Polynomial Graphical Lasso: Learning Edges from Gaussian Graph-Stationary Signals

Abstract

This paper introduces Polynomial Graphical Lasso (PGL), a new approach to learning graph structures from nodal signals. Our key contribution lies in modeling the signals as Gaussian and stationary on the graph, enabling the development of a graph-learning formulation that combines the strengths of graphical lasso with a more encompassing model. Specifically, we assume that the precision matrix can take any polynomial form of the sought graph, allowing for increased flexibility in modeling nodal relationships. Given the resulting complexity and nonconvexity of the resulting optimization problem, we (i) propose a low-complexity algorithm that alternates between estimating the graph and precision matrices, and (ii) characterize its convergence. We evaluate the performance of PGL through comprehensive numerical simulations using both synthetic and real data, demonstrating its superiority over several alternatives. Overall, this approach presents a significant advancement in graph learning and holds promise for various applications in graph-aware signal analysis and beyond.

Index Terms:

Network-topology inference, graph learning, Gaussian signals, graph stationary signals, covariance estimation.I Introduction

Modern datasets often exhibit an irregular non-Euclidean support. In such scenarios, graphs have emerged as a pivotal tool, facilitating the generalization of classical information processing and structured learning techniques to irregular domains. Today, there is a wide range of applications that leverage graphs when processing, learning, and extracting knowledge from their associated datasets (see, e.g., problems in the context of electrical, communication, social, geographic, financial, genetic, and brain networks [2, 3, 4, 5, 6], to name a few). When using graphs to process structured non-Euclidean data, it is usually assumed that the underlying network topology is known. Unfortunately, this is not always the case. In many cases, the structure of the graph is not well defined, either because there is no underlying physical network or because the (best) metric to assess the level of association between the nodes is not known.

Since in most cases the existing relationships are not known beforehand, the standard approach is to infer the structure of the network from a set of available nodal observations/signals/features. To estimate the interactions between the existing nodes, the first step is to formally define the relationship between the topology of the graph and the properties of the signals defined on top of it. Early graph topology inference methods [7, 8] adopted a statistical approach, such as the correlation network [2, Ch. 7.3.1], partial correlations, or Gaussian Markov random fields (GMRF), with the latter leading to the celebrated graphical Lasso (GL) scheme [9, 2]. Partial correlation methods have been generalized to nonlinear settings [10]. Also in the nonlinear realm, less rigorous approaches simply postulate a similarity scores, with links being drawn if their score exceeds a given threshold. In recent years, graph signal processing (GSP) based models [11, 12, 13] have brought new ideas to the field, considering more complex relationships between the signals and the sought graph. These approaches have been generalized to deal with more complex scenarios that often arise in practice, such as the presence of hidden variables [14, 15, 16] or the simultaneous inference of multiple networks [17, 18].

The existing graph-learning methods exhibit different pros and cons, with relevant tradeoffs including computational complexity, expressiveness, model accuracy, or sample complexity, to name a few. For instance, correlation networks need very few samples and can be run in parallel for each pair of nodes, but fail to capture intermediation nodal effects. On the other hand, GL (a maximum likelihood estimator for GMRF) can handle the intermediation effect while still requiring a relatively small number of samples compared to the size of the network. Some disadvantages of GL include assuming a relatively simple signal model (failing to deal with, e.g., linear autoregressive network models) and forcing the learned graph to be a positive definite matrix. To overcome some of these issues, [13] proposed a more general model that assumed that the signals were stationary in the network (GSR) or, equivalently, that the covariance matrix can be defined as a polynomial of the adjacency of the graph [19]. Since GSR is a more general model, it is less restrictive in terms of the signals it can handle. However, it has the disadvantage of requiring a significantly larger number of observations than GL [13].

Our proposal is to combine the advantages of assuming Gaussianity, which implies solving a maximum likelihood problem that requires fewer node observations, with the larger generality of graph-stationary approaches. Our ultimate goal is to generalize the range of scenarios where GL can be used, while keeping the number of observations and computational complexity under control. To be more precise, we introduce Polynomial Graphical Lasso (PGL), a new scheme to learn graphs from signals that works under the assumption that the samples are Gaussian and graph stationary, so that the covariance (precision) matrix of the observations can be written as a polynomial of a sparse graph. These assumptions give rise to a constrained log-likelihood minimization that is jointly optimized over the precision and adjacency matrices, with GL being a particular instance of our problem. The price to pay is that the postulated optimization, even after relaxing the sparsity constraints, is more challenging, leading to a biconvex problem. To mitigate this issue we provide an efficient alternating algorithm with convergence guarantees.

Contributions. To summarize, our main contributions are:

-

•

Introducing PGL, a novel graph-learning scheme that, by assuming that the observations are Gaussian and graph-stationary, generalizes GL and is able to learn a meaningful graph structure in scenarios where the precision/covariance matrices are polynomials of the sparse matrix that represents the graph.

-

•

Formulating the inference problem as a biconvex constrained optimization, with the variables to optimize being the precision matrix and the graph. While our focus is on learning the graphs, note that this implies that PGL can also be used in the context of covariance estimation.

-

•

Developing an efficient algorithm to solve the proposed optimization, together with convergence guarantees to a stationary point (block coordinatewise minimizer).

-

•

Evaluating the performance of the proposed approach through comparisons with alternatives from the literature on synthetic and real-world datasets.

Outline. The remainder of the paper is organized as follows. Section II surveys the basic graph and GSP background, placing special emphasis on the concepts of graph stationarity and Gaussian graph signals. In Section III, the problem of learning (inferring) graphs from signals under different assumptions on the observations is formally stated. Section IV presents a computationally tractable relaxation of the graph-learning problem, along with an efficient algorithm and its associated convergence guarantees. Section V quantifies and compares the recovery performance of the proposed approach with other methods from the literature using both synthetic and real data. Section VI closes the paper with concluding remarks.

II Graphs and Random Graph Signals

This section introduces the notation used in the paper and fundamental concepts of graphs and GSP that will help to explain the relationship between the available signals and the topology of the underlying graph.

Notation. We represent scalar, vectors and matrices using lowercase (), bold lowercase (), and bold uppercase () letters, respectively. represents the values of the entry of matrix . denotes the identity matrix of size . The expression diag() represents a diagonal matrix with the values of in the diagonal. The expressions and refer to the entry-wise (vectorized) and matrix norms, and , and is the Frobenious norm.

Graphs. Let be a weighted and undirected graph with nodes, where and denote the vertex and edge set, respectively. The topology of the graph is encoded in the sparse, weighted adjacency matrix , where represents the weight of the edge between nodes and , and if and are not connected. A more general representation of the graph is the Graph Shift Operator (GSO), denoted by , where if and only if or . Common choices for the GSO are the adjacency matrix [20], the combinatorial graph Laplacian [4], and their degree-normalized variants. Since the graph is undirected, the GSO is symmetric and can be diagonalized as , where the orthogonal matrix contains the eigenvectors of the GSO, and the diagonal matrix contains its eigenvalues.

Graph signals and filters. A graph signal is represented by a vector , where denotes the signal value observed at node . Alternatively, a graph signal can be understood as a mapping, so that the signal values can represent features associated with the node at hand. Graph filters provide a flexible tool for either processing or modeling the relationship between a signal and its underlying graph . Succinctly, a graph filter is a linear operator that takes into account the topology of the graph and is defined as a polynomial of the GSO of the form

| (1) |

where represent the filter coefficients, and and are the eigenvectors and eigenvalues of the GSO respectively. Since is a polynomial of , it readily follows that both matrices have the same eigenvectors .

