Sparse Extended Mean-Variance-CVaR Portfolios with Short-selling

Abstract

This paper introduces a novel penalty decomposition algorithm customized for addressing the non-differentiable and nonconvex problem of extended mean-variance-CVaR portfolio optimization with short-selling and cardinality constraints. The proposed algorithm solves a sequence of penalty subproblems using a block coordinate descent (BCD) method while striving to fully exploit each component of the objective function or constraints. Through rigorous analysis, the well-posed nature of each subproblem of the BCD method is established, and closed-form solutions are derived where possible. A comprehensive theoretical convergence analysis is provided to confirm the efficacy of the introduced algorithm in reaching a local minimizer of this intractable optimization problem in finance, whereas generic optimization techniques either only capture a partial minimum or are not efficient. Numerical experiments conducted on real-world datasets validate the practical applicability, effectiveness, and robustness of the introduced algorithm across various criteria. Notably, the existence of closed-form solutions within the BCD subproblems prominently underscores the efficiency of our algorithm when compared to state-of-the-art methods.

1 Introduction

The mean-variance CVaR problem is crucial in finance as it provides a robust framework for optimizing portfolios by considering both expected returns (mean) and associated risks (variance and conditional value at risk). This approach helps investors balance the trade-off between maximizing returns and minimizing losses, enhancing portfolio performance and risk management in volatile markets [12, 18, 23] . Including short-selling is essential as it allows investors to profit from downward market movements, improving portfolio diversification and risk management by providing additional opportunities for profit generation in declining markets [6, 19, 24].

Moreover, sparse optimization plays a critical role in various fields such as machine learning, signal processing, and finance, offering efficient solutions for problems where the underlying data or parameters exhibit sparsity [3, 10, 13, 16, 21, 25, 26]. In portfolio optimization, having only a few assets can significantly impact diversification, potentially increasing exposure to individual asset risk and volatility, thus highlighting the importance of careful asset selection and risk management strategies. As such the cardinality constraints have been imposed in portfolio optimization models [2, 9, 14, 15, 17].

In this paper, we tackle the following extended mean-variance-CVaR portfolio problem that includes short-selling and nonconvex cardinality constraints:

| () | ||||

| subject to |

where with element-wise, for each . Also, we have

where is the risk-neutral interest rate, is the proportions of the weight invested in th stock and is the return vector. Problem () has been the subject of several research [7, 22, 20]. When , it reduces to the widely studied mean-CVaR with cardinality constraint, see for example [4, 8] and references therein.

Most recently, the authors in [7] applied the penalty decomposition method (PDM) to solve () and reported promising numerical results. Nevertheless, the full structure of the problem was not exploited. Therefore, we here introduce a novel penalty decomposition algorithm customized to fully leverage every component of the objective function in () along with its constraints. We go through a sequence of penalty subproblems that a saddle point of them is efficiently identified using a BCD method. We meticulously examine each corresponding subproblem within this BCD method to derive closed-form solutions whenever feasible. Specifically, to handle the norm in the objective function along with bound constraints, we introduce a new variable. Additionally, another variable is required to manage the softmax function in the objective function. Lastly, we resort to a third variable to address the cardinality constraint along with the short-selling constraints. Our discussions show how these new variables lead to structured subproblems and efficient We rigorously establish the convergence of our introduced algorithm towards a local minimizer of the non-differentiable problem () with non-convex constraints.

Section 2 introduces Algorithm 2, a penalty decomposition algorithm designed to tackle the non-differentiable and nonconvex problem (). This algorithm employs a block coordinate Algorithm 1 to address each penalty subproblem. We establish the well-posedness of these subproblems and derive closed-form solutions for three of them. The convergence analysis of both Algorithm 1 and Algorithm 2 is provided in Section 3, demonstrating that our introduced algorithm effectively reaches a local minimizer of (). Additionally, Section 4 presents extensive numerical results obtained from real-world data.

Notation. The complement of a set is denoted as . We use to represent its cardinality. For a natural number , we define as the set . Now, consider a set given by , which is a subset of . For any vector in , we denote the coordinate projection of with respect to the indices in as , which means that the th element of this vector equals to when belongs to , and it equals to for in . We determine whether a matrix is positive semidefinite or definite by the notations and , respectively. In this paper, we let for for and . For and , shows the Hadamard (element-wise) multiplication of and . Recall that

and

2 An Efficient Customized Penalty Decomposition Algorithm

Here, we propose our customized penalty decomposition algorithm for solving () that fully exploits all the available structures of the objective function and constraints of this problem.

