Student -Lévy regression model in YUIMA

Abstract.

The aim of this paper is to discuss an estimation and a simulation method in the R package YUIMA for a linear regression model driven by a Student- Lévy process with constant scale and arbitrary degrees of freedom. This process finds applications in several fields, for example finance, physic, biology, etc. The model presents two main issues. The first is related to the simulation of a sample path at high-frequency level. Indeed, only the -Lévy increments defined on an unitary time interval are Student- distributed. In YUIMA , we solve this problem by means of the inverse Fourier transform for simulating the increments of a Student- Lévy defined on a interval with any length. A second problem is due to the fact that joint estimation of trend, scale, and degrees of freedom does not seem to have been investigated as yet. In YUIMA , we develop a two-step estimation procedure that efficiently deals with this issue. Numerical examples are given in order to explain methods and classes used in the YUIMA package.

Key words and phrases:

Numerical implemetation, High-frequency sampling, Student Lévy Regression Model.1. Introduction

YUIMA package in R provides several simulation and estimation methods for stochastic processes [4, 16]. This paper introduces new classes and methods in YUIMA for simulating and estimating a -Lévy regression model based on high-frequency observations. This model can be seen as a generalization of a -Lévy process (cf. [14, 7]) by adding covariates, which can be either deterministic or stochastic processes. Adding covariates to a continuous-time stochastic process is a widely used approach for constructing new processes in various fields. For example, in finance, periodic deterministic covariates can be employed to capture the seasonality observed in commodity markets [24]. Alternatively, in insurance and medicine, covariates are often incorporated into mortality rate dynamics to account for age and cohort effects (see [13, 5] and references therein).

In such fields, data often exhibit heavy-tailed behavior in the margins and thus, the inclusion of a -Lévy process as a driving noise would be useful. However, despite the simple mathematical definition of a -Lévy regression model, it poses significant challenges both in deriving its mathematical properties and in implementing numerical methods. A key difficulty arises from the fact that the -Lévy driving noise is not closed under convolution. Consequently, the distribution of its increments follows a -distribution only over a unit-time interval.

Motivated by this fact, in YUIMA , we propose three simulation methods for a -Lévy regression model. The key element is the construction of a random number generator for the noise increments, which is essential for several discretized simulation methods and involves the numerical inversion of the characteristic function. More specifically, our method is based on the approximation of the cumulative distribution function, and our method can relieve numerical instability compared with directly using the density function especially for simulating small time increments. Additionally, YUIMA provides a two-stage estimation procedure and the corresponding estimator has consistency and asymptotic normality as shown in [21].

The rest of this paper is organized as follows. We briefly summarize the -Lévy regression model in Section 2. We introduce the new YUIMA classes and methods in Section 3 and we show some examples with simulated and real data that highlight their usage in Section 4. Finally, Section 5 concludes the paper.

2. t-Lévy regression model

In this section, we review the main characteristics of the -Lévy regression model and the -Lévy process used as its driving noise. We highlight the main issues that arise in the simulation and estimation procedures for these models. For a complete discussion on all mathematical aspects and the properties of these procedures in both cases, we refer to [21].

The proposed -Lévy regression model is a continuous-time stochastic process of the form:

| (2.1) |

where the -dimensional vector process with càdlàg paths contains the covariates; the dot denotes the inner product in and is a -Lévy process such that its unit-time distribution is given by:

| (2.2) |

where denotes the scaled Student- distribution with density:

The parameters , and represent the degree of freedom, position, and scale parameters, respectively (see [14, 7] for more details on a -Lévy process). For this model, we consider the situation where we estimate these three unknown parameters based a discrete-time sample with and as .

To develop the YUIMA simulation and estimation algorithms for the model in (2.1), we need to address two problems: first, the simulation of the sample path of on a small time grid with which is essential for handling the increments:

where denotes for any stochastic process . Second, the identification of an efficient procedure for estimating the model parameters in (2.1) and the degree of freedom in (2.2). We will introduce both the simulation and estimation methods below.

Due to the stationary behavior of the Lévy increments, i.e. and for , admits the Lebesgue density:

| (2.3) |

where , the characteristic function of is given by

| (2.4) |

and denotes the modified Bessel function of the second kind (, ):

We here remark that although the explicit expression of (2.3) cannot be obtained for general , the tail index of is the same as that of (cf. [3] Theorem 2), and hence, modeling tail index via student -Lévy process makes sense. A classical method for simulating -Lévy increments based on this Fourier inversion representation is through the rejection method, as discussed in [15] and [8]. However, this method can become time-consuming and unstable when dealing with very small values of , primarily due to the oscillatory behavior encountered during the numerical evaluation of density. Such a problem often arises since to express the high-frequently observed situation from a continuous process, we should take a finer mesh of simulating the underlying process than that of simulating the discrete observations. For this issue, in YUIMA , the Random Number Generator for the increments is developed using the inverse quantile method. The first step involves integrating the density in (2.3) to obtain the cumulative distribution function (CDF). This approach leads to a more stable behavior in the tails of the CDF compared to the density tails, owing to a mitigation effect observed during the numerical evaluation of the following double integral:

| (2.5) |

Further details on our approach are provided in the next section. Another way to simulate -Lévy process is using series representation. Numerically, for each time , we need ad-hoc truncation of the infinite sum. The Gaussian approximation of a small-jump part is also valid [1], but the associated error may not be easy to control in a practical manner. For more details, see [19].

Following [21], YUIMA provides a two-stage estimation algorithm for . Denote by the parameter true values of the model in (2.1); the two-step algorithm can be summarized as follows:

-

(1)

An estimator of is obtained by maximizing the Cauchy quasi-likelihood:

(2.6) The Cauchy quasi-(log-)likelihood conditional on has the following form:

where denotes the density function of the standard Cauchy distribution and the term does not depend on . is the number of observations in the part of the entire period where is a positive sequence satisfying and for some .

-

(2)

Then, we construct an estimator of using the Student- quasi-likelihood on the “unit-time” residual sequence :

for , which is expected to be approximately i.i.d. -distributed. Therefore solves:

where

We note that the first estimation scheme is based on the locally Cauchy property of : (standard Cauchy) as . Let and . Under some regularity conditions on the covariate process (see Assumption 2.1 in [21]for all requirements on ), the estimators have the following joint asymptotic normality:

where denotes the trigamma function and

Since and can be constructed only by the observations, we can easily obtain the confidence intervals of each parameter.

3. Classes and Methods for t-Lévy Regression Models

This section provides an overview of the new classes and methods introduced in YUIMA for the mathematical definition, trajectory simulation, and estimation of a Student Lévy Regression model. To handle this model, the first step involves constructing an object of the yuima.LevyRM-class. As an extension of the yuima-class (refer to [4] for more details), yuima.LevyRM-class inherits slots such as @data, @model, @sampling, and @functional from its parent class. The remaining slots store specific information related to the Student--Lévy regression model.

