disposition

Measuring Dependence between Events††thanks: We thank seminar participants at Goethe University Frankfurt and Heidelberg Institute for Theoretical Studies and conference participants at CMStatistics 2023 in Berlin, Statistical Week 2023 in Dortmund and the 10th HKMetrics Workshop in Karlsruhe, 2023, for helpful comments. Marc-Oliver Pohle is grateful for support by the Klaus Tschira Foundation. Timo Dimitriadis gratefully acknowledges support of the Deutsche Forschungsgemeinschaft (DFG, German Research Foundation) through grant 502572912.

Abstract

Abstract

Measuring dependence between two events, or equivalently between two binary random variables, amounts to expressing the dependence structure inherent in a contingency table in a real number between and 1. Countless such dependence measures exist, but there is little theoretical guidance on how they compare and on their advantages and shortcomings. Thus, practitioners might be overwhelmed by the problem of choosing a suitable measure. We provide a set of natural desirable properties that a proper dependence measure should fulfill. We show that Yule’s and the little-known Cole coefficient are proper, while the most widely-used measures, the phi coefficient and all contingency coefficients, are improper. They have a severe attainability problem, that is, even under perfect dependence they can be very far away from and , and often differ substantially from the proper measures in that they understate strength of dependence. The structural reason is that these are measures for equality of events rather than of dependence. We derive the (in some instances non-standard) limiting distributions of the measures and illustrate how asymptotically valid confidence intervals can be constructed. In a case study on drug consumption we demonstrate how misleading conclusions may arise from the use of improper dependence measures.

Keywords: Binary Variables; Correlation; Phi Coefficient; Contingency Coefficients; Odds Ratio

1 Introduction

Analyzing dependence between two random variables is a fundamental task in statistics. The arguably simplest setting is the one of two binary random variables or, equivalently, two events, which is fully characterized by two marginal and a joint probability, and is conveniently represented in a contingency table. It is often useful to quantify the dependence structure inherent in the contingency table with a dependence measure, that is, a number lying between and 1 and indicating direction of dependence via its sign and strength of dependence via the closeness of its absolute value to 1. However, there exist many dependence measures for this task and hardly any theoretical guidance on the advantages and shortcomings of those measures and on their relationships. In this paper, we provide such a theoretical guidance based on a formal discussion of dependence concepts for events, an axiomatic approach to dependence measures and a theoretical analysis of existing measures and their relationships, leading to clear recommendations for statistical practice. We also develop statistical inference for the recommended measures.

1.1 Motivating Example

The quest for the most suitable dependence measure in the binary case already led to fierce debates among two of the greats of statistics, see Ekström, (2011) for an account of the so-called Pearson-Yule debate. We consider a motivating data example popular in that period, namely the relation between vaccination against and survival of smallpox. The left part of Table 1 contains absolute marginal and joint frequencies for the events and and their complements for the smallpox epidemic in Leicester in 1892/93 taken from Yule, (1912). Looking at the table, the relation between the two events seems positive and quite strong. However, of course a formal way to quantify this dependence is required.

Contingency Table recovery death vaccinated 197 2 199 unvaccinated 139 19 158 336 21 357

Estimated Dependence Measures measure value 90% CI Phi coefficient 0.23 Yule’s 0.86 Cole’s coefficient 0.83

While countless measures for this task have been proposed (see Warrens, (2019) for a comprehensive overview of such measures and their use in different disciplines), their theoretical properties and relationships have hardly been studied. Thus, it is difficult to pick a measure in practice and, if multiple measures are used, to understand why they often lead to different conclusions. Due to the lack of theoretical guidance, practitioners understandably are likely to choose the most popular measures. Table 2 contains the hits of a recent search for eight measures on Google and Google Scholar as a proxy for their popularity in practice and academia together with their estimated values on the smallpox data example of Table 1. The most popular measures can clearly be found on the left side, namely the phi coefficient (referred to as Matthews correlation coefficient in the machine learning literature (Matthews,, 1975)) and contingency coefficients, of which Cramér’s V is the most well-known representative.111Note that contingency coefficients are applicable to general contingency tables. Thus, the hits may overstate the importance of Cramér’s V for the specific case. Those measures take rather small values between 0.22 and 0.23, suggesting weak positive dependence between the two events. In contrast, the measures on the right side lie between 0.45 and 0.83, indicating a rather strong dependence and being more in line with the impression one gets when looking at the contingency table. We demonstrate in this article that there is a reason for this impression and that indeed the measures on the right-hand side are theoretically superior to the ones on the left-hand side. The former, even though less widely-used, fulfill a set of crucial properties of dependence measures and thus give a sensible assessment of dependence.

Improper Dependence Measures measure value Google Scholar Cramér’s V Matthews cor. Phi coef. Pearson cont. coef.

Proper Dependence Measures measure value Google Scholar Tetrach. cor. Yule’s Yule’s Cole’s coef.

1.2 Plan of the Paper

A sound discussion of dependence measures and their properties requires underlying dependence concepts as a fundament: In Section 2 we introduce concepts of positive and negative, of stronger and weaker and of perfect dependence between two events. In Section 3 we provide a formal definition of dependence measures for events, postulate desirable properties for them and call a dependence measure proper if it fulfills them.

After a discussion of the covariance in the case of binary random variables, which serves as a building block for most of the other measures, Section 4 treats the popular, but improper, measures. We show that the phi coefficient, which is just a special case of the classical Pearson correlation coefficient, lacks the fundamental property of attainability. That is, it does in general not take the values 1 and under perfect positive and negative dependence. We further demonstrate that it may take very small (absolute) values in those cases and usually strongly understates strength of dependence, where the severity of this problem depends on the marginal event probabilities. The phi coefficient consequently cannot provide a reliable assessment of strength of dependence and the usual interpretation of values close to 0 indicating weak and absolute values close to 1 indicating strong dependence does not apply here. While the phi coefficient can hence not be regarded as a suitable dependence measure, we show that it is instead useful for a different task, namely measuring closeness to equality of two events. This is for example required in the evaluation of binary classifiers, where equality of classification and outcome characterizes a perfect classifier. We also discuss several popular contingency coefficients and show that for contingency tables they are simple functions of the phi coefficient and thus inherit its shortcomings.

Section 5 is dedicated to proper dependence measures. Cole’s coefficient is a very natural measure, just normalizing the covariance with its values under perfect positive and negative dependence. Yule’s uses a different normalization, not requiring a case distinction between positive and negative dependence. We also touch upon a whole class of measures that generalize , including Yule’s , and on tetrachoric correlation. A measure that falls out of the classical framework of dependence measures lying between and 1, but is extremely popular and nicely interpretable, is the odds ratio, which is closely connected to Yule’s as well. We show that it is proper too.

Our focus for the rest of the paper then lies on the phi coefficient, Yule’s and Cole’s coefficient as basically all the other measures discussed are closely related to the first two and share their properties. We first compare their values under different marginal event probabilities, which demonstrates that the phi coefficient differs in general quite strongly from the proper measures and sheds light on their relation as well.

In Section 6 we derive the asymptotic distributions of their empirical counterparts , and , under assumptions covering independent and identically distributed observations, but also time series data. and are asymptotically normal, allowing for tests and confidence intervals in the classical way. For the limiting distribution is highly nonstandard and involves case distinctions with respect to the value of the true due to the case distinction used in its normalization. While testing is straightforward, we construct possibly conservative confidence intervals by a Bonferroni-corrected combination of inverted tests that are built on the different asymptotic distributions. For all three measures, we also derive the limiting distribution of the Fisher transformation, which leads to a better approximation than the classical limit distribution when the measures lie close to or 1 and employ them for testing and confidence intervals. E.g., the right side of Table 1 shows -confidence intervals based on the Fisher transform for the data example.

Section 7 presents an application to drug use data, where we analyze the interdependence between the consumption of different drugs. It illustrates the relevance of using proper dependence measures: The phi coefficient suggests a very weak interdependence, while the proper measures indicate that it is quite strong, being in line with the gateway hypothesis of drug use.

Section 8 concludes. The Appendix contains all proofs, further details on some of the discussed dependence measures and on asymptotics, additional tables and graphs and simulations investigating the finite sample performance of our confidence intervals. An accompanying R package called BCor is available at https://github.com/jan-lukas-wermuth/BCor and replication material is available under https://github.com/jan-lukas-wermuth/replication_BCor.

1.3 Literature

The most popular dependence measures for binary random variables were already introduced around the year 1900. According to Ekström, (2011), the phi coefficient was independently proposed by Pearson, (1900), Boas, (1909) and Yule, (1912). Yule’s was introduced by Yule, (1900) and tetrachoric correlation in Pearson, (1900). Yule, (1912) is a foundational paper too, amongst others introducing Yule’s as a variant of Yule’s . In the subsequent decades, several contingency coefficients have been proposed such as Pearson’s contingency coefficient (Pearson,, 1904), Cramér’s V (Cramér,, 1945) and Tschuprow’s T (Tschuprow,, 1925). Cole’s coefficient was introduced by the ecologist Cole, (1949) and remained largely unnoticed by the statistical literature.

Despite this strong early interest and the widespread use of these measures in applications, the theoretical literature on them has surprisingly been very slim since those early years. Bishop et al., (2007, Chapter 11) and Warrens, (2008) are noteworthy exceptions, taking into account some theoretical properties.

The literature on dependence measures for general random variables is much larger, see Balakrishnan and Lai, (2009); Mari and Kotz, (2001); Tjøstheim et al., (2022) for overviews. The axiomatic approach to the study of general dependence measures originating in Rényi, (1959) is the role model for our treatment of the binary case. However, the literature usually restricts itself to the case of continuous random variables (e.g. Schweizer and Wolff, (1981), Embrechts et al., (2002)), which excludes the binary case, and entails important differences. Nešlehová, (2007) marks a noteworthy exception, providing a discussion of rank correlations in the discrete case from a copula perspective.

Asymptotic sampling variances for estimators of and are already discussed in the original papers cited above, but restricted to the case of independent and identically distributed data. Inference for Cole’s coefficient has not been developed yet.

