Nadav Merlis

\addrFairPlay Joint Team, CREST, ENSAE Paris

and \NameDorian Baudry

\addrFairPlay Joint Team, CREST, ENSAE Paris

Institut Polytechnique de Paris and \NameVianney Perchet

\addrFairPlay Joint Team, CREST, ENSAE Paris

Criteo AI Lab

The Value of Reward Lookahead in Reinforcement Learning

Abstract

In reinforcement learning (RL), agents sequentially interact with changing environments while aiming to maximize the obtained rewards. Usually, rewards are observed only after acting, and so the goal is to maximize the expected cumulative reward. Yet, in many practical settings, reward information is observed in advance – prices are observed before performing transactions; nearby traffic information is partially known; and goals are oftentimes given to agents prior to the interaction. In this work, we aim to quantifiably analyze the value of such future reward information through the lens of competitive analysis. In particular, we measure the ratio between the value of standard RL agents and that of agents with partial future-reward lookahead. We characterize the worst-case reward distribution and derive exact ratios for the worst-case reward expectations. Surprisingly, the resulting ratios relate to known quantities in offline RL and reward-free exploration. We further provide tight bounds for the ratio given the worst-case dynamics. Our results cover the full spectrum between observing the immediate rewards before acting to observing all the rewards before the interaction starts.

keywords:

Reinforcement Learning, Reward Lookahead, Competitive Ratio1 Introduction

Reinforcement Learning (RL, Sutton and Barto, 2018) is the problem of learning how to interact with a changing environment. The setting usually consists of two major elements: a transition kernel, which governs how the state of the environment evolves due to the actions of an agent, and a reward given to the agent for performing an action at a given environment state. Agents must decide which actions to perform in order to collect as much reward as possible, taking into account not only the immediate reward gain, but also the long-term effects of actions on the state dynamics.

In the standard RL framework, reward information is usually observed after playing an action, and agents only aim to maximize their cumulative expected reward, also known as the value (Jaksch et al., 2010; Azar et al., 2017; Jin et al., 2018; Dann et al., 2019; Zanette and Brunskill, 2019; Efroni et al., 2019b; Simchowitz and Jamieson, 2019; Zhang et al., 2021). Yet, in many real-world scenarios, partial information about the future reward is accessible in advance. For example, when performing transactions, prices are usually known. In navigation settings, rewards are sometimes associated with traffic, which can be accurately estimated for the near future. In goal-oriented problems (Schaul et al., 2015; Andrychowicz et al., 2017), the location of the goal is oftentimes revealed in advance. This information is completely ignored by agents that maximize the expected reward, even though using this future information on the reward should greatly increase the reward collected by the agent.

As an illustration, consider a driving problem where an agent travels between two locations, aiming to collect as much reward as possible. In one such scenario, rewards are given only when traveling free roads. It would then be reasonable to assume that agents see whether there is traffic before deciding in which way to turn at every intersection (‘one-step lookahead’). In an alternative scenario, the agent participates in ride-sharing and gains a reward when picking up a passenger. In this case, agents gain information on nearby passengers along the path, not necessarily just in the closest intersection (‘multi-step lookahead’). Finally, the destination might be revealed only at the beginning of the interaction, and reward is only gained when reaching it (‘full lookahead’). In all examples, the additional information should be utilized by the agent to increase its collected reward.

In this paper, We analyze the value of future (lookahead) information on the reward that could be obtained by the agent through the lens of competitive analysis. More precisely, we study the competitive ratio (CR) between the value of an agent that only has access to reward distributions and that of a lookahead agent who sees the actual reward realizations for several future timesteps before choosing each action. Our contributions are the following: (i) Given an environment and its expected rewards, we characterize the distribution that maximizes the value of lookahead agents, for all ranges of lookahead from one step to full lookahead; this distribution therefore minimizes the CR. (ii) We derive the worst-case CR as a function of the dynamics of the environment (that is, for the worst-case reward expectations). Surprisingly, the CR that emerges is closely related to fundamental quantities in reward-free exploration and offline RL (Xie et al., 2022; Al-Marjani et al., 2023). (iii) We analyze the CR for the worst-possible environment. In particular, tree-like environments that require deciding both when and where to navigate exhibit near-worst-case CR. (iv) Lastly, we complement these results by presenting different environments and their CR, providing more intuition to our results.

1.1 Related Work

The idea of utilizing lookahead information to update the played policy is related to a control concept called Model Predictive control (MPC, Camacho et al., 2007), also known as receding horizon control. In complex control problems, it could be challenging to predict the system behavior in long horizons due to errors in the model or nonlinear dynamics. To mitigate this, MPC designs a control scheme for much shorter horizons, where the model is approximately accurate, oftentimes on a simplified (e.g., linearized) model. Then, to correct the deviations due to modeling errors, MPC continuously updates the controller according to the actual system state. In our context, the localized system estimates could be seen as lookahead information. Similar ideas have also been used for planning in reinforcement learning settings (Tamar et al., 2017; Efroni et al., 2019a, 2020). Yet, these concepts are mainly used to improve planning efficiency and account for nonlinearities/disturbances in the model. In contrast, we focus on new information that is revealed to the agent in the form of future reward realization; to our knowledge, such a model was never studied in the context of MPC.

