Estimation and Inference in Ultrahigh Dimensional Partially Linear Single-Index Models††thanks: All authors make equally contribution to this work and are listed in the alphabetic order.

Abstract

This paper is concerned with estimation and inference for ultrahigh dimensional partially linear single-index models. The presence of high dimensional nuisance parameter and nuisance unknown function makes the estimation and inference problem very challenging. In this paper, we first propose a profile partial penalized least squares estimator and establish the sparsity, consistency and asymptotic representation of the proposed estimator in ultrahigh dimensional setting. We then propose an -type test statistic for parameters of primary interest and show that the limiting null distribution of the test statistic is distribution, and the test statistic can detect local alternatives, which converge to the null hypothesis at the root- rate. We further propose a new test for the specification testing problem of the nonparametric function. The test statistic is shown to be asymptotically normal. Simulation studies are conducted to examine the finite sample performance of the proposed estimators and tests. A real data example is used to illustrate the proposed procedures.

Keywords: Local alternative; penalized least squares; semiparametric regression modeling; sparsity.

1 Introduction

Thanks to advances in computing technologies, high dimensional modeling has been increasingly common in economics and finance, including microeconomics, macroeconomics, marketing, and portfolio selection as well as other areas such as medical studies and health studies. See Fan et al. (2020) for an overview. In high dimensional analysis, statistical inference has attracted considerable attention. Recently there are many developments for testing low dimensional parametric components in high dimensional models, see for instance Barber and Candès (2015), Lan et al. (2016), Ning and Liu (2017), Candès et al. (2018) Shi et al. (2019), Liu et al. (2021) and references therein. However, these works focused on high dimensional parametric modeling. It is unknown whether their works apply to more general settings, e.g. semiparametric setting.

Compared with parametric regression modeling, semiparametric models relax restrictive assumptions on parametric models and are flexible enough to capture the relationship between the response and the covariates. The partially linear single-index model (PLSIM) is one of the popular semiparametric regression models and is widely used in economics. See, for example, Example 1.1.6 in Härdle et al. (2012) for an interesting application of PLSIM.

Let be the response, and be the - and -dimensional covariates, respectively. In this paper, is fixed while is allowed to be exponential order of the sample size. Thus we consider the ultrahigh dimensional setting. The PLSIM is

| (1.1) |

where and are unknown parameters, is an unknown smooth function, , and . For model identification, assume that and its first element is positive, where is the norm. Model (1.1) is quite general. When , it reduces to the partially linear model (Speckman, 1988) while it turns to be the single-index model (Ichimura, 1993) when .

To estimate the parameters in model (1.1), Carroll et al. (1997) proposed a backfitting algorithm, which may lead to unstable estimators. To deal with this issue, Yu and Ruppert (2002) introduced a penalized spline estimation procedure. Xia and Härdle (2006) developed an estimator based on the minimum average variance estimation. Liang et al. (2010) proposed a profile least squares estimation procedure. Under a mild assumption that the covariate has a dimension reduction structure on the covariate , Wang et al. (2010) proposed a two-stage procedure. Zhu and Xue (2006) conducted confidence regions for the parameters in model (1.1) based on bias-corrected empirical likelihood. However, these works only deal with the case when dimension of is small and fixed.

When the dimension of is large compared with the sample size , it is challenging to estimate the parameters. To handle this issue, it is natural to assume that the high dimensional nuisance parameter is sparse. In other words, only a small number of elements of are nonzero. Under this sparsity assumption, variable selection procedures are developed by many authors. See for instance, Liang et al. (2010), Zhang et al. (2013), Lai et al. (2014), and Zhang et al. (2017). However, these studies all focus on the situation that and are both fixed. As an exception, when the dimension , Zhang et al. (2012) considered the estimation and variable selection problem for PLSIM. In this paper, we adopt penalty-based variable selection methods such as Tibshirani (1996) and Fan and Li (2001) to ultrahigh dimensional PLSIM. A notable feature of our approach is that we only penalize the nuisance parameter , and do not penalize the parameter of interest .

In addition to estimation and variable selection, we are also interested in making statistical inference on the parametric component and the nonparametric function . That is, to test whether and with being known up to an unknown parameter vector . The hypothesis is usually called significance testing problem, while the hypthesis is referred to as model-specification testing problem. When the dimension of is fixed, the specification testing problem has been investigated by many authors. See for instance, Zheng (1996), Lavergne and Patilea (2012), Guo et al. (2016), and Li et al. (2016). The tests for and may be used to address the following interesting and important questions: given , does carry additional information about the response ? Is the function form of linear or not? For these questions, when the dimensions of and are fixed, Liang et al. (2010) constructed suitable test statistics based on residual sums of squares under the null and alternative hypotheses. However, the procedure developed in Liang et al. (2010) are not directly applicable for high dimensional . Moreover, due to the presence of nonparametric function the setting studied in this paper is distinguished from the existing works on statistical inference for the high dimensional parametric regression model. To make inference for the parameter in model (1.1), we have to estimate the nuisance parameter and the nuisance function . For high dimensional , this is very challenging. Without an appropriate estimation, high dimensional nuisance parameter and the nuisance function may significantly deteriorate the detection power of related testing methods. We show that our proposed estimators are very helpful to make suitable inference about the parametric component and the nonparametric function .

This work makes several interesting contributions to the literature. Firstly, we establish the asymptotic distributions of partial penalized least squares estimator for high dimensional and even ultrahigh dimensional PLSIM. Previous studies mainly focus on the finite and fixed dimension setting, while our procedure allows the dimensionality to be exponential order of the sample size and the sparsity level to be diverging. Secondly, we propose an F-type test for the parametric component and show that the limiting null distribution is distribution. Thirdly, we study the specification testing problem for the nonparametric component , propose a test statistic and show that it follows an asymptotic normal distribution.

