Optimal Network Revenue Management with Nonparametric Demand Learning

Demand Balancing in Primal-Dual Optimization for Blind Network Revenue Management

Sentao Miao††thanks: Author names listed in alphabetical order.

\AFFLeeds School of Business, University of Colorado, Boulder, CO 80309, USA

sentao.miao@colorado.edu

\AUTHORYining Wang

\AFFNaveen Jindal School of Management, University of Texas at Dallas, Richardson, TX 75019, USA

yining.wang@utdallas.edu

This paper proposes a practically efficient algorithm with optimal theoretical regret which solves the classical network revenue management (NRM) problem with unknown, nonparametric demand. Over a time horizon of length , in each time period the retailer needs to decide prices of types of products which are produced based on types of resources with unreplenishable initial inventory. When demand is nonparametric with some mild assumptions, Miao & Wang (2021) is the first paper which proposes an algorithm with type of regret (in particular, plus additional high-order terms that are with sufficiently large ). In this paper, we improve the previous result by proposing a primal-dual optimization algorithm which is not only more practical, but also with an improved regret of free from additional high-order terms. A key technical contribution of the proposed algorithm is the so-called demand balancing, which pairs the primal solution (i.e., the price) in each time period with another price to offset the violation of complementary slackness on resource inventory constraints. Numerical experiments compared with several benchmark algorithms further illustrate the effectiveness of our algorithm.

demand learning, network revenue management problem, primal-dual optimization, gradient descent, demand balancing.

1 Introduction

The price-based network revenue management (NRM) is a classical problem in operations management, which has the following problem formulation. Let be the time horizon, be the total number of product types and be the total number of resource types. At the beginning of each time period , an algorithm posts a price vector , which incurs a realized demand vector of products , and collects revenue while incurring resource consumption , where is the resource consumption matrix. Each resource type has a non-replenishable initial inventory level of and a product cannot be sold if its required resources’ inventory is depleted. The objective of NRM is to maximize the expected total revenue over time periods, subject to resource inventory constraints.

In this paper we study a setting in which the expectations of realized demands are governed by a fixed but unknown demand curve , with demand noises being independently and identically distributed and well-behaved (see Section 2 for detailed problem set-up and assumptions). Such a setting is usually referred to as blind network revenue management because the unknown demand curve needs to be learnt on the fly, and has been the subject of extensive studies over the past decade, pioneered by the seminal work of Besbes & Zeevi (2012). We present a high-level summary of important existing results next, which motivate our approaches and give the context for better understanding our contributions.

When the demand curve belongs to a certain parametric function class (e.g., linear, logistic or exponential functions with unknown parameters), the standard method is to use linear regression or maximum likelihood estimation to obtain an estimated demand curve (or an upper bound of it) and then carry out optimizations. This is for example the underlying strategy of Broder & Rusmevichientong (2012), Ferreira et al. (2018), some of which also have model estimation and price optimization procedures intertwined. For non-parametric models, it is possible to estimate the entire demand function by either using a binning approach in one dimension (Besbes & Zeevi 2012), or by using spline approximation in higher dimensions when the demand curve is very smooth (Chen et al. 2019a). Such approaches are not likely to be optimal for nonparametric demand curves in high dimension due to the curse of dimensionality, as evident in the results of (Lei et al. 2015, Chen et al. 2019a, Wang et al. 2021, Chen & Gallego 2021). More specifically, the regret must depend exponentially on the dimension or .

Another line of research for blind NRM focuses primarily on inexact optimization methods applied to certain fluid approximation of the NRM problem, thus circumventing the curse of dimensionality by exploiting concavity structures in the problem satisfied by most commonly used demand models (Li & Huh 2011). With and (expected) demands being stationary (meaning that does not change over time), it is well-known that (Gallego & Van Ryzin 1994, 1997) the optimal solution of NRM could be approximated by an optimization problem subject to , with being the expected revenue function and being the normalized inventory vector. With being concave in and being a polytope or halfspace feasible region, it is possible to optimize over using either first-order methods (Chen & Shi 2023) or cutting plane methods (Wang et al. 2014, Miao & Wang 2021). The challenge of this type of methods is obvious: because the algorithm cannot really operate in the demand domain (since the demand curve is unknown), meaning that an algorithm cannot directly set exact demand rates but can only affect demand rates via an unknown demand curve by setting up prices, conversions between the price and demand domains need to be carried out, which is highly non-trivial in multiple dimensions leading to sub-optimal regret (Chen & Shi 2023) or high dimensional overheads (Miao & Wang 2021).

Finally, the seminal work of Badanidiyuru et al. (2018) initialized the study of primal-dual methods in bandits with knapsacks problems. When learning is required, such methods are typically applied to parametric problems, because (approximate) optimal primal solutions are requested for every dual variable being obtained at the beginning of each time periods. See for example the works of Agrawal & Devanur (2016), Miao et al. (2021), Balseiro et al. (2023). The main advantage of such methods is that the primal optimization problem could be solved without constraints, which is feasible even for some non-concave objectives that are well-behaved (e.g., satisfying Polyak-Lojasiewicz conditions (Karimi et al. 2016)). In contrast, without Lagrangian multipliers the fluid approximation in the price domain has an unknown, non-convex feasible region which is much harder to solve.

For nonparametric problems, the major challenge of applying such primal-dual methods is the fact that multiple time periods are necessary to obtain reasonably good primal solutions for a fixed dual vector, but in the framework of (Badanidiyuru et al. 2018) (and also all its follow-up works) the dual vectors must be constantly updated, interfering with the primal optimization procedure. Indeed, such a challenge has deeper roots from a feasibility perspective, which we shall elaborate in much more details in the next section, that also motivates our solutions.

1.1 Infeasible primal-dual methods with frequent dual updates

To gain deeper understanding of the primal-dual framework in (Badanidiyuru et al. 2018), let us first summarize it at a very high level. Let subject to be a constrained optimization problem where is the action (in our problem, denotes price vectors), and be the Lagrangian corresponding to non-negative dual vector , and be the dual function. The work of (Badanidiyuru et al. 2018) optimizes the constrained problem in an iterative manner: at iteration , first compute as a maximizer of the Lagrangian at dual vector ; afterwards, slack is used to update dual vector for the next period using an online convex optimization (OCO) method, such as online mirror descent. When or is unknown, their estimates are used to perform primal and dual updates.

This method is very similar to dual descent, a natural algorithm for convex optimization. Note that is a convex function in and if there is a unique that maximizes . Hence, updating dual vectors using online mirror descent based on naturally minimizes the dual function, which in turn maximizes the primal function.

One key difference between BwK type algorithms and the classical dual descent algorithm, which arises because of the nature of bandit problems, is the handling of violation of primal feasible constraints. Recall that dual descent is an infeasible method, meaning that all primal solutions obtained on the optimization path are likely infeasible to the primal problem. Furthermore, the violation of primal feasibility constraints of at a sub-optimal could be arbitrarily large, even if is very close to and strong duality holds (meaning that there exists a primal feasible that maximizes ). Indeed, this is the case for LP dual problems or in general any dual problems that are not smooth, as even the slightest amount of deviation from leads to significantly infeasible primal solutions.

Note that, when the primal objective is concave, an averaging procedure of primal solutions could lead to approximately primal feasible solutions without additional constraints or measures. See for example, the works of (Nesterov 2009, Nedić & Ozdaglar 2009). Such an approach is not applicable in our problem for two reasons. First, the objective function is non-concave in the price domain, which invalidates the averaging argument in the approximate feasibility analysis. Second, approximate primal feasibility only applies to averaged primal solutions, which cannot be extended to analyze the optimization algorithm with cumulative regret upper bounds because the cumulative regret definition tracks all solutions at which function values are queried.

When dual descent is applied as an optimization algorithm with full information, the infeasible nature of the method is not a big deal as our purpose is only to find an optimal (thus feasible) solution in the end. However, in bandit problems the (infeasible) primal solutions are actually implemented in sequential time periods, raising serious concerns if they are far from primal feasible. Therefore, BwK algorithms must implement additional measures to control the violation of primal feasibility constraints, because the mere convergence of dual variables is usually not sufficient. One of the key ideas in (Badanidiyuru et al. 2018) is to use online convex optimization formulation that treats the slacks (gradients of the dual function) as an adversarial sequence of vectors, arguing that there exists a dual vector that limits the (cumulative) violation of primal feasibility of . Afterwards, online convex optimization methods are analyzed showing that are competitive against any fixed benchmark, even if are adversarial.

