costs and the \sayfirst note Positions (see next Sec. 7 for further details).

In any Structuring Method, for the sake of transparency, consistency, and cross-comparability, it should become customary to define always the , the , and the (together the Tranches). Indeed, these 3 categories exist in any Structuring Method since they are necessary to compute the regulatory capital (see Sec. 7.2 and Sec. 11.3). Considering that each Position (with ) may absorb less or more than one of the above-mentioned 3 Tranches, the arranger must be transparent in indicating what percentage of each Tranche each Position absorbs.

6.6.2 FLT substantial margin

In the previous Sec. 6.6.1 we explained that the CRR links the computation to the concept of a \saysignificant margin , without mathematically defining it. To the best of our knowledge, there is no conclusive evidence on how the Supervisory Authorities apply this concept, and yet it is a core aspect in computing regulatory capital (see Sec. 11.3). When the CRR entered into force in 2013, practitioners computed the on the cumulative PDF of the total net loss at the Positions’ maximum duration

| (42) |

instead of on an ongoing basis as currently required by the Reg 2402, that entered into force in 2017. Thus, we propose a solution in implementing the \saysignificant margin of the 2013’s CRR that takes into account the ongoing nature of the FLT defined by Reg 2402. Indeed, the following ratio

| (43) |

is when is defined as equation (36), and is defined as equation (42). A criterion to understand if the margin is \saysignificant could be to check that it covers more than a standard deviation of the total first loss tranche (i.e. ). By definition, our of equation (36) already has a \saysignificant margin embedded within its formulation versus the methodology applied back in 2013 when this concept was introduced. This is also why in the previous Sec. 6.6.1 we ignore the parameter.

7 Step 5: Select the number of Positions

As further explained in this Section, the total inbound cash flows are allocated to one macro building-block called \sayPosition, composed of 2 regulatory building-blocks called \sayCost and \sayNote Positions and 1 \sayephemeral called \sayEmbedded Position. The 5th Step of any Structuring Method is to select the number of Cost Positions and the number of Note Positions. This Section is divided in 4 parts: in Sec. 7.1 we define the concept of Position from a regulatory perspective; in Sec. 7.2 we define the concept of Position \sayQuality; in Sec. 7.3 we define the concept of Embedded Positions; and in Sec. 7.4 we explain how to compute the number of Positions.

7.1 Position definition

Reg 2402 does not define the concept of positions, instead its Article 2(19) only defines the concept of securitization position as \sayan exposure to a securitization. In the whole Reg 2402, the concept of position is used equivalently and indistinctly to securitization positions, thus we use the same hermeneutic interpretation of equating position with securitization position.

European Regulation No. 2401/2017 (Reg 2401), Article 242(6) defines senior securitization position as a Position \saybacked or secured by a first claim on the whole of the underlying exposures, disregarding for these purposes amounts due under interest rate or currency derivative contracts, fees or other similar payments, and irrespective of any difference in maturity with one or more other senior tranches with which that position shares losses on a pro-rata basis. The previous Article 242(6) points out something that is often overseen: \sayfees or other similar payments has to be disregarded when assessing if a Position is \saysenior or not. Indeed, in current Structuring Methods, servicing fees are often the ones with the utmost priority in the payments versus the most senior Note Positions. Thus, in the first place, if the servicing fees were not actually considered Positions by Reg 2401, then Article 242(6) would have not needed to carve them out from the \saysenior position definition. It follows that Reg 2401 considers servicing fees a Position (Cost Position) not differently than the notes (Note Position). Indeed, since servicing fees receive a fraction of the total inbound cash flows , they must be considered absorbing as well a fraction of credit risk (i.e. if the whole portfolio were to default at time , then also the servicing fees would not be paid accordingly to the Base Scenario).

On the other hand, Reg 2401, Article 242(6), defines a mezzanine securitization position as a \sayposition [] which is subordinated to the senior [] and more senior than the first loss tranche. Finally, neither Reg 2401 nor Reg 2402 defines the concept of junior securitization position but generally refers to the First Loss Tranche. Then, we can assume that a Position is \sayjunior if it absorbs the First Loss Tranche . Consequently, we can assume that a Position is \saymezzanine if it absorbs the Second Loss Tranche and \saysenior if it absorbs the Complementary Loss Tranche .

Notice that some practitioners do not consider the Costs as Positions because they net the total inbound cash flows of the various expenditures toward the servicers and agents before redistributing the cash flows to the Notes Positions. This practice goes against many International Financial Reporting Standards (IFRS) principles described into the (IASB, 2018), in particular the one that requires to \sayseparately reporting the components of financial statements. This principle emphasizes the importance of presenting revenues, expenses, and cash flows separately in financial statements rather than netting them together. It ensures transparency and provides users of financial statements with a clear understanding of an entity’s financial performance and financial position. Therefore, the investment memorandum shall always respect the same IFRS principles and thus clearly shows the Cost Positions in at least 2 different forms: (i) the -th Net Dimensioned Cost Positions as defined in Equation (10.5); and (ii) the ratio of to the total inbound cash flows . These 2 Features should be reported not only as their average value, but also as their empirical (i.e. from the simulated scenarios) ongoing probability density function, because in certain Scenarios the cost of recovery of defaulted Exposures might be so relevant to impact both the mezzanine and the senior Positions, especially in Negative Event Exposures. Thus, it is crucial to not only consider the Costs as Positions, but to compute all the above Features to enable the investors to make an informed judgement on the real intrinsic riskiness of the Notes they are purchasing.