The paper is organized as follows. In section 2, we propose the partial penalized least squares estimators and derive their asymptotic distributions. In section 3, we propose tests for the parametric component and the nonparametric part , and derive their asymptotical distributions. In section 4, numerical studies are conducted to illustrate the performances of our proposed test statistics. Conclusions and discussions are given in section 5. All proofs are given in the supplementary material of this paper.

2 Profile partial penalized least squares estimators

Suppose that , is a sample from model (1.1). To ensure model (1.1) identifiable, we assume that and its first element is positive. This constraint reduces dimension of from to . As in Yu and Ruppert (2002), Wang et al. (2010) and Cui et al. (2011), we adopt the ‘delete-one-component’ method and write with . Thus can be viewed as a function of , and the Jacobian matrix is

| (2.3) |

Let , and denote to be the true value of . Let . Further denote the estimator of by , which will be specified later.

We next develop an estimation procedure for model (1.1) based on profile least squares method. Specifically, for any given , we use local linear regression to estimate by minimizing

| (2.4) |

with respect to and , where is for a kernel function with bandwidth . Denote to be the minimizer of (2.4). Then for given , and for a specific . Specifically, define

Then

| (2.5) |

Define partial penalized least squares function as

| (2.6) |

where is a penalty function with tuning parameter . Minimizing (2.6) with respect to and leads to their estimates and . It is worth noting that the nonparametric function is estimated locally, while the parametric vectors and are obtained globally by incorporating the penalty function. It is crucial that we penalize only the nuisance parameter . On one hand, it can significantly reduce the dimension of the nuisance parameter. On the other hand, it would not shrink the small elements of to be zero, and thus we can construct hypothesis testing on with local power.

2.1 Theoretical results

We next study the theoretical properties of the proposed estimation procedure. Assume that the penalty function is increasing and concave in , and has a continuous derivative with . Let for . In addition, assume is increasing in and is independent of . For any vector , define

where . Following Fan and Lv (2011a), we further define the local concavity of the penalty function at as

Before we proceed further, let us introduce some notations. Denote and be the number of elements in . Define be the complement set of . Let be the subvector of formed by elements in . Similarly let be the submatrix of a matrix formed by columns in . Moreover , and are similarly defined. Further let be the submatrix of formed as follows

. Let , the half minimum signal of . Define . Let , and . Further let , , , and . Define , For a vector . For matrix , denote and to be the minimum and maximum eigenvalues of the matrix . . Throughout the paper, and are two generic positive constants.

We impose the following conditions:

-

(A1)

, . For any , are uniformly bounded.

-

(A2)

with some and some arbitrary small , , where . Here means .

-

(A3)

Assume that and . For any with , let . Let and . Assume that

is bounded uniformly for .

-

(A4)

is twice order continuously differentiable on its support . and are bounded on . For any with , the density function of , is bounded away from 0 on . . For some and , . If is one of the following:

First order derivatives of exist and are L-Lipschitz, and are L-Lipschitz, where , are the th and th components of , respectively, , , .

-

(A5)

Suppose is a differentiable and symmetric kernel function and is one of the following: . is satisfying that . When , , for some , and .

-

(A6a)

Assume that , , , and

. -

(A6b)

Assume that and .

These conditions are mild and commonly assumed. The uniform boundedness of elements of covariate in condition (A1) is usually assumed to facilitate the technical arguments, see for instance Wang et al. (2010) and Sherwood and Wang (2016). But for , uniform boundedness is not required. The effect of nonparametric estimation is taken into account in Condition (A2). The rates of and are required for sparsity. In condition (A2), a minimum signal assumption is imposed on the nuisance parameter . This is required for variable selection consistency and evaluation of the uncertainty of the estimation for small signals. However, we should emphasize that no minimum signal condition is imposed on , the parameter of primary interest. Thus, we can still detect local alternative hypotheses effectively. This condition is reasonable in many practical applications. Van de Geer et al. (2014) and Ning and Liu (2017) do not impose such conditions. However, some additional assumptions are imposed. In fact, the validity of the decorrelated score statistic depends on the sparsity of additional parameter . From Remark 6 in Ning and Liu (2017), we know that for testing univariate parameters of high dimensional linear regression model, this requires the degree of a particular node in the graph to be relatively small when the covariate follows a Gaussian graphical model. A further discussion about the decorrelated score statistic is given in Remark 1. From Conditions (A2) and (A3), clearly the dimensionality is allowed to be exponential order of the sample size . In the theory of high dimensional regression, Gaussian or sub-Gaussian tail condition for the random error is usually assumed. However, in this paper, we only require a very mild moment condition. Condition (A4) is some regularity conditions for uniform convergence for kernel estimation and for the smoothness of related functions. Condition (A5) is the usual condition for the kernel function and is satisfied when is the density of normal distribution or a smooth density function with compact support.

Condition (A6a) is required to control the estimation error due to nonparametric estimators, while (A6b) is stronger and needed for asymptotic representation of . If we set to be fixed, then conditions (A6a) and (A6b) reduce to be and , which are assumed by many authors for partially linear single-index model with fixed dimension. Thus conditions (A6a) and (A6b) are modifications of classical conditions to accounting for the effect of . Take , then conditions in (A6a) are satisfied when . This leads to If we set , we can get . For condition (A6b), it requires that

These lead to

If we set , the condition is satisfied provided that .

We first establish the rate of convergence of and its sparsity, and then derive an asymptotic representation of in the following theorem.

Theorem 1.