2.1 Methodology

In this subsection, we elaborate on how we design our customized penalty decomposition algorithm. Observe that can equivalently reformulate this nonconvex problem as follows:

| (1) | ||||

| subject to | ||||

Specifically, we introduce to deal with sparsity, to handle , and to effectively manage the last term of the objective function in (). The constraints are also accordingly decoupled using these new variables such that we possibly can obtain closed-form solutions or if not, much simpler penalty subproblems in our customized penalty decomposition algorithm (see Subsection 2.2).

More precisely, suppose that

| (2) |

and

In our method, we consider a sequence of penalty subproblems as follows:

| () |

The idea is that by gradually increasing the value of towards infinity, we can effectively address the optimization problem (1). It is important to emphasize that () is yet nonconvex. However, the following BCD method efficiently converges to a saddle point of it (see Theorem 3.1).

We are now prepared to introduce our penalty decomposition algorithm, which begins with a positive penalty parameter and gradually increases it until convergence is achieved. Algorithm 1 handles the corresponding subproblem for a fixed . For the problem (), we assume having a feasible point denoted as in hand, which is easy to obtain. To present this algorithm and its subsequent analysis, we define:

| (3) |

We stop the inner loop if

| (4) |

and the outer loop when a convergence criterion is met:

| (5) |

2.2 Subproblems of Algorithm 1

We discuss how to efficiently solve the constrained subproblems presented in Algorithm 1 below.

2.2.1 Subproblem of

This subproblem () becomes the following convex quadratic optimization problem:

| () |

Since and , we have . Hence, this strictly convex problem has a unique solution, and, for , its KKT conditions are as follows:

| (6) |

Thus, . By letting

| (7) |

we see , which together with implies

This in turn yields

| (8) |

2.2.2 Subproblem of

Recall that we let so by slightly abusing the notation, this subproblem () is as follows:

| () |

To provide a closed-form solution to the latter problem, we first define the following generalized sparsifying operator.

Definition 2.1.

Let and and a natural number be given. Denote and . Then, the generalized sparsifying operator is defined as follows:

| (9) |

where is an index set corresponding to the largest components of in absolute value.

Lemma 2.1.

The solution to the problem () is defined in (9).

Proof.

For any with , we can write such that for some index set with . Hence, for any index set with , can be written as the following indexed problem:

which is equivalent to solving:

For any , we do not have any constraints, which shows that for all . Thus, by letting , it suffices to only focus on the following:

The KKT conditions for the global minimizer of this strictly convex problem can be written as:

Let , then it is known that for and and . It is easy to see that and for any , that is,

satisfy the given KKT conditions above. By recalling and defined inside (), we see

Therefore, we have

So, for any index specified above, the optimal value of the indexed problem is given by

where

and

Consequently, the optimal value becomes

This implies that the minimal value of is achieved when is maximal or equivalently when , where selects the largest components in absolute value. Therefore, a minimizer is defined in (9). ∎

2.2.3 Subproblem of

This subproblem () becomes the following generalized soft thresholding operator problem:

| () |

First, note that if then we have:

In this case if , if , and otherwise , for any , which can be rewritten as

| (10) |

Next, suppose that , due to the separability property of (), letting and , for , we shall focus on the following:

Let us assume that , then we have . Thus, if and , then . If , we must have . If , then . In the case of , taking derivative gives . Thus, if , and , we have . If , and , then we must have . Otherwise, and , so we have . For we also consider three different possibilities. In this case, optimality conditions are: . It can be shown that we must have and next depending on three scenarios that or , we get solutions reported in below:

If we summarize the above based on the original variables, we get the following:

2.2.4 Subproblem of and

This subproblem ( becomes the following:

| () | ||||

| subject to |

Proof.

We first show the existence of a solution. It is enough to show that the objective function is bounded below over its feasible set. Since , we have such that

where we used that whenever for and , and in (2.2.4). This implies that

| (14) | |||||

which establishes the problem () is bounded below and thus it has a solution.

Note that is unique because the Hessian of the objective function is positive definite with respect to . Once is known, it can be shown that is either zero or it must be equal to for some . To see this, without loss of generality, suppose for with , we have , thus () reduces to

If , then , otherwise we have . ∎

We need the KKT conditions for in our convergence analysis later:

| (15) |

Eventually, we point out that solving this convex problem can be done using a standard solver because it can be transformed into the following convex quadratic program with linear constraints:

| (16) | ||||

| subject to |

3 Convergence Analysis

In this section, we begin by examining Algorithm 1 to address the penalty subproblem () with a fixed . We demonstrate its efficacy in locating a saddle point for this subproblem. Subsequently, our attention shifts to Algorithm 2, where we illustrate its capability in identifying a convergent subsequence that converges a local minimizer of the original problem ().

