Risk premium and rough volatility

Abstract.

One the one hand, rough volatility has been shown to provide a consistent framework to capture the properties of stock price dynamics both under the historical measure and for pricing purposes. On the other hand, market price of volatility risk is a well-studied object in Financial Economics, and empirical estimates show it to be stochastic rather than deterministic. Starting from a rough volatility model under the historical measure, we take up this challenge and provide an analysis of the impact of such a non-deterministic risk for pricing purposes.

Key words and phrases:

risk premium, fractional Brownian motion, rough volatility2010 Mathematics Subject Classification:

60F17, 60F05, 60G15, 60G22, 91G20, 91G60, 91B25Introduction

Rough volatility is a recent paradigm proposed by Gatheral, Jaisson and Rosenbaum [10], which has attracted the attention of many academics and practitioners thanks to its numerous attractive properties. Despite some debate about whether volatility should be rough [12, 13, 17, 16, 23], this class of models provides a general framework to analyse both time series of the instantaneous volatility (under the historical measure ) and prices of financial derivatives (under the pricing measure ). Starting from a rough version of the Bergomi model [5] under , Bayer, Friz and Gatheral [3] showed that a deterministic market price of risk preserved its structure under (somehow akin to the Heston model [14] specification).

However, the Financial Economics literature has long shown that this market price of risk, monitoring the transition from to via Girsanov’s transform, is not constant nor deterministic but instead stochastic. Its estimation has been the source of long academic discussions, outside the scope of the present paper though, and we refer the interested reader to [1, 6, 7, 8, 19, 21] for some useful pointers. This of course has serious practicals implications for risk management, and [11, 24] are fascinating sources of information. We focus here on this particular bridge between and and show, not surprisingly, that the required stochasticity of the market price of risk unfortunately breaks the structure of the rough Bergomi model under . However, we link the Hölder regularity of the volatility process (lower in this class of rough models) with that of the change of measure, and design several specifications making the model tractable under . While the rough Bergomi model tracks well the behaviour of the historical volatility, it is less powerful for option prices, especially when considering VIX smiles (which are more or less flat under this model). Our new setup allows for more flexibility there, while preserving the -tractability of the model.

Section 1 provides the technical setup and analysis of the market price of risk, while the design of useful continuous-time rough stochastic volatility models with non-deterministic market prices of risk is detailed in Section 2. Finally, in Section 3, we perform an empirical analysis, estimating risk premia from historical options data.

1. Rough volatility models and change of measure

Rough volatility models are a natural extension of classical stochastic volatility models. Starting from such a model under the historical measure , we characterise below its dynamics under equivalent martingale measures , which then, by the fundamental theorem of asset pricing, allows for arbitrage-free option pricing. Following for example [4, 10] we consider a rather general class of (rough) stochastic volatility model under , where the stock price process admits the following dynamics:

| (1.1) |

starting from , over a fixed time interval , for . Here is a two-dimensional standard Brownian motion defined on a given filtered probability space , with , and , with and . We further introduce the set of -bounded and -progressively measurable process and recall the Doléans-Dade stochastic exponential of a square integrable process :

We finally consider the following set of assumptions, in place for the rest of the paper:

Assumption 1.1.

-

(i)

The function is continuous, bounded, and bounded away from the origin on for each ;

-

(ii)

For each , is finite;

-

(iii)

The process belongs to ;

-

(iv)

Given an interest rate process , there exist a sequence and a process in and bounded -almost surely, for each , such that

where we introduce the Sharpe ratio and

(1.2) -

(v)

The correlation is negative: ;

-

(vi)

For each , the kernel is null on and is a well-defined Gaussian process.

Remark 1.2.

Condition (vi) may be replaced in terms of conditions on the kernel, for example for each . In light of (v), the first constraint in (iv) may be rewritten as , , for all .

The following examples are common choices of such kernels:

Example 1.3.

The Gamma kernel, common in the literature pioneered by Barndorff-Nielsen and Schmiegel [2], is given by

| (1.3) |

In order to state the main result, define the Radon-Nikodym derivative, for each ,

| (1.4) |

so that, from (1.2) above, .

Proposition 1.4.

For any satisfying Assumption 1.1(iv), the process is a -local martingale on .

Proof.

Recall that the sum of two local martingale (with respect to the same filtration) is a local martingale whose sequence of stopping times is given by the minimum of the sequences of stopping times for the terms in the sum. The boundedness of implies that is a true -martingale. Regarding , the integrand is -measurable and locally bounded with respect to the sequence of stopping times in (1.2) thanks to Assumption 1.1(i)-(iii)-(iv). Exploiting Assumption 1.1(ii)-(iii)-(iv), then is finite for all . Thus, the first term in the sum is a local martingale as well, and so is the whole sum. ∎

Proposition 1.4 justifies the use of a Doléans-Dade stochastic exponential in the definition of . Furthermore, we obtain the following result.

Theorem 1.5.

Under Assumption 1.1, for any as in Assumption 1.1(iv), then

-

(I)

the Radon-Nikodym derivative process in (1.4) is a true -martingale;

-

(II)

under the (arbitrage-free) equivalent risk-neutral martingale measure ,

(1.5) with , and is the market price of volatility risk defined by

(1.6) and where and are -Brownian motions defined as

(1.7) -

(III)

the discounted stock price with , , is a true -martingale.

