subsecref \newrefsubsecname = \RSsectxt \RS@ifundefinedthmref \newrefthmname = theorem \RS@ifundefinedlemref \newreflemname = lemma \newrefthmname = Theorem \newrefpropname = Proposition \newreflemname = Lemma \newrefcorname = Corollary \newrefassname = \newrefexaname = Example \newrefremname = Remark \newrefdefname = Definition \newrefeqrefcmd = (LABEL:#1) \newrefsecname = Section \newrefsubname = Section \newrefsubsecname = Section \newrefappname = Appendix \newrefsuppname = Online Appendix \newreffigname = Figure \newreftblname = Table \setstackgapS5pt \newreflrname = LR. \newreflrpname = LR.

Common Trends and Long-Run Multipliers

in Nonlinear Structural

VARs

Abstract

While it is widely recognised that linear (structural) VARs may omit important features of economic time series, the use of nonlinear SVARs has to date been almost entirely confined to the modelling of stationary time series, because of a lack of understanding as to how common stochastic trends may be accommodated within nonlinear models. This has unfortunately circumscribed the range of series to which such models can be applied – and/or required that these series be first transformed to stationarity, a potential source of misspecification – and prevented the use of long-run identifying restrictions in these models. To address these problems, we develop a flexible class of additively time-separable nonlinear SVARs, which subsume models with threshold-type endogenous regime switching, both of the piecewise linear and smooth transition varieties. We extend the Granger–Johansen representation theorem to this class of models, obtaining conditions that specialise exactly to the usual ones when the model is linear. We further show that, as a corollary, these models are capable of supporting the same kinds of long-run identifying restrictions as are available in linearly cointegrated SVARs.

1 Introduction

For more than four decades, the linear structural VAR (SVAR) model,

| (1.1) |

has played a central role in empirical macroeconomics. Structural VARs provide a satisfyingly coherent framework within which the problem of identifying causal relations, in the presence of simultaneity, may be approached by regarding the endogenous variables as dependent on an underlying sequence of exogenous structural shocks . Viewed through the lens of these models, the identification problem reduces to one of identifying these structural shocks and their associated impulse responses: equivalently, of identifying the mapping between and .

The early literature on structural VARs, following the seminal contribution of Sims (1980), developed contemporaneously with some major advances in the modelling of common (stochastic) trends in macroeconomic time series. This latter work culminated in the development of the theory of the cointegrated VAR, and in particular the Granger–Johansen representation theorem (GJRT), which showed how a VAR could be configured so as to accommodate the presence of common stochastic trends, and the cointegrating relations that are dual to them (Engle and Granger, 1987; Johansen, 1991). This demonstrated that the SVAR model could be reconciled with some of the evident properties of the (levels of) nonstationary macroeconomic time series, obviating the need to difference these series to stationarity prior to analysis (indeed, an implication of this work was that such pre-filtering was not only unnecessary, but could induce model misspecification). An important corollary to the GJRT was that by uncovering the mapping between the common trends and the endogenous variables, it made available a class of long-run identifying restrictions, relating to whether certain structural shocks were regarded as having permanent, or merely transient, effects (Blanchard and Quah, 1989; King et al., 1991).

Some subsequent research on the (S)VAR model has sought to extend it so as to allow for various forms of nonlinearity: typically as modelled via some sort of regime switching, possibly with smooth transitions between these regimes (see e.g. Chan, 2009; Teräsvirta et al., 2010; Hubrich and Teräsvirta, 2013). Recent interest in macroeconomic models that incorporate the possibility of occasionally binding constraints, of which the zero lower bound on interest rates is a leading instance, has its counterpart in the development of new class of regime-switching nonlinear VARs. These newer models are notably distinguished from that earlier literature by being able to accommodate endogenous regime switching, i.e. of allowing the current regime to depend on the current values of the endogenous variables, rather than being pre-determined, or being dependent on some exogenous switching process (Mavroeidis, 2021; Aruoba et al., 2022).

However, there remains a significant disconnect between the literature on nonlinear (S)VARs, and that on cointegration and common trends. In this respect, the situation is reminiscent of that of the literature on linear VARs in the early 1980s, with there being little theoretical understanding of how common trends may be accommodated within nonlinear VARs, such that the removal of common trends by pre-filtering remains a necessity. One area where significant efforts have been made to remedy this pertain to a certain class of ‘nonlinear VECM’ models. These are VAR models that are specified directly in VECM form, with a linear cointegrating space, but in which the stationary components of the model (the equilibrium errors and the lagged differences) are permitted to enter nonlinearly (see e.g. Escribano and Mira, 2002; Bec and Rahbek, 2004; Saikkonen, 2005, 2008; Kristensen and Rahbek, 2010, 2013). This class of models has proved sufficiently tractable to facilitate a nonlinear extension of the GJRT, but the assumptions made are such as to leave a substantial portion of the space of nonlinear VAR models unexplored.

In this paper, we generalise (LABEL:svar-intro) in the direction of the additively time-separable SVAR

| (1.2) |

where is continuous and has a continuous inverse (i.e. it is a homeomorphism), and each is continuous. We aim not only to extend the GJRT, but also to preserve exactly the kind of long-run identifying restrictions that are yielded by the GJRT in a linear setting, such that it remains possible to fruitfully discriminate between structural shocks on the basis of the permanence (or transience) of their effects. Through an associated VECM representation, this leads us to consider VARs for which the image of the map

is an -dimensional subspace of , a requirement that we term the common row space condition (CRSC); effectively, this entails a decomposition of the form . This reverses a key assumption of the nonlinear VECM literature, where is a fixed linear function, but is allowed to vary (as a function of and , or their lags). As we discuss, the principal motivation for the CRSC is that it ensures that only structural shocks may have permanent effects – whereas if the CRSC is violated, all structural shocks may have permanent effects, even though is driven by only common stochastic trends.

Our conditions on the nonlinear SVAR (LABEL:SVAR-intro) are otherwise rather general, and unlike the preceding literature allow for common stochastic trends to enter nonlinearly, thereby giving rise to nonlinear cointegrating relations between elements of . (A rigorous discussion of ‘cointegration’ in this nonlinear setting is deferred to a companion paper, in which the limiting distribution of the standardised process is derived; for a discussion of this in the context of the censored and kinked SVAR, see Duffy et al., 2023.) These conditions, along with a brief discussion of how they connect with the existing nonlinear VECM literature, are presented in 2. We further show that our conditions reduce to exactly those of the linear cointegrated VAR, when each is linear: and thus they do not appear to be particularly restrictive.