3.1 Analysis of Algorithm 1

We analyze a sequence generated by Algorithm 1 and provide a customized proof that any such sequence obtains a saddle point of (). This justifies the use of Algorithm 1 for this nonconvex problem.

Lemma 3.1.

Let and with , with element-wise, for each and . Consider the iterates of Algorithm 1. Then, we have

| (17) |

Proof.

For simplicity, we drop the subscript whenever it is clear. First, simply . In Lemma 2.2, we also proved that for some . Thus, we have , which implies that

| (18) |

Also, clearly . Since from (2.1), we are remained to prove that is bounded. Recall the definitions in (7) and let . We see

and

Also,

Thus, the equation (8) together with leads to

Thus, whenever , we have Consequently, we can say that is bounded above and its bound is independent from . ∎

The provided lemma above proves that any sequence formed by Algorithm 1 is bounded and specifically, this bound is independent of whenever , which is the case for our penalty decomposition algorithm. Hence, every sequence produced by Algorithm 1 possesses at least one accumulation point. The subsequent theorem further confirms that each accumulation point is indeed a saddle point of ().

Theorem 3.1.

Let be a sequence generated by Algorithm 1 for solving (). Then, its accumulation point is a saddle point of the nonconvex problem (). Moreover, is a non-increasing sequence.

Proof.

By observing definitions of and in steps 6-9 of Algorithm 1, we get

| (19) |

This leads to the following:

| (20) | ||||

which shows that is non-increasing sequence. Since it is also bounded below when , we conclude its convergence.

Next, let be an accumulation point of , there exists a subsequence such that . The continuity of yields

By the continuity of and taking the limit of both sides of (3.1) as , we have

∎

3.2 Analysis of Algorithm 2

Here, we establish that our proposed customized penalty decomposition Algorithm 2 obtains a local minimum of the original nondifferentiable nonconvex problem (). Recall that Robinson’s constraint qualification conditions for a local minimizer of () is the existence of an index set such that and such that the following holds [11]:

| (26) |

Through the linearity of constraints in () except the cardinality constraint, it is easy to show that Robinson’s conditions above always hold for an arbitrary . Under these Robinson’s conditions, the KKT conditions for a local minimizer of () are the existence of Lagrangian multipliers with and with such that and the following holds:

| (28) |

Theorem 3.2.

Suppose that and with , with element-wise, for each and . Let be a sequence generated by Algorithm 2 for solving (). Then, the following hold:

-

(i)

has a convergent subsequence whose accumulation point satisfies . Further, there exists an index subset with such that .

-

(ii)

Suppose that Robinson’s condition given in (26) holds at with the index subset indicated above. Then, is a local minimizer of satisfying ().

Proof.

Due to Lemma 3.1, the sequence is bounded and therefore, has a convergent subsequence. For our purposes, without loss of generality, we suppose that the sequence itself is convergent. Let be its accumulation point. Under the given assumptions, in view of a similar technique used in Lemma 2.2, we can show that

Thus, using definition (2.1) and step 14 of Algorithm 2 leads to

and thus,

Hence, when ; proving that .

Let be defined such that , and for every and . Given that is a bounded sequence of indices, it possesses a convergent subsequence. This implies the existence of an index subset with and a subsequence from the aforementioned convergent subsequence, such that for all sufficiently large ’s. Consequently, because and , it follows that .

(ii) Recall that is a saddle point of () due to Theorem 3.1 and consequently, the KKT conditions of the problems (), (), (), and () yield:

| (29) |

Since for each we have and , from the part (i), we can conclude and . Further, and with . Next, by injecting the second, third, and fourth equations of (29) into its first one, we get the following:

| (30) | |||||

From the other side, and using the second equation in (29), after dropping the superscript , we get

Therefore, we (30) reduces to:

| (31) | |||||

Further, note that and .