Under Conditions (A1)-(A6a), the following holds. With probability tending to 1, must satisfy (i) . (ii) . If further condition (A6b) holds, we obtain that

| (2.9) |

The proof of this theorem is given in the supplementary material of this paper. Theorem 1 establishes the sparsity, consistency and asymptotic representation of the proposed profile partial penalized least squares estimators. Our results allow the dimensionality to be exponential order of the sample size . The sparsity level is also allowed to be diverging. Theorem 1 implies that the optimal bandwidth may be used for not only the sparsity and consistency, but also for the asymptotic representation, and may be of order for the sparsity and consistency. However, for the asymptotic representation, more restrictive conditions on and as in condition (A6b) are required.

3 Hypothesis testing

This section aims for developing hypothesis testing procedures for both and .

3.1 Testing the parametric component

Of interest is to test hypothesis

| (3.1) |

Under , the residual sum of squares is

| (3.2) |

Under , we need to consider the constrained penalized least squares estimators. Specially, for any given with , we first obtain the constrained profile estimator for the nonparametric function:

| (3.3) |

Denote the constrained penalized least squares function as

| (3.4) |

for some penalty function with a tuning parameter . Minimizing the above objective function with respect to leads to the estimator . Afterwards, we define the residual sum of squares under the null hypothesis:

| (3.5) |

Here . Under the null hypothesis, and should be close, while under the alternative hypothesis, should be larger than . This motivates us to consider the following test statistic:

| (3.6) |

We impose the following condition.

-

(A7)

Assume that . Here corresponds to local alternative hypotheses .

Theorem 2.

Suppose that Conditions (A1)-(A7) hold, then we have

| (3.7) |

where and is a noncentral chi-square random variable with degrees of freedom and noncentrality parameter which is allowed to vary with .

The proof of Theorem 2 is given in the supplementary material of this paper. From Theorem 2, it is clear that the null distribution of is a chi-square random variable with degrees of freedom, which does not depend on nuisance parameter nor the nuisance function . This implies that the so-called Wilks phenomenon still holds even in the (ultra)high dimensional partially linear single-index model. Further, the test statistic can detect local alternatives, which converge to the null hypothesis at the root- rate.

Remark 1.

In a case that the minimum signal assumption in (A2) is believed to be invalid, we may want to extend the decorrelated score statistic to make inference about . However, this is not straightforward. For high dimensional partially linear single index models, the negative Gaussian quasi-loglikelihood (i.e., the least squares loss) is

By adopting the notations in Ning and Liu (2017), we may consider the score functions and . When the dimension of is high, we cannot directly use to make inference for the parameter of interest . Instead we let

Here . Immediately, it follows that . That is, is uncorrelated with . We then regard as the decorrelated score function for . The key idea is to apply a high dimensional projection of the score function of the interested parameter to the nuisance parameter space.

To make inference about based on , we need to estimate the nuisance parameter , the unknown matrix and the unknown functions and . For , and , we may adopt the partial penalized least squares estimators introduced in this paper. While for the estimator of , we can consider the following formula:

for some penalty function with tuning parameter . Besides the sparsity of , we also require to be sparse. The estimated de-correlated score function is:

To prove the asymptotic normality of , it is required to check the assumptions 3.1-3.4 in Ning and Liu (2017). Due to the complicated formula of , these four assumptions are not easy to verify. The investigation of the asymptotic behavior of the decorrelated score statistic is beyond the scope of this work.

3.2 Testing the nonparametric component

In practice, it is of interest in testing whether the nonparametric function is in a specific form, for example linear, or not, or even whether it is constant. This motivates us to consider the following null hypothesis

where the form is known, and with being fixed is an unknown parametric vector. For example, if we set , a constant, then corresponds to testing whether the predictor contributes to the response or not. When the dimension of is fixed, this kind of specification testing problem has been investigated by many authors. See for instance, Zheng (1996), Guo et al. (2016), and Li et al. (2016).

Let . Then it follows that . Clearly, under , , while under , it is not equal to zero. Further we have under , , while under , we have

This motivates us to propose the following test statistic

| (3.8) |

where is a kernel function, is the bandwidth, , are the partial penalized least squares estimators defined in section 2, and is the nonlinear least squares estimator obtained by minimizing

Denote

The following conditions are needed to facilitate the technical proofs.

-

(B1)

The kernel function is univariate bounded, continuous and symmetric density function satisfying , and for . The second order derivative of is bounded.

-

(B2)

.

-

(B3)

is bounded and satisfies the first order Lipschitz condition for in a neighborhood of . Further assume that .

We then have the asymptotic normality of the proposed test statistic.

Theorem 3.

Suppose that Conditions (A1)-(A6a) and (B1)-(B3) hold, under with conditions and , we obtain that

| (3.9) |

From the proof of Theorem 3 given in the supplementary material, we can find that it is not necessary to assume homoscedasticity in order to derive the asymptotic distribution of . In fact, even under heteroscedasticity, it can be obtained that . This may further induce the results in Theorem 3. If is set to be fixed, the conditions about the bandwidth boil down to and , which are very mild. On the other hand, if also diverges, restrictions are necessary. That is, we need .

We now standardize to obtain a scale-invariant statistic:

Corollary 1.

Suppose that Conditions (A1)-(A6a) and (B1-B3) hold, under the null hypothesis with conditions and , we obtain that

| (3.10) |

Here is the chi-square distribution with one degree of freedom.

3.3 Practical implementation issues

In practice, it is desirable to have a data-driven method to choose the tuning parameter . We modify the high-dimensional BIC-type (HBIC) criterion proposed by Wang et al. (2013) to select by minimizing

where is the model identified by minimizing (2.6),

and is a sequence of numbers that should diverge to slowly. Wang et al. (2013) suggested setting . This works well in a variety of settings in this paper.

