Functional Bilevel Optimization for Machine Learning

Abstract

In this paper, we introduce a new functional point of view on bilevel optimization problems for machine learning, where the inner objective is minimized over a function space. These types of problems are most often solved by using methods developed in the parametric setting, where the inner objective is strongly convex with respect to the parameters of the prediction function. The functional point of view does not rely on this assumption and notably allows using over-parameterized neural networks as the inner prediction function. We propose scalable and efficient algorithms for the functional bilevel optimization problem and illustrate the benefits of our approach on instrumental regression and reinforcement learning tasks, which admit natural functional bilevel structures.

1 Introduction

Bilevel optimization is a class of methods for solving optimization problems with a hierarchical structure [Von Stackelberg, 2010]. These problems typically require optimizing the parameters of two interdependent objectives, an inner-level objective and an outer-level objective . The hierarchical structure arises by taking into account the dependence of the inner-level solution on the outer-level variable. Introduced in machine learning for model selection by Bennett et al. [2006] and later for sparse feature learning [Mairal et al., 2012], gradient-based bilevel optimization methods have recently gained a lot of attraction [Feurer and Hutter, 2019, Lorraine et al., 2019, Franceschi et al., 2017] as they offer an alternative to computationally expensive grid search procedures for multiple hyper-parameter tuning. Since then, numerous new applications have emerged, such as meta-learning [Bertinetto et al., 2019], auxiliary task learning [Navon et al., 2021], reinforcement learning [Hong et al., 2023, Liu et al., 2021a, Nikishin et al., 2022], inverse problems [Holler et al., 2018] and invariant risk minimization [Arjovsky et al., 2019, Ahuja et al., 2020].

Bilevel problems are notoriously challenging to solve, even in the most favorable well-defined bilevel setting, where the inner-level problem admits a unique solution. These challenges arise due to the need for approximating both an inner-level solution and its sensitivity to the outer-level variable when performing gradient-based optimization. Several methods, intended for the well-defined setting were devised to address these challenges, such as Iterative Differentiation (ITD, Baydin et al., 2017), or Approximate Implicit Differentiation (AID, Ghadimi and Wang, 2018), often resulting in scalable algorithms with strong convergence guarantees [Domke, 2012, Gould et al., 2016, Ablin et al., 2020, Arbel and Mairal, 2022a, Blondel et al., 2022, Liao et al., 2018, Liu et al., 2022, Shaban et al., 2019].

The well-defined bilevel setting allows devising provably efficient algorithms. However, it typically requires the inner-level objective to be strongly convex. This assumption is often limiting for modern machine learning applications where the inner-level variables are the parameters of a neural network. In these cases, the inner-level problem can possess multiple solutions, making the dependence on the outer-level variable ambiguous [Liu et al., 2021b]. In principle, considering amended versions of the bilevel problem can resolve such an ambiguity. This is the case of optimistic/pessimistic versions of the problem, often considered in the literature on mathematical optimization, where the outer-level objective is optimized over both outer and inner variables, under the optimality constraint of the inner-level variable [Dempe et al., 2007, Ye and Ye, 1997, Ye and Zhu, 1995, Ye et al., 1997]. While tractable methods were recently proposed to solve them [Liu et al., 2021a, b, 2023, Kwon et al., 2024], it is unclear how well would the resulting solutions behave on unseen data in the context of machine learning. For instance, when using an over-parameterized models for the inner-level problem, their parameters must be further optimized for the outer-level objective, possibly resulting in over-fitting [Vicol et al., 2021]. More recently, Arbel and Mairal [2022b] proposed a game formulation involving a selection map to deal with multiple inner-level solutions. Such a formulation justifies the use of ITD/AID outside the well-defined bilevel setting, by viewing those methods as approximations to the Jacobian of the selection map. However, the resulting justifications only hold under rather strong geometric assumptions.

In this work, we identify a functional structure that often arises in bilevel optimization for machine learning problems, and propose a method exploiting this structure to bypass many of the challenges mentioned above. We start from the observation that many bilevel problems arising in machine learning involve an inner-level objective that is optimized to learn a model, approximating some optimal prediction function, that is then provided to the outer-level objective . Furthermore, the inner-level objective is often strongly convex in the outputs of the prediction function (e.g., the mean squared error) even though it might be non-convex as a function of model parameters. These observations enable us to view the machine learning model, typically a neural network, as a function approximation tool within a larger functional space where the bilevel formulation is well defined without the need for strong convexity with respect to model parameters. Formally, we consider bilevel problems involving a prediction function optimized by the inner-level problem over a Hilbert space of functions defined over an input space and taking values in a finite dimensional vector space . The optimal prediction function is then evaluated in the outer level to optimize an outer-level parameter in a finite dimensional space giving rise to the following functional bilevel structure:

| (FBO) | ||||

The inner-level objective is assumed to be strongly convex in the prediction function for any outer-parameter value , thus ensuring the uniqueness of the solution . The outer-level objective depends on the outer parameter and the optimal prediction function , which implicitly depends on the outer parameter . The strong convexity assumption with respect to the prediction function is much weaker than the strong convexity assumption with respect to model parameters made in classical bilevel formulations for machine learning, and often holds in practice. For instance, consider a supervised prediction task with pairs of features/labels drawn from some empirical training data distribution, formulated as a regularized empirical minimization problem:

| (1) |

where is the space of square integrable functions w.r.t. the distribution of , whereas is a strongly convex regularization function (e.g. ) and is a positive outer parameter controlling the amount of regularization. The strong convexity of the regularization in ensures that the inner-level objective is also strongly convex with respect to . Nonetheless, the optimal prediction function can be a highly nonlinear function of the input , that may be approximated, for instance, by an overparameterized deep neural network. This is the first work to propose a functional point of view that can leverage deep networks for function approximation. The closest works are either restricted to kernel methods [Rosset, 2008, Kunapuli et al., 2008] and thus cannot be used for deep learning models, or propose abstract algorithms that can only be implemented for finite Hilbert spaces [Suonperä and Valkonen, 2024].

We propose an efficient algorithm to solve bilevel problems with the inner objective similar to Equation 1. More precisely, we present a method to solve (FBO) when both outer and inner objectives can be expressed as expectations over data of some point-wise objectives that only require access to the outputs of a prediction function . Additionally, the inner objective is assumed to be strongly convex in the output of the prediction function. This setting covers many problems in machine learning, where the prediction function belongs to a Hilbert space of square-integrable functions (see Sections 5.1, 5.2, and Appendix A). Our method uses a functional version of the implicit function theorem [Ioffe and Tihomirov, 1979], and the adjoint sensitivty method [Pontryagin, 2018], to derive an expression of the total gradient . The resulting expression involves an adjoint function that captures the constraints imposed on the optimal inner prediction function. The adjoint is obtained by solving a regression problem in corresponding to a well-defined functional linear system. Both the prediction and the adjoint functions can be approximated using parametric models, such as neural networks, that are learned using standard optimization tools, resulting in scalable and efficient algorithms. The proposed method, functional implicit differentiation (FuncID), can be viewed as a functional version of AID, albeit the functional point of view provides advantages that are absent in the original method. AID approximates the solution of a finite dimensional linear system, which involves second order derivatives of the inner objective with respect to the parameters of the model approximating the prediction function . Such a linear system might be ill-posed when the inner objective is non-convex in the model parameters, thus resulting in instabilities [Arbel and Mairal, 2022b]. Instead, FuncID only requires second order information with respect to the output of to solve the functional linear system. Our method leverages the strong convexity of the inner objective in the output of to obtain well-defined solutions while also reducing time and memory cost.

Before describing the FuncID method, we discuss some related works in Section 2, and present a theoretical framework for functional implicit differentiation in an abstract Hilbert space in Section 3, before specializing it to the common scenario in machine learning, where the Hilbert space is an space and the objectives are expectations of suitable point-wise losses. In Section 4, we present the FuncID algorithm and illustrate it experimentally on instrumental regression and reinforcement learning tasks in Section 5.

2 Related Work

Bilevel optimization in machine learning.

Two families of bilevel methods are prevalent in machine learning literature due to their scalability: iterative (or “unrolled”) differentiation (ITD, Baydin et al., 2017) and Approximate Implicit Differentiation (AID, Ghadimi and Wang, 2018). ITD approximates the optimal inner-level solution using an ”unrolled” function obtained by applying a sequence of differentiable optimization steps. The outer variable is then optimized by back-propagation through all or parts of these steps to minimize the outer objective [Shaban et al., 2019, Bolte et al., 2024]. When the inner-level is strongly convex, the approximation error of the gradient is known to decrease linearly with the number of optimization steps, albeit at an increased computational and memory cost [Grazzi et al., 2020, Theorem 2.1]. ITD is popular, both in the context of bilevel problems [Grazzi et al., 2020, Marrie et al., 2023] and back-propagation-through-time (BPTT) algorithms [Williams and Peng, 1990], for its simplicity and availability in main deep learning libraries [Bradbury et al., 2018]. However, instabilities in the optimization process are known to arise, especially when the inner-level objective is non-convex [Pascanu et al., 2013, Bengio et al., 1994, Arbel and Mairal, 2022b]. The second approach, AID, uses the Implicit Function Theorem (IFT) to derive the Jacobian of the inner-level solution with respect to the outer variable [Lorraine et al., 2019, Pedregosa, 2016]. It involves (approximately) solving a finite-dimensional linear system to find an adjoint vector representing the optimality constraints imposed on the inner-level solution. AID leverages the hierarchical structure of the bilevel problem through the IFT and offers strong convergence guarantees when the inner objective is smooth and strongly convex [Ji et al., 2021, Arbel and Mairal, 2022a]. However, without strong convexity, the resulting linear system might become ill-posed, as it depends on the possibly degenerate Hessian of the the inner objective with respect to the inner level variables. Degeneracy of the Hessian can occur when the inner variables represent parameters of an overparameterized deep neural network, a common scenario in machine learning that can result in instabilities when using AID. By contrast, our proposed approach does not suffer from this issue even when employing deep networks for function approximation.

Adjoint sensitivity method.

The adjoint sensitivity method [Pontryagin, 2018] is a general technique used to efficiently differentiate a controlled variable with respect to a control parameter. In bilevel optimization, AID can be seen as a direct application of a finite-dimensional version of the adjoint method [Margossian and Betancourt, 2021, Section 2]. Infinite-dimensional versions have also been considered to differentiate solutions of ordinary differential equations [Margossian and Betancourt, 2021, Section 3] with respect to some parameter defining these solutions. In particular, it has been recently exploited in machine learning for optimizing the parameters of a vector field describing an ordinary differential equation (ODE) [Chen et al., 2018]. There, the vector field of the ODE is parameterized by a neural network that is optimized to generate a dynamical system matching some observations. The adjoint sensitivity method provides an efficient alternative to the costly and unstable process of back-propagation through ODE solvers, when differentiating the dynamical system with respect to the parameters of the vector field defining it. The method only requires solving an adjoint ODE, constructed given the original ODE and the loss function, to compute the gradient updates to the parameters, thus resulting in improved performance [Jia and Benson, 2019, Zhong et al., 2019, Li et al., 2020]. The adjoint method for ODEs has also been recently adapted to meta-learning [Li et al., 2023], where the inner optimization procedure is seen as the evolution of an ODE whose gradients are obtained by the adjoint ODE. In all these works, the infinite-dimensional structure arises from applying the adjoint method to solutions of an ODE, where the solutions are functions of the time variable. In the present work, we also consider an infinite-dimensional version of the adjoint sensitivity method. However, unlike the aforementioned works, the infinite-dimensional structure arises from application of the adjoint method to solutions of general learning problems which are functions of input data rather than a single time variable.

