Stochastic Approximation Proximal Subgradient Method for

Stochastic Convex-Concave Minimax Optimization

Yu-Hong Dai111LSEC, ICMSEC, AMSS, Chinese Academy of Sciences, Beijing 100190, China. Email: dyh@lsec.cc.ac.cn.

This author was supported by the Natural Science Foundation of China (Nos. 11991021, 12021001, 11991020 and 11971372) and the Strategic Priority Research Program of Chinese Academy of Sciences (No. XDA27000000). Jiani Wang222School of Science, Beijing University of Posts and Telecommunications, Beijing 100876, China. Email: wjiani@lsec.ac.cc.cn and Liwei Zhang 333National Frontiers Science Center for Industrial Intelligence and Systems Optimization, Northeastern University, Shenyang 110819, China; Key Laboratory of Data Analytics and Optimization for Smart Industry (Northeastern University), Ministry of Education, Shenyang 110819, China. Email: Zhanglw@ mail.neu.edu.cn. This author was supported by the Major Program of National Natural Science Foundation of China (Nos. 72192830 and 72192831), National Natural Science Foundation of China (No.12371298) and the 111 Project (B16009)

Abstract

This paper presents a stochastic approximation proximal subgradient (SAPS) method for stochastic convex-concave minimax optimization. By accessing unbiased and variance bounded approximate subgradients, we show that this algorithm exhibits expected convergence rate of the minimax optimality measure if the parameters in the algorithm are properly chosen, where denotes the number of iterations. Moreover, we show that the algorithm has minimax optimality measure bound with high probability. Further we study a specific stochastic convex-concave minimax optimization problems arising from stochastic convex conic optimization problems, which the the bounded subgradient condition is fail. To overcome the lack of the bounded subgradient conditions in convex-concave minimax problems, we propose a linearized stochastic approximation augmented Lagrange (LSAAL) method and prove that this algorithm exhibits expected convergence rate for the minimax optimality measure and minimax optimality measure bound with high probability as well. Preliminary numerical results demonstrate the effect of the SAPS and LSAAL methods.

Key words: stochastic convex-concave minimax optimization, stochastic convex conic optimization, stochastic approximation, proximal point method, linearized stochastic approximation augmented Lagrange method, expected convergence rate, high probability bound.

AMS subject classification: 90C30

1 Introduction

Consider the following stochastic minimax optimization

(1.1)

where and are proper lower semicontinuous convex functions, is a random vector whose probability distribution is supported on and is a real-valued function.

Let us denote the expected value function

Assume that this function is well defined and finite valued for every . Meanwhile, assume that is continuous and convex-concave on , but may not be differentiable (this clearly holds if for every

, the function is convex-concave on ).

Under the above assumptions, the problem (1.1) becomes a convex-concave minimax problem.

1.1 Special Cases

As a stochastic minimax problem with a general convex-concave structure, the problem (1.1) has a wide range of applications such as stochastic convex programming [15], linear regression [14], robust optimization [3] and adversarial generative networks [18]. Below we list three special cases of the problem (1.1), where and are defined as different forms.

Minimax problems over convex sets.

If and , where are two convex sets and are the indicator functions, the problem (1.1) is reduced to

(1.2)

Many machine learning problems such as reinforcement learning ([45, 46]),

black-box adversarial attack ([31, 47, 50]) and adversarial training ([18, 30]) can be expressed as the minimax problem (1.2).

Minimax problems with regularized functions.

Another case is the minimax problem with the functions and , where and are regularized functions; namely,

(1.3)

To solve the overfitting problem while making the model sparse or low-rank, some regularized function is usually added to the objective function. However, many regularized functions are non-differentiable, such as -norm , -norm , -norm , which are common in regression analysis in statistics [13], model training in machine learning [12, 23, 54] and sparse two-matrix game problems [8].

Stochastic convex conic optimization.

Consider the stochastic convex conic optimization problem

(1.4)

In the above, is a random vector whose probability distribution is supported on , is a real-valued function, is a mapping for an open convex set , is a nonempty convex compact set, is a closed convex cone and is a finite-dimensional Hilbert space. The conjugate dual of the stochastic convex programming problem (1.4) is defined as

(1.5)

where the Lagrangian function for (1.4) is defined by for any and is the conjugate function of the indicator function . Under some regularity conditions (see Section 3 for more details), the conjugate dual (1.5) can be expressed as a convex-concave minimax problem of the form (1.1) with functions and being indicator functions related to the constraints and it has the same optimal value as the stochastic convex programming problem (1.4).

1.2 Motivation and Contributions

One difficulty in solving the problem (1.1) is that the probability distribution function may not be available. Even if the distribution function is easy to obtain, the expectation with respect to may be difficult to calculate within a high accuracy in the large scale case. In order to overcome this difficulty, a popular approach is to utilize the stochastic approximation (SA) technique, where approximations can be accessed via calls to stochastic oracles considered as the noisy computable version of

the “real” function. To this aim, the following general assumptions are used throughout this paper.

(A1)

The samples of realizations of random vector are

generated by independent identical distribution (i.i.d.) ;

(A2)

First-order oracles are unbiased estimators of the subgradient of ; namely, for any point , return a stochastic subgradient

such that

is well-defined, where and .

For every , if the function is convex-concave and its

respective subdifferential and integral operators are interchangeable, we can ensure (A2)

by setting

In a pioneering and profound work [34], Nemirovski et al. proposed the robust stochastic approximation (RSA) method for stochastic convex optimization. This method stimulates the development of stochastic approximation algorithms in machine learning [7, 11, 19, 26, 27, 39, 41] and now is widely used in distributed deep learning [4], multiple access channel [42] and low-rank matrix factorization [10].

However, to the best of our knowledge, there is no algroithm for solving stochastic general convex-concave non-differentiable minimax optimization (1.1). Therefore, we shall propose the stochastic approximation proximal subgradient method for the problem (1.1), which is a fundamental idea that extends the algorithm from stochastic convex optimization to stochastic general convex-concave minimax problems.

The main contributions of this paper are as follows.

•

For the stochastic minimax problem (1.1) with lower semicontinuous convex items and , we design a stochastic approximation proximal subgradient (SAPS) method and verify the sublinear convergence rates of the method for general convex-concave case, where the estimators are generated by unbiased first-order oracles with bounded variance. Moreover, SAPS can obtain minimax optimality measure bound with high probability under the bounded subgradient condition, where is the number of iterations. To the best of our knowledge, SAPS is the first stochastic algorithm for solving the stochastic general convex-concave non-differentiable minimax problem (1.1).

•

A linearized stochastic approximation augmented Lagrange (LSAAL) method is developed for the stochastic convex-concave minimax problem (1.5) arising from stochastic convex conic constrained programming (1.4), in which case the bounded subgradient condition dose not satisfied. Under

mild conditions, the optimal value of the stochastic convex cone constrained

optimization is equivalent to its dual problem. The sublinear convergence of the LSAAL method is proved with respect to the expected minimax optimal measure of the augmented Lagrangian function of (1.3). Meanwhile, we show that LSAAL exhibits minimax optimality measure bound with high probability as well. It is worth noting that LSAAL can be widely used to solve stochastic convex cone constrained programming including nonlinear programming, second-order cone optimization and semidefinite programming.

•

We test the effect of the SAPS method for strongly convex-concave case and general convex-concave case and conduct numerical experiments of the LSAAL method for the multi-class

Neyman-Pearson classification on four

real data sets. Numerical results reveal promising performances of the SAPS and LSAAL methods.

1.3 Related Work

Stochastic minimax problems

Many methods for stochastic minimization problems are proposed to solve the stochastic minimax problem (1.2), such as zero-order (namely, gradient-free) algorithms [1, 16, 50, 48, 49] and first-order algorithms [21, 29, 32, 34, 51]. First-order stochastic algorithms have been extended to the case where function is continuous differentiable. Zhang et al. [57] proposed a stochastic accelerated primal-dual algorithm for strongly-convex-strongly-concave saddle point problems and established the linearly convergence to a neighborhood of the unique saddle point.

Yang et al. [53] proposed the stochastic alternating gradient descent ascent (SAGDA) algorithm for a subclass of the nonconvex-nonconcave minimax problem, and showed a sublinear rate of SAGDA under the two-sided Polyak-Lojasiewicz condition.

In [44], Tran-Dinh et al. considered the following stochastic nonconvex-concave minimax problem

(1.6)

where the randomness of the objective function is only on the variable and is continuous differentiable. They developed a single-loop variance-reduced algorithm and achieved the convergence rate of order .

Many stochastic zero-order and subgradient algorithms are used to solve the case where function in the problem (1.2) is non-differentiable. Under conditions (A1)-(A2), Nemirovski et al. [34] proposed a robust stochastic approximation approach for solving the problem (1.2) when and are nonempty convex compact sets. They proved that the expected

convergence in terms of an minimax optimality measure is of the order . Moreover, they established a high probability guarantee of the algorithm. The RSA approach in [34] is in fact a projection gradient method for solving the problem (1.2)

combining the averaging technique developed by [37] and [38]. The epoch-wise stochastic gradient descent ascent method is an extension of the epoch gradient descent method for solving strongly-convex-strongly-concave minimax problems in [52],

and achieved the optimal rate of for the duality gap. The ZO-Min-Max framework was proposed by [31], where

Liu et al. integrated the zeroth-order gradient estimator with an alternating projected stochastic gradient descent-ascent method, and obtained the sublinear convergence rate and scales with problem size. In [50], for the nonconvex-strongly-concave minimax stochastic optimization, a zeroth-order variance reduced gradient descent ascent (ZO-VRGDA) algorithm was proposed, and ZO-VRGDA achieved the iteration complexity of order for finding an -stationary point. A class of accelerated zeroth-order and first-order momentum

methods were analyzed in [20] for both nonconvex minimization and minimax optimization of the form (1.2). Nevertheless, to the best of our knowledge, there is no algorithm for solving the stochastic general convex-concave minimax problem (1.1), which is a more general form including the problems (1.2) and (1.6). This promotes us to explore the properties of the problem (1.1) and develop a fast stochastic algorithm for solving (1.1).

Stochastic convex programming problems

Currently, there have been some methods to solve the stochastic nonlinear programming, such as [15, 35, 36, 56]. Mahdavi et al. [35] studied an online gradient descent method for the online convex optimization and obtained objective regret and constraint violation by analyzing the convergence of the optimal value depending on the sufficiently large sample and the boundedness of the gradient of the constraint functions. Moreover, they proposed a stochastic primal-dual algorithm for stochastic nonlinear programming in [36] and attained the optimal convergence rate of for the general Lipschitz continuous objective functions with high probability. Zhang et al. in [56] designed a proximal

point method for solving convex stochastic nonlinear programming, which had no more than objective regret and no more than constraint violation with high probability. In this paper, stochastic convex conic optimization problems, which contain the convex nonlinear programming, are solved by reformulating as convex-concave minimax problems of the form (1.1). However, for these stochastic convex-concave minimax problems, is an unbounded set and hence the bounded gradient condition, which is normally required for the convergence analysis of RSA, does not hold. This means that we can not use RSA to solve stochastic convex programming problems. Such an observation motivates us to put forward the linearized stochastic approximation augmented Lagrange method, which is based on the augmented Lagrange duality of the convex programming.

1.4 Organization and notations

Organization. The remainder of this paper is organized as follow. In Section

2, we propose the stochastic approximation proximal subgradient method for solving the problem (1.1), and prove the convergence rates for general convex-concave minimax problems. In Section 3, we put forward the linearized stochastic approximation augmented Lagrange method for solving stochastic convex conic optimization problems. In Section 4, we report our numerical results of the SAPS and LSAAL methods. Finally, we draw some discussion in Section 5.

