Non-concave distributionally robust stochastic control

in a discrete time finite horizon setting

Abstract.

In this article we present a general framework for non-concave distributionally robust stochastic control problems in a discrete time finite horizon setting. Our framework allows to consider a variety of different path-dependent ambiguity sets of probability measures comprising, as a natural example, the ambiguity set defined via Wasserstein-balls around path-dependent reference measures, as well as parametric classes of probability distributions. We establish a dynamic programming principle which allows to derive both optimal control and worst-case measure by solving recursively a sequence of one-step optimization problems.

As a concrete application, we study the robust hedging problem of a financial derivative under an asymmetric (and non-convex) loss function accounting for different preferences of sell- and buy side when it comes to the hedging of financial derivatives. As our entirely data-driven ambiguity set of probability measures, we consider Wasserstein-balls around the empirical measure derived from real financial data. We demonstrate that during adverse scenarios such as a financial crisis, our robust approach outperforms typical model-based hedging strategies such as the classical Delta-hedging strategy as well as the hedging strategy obtained in the non-robust setting with respect to the empirical measure and therefore overcomes the problem of model misspecification in such critical periods.

Keywords: Distributionally robust stochastic control, model uncertainty, dynamic programming, hedging, data-driven optimization

1NTU Singapore, Division of Mathematical Sciences,

21 Nanyang Link, Singapore 637371.

2National University of Singapore, Department of Mathematics,

21 Lower Kent Ridge Road, 119077.

1. Introduction

Consider an agent executing a sequence of actions based on the observation she makes in her random environment with the goal to maximize her expected payoff at a predetermined future maturity date. The agent may take decisions based on the current and past observations of the environment, as well as based on her past executions. Sequential decision making problems of this type are usually referred to as (non-Markovian) stochastic control problems and have found a wide range of applications including many in physics (e.g., [28], [31], [46], [77]), economics (e.g., [19], [26], [39], [42], [63]), and finance (e.g., [7], [9], [57], [64], [65], [79]), to name but a few.

However, modeling the underlying probability distribution of the environment in stochastic control problems is, in practice, extraordinarily difficult, as the model choice is subject to a high degree of possible model misspecification, typically referred to as Knightian uncertainty ([41]) or simply as model risk. To account for model risk, one approach known as distributionally robust stochastic control or distributionally robust optimization is to consider an ambiguity set of probability measures, instead of of singleton, which represents the candidates for the true but to the agent unknown probability measure ([12], [14], [23], [29], [33], [44], [47], [62]). The agent then chooses a sequence of actions in order to robustly optimize her expected payoff at maturity with respect to the worst-case probability measure among those in the ambiguity set.

A natural approach to define an ambiguity set of probability measures is to first consider one reference probability measure that can be regarded as the best guess or estimate of the stochastic behavior of the environment. Based on this reference probability measure one then considers all probability measures that are in a certain sense close to the reference probability measure, where proximity is typically measured via the distance of parameters in parametric approaches ([25], [35], [72]) or via some distance between probability measures in non-parametric approaches ([5], [32], [56], [73], [75]). In such a setting, the agent is more protected against model misspecification and typically performs well even if her first guess for the true law of the environment, modeled by the reference measure, is not correct, but in some sense close enough.

In this article we analyze a general setting for distributionally robust stochastic control problems in a discrete time finite horizon setting.

In our main result presented in Theorem 3.1 we prove the existence of both an optimal control and a worst-case measure. More precisely, we establish in Theorem 3.1 a dynamic programming principle which allows us to obtain both optimal control and worst-case measure by solving recursively a sequence of one step optimization problems.

Our framework to model distributional uncertainty is formulated in great generality and is not restricted to a specific type of model ambiguity but rather pursues a principled approach by imposing general conditions on ambiguity sets of probability measures, cf. Assumption 2.1. From a technical point of view, we introduce a new stability condition on the ambiguity sets of probability measures (see Assumption 2.1 (iii)) which then, together with an application of Berge’s maximum principle [8], allows to derive the main result described above.

We demonstrate in Section 4 that Assumption 2.1 is naturally fulfilled by important classes of ambiguity sets such as Wasserstein-balls around reference probability measures and by parametric classes of probability distributions. Therefore, we present a unified framework for both parametric and non-parametric (in particular data-driven) approaches to describe distributional uncertainty.

Moreover, in contrast to most literature on (distributionally robust) stochastic optimal control (see, e.g., [3], [4], [6], [10], [11], [13], [16], [24], [27], [34], [37], [43], [45], [50], [52], [53], [55], [59], [60], [76]) our objective function is not required to be concave (nor convex) and hence opens the door to analyze the distributionally robust optimization of important classes of problems that are usually difficult to solve due to the obstacle of non-concavity ([2], [17], [21], [22], [48], [49], [51], [58], [66]).

As a concrete application, we study in Section 5 the robust hedging of a financial derivative under an asymmetric (and non-convex) loss function accounting for different preferences of sell- and buy side when it comes to the hedging of financial derivatives ([15], [18], and [30]). As our entirely data-driven ambiguity set of probability measures, we consider Wasserstein-balls around the empirical measure derived from real financial data. We demonstrate that during adverse scenarios such as a financial crisis, our robust approach outperforms typical model-based hedging strategies such as the classical Delta-hedging strategy as well as the hedging strategy obtained in the non-robust setting with respect to the empirical measure and therefore overcomes the problem of model misspecification in such critical periods. To provide evidence, we test on data from the peak of the financial disruptions during the COVID-19 crisis in March which constitutes a recent example for a major adverse distribution change in financial markets.

The remainder of this paper is as follows. In Section 2 we introduce the setting of our distributionally robust stochastic control problem. Section 3 contains our main result: a dynamic programming principle guaranteeing the existence of an optimizer as well as a worst-case probability measure for our distributionally robust stochastic control problem. In Section 4 we present several possible ambiguity sets of probability measures satisfying our assumptions. Section 5 contains a description of our deep learning based numerical routine which we apply to analyze a data-driven hedging problem under asymmetric preferences. The proofs are provided in Section 6.