Stationary graph signals. A graph signal is defined to be stationary on the graph if it can be expressed as the output of a graph filter excited by a zero-mean white signal [19, 21, 22]. In other words, if has a covariance of , and , then the covariance of is . This reveals that assuming that is stationary on is equivalent to saying that the covariance matrix can be written as a polynomial of the GSO , and that, as a result, and have the same eigenvectors [cf. (1)]. Hence, graph stationarity implies that the matrices and commute, which is a significant property to be exploited later on.

Gaussian graph signals. A Gaussian graph signal is an -dimensional random vector whose (vertex-indexed) entries are jointly Gaussian. Hence, if is distributed as , we have that both the covariance matrix and the precision matrix are matrices whose entries capture statistical relationships between the nodal values. In particular, using the distribution of the Gaussian, it holds that:

| (2) |

demonstrating that, in the context of graph signals, the entries of account for conditional dependence relationships between the (features of the) nodes of the graph [7].

Suppose now that we have a collection of Gaussian signals each of them independently drawn from the distribution in (2). The log-likelihood associated with is

| (3) |

This expression will be exploited when formulating our proposed inference approach and establishing links with classical methods.

III Graph learning problem formulation

This section begins with a formal definition of the graph learning problem, followed by an explanation of some common approaches used in the literature to tackle this problem. Afterwards, we proceed to formalize the learning problem we aim to address and cast it as an optimization problem. We then provide an overview of the key features of our formulation and conduct a comparative analysis with the two closest approaches available in the literature.

To formally state the graph learning problem, let us recall that we assume: i) is an undirected graph with nodes, ii) there is a random process associated with , and iii) we denote by a collection of independent realizations of such a process. The goal in graph learning is to use a given set of nodal observations to find the (estimates of the) links/associations between the nodes in the graph (i.e., use to estimate the associated with ).

This problem has been addressed under different approaches [23, 24, 19]. Differences among these models typically arise from the underlying assumptions that are made regarding 1) the graph, which almost universally entails just considering that the graph is sparse (see, e.g., [25] for a recent exception), 2) the signals, which assume certain properties related to the nature of the signals such as smoothness [24] or Gaussianity, [23] among others, and 3) the relationship between the graph and the signal, such as the stationarity property [19].

The model we propose aims to incorporate several assumptions about both the graph and the graph signals. To that end, we propose an approach for which we assume that: 1) the graph is sparse, 2) the signals are Gaussian and, 3) the signals are stationary in the underlying graph.

Having established these assumptions, we now proceed to formally state our graph learning problem as follows

Problem 1 Given a set of signals , find the underlying sparse graph structure encoded in under the assumptions:

(AS1): The graph signals are i.i.d. realizations of .

(AS2): The graph signals are stationary in .

Our approach is to recast Problem 1 as the following optimization

| (4) |

where is a generic set representing additional constraints that is known to satisfy (e.g., the GSO being symmetric and its entries being between zero and one). The minimization takes as input the sample covariance matrix and generates as output the estimate for and, as a byproduct, the estimate for . For the problem in (III), we require to be positive semidefinite. This constraint arises because is the inverse of which is symmetric and positive definite by construction. Consequently, inherits the properties of being symmetric and positive semidefinite.

Next, we explain the motivation for each term in (III) with special emphasis on the constraint , which is a fundamental component of our approach.

-

•

The first two terms in the objective function are due to (AS1) and arise from minimizing the negative log-likelihood expression in (3). Indeed, it is clear that substituting (2) into (3) yields

Since constants are irrelevant for the optimization, we drop the first term and divide the other two by , yielding

(5) -

•

The term accounts for the fact of being a GSO (hence, sparse), with being a regularization parameter that determines the desired level of sparsity in the graph.

-

•

Finally, the equality constraint serves to embody (AS2). It is important to highlight that the polynomial relationship between and , as implied by (AS2), is typically addressed in estimation and optimization problems through either: i) extracting the eigenvectors of and enforcing them to be the eigenvectors of [13], or ii) imposing the constraint [16]. In contrast, our approach encodes the polynomial relation implied by (AS2) by enforcing commutativity between and . Note that if and are full-rank matrices and commute, it follows that and also commute. In other words, can be represented as a polynomial in , which can be verified by the Cayley-Hamilton theorem.

It is important to note that the assumption of stationarity may seem stringent since it implies commutativity between and . However, it provides more degrees of freedom than many existing methods. For example, in partial correlation methods, is restricted to be , while in our case, assuming stationarity allows to be any polynomial in . This leads to a more general approach, including partial correlation as a particular case. To further illustrate this point, consider the sparse structural equation model , with being white noise. GL will identify , while PGL will identify .

To better understand the features of PGL, let us briefly discuss the main differences relative to its two closest competitors: GSR and GL.

GSR handles Problem 1 without considering the Gaussian assumption in (AS1). As a result, the first two terms in (III), which are associated with the log-likelihood function, are not present. This reduces the problem to inferring a sparse graph under the stationarity constraint. The stationarity assumption is incorporated into (III) through the expression , which is equivalent to if is a full-rank matrix. This property enables learning the graph by solving the following optimization problem with the commutativity constraint between and :

| (6) |

where the constraint is typically relaxed as to account for the fact that we have . By assuming stationarity, the formulation in (6) allows the sample covariance to be modeled as any polynomial in , making it more general than the formulation in (III). However, the absence of Gaussianity in (6) means that it is no longer a maximum likelihood estimation. As a result, correctly identifying the ground truth requires very reliable estimates of , which usually entails having access to a large number of signals to set close to zero. This is indeed a challenge, especially in setups with a large number of nodes.

For the second scenario, suppose we simplify (AS2) and instead of considering as any polynomial in , we restrict it to a particular case with the following structure: . Then, up to the diagonal values and scaling issues, the sparse matrix to be estimated and are the same. Consequently, it suffices to optimize over one of them, leading to the well-known GL formulation:

| (7) |

The main advantages of (7) relative to (III) are that the number of variables is smaller and the resulting problem (after relaxing the norm) is convex. The main drawback is that by forcing the support of and to be the same, the set of feasible graphs (and their topological properties) is more limited. Indeed, GL can only estimate graphs that are positive definite, while the problem in (III) can yield any symmetric matrix. Remarkably, when the model assumed in (7) holds true (i.e., data is Gaussian and is sparse), GL is able to find reliable estimates of even when the number of samples is fairly low. On the other hand, simulations will show that GL does a poor job estimating when the relation between the precision matrix and is more involved.

In conclusion, from a conceptual point of view, our formulation reaches a favorable balance between GL and graph-stationarity approaches. This leads to the following two main advantages i) a more general model than GL since our approach models as any polynomial in and ii) a model with more structure than the graph-stationarity approaches due to the incorporation of (AS1). However, it is important to note that the optimization in (III), even if the norm is relaxed, lacks convexity due to the presence of a bilinear constraint that couples the optimization variables and . These challenges will be addressed in the subsequent section.

IV Biconvex relation and algorithm design

As explained in the previous section, the problem in (III) is not convex and this challenges designing an algorithm to find a good solution. This section reformulates (III), develops an iterative algorithm, referred to as PGL, to estimate and , and characterizes its convergence to a coordinate-wise minimum point. The proposed approach involves several modifications: 1) we replace the -norm with an elastic net regularizer, which is convex [26]; and 2) we relax the commutativity constraint using an inequality instead of an equality. Next, we explain step by step the resulting formulation.

IV-A Biconvex relaxation

The first modification to reformulate (III) is to relax the constraint that imposes commutativity between and . Such a constraint is stringent and significantly narrows the feasible solution set of (III), which may not be practical in real-world scenarios. Furthermore, considering that our access to the covariance (or precision) matrix is limited to its sampled estimates, enforcing exact commutativity is excessively restrictive. To mitigate this, we relax the original constraint by replacing the matrix equality with the scalar Frobenius norm-based inequality . This modification not only expands the feasible region but also endows the model with a greater degree of robustness.