7.2 Position Qualities

Why is it important to define if a Position is \saysenior, \saymezzanine, or \sayjunior? From a Structuring Method perspective, these regulatory definitions are mathematically irrelevant. Indeed, if at any time the Regulator were to decide to abolish these concepts, the securitization modelling would not be impacted. Therefore, the \sayseniority is not an intrinsic element of any securitization, but more like a quality that a Position obtains depending on multiple factors. Assigning the right quality to a Position is not just an aesthetic quirk: in fact, to compute the Regulatory Capital (RC) we need to assess, for each Position, the relative risk weights (RWs) applicable to a slice or to the Position as a whole. Indeed, as it can be seen in the table of Reg 2401 Article 259(1), the regulator has assigned different RWs to senior or non-senior Positions and thus assigning the right quality has direct implications on the RC computation. In conclusion, the quality is not an embedded characteristic that each Position has by default, but depends on its Designing (i.e. defining the relative \saylocation of the X Cost relative to the Y Notes Positions, see next Sec. 8) and its Dimensioning (i.e. assigning a \sayvalue to the Positions, see next Sec. 9) whose effect is only relevant when computing the RC. Given the same Dimensioning, a diverse Designing would assign to each Position a different quality.

See the next Sec. 11.3 for a deep-dive on Regulatory Capital: for now, just remember that for the purpose of this paper, to each Position, in part or as a whole, is assigned over time one (or more!) of the following 3 Qualities:

-

•

Senior: if a Position slice absorbs a % of ;

-

•

Mezzanine: if a Position slice absorbs a % of ;

-

•

Junior: if a Position slice absorbs a % of .

since, as it will be further explained in the next Sec. 8, each Position might absorb different tranches of the risk depending on their Designing. Therefore a Position might not receive the \sayquality of Senior, Mezzanine or Junior as a whole, but each different \sayslice absorbing a tranche of the FLT, SLT or CLT should receive the consequent \sayquality.

Now, our statement about the Qualities might seem to contradict the previous Article 242(6) of Reg 2401, where it is clearly stated that a Cost Position cannot be considered Senior, whilst with our definition a Cost Position could get the quality of Senior if it were absorbing a slice of the complementary loss tranche . This contradiction will be resolved in the next Sec. 11.3: indeed, the Regulator removed Cost Positions ex-ante from the computation of , whilst instead of making Cost Positions lose their Qualities ex-ante, in the PEAL Method we assign to the Cost Positions a risk weight ex-post as shown in Equation (74). In fact, as we will show in the next Sec. 8.1, our Structuring Method allows to design \sayvertical Cost and Note Positions, and thus it becomes crucial to provide the securitization stakeholders with a transparent picture of which part of which Position has which Quality, irrespectively if a Position bears or not regulatory capital (). Indeed, Qualities are currently used to intuitively understand the liability-side payment priorities of the Positions but, since our approach allows for \sayVertical Positions that can even be Senior, Mezzanine and Junior at the same time, the direct link between Qualities and payment priorities breaks. Thus, in general, Qualities should not be used as a proxy for the payment priorities, but only to calculate the Regulatory Capital.

7.3 Embedded Positions

Let a Position be \sayEmbedded if it is equal to zero for any in the Base Scenario: . Embedded Positions can be different from only in some Scenario : . Embedded Positions are divided into two: (i) Super Senior (SSE) and (ii) Super Junior (SJE). We introduced the Embedded Positions because currently they are not properly described within the documents provided to the stakeholders. Therefore, the information about these variables is often overseen and it becomes incredibly complex for 3rd-parties to clearly understand their impact on their overall returns. Following the same principles of clarity and transparency described in the previous Sec. 7.1, we believe that the introduction of the Embedded Positions makes the risk assessment in the different Scenarios way simpler for all stakeholders.

7.3.1 Super Senior Embedded Positions

The Super Senior Embedded (SSE) are those Positions that have always the first claim on the total available funds , irrespectively from any possible Designing (see next Sec. 8). To date, we have identified only types of SSE that are the following:

-

•

EC: stands for Excessive Costs, which are all the una-tantum fines issued by any authority in case of infringement of one or more national or sovra-national laws (e.g. tax fines) plus the legal costs to defend from such accusations. It is Super Senior because any legal fees have always the utmost priority in any possible Designing;

-

•

CR: stands for Cost of Recovery, that are the costs that the securitization pays on an ongoing basis to recover the defaulted Exposures. It is Super Senior because the agents that recovery the distressed credits shall be paid before anyone else;

-

•

ER: stands for Excessive Recovery, which are the eventual excess cash flows that in each Scenario derives from the difference between an Exposure outstanding capital at the time of the default , plus the cumulative recovery Cost , and the recovered value at the time of recovery as

(44) It is Super Senior because the Excessive Recovery belongs to the respective Exposures from which they have derived and must be revert as soon as the excessive cash is made available to the securitization, without further ado.