2. Setting

To formulate our optimization problem, we consider a fixed and finite time horizon as well as a closed set for . Then, we introduce the set

and we define a filtration by setting for as well as , where we abbreviate

For every , , and , we define the set of continuous functions which additionally possess polynomial growth at most of degree via

where denotes the set of continuous functions mapping from to , and where here and in the following always denotes the Euclidean norm on the respective Euclidean space. We define on the norm

Moreover, for each and , we denote by the set of all probability measures on with finite -th moment111We write for , i.e., for the set of all probability measures on with no moment restrictions.. We define an ambiguity set of probability measures by fixing for a set of probability measures , whereas for all we consider a correspondence

where for some fixed refers to the topology induced by convergence of measures in with respect to , i.e., we have

| (2.1) |

In particular, for , the topology coincides with the topology of weak convergence, whereas for , coincides with the topology induced by the -Wasserstein metric . Recall that for we have for two probability measures with finite -moment that their Wasserstein-distance of order is defined as

where denotes the set of all joint distributions of and , i.e., the set of all probability measures on with first marginal and second marginal , compare for more details, e.g., [70].

Then, we impose the following assumption on the correspondences .

Assumption 2.1.

Fix . Then, for every we assume the following.

-

(i)

The correspondence is compact-valued, continuous222Continuous here refers to both lower-hemicontinuous and upper-hemicontinuous, see, e.g., [1]., and non-empty. Moreover, if , we additionally assume that for all .

-

(ii)

There exists some such that for all and for all we have

(2.2) -

(iii)

There exists some such that for all , and for all there exists some satisfying

(2.3) -

(iv)

The set is non-empty, compact, and there exists such that

(2.4) for all .

We can now define a probability measure by

| (2.5) |

for . This allows us to define the ambiguity set of admissible probability measures on by

Remark 2.2.

Kuratovskis Theorem (see, e.g., [1, Theorem 18.13]) provides for each the existence of a measurable kernel such that for all .

Next, we consider at each time a compact set for some , and define the set of -valued controls by

To define our optimization problem, we consider333We define for each the set by . a function which fulfils the assumptions below.

Assumption 2.3.

Let be the integer from Assumption 2.1. Then, we assume the map

satisfies the following:

-

(i)

There exists some such that for all and for all we have

(2.6) -

(ii)

There exists some such that for all and for all we have

This allows to analyze the following distributionally robust stochastic optimal control problem which consists in solving the max-min problem

| (2.7) |

i.e., our goal is to choose a control that maximizes the expected valued of under the worst case probability measure.

3. Dynamic Programming Principle and Main Result

Let , let , and write . Then, we set

which allows for all to define recursively the following quantities:

| (3.1) | ||||

as well as

| (3.2) |

Moreover, for we define

| (3.3) | ||||

In the following theorem we formulate our main result that establishes the existence of an optimal control and a worst-case measure for our distributionally robust stochastic optimal control problem (2.7) as well as a dynamic programming principle.

Theorem 3.1.

Suppose Assumption 2.1 and Assumption 2.3 are fulfilled. Then the following holds.

-

(i)

Let . Then, there exists a measurable selector

(3.4) such that for all

(3.5) In addition, there exists such that

(3.6) Moreover, for all there exists a measurable selector

(3.7) such that for all we have

(3.8) In addition, there exists a measurable selector such that for all we have

(3.9) - (ii)

4. Modeling Ambiguity

In this section we propose two important possible choices to model ambiguity sets and show that our framework supports the use of these ambiguity sets. In Section 4.1 we discuss ambiguity sets that are modeled as Wasserstein-balls around reference measures while in Section 4.2 we present ambiguity sets incorporating parametric uncertainty.

4.1. Modeling ambiguity with the Wasserstein distance

The following result shows that the important canonical example of an ambiguity set given by a -Wasserstein-ball with radius fulfils the assumption formulated in Assumption 2.1.

Proposition 4.1.

For , , let be -Lipschitz continuous for some , i.e., for all we have and let . Moreover, consider some and some . Furthermore, assume that is convex.

4.2. Modeling ambiguity in parametric models

In this section we show that the setting from Section 2 also allows to consider parametric families of distributions as ambiguity sets with corresponding ambiguity described by time-dependent parameter sets .

To this end, for each let be a family of probability measures parameterized by , and let be the integer from Assumption 2.1. Then, we impose the following assumptions.

-

(A1)

For each let for some be non-empty, convex, and closed.

-

(A2)

For each let the map

be Lipschitz, i.e., there exists some constant such that for all .

-

(A3)

For each let the map

be Lipschitz, i.e., there exists some constant such that for all .

-

(A4)

For each and for any we define

-

(A5)

For let , and for any we define

Proposition 4.2.

With the following example we present a parametric family of distributions fulfilling the above mentioned assumptions (A1) - (A5) and therefore also, according to Proposition 4.2, Assumption 2.1.

Proposition 4.3.

Remark 4.4.

-

(i)

Note that for each with we have that converges for any in to . Indeed, the corresponding characteristic function satisfies

which by Lévy’s continuity theorem for characteristic functions implies the result for . If note that additionally

Therefore, the result now follows by [54, Theorem 2.2.1].

-

(ii)

Further, note that defined in (4.1) corresponds to the maximum likelihood estimator for the parametric family of distributions . Indeed, for any , let denote the likelihood function and

the log-likelihood function. Then, the partial derivative of the log-likelihood function w.r.t. is given by

which vanishes, since by assumption, if and only if .

5. Applications

5.1. Numerics

To solve our optimization problem (2.7) numerically, we apply the dynamic programming principle from Theorem 3.1. The numerical routine which is summarized in Algorithm 1 approximates optimal actions as defined in Theorem 3.1 by means of deep neural networks.

5.2. Data-driven hedging with asymmetric loss functions

We consider some underlying financial asset attaining values over the future time horizon as well as some financial derivative with payoff paid at maturity . We face the problem of having sold the derivative at initial time and therefore being exposed to possibly unexpected high payoff obligations . To reduce this risk, we are interested in hedging the payoff obligation by investing in the underlying asset such that our potential exposure is reduced, compare also, e.g. [36] for further financial background on hedging of financial derivatives.