The second modification addresses the non-convexity of the objective in (III), which originates from the use of the -norm. To alleviate this issue, we relax the problem using an elastic net regularizer. Specifically, we replace the penalty with , where the parameter controls the trade-off between the -norm and the Frobenius norm components, and is typically set to a very small value. Although elastic net regularizers have demonstrated practical effectiveness, alternative methods for relaxing the -norm exist (see, for example, [27, 28]), each offering distinct trade-offs in computational complexity, convergence speed, and theoretical underpinnings.

With the incorporation of these two modifications, we reformulate the original graph learning problem presented in (III) as follows

| (8) |

In this setup, serves as a hyperparameter chosen according to the quality of the estimation of which affects the estimation of . A smaller value of is appropriate when the quality of is high, which typically corresponds to having a sample size that is substantially larger than the number of nodes. While the relaxation of the commutativity constraint enhances the robustness of our formulation to data quality and simplifies the optimization by reducing the number of Lagrange multipliers, the product of and still introduces nonconvexity into the problem. The way we propose for dealing with the (updated) biconvex constraint is to solve (8) using an alternating optimization algorithm. This family of algorithms is widely used to approximate nonconvex problems by dividing the original problem into several convex subproblems and solving them with respect to each of the variables by fixing all the others. In our particular case, this methodology involves alternately solving for with held fixed, and then updating using the newly updated , at each iteration.

In the subsequent two subsections, we delve into the detailed methodologies employed to solve each of the two subproblems. Following this, we outline the overall algorithm and discuss its convergence properties. To simplify exposition, in the remainder of the section, we will assume that represents the adjacency matrix of an undirected graph. Consequently, the feasible solution set for is defined as:

| (9) |

where is constrained to be symmetric with zero diagonal entries and non-negative off-diagonal elements. The additional condition is imposed to preclude the trivial solution, i.e., . Nonetheless, the techniques presented next can be readily extended to accommodate different forms of .

IV-B Solving subproblem for

We begin by addressing the subproblem with respect to , while holding fixed. The subproblem is formulated as:

| (10) |

To solve (10), we adopt a linearized ADMM approach, which introduces an auxiliary variable and leads to the following equivalent formulation:

| (11) |

The augmented Lagrangian associated with (11) is then given by

| (12) | |||||

where is the Lagrange multiplier.

To update at the -th iteration, we address the following minimization problem:

| (13) |

where, for the sake of simplicity, we omit the iteration subscript from and . Problem (13) does not admit a closed-form solution due to the term . To deal conveniently with this problem we resort to the majorization-minimization (MM) algorithm [29]. We denote this term as and proceed to majorize both and at the point , resulting in the following problem:

| (14) |

where represents the gradient of , detailed in the equation:

| (15) | |||||

Now, Problem (14) has a closed-form solution, allowing for the update of as follows:

| (16) |

where is the projection onto the set with respect to the Frobenius norm, which can be computed efficiently by the Dykstra’s projection algorithm [30]. More specifically, the set can be written as the intersection of two closed convex sets as follows:

| (17) |

where and . We employ Dykstra’s projection algorithm [30] to compute the nearest point projection of a given point onto the intersection of sets and . Dykstra’s algorithm achieves this by alternately projecting the point onto and until the solution is reached. For a more comprehensive understanding of Dykstra’s projection algorithm, the reader is directed to [30]. Detailed descriptions of the projection computations onto sets and are provided in Appendix A.

Returning to the augmented Lagrangian in (IV-B), we update at the -th iteration by solving the following problem:

| (18) |

where we have simplified the notation by omitting the iteration subscripts from and . Problem (18) has a closed-form solution. As a result, can be updated by

| (19) |

where denotes the projection defined by:

| (22) |

Finally, the dual variable is updated according to:

| (23) |

where the iteration subscripts from and have been omitted for simplicity. A pseudocode of the steps to be performed for the update of is summarized in Algorithm 1.

If the parameter in (14) is larger than the Lipschitz constant of the gradient of , then the sequence converges to the optimal solution of Problem (11), and converges to the optimal solution of the dual of problem (11), which follows from the existing convergence result of majorized ADMM [31]. To enhance empirical convergence rates, adopting a more proactive strategy for selecting the parameter is beneficial. For example, utilizing a backtracking line search to determine the stepsize in (16) can help to accelerate convergence.

We note that the choice of the penalty parameter can affect the convergence speed of the ADMM algorithm. A poorly chosen may lead to very slow convergence in practice. Adaptive schemes that adjust have been shown to often result in better practical performance. For example, we can adopt the adaptive update rule presented in [32]:

| (27) |

where , , and are predefined parameters. Here, and represent the primal and dual residuals at iteration , respectively. They are defined as

and

Although it can be challenging to prove the convergence of ADMM when varies by iteration, the convergence theory established for a fixed remains applicable if one assumes that becomes constant after a finite number of iterations.

IV-C Solving subproblem for

Using the formulation from (8), we now turn our attention to the subproblem for

| (28) |

Similarly to the approach taken for the subproblem, we reformulate the subproblem (28) for as follows

| (29) |

The augmented Lagrangian associated with (29) is given by

| (30) | ||||

To update at the -th iteration, we solve the following optimization problem

| (31) |

where we have omitted the iteration subscripts from and for simplicity.

Let . We then construct the majorizer of the objective function in (IV-C) at the point and obtain

| (32) |

where denotes the gradient of

| (33) |

Lemma 1. The optimal solution of problem (IV-C) is [33]

| (34) |

where and contain the eigenvalues and eigenvectors of , respectively.

Then, is updated by addressing the following problem

| (35) |

where the iteration subscripts from and have been omitted for simplicity. Similar to the case of updating , we update as

| (36) |

Finally, the Lagrange multiplier is updated as follows

| (37) |

where the iteration subscripts from and have been similarly omitted for clarity.

IV-D Graph-learning algorithm and convergence analysis

Leveraging the results presented in the previous two subsections, the steps to run our iterative scheme to find a solution to (8) are summarized in Algorithm 3.

Before presenting the associated theoretical analysis, several comments regarding the implementation of Algorithm 3 are in order:

-

•

For simplicity, the algorithm considers a fixed number of iterations, but a prudent approach is to monitor the cost reduction at each iteration and implement an early exit approach if no meaningful improvement is achieved.

-

•

The value of the hyperparameters , and is an input to the algorithm. We note that is typically set to a small value to guarantee that the (sparsity promoting) norm plays a more prominent role. Moreover, the value of should be chosen based on the quality of the estimate of the sample covariance matrix . The higher the number of observations (hence, the better the quality of ), the smaller the value of . Similarly, if the number of nodes is high, the value of should be re-scaled accordingly, so that the constraint does not become too restrictive.

-

•

The update of poses the primary computational challenge, mainly due to the complex nature of its estimation. In contrast to , which is primarily estimated from the data matrix , the estimation of relies on its interplay with through the relaxed commutativity constraint. This indirect relationship adds to the complexity of the estimation, as it does not directly benefit from data-driven insights, often necessitating greater precision in solving the corresponding subproblem. Furthermore, the constraints imposed on are substantially more complex than those on , thereby increasing the computational load to obtain a solution that lies within the feasible set. To alleviate the computational demand, we may employ a relatively loose stopping criterion for the subproblem, which can expedite convergence without significantly affecting the quality of the solution.

To establish the theoretical convergence of Algorithm 3, we begin by introducing several definitions and (mild) assumptions pertinent to Problem (8).