Therefore, the Scenario Super Senior Embedded Position is

| (45) |

whilst the average Scenario Super Senior Embedded Position is

| (46) |

7.3.2 Super Junior Embedded Positions

The Super Junior Embedded (SJE) are those Positions that have always the last claim on the total available funds , irrespectively from any possible Designing (see next Sec. 8). To date, we have identified only type of SJE that is:

-

•

B: stands for Buffer, which are those excess cash flows that in each Scenario derive from the difference between and as

(47) The can be caused by an excess of euribor or other factors that generate a negative losses. The Buffer is Super Junior because it is an excess cash used to absorb the first loss tranche , even before any -th Position, and it is normally paid out pari-passu to the \saylower-tier Positions.

7.4 Compute the number of Positions

As detailed in the previous Sec. 7.1, there are of 2 types of Positions: those owned by the securitization servicers (Cost Positions) whose total number is described by the letter , and those issued as notes and detained by bondholders (Note Positions) whose total number is described by the letter . Thus, the total number of Positions is

| (48) |

Pursuant Reg 2402, a transaction is a securitization if and only if , of which one must be a Cost Position and one a Note Position . Indeed, securitization vehicles are empty shells and need servicers to operate them. Notice that, for the purpose of this paper, if there are service providers paid pari-passu, we can sum their cash flows and consider them being one single Cost Position when computing the payment priority waterfall. The same reasoning shall be applied to the notes: if two or more Note Positions are completely \saypari-passu, sharing the same risk and being paid with the same frequency, then they shall be deemed as one single Note Position, summing their cash flows.