Amortization.

Recently, several methods exploited the idea of amortization to approximately solve bilevel problems [MacKay et al., 2019, Bae and Grosse, 2020]. These methods introduce a parametric model called the hypernetwork [Ha et al., 2017, Brock et al., 2018, Zhang et al., 2019] that is optimized to directly predict the inner-level solution, given the outer-level parameter as input. Amortized methods do not fully exploit the implicit dependence in the two levels of a bilevel problem. Instead, they split the two levels into two independent optimization problems: (1) learning the hyper-network on a neighborhood of the outer-level parameter , and (2) doing first-order descent on using the learned hyper-network as a replacement for the optimal inner-level solution. These amortized approaches are unlike ITD, AID, or our functional implicit differentiation method, neither of which explicitly model the parametric dependence between the optimal inner-level solution and the outer level variable . Amortization techniques are closer to amortized variational inference [Kingma and Welling, 2014, Rezende et al., 2014], where a parametric model is learned to directly produce approximate samples from a posterior distribution, given an observation, instead of applying costly sampling algorithms for each new observation. In the bilevel framework, amortization methods typically perform well when the inner solution has a simple predictable dependence on the outer-level variable and might fail otherwise [Amos et al., 2023, pages 71-72]. By contrast, the functional implicit differentiation framework can adapt to the complex implicit dependence between the inner solution and the outer-level parameter.

3 Functional Bilevel Optimization

The functional bilevel problem (FBO) requires finding the optimal prediction function by optimizing the inner objective in a Hilbert space for each value of the outer-level parameter . The optimal solution can then be used for characterizing the local variations of at a point , assuming it is Fréchet differentiable, by evaluating its partial derivatives denoted as in and in :

| (2) |

However, solving (FBO) by using a first-order method further requires characterizing the implicit dependence of the optimal prediction function on the outer-level parameter to evaluate the total gradient in . Indeed, assuming that is also Fréchet differentiable (this assumption will be discussed later), the gradient may be obtained by an application of the chain rule:

| (3) |

The Fréchet derivative is a linear operator acting on functions in and measures the sensitivity of the optimal solution on the outer variable. We will refer to this quantity as the “Jacobian” in the rest of the paper. While the expression of the gradient in Equation 3 might seem intractable in general, we will see in Section 4 a class of practical algorithms to estimate it. In the present section, we derive general results that guide the construction of these algorithms, starting with a functional version of implicit differentiation.

3.1 Functional implicit differentiation

Our starting point is to characterize the dependence of on the outer variable. To this end, we rely on the following implicit differentiation theorem (proven in Appendix B) which can be seen as a functional version of the one used in AID [Domke, 2012, Pedregosa, 2016], albeit, under a much weaker strong convexity assumption that holds in most practical cases of interest.

Theorem 3.1 (Functional implicit differentiation).

Consider problem (FBO) and assume that:

-

•

For any , there exists for which is -strongly convex for any near .

-

•

has finite values and is Fréchet differentiable on for all .

-

•

is Hadamard differentiable on (in the sense of Definition B.1 in Section B.1).

Then, is uniquely defined and is Fréchet differentiable with a Jacobian given by:

| (4) |

Theorem 3.1 provides a formal expression of the Jacobian as the solution of a linear system in the Hilbert space . The strong convexity assumption on the inner-level objective ensures the existence and uniqueness of the solution , while the differentiability assumptions on and ensure that the map is Fréchet differentiable. Similar conclusions could be obtained by directly applying the implicit function theorem for abstract Banach spaces [see Ioffe and Tihomirov, 1979]. However, such a theorem requires making the stronger assumption that is continuously Fréchet differentiable. This assumption turns our to be quite restrictive, in our setting, as it would only hold for objectives that are quadratic in (see [Nemirovski and Semenov, 1973, Corollary 2, p 276] and discussions in [Noll, 1993, Goodman, 1971]). To allow more generality, Theorem 3.1 employs the weaker notion of Hadamard differentiability for . Hadamard differentiability is widely used in statistics, in particular for deriving the delta-method, as it holds for a much larger class of functionals [van der Vaart and Wellner, 1996, Chapter 3.9], and happens to be the right notion of differentiability in our setting as we further show in Section 4.

Similarly to AID, constructing the full Jacobian can be avoided, since only a Jacobian-vector product is needed when computing the total gradient . The result in Proposition 3.2 below, relies on the adjoint sensitivity method [Pontryagin, 2018] to provide a more convenient expression for and is proven in Section B.2.

Proposition 3.2 (Functional adjoint sensitivity).

Under the same assumption on as in Theorem 3.1 and further assuming that is jointly differentiable in and , the total objective is differentiable with given by:

| (5) |

where the adjoint function is an elemen of that minimizes the quadratic objective:

| (6) |

The new expression of the total gradient provided by Proposition 3.2 requires finding an adjoint function in by optimizing a strongly convex quadratic objective in . The strong convexity of the adjoint objective guarantees the existence of a unique minimizer and is a direct consequence of the Hessian operator being positive definite by the strong convexity of the inner-objective in . Equation 5 suggests that, in addition to finding the optimal prediction , obtained by solving the inner-level optimization problem, computing the total gradient requires optimizing the quadratic objective (6) to find the adjoint function . Both optimization problems occur in the same function space and are equivalent in terms of conditioning since their Hessian operators at the optimum are identical.

Connection with parametric implicit differentiation. As shown in Appendix C, it is possible to approximate the functional problem in Equation FBO with a parametric bilevel problem where the inner-level functions are restricted to have a parametric form with parameters . There, the inner-level variable becomes instead of the function (see Equation PBO of Appendix C). One can then apply standard algorithms for bilevel optimization such as AID which are derived from the parametric version of implicit differentiation and require differentiating twice w.r.t. the parametric model. However, for models such as deep neural networks, the inner objective in the parametric formulation is no longer strongly convex in the inner-variables (the model’s parameters ), since the parametric Hessian can be non-positive and even degenerate (see Proposition C.1 of Appendix C). The resulting total gradient is, in general, different from the one in Equation 5 (see Proposition C.2 of Appendix C) and can cause numerical instabilities, particularly when using algorithms such as AID for which an adjoint vector is obtained by solving a quadratic problem defined by the parametric Hessian matrix. Moreover, if the model admits multiple solutions, the Hessian is likely to be degenerate making the implicit function theorem inapplicable. On the other hand, the functional implicit differentiation requires finding an adjoint function by solving a positive definite quadratic problem in which is always guaranteed to have a solution, even when the inner-level prediction function is approximated by a sub-optimal solution, thanks to the strong convexity of the lower-level objective . This stability property w.r.t. sub-optimal solutions is crucial for deriving practical algorithms such as the one presented in Section 4, where the optimal prediction function is approximated within a parametric family, such as neural networks.

3.2 Functional bilevel optimization in spaces

We specialize the abstract results in Section 3.1 to a more common situation in machine learning when both inner and outer level objectives of FBO are given as expectations of some point-wise functions over observed data. More precisely, we consider two data distributions and defined over a product space and denote by the Hilbert space of functions that are square integrable under , where is a finite dimensional vector space (i.e. . Given an outer parameter space , we consider the following functional bilevel problem:

| (7) | ||||

where , are point-wise loss functions defined on and where the outer expectation is taken w.r.t. while the inner one is w.r.t. . This setting encompasses a large family of problems in deep learning of which a few are discussed in Sections 5.1 and 5.2, and in Appendix A and is a particular case of Equation FBO. In addition to modelling a large family of prediction functions, the Hilbert space of square-integrable functions allows us to obtain more concrete expressions for the the total gradient , from which we derive practical algorithms in Section 4.

The following proposition, proved in Appendix D, makes mild technical assumptions on , and and provided in Section D.1 to ensure that the conditions on and in Proposition 3.2 hold and derives expression for the total gradient in the form of expectations under and .

Proposition 3.3 (Functional Adjoint sensitivity in spaces.).

Under Assumptions (B), (C), (D), (E), (F), (G) and (A) on , Assumptions (H), (I) and (J) on and Assumptions (K) and (L) on and stated in Section D.1, the conditions on and in Proposition 3.2 hold, so that the total gradient of is expressed as with being the minimizer of the objective in Equation 6. Moreover, , and admit the following expressions:

| (8) | ||||

| (9) |

where and are the partial derivatives of in its first and second arguments (i.e. and ), is the cross-derivative of w.r.t. to and , while is the second-order derivatives of w.r.t. to .

The assumptions on and ensure their second moments are finite and that the marginal of under has a bounded Radon-Nikodym derivative w.r.t. the marginal of under . These are mild requirements to obtain a well-defined problem in Equation 7 by ensuring that square integrable functions under are also square integrable under . The assumptions on and are essentially integrability, differentiability and Lipschitz continuity assumptions on the objectives and in addition to the strong convexity of in its second argument. These assumptions typically hold for objectives such as the squared error or the cross entropy objective as shown in Proposition D.1 of Section D.1.

4 Methods for Functional Bilevel Optimization in Spaces

We propose a flexible class of algorithms for solving the functional bilevel problem in spaces described in Section 3.2 when samples from distributions and are available. We call the method Functional Implicit Differentiation (FuncID) and provide its general structure in Algorithm 1. FuncID relies on three main components:

-

1.

Empirical objectives. These approximate the three population objectives , and as empirical expectations over samples from inner and outer datasets and , distributed according to and .

-

2.

Function approximation. The search space for both the prediction and adjoint functions is restricted to parametric spaces with finite-dimensional parameters and . Approximate solutions and to the optimal functions and are obtained using standard optimization procedures over the empirical objectives.

-

3.

Total gradient approximation. FuncID estimates the total gradient using the empirical objectives, and the approximations and of the prediction and adjoint functions.

Sections 4.1, 4.2 and 4.3 present the three components of FuncID while Section 4.4 discusses its computational cost.

4.1 From population losses to empirical objectives

We assume that we have access to two datasets and consisting of pairs of samples in and in that we use to define an empirical version of the population objectives in Equation 7. We may assume, for simplicity, that the samples are i.i.d. samples of and , respectively. However, such an assumption may be relaxed, for instance, when using samples from a Markov chain or a Markov Decision Process, which can still be used to approximate the population objectives. Additionally, if and are very similar, the two datasets might be equal or be two separate sets as long as they provide a good approximation to the population distributions. For scalability in the size of datasets, we consider a mini-batch setting where batches of data are sub-sampled from datasets and used to define the approximate objectives.

Approximating both inner and outer level objectives in Equation 7 is straightforward and can be done, for instance, using the following empirical versions:

Adjoint objective. Using the expression of from Proposition 3.3, we derive a finite-sample approximation of the adjoint loss by replacing the population expectations by their empirical counterparts. More precisely, assuming we have access to an approximation to the inner-level prediction function obtained by a procedure that we describe later in Section 4.2, we consider the following empirical version of the adjoint objective:

| (10) | ||||

The adjoint objective in Equation 10 requires computing a Hessian-vector product with respect to the output of the prediction function . Meanwhile, AID methods necessitate a Hessian-vector product with respect to the parameters of a parameterized version of , which are usually of a much higher dimension then . We detail the computational cost differences of FuncID and AID in Section 4.4.

4.2 Approximate prediction and adjoint functions

To find approximate solutions to the prediction and adjoint functions we rely on three steps: 1) specifying parametric search spaces for both functions, 2) introducing optional regularization to prevent overfitting and, 3) defining a gradient-based optimization procedure using the approximate objectives defined in Section 4.1.