2 Dependence Concepts for Events

2.1 Setup

Consider a probability space and two events with and . We are interested in measuring direction and strength of dependence between those two events, or equivalently, between the two dichotomous or binary random variables and , which take the value 1 if or , respectively, happen and 0 if not. Denote the complements of and by and . The joint distribution is fully characterized by three of the four joint probabilities , , and or one joint and the two marginal probabilities, e.g., , and . It can conveniently be represented in a contingency table as in Table 3.

| 1 |

2.2 Direction of Dependence and Dependence Ordering

We now define some fundamental dependence concepts. Even nominal dichotomous variables can be treated as ordinal when it comes to measuring dependence as there is always a natural ordering, namely the event happening or not. Thus, it makes sense to not only analyze strength, but also direction of dependence in this setting. We speak of positive (negative) dependence when makes more (less) likely or vice versa. Recall the ubiquitous definition of independence of and via . A surprisingly much lesser-known, but equally fundamental, definition is the following (Falk and Bar-Hillel,, 1983), which is a special case of the notion of quadrant dependence for arbitrary random variables introduced by Lehmann, (1966).

Definition 2.1 (Positive and Negative Dependence).

Two events are positively dependent if . They are negatively dependent if

An equivalent expression for positive (negative) dependence can be found in terms of conditional probabilities, i.e. or .

The following definition captures a natural way of ordering pairs of events in terms of strength of dependence if the respective marginal event probabilities are equal. The more likely two events are to occur together, that is, the larger their intersection is, the stronger positively dependent they are and vice versa for negative dependence.

Definition 2.2 (Stronger Dependence).

Consider two pairs of events and with and . Then and are stronger positively dependent than and if . and are stronger negatively dependent than and if . They are equally dependent if .

Again, stronger positive (stronger negative) [equal] dependence can equivalently be expressed in terms of conditional probabilities: or . This definition can be seen as a special case of the dependence ordering for random variables with identical marginals discussed by Yanagimoto and Okamoto, (1969) and Tchen, (1980). While for non-binary random variables this ordering is only partial, here in the binary case we get a complete ordering.

2.3 Perfect Dependence

We now introduce concepts of perfect positive and negative dependence between events. We are not aware of a discussion of this key issue in the literature, even though a thorough treatment of dependence measures is not possible without such concepts. Fortunately, they are very natural as well. From Definition 2.2 we know that for fixed event probabilities the dependence between and gets stronger in the positive direction if the intersection grows. The dependence gets maximal when and occur together as often as possible. This is the case when the intersection reaches its maximal size, that is, when the smaller event is a subset of the larger and thus the intersection is equal to the smaller event almost surely. Conversely, the dependence gets strongest in the negative sense when and occur together as little as possible, that is, when their intersection reaches the minimal size or, in other words, if one event is a subset of the complement of the other event or vice versa almost surely.

Definition 2.3 (Perfect Dependence).

and are perfectly positively dependent if . They are perfectly negatively dependent if . We call and perfectly dependent if they are perfectly positively or perfectly negatively dependent.

We establish three characterizations of perfect dependence.

Proposition 2.4 (Characterizations of Perfect Dependence).

-

(i)

and are perfectly positively dependent if and only if . They are perfectly negatively dependent if and only if . It further holds that .

-

(ii)

and are perfectly positively dependent if and only if it holds that or . They are perfectly negatively dependent if and only if it holds that or .

-

(iii)

and are perfectly positively dependent if and only if it holds that or . They are perfectly negatively dependent if and only if it holds that or .

Part (i) of this Proposition expresses perfect dependence in terms of the relationship between the joint probability of the events and and their marginal probabilities. The bounds established there are crucial for the construction and understanding of dependence measures. They are the essence behind and at the same time special cases of the Fréchet-Hoeffding bounds for bivariate cumulative distribution functions (CDFs) (Fréchet,, 1951; Hoeffding,, 1940) and we call them Fréchet-Hoeffding bounds for probabilities. Part (i) also establishes that our definition of perfect dependence from Definition 2.3 falls under the notion of co- and countermonotonicity of two random variables, which is usually defined via the Fréchet-Hoeffding bounds for CDFs (Embrechts et al.,, 2002), when considering the two indicators and . From now on we therefore use the terms perfect positive (negative) dependence and comonotonicity (countermonotonicity) of events interchangeably. Part (ii) reformulates Definition 2.3 in terms of conditional probabilities. Part (iii) states that perfect positive dependence is equivalent to at least one of the elements of the secondary diagonal of Table 3 being 0 and perfect negative dependence is equivalent to at least one of the elements of the primary diagonal being 0. As a consequence, and are perfectly dependent if and only if any of the joint probabilities in the contingency table is 0.

Finally, we state a lemma on dependence concepts for complements for later use.

Lemma 2.5 (Dependence Concepts for Complements).

-

(i)

and are positively (negatively) dependent if and only if and are negatively (positively) dependent.

-

(ii)

and are stronger positively (negatively) dependent than and if and only if and are stronger negatively (positively) dependent than and .

-

(iii)

and are perfectly positively (negatively) dependent if and only if and are perfectly negatively (positively) dependent.

3 Desirable Properties of Dependence Measures

We want to express the dependence between two events and or the corresponding binary random variables by a single number, a dependence measure.

Definition 3.1 (Dependence Measure).

A dependence measure for the events and is a mapping , , where . We write .

We consider dependence measures that indicate direction as well as strength of dependence. To be useful, they should fulfill certain properties. Many such sets of properties have been put forward since Rényi, (1959), which, however, usually focus on the case of continuous random variables (e.g. Schweizer and Wolff, (1981), Embrechts et al., (2002), Mari and Kotz, (2001), Balakrishnan and Lai, (2009), Fissler and Pohle, (2023)). Hence, the following definition establishes such a desirable set of properties for the binary case.

Definition 3.2 (Proper Dependence Measure).

We call a dependence measure for the events and proper if it fulfills the following properties.

-

(A)

Normalization: .

-

(B)

Independence: if and only if and are independent.

-

(C)

Attainability: if and only if and are perfectly positively (negatively) dependent.

-

(D)

Monotonicity: Let and be two further events with and . Then, if and only if and are stronger positively (negatively) dependent than and .

-

(E)

Symmetry: and .

Usually, directed dependence measures lie in the interval (property (A)), where negative values indicate negative and positive values indicate positive dependence. (B) and (C) make sure that correctly indicates the extreme cases of independence as well as perfect positive and negative dependence. Note that, contrary to the case of two general random variables, a dependence measure in the binary case is not a summary measure in the sense of having to condense information (a complicated dependence structure characterized fully by a joint CDF or copula) into a single number, but it usually characterizes the full dependence structure in this single number in the sense that given the marginal event probabilities and and the dependence measure , we can recover (indeed, this is possible for all measures discussed in this paper except for the contingency coefficients). As a consequence of this, the “only if” in (B) is infeasible for directed measures of dependence for arbitrary random variables (Embrechts et al.,, 2002), but in the binary case it is feasible. (D) is a very natural property, making sure that stronger dependence leads to more extreme values of . It is related to the property of coherence proposed by Scarsini, (1984). (C) and (D) ensure that a dependence measure is a sensible indicator of strength of dependence in that larger absolute values of the measure indicate stronger dependence and absolute values close to 0 and 1 indicate weak and strong dependence, respectively. Properties (B) and (D) also imply that the measure correctly indicates the direction of dependence as formalized through the following Proposition.

Proposition 3.3.

For a dependence measure satisfying and from Definition 3.2, it holds that if and only if and are positively (negatively) dependent.

The first part of (E) is just classical symmetry and the second part demands that when considering the complement of one event (or, in other words, exchanging rows or columns of the corresponding contingency table), the sign of the dependence measure should be reversed. It also implies that .

4 Improper Dependence Measures

4.1 Covariance

The definition of positive (negative) dependence (see Definition 2.1) suggests a natural way to measure direction and strength of dependence: Consider the deviation of the joint probability from the joint probability under independence, , which equals the covariance of and .

Definition 4.1 (Covariance).

We call the covariance of the events and .

The covariance can be rewritten as

| (1) |

that is, as the difference of the products of the elements of the primary and the secondary diagonal of the corresponding contingency table. Covariance is the foundational building block for most dependence measures discussed in this article.

It already fulfills all but one of the properties of a proper dependence measure. Using the Fréchet-Hoeffding bounds for probabilities from Proposition 2.4, we get what we call Fréchet-Hoeffding bounds for covariance,

| (2) |

They imply . Thus, property (A) is fulfilled, but property (C) is not. Properties (B) and (D) follow by definition of independence and stronger positive (negative) dependence, (E) directly by representation (1).

Proposition 4.2.

fulfills properties (A), (B), (D) and (E) from Definition 3.2, but not (C).

Thus, if one found a suitable normalization that made the covariance attainable, a proper dependence measure would arise. Indeed, the phi coefficient, Cole’s and Yule’s , which we discuss below, all turn out to be normalized versions of the covariance.

4.2 Phi Coefficient

The phi coefficient is just the classical Pearson correlation coefficient (as well as Spearman’s and Kendall’s , which all coincide in this setting) of and and thus a normalized version of .

Definition 4.3 (Phi Coefficient).

The phi coefficient is defined as

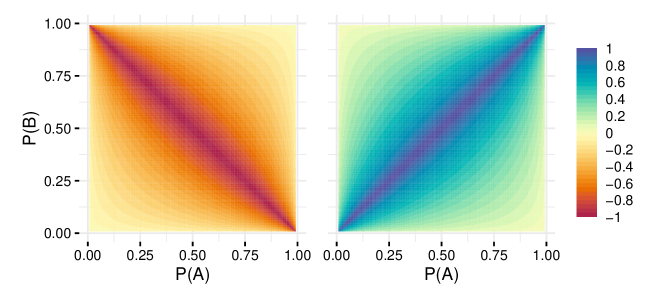

As the normalization only depends on the marginal event probabilities, the phi coefficient inherits properties (B), (D) and (E) from the covariance and also fulfills (A) by applying the Cauchy-Schwarz inequality. However, by the Fréchet-Hoeffding bounds for the covariance from (2), it is bounded by what we call Fréchet-Hoeffding bounds for the phi coefficient, that is, its values under perfect negative and positive dependence:

| (3) |

As these bounds are in general not equal to and and depend on the marginal event probabilities and , the phi coefficient is not attainable.

Proposition 4.4.

fulfills properties (A), (B), (D) and (E) from Definition 3.2, but not (C).