8 Step 6: Positions’ Designing to absorb the Tranches

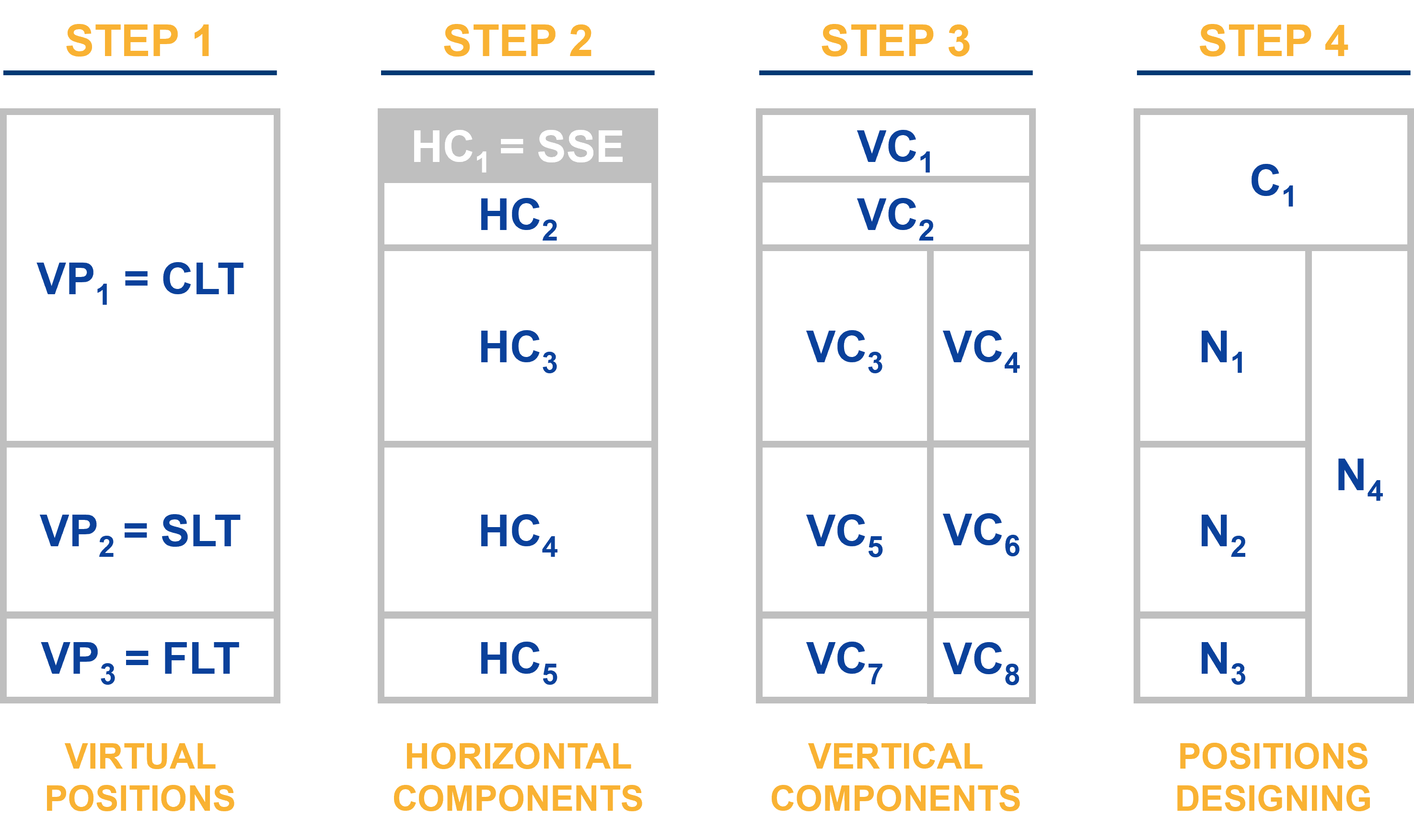

Positions’ Designing determines the way the inbound risk is distributed among the outbound Positions. This Section is divided in seven parts: in Sec. 8.1 we define the process to organize the Positions to design a Waterfall Configuration; in Sec. 8.2 we introduce the concept of Virtual Positions; in Sec. 8.3 we introduce the concept of Horizontal Components; in Sec. 8.4 we introduce the concept of Vertical Components; in Sec. 8.5 we introduce the concept of Positions’ Designing; in Sec. 8.6 we analize in detail the illustrative Design of Figure 1; and finally in Sec. 8.7 we explain why the current traditional Horizontal Position Designs are particular cases of our general PEAL Method.

8.1 Designing definition

We define the process of organizing the Cost and the Note Positions so as to absorb all the Tranches as Designing, and its synoptic graphical representation as a Waterfall Configuration999In technical jargon, we refer to a \sayWaterfall because the cash \sayflows down from the \sayhigher-tier Position to the \saylower-tiers Positions, in a way for which the \sayhigher-tier Positions are paid before the others, following the Waterfall Configuration, and the \saylowest-tier Position is paid only if there is any cash flow left.. The 6th Step of any Structuring Method is to Design the Positions into a Waterfall Configuration. The Designing process is made of 4 steps (see Figure 1):

-

1.

Virtual Positions: define a superstructure that bridges the inbound and the outbound cash flows;

-

2.

Horizontal Components: define a superstructure that horizontally subdivide, and mathematically links, each Virtual Position in smaller horizontal rectangles;

-

3.

Vertical Components: define a superstructure that vertically subdivides, and mathematically links, each Horizontal Position in smaller rectangles;

-

4.

Positions Design: define the equations that logically connect each Cost and the Note Position to their relative Vertical Components.

To date, there are 3 Waterfall Configurations: horizontal; vertical; and hybrid. In the Horizontal Waterfall, each Position absorbs the Tranching in horizontal slices: the flows down from the top to the bottom Position following the Designing (i.e. the Position has higher payment priority than the Position if and only if ). In the Vertical Waterfall, each Position absorbs the Tranching in vertical slices: the is allocated to the vertical Positions pro-rata basis. In the Hybrid Waterfall, each Position absorbs the Tranching in a hybrid combination of horizontal and vertical: the is allocated to the Positions indirectly, through the Virtual Components.

8.2 Virtual Positions

Let a Virtual Position be a mathematical superstructure that bridges the inbound and the outbound cash flows. Let be the number of Virtual Positions (see Step 1 in Figure 1). In this paper, the number of Virtual Positions is fixed at . Thus, let the system of equations that connect the Virtual Positions outbound cash flows to the inbound cash flows be

| (49) |

This choice was made to simplify the regulatory capital optimization and computation. Indeed, as explained in the previous Sec. 7.2, the First Loss Tranche, the Second Loss Tranche, and the Complementary Loss Tranche on the asset-side correspond to the Junior Quality, the Mezzanine Quality, and the Senior Quality on the liability-side. It follows that , , and .

Being a Horizontal Waterfall type, Virtual Positions are useful because they have a robust mathematical link to the inbound cash flows and introduce a clear priority in the Positions’ payments, enabling simpler computation in preparation of the next steps. We will use the Virtual Positions as a pivotal element to compute the net cash flows to the Positions in the different Scenario in the following Sec. 10.

8.3 Horizontal Components

Let a Horizontal Component be a mathematical superstructure that horizontally subdivides, and mathematically links, the -th Virtual Position into horizontal rectangles (see Step 2 in Figure 1). Let the set of horizontal slices of the Virtual Positions be and

| (50) |

be the number of total horizontal slices, where . Notice that the first Horizontal Component is always the average Super Senior Embedded Position (i.e. ). Let be the index of the -th slice (from top to bottom) and let be the Horizontal Percentage with respect to its Virtual Position . As an example, let consider the Step 2 in the previous Figure 1 where: , , . We can infer that , and \sayslice , \sayslices and \sayslices . Obviously, we have that , , and . Then, the equations that connect the Virtual Positions to the Horizontal Components are

where in any Structuring Method.

8.4 Vertical Components

Let a Vertical Component be a mathematical superstructure that vertically subdivides, and mathematically links, the -th Horizontal Component in smaller rectangles (see Step 3 in Figure 1). Let the set of vertical slices of the Horizontal Components be and

| (51) |

be the number of total rectangles composing the securitization liability-side, where . Notice that the first Vertical Component cannot be subdivided and it is always equal to the Super Senior Embedded Position (i.e. ).