Notations. Throughout the paper, we use the following notations. By , we denote the Euclidean norm of vector

; namely, . Let be a finite-dimensional Hilbert space. The inner product in is defined as and the induced norm of vector is .

For a lower semicontinuous convex function , by for , we denote the proximal mapping of ; namely,

It follows from Page 878 of [40] that the proximal mapping is a nonexpanding

operator; namely,

for all

The conjugate function of , denoted by , is defined by

For a nonempty close convex set , we use to denote the indicator function

of ,

The conjugate of is the supporting function of ; namely,

The proximal mapping of is the metric projection operator onto

the set ; namely, , where

Obviously we have that is a nonexpanding

operator; namely,

for all

For a closed convex cone , any has the following decomposition

with , where is the polar cone of .

In this section, we propose a stochastic approximation proximal subgradient method for solving the convex-concave minimax problem (1.1) and discuss the convergence results of the iterations with general convex-concave structures. Particularly, the sublinear convergence rate with expectation is established for the general convex-concave case if the approximate subgradients of the function are unbiased provided with bounded variance. Ulteriorly, the convergence rate of SAPS with high probability can be obtained when the approximate subgradients are bounded.

Define

We give the existence assumption of the minimax point of the problem (1.1).

(A3)

There exists a point such that

(2.1)

For the minimax point defined as (2.1), the optimality conditions of the problem (1.1) at are expressed as

(2.2)

which are equivalent to the following equalities

(2.3)

We introduce the function by

Then for , we have

With this notation, the optimal conditions (2.3) can be expressed as

(2.4)

where .

Suppose that the first-order oracles are functions444It is said that the function is a function [43] if is continuous w.r.t. for any in and measurable w.r.t. for any ., which are satisfied conditions (A1)-(A2). By the optimality condition (2.4), a natural idea for finding the minimax point is that at the -th iteration, we compute the following subproblem

(2.5)

where .

Specifically, in each iteration, the algorithm alternately solves proximal subproblems with respect to and , which are generated by the first-order oracles . A detailed algorithmic framework is presented as follows.

1:Given . Generate i.i.d. samples of random vector . Generate a stochastic subgradient . Set .

2:Choose a step size and compute

(2.6)

3:Generate a stochastic subgradient

Update to , and go to Step 2.

Obviously, we can express as

(2.7)

If is continuously differentiable on and , the first-order oracles become the gradients of and Algorithm 1 is reduced to stochastic alternating gradient descent

ascent (SAGDA) algorithm as [53]. In addition, if functions and are the indicator functions shown in (1.2). Algorithm 1 is reduced to the stochastic gradient descent (SGD) method in [17, 25].

The averaging technique, developed by [37] and [38], considers an averaged iterated point defined as follows. Let

The averaged iterated point is defined as

(2.8)

Let us analyze convergence properties of the update (2.8), where are generated by Algorithm 1. Under the condition (A3), for a saddle point of , from (2.1), it is reasonable to measure the quality of

an approximate solution by the error

(2.9)

which is called the minimax optimality measure at . Obviously, for any and is a saddle point of if and only if .

2.1 Expected convergence rate analysis

Now we consider the convergence properties of the averaged iterated point defined as (2.8), where is generated by Algorithm 1 for solving a general stochastic convex-concave minimax problem (1.1). By assuming first-order oracles with bounded variance, we discuss the convergence rate of the function value of the iterations with expectation.

The following proposition gives a key property for the sequence generated by Algorithm 1.

Proposition 2.1.

Let be generated by Algorithm 1, for integer , and be computed by formula (2.8). Assume that conditions (A1) and (A2) are satisfied. Denote . Then for integer , for any , the following inequality

(2.10)

holds for any with and .

Proof.

Define

Then the two problems for generating in (2.6) can be expressed as

(2.11)

respectively. It follows from Lemma A.1 (see the Appendix) that for any ,

Summing the above two inequalities yields

(2.12)

Since and are convex functions, for any and , we have

(2.13)

Combining (2.12) and (2.13), we obtain the following inequality

Multiplying on both sides of (2.17) and summing up over , we obtain

(2.18)

From the convexity of and for , using the definition of , we obtain

(2.19)

Thus, by combining (2.18) and (2.19), we obtain (2.10).

To develop the expected convergence rate, we need modify the condition (LABEL:s2.5) as follows.

(A4)

There is a positive constant such that for any , there exists , where

and , such that

(2.20)

One sufficient condition for (A4) is that stochastic subgradients has bounded variance and the subgradients of and are bounded. The latter is true for the special cases (1.2) and (1.3) and hence they satisfy (A4).

Theorem 2.1.

Let be generated by Algorithm 1, for integer , and be computed by formula (2.8). Assume that conditions (A1)-(A4) are satisfied. Then for integer , the following properties hold.

Notice that and , where . Taking expectations of both sides of (2.21), we obtain from (A4) and the definition of that

(2.22)

The results in (a), (b) and (c) are easily obtained by the selection of the step size .

Remark 2.1.

Let be bounded. Then there exists a positive number such that

We can easily obtain

(1)

For , one has

(2)

For , one has

(3)

For for , one has

Remark 2.2.

For strongly-convex-strongly-concave minimax problems, the convergence results of SAPS can be strengthened to the convergence rate of the iterations by [34]. Select step sizes with the positive constant , where is -strongly convex-concave function on . Assume that conditions (A1) and (A2) are satisfied, and there is a positive constant such that

then

one has

Notice that the convergence results of the stochastic algorithm SAPS is an extension of the nonsmooth convex minimization problem to the convex-concave minimax optimization. In the next subsection, we shall give the related high probability convergence results for general convex-cancave minimax optimization.

2.2 High probability performance analysis

In this subsection, we focus on the high probability convergence of Algorithm 1, which is a stronger conclusion than Theorem 2.1. To develop the high probability guarantee of the update (2.8) with being generated by Algorithm 1, we need the following conditions.

(B1)

There is a positive constant such that for any , there exists , where

and , such that

(2.23)

(B2)

There is a positive constant such that for any and ,

(2.24)

(B3)

Let be generated by Algorithm 1 with the step size defined by

for , and for . Then one has

(2.25)

where is some positive constant depending on .

Remark 2.3.

The condition (B1) implies the condition (A4). Indeed, it follows from the Jensen inequality that for the convex function ,

which induces the condition (A4).

Remark 2.4.

There are two natural cases that the

assumption (B3) holds. One is the case when is a bounded set. The other is when is level-bounded.

The follow theorem derives the convergence result of the minimax optimality measure with probability.

Theorem 2.2.

Let (A1)–(A3), (B1)–(B3) be satisfied. Let be generated by Algorithm 1 with the step sizes being defined by

for . Then, one has for any ,

Thus, by the Markov inequality, we have for any ,

Namely, we obtain the following estimate

(2.30)

Secondly, we calculate the boundedness of the term . Let for . Observing that is a deterministic function

of while , we know that the sequence of random real

variables forms a martingale difference. It follows from the condition (B2) that . We have from the

assumption (B3) that . Therefore

Define . Since is a deterministic function of with and , we have that for any and ,

where the first inequality is derived from . When , we have

Thus, in both cases, we have

Therefore, we have

which implies

By the Markov inequality for , it holds

When choosing , we get the following estimate

(2.31)

Finally, combining (2.27), (2.30) and (2.31), we get the following for any positive and ,

(2.32)

Let . Noting , we have that . Hence, (2.32) implies

In this section, we consider the special stochastic convex-concave minimax problem coming from the stochastic convex conic optimization problem (1.4). However, this is a typical problem which does not satisfy conditions (A4) or (B1). This motivates us to consider an improved version of Algorithm 1 for solving the minimax problem in terms of the augmented Lagrangian function.

We assume that is a convex function and the set-valued mapping is graph convex in the problem (1.4). Under these conditions, (1.4) becomes a convex programming problem, see Definition 2.163 of [5]. Certainly, if we assume that for every

, is convex and the set-valued mapping is graph-convex over , then is a convex function and is graph-convex over . Moreover, we assume that for every

, the function and the mapping are smooth over so that and are smooth over , too. Under the above conditions, the problem (1.4) is a smooth convex conic optimization problem.

It can be easily check that the mapping is graph-convex over if and only if

(3.1)

The following lemma lists some important properties of the graph-convexity of the set-valued mapping .

Lemma 3.1.

Let the mapping be graph-convex over an open convex set and be differentiable at . Then

In view of the graph-convexity of the set-valued mapping , we have for ,

Thus, if , then

which implies that the feasible region for defining is a subset of that for defining . Therefore we have . The proof is completed.

The general assumptions by using the stochastic approximation (SA) technique include the independent identically distributed (i.i.d.) samples and the unbiased gradients and . For the stochastic convex problem (1.4), assume that the condition (A1) is satisfied and replace (A2) with the following assumption.

(C1)

For any point , stochastic gradients and satisfy

and .

Furthermore, we assume the following assumptions about the problem (1.4).

(D1)

Let be a positive parameter such that for any ,

(D2)

There exists a constant such that for any and ,

(D3)

There exist constants and such that for each and ,

(D4)

Assume that the Slater condition holds; namely, there exists

If the optimal solution set of the problem (1.4) is nonempty, it follows from Theorem 2.165 of [5] that, under the above Slater condition (D4), the conjugate dual (1.5) of the problem (1.4) has a compact optimal solution set and the optimal value of the problem (1.4) is equal to the optimal value of the problem (1.5). Since is a closed convex cone, we have . In this case, the problem (1.4) can be expressed as the following convex-concave minmax problem

(3.5)

with

(3.6)

Let and be optimal solutions to the problem (1.4) and the problem (1.5), respectively. Then

Obviously we have the following expression

Noting that is an unbounded set, it is not possible to guarantee the boundedness of , which implies that neither (A4) nor (B1) is satisfied. This observation motives us to consider a variant of Algorithm 1, which is able to handle this difficulty. For this purpose, instead of the ordinary Lagrange dual (1.5),

we use the following augmented Lagrange dual of the problem (1.4):

(3.7)

Due to the convexity of the problem (1.4), the optimal value of (3.7) is equal to that of the following minimax problem

(3.8)

Now we focus on solving the stochastic convex-concave minimax problem (3.8). Define the linearized approximations of at and at as

(3.9)

respectively. The corresponding augmented Lagrangian function is expressed as

(3.10)

We propose the following linearized stochastic approximation method in terms of the augmented Lagrangian function for solving the minimax problem (3.8).

1:Choose an initial point , and select parameters

. Generate i.i.d. sample of random vector . Compute the stochastic gradient and the stochastic derivative . Set .

2:Compute

(3.11)

3:Compute the stochastic gradient and the stochastic derivative .

Update to , and go to Step 2.

The following auxiliary lemma will be used for several times in the sequel.

Lemma 3.2.

For any , we have

(3.12)

In particular, if we take , it yields

(3.13)

Proof.

From the definition of in (3.11) and its optimality conditions, we have that is also the optimal solution to the following problem

Under the Slater condition (D4), we can prove the following conditional expected estimate related to the multipliers.

Lemma 3.3.

Let assumptions (A1), (C1), (D4) be satisfied and be generated by Algorithm 2. Then, there exists a positive number such that for any positive integers ,

Proof.

It follows from (C4) that there exists an positive number such that

This implies that for any nonzero ,

which yields

Noticing that and for , we have

from that

The proof is completed.

The next result shows a self-adjusting property of , which is essential to establish the expected convergence rate of the minmax optimality measure.

Lemma 3.4.

Let assumptions (A1), (C1), (D1)-(D4) be satisfied. Let be generated by Algorithm 2 and be an arbitrary integer. Define

Together with the Jensen inequality and the fact that , we have

The proof is completed.

If we take

it follows from Lemma 3.4 that the conditions of Lemma A.2 are satisfied with respect to .