Let denote the objective function and the feasible set of Problem (8), respectively. We define as a block coordinatewise minimizer of Problem (8) if:

| (38) |

and

| (39) |

where , and .

Furthermore, we introduce the following assumptions for our analysis:

Assumption 1.

We require Assumption 1 because the intersection may otherwise be empty, implying that the feasible set of subproblem (10) could be nonexistent. However, Assumption 1 is relatively mild, as we can always choose a sufficiently large to ensure that the feasible set of subproblem (10) remains nonempty at every iteration. Given Assumption 1, our algorithm is guaranteed to find a minimizer of subproblem (10) throughout its iterations. Additionally, the feasibility of subproblem (28) is inherently assured.

Assumption 2.

The matrix in Problem (8) is positive definite.

Assumption 2, which requires all the eigenvalues to be nonzero, guarantees that subproblem (28) is well defined. Without this assumption, the objective function in (28) may fail to achieve a finite minimum value. In cases where Assumption 2 may not hold, incorporating an norm regularizer for would bound the solution, thereby ensuring the existence of a minimizer.

(a)

(b)

(c)

Theorem 1.

The proof of Theorem 1 is deferred to Appendix C. This theorem asserts the subsequence convergence of our algorithm to a block coordinatewise minimizer of Problem (8). When the block coordinatewise minimizer lies within the interior of the feasible set, it becomes a stationary point. The theorem’s assertions are significant both theoretically and practically. As discussed earlier in the paper, GMRFs are a particular case of Gaussian graph-stationary processes. Taking this into account, we can always initialize our algorithm using the solution estimated by GL (which is optimal for GMRF) and then, run iteratively the updates over and in Algorithm 3, to get an (enhanced) coordinatewise minimum estimate.

V Numerical experiments

This section evaluates quantitatively the performance of PGL. Since PGL can be understood as a generalization of the widely adopted GL (with being any polynomial in ), in most test cases, we will test both algorithms. Similarly, we also test the learning performance of GSR [13], which assumes stationarity but not Gaussianity. The performance results obtained from both synthetic and real-data experiments are summarized in Figs. 1-4. Unless otherwise stated, to assess the quality of the estimated GSO, we use the normalized mean error between the estimated and true . Mathematically, this entails computing111Results for other recovery metrics (including accuracy and F1 score) as well as additional simulations can be found both in our conference precursor [1] and in our online repository https://github.com/andreibuciulea/GaussSt˙TopoID.

| (40) |

where and represent the estimated and true respectively. Moreover, for the synthetic experiments we test the graph learning algorithms over realizations of random graphs and report the average normalized mean error .

If not specified otherwise, in our synthetic experiments, we consider graphs with nodes generated using the Erdös-Rényi (ER) model with a link probability of . Regarding the generation of the graph signals, three different setups for the covariance matrices have been studied. For the setup referred to as “Poly”, the covariance matrix is generated as a random polynomial of the GSO of the form , where are random coefficients drawn from a normalized zero-mean Gaussian distribution, and the square operator guarantees matrix to be positive definite. The setup referred to as “SSEM” constructs the covariance matrices following the sparse structural equation model [34] for graph signal generation as , where is selected to ensure that is positive definite. The setup referred to as “MRF” constructs the covariance matrices following the assumptions made by GL as , where is some positive number large enough to assure that is positive definite and is some positive random number.

V-A Test case 1: Estimation error vs. number of samples for multiple synthetic scenarios.

In this first test case, we employ synthetic scenarios for testing the performance of our approach in terms of nme vs. and also compare the results with other methods from the literature. The different scenarios considered are detailed below.

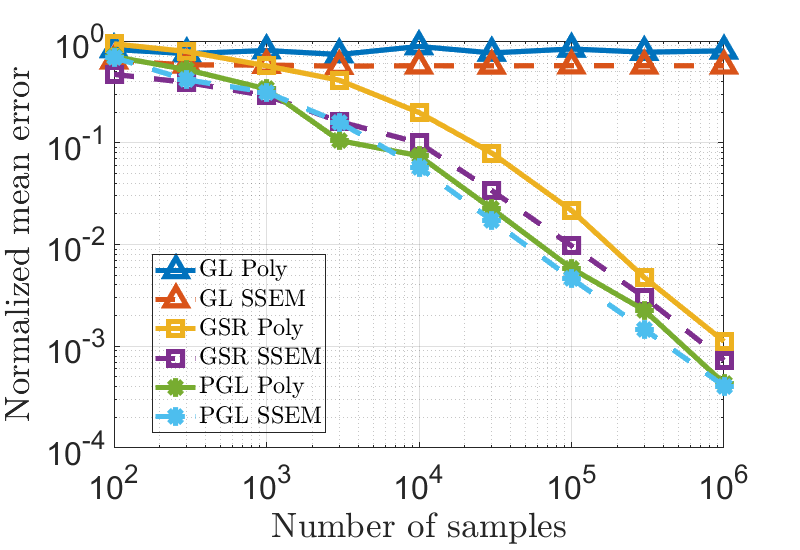

Error vs. number of samples for different graph learning methods and signal models. The results of the experiment depicted in Fig. 1a, compare the nme (y-axis) of various algorithms with respect to the number of available samples (x-axis). Moreover, we consider SSEM and Poly setups for data generation. The results shown in Fig. 1a reveal that: i) PGL outperforms its competitors, ii) the error decreases as increases, and iii) estimation is more accurate for SSEM than for Poly. Next, we discuss these three main findings in greater detail. All algorithms do a better job estimating the graph for the SSEM model. Since for SSEM is a specific second-order polynomial in it can be seen as a particular case of Poly, and consequently, a scenario from which the graph structure is easier to estimate. Indeed, while GL fails to estimate the graph for the Poly model, it is able to estimate some of the links for the SSEM. However, the estimation error of GL is quite large and does not change with the number of samples , demonstrating that the poor performance is due to a model mismatch. This will be further confirmed in Section V-B, where we simulate a GMRF data generation setup that aligns perfectly with the assumptions made by GL. Regarding PGL and GSR, we observe that the error decreases almost linearly with the number of samples . Perhaps more importantly, we also observe that, as increases, the gap between PGL and GSR diminishes. For example, while for the Poly case GSR needs 10 times more samples than PGL to achieve an error of , GSR only needs 3 times more samples than PGL to achieve an error of . This illustrates that, as expected, the gains associated with assuming Gaussianity are stronger when the number of observations is small, vanishing as grows very large.

Error vs. number of samples for noisy observations. Next, we assess the performance of the graph-learning algorithms in the presence of additive white Gaussian observation noise. The results are shown in Fig. 1b. As in the previous test case, we report nme vs for PGL, GL and GSR. The difference here is that we consider only the more intricate signal generation model (Poly) and two normalized noise levels ( = 0.05, = 0.2). The main observations in this case are: i) PGL outperforms GSR and GL, ii) the error for PGL and GSR decreases as increases, while the one for GL is flat and close to , iii) the estimation performance for PGL and GSR worsens as the noise level increases, deteriorating noticeably with respect to the setup in Fig. 1a, and iv) the gap between PGL and GSR grows. The findings in i) and ii) are consistent with those found in the previous test case. Finding iii) is expected and common in all graph-learning approaches. Finally, the larger gap in finding iv) is due to the fact that this is a more challenging scenario (high-order polynomial covariances and observation noise), and, as a result, the higher level of sophistication of PGL relative to GSR translates into more noticeable gains.