Figure 1 visualizes the bounds from as a function of the marginal event probabilities. It shows that the values of the phi coefficient under perfect positive and negative dependence can be very far away from and . This seriously compromises the interpretability of this measure as it cannot reliably indicate strength of dependence, which should be indicated by being close to 1. For most combinations of and such values cannot be reached and instead very small absolute values arise under strong dependence. The phi coefficient is only attainable for the special case of (see Proposition 4.5 below). This shortcoming may be surprising given that the phi coefficient is just a special case of the popular and widely-used Pearson correlation. However, Pearson correlation has serious attainability problems itself and should be used with care (Embrechts et al.,, 2002). In the binary case, they become particularly serious (as two binary random variables are particularly far away from fulfilling the conditions for attainability of Pearson correlation formulated in Fissler and Pohle, (2023, Lemma 3.1), that is, from being symmetric and of the same type).

Thus, the phi coefficient is not a particularly useful measure of dependence for events or binary random variables. Instead, it may be useful for a different task, which becomes clear by analyzing under which conditions takes the values and 1.

Proposition 4.5.

The following statements are equivalent:

-

(i)

().

-

(ii)

() almost surely.

-

(iii)

and are perfectly positively (negatively) dependent and ().

-

(iv)

and ( and ).

-

(v)

() almost surely.

-

(vi)

and are increasing (decreasing) functions of each other almost surely.

-

(vii)

and are increasing (decreasing) linear functions of each other almost surely.

Considering (ii), the phi coefficient measures how close two sets and are to being equal (where would be regarded as being maximally far away from being equal), which is however different from our characterization of perfect dependence in Definition 2.3. By (iii), this amounts to jointly measuring closeness to perfect dependence and to a restriction on the marginal distributions, in the case of positive (and in the case of negative) dependence. We however want to measure dependence of arbitrary events and hence take the marginal event probabilities and as given, which makes the restriction (or ) unacceptable. The restrictions and in (iii) jointly amount to and can hence be interpreted as an intuitive reason for the non-attainability of the phi coefficient.

Even though we have established that the phi coefficient should not be used for measuring dependence, Proposition 4.5 shows that it is useful for a different task, namely measuring closeness to equality of events. For example when evaluating binary classifiers, where is the event of interest and indicates that was predicted to happen, a perfect classifier fulfills . This task is distinct from measuring dependence, where we take the marginal event probabilities as given, since for the classification task is not fixed, but needs to adopt to . In the literature this crucial distinction between measures of dependence and measures of event equality has not been made. While the phi coefficient is indeed widely-used for the evaluation of binary classifiers (Matthews,, 1975), it is as widely-used as a measure of dependence, which should be avoided. At the same time the odds ratio, which is a proper dependence measure (as discussed in the next section) and not a measure of set equality, has been put forward as a tool for the evaluation of binary classifiers (Stephenson,, 2000).

What has been recognized in the literature (e.g. Bishop et al., (2007)), is that the phi coefficient equals 1() under condition (iv), that is, if there are two zeros on the primary (secondary) diagonal of the contingency table, while other measures like Yule’s (in fact, all proper measures by (C) from Definition 3.2 and (iii) in Proposition 2.4) require only one zero on the primary (secondary) diagonal to equal 1 (1). However, the underlying reasons for this as made clear by Propositions 2.4 and 4.5 have not been uncovered.

The items (vi) and (vii) in Proposition 4.5 are interesting because they establish the connection to conditions well-known from the theory of Pearson correlation and rank correlations, of which is a special case. (vii) reproduces the well-known condition that Pearson correlation is 1 (1) if and only if the two variables are linear functions of each other, (vi) the well-known condition that Spearman’s and Kendall’s are 1 (1) if and only if one variable is a monotonic function of the other (Embrechts et al.,, 2002). Thus, equality between the events (or one event and the complement of the other) corresponds to positive (negative) monotonic and linear (the two coincide in the binary case) dependence. Note that neither linear nor monotonic functional relations are useful concepts of perfect dependence in the binary case (or more generally in the discrete case) as a functional relation is only possible under the restriction from (iii) on the marginal distributions, which is in general not fulfilled.

4.3 Contingency Coefficients

Contingency coefficients aim at measuring dependence inherent in a general contingency table. For two categorical random variables and , where takes values and takes values , Pearson’s Mean Square Contingency () coefficient (Pearson,, 1904) is just the population analogue of the test statistic of Pearson’s chi-squared test of independence:

| (4) |

Contingency coefficients arise by normalizing . As they are designed for nominal random variables, direction of dependence is not a sensible concept and they map to , only trying to indicate strength of dependence. However, as discussed above, binary random variables can always be regarded as ordinal. Thus, in the case, measures of dependence that indicate strength and direction of dependence can be used and the question arises why one should throw away the information on direction of dependence. Since they are widely-used in the binary case, we nevertheless discuss them. In Appendix A.1, we consider Cramérs V, Tschuprow’s T, and Pearson’s contingency coefficient and show that they are closely related to the phi coefficient in the binary setting (for example the first two just equal ) and thus inherit its deficiencies, in particular not being proper dependence measures.

5 Proper Dependence Measures

5.1 Cole’s Coefficient

After its introduction by Cole, (1949) the formula for Coles’s coefficient had to be corrected twice by Ratliff, (1982) and Warrens, (2008). An equivalent reformulation of it arises naturally from our discussion of dependence concepts: From the Fréchet-Hoeffding bounds of from Proposition 2.4 arise the bounds on from (2), which are attained only under perfect positive and negative dependence of and and whose absolute values are in general different from each other. Thus, it is natural to distinguish the cases of positive and negative dependence and normalize covariance with (the absolute values of) those bounds.

Definition 5.1 (Cole’s Coefficient).

Cole’s is defined as

The idea of normalizing with the cases of perfect positive and negative dependence has later been used for rank correlations (Vandenhende and Lambert, (2003), Genest and Nešlehová, (2007)) and for Pearson correlation and generalizations of it by Fissler and Pohle, (2023). Indeed, Cole’s is a special case of attainable modifications of Kendall’s tau, Spearman’s rho and Pearson correlation as well as of threshold correlation (see Genest and Nešlehová, (2007) for the former two and Fissler and Pohle, (2023) for the latter two).

Cole’s coefficient is normalized and attainable by construction and essentially inherits properties (B), (D) and (E) from the covariance such that it is a proper dependence measure.

Proposition 5.2.

is proper.

5.2 Yule’s Q, the Odds Ratio and Relatives

Besides the phi coefficient and Cole’s coefficient, Yule’s can be viewed as yet another approach to normalizing covariance. It just replaces the minus in the alternative representation of from (1) with a plus and normalizes by the resulting term.

Definition 5.3 (Yule’s ).

Yule’s is defined as

| (5) |

Via (1), Yule’s can be rewritten as

| (6) |

Considering (6), it is clear that lies in and fulfills the symmetry properties (E). Its attainability directly follows by invoking part (iii) of Proposition 2.4. The independence property (B) is inherited from the covariance (since the normalization is nonzero). Monotonicity follows from the strictly monotonic relation between Yule’s and the odds ratio (Lemma 5.6) and the monotoniticy of the odds ratio (part (D) of Proposition A.3).

Proposition 5.4.

is proper.

The normalization of Yule’s is rather ad hoc, in particular compared to the natural normalization of Cole’s . The normalization does not use the Fréchet-Hoeffding bounds for covariance, but continuously changes with the joint probabilities. Thus, the measure is not as nicely interpretable in terms of covariance relative to its values under perfect positive or negative dependence. On the other hand, it avoids the need to use a case distinction in the normalization as Cole’s does, which makes asymptotic theory and inference much easier (see Section 6). One way to interpret Yule’s is by realizing that it is a special case of Goodman-Kruskal’s (Goodman and Kruskal,, 1954) and can therefore be interpreted in the same vein (Bishop et al.,, 2007).

A very natural way to motivate and interpret Yule’s is via its relation to the odds ratio. The odds ratio is different from the other measures of dependence discussed so far in that it does not build on the covariance and does not fall into the class of classical dependence measures mapping to or as it maps to the extended nonnegative real numbers. Even though it thus falls a bit out of the framework of this paper, we nevertheless discuss it here shortly due to its popularity and to it being nicely interpretable and having nice properties.

Definition 5.5 (Odds Ratio).

The odds ratio is defined as

if and if .

We discuss further details on the motivation behind the odds ratio, its interpretation and popularity in Appendix A.2. Note that the odds ratio is closely related to the covariance in that it just replaces the subtraction in (1) by a division. Fittingly, it is also sometimes called the cross-product ratio, referring to the underlying contingency table. The odds ratio and Yule’s are closely related: They are strictly monotonic functions of each other.

Lemma 5.6.

It holds that

Thus, Yule’s can be viewed as a transformation of the odds ratio to a new scale. Hence, it is unsurprising that the odds ratio is proper in an appropriate sense as well. Indeed, we show that it fulfills a modified set of axioms adopted to its codomain and its multiplicative rather than additive nature in Proposition A.3 in the appendix.

Furthermore, Yule’s has been generalized in the sense of

with special cases , (Yule,, 1912) and (Digby,, 1983). The generalized Yule’s also has a one-to-one relation to the odds ratio and can be shown to be proper along the same lines as Yule’s . Further, is weakly increasing in and strictly increasing if , which can be seen by computing the derivative with respect to .

We discuss a further property of , and the odds ratio, which has been interpreted as a form of invariance to the marginal distributions, in Appendix A.3.

Another interesting measure is tetrachoric correlation. It is constructed via the assumption that the contingency table arises by dichotomization of an underlying bivariate normal distribution, of which it is the Pearson correlation coefficient. Even though its construction seems a bit artificial, it is quite popular compared to the other proper measures and we discuss it in Appendix A.4 and show that it is proper as well. It is related to in that versions of the latter have been used to approximate the former, which has no closed-form solution (Digby,, 1983).