Proof.

To satisfy the no-arbitrage conditions, the change of measure for is constrained by the martingale restriction on the discounted spot dynamics, while the Brownian motion gives freedom to the model and makes the market incomplete by the free choice of the process . Consequently, the change of measure from to and the corresponding Radon-Nikodym derivative directly follow from Girsanov’s Theorem via (1.4), provided that and is a true martingale. Thus, once we have shown (I), then (II) automatically follows. By Proposition 1.4, and, being a non-negative local martingale, it is a supermartingale, and a true martingale on if and only if . To prove this, we closely follow [9, Proof of Theorem 1.1] with some modifications, and recall the stopping time from (1.2). For any , the random function is -bounded on for any since and are -bounded, and bounded away from zero on intervals of the form , by Assumption 1.1(iii)-(iv)-(i), respectively. Then, again by Proposition 1.4,

| (1.8) |

The first term in (1.8) converges to as tends to infinity, yielding

Girsanov’s theorem implies , where is defined such that

is a -Brownian motion. Then, under , the process becomes

where and

for , where is a -Brownian motion. Furthermore, by Assumption 1.1(iv), there exists such that -almost surely, and

where . Then, an application of Assumption 1.1(iv), we obtain

| (1.9) |

Inequality (1.9), in turn, implies , for . Finally, since is a -Brownian motion, we obtain

and it follows that is indeed a true martingale and note that . In the sense that the relation (1.7) holds between the and Brownian motions. This concludes the proof of (I) and, as stated in the beginning, the results in (II) then readily follow by direct application of the change of measure theorem.

We now prove (III): the discounted price is a true martingale for . A straightforward application of Itô’s formula yields under

| (1.10) |

Define the stopping time . For any , the random function is bounded -almost surely on by Assumption 1.1(i)-(iii)-(iv), with in (1.6), and by boundedness of , so that, since is a -local martingale:

| (1.11) |

The first term converges to as tends to infinity, hence

| (1.12) |

Girsanov’s Theorem further gives , where is such that

| (1.13) |

is a -Brownian motion. Note that, for , , where and is also a -Brownian motion. We conclude that, if , then and

where , and hence is a true martingale. ∎

Discussion

Under Assumption 1.1, consider , some valid function and kernel , and the constant values and for ensuring Assumption 1.1(iv)., so that Theorem 1.5 applies. In this scenario, a sufficient condition for the change of measure to be well defined is that the physical drift must be smaller than the risk-free rate.

1.1. Characterisation of rough volatility models via Generalised Fractional Operators

It is natural to represent rough volatility models in terms of fractional operators. In this section we present the Generalised Fractional Operators (GFO) and a representation result for rough volatility models in terms of GFO. To do so, let us first present the GFO introduced in [15, Definition 1.1] defined as follows.

Definition 1.6.

For any , and such that , the GFO associated to the kernel applied to is defined as

| (1.14) |

To simplify future notations, we let for . We now introduce a specific setup that will drive the rest of our computations: consider the power-law kernel

| (1.15) |

as well as the set

| (1.16) |

To this particular power-law kernel, the GFO (from Definition 1.6, since ) reads

Denote further

so that the corresponding GFO is precisely . To streamline notations and emphasise nice symmetries, we introduce the notations

| (1.17) |

From the properties of GFO [15, Proposition 1.2], then as soon as .

Corollary 1.7 (GFO representation of rough volatility).

Proof.

The fact that is straightforward by the properties of GFO in [15, Proposition 1.4]. Furthermore, for any and any ,

∎

Note that since , then the risk premium has sample paths with Hölder regularity greater than , regardless of the value of .

2. Modelling the risk premium process: A practical approach

In practice, the process is directly modelled without resorting to a change of measure starting from . We now consider different modelling choices for the risk premium and analyse some of its properties. In spite of the formal derivation of Theorem 1.5, a numerical treatment of the integral is rather intricate. To overcome this issue, Bayer, Friz and Gatheral [3] elegantly came up with the forward variance form of rough volatility in the spirit of Bergomi [5]. We shall restrict ourselves to this functional form (defined in the following proposition) for the reminder of the section. Consider (1.5) with , with and . Then the risk-neutral dynamics in forward variance form read

| (2.1) |

In the remaining of this section, the process will denote a -Brownian motion possibly correlated with and .

2.1. Risk premium driven by Itô diffusion

Generalised Fractional Operators provide a natural framework to model risk premium processes driven by diffusions. The statement below shows the details of such a construction. Recall that the Beta function is defined as , for .

Proposition 2.1.

For and , consider , where and

where and satisfy Yamada-Watanabe conditions [20, Section 5.2, Proposition 2.13] for pathwise uniqueness ensuring that a weak solution exists. Then and

| (2.2) |

Furthermore, if and with , then

| (2.3) | ||||

| (2.4) |

where for , and similarly for .

Proof.

We first prove (2.2), which follows from [15, Proposition 1.2] and the identities highlighted above in Corollary 1.7. Indeed, in view of Corollary 1.7 we only need to show that

Replacing the expression for in the integral and using stochastic Fubini theorem, we obtain

Now, direct computations for the inner integral yields

Therefore

We now move to the proof of the identity (2.3). Exploiting the representation of in this specific case and the measurability and independence properties of the Brownian increments,

Thus we only have to show that

We prove the first identity, the second being analogous. It is a straightforward consequence of the definitions and the properties of Brownian increments:

∎

Remark 2.2.