Let be the index of the -th slice (from top to bottom, from left to right) and let be the Vertical Percentages utilized to subdivide the Horizontal Components into their Vertical Components. As an example, let consider the Step 3 in the previous Figure 1 where: , , , , . We can infer that: \sayslices , \sayslices , and \sayslice , and \sayslice , and and \sayslice . It naturally follows that , , , , . Then, the equations that connect the Horizontal Components to the Vertical Components are

Notice that, while the order of the Horizontal Components provides some information on their payment priorities, the order of the Vertical Components do not. Any order is acceptable because it is the arranger that provide the system of equations to link each -th Horizontal Component to the relative -th Vertical Component.

8.5 Positions’ Designing

Let the process to mathematically connect each Cost and Note Position to their relative Vertical Components be defined as Positions’ Designing (see Step 4 in Figure 1). Following on the example described in the previous Sections, we can define the system of equations of Step 4 of the previous Figure 1 that connect the Vertical Components outbound cash flows to each Cost and Note Position outbound cash flows as

8.6 Illustrative example

We choose the specific example of a design (Figure 1) to illustrate the utilization of horizontal and vertical components in defining Note Positions. Moreover, the introduction of this type of design could have significant implications in the practice of securitization.

Reg 2402, article 6(3)(a) requires that certain actors shall retain on an ongoing basis a material net economic interest which, in any event, shall not be less than of the nominal value of each of the Tranches sold or transferred to investors (i.e. a vertical slice of the Note Positions). In addition, pursuant article 5(1)(c) of Reg 2402, institutional investors are required to verify that the mandatory retention is maintained on an ongoing basis by the relevant actors. Unfortunately, the operation to verify the continuous maintaining of the mandatory retention is currently extremely impervious, and often times, almost impossible due to operative constraints. Thus, the possibility to create a vertical Note - in step 4 of Figure 1 - dimensioned to respect the said mandatory retention, might solve all the current operative issues at once. If be hold by a third-party, then any investor could just request at any point in time the trustee to certify that the vertical Position be in the possession of the relevant actors. This alone might automatically fulfill Reg 2402 due diligence requirements.

Therefore, the usage of vertical Positions is not just a theoretical or aesthetic choice, but has profound regulatory implications. Indeed, just by creating such Position, it would be possible to minimize the due diligence operative complexity and costs for both the institutional investors and the supervisory authorities.

8.7 A particular Design of a general method

As explained in the previous Sec. 8.1, there are 3 type of Waterfall Configurations. Nowadays, the most used Waterfall Configurations pertains of Cost Position and Note Positions. Such notes follow the same order of Figure 1 where does not exist and , , , and . Thus, the current typical Horizontal Waterfall Configurations are just particular cases of the PEAL Method general framework, where the Positions are perfectly superimposable to the Vertical Components and to the Horizontal Components. The Designing of Sec. 8, the Gross Dimensioning of Sec. 9, and the Net Dimensioning of Sec. 10 processes remain the same.

9 Step 7: Dimension the Gross Cost & Gross Notes

In this section we outline the process of gross dimensioning divided into seven steps. In Sec. 9.1 we define the process to dimension the Gross Cost and Gross Notes . In Sec. 9.2 we introduce the concept of payment frequencies, that are crucial in understanding payment waterfalls, and discuss how to avoid incongruities with the specific rules of Reg 2402. In Sec. 9.3 we introduce the frequency transformation function to adjust cash flow vectors into constant intervals. in Sec. 9.4 we dimension the Gross Vertical Component ; in Sec. 9.5 we dimension the Gross Cost and the Gross Note ; in Sec. 9.6 we dimension the Gross Horizontal Component ; and finally in Sec. 9.7 we provide a simple test to check if we are correctly applying the \sayhorizontal rule of Reg 2402.

9.1 Gross Dimensioning definition

We define the process to indirectly dimension the Gross Cost and the Gross Note following the system of equations described in the previous Designing phase, putting their monthly cash flows at their relevant payment frequency, as Gross Dimensioning. The 7th Step in any Structuring Method is to compute and . The Gross Dimensioning process is divided in 5 steps:

-

1.

Frequencies: select the Vertical Components’ payment frequencies;

-

2.

GV: compute the Vertical Component Gross Dimensioning;

-

3.

GC & GN: compute Costs’ and Notes’ Gross Dimensioning;

-

4.

GH: compute the Horizontal Components’ Gross Dimensioning;

-

5.

g-check: compute the ratio to check for coherence with Reg 2402.

9.2 Select the frequencies

In any Structuring Method, the frequencies are the \saykeystones to understand the functioning of the payment waterfalls. In a pure mathematical modelling perspective, any Vertical Component could have its own payment frequency , without considering its relation with the others and without any regulatory restriction. In practice, there are some constraints that shall be respected in selecting the payment frequencies. Reg 2402 article 2(1)(b), requires that the distribution of losses on the ongoing life of the transaction be dependent on the subordination of the Tranches. In order to respect such prescription, the payment frequency must follow 3 rules:

-

•

vertical: the \sayhigher Horizontal Components must have an higher payment frequency than the \saylower Horizontal Components (i.e. );

-

•

multiple: the \saylower Horizontal Components must have a frequency that is a multiple of the \sayhighest Horizontal Component (i.e. ;

-

•

horizontal: the Vertical Components that belong to the same Horizontal Component must have the same frequency (i.e. if .