Because the slacks are treated as adversarial in (Badanidiyuru et al. 2018), which is also the case in all the subsequent follow-up works (Agrawal & Devanur 2016, 2019, Miao et al. 2021, Balseiro et al. 2023), the “frequent” updates of dual vectors are essentially unavoidable. Otherwise, the effectiveness of the dual vectors can no longer be ensured via adversarial linear optimization arguments. Therefore, we call this type of methods “infeasible primal-dual methods with frequent dual updates”. The nature that dual vectors must be updated frequently has two disadvantages. First, in some applications such as online ad allocation, dual vectors (measuring budget spending of ad-liners) cannot be updated too often due to computational constraints as the number of ad bidding opportunities over a given time period is huge. In applications such as dynamic pricing, it is not a good idea either to have frequent dual updates (and hence frequent primal/price updates) as frequent changes of prices do not look good. Second, as is the focus of this paper, when or are nonparametric functions to be learnt, the primal optimization problem cannot be accomplished using a few number of time periods. Because updates of dual vectors directly change the primal objectives to be maximized, analyzing such a scheme is going to be extremely difficult. 111One idea is to apply bandit convex optimization algorithms which might allow functions to be optimized to change adversarially over time. This has two disadvantages. First, such methods are typically very complex and most of the time impractical (Bubeck et al. 2021). More importantly, unlike the stationary case where non-concave objectives could be tractable with additional constraints, in bandit convex optimization the analysis relies crucially on the first-order conditions of each function which essentially rules out extensions to revenue functions that are not concave in price vectors.

1.2 Infeasible primal-dual methods with infrequent dual updates

Motivated by the discussion in the previous section, in this paper we aim at an improved BwK algorithm by limiting the number of dual variable updates, which facilitates primal optimization of nonparametric functions and also has potential impacts in operational practice. To this end, we discard the perspective of treating slacks as a completely adversarial sequence, and recover the original meanings of as gradients of the dual function at . With suitable conditions, the dual function in our problem is strongly smooth and convex, meaning that gradient descent methods with fixed step sizes shall have linear convergence and therefore only an number of dual updates are required. 222When is not smooth or strongly convex, it is also possible to limit the number of dual updates by using cutting-plane methods, such as the ellipsoid method (Khachiyan 1979) or interior-point methods (Vaidya 1996) which enjoys linear convergence for non-smooth functions. Such methods however are beyond the scope of this paper. This not only limits the number of dual variable updates, but also allows ample time periods to solve an unconstrained primal problem without specific parametric forms.

Because we have discarded the adversarial linear optimization perspective in (Badanidiyuru et al. 2018), we have to implement additional measures to control the violation of primal feasibility constraints. Because the dual function in our problem is smooth, it is natural to conjecture that, hypothetically if is small, the violation of primal constraints at is also small, because is supposedly small due to Lipschitz continuity of gradients of . With strong duality is primal feasible, and therefore should be approximately feasible too.

While such an argument is intuitively correct, the regret it leads to is unfortunately sub-optimal asymptotically. It is difficult to explain the sub-optimality in a precise mathematical manner, but here we give a sketch of the calculations. With inexact gradients, it is possible to obtain a sub-optimal dual vector with sub-optimality gap upper bounded by after time periods. With strong smoothness and convexity of , this implies that is on the order of , indicating that on average violates primal feasibility constraints by an amount of . This shows that, the inventory of resources will be depleted with time periods still remaining, yielding a cumulative regret of which is significantly higher than the optimal regret of . Consequently, more refined control of primal feasibility violation in addition to near optimality of dual variables is needed, which is the main contribution of this paper summarized in the next section.

1.3 Summary of our contributions

Demand balancing in primal optimization. Our first contribution, as mentioned in the previous discussion, is to solve the problem of excessive primal feasible constraint violation. The idea of our method is the following. We shall now use to denote the price vectors and the price vector that maximizes the Lagrangian function at dual variable , which correspond to and notations in previous sections. It can be established that if then the violation of primal feasible constraints at is on the order of . We will need to implement additional measures to bring down such violation to the order of in order to achieve an optimal overall regret. To accomplish this, we borrow the idea of Linear Rate Control (LRC) from the full-information re-adjustment optimization literature (Jasin 2014) to carefully balance the demands realized at , so that the aggregated deviation from targeted resource consumption levels are de-biased to a level of instead of . Compared with the literature, a key challenge in our problem is that the demand is unknown so we cannot follow LRC directly which operates in the demand rate domain. Instead, we use local Taylor expansion to approximate the demand functions and adjust prices locally, which has a low-order of bias. We shall discuss more details of our method in Section 4.1.

Primal-dual gradient descent algorithm with near-optimal regret. Based on the technique of demand balancing in primal optimization, we propose a primal-dual optimization algorithm, named Primal-Dual NRM (PD-NRM), to solve NRM based on gradient descent. The structure of the algorithm is as follows. The time horizon is divided into epochs with exponentially growing lengths. At the beginning of each epoch , there is a dual variable fixed and the primal optimization aims to find the optimal price corresponding to . By combining gradient descent and the demand balancing technique, we can show that the primal optimization can find approximately optimal prices with minimal primal feasible constraint violations, which are further used to update the dual variable via (proximal) gradient descent. Our algorithm has the following advantages compared with the literature. First, we prove that our algorithm has a regret of , which slightly improves the best bound in the literature (i.e., in Miao & Wang 2021). It is also free from high-order regret terms , which appears in the regret bound Miao & Wang (2021) with quite heavy dimension dependency. Compared with Miao & Wang (2021), our algorithm is much more practical as it does not involve translating back and forth between the price and demand rate domain. Second, our algorithm is computationally efficient even with relatively large number of products (as we use gradient descent which is efficient even with large dimension) and long time horizon (as we only need to update the policy for time). Third, numerical experiments using the example in the literature (see e.g., Chen et al. 2019a) demonstrate that our algorithm is practical and effective, as it outperforms several benchmark algorithms selected from the related literature.

1.4 Other related works

We first review the literature of revenue management with demand learning that we did not mention in earlier subsections. Note that this literature review is only to illustrate some most related works of our paper, and we refer the interested readers to Bitran & Caldentey (2003), den Boer (2015), Chen & Chen (2015) for a comprehensive summary of this field. Let us first review the literature on revenue management with parametric demand learning. For instance, some earlier work such as Araman & Caldentey (2009), Farias & Van Roy (2010), Harrison et al. (2012) study this problem using Bayesian learning and updating. When there is resource inventory constraints, den Boer & Zwart (2015) study a modified certainty-equivalent pricing policy with near-optimal regret. When demand is nonparametric, Besbes & Zeevi (2015) show that using a simple linear model is sufficient to approximate the nonparametric demand which achieves near-optimal regret. If demand is further determined by some changing covariates in some nonparametric manner, Chen & Gallego (2021) proposes a “divide and approximate” learning approach with approximately optimal performance. Besides nonparametric and parametric demand, some paper also study the so-called semi-parametric model. For example, Nambiar et al. (2019) study the learning error of a semi-linear demand model of the format (where is the demand covariates) is approximated by linear demand; similar problem is studied in Bu et al. (2022) as well.

Another related stream of literature is on solving revenue management problem with approximate heuristics when demand information is known. The seminal paper by Gallego & Van Ryzin (1994, 1997) propose a fluid approximation heuristic with a static price charged throughout the time horizon, and this heuristic is proved to have regret . Following these two papers, many follow-up research focus on improving this fluid approximation heuristic by policy re-adjustment/re-solving. Besides Jasin (2014) we have mentioned earlier, another related paper is Chen et al. (2016) which propose a flexible adjustment approach with minimal price adjustments. Later on Wang & Wang (2020) show that such re-solving technique achieves constant regret, and shows that there is an optimality gap of between the optimal revenue and the fluid approximation revenue. Besides these paper which discuss the continuous price control, some other literature focus on the discrete decisions in revenue management such as whether the decision maker should accept or reject an order (see e.g., Cooper 2002, Reiman & Wang 2008, Secomandi 2008, Jasin & Kumar 2012, Bumpensanti & Wang 2020).