The principal contribution of this paper is to provide an extension of the GJRT to the setting of a nonlinear VAR (3), demonstrating how the model (LABEL:SVAR-intro) may be configured so as to generate common stochastic trends. This in turn permits an analysis of the stability of the steady state equilibria of the model, and a characterisation of the directions in which the shocks have only transient effects (4), and thereby yields identifying restrictions on . The GJRT also facilitates the calculation of the implied long-run multipliers associated with the shocks (5). We subsequently return, in 6, to a discussion of the role played by the CRSC in ensuring the availability of long-run identifying restrictions. Finally, 7 elaborates on a class of models in which each is piecewise affine (or a smooth, convex combination of piecewise affine functions) showing how the abstract conditions imposed on the model may be specialised for this class of models. 8 concludes. Proofs of all results appear in the appendices.

Notation.

denotes the th column of an identity matrix; when is clear from the context, we write this simply as . denotes the Euclidean norm on . Matrix norms are always those induced by the corresponding vector norm. For a random vector and , . For a matrix with , denotes some matrix, with , such that . For a collection of matrices, denotes the matrix formed as . The convex hull of is denoted . For a continuously differentiable function , denotes the Jacobian of at .

2 Model

2.1 ‘Structural’ and ‘reduced form’

We consider an additively time-separable nonlinear VAR() model for a -dimensional time series , of the form

| (2.1) |

where for , and is a sequence of ‘innovations’ taking values in in . (As a convenient location normalisation, we shall suppose throughout that for all .) By defining

| (2.2) |

for , we can write the model in nonlinear VECM form as

| (2.3) |

where

| (2.4) |

(see also 2.1 below).

In macroeconomics, a conventional starting point for empirical work is the structural (linear) VAR model, in which the observed series are assumed to be generated from an underlying i.i.d. sequence of structural shocks , also of dimension , whose elements are mutually orthogonal (or independent), and each of which have an economic interpretation (as e.g. an aggregate supply shock, a monetary policy shock, etc.). In the present setting, this amounts to positing that that there exists a parametrisation of the model (LABEL:nlVAR) for which

For the purposes of this paper, we will suppose – via restrictions on the parameter space for and/or the distribution of – that is identified up to an unknown invertible linear transformation of , i.e.

| (2.5) |

where . (Sufficient conditions for (2.5) to hold will be developed in detail elsewhere; these are not quite so trivial as in the linear case, since we now allow each to belong to some class of nonlinear transformations.) By analogy with the linear model, we henceforth term the reduced form innovations, even though they do not actually correspond to the innovations of a ‘reduced form model’ in the usual sense of the term.111The principal implication of (LABEL:red2struct) here is that, for the purposes of calculating the long-run effects of the structural shock – the structural long-run multipliers – it suffices to compute the corresponding effects of the reduced form shocks, and then postmultiply these by . By focusing on the latter, as we do in this paper, we can separate the analysis of the model’s dynamics from the identification of the structural shocks.

2.2 The common row space condition

In the linear VAR, where , the key assumption required for the model to generate common stochastic trends (i.e. cointegrated processes) is that , where is the number of unit roots in the autoregressive polynomial. Equivalently, this condition may be expressed in terms of the image of the map ,

being an -dimensional (linear) subspace of . In extending the GJRT to the setting of the nonlinear VAR (LABEL:nlVAR), the role of (or more precisely, ) will now be played by , and our high-level assumptions below will ensure that

remains an -dimensional (linear) subspace of , exactly as in the linear case. We term this the common row space condition (CRSC). (Note that there is no corresponding restriction on ; in particular, this will not be required to be a -dimensional subspace of .)

The existing literature on nonlinear VECM models effectively reverses this condition by requiring that be a -dimensional subspace of , without restricting (see in particular Kristensen and Rahbek, 2010). Loosely speaking, if we suppose that may be decomposed, for each , as

| (2.6) |

where , then the CRSC effectively entails (if is appropriately normalised), but that is otherwise unrestricted; whereas in the existing literature, is constant, with the result that there is a globally linear cointegrating space, whereas the models developed here allow the cointegrating relations to be nonlinear. The representation theory in the nonlinear VECM literature is thus strictly complementary to the present work. (Note that even the case where in our model is not encompassed by that literature, because we allow the dynamics of the implied VECM to depend on the level of , whereas that literature requires that these be governed entirely by the equilibrium errors and differences .)

The motivation for imposing the CRSC lies in our desire to maintain two key properties of the linear structural VAR. Recall that in that model, common stochastic trends arise because some subset of the structural shocks (say, in number) have permanent effects on , while the remaining shocks have only transitory effects. This provides not only an underpinning economic explanation for the patterns of long-run co-movement present in the data, but also a fruitful source of long-run identifying restrictions (following Blanchard and Quah, 1989, and King et al., 1991): properties that we would like to preserve as we generalise the cointegrated linear structural VAR in the direction of (LABEL:nlVAR).

However, these properties appear to be highly sensitive to departures from the CRSC, even when the assumption of a globally linear cointegrating space is maintained (i.e. when for all in (LABEL:factor) above). In models where this condition fails, it will generally be the case that the direction in which an impulse has no permanent effect on will vary with the magnitude . In 6 below, we provide a simple example to illustrate how this may imply that all structural shocks must have a permanent effect on , even though has only common stochastic trends. Thus, if we want to work with a class of nonlinear VAR models in which (structural) shocks may be distinguished on the basis of their long-run effects – and in which, as a corollary, common stochastic trends arise because only a subset of these shocks have permanent effects – then it would appear that the CRSC cannot be easily dispensed with.

2.3 High-level assumptions

To state our main assumptions on the model (LABEL:nlVAR), we first provide a more compact representation for (LABEL:VECM-first); its proof appears in B.

Lemma 2.1.

Suppose follows (LABEL:nlVAR). Then (LABEL:VECM-first) holds. Defining , where

and letting , we also have

| (2.7) |

for ,

and the first rows of .

Remark 2.1.

(i). The preceding holds exactly as stated when ; the model with may be handled as a special case of with and (possibly also) . Alternatively, we may specialise the above to by taking to be an ‘empty’ matrix when , and when . (In the proofs and statements of all results, to avoid these kinds of complications, we shall implicitly maintain throughout, without loss of generality, that .)

(ii). (LABEL:VECM-system) differs notably from the companion form representation that is typically employed in the analysis of linear VECMs. In particular, the state vector is not

but rather

| (2.8) |

where the final equality holds only in the case of a linear VAR. By comparison with , we have defined so that the r.h.s. (LABEL:VECM-system) involves a nonlinear transformation of only , and is otherwise linear in . This permits a major simplification of the problem when ; for this the assumption of additive separability is crucially important.