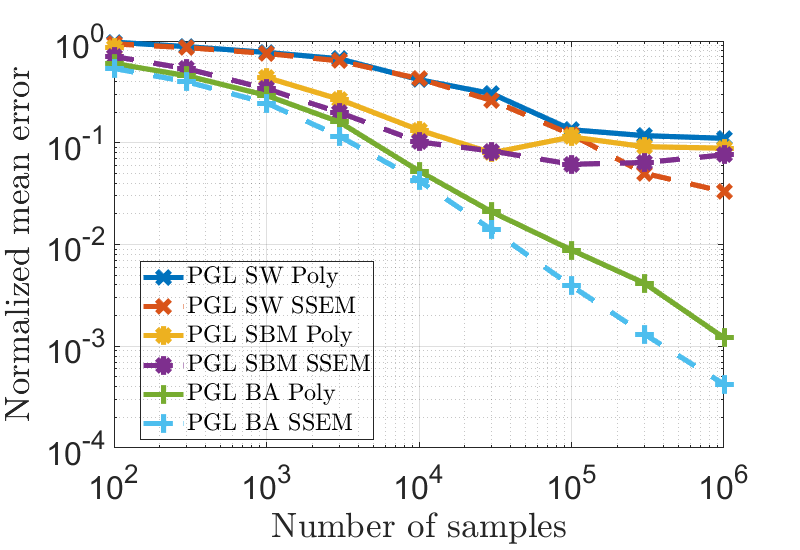

Error vs. number of samples for different graph models. This test case considers network models other than ER. In particular, three different types of graphs are considered: 1) Small World (SW) graphs with mean node degree and rewiring probability ; 2) Stochastic block model (SBM) graphs with clusters, and intra and inter-cluster edge probability of 0.8 and 0.05, respectively; and 3) Barabási-Albert (BA) graphs with edges to attach at every step. As in the first test case, we consider two types of signal generation models: SSEM and Poly. Fig. 1c reports the error vs. the number of samples for the six combinations considered (3 types of graphs and 2 types of signal generation models). The results show that there is a significant difference in performance between SW, SBM, and BA, which is part due to the sparsity level present in each graph. One of the assumptions codified in our model is that the graph is sparse, and, as a result, our algorithm does a better job estimating BA (the one with the lowest average degree) than SBM and SW (the one with the highest average degree). Finally, we also note that the estimation error achieved with SSEM consistently outperforms that of the Poly setup. These findings align with the results presented in Fig. 1a for ER graphs and are in accordance with the theoretical discussion that postulated SSEM as a specific instance of Poly.

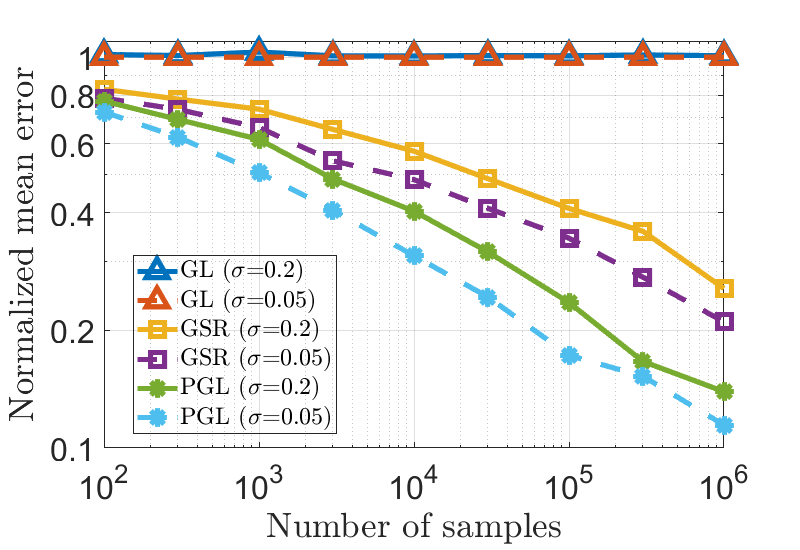

V-B Test case 2: Noisy GMRF graph signals.

In this test case, the goal is to assess the behavior of PGL for GMRF observations, which is the setup that motivated the development of the GL algorithm.

| Alg. | 20 | 30 | 40 | 50 | 60 | 70 | 80 | Metric |

|---|---|---|---|---|---|---|---|---|

| PGL-CVX | —- | —- | Time (s) | |||||

| PGL-Alg.3 | ||||||||

| PGL-CVX | —- | —- | nme | |||||

| PGL-Alg.3 |

Estimation error considering noisy GMFR signals. In this experiment, we replicate the scenario from Fig.1b, utilizing a GMFR model to generate the signals. The performance of PGL, GL and GSR for two different noise levels, , is depicted in Fig. 2. The main observations are: i) across all considered approaches, increasing the noise level leads to a deterioration in terms of nme; ii) GSR always performs worse than PGL, providing very poor results when ; and iii) GL outperforms PGL when the number of observations is small. Findings i) and ii) are unsurprising and consistent with the behavior observed in the previous experiments, showcasing the benefits of considering the log-likelihood regularization in the optimization run by PGL. Regarding iii), GL outperforming PGL is expected, since the latter needs to ”learn” the particular polynomial between and .

However, as the value of increases, the error in PGL gradually decreases, while the error in GL remains relatively constant, leading to PGL outperforming GL for large values of . This behavior is more surprising and can be attributed to the fact that GL focuses on learning the precision matrix , while PGL balances the accuracy in terms of both the precision and the graph . Since the reported error focuses on the estimation , the values of the diagonal of are not relevant for nme and this can explain that GL, which is a maximum likelihood estimate for , does not yield the minimum nme.

V-C Test case 3: Computational complexity.

Here, we compare the runtime obtained by the efficient implementation of our PGL scheme provided in Algorithm 3 and a generic block-coordinate alternating minimization algorithm that uses CVX [35], the most common off-the-shelf solver for convex problems.

Computational complexity and estimation error. The objective of this experiment is to evaluate the running time and estimation error for different versions of our algorithm as the number of nodes increases. In particular, the experiment focuses on the Poly setup, utilizing graph signals, and averages the results over 50 graph realizations. Table I lists the elapsed time required to obtain the graph and precision estimates for problems with different numbers of nodes using two algorithms: 1) solving the optimization in (8) with a block coordinate approach where the minimization over given and the minimization over given are run using CVX (this algorithm is labeled as PGL-CVX) and 2) employing the efficient scheme outlined in Algorithm 3 (this choice is labeled as PGL-Alg.3). To guarantee that the results are comparable, the nme is also reported. Examining the listed running times, we observe that as the number of nodes increases, both solvers require more time to estimate the graph (note that the number of variables scales with ). More importantly, there exists a noticeable difference between PGL-CVX and PGL-Alg.3. Not only the latter is faster for small graphs, but the gains grow significantly as increases. Note that the results for graphs with more than nodes are not reported for PGL-CVX, since the computation time exceeded two hours. In terms of nme, our approach achieves similar (slightly better) results than PGL-CVX. In conclusion, the experiment demonstrates that the efficient implementation described in Section IV is more efficient than readily available convex solvers, rendering it particularly well-suited for large graphs while yielding comparable nme.

V-D Test case 4: Real data scenarios.

Finally, we compare different graph-learning algorithms (including PGL) in the context of two different graph-aware applications. The details and results are provided next.