Notably, the slot @unit_Levy contains an object of the yuima.th class, which represents the mathematical description of the Student- Lévy process (see the subsequent section for detailed explanations). The labels of the regressors are saved in the slot @regressors, while slots @LevyRM and @paramRM respectively cache the names of the output process and a string vector reporting the regressors’ coefficients, the scale parameter, and the degree of freedom. The yuima.th-class is obtained by the new setLaw_th constructor. This function requires the arguments used for the numerical inversion of the characteristic function, and its usage is discussed in the next section.

Once the yuima.th-object is created, we define the system of stochastic differential equations (SDEs) that describes the behavior of the regressors, with their mathematical definitions stored in an object of the yuima.model-class. Both yuima.th and yuima.model objects are used as inputs for the setLRM constructor, which returns an object of the yuima.LevyRM-class. The following chunk code reports the input for this new function.

setLRM(unit_Levy, yuima_regressors, LevyRM = "Y", coeff = c("mu", "sigma0"), data = NULL, sampling = NULL, characteristic = NULL, functional = NULL) As is customary for any class extending the yuima-class, the simulate method enables the generation of sample paths for the Student Lévy Regression model. To simulate trajectories, an object of the yuima.sampling-class is constructed to represent an equally spaced grid-time used in trajectory simulation. The regressors’ paths are obtained using the Euler scheme, while the increments of the Student- Lévy process are simulated using the random number generator available in the slot @rng of the yuima.th-object.

The last method available in YUIMA is estimation_LRM. This method allows the users to estimate the model using either real or simulated data. The estimation follows a two-step procedure, introduced in [21].

estimation_LRM(start, model, data, upper, lower) For this function, the minimal inputs are start, model, data, upper and lower. The arguments start are the initial points for the optimization routine while upper and lower corresponds to the box constraints. The yuima.LevyRM-object is passed to the function through the input model while the input data is used to pass the dataset to the internal optimization routine. Figure 1 describes these new classes and methods, along with their respective usage.

3.1. yuima.th: A new class for mathematical description of a Student-t Lévy process

In this section, the steps for the construction of an yuima.th-object are presented. As remarked in Section 3, this object contains all information on the Student- Lévy process. Moreover, detailed information is provided regarding the numerical algorithms utilized for evaluating the density function (2.3). The construction of this object is accomplished using the setLaw_th constructor, and the subsequent code snippet displays its corresponding arguments.

setLaw_th(h = 1, method = "LAG", up = 7, low = -7, N = 180, N_grid = 1000, regular_par = NULL) The input h is the length of the step-size of each time interval for the Student- Lévy increment . Its default value, h=1, indicates that the yuima.th-object describes completely the process at time 1. The argument method refers to the type of quadrature used for the computation of the integral in (2.3) while the remaining arguments govern the precision of the integration routine.

The yuima.th-class inherits the slots @rng, @density, @cdf and @quantile from its parent class yuima-law [20]. These slots store respectively the random number generator, the density function, the cumulative distribution function and the quantile function of .

As mentioned in Section 1, the density function with does not have a closed-form formula and, therefore, the inversion of the characteristic function is necessary. YUIMA provides three methods for this purpose: the Laguerre quadrature, the COS method and the Fast Fourier Transform. The Gauss-Laguerre quadrature is a numerical integration method employed for evaluation integrals in the following form:

This procedure has been recently used for the computation of the density of the variance gamma and the transition density of a CARMA model driven by a time-changed Brownian motion [18, 22], this motivates its application in this paper.

Let be a continuous function defined on such that:

the integral can be approximated as follows:

| (3.1) |

where is the th-root of the -order Laguerre polynomial111The Laguerre polynomial can be defined recursively as follows: and the weights are defined as:

| (3.2) |

To apply the approximation in (3.1), we rewrite the inversion formula in (2.3) as follows:

| (3.3) | |||||

Applying the result in (3.1), the density function of can be approximated with the formula reported below:

Notably, the approximation formula’s precision in equation (3.1) can be enhanced through the argument N in the setLaw_th constructor. The roots and the weights are internally computed using the gauss.quad function from the R package statmod, with a maximum allowed order of 180 for the Laguerre polynomial.

The COS method is based on the Fourier Cosine expansion employed for an even function with the compact domain . This method has been widely applied in the finance literature for the computation of the exercise probability of an option and its no-arbitrage price, we refer to [10, 11] and references therein for details. Let be an even function, its Fourier Cosine expansion reads:

| (3.4) |

with

Denoting with the density function of the increment , the new function is defined as:

| (3.5) |

The function is still an even function for any and the Fourier Cosine expansion in (3.4) can be applied. The coefficient is determined as follows:

Setting , we have:

| (3.6) |

The coefficient can be rewritten using the characteristic function of at , i.e.:

| (3.7) |

For a sufficiently large , the coefficient can be approximated as follows:

| (3.8) |

The following series expansion is achieved:

| (3.9) |

with

Finally, (3.9) can be approximated by truncating the series as follows:

| (3.10) |

with

The precision of in (3.10) depends on and . Users can select these two quantities using N and the couple (up, low) respectively. is computed internally in the setLaw_th constructor as L = max(|low|,up).

The last method available in YUIMA is the Fast Fourier Transform (FFT) [23, 6] for the inversion of the characteristic function. YUIMA uses the FFT method developed internally in the function FromCF2yuima_law for the inversion of any characteristic function defined by users. In the latter case, the density function of is based on the following general inversion formula:

| (3.11) |

As first step, we apply to the integral in (3.11) the change variable and we have:

| (3.12) |

We consider discrete support for and . The grid has the following structure:

| (3.13) |

with where is the number of the points in the grid in (3.13). Similarly, we define a grid:

| (3.14) |

where . Both grids have the same dimension , shrinks as while reduces for large values of . For any in the grid we can approximate the integral in (3.11) using the left Riemann summation, therefore, we have the approximation :

| (3.15) |

The last equality in (3.15) is due to the identity . To evaluate the summation in (3.15), we use the FFT algorithm and

| (3.16) |

In this case, we have two sources of approximation errors that we can control using the arguments up, low and N in the setLaw_th constructor. N denotes the number of intervals in the grid used for the Left-Riemann summation while up, low are used to compute the step size of this grid.

Once the density function has been obtained using one of the three methods described above, it is possible to approximate the cumulative distribution function using the Left-Riemann summation computed on the grid in (3.13), therefore the cumulative distribution function for each on the grid is determined as follows:

| (3.17) |

In this way, we can construct a table that we can use internally in the cdf and quantile functions. Moreover, to evaluate the cumulative distribution function at any , we interpolate linearly its value using the couples and . The random numbers can be obtained using the inversion sampling method.

