Watanabe’s expansion: A Solution for the convexity conundrum

David Garcia-Lorite

Corresponding author, david.garcia.lorite@gmail.comCaixaBank, Quantitative Analyst Team, Plaza de Castilla, 3, 28046 Madrid, Spain,

Facultat de Matemàtiques i Informàtica, Universitat de Barcelona,

Gran Via 585, 08007 Barcelona, Spain,

Raúl Merino

VidaCaixa S.A., Market Risk Management Unit,

C/Juan Gris, 2-8, 08014 Barcelona, Spain.

Abstract

In this paper, we present a new method for pricing CMS derivatives. We use Mallaivin’s calculus to establish a model-free connection between the price of a CMS derivative and a quadratic payoff. Then, we apply Watanabe’s expansions to quadratic payoffs case under local and stochastic local volatility. Our approximations are generic. To evaluate their accuracy, we will compare the approximations numerically under the normal SABR model against the market standards: Hagan’s approximation, and a Monte Carlo simulation.

1 Introduction

Option pricing is one of the main tasks of a derivatives desk. Not only to obtain the derivatives prices and trade them but also to calibrate more complex models or manage all the associated risks. In practice, most institutions consider stochastic volatility models to better capture market dynamics. However, including this feature adds more complexity to the calculations, making the processes more complicated and requiring more time to execute.

Over the last decades, a research line has consisted of finding different methods to approximate the price accurately. On the one hand, there are approximations focused on finding an expansion of the implied volatility. For example, using perturbation methods as in Hagan and Woodward (1999), Hagan et al. (2002) and Jacquier and Lorig (2015), using heat kernel expansions as in Gatheral et al. (2012) or Henry-Labordère (2008), or asymptotic expansion method as in Karami and Shiraya (2018). On the other hand, others focused on prices. For example, the Alòs decomposition formula in Alòs (2012) expanded later in Alòs et al. (2020) and Gulisashvili et al. (2020), adjoint expansions as in Pagliarani and Pascucci (2013), the cos methods as in Fang and Oosterlee (2009) or Watanabe’s expansion in Kunitomo and Takahashi (2003), Takahashi and Yamada (2015) and Nagami (2021).

Despite the vast literature on option approximations, there are few written references on quadratic payoffs. These products are not commonly traded but are useful to calculate the convexity’s correction for CMS. The main references are Hagan et al. (2019) and Hagan and Woodward (2020). The value of a quadratic call, put, and swaps are given by

(1)

(2)

(3)

where is the expiration date, the payment date and is the forward rate process associated to the derivative. On the other hand, is the expected value associated to the numeraire . Although there is a closed formula for normal and log-normal when volatility is constant, it is not good enough since these products depend more on market skews and smiles than vanilla options.

Many banks use replication to price these structures. Note that

(4)

therefore, it is possible to approximate the value as the sum of options with different strikes. That is the main advantage of this approach, as it is consistent with vanilla option pricing, easy to implement, and automatically satisfies the put-call parity. Unfortunately, from a practical standpoint, it is necessary a dense option grid with different strikes. Only a few options are traded per expiration and strike, so it is essential to calculate the grid, making it computationally intensive. In addition, the option prices with higher strikes, which are required for the calculation, are illiquid and have a ‘fictitious’ market price. To overcome this, an alternative methodology based on finding an approximation formula under the SABR model has been proposed by Hagan et al. (2019) and Hagan and Woodward (2020).

The paper aims to obtain an alternative approach for pricing CMS derivatives. Firstly, we will establish a connection between the price of a CMS derivative and a quadratic payoff using a bit of Mallivin calculus. This relationship is obtained without relying on any specific model. Then, we will extend the results of Watanabe’s expansions to the case of quadratic payoffs over local and stochastic local volatility. The approximations are generic. To evaluate their accuracy, we will compare the approximations numerically under the normal SABR model against the market standards: Hagan’s approximation, and a Monte Carlo simulation.

The structure of the paper is as follows. In Section 2, we will introduce the main concepts of the CMS market to make the paper self-contained. In Section 3, we explain how to derive a general expression for the convexity adjustment for CMS caps, CMS floors, and CMS swaps using Malliavin calculus. This expression will depend on the different quadratic payoffs explained above. In Section 4, we provide a brief explanation of the Watanabe calculus. We will also give an example of the normal SABR model contrasting the accuracy of the approximation. In Section 5, we prove how to use Watanabe calculus to obtain the price of a quadratic call, quadratic put, and quadratic swaps under different models. The approximation is applied to local and stochastic local volatility models. In particular, the accuracy is tested for the normal SABR model by comparing the results against Monte Carlo and Hagan’s approximation. Finally, in Section 7, we will present our conclusions.

One of the principal uses of quadratic payoffs is the convexity adjustment calculation, especially for CMS products. Therefore, to make the article self-contained, in this section, we will do a brief introduction to the CMS market.

We will consider the market standard of two curves: one to discount the cash flows and another to estimate the floating coupon. These two curves are equivalent to the discount and repo curves in the equity market.

The following notation will be used throughout the paper:

•

We will denote the discount curve by and the estimated curve by .

•

is the spot discount factor to T using the curve i=d, e.

•

is the forward discount factor associated to the curve i=d, e from t to T.

•

is the fraction’s year between and .

•

is the floating rate associated with the curve i=d, e.

The swap is the most commonly traded derivative in the interest rate market. While there are various swaps types, the market standard is to exchange a fixed coupon for a floating one until the end of the contract. Fixed and floating rate payments can be scheduled on different dates and periods. But, to simplify the notation, we assume that payments are made on the same dates and in the same fractions of the year. Today is denoted as , and the future payment dates are scheduled by

The standard swap price is

(5)

When we receive a fixed coupon, , we are in a receiver swap. On the other hand, if we pay the fixed coupon, , we are in a payer swap. The measure used on the floating leg is associate to the numeraire .