For simplicity, we define

where and are constants given by

We can also observe that

and are exactly the same as the right-hand sides of (A.2) and (A.3) in Lemma A.2, respectively. Therefore, in view of Lemma 3.4, the following lemma is a direct consequence of Lemma A.2.

Lemma 3.5.

Let the conditions of Lemma 3.4 be satisfied. It follows that

(3.19)

Moreover, for any constant , we have

The next lemma is a technical result, which will be used in estimating the difference .

Let

Then and

with probability . It follows from Lemma A.3 that for any ,

which implies that

(3.40)

with

(3.41)

Combining (3.34) with (3.35)-(3.41), by choosing , we obtain

(3.42)

From Theorem 3.1 and 3.2, Algorithm 2 exhibits the same expected sublinear convergence rate as Algorithm 1 and

minimax optimality measure bound with high probability.

4 Preliminary Numerical Experiments

We applied the proposed algorithms to solve three classes of problems. Firstly, we tested the SAPS method for stochastic strongly convex-concave minimax problems with three regularization functions including 1-norm, 2-norm and maximum function. And the impact of the step sizes are analyzed. Secondly, we demonstrated the SAPS method for general stochastic convex-concave minimax problems and observed the performance of Algorithm 1 with different dimensions and constraints. Thirdly, we used the LSAAL method in Algorithm 2 to solve the multi-class Neyman-Pearson classification, which is equivalent to a finite-sum convex-concave minimax problem. We selected three multi-class classification LIBSVM data sets to report the performance of LSAAL. In this section, all numerical experiments were implemented by MATLAB R2019a on a laptop with Intel(R) Core(TM) i5-6200U 2.30GHz and 8GB memory.

We tested the SAPS method in Algorithm 1 for solving the following stochastic strongly convex-concave minimax

problem

(4.43)

where is a real random vector uniformly distributed in the hypercube and is a regular term or projection. In our experiments, let , , and be chosen as 1-norm, 2-norm and maximum function, respectively.

For solving (4.43),

we randomly draw a sample from the hypercube at the -th iteration in Algorithm 1 and compute in (2.5) as the output of Algorithm 1. In the following experiments, the initial point is randomly selected and the error is computed by