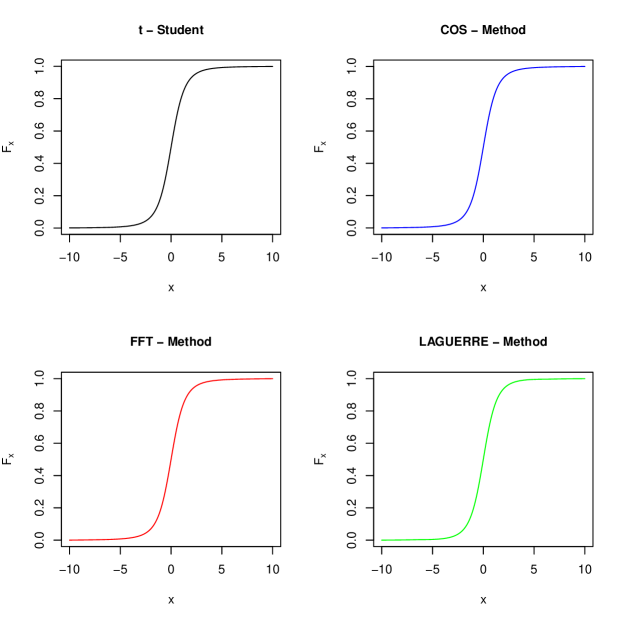

We conclude this section with a numerical comparison among the three methods implemented in YUIMA . To assess the precision of our code we use as a target the cumulative distribution function of a Student- with computed through the R function pt available in the package stats. To conduct this comparison, we construct three yuima.th-objects as displayed in the code snippet reported below.

# To instal YUIMA from Github repositoryR> library(devtools)R> install_github("yuimaproject/yuima")########### Inputs ###########R> library(yuima)R> nu <- 3R> h <- 1 # step size for the interval timeR> up <- 10R> low <- -10# Support definition for variable xR> x <- seq(low,up,length.out=100001)# Definition of yuima.th-objectR> law_LAG <- setLaw_th(h = h, method = "LAG", up = up, low = low, N = 180) # LaguerreR> law_COS <- setLaw_th(h = h, method = "COS", up = up, low = low, N = 180) # COSR> law_FFT <- setLaw_th(h = h, method = "FFT", up = up, low = low, N = 180) # FFT# Cumulative Distribution Function: we apply the cdf method to the yuima.th-objectR> Lag_time <- system.time(ycdf_LAG <- cdf(law_LAG, x, list(nu=nu))) # LaguerreR> COS_time <- system.time(ycdf_COS<-cdf(law_COS, x, list(nu=nu))) # COSR> FFT_time <- system.time(ycdf_FFT<-cdf(law_FFT, x, list(nu=nu))) # FFT User can specify the numerical methods of the inversion of the characteristic function using the input method. This argument assumes three values: "LAG" for the Gauss-Laguerre quadrature, "COS" for the Cosine Series Expansion and "FFT" for the Fast Fourier Transform. Once the yuima.th-object has been constructed, its cumulative distribution function is computed by applying the YUIMA method222An object of yuima.th-class inherits the dens method for the density computation, cdf for the evaluation of the cumulative distribution function, quantile for the quantile function and rand for the generation of the random sample. We refer to [20] for the usage of these methods. cdf that returns the cumulative distribution function for the numeric vector x.

Figure 2 compares the cumulative distribution functions of the Student- obtained using the methods in YUIMA with the pt function. In all cases, we have a good level of precision that is also confirmed by Table 1. As expected the fastest method is the FFT which seems to be also the most precise.

| COS | FFT | LAG | |

|---|---|---|---|

| RMSE | 0.021 | 0.021 | 0.064 |

| Max | 0.032 | 0.032 | 0.085 |

| Min | 7.88e-05 | 2.18e-05 | 4.97e-04 |

| sec. | 1.47 | 4.00e-02 | 1.2 |

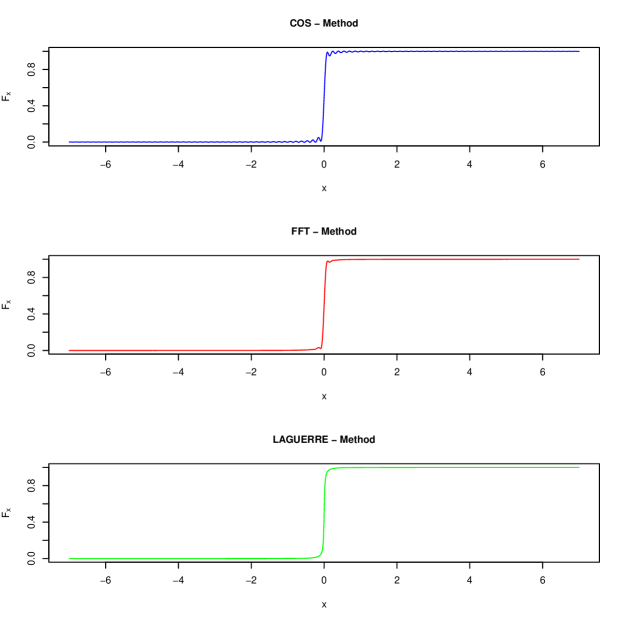

To further investigate this fact, we study the behaviour of the cumulative distribution function when varies. For , we observe an oscillatory behaviour on tails for the FFT and COS while the Laguerre method seems to be more stable as shown in Figure 3. To have a fair comparison, we set N = 180, however we notice that the precision of FFT can be drastically improved by tuning the inputs N, up and low.

4. Numerical examples

This section presents a series of numerical examples demonstrating the practical application of newly developed classes and methods within the Student- Regression model. Specifically, we showcase the simulation and estimation of models where the regressors are determined by deterministic functions of time in the first example. The second example introduces integrated stochastic regressors. Lastly, we perform an analysis using real data in the final example.