If we relax even just one of the above rules, some of the Features of the next Sec. 11 will show signs of incongruities. For example if we relax the \sayvertical rule and we pay a \saylower-tier Horizontal Component (e.g. the -th ) with a higher frequency than the \sayhigher-tier Horizontal Component (e.g. the -th ), then in case of stressed scenarios the \sayhigher-tier might be less protected than the \saylower-tier, and thus bear more losses than what it would have done otherwise, contradicting the Reg 2402 prescriptions. If we relax the \sayhorizontal rule and pay two Vertical Components that are virtually \saypari-passu with two different frequencies, we are making the part that is paid with a higher frequency less risky than the other on an ongoing basis, thus contradicting the Reg 2402. Finally, even if we respect both the \sayvertical and \sayhorizontal rules, if we relax the \saymultiple rule, then in certain periods we might be providing protection to a \saylower-tier Horizontal Component whose cash flows should have been used in the next periods to protect the \sayhigher-tiers from negative events, contradicting Reg 2402.

As we will further explain, we will use the Coefficient of Variation Adjusted , described in the next Sec. 11, to detect breaches of Reg 2402 requirements: indeed, if any Horizontal Component line were to intersect during the ongoing life of the transaction it would mean that at that time a \saylower-tier Horizontal Component was less risky than a \sayhigher-tier Horizontal Component, contradicting Reg 2402 requirements.

9.3 Frequency transformation function

Since typically payments to the Positions have a lower frequency than the payments on the asset side, we need a function to transform the monthly inbound cash flows to the Position respective outbound cash flows frequencies. Let be the monthly cash flow vector to be transformed to a frequency paid each months. Then the transformation

| (52) |

9.4 Compute GV

Let be the Gross Dimensioning of the -th Vertical Component as

| (53) |

where , is defined as Equation (52) and is the frequency of the outbound cash flows of the -th Vertical Component .

9.5 Compute GC & GN

Let be the Gross Dimensioning of the -th Cost Position as the sum of its Gross Dimensioned Vertical Components. Let be the Gross Dimensioning of the -th Note Position as the sum of its Gross Dimensioned Vertical Components. Therefore, if we consider the Cost and Note Positions of the example of Sec. 8.5, the result is

where is function (53).

9.6 Compute GH

9.7 Horizontal rule g-check

Let be the ratio of the -th Gross Vertical to the -th Gross Horizontal Component

| (54) |

with as described in each system of equations that will be used in the relative Structuring Method, as shown in the example of the previous Sec. 9.6. The -check is a simple mechanism through which we immediately know if the payment frequencies we chose are respecting the 3 frequency rules explained in the previous Sec. 9.2. This test states that if the -th gross ratio of a certain Gross Vertical Component to its -th Gross Horizontal Component is equivalent to the percentage used to transform the monthly -th Horizontal Component into its monthly -th Vertical Component (i.e. ) then the selected payment frequencies are respecting the \sayhorizontal rule of Reg 2402 prescriptions. Otherwise, if for any then it means that one or more Gross Vertical Components belonging to the same Horizontal Component do not have the same frequency. Therefore, although they shall be \saypari-passu, they are partially not, thus breaching Reg 2402.

10 Step 8: Dimension the Net Costs & Net Notes

This Section is divided in six parts: in Sec. 10.1 we define the process to dimension the Net Cost and Net Notes ; in Sec. 10.2 we introduce the Gross Dimensioning Matrix ; in Sec. 10.3 we introduce the waterfall payment function used to compute the Net Dimensioning Matrix ; in Sec. 10.4 we dimension the Net Vertical Component ; in Sec. 10.5 we dimension the Net Cost and the Net Notes ; and in Sec. 10.6 we compute the Cost Losses and the Note Losses .

10.1 Net Dimensioning Definition

In a Scenario , we define the indirect process to dimension the Net Cost and the Net Notes by computing the Net Dimensioning Matrix , allocating the total available funds on the Gross Dimensioning Matrix using the Waterfall Payment Function , as Net Dimensioning. The 8th Step of any Structuring Method is to compute the Net Dimensioning of the Cost and the Note Positions. The Net Dimensioning process is divided in 5 steps:

-

1.

GDM: define the Gross Dimensioning Matrix;

-

2.

NDM: compute the Net Dimensioning Matrix;

-

3.

NV: compute the Vertical Components Net Dimensioning;

-

4.

NC & NN: compute the Cost and Note Net Dimensioning;

-

5.

LC & LN: compute the Cost and Note Losses.

10.2 Gross Dimensioning Matrix

Let the Gross Dimensioning Matrix be the matrix whose columns follow the as , where . Notice that, the GDM is a pure Horizontal Configuration: as it will be shown in the next Sec. 10.3, the Waterfall Payment Function allocates, on an ongoing basis, the total available funds from left to right: thus, the first column on the left is the first Position to have a claim on the total available funds, the second column has the second claim and so forth until the last column whom has the last claim on any residual liquidity. Therefore, in order to perfectly match the Horizontal Components Designing described in the selected Waterfall Configuration, the Super Senior Embedded Position must always be the first column because it has anyway the first claim on any available funds. Then, the following columns, should be the other Gross Dimensioned Horizontal Components in an ascending order: indeed, we know that has always an higher claim than that has an higher claim on and so forth to .