We next discuss how to make minimization of (2.6) and (3.4) faster by using local linear approximation. Minimization problems of (2.6) and (3.4) are similar, so we only work on (2.6) as an example. To minimize (2.6), noticing that a local linear approximation of is

can be approximated by

| (3.11) |

where

and

We can solve (2.6) by iteratively minimizing penalized least squares functions. Specifically, we could take the LASSO estimate for the whole model as the initial value : For we iteratively solve (3.12) until the sequence of converges. Our numerical study shows that the algorithm can converge very fast even if the initial value is not taken close to the true value.

| (3.12) |

Zou and Li (2008) proposed an algorithm for maximizing the penalized likelihood for concave penalty functions based on local linear approximation (LLA). Here we may apply local linear approximation to the penalty term in (3.11),

| (3.13) |

The minimization problem (3.12) becomes

| (3.15) |

In that way, we transform the original problem into iteratively solving penalized least squares with penalty. There are effective algorithms for solving (3.15) because dealing with penalty can take advantage of kinds of computationally efficient algorithms for the LASSO, such as the least angle regression (LARS) algorithm proposed by Efron et al. (2004).

4 Numerical studies

4.1 Simulation studies

In this section, we conduct simulation studies to assess the finite-sample performance of the proposed estimation and testing methods. The SCAD penalty function (Fan and Li, 2001) is adopted in our simulation study. We also compare the proposed estimator and tests with the oracle estimator and oracle tests, where the true signal set is assumed to be known and models are fitted based on that. Denote and to be the oracle test statistics. We report the performances of the profile partial penalized least squares estimator and different test statistics based on 500 replications. The sample size is taken to be 200. All simulations were conducted using MATLAB code.

Example 1. To evaluate the performance of the proposed profile partial penalized least squares estimator and F-type test statistic , we generate simulation data from the following models.

Model 1a. ,

Model 1b. .

For both models, we take the dimension of to be and generate from . In model 1a, the coefficient for the mean function is and when . We generate and from multivariate normal distributions with zero mean and covariance matrix and respectively, with . We consider two scenarios for the dimension of , : (i) ; (ii) . This is used to investigate the impact of dimensionality . In model 1b, we set and when . To evaluate the influence of correlation among covariates, three scenarios for model 1b are considered. In scenarios (i) and (ii), and are generated in the same way as in model 1a, but now we take , , and consider (i) and (ii) . In scenario (iii), and are correlated. We generate from normal distribution with zero mean and covariance matrix with . We let , . In real data analysis in Section 4.2, we use 10-fold cross-validation to choose the bandwidth. But this is too time-consuming in simulation. As an alternative, we generated several data sets to get an idea about the range of an appropriate bandwidth. In simulation study of model 1a, we set the bandwidth . Note that the standard error of is 1.08 in this simulation setting. So 95% values of lies between to 2.1. This implies that for a given , we estimate based on about 9 percent of observations. Similarly in model 1b, the bandwidth is set to be for each scenario so that we use about 9 percent of data to estimate for a given .

We first examine the finite sample performance of the proposed estimators. Table LABEL:est reports the ratio of the true nonzero coefficients correctly set to nonzero, denoted by ‘T’ in the table, the ratio of the true zero coefficients incorrectly set to nonzero, denoted by ‘F’, bias and mean squared error of the resulting estimates over the 500 replications for both models under different scenarios and . In model 1a, two scenarios share the same oracle model. The ratio of the true nonzero coefficient that were correctly set to nonzero is always close to 1 and the ratio of the truly zero coefficients that are incorrectly set to nonzero is always close to 0, indicating that our method can always correctly identify the true submodel. Compared with the oracle estimator, both bias and mean squared error of behave similar to the oracle one. Bias and mean squared error of is usually a little bit larger than oracle setting. The error mainly comes from the partial penalization on using the SCAD penalty and also from the limitation of finite sample and imperfect selection of tuning parameter . However, the error is in a reasonable order and is acceptable. We find from the empirical size and power for (4.1) below that the small error does not affect much statistical inference on parameters of interest.

Further we consider the following null and alternative hypotheses:

| (4.1) |

where for model 1a and for model 1b. When , it corresponds to , thus we can examine Type I error rate. When , it corresponds to the alternative hypothesis, which allows us to examine the power of the proposed test.

Figure 1 depicts the empirical sizes and powers of the tests under model 1a. As expected, controls the size well and is powerful since it performs as well as the oracle test . The empirical power of remains roughly the same when increases from 300 to 1500. This implies that the dimension of does not have a dramatic impact on the performance of .

| 0 | 0.01 | 0.02 | 0.03 | 0.04 | 0.05 | 0.10 | 0.15 | 0.20 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| (i) | 0.042 | 0.080 | 0.118 | 0.192 | 0.360 | 0.466 | 0.980 | 1 | 1 | |

| 0.058 | 0.086 | 0.109 | 0.266 | 0.343 | 0.506 | 0.937 | 1 | 1 | ||

| (ii) | 0.058 | 0.078 | 0.150 | 0.286 | 0.442 | 0.656 | 0.998 | 1 | 1 | |

| 0.042 | 0.068 | 0.116 | 0.196 | 0.406 | 0.604 | 0.994 | 1 | 1 | ||

| (iii) | 0.048 | 0.060 | 0.122 | 0.194 | 0.312 | 0.428 | 0.998 | 1 | 1 | |

| 0.052 | 0.076 | 0.125 | 0.188 | 0.296 | 0.436 | 0.960 | 1 | 1 |

Empirical sizes and powers of tests under model 1b are demonstrated in Table 1, from which it can be seen clearly that the empirical sizes of are close to the nominal level 0.05. Furthermore, the powers of and are close. When the covariance matrix structure changes with increasing from 0.25 to 0.75, the powers of and increase. This implies that covariance matrix of covariates has some impact on powers of and . When and are correlated, there is little power loss. In summary, the proposed test performs as well as the oracle test in terms of power, and controls the empirical sizes very well.