2 Problem Formulation and Assumptions

In the blind network revenue management problems, there are product types, resource types, and customers arrive sequentially over time periods. At the beginning of time period , a pricing algorithm posts a price vector , and when inventory is sufficient, receives realized demand . The expected demand given price is denoted as

| (1) |

with is an unknown demand rate function. Afterwards, a resource vector of is consumed, with being a known resource consumption matrix. Each resource type has a known initial inventory level . If the inventory of a resource type is completely depleted, we set almost surely (i.e., we allow a “shut-off” price for all ). 333Note that in practice, when only one resource type is depleted, products not using the depleted resource type could still be sold and the realized demand could be positive. Nevertheless, in this paper we adopt a “hard cutoff” model in which demand realization is completely halted once any resource type is depleted. This shall not affect the analysis of this paper because with high probability the designed algorithm will only exhaust resources near the very end of the time horizon .

2.1 Admissible policy and rewards

We first give the rigorous definition of an admissible policy in the sequential decision making problem.

Definition 2.1 (admissible policy)

A policy is admissible if it can be written as such that is measurable conditioned on the filtration of , and furthermore satisfies almost surely whenever a resource type requested by product is depleted at time .

To simplify our analysis, we will assume throughout this paper that almost surely for some constant , which is a common assumption in bandit and contextual bandit problems (Bubeck et al. 2012). Let be the class of all admissible policies. For any admissible policy , its expected reward is defined as

where . Let be the optimal policy. Then for any admissible policy , its cumulative regret is defined as

Clearly, for all admissible policy by definition, and the smaller the regret the better the designed policy is.

2.2 Assumptions

Throughout this paper we impose the following assumptions on the demand function, resource consumption matrix and other problem parameters.

Our first assumption concerns the demand function , one of the major problem specification that is unknown in advance and must be learnt on the fly through interactions with sequentially arriving customers.

[Assumptions on the demand curve] The domain of is and the image of is for some . Furthermore, is continuously differentiable on with bounded, Lipschitz continuous and non-degenerate Jacobians: for every , it holds that , and , where is the Jacobian matrix of , indicates the smallest singular value, and , are constants.

Assumption 2.2 gives quantitative specifications on the smoothness and invertibility of the multi-variate multi-value demand curve , which are standard assumptions in the literature. More specifically, Assumption 2.2 assumes that is continuously differentiable with its Jacobian matrix being Lipschitz continuous in matrix operator norm, and therefore the expected demand rates are smooth functions of the offered prices. On the other hand, Assumption 2.2 states that the Jacobian matrix of is non-degenerate with strictly positive least singular values, which implies that is invertible and the inverse function is Lipschitz continuous as well.

With Assumption 2.2, it is clear that is a bijection between and . Let be the inverse function of . Define the expected reward function as

Equivalently, we may also express the (expected) reward as a function of the demand rate vector , with the help of the inverse function of :

We impose the following conditions on the expected reward functions and : {assumption}[Assumptions on the total revenue] Both and are twice continuously differentiable, and for every and , it holds that , for some constants . Furthermore, is strongly concave in , meaning that for every , for some constant .

At a higher level, Assumption 2.2 assumes that the expected revenue is a smooth function of the offered prices and expected demand rates with Lipschitz continuous gradients, which is compatible with the smoothness of the demand curve itself as characterized in Assumption 2.2. Furthermore, Assumption 2.2 assumes that the expected revenue is strongly concave in the expected demand rates. The concavity of the expected total revenue as a function of demands rates is also a “regular” condition in asymptotic analysis of network revenue management problems, as it enables approximation through size-independent concave fluid approximation problems (Section 3.1, see also Gallego & Van Ryzin 1994, 1997). The work of Miao & Wang (2021) also analyzed several important demand classes and demonstrated that they satisfy Assumption 2.2 rigorously. Note that, importantly, we do not assume is strongly concave in the price vector , a condition frequently violated by common demand models such as the logistic demand or the exponential demand. However, for these demand models is indeed strongly concave in demand rates , as established in the work of Li & Huh (2011).

We next impose assumptions on initial inventory levels: {assumption}[Assumption on inventory levels] There exists such that scales linearly with time horizon , where and are constants. Assumption 2.2 states that the initial inventory levels of each resource type scales linearly (albeit with different slopes) with the time horizon , which is a conventional condition when asymptotic analysis (i.e. ) is carried out in inventory systems (Wang et al. 2014, Besbes & Zeevi 2012).

Finally, we impose the following condition on the resource consumption matrix . {assumption}[Assumption on resource consumption] The number of resource types is smaller than or equal to the number of product types . Furthermore, the resource consumption matrix satisfies and , where is the th largest singular value of , and and are constants.

Assumption 2.2 asserts that there are fewer (or equal number) of resource types compared to product types, and the matrix is bounded and has full row rank. For instance, if each resource type represents the inventory of each product itself, then we naturally have . In other applications such as selling modular products (e.g., laptops), different modules typically can be assembled into many more types of final products, leading to the fact that . Technically, we need the assumption that has full row rank (hence necessary to have ) to guarantee that the dual function is strongly convex, which is crucial to obtain the linear convergence of gradient descent. Unfortunately, our current analysis cannot handle the case when . Our conjecture is that we shall separately analyze the dual variable domain, which guarantees strong convexity of the dual function, and its complement, and we leave this as a future research opportunity.

Apart from the assumptions in blind network revenue management listed in this section, we also impose and discuss several technical assumptions in Section 3.3, which are better stated and discussed after the introduction of the fluid approximation problem and its dual problem, and their properties.

3 Fluid Approximation and the Dual Problem

In this section, we introduce the standard size-independent fluid approximation of the network revenue management problem, and its Lagrangian dual problem. Properties of the dual problem are also discussed, together with several additional technical assumptions facilitating our analysis.

3.1 Fluid approximation

Consider the following fluid approximation to the network revenue management problem:

where the operator is understood in an element-wise sense. Because is concave and the feasible region is linear, the fluid approximation can be reduced to

| (2) |

where . By the bijective nature of the demand curve , Eq. (2) is also equivalent to

| (3) |

though neither the objective function nor the feasible region of Eq. (3) is concave/convex.

The following proposition is standard in network revenue management, which shows that we can use the fluid approximation as a benchmark to bound the regret.

3.2 Dual problem

For a price vector and a dual vector , the Lagrangian of Eq. (3) is

| (4) |

Equivalently, for , define

| (5) |

Because is concave in and therefore has better properties, we shall deal with this Lagrangian whenever possible, though both forms of and are equivalent.

For a dual vector , let

| (6) |

be the price vector and its corresponding demand rate vector that maximizes the Lagrangian. Define the dual function

| (7) |

Note that Eq. (2) satisfies the Slater’s condition because the objective is concave, and all constraints are linear. Subsequently, the duality gap of this problem is zero:

Lemma 3.2 (strong duality)

Let be the optimal solution to Eq. (2). Then there exists such that , , and furthermore for any other .

Our second lemma shows that is twice continuously differentiable and strongly convex, whose proof can be found in Section 8 in the appendix.

3.3 Additional technical assumptions

We impose the following additional technical assumption on the primal and dual space. {assumption}[Assumption on primal dual space] There are known convex compact sets and and constants , , such that the following hold:

-

1.

, ;

-

2.

For every , and lies in the interior of ;

-

3.

For every , ; for every , ;

-

4.

For every with , for all , where .

Although we call all the conditions above as assumptions, we shall note that they are indeed about problem parameter designs. For instance, for the first two points in the assumption, we can always make the price range large enough such that is in the interior of the domain (hence so does ) for any . On the other hand, and are just some reasonable guess of the range of and respectively (as if is too large, any products using resource will have their prices equal to , implying have to be bounded).

4 Algorithm Design and Theoretical Results

In this section, we introduce the details of our proposed Algorithm PD-NRM, which consists of Algorithms 1-3. Before we go into details in the next several subsections, let us first introduce the high-level ideas of the proposed algorithm.