There are two key concepts when working with swaps: the swap rate and the annuity factor. The swap rate is the fixed coupon that makes the structure fair. It is defined by

The annuity factor is defined by

A constant maturity swap (CMS) is a fixed-for-floating swap, where the floating leg pays, or receives, periodically a swap rate with a fixed time to maturity. It has the same structure as the standard swap, but changing the floating payment from to with .

The CMS swap price is given by

(6)

There is a significant difference between valuing a standard swap and a CMS swap. The floating coupon of the standard swap is a martingale under the forward measure . In other words,

But the swap rate is not, it implies that

The swap rate is a martingale respect to the measure induced by the numeraire . Since the floating rate and the swap rate are martingales with respect to different numeraries, a convexity adjustment is necessary for CMS products.

In fact, we have that

The essence of CMS modeling lies on the definition of a mapping function . In Andersen and Piterbarg (2010), a comprehensive discussion is presented regarding the selection of the mapping function and the requirements it must satisfy. We use the following mapping function:

Then, we have that

(7)

The second term in the summand of the right side is known as convexity adjustment for the CMS rate, see Hagan (2003) for more details.

Concluding this section, we introduce CMS Caps and Floors, the most common CMS derivative products. The paper aims to develop different price expansions under various models for calculating their convexity adjustments. A CMS Cap and CMS Floor consist of a series of calls and puts, named caplets or floorlets, with the underlying . The payoff is given by

Now, we will focus on calculating the value of a single caplet, that is

Using a change of numeraire, we have that

where

and The second term is the convexity adjustment for a CMS Cap. To calculate this term, it is usually assumed that

and use the following replication formula

with

The primary concern with this formula is that it requires knowledge of the swaption price on the strike grid where the right side tends to . Consequently, the convexity adjustment heavily relies on the extrapolation assumption.

In recent papers such as Hagan et al. (2019) and Hagan and Woodward (2020), the authors have proposed a new methodology that expresses the convexity adjustment for CMS Caps, CMS Floors, and CMS Swaps as a quadratic payoff. Using the singular perturbation technique, they obtain an expansion of the implied volatility for the quadratic payoff when the dynamics of the underlying follow a SABR-type model.

In the following sections, we will demonstrate how to use the Watanabe calculus to compute the price of quadratic payoff under a general stochastic local volatility model.

3 The connection between Quadratic Payoffs and the CMS Cap-Floor convexity

In this section, we will illustrate the connection between the quadratic payoffs and the convexity adjustment for CMS Cap, Floor, and Swap instruments. We will use Malliavin’s techniques to derive a generic representation for this adjustment. For more detailed content on Malliavin calculus see Alòs and García Lorite (2021) or Nualart (1995).

We will start with the convexity adjustment for a CMS Cap, as we saw in Section 2. We have that

where we will define

Here, the function is called the mapping function. A popular choice for this function is the linear model. In this model, it is assumed that

The parameters and are chosen according to the properties of under the measure associated with the numeraire . Using the Clark-Ocone formula with , we have

If we freeze in , we get the following approximation

Therefore, if we substitute the above equality in (3), we get that

Likewise, in the CMS Floor case, we obtain that

and, in the swap case, we find that

Example 3.1.

In the SABR model, to compute when , practitioners often use the replication formula

Then, if we take , we get that

(9)

Now, we have that

Then, we can utilize the replication formula (3.1) with to calculate the convexity adjustment. However, this approach requires assumptions about the distributional behavior of in both the left and right tails. It is necessary to choose a cut-off point until the SABR parametrization works accurately and implement an extrapolation mechanism outside this region.

There is another approximation using the quadratic payoff provided by the following formula:

The essence of this approach is to calculate, or approximate, the value of .

4 Basic introduction to Watanabe’s exapansion

In this section, we will give a brief introduction to Watanabe’s expansion in the field of quantitative finance, see Kahl (2008) for more details. This method supposes that we can find an expansion of the underlying in terms of a small parameter

(10)

where

The expansion is constructed such that . We refer to as the initial volatility and as the time to maturity. We use the auxiliary term to derive the asymptotic option pricing formula.

To calculate

we will use the forward expansion (4). It is easy to show that

(11)

where

(12)

and

Then, using a Taylor’s expansion on around , we get the following price expansion

(13)

Note that to use the price expansion given in (4), we need to know the terms for . These terms are expressed as

(14)

where is a non-stochastic function and

is the next iterated integral

(15)

with and correlated Brownian motions of the underlying and volatility processes, respectively. The integral (15) may seem complex, but using the Brownian bridge and conditioning on , the expectation of the integral (14) is simplified to

(16)

where is the pdf of and

is a function to be defined.

To illustrate, we will consider the normal SABR model and we will obtain the order approximation as described above.

Remark 4.1.

To simplify the notation, when we have a single Brownian motion driving the dynamics of the underlying, then we will denote

Example 4.2.

The objective of this example is to provide a brief overview of how can be used the Watanabe calculus to approximate the price of a call option when the underlying follows a normal SABR model. Consider that the forward price dynamics are given by

with . Then, if we will suppose that is small, i.e there is a parameter such that . Therefore, we have that

(17)

Lemma 4.3.

Under the dynamics given by (4.2), we can re-write the forward price dynamics as:

Proof.

The result is straightforward by iteratively applying the Itô-Taylor expansion.

∎

For practical reasons, an option price approximation is sought. Therefore, we consider an approximation of the forward price dynamics.

Remark 4.4.

The 4th order forward price dynamics is

To obtain the Watanabe price expansion (4), we need to find an expression for the terms. Using Remark 4.4 makes it easy to see the analytical expression for each term. Therefore

(18)

On other hand, we have that

(19)

(20)

Theorem 4.5(Option price expansion of 2nd order under normal SABR).

Under the model (4.2), the 2nd order call option approximation price is

(21)

where is given by (12), , is standard normal pdf, the standard normal cdf and .

Proof.

We consider the price expansion (4) until order . Then, we use the calculation of the terms given in (A.1). Finally, we take the limit to obtain the price approximation.