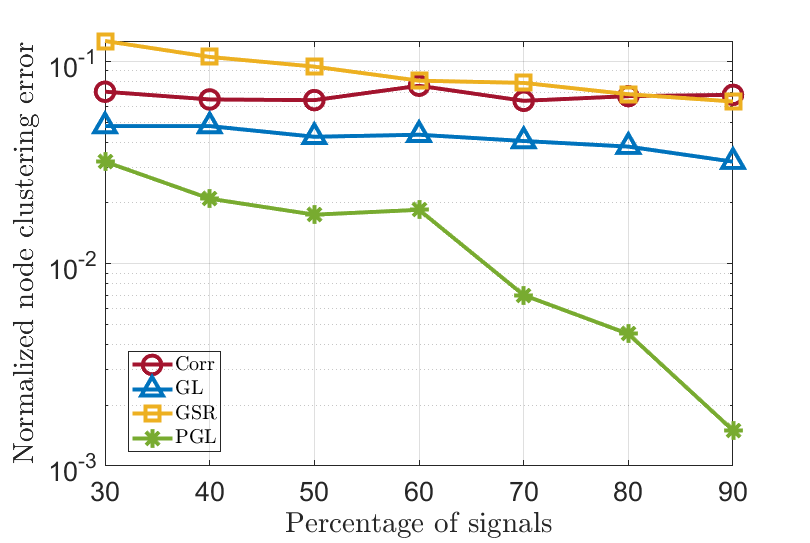

Stock graph-based clustering from returns. For this real-data experiment, we tested our graph learning algorithm on financial data and further performed a clustering task. Specifically, 40 companies from 4 different sectors of the S&P 500 were selected (10 companies from each sector) and the market data (log returns) of each company in the period 2010-2015 was retrieved. This gives rise to a data matrix of size . In this application, as in many others dealing with graph learning, we do not have access to the ground truth graph. Hence, we cannot quantify the quality of the estimated network directly by using a metric like or F1 score. As a result, we need to assess the quality of the estimated graph indirectly, using the graph as input for an ulterior task. In this experiment, we use the graph to estimate the community each company belongs to in an unsupervised manner. More specifically, we implement the following pipeline: 1) estimate several graphs from a subset of the available graph signals, 2) use spectral clustering to group the nodes into 4 communities (as many as sectors were selected), and 3) compute the ratio of incorrectly clustered nodes. To obtain more reliable results, we averaged the clustering errors over 50 realizations in which the subset of graph signals was chosen uniformly at random. The vertical axis of Fig.3 represents the normalized clustering error which is computed as the average of the fraction between the number of wrongly clustered nodes and the total number of nodes over graph realizations. The horizontal axis of Fig. 3 represents the percentages of graph signals used to estimate . Results are provided for 4 graph-learning approaches: PGL, GL, GSR, and “Corr”, which estimates the graph as a thresholded version of the correlation matrix. The idea is that companies from the same sector have stronger ties among them and, as a result, when running a graph-based clustering method, the 4 sectors should arise. Based on the results presented in Fig.3, it can be observed that PGL outperforms the other alternatives and additionally, as the number of available signals increases, the clustering error for PGL drops significantly. The superiority of PGL may indicate that considering more complex relationships among stocks (beyond the simple correlations considered in “Corr” or the partial correlations considered in GL) is a better model to understand the dependencies between log-returns in the stock market. On the other hand, GSR shows high clustering error with a limited number of samples, but it improves as the number of available samples increases. This observation aligns with our earlier discussion in Section III, where we highlighted that this particular model offers greater generality but necessitates a substantial number of samples to accurately estimate the graph.