5.3 Comparison of , and

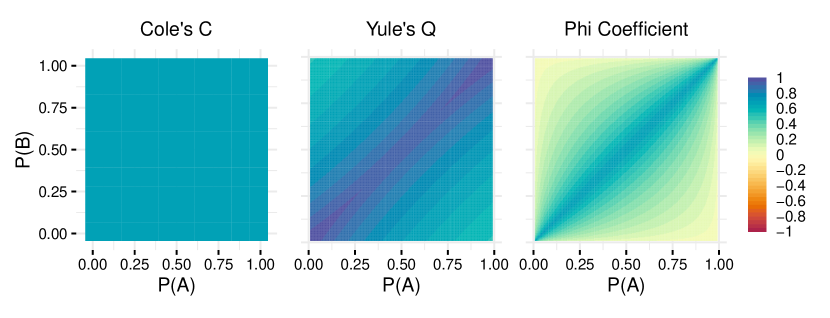

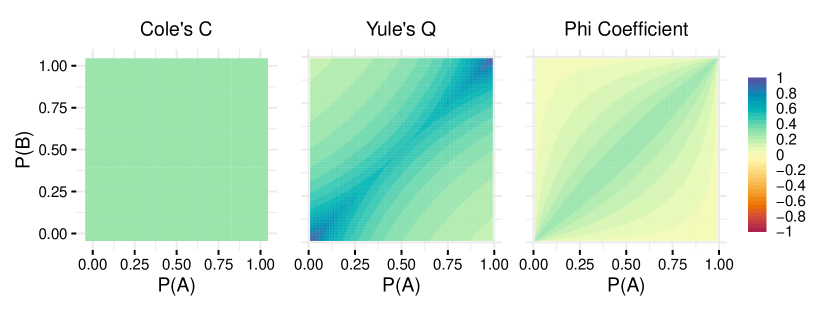

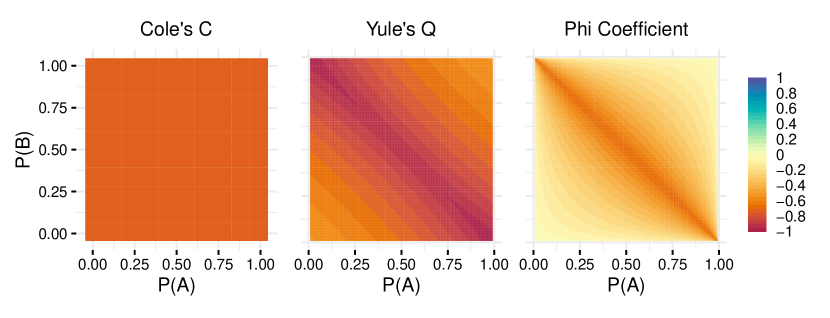

It is possible to directly compare the discussed dependence measures in terms of the values they take since they only depend on the marginal event probabilities and and the joint probability or the value of one of the competing dependence measures, respectively. In Figure 2 we plot Yule’s and the phi coefficient for a fixed value of Cole’s of 0.7 over all combinations of event probabilities and .

Firstly, the distinction between the two proper measures and the phi coefficient is clearly visible. The serious attainability problems of the phi coefficient (see also Figure 1) can lead to it having very small values despite the quite strong positive dependence. The attainability problems become more serious the further away we move from the diagonal, that is from the condition (also see the discussion around Proposition 4.5).

Secondly, even though the two proper measures are much closer to each other, they of course also take different values in general. In particular, for equal and at the same time very small or large event propabilities, Yule’s takes values close to 1 instead of close to 0.7.

For different values of Cole’s coefficient qualitatively the same picture arises. We show the cases where it takes the values 0.3 and in Figures 11 and 12 in the Appendix. The latter figure in comparison with Figure 2 also illustrates the symmetry relation formulated in the second part of property (E), which all the coefficients possess.

6 Statistical Inference

6.1 Estimators and Asymptotic Distributions

We consider a sequence of binary random variables that are distributed as for all and use the shorthand notations , , and . For a given sample of size , we introduce the natural estimators , and as well as , and . Assume that holds such that we can define the following plug-in estimators for , , and based on Definitions 4.3, 5.1 and 5.3, respectively,

| (7) | ||||

| (8) | ||||

| (9) |

that are well-defined given the condition , which holds asymptotically with probability one (see (15) for details) by the following assumption.

Assumption 6.1.

Let and .

Assumption 6.1 is imposed to rule out boundary effects: Violating the conditions would imply that the corresponding estimators are almost surely zero or one. The condition would imply perfect negative dependence and perfect positive dependence such that our estimators for and (and in the attainable case) would be either plus or minus 1 almost surely, and hence their asymptotic distributions would be degenerate.

The basis for the asymptotics for the three dependence coefficients in (7)–(9) is a central limit theorem (CLT) for with , , in Lemma E.2 that can be derived under either one of the following two conditions:

Assumption 6.2.

Let be a sequence of independent and identically distributed (iid) random variables and let .

Assumption 6.3.

Let be a stationary ergodic adapted mixingale of size and let the “long-run” covariance matrix be strictly positive definite.

In the iid case of Assumption 6.2, is positive definite through Assumption 6.1 that assures that the entries in are not perfectly dependent; see the proof of Lemma E.2 for details. Instead, an equivalent condition has to be imposed on the long run variance in the time series case of Assumption 6.3. See White, (2001, Section 5.3) for details on mixingale processes. While time series asymptotics usually come at the cost of more restrictive moment conditions, these are of no concern here due to the boundedness of the binary random variables. We further discuss the time series case in Appendix C.

We start by giving the asymptotic distribution of , which is Gaussian.

As is a continuously differentiable transformation of and (with Jacobian matrix at ), the proof of Proposition 6.4 is a straightforward application of the delta method, but is complicated by the need to show non-degeneracies in the Jacobian .

In contrast, the asymptotic distribution of (and its derivation) is much more involved.

Proposition 6.5.

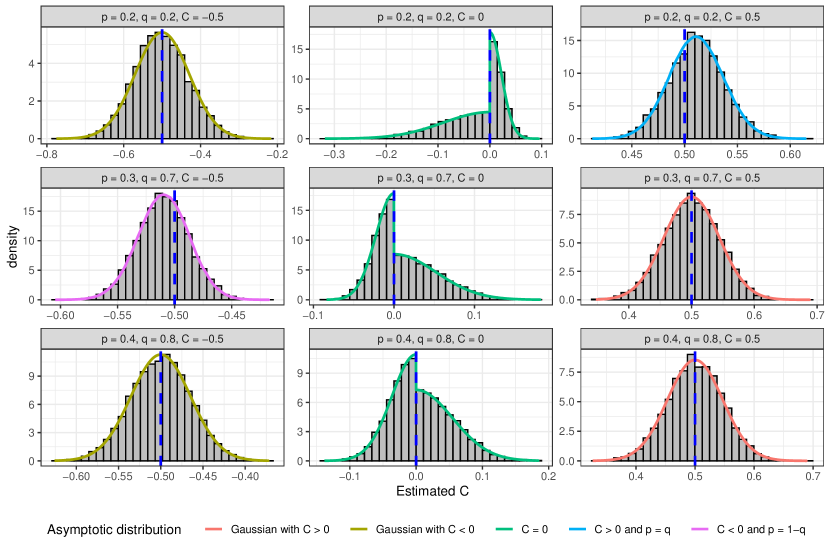

Proposition 6.5 shows that the asymptotic behavior of is highly non-standard and exhibits discontinuities that depend on the unknown population quantities , and . The case distinction in whether (or equivalently ) is zero, positive or negative arises due to the differing normalizations in the definition of : For the case of , the asymptotic distribution is given by two half-normals with different variances. For and , we obtain a standard asymptotic normal distribution. We however get non-standard asymptotic distributions for the cases and that arise due to the minimum and maximum operators in the normalizations and .

Figure 3 illustrates the five different cases of the asymptotic distribution through simulations. Besides the standard asymptotic normality, we can clearly see the two half-normal distributions for , where the difference of the variances depends on the specific setting governed by and . The complicated cases and arise in the upper right and middle left subplots. There we also find a bias in the estimates, which is reflected in the asymptotic distributions through the terms and , respectively. For , this bias can be explained by the normalization , which is negatively biased through , which tends to underestimate its population counterpart in the case . The argument is similar for the case .

For completeness, we also report the asymptotic distribution of , whose proof is a straightforward application of the delta method.

6.2 Feasible Inference, Tests and Confidence Intervals

Feasible inference requires consistent estimates of the asymptotic distributions. Denote by , , , , , , , , , and the estimated counterparts of the vectors and matrices defined in Propositions 6.4, 6.5 and 6.6 that arise by simply replacing the true probabilities , and by their estimators , and . In the iid case, consistent estimation of through a plug-in estimator using and in (20) in Appendix E is straight-forward. In the time series case, we employ the well-known “HAC”-estimator of Newey and West, (1987) whose consistency is shown in Proposition C.1. The continuous mapping theorem implies that the empirical “variance” matrices in Propositions 6.4, 6.5 and 6.6 are consistent estimators of their population counterparts, which ensures that the asymptotic distributions are unchanged when the population matrices are replaced with these estimators.

Feasible inference in the form of testing and confidence intervals for and can be carried out by standard methods based on the above asymptotic normality statements. In contrast, the case distinctions in the asymptotic distribution of in Proposition 6.5 complicate the construction of tests and confidence intervals as the population quantities , and are unknown.

For confidence intervals, we leverage the idea of building them through inverted hypothesis tests by running a sequence of tests (described below) with null hypotheses for all (or in practice, a fine sequence of) values . The confidence interval at level then consists of all values , for which the hypothesis is not rejected at level .

Tests for (or for or }) are straightforward using the respective limiting distribution for in Proposition 6.5.222With the same reasons as given after “second” in the following paragraph, we write and include a two-sided test for and obtain the final -value with a Bonferroni correction. When testing for for any , we are however uncertain whether we are in the case or such that a valid testing approach must accommodate both possibilities. Hence, we write with and , where and can be tested using the asymptotically valid -values and that arise from the respective asymptotic distributions in Proposition 6.5. Thus, testing for through the union of these two hypotheses becomes an intersection-union (IU) test, for which is an asymptotically valid -value (Berger,, 1982).

This testing procedure is however overly conservative for two reasons: First, given the predominant case , the -value is often non-informative and dominates the IU-construction . We resolve this by writing with , which we test for by the joint CLT for in Lemma E.2 in the Appendix with -value . Second, the estimated asymptotic variances often differ substantially for positive and negative values of (see e.g., the middle column of Figure 3), resulting in cases where for a large positive value of , we reject many positive values , but cannot reject values due to a higher estimated variance in the negative case. We solve this by writing with , which is a necessary condition for . A test for with -value is easily constructed based on the CLT for provided in Lemma E.3 in the Appendix. Both these refinements are union-intersection (UI) tests, for which Bonferroni corrections are necessary. Hence, our final -value is given by corresponding to the hypothesis .