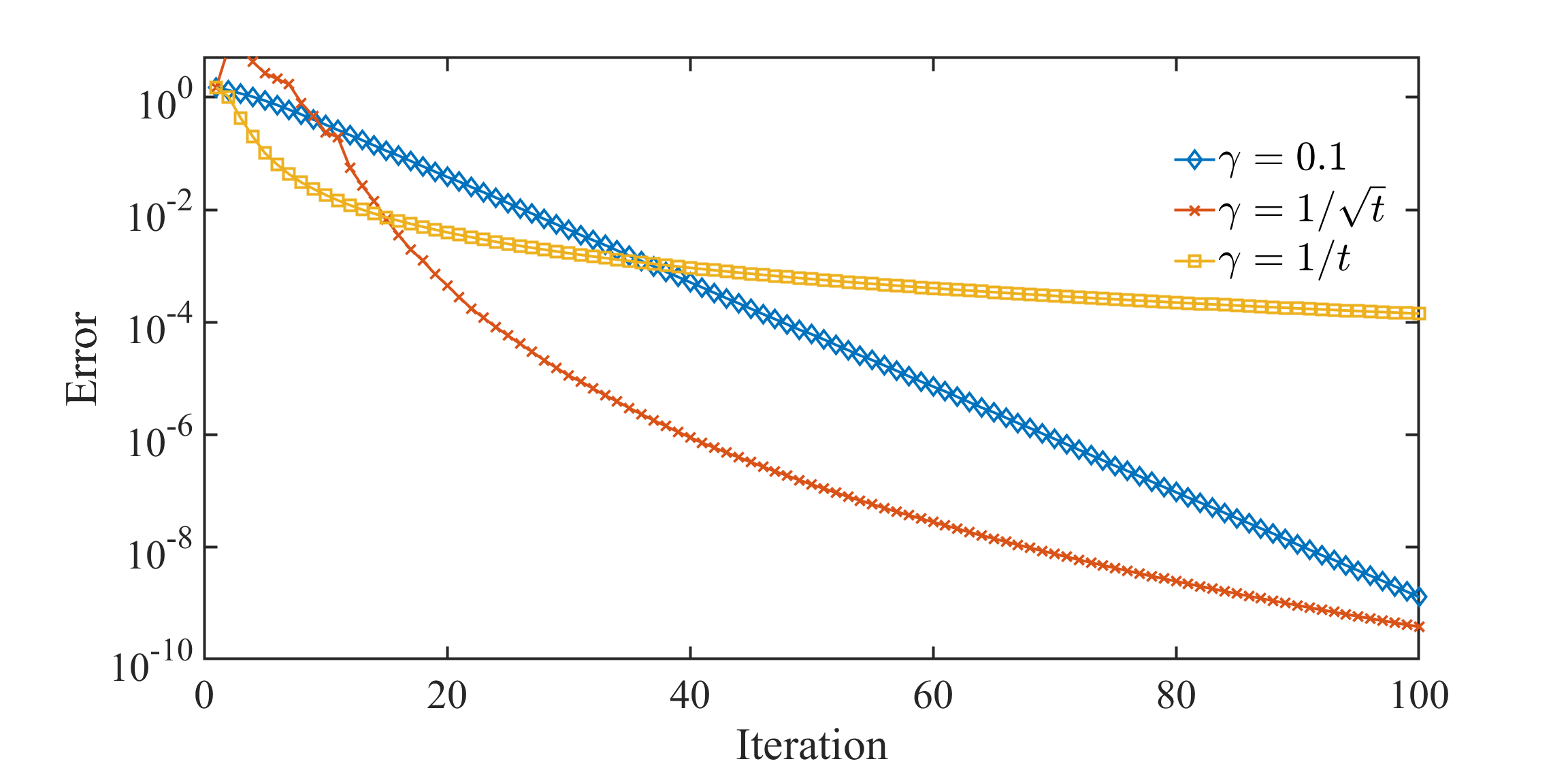

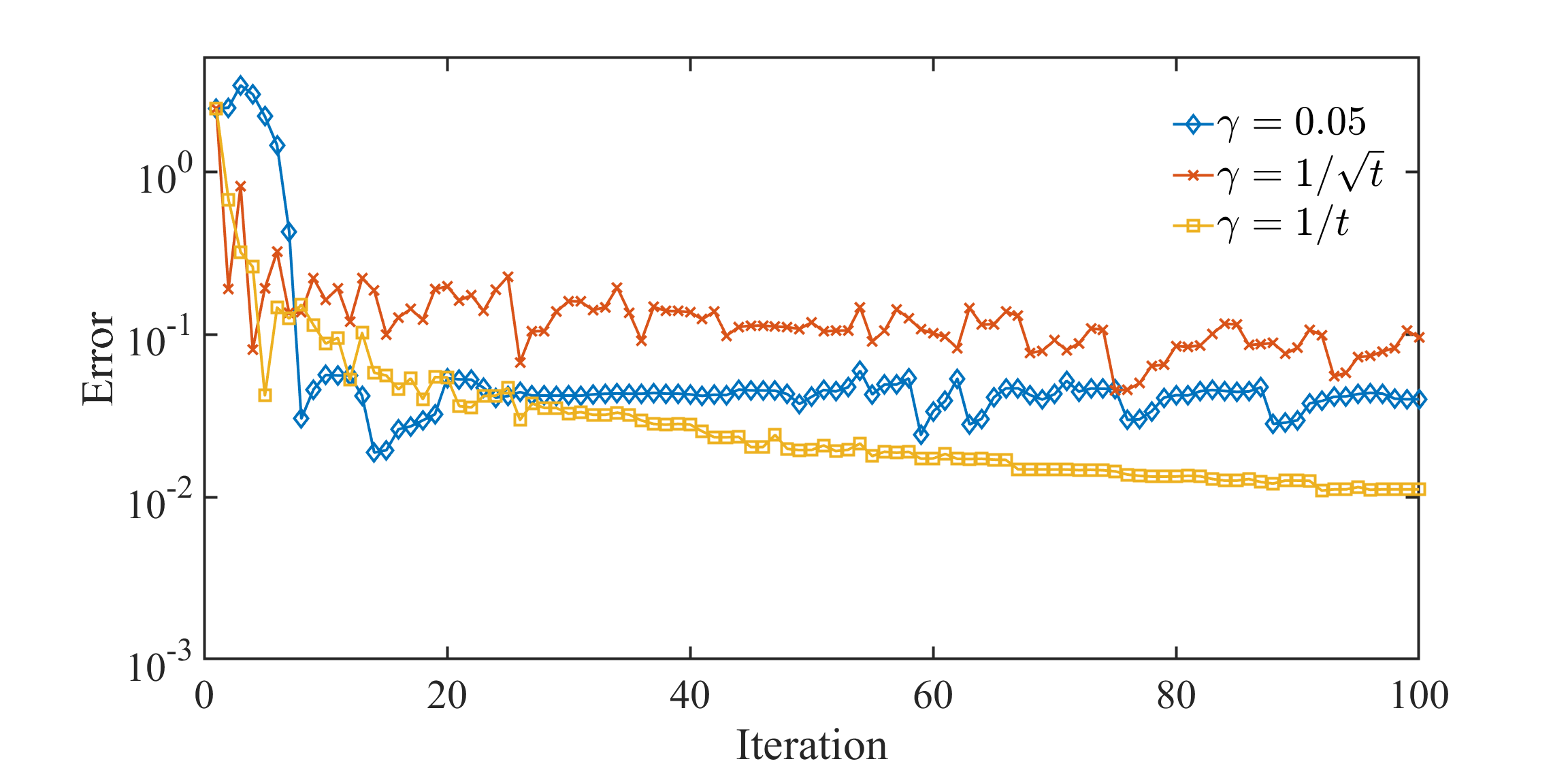

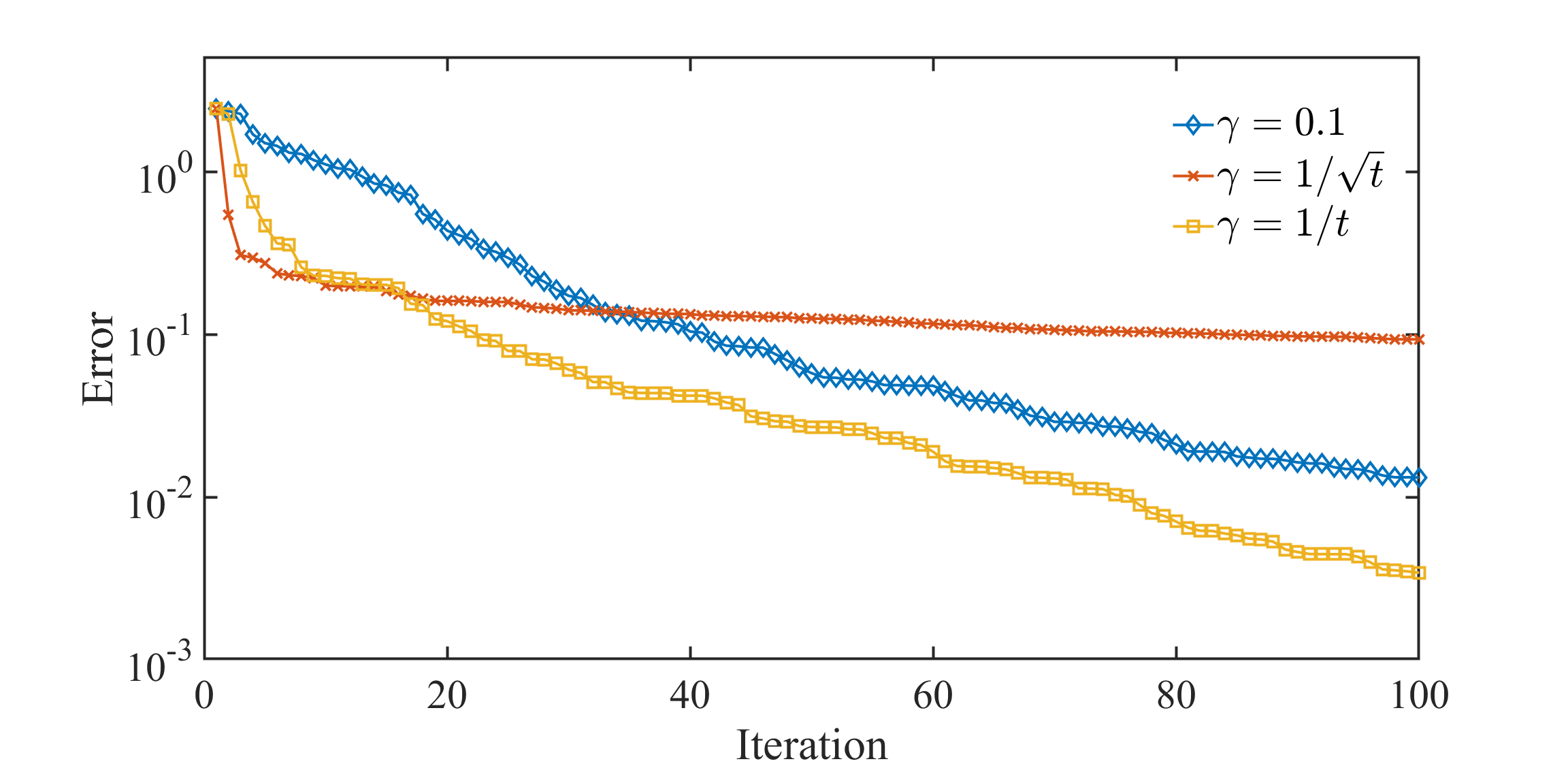

where is defined as (2.5). We detect the impact of the step sizes on the performance of Algorithm 1 with and constant step size under different regular terms and projection. From Figure 1, we can observe that for minimax problems with 2-norm and maximum function, compared to other step sizes, allows Algorithm 1 to obtain a faster convergence rate. Moreover, as can be seen from the three examples, makes the convergence more robust, which implies that the variance of the error generated by Algorithm 1 is smaller. Therefore, is a better choice for solving stochastic problems, which further confirms the conclusions numerically.

(a)

(b)

(c)

Figure 1: The trend of the error for (4.43) with respect to iteration.

4.2 General stochastic convex-concave minimax problems

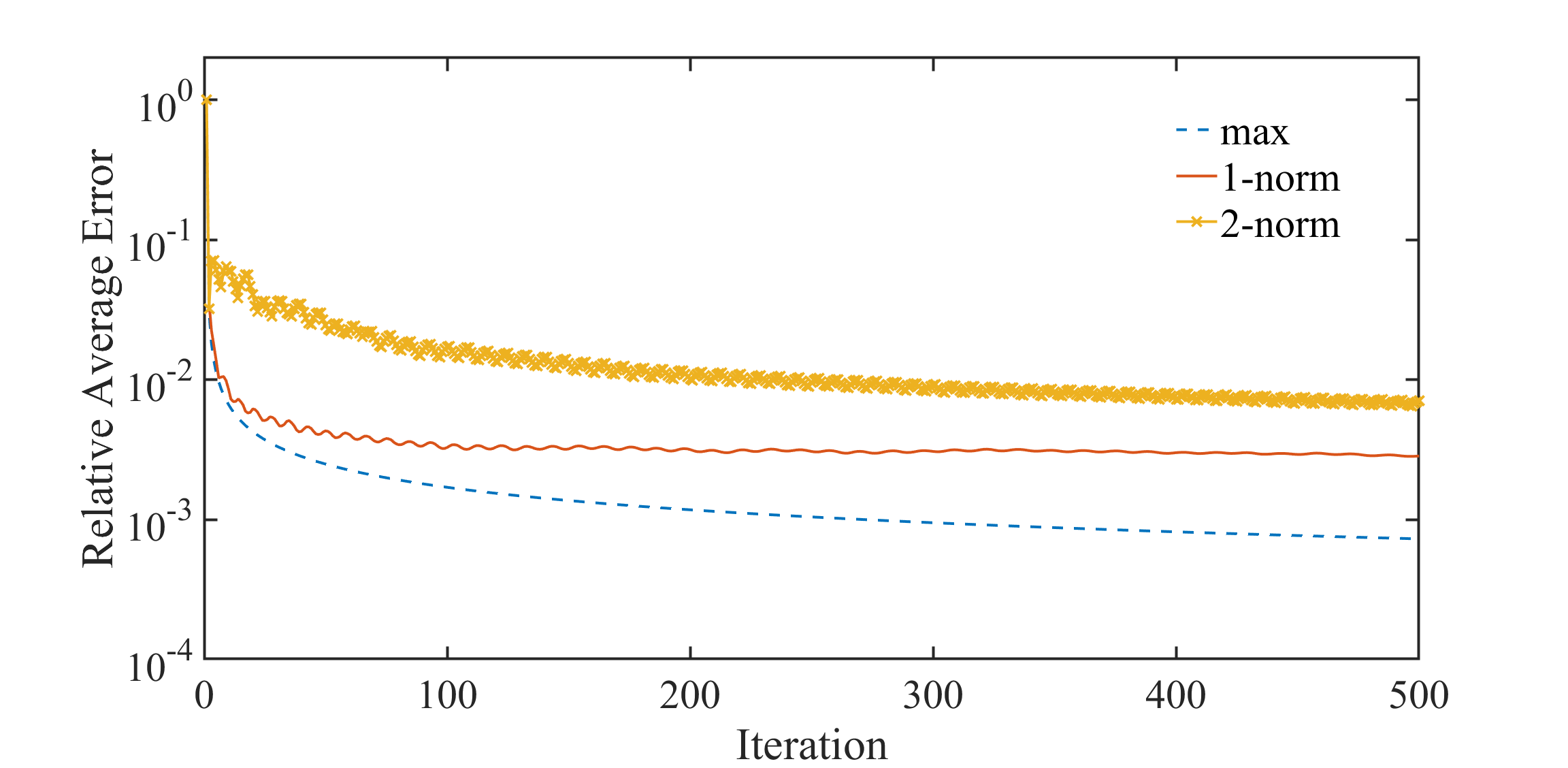

We considered the SAPS method in Algorithm 1 for solving a general stochastic convex-concave minimax problem as follows

(4.44)

where the feature vector are real random vectors uniformly distributed in the hypercube and represent the labels of the feature vector in the binary classification problem. Here we choose for some and for some . Let and be chosen as 1-norm, 2-norm and maximum function, respectively.

For Algorithm 1, we select the sub-samples

uniformly randomly from at th iteration and calculate

Moreover, we compute in (2.8) as the output of Algorithm 1. In order to verify the performance of our stochastic algorithm, it is necessary to find an approximate optimal solution to (4.44), since it is difficult to obtain “true” optimal solutions for (4.44) in high dimensions. Therefore, (4.44) is approximated by

where is a sufficiently large sample size. Let be the optimal solution of the above problem. In the following experiments, set the sample size , the initial points are randomly selected and the relative average error is computed by

The step size in Algorithm 1 is selected as .

(a)

(b)

(c)

(d)

Figure 2: The trend of the relative error for solving (4.44) with respect to iteration

Figure 2 shows the performance of Algorithm 1 for (4.44) with different dimensions and nonsmooth terms. As seen from Figure 2, Algorithm 1 has a rapid convergence in early iterations, and then maintains a linear convergence rate.