Since the instantaneous variance in this model is log-Normal, the results in [18, Proposition 3.1] and numerical methods therein still apply for the VIX with minimal changes.

2.2. A risk premium driven by a CIR process

A second natural choice is to consider the Cox-Ingersoll-Ross (CIR) process

| (2.5) |

with . As tempting as this approach might seem, it is not trivial at all to compute the basic quantity here, as the following proposition shows.

Proposition 2.3.

Assume that the Brownian motions and are independent and consider , with defined in (2.5). Then, for any ,

where and satisfies the Riccati equation

for , with boundary condition .

Proof.

By independence of the driving Brownian motions we have, for any ,

where the first expected value is the MGF of a Gaussian random variable, hence

We are now interested in computing the second expectation

where

This is, in spirit, similar to computing a bond price in the CIR model. To do so, define

where . We note that is a semimartingale as is fixed, therefore applying the conditional version of Feynman-Kac’s formula, we obtain

| (2.6) |

where is such that is a solution to the moment generating function. With an ansatz of the type , we have at ,

and the PDE (2.6) becomes, with ,

which further simplifies to

The second term cancels when , and a Riccati equation remains:

with boundary conditions . ∎

Already in the uncorrelated case the computation of becomes very costly, having to solve a PDE for each time . In the correlated case there is no hope to obtain any semi-analytic result since one would need to compute cross terms and there is no tool coming from Itô’s calculus available in that case.

3. Roughly extracting the Risk Premium from the Market

In this section we consider the risk premium process to be deterministic, with the aim of obtaining a formula that links and market observable quantities. The following theorem shows how to infer the risk premium from the market using forecasts under the physical measure and Variance Swap prices in the pricing measure.

Theorem 3.1.

Consider the rough volatility model (1.1) under . If , for all and is deterministic, then

| (3.1) |

Proof.

If almost surely, the Radon-Nikodym derivative (1.4) in Theorem 1.5 reads

| (3.2) |

where we recall , and the inverse Radon-Nikodym derivative is given by

| (3.3) |

Then, the conditional change of measure formula yields

| (3.4) |

On the one hand, by the properties of the stochastic exponential and Gaussian moment generating functions. On the other hand, since, for , and is deterministic, then

| (3.5) | ||||

| (3.6) |

where the second factor in the last term is just the conditional moment generating function of a Gaussian random variable. Applying Itô’s isometry then, conditionally on , the random variable is distributed as with

since . Exploiting the identities above and reordering terms,

| (3.7) | ||||

by using the decomposition of as the sum of three terms, and so

| (3.8) |

Finally, going back to (3.4) and exploiting the identity in (3.8), the result follows from

| (3.9) |

∎

3.1. Estimating the risk premium in rough Bergomi

In this section we work with the rough Bergomi model under and its -version:

Assuming deterministic, Theorem 3.1 gives an explicit procedure to compute the risk premium. In practice however, we are only able to observe variance swap quotes in discrete times, and hence it is natural to consider piecewise constant.

Assumption 3.2.

The deterministic process admits the following piecewise constant representation on the time partition , namely for :

| (3.10) |

Similarly the forward variance admits the following piecewise constant representation with for , where and is a market variance swap quote.