Parametric search space.

We approximate both prediction and adjoint functions using parametric search spaces. We consider a parametric family of functions defined by a map over a set of parameters . We then constrain the prediction function to be a model of the form . We only need to be continuous and differentiable almost everywhere so that back-propagation is applicable [Bolte et al., 2021]. Importantly, we do not require twice differentiability of , as AID would, because the Hessian in functional implicit differentiation is computed w.r.t. the output of , and not w.r.t. its parameters. To allow for more generality, we can consider a different parameterized model for approximating the adjoint function, which is defined over a possibly different set of parameters . We then constrain the adjoint to be of the form . Again, we require it to be continuous and differentiable almost everywhere. In practice, we use the same parameterization, typically a neural network, for both the inner-level and the adjoint models.

Regularization.

With the empirical objectives and parametric search spaces defined earlier, we can directly optimize the parameters of both the inner-level model and the adjoint model . However, due to finite samples, it is often desirable to introduce a regularization to these empirical objectives to obtain approximations that generalize better to unseen data. The method does not impose any constraint on the choice of the regularization, as it is simply introduced to account for finite samples effect. Therefore, we may regularize both inner and outer objectives using functions and such as the ridge penalty or any other commonly used regularization.

Optimization.

All the operations that require differentiation in FuncID, including Hessian-vector products, and learning the models and , can be implemented using standard optimization procedures leveraging automatic differentiation packages such as Pytorch [Paszke et al., 2019] or Jax [Bradbury et al., 2018]. The function InnerOpt() defined in Algorithm 2 optimizes the parameters of the inner model for a given value of , initialization and data . The optimization procedure consists of gradient updates to the inner model’s parameters using any standard optimizer. The algorithm then returns a pair of optimized parameters and the corresponding inner model , the latter being the approximate solution to the inner-level problem, i.e. . Similarly, AdjointOpt() defined in Algorithm 3 optimizes the adjoint model’s parameters in the same way as Algorithm 2 with gradient updates and whose output defines the approximate adjoint function . Other optimization procedures can be used for finding the adjoint function especially for some particular losses and model choices for which closed-form solutions are possible to obtain, as we exploit in some of our experiments in Section 5.

4.3 Total gradient estimation

We provide the algorithmic steps for estimating the theoretical total gradient . We exploit Proposition 3.3 to derive Algorithm 4, which allows us to approximate the total gradient using observed data points, after computing the approximate solutions and . Algorithm 4 defines a function TotalGrad() for approximating the total gradient given approximations and a batch of data . There, we decompose the gradient into two terms: , an empirical approximation of in Equation 9 using the approximations and representing the explicit dependence of the outer variable on , and , an approximation to the implicit gradient term in Equation 9. The term is simply obtained by replacing the expectation in Equation 9 by an empirical average over a batch of inner-level data, and using the approximations and instead of the exact solutions.

4.4 Computational cost and scalability

Algorithm 1 has a double loop structure similar to AID, where the inner loops sequentially update the prediction and adjoint models using scalable algorithms such as stochastic gradient descent [Robbins and Monro, 1951, Bottou, 2010]. It employs a warm-start procedure, which consists of initializing both model parameters for each new outer-level iteration using the ones obtained at the previous iteration. A similar warm-start strategy is provably known to be beneficial in the case of AID [Arbel and Mairal, 2022a] and was also empirically useful in our experiments.

The optimization of the prediction function in the inner-level optimization loop is similar to AID, although the total gradient computation differs significantly. Unlike AID, Algorithm 1 does not require differentiating through the parameters of the prediction model when estimating the total gradient . This property results in an improved cost in time and memory in most practical cases as shown in Table 1 and Figure 1. More precisely, AID requires computing Hessian-vector products of size , which corresponds to the number of hidden layer weights of the neural network . While FuncID only requires Hessian-vector products of size , i.e. the output dimension of . In many practical cases, the network’s parameter dimension is much larger than its output size , which results in considerable benefits in terms of memory when using FuncID rather than AID, as shown in Figure 1 (left). Furthermore, unlike AID, the overhead of evaluating Hessian-vector products in FuncID is not affected by the time cost for evaluating the prediction network. When is a deep network, such an overhead increases significantly with the network size, making AID significantly slower (Figure 1 (right)).

5 Applications

We consider two applications of the functional bilevel optimization problem: two stage least squares regression (2SLS) and model-based reinforcement learning. To illustrate its effectiveness we compare it with other approaches to bilevel optimization such as AID or ITD as well as state-of-the-art methods for each of the considered applications. We provide a general implementation of FuncID in PyTorch [Paszke et al., 2019] and use it for the 2SLS application. Our implementation is compatible with any standard optimizer (such as Adam [Kingma and Ba, 2015]) and supports standard regularization techniques. For the reinforcement learning application, we leverage an existing implementation in JAX [Bradbury et al., 2018] of the model-based RL from Nikishin et al. [2022] and build on it to apply funcID. To ensure fair comparison, we conduct experiments with comparable computational budgets for hyper-parameter tuning of all methods. Moreover, we use the same neural network architectures for all methods and repeat the experiments multiple times with different random seeds.

5.1 Two-stage least squares regression (2SLS)

Two-stage least squares regression is a class of methods often encountered in causal representation learning such as instrumental regression or proxy causal learning [Stock and Trebbi, 2003]. 2SLS was recently addressed using bilevel optimization approaches showing promising results [Xu et al., 2021b, a, Hu et al., 2023]. We focus on 2SLS for Instrumental Variable (IV) regression as it is a widely-used statistical framework for handling endogeneity in econometrics [Blundell et al., 2007, 2012], medical economics [Cawley and Meyerhoefer, 2012], sociology [Bollen, 2012], and, recently, for handling confounders in off-line reinforcement learning [Fu et al., 2022].

Problem formulation.

In an IV problem, the goal is to learn a model that approximates the true structural function using independent samples from a data distribution , where is an instrumental variable. The function describes the true effect of a treatment on an outcome . The main challenge in IV is the existence of an unobserved confounder influencing both and additively and making the recovery of using standard regression impossible Figure 2. Instead, if the instrumental variable affects the outcome only through the treatment and is independent from the confounder , one can use it to recover the direct relationship between the treatment and the outcome using the 2SLS framework under a mild assumption on the confounder [Singh et al., 2019]. The regression problem is then replaced by a variant that averages the effect of the treatment conditionally on :

| (11) |

Directly estimating the conditional expectation is hard in general. Instead, it is easier to express it, equivalently, as the solution of another regression problem predicting from :

| (12) |

Both equations result in the bilevel formulation in Equation 7 with , and the point-wise losses and given by and . It is, therefore, possible to directly apply Algorithm 1 to learn as we illustrate below.

Experimental setup.