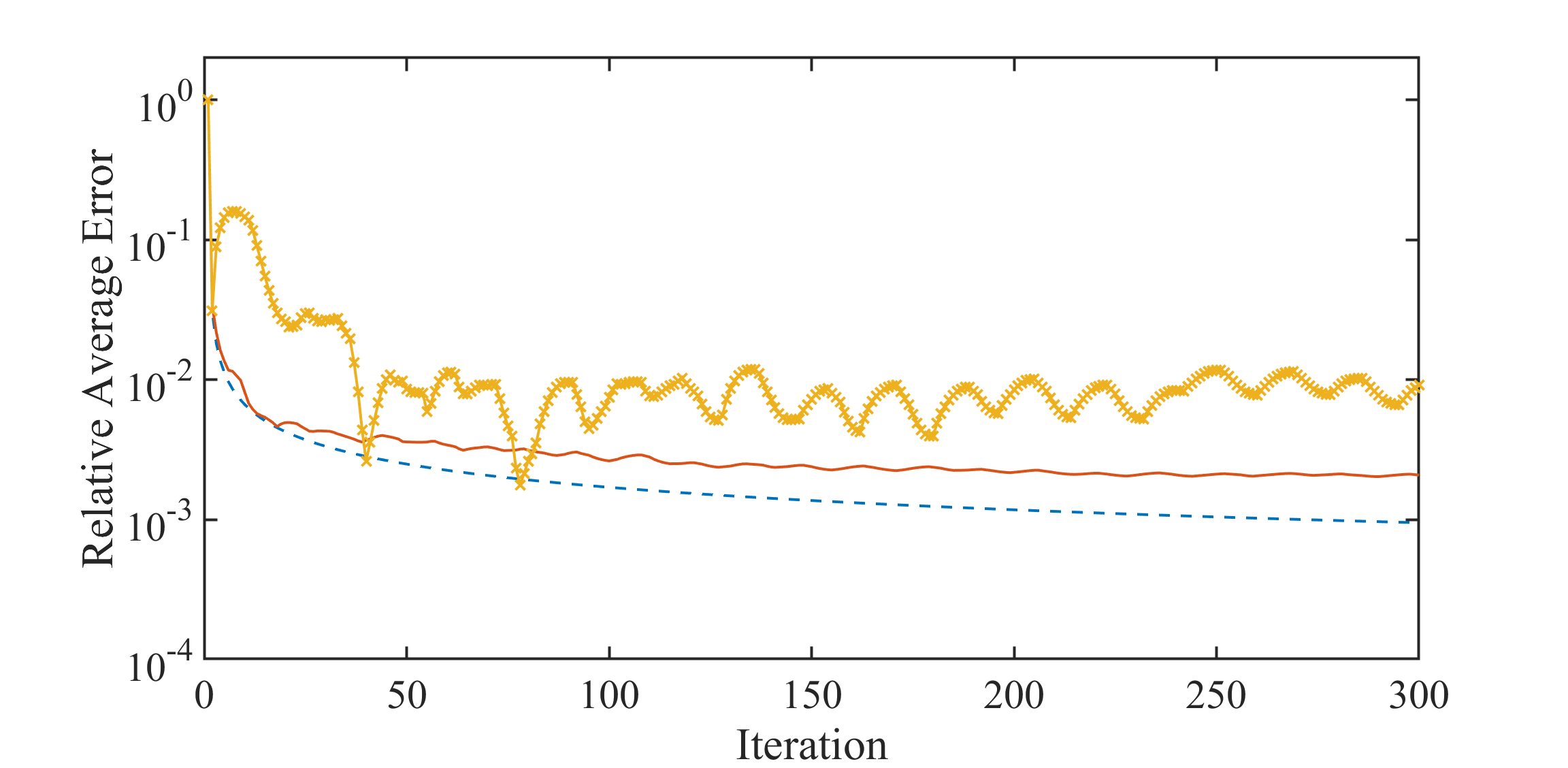

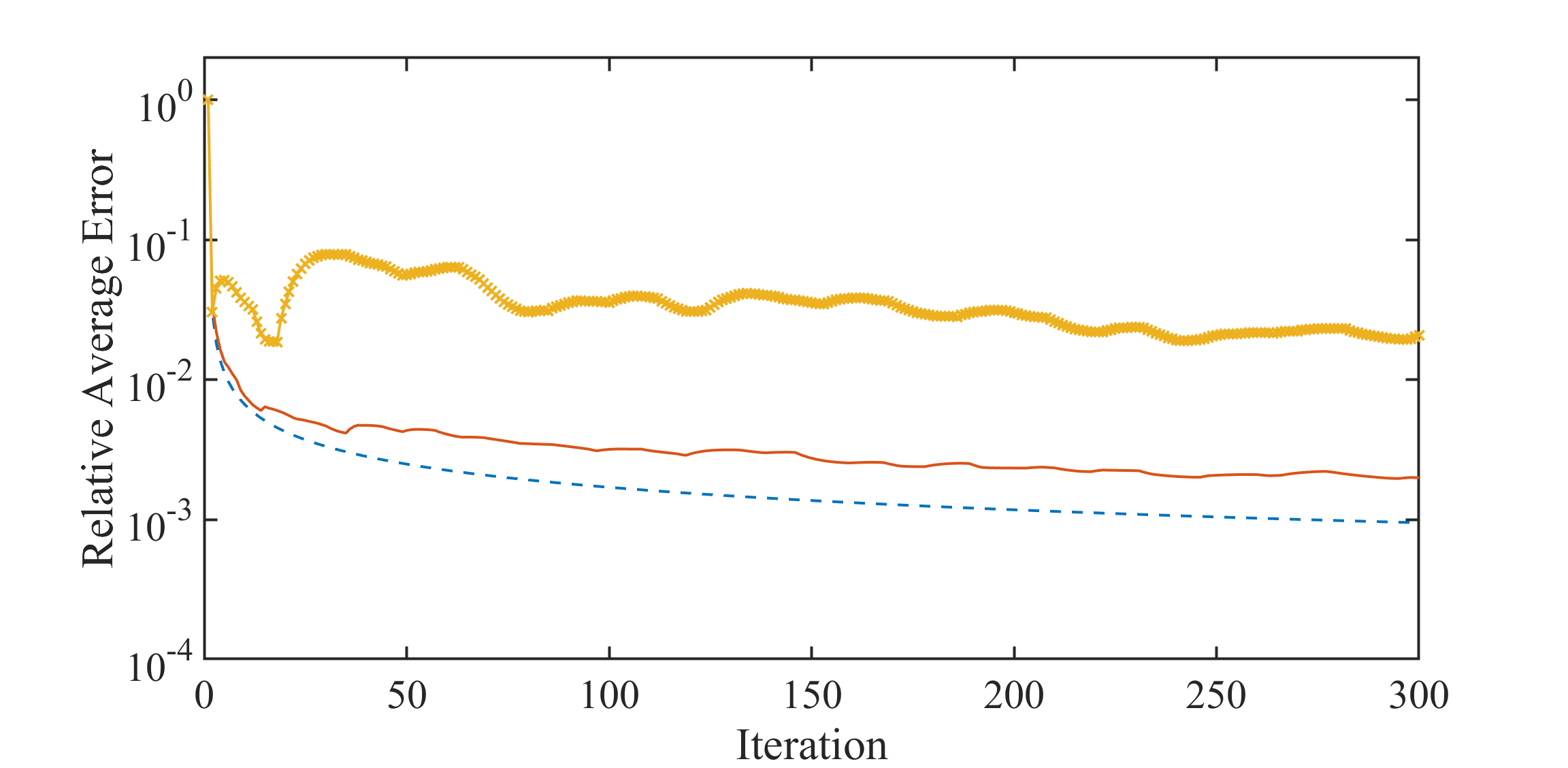

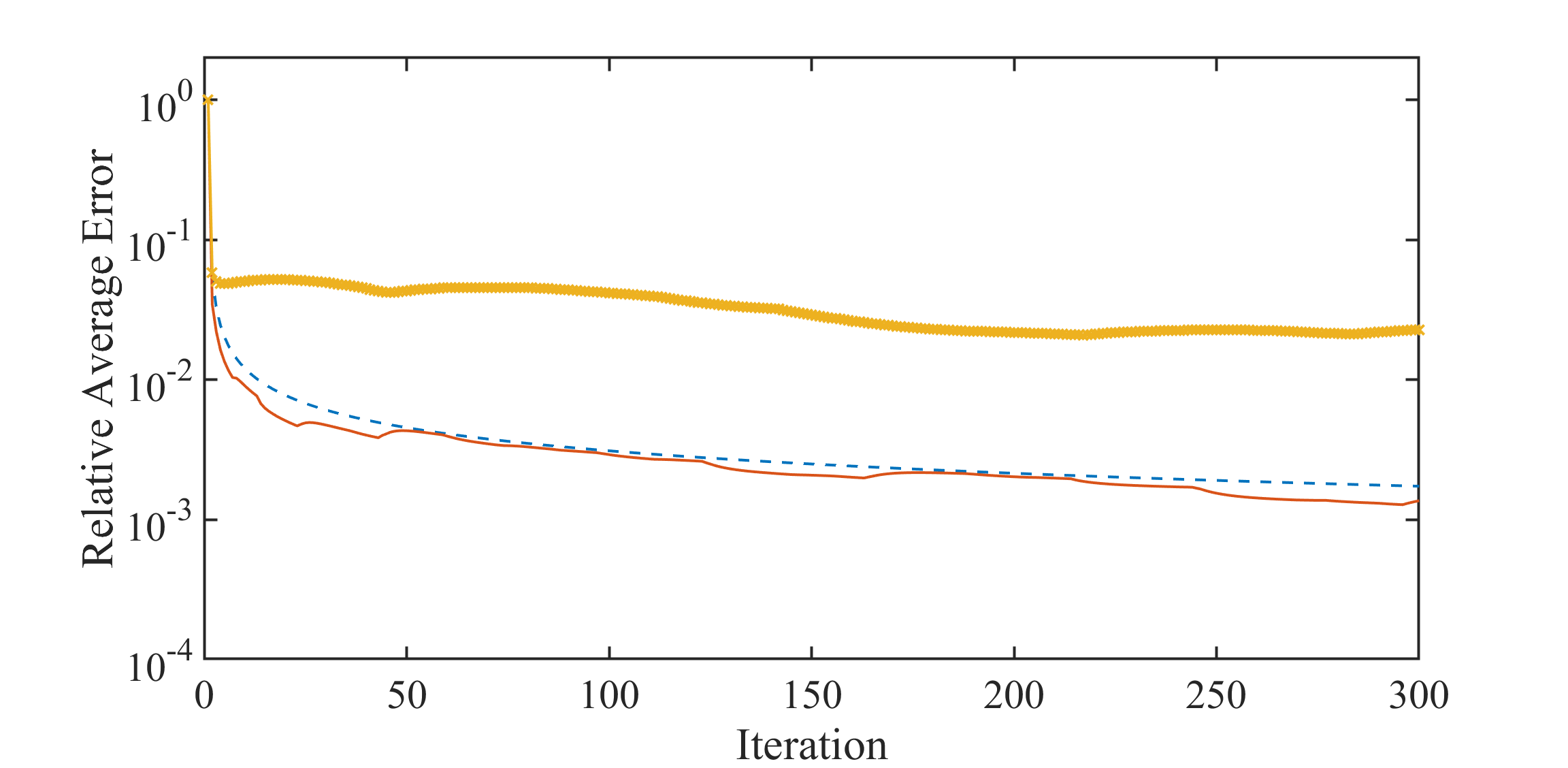

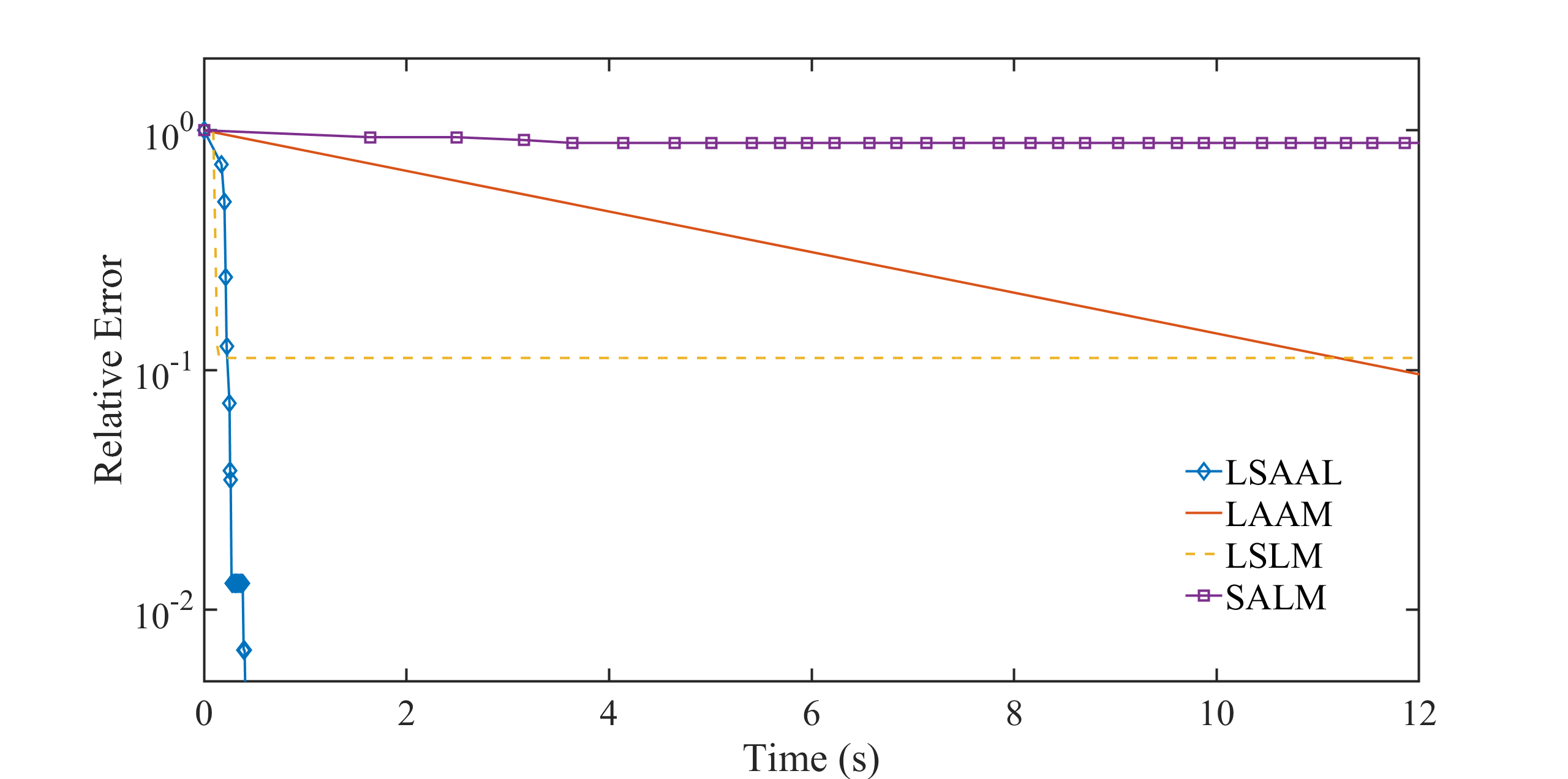

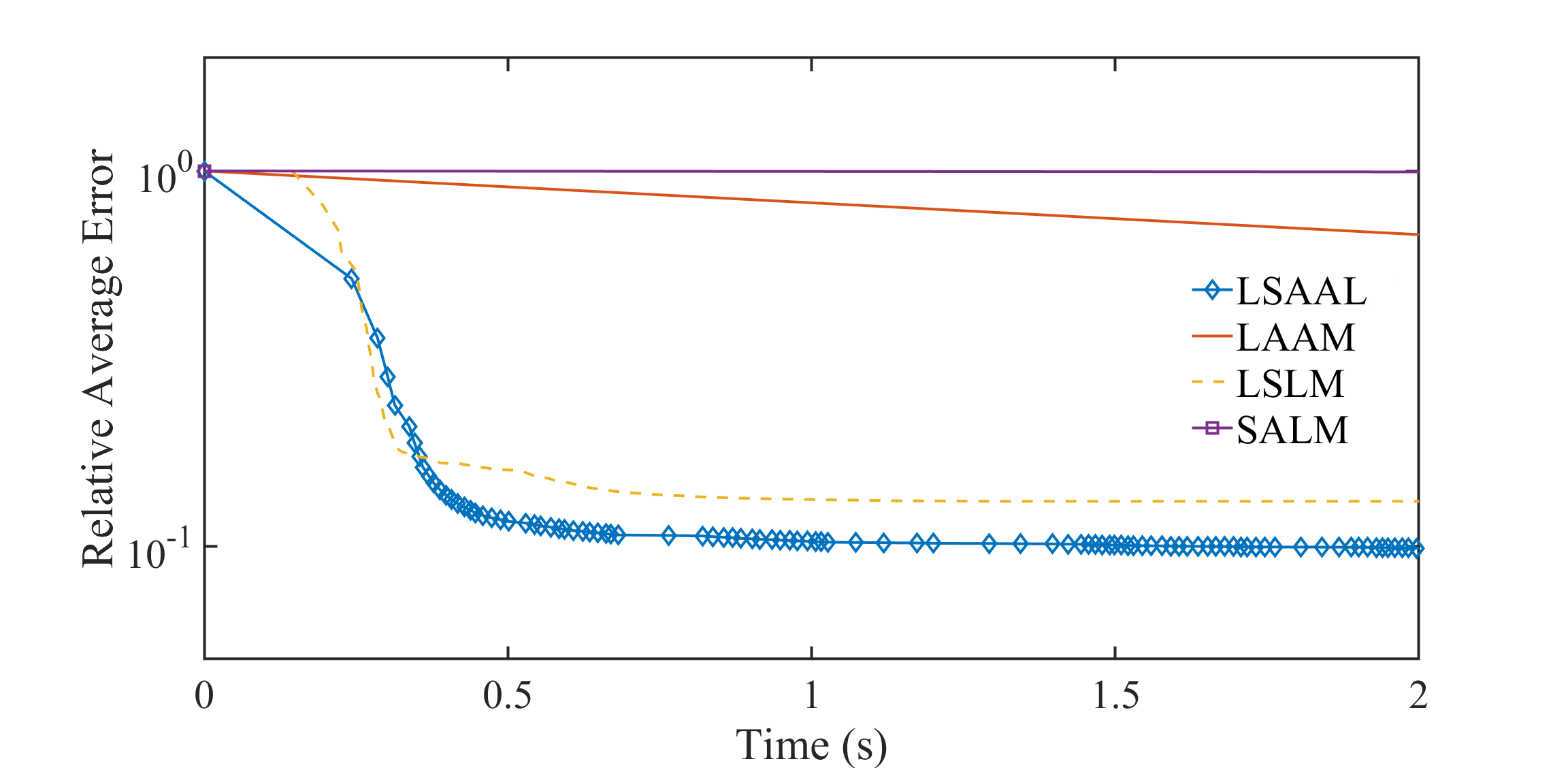

4.3 Multi-class Neyman-Pearson classification

We tested the LSAAL method in Algorithm 2 for the well-known multi-class Neyman-Pearson classification (see [Lin2020] for more details) as follow

(4.45)

where is a non-increasing

convex loss function defined as

For classes of data,

, denotes a random

variable defined using the distribution of data points associated with the -th class and the value of

is chosen to capture the misclassification cost of class . Here is a

regularization parameter. In numerical tests, we compared Algorithm 2 with the following three algorithms on data sets in Table 1.

LAAM

The deterministic linearized

approximation augmented Lagrange method.

LSLM

The proposed in [55] for stochastic convex programming.

SALM

The stochastic augmented

Lagrangian method proposed in [56] for stochastic convex programming.

Let follow the empirical distribution over the data set of class for , which

implies that all the expectations in (4.45) become finite-sample averages over data classes. We set parameters and for .

In order to test the performance of the algorithms more comprehensively,

we use in (2.5) and in (3.26) as the output of the algorithms to verify the convergence, respectively.

In the following experiments, the initial point is selected as the unit vector.

Due to the difficulty in solving the optimal solution of the stochastic convex programming (4.45),

we use the KKT condition to verify whether the output of the algorithms satisfies the optimality condition of (4.45).

Let , where is defined in (3.6).

The relative error and the relative average error are computed by

In the first numerical experiment with the relative error,

the step sizes are selected as in connect-4, covtype,

news20, respectively. In the second one with the relative average error,

the step sizes are selected as .