We start by modeling an ambiguity set of probability measures and follow to this end the approach outlined in Section 4.1. The underlying asset returns in the time period between and are given by

where for some constant value . To construct ambiguity sets of probability measures, we consider a time series of historical realized returns

| (5.1) |

Relying on the time series from (5.1), we design ambiguity sets , . To this end, we define through a sum of Dirac-measures given by

| (5.2) |

and for by

| (5.3) |

where , with . We want to weight the distance between the past returns before and the returns before , while assigning higher probabilities to more similar sequences of returns. This means, the measure relies its probabilities for the realization of the next return on the best fitting sequence of consecutive returns that precede the prediction. To this end, we set

for and with

for all . Then, for any we define ambiguity sets of probability measures via

| (5.4) | ||||

where denotes a Wasserstein-ball of order with radius around some probability measure , as defined in Proposition 4.1.

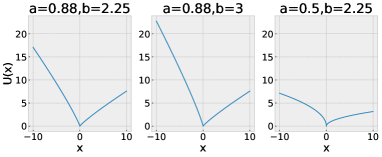

As our assumptions on the objective function formulated in Assumption 2.3 do not require the objective function to be concave, we are able to consider non-concave objective function as they appear in behavorial economics and, in particular, in prospect theory ([38]). To this end, we consider a loss function of the form

| (5.5) |

which assigns the value to positive inputes and to negative inputs , see also [67] or [74], and compare the illustration in Figure 1 (a). Considering an asymmetric loss function as in (5.5) accounts for the empirical fact that agents exhibit distinct behaviors in response to gains and losses, namely they are much more sensitive with respect to losses. Experimental studies reported in [68] provide estimates of , .

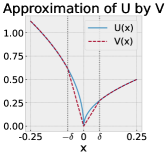

(b) The plot shows an approximation of with , by the function described in (5.6) with

Note that is not Lipschitz-continuous at , hence to meet the requirements from Assumption 2.3, we modify the function slightly by defining for some fixed small

| (5.6) |

i.e., we simply interpolate linearly between , , and , compare also Figure 1 (b). Note that, by construction, is Lipschitz-continuous. To define our optimization problem, we consider some financial derivative with payoff function . The agent’s goal is to find a hedging strategy, i.e., a combination of an initial cash position and time-dependent positions invested in the underlying asset minimizing the hedging error between the time- value of the self-financing hedging strategy given by

and the payoff of . To this end, we identify the financial positions of the agent with her actions and define for some and the sets of actions by

and further introduce the objective function

| (5.7) |

where we abbreviate .

Solving with as defined in (5.7) corresponds to minimizing the distributionally robust expected hedging error induced by between the outcome of a self-financing hedging strategy and some financial derivative. Considering the situation of a financial institution which has sold the derivative , the asymmetry of accounts for the fact that a hedging-strategy that leads to higher payoffs than the derivative is considered a better outcome than a hedging-strategy that leads to smaller payoffs than the derivative payoff and therefore to unexpected losses. We refer to [15], [18], and [30] for related literature on asymmetric hedging, but without model uncertainty.

Proposition 5.1.

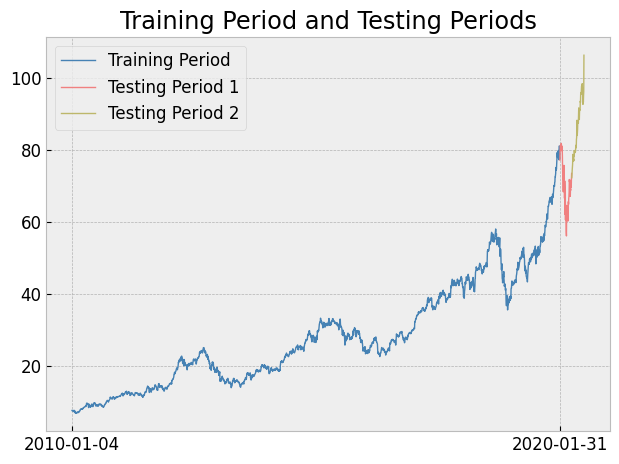

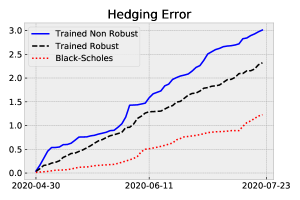

To test our approach empirically, we consider a time-series of daily returns of the stock of Apple between beginning of January and beginning of Feburary to construct data-driven ambiguity sets of probability measures, as described in (5.3) and (5.4), which we use to train our agent. To evaluate the trained strategy, we consider two test periods ranging from beginning of Feburary until end of May , and between beginning of May and end of August , respectively, compare also Figure 2.

We set and we train both a non-robust () and a robust hedging strategy with respect to according to444To apply the numerical method from Section 5.1, we use the following hyperparameters: Number of measures ; Monte-Carlo sample size ; number of iterations for : ; number of iterations for : . The neural networks that approximate and constitute of layers with neurons each possessing ReLu activation functions in each layer, except for the output layers. The learning rate used to optimize the networks and when applying the Adam optimizer ([40]) is . Further details of the implementation can be found under https://github.com/juliansester/Robust-Hedging-Finite-Horizon. Algorithm 1 for an at-the-money call option with payoff function , where we normalize to .

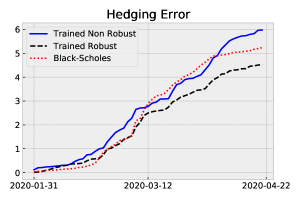

To evaluate the performance of our strategy we evaluate on testing period 1 and testing period 2 and show the results in Figure 3 and Tables 1, 2.