We next show that is bounded under Robinson’s condition on . Suppose not and consider the following normalized sequence:

Since this normalized sequence is bounded, it has a convergent subsequence, without loss of generality itself, whose limit is given by such that . After dividing both sides of (31) by and then passing the limit , in virtue of the part (i) and boundedness of the remaining terms in (31), continuity of and , and boundedness of their subgradients, we get:

| (32) |

where with for and for and . In light of Robinson’s condition (26), there exists such that and . Since and , we see that . By multiplying (32) and using the equations above, we get the following:

which leads to

implying that . This is a contradiction! Consequently, the sequence is bounded and has a convergent subsequence. Let be the limit point of this sequence, through passing limit in (31) and applying the results of the part (i), one can see the KKT conditions (29) are satisfied.

So far, we have proved that all the KKT conditions in (29) hold at except its second equation. To show this, recall the fourth equation in (30):

By taking limit as , boundedness of shown in (3.1), continuity of , and considering part (i), we see that

Therefore, we showed all the KKT conditions hold at . Together with the linearity of constraints in () except the cardinality one, we conclude that Algorithm 2 obtains a local minimizer of this problem under the given assumptions. ∎

4 Numerical Results

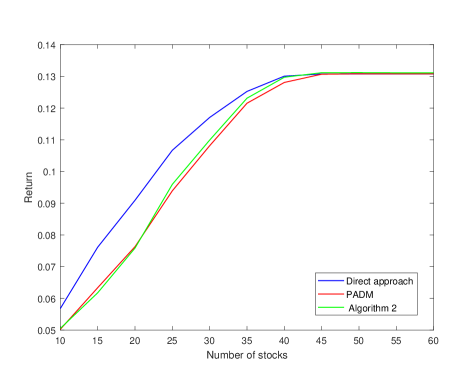

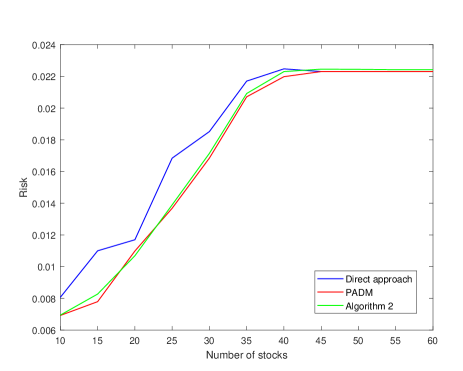

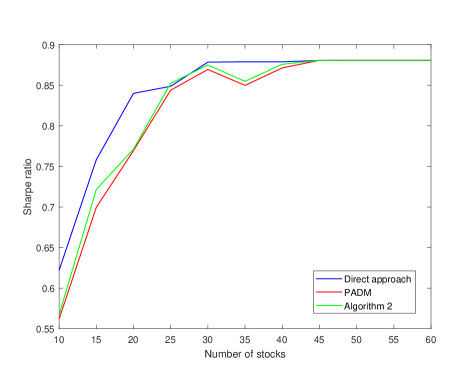

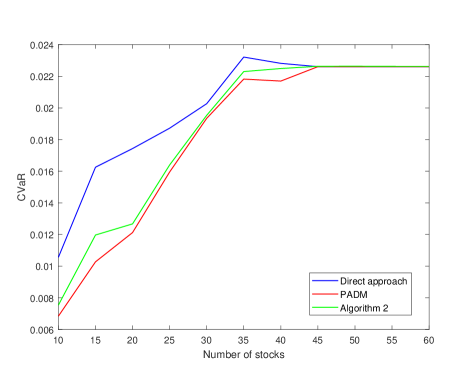

In this section, we compare the performance of Algorithm 2 with the algorithm in [7]. The direct approach of solving () by CVX-Mosek is also reported for gap computing. We use the data of S&P index for 2018-2021 with 120 stocks when , , and . Moreover, we apply the Geometric Brownian Motion (GBM) model in [1] to generate scenarios. In the PADM algorithm of [7], the initial penalty parameter is set to and it is updated with the factor 3. The inner loop is stopped when . It terminates with a partial minimum if . In Algorithm 2, the initial penalty parameter is set to as well and it is updated with the factor 3. In this Algorithm, the inner loop is stopped when and the outer loop is stopped when a convergence criterion is met . All computations are performed in MATLAB R2017a on a 2.50 GHz laptop with 4 GB of RAM, and CVX 2.2 ([5]) is used to solve the optimization models. The results comparing returns, risks, Sharpe ratios, CVaR values, CPU times, and gaps for different values are reported in Table 1. The gap in this table is where is the return (risk, Sharpe ratio, CVaR) for direct solution approach and is the return (risk, Sharpe ratio, CVaR) for the PADM algorithm or Algorithm 2.