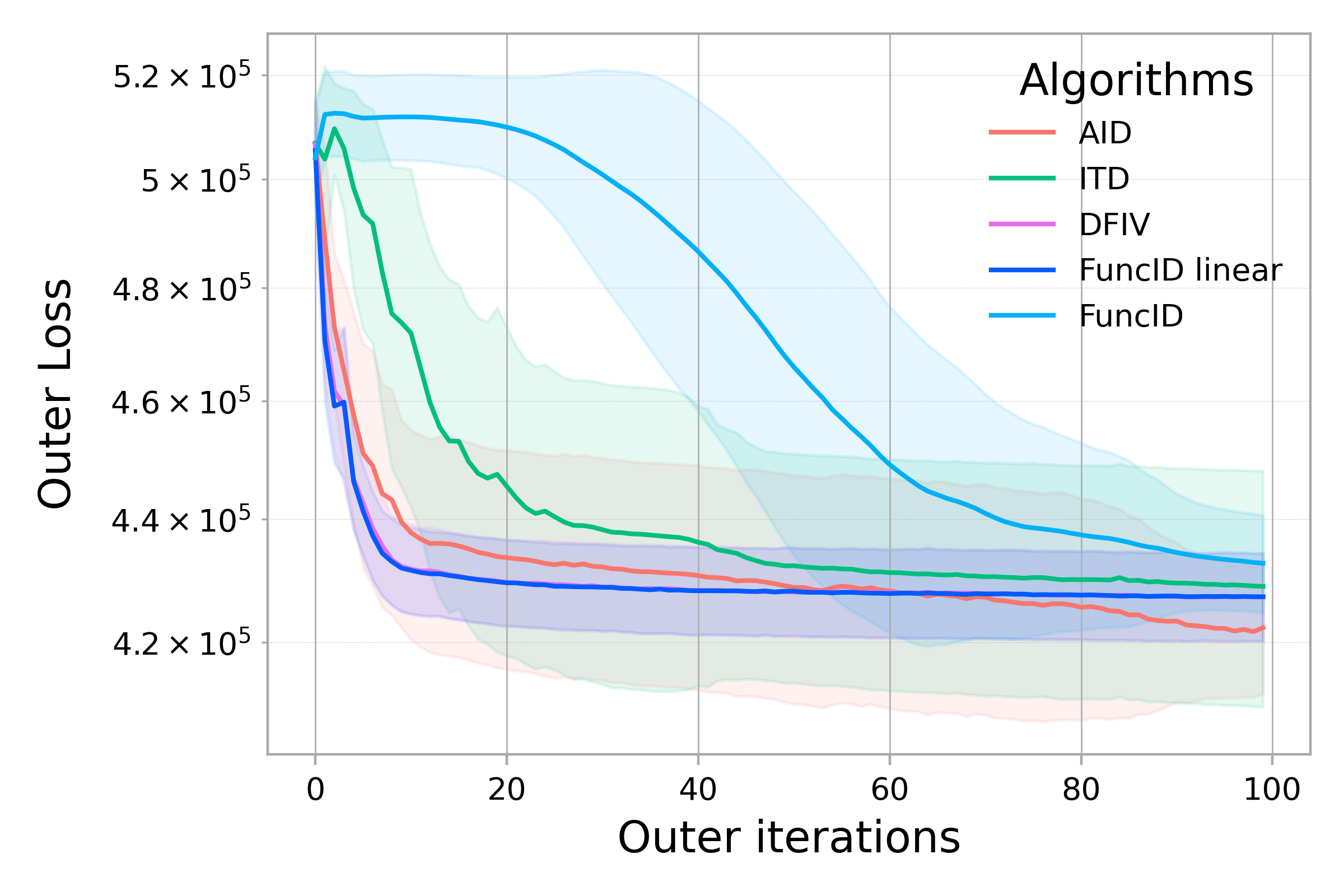

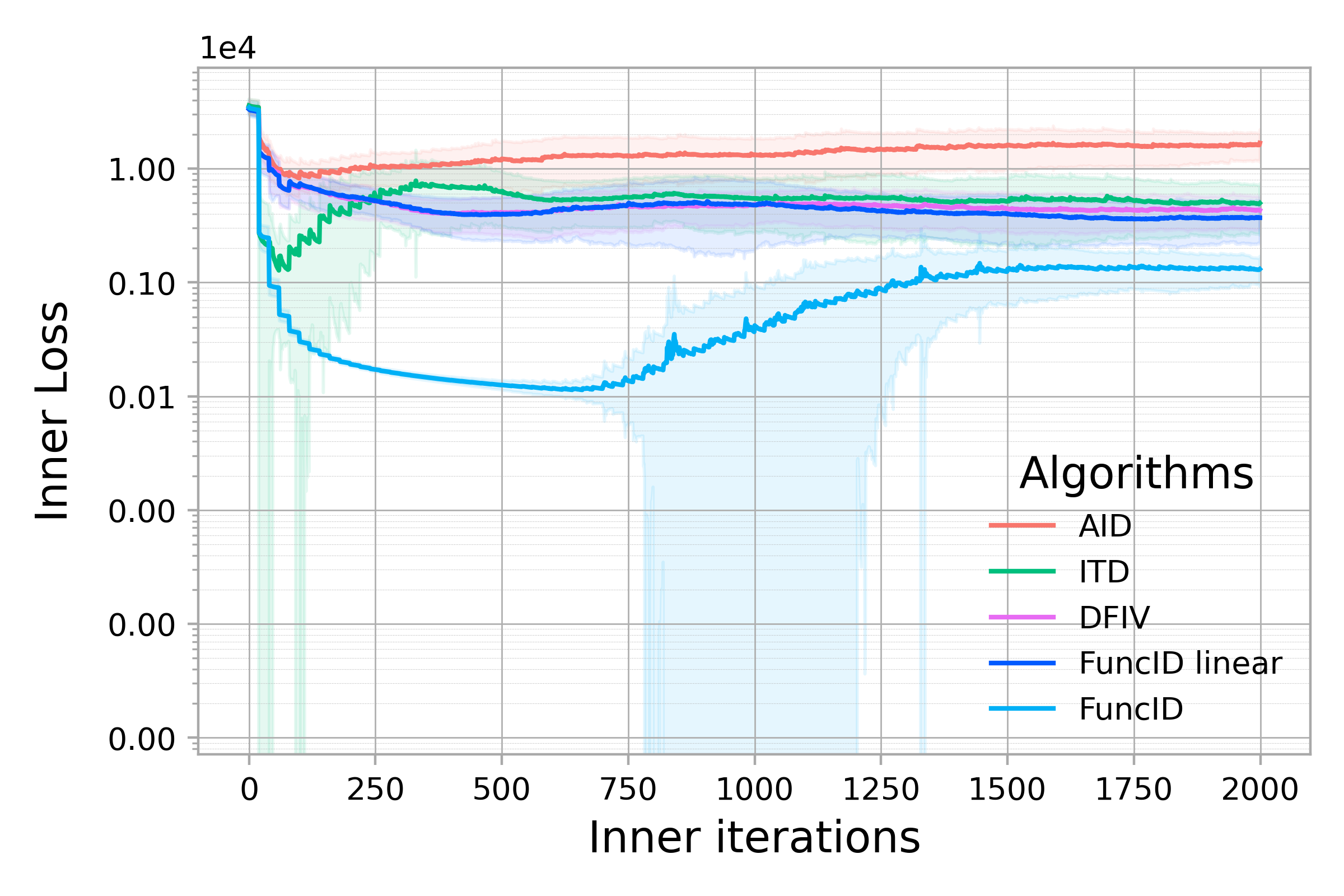

We solve a benchmark IV problem on the dsprites dataset [Matthey et al., 2017], a collection of synthetic images each representing a single object generated using five latent parameters: shape, scale, rotation, and posX, posY positions on the image coordinates. In this setting, the treatment variable are the images, the hidden confounder is the second coordinate posY, while the other four latent variables form the instrumental variable . The outcome is some predefined but unknown structural function of that is contaminated by the confounder as described in Section E.1. We closely follow the setting of Deep Feature Instrumental Variable Regression (DFIV) dsprites experiment described by Xu et al. [2021a, Section 4.2], which reports state-of-the-art performance. There, the prediction function and the structural model are neural networks that are optimized to solve the bilevel problem in Equations 11 and 12. We consider two versions of our method to solve this problem, both of which use an adjoint network that has the same architecture as the inner prediction function: FuncID, which optimizes all parameters of the adjoint network and FuncID linear, which only learns the last layer in closed-form while setting the hidden layer parameters to those of the inner prediction function. We then compare our method with DFIV, AID and ITD using the same network architectures and the same computational budget for selecting hyper-parameters. Full details on the network architectures, hyperparameters and the training setting are described in Section E.2.

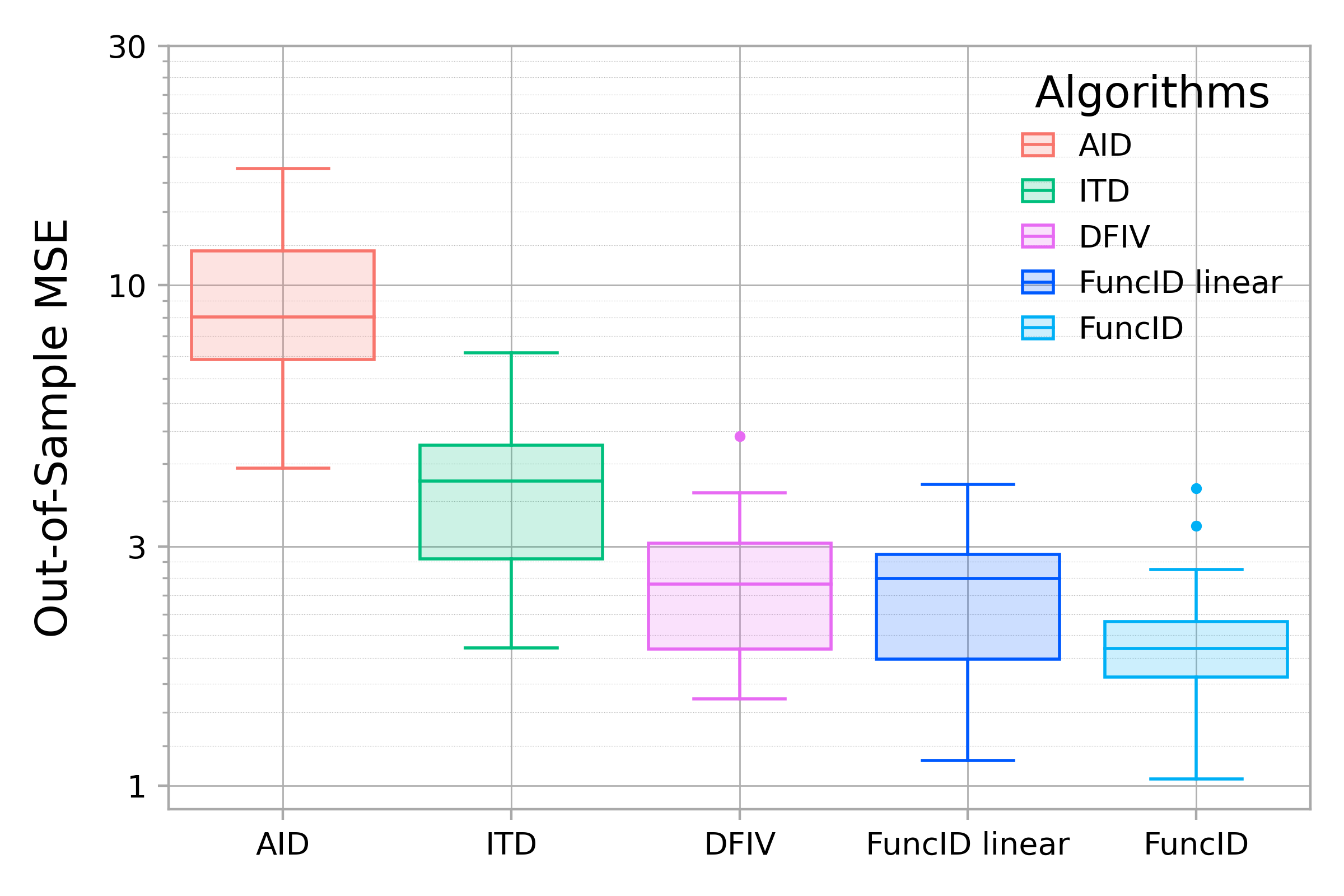

Results.