∎

To check the accuracy of (4.5), we will use a Monte Carlo method and the implied volatility approximation proposed in Hagan et al. (2002) for a range of strikes. The parameters used have been calibrated to the swaption market with the underlying swap tenor of 5 years and maturities of 5 years, 10 years, and 15 years.

SABR Parameters

5Y

10Y

15Y

0.0083

0.0075

0.0068

0.335

0.243

0.215

0.230

0.235

0.195

Table 1: Normal SABR parameters considering an underlying swap tenor of 5 years.

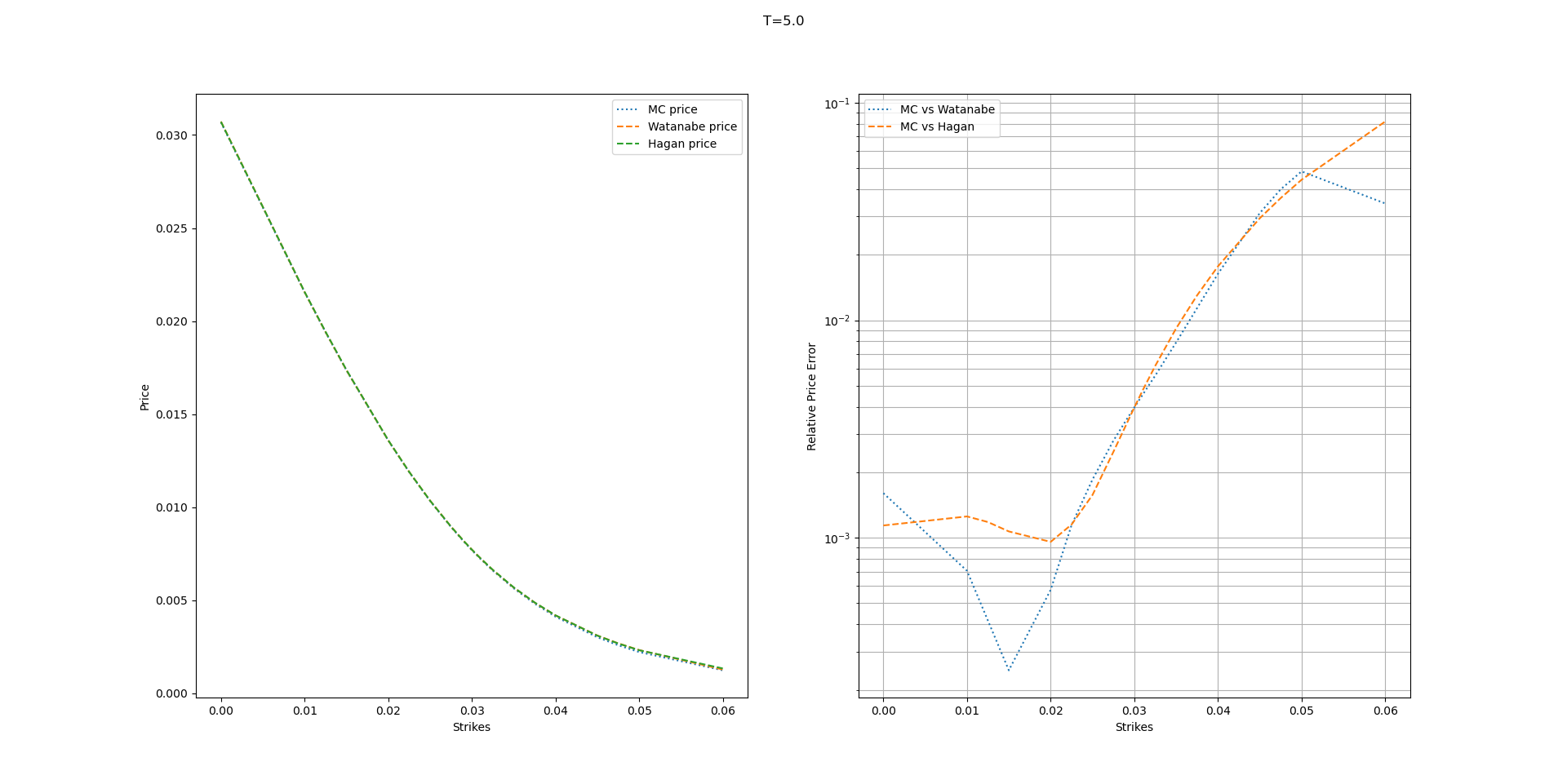

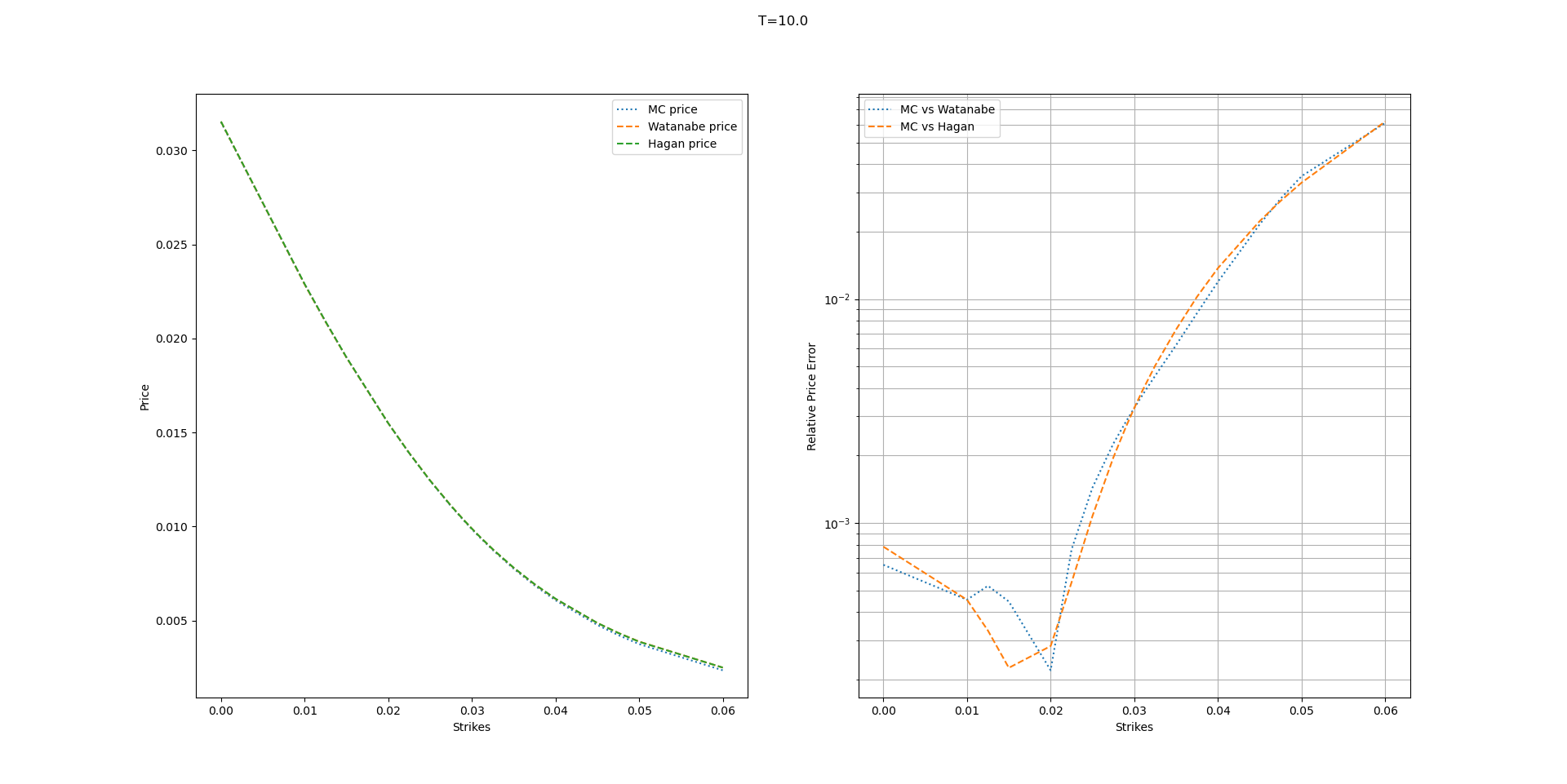

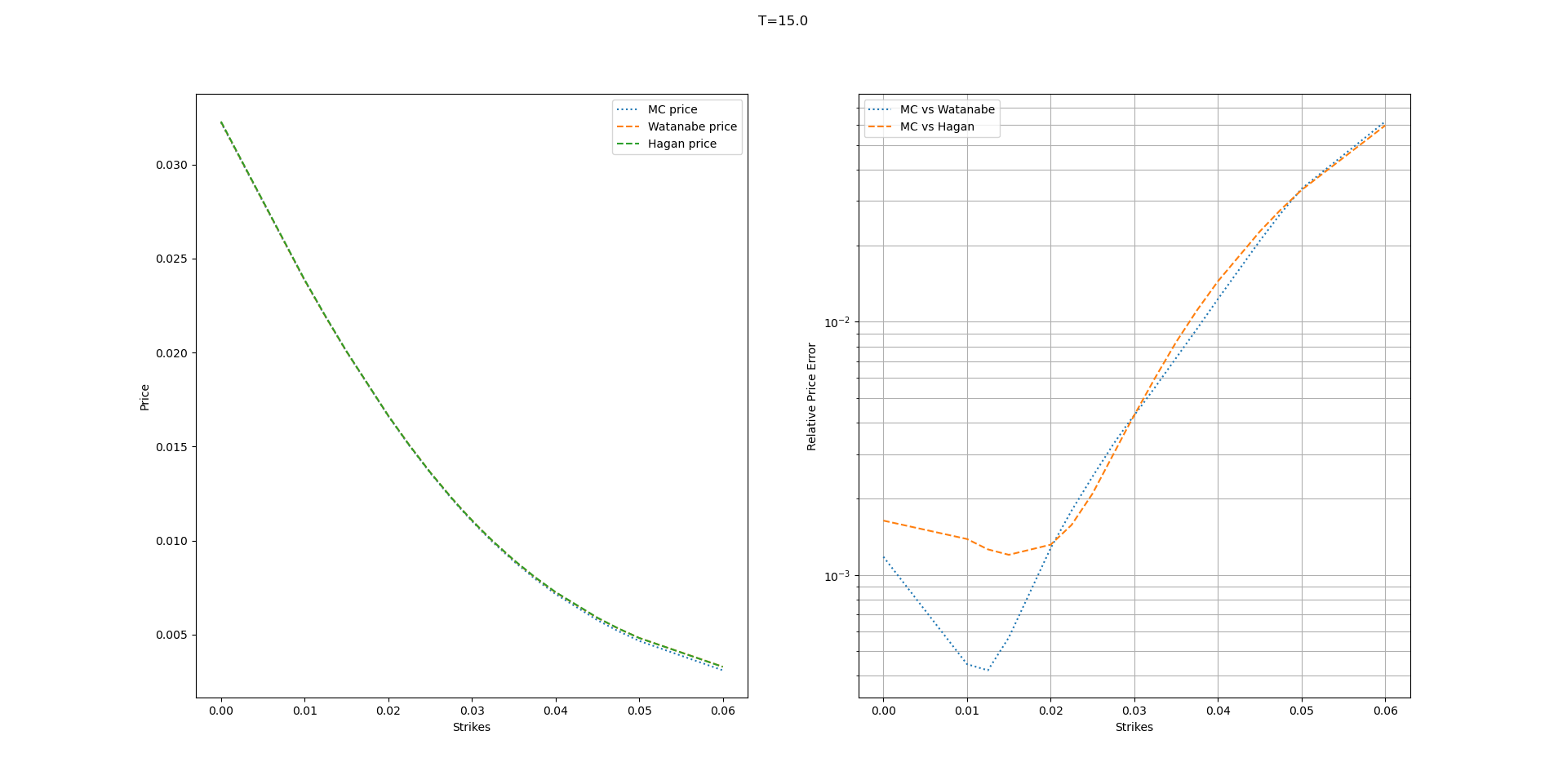

In figures 1, figures 2, and figures 3 we compare the numerical performance of the Watanabe approximation against Hagan’s approximation and a Monte Carlo simulation. We observe that the Watanabe approximation is slightly better than Hagan’s.