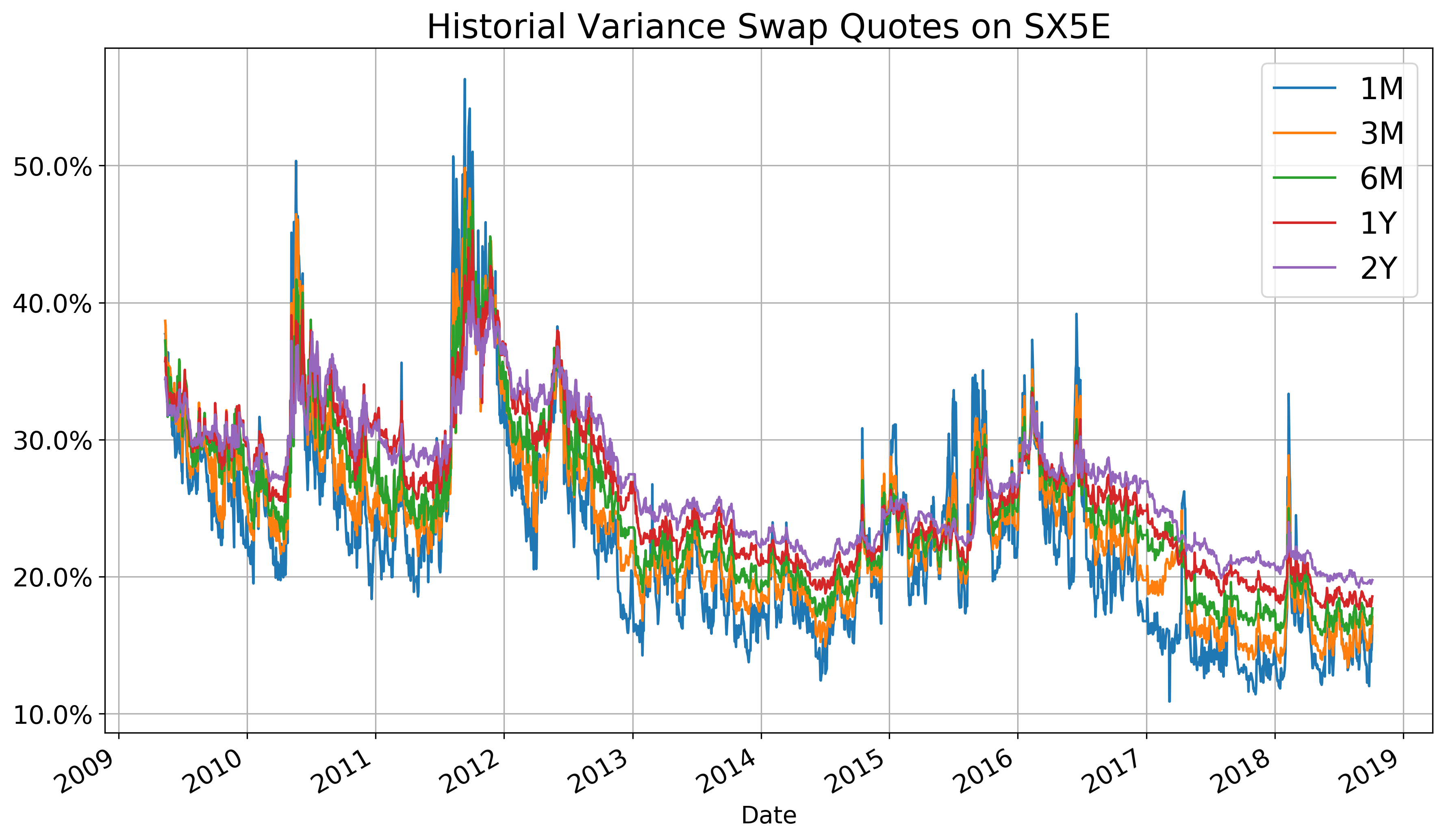

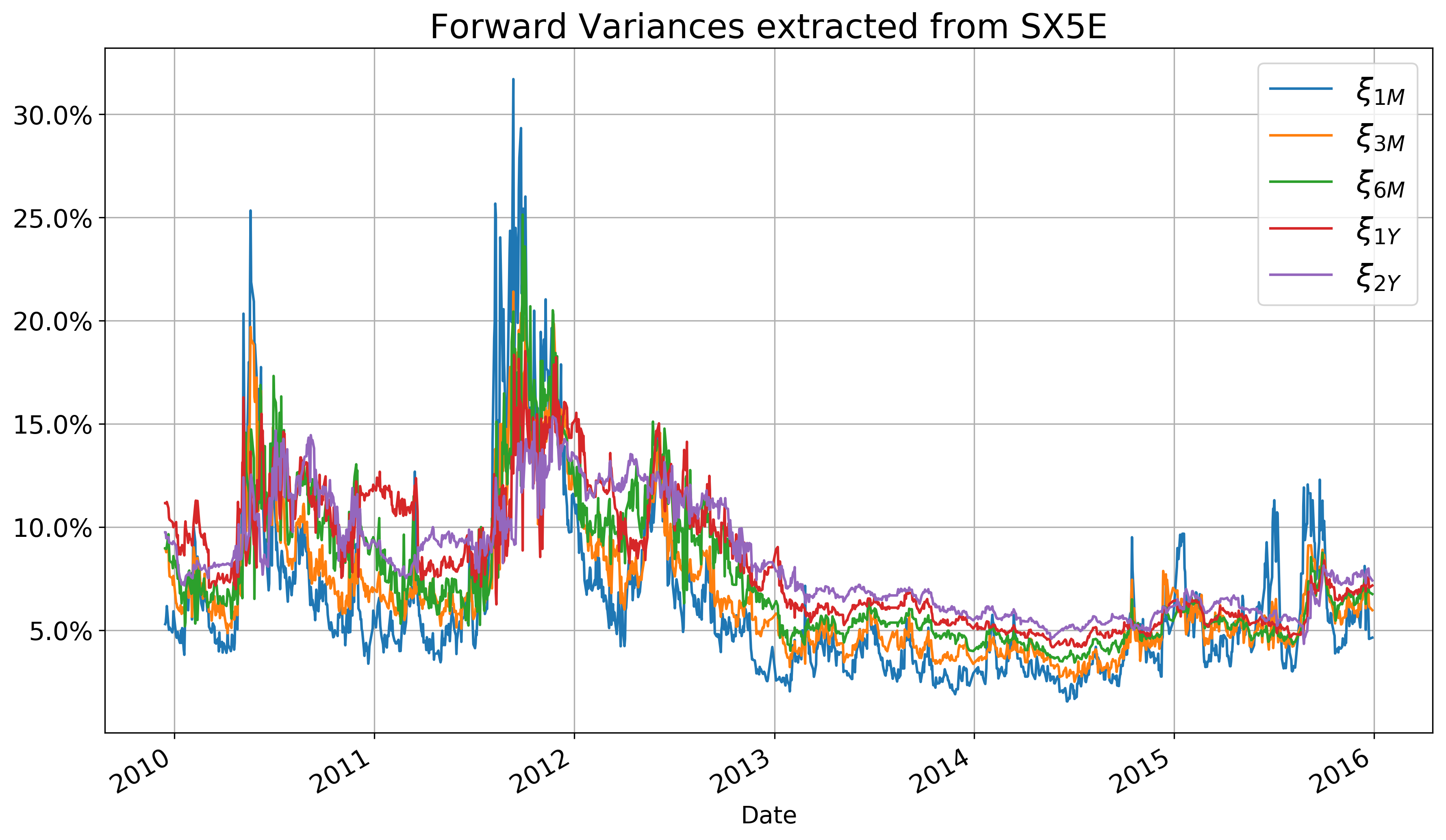

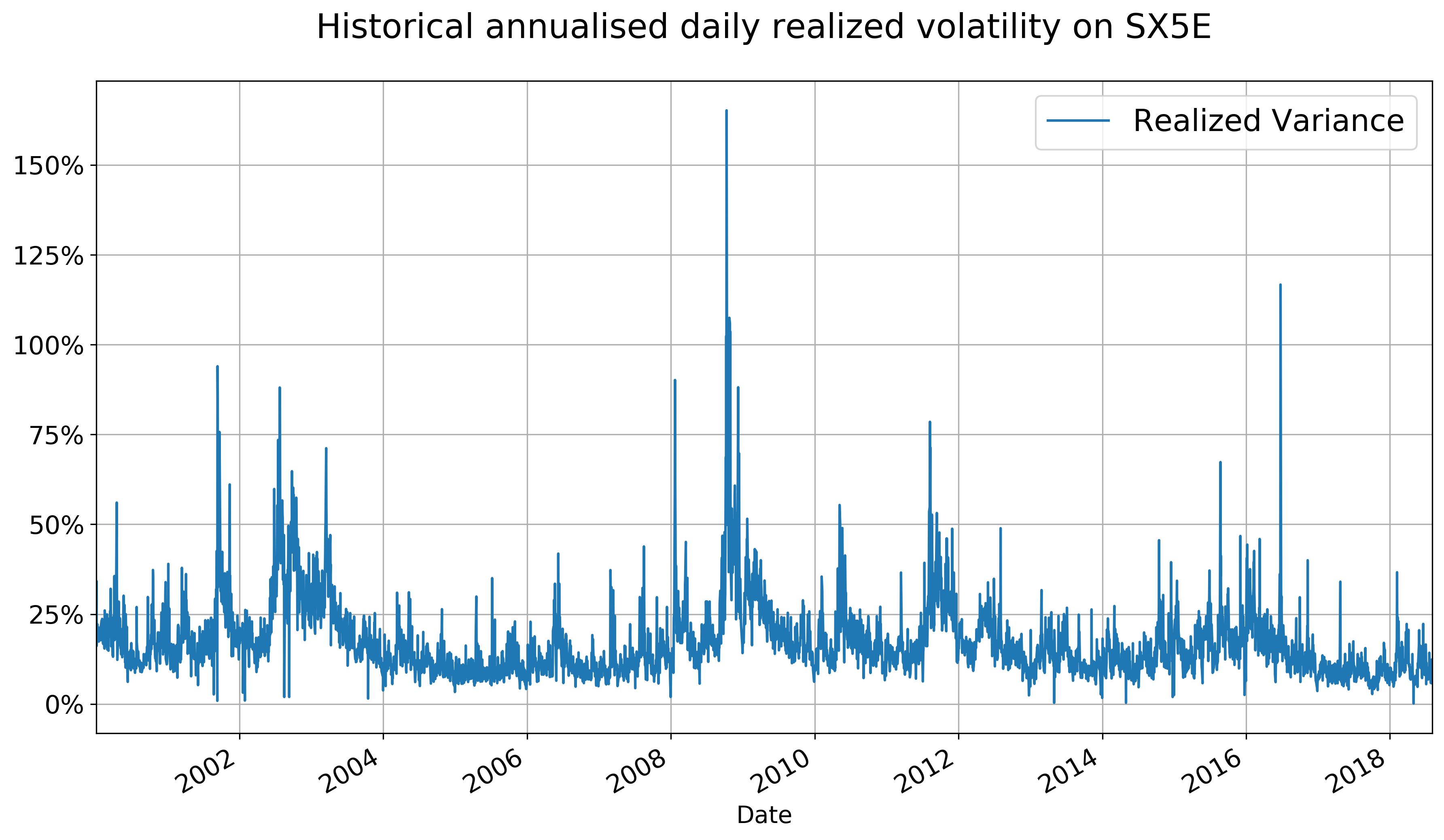

We now estimate . The dataset consists of daily Eurostoxx variance swap quotes for maturities (Figures 1 and 2), while Figure 3 shows the daily realised volatility obtained from Oxford-Man institute data.