We next define a class of nonlinear VAR models (parametrisations of (LABEL:nlVAR)), that will be shown to be consistent with the presence of common (possibly nonlinear) stochastic trends in , and ‘cointegrating relations’ between those series. For some , define

| (2.9) |

and for with ,

| (2.10) |

Recall that a function is a homeomorphism if it is continuous, bijective, and has a continuous inverse. is bi-Lipschitz if there exists a such that for all ; we term any such a bi-Lipschitz constant for . For a bounded collection of matrices, let denote its joint spectral radius (JSR; e.g. Jungers, 2009, Defn. 1.1), where is the set of -fold products of matrices in , and the spectral radius of .

Definition 2.1.

Let , have , , and . We say that the VAR() model (LABEL:nlVAR), parametrised by and , belongs to class if:

-

(.i)

is a homeomorphism;

-

(.ii)

there exists and such that

for all ;

-

(.iii)

for every and in , there exists a (possibly depending on and ) such that

(2.11) where is closed and , and

(2.12)

Let denote those models in for which , the identity on . We denote by (resp. ) the union of all classes (resp. ) with having , and .

Remark 2.2.

(i). We allow to be non-trivial to permit (linear and nonlinear) structural VARs to be accommodated within the present setting. In the linear case, is trivially continuous; requiring to be a homeomorphism extends this to a nonlinear setting. When deriving the properties of the series generated by the models in class , we shall first rewrite the system in terms of , which is itself generated by a model in class (see A.2 in A).

(ii). It follows from the preceding conditions, and principally from (iii), that is continuous for each ; indeed, these are Lipschitz when (see A.4 in A).

(iii). A fundamental role will be played throughout the following by the map defined by

| (2.13) |

where

| (2.14) |

As developed in 3 below, if is generated by a model from class , then and respectively provide a representation for the ‘common trends’ and ‘equilibrium errors’ in the system. Since is guaranteed to be a homeomorphism under our assumptions (see A.4 in A), these maps provide an exhaustive description of . As a further consequence of the invertibility of , we have and hence , an -dimensional subspace of ; our assumptions thus ensure that the model satisfies the common row space condition discussed in 2.2 above.

(iv). The case corresponds to and for all . The results in this paper will be seen to cover this case, if the appropriate adjustments are made by deleting and from those objects in which they appear, so that e.g. now and . (To keep this paper to a manageable length, we do not treat this case explicitly in our proofs.) At the other extreme, the case corresponds to a system with no common trends, and the VAR is stationary. For this reason, we generally restrict the statements of our results to the case where .

(v). (iii) is our principal assumption on the stability of the weakly dependent components of the system, which comprise the ‘equilibrium errors’ , and the ‘lagged differences’ for . In a linear cointegrated VAR, these reduce to the familiar and , which are stationary by the GJRT. Though in the present setting, and will generally not be stationary, (LABEL:jsr) nonetheless ensures that these are of strictly smaller order than itself, exactly as in a linearly cointegrated system. As shown in 2.4 below, in a linear VAR (iii) reduces to precisely the familiar conditions on the roots of the associated autoregressive polynomial; whereas the form in which it is stated here is applicable to models which depart so far from linearity that no useful notion of ‘autoregressive roots’ is available.

(vi). The requirement that (LABEL:gradient) hold with implies is Lipschitz, with a Lipschitz constant that is bounded by ; the converse is also true (see A.1 in A). Excepting cases where and interact in a very particular way, this condition signals that our concern here is principally with models in which the equilibrium errors are defined by a function for which as , i.e. which exhibits at most linear asymptotic growth. For example, if and , for , then (iii) requires to be Lipschitz, and thus that as , for .

Our assumptions on the data generating process may now be stated.

Assumption CVAR.

Given , follows (LABEL:nlVAR) for , where belong to class .

For the purposes of this paper, the sequence of innovations may be generally treated as a given non-random sequence in , since our results are either non-asymptotic, or take limits under the assumption that the shocks cease at some finite horizon . However, it will occasionally be useful to indicate the implications of our results in cases where the following holds (as is further developed in a companion paper to the present work).

Assumption ERR.

is a random sequence in , such that for some , and

| (2.15) |

on , where is a -dimensional Brownian motion with positive-definite variance .

2.4 Relationship to the linear VAR

To help cast further light on the defining conditions of class , we now show that when (LABEL:nlVAR) is specialised to a linear VAR, these conditions reduce to exactly the usual conditions for a linear VAR to generate common components, as per the GJRT (Johansen, 1995, Ch. 4). This provides a clear indication that our conditions on the general, nonlinear VAR are not overly restrictive. By a linear VAR, we mean one in which for some , for , so that (LABEL:nlVAR) becomes

| (2.16) |

Let denote the associated autoregressive polynomial.

Proposition 2.1.

Suppose is a linear VAR, where for some ,

-

LIN.1

is invertible;

-

LIN.2

and ; and

-

LIN.3

has roots at unity, and all others outside the unit circle.

Then belongs to class , with: , where for ; and

for such that .

3 Common trends

The starting point for the analysis of the linear cointegrated VAR is the Granger–Johansen representation theorem (GJRT), which decomposes into the sum of: (i) an initial condition, (ii) a stochastic trend, and (iii) a weakly dependent process (which is stationary if is suitably initialised). This may be rendered in various ways: to facilitate the comparison with 3.1 below (from which it follows in the linear case), we shall here write this for a linear VAR satisfying (i)–3, as

| (3.1) |

where: (i) captures the dependence on the initial values ; (ii) is a stochastic trend of dimension ; and (iii)

| (3.2) |

follows a VAR, where and are as in (LABEL:lin-boldbeta) above. The stability of this VAR follows from 2.1, because membership of implies, via (iii), that all the eigenvalues of must lie inside the unit circle. (It may also be noted from (LABEL:bz-in-linear) above that, in this case, is itself a linear function of .) may thus be rendered stationary through an appropriate choice of the initial conditions ( or, equivalently, ).

Before providing our extension of the GJRT to the general setting of (LABEL:nlVAR), we first note that the counterpart of will continue to follow an autoregression of the form (LABEL:eqerr-linear), but now with time-varying coefficients, in particular with now depending on the level of . While such processes cannot be rendered stationary, we still have a well-defined notion of stability for such processes, which is important for ensuring that remains of strictly smaller stochastic order than the common trends.

Definition 3.1.