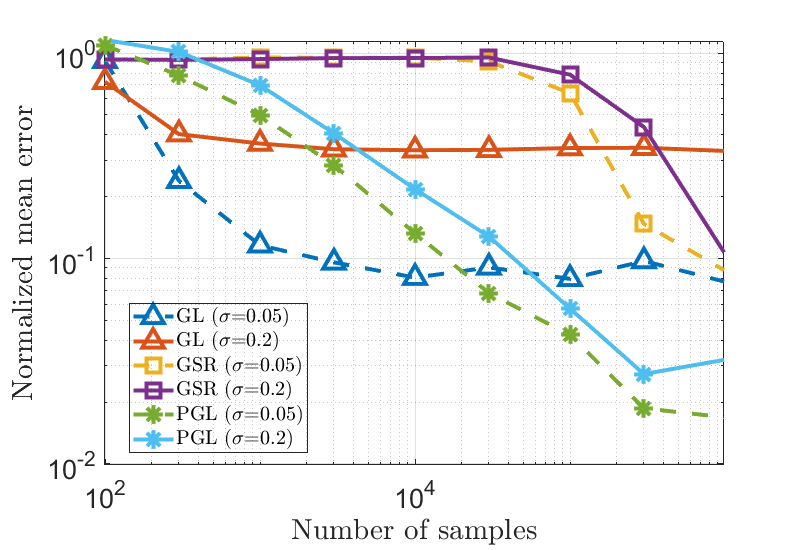

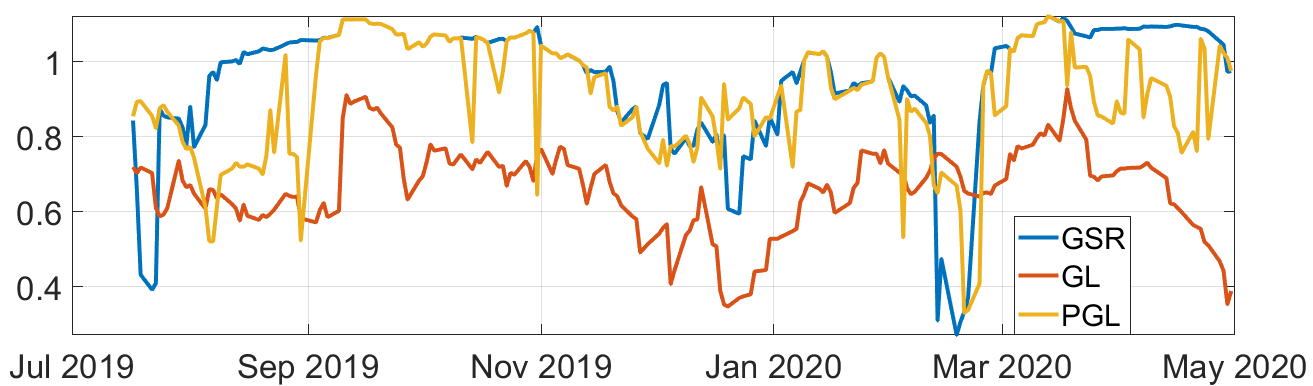

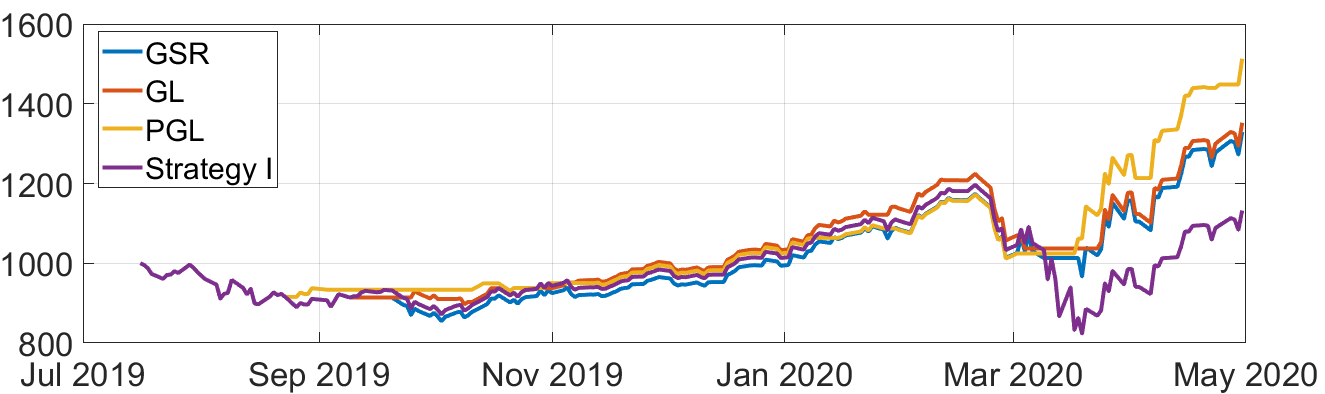

Learning sequential graphs for investing. This experiment deals with a different real-world problem and dataset. We still look at stocks, but consider now the close price of the 7 FAAMUNG222Facebook, Amazon, Apple, Microsoft, Uber, Netflix, and Google companies from Jul 2019 to May 2020. The goal is to design an investment strategy to maximize the benefits using as input a graph describing the relationships among the companies. Inspired by the approach in [36], we first build a graph, analyze its connectivity and then, invest (or not) in a stock according to the graph connectivity. To be more specific, we use the close price to estimate multiple adjacency matrices. We estimate a total of 200 matrices, where each adjacency matrix (graph) is estimated in a rolling window fashion. The window consists of 30 consecutive days and for each graph estimation, we shift the window one day at a time. These graph estimations help to visualize how the graph topology changes during this time period. The finding in [36] is that big changes in the graph connectivity indicate opportunities to invest. To that end, we keep track of the algebraic connectivity value, which is the second smallest eigenvalue () of the estimated Laplacian matrix. The lower the value, the less connected the graph is and, as a result, the easier breaking the graph into multiple components is. Fig.4 shows the value of for each of the 200 considered graphs (each associated with a 30-day period). Then, using the approach in [36] we invest only if is below a fixed threshold. We learn the graph using 3 methods (GL, GSR, and PGL) and, for each of them, we select the best possible threshold (the one that maximizes the benefits). Correlation was not used here due to its poor performance. The results of applying the graph-connectivity-based investment strategy to the graphs estimated with each of the algorithms are shown in Fig. 4. The blue line labeled as “Strategy I” represents the benefits of investing every day the available amount and is used as a baseline. By analyzing the results obtained, we can observe that: i) the graph-based strategies outperform (gain more money than) the baseline; ii) the strategies based on GL and GSR provide similar gains; and iii) the strategy based on GSSR yields the highest gains. This provides additional validation for the graph-learning methodology proposed in this paper.

(a)

(b)

VI Conclusions

This paper has introduced PGL, a novel scheme for learning a graph from nodal signals, with our key contribution being the modeling of the signals as Gaussian and stationary on the graph. This approach opens the door to a graph-learning formulation that leverages the advantages of GL (needing a relatively small number of signals to get a good estimation of the graph structure) while encompassing a more comprehensive model (because it handles cases where the precision matrix can be any polynomial form of the sought graph). Given the increased complexity and nonconvex nature of the resulting optimization problem, we have developed a low-complexity algorithm that alternates between estimating the graph and precision matrices and have characterized its convergence to a block coordinatewise minimum. To assess its efficacy, we have conducted numerical simulations comparing PGL with various alternatives, using both synthetic and real data. The results have showcased the benefits of our approach, motivating the adoption and further investigation of the proposed graph-learning methodology.

Appendix A Computations of projections

We present the details about how to compute the projections and .

The computation of is straightforward as follows:

| (41) |

The projection is defined as the minimizer of the optimization problem as follows:

| (42) |

To compute the projection , we solve Problem (42) row by row. For the -th row, we solve the following problem,

| (43) |

where contains all entries of the -th row of , denotes the -th entry of , and contains all entries of except the -th one.

Let denote the optimal solution of Problem (43). Proposition 1 below, proved in Appendix B, presents the optimal solution of Problem (43).

Proposition 1.

The optimal solution to Problem (43) can be obtained as follows:

-

•

If , then , and , for .

-

•

If , then , and , for , where satisfies .

Several efficient approaches have been developed to tackle the piecewise linear equation . Among these, the sorting-based method described in [37] is noteworthy. Central to this method is the sorting of the vector , which constitutes the most computationally intensive step, generally necessitating operations.

Appendix B Proof of Proposition 1

Proof.

The Lagrangian of the optimization in (43) is

where and are KKT multipliers. Let be the primal and dual optimal point. Then must satisfy the KKT system:

| (44) | ||||

| (45) | ||||

| (46) | ||||

| (47) | ||||

| (48) |

Therefore, for any , it holds that . Then we obtain the following results:

-

•

If , then and , following from the fact that and .

-

•

If , then . This can be obtained as follows: if , then . Since , one has ; On the other hand, if , then , following from the fact that . As a result, we get .

Overall, we obtain that

| (49) |

On the other hand, and satisfy that , , and . To this end, we can obtain the following results:

-

•

If , then , indicating that , for any .

-

•

If , then . This is because will result in , which does not satisfy the KKT system. Together with the KKT condition that , one has . Therefore, one obtains that, for any , , where is chosen such that .

We note that the in Proposition 1 is exactly the dual optimal point . ∎

Appendix C Proof of Theorem 1

Proof.

The convergence result stated in Theorem 1 is based on the framework established by Theorem 2.3 in [38]. To demonstrate the validity of Theorem 1, it suffices to establish that the conditions and assumptions of Theorem 2.3 are satisfied in our context. Our approach to block updates aligns with the procedure delineated in equation (1.3a) of [38].

We first verify the conditions the requisite conditions of Theorem 2.3 in [38] are met. Specifically, Theorem 2.3 stipulates that the objective function, along with the feasible set of the optimization problem, should exhibit block multiconvexity. For Problem (8), the objective function is convex with respect to each of the blocks and when the other block is fixed, a property that defines block multiconvexity as per [38]. Moreover, the function is strongly convex with respect to both and .

The feasibility constraints of Problem (8) form a set that satisfies the criteria for block multiconvexity as defined in [38]. This is due to the convexity of the individual set maps and . The set map is defined as

| (50) |

for some given , and similarly, the set map is defined as

| (51) |

for some given . Consequently, the optimization subproblems with respect to and in Problem (8) are convex.

We now validate the assumptions required by Theorem 2.3 in [38] within the context of our setting. Specifically, it is required that the objective function is bounded below over the feasible set , that is, . This is indeed the case here, because the term is nonnegative. Additionally, the function attains a finite infimum when is positive definite under Assumption 2. To see this, first observe that , where is the largest eigenvalue of . Consequently, . Further, since , with being the smallest eigenvalue of , we obtain

| (52) |

which indeed has a finite minimum. Thus, we conclude that .

Furthermore, the existence of block coordinatewise minimizers is assured by the compactness of the feasible set. Moreover, Theorem 2.3 in [38] stipulates that set maps change continuously during iterations. Referring to (50) and (51), it is clear that the only constraint that changes through iterations is , while the other constraints, and , remain constant. Given that is a continuous function with respect to both and , the set maps indeed change continuously, satisfying the theorem’s conditions.

These verifications above have demonstrated that the conditions and assumptions of Theorem 2.3 are satisfied in our context, completing the proof. ∎

References

- [1] A. Buciulea and A. G. Marques, “Graph learning from Gaussian and stationary graph signals,” in IEEE Intl. Conf. Acoust., Speech and Signal Process. (ICASSP), 2023, pp. 1–5.

- [2] E. D. Kolaczyk, Statistical Analysis of Network Data: Methods and Models, Springer, New York, NY, 2009.

- [3] O. Sporns, Discovering the Human Connectome, MIT Press, Boston, MA, 2012.

- [4] D.I Shuman, S.K. Narang, P. Frossard, A. Ortega, and P. Vandergheynst, “The emerging field of signal processing on graphs: Extending high-dimensional data analysis to networks and other irregular domains,” IEEE Signal Process. Mag., vol. 30, no. 3, pp. 83–98, May 2013.