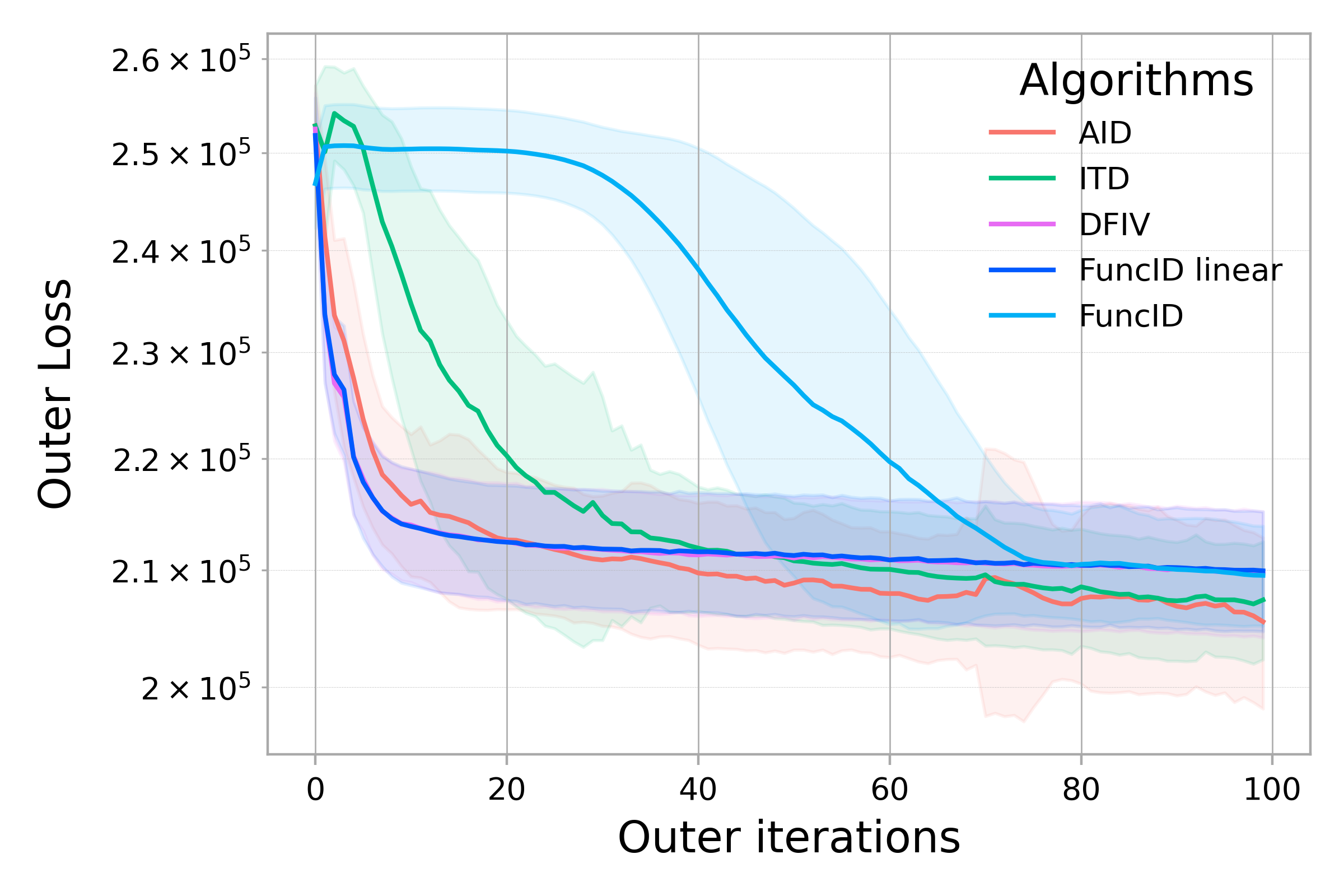

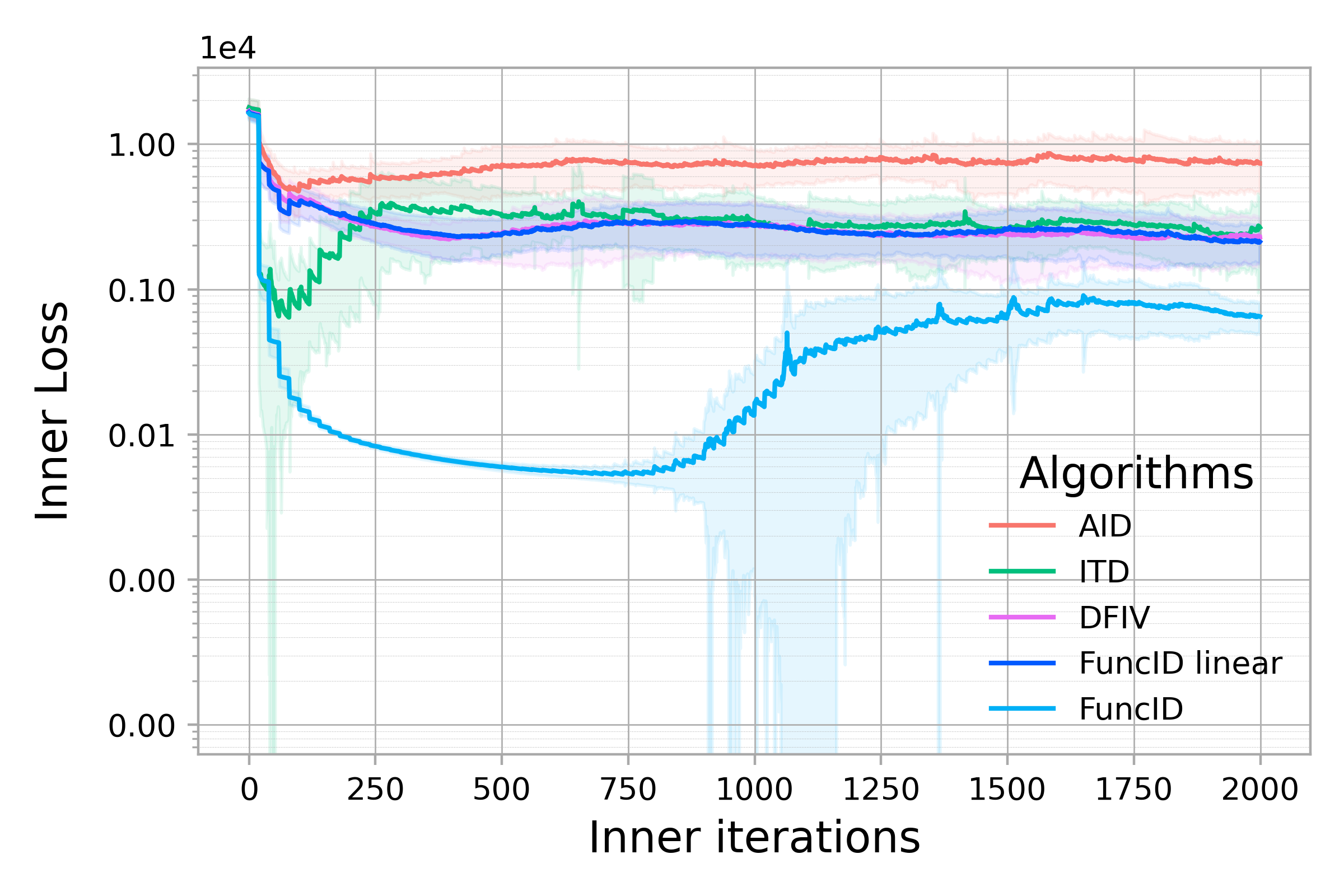

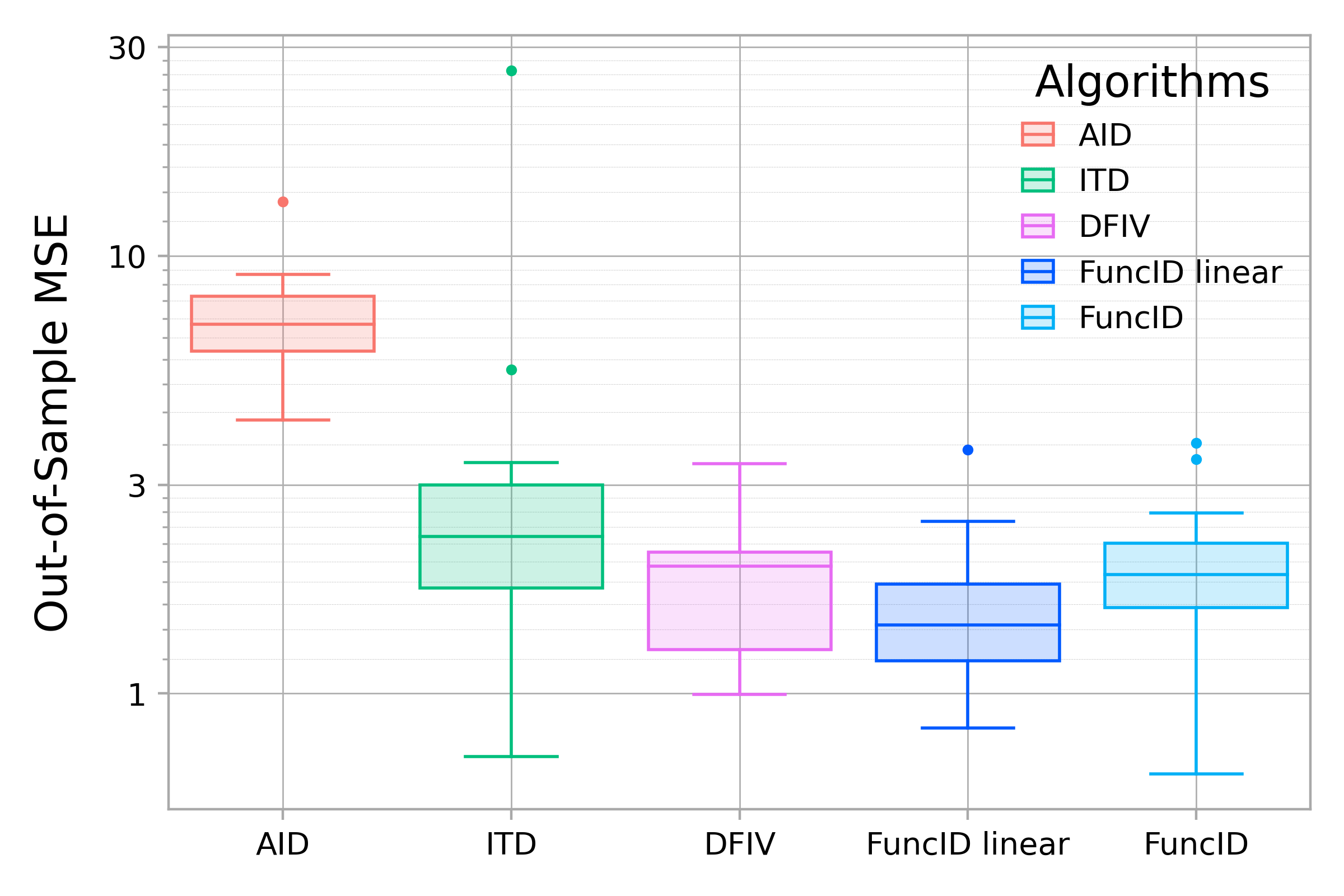

Figure 3 compares the structural models learned by the different methods using 5K training samples (see Figure 5 in Section E.3 for similar results using 10K samples). Figure 3 (left) shows the out-of-sample mean squared error of the learned structural models compared to ground truth outcomes (uncontaminated by the confounding noise ), while Figure 3 (middle and right) show the evolution of the outer and inner objectives as a function of iterations. Our method FuncID improves over the reported state-of-the-art performance of DFIV [Xu et al., 2021a] on the dsprites dataset in terms of out-of-sample error. On the other hand, AID is the worst performing method followed by ITD. This suggests that, on the contrary to FuncID, the parametric point of view adopted by AID and ITD does not take full advantage of the functional structure in Equations 11 and 12. All methods recover similar outer losses (middle Figure 3), while inner solutions differ (right Figure 3) with FuncID obtaining the lowest value. This suggests that a smaller value for the outer loss in a 2SLS problems does not always imply a better generalization performance on the evaluation set, since imposing the correct inner-level constraint is also important. Overall, FuncID solves the considered 2SLS problem efficiently by effectively taking into account its functional structure, leading to better generalization.

5.2 Model-based reinforcement learning

Model-based reinforcement learning (RL) has proven to be a learning paradigm that naturally gives rise to bilevel optimization, since several components of an RL agent need to be learned using different objectives. Recently, Nikishin et al. [2022] showed that casting model-based reinforcement learning as a bilevel problem can result in better tolerance to model-misspecification. Our experiments show that the functional bilevel framework yields improved results even when the model is well-specified, suggesting a broader use of the bilevel formulation for model-based RL.

Problem formulation.

In model-based RL, the Markov Decision Process (MDP) is approximated by a probabilistic model with parameters that can predict the next state and reward , given a pair where is the current environment state and is the action of an agent. A second model can be used to approximate the action-value function that computes the expected cumulative reward given the current state-action pair. Traditionally, the action-value function is learned using the current MDP model, while the latter is learned independently from the action-value function using Maximum Likelihood Estimation (MLE) [Sutton, 1991].

In the bilevel formulation of model-based RL proposed in Nikishin et al. [2022], the inner-level problem is to learn the optimal action-value function using the current MDP model and minimizing the Bellman error relatively to the MDP model. The inner-level objective can be written as an expectation of a point-wise loss with samples , obtained from the interaction between the agent and its environment:

| (13) |

Here the future state and reward are replaced by the MDP model predictions and . In practice, samples from are obtained using a replay buffer. The buffer accumulates data over several episodes of interactions with the environment, and can therefore be considered independent of the agent’s policy. The point-wise loss function represents the error between the action-value function prediction and the expected cumulative reward given the current state-action pair:

with a lagged version of (exponentially averaged network) and a discount factor. The MDP model is learned implicitly using the optimal function , by minimizing the Bellman error relatively to the true MDP w.r.t. :

| (14) |

Equations 14 and 13 define a bilevel problem as in Equation 7, where , , and the point-wise losses and are given by: and . Therefore, we can directly apply Algorithm 1 to learn both the MDP model and the optimal action-value function .

Experimental setup.