Suppose that follows the time-varying VAR,

| (3.3) |

where , , and for all , from some given . We say that is exponentially stable if and are bounded, and there exists a and a such that

A sufficient condition for exponential stability is that (e.g. Jungers, 2009, Cor. 1.1), which motivates the restriction on the JSR that appears in (iii). Notable consequences are that if for all , then , while if and have uniformly bounded moments, then . (For this last, see Lemma A.1 in Duffy et al., 2023.)

Theorem 3.1.

Suppose CVAR holds. Then in (LABEL:co-map) is a homeomorphism, and

| (3.4) |

where

is the matrix given by

and

follows the exponentially stable VAR

| (3.5) |

with for all .

Remark 3.1.

(i). That the preceding specialises to (LABEL:GJ-type-rep) in the linear case follows from the fact that and by 2.1, and that for as in (LABEL:lin-boldbeta). To illustrate more clearly the connection between (LABEL:GJ-type-rep) and conventional statements of the GJRT, we note that the part of the r.h.s. of (LABEL:GJ-type-rep) that depends on the common stochastic trends may be written as

| (3.6) |

by D.1 in D, which agrees precisely with Johansen (1995, Ch. 4).

(ii). Suppose that satisfies ERR. Then it follows by Lemma A.1 in Duffy et al. (2023) that , and so is strictly of smaller order than . This is crucial for obtaining the limiting distribution of the standardised process : though here further assumptions are required, because of the presence of the nonlinear map in (LABEL:gjrt-z). Results of this kind, which were obtained in the setting of the CKSVAR by Duffy et al. (2023), are the subject of a companion paper to the present work.

(iii). Applying to both sides of (LABEL:gjrt-z), we obtain

Asymptotically, under ERR, the dominant component of would be the common trends , which would in turn dominate , since the latter equals the first components of the stable autoregressive process . In this sense, the action of separates into its ‘common trend’ and ‘equilibrium error’ components. Since is purged of these common trends – while being restricted by the requirement that be a homeomorphism – it may be said to provide a representation of the ‘nonlinear cointegrating relations’ that exist between the elements of .

4 Attractor spaces

A first application of 3.1 is to verify the stability of the (non-stochastic) steady state solutions to (LABEL:nlVAR). By considering (LABEL:VECM-first) when for some and , we see that for to be a steady state equilibrium, it must satisfy

or equivalently , since and . Thus the set of steady state equilibria is given by the -dimensional manifold

| (4.1) |

where the fact that is indeed a -dimensional manifold follows from the second equality, since is a homeomorphism.

For the purposes of analysing the stability of , we shall suppose that the shocks are set to zero after some : that is, for all , and then consider how evolves from time forward. In other words, we shall fix the state of the model at time at

| (4.2) |

allow one final shock to occur at time ; and then evaluate the (non-stochastic) limit of as . We aim to show that is strictly stable, in the sense of the following.

Definition 4.1.

is stable if for every , there exists a such that . is a non-trivial attractor if for every , there exists a non-empty such that for all ; we term the domain of attraction for , given . is strictly stable if it is stable and contains only non-trivial attractors.

In other words, if is strictly stable, then whatever the current state of the model and the given , there is always a value for the -dated shock that would lead to converge to ; every element in may ultimately be ‘reached’ from . (Note that this is not as trivial as choosing such that immediately, since what is required is that converge to a steady state in which Since is exponentially stable by 3.1, it follows that as . Hence, noting that , we have by that result that

Because the r.h.s. depends on only through , and as varies ranges freely over , we can induce to take any desired value . We thus obtain the following.

Theorem 4.1.

Suppose CVAR holds. Then

-

(i)

for every , as

(4.3)

-

(ii)

for any the -dimensional affine subspace

(4.4) is the domain of attraction for , given ;

and hence is strictly stable.

Remark 4.1.

(i). In view of the preceding, we are justified in referring to as the attractor space for .

(ii). If the model is in a steady state equilibrium at some , immediately prior to the incidence of , so that for all , then

and in this case the domain of attraction (LABEL:domain-of-attraction) reduces to .

(iii). In the linear VAR, , and thus the attractor space simplifies to the -dimensional affine subspace

while the domain of attraction for is the -dimensional affine subspace

As a direct consequence of the preceding, we obtain the following characterisation of the linear combinations of the (reduced form) shocks that do not have permanent effects.

Corollary 4.1.

Suppose CVAR holds. Then for every ,

i.e. a shock has no permanent effect on , if and only if it lies in .

The significance of this result may be explained as follows. Suppose that we have the nonlinear SVAR

belonging to class , where is suitably normalised such that is identified up to premultiplication by an orthogonal matrix, as it is in the linear SVAR. (The reader may find it helpful to consider the simplified setting in which is linear, so that such a normalisation could be achieved simply by imposing , though this is not necessary for the argument that follows). Suppose that we partition the structural shocks as

where takes values in , and consists of structural shocks that are regarded as having no permanent effect on . Then 4.1 implies that

which provides long-run identifying restrictions on , exactly as in a linear SVAR (see Kilian and Lütkepohl, 2017, Sec. 10.2).

5 Long-run multipliers

Having obtained a characterisation of the attractor space for , we may finally say something about the permanent effect of a shock at time . The limiting impulse responses or long-run multipliers can be computed by differentiating with respect to , i.e. by computing the Jacobian

| (5.1) |

One concern we might have here, in the general nonlinear case, is the apparent dependence of these long-run multipliers on , which potentially ranges over a very ‘large’ space. However, it will be noted that only depends on through : and as shown in the proof of the next result, it is always possible to find a such that . Therefore, for the purposes of computing the full set of possible long-run effects of shocks in the model, it suffices to consider cases in which the model is in a steady state equilibrium (i.e. where for some ) immediately prior to the incidence of the shock.

Because is not necessarily differentiable everywhere, the long-run multipliers as defined in (LABEL:multipliers) may not exist for every . However, in most cases of interest, the subset at which this occurs will be exceptionally small, corresponding e.g. in the case of piecewise affine models (see 7 below) to points exactly on the boundary between two regimes. It is also possible that the Jacobian of may fail to be invertible at exceptional points: though it must be invertible almost everywhere, since is invertible.

Theorem 5.1.

Suppose CVAR holds. Let denote the set of all at which

is not differentiable with respect to , when , and denote the union of with the set of at which the Jacobian of the preceding is non-invertible. Then

-

(i)

the full set of long-run multiplier matrices is given by

(5.2) for ; and

-

(ii)

for every .

Remark 5.1.

(i). In the linear VAR, it follows by 2.1 and D.1 that

consistent with (LABEL:gjrt-linear) above. In this case, the limiting IRF is invariant to the state of the process prior to the incidence of the final shock.