4.1. Model with deterministic regressors.

In this example, we consider two deterministic regressors and the dynamics of the model have the following form:

| (4.1) |

with the true values . The estimation of the model (4.1) has been investigated in [21] where the empirical distribution of the studentized estimates has been discussed. To use the simulation method in YUIMA we have to write the dynamics of the regressors and , that is:

| (4.2) |

with the initial condition:

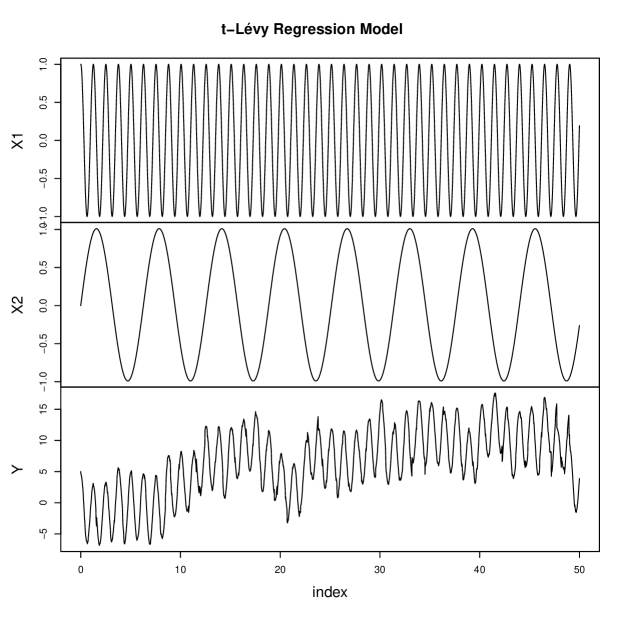

In the following, we show how to implement this model in YUIMA . In this example, we set , and thus the number of the observations over unit time is . We also set the terminal time of the whole observations and that of the partial observations .

R> library(yuima)########### Inputs ############ Inputs for Fourier InversionR> method_Fourier = "FFT"; up = 6; low = -6; N = 2^17; N_grid = 60000# Inputs for the sample grid timeR> Factor <- 1R> Factor1 <- 1R> initial <- 0; Final_Time <- 50 * Factor; h <- 0.02/Factor1

We notice that the variable Factor1 controls the step size of the time grid. Indeed for different values of this quantity, we have a different value for for example Factor1 = 1, 2, 4, 7.2 corresponds h = 0.02, 0.01, 0.005, 1/365.

The first step is the definition of an object of yuima.th-class using the constructor setLaw_th.

This object contains the random number generator, the density function, the cumulative distribution function and the quantile function for constructing the increments of a Student- Lévy process.

######################################## Example 1: Deterministic Regressors ########################################R> mu1 <- 5; mu2 <- -1; scale <- 3; nu <- 3 # Model Parameters# Model DefinitionR> law1 <- setLaw_th(method = method_Fourier, up = up, low = low, N = N, N_grid = N_grid) # yuima.thR> class(yuima_law)

[1] "yuima.th"attr(,"package")[1] "yuima"

The next step is to define the dynamics of the regressors described in (4.2). This set of differential equations is defined in YUIMA using the standard constructor setModel. Once an object containing the mathematical description of the regressors has been defined, we use setLRM to obtain the yuima.LevyRM. In the following, we report the command lines for the definition of the Student Lévy Regression Model in (4.1).

R> regr1 <- setModel(drift = c("-5*sin(5*t)", "cos(t)"), diffusion = matrix("0",2,1), solve.variable = c("X1","X2"), xinit = c(1,0)) # Regressors definitionR> Mod1 <- setLRM(unit_Levy = law1, yuima_regressors = regr1) # t-Regression ModelR> class(Mod1)

[1] "yuima.LevyRM"attr(,"package")[1] "yuima"

Using the object Mod1 we simulate a trajectory of the model in (4.1) using the YUIMA method simulate.

# SimulationR> samp <- setSampling(initial, Final_Time, n = Final_Time/h)R> true.par <- unlist(list(mu1 = mu1, mu2 = mu2, sigma0 = scale, nu = nu))R> set.seed(1)R> sim1 <- simulate(Mod1, true.parameter = true.par, sampling = samp) Figure 4 reports the simulated sample paths for the regressors , and the Student Lévy Regression model .

The next step is to study the behaviour of the two-step estimation procedure described in Section 2. To run this procedure, we use the method estimation_LRM and then we initialize randomly the optimization routine as shown in the following command lines.

# EstimationR> lower <- list(mu1 = -10, mu2 = -10, sigma0 = 0.1)R> upper <- list(mu1 = 10, mu2 = 10, sigma0 = 10.01)R> start <- list(mu1 = runif(1, -10, 10), mu2 = runif(1, -10, 10),+ sigma0 = runif(1, 0.01, 4))R> Bn <- 15*FactorR> est1 <- estimation_LRM(start = start, model = sim1, data = sim1@data,+ upper = upper, lower = lower, PT = Bn)R> class(est1)

[1] "yuima.qmle"attr(,"package")[1] "yuima"

R> summary(est1)

Quasi-Maximum likelihood estimationCall:estimation_LRM(start = start, model = sim1, data = sim1@data, upper = upper, lower = lower, PT = Bn)Coefficients: Estimate Std. Errormu1 5.029555 0.03538355mu2 -1.128905 0.18026088sigma0 2.425147 0.12523404nu 2.735344 0.47457435-2 log L: 3236.535 73.3833

It is also possible to construct the dataset without the method simulate. This result can be achieved by constructing an object of yuima.th-class that represents the increment of the Student- Lévy process on the time interval with length .

# Dataset construction without YUIMAR> time_t <- index(get.zoo.data(sim1@data)[[1]])R> X1 <- zoo(cos(5*time_t), order.by = time_t)R> X2 <- zoo(sin(time_t), order.by = time_t)R> law1_h <- setLaw_th(h = h, method = method_Fourier, up = up, low = low, N = N, N_grid = N_grid)R> print(c(law1_h@h,law1@h))

[1] 0.02 1.00

The object law1_h refers to the Student- Lévy increment over an interval with length as it can be seen looking at the slot ...@h.

R> set.seed(1)R> names(nu)<- "nu"R> J_t <- zoo(cumsum(c(0,rand(law1_h, Final_Time/h,nu))), order.by = time_t)R> Y <- mu1 * X1 + mu2 * X2 + scale/sqrt(nu) * J_tR> data1_a <- merge(X1, X2, Y)

The estimation is performed by means of the method estimation_LRM as in the previous example.

R> est1_a <- estimation_LRM(start = start, model = Mod1, data = setData(data1_a),+ upper = upper, lower = lower, PT = Bn)R> summary(est1_a)

Quasi-Maximum likelihood estimationCall:estimation_LRM(start = start, model = Mod1, data = setData(data1_a), upper = upper, lower = lower, PT = Bn)Coefficients: Estimate Std. Errormu1 4.987778 0.03642823mu2 -1.164138 0.18558422sigma0 2.495930 0.12888927nu 2.407683 0.41221590-2 log L: 3232.784 85.32438

Using the result stored in the summary we can construct a confidence interval using the command lines reported below.