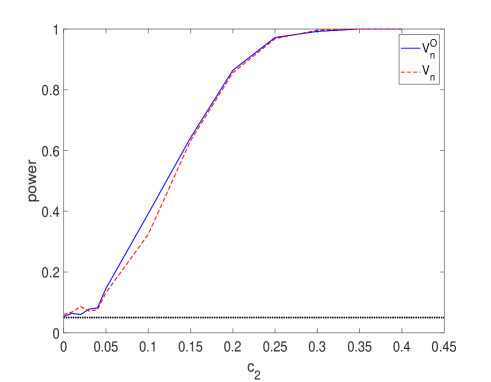

Example 2. This example is designed to study the performance of the nonparametric component test statistic . To this end, we generate data from

Model 2. .

In this example, and are generated in the same way as in model 1.a. The dimension of , is chosen to be 1500 here. We consider hypotheses:

where , and are chosen to be 1.3409 and 0.3912 respectively. This model setting was used by Liang et al. (2010) with fixed . True value of is chosen to be 1. Again, when , the null hypothesis is true, while if , the alternative hypothesis holds.

Figure 2 depicts the empirical sizes and powers of and at significance level 0.05. Figure 2 indicates that the empirical size of is close to the level 0.05. The empirical power of is greater than 0.95 when is greater than 0.30. Further, the empirical power of is very close to that of the oracle test .

4.2 A real data example

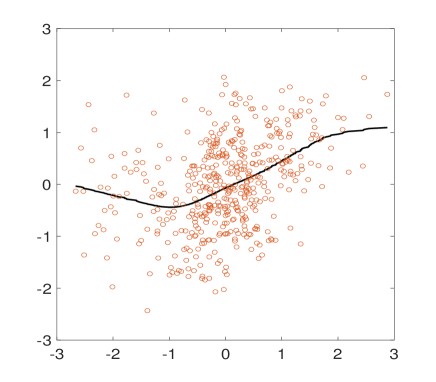

We now illustrate the proposed methodology by an application to the supermarket data set (Wang, 2009). The data consists of daily records in a supermarket. Each record corresponds to the number of customers as the response and sale amount of 6398 products as predictors. We standardize both response and predictors to be with zero mean and unit variance. We fit a partially linear single-index model to the data set and aim to locate products whose sale volumes are mostly correlated with the number of customers, and perform related hypothesis testings to the regression function.

We carry out a preprocessing step that we reduce the dimension of predictors to 1000 by employing the feature screening scheme in Li et al. (2012). To decide which variables belong to the linear part or the nonlinear part , we adopt the strategy suggested by Xia et al. (1999) and Zhang et al. (2012). Their ideas are based on dealing with the scatterplot of each variable versus the response. To take both linear behavior and goodness of fit into account, we first compute the Pearson correlation between the response and each variable and select variables with an absolute value of the correlation greater than 0.3. Then we fit the response and each covariate with local linear smoothing. We obtain the estimated mean function and corresponding pointwise confidence band by computing the mean plus and minus times the estimated standard deviation function. We also fit a linear regression. If the linear straight line lies in the confidence band, the variable goes into the linear part of our model. In this example, we choose as the threshold. Otherwise, if the correlation is smaller than 0.3 or the linear regression line cannot be encompassed by the confidence band, the variable goes into the single-index part. This leads to a number of 994 variables () for single-index component and 6 variables () for the linear component. Model 3 below is fitted. We use 10-fold cross-validation to choose the bandwidth and HBIC to choose . This leads to the selected bandwidth and the selected tuning parameter . The fit of the semiparametric part of the model is shown in Figure 3. There are in total of 12 active variables selected from covariates .

Model 3.

From Figure 3, there seems to exist a nonlinear pattern for the relationship between and the response .

We apply the proposed hypothesis testing procedures for this data set. We first consider the following two testing problems: and , where is a constant. These two hypotheses and aim to test whether the covariates and contribute to the response or not, respectively. Based on the proposed test statistics and , the -values of the two hypotheses are 0. This implies that the selected variables indeed show a significant influence on the response. Then we further test whether the contribution of the single-index components to the response is linear or not and perform hypothesis testing . The corresponding -value is 0.004. Therefore, we reject the null hypothesis that the link function for single-index part is linear at level 0.05. This is consistent with our observation on the fitting plot of the semiparametric part shown in Figure 3. In conclusion, we find there is a significant effect of the selected variables and potential non-linear relationship between selected variables and the response. It is worth pointing out that Liu et al. (2016) and Lan et al. (2016) did the analysis on the same data set but fitted high dimensional linear model on it. However, from our analysis, we find evidence that the linear model is not suitable and recommend fitting a semiparametric model on this data and data with similar attributes.

5 Conclusions and discussions

In this paper, we developed new statistical inference procedures for high dimensional partially linear single-index model. Different from linear regression model, we have to deal with the nuisance unknown function. To derive powerful hypothesis tests, we first propose a profile penalized least squares estimator and study its asymptotic properties. Then we propose an F-type test for the parametric component. We further study the specification testing problem for the nonparametric component and propose a test statistic with an asymptotic normal distribution. A notable feature is that the optimal rate for the bandwidth is allowed, even the covariate is of high dimensional. No under-smoothing or over-smoothing is required. The dimensionality is allowed to be exponential order of the sample size and the sparsity level can also be diverging.

In this paper, we focus on testing the low dimensional parametric vector , while regard the high dimensional parametric vector as nuisance parameter. In practice, it may also be interesting to make inference on components of . This issue was studied recently by Eftekhari et al. (2021) for single index model under elliptical symmetry assumption on the covariates. The extension of their procedure to PLSIM without elliptical assumption would be an interesting topic for future research.

Supplement

The supplementary material consists of three technical lemmas, the proofs of these three lemmas and proofs of all theorems in this paper.