In order to apply formula (3.1) we need the following ingredients:

| (3.11) |

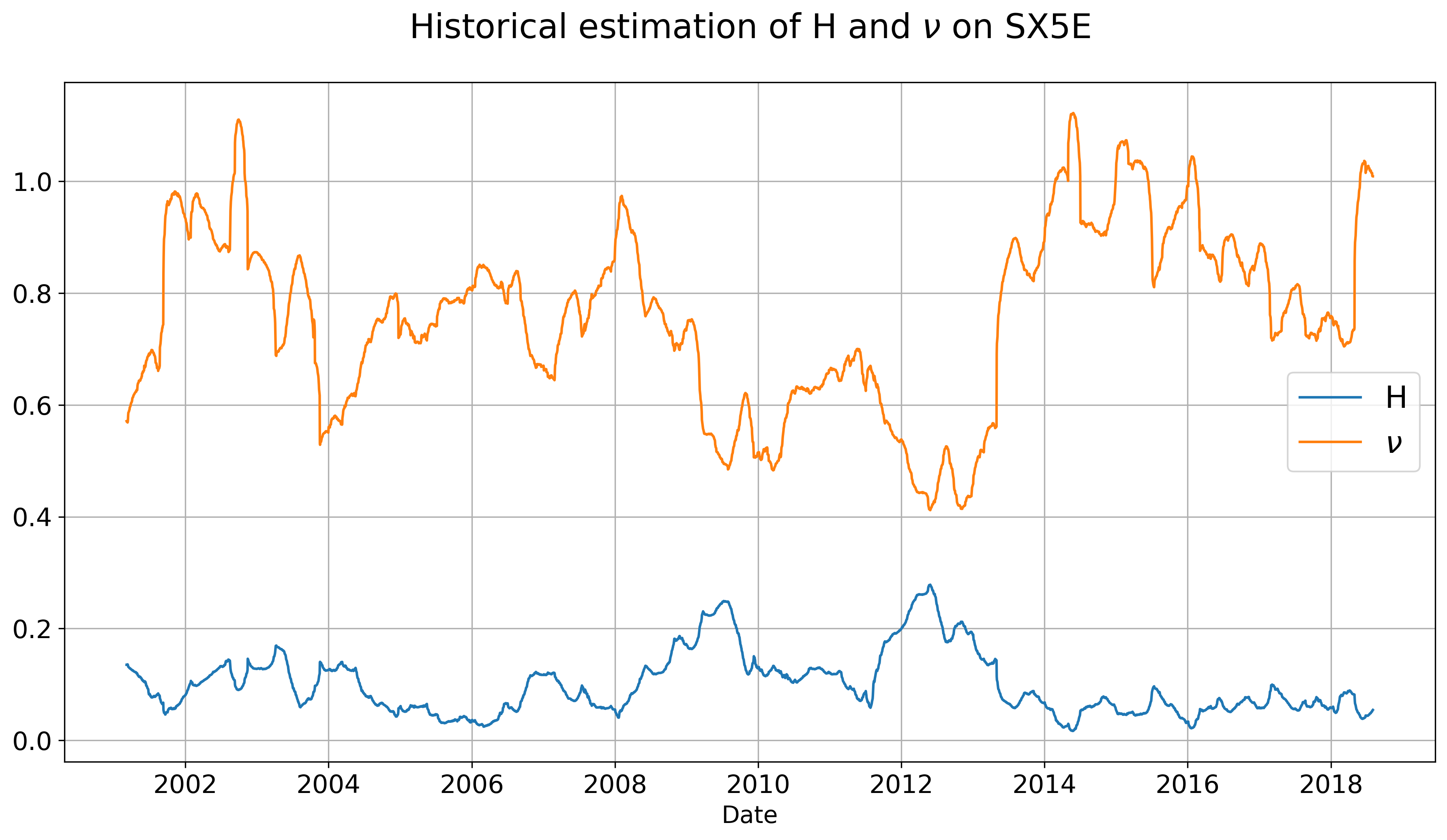

So far we have obtained from Variance Swap market quotes. The next step is to estimate using historical time-series. Gatheral, Jaisson and Rosenbaum [10], explain how to estimate and from daily volatility data (Figure 3), and we follow their approach using a 100-day rolling window (Figure 4) and refer the reader to the original paper for details.