(ii). In nonlinear VARs such as (LABEL:nlVAR), impulse responses with respect to a shock incident at time are well known to be dependent on both the current state of the model, and on the shocks that occur subsequent to time . In computing the long-run multipliers above, we have allowed for dependence on the current state, but deliberately forced for . This not only simplifies the analysis but, we would argue, provides a reasonable basis on which to determine whether the structural VAR permits certain (small) shocks to have permanent effects on the model variables, particularly in a nonstationary model of this kind, where subsequent shocks may push in any region of the state space (though it will, in some sense, still remain ‘attracted’ to ).

Nonetheless, let us suppose that, following Koop et al. (1996), one is also interested in ‘generalised’ impulse responses that are computed conditional on , but which average over all (potential) histories of the shocks subsequent to . Then while we could not hope to obtain as clean a characterisation of the limiting IRF as is given above the fact that the major implication of (LABEL:multipliers), that

is invariant to the state of the process suggests that this property would continue to hold for the generalised impulse responses. However, because of the possible long-range dependence of on past shocks, via (and hence ), these calculations far from straightforward, and are therefore deferred to future work.

6 Without the common row space condition

As noted in 2.2 above, a key property of models in is that they satisfy the CRSC, the requirement that be an -dimensional linear subspace of . Here we provide a simple example to substantiate the claim made above, that a violation of the CRSC will generally lead to a situation in which all the structural shocks have permanent effects, and as such the long-run identification restrictions that stem from 4.1 above are rendered unavailable.

To this end, we consider a nonlinear VAR(1), specified in VECM form as

where for a smooth function satisfying and , and , each having rank ,

so that the model is one in which the kernel of is a fixed -dimensional subspace (given by ), but the image of is not a linear subspace. (If we further suppose that the eigenvalues of lie strictly inside the unit circle, then the model satisfies conditions (A.2) and (A.3) of Kristensen and Rahbek (2010), who provide a GJRT for these models.) This model may be regarded as smoothly combining two regimes: an ‘inner’ or ‘near equilibrium’ regime in which

and an ‘outer’ or ‘far from equilibrium’ regime where is replaced by . If the eigenvalues of associated to the inner regime are also strictly inside the unit circle, then is a strictly stable attractor in the sense of 4.1 above.

Now suppose we were to repeat the analysis of 4 for this model: i.e. fixing the state of the model in time , having the model impacted by a final shock , and then computing the limit in the absence of any further shocks (so for all ). We may then ask: what values of would leave unchanged? That is, we would like to determine the set

Let us suppose (unlike what is maintained in 4 above), that , so that , and the model is in equilibrium prior to the incidence of . Locally to , we would expect shocks in the direction of to have no permanent effects; whereas further from , shocks in directions lying progressively closer to should have no permanent effects.

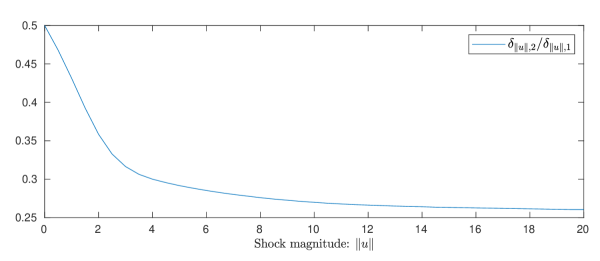

6.1 illustrates this is indeed the case for a bivariate () model with

and . (Without loss of generality, we take .) For each between and , the figure reports the (unique) direction such that has no permanent effect on ; for the sake of comparability with and , both of which have unit first element, this is reported in terms of the ratio . We see here that takes the value when , and tends towards as grows (equalling when ). As a consequence

and as such there is no direction along which the reduced form shocks will only have transient effects. There is thus no possibility of discriminating between the underlying structural shocks according to whether not they have permanent effects: each must, depending on the magnitude of the shock.

7 Piecewise affine VARs

Finally, we introduce a class of regime-switching models in which the conditions required for our results may be verified relatively straightforwardly. Suppose that for each ,

| (7.1) |

where is a collection of convex sets that partition , and .222If instead , with a partition that depends on , the model can nonetheless be written in terms of of the form (LABEL:pwa), i.e. with a lag-independent partition , by forming each from a refinement of the sets in , as ranges over . When these parameters are such that is continuous for each , we shall say that each is a piecewise affine function, and refer to the model as a piecewise affine VAR. (We do not consider cases in which may be discontinuous; so continuity is always implied when a function or VAR is described as being piecewise affine.)

Piecewise affine VARs, of which the CKSVAR of Mavroeidis (2021) is a recent instance, provide a flexible but tractable means of introducing nonlinearity into a vector autoregressive model. Defining

we see that

This is a kind of endogenous regime-switching VAR, in which the sets demarcate distinct ‘regimes’. However, unlike in typical models of this kind, there is no requirement that the same ‘regime’ apply e.g. to and – each may lie in a different member of – and so it might be more correct to say that there are a total of autoregressive regimes, once all the possible patterns of membership of in the sets are allowed for. Nonetheless, it turns out that a fruitful approach to analysing the long-run behaviour of these systems focuses attention on those ‘linear submodels’ that arise when each of lie in the same , to each of which we may associate the autoregressive polynomial

| (7.2) |

7.1 Simplification of the JSR condition

The conditions for membership of , for piecewise affine VARs, will parallel (i)–3. Before stating these, we first give a result that reduces (iii) to a condition on the JSR of a collection of only matrices (rather than a collection of uncountably many matrices). To state it, observe that

| (7.3) |

In this context, we note that (ii) effectively requires that

| (7.4) |

where with . Further, let , , and

| (7.5) |

Lemma 7.1.

Suppose that is a piecewise affine model, for which there exists an with such that

-

(i)

, and , for , for all ; and

-

(ii)

is a homeomorphism.

Then satisfies (LABEL:gradient) with equal to , and so

Since the eigenvalues of correspond to the inverses of the non-unit roots of , a necessary, though not sufficient condition for

is that the eigenvalues of should lie strictly inside the unit circle, for all . Thus, if , as per (LABEL:Pi-ell), then will have roots at unity, and all others strictly outside the unit circle (this follows e.g. from arguments given in the proof of 2.1). In other words, for a piecewise affine model to belong to class (for some ), it is essentially necessary that each of its linear submodels satisfy the usual conditions for a linear VAR to give rise to common trends and cointegrating relations (i.e. conditions (ii) and (iii) above).