Appendix: Technical Proofs

The following three lemmas will be used in the proofs for the main theorems, and their proofs are given in the supplementary material of this paper.

We first establish some results on uniform convergence for kernel estimation, which has been considered in several authors (Mack and Silverman, 1982; Liebscher, 1996; Hansen, 2008), but none of them considered estimating several regression functions simultaneously with the number of regression functions growing with . Thus, their results cannot be directly applied for nonparametric estimation in the presence of high dimensional covariates. In Lemma A.1 below, we establish the uniform convergence rate for kernel estimation for the regression functions when the number of regression functions grows with sample size . Let and be a - and -dimensional continuous random vector, respectively. With a slight abuse of notation, here and represent general random variable and vector, respectively, and are not the covariate and the response in the main text.

Lemma A.1.

Suppose that is a random sample from , where the dimension of grows with . Let be a kernel function, and

It follows that

| (A.1) |

under the following three assumptions:

-

Assumption 1. The density of , , satisfies that . For some and , and

-

Assumption 2. is differentiable and . . There exist some constants , and such that , for .

-

Assumption 3. The bandwidth satisfies and for some .

We introduce some notation for the following. Let , and . Further let and . Denote , , . Define

Lemma A.2.

Under conditions (A1), (A4) and (A5), for any which satisfies and , it follows that

uniformly for .

Lemma A.3.

Under conditions (A1), (A4), (B2) and (B3), for any which satisfies and , we have:

Proof of Theorem 1:

To enhance the readability, we divide the proof of Theorem 1 into three steps. In the first step, we show that there exists a local minimizer of with the constraints , such that . In the second step, we prove that is indeed a local minimizer of . This implies . In the final step, we derive the asymptotic expansion of .

Step 1: Consistency in the -dimensional subspace: We first constrain on the -dimensional subspace of of . This partial penalized least squares function is given by

Here and . We now show that there exists a strict local minimizer of such that . To this end, we consider an event

where with , , and denotes the boundary of the closed set . Clearly, on the event , there exists a local minimizer of in . Thus, we only need to show that as when is large. To this end, we next study the behavior of on the boundary .

Define

| (A.3) |

Note that

| (A.4) | |||||

Let be between and , , and

We have that

Thus it follows that

| (A.6) | |||||

| (A.7) |

and

In what follows, we will show that , and are all of the order . Thus they are dominated by and .

It follows by the Cauchy-Schwarz inequality that

| (A.10) | |||||

From Lemma A.2 and condition (A1), it follows that

hold uniformly for when , , and . Thus . Similarly we can show that . We next deal with . By

| (A.11) | ||||

under condition that , and .

The orders of and can be derived using the same argument. We only show the proof for . For the term , it follows that

For the term , by Lemma A.2 and condition (A3),

For the term , noticing that , and is bounded uniformly of , we can show applying martingale central limit theorem (Corrollary 3.1 in (Hall and Heyde, 2014)),

Up to now, we show that , and are all of the order . As a result, it follows that

| (A.12) |

Under conditions and , we have

Further note that

On the boundary , , , and thus

| (A.13) |

In summary, by allowing to be large enough, all terms of is dominated by the first term which is positive under condition (A1).

Using Taylor’s expansion, we have

Here is a diagonal matrix. By condition (A2), the maximum eigenvalue of is bounded by . It follows from the concavity of , , and condition (A2) that

These results imply that

Finally, by allowing to be large enough, we conclude that is dominated by a positive value. Consequently, step 1 is obtained.

Step 2: Sparsity. According to Theorem 1 in Fan and Lv (2011b), it suffices to show that with probability tending to 1, we have

| (A.14) |

Here satisfies that and .

Firstly, define

| (A.15) |

Secondly note that

As a result, we obtain that

In the following, we aim to determine the orders of . Let . First, by condition (A3) and Markov inequality, we can show that

Let with being large enough. Then by using Bernstein inequality, we obtain that

Thus we get

Further we have that

Now we turn to consider the third term . According to the proof of Lemma A.2, holds uniformly over . Thus, we have

Similarly, we can show that

Lastly,

under condition (A6a). Thus step 2 is finished.

Step 3: Asymptotic expansions. Steps 1 and 2 show that with probability 1, and further .

First let

| (A.18) |

For , let

| (A.19) |

Under condition (A2), we have . This implies that

By the concavity of and condition (A2), we obtain that.

Thus we obtain

| (A.20) |

Next we decompose as follows.

For the term , we have

| (A.21) |

In the following, we will show that are all .

Recall that . Then from the argument for the term in the proof of step 1, we know that

under conditions and satisfied by (A6b).

While for the term , we have

under conditions that and satisfied by (A6b).

From the argument for the term in the proof of step 1, we know that is of the following order

under conditions that and satisfied by (A6b).

Thus we obtain that

Recall that

Thus it follows that

under condition that .

As a result, we obtain that

| (A.22) |

Proof of Theorem 2:

Similar to the arguments in the proof of Theorem 1, we can show that with probability 1, and further . For , we have

| (A.23) |

Similar to the argument for , we have

Recall that . Then we have

Let

Under condition (A1), we have . This implies that , and then . Finally we get .

Then we obtain that

Consequently, it follows that

| (A.31) | |||||

Or equivalently

| (A.34) | |||||

Here

It is easy to see that is an idempotent matrix with rank .

Recall that

| (A.38) |

Then we can obtain

It follows that

Consequently, under condition (A7), we have

| (A.39) |

Now we are ready to investigate the asymptotic distribution of the F-type test . Let . Under the event and recalling (A.19), we obtain that

| (A.42) | |||||

The second equation follows from (A.39) and based on condition (A2). The last equation holds due to equation (A.34). Recall that

Further denote that

It follows that

| (A.45) | |||||

| (A.50) | |||||

| (A.51) |

Thus we obtain that

| (A.52) |

It is easy to know that .