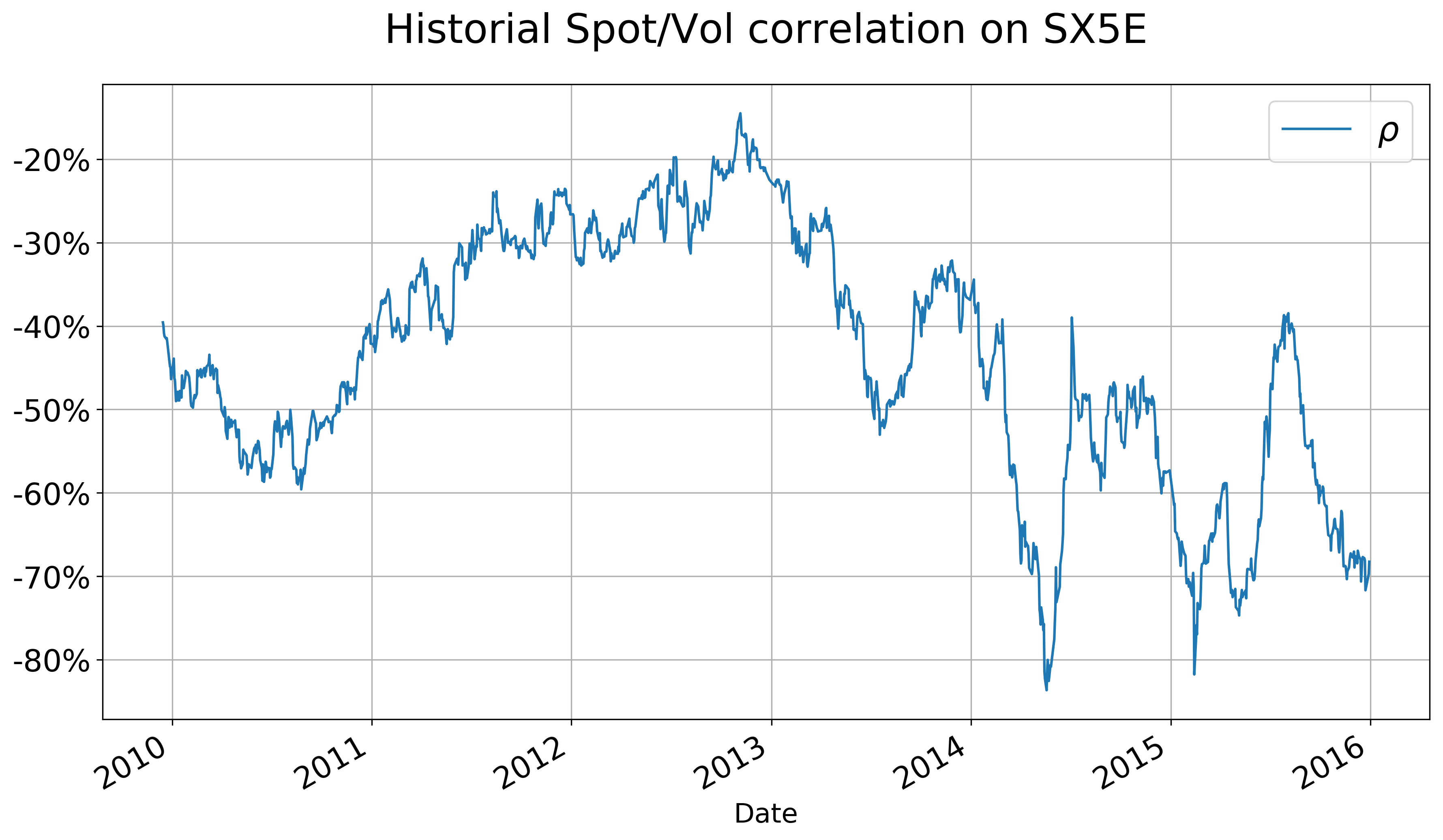

In order to estimate the correlation parameter we use the formula

| (3.12) |

which allows us to estimate the correlation with the proxy

| (3.13) |

Figure 5 below displays the historical estimates using a estimation window of 100 days.

To forecast volatility and obtain , we proceed as in [10] and use the forecasting formula for the fractional Brownian motion due to Nuzman and Poor [22]:

| (3.14) |

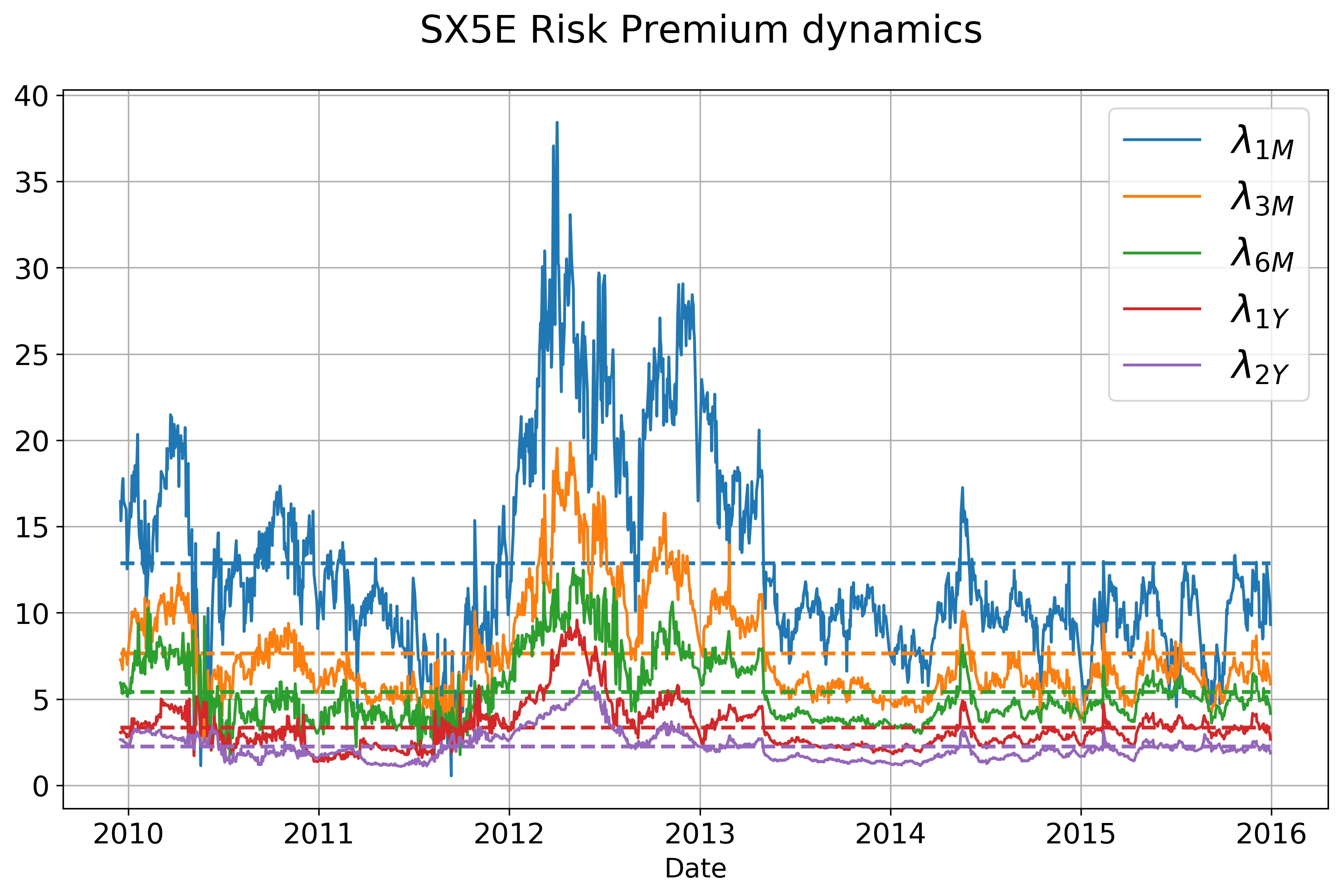

Finally, we orderly estimate for each using Theorem 3.1 and the piecewise constant assumption (3.10), as

| (3.15) |

Figure 6 shows the historical evolution of the risk premium process.

References

- [1] R. Bansal and C. Lundblad, Market efficiency, asset returns, and the size of the risk premium in global equity markets, Journal of Econometrics, 109 (2002), pp. 195–237.

- [2] O. E. Barndorff-Nielsen and J. Schmiegel, Brownian semistationary processes and volatility/intermittency, Advanced Financial Modelling, 8 (2009), pp. 1–25.

- [3] C. Bayer, P. Friz, and J. Gatheral, Pricing under rough volatility, Quantitative Finance, 16 (2016), pp. 887–904.

- [4] M. Bennedsen, A. Lunde, and M. S. Pakkanen, Decoupling the short-and long-term behavior of stochastic volatility, Journal of Financial Econometrics, 20 (2022), pp. 961–1006.

- [5] L. Bergomi, Smile dynamics II, Risk Magazine, October (2005).

- [6] P. Carr and L. Wu, Analyzing volatility risk and risk premium in option contracts: A new theory, Journal of Financial Economics, 120 (2016), pp. 1–20.

- [7] F. Chabi-Yo, Pricing kernels with stochastic skewness and volatility risk, Management Science, 58 (2012), pp. 624–640.

- [8] J.-C. Duan and W. Zhang, Forward-looking market risk premium, Management Science, 60 (2014), pp. 521–538.

- [9] P. Gassiat, On the martingale property in the rough Bergomi model, Electronic Communications in Probability, 24 (2019), pp. 1–9.

- [10] J. Gatheral, T. Jaisson, and M. Rosenbaum, Volatility is rough, Quantitative Finance, 18 (2018), pp. 933–949.

- [11] J. R. Graham and C. R. Harvey, The long-run equity risk premium, Finance Research Letters, 2 (2005), pp. 185–194.

- [12] J. Guyon and M. El Amrani, Does the term-structure of equity at-the-money skew really follow a power law?, SSRN:4174538, (2022).

- [13] J. Guyon and J. Lekeufack, Volatility is (mostly) path-dependent, Quantitative Finance, 23 (2023), pp. 1221–1258.

- [14] S. L. Heston, A closed-form solution for options with stochastic volatility with applications to bond and currency options, The Review of Financial Studies, 6 (1993), pp. 327–343.

- [15] B. Horvath, A. Jacquier, A. Muguruza, and A. Sojmark, Functional central limit theorems for rough volatility, Finance and Stochastics, to appear, (2024).

- [16] E. A. Jaber, C. Illand, and S. Li, The quintic Ornstein-Uhlenbeck volatility model that jointly calibrates SPX & VIX smiles, arXiv:2212.10917, (2022).

- [17] E. A. Jaber and S. Li, Volatility models in practice: Rough, path-dependent or Markovian?, arXiv:2401.03345, (2024).

- [18] A. Jacquier, C. Martini, and A. Muguruza, On VIX Futures in the rough Bergomi model, Quantitative Finance, 18 (2018), pp. 45–61.

- [19] H. Kaido and H. White, Inference on risk-neutral measures for incomplete markets, Journal of Financial Econometrics, 7 (2009), pp. 199–246.

- [20] I. Karatzas and S. Shreve, Brownian motion and stochastic calculus, vol. 113, Springer, 2012.

- [21] R. McDonald and D. Siegel, Option pricing when the underlying asset earns a below-equilibrium rate of return: A note, The Journal of Finance, 39 (1984), pp. 261–265.

- [22] C. J. Nuzman and H. V. Poor, Linear estimation of self-similar processes via Lamperti’s transformation, Journal of Applied Probability, 37 (2000), pp. 429–452.

- [23] S. E. Rømer, Empirical analysis of rough and classical stochastic volatility models to the SPX and VIX markets, Quantitative Finance, 22 (2022), pp. 1805–1838.

- [24] C. Smithson and B. J. Simkins, Does risk management add value? A survey of the evidence, Journal of Applied corporate finance, 17 (2005), pp. 8–17.