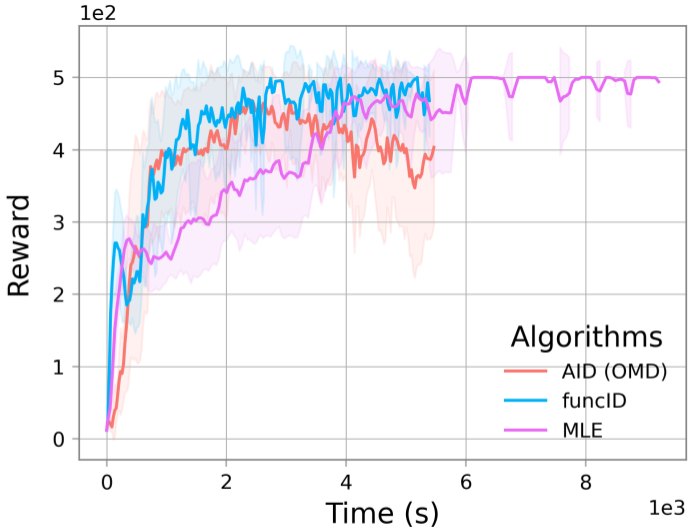

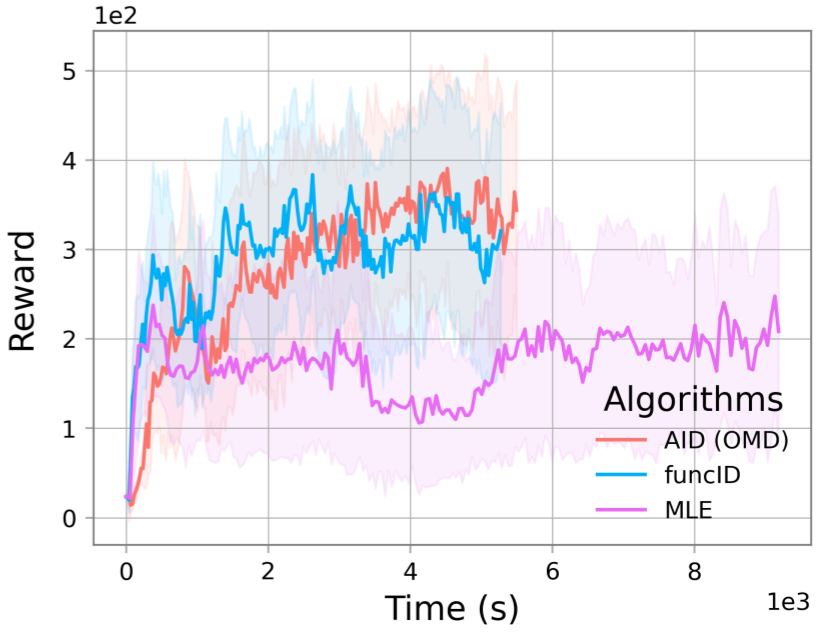

We apply our FuncID method to the CartPole learning control problem, a well-known benchmark task in reinforcement learning [Brockman et al., 2016, Nagendra et al., 2017]. In this problem, a cart is attached to a pole via a joint, and the maximum reward is achieved when the agent can balance the pole upright by moving the cart horizontally. Following Nikishin et al. [2022], we use a model-based approach and consider two choices for the MDP model: a well-specified network, that can accurately represent the ground truth MDP, and a misspecified one, with a limited number of hidden layer units. Less hidden layer units limits the model’s capacity to represent the ground truth MDP. Using the bilevel formulation in Equations 13 and 14, we compare our method, FuncID, with the Optimal Model Design (OMD) algorithm from Nikishin et al. [2022], a variant of AID. Additionally, we compare against a commonly used single-level formulation of model-based RL that uses MLE to learn the MDP model independently from the action-value function [Sutton, 1991]. For the adjoint function unsed in funcID, we exploit the structure of the adjoint objective to provide a simple closed-form expression as further discussed in Section F.1. We then closely follow the experimental setup in Nikishin et al. [2022] and provide full details and hyperparameters in Section F.2.

Results.

Figure 4 shows the evolution of the reward during training for FuncID, OMD and MLE in both well-specified and misspecified settings. FuncID is consistently amongst the best performing methods in both settings. In the well-specified setting, where OMD under-performs MLE and attains only a reward of , FuncID attains the maximum possible reward of performing as well as MLE (left Figure 4). In the miss-specified setting, FuncID demonstrates a performance comparable to OMD and significantly better than MLE (right Figure 4). Additionally, we find that FuncID tends to converge faster than MLE (see Figure 6 in Section F.3) and results in consistently better prediction error than OMD (see Figure 7 in Section F.3). These results are consistent with those in Nikishin et al. [2022], and support the hypothesis that MLE might prioritize reducing errors in predictions in the misspecified setting, leading to the model fitting irrelevant features in the data, and negatively impacting the performance of the agent. On the other hand, OMD and FuncID explicitly target maximizing the expected returns by learning a model that is more effective for decision-making, especially in the presence of MDP model misspecification. Our results further show that the bilevel formulation can also be beneficial in the well-specified setting when using algorithm such as FuncID, that exploit the functional structure of the problem.

Acknowledgments

This work was supported by the ERC grant number 101087696 (APHELAIA project) and by ANR 3IA MIAI@Grenoble Alpes (ANR-19-P3IA-0003) and the ANR project BONSAI (grant ANR-23-CE23-0012-01).

References

- Ablin et al. [2020] P. Ablin, G. Peyré, and T. Moreau. Super-efficiency of automatic differentiation for functions defined as a minimum. International Conference on Machine Learning (ICML), 2020.

- Ahuja et al. [2020] K. Ahuja, K. Shanmugam, K. Varshney, and A. Dhurandhar. Invariant risk minimization games. International Conference on Machine Learning (ICML), 2020.

- Amos et al. [2023] B. Amos et al. Tutorial on amortized optimization. Foundations and Trends® in Machine Learning, 16(5):592–732, 2023.

- Arbel and Mairal [2022a] M. Arbel and J. Mairal. Amortized implicit differentiation for stochastic bilevel optimization. International Conference on Learning Representations (ICLR), 2022a.

- Arbel and Mairal [2022b] M. Arbel and J. Mairal. Non-convex bilevel games with critical point selection maps. Advances in Neural Information Processing Systems (NeurIPS), 2022b.

- Arjovsky et al. [2019] M. Arjovsky, L. Bottou, I. Gulrajani, and D. Lopez-Paz. Invariant risk minimization. arXiv preprint 1907.02893, 2019.

- Bae and Grosse [2020] J. Bae and R. B. Grosse. Delta-stn: Efficient bilevel optimization for neural networks using structured response jacobians. Advances in Neural Information Processing Systems (NeurIPS), 2020.

- Bansal et al. [2023] D. Bansal, R. T. Chen, M. Mukadam, and B. Amos. Taskmet: Task-driven metric learning for model learning. Advances in Neural Information Processing Systems (NeurIPS), 2023.

- Bauschke and Combettes [2011] H. H. Bauschke and P. L. Combettes. Convex Analysis and Monotone Operator Theory in Hilbert Spaces. Springer Publishing Company, Incorporated, 1st edition, 2011. ISBN 1441994661.

- Baydin et al. [2017] A. G. Baydin, B. A. Pearlmutter, A. A. Radul, and J. M. Siskind. Automatic differentiation in machine learning: A survey. Journal of Machine Learning Research (JMLR), 18(153):1–43, 2017.

- Bengio et al. [1994] Y. Bengio, P. Simard, and P. Frasconi. Learning long-term dependencies with gradient descent is difficult. IEEE Transactions on Neural Networks, 5(2):157–166, 1994.

- Bennett et al. [2006] K. P. Bennett, J. Hu, X. Ji, G. Kunapuli, and J.-S. Pang. Model selection via bilevel optimization. IEEE International Joint Conference on Neural Network Proceedings, 2006.

- Bertinetto et al. [2019] L. Bertinetto, J. F. Henriques, P. H. Torr, and A. Vedaldi. Meta-learning with differentiable closed-form solvers. International Conference on Learning Representations (ICLR), 2019.

- Bińkowski et al. [2018] M. Bińkowski, D. J. Sutherland, M. Arbel, and A. Gretton. Demystifying mmd gans. arXiv preprint arXiv:1801.01401, 2018.

- Blondel et al. [2022] M. Blondel, Q. Berthet, M. Cuturi, R. Frostig, S. Hoyer, F. Llinares-López, F. Pedregosa, and J.-P. Vert. Efficient and modular implicit differentiation. Advances in Neural Information Processing Systems (NeurIPS), 2022.

- Blundell et al. [2007] R. Blundell, X. Chen, and D. Kristensen. Semi-nonparametric iv estimation of shape-invariant engel curves. Econometrica, 75(6):1613–1669, 2007.

- Blundell et al. [2012] R. Blundell, J. L. Horowitz, and M. Parey. Measuring the price responsiveness of gasoline demand: Economic shape restrictions and nonparametric demand estimation. Quantitative Economics, 3(1):29–51, 2012.

- Bollen [2012] K. A. Bollen. Instrumental variables in sociology and the social sciences. Annual Review of Sociology, 38:37–72, 2012.

- Bolte et al. [2021] J. Bolte, T. Le, E. Pauwels, and T. Silveti-Falls. Nonsmooth implicit differentiation for machine-learning and optimization. Advances in Neural Information Processing Systems (NeurIPS), 2021.

- Bolte et al. [2024] J. Bolte, E. Pauwels, and S. Vaiter. One-step differentiation of iterative algorithms. Advances in Neural Information Processing Systems (NeurIPS), 2024.

- Bottou [2010] L. Bottou. Large-scale machine learning with stochastic gradient descent. International Conference on Computational Statistics (COMPSTAT), 2010.

- Bradbury et al. [2018] J. Bradbury, R. Frostig, P. Hawkins, M. J. Johnson, C. Leary, D. Maclaurin, G. Necula, A. Paszke, J. VanderPlas, S. Wanderman-Milne, and Q. Zhang. JAX: composable transformations of Python+NumPy programs, 2018. URL http://github.com/google/jax.

- Brock et al. [2018] A. Brock, T. Lim, J. Ritchie, and N. Weston. SMASH: One-shot model architecture search through hypernetworks. International Conference on Learning Representations (ICLR), 2018.

- Brockman et al. [2016] G. Brockman, V. Cheung, L. Pettersson, J. Schneider, J. Schulman, J. Tang, and W. Zaremba. Openai gym. arXiv preprint 1606.01540, 2016.

- Cawley and Meyerhoefer [2012] J. Cawley and C. Meyerhoefer. The medical care costs of obesity: an instrumental variables approach. Journal of Health Economics, 31(1):219–230, 2012.

- Chen et al. [2018] R. T. Chen, Y. Rubanova, J. Bettencourt, and D. K. Duvenaud. Neural ordinary differential equations. Advances in Neural Information Processing Systems (NeurIPS), 2018.

- Debnath and Mikusinski [2005] L. Debnath and P. Mikusinski. Introduction to Hilbert spaces with applications. Academic press, 2005.

- Dempe et al. [2007] S. Dempe, J. Dutta, and B. Mordukhovich. New necessary optimality conditions in optimistic bilevel programming. Optimization, 56(5-6):577–604, 2007.

- Domke [2012] J. Domke. Generic methods for optimization-based modeling. International Conference on Artificial Intelligence and Statistics (AISTATS), 2012.

- Fang and Santos [2018] Z. Fang and A. Santos. Inference on Directionally Differentiable Functions. The Review of Economic Studies, 86(1):377–412, 2018.

- Feurer and Hutter [2019] M. Feurer and F. Hutter. Hyperparameter optimization. Springer International Publishing, 2019.

- Franceschi et al. [2017] L. Franceschi, M. Donini, P. Frasconi, and M. Pontil. Forward and reverse gradient-based hyperparameter optimization. International Conference on Machine Learning (ICML), 2017.

- Fu et al. [2022] Z. Fu, Z. Qi, Z. Wang, Z. Yang, Y. Xu, and M. R. Kosorok. Offline reinforcement learning with instrumental variables in confounded markov decision processes. arXiv preprint 2209.08666, 2022.

- Ghadimi and Wang [2018] S. Ghadimi and M. Wang. Approximation methods for bilevel programming. Optimization and Control, 2018.

- Goodman [1971] V. Goodman. Quasi-differentiable functions of banach spaces. Proceedings of the American Mathematical Society, 30(2):367–370, 1971.