The results show that during test period 1 (the advent of the Covid-19 pandemic), the robust hedging strategy outperforms both the non-robust strategy and the classical Black–Scholes delta hedging strategy while in test period 2 the Black–Scholes delta hedging strategy555The Black–Scholes delta hedging strategy for a call option with strike and maturity , invests at time , the amount in the underlying asset with value , where denotes the cdf of a standard normal distribution and where . Note that we set the interest rate to be . To apply the strategy, we estimate the annual volatility from historical data. In the case of Apple we use . is the best performing strategy. This accounts for the fact that in turbulent times, where the underlying empirical distributions of the asset returns might change dramatically compared to the training period, it turns out to be favourable to take model uncertainty into account as both the non-robust model and the Black–Scholes model rely on misspecified probability distributions. However, in good weather periods (as in test period 2) it is hard to beat a strategy such as the Black–Scholes delta hedging strategy which, due to the assumption of normal asset returns, works reasonably well if no extreme events occur.

| Non-Robust | Robust | Black–Scholes | |

|---|---|---|---|

| No. of days | 57 | 57 | 57 |

| mean | 0.104865 | 0.079407 | 0.091882 |

| std | 0.092339 | 0.076183 | 0.102653 |

| min | 0.000900 | 0.004800 | 0.000000 |

| 25% | 0.031000 | 0.024500 | 0.024000 |

| 50% | 0.079800 | 0.056700 | 0.061400 |

| 75% | 0.154100 | 0.101000 | 0.130600 |

| max | 0.363800 | 0.371400 | 0.600100 |

| Non-Robust | Robust | Black–Scholes | |

|---|---|---|---|

| No. of days | 59 | 59 | 59 |

| mean | 0.051024 | 0.039310 | 0.020795 |

| std | 0.048292 | 0.025909 | 0.021392 |

| min | 0.001400 | 0.001700 | 0.000000 |

| 25% | 0.018350 | 0.019050 | 0.006700 |

| 50% | 0.036400 | 0.037400 | 0.013000 |

| 75% | 0.069700 | 0.055700 | 0.024550 |

| max | 0.248600 | 0.119700 | 0.100300 |

6. Proofs

6.1. Proofs of Section 3

Before reporting the proof of Theorem 3.1, we establish the following lemma.

Lemma 6.1.

Let and let be defined in (3.2). Assume that there exists some and such that for all and for all we have

| (6.1) |

as well as

| (6.2) |

Then, the following holds.

-

(i)

There exists a measurable map satisfying for all that and

-

(ii)

There exists a measurable map satisfying for all that

-

(iii)

There exists some , and some such that for all and for all the following inequalities hold

(6.3) (6.4)

Proof of Lemma 6.1.

Let .

We first show the continuity of . To that end, we consider the map

We aim at applying Berge’s maximum theorem (see, e.g., [8] or [1, Theorem 18.19]) to , and therefore first want to show that is continuous.

We consider a sequence with as for some , , and . Moreover, we have

Note that with in we obtain that as is by assumption continuous and of polynomial growth of order . Further, we use (6.2) and compute

We have thus shown that is continuous. Therefore, by using Assumption 2.1 (i), we may now apply Berge’s maximum theorem which yields that

| (6.5) |

is continuous. Note that the above application of Berge’s maximum theorem also implies the existence of a minimizer of (6.5). With the measurable maximum theorem (see, e.g., [1, Theorem 18.19]) we therefore obtain a measurable map satisfying for all that

showing (i).

Since is compact, we obtain by a repeated application of Berge’s maximum theorem also that

| (6.6) |

is continuous and that the maximizer exists. By the measurable maximum theorem we deduce therefore the existence of a measurable map satisfying for all that

which shows (ii).

It remains to prove (iii). We assume that (6.1) holds and show the polynomial growth condition stated in (6.3). To this end, we consider elements , , , , we set and obtain by (2.2) and (6.1) that

which indeed proves (6.3). Next, we assume that (6.2) holds and aim at showing (6.4). We first compute

| (6.7) | ||||

where with denoting the minimizer from (ii), where with being the maximizer from (i), and where is chosen such that inequality (2.2) in Assumption 2.1 (iii) is fulfilled w.r.t. . Then, we denote by the set of probability measures on with respective marginal distributions and . We use the representation from (6.7), apply the assumption from (6.2), and have

where in the last step we applied the definition of the -Wasserstein distance. We now use Assumption 2.1 (iii), set and obtain

By interchanging the roles of and we obtain

This shows (6.4). ∎

As a consequence of Lemma 6.1 we obtain the following corollary for the case .

Corollary 6.2.

Let be defined in (3.2). Assume that there exists some and such that for all and for all we have

| (6.8) |

as well as

| (6.9) |

Then, the following holds.

-

(i)

There exists a measurable map satisfying for all that and

-

(ii)

There exists some such that

Proof.

This follows by the same arguments as the proof of Lemma 6.1. ∎

Proof of Theorem 3.1.

- (i)

-

(ii)

Let . In the following, for we denote for any by the first coordinates of .

Note that by definition of the kernel we have for all that

(6.10) Then, by definition of , and of , we obtain for all that

Further, by definition of , we have for all that

(6.11) Repeatedly applied, the above inequality (6.11) yields

(6.12) and since was chosen arbitrarily we also get, by using , that

(6.13) By considering the measure

and by using (6.10), we obtain equality in (6.11) and (6.12). This means, together with (6.13), that we have

(6.14) Now let be an arbitrary control. Then, we have for all that

(6.15) Let be arbitrary and define

Then (6.15) implies

(6.16) Hence, as was arbitrary, we obtain from (6.16) that

(6.17) By a repeated application of the latter inequality (6.17) one sees that

(6.18) Since was also chosen arbitrarily we obtain that

(6.19) which implies together with (6.14) that

∎

6.2. Proofs of Section 4

Before reporting the proofs of Proposition 4.1 and 4.2, we establish four auxiliary results. To this end, in the following we use the notation to describe the set of all joint distributions of probability measures on some space .

Lemma 6.3.

Let and let be a separable Banach space. Let converging in to some . Then is relatively compact w.r.t. .

Proof.

For the case , this result follows from, e.g., the proof of [20, Lemma 5.2]. Hence, w.l.o.g. we can assume . By [20, Proof of Lemma 5.2] we further know that is weakly relatively compact. Let be the norm on defined by

Then, we have for all that

as well as . Hence, we have for all

| (6.20) | ||||

Now, the convergence in implies with [54, Theorem 2.2.1 (3)] both that

and that

Therefore, the integral in (6.20) vanishes as , and the relative compactness of in follows directly by [54, Proposition 2.2.3]. ∎

Lemma 6.4.