Figure 1: Comparison of call options using Watanabe’s expansion against the industry standards. The parameters considered are and Figure 2: Comparison of call options using Watanabe’s expansion against the industry standards. The parameters considered are and Figure 3: Comparison of call options using Watanabe’s expansion against the industry standards. The parameters considered are and

5 Quadratic option price

In this section, following the methodology presented in Section 4, we will derive a Watanabe expansion for quadratic payoff derivatives when the underlying follows a stochastic volatility model, a local volatility model, and a local stochastic volatility. It is worth noting that the quadratic payoff is more influenced by the tail of the distribution than the call option price . In the case of local volatility, we will explain why this happens.

Consider that the forward price dynamics are given by

(22)

where is Lipschitz function to ensure existence and uniqueness of the solution. Now, if we use Itô-Tanaka formula to , we get that

(23)

It is noteworthy that the value of depends on the value of when . For this reason, the quadratic call price is highly sensitive to our assumptions about the behavior of the local volatility function at extreme strikes.

As seen in Section 4, we will find the Watanabe’s price expansion for the quadratic call, put, and swap.

Theorem 5.1(Price Approximation for a Quadratic Call, Put, and Swaps).

Let’s suppose there exists a forward price expansion given by (4). Let defined by (12), and defined in (19). Then, the -approximation for Watanabe’s expansion of a quadratic call option price is

(24)

The -approximation of a quadratic put option price is

(25)

The -approximation of a quadratic swap price is

(26)

Proof.

We proceed as in (4). We use the forward expansion (4) to re-write the option price. Then, we use a Taylor’s expansion on around for each product.

∎

5.1 Quadratic option under local volatility

When the volatility is constant, that is , the quadratic call option price is

(27)

where and are, respectively, the density and cumulative function for a standard normal distribution. We are interested in building an option price expansion with base (27). We will consider the small diffusion model

(28)

where is a positive function such that belongs to .

Lemma 5.2.

Under the dynamics given by (28), we can re-write the forward price dynamics as:

(29)

where under usual regularity conditions in we have that .

Proof.

The result is straightforward by iteratively applying the Itô-Taylor expansion.

∎

As previously stated, to obtain the Watanabe’s price expansion, we need to find an expression for the terms. Comparing Lemma 5.2 with the price expansion (4), we have that

(30)

Theorem 5.3(Local volatility expansion for quadratic payoffs).

Under the model (28), consider is given by (12), is standard normal pdf, the standard normal cdf and . Then, the 3rd order quadratic call option approximation price is

(31)

where .

The 3rd order quadratic put option approximation price is

(32)

where .

Finally, the quadratic swap price is

(33)

Proof.

We consider the quadratic price expansion of Theorem 5.1. In the quadratic call option price, unifying (D.4.1), (D.4.2) and (D.4.3) along with (5.2). Then, we take the limit to obtain the quadratic call option price approximation. We proceed similarly with the quadratic put option price approximation and the quadratic swap option price.

∎

Remark 5.4.

It is important to note that the last expressions satisfy parity for quadratic options, that is

Example 5.5.

To verify the accuracy of (5.3), we will apply it to the normal SABR model, i.e. . In this case, the equivalent local volatility has a closed-form solution, given by Balland and Tran (2013). The expression for the equivalent local volatility is as follows:

(34)