As we discussed in the introduction, our algorithm is based on a primal-dual framework with infrequent update for both dual and primal optimization. More specifically, the time horizon is divided into epochs with exponentially increasing lengths, each of which is used to update the dual variable. Besides the dual optimization which is our main algorithm, there are two sub-routines: PrimalOpt (which aims to calculate and gradient of dual function for any ) and GradEst (which is used to estimate the gradient of Lagrangian for any and do the demand balancing). We refer to Figure 1 for a graphic representation of our Algorithm PD-NRM.

From Figure 1, we can see the structure of Algorithm PD-NRM as well as how sub-routines are applied. In particular, for each epoch , PrimalOpt takes the dual variable as the input and its output helps to update the new dual variable , which will be used for the next epoch. To implement PrimalOpt, epoch is further divided into smaller epochs (to avoid confusion with the outer epoch, we call them loops) with exponentially increasing lengths again. In each loop , is the current price (for estimating ) which is an input of the sub-routine GradEst. GradEst runs through loop to estimate the gradient of the Lagrangian and balance the demand, and thus is updated at the end of loop .

In the next several subsections, we will discuss the details of each algorithm and their theoretical results. Since there are many learning parameters in the algorithms and technical lemmas, we summarize them in Table 1 including where they are specified, which parameters they depend on, and their asymptotic orders with respect to problem size and .

| Constants | Specified in … | Depending on … | Asymptotic order |

|---|---|---|---|

| Lemma 4.5 | |||

| Algorithm 2 | |||

| Algorithm 2 | |||

| Algorithm 1 | |||

| Lemma 4.5 | N/A | ||

| Lemma 4.6 | |||

| Lemma 4.6 | |||

| Lemmas 4.5, 4.6 | N/A | ||

| Lemma 4.6 | N/A | ||

| Lemma 4.6 | N/A |

Remark 4.1

Although Table 1 and the corresponding lemmas outline how to choose the learning parameters from a theoretical perspective, directly implementing such parameter values might be challenging or even impractical due to the numerical constants omitted in asymptotic notations. Fortunately, we show later on in our numerical experiments in Section 6 that some simple, ad-hoc parameter tuning is already sufficient to achieve reasonable performances, especially compared with other baseline and competing algorithms. This also shows that practical effectiveness and robustness of our proposed algorithm based on first-order methods. On the other hand, it is in general a challenging task to tune algorithm parameters in a data-driven way for machine learning and bandit learning algorithms for optimal practical performances, which we refer the readers to the works of Bardenet et al. 2013, Frazier 2018, Yang & Shami 2020 and would be an excellent topic for future research.

4.1 Gradient estimation and demand balancing

Our first sub-routine is presented in Algorithm 1, which accomplishes two goals simultaneously with an input of price vector , dual vector , sample budget (i.e., the length of the sub-routine), returns an estimated gradient and also performs demand balancing at .

The main idea of the algorithm is as follows. First, the length of the sub-routine is divided into two phases with equal length . In the first phase, we essentially uniformly sample around in order to estimate simultaneously. Such estimation method was first studied in the seminal work Nemirovskij & Yudin (1983), Flaxman et al. (2005), and has been applied in several works including Hazan & Levy (2014), Besbes et al. (2015), Chen & Shi (2023), Chen et al. (2019b), Miao & Wang (2021). However, simply implementing might violate the primal feasible constraints by too much, as discussed in Section 1.2, and this motivates our demand balancing which leads to a modified price . The balanced price is then applied in the second phase for another time periods.

-

1.

For every , ;

-

2.

For every , ;

-

3.

For every , ;

Now let us discuss the details of demand balancing and why we need it. By the algorithm design of Algorithm PD-NRM, whenever we are implementing GradEst, we have (with high probability), implying that by strong smoothness of the revenue and the fact that is an interior optimizer. Such difference in the revenue function will eventually lead to an eventual regret of (ignoring factor of ) which is exactly what we want, if we disregard the possible violation complementary slackness of inventory constraints. Unfortunately, when we take into account such violation it is challenging to obtain regret, as explained below:

-

1.

When resource is scarce (i.e., ), we need (if we only have the first phase in GradEst as we want ) in order to have the cumulative violation of the primal feasible constraints at most , so that the algorithm will not run out of inventory until time periods remain. However, this target is not possible because by Lipschitz continuity of and the fact that . This means that, the algorithm could potentially run out of inventory with approximately time periods still remaining, leading to a regret of .

-

2.

When the dual variable is non-zero, the total rewards collected by the algorithm might suffer if the actual resource consumption is far below the average inventory level as well. In such cases, though the algorithm is unlikely to run out of inventory (at least not on resource type ), the term in the Lagrangian function would be large meaning that is actually much smaller than . In other words, by consuming too little inventory for resource type whose inventory constraint in the fluid approximation is supposed to be binding, the regret of the algorithm also increases.

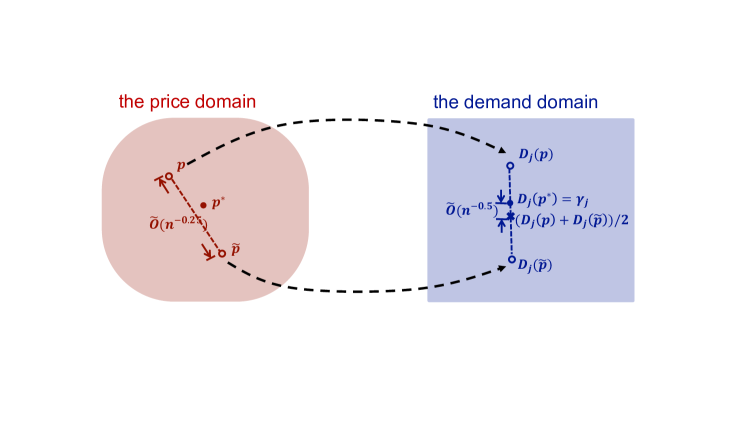

This figure depicts the demand balancing step on Line 10 of Algorithm 1 in both the price domain and the demand domain (for resource type whose inventory constraint in the fluid-approximation is binding). Note that in the price domain, the distance between and is on the order of which is the order of the estimation error between and . With the balancing step, the average consumption of resource type between and will be on the lower order of , thanks to the local Taylor expansion step that eliminates first-order error terms between and .

To resolve the above-mentioned challenges, we propose the following idea which we call demand balancing, with a graphical illustration given in Figure 2. The key idea is to “de-bias” the price offering so that the consumption of type- resource approximately matches its normalized inventory level , provided that is not too small. Instead of sampling around for the whole time horizon of periods, in the second phase, we can try to find another price such that for any ,

| (8) |

and apply for another time periods. Then we have the total primal violation in two phases is roughly equal to which is exactly what we want to achieve. However, since we only have access to the estimated and do not know for any other price either, we need to apply certain (estimated) local Taylor expansion of the demand curve in order to achieve (8), which is exactly the procedure in Line 10 of Algorithm 1.

In spirit, our idea of demand balancing is similar to the Linear Rate Control (LRC) in Jasin (2014), which is to re-adjust the fluid approximation policy under the full demand information. According to Jasin (2014), LRC re-adjusts the fluid price in order to de-bias the “error” of previous time periods, which means that whenever the realized cumulative demand of previous time periods goes up/down compared with the expected fluid demand , the price is adjusted up/down correspondingly. In our case, demand balancing aims to de-bias the “error” of in order to guarantee that on average the primal feasible constraints are approximately satisfied. As a result, besides unknown demand information, a key difference in demand balancing is that the error to de-bias does not come from the deviation between realized and expected demand, but from the estimation error of (hence ).

Next we introduce two technical lemmas which show the effectiveness of GradEst. First, the following lemma upper bounds the estimation error of the expected demand rates and its Jacobian .

Lemma 4.2

With probability the following hold:

-

1.

For every , ; furthermore, if then ;

-

2.

For every , ; furthermore, if then ;

-

3.

; furthermore, if then .