(a)connect-4

(b)covtype

(c)news20

(d)connect-4

(e)covtype

(f)news20

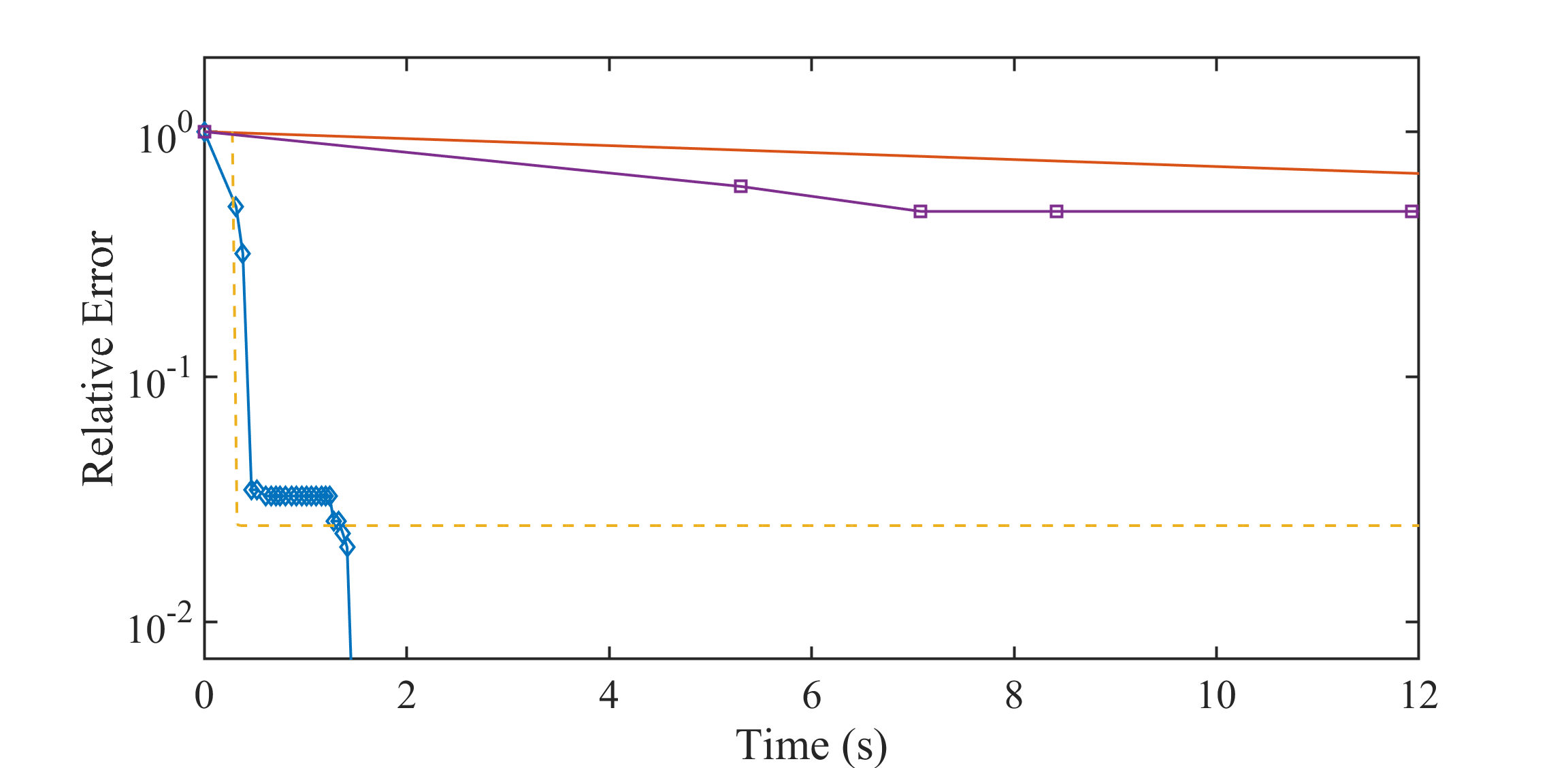

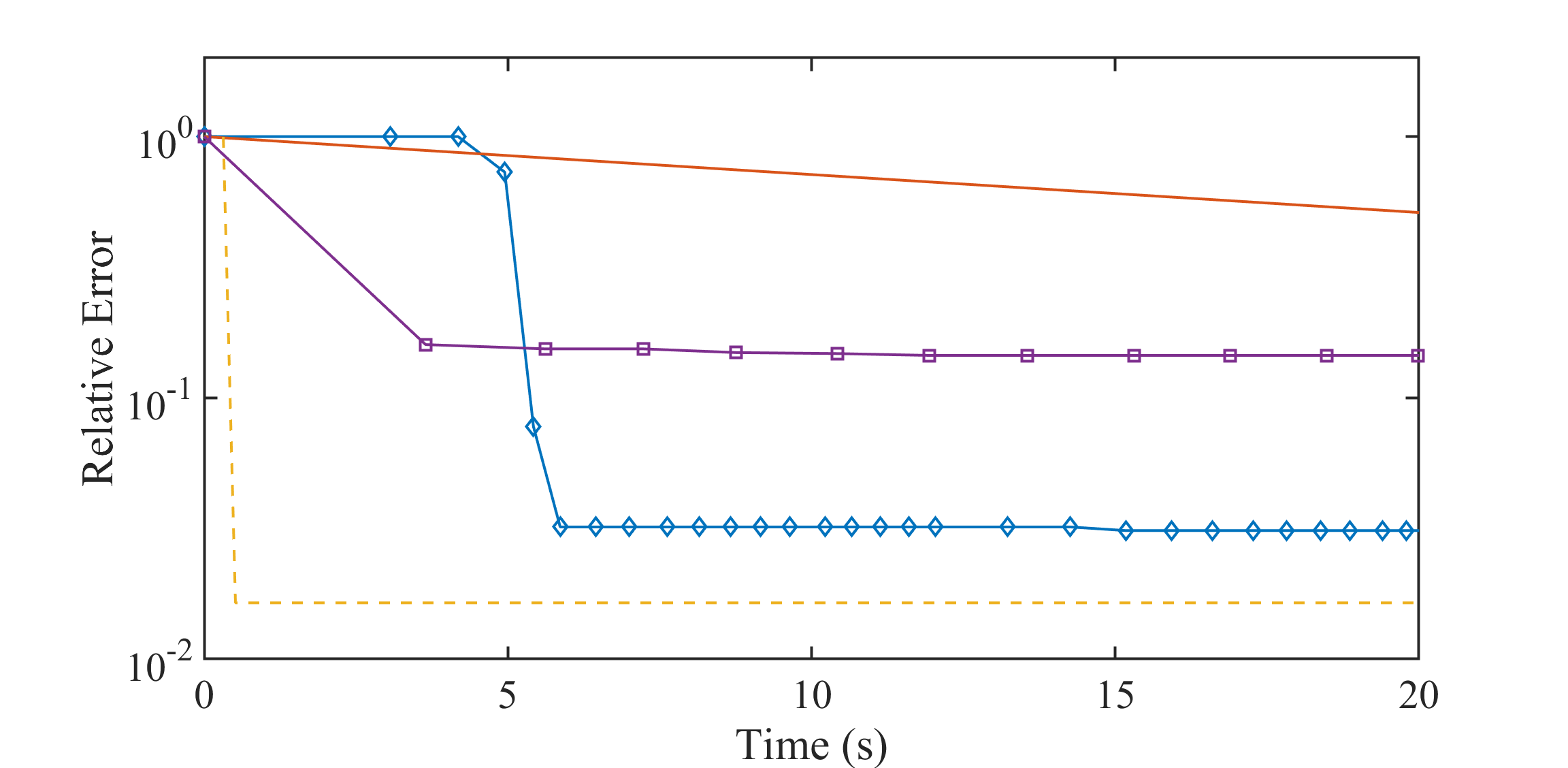

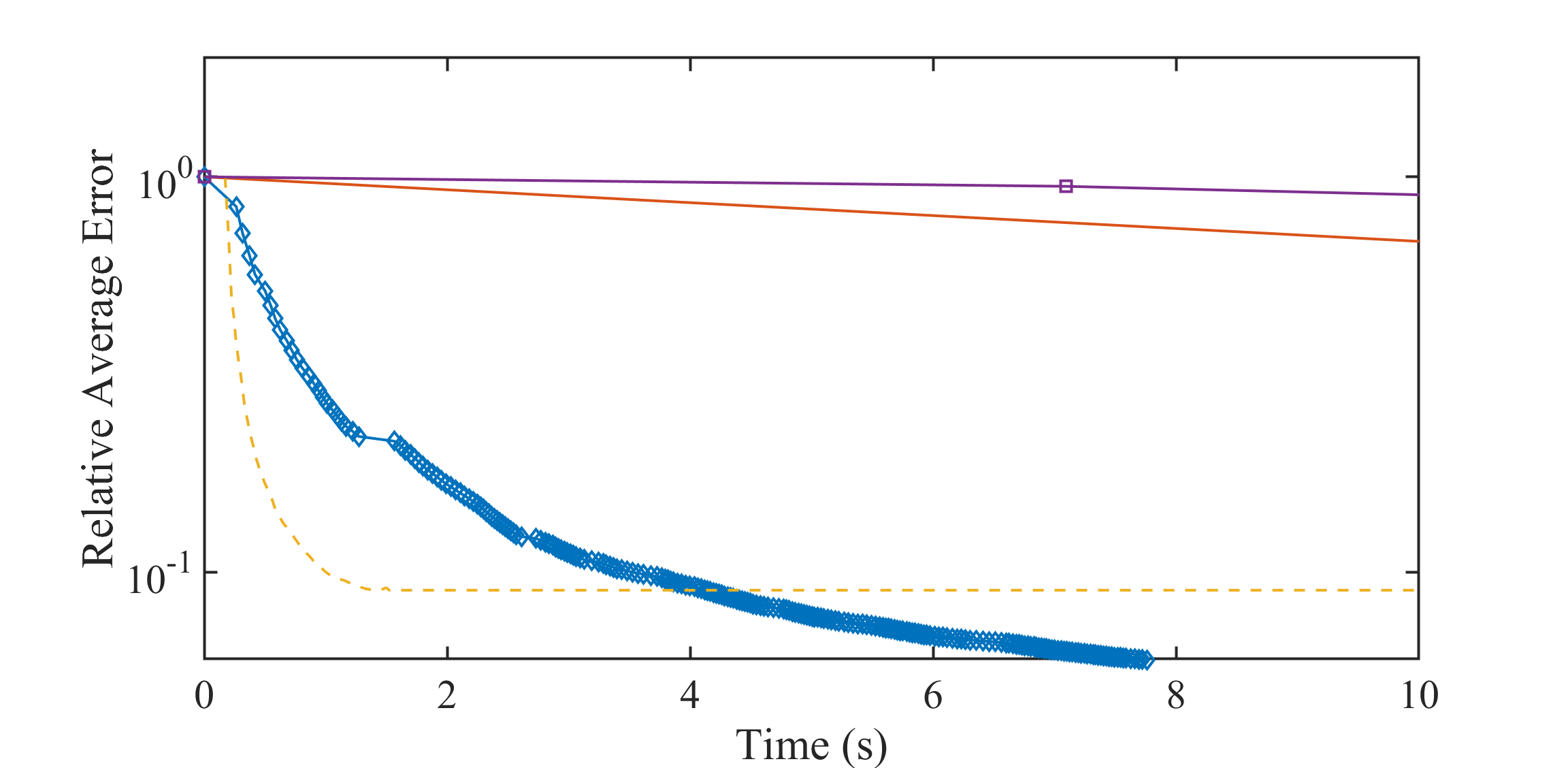

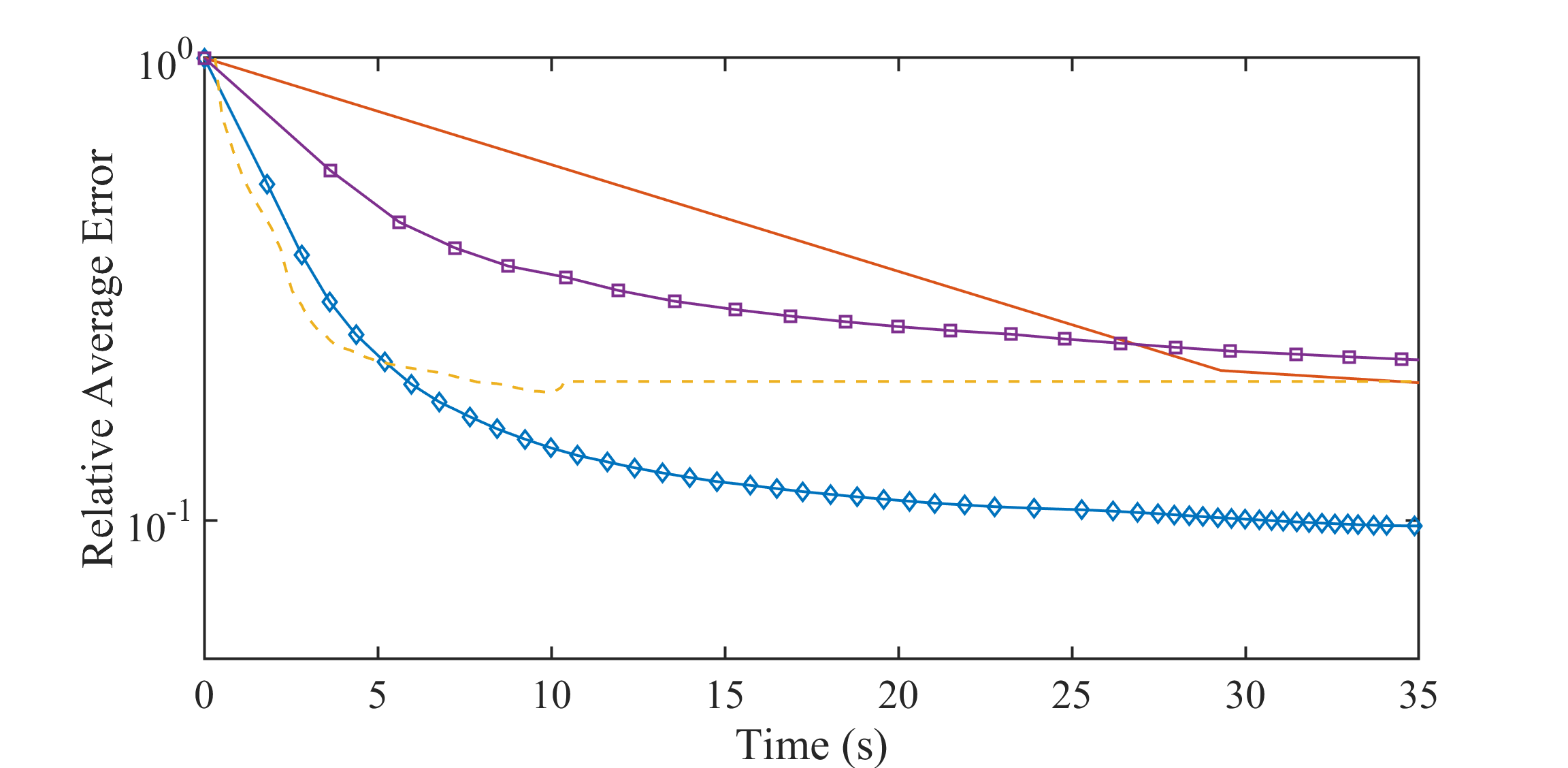

Figure 3: The trend of the relative error for solving (4.45) with respect to CPU time

The comparison between four algorithms is presented in Figure 3.

Here, “Time (s)” denotes the CPU time in seconds. Generally, LSAAL

performs faster than the other three algorithms.

Besides, the error generated in LSAAL decreases more

rapidly compared with other three algorithms in the early stage of iteration, especially on data set connect-4. This reveals that the combination of

linearization techniques and augmented Lagrange methods indeed does

benefit to the numerical performance of the algorithm.

5 Some dicussion

For the deterministic minimax optimization, there are many numerical methods in the literature, especially there are many mature numerical algorithms for the convex-concave minimax optimization.

However, for the stochastic minimax optimization, much attention should be paid to stochastic approximation algorithms. In this paper, we have studied the stochastic approximation proximal gradient method for stochastic convex-concave optimization of the form (1.1) and the linearized stochastic approximation augmented Lagrangian method for solving the minimax optimization arising from the stochastic convex conic optimization problems. We have shown that in the expectation sense the SAPS and LSAAL methods

exhibit sublinear convergence rate in terms of the minimax optimality measure if the parameters in the algorithm are properly chosen. Moreover, the large-deviation properties of the SAPS and LSAAL methods have been established under standard light-tail assumptions. The preliminary numerical experiments have demonstrated that the proposed algorithms are effective for solving the stochastic convex-concave minimax optimization. To the best of our knowledge, SAPS and LSAAL are the first stochastic algorithms for

solving the stochastic nonsmooth convex-concave minimax optimization and stochastic convex conic optimization. We believe that the SAPS and LSAAL methods extends the existing stochastic methods and are used to solve saddle point problems in

both modern machine learning and tradition research

areas such as saddle point problems, numerical partial differential equations and various types of bi-level optimization problems.

There are some recent works for the smooth nonconvex-concave stochastic optimization, see for instance [6] and [33]. For further work, an interesting topic is how to use the techniques in this paper to investigate the stochastic approximation proximal subgradient method to find optimal solutions of stochastic nonsmooth nonconvex-concave optimization (1.1) defined in [22].

References

[1]A. Akhavan, M. Pontil and A. Tsybakov, Distributed zero-order optimization under adversarial noise, Advances in Neural Information Processing Systems, 34, 2021, pp. 10209-10220.

[2]

A. Beck, First-Order Methods

in Optimization, Society for Industrial and Applied Mathematics,

Philadelphia, 2017.

[3] A. Ben-Tal, L. E. Ghaoui and A. Nemirovski, Robust Optimization, Princeton University Press, 2009.

[4]T. Ben-Nun and T. Hoefler, Demystifying parallel and distributed deep learning: An in-depth concurrency analysis, ACM Computing Surveys (CSUR), 52:4, 2019, pp. 1-43.