10.3 Net Dimensioning Matrix

Let the Waterfall Payment Function be the function that, in a Scenario , allocates the inbound total available funds on the Gross Dimensioning Matrix to respect their loss allocation Designing and their Gross Dimensioning, thus computing the Positions’ Net Horizontal Dimensioning synthesized into the Net Dimensioning Matrix . The Waterfall Payment Function is a system of recursive equations that loops from the top left to the bottom right of the GDM. The loop system is not obvious, and thus we decided to sub-divide it into 3 sequential steps:

-

1.

Step 1: compute the total gross position ;

-

2.

Step 2: compute the total net position ;

-

3.

Step 3: compute the Net Dimensioning Matrix .

In synthesis, in any Scenario , we first compute the total net position , allocating the total available funds (plus eventual residual cash flows from previous periods) on the total gross position (plus eventual debts from previous periods). Then, we compute the Net Dimensioning Matrix by allocating the total net position payments to each Horizontal Component according to its payment priorities.

10.3.1 Step 1: compute the total gross position

Let the sum of the Gross Dimensioned Horizontal Component be the total gross position as

| (55) |

10.3.2 Step 2: compute the total net position

In any Scenario , in each period , let the allocation of the inbound total available funds to the total gross position be

| (56) |

that is a set of recursive Equations where is and represents an indicator of when payments occur: in fact, is if and only if any outbound payment to any Position is due at a given period as follow

| (57) |

Notice that in a generic Scenario the periodical total available funds can be in general larger than the total available funds , since there can be cash advances from the previous period. A simple example is when the Positions are paid starting from the second period: in this case, introducing a dummy variable accounting for the total cash advances, . On the same footing, we have to introduce a dummy variable accounting for the fact that, if in a payment period there is not enough cash to pay for the total gross position , then in the following payment period we consider what is due to the positions is plus what was not paid at . Thus, we indicate with the total amount due to all the Positions. We have explicitly considered that if at period there is a payment, then the difference between available and due can either increase or according to the sign. Notice that it is also necessary to specify the initial value of the dummy variables; the natural choice is , . NB: is different from zero only at the payment periods. Finally, let the minimum between the periodical total available funds and the total amount due to all the Positions be

| (58) |

where the total net position takes into account the maximum amount of periodical inbound cash flows that can be allocated to all the Positions at any given period . Notice that .

10.3.3 Step 3: compute the net dimensioning matrix

In any Scenario , in each period , let the Net Dimensioning Matrix be the matrix whose columns are composed of the Net Dimensioned Horizontal Components , computed using the following system of recursive equations

| (59) |

where, for compactness, we indicate as . The expression for in Equation (59) ensures that any -th Horizontal Component cannot receive more than their respective plus any eventual debt of the previous period, and at most the cash amount residual after paying the Horizontal Component . The expression for accounts for the eventual debt from the previous period and for the difference between the due amount and the net amount that has really been paid net of any loss .

We recall that indicates whether any payment to the -th Horizontal Component is occurring at period . accounts for the fact that the residual cash for -th Horizontal Component equals the difference between the residual cash for the Horizontal Component and what has been paid to that Horizontal Component. Also in this case it is necessary to specify the initial values of the dummy variables and . Notice that .

10.4 Vertical Components Net Dimensioning

10.5 Cost & Note Net Dimensioning

Let be the Net Dimensioning of the -th Cost Position as the sum of its Net Dimensioned Vertical Components. Let be the Net Dimensioning of the -th Note Position as the sum of its Net Dimensioned Vertical Components. Therefore, if we consider the Cost and Note Positions of the example of Sec. 8.5, the result is

where is function (60).

10.6 Cost & Note Losses

Let be the Loss of the -th Cost Position as the difference between the Gross Dimensioned Cost Position and the Net Dimensioned Cost Position as

| (61) |

Let be the Loss of the -th Note Position as the difference between the Gross Dimensioned Note Position and the Net Dimensioned Note Position as

| (62) |

Notice that both the Cost and Note Losses amounts and probability density functions are information often not shared with the stakeholders, although many institutional investors would appreciate to have access to these forecasting to hedge their Positions from excessive risk. Therefore, as with the other securitization Features computed in the next Sec. 11, these key performance indicators shall always be computed and made available to the interested third parties for the ongoing life of the securitization.

11 Step 9: Compute the relevant Features

As introduced in Sec. 10.6, there are a number of securitization key performance indicators that the servicers should always provide to the investors on an ongoing basis (Features) to enable better and more transparent risk assessments. The 9th Step of any Structuring Method is to compute, in every Scenario , all the relevant Features. The following is a non-exhaustive list of some of the main Features that we strongly believe the servicers should always provide to the stakeholders on an ongoing basis:

-

•

: the Exposures Performance (Sec. 11.1);

-

•

: the Positions’ Thickness (Sec. 11.2);

-

•

: the Regulatory Capital (Sec. 11.3);

-

•

: the Coefficient of Variation Adjusted (Sec. 11.4);

-

•

: the Fair Value (Sec. 11.5);

-

•

: the gross internal rate of return (Sec. 11.6).