Let be a separable Banach space, and let and with . Moreover, let be non-negative. Then

is lower semicontinuous w.r.t. .

Proof.

If , then the map is continuous by definition of . Hence, w.l.o.g. we can assume . We define for each the function

One sees directly that and that for all . Moreover, we have monotonically as . Now, let and such that in . Then, we have by the monotone convergence theorem, since , and since that

∎

Lemma 6.5.

Let be a separable Banach space, and let and with . Then, the map

is lower semicontinuous in .

Proof.

The case follows from [20, Corollary 5.3]. Hence, w.l.o.g. we may assume . Let , and let be a sequence with in . To prove the lower semicontinuity we need to show that

| (6.21) |

Let be a subsequence such that

| (6.22) |

For all let denote the optimal coupling w.r.t. , i.e.,

| (6.23) |

Since , we have by Lemma 6.3 that is relatively compact w.r.t. .

Let be a limit point of some subsequence w.r.t. . Let denote the projection on the -th component for . Since for all and since in for as , we have by the continuous mapping theorem that

where the limits are w.r.t. weak convergence. This means that . Hence, it follows

| (6.24) | ||||

| (6.25) | ||||

| (6.26) |

Indeed, (6.24) follows by Lemma 6.4, (6.25) follows with (6.23), and (6.26) follows from (6.22). ∎

Lemma 6.6.

Let and such that . Moreover, let be a separable Banach space. Then, for any and , the set

is compact w.r.t. .

Proof.

Proof of Proposition 4.1.

Let be fixed. We verify that the conditions (i)-(iv) of Assumption 2.1 are fulfilled.

-

(i)

The ambiguity set contains, by definition, for all the reference measure and is hence non-empty. Moreover, by, e.g., [78, Lemma 1] we have for all as .

The compactness of w.r.t. follows from Lemma 6.6 as .

To show the upper hemicontinuity we mainly follow the lines of the proof of [49, Proposition 3.1]. Therefore, the goal is to apply the characterization of upper hemicontinuity provided in Lemma [1, Theorem 17.20]. Let such that for . Further, consider a sequence such that for all , i.e., we have , where denotes the graph of .Let with . Note that, since is, by assumption, -Lipschitz continuous we have

Hence, there exists a subsequence such that

(6.28) This implies for each , , that

Hence, for all . According to Lemma 6.6, is compact in , implying the existence of a subsequence such that as for some . In particular, since by assumption possesses finite -th moments, has also finite -th moments, see [78, Lemma 1]. It remains to prove that . To that end, define for each

(6.29) Then, for each we have

(6.30) Therefore, by (6.28) and (6.30) we have for each that

(6.31) Furthermore, we have by (6.29) that

(6.32) Since is lower semicontinuous in , see Lemma 6.5, we obtain from (6.31) and (6.32) that

and hence . The assertion that is upper hemicontinuous follows now with the characterization of upper hemicontinuity provided in [1, Theorem 17.20].

To show the lower hemicontinuity we use the same arguments that were used to prove [49, Proposition 3.1]. To this end, we first define the set-valued map

and conclude the lower hemicontinuity of with [1, Theorem 17.21]. To this end, we consider a sequence such that for , and we consider some . Note that since is defined as an open ball with respect to , there exists some such that . We define for the measure

Then, we claim that for all . Indeed, if this follows by definition of , whereas if , then , and hence by the triangle inequality

By the -Lipschitz continuity of , we have that

Thus, there exists some such that we have for all and thus, in particular w.r.t. for , which concludes the lower hemicontinuity of with [1, Theorem 17.21]. Next, we claim that the -closure of , denoted by , coincides with . Indeed, the inclusion follows, since is closed in and hence also in . To show the reverse inclusion let . Then, there exists a sequence with as . Hence, by using the lower semicontinuity of with respect to (see Lemma 6.5), we obtain

Hence, and [1, Lemma 17.22] implies that the set-valued map is lower hemicontinuous.

-

(ii)

Define the constant

For all and let be the optimal coupling of and w.r.t. the -Wasserstein distance . Then, by Minkowski’s inequality we have

(6.33) Now for any arbitrary let be the optimal coupling of and w.r.t. the -Wasserstein distance . Then, by (6.33), Minkowski’s inequality, the Lipschitz continuity of , and that we have

(6.34) Since was arbitrary, we conclude that

This implies that

-

(iii)

Let and let . Without loss of generality assume .

In the following, we denote , as well as , , , , i.e., we simply consider copies of . Then, we consider a probability measure which fulfils the following marginal constraints.

-

(1)

The marginal of on is .

-

(2)

The marginal of on is .

-

(3)

The marginal of on is .

-

(4)

The marginal of on minimizes the -Wasserstein distance between and .

-

(5)

The marginal of on minimizes the -Wasserstein distance between and .

The existence of such a probability measure follows by the Gluing Lemma, see, e.g. [71, Lemma 7.6.]. Then, define the map

(6.35) Note that by the convexity of we have that the image of is contained in . We set

Let be defined as the marginal of on .

For any we claim the following inequalities hold

(6.36) (6.37) In the case the inequalities (6.36) and (6.37) are trivial, so without loss of generality () does not hold. For (6.36) note that, by definition of , we have

Similarly, to see (6.37), note that

Next, we claim . Note that, by construction, the second and fourth marginals of are and , respectively. Hence, by (6.37), by the definition of , and as we have indeed that

Moreover, we claim that

(6.38) Indeed, by construction, the third and fourth marginals of are and , respectively. Hence, by (6.36) and by the definition of we have

Finally, since , , and by the assumption that , we obtain with (6.38) that

(6.39) This shows with Hölder’s inequality that Assumption 2.1 (iii) holds.

-

(1)

-

(iv)

The ambiguity set contains, by definition, the reference measure and is hence non-empty. Moreover, by, e.g., [78, Lemma 1] we have since .