7.2 Membership of

It remains to consider (i), i.e. the requirement that be a homeomorphism. For the purposes of verifying this condition, two important special cases of the piecewise affine VAR are:

-

•

the piecewise linear VAR (PLVAR), in which there exists a basis for such that each can be written as a union of cones of the form

where ranges over the subsets of , and for all and ; and

-

•

the threshold affine VAR (TAVAR), in which there exists an and thresholds with , and , such that

i.e. the sets take the forms of ‘bands’ in . (In typical examples, , i.e. it picks out one ‘threshold variable’ from the elements of .)

In these models, the results of Gourieroux et al. (1980) provide necessary and sufficient conditions for to be invertible, which can be expressed in terms of the determinants of . We thus have the following

Proposition 7.1.

Suppose is is either a piecewise linear or threshold affine VAR, such that:

-

PWA.1

for all ;

-

PWA.2

, , and , where have rank , for all ; and

-

PWA.3

.

Then belongs to class , for , with

| (7.6) |

where

for . Moreover, the same conclusion holds if is a general piecewise affine model satisfying (ii) and (iii) above, if is a homeomorphism.

7.3 Smooth transitions

The model (LABEL:pwa) may also be extended to allow for smooth transitions between the regimes. In the literature on smooth transition (vector) autoregressive models, the conventional approach (e.g. Hubrich and Teräsvirta, 2013, Sec. 3.3) is to replace the indicator functions by smooth maps , so that now

where and for all , so that is a always a smooth, convex combination of the affine functions . While models of this kind may be accommodated within our framework (under certain regularity conditions), the fact that the gradient of is not a convex combination of those underlying affine regimes makes it difficult to reduce (iii) to a bound on the JSR of a finite collection of matrices, in the manner of 7.1. As an alternative specification that allows for smooth transitions between regimes, while also keeping (iii) tractable, consider

| (7.7) |

where is a (continuous) piecewise affine function as in (LABEL:pwa) above, and is a smooth kernel with mean zero. Then we have the following.

Proposition 7.2.

Suppose that:

-

(i)

is either a piecewise linear or threshold affine VAR satisfying (i)–3;

-

(ii)

for all , for some nonsingular ;

-

(iii)

is continuous and non-negative, with and ;

-

(iv)

is constructed by smoothing with as in (LABEL:smoothed), for .

Then belongs to class , for , for as in (LABEL:beta_l) above.

The requirement in (ii) that be linear is needed principally to facilitate the verification of (iii), because of the role played by there. We expect that it should be possible to extend the preceding to allow to be a general piecewise affine function, albeit possibly at the cost of additional regularity conditions. (Indeed, it may be shown that the smooth counterpart of is a homeomorphism if every is invertible, thereby satisfying (i).)

8 Conclusion

This paper has extended the Granger–Johansen representation theorem to a flexible class of additively time-separable, nonlinear SVAR models. This shows that such models may be applied directly to time series in which (common) stochastic trends are present, without the need for pre-filtering, thus avoiding the potential for misspecification that this entails. As an important corollary to our results, we show that these models are capable of supporting the same kinds of long-run identifying restrictions as are available in linear cointegrated SVARs. A companion paper to the present work provides limit theory for , and a further discussion of nonlinear cointegration, under the assumptions maintained here.

References

- Aruoba et al. (2022) Aruoba, S. B., M. Mlikota, F. Schorfheide, and S. Villalvazo (2022): “SVARs with occasionally-binding constraints,” Journal of Econometrics, 231, 477–499.

- Bec and Rahbek (2004) Bec, F. and A. Rahbek (2004): “Vector equilibrium correction models with non-linear discontinuous adjustments,” The Econometrics Journal, 7, 628–651.

- Blanchard and Quah (1989) Blanchard, O. J. and D. Quah (1989): “The dynamic effects of aggregate demand and supply disturbances,” American Economic Review, 79, 655–73.

- Chan (2009) Chan, K. S., ed. (2009): Exploration of a Nonlinear World: an appreciation of Howell Tong’s contributions to statistics, World Scientific.

- Duffy et al. (2023) Duffy, J. A., S. Mavroeidis, and S. Wycherley (2023): “Cointegration with Occasionally Binding Constraints,” arXiv:2211.09604v2.

- Engle and Granger (1987) Engle, R. F. and C. W. J. Granger (1987): “Co-integration and error correction: representation, estimation, and testing,” Econometrica, 251–276.

- Escribano and Mira (2002) Escribano, A. and S. Mira (2002): “Nonlinear error correction models,” Journal of Time Series Analysis, 23, 509–522.

- Gourieroux et al. (1980) Gourieroux, C., J. J. Laffont, and A. Monfort (1980): “Coherency conditions in simultaneous linear equation models with endogenous switching regimes,” Econometrica, 48, 675–695.

- Horn and Johnson (2013) Horn, R. A. and C. R. Johnson (2013): Matrix Analysis, C.U.P., 2nd ed.

- Hubrich and Teräsvirta (2013) Hubrich, K. and T. Teräsvirta (2013): “Thresholds and smooth transitions in vector autoregressive models,” in VAR Models in Macroeconomics – New Developments and Applications: essays in honor of Christopher A. Sims.

- Johansen (1991) Johansen, S. (1991): “Estimation and hypothesis testing of cointegration vectors in Gaussian vector autoregressive models,” Econometrica, 1551–1580.

- Johansen (1995) ——— (1995): Likelihood-based Inference in Cointegrated Vector Autoregressive Models, O.U.P.

- Jungers (2009) Jungers, R. M. (2009): The Joint Spectral Radius: theory and applications, Springer.

- Kilian and Lütkepohl (2017) Kilian, L. and H. Lütkepohl (2017): Structural Vector Autorgressive Analysis, C.U.P.

- King et al. (1991) King, R. G., C. I. Plosser, J. H. Stock, and M. W. Watson (1991): “Stochastic Trends and Economic Fluctuations,” American Economic Review, 81, 819–840.

- Koop et al. (1996) Koop, G., M. H. Pesaran, and S. M. Potter (1996): “Impulse response analysis in nonlinear multivariate models,” Journal of econometrics, 74, 119–147.

- Kristensen and Rahbek (2010) Kristensen, D. and A. Rahbek (2010): “Likelihood-based inference for cointegration with nonlinear error-correction,” Journal of Econometrics, 158, 78–94.

- Kristensen and Rahbek (2013) ——— (2013): “Testing and inference in nonlinear cointegrating vector error correction models,” Econometric Theory, 29, 1238–1288.

- Mavroeidis (2021) Mavroeidis, S. (2021): “Identification at the zero lower bound,” Econometrica, 69, 2855–2885.

- Saikkonen (2005) Saikkonen, P. (2005): “Stability results for nonlinear error correction models,” Journal of Econometrics, 127, 69–81.