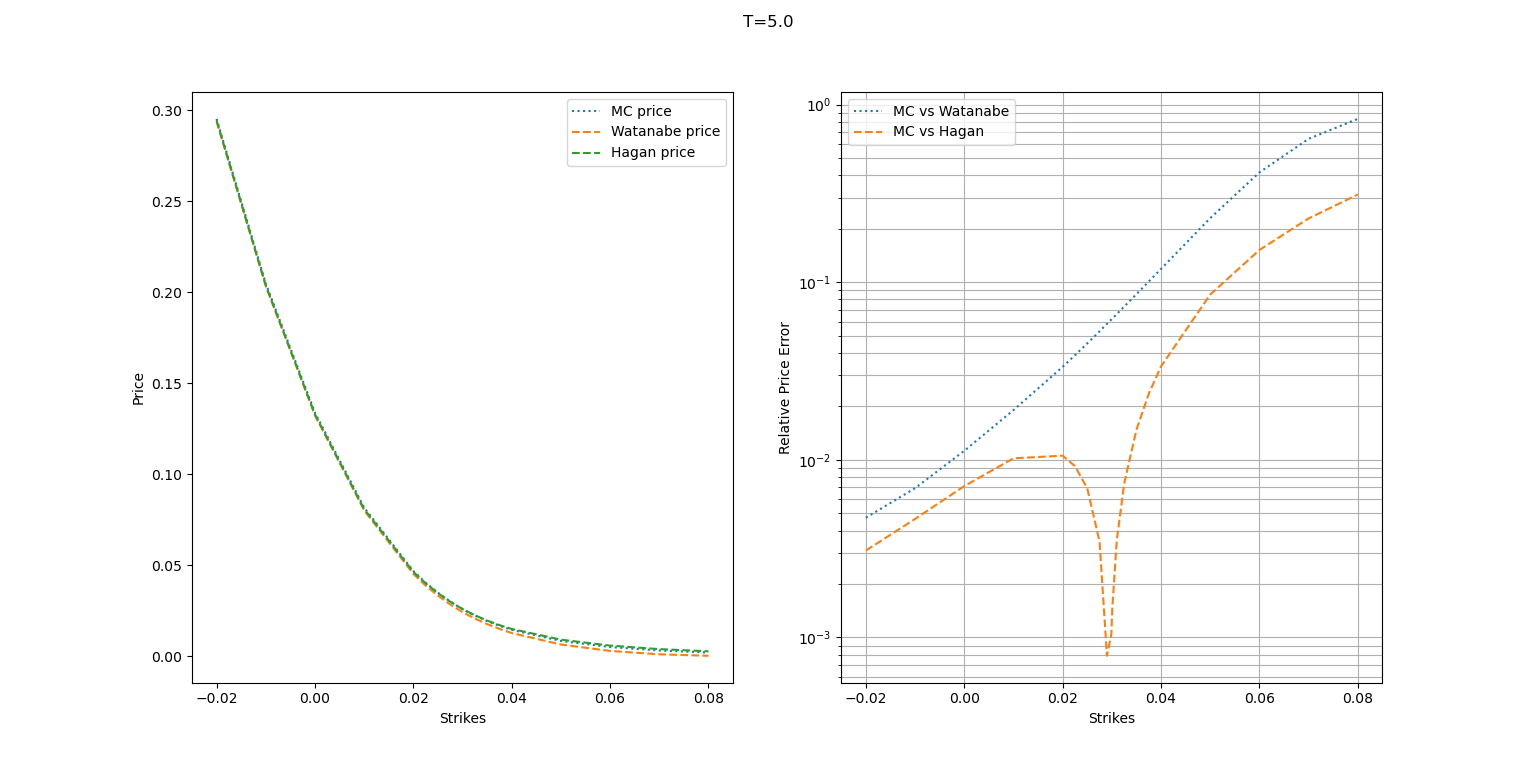

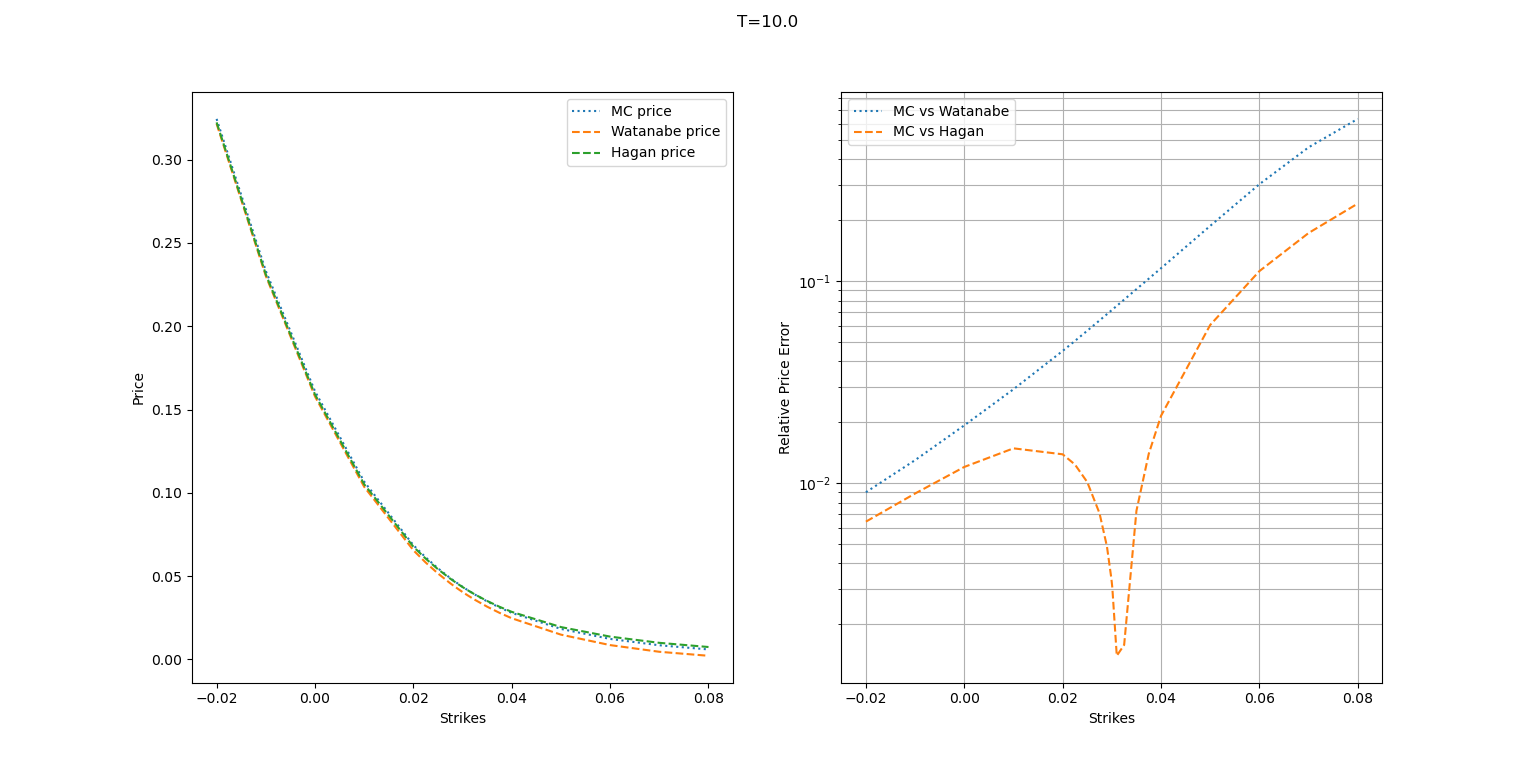

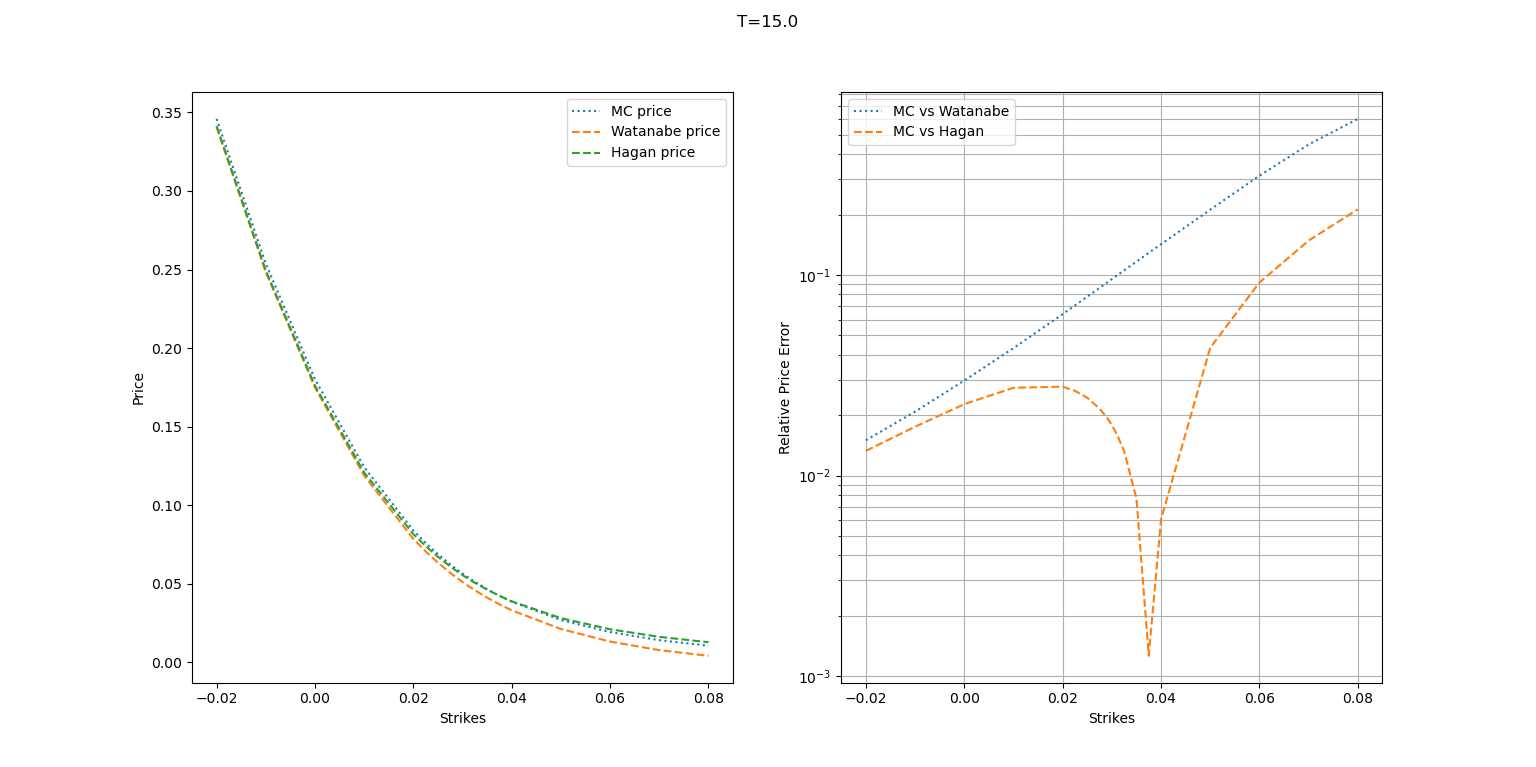

We will compare the accuracy of (5.3) with the Monte Carlo method and the approximation proposed in (Hagan et al. (2019)) for a range of strikes and maturities. As we have done in Section 4, we use SABR parameters calibrated to the swaption market.

The parameters used are listed in Table 1.

In this case, we can see that

When we replace the above equalities in the Watanabe’s call option expansion (5.3), we obtain the following approximation for .

(35)

In this analysis, we compare the numerical performance of the Watanabe approximation against Hagan’s approximation and a Monte Carlo simulation. The comparison is presented in figures 4, 5, and 6. Our observation is that Hagan’s approximation yields better results than Watanabe’s approximation. We also noticed that the accuracy of Watanabe’s approximation does not vary with maturity and declines linearly within the strike.

Figure 4: Comparison of quadratic call options using Watanabe’s expansion against the industry standards. The parameters considered are and Figure 5: Comparison of quadratic call options using Watanabe’s expansion against the industry standards. The parameters considered are and Figure 6: Comparison of quadratic call options using Watanabe’s expansion against the industry standards. The parameters considered are and

5.2 Quadratic option under stochastic local volatility