The compactness of w.r.t. follows from Lemma 6.6. Let and denote by the optimal coupling between and w.r.t. the -Wasserstein distance . Then, by Minkowski’s inequality we have(6.40)

∎

Proof of Proposition 4.2.

We verify all four properties of Assumption 2.1. To this end, let be arbitrary.

To see that Assumption 2.1 (iv) holds, note that we can w.l.o.g. assume that , as for , Assumption 2.1 (iv) holds trivially.

For the case let . Then, by definition of in (A5), there exists some with such that . Next, let be the optimal coupling of and w.r.t. the -Wasserstein distance . Then, by using Minkowski’s inequality and (A2) we obtain that

Moreover, is compact as is closed. The map

is continuous by (A2), and is an image of a compact set under a continuous map and thus compact.

The non-emptiness of follows as is non-empty by (A1). Hence, we have shown that Assumption 2.1 (iv) is satisfied.

Next, we show that Assumption 2.1 (i) is fulfilled. To this end, let be fixed. The non-emptiness of follows by definition and by (A1). We define the correspondence

Since by assumption (A3) the map is continuous, by the same argument as in the proof of [49, Proposition 4.2] one shows that is a non-empty, compact-valued continuous correspondence.

Then, as for any we have , the result follows directly by [49, Proposition 3.2]. Hence, Assumption 2.1 (i) is satisfied.

To see Assumption 2.1 (ii) we again assume w.l.o.g. . In this case, let and . By definition of in (A4), there exists some such that and such that . Let denote an optimal coupling of and with respect to the Wasserstein- distance . Then, by Minkowski’s inequality we have

| (6.41) | ||||

By Assumption (A2), as , we have

| (6.42) |

Next, for any arbitrary , let be an optimal coupling of and with respect to . Then, due to Minkowski’s inequality, (A2), and (A3), we have

Since was arbitrarily chosen, we obtain that

| (6.43) | ||||

Therefore, we see that (6.41), (6.42), and (LABEL:eq_proof_param_3) together imply that

for

which shows Assumption 2.1 (ii).

It remains to show Assumption 2.1 (iii). To that end, let and let . Then, by definition of in (A4), there exists some with such that . For the ease of notation we set , , . Then, we define

Note that as is convex. By construction, one can check that and . Hence, it follows that and by (A2) and (A3) that

showing that Assumption 2.1 (iii) is fulfilled. ∎

Proof of Proposition 4.3.

We verify assumptions (A1) – (A5).

-

(A1)

By assumption is non-empty, convex, and closed.

-

(A2)

Let and let with . We distinguish two cases.

Case 1:

Then, we have the representation(6.44) where denotes the quantile function of for , see, e.g. [61, Equation (3.5)] or [69]. For any note that the cumulative distribution function is given by . Hence, the quantile function computes as

We set

(6.45) By (6.44), we obtain

Case 2: or

Without loss of generality and . Then, we haveTherefore, by (6.44) and by the definition of in (6.45), we obtain

-

(A3)

Let , and let . Then, we have

-

(A4)

Follows by definition of .

-

(A5)

Follows by definition of .

∎

6.3. Proofs of Section 5

Proof of Proposition 5.1.

To verify Assumption 2.1, we aim to apply Proposition 4.1 with . This means we need to show that for all there exists some such that we have . First, for any function , we define the quantity

Note that is Lipschitz-continuous if and only if . Next, note that by construction is Lipschitz-continuous for all with Lipschitz constant since the partial derivatives of exist and are bounded on . We use this observation to define . Then, we apply the Kantorovich–Rubinstein duality (see, e.g. [70, Remark 6.5]) to compute

Hence, according to Proposition 4.1, Assumption 2.1 is fulfilled. Next, to verify Assumption 2.3, note first that is compact and . Hence, Assumption 2.3 (ii) follows directly as defined in (5.7) is continuous. Therefore, we only need to verify Assumption 2.3 (i). To this end, we recall that , defined in (5.6), is Lipschitz-continuous and that the payoff of the derivative is Lipschitz-continuous. Moreover,

| (6.46) |

is continuously differentiable, and is compact, hence (6.46) is Lipschitz continuous. Therefore defined in (5.7) being a composition of Lipschitz continuous functions is Lipschitz continuous. ∎

Acknowledgments

Financial support by the Nanyang Assistant Professorship Grant (NAP Grant) Machine Learning based Algorithms in Finance and Insurance is gratefully acknowledged.

References

- [1] Charalambos D. Aliprantis and Kim C. Border. Infinite dimensional analysis. Springer, Berlin, third edition, 2006. A hitchhiker’s guide.

- [2] Olena Bahchedjioglou and Georgiy Shevchenko. Optimal investments for the standard maximization problem with non-concave utility function in complete market model. Mathematical Methods of Operations Research, 95(1):163–181, 2022.

- [3] Daniel Bartl. Exponential utility maximization under model uncertainty for unbounded endowments. The Annals of Applied Probability, 29(1):577–612, 2019.

- [4] Daniel Bartl, Patrick Cheridito, and Michael Kupper. Robust expected utility maximization with medial limits. Journal of Mathematical Analysis and Applications, 471(1-2):752–775, 2019.

- [5] Erhan Bayraktar and Tao Chen. Nonparametric adaptive robust control under model uncertainty. SIAM Journal on Control and Optimization, 61(5):2737–2760, 2023.

- [6] Erhan Bayraktar and Tao Chen. Data-driven non-parametric robust control under dependence uncertainty. In Peter Carr Gedenkschrift: Research Advances in Mathematical Finance, pages 141–178. World Scientific, 2024.

- [7] Fred E Benth, Kenneth H Karlsen, and Kristin Reikvam. On the existence of optimal controls for a singular stochastic control problem in finance. In Mathematical Finance: Workshop of the Mathematical Finance Research Project, Konstanz, Germany, October 5–7, 2000, pages 79–88. Springer, 2001.

- [8] Claude Berge. Espaces topologiques: Fonctions multivoques. Collection Universitaire de Mathématiques, Vol. III. Dunod, Paris, 1959.

- [9] Dimitri Bertsekas and Steven E Shreve. Stochastic optimal control: the discrete-time case, volume 5. Athena Scientific, 1996.