For any , we use an equivalent construction with and , and .

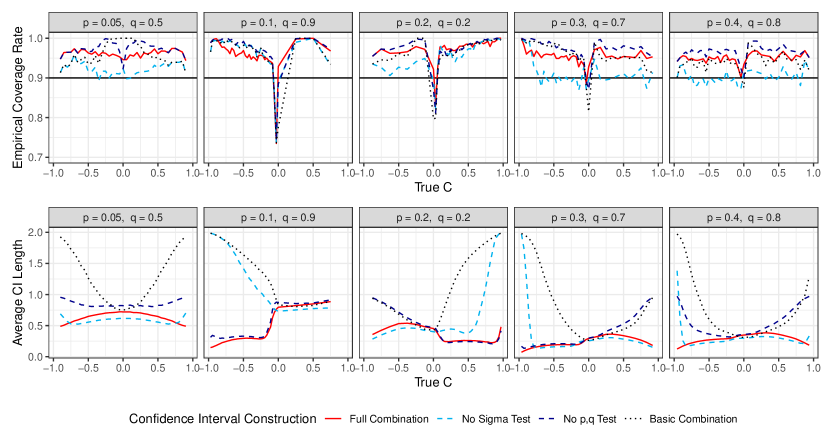

In Appendix D, we illustrate the good finite sample properties for the standard confidence intervals for and and for the more refined construction for . For the latter, we also demonstrate the superiority of our approach based on the two auxiliary UI-tests for and in terms of length of the resulting confidence intervals.

6.3 Fisher Transformations

As the sampling distributions of the estimated measures are bounded, they are in finite samples often heavily influenced by the theoretical upper and lower bounds when the true measures are close (relative to the sample size) to these bounds. This leads to skewed distributions, for which asymptotic normality (and the more complicated distributions for ) are bad approximations and hence deteriorates the finite sample performance of the associated tests and confidence intervals. To combat this problem, we adopt the classical Fisher transformation (Fisher,, 1915), originally proposed for Pearson correlation,

| (10) |

for a generic (population or estimated) dependence measure . The in (10) bijectively maps the interval to and hence provides a better approximation when the dependence measure is close to the boundary.

7 Case Study on Drug Use

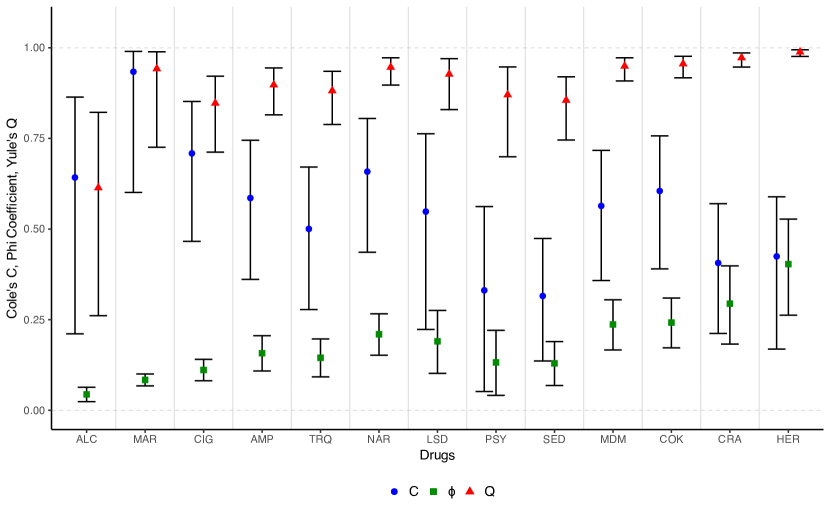

We use data from the 2018 wave of the Monitoring the Future (MTF) study on drug use among the contemporary American youth (Miech et al.,, 2019, DS1 Core Data).333We use data from 2018 because subsequent waves have sizeably fewer observations. We are interested in interdependence between consumption of different drugs and consider the events of ever having consumed certain drugs. The sample size is , but for certain drugs there is a large number of non-responses.444The dataset is an aggregation of six different questionnaires students get randomly assigned to. Some drugs do not appear in all six questionnaires. The different drugs, the abbreviations we use for them in subsequent plots, their marginal relative consumption frequencies and the respective (univariate) sample sizes are listed in Table 4.

| drug | abbreviation | relative frequency | sample size |

|---|---|---|---|

| alcohol | ALC | ||

| marijuana | MAR | ||

| cigarettes | CIG | ||

| amphetamines | AMP | ||

| tranquilizers | TRQ | ||

| narcotics | NAR | ||

| LSD | LSD | ||

| psychedelics∗ | PSY | ||

| sedatives | SED | ||

| MDMA | MDM | ||

| cocaine | COK | ||

| crack | CRA | ||

| methamphetamines | MET | ||

| heroin | HER |

-

*

without LSD

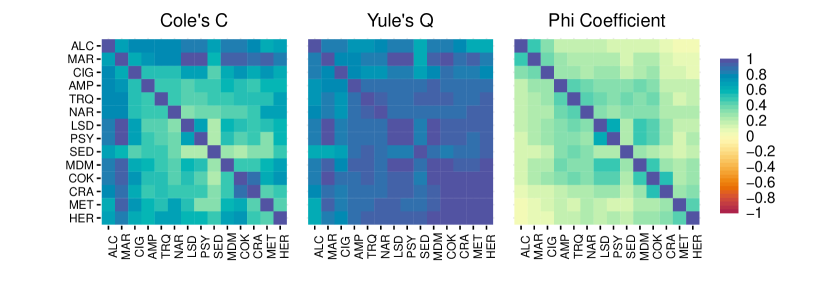

Figure 4 shows contour plots of estimated correlation matrices between all pairs of those events for Cole’s , Yule’s and the phi coefficient. All three measures indicate a positive relationship between the consumption of all the drugs considered. However, most values of the phi coefficient are very close to 0, which would usually be interpreted as evidence for very weak dependence, while the proper dependence measures tend to have very high values, indicating strong dependence. Thus, the dependence is structurally underrated by the phi coefficient due to its severe attainability issues. If the phi coefficient or one of the equally popular contingency coefficients was used in such a context, it could thus lead to possibly severe misperceptions with respect to the nature of polydrug use.

What is more, the phi coefficient might give rise to very different policy advice with respect to prevention of hard drug usage among adolescents. While it especially accentuates the dependence between drugs of similar “hardness” such as alcohol and marijuana or meth and heroin, the proper correlations also yield sizeable results for dependence between drugs of very different “hardness” such as alcohol and meth. The reason for this behaviour are the very different marginal distributions of those drug use variables, which lead to a much narrower interval of values which can attain (see again Figures 1 and 2). However, thus concluding that the gateway drug effect (alternatively, escalation hypothesis, progression hypothesis, or stepping-stone theory), describing the process of starting with soft drugs like alcohol and subsequently progressing to harder drugs, is negligible, would result in misleading policy advice. Instead, this effect has been extensively researched since Kandel, (1975) and is nowadays widely accepted in the literature (Kandel and Kandel,, 2015).555The question to which degree the observed sequential pattern of drug use is causal is still up for debate. Though, the existence of a sizeable association is consensus, but not mirrored by the phi coefficient.

While the two proper correlation matrices all indicate a very strong dependence overall, there are nevertheless clearly visible differences between them. Those differences can be very well understood by looking again at Figure 2. For example, Yule’s takes considerably higher values than Cole’s for all drugs except for the three softest. This is due to the marginal event probabilities being rather small and similar, corresponding to a situation as in the lower left corner of the corresponding panels of Figure 2. Thus, this data example also illustrates that even though the proper dependence measures are usually close to each other (see again Figure 2), there may be substantial differences between them.