These results show that both Algorithm 2 and PADM are extremely faster than the direct solution approach. Also, Algorithm 2 is about twice as fast as the PADM while having competitive gaps of returns, risks, CVaR, and Sharpe ratios; for all values. These results for also are depicted in Figure 1 for different numbers of stocks showing the competitiveness of Algorithm 2. These results confirm that Algorithm 2 is a better alternative to the direct solution approach than the PADM in [7].

5 Conclusion

In conclusion, this paper designs a penalty decomposition algorithm customized for tackling the challenging sparse extended mean-variance-CVaR portfolio optimization problem in finance. This algorithm needs to solve a sequence of penalty subproblems. By employing a block coordinate method, we adeptly exploit every structure in the problem to manage each penalty subproblem, establishing their well-posed nature and deriving closed-form solutions wherever feasible. Our comprehensive convergence analysis demonstrates the efficacy of our introduced algorithm in efficiently reaching a local minimizer of this non-differentiable and nonconvex optimization problem. Furthermore, extensive numerical experiments conducted on real-world datasets validate the practical applicability, effectiveness, and robustness of our introduced algorithm across various evaluation criteria. Overall, this research contributes significantly to the field of portfolio optimization by offering a novel and efficient solution approach with promising practical implications in finance.

| Model | m=1000 | m=3000 | m=5000 | ||||

| Direct approach | |||||||

| Return | 0.1202 | 0.1195 | 0.1178 | ||||

| Risk | 0.0201 | 0.0188 | 0.0161 | ||||

| Sharpe ratio | 0.8470 | 0.8728 | 0.0242 | ||||

| CVaR | 0.0191 | 0.0211 | 0.0194 | ||||

| CPU time | 472.8531 | 2.0029e+03 | 2.0029e+03 | ||||

| PADM | |||||||

| Return | 0.1134 | 0.1087 | 0.1109 | ||||

| Risk | 0.0169 | 0.0159 | 0.0144 | ||||

| Sharpe ratio | 0.8709 | 0.8625 | 0.9242 | ||||

| CVaR | 0.0177 | 0.0183 | 0.0217 | ||||

| CPU time | 53.2698 | 119.9078 | 312.8421 | ||||

| Return gap | 0.0060 | 0.0097 | 0.0062 | ||||

| Risk gap | 0.0031 | 0.0028 | 0.0016 | ||||

| Sharpe ratio gap | 0.0130 | 0.0055 | 0.0030 | ||||

| CVaR gap | 7.4739e-04 | 0.0019 | 0.0023 | ||||

| Algorithm 2 | |||||||

| Return | 0.1151 | 0.1108 | 0.1111 | ||||

| Risk | 0.0173 | 0.0162 | 0.0147 | ||||

| Sharpe ratio | 0.8755 | 0.8695 | 0.9174 | ||||

| CVaR | 0.0188 | 0.0197 | 0.0224 | ||||

| CPU time | 38.4394 | 58.4394 | 61.2368 | ||||

| Return gap | 0.0045 | 0.0078 | 0.0060 | ||||

| Risk gap | 0.0028 | 0.0025 | 0.0014 | ||||

| Sharpe ratio gap | 0.0154 | 0.0018 | 0.0065 | ||||

| CVaR gap | 3.0090e-04 | 0.0015 | 0.0018 |

References

- [1] W Farida Agustini, Ika Restu Affianti, and Endah RM Putri. Stock price prediction using geometric brownian motion. In Journal of Physics: Conference Series, volume 974, page 012047. IOP Publishing, 2018.

- [2] Weichuan Deng, Paweł Polak, Abolfazl Safikhani, and Ronakdilip Shah. A unified framework for fast large-scale portfolio optimization. Data Science in Science, 3(1):2295539, 2024.

- [3] Jin-Hong Du, Yifeng Guo, and Xueqin Wang. High-dimensional portfolio selection with cardinality constraints. Journal of the American Statistical Association, pages 1–13, 2022.

- [4] Fernando GDC Ferreira and Rodrigo TN Cardoso. Mean-cvar portfolio optimization approaches with variable cardinality constraint and rebalancing process. Archives of Computational Methods in Engineering, 28(5):3703–3720, 2021.

- [5] Michael Grant, Stephen Boyd, and Y Ye. Cvx: Matlab software for disciplined convex programming, version 2.0 beta, 2013.

- [6] Gustavo Grullon, Sébastien Michenaud, and James P Weston. The real effects of short-selling constraints. The Review of Financial Studies, 28(6):1737–1767, 2015.