R> info_sum <- summary(est1_a)@coefR> alpha <- 0.025R> Confidence_Int_95 <- rbind(info_sum[,1]+info_sum[,2]*qnorm(alpha),+ info_sum[,1]+info_sum[,2]*qnorm(1-alpha),unlist(true.par),+ info_sum[,1])R> rownames(Confidence_Int_95) <- c("LB","UB","True_par","Est_par")R> print(Confidence_Int_95, digit = 4)

mu1 mu2 sigma0 nuLB 4.916 -1.5279 2.243 1.600UB 5.059 -0.8004 2.749 3.216True_par 5.000 -1.0000 3.000 3.000Est_par 4.988 -1.1641 2.496 2.408 Based on the aforementioned examples, the estimated value for the parameter deviates from its true value. To further investigate this observation, we conducted a comparative analysis using the three integration methods discussed in Section 3.1. This exercise was repeated for three different values of and . To ensure a fair comparison among the Laguerre, Cosine Series expansion, and Fast Fourier Transform methods, we set the argument N = 180. The obtained results are presented in Table 2.

| Laguerre Method | COS Method | FFT Method | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 0.01 | 0.005 | 0.01 | 0.005 | 0.01 | 0.005 | ||||

| 4.968 | 5.019 | 4.976 | 4.939 | 5.065 | 4.875 | 4.934 | 5.069 | 4.876 | |

| (0.029) | (0.020) | (0.014) | (0.041) | (0.049) | (0.054) | (0.042) | (0.049) | (0.054) | |

| -1.065 | -1.044 | -0.914 | -1.192 | -1.195 | -0.555 | -1.179 | -1.178 | -0.528 | |

| (0.146) | (0.104) | (0.074) | (0.210) | (0.247) | (0.277) | (0.213) | (0.248) | (0.277) | |

| 2.770 | 2.794 | 2.657 | 3.993 | 6.654 | 10.010 | 4.055 | 6.674 | 10.010 | |

| (0.101) | (0.072) | (0.051) | (0.145) | (0.172) | (0.192) | (0.148) | (0.172) | (0.193) | |

| 3.462 | 3.281 | 3.067 | 2.827 | 2.223 | 2.227 | 5.749 | 8.310 | 15.175 | |

| (0.615) | (0.580) | (0.538) | (0.492) | (0.377) | (0.378) | (1.063) | (1.571) | (2.940) | |

| sec. | 2.07 | 2.02 | 2.07 | 1.10 | 1.24 | 1.34 | 0.15 | 0.24 | 0.39 |

In the Laguerre method, we observe that reducing the step size leads to improved estimates of , however looking at the asymptotic standard error, the estimates for seem to maintain the bias. As for the remaining methods, the estimates exhibit unsatisfactory performance due to the imposed restriction of N = 180 (that is the maximum value allowed for the Laguerre quadrature in the evaluation of the density in (3.3)). This outcome is not unexpected, given the Laguerre method’s ability to yield a valid distribution even with a relatively small value of N, as demonstrated in Figure 3. Nevertheless for the COS and the FFT, it is possible to enhance the results by increasing the value of the argument N that yields a more accurate result in the simulation of the sample path for the model described in (4.1).

| COS Method | FFT Method | |||||

|---|---|---|---|---|---|---|

| N | 1000 | 5000 | 10000 | 1000 | 5000 | 10000 |

| 4.968 | 4.975 | 4.975 | 4.968 | 4.975 | 4.975 | |

| (0.034) | (0.016) | (0.016) | (0.035) | (0.306) | (0.016) | |

| -0.887 | -0.909 | -0.909 | -0.886 | -0.908 | -0.908 | |

| (0.174) | (0.082) | (0.082) | (0.177) | (0.022) | (0.082) | |

| 3.300 | 2.964 | 2.964 | 3.363 | 2.963 | 2.964 | |

| (0.064) | (0.057) | (0.057) | (0.065) | (0.057) | (0.057) | |

| 2.713 | 2.765 | 2.765 | 3.279 | 2.760 | 2.702 | |

| (0.470) | (0.480) | (0.480) | (0.579) | (0.479) | (0.468) | |

| sec. | 3.49 | 14.83 | 33.70 | 0.38 | 0.44 | 0.45 |

Table 3 shows the estimated parameters for the varying value of N and . As expected increasing the precision in the quadrature improved estimates for both methods. Notably for N 5000, all estimates fall within the asymptotic confidence interval at the level.

4.2. Model with integrated stochastic regressors

In this section, we consider two examples whose regressors are stochastic. Moreover, to satisfy the regularity conditions, the regressors are supposed to be an integrated version of stochastic processes.

Example 1

In this example, we consider the following continuous time regression model with a single regressor:

| (4.3) |

with the true values , and the process is supposed to be the Lévy driven Ornstein-Uhlenbeck process defined as:

where the driving noise is the Lévy process with . The normal inverse Gaussian (NIG) random variable is defined as the normal-mean variance mixture of the inverse Gaussian random variable, and the probability density function of is given by

where and . More detailed theoretical properties of the NIG-Lévy process are given for example in [2].

For the simulation by YUIMA , we formally introduce the following system:

| (4.4) |

with the initial condition:

The process corresponds to the regressor in the regression model (4.3). Due to the specification of the new YUIMA function, we will additionally construct the “full” model:

| (4.5) |

and simulate the trajectory of with . After that, we will estimate the parameters by the original model (4.3). From now on, we show the implementation of this model in YUIMA . The sampling setting is unchanged from the previous example code: .

R> library(yuima)########### Inputs ############ Inputs for Fourier InversionR> method_Fourier = "FFT"; up = 6; low = -6; N = 2^17; N_grid = 60000# Inputs for the sample grid timeR> Factor <- 1R> Factor1 <- 1R> initial <- 0; Final_Time <- 50 * Factor; h <- 0.02/Factor1

The role of the variable Factor1 is the same as in the previous section.

By using the constructor setLaw_th, we define yuima.th-class in a similar manner.

After that, we construct the “full” model (4.5) by the constructors setModel and setLRM.

A trajectory of and its regressors can be simulated by the YUIMA method simulate.