- [10] Romain Blanchard. Stochastic control applied in the theory of decision in a discrete time non-dominated multiple-priors framework. PhD thesis, Université de Reims Champagne-Ardenne, 2017.

- [11] Romain Blanchard and Laurence Carassus. Multiple-priors optimal investment in discrete time for unbounded utility function. The Annals of Applied Probability, 28(3):1856–1892, 2018.

- [12] Jose Blanchet and Karthyek Murthy. Quantifying distributional model risk via optimal transport. Mathematics of Operations Research, 44(2):565–600, 2019.

- [13] Giuliana Bordigoni, Anis Matoussi, and Martin Schweizer. A stochastic control approach to a robust utility maximization problem. In Stochastic Analysis and Applications: The Abel Symposium 2005, pages 125–151. Springer, 2007.

- [14] Bruno Bouchard and Marcel Nutz. Arbitrage and duality in nondominated discrete-time models. The Annals of Applied Probability, 25(2):823 – 859, 2015.

- [15] Udo Broll, Martín Egozcue, Wing-Keung Wong, and Ričardas Zitikis. Prospect theory, indifference curves, and hedging risks. Applied Mathematics Research Express, 2010(2):142–153, 2010.

- [16] Laurence Carassus and Massinissa Ferhoune. Discrete time optimal investment under model uncertainty. arXiv preprint arXiv:2307.11919, 2023.

- [17] Laurence Carassus and Massinissa Ferhoune. Nonconcave robust utility maximization under projective determinacy. arXiv preprint arXiv:2403.11824, 2024.

- [18] Alexandre Carbonneau and Frédéric Godin. Deep equal risk pricing of financial derivatives with non-translation invariant risk measures. Risks, 11(8):140, 2023.

- [19] Gregory C Chow. Optimal stochastic control of linear economic systems. Journal of Money, Credit and Banking, 2(3):291–302, 1970.

- [20] Philippe Clément and Wolfgang Desch. Wasserstein metric and subordination. Studia Mathematica, 1(189):35–52, 2008.

- [21] Min Dai, Steven Kou, Shuaijie Qian, and Xiangwei Wan. Non-concave utility maximization without the concavification principle. Available at SSRN 3422276, 2019.

- [22] Min Dai, Steven Kou, Shuaijie Qian, and Xiangwei Wan. Nonconcave utility maximization with portfolio bounds. Management Science, 68(11):8368–8385, 2022.

- [23] Erick Delage and Yinyu Ye. Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations research, 58(3):595–612, 2010.

- [24] Laurent Denis and Magali Kervarec. Optimal investment under model uncertainty in nondominated models. SIAM Journal on control and optimization, 51(3):1803–1822, 2013.

- [25] David Easley and Nicholas M Kiefer. Controlling a stochastic process with unknown parameters. Econometrica: Journal of the Econometric Society, pages 1045–1064, 1988.

- [26] Wendell H Fleming and Tao Pang. An application of stochastic control theory to financial economics. SIAM journal on control and optimization, 43(2):502–531, 2004.

- [27] Jean-Pierre Fouque, Chi Seng Pun, and Hoi Ying Wong. Portfolio optimization with ambiguous correlation and stochastic volatilities. SIAM Journal on Control and Optimization, 54(5):2309–2338, 2016.

- [28] Jan A Freund and Thorsten Pöschel. Stochastic processes in physics, chemistry, and biology, volume 557. Springer Science & Business Media, 2000.

- [29] Itzhak Gilboa and David Schmeidler. Maxmin expected utility with non-unique prior. Journal of mathematical economics, 18(2):141–153, 1989.

- [30] Emmanuel Gobet, Isaque Pimentel, and Xavier Warin. Option valuation and hedging using an asymmetric risk function: asymptotic optimality through fully nonlinear partial differential equations. Finance and Stochastics, 24:633–675, 2020.

- [31] Francesco Guerra and Laura M Morato. Quantization of dynamical systems and stochastic control theory. Physical review D, 27(8):1774, 1983.

- [32] Astghik Hakobyan and Insoon Yang. Wasserstein distributionally robust motion control for collision avoidance using conditional value-at-risk. IEEE Transactions on Robotics, 38(2):939–957, 2021.

- [33] Lars Peter Hansen and Thomas J Sargent. Robust control and model uncertainty. American Economic Review, 91(2):60–66, 2001.

- [34] Daniel Hernández-Hernández and Alexander Schied. Robust utility maximization in a stochastic factor model. Statistics & Risk Modeling, 24(1):109–125, 2006.

- [35] Ulrich Horst, Xiaonyu Xia, and Chao Zhou. Portfolio liquidation under factor uncertainty. The Annals of Applied Probability, 32(1):80–123, 2022.

- [36] John Hull. Options, futures, and other derivative securities, volume 7. Prentice Hall Englewood Cliffs, NJ, 1993.

- [37] Amine Ismail and Huyên Pham. Robust markowitz mean-variance portfolio selection under ambiguous covariance matrix. Mathematical Finance, 29(1):174–207, 2019.

- [38] Daniel Kahneman and Amos Tversky. Prospect theory: An analysis of decision under risk. Econometrica, 47(2):263–292, 1979.

- [39] David A Kendrick. Stochastic control for economic models: past, present and the paths ahead. Journal of economic dynamics and control, 29(1-2):3–30, 2005.

- [40] Diederik P Kingma and Jimmy Ba. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980, 2014.

- [41] Frank Hyneman Knight. Risk, uncertainty and profit, volume 31. Houghton Mifflin, 1921.

- [42] Daniel Leonard and Ngo Van Long. Optimal control theory and static optimization in economics. Cambridge University Press, 1992.

- [43] Qian Lin and Frank Riedel. Optimal consumption and portfolio choice with ambiguous interest rates and volatility. Economic Theory, 71(3):1189–1202, 2021.

- [44] Fabio Maccheroni, Massimo Marinacci, and Aldo Rustichini. Ambiguity aversion, robustness, and the variational representation of preferences. Econometrica, 74(6):1447–1498, 2006.