- Saikkonen (2008) ——— (2008): “Stability of regime switching error correction models under linear cointegration,” Econometric Theory, 24, 294–318.

- Sims (1980) Sims, C. A. (1980): “Macroeconomics and reality,” Econometrica, 1–48.

- Teräsvirta et al. (2010) Teräsvirta, T., D. Tjøstheim, and C. W. J. Granger (2010): Modelling Nonlinear Economic Time Series, O.U.P.

Appendix A Auxiliary lemmas

As noted in 2.12.1, we shall not generally indicate how our results may specialise in cases where ; the reader is accordingly advised to treat these models as particular degenerate instances of the VAR() model with .

Lemma A.1.

Suppose . Then the following are equivalent:

-

(i)

is Lipschitz, with Lipschitz constant ;

-

(ii)

for every , there exists a with such that

(A.1)

Recall the definitions of , and given in (LABEL:ge), (LABEL:pi-def) and (LABEL:co-map).

Lemma A.2.

Suppose belongs to class . Then the model , with and for belongs to class , with for , , and

Moreover, we may take , where and satisfy (iii) for models and respectively.

Recall the definition of from (LABEL:bold-alpha).

Lemma A.3.

Let with , and . Then

Recall the definition of a bi-Lipschitz function given in 2.3.

Lemma A.4.

Suppose belongs to class , for some and . Then is continuous for , and the map in (LABEL:co-map) is a homeomorphism. If in addition is bi-Lipschitz, with bi-Lipschitz constant , then is also bi-Lipschitz, with bi-Lipschitz constant that depends only on , , and .

Appendix B Proofs of auxiliary lemmas

Since some of the proofs rely on the representation given in 2.1, the proof of this result is given first.

Proof of 2.1.

By direct calculation,

whence it follows from (LABEL:nlVAR) and the definition of that

which yields (LABEL:VECM-first). Further, since ,

so that

as per the first elements of (LABEL:VECM-system). Finally, we note that for ,

and

so that stacking these equations as ranges over yields the remaining elements of (LABEL:VECM-system). ∎

Proof of A.1.

(ii) trivially implies (i); it remains to prove the reverse implication. Let with be given, and let and , so that by (i). Taking satisfies (LABEL:f-x). Finally, we note

where holds because the maximum is achieved by taking . ∎

Proof of A.2.

The claimed forms of , and follow immediately from the definitions of these objects, e.g. from (LABEL:ge) we have

etc. It remains to verify the three conditions required for to belong to class , as per 2.1.

(i). is the identity by construction, and thus trivially a homeomorphism.

Proof of A.3.

Let be such that , and . For any ,

where and are as defined in (LABEL:bold-alpha). By construction, and have full column rank, and . They thus span the whole of , whence the second r.h.s. matrix is invertible. It will be shown below that is invertible, and hence so too is the first r.h.s. matrix. Therefore

Let denote the closed ball centred at zero, of radius , in , and

Then is a closed subset of . Suppose that is compact, with . It follows by Jungers (2009, Prop. 1.4) that that there exists a norm on such that

Hence, by the equivalence of and , there exists a such that for all ,

where holds by Theorem 5.6.18 in Horn and Johnson (2013). Thus is indeed invertible as claimed. Since the final bound is independent of , it follows that

while also

Since does not depend on , the claim follows. ∎

Proof of A.4.

We first suppose that , i.e. the model is in class . We shall show in this case that each is Lipschitz; and that is bi-Lipschitz, and therefore a homeomorphism.

To that end, define as

| (B.1) |

where for and . By evaluating (LABEL:bold-chi) when , and applying A.1, we see that (iii) implies that and are Lipschitz, with Lipschitz constant depending only on . Hence is Lipschitz for , and moreover so too is

Since by (LABEL:ge), it follows that is Lipschitz for .

We now turn to . Let , , and . Then

and hence

Let , and . Then by the preceding (recalling denotes the Euclidean norm),

while by (iii) (with ), there exists a such that

| (B.2) |

Since for all , there exists a (depending only on ) such that

| (B.3) |

As noted above, is Lipschitz: hence there exists a (depending only on ) such that

| (B.4) |

By A.3, the matrix on the r.h.s. of (LABEL:boldco) is invertible; hence

That lemma further implies that there exists a , depending only on , and , such that

| (B.5) |

where follows since

Deduce from (LABEL:boldco)–(LABEL:co-diff-3) that there exists a , depending only on , and , such that

for all . Hence is bi-Lipschitz, as required.

Finally, suppose that is not the identity, but merely a homeomorphism (as per (i)). By A.2, the model , with and for is in class , and it follows by the preceding that each is Lipschitz, and the associated is bi-Lipschitz. Clearly is continuous for each . Moreover , whence is also a homeomorphism. If is bi-Lipschitz with bi-Lipschitz constant , then is bi-Lipschitz, with bi-Lipschitz constant depending only on , , and . ∎

Appendix C Proofs of high-level results

This section provides proofs of our main results under the high-level conditions provided by the definition of class (see 2.1).

Proof of 3.1.

We note that is a homeomorphism by A.4.

To obtain (LABEL:gjrt-z), we first evaluate each of and in turn. Regarding the former, we observe that by (LABEL:DZ)–(LABEL:Crep),

Since the VAR belongs to class , for each there exists a such that

and hence

| (C.4) |

as per (LABEL:gjrt-xi). By definition of and ,

| (C.5) |

where the final equality follows from the final equations in (LABEL:VECM-system), whence

| (C.6) |

for

We next turn to . By (LABEL:DZ)–(LABEL:Crep), and the definition of in (LABEL:bold-alpha),

whence

| (C.7) |

We need to relate the l.h.s. to

where the second equality follows since

| (C.8) |

To that end, we note that

for where the final equality follows by (LABEL:xi-components), for the matrix of the form

Hence by (LABEL:ctsum),

| (C.9) |

It then follows from (LABEL:eqrep) and (LABEL:ctrep) that

which yields (LABEL:gjrt-z) with .

Finally, suppose that is a general homeomorphism. Observe that satisfies

i.e. it is generated by a model with . By A.2, this model belongs to class , with the same and . Therefore, by the arguments given above, (LABEL:gjrt-z) holds in the form

It additionally follows from A.2 that the l.h.s. is equal to , while

and, recalling (LABEL:xi-components) above,

| (C.10) |

since . Since (LABEL:xi-lom) holds as

where for each , it then follows by (LABEL:xi-ast-xi) and A.2 that

where for each , since . ∎

Proof of 4.1.