In the following, we aim to show that is a consistent estimator of . In fact, we have

Due to the consistencies of the related estimators, it is clear that

Thus we obtain that

As a result, we have

Thus

Proof of Theorem 3:

Under the null hypothesis,

Further denote . Thus we have

| (A.53) | |||||

For the first term , we have

Note that

Thus is a degenerate U-statistic. From Zheng (1996), we get

| (A.54) |

Here

Next, we aim to show that are all of order .

Denote

Clearly, we have

Since is a symmetric function, similar to , the following term

is also a degenerate U-statistic. To determine its order, we can compute its second order moment as follows

Since , we only need to consider the terms with or . Then, it follows that

Consequently, we have that Under the event with probability tending to 1, we obtain that

| (A.55) |

under condition that . Denote and . Further let

Clearly, we have

Similar to the argument for and from Lemma 2 in Guo et al. (2016) and Lemma 2, we can derive that

| (A.56) |

under condition that .

Further let

Under assumption that and based on Lemma 2, we can also obtain that

| (A.57) |

In sum, under the null hypothesis with conditions that and , we obtain that

Since is actually unknown, an estimate is defined as

The proof follows from the U-statistic theory and the consistencies of parametric estimators, and thus the details are omitted here.

The following two Lemmas are used in the proof of the main Theorems. We first present the following lemma,

Lemma A.4.

Under conditions (A4) and (A5), for any which satisfies , we have

Proof: Since the proof for the second statement is more complicated, we only focus on the second result. The first result can be similarly demonstrated and thus omitted here. Recall that

| (A.58) |

where

for and .

Define

Clearly,

Further

| (A.59) |

In the following, we only deal with the first term of .

Recall that

Here . Notice that

For the term , we have:

Now we determine the expectation and variance of and . In fact, under conditions (A4) and (A5), we have:

Similarly, we get

Next note that:

In sum, we get:

Similarly, we obtain that

Note that . Consequently, we get:

Next we turn to consider the term . Denote and , which are both of order . Further note that

Then we get:

under condition that .

Further note that

Then we have:

Other terms of and also can be handled similarly. After tedious calculations, we finally get:

| (A.60) |

Further note that

Then eventually we obtain that

We present the following lemma about the convergence rate of :

Lemma A.5.

Under conditions (B2) and (B2), and the assumption that , we have:

Proof: In fact, the proof follows from the proof for Lemma 4.2 in Van Keilegom et al. (2008). From Van Keilegom et al. (2008), we know that the convergence rate of is determined by the following term:

Here .

First note that under the event with probability tending to 1, we have:

Here and are similarly defined and .

Secondly

Thus we get

Under the assumption that is bounded and satisfies Lipschitz condition of order 1 for in a neighborhood of , it is known that the order is determined by the second term.

We note that for any which satisfies that ,

The last equation holds under condition that . Thus the results follow.

References

- Barber and Candès (2015) Barber, R. F. and Candès, E. J. (2015), “Controlling the false discovery rate via knockoffs,” The Annals of Statistics, 43, 2055–2085.

- Candès et al. (2018) Candès, E., Fan, Y., Janson, L., and Lv, J. (2018), “Panning for gold: ‘model-X’ knockoffs for high dimensional controlled variable selection,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80, 551–577.

- Carroll et al. (1997) Carroll, R. J., Fan, J., Gijbels, I., and Wand, M. P. (1997), “Generalized partially linear single-index models,” Journal of the American Statistical Association, 92, 477–489.

- Cui et al. (2011) Cui, X., Härdle, W. K., and Zhu, L. (2011), “The EFM approach for single-index models,” The Annals of Statistics, 39, 1658–1688.

- Efron et al. (2004) Efron, B., Hastie, T., Johnstone, I., and Tibshirani, R. (2004), “Least angle regression,” The Annals of Statistics, 32, 407–499.

- Eftekhari et al. (2021) Eftekhari, H., Banerjee, M., and Ritov, Y. (2021), “Inference In High-dimensional Single-Index Models Under Symmetric Designs,” J. Mach. Learn. Res., 22, 27–1.

- Fan and Li (2001) Fan, J. and Li, R. (2001), “Variable selection via nonconcave penalized likelihood and its oracle properties,” Journal of the American Statistical Association, 96, 1348–1360.

- Fan et al. (2020) Fan, J., Li, R., Zhang, C.-H., and Zou, H. (2020), Statistical Foundations of Data Science, Chapman and Hall/CRC.

- Fan and Lv (2011a) Fan, J. and Lv, J. (2011a), “Nonconcave penalized likelihood with NP-dimensionality,” IEEE Trans. Inform. Theory, 57, 5467–5484.

- Fan and Lv (2011b) — (2011b), “Nonconcave penalized likelihood with NP-dimensionality,” IEEE Transactions on Information Theory, 57, 5467–5484.

- Guo et al. (2016) Guo, X., Wang, T., and Zhu, L. (2016), “Model checking for parametric single-index models: a dimension reduction model-adaptive approach,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78, 1013–1035.

- Hall and Heyde (2014) Hall, P. and Heyde, C. C. (2014), Martingale Limit Theory and its Application, Academic press.

- Hansen (2008) Hansen, B. E. (2008), “Uniform convergence rates for kernel estimation with dependent data,” Econometric Theory, 726–748.

- Härdle et al. (2012) Härdle, W., Liang, H., and Gao, J. (2012), Partially Linear Models, Springer Science & Business Media.

- Ichimura (1993) Ichimura, H. (1993), “Semiparametric least squares (SLS) and weighted SLS estimation of single-index models,” Journal of Econometrics, 58, 71–120.