##################################################### Regressor: Integrated NIG-Levy driven OU process #####################################################R> mu1 <- -3; mu2 <- 0; scale <- 3; nu <- 2.5 # Model Parameters# Model DefinitionR> lawILOU <- setLaw_th(method = method_Fourier, up = up, low = low, N = N,+ N_grid = N_grid) # yuima.thR> regrILOU <- setModel(drift = c("X2", "-X2"), jump.coeff = c("0", "2"),+ solve.variable = c("X1","X2"), xinit = c(0,0), measure.type = "code",+ measure = list(df = "rNIG(z, 1, 0, 1, 0)")) # Regressors definition# t-Regression modelR> ModILOU <- setLRM(unit_Levy = lawILOU, yuima_regressors = regrILOU)# SimulationR> sampILOU <- setSampling(initial, Final_Time, n = Final_Time/h)R> true.parILOU <- unlist(list(mu1 = mu1, mu2 = mu2, sigma0 = scale, nu = nu))R> set.seed(1)R> simILOU <- simulate(ModILOU, true.parameter = true.parILOU, sampling = sampILOU)

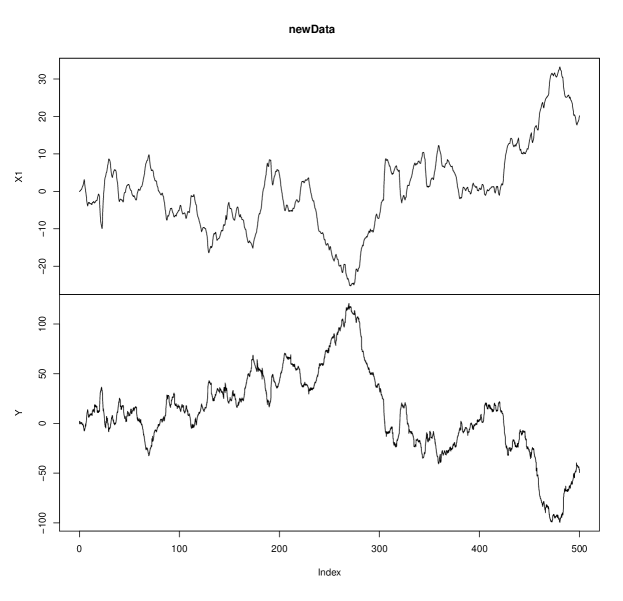

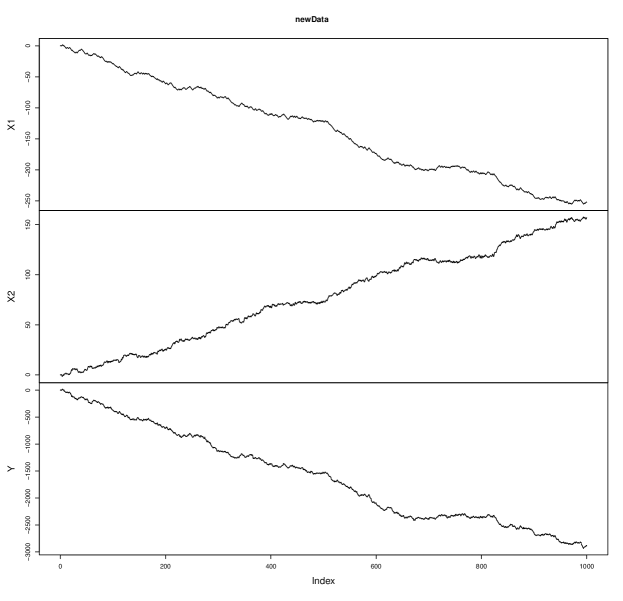

Next we extract the trajectories of and from the yuima.LevyRM-class: simILOU and construct the new model for the estimation of the parameters. Figure 5 shows the simulated sample paths for the regressor and the response process .

# Data extractionR> Dataset<-get.zoo.data(simILOU)R> newData <-Dataset[-2]R> newData <- merge(newData$X1, newData$Y)R> colnames(newData) <- c("X1","Y")R> plot(newData)# Define the model for estimationR> regrILOU1 <- setModel(drift = c("0"), diffusion = matrix(c("0"),1,1),+ solve.variable = c("X1"), xinit = c(0)) # Regressors definition# t-Regression modelR> ModILOU1 <- setLRM(unit_Levy = lawILOU, yuima_regressors = regrILOU1)# EstimationR> lower1 <- list(mu1 = -10, sigma0 = 0.1)R> upper1 <- list(mu1 = 10, sigma0 = 10.01)R> startILOU1<- list(mu1 = runif(1, -10, 10), sigma0 = runif(1, 0.01, 4))R> Bn <- 15*FactorR> Data1 <- setData(newData)R> estILOU1 <- estimation_LRM(start = startILOU1, model = ModILOU1, data = Data1,+ upper = upper1, lower = lower1, PT = Bn)R> summary(estILOU1)

Quasi-Maximum likelihood estimationCall:estimation_LRM(start = startILOU1, model = ModILOU1, data = Data1, upper = upper1, lower = lower1, PT = Bn)Coefficients: Estimate Std. Errormu1 -2.959621 0.02112734sigma0 2.778659 0.03208519nu 2.404843 0.13018410-2 log L: 69711.32 854.3838

Example 2

In this example, we consider the following regression model:

| (4.6) |

where the process satisfy

| (4.7) | |||

| (4.8) |

with

and standard Wiener process . We set the true values

The process is the so-called stochastic FitzHugh-Nagumo process which is a classical model for describing a neuron; expresses the membrane potential of the neuron and represents a recovery variable. Its theoretical properties such as hypoellipticity, and Feller and mixing properties are well summarized in [17]. The paper also provides a nonparametric estimator of the invariant density and spike rate. Similarly, other integrated degenerate diffusion can be considered as regressors. Its ergodicity for the regularity condtions is studied for example in [25]. For the statistical inference for degenerate diffusion processes, we refer to [9] and [12].

For the implementation of the regression model (4.6) on YUIMA, we formally consider the following dynamics:

| (4.9) |

with the initial condition:

The first and second elements correspond to the regressor in (4.6). As in the previous example, we first simulate data by the “full” model defined as:

| (4.10) |

with , and after that, we extract the simulated data and estimate the parameters based on the original regression model (4.6). Below we show how to implement on YUIMA. In this example, we set . The values of them are controlled by the variables Factor and Factor1 in the example code.

R> library(yuima)########### Inputs ############ Inputs for Fourier InversionR> method_Fourier = "FFT"; up = 6; low = -6; N = 2^17; N_grid = 60000# Inputs for the sample grid timeR> Factor <- 20R> Factor1 <- 4R> initial <- 0; Final_Time <- 50 * Factor; h <- 0.02/Factor1############################################################# Regressor: Integrated stochastic FitzHugh-Nagumo process #############################################################R> mu1 <- 8; mu2 <- -4; mu3 <- 0; mu4 <- 0; scale <- 8; nu <- 3 # Model Parameters# Model DefinitionR> lawFN <- setLaw_th(method = method_Fourier, up = up, low = low,+ N = N, N_grid = N_grid) # yuima.thR> regrFN <- setModel(drift = c("V3", "V4", "3*(V3-V3^3-V4)", "1.5*V3-V4+0.5"),+ diffusion = matrix(c("0", "0", "0", "2"),4,1),+ solve.variable = c("V1","V2", "V3", "V4"),+ xinit = c(0,0,0,0)) # Regressors definitionR> ModFN <- setLRM(unit_Levy = lawFN, yuima_regressors = regrFN) # t-regression model# SimulationR> sampFN <- setSampling(initial, Final_Time, n = Final_Time/h)R> true.parFN <- unlist(list(mu1 = mu1, mu2 = mu2, mu3 = mu3, mu4 = mu4,+ sigma0 = scale, nu = nu))R> set.seed(12)R> simFN <- simulate(ModFN, true.parameter = true.parFN, sampling = sampFN)

In this example, both Factor and Factor1 are larger than the previous example, and hence it takes a higher computational load than the previous one. Figure 6 shows the simulated sample paths for the regressor and the Student Lévy Regression model . Now we move on to the estimation phase.