- [5] A. Ortega, P. Frossard, J. Kovacevic, J. M. F. Moura, and P. Vandergheynst, “Graph signal processing: Overview, challenges, and applications,” Proc. IEEE, vol. 106, no. 5, pp. 808–828, 2018.

- [6] J. V. D. M. Cardoso, J. Ying, and D. P Palomar, “Algorithms for learning graphs in financial markets,” arXiv preprint arXiv:2012.15410, 2020.

- [7] G. Mateos, S. Segarra, A. G. Marques, and A. Ribeiro, “Connecting the dots: Identifying network structure via graph signal processing,” IEEE Signal Process. Mag., vol. 36, no. 3, pp. 16–43, 2019.

- [8] S. Sardellitti, S. Barbarossa, and P. Di Lorenzo, “Graph topology inference based on sparsifying transform learning,” IEEE Trans. Signal Process., vol. 67, no. 7, pp. 1712–1727, 2019.

- [9] N. Meinshausen and P. Buhlmann, “High-dimensional graphs and variable selection with the lasso,” Ann. Statist., vol. 34, pp. 1436–1462, 2006.

- [10] G. V. Karanikolas, G. B. Giannakis, K. Slavakis, and R. M. Leahy, “Multi-kernel based nonlinear models for connectivity identification of brain networks,” in IEEE Intl. Conf. Acoust., Speech and Signal Process. (ICASSP), Shanghai, China, Mar. 20-25, 2016.

- [11] J. Mei and J.M.F. Moura, “Signal processing on graphs: Estimating the structure of a graph,” in IEEE Intl. Conf. Acoust., Speech and Signal Process. (ICASSP), 2015, pp. 5495–5499.

- [12] H. E. Egilmez, E. Pavez, and A. Ortega, “Graph learning from data under Laplacian and structural constraints,” IEEE J. Sel. Topics Signal Process., vol. 11, no. 6, pp. 825–841, 2017.

- [13] S. Segarra, A. G. Marques, G. Mateos, and A. Ribeiro, “Network topology inference from spectral templates,” IEEE Trans. Signal Info. Process. Networks, vol. 3, no. 3, pp. 467–483, Sep. 2017.

- [14] V. Chandrasekaran, P. A. Parrilo, and A. S. Willsky, “Latent variable graphical model selection via convex optimization,” Ann. of Statist., vol. 40, no. 4, pp. 1935–1967, 2012.

- [15] A. Chang, T. Yao, and G. I. Allen, “Graphical models and dynamic latent factors for modeling functional brain connectivity,” in 2019 IEEE Data Science Wrksp. (DSW). IEEE, 2019, pp. 57–63.

- [16] A. Buciulea, S. Rey, and A. G. Marques, “Learning graphs from smooth and graph-stationary signals with hidden variables,” IEEE Trans. Signal Process., vol. 8, pp. 273–287, 2022.

- [17] P. Danaher, P. Wang, and D. M. Witten, “The joint graphical lasso for inverse covariance estimation across multiple classes,” J. of the Roy. Statistical Soc.: Ser. B (Statistical Methodology), vol. 76, no. 2, pp. 373–397, 2014.

- [18] M. Navarro, Y. Wang, A. G. Marques, C. Uhler, and S. Segarra, “Joint inference of multiple graphs from matrix polynomials,” J. of Machine Learning Research (JMLR), vol. 23, no. 1, pp. 3302–3336, 2022.

- [19] A. G. Marques, S. Segarra, G. Leus, and A. Ribeiro, “Stationary graph processes and spectral estimation,” IEEE Trans. Signal Process., vol. 65, no. 22, pp. 5911–5926, 2017.

- [20] A. Sandryhaila and J.M.F. Moura, “Discrete signal processing on graphs,” IEEE Trans. Signal Process., vol. 61, no. 7, pp. 1644–1656, Apr. 2013.

- [21] N. Perraudin and P. Vandergheynst, “Stationary signal processing on graphs,” IEEE Trans. Signal Process., vol. 65, no. 13, pp. 3462–3477, 2017.

- [22] B. Girault, “Stationary graph signals using an isometric graph translation,” in European Signal Process. Conf. (EUSIPCO), Aug 2015, pp. 1516–1520.

- [23] J. Friedman, T. Hastie, and R. Tibshirani, “Sparse inverse covariance estimation with the graphical lasso,” Biostatistics, vol. 9, no. 3, pp. 432–441, 2008.

- [24] X. Dong, D. Thanou, M. Rabbat, and P. Frossard, “Learning graphs from data: A signal representation perspective,” IEEE Signal Process. Mag., vol. 36, no. 3, pp. 44–63, 2019.

- [25] S. Segarra M. Sevilla, A. G. Marques, “Estimation of partially known gaussian graphical models with score-based structural priors,” in 27th Intl. Conf. Artificial Intelligence and Statistics (AISTATS), 2024.

- [26] H. Zou and T. Hastie, “Regularization and variable selection via the elastic net,” J. of the Roy. Statistical Soc.: Ser. B (Statistical Methodology), vol. 67, no. 2, pp. 301–320, 2005.

- [27] R. Tibshirani, “Regression shrinkage and selection via the lasso,” J. of the Roy. Statistical Soc.: Ser. B (Statistical Methodology), vol. 58, no. 1, pp. 267–288, 1996.

- [28] E. J Candes, M. B. Wakin, and S. P. Boyd, “Enhancing sparsity by reweighted minimization,” J. of Fourier Anal. and Appl., vol. 14, no. 5-6, pp. 877–905, 2008.

- [29] Y. Sun, P. Babu, and D. P. Palomar, “Majorization-minimization algorithms in signal processing, communications, and machine learning,” IEEE Trans. on Signal Processing, vol. 65, no. 3, pp. 794–816, 2017.

- [30] J. P. Boyle and R. L. Dykstra, “A method for finding projections onto the intersection of convex sets in Hilbert spaces,” in Advances in order restricted statistical inference, pp. 28–47. Springer, 1986.

- [31] M. Li, D. Sun, and K.-C. Toh, “A majorized ADMM with indefinite proximal terms for linearly constrained convex composite optimization,” SIAM J. on Optimization, vol. 26, no. 2, pp. 922–950, 2016.

- [32] S. Boyd, N. Parikh, E. Chu, B. Peleato, and J. Eckstein, “Distributed optimization and statistical learning via the alternating direction method of multipliers,” Foundations and Trends® in Machine learning, vol. 3, no. 1, pp. 1–122, 2011.

- [33] J. V. de M. Cardoso, J. Ying, and D. Palomar, “Learning bipartite graphs: Heavy tails and multiple components,” Adv. in Neural Inf. Process. Syst., vol. 35, pp. 14044–14057, 2022.

- [34] X. Cai, J. A. Bazerque, and G. B. Giannakis, “Sparse structural equation modeling for inference of gene regulatory networks exploiting genetic perturbations,” PLoS, Computational Biology, June 2013.

- [35] M. Grant and S. Boyd, “CVX: Matlab software for disciplined convex programming, version 2.1,” https://cvxr.com/cvx, Mar. 2014.

- [36] J. V. de M. Cardoso and D. Palomar, “Learning undirected graphs in financial markets,” in Asilomar Conf. Signals, Systems, and Computers, 2020, pp. 741–745.

- [37] L. Condat, “Fast projection onto the simplex and the ball,” Mathematical Programming, vol. 158, no. 1-2, pp. 575–585, 2016.

- [38] Y. Xu and W. Yin, “A block coordinate descent method for regularized multiconvex optimization with applications to nonnegative tensor factorization and completion,” SIAM J. on imaging sciences, vol. 6, no. 3, pp. 1758–1789, 2013.