- [45] Anis Matoussi, Dylan Possamaï, and Chao Zhou. Robust utility maximization in nondominated models with 2bsde: the uncertain volatility model. Mathematical Finance, 25(2):258–287, 2015.

- [46] Grigori N Milstein and Michael V Tretyakov. Stochastic numerics for mathematical physics, volume 39. Springer, 2004.

- [47] Peyman Mohajerin Esfahani and Daniel Kuhn. Data-driven distributionally robust optimization using the wasserstein metric: performance guarantees and tractable reformulations. Mathematical Programming, 171(1-2):115–166, 2018.

- [48] Ariel Neufeld, Matthew Ng Cheng En, and Ying Zhang. Robust SGLD algorithm for solving non-convex distributionally robust optimisation problems. arXiv preprint arXiv:2403.09532, 2024.

- [49] Ariel Neufeld, Julian Sester, and Mario Šikić. Markov decision processes under model uncertainty. Mathematical Finance, 33(3):618–665, 2023.

- [50] Ariel Neufeld and Mario Šikić. Robust utility maximization in discrete-time markets with friction. SIAM Journal on Control and Optimization, 56(3):1912–1937, 2018.

- [51] Ariel Neufeld and Mario Šikić. Nonconcave robust optimization with discrete strategies under Knightian uncertainty. Mathematical Methods of Operations Research, 90(2):229–253, 2019.

- [52] Marcel Nutz. Utility maximization under model uncertainty in discrete time. Mathematical Finance, 26(2):252–268, 2016.

- [53] Jan Obłój and Johannes Wiesel. Distributionally robust portfolio maximization and marginal utility pricing in one period financial markets. Mathematical Finance, 31(4):1454–1493, 2021.

- [54] Victor M Panaretos and Yoav Zemel. An invitation to statistics in Wasserstein space. Springer Nature, 2020.

- [55] Kyunghyun Park and Hoi Ying Wong. Robust retirement with return ambiguity: Optimal-stopping time in dual space. SIAM Journal on Control and Optimization, 61(3):1009–1037, 2023.

- [56] Ian R Petersen, Matthew R James, and Paul Dupuis. Minimax optimal control of stochastic uncertain systems with relative entropy constraints. IEEE Transactions on Automatic Control, 45(3):398–412, 2000.

- [57] Huyên Pham. Continuous-time stochastic control and optimization with financial applications, volume 61. Springer Science & Business Media, 2009.

- [58] Traian A Pirvu and Klaas Schulze. Multi-stock portfolio optimization under prospect theory. Mathematics and Financial Economics, 6:337–362, 2012.

- [59] Miklós Rásonyi and Andrea Meireles-Rodrigues. On utility maximization under model uncertainty in discrete-time markets. Mathematical Finance, 31(1):149–175, 2021.

- [60] Napat Rujeerapaiboon, Daniel Kuhn, and Wolfram Wiesemann. Robust growth-optimal portfolios. Management Science, 62(7):2090–2109, 2016.

- [61] Ludger Rüschendorf. Monge-Kantorovich transportation problem and optimal couplings. Jahresbericht der DMV, 3:113–137, 2007.

- [62] Mete Soner, Nizar Touzi, and Jianfeng Zhang. Quasi-sure Stochastic Analysis through Aggregation. Electronic Journal of Probability, 16(none):1844 – 1879, 2011.

- [63] Nancy L Stokey. The Economics of Inaction: Stochastic Control models with fixed costs. Princeton University Press, 2008.

- [64] Nizar Touzi. Stochastic control and application to finance. Scuola Normale Superiore, Pisa. Special Research Semester on Financial Mathematics, 2002.

- [65] Nizar Touzi. Optimal stochastic control, stochastic target problems, and backward SDE, volume 29. Springer Science & Business Media, 2012.

- [66] Alex SL Tse and Harry Zheng. Speculative trading, prospect theory and transaction costs. Finance and Stochastics, 27(1):49–96, 2023.

- [67] Amos Tversky and Daniel Kahneman. Rational choice and the framing of decisions. In Multiple criteria decision making and risk analysis using microcomputers, pages 81–126. Springer, 1989.

- [68] Amos Tversky and Daniel Kahneman. Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and uncertainty, 5:297–323, 1992.

- [69] SS Vallender. Calculation of the Wasserstein distance between probability distributions on the line. Theory of Probability & Its Applications, 18(4):784–786, 1974.

- [70] Cédric Villani. Optimal transport, volume 338 of Grundlehren der mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, 2009. Old and new.

- [71] Cédric Villani. Topics in optimal transportation, volume 58. American Mathematical Soc., 2021.

- [72] Michael P Vitus, Zhengyuan Zhou, and Claire J Tomlin. Stochastic control with uncertain parameters via chance constrained control. IEEE Transactions on Automatic Control, 61(10):2892–2905, 2015.

- [73] Hong Wang. Minimum entropy control of non-gaussian dynamic stochastic systems. IEEE Transactions on Automatic Control, 47(2):398–403, 2002.

- [74] Elke U Weber and Eric J Johnson. Decisions under uncertainty: Psychological, economic, and neuroeconomic explanations of risk preference. In Neuroeconomics, pages 127–144. Elsevier, 2009.

- [75] Insoon Yang. Wasserstein distributionally robust stochastic control: A data-driven approach. IEEE Transactions on Automatic Control, 66(8):3863–3870, 2020.

- [76] Zhou Yang, Jing Zhang, and Chao Zhou. Robust control problems of bsdes coupled with value functions. SIAM Journal on Financial Mathematics, 14(3):721–750, 2023.

- [77] Kunio Yasue. Quantum mechanics and stochastic control theory. Journal of Mathematical Physics, 22(5):1010–1020, 1981.

- [78] Man-Chung Yue, Daniel Kuhn, and Wolfram Wiesemann. On linear optimization over Wasserstein balls. Mathematical Programming, 195(1-2):1107–1122, 2022.

- [79] Thaleia Zariphopoulou. Stochastic control methods in asset pricing. In Handbook of stochastic analysis and applications, pages 705–770. CRC Press, 2001.