R> Dataset<-get.zoo.data(simFN)R> newData <-Dataset[-c(3,4)]R> newData <- merge(newData$X1,newData$X2, newData$Y)R> colnames(newData) <- c("X1","X2", "Y")R> plot(newData)# Define the model for estimationR> regrFN1 <- setModel(drift = c("0", "0"), diffusion = matrix(c("0", "0"),2,1),+ solve.variable = c("X1", "X2"), xinit = c(0,0)) # Regressors definitionR> ModFN1 <- setLRM(unit_Levy = lawFN, yuima_regressors = regrFN1) # t-Regression model.# EstimationR> lower1 <- list(mu1 = -10, mu2 = -10, sigma0 = 0.1)R> upper1 <- list(mu1 = 10, mu2 =10, sigma0 = 10.01)R> startFN1<- list(mu1 = runif(1, -10, 10), mu2 = runif(1, -10, 10),+ sigma0 = runif(1, 0.01, 4))R> Bn <- 15*FactorR> Data1 <- setData(newData)R> estFN1 <- estimation_LRM(start = startFN1, model = ModFN1, data = Data1,+ upper = upper1, lower = lower1, PT = Bn)R> summary(estFN1)

Quasi-Maximum likelihood estimationCall:estimation_LRM(start = startFN1, model = ModFN1, data = Data1, upper = upper1, lower = lower1, PT = Bn)Coefficients: Estimate Std. Errormu1 8.041838 0.04895791mu2 -4.041518 0.04495255sigma0 7.712157 0.04452616nu 3.020972 0.11837331-2 log L: 403960.9 1291.516

4.3. Real data regressors

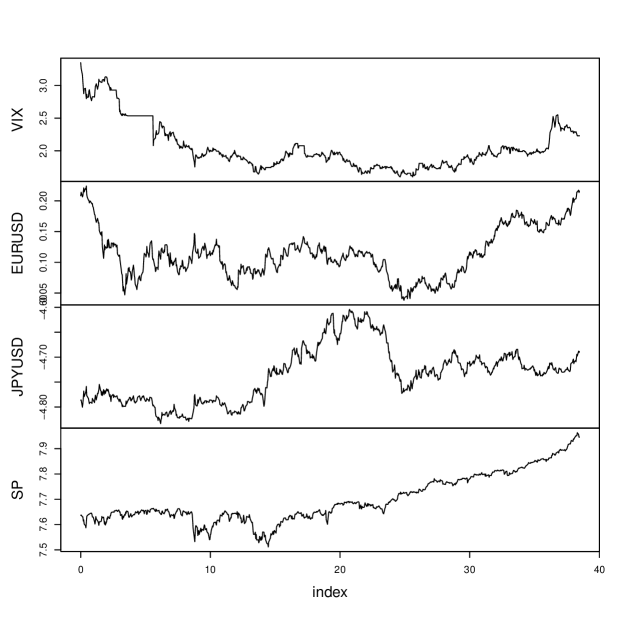

In this section, we show how to use the YUIMA package for the estimation of a Student Lévy Regression model in a real dataset. We consider a model where the daily price of the Standard and Poor 500 Index is explained by the VIX index and two currency rates: the YEN-USD and the Euro Usd rates. The dataset was provided by Yahoo.finance and ranges from December 14th 2014 to May 12th 2023. We downloaded the data using the function getSymbol available in quantmod library. To consider a small value for the step size we estimate our model every month (). We report below the code for storing the market data in an object of yuima.data-class

R> library(yuima)R> library(quantmod)R> getSymbols("^SPX", from = "2014-12-04", to = "2023-05-12")# RegressorsR> getSymbols("EURUSD=X", from = "2014-12-04", to = "2023-05-12")R> getSymbols("VIX", from = "2014-12-04", to = "2023-05-12")R> getSymbols("JPYUSD=X", from = "2014-12-04", to = "2023-05-12")R> SP <- zoo(x = SPX$SPX.Close, order.by = index(SPX$SPX.Close))R> Vix <- zoo(x = VIX$VIX.Close/1000, order.by = index(VIX$VIX.Close))R> EURUSD <- zoo(x = ‘EURUSD=X‘[,4], order.by = index(‘EURUSD=X‘))R> JPYUSD <- zoo(x = ‘JPYUSD=X‘[,4], order.by = index(‘JPYUSD=X‘))R> Data <- na.omit(na.approx(merge(Vix, EURUSD, JPYUSD, SP)))R> colnames(Data) <- c("VIX", "EURUSD", "JPYUSD", "SP")R> days <- as.numeric(index(Data))-as.numeric(index(Data))[1]# equally spaced grid time dataR> Data <- zoo(log(Data), order.by = days)R> Data_eq <- na.approx(Data, xout = days[1] : tail(days,1L))R> yData <- setData(zoo(Data_eq, order.by = index(Data_eq)/30)) # Data on monthly basis We decided to work with log-price (see Data variable in the above code) to have quantities defined on the same support of a Student- Lévy process, i.e.: the real line. Since the estimation method in YUIMA requires that the data are observed on an equally spaced grid time, we interpolate linearly to estimate possible missing data to get a log price for each day. Figure 7 shows the trajectory for each financial series.

To estimate the model we perform the same steps discussed in the previous examples and we report below the code for reproducing our result.