SLV-type models are widely used in the industry; see, for example, Bang (2019) and Henry-Labordère (2005). These models allow for control of the backbone through a layer of local volatility and its movement over time. In the interest rate market, a SABR dynamic is the market standard. We will consider a general SABR dynamics given by:

(36)

Here, and is a positive function that belongs to . To achieve an expansion for similar to (5.2), we will consider the next parametrization of the above dynamic

(37)

Lemma 5.6.

Under the dynamics given by (5.2), we can re-write the forward price dynamics as:

(38)

where under usual regularity conditions in we have that .

Proof.

The result is straightforward by iteratively applying the Itô-Taylor expansion.

∎

Then, as we have seen before, we can imply the terms.

(39)

Theorem 5.7(Stochastic local volatility expansion for quadratic payoffs).

Under the model (5.2), consider is given by (12), is standard normal pdf, the standard normal cdf and . Then, the 3rd order quadratic call option approximation price is

(40)

where .

The 3rd order quadratic put option approximation price is

(41)

where .

Finally, the 3rd order quadratic swap price is

(42)

Proof.

We consider the quadratic price expansion of Theorem 5.1 and the conditional expectations values calculated in (B.2.1), (B.2.2) and (B.2.3). Then, the quadratic call option price, unifying (E.5.1)

(E.5.2), and (E.5.3) along with Lemma 5.6. Then, we take the limit to obtain the quadratic call option price approximation. We proceed similarly with the quadratic put option price approximation and the quadratic swap option price.

∎

Remark 5.8.