Our next lemma shows that, with high probability any feasible solution to the problem on Line 10 “balances” the demand at price towards the normalized target inventory level . It also shows that, when itself is not too far away from , feasibility of Line 10 is guaranteed.

Lemma 4.3

Suppose the GradEst sub-routine is executed with , and that for all . Jointly with the success events in Lemma 4.2, which occurs with probability , the following hold:

The second point of Lemma 4.3 basically says that whenever and are close to and , the feasibility problem in Line 10 is always feasible, which leads to the property in the first point of Lemma 4.3. As we discussed earlier, the conditions regarding and in the second property can be proved to hold with high probability whenever we invoke sub-routine GradEst. Therefore, we can almost guarantee to find satisfying the two inequalities in the first point. Regarding these two inequalities, we can immediately see that

approximately guarantees the primal feasible constraint of resource . On the other hand, the other inequality

is to guarantee the approximate strong duality of the algorithm. Notice that, in addition to the term that takes care of the stochastic error, there is an additional term that scales inverse linearly with on the lower bound side of the constraint. Intuitively, this enforces approximate complementary slackness and allows the resource consumption to be significantly lower than the initial inventory level provided that is close to zero, indicating a resource constraint that may not be binding at optimality. (At exact optimality, must be exactly zero if the constraint on resource type is not binding, but the lower bound in Lemma 4.3 allows non-zero but small dual variable values to accommodate for errors in dual optimization.)

4.2 Primal optimization

When the dual variable is given, the primal optimization procedure optimizes the penalized Lagrangian function

over . Note that is not necessarily concave in ; however, it satisfies the Polyak-Lojasiewicz (PL) inequality (Karimi et al. 2016) and is equipped with a quadratic decay property, as established in the following lemma:

Lemma 4.4

For every let , which belongs to thanks to Assumption 3.3. Then for any , it holds that

Furthermore, for any it holds that

Because of Lemma 4.4, we can essentially use gradient descent to optimize , and the proposed primal optimization method is presented in Algorithm 2. At a higher level, the algorithm carries out inexact gradient descent on , with gradients estimated by the GradEst sub-routine in Algorithm 1 with carefully chosen sample budget parameters as well as demand balancing being performed in the meantime. The effectiveness of Algorithm 2 is summarized in the next lemma, which upper bounds the (cumulative) errors of both Lagrangian objectives and violation of complementary slackness at all resource constraints.

Lemma 4.5

Suppose PrimalOpt is executed with , , , with , and . Then with probability it holds for every that

where is the constant specified in Assumption 3.3, is the constant specified on Line 4 in Algorithm 2; is the constant specified on Line 2 in Algorithm 1, and is the demand balancing price vector produced on Line 10 in Algorithm 1.

There are several implications of Lemma 4.5. When the dual variable is sufficiently close to (as reflected by , which can be proved to hold with high probability), the first three conclusions in Lemma 4.5 show that is close to , depending on how long the loop is, for every loop . As we have seen in Lemma 4.3, this proximity of price, together with , guarantees that there exists some feasible satisfying the two inequalities in Lemma 4.3. Then the last two conclusions in Lemma 4.5 are mainly from Lemma 4.3, which guarantee that in each loop the revenue of Algorithm 2 is approximately optimal (with gap at most ) and the primal feasible constraints are approximately satisfied (with violation at most ) as well.

4.3 Dual optimization and the main algorithm

In the previous two sub-sections, we introduced the two sub-routines GradEst and PrimalOpt which are used to solve the primal optimization to find in epoch (with dual variable ). In this subsection, we present a dual optimization DualOpt to minimize described in Algorithm 3. Together with the previous two sub-routines, they form Algorithm PD-NRM. For DualOpt, on the dual space we use the accelerated proximal gradient method with inexact gradient oracles to carry out updates of dual vectors .

Algorithm 3 describes a projected gradient descent method with inexact gradient estimates to optimize the dual problem, which serves as the entry point of the entire algorithm and is the outermost loop of the whole algorithm. More specifically, with the dual function being both strongly convex and smooth thanks to Lemma 3.3, and the feasible region of the dual vectors is , Algorithm 3 carries out a projected gradient descent with constant step sizes . For each iteration in the projected gradient descent, the gradient is the slack at the primal solution that optimizes the Lagrangian function with dual variables being , which is obtained by invoking the PrimalOpt procedure described in previous sections.

Next lemma is the last piece we need to prove the regret of Algorithm PD-NRM. In particular, it shows that for every epoch , is a sufficiently good estimator of in that with high probability, which is the condition we need in order to have Lemma 4.5 to hold.

Lemma 4.6

Suppose DualOpt is executed with , , , with , and . Then with probability the following hold for all iterations :

| (9) |

where and .

5 Regret analysis

The following theorem is our main result upper bounding the regret of Algorithm PD-NRM (Algorithm 1-3).

Theorem 5.1

From Theorem 5.1, we can see that the regret can be bounded above by , which slightly improves the best regret upper bound in the literature (see Miao & Wang 2021). On top of the regret improvement, our approach is much more practical as it uses gradient descent instead of ellipsoid method which is known to be empirically inefficient. Moreover, since Miao & Wang (2021) do the optimization on the demand rate domain, it involves translating back and forth between price and demand, which further makes the approach less effective. Mathematically, the overhead of translating back and forth between price and demand rate domains is reflected in an high-order regret term that is asymptotically but with a high-degree polynomial dependency on the problem dimension and , making the algorithm far less practical when the or (number of product or resource types) is not very small.

Now let us provide a proof sketch of Theorem 5.1, whose details can be found in Section 11 in the appendix. Essentially, there are two parts of the regret we need to bound: the cumulative revenue deviation from the optimal price (i.e., ), and the cumulative violation of the primal feasible/resource inventory constraints. Let us fix an epoch and a loop inside the epoch (and we denote these time periods as ), by Lemma 4.6 and Lemma 4.5, we have with high probability,

where is the price for demand balancing in GradEst. Combining with our choice of price perturbation factor in GradEst, we have

Since by algorithm design we have at most loops in each epoch and epochs, summing over all the loops and epochs, we have that

which lead to the final regret we want.

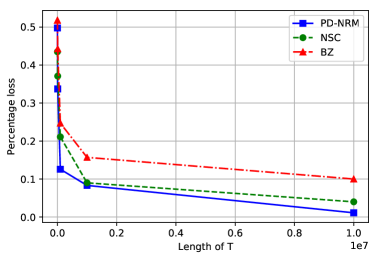

6 Numerical Experiment

In this section, we illustrate the numerical performance of our algorithm PD-NRM by comparing with two benchmark algorithms in the literature.

- •

-

•

NSC: This is the algorithm named Nonparametric Self-adjusting Control (NSC) proposed in Chen et al. (2019a), which essentially studies the same problem as in this paper but with stronger conditions.

Note that we did not study the performance of the algorithm in Chen & Shi (2023) because their regret with respect to is which is significantly worse than . On the other hand, the regret of NSC is for arbitrarily small is nearly the same as . As a result, we choose NSC over the algorithm in Chen & Shi (2023) as our main benchmark.

As an illustrative example, we take , , . The demand function is a logistic function defined as

and the range of price is set as . In this problem, we vary from to which means the initial inventory for each product is from to . To obtain the performance of our algorithm, we run 50 independent instances and take the average. To evaluate the performance of each algorithm, we use the percentage loss (of algorithm ) defined as . As we can see, this example is the same as the one used in Chen et al. (2019a). The only difference is the price sensitivity in Chen et al. 2019a which is instead of . However, with in the code of Chen et al. 2019a (we thank George Chen for providing their code), it is indeed equivalent to our example through normalization. As a result, for two benchmark algorithms, we simply use the results obtained in Chen et al. (2019a) directly.