# Inputs for integration in the inversion formulaR> method_Fourier <- "FFT"; up <- 6; low <- -6; N <- 10000; N_grid <- 60000# Model DefinitionR> law <- setLaw_th(method = method_Fourier, up = up, low = low, N = N,+ N_grid = N_grid)R> regr <- setModel(drift = c("0", "0", "0"), diffusion = matrix("0",3,1),+ solve.variable = c("VIX", "EURUSD", "JPYUSD"), xinit = c(0,0,0))Mod <- setLRM(unit_Levy = law, yuima_regressors = regr, LevyRM = "SP")# EstimationR> lower <- list(mu1 = -100, mu2 = -200, mu3 = -100, sigma0 = 0.01)R> upper <- list(mu1 = 100, mu2 = 100, mu3 = 100, sigma0 = 200.01)R> start <- list(mu1 = runif(1, -100, 100), mu2 = runif(1, -100, 100),+ mu3 = runif(1, -100, 100), sigma0 = runif(1, 0.01, 100))R> est <- estimation_LRM(start = start, model = Mod, data = yData, upper = upper,+ lower = lower, PT = floor(tail(index(Data_eq)/30,1L)/2))R> summary(est)

Quasi-Maximum likelihood estimationCall:estimation_LRM(start = start, model = Mod, data = yData, upper = upper, lower = lower, PT = floor(tail(index(Data_eq)/30, 1L)/2))Coefficients: Estimate Std. Errormu1 0.000335328 0.004901559mu2 -0.062235188 0.033027232mu3 0.016291220 0.039382559sigma0 0.082031691 0.004859138nu 3.062728822 0.616466913-2 log L: -1506.067 48.17592

5. Conclusion

In this paper, we have presented classes and methods for a -Lévy regression model. In particular, the simulation and the estimation algorithm have been introduced from a computational point of view. Moreover three different algorithms have been developed for computing the density, the cumulative distribution and the quantile functions and the random number generator of the -Lévy increments defined over a non-unitary interval. These latter methods can be also used in any stochastic model available in YUIMA for the definition of the underlying noise.

Based on our simulated data, for the estimation of the degrees of freedom the Laguarre method seems to be more accurate. However, due to the restriction on the number of roots used in the evaluation of the integral, we notice a bias on the estimation of the scale parameter. Such bias seems to be observable also in the other implemented methods when the same number of points is used in the evaluation of the integral for the inversion of the characteristic function. However the COS and the FFT methods, the numerical precision can be improved. In particular, it is possible to ensure that the estimates fall in the asymptotic confidence interval at 95% level even if the estimates of the degrees of freedom in the simplest model (first example) seem to underestimate the true value. As concerns computational time, the FFT methods with a sufficiently large computational precision () and sufficiently small seems to be an acceptable compromise.

Acknowledgment

This work is supported by JST CREST Grant Number JPMJCR2115, Japan and by the MUR-PRIN2022 Grant Number 20225PC98R, Italy CUP codes: H53D23002200006 and G53D23001960006.

References

- [1] S. Asmussen and J. Rosiński. Approximations of small jumps of lévy processes with a view towards simulation. Journal of Applied Probability, 38(2):482–493, 2001.

- [2] O. E. Barndorff-Nielsen. Processes of normal inverse Gaussian type. Finance Stoch., 2(1):41–68, 1998.

- [3] C. Berg and C. Vignat. On some results of cufaro petroni about student t-processes. Journal of Physics A: Mathematical and Theoretical, 41(26):265004, 2008.

- [4] A. Brouste, M. Fukasawa, H. Hino, S. Iacus, K. Kamatani, Y. Koike, H. Masuda, R. Nomura, T. Ogihara, Y. Shimuzu, M. Uchida, and N. Yoshida. The yuima project: A computational framework for simulation and inference of stochastic differential equations. Journal of Statistical Software, 57(4):1-51, 2014.

- [5] L. V. Castro-Porras, R. Rojas-Martínez, C. A. Aguilar-Salinas, O. Y. Bello-Chavolla, C. Becerril-Gutierrez, and C. Escamilla-Nuñez. Trends and age-period-cohort effects on hypertension mortality rates from 1998 to 2018 in mexico. Scientific Reports, 11(1):17553, 2021.

- [6] J. W. Cooley and J. W. Tukey. An algorithm for the machine calculation of complex fourier series. Mathematics of computation, 19(90):297–301, 1965.

- [7] N. Cufaro Petroni. Mixtures in nonstable Lévy processes. J. Phys. A, 40(10):2227–2250, 2007.

- [8] L. Devroye. On the computer generation of random variables with a given characteristic function. Comput. Math. Appl., 7(6):547–552, 1981.

- [9] S. Ditlevsen and A. Samson. Hypoelliptic diffusions: filtering and inference from complete and partial observations. J. R. Stat. Soc. Ser. B. Stat. Methodol., 81(2):361–384, 2019.

- [10] F. Fang and C. W. Oosterlee. A novel pricing method for european options based on fourier-cosine series expansions. SIAM Journal on Scientific Computing, 31(2):826–848, 2009.

- [11] F. Fang and C. W. Oosterlee. A fourier-based valuation method for bermudan and barrier options under heston’s model. SIAM Journal on Financial Mathematics, 2(1):439–463, 2011.

- [12] A. Gloter and N. Yoshida. Adaptive estimation for degenerate diffusion processes. Electron. J. Stat., 15(1):1424–1472, 2021.

- [13] S. Haberman and A. Renshaw. On age-period-cohort parametric mortality rate projections. Insurance: Mathematics and Economics, 45(2):255–270, 2009.

- [14] C. C. Heyde and N. N. Leonenko. Student processes. Adv. in Appl. Probab., 37(2):342–365, 2005.

- [15] F. Hubalek. On simulation from the marginal distribution of a student t and generalized hyperbolic lévy process. 2005.

- [16] S. M. Iacus and N. Yoshida. Simulation and inference for stochastic processes with yuima. A comprehensive R framework for SDEs and other stochastic processes. Use R, 2018.

- [17] J. R. León and A. Samson. Hypoelliptic stochastic FitzHugh-Nagumo neuronal model: mixing, up-crossing and estimation of the spike rate. Ann. Appl. Probab., 28(4):2243–2274, 2018.

- [18] A. Loregian, L. Mercuri, and E. Rroji. Approximation of the variance gamma model with a finite mixture of normals. Statistics & Probability Letters, 82(2):217–224, 2012.

- [19] T. Massing. Simulation of student–lévy processes using series representations. Computational Statistics, 33(4):1649–1685, 2018.

- [20] H. Masuda, L. Mercuri, and Y. Uehara. Noise inference for ergodic Lévy driven SDE. Electronic Journal of Statistics, 16(1):2432 – 2474, 2022.

- [21] H. Masuda, L. Mercuri, and Y. Uehara. Quasi-likelihood analysis for student-lévy regression. arXiv preprint arXiv:2306.16790, 2023.

- [22] L. Mercuri, A. Perchiazzo, and E. Rroji. Finite mixture approximation of carma (p, q) models. SIAM Journal on Financial Mathematics, 12(4):1416–1458, 2021.

- [23] R. Singleton. An algorithm for computing the mixed radix fast fourier transform. IEEE Transactions on audio and electroacoustics, 17(2):93–103, 1969.

- [24] C. Sørensen. Modeling seasonality in agricultural commodity futures. Journal of Futures Markets: Futures, Options, and Other Derivative Products, 22(5):393–426, 2002.

- [25] L. Wu. Large and moderate deviations and exponential convergence for stochastic damping Hamiltonian systems. Stochastic Process. Appl., 91(2):205–238, 2001.