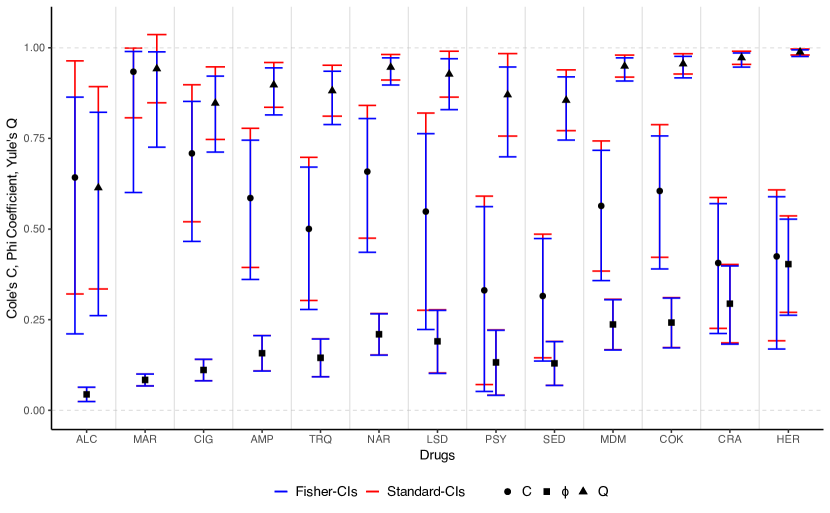

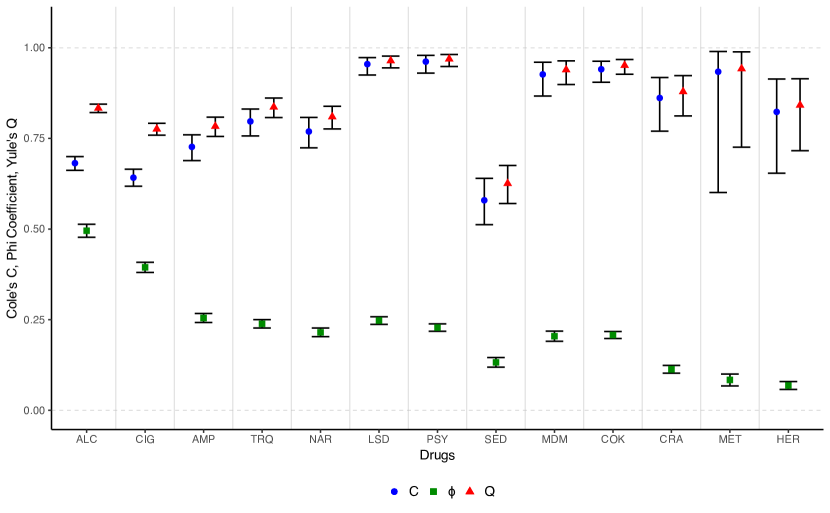

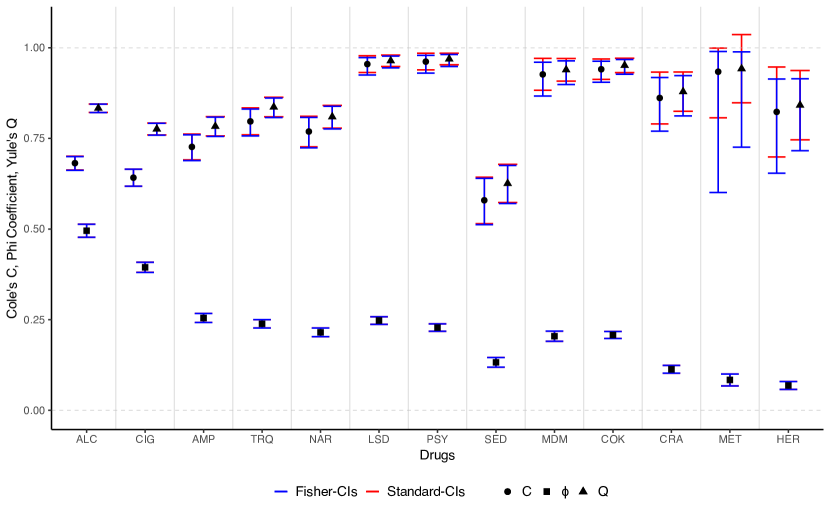

To get an idea of sampling uncertainty, we first focus on the dependence between marijuana and all other drugs (the second row or column of the correlation matrices above) and plot , and and 90% confidence intervals based on the Fisher transformation in Figure 5. Even though the consumption events for the harder drugs are rather rare events (that is, the marginal and even more so the joint consumption probabilities can be quite small), the confidence intervals are quite narrow due to the large sample size. As expected, the intervals for are slightly wider than the intervals for due to their more complicated and possibly conservative construction method. Notice that the narrow confidence intervals for are not an advantage of this measure but are caused by the suboptimal normalization of that forces to be much smaller in absolute value due to its non-attainability.

In general, the intervals tend to get wider the smaller the consumption probability for the drug gets as this increases the asymptotic variance. Another important factor is the effective sample size for a pair of drugs, which amounts to the joint number of respondents for those drugs as listed in Table 7 in the appendix. It is lowest for methamphetamines, which explains the wider intervals in this case. In Figure 14 in the appendix we also show the analogous graph for the combination of methamphetamines with all other drugs, where the sampling uncertainty is higher due to the consumption of this drug being a rare event and the smaller sample size when pairing this drug with others (see Table 8).

8 Conclusion

This paper deals with dependence measures for events or binary random variables. We introduce dependence concepts for events and the notion of a proper dependence measure. We then discuss theoretical properties of, statistical inference for, and relations between different measures. Important recommendations for statistical practice arise: The most widely-used measures, the phi coefficient and the closely related contingency coefficients, should be avoided for this purpose. They lack the crucial property of attainability and can hence severely understate strength of dependence, leading to possibly misleading conclusions. Instead, proper dependence measures should be used. The largely unknown Cole coefficient is a very natural and nicely interpretable representative of this class. Even though its statistical inference is challenging due to the case distinction in its definition, we construct tests and confidence intervals based on the asymptotic distribution that we derive. Yule’s is an attractive alternative, avoiding the case distinction in the normalization, and making possible the use of classical inferential procedures. We further discuss a generalized Yule’s , the also closely related and popular odds ratio and tetrachoric correlation and establish their propriety.

Generalizing the notion of a proper dependence measure to arbitrary random variables is an important task for future research. While in the case of continuous random variables several sets of desirable properties have been put forward since Rényi, (1959) as discussed in the introduction, firstly the extension to the discrete case and secondly the agreement on a set of axioms need to be tackled. We see our work in the binary case as a foundation for this endeavor. A subsequent and equally important task is the search for or the development of measures fulfilling those properties. While in the continuous case rank correlations such as Kendall’s and Spearman’s fulfill many desirable properties, they are not attainable in the discrete case as well.

References

- Balakrishnan and Lai, (2009) Balakrishnan, N. and Lai, C.-D. (2009). Continuous Bivariate Distributions. Springer, New York, 2nd edition.

- Berger, (1982) Berger, R. L. (1982). Multiparameter hypothesis testing and acceptance sampling. Technometrics, 24(4):295–300.

- Bishop et al., (2007) Bishop, Y. M., Fienberg, S. E., and Holland, P. W. (2007). Discrete Multivariate Analysis: Theory and Practice. Springer, New York.

- Boas, (1909) Boas, F. (1909). Determination of the coefficient of correlation. Science, 29(751):823–824.

- Bonett and Price, (2007) Bonett, D. G. and Price, R. M. (2007). Statistical inference for generalized Yule coefficients in 22 contingency tables. Sociological Methods & Research, 35(3):429–446.

- Cole, (1949) Cole, L. C. (1949). The measurement of interspecific association. Ecology, 30(4):411–424.

- Cornfield, (1951) Cornfield, J. (1951). A method of estimating comparative rates from clinical data. Applications to cancer of the lung, breast, and cervix. JNCI: Journal of the National Cancer Institute, 11(6):1269–1275.

- Cramér, (1945) Cramér, H. (1945). Mathematical Methods of Statistics. Almqvist & Wiksells, Uppsala, Sweden.

- Digby, (1983) Digby, P. G. N. (1983). Approximating the tetrachoric correlation coefficient. Biometrics, 39(3):753–757.

- Edwards, (1963) Edwards, A. W. (1963). The measure of association in a 22 table. Journal of the Royal Statistical Society Series A: Statistics in Society, 126(1):109–114.

- Ekström, (2011) Ekström, J. (2011). The phi-coefficient, the tetrachoric correlation coefficient, and the Pearson-Yule debate. UCLA: Department of Statistics.

- Embrechts et al., (2002) Embrechts, P., McNeil, A., and Straumann, D. (2002). Correlation and dependence in risk management: properties and pitfalls. In Dempster, M., editor, Risk Management: Value at Risk and Beyond, pages 176–223. Cambridge University Press, Cambridge, MA.

- Falk and Bar-Hillel, (1983) Falk, R. and Bar-Hillel, M. (1983). Probabilistic dependence between events. The Two-Year College Mathematics Journal, 14(3):240–247.

- Fisher, (1915) Fisher, R. A. (1915). Frequency distribution of the values of the correlation coefficient in samples from an indefinitely large population. Biometrika, 10(4):507–521.

- Fissler and Pohle, (2023) Fissler, T. and Pohle, M.-O. (2023). Generalised covariances and correlations. arXiv Preprint: 2307.03594.

- Fréchet, (1951) Fréchet, M. (1951). Sur les tableaux de corrélation dont les marges sont données. Annales de l’Université Lyon A (3), 14:53–77.

- Genest and Nešlehová, (2007) Genest, C. and Nešlehová, J. (2007). A primer on copulas for count data. ASTIN Bulletin, 37(2):475–515.

- Goodman and Kruskal, (1954) Goodman, L. A. and Kruskal, W. H. (1954). Measures of association for cross classifications. Journal of the American Statistical Association, 49(268):732–764.

- Greenhouse, (1982) Greenhouse, S. W. (1982). Jerome Cornfield’s contributions to epidemiology. Biometrics, 38:33–45.

- Hoeffding, (1940) Hoeffding, W. (1940). Masstabinvariante Korrelationstheorie. Schriften des Mathematischen Instituts und Instituts fur Angewandte Mathematik der Universitaet Berlin, 5:181–233.

- Kandel, (1975) Kandel, D. (1975). Stages in adolescent involvement in drug use. Science, 190(4217):912–914.

- Kandel and Kandel, (2015) Kandel, D. and Kandel, E. (2015). The gateway hypothesis of substance abuse: developmental, biological and societal perspectives. Acta Paediatrica, 104(2):130–137.

- Lehmann, (1966) Lehmann, E. L. (1966). Some concepts of dependence. Annals of Mathematical Statistics, 37(5):1137–1153.

- Liebetrau, (1983) Liebetrau, A. M. (1983). Measures of Association. Sage, Newbury Park, CA.

- Mari and Kotz, (2001) Mari, D. D. and Kotz, S. (2001). Correlation and Dependence. Imperial College Press, London, UK.

- Matthews, (1975) Matthews, B. W. (1975). Comparison of the predicted and observed secondary structure of T4 phage lysozyme. Biochimica et Biophysica Acta (BBA)-Protein Structure, 405(2):442–451.

- McLeish, (1974) McLeish, D. L. (1974). Dependent central limit theorems and invariance principles. Annals of Probability, 2(4):620–628.

- Miech et al., (2019) Miech, R. A., Johnston, L. D., Bachman, J. G., O’Malley, P. M., and Schulenberg, J. E. (2019). Monitoring the future: A continuing study of American youth (12th-grade survey), 2018.

- Mosteller, (1968) Mosteller, F. (1968). Association and estimation in contingency tables. Journal of the American Statistical Association, 63(321):1–28.

- Nešlehová, (2007) Nešlehová, J. (2007). On rank correlation measures for non-continuous random variables. Journal of Multivariate Analysis, 98(3):544–567.

- Newey and West, (1987) Newey, W. and West, K. (1987). A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica, 55(3):703–08.

- Pearson, (1900) Pearson, K. (1900). Mathematical contributions to the theory of evolution. VII. On the correlation of characters not quantitatively measurable. Philosophical Transactions of the Royal Society of London. Series A, Containing Papers of a Mathematical or Physical Character, 195:1–405.

- Pearson, (1904) Pearson, K. (1904). Mathematical contributions to the theory of evolution. XIII. On the theory of contingency and its relation to association and normal correlation. Drapers’ Company Research Memoirs. Biometric Series 1. Dulau and Co., London, UK.