[5] J. F. Bonnans and A. Shapiro, Perturbation Analysis of Optimization Problems,

New York, Springer, 2000.

[6]

R. I. Boţ and A. Böhm, Alternating proximal-gradient steps for (stochastic)

nonconvex-concave minimax problems, arXiv preprint arXiv:2007.13605, 2020.

[7]L. Bottou, F. E. Curtis and J. Nocedal, Optimization methods for large-scale machine learning, SIAM review, 60:2, 2018, pp. 223-311.

[8]Y. Carmon, Y. Jin, A. Sidford and K. Tian, Coordinate methods for matrix games, In 2020 IEEE 61st Annual Symposium on Foundations of Computer Science (FOCS), 2020, pp. 283-293.

[9]C. C. Chang and C. J. Lin, LIBSVM: A library for support vector machines.

ACM Transactions on Intelligent Systems and Technology, 2:27, 2011, pp. 1-27. Software

available at http://www.csie.ntu.edu.tw/ cjlin/libsvm.

[10]Y. Chi, Y. M. Lu and Y. Chen, Nonconvex optimization meets low-rank matrix factorization: An

overview, IEEE Transactions on Signal Processing, 67:20, 2019, pp. 5239-5269.

[11]D. Davis and D. Drusvyatskiy,

Stochastic model-based minimization of weakly convex functions, SIAM Journal on Optimization, 29:1, 2019, pp. 207-239.

[12]T. Dietterich, Overfitting and undercomputing in machine learning, ACM Computing Surveys (CSUR), 27:3, 1995, pp. 326-327.

[13] P. Domingos, Bayesian averaging of classifiers and the overfitting problem, In International Conference on Machine Learning, 747, 2000, pp. 223-230.

[14] S. S. Du, J. Chen, L. Li, L. Xiao

and D. Zhou, Stochastic variance reduction

methods for policy evaluation, In Proceedings of the 34 th International Conference on Machine

Learning, 70, 2017, pp. 1049-1058.

[15] J. C. Duchi, M. I. Jordan, M. J. Wainwright and A. Wibisono, Optimal rates for zero-order convex optimization: The power of two function evaluations, IEEE Transactions on Information Theory, 61:5, 2015, pp. 2788-2806.

[16] D. Dvinskikh, V. Tominin, Y. Tominin and A. Gasnikov, Gradient-free optimization for non-smooth minimax problems with maximum value of adversarial noise, arXiv preprint arXiv:2202.06114, 2022.

[17]F. Farnia and A. Ozdaglar, Train simultaneously, generalize better: Stability of gradient-based minimax learners, International Conference on Machine Learning, 2021, pp. 3174-3185.

[18]

I. Goodfellow, J. Pouget-Abadie, M. Mirza, B. Xu, D. Warde-Farley, S.

Ozair, A. Courville and Y. Bengio, Generative adversarial nets, In Advances in

Neural Information Processing Systems, 2014, pp. 2672-2680.

[19]R.M. Gower, N. Loizou, X. Qian, A. Sailanbayev, E. Shulgin and P. Richtárik, Sgd: General analysis and improved rates, International Conference on Machine Learning, 2019, pp. 5200-5209.

[20]

F. H. Huang, S. Q. Gao, J. Pei and H. Huang,

Accelerated zeroth-order and first-order momentum

methods from mini to minimax optimization, Journal of Machine Learning Research, 23, 2022, pp. 1-70.

[21]K. Huang and S. Zhang, New first-order algorithms for stochastic variational inequalities, SIAM Journal on Optimization, 32:4, 2022, pp. 2745-2772.

[22]

C. Jin, P. Netrapalli and M. I. Jordan, What is local optimality in nonconvex-nonconcave minimax

optimization? In International Conference on Machine Learning, 2020, pp. 4880-4889.

[23]J. Kolluri, V. K. Kotte, M. S. B. Phridviraj and S. Razia, Reducing overfitting problem in machine learning using novel regularization method, In 2020 4th International Conference on Trends in Electronics and Informatics, 48184, 2020, pp. 934-938.

[24]

G. Lan, First-order and Stochastic Optimization Methods for Machine Learning,

Springer Series in the Data Sciences, Springer, Cham, 2020.

[25]Y. Lei, Z. Yang, T. Yang and Y. Ying, Stability and generalization of stochastic gradient methods for minimax problems, International Conference on Machine Learning, 2021, pp. 6175-6186.

[26]D. Levy, Y. Carmon, J. C. Duchi and A. Sidford, Large-scale methods for distributionally robust optimization, Advances in Neural Information Processing Systems, 33, 2020, pp. 8847-8860.

[27]X. Li and F. Orabona, On the convergence of stochastic gradient descent with adaptive stepsizes, The 22nd International Conference on Artificial Intelligence and Statistics, 2019, pp. 983-992.

[28] Q. Lin, S. Nadarajah, N. Soheili and T. Yang, A data efficient and feasible level set method for stochastic convex optimization with expectation constraints, Journal of Machine Learning Research, 21:143, 2020, pp. 1-45.

[29] T. Lin, C. Jin and M. I. Jordan, Near-optimal algorithms for minimax optimization, In Conference on Learning Theory, 2020, pp. 2738-2779.

[30] M. Liu, Y. Mroueh, J. Ross, W. Zhang, X. Cui, P. Das and T. Yang, Towards better understanding of adaptive gradient algorithms in generative

adversarial nets, arXiv preprint arXiv:1912.11940, 2019.

[31]

S. Liu, S. Lu, X. Chen, Y. Feng, K. Xu, A. Al-Dujaili, M.

Hong and U. Obelilly, Min-max optimization without gradients: convergence and applications to black-box evasion and poisoning attacks, In International conference on machine learning, 2020, pp. 6282-6293.

[32]L. Luo, G. Xie, T. Zhang and Z. Zhang, Near optimal stochastic algorithms for finite-sum unbalanced convex-concave minimax optimization, arXiv preprint arXiv:2106.01761, 2021.

[33] L. Luo, H. Ye and T. Zhang, Stochastic recursive gradient descent ascent for stochastic nonconvex-strongly-concave minimax problems, arXiv preprint

arXiv:2001.03724, 2020.

[34]

A. Nemirovski, A. Juditsky, G. Lan and A. Shapiro, Robust stochastic approximation approach to stochastic programming, SIAM Journal on Optimization, 19, 2009, pp. 1574-1609.

[35] M. Mahdavi, R. Jin and T. Yang, Trading regret for efficiency: online convex optimization with long term constraints, Journal of Machine Learning Research, 13:3, 2011, pp. 2503-2528.

[36]M. Mahdavi, T. Yang and R. Jin, Stochastic convex optimization with multiple objectives, in Proceedings of Neural Information Processing Systems, 2013, pp. 1115-1123.

[37]

B. T. Polyak,

New stochastic approximation type procedures,

Automat. i Telemekh.,

7, 1990, pp. 98-107.

[38]

B. T. Polyak and A. B. Juditsky,

Acceleration of stochastic approximation by averaging,

SIAM Journal on Control and Optimization,

30:4, 1992, pp. 838-855.

[39]S. Pu and A. Nedić, Distributed stochastic gradient tracking methods, Mathematical Programming, 187, 2021, pp. 409-457.

[40]

R. T. Rockafellar, Monotone operators and the proximal point algorithm,

SIAM Journal on Control and Optimization, 14, 1976, pp. 877-898.

[41]M. Schmidt, N. Le Roux and F. Bach, Minimizing finite sums with the stochastic average gradient, Mathematical Programming, 162, 2017, pp. 83-112.

[42]T. Sery and M. Cohen, On analog gradient descent learning over multiple access fading

channels, IEEE Transactions on Signal Processing, 68, 2020, pp. 2897-2911.

[43]A. Shapiro, D. Dentcheva and A. Ruszczynski, Lectures on Stochastic Programming: Modeling and Theory, MOS-SIAM Series on Optimization, 2021.

[44]Q. Tran-Dinh, D. Liu and L. M. Nguyen, Hybrid variance-reduced sgd algorithms for nonconvex-concave minimax problems, arXiv preprint arXiv:2006.15266, 2020.

[45]

H. Wai, Z. Yang, Z. Wang and M. Hong, Multi-agent reinforcement

learning via double averaging primal-dual optimization, In Advances in Neural Information Processing Systems, 2018, pp. 9649-9660.

[46]

H. Wai, M. Hong, Z. Yang, Z. Wang and K. Tang, Variance

reduced policy evaluation with smooth function approximation, In Advances in Neural

Information Processing Systems, 2019, pp. 5784-5795.

[47]

Z. Wang, K. Balasubramanian, S. Ma and M. Razaviyayn,

Zeroth-order algorithms for nonconvex minimax problems with improved complexities,

arXiv preprint arXiv:2001.07819, 2020.

[48]Z. Xu, J. Shen, Z. Wang and Y. Dai, Zeroth-order alternating randomized gradient projection algorithms for general nonconvex-concave minimax problems, arXiv preprint arXiv:2108.00473, 2021.

[49] Z. Xu, H. Zhang, Y. Xu and G. Lan, A unified single-loop alternating gradient projection algorithm for nonconvex-concave and convex-nonconcave minimax problems, Mathematical Programming, 2023, pp. 1-72.

[50]

T. Xu, Z. Wang, Y. Liang and H. V. Poor, Enhanced first and zeroth order

variance reduced algorithms for min-max optimization, arXiv preprint arXiv:2006.09361,

2020

[51]W. Xian, F. Huang, Y. Zhang and H. Huang, A faster decentralized algorithm for nonconvex minimax problems, Advances in Neural Information Processing Systems, 34, 2021, pp. 25865-25877.

[52]Y. Yan, Y. Xu, Q. Lin, W. Liu and T. Yang, Optimal epoch stochastic gradient descent ascent methods for min-max optimization, Advances in Neural Information Processing Systems, 33, 2020, pp. 5789-5800.

[53]J. Yang, N. Kiyavash and N. He, Global convergence and variance-reduced optimization for a class of nonconvex-nonconcave minimax problems, arXiv preprint arXiv:2002.09621, 2020.

[54]X. Ying, An overview of overfitting and its solutions, In Journal of Physics: Conference series, 1168:022022, 2019.

[55]

H. Yu, M. Neely and X. Wei, Online convex optimization with stochastic constraints,

Advances in Neural Information Processing Systems, 30, 2017.

[56]L. Zhang, Y. Zhang, X. Xiao and J. Wu, Stochastic approximation proximal method of multipliers for convex stochastic programming, Mathematics of Operations Research, 48:1, 2023, pp. 177-193.

[57]X. Zhang, N. S. Aybat and M. Gürbüzbalaban, Robust accelerated primal-dual methods for computing saddle points, arXiv preprint arXiv:2111.12743, 2021.

Appendix

In the proposed algorithms, we have to minimize a strongly convex function at each iteration, the following lemma plays an important role.

Lemma A.1.

Let be a finite-dimensional Hilbert space and be a proper lower semicontinuous convex function. Let be given and be a positive definite self-adjoint operator. Then the problem

has a unique solution, denoted by . For any ,

(A.1)

By , we denote the history of the process

up to time . Unless stated otherwise, all relations between random variables

are supposed to hold almost surely.

The following two lemmas are directly from [55, Lemma 5] and [24, Lemma 4.1], which are important in the convergence analysis.

Lemma A.2.

Let be a discrete time stochastic process adapted to a filtration with and . Suppose there exist an integer , real constants , and such that

hold for all Then the following properties are satisfied.

(i)

The following inequality holds,

(A.2)

(ii)

For any constant , we have

where

(A.3)

Lemma A.3.

Let be a sequence of i.i.d. random variables, and

be deterministic Borel functions of such that a.s. and

a.s., where are deterministic. Then