- Gould et al. [2016] S. Gould, B. Fernando, A. Cherian, P. Anderson, R. S. Cruz, and E. Guo. On differentiating parameterized argmin and argmax problems with application to bi-level optimization. arXiv preprint 1607.05447, 2016.

- Grazzi et al. [2020] R. Grazzi, L. Franceschi, M. Pontil, and S. Salzo. On the iteration complexity of hypergradient computation. International Conference on Machine Learning (ICML), 2020.

- Ha et al. [2017] D. Ha, A. M. Dai, and Q. V. Le. Hypernetworks. International Conference on Learning Representations (ICLR), 2017.

- Holler et al. [2018] G. Holler, K. Kunisch, and R. C. Barnard. A bilevel approach for parameter learning in inverse problems. Inverse Problems, 34(11):115012, 2018.

- Hong et al. [2023] M. Hong, H. Wai, Z. Wang, and Z. Yang. A two-timescale stochastic algorithm framework for bilevel optimization: Complexity analysis and application to actor-critic. SIAM Journal on Optimization, 33(1):147–180, 2023.

- Hu et al. [2023] Y. Hu, J. Wang, Y. Xie, A. Krause, and D. Kuhn. Contextual stochastic bilevel optimization. Advances in Neural Information Processing Systems (NeurIPS), 2023.

- Ioffe and Tihomirov [1979] A. D. Ioffe and V. M. Tihomirov. Theory of Extremal Problems. Series: Studies in Mathematics and its Applications 6. Elsevier, 1979.

- Ji et al. [2021] K. Ji, J. Yang, and Y. Liang. Bilevel optimization: Convergence analysis and enhanced design. International Conference on Machine Learning (ICML), 2021.

- Jia and Benson [2019] J. Jia and A. R. Benson. Neural jump stochastic differential equations. Advances in Neural Information Processing Systems (NeurIPS), 2019.

- Kingma and Ba [2015] D. P. Kingma and J. Ba. Adam: A method for stochastic optimization. International Conference on Learning Representations (ICLR), 2015.

- Kingma and Welling [2014] D. P. Kingma and M. Welling. Auto-encoding variational bayes. International Conference on Learning Representations (ICLR), 2014.

- Kunapuli et al. [2008] G. Kunapuli, K. Bennett, J. Hu, and J.-S. Pang. Bilevel model selection for support vector machines. CRM Proceedings and Lecture Notes, 45:129–158, 2008.

- Kwon et al. [2024] J. Kwon, D. Kwon, S. Wright, and R. D. Nowak. On penalty methods for nonconvex bilevel optimization and first-order stochastic approximation. International Conference on Learning Representations (ICLR), 2024.

- Li et al. [2023] S. Li, Z. Wang, A. Narayan, R. Kirby, and S. Zhe. Meta-learning with adjoint methods. International Conference on Artificial Intelligence and Statistics (AISTATS), 2023.

- Li et al. [2020] X. Li, T.-K. L. Wong, R. T. Chen, and D. Duvenaud. Scalable gradients for stochastic differential equations. International Conference on Artificial Intelligence and Statistics (AISTATS), 2020.

- Liao et al. [2018] R. Liao, Y. Xiong, E. Fetaya, L. Zhang, K. Yoon, X. Pitkow, R. Urtasun, and R. Zemel. Reviving and improving recurrent back-propagation. International Conference on Machine Learning (ICML), 2018.

- Liu et al. [2021a] R. Liu, X. Liu, S. Zeng, J. Zhang, and Y. Zhang. Value-function-based sequential minimization for bi-level optimization. IEEE Transactions on Pattern Analysis and Machine Intelligence (PAMI), 45:15930–15948, 2021a.

- Liu et al. [2021b] R. Liu, Y. Liu, S. Zeng, and J. Zhang. Towards gradient-based bilevel optimization with non-convex followers and beyond. Advances in Neural Information Processing Systems (NeurIPS), 2021b.

- Liu et al. [2022] R. Liu, J. Gao, J. Zhang, D. Meng, and Z. Lin. Investigating bi-level optimization for learning and vision from a unified perspective: a survey and beyond. IEEE Transactions on Pattern Analysis and Machine Intelligence (PAMI), 44:10045–10067, 2022.

- Liu et al. [2023] R. Liu, Y. Liu, W. Yao, S. Zeng, and J. Zhang. Averaged method of multipliers for bi-level optimization without lower-level strong convexity. International Conference on Machine Learning (ICML), 2023.

- Lorraine et al. [2019] J. Lorraine, P. Vicol, and D. K. Duvenaud. Optimizing millions of hyperparameters by implicit differentiation. International Conference on Artificial Intelligence and Statistics (AISTATS), 2019.

- MacKay et al. [2019] M. MacKay, P. Vicol, J. Lorraine, D. Duvenaud, and R. B. Grosse. Self-tuning networks: Bilevel optimization of hyperparameters using structured best-response functions. International Conference on Learning Representations (ICLR), 2019.

- Mairal et al. [2012] J. Mairal, F. Bach, and J. Ponce. Task-driven dictionary learning. IEEE Transactions on Pattern Analysis and Machine Intelligence (PAMI), 34(4):791–804, 2012.

- Margossian and Betancourt [2021] C. C. Margossian and M. Betancourt. Efficient automatic differentiation of implicit functions. arXiv preprint 2112.14217, 2021.

- Marrie et al. [2023] J. Marrie, M. Arbel, D. Larlus, and J. Mairal. Slack: Stable learning of augmentations with cold-start and kl regularization. Conference on Computer Vision and Pattern Recognition (CVPR), 2023.

- Matthey et al. [2017] L. Matthey, I. Higgins, D. Hassabis, and A. Lerchner. dsprites: Disentanglement testing sprites dataset, 2017.

- Nagendra et al. [2017] S. Nagendra, N. Podila, R. Ugarakhod, and K. George. Comparison of reinforcement learning algorithms applied to the cart-pole problem. International Conference on Advances in Computing, Communications and Informatics (ICACCI), 2017.

- Navon et al. [2021] A. Navon, I. Achituve, H. Maron, G. Chechik, and E. Fetaya. Auxiliary learning by implicit differentiation. International Conference on Learning Representations (ICLR), 2021.

- Nemirovski and Semenov [1973] A. Nemirovski and S. Semenov. On polynomial approximation of functions on hilbert space. Mathematics of the USSR-Sbornik, 21(2):255, 1973.

- Nikishin et al. [2022] E. Nikishin, R. Abachi, R. Agarwal, and P.-L. Bacon. Control-oriented model-based reinforcement learning with implicit differentiation. AAAI Conference on Artificial Intelligence, 2022.

- Noll [1993] D. Noll. Second order differentiability of integral functionals on Sobolev spaces and L2-spaces. Walter de Gruyter, Berlin/New York Berlin, New York, 1993.

- Pascanu et al. [2013] R. Pascanu, T. Mikolov, and Y. Bengio. On the difficulty of training recurrent neural networks. International Conference on Machine Learning (ICML), 2013.

- Paszke et al. [2019] A. Paszke, S. Gross, F. Massa, A. Lerer, J. Bradbury, G. Chanan, T. Killeen, Z. Lin, N. Gimelshein, L. Antiga, A. Desmaison, A. Kopf, E. Yang, Z. DeVito, M. Raison, A. Tejani, S. Chilamkurthy, B. Steiner, L. Fang, J. Bai, and S. Chintala. Pytorch: An imperative style, high-performance deep learning library. Advances in Neural Information Processing Systems (NeurIPS), 2019.

- Pedregosa [2016] F. Pedregosa. Hyperparameter optimization with approximate gradient. International Conference on Machine Learning (ICML), 2016.

- Pontryagin [2018] L. S. Pontryagin. Mathematical Theory of Optimal Processes. Routledge, 2018.

- Rezende et al. [2014] D. J. Rezende, S. Mohamed, and D. Wierstra. Stochastic backpropagation and approximate inference in deep generative models. International Conference on Machine Learning (ICML), 2014.

- Robbins and Monro [1951] H. Robbins and S. Monro. A stochastic approximation method. The Annals of Mathematical Statistics, pages 400–407, 1951.

- Rosset [2008] S. Rosset. Bi-level path following for cross validated solution of kernel quantile regression. International Conference on Machine Learning (ICML), 2008.

- Shaban et al. [2019] A. Shaban, C.-A. Cheng, N. Hatch, and B. Boots. Truncated back-propagation for bilevel optimization. International Conference on Artificial Intelligence and Statistics (AISTATS), 2019.

- Singh et al. [2019] R. Singh, M. Sahani, and A. Gretton. Kernel instrumental variable regression. Advances in Neural Information Processing Systems (NIPS), 2019.

- Stock and Trebbi [2003] J. H. Stock and F. Trebbi. Retrospectives: Who invented instrumental variable regression? Journal of Economic Perspectives, 17(3):177–194, 2003.

- Suonperä and Valkonen [2024] E. Suonperä and T. Valkonen. Linearly convergent bilevel optimization with single-step inner methods. Computational Optimization and Applications, 87(2):571–610, 2024.

- Sutton [1991] R. S. Sutton. Dyna, an integrated architecture for learning, planning, and reacting. ACM Sigart Bulletin, 2(4):160–163, 1991.

- van der Vaart [1991] A. van der Vaart. Efficiency and hadamard differentiability. Scandinavian Journal of Statistics, 18(1):63–75, 1991.

- van der Vaart and Wellner [1996] A. W. van der Vaart and J. A. Wellner. Weak Convergence and Empirical Processes with Applications to Statistics, pages 16–28. Springer New York, 1996.

- Vicol et al. [2021] P. Vicol, J. Lorraine, D. Duvenaud, and R. Grosse. Implicit regularization in overparameterized bilevel optimization. International Conference on Machine Learning (ICML), 2022.

- Von Stackelberg [2010] H. Von Stackelberg. Market Structure and Equilibrium. Springer Science & Business Media, 2010.

- Williams and Seeger [2000] C. Williams and M. Seeger. Using the nyström method to speed up kernel machines. Advances in Neural Information Processing Systems (NIPS), 2000.

- Williams and Peng [1990] R. J. Williams and J. Peng. An efficient gradient-based algorithm for on-line training of recurrent network trajectories. Neural Computation, 2(4):490–501, 1990.

- Xu et al. [2021a] L. Xu, Y. Chen, S. Srinivasan, N. de Freitas, A. Doucet, and A. Gretton. Learning deep features in instrumental variable regression. International Conference on Learning Representations (ICLR), 2021a.

- Xu et al. [2021b] L. Xu, H. Kanagawa, and A. Gretton. Deep proxy causal learning and its application to confounded bandit policy evaluation. Advances in Neural Information Processing Systems (NeurIPS), 2021b.

- Ye and Ye [1997] J. Ye and X. Ye. Necessary optimality conditions for optimization problems with variational inequality constraints. Mathematics of Operations Research, 22(4):977–997, 1997.

- Ye and Zhu [1995] J. Ye and D. Zhu. Optimality conditions for bilevel programming problems. Optimization, 33(1):9–27, 1995.

- Ye et al. [1997] J. Ye, D. Zhu, and Q. J. Zhu. Exact penalization and necessary optimality conditions for generalized bilevel programming problems. SIAM Journal on Optimization, 7(2):481–507, 1997.

- Zhang et al. [2019] C. Zhang, M. Ren, and R. Urtasun. Graph hypernetworks for neural architecture search. International Conference on Learning Representations (ICLR), 2019.

- Zhong et al. [2019] Y. D. Zhong, B. Dey, and A. Chakraborty. Symplectic ode-net: Learning hamiltonian dynamics with control. arXiv preprint 1909.12077, 2019.