To run Algorithm PD-NRM, it is important to tune the learning parameters illustrated in Table 1 for better empirical performance. While we recognize that optimal parameter tuning is non-trivial, we only did some ad-hoc manual tuning to obtain the parameters as in Table 2.

| Constants | Value |

|---|---|

| 1 | |

| 1 | |

| 1 |

The performance of all algorithms interms of percentage loss is summarized in Figure 3 and Table 3. From the results, we can see that our algorithm and NSC have better performance than BZ, while our algorithm also outperforms NSC in most of the cases. We shall note that the demand function we test is smooth so that NSC can be applied, and the dimension of our problem is only . According to Chen et al. (2019a), it uses spline approximation to estimate the nonparametric demand function , which requires a large number of base functions which is exponential in , while our algorithm does not have this issue.

| T= | BZ (%) | NSC (%) | PD-NRM (%) |

|---|---|---|---|

| 500 | 52.6 | 46.2 | 53.0 |

| 1,000 | 51.8 | 43.5 | 49.7 |

| 2,000 | 50.1 | 42.7 | 44.6 |

| 3,000 | 49.5 | 43.8 | 41.9 |

| 4,000 | 48.3 | 42.5 | 37.0 |

| 5,000 | 48.3 | 40.3 | 34.1 |

| 6,000 | 47.5 | 40.8 | 34.7 |

| 7,000 | 46.1 | 40.4 | 35.7 |

| 8,000 | 46.3 | 38.4 | 34.6 |

| 9,000 | 45.4 | 38.8 | 32.9 |

| 44.3 | 37.1 | 33.7 | |

| 24.7 | 21.1 | 12.5 | |

| 15.7 | 9.0 | 8.3 | |

| 10.0 | 4.0 | 1.1 |

7 Conclusion

This paper proposes a practical algorithm named PD-NRM to solve the classical blind NRM problem, which is based on a primal-dual optimization scheme. In particular, we use Lagrangian dual variables to relax the resource inventory constraints, and then search for an optimal price corresponding to the Lagrangian with fixed. The time horizon is divided into epochs with exponentially growing lengths for updating the dual variable; during each epoch, it is further divided into loops in a similar fashion for updating the price. More specifically, for both dual and primal optimization, we use some estimated (proximal) gradient descent for updating the decision variable, where the estimated gradients are outputs from the sub-routine PrimalOpt (see Algorithm 2) and GradEst (see Algorithm 1) respectively.

A key technical contribution of our paper is the demand balancing technique. In particular, we cannot simply apply the price we obtain from the estimated gradient descent in each loop because it may have significant violation of the resource inventory constraints due to the estimation error, which leads to sub-optimal regret in the end. To tackle that, we split each loop into two phases so that in the second phase, another price is computed to offset the violation of resource inventory constraint. With this technique, our algorithm PD-NRM is proved to have regret (see Theorem 5.1) which is, to the best of our knowledge, the best result in the literature.

There are a few future research directions people may explore. The first direction is a technical issue we discussed under Assumption 2.2: how do we design algorithms which achieve similar performance when or does not have full row rank. Another research direction is to investigate how we can generalize the idea of demand balancing technique to other (potentially more general) online resource-constrained optimization.

References

- Agrawal & Devanur (2016) Agrawal, S., & Devanur, N. (2016). Linear contextual bandits with knapsacks. Advances in Neural Information Processing Systems, 29.

- Agrawal & Devanur (2019) Agrawal, S., & Devanur, N. R. (2019). Bandits with global convex constraints and objective. Operations Research, 67(5), 1486–1502.

- Araman & Caldentey (2009) Araman, V. F., & Caldentey, R. (2009). Dynamic pricing for nonperishable products with demand learning. Operations Research, 57(5), 1169–1188.

- Badanidiyuru et al. (2018) Badanidiyuru, A., Kleinberg, R., & Slivkins, A. (2018). Bandits with knapsacks. Journal of the ACM, 65(3), 1–55.

- Balseiro et al. (2023) Balseiro, S., Lu, H., & Mirrokni, V. (2023). The best of many worlds: Dual mirror descent for online allocation problems. Operations Research (to appear).

- Bardenet et al. (2013) Bardenet, R., Brendel, M., Kégl, B., & Sebag, M. (2013). Collaborative hyperparameter tuning. In International conference on machine learning, (pp. 199–207). PMLR.

- Bertsekas (1997) Bertsekas, D. P. (1997). Nonlinear programming. Journal of the Operational Research Society, 48(3), 334–334.

- Besbes et al. (2015) Besbes, O., Gur, Y., & Zeevi, A. (2015). Non-stationary stochastic optimization. Operations Research, 63(5), 1227–1244.

- Besbes & Zeevi (2012) Besbes, O., & Zeevi, A. (2012). Blind network revenue management. Operations Research, 60(6), 1537–1550.

- Besbes & Zeevi (2015) Besbes, O., & Zeevi, A. (2015). On the (Surprising) Sufficiency of Linear Models for Dynamic Pricing with Demand Learning. Management Science, 61(4), 723–739.

- Bitran & Caldentey (2003) Bitran, G., & Caldentey, R. (2003). An overview of pricing models for revenue management. Manufacturing & Service Operations Management, 5(3), 203–229.

- Broder & Rusmevichientong (2012) Broder, J., & Rusmevichientong, P. (2012). Dynamic pricing under a general parametric choice model. Operations Research, 60(4), 965–980.

- Bu et al. (2022) Bu, J., Simchi-Levi, D., & Wang, C. (2022). Context-based dynamic pricing with partially linear demand model. Advances in Neural Information Processing Systems, 35, 23780–23791.

- Bubeck et al. (2012) Bubeck, S., Cesa-Bianchi, N., et al. (2012). Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends® in Machine Learning, 5(1), 1–122.

- Bubeck et al. (2021) Bubeck, S., Eldan, R., & Lee, Y. T. (2021). Kernel-based methods for bandit convex optimization. Journal of the ACM, 68(4), 1–35.

- Bumpensanti & Wang (2020) Bumpensanti, P., & Wang, H. (2020). A re-solving heuristic with uniformly bounded loss for network revenue management. Management Science, 66(7), 2993–3009.

- Chen & Chen (2015) Chen, M., & Chen, Z.-L. (2015). Recent developments in dynamic pricing research: multiple products, competition, and limited demand information. Production and Operations Management, 24(5), 704–731.

- Chen & Gallego (2021) Chen, N., & Gallego, G. (2021). Nonparametric pricing analytics with customer covariates. Operations Research, 69(3), 974–984.

- Chen et al. (2016) Chen, Q., Jasin, S., & Duenyas, I. (2016). Real-time dynamic pricing with minimal and flexible price adjustment. Management Science, 62(8), 2437–2455.

- Chen et al. (2019a) Chen, Q., Jasin, S., & Duenyas, I. (2019a). Nonparametric self-adjusting control for joint learning and optimization of multiproduct pricing with finite resource capacity. Mathematics of Operations Research, 44(2), 601–631.

- Chen et al. (2019b) Chen, X., Wang, Y., & Wang, Y.-X. (2019b). Nonstationary stochastic optimization under -variation measures. Operations Research, 67(6), 1752–1765.

- Chen & Shi (2023) Chen, Y., & Shi, C. (2023). Network revenue management with online inverse batch gradient descent method. Production and Operations Management (to appear).

- Cooper (2002) Cooper, W. L. (2002). Asymptotic behavior of an allocation policy for revenue management. Operations Research, 50(4), 720–727.

- Danskin (2012) Danskin, J. M. (2012). The theory of max-min and its application to weapons allocation problems, vol. 5. Springer Science & Business Media.

- den Boer (2015) den Boer, A. V. (2015). Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in Operations Research and Management Science, 20(1), 1–18.

- den Boer & Zwart (2015) den Boer, A. V., & Zwart, B. (2015). Dynamic pricing and learning with finite inventories. Operations research, 63(4), 965–978.

- Farias & Van Roy (2010) Farias, V. F., & Van Roy, B. (2010). Dynamic pricing with a prior on market response. Operations Research, 58(1), 16–29.

- Ferreira et al. (2018) Ferreira, K. J., Simchi-Levi, D., & Wang, H. (2018). Online network revenue management using thompson sampling. Operations Research, 66(6), 1586–1602.

- Flaxman et al. (2005) Flaxman, A. D., Kalai, A. T., & McMahan, H. B. (2005). Online convex optimization in the bandit setting: gradient descent without a gradient. In Proceedings of the 16th annual ACM-SIAM Symposium on Discrete Algorithms (SODA), (pp. 385–394).