- [7] Abdelouahed Hamdi, Tahereh Khodamoradi, and Maziar Salahi. A penalty decomposition algorithm for the extended mean–variance–cvar portfolio optimization problem. Discrete Mathematics, Algorithms and Applications, 16(03):2350021, 2024.

- [8] Ken Kobayashi, Yuichi Takano, and Kazuhide Nakata. Bilevel cutting-plane algorithm for cardinality-constrained mean-cvar portfolio optimization. Journal of Global Optimization, 81(2):493–528, 2021.

- [9] AmirMohammad Larni-Fooeik, Hossein Ghanbari, Mostafa Shabani, and Emran Mohammadi. Bi-objective portfolio optimization with mean-cvar model: An ideal and anti-ideal compromise programming approach. In Progressive Decision-Making Tools and Applications in Project and Operation Management: Approaches, Case Studies, Multi-criteria Decision-Making, Multi-objective Decision-Making, Decision under Uncertainty, pages 69–79. Springer, 2024.

- [10] Man-Fai Leung and Jun Wang. Cardinality-constrained portfolio selection based on collaborative neurodynamic optimization. Neural Networks, 145:68–79, 2022.

- [11] Zhaosong Lu and Yong Zhang. Sparse approximation via penalty decomposition methods. 2012.

- [12] Khin T Lwin, Rong Qu, and Bart L MacCarthy. Mean-var portfolio optimization: A nonparametric approach. European Journal of Operational Research, 260(2):751–766, 2017.

- [13] Hossein Moosaei, Ahmad Mousavi, Milan Hladík, and Zheming Gao. Sparse l1-norm quadratic surface support vector machine with universum data. Soft Computing, 27(9):5567–5586, 2023.

- [14] Ahmad Mousavi and George Michailidis. Mean-reverting portfolios with sparsity and volatility constraints. arXiv preprint arXiv:2305.00203, 2023.

- [15] Ahmad Mousavi and George Michilidis. Statistical proxy based mean-reverting portfolios with sparsity and volatility constraints. International Transactions in Operational Research, 2024.

- [16] Ahmad Mousavi, Mehdi Rezaee, and Ramin Ayanzadeh. A survey on compressive sensing: classical results and recent advancements. Journal of Mathematical Modeling, 8(3):309–344, 2020.

- [17] Ahmad Mousavi and Jinglai Shen. A penalty decomposition algorithm with greedy improvement for mean-reverting portfolios with sparsity and volatility constraints. International Transactions in Operational Research, 2022.

- [18] Diana Roman, Kenneth Darby-Dowman, and Gautam Mitra. Mean-risk models using two risk measures: a multi-objective approach. Quantitative Finance, 7(4):443–458, 2007.

- [19] Pedro AC Saffi and Kari Sigurdsson. Price efficiency and short selling. The Review of Financial Studies, 24(3):821–852, 2011.

- [20] Yu Shi, Xia Zhao, Xin Yan, et al. Optimal asset allocation for a mean-variance-cvar insurer under regulatory constraints. American Journal of Industrial and Business Management, 9(07):1568, 2019.

- [21] Ralph E Steuer, Yue Qi, and Maximilian Wimmer. Computing cardinality constrained portfolio selection efficient frontiers via closest correlation matrices. European Journal of Operational Research, 313(2):628–636, 2024.

- [22] A Taik, R Aboulaich, R Ellaia, and S El Moumen. The mean-variance-cvar model for portfolio optimization modeling using a multi-objective approach based on a hybrid method. Mathematical Modelling of Natural Phenomena, 5(7):103–108, 2010.

- [23] Pieter M van Staden, Duy-Minh Dang, and Peter A Forsyth. The surprising robustness of dynamic mean-variance portfolio optimization to model misspecification errors. European Journal of Operational Research, 289(2):774–792, 2021.

- [24] Shuang Wang, Li-Ping Pang, Shuai Wang, and Hong-Wei Zhang. Distributionally robust mean-cvar portfolio optimization with cardinality constraint. Journal of the Operations Research Society of China, pages 1–31, 2023.

- [25] Siwei Xia, Yuehan Yang, and Hu Yang. High-dimensional sparse portfolio selection with nonnegative constraint. Applied Mathematics and Computation, 443:127766, 2023.

- [26] Ziping Zhao, Rui Zhou, and Daniel P Palomar. Optimal mean-reverting portfolio with leverage constraint for statistical arbitrage in finance. IEEE Transactions on Signal Processing, 67(7):1681–1695, 2019.