Appendix A Examples of FBO formulations

The functional bilevel setting covers several bilevel problems encountered in practice where the objectives depend only on the model predictions regardless of its parameterization. We discuss a few examples below.

Auxiliary task learning.

As in Equation 1, consider a main prediction task with features and labels , equipped with a loss function . The goal of auxiliary task learning is to learn how a set of auxiliary tasks represented by a vector could help solve the main task. This problem is formulated by Navon et al. [2021] as a bilevel problem, which can be written as (FBO) with

where the loss is evaluated over a validation dataset , and

where an independent training dataset is used, and is a function that combines the auxiliary losses into a scalar value.

Task-driven metric learning.

Considering now a regression problem with features and labels , the goal of task-driven metric learning formulated by Bansal et al. [2023] is to learn a metric parameterized by for the regression task such that the corresponding predictor performs well on a downstream task . This can be formulated as (FBO) with and

where is the squared Mahalanobis norm with parameters and is a data-dependent metric that allows emphasizing features that are more important for the downstream task.

Appendix B General functional implicit differentiation

B.1 Preliminary results

We recall the definition of Hadamard differentiability and provide in Proposition B.2 a general property for Hadamard differentiable maps that we will exploit to prove Theorem 3.1 in Section B.2.

Definition B.1.

Hadamard differentiability. Let and be two separable Banach spaces. A function is said to be Hadamard differentiable [van der Vaart, 1991, Fang and Santos, 2018] if for any , there exist a continuous linear map so that for any sequence in converging to an element , and any real valued and non-vanishing sequence converging to , it holds that:

| (15) |

Proposition B.2.

Let and be two separable Banach spaces. Let be a Hadamard differentiable map with differential at point . Consider a bounded linear map defined over a euclidean space of finite dimension and taking values in , i.e . Then, the following holds:

Proof.

Consider a sequence in so that converges to with for all and define the first order error as follows:

The goal is to show that converges to . We can write as with and , so that:

If were unbounded, then, by contradiction, there must exist a subsequence converging to , with increasing and . Moreover, since is bounded, one can further choose the subsequence so that converges to some element . We can use the following upper-bound:

| (16) |

where we used that is bounded. Since is Hadamard differentiable, converges to . Moreover, also converges to . Hence, converges to which contradicts . Therefore, is bounded.

Consider now any convergent subsequence of . Then, it can be written as with increasing and . We then have by construction. Since is bounded, one can further choose the subsequence so that converges to some element . Using again Equation 16 and the fact that is Hadamard differentiable, we deduce that must converge to , and by definition of , that converges to . Therefore, it follows that , so that . We then have shown that is a bounded sequence and every subsequence of it converges to . Therefore, must converge to , which concludes the proof. ∎

B.2 Proof of the Functional implicit differentiation theorem

Proof of Theorem 3.1.

The proof strategy consists in establishing the existence and uniqueness of the solution map , deriving a candidate Jacobian for it, then proving that is differentiable.

Existence and uniqueness of a solution map . Let in be fixed. The map is lower semi-continuous since it is Fréchet differentiable by assumption. It is also strongly convex. Therefore, it admits a unique minimier [Bauschke and Combettes, 2011, Corollary 11.17]. We then conclude that the map is well-defined on .

Strong convexity inequalities. We provide two inequalities that will be used for proving differentiability of the map . The map is Fréchet differentiable on and -strongly convex (with positive by assumption). Hence, for all in the following quadratic lower-bound holds:

| (17) |

From the inequality above, we can also deduce that is a -strongly monotone operator:

| (18) |

Finally, note that, since is Fréchet differentiable, its gradient must vanish at the optimum , i.e :

| (19) |

Candidate Jacobian for . Let be in . Using Equation 18 with and for some , and a non-zeros real number we get:

| (20) |

By assumption, is Hadamard differentiable and, a fortiori, directionally differentiable. Thus, by taking the limit when , it follows that:

| (21) |

Hence, defines a coercive quadratic form. By definition of Hadamard differentiability, it is also bounded. Therefore, it follows from Lax-Milgram’s theorem [Debnath and Mikusinski, 2005, Theorem 4.3.16], that is invertible with a bounded inverse. Moreover, recalling that is a bounded operator, its adjoint is also a bounded operator from to . Therefore, we can define which is a bounded linear map from to and will be our candidate Jacobian.

Differentiability of . By the strong convexity assumption (locally in ), there exists an open ball centered at the origin that is small enough so that we can ensure the existence of for which is -strongly convex for all . For a given , we use the -strong monotonicity of (18) at points and to get:

where the second line follows from optimality of (Equation 19), and the last line uses Cauchy-Schwarz’s inequality. The above inequality allows us to deduce that:

| (22) |

Moreover, since is Hadamard differentiable, by Proposition B.2 it follows that:

| (23) |

where the first term vanishes thanks to Equation 19, since is a minimizer of . Additionally, note that the differential acts on elements as follows:

| (24) |

where and are bounded operators and denotes the adjoint of . By definition of , and using Equation 24, it follows that:

Therefore, combining Equation 23 with the above equality yields:

| (25) |

Finally, combining Equation 22 with the above equality directly shows that . We have shown that is differentiable with a Jacobian map given by . ∎

B.3 Proof of the functional adjoint sensitivity in Proposition 3.2

Proof of Proposition 3.2.

We use the assumptions and definitions from Proposition 3.2 and express the gradient using the chain rule:

The Jacobian is the solution of a linear system obtained by applying Theorem 3.1 :

We note and . It follows that the gradient can be expressed as:

In other words, the implicit gradient can be expressed using the adjoint function , which is an element of and can be defined as the solution of the following functional regression problem:

∎

Appendix C Connection with parametric implicit differentiation

To establish a connection with parametric implicit differentiation, let us consider to be a map from a finite dimensional set of parameters to the functional Hilbert space and define a parametric version of the outer and inner objectives in Equation FBO restricted to functions in :

| (26) |

The map can typically be a neural network parameterization and allows to obtain a “more tractable” approximation to the abstract solution in where the function space is often too large to perform optimization. This is typically the case when is an -space of functions as we discuss in more details in Section 4. When is a Reproducing Kernel Hilbert Space (RKHS), may also correspond to the Nyström approximation [Williams and Seeger, 2000], which performs the optimization on a finite-dimensional subspace of an RKHS spanned by a few data points.

The corresponding parametric version of the problem (FBO) is then formally defined as:

| (PBO) | ||||

The resulting bilevel problem in Equation PBO often arises in machine learning but is generally ambiguously defined without further assumptions on the map as the inner-level problem might admit multiple solutions [Arbel and Mairal, 2022b]. Under the assumption that is twice continuously differentiable and the rather strong assumption that the parametric Hessian is invertible for a given , the expression for the total gradient follows by direct application of the parametric implicit function theorem [Pedregosa, 2016]:

| (27) |

where is the adjoint vector in . Without further assumptions, the expression of the gradient in Equation 27 is generally different from the one obtained in Proposition 3.2 using the functional point of view. Nevertheless, a precise connection between the functional and parametric implicit gradients can be obtained under expressiveness assumptions on the parameterization , as discussed in the next two propositions.

Proposition C.1.

Under the same assumptions as in Proposition 3.2 and assuming that is twice continuously differentiable, the following expression holds for any :

| (28) |

where is a linear operator measuring the distortion induced by the parameterization and acts on functions in by mapping them to a matrix where is the dimension of the parameter space . If, in addition, is expressive enough so that , then the above expression simplifies to:

| (29) |

Proposition C.1 follows by direct application of the chain rule, noting that the distortion term on the right of (28) vanishes when since by optimality of . A consequence is that, for an optimal parameter , the parametric Hessian is necessarily symmetric positive semi-definite. However, for an arbitrary parameter , the distortion does not vanish in general, making the Hessian possibly non-positive. This can result in numerical instability when using algorithms such as AID for which an adjoint vector is obtained by solving a quadratic problem defined by the Hessian matrix evaluated on approximate minimizers of the inner-level problem. Moreover, if the model admits multiple solutions , the Hessian is likely to be degenerate making the implicit function theorem inapplicable and the bilevel problem in Equation PBO ambiguously defined111although a generalized version of such a theorem was recently provided under restrictive assumptions [Arbel and Mairal, 2022b].. On the other hand, the functional implicit differentiation requires finding an adjoint function by solving a positive definite quadratic problem in which is always guaranteed to have a solution even when the inner-level prediction function is only approximately optimal.

Proposition C.2.

Assuming that is twice continuously differentiable and that for a fixed we have , and has a full rank, then, under the same assumptions as in Proposition 3.2, is given by:

| (30) |

where is a projection operator of rank . If, in addition, the equality holds for all in a neighborhood of , then .

Proposition C.2, which is proven below, shows that, even when the parametric family is expressive enough to recover the optimal prediction function at a single value , the expression of the total gradient in Equation 30 using parametric implicit differentiation might generally differ from the one obtained using its functional counterpart. Indeed the projector , which has a rank equal to , biases the adjoint function by projecting it into a finite dimensional space before applying the cross derivative operator. Only under a much stronger assumption on , requiring it to recover the optimal prediction function in a neighborhood of the outer-level variable , both parametric and functional implicit differentiation recover the same expression for the total gradient. In this case, the projector operator aligns with the cross-derivative operator so that . Finally, note that the expressiveness assumptions on made in Propositions C.1 and C.2 are only used here to discuss the connection with the parametric implicit gradient and are not required by the method we introduce in Section 4.

Proof of Proposition C.2.

Here we want to show the connection between the parametric gradient of the outer variable usually used in approximate differentiation methods and the functional gradient of the outer variable derived from the functional bilevel problem definition in Equation FBO. Recall the definition of the parametric inner objective . According to Proposition C.1, we have the following relation

By assumption, has a full rank which matches the dimension of the parameter space . Recall from the assumptions of Theorem 3.1 that the Hessian operator is positive definite by the strong convexity of the inner-objective in the second argument. We deduce that must be invertible, since, by construction, the dimension of is smaller than that of the Hilbert space which has possibly infinite dimension. Recall from Theorem 3.1, and the assumption that . We apply the parametric implicit function theorem to get the following expression of the Jacobian :

Hence, differentiating the total objective and applying the chain rule directly results in the following expression:

| (31) |

with previously defined and .

We now introduce the operator . The operator is a projector as it satisfies . Hence, using the fact that the Hessian operator is invertible, and recalling that the adjoint function is given by , we directly get form Equation 31 that:

If we further assume that holds for all in a neighborhood of , then differentiating with respect to results in the following identity:

Using the expression of from Equation 4, we have the following identity:

In other words, is of the form for some finite dimensional matrix of size . Recalling the expression of the total gradient, we can deduce the equality between parametric and functional gradients:

The first equality follows from the general expression of the total gradient . In the second line we use the expression of which then allows to simplify the expression in the third line. Then, recalling that the Hessian operator is invertible, we get the fourth line. Finally, the result follows by using again the expression of and recalling the definition of the adjoint function . ∎

Appendix D Functional adjoint sensitivity result in spaces

In this section we provides full proofs of Proposition 3.3. We start by stating the assumptions needed on the point-wise losses in Section D.1, then provide some differentiation results in Section D.2 and conclude with the main proofs in Section D.3.

D.1 Assumptions

Assumptions on .

-

(A)

For any , there exists a positive constant and a neighborhood of for which is -strongly convex in its second argument for all .

-

(B)

For any , .

-

(C)

is continuously differentiable for all .

-

(D)

For any fixed , there exists a constant and a neighborhood of s.t. is -smooth for all .