- Frazier (2018) Frazier, P. I. (2018). A tutorial on bayesian optimization. arXiv preprint arXiv:1807.02811.

- Gallego & Van Ryzin (1994) Gallego, G., & Van Ryzin, G. (1994). Optimal dynamic pricing of inventories with stochastic demand over finite horizons. Management Science, 40(8), 999–1020.

- Gallego & Van Ryzin (1997) Gallego, G., & Van Ryzin, G. (1997). A multiproduct dynamic pricing problem and its applications to network yield management. Operations Research, 45(1), 24–41.

- Harrison et al. (2012) Harrison, J. M., Keskin, N. B., & Zeevi, A. (2012). Bayesian dynamic pricing policies: Learning and earning under a binary prior distribution. Management Science, 58(3), 570–586.

- Hazan & Levy (2014) Hazan, E., & Levy, K. (2014). Bandit convex optimization: Towards tight bounds. Advances in Neural Information Processing Systems (NeurIPS), 27, 784–792.

- Jasin (2014) Jasin, S. (2014). Reoptimization and self-adjusting price control for network revenue management. Operations Research, 62(5), 1168–1178.

- Jasin & Kumar (2012) Jasin, S., & Kumar, S. (2012). A re-solving heuristic with bounded revenue loss for network revenue management with customer choice. Mathematics of Operations Research, 37(2), 313–345.

- Karimi et al. (2016) Karimi, H., Nutini, J., & Schmidt, M. (2016). Linear convergence of gradient and proximal-gradient methods under the polyak-łojasiewicz condition. In Joint European Conference on Machine Learning and Knowledge Discovery in Databases (ECML/PKDD), (pp. 795–811). Springer.

- Khachiyan (1979) Khachiyan, L. G. (1979). A polynomial algorithm in linear programming. In Doklady Akademii Nauk, vol. 244, (pp. 1093–1096). Russian Academy of Sciences.

- Lei et al. (2015) Lei, Y. M., Jasin, S., & Sinha, A. (2015). Multidimensional bisection search for constrained optimization with noisy observations. Working Paper.

- Li & Huh (2011) Li, H., & Huh, W. T. (2011). Pricing multiple products with the multinomial logit and nested logit models: Concavity and implications. Manufacturing & Service Operations Management, 13(4), 549–563.

- Miao & Wang (2021) Miao, S., & Wang, Y. (2021). Network revenue management with nonparametric demand learning:sqrt T-regret and polynomial dimension dependency. Available at SSRN 3948140.

- Miao et al. (2021) Miao, S., Wang, Y., & Zhang, J. (2021). A general framework for resource constrained revenue management with demand learning and large action space. Available at SSRN 3841273.

- Nambiar et al. (2019) Nambiar, M., Simchi-Levi, D., & Wang, H. (2019). Dynamic learning and pricing with model misspecification. Management Science, 65(11), 4980–5000.

- Nedić & Ozdaglar (2009) Nedić, A., & Ozdaglar, A. (2009). Approximate primal solutions and rate analysis for dual subgradient methods. SIAM Journal on Optimization, 19(4), 1757–1780.

- Nemirovskij & Yudin (1983) Nemirovskij, A. S., & Yudin, D. B. (1983). Problem complexity and method efficiency in optimization.

- Nesterov (2009) Nesterov, Y. (2009). Primal-dual subgradient methods for convex problems. Mathematical Programming, 120(1), 221–259.

- Reiman & Wang (2008) Reiman, M. I., & Wang, Q. (2008). An asymptotically optimal policy for a quantity-based network revenue management problem. Mathematics of Operations Research, 33(2), 257–282.

- Schmidt et al. (2011) Schmidt, M., Roux, N., & Bach, F. (2011). Convergence rates of inexact proximal-gradient methods for convex optimization. Advances in neural information processing systems, 24.

- Secomandi (2008) Secomandi, N. (2008). An analysis of the control-algorithm re-solving issue in inventory and revenue management. Manufacturing & Service Operations Management, 10(3), 468–483.

- Tropp (2012) Tropp, J. A. (2012). User-friendly tail bounds for sums of random matrices. Foundations of Computational Mathematics, 12(4), 389–434.

- Vaidya (1996) Vaidya, P. M. (1996). A new algorithm for minimizing convex functions over convex sets. Mathematical programming, 73(3), 291–341.

- Wang et al. (2021) Wang, Y., Chen, B., & Simchi-Levi, D. (2021). Multi-modal dynamic pricing. Management Science, 67(10), 6136–6152.

- Wang & Wang (2020) Wang, Y., & Wang, H. (2020). Constant regret re-solving heuristics for price-based revenue management. arXiv preprint arXiv:2009.02861.

- Wang et al. (2014) Wang, Z., Deng, S., & Ye, Y. (2014). Close the gaps: A learning-while-doing algorithm for single-product revenue management problems. Operations Research, 62(2), 219–482.

- Yang & Shami (2020) Yang, L., & Shami, A. (2020). On hyperparameter optimization of machine learning algorithms: Theory and practice. Neurocomputing, 415, 295–316.

Supplementary material: proofs of technical lemmas

8 Proof of results in Section 3

8.1 Proof of Lemma 3.3

When lies in the interior of , the maximizing is unique because is strongly concave. The formula of is then a direct consequence of the Danskin-Bertsekas theorem (Danskin 2012, Bertsekas 1997).

We next derive the Hessian of . Because lies in the interior of , we have that , which holds for a neighborhood of as well. Define . By the chain rule and inverse function theorem,

which is to be proved.

9 Proofs of results in Section 4.1

9.1 Proof of Lemma 4.2

By vector Hoeffding’s inequality (Tropp 2012) and the fact that almost surely, it holds with probability that

| (10) |

On the other hand, by Assumption 2.2 the Jacobian of is Lipschitz continuous, and therefore by the mean-value theorem, for every ,

| (11) |

Combining Eqs. (10,11) and noting that the terms in Eq. (11) are canceled out, we prove the first property of Lemma 4.2.

Next fix . Dividing both sides of Eq. (11) by , we obtain

| (12) |

Similarly, dividing both sides of Eq. (10) by (for a particular ) we obtain

| (13) |

Combining Eqs. (12,13) we prove the second property of Lemma 4.2.

Finally we prove the third property. Fix an arbitrary . By the mean-value theorem and Assumption 2.2,

| (14) |

Dividing both sides of Eq. (14) and do a differentiation at minus , we obtain

| (15) |

On the other hand, note that , and that almost surely. By Hoeffding’s inequality, it holds with probability that

Dividing both sides of the above inequality by and do a differentiation at minus , we obtain

| (16) |

Combining Eqs. (15,16) and extend to all product types we complete the proof of the third property.

9.2 Proof of Lemma 4.3.

Let be any price vector feasible to Line 10 and fix . By the mean-value theorem, there exists such that . Using the Lipschitz continuity of in Assumption 2.2, we obtain

| (17) |

On the other hand, invoking Lemma 4.2 and noting that with satisfying the conditions in Lemma 4.3, we have that

| (18) | ||||

| (19) |

Combine Eqs. (17,18,19) and note that . We have

| (20) |

and therefore

| (21) |

because thanks to Assumption 2.2. The first property in Lemma 4.3 is then proved by applying the Cauchy-Schwarz inequality.

We next prove the second property. Construct , which satisfies the first constraint on Line 10, , by the condition that . Applying the mean-value theorem at and using the Lipschitz continuity of thanks to Assumption 2.2, it holds that

| (22) | ||||

| (23) |

With , combining Eqs. (22,23) we obtain

| (24) |

This together with Eq. (21) and the fact that since is primal feasible, establishes that the second constraint on Line 10 is satisfied.

We next establish the third constraint. If , then by complementary slackness and therefore the third constraint is satisfied, by a simple symmetric argument. Now consider any with . Because is convex, we have that . On the other hand, because since thanks to primal feasibility, and whenever , we know that for all . Hence, , which implies

| (25) |

Combining Eq. (25) with Eqs. (24,21) we established that the third constraint on Line 10 is feasible too.