The special case of one-step lookahead, where immediate rewards are observed before making a decision, has been studied in various problems. Possibly the most famous instance of such a problem is the prophet inequality. There, a set of known distributions is sequentially observed, and agents choose whether to either take a reward and end the interaction or discard it and move to the next distribution (Correa et al., 2019b). This could be formulated as a chain environment with two actions – a rewarding action that moves to an absorbing state and a non-rewarding one that moves forward in the chain. A generalization of the prophet problem to resource allocation over Markov chains was studied in (Jia et al., 2023). To obtain a CR that is independent of the interaction length, the authors allow both the online and offline algorithms to choose their initial state. In both cases (and many other problems), the CR is measured between a one-step lookahead and a full lookahead agent, which observes all rewards in advance. In contrast, we measure the CR between no-lookahead agents and all possible lookaheads, so our results are complementary.

Finally, Garg et al. (2013) studied another related resource allocation model. In their work, the competitive ratio for Markov Decision Processes is measured between an online agent with access to the -future reward distributions and transition probabilities, versus an agent who observes all statistical information in advance. A similar adversarial notion is also presented specifically for resource allocation. In contrast, we assume that the distributions are known to both agents and only the oracle observes reward realizations.

While these research lines demonstrate the applicability of lookahead information, they all focus on different objectives than ours.

2 Preliminaries

2.1 Markov Decision Processes

We work under the episodic tabular reinforcement learning model. The environment is modeled as a Markov Decision Process (MDP), defined by the tuple , where is the state space (), is the action space (), is the horizon, is the transition kernel, is the stochastic reward and is the initial state distribution. At the first timestep, an initial state is generated . Then, at every timestep , given environment state , the agent performs an action , obtains a stochastic reward and transitions to a state with probability . For brevity, we use the notation .

We assume that rewards at different timesteps are independent, but allow them to be arbitrarily correlated between state-actions at the same step. We denote the expected reward by and assume that the rewards are non-negative.111This assumption is standard when the performance is measured by a ratio, since otherwise, ratios are not well-defined. Rewards and transitions are always assumed to be mutually independent, and transitions are independent between rounds. While we focus on non-stationary models, where the reward and transition distributions could depend on the timestep , our analysis techniques could be easily adapted to stationary models, where the distributions are timestep-independent, and all the proofs in the appendix also state the results for stationary models.222In stationary environments, reward expectations have to be identical for all timesteps; this additional constraint affects the results when looking at the worst-case reward expectations.

2.2 Lookahead Policies and Values

We assume w.l.o.g. that all rewards are generated before the interaction starts. We denote by , the set of all rewards at timestep and by , the -lookahead reward information, containing all reward information for -timesteps starting from . By convention, is the empty set. A lookahead policy is defined as follows.

Definition 2.1.

A lookahead policy is a policy that for each timestep , observes the state and the lookahead reward information and generates an action with probability . The set of all lookahead policies is denoted by .

For example, a one-step lookahead policy observes the immediate rewards at the current state before acting, while a full lookahead policy has access to all reward realizations before the interaction starts. When , the policy only depends on the state and is Markovian; we therefore denote .

The goal of any agent is to maximize its cumulative reward, also known as the value, . For brevity, we omit the conditioning on the initial state distribution. The optimal value given a lookahead is . If we want to emphasize that an environment parameter (say, the transition kernel ) is fixed, we shall specify it, e.g., .

We analyze the relation between the ‘standard value’ of an agent that plays optimally using no future information () and a lookahead agent that observes the -future rewards before acting (). Formally, let be the set of all non-negative distributions with rewards expectations . The -lookahead competitive ratio (CR) is defined as

| (1) |

That is, the competitive ratio is the worst-possible multiplicative loss of the standard (no-lookahead) policy, compared to an -lookahead policy, given fixed transition kernel and expected rewards. For ratios to be well-defined, we follow the convention that any division by zero equals .

Remark 2.2.

We emphasize that the reward distributions are known in advance to both the no-lookahead and the -step lookahead agents, in striking contrast to adversarial settings. In the latter, the reward could be arbitrary and is only given to an oracle agent. In particular, any upper bound on will also apply to adversarial settings.

Remark 2.3.

Without lookahead information, and suffice to calculate the optimal value (Sutton and Barto, 2018), so one could also write .

We similarly study the -lookahead CR for the worst-case reward expectations, defined as333While we limit the expectations to , the same results would hold for (see \Crefremark: unbounded expected rewards in the appendix).

Finally, we study the CR for the worst-case environment and initial state distribution , denoted by . In particular, we show that stationary environments achieve near-worst-case CR.

2.3 Occupancy Measures

Occupancy measures are the visitation probabilities of an agent in different state-actions. In particular, for any (potentially lookahead) policy, we define and , where randomness is w.r.t. both transitions, rewards and internal policy randomization, given that actions are generated from the policy . For , the state distribution only depends on the initial state distribution , and we use , and interchangeably. We also define the conditional occupancy measure as for some and similarly use . Intuitively, this is the reaching probability from state at time to a state at time when playing a policy . Without lookahead information, it is well-known that the set of occupancy measures induced by Markovian policies is a convex compact polytope (Altman, 2021), and the value of any Markovian policy could be expressed using occupancies by