- Plackett, (1965) Plackett, R. L. (1965). A class of bivariate distributions. Journal of the American Statistical Association, 60(310):516–522.

- Ratliff, (1982) Ratliff, R. D. (1982). A correction of Coles’s C7 and Hurlbert’s C8 coefficients of interspecific association. Ecology, 63(5):1605–1606.

- Rényi, (1959) Rényi, A. (1959). On measures of dependence. Acta Mathematica Academiae Scientiarum Hungarica, 10(3-4):441–451.

- Scarsini, (1984) Scarsini, M. (1984). On measures of concordance. Stochastica, 8(3):201–218.

- Schweizer and Wolff, (1981) Schweizer, B. and Wolff, E. F. (1981). On nonparametric measures of dependence for random variables. Annals of Statistics, 9(4):879–885.

- Stephenson, (2000) Stephenson, D. B. (2000). Use of the “odds ratio” for diagnosing forecast skill. Weather and Forecasting, 15(2):221–232.

- Tchen, (1980) Tchen, A. H. (1980). Inequalities for distributions with given marginals. Annals of Probability, 8(4):814–827.

- Tjøstheim et al., (2022) Tjøstheim, D., Otneim, H., and Støve, B. (2022). Statistical dependence: Beyond Pearson’s rho. Statistical Science, 37(1):90–109.

- Tschuprow, (1925) Tschuprow, A. A. (1925). Grundbegriffe und Grundprobleme der Korrelationstheorie. Teubner, Berlin, Germany.

- van der Vaart, (1998) van der Vaart, A. W. (1998). Asymptotic Statistics. Cambridge University Press.

- Vandenhende and Lambert, (2003) Vandenhende, F. and Lambert, P. (2003). Improved rank-based dependence measures for categorical data. Statistics & Probability Letters, 63(2):157–163.

- Warrens, (2008) Warrens, M. J. (2008). On association coefficients for tables and properties that do not depend on the marginal distributions. Psychometrika, 73(4):777–789.

- Warrens, (2019) Warrens, M. J. (2019). Similarity measures for tables. Journal of Intelligent & Fuzzy Systems, 36(4):3005–3018.

- White, (2001) White, H. (2001). Asymptotic Theory for Econometricians. Academic Press, San Diego.

- Yanagimoto and Okamoto, (1969) Yanagimoto, T. and Okamoto, M. (1969). Partial orderings of permutations and monotonicity of a rank correlation statistic. Annals of the Institute of Statistical Mathematics, 21(1):489–506.

- Yule, (1900) Yule, G. U. (1900). On the association of attributes in statistics: With illustrations from the material of the childhood society, &c. Philosophical Transactions of the Royal Society of London. Series A, Containing Papers of a Mathematical or Physical Character, 194:257–319.

- Yule, (1912) Yule, G. U. (1912). On the methods of measuring association between two attributes. Journal of the Royal Statistical Society, 75(6):579–652.

Appendix A Details on Further Dependence Measures

A.1 Contingency Coefficients

Several contingency coefficients have been defined based on Pearson’s Mean Square Contingency coefficient from (4) (see Liebetrau, (1983) for an overview), including Cramérs , Tschuprow’s , and Pearson’s contingency coefficient

In the binary case, becomes

| (11) | ||||

Further, in the binary case the mean square contingency coefficient just equals the squared phi coefficient. The result seems to be known in the literature, but a proof is hard to find, so we provide one.

Lemma A.1.

It holds that .

We write and analogously and . Here, Cramérs and Tschuprow’s coincide, . Thus, the contingency coefficients are just functions of the phi coefficient.

Corollary A.2.

It holds that

and

Thus, in the binary case, Cramérs and Tschuprow’s just report the same information on strength of dependence as the phi coefficient, but remove the sign, that is, the information on direction of dependence. They of course inherit the attainability problems of and are thus no proper dependence measures (not even in terms of a modified set of axioms adopted to measures of strength of dependence mapping to ). Pearson’s contingency coefficient exhibits even more shortcomings, for example its maximum value is instead of 1.

A.2 Odds Ratio

The origin of the odds ratio seems to be unknown, but Cornfield, (1951) has played an important role in popularizing the measure in epidemiology (Greenhouse,, 1982). It is very popular in medicine. Indeed, it surmounts all the classical dependence measures discussed here in terms of Google and Google Scholar citations (12th March 2024, compare Table 2), presumably due to the sheer size of the medical literature. The quotient between a probability (here: or ) and its counterprobability is called the odds. Dividing the odds for conditional on and the odds for conditional on by each other yields the odds ratio,

| (12) |

Thus, it measures dependence between and by considering how the odds of increase given . At first, it seems that the odds ratio does not fit into the framework of this paper, where we are interested in mutual dependence between events, that is, and should play an interchangeable role, which is guaranteed by the symmetry of a measure. Instead, the odds ratio considers conditional on . However, the odds ratio is indeed symmetric as it can be rewritten as the second and third equalities in (12). In our Definition 5.5, we also take into account that the terms from (12) would be undefined in case of perfect positive dependence.

The odds ratio can be regarded as proper as it fulfills a modified set of axioms, that is, suitable adaptations of the properties from 3.2 to its scale and multiplicative nature.

Proposition A.3.

-

(A)

Normalization: .

-

(B)

Independence: if and only if and are independent.

-

(C)

Attainability: if and only if and are perfectly positively (negatively) dependent.

-

(D)

Monotonicity: Let and . if and only if and are stronger positively (negatively) dependent than and .

-

(E)

Symmetry: and .

A.3 Invariance to the Marginals of , and the Odds Ratio

, and have an interesting property, which is discussed already in Yule, (1912) and later in Edwards, (1963), Plackett, (1965) and Mosteller, (1968) for empirical contingency tables containing absolute frequencies: When the columns and rows of a contingency table (see Table 3 again) are multiplied by constants and and then the numbers are normalized by an appropriate normalising constant so that the joint probabilities sum up to 1 again, those measures do not change. Considering the odds ratio, it is easy to see that those constants cancel out:

By Lemma 5.6, this directly carries over to Yule’s . This property is seen as a desirable property by the papers cited above and often described as invariance of those measures to the marginal event probabilities because the measures do not change when the marginal event probabilities change and the respective joint and conditional probabilities change accordingly. On the one hand, this is indeed a very nice property as it allows to really disentangle the marginal distributions of the events and their dependence. On the other hand, this property is incompatible with the property that after distinguishing positive and negative dependence the dependence measure is proportional to and a linear function of . This is a property that only Cole’s possesses, whereas the normalization of changes with the joint probabilities. We do not take a strong stance regarding those properties. Both measures fulfill the more fundamental properties leading to propriety and both are very natural dependence measures.

A.4 Tetrachoric Correlation

Tetrachoric correlation is constructed via the assumption that the contingency table arises by dichotomization of an underlying bivariate normal distribution. The joint probability has to match the area under the bivariate density below quantiles of the two marginals determined by the event probabilities and . As the means and variances play no role here, the correlation coefficient of this underlying bivariate normal is uniquely determined by the joint probability. We adopt the definition from Ekström, (2011).

Definition A.4 (Tetrachoric Correlation).

For interior cases , tetrachoric correlation is implicitly defined via the equation

where denotes the density of a bivariate standard normal distribution with zero means, unit variances and correlation coefficient . Otherwise, we have for and for .

Even though tetrachoric correlation does not seem to be a very natural measure (except for cases, where the binary variables and are really or at least approximately generated by an underlying normal distribution), it is proper. This may at first be surprising, but is essentially due to the fact that under normality the Pearson correlation coefficient has desirable properties, in particular the attainability and independence property.

Proposition A.5.

is proper.

Appendix B Inference Using the Fisher Transformation

As already mentioned in Section 6.3, the sampling distributions of , and are heavily influenced by their theoretical Fréchet-Hoeffding bounds when the true measures are close to these bounds. This leads to skewed empirical distributions for which the asymptotic normal approximations (and similarly for ) are bad. This can strongly deteriorate the finite sample performance of associated tests and confidence intervals as can be seen from our simulation results in Appendix D.

In the case of Pearson correlation, where the analogous problem occurs, the classical tool to combat this problem is Fisher’s transformation (Fisher,, 1915),

| (13) |

for a generic dependence measure . This transformation maps the bounded dependence measures to an unbounded scale while leaving values in the center (approximately the interval ) almost unchanged. On this unbounded scale, asymptotic normality is usually a much better finite sample approximation, especially when the dependence measure is close to the boundary. We therefore apply the Fisher transformation to construct more reliable tests and confidence intervals for (as brought up in Bonett and Price, (2007)), and . Even though the limiting distribution is not Gaussian for , the same problem applies here (unless ).

Starting with the limiting distributions of the Fisher transformation as given below in Propositions B.1–B.3, we obtain non-normal limiting distributions for , and by applying the inverse transformation of (13). These usually lead to much better approximations of the sampling distributions close to the boundaries as illustrated in Figure 6. For the true with , we plot the standard (red) and Fisher transformed (blue) limiting distributions, their implied confidence intervals in dashed lines, and a histogram depicting estimates for a sample size of from simulated data. We see that the finite sample histogram is much better approximated by the blue Fisher transformed limiting distribution.

Consequently, the Fisher transformation leads to more reliable tests and confidence intervals close to the boundaries and almost identical results away from them. To execute a test for one just needs to Fisher transform the hypothesized value and test using the respective asymptotic distribution of the Fisher transformation (again using Bonferroni corrections as described above in the case of ).

We construct confidence intervals as follows. For and , we obtain a confidence interval for the Fisher transform based on its asymptotic normality and then apply the inverse Fisher transformation to these bounds. For , we modify the algorithm described in Section 6.2 by using (inverted) tests based on the asymptotic distribution of the Fisher transforms from Proposition B.2 instead of Proposition 6.5. We illustrate the improved performance of the confidence intervals based on the Fisher transform compared to the ones based on the usual limiting distributions in simulations in Appendix D. The importance of the Fisher transformation is also illustrated when comparing the confidence intervals based on it to standard confidence intervals in the introductory example, where they differ substantially as the sampling distribution is close to the upper bound 1, see Table 6 in the Appendix, and in the case study in Section 7, where they differ in those cases and are very close to each other otherwise, see Figures 13 and 15 in the Appendix.