10 Proofs of results in Section 4.2

10.1 Proof of Lemma 4.4

Let , and recall the definition that . By the chain rule, we have that

| (26) |

Hence,

| (27) |

where the last inequality holds because is square and thanks to Assumption 2.2. On the other hand, note that is smooth and -strongly concave in , thanks to Assumption 2.2. Also, is an interior maximizer thanks to Assumption 3.3, which implies . Subsequently, for some it holds that

| (28) |

Combining Eqs. (27,28) we complete the proof of the first inequality.

10.2 Proof of Lemma 4.5

We first prove the upper bound on . Let be the error of gradient estimation at iteration , and be its magnitude. Note that has Lipschitz continuous gradients, or more specifically for any ,

| (31) |

where the last inequality holds thanks to Assumptions 2.2, 2.2, and the definition that . Subsequently, by the mean-value theorem it holds that, for some ,

| (32) |

Note that, with . We have that

| (33) | ||||

| (34) |

Incorporating Eqs. (33,34) into Eq. (32), we obtain

| (35) |

With , Eq. (32) can be simplified to

| (36) |

Using the PL inequality established in Lemma 4.4, Eq. (36) is further simplified to

| (37) |

Let and . Re-arranging terms in Eq. (37), we obtain

| (38) |

Expanding Eq. (38) all the way to , we obtain for every that

| (39) |

Note that for , thanks to Assumption 3.3. Hence, , where . Note also that because is an interior maximizer thanks to Assumption 3.3, and thanks to Assumption 2.2, we have . This means that we can simply take as an upper bound of without affecting our analysis.

With the choice for sufficiently large (we will calculate precisely the value of later) so that at iteration in the GradEst sub-routine, Lemma 4.2 implies that with probability ,

where . Subsequently,

Subsequently, the above inequality together with Eq. (39) yields

| (40) |

Note that the total number of iterations is upper bounded by . With the choice of such that

| (41) |

and noting that for all , and that , the second term in Eq. (40) is upper bounded by . Consequently,

| (42) |

where the last inequality is due to the definition of . This proves the first property in Lemma 4.5. Invoking the quadratic growth property in Lemma 4.4, the above inequality is further simplified to

| (43) |

which proves the second property in Lemma 4.5.

To prove the third property, note that Eqs. (40,41) together imply that for all . Hence, by Lemma 4.4 it holds that

where is the constant specified in Assumption 3.3. The third property of Lemma 4.5 is then implied by the fourth item in Assumption 3.3.

With the choice of

and the third property, it holds that in the invocation of GradEst.

We next focus on the last two properties in Lemma 4.5. With the choices that and , together with the stopping rule of for some , it is easy to check through Eq. (43) that , and that . By Lemma 4.3, this implies that, with probability , the problem on Line 10 in the GradEst sub-routine is feasible, and therefore with high probability satisfies all properties listed in Lemma 4.3. More specifically,

which establishes the last property in Lemma 4.5. Finally, to prove the second to last inequality, note that for any , . Subsequently,

| (44) | |||

| (45) | |||

| (46) | |||

| (47) | |||

| (48) |

Here, Eq. (44) holds by the definition that , and that thanks to strong duality as established in Lemma 3.2; Eq. (45) holds because is smooth and is its interior maximizer, yielding and therefore with Eq. (31) and the mean-value theorem,

Eq. (46) holds because by the choice of parameter , with high probability, and thanks to the constraint on Line 10 of Algorithm 1; Eq. (47) holds by invoking the first property in Lemma 4.3, and noting that . This proves the fourth property in Lemma 4.5.

10.3 Proof of Lemma 4.6

To prove the lemma, we first present a technical result upper bounding a properly average sub-optimality gaps of proximal gradient descent when gradients contain errors.

Lemma 10.1

At a higher level, Lemma 10.1 is similar to (Schmidt et al. 2011, Proposition 3), analyzing proximal gradient descent with inexact gradients. However, Proposition 3 of Schmidt et al. (2011) only upper bounds the distance between and in -norm, which is insufficient for our purpose because our may well lie on the boundary of (e.g., in the form of non-binding inventory constraints for certain resource types). Instead, here in Lemma 10.1 we directly prove upper bounds on the sub-optimality gap, via a proper averaging argument.

We now carry out the proof by an inductive argument on the iteration . For , the conclusion that and clearly holds because

because and for all . We next prove the desired properties for iteration , assuming they hold for iteration .

Note that for iteration in Dual-Opt, the last iteration in Primal-Opt satisfies , where . By inductive hypothesis, all conditions in Lemma 4.5 are met and therefore with probability it holds that

| (49) |

where . By Lemma 4.2, it also holds with probability that

| (50) |

where is the constant defined in the GradEst sub-routine. Subsequently,

| (51) |

Note that, by inductive hypothesis, Eq. (51) holds with replaced by for all prior iterations as well.

Invoke Lemma 10.1 and incorporate the upper bounds on for in Eq. (51). We have for iteration that

| (52) |

where . For notational simplicity, denote , and , so that for all . Incorporating Eq. (51), Eq. (52) is simplified to

| (53) |

Here, Eq. (53) holds because almost surely. With the choice that 444Note the choice of earlier and later, holds.

both terms on the right-hand side in Eq. (53) can be upper bounded by separately. Subsequently,

| (54) |

Note that

Note also that for all thanks to the optimality of . Subsequently, Eq. (54) is reduced to

| (55) |

With the choice that

we have that , which is to be proved.

In the remainder of this section we present the proof of Lemma 10.1.

Proof 10.2

Proof of Lemma 10.1. Let . By Lemma 3.3, is -strongly smooth and -strongly convex, meaning that and for any . Let also be the condition number of .

Note that , where . Let . It is easy to verify that is continuously differentiable and -strongly convex. By Line 7 in Algorithm 3, we know that . The first-order KKT condition yields that for all , and furthermore by the strong convexity of it holds that for all . Subsequently,

| (56) |

On the other hand, because is continuously differentiable with -Lipschitz continuous gradients, it holds that

| (57) |

Additionally, using the definition of , we have for every that

| (58) |

where in Eq. (58) we use the convexity of and the Cauchy-Schwarz inequality. Combining Eqs. (56,57,58) and using the fact that , we obtain

| (59) |

Next, recall the definition of the averaging coefficients that , so that and . Invoking Eq. (59) and setting , we have

| (60) |

Summing both sides of Eq. (60) over and telescoping, we obtain

| (61) |

Now, let , and for . From Eq. (61), it is easy to verify that for all , and . Let and for all , so that and is non-negative and non-decreasing. Then, for all ,

and therefore

Summing both sides of the above inequality over , we obtain

Subsequently,

| (62) |

11 Proof of results in Section 5

11.1 Proof of Theorem 5.1

Note that to prove Theorem 5.1, it suffices to upper bound the cumulative deviation from the optimal price , as well as the cumulative “over-demand” so that the inventory of all resources will not be depleted too early. Fix an iteration in DualOpt and an iteration in PrimalOpt, and let be the set of time periods, which satisfies . Let also be the input of GradEst. For the first half of (denoted as , we have for some that

| (64) | ||||

| (65) | ||||

| (66) |

Here, the second inequality of Eq. (64) holds by the Taylor expansion of at with Lagrange remainders; the second inequality of Eq. (65) holds because for all , thanks to Assumption 2.2; the first inequality in Eq. (66) holds because , thanks to the third property of Lemma 4.5.

Similarly, the expected resource consumptions over the first half of can be analyzed as

| (67) |

Next, let be the second half of , where the price vectors are committed to for all , with being obtained on Line 10 in the GradEst sub-routine. By Lemma 4.5, it holds with probability that

| (68) | ||||

| (69) |

Combine Eqs. (66,67,68,69). We obtain

| (70) | ||||

| (71) |

with

Let be the last iteration in DualOpt, and be the last iteration in PrimalOpt when the outer iteration in DualOpt is . It is easy to verify that and almost surely for all , where . Note also that . Subsequently, applying Cauchy-Schwarz inequality, Eqs. (70,71) lead to

| (72) | ||||

| (73) |

where

Note that Eq. (73) together with and the Hoeffding-Azuma’s inequality, implies that inventory will not be depleted until the last time periods, during which an amount of revenue per period might be lost due to insufficient resources. Subsequently, the total regret can be upper bounded by

which is to be proved.