- Lai et al. (2014) Lai, P., Tian, Y., and Lian, H. (2014), “Estimation and variable selection for generalised partially linear single-index models,” Journal of Nonparametric Statistics, 26, 171–185.

- Lan et al. (2016) Lan, W., Zhong, P.-S., Li, R., Wang, H., and Tsai, C.-L. (2016), “Testing a single regression coefficient in high dimensional linear models,” Journal of Econometrics, 195, 154–168.

- Lavergne and Patilea (2012) Lavergne, P. and Patilea, V. (2012), “One for all and all for one: regression checks with many regressors,” Journal of Business & Economic Statistics, 30, 41–52.

- Li et al. (2016) Li, H., Li, Q., and Liu, R. (2016), “Consistent model specification tests based on k-nearest-neighbor estimation method,” Journal of Econometrics, 194, 187–202.

- Li et al. (2012) Li, R., Zhong, W., and Zhu, L. (2012), “Feature screening via distance correlation learning,” Journal of the American Statistical Association, 107, 1129–1139.

- Liang et al. (2010) Liang, H., Liu, X., Li, R., and Tsai, C.-L. (2010), “Estimation and testing for partially linear single-index models,” Annals of Statistics, 38, 3811–3836.

- Liebscher (1996) Liebscher, E. (1996), “Strong convergence of sums of -mixing random variables with applications to density estimation,” Stochastic Processes and Their Applications, 65, 69–80.

- Liu et al. (2016) Liu, H., Yao, T., and Li, R. (2016), “Global solutions to folded concave penalized nonconvex learning,” Annals of Statistics, 44, 629–659.

- Liu et al. (2021) Liu, W., Ke, Y., Liu, J., and Li, R. (2021), “Model-free feature screening and FDR control with knockoff features,” Journal of the American Statistical Association, In press.

- Mack and Silverman (1982) Mack, Y.-P. and Silverman, B. W. (1982), “Weak and strong uniform consistency of kernel regression estimates,” Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 61, 405–415.

- Ning and Liu (2017) Ning, Y. and Liu, H. (2017), “A general theory of hypothesis tests and confidence regions for sparse high dimensional models,” The Annals of Statistics, 45, 158–195.

- Sherwood and Wang (2016) Sherwood, B. and Wang, L. (2016), “Partially linear additive quantile regression in ultra-high dimension,” The Annals of Statistics, 44, 288–317.

- Shi et al. (2019) Shi, C., Song, R., Chen, Z., and Li, R. (2019), “Linear hypothesis testing for high dimensional generalized linear models,” The Annals of Statistics, 47, 2671–2703.

- Speckman (1988) Speckman, P. (1988), “Kernel smoothing in partial linear models,” Journal of the Royal Statistical Society: Series B (Methodological), 50, 413–436.

- Tibshirani (1996) Tibshirani, R. (1996), “Regression shrinkage and selection via the lasso,” Journal of the Royal Statistical Society: Series B (Methodological), 58, 267–288.

- Van de Geer et al. (2014) Van de Geer, S., Bühlmann, P., Ritov, Y., and Dezeure, R. (2014), “On asymptotically optimal confidence regions and tests for high-dimensional models,” The Annals of Statistics, 42, 1166–1202.

- Van Keilegom et al. (2008) Van Keilegom, I., Manteiga, W. G., and Sellero, C. S. (2008), “Goodness-of-fit tests in parametric regression based on the estimation of the error distribution,” Test, 17, 401–415.

- Wang (2009) Wang, H. (2009), “Forward regression for ultra-high dimensional variable screening,” Journal of the American Statistical Association, 104, 1512–1524.

- Wang et al. (2010) Wang, J.-L., Xue, L., Zhu, L., and Chong, Y. S. (2010), “Estimation for a partial-linear single-index model,” The Annals of Statistics, 38, 246–274.

- Wang et al. (2013) Wang, L., Kim, Y., and Li, R. (2013), “Calibrating non-convex penalized regression in ultra-high dimension,” Annals of Statistics, 41, 2505–2536.

- Xia and Härdle (2006) Xia, Y. and Härdle, W. (2006), “Semi-parametric estimation of partially linear single-index models,” Journal of Multivariate Analysis, 97, 1162–1184.

- Xia et al. (1999) Xia, Y., Tong, H., and Li, W. K. (1999), “On extended partially linear single-index models,” Biometrika, 86, 831–842.

- Yu and Ruppert (2002) Yu, Y. and Ruppert, D. (2002), “Penalized spline estimation for partially linear single-index models,” Journal of the American Statistical Association, 97, 1042–1054.

- Zhang et al. (2012) Zhang, J., Wang, T., Zhu, L., and Liang, H. (2012), “A dimension reduction based approach for estimation and variable selection in partially linear single-index models with high-dimensional covariates,” Electronic Journal of Statistics, 6, 2235–2273.

- Zhang et al. (2013) Zhang, J., Yu, Y., Zhu, L., and Liang, H. (2013), “Partial linear single index models with distortion measurement errors,” Annals of the Institute of Statistical Mathematics, 65, 237–267.

- Zhang et al. (2017) Zhang, Y., Lian, H., and Yu, Y. (2017), “Estimation and variable selection for quantile partially linear single-index models,” Journal of Multivariate Analysis, 162, 215–234.

- Zheng (1996) Zheng, J. X. (1996), “A consistent test of functional form via nonparametric estimation techniques,” Journal of Econometrics, 75, 263–289.

- Zhu and Xue (2006) Zhu, L. and Xue, L. (2006), “Empirical likelihood confidence regions in a partially linear single-index model,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), 68, 549–570.

- Zou and Li (2008) Zou, H. and Li, R. (2008), “One-step sparse estimates in nonconcave penalized likelihood models,” Annals of Statistics, 36, 1509–1533.