Without loss of generality, we may take . We note that is a homeomorphism by A.4.

(i). Regarding (LABEL:zt-det-lim), we have from 3.1 with and that

where satisfies (LABEL:gjrt-z) with for all ; whence

for some . Since , it follows by Jungers (2009, Prop. 1.4) that there exists a norm such that

as . (LABEL:zt-det-lim) then follows.

(ii). By (LABEL:zt-det-lim), if and only if

whence

Since is non-empty for every , it follows that is strictly stable. ∎

Proof of 5.1.

(i). We note that depends on only through , and that setting

yields a with . Since the l.h.s. of

is differentiable with respect to (at ) if and only if the r.h.s. is, the long-run multipliers are only well defined when , and the full set of long-run multipliers can thus be recovered by computing

for each . The second equality in (LABEL:lrmult) then follows by the chain rule.

Appendix D Proofs relating to examples

D.1 Linear systems

Proof of 2.1.

We verify the conditions required for a model to be in class (see 2.1); the other claims follow either in the course of the subsequent arguments, or directly from the relevant definitions.

(i). Since is invertible, is trivially a homeomorphism.

(ii). Since , there exist having full column rank, such that . Then implies that for some .

(iii). First recognise that

so that , and that

Letting , so that we thus have

which is linear, and so (LABEL:jsr) will be satisfied if the eigenvalues of are less than some in modulus.

By the Weinstein–Aronszajn identity, the non-unit eigenvalues of coincide with those of . Therefore, consider

| (D.1) |

whence

Noting that

and

it follows that

The transpose of this matrix is the companion form for a VAR with autoregressive polynomial

the roots of which are exactly the roots of .

It follows that the eigenvalues of coincide with the inverses of the non-unit roots of , which by assumption lie strictly inside the unit circle, and are thus (in modulus) bounded above by some , as required. ∎

The following is used in 3.

Lemma D.1.

Suppose is a linear VAR satisfying (i)–3. Then for ,

D.2 Piecewise affine systems

Recall from 7 that is piecewise affine if it is a continuous function of the form

| (D.2) |

where the sets are convex and partition . We say that such an is:

-

•

piecewise linear if there exists a basis for such that each can be written as a union of cones of the form

where ranges over the subsets of , and for all and ;

-

•

threshold affine if there exists an and thresholds with , and , such that

(D.3)

We now give three auxiliary results relating to functions of these kinds, each of whose proofs follow immediately.

Lemma D.2.

Suppose is the piecewise affine function in (LABEL:piecewiseaffine). Then:

-

(i)

for every , there exists a such that

-

(ii)

if is invertible, then partition , and

Suppose further that is threshold affine function, i.e. (LABEL:thresholdaffine) holds. Then

-

(iii)

if is invertible,

where , and for

Proof.

(i). Let and , so that these are constant on each , and . Now let ; with this notation,

| (D.4) |

Define

for . Since is continuous, so too is . Because and are piecewise constant, and is a convex partition of , it follows that and have points of discontinuity, located at some with for all . Let be chosen such that for some , and set and . By the continuity of at each , we must have

| (D.5) |

for . Noting also that

| (D.6) |

we may write the final term on the r.h.s. of (LABEL:dfdecomp) as

where follows from (LABEL:xmxd), and from (LABEL:ctyatdty). We note that

and that setting and , we have

and whence

where and so . It follows from (LABEL:dfdecomp) that

Finally, noting that for each , there exists an such that , we have as required.

(ii). Since is surjective, and the sets partition ,

while for every , since is injective. The claimed form for then follows from the linearity of , for each .

(iii). Because in invertible, it follows from Theorem 4 in Gourieroux et al. (1980) that for . Since is continuous at the thresholds,

| (D.7) |

for all such that . Hence, there exists an such that

where , whence

| (D.8) |

and so by the Sherman–Morrison–Woodbury formula and Cauchy’s formula for a rank-one perturbation (see (0.7.4.1) and (0.8.5.11) in Horn and Johnson, 2013), that

| (D.9) |

and

| (D.10) |

Now by the invertibility of and the result of part (ii), it may be verified that for

By (LABEL:aTPhi), the final condition is equivalent to

where . Observe . Finally, we note that for such that ,

where holds by (LABEL:fcty) and (LABEL:Phiell), and by (LABEL:c-ell), whence

Lemma D.3.

Suppose

-

(i)

is either a

-

(a)

piecewise linear function, or

-

(b)

threshold affine function; and

-

(a)

-

(ii)

for all .

Then is a homeomorphism.

Proof.

By either Theorem 1 and 4 in Gourieroux et al. (1980), which are applicable in cases (i)(i)(a) and (i)(i)(b) respectively, is invertible. Being continuous by assumption, its restriction to any compact subset of is accordingly a homeomorphism onto its image, i.e. is continuous on , for any compact.

Let and respectively denote the open and closed balls of radius , centred at , in . We shall show below that, in each of cases (i)(i)(a) and (i)(i)(b), that

| (D.11) |

as . By construction, if is such that , then we must have : deduce by the invertibility of that . Therefore for every and , there exists an such that

for all . But as noted above, is continuous on ; therefore it is continuous at . Since was arbitrary, is continuous on the whole of , whence is a homeomorphism.

It remains to prove (LABEL:delta-diverge). Suppose (i)(i)(a) holds. Then , and is non-negative homogeneous of degree one: so that for any , . Hence

Since is continuous on , and , we must have . Hence as required. Alternately, suppose (i)(i)(b) holds. Then

Because for all , each has full rank, and so there exists a such that for all . Hence

Proof of 7.1.

By (LABEL:pi-piecewise) and the maintained assumptions,

| (D.12) |

and for ,

| (D.13) |

where and . Letting and , it follows from the preceding that

| (D.14) |

so that is piecewise affine, with and being constant on each . By the assumed continuity of , and are continuous, and hence so too is .

In view of (LABEL:gradient), we need to consider , where by assumption exists and is continuous. Recalling that

where . Since and in (LABEL:beq-decomp) are constant on on each , and , the compositions and must themselves be constant on each . Letting and for , we thus have

Letting for , it follows that

is piecewise affine on , which provide a convex partition of . Therefore by D.2, for any ,

where lies in the convex hull formed from

for . Deduce that (LABEL:gradient) holds with , and therefore

where the second equality follows by Jungers (2009, Prop. 1.8). ∎

Proof of 7.1.

We verify the conditions required for membership of .

(i). In view of (i), D.3 yields that is a homeomorphism. (Note that the subsequent arguments only require that be piecewise affine, so that the conclusions of the theorem also hold when it is directly assumed that is a homeomorphism.)