We must note that when and , the model (5.2) is a pure local volatility model. But, when we substitute these parameters in (5.7), then we recover exactly (5.3).

Example 5.9.

If , then we recover the normal SABR model. For this case, and . Therefore (5.7) is reduced to (5.5)), which is consistent with the fact that the local volatility is the equivalent local volatility for the normal SABR model.

6 Future works

In a recent paper Skoufis (2024), the author proposes a closed formula for the convexity adjustment in the case of average RFR indexes when the underlying follow a time-dependent SABR model. This problem was addressed in Garcia-Lorite and Merino (2023) in the case of the Cheyette model with local volatility using Malliavin calculus. To make the paper self-contained, let us introduce the basic concepts. Let us define

and . In addition, we will suppose that

(43)

where with . From the definition of , we have that

Then, the issue is to compute when follow the dynamic (6). Using Itô formula, we obtain that

where

Let us suppose that we have an expansion similar to (4). Then, it is easy to show that

The challenge for future papers is to obtain the expansion of under a general SLV dynamic, this way could compute the convexity adjustment of CMS or average RFR, even the pricing of generic terminal payoff for a general SLV model.

7 Conclusions

In conclusion, we have proposed a new approach for pricing CMS derivatives. Our method uses Mallaivin’s calculus and Watanabe’s expansions. Firstly, we establish a model-independent connection between the price of a CMS derivative and the quadratic payoffs using Mallaivin calculus. Then, we extend the results of Watanabe’s expansions to the quadratic payoff case under local and stochastic local volatility. The approximations obtained are generic. To evaluate its accuracy, we compare the approximations numerically under the SABR model against the industry standards: Hagan’s approximation, and a Monte Carlo simulation. Our approximations are as precise as Hagan’s approximation, but they cover a wider range of models.

Appendix

We will consider , two independent Brownian motions.

Appendix A.1 Normal SABR

A.1.1 Calculation of

We have that

Therefore,

(44)

A.1.2 Calculation of

We will follow the same approach as in the previous section. Therefore, we have

In one hand, we obtain that

(45)

On other hand, we have that

(46)

(47)

Therefore, when combine it, we get that

(48)

A.1.3 Calculation of

From the definition of , we have that

Now, we will compute for each term. The easiest one is , due to the independence of and . We get

Then, we will compute the rest of the terms

(49)

For the last term, we must remember the next identity for a Brownian bridge with and

Alòs (2012)

Alòs E (2012) A decomposition formula for option prices in the Heston

model and applications to option pricing approximation. Finance Stoch

16(3):403–422, DOI 10.1007/s00780-012-0177-0

Alòs and García Lorite (2021)

Alòs E, García Lorite D (2021) Malliavin Calculus in Finance: Theory and

Practice. Chapman and Hall/CRC

Alòs et al. (2020)

Alòs E, Gatheral J, Radoičić R (2020) Exponentiation of conditional

expectations under stochastic volatility. Quantitative Finance (1):12–27,

DOI 10.1080/14697688.2019.1642506

Andersen and Piterbarg (2010)

Andersen L, Piterbarg V (2010) Interest Rate Modeling. Volume 3: Term Structure

Models. Atlantic Financial Press

Bang (2019)

Bang D (2019) Local-stochastic volatility for vanilla modeling: A tractable and

arbitrage free approach to option pricing. SSRN

Fang and Oosterlee (2009)

Fang F, Oosterlee CW (2009) A novel pricing method for European options based

on Fourier-cosine series expansions. SIAM J Sci Comput 31(2):826–848,

DOI 10.1137/080718061

Gulisashvili et al. (2020)

Gulisashvili A, Lagunas M, Merino R, Vives J (2020) Higher order approximation

of call option prices under stochastic volatility models. J Comput Finance

24(1):1–20, DOI 10.21314/JCF.2020.387

Hagan (2003)

Hagan P (2003) Convexity conundrums: Pricing cms swaps, caps and floors.

Wilmott 2003:38–45, DOI 10.1002/wilm.42820030211

Hagan and Woodward (2020)

Hagan P, Woodward D (2020) An end to replication. Preprint

Hagan and Woodward (1999)

Hagan PS, Woodward DE (1999) Equivalent Black volatilities. Applied

Mathematical Finance 6(3):147–157

Hagan et al. (2002)

Hagan PS, Kumar D, Lesniewski A, Woodward DE (2002) Managing smile risk.

Wilmott Magazine 2002(January):84–108

Henry-Labordère (2005)

Henry-Labordère P (2005) A general asymptotic implied volatility for

stochastic volatility models. Preprint

Henry-Labordère (2008)

Henry-Labordère P (2008) Analysis, Geometry, and Modeling in Finance:

Advanced Methods in Option Pricing. Chapman and Hall/CRC

Jacquier and Lorig (2015)

Jacquier A, Lorig M (2015) From characteristic functions to implied volatility

expansions. Advances in Applied Probability 47(3):837–857,

URL http://www.jstor.org/stable/43859532

Kunitomo and Takahashi (2003)

Kunitomo N, Takahashi A (2003) On validity of the asymptotic expansion approach

in contingent claim analysis. The Annals of Applied Probability

13(3):914–952, URL http://www.jstor.org/stable/1193231

Nagami (2021)

Nagami K (2021) Expansion method for pricing foreign exchange options under

stochastic volatility and interest rates. Journal of Computational Finance

25(2):29–50

Nualart (1995)

Nualart D (1995) The Malliavin Calculus and Related Topics, 2nd edn.

Springer-Verlag, Berlin

Skoufis (2024)

Skoufis G (2024) Sabr model convexity adjustment for the valuation of an

arithmetic average approach to option pricing. SSRN

DOI http://dx.doi.org/10.2139/ssrn.4694635

Takahashi and Yamada (2015)

Takahashi A, Yamada T (2015) On error estimates for asymptotic expansions with

malliavin weights: Application to stochastic volatility model. Mathematics of

Operations Research 40(3):513–541,

URL http://www.jstor.org/stable/24540963