We continue by formally providing the limiting distributions of the Fisher transformations of , and introduced in Section 6.3, which can be obtained from the asymptotic distributions from Subsection 6.1 together with the delta method. For Yule’s , we instead derive the limit distribution directly as in this case the transformation is a simpler expression than Yule’s itself, namely with the plug-in estimator

Proof of Proposition B.1.

Proposition B.2.

Proof of Proposition B.2.

Proposition B.3.

Proof of Proposition B.3.

As discussed for all the other quantities showing up in the asymptotic variances in Section 6, , and can as well be estimated consistently by their empirical plug-in counterparts , and .

Appendix C Time Series Asymptotics

All our asymptotic results hold under independence as well as under classical time series dependencies, namely by imposing through Assumption 6.3 that , , follows a stationary ergodic adapted mixingale, going back to McLeish, (1974). Mixingales behave asymptotically like martingale difference processes, analogous to mixing processes that behave asymptotically like independent processes (White,, 2001). Generalizations to non-stationarity would be feasible at the cost of a more involved notation as e.g., even the population values would depend on the sample size . In these cases, a CLT different from Lemma E.2 would have to be invoked in the proofs. While allowing for more general dependence and non-stationarity conditions in CLTs usually comes at the cost of more restrictive moment conditions, this is not the case here as all moments exist due to the boundedness of our binary random variables.

To incorporate a possible time series dependence of our random variables, we employ a Heteroskedasticity and Autocorrelation Consistent (HAC) estimator for the long-run covariance matrix (Newey and West,, 1987). For a bandwidth sequence of integers with and a triangular array of weights with for all , , and for all as , let

| (14) |

where . The following proposition shows that this estimator is consistent.

Proposition C.1.

Given that is -mixing of size for some , we have .

Proof of Proposition C.1.

The claim follows from White, (2001, Theorem 6.20) as the triangular array is assumed to be -mixing, the are bounded and hence any moments are bounded, and by construction, . ∎

The estimation and consistency of all other matrices involved in the asymptotic distributions is unchanged compared to the iid case.

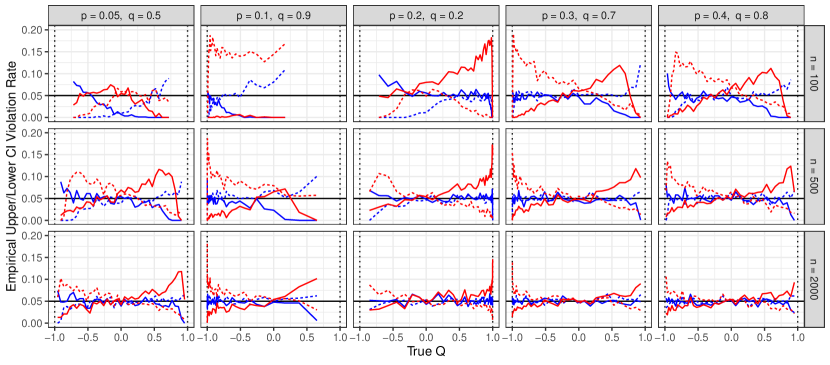

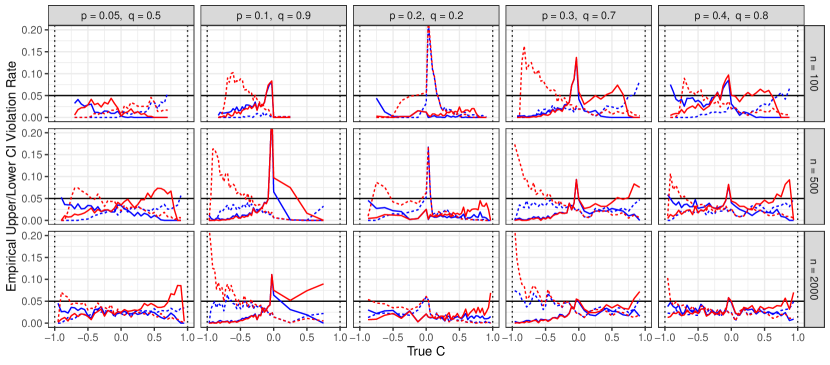

Appendix D Simulations

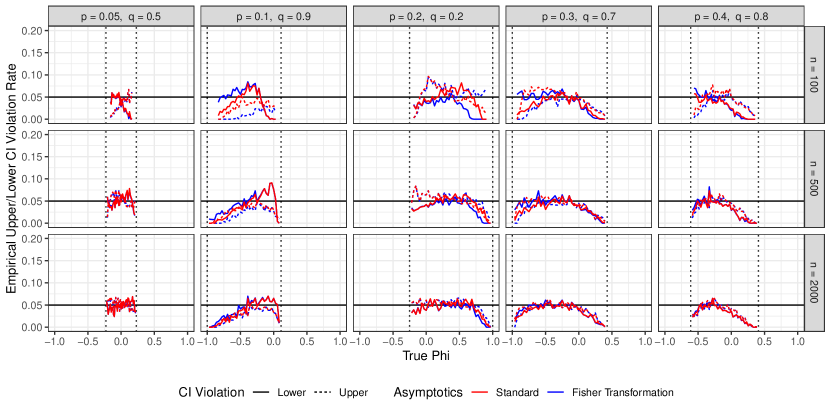

We analyze the finite sample performance of the confidence intervals described in Section 6.2 based on the standard asymptotics in Propositions 6.4–6.6 as well as the Fisher transformations described in Section 6.3, Appendix B and Propositions B.1–B.3. We simulate the pairs of binary random variables independently for different and use . The joint behavior of is characterized by the probabilities , and . In order to cover the different settings in Proposition 6.5, we use . For each of these combinations of and , we choose equally spaced values for between and . In the following, we only report results for the settings where the empirical boundary-conditions and are satisfied in at least of the simulation runs.

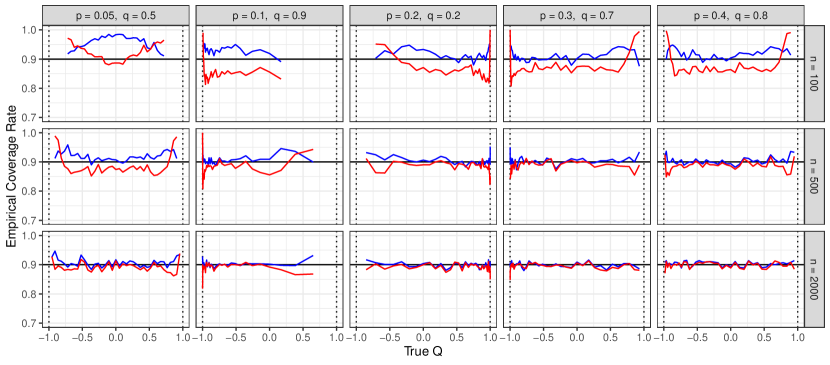

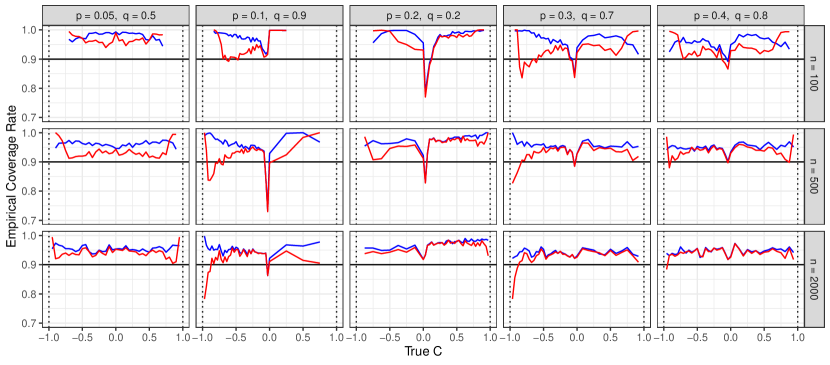

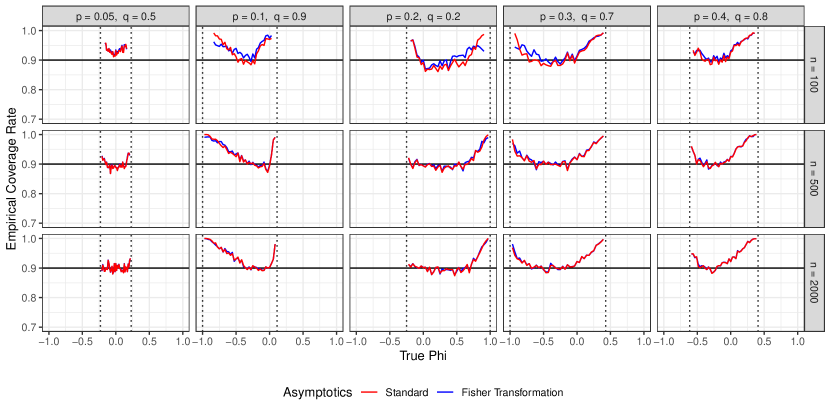

Figure 7 shows the coverage rates of the confidence intervals that are constructed based on the standard and the Fisher-transformed asymptotic distributions for , and in the respective panels. For , we obtain very accurate coverage rates that converge to the nominal level of . While the standard approach displays inaccuracies close to the boundaries, the Fisher transformation expectedly improves the accuracy in these regions.

For , we observe mostly conservative coverage rates that are caused by the multiple testing corrections in the construction of the confidence intervals. The Fisher transformation again improves the accuracy close to the boundaries. The notable downside peak in the coverage rates close to the value of can be explained by the piecewise normalization of . In particular, for a true , the last two terms in (19) involving the quantity in the proof of Proposition 6.5 are shown to be and hence do not contribute to the asymptotic distribution, but deliver non-negligible contributions to the finite sample distributions.

For , we again see the drastic effect of the non-attainability through the theoretical boundaries depicted with the vertical dashed lines. While the coverage rates of the standard method are very accurate in the center, we observe an over-coverage closer to the boundaries that cannot be improved with the Fisher transformation. As the Fisher transformation leaves the central part almost unchanged, it is ineffective when the theoretical boundaries of are far from and , once again illustrating a fundamental deficiency of the phi coefficient.