Inferring the Features statistics by Monte Carlo simulations allows for a better understanding of the real securitization ongoing intrinsic riskiness. It becomes easier to make all those advanced analyses that note-holders may need to demonstrate to their supervisory authorities that they have done proper risk due diligence during the purchasing and, afterwards, in the ongoing management process. Indeed, the PEAL Method increases the transparency that, in turn, might attract new investors and revive the securitization industry that, since 2008, has shown little sign of resilience. In fact, the European Corporate Loan niche alone lost more than 50% of new issuance between 2008 and 2017 (Kraemer-Eis, 2018) and has never recovered since.

11.1 Exposure Performance (EP)

Let the Exposure Performance be the function that describes the \sayperformance of each Exposure in any Scenario assigning a Mutually Exclusive and Commonly Exhaustive \saystate. The 4 possible states are: Full-Performing, Performing, Non-Performing, Super-Performing. The Exposure Performance is the -st Feature that shall be provided to the securitization stakeholders on an ongoing basis.

When applying the IAS-IFRS accounting principles, Exposures mainly exist in 3 \saystates: (i) performing; (ii) unlikely-to-pay (UTP); and (iii) non-performing (NPE). This typification does not provide any information on the real performance of the underlying Exposures in the different Scenarios versus the Base Scenario. For the purpose of standardization, we propose that the definition of performing and non-performing be shifted from the current IAS-IFRS accounting principles to the Exposures Performance , using the following Mutually Exclusive and Commonly Exhaustive function

| (63) |

where is Equation (20); is Equation (18); is Equation (27); and are components of Equation (45); and finally is the annual expected inflation rate (e.g. ) while is the monthly inflation rate (e.g. ). Although some Events per se might be inherently negative (e.g. Exposure defaults) or positive (e.g. Exposure return to life), when more than one Event jointly affects the Exposure at different times in a specific Scenario , it becomes extremely difficult ex-ante to define if the overall ex-post outcome. Considering that every Event materializes at a certain time , where (i.e. , , ), then

| (64) |

is the first time when any Event affects the Exposure in Scenario . In a Scenario let an Exposure be Performing in the range : indeed Equation (63) is always 0 because when an Exposure is Performing it means that its paying exactly as expected in the Base Scenario and thus and . In a Scenario let an Exposure be Full-Performing if . In a Scenario let an Exposure be Non-Performing when if . Finally, in a Scenario let an Exposure be Super-Performing when if . Notice that, even Exposures that are natively or under the IAS-IFRS, in the PEAL Method can still be considered Fully-Performing, Performing or Super-Performing in the different Scenarios if they follow the rules of Equation (63).

The novel approach of this Section typifies the Exposures to provide concrete and timely information to stakeholders. Indeed, it is not irrelevant to make advanced risk analyses to properly communicate overtime the mean, the median, and the estimated likelihood of the number of Exposures that, in the various relevant Scenario , are expected to be Full-Performing, Performing, Non-Performing, or Super-Performing.

11.2 Position Thickness (TH)

In this Section we will explain the regulatory definition of the -th Position Thickness , and then provide a simplified definition within the PEAL Method that is substantially equal, although formally different, as the ones of the European Regulations. The Position Thickness is the -nd Feature that shall be provided to the securitization stakeholders on an ongoing basis.

11.2.1 The Thickness regulatory definition

Reg 2401, Article 263(5), defines the -th Position thickness percentage as

| (65) |

where and where, pursuant Article 256 of Reg 2401, is the detachment point of Position ; and is the attachment point of Position . Reg 2401 implicitly assumes that the Positions be perfectly superimposable at the Horizontal Components, and thus that any Design the arranger could come up with would have no Vertical Positions. Such an hidden assumption not only is extremely strong, but we have already debunked it in the example of the previous Figure 1. Therefore, it becomes mandatory to provide an alternative solution to the computation of the Positions’ Thickness as the one proposed in the next Sec. 11.2.2.

Reg 2401, Article 256(1), defines the attachment point of the -th Position as \saythe threshold at which losses within the pool of underlying exposures would start to be allocated to the relevant securitization position. The attachment point shall be expressed as a decimal value between zero and one and shall be equal to the greater of zero and the ratio of the outstanding balance of the pool of underlying exposures in the securitization minus the outstanding balance of all tranches that rank senior or pari-passu to the tranche containing the relevant securitization position including the exposure itself to the outstanding balance of all the underlying exposures in the securitization. Then

| (66) |

is the attachment point, where

| (67) |

is the total outstanding balance, and where

| (68) |

is the outstanding balance of the each -th Position. Remember that . Notice that represents the -th column of the Gross Dimensioning Matrix as explained in the previous Sec. 10.2 and that this formula works if and only if the Positions are perfectly superimposable to their Horizontal Components (i.e. the Waterfall Configuration is composed of only horizontal slices). In the moment that the Positions were vertical or had other shapes, the Regulatory approach would fail and the PEAL Method general equation would be required (see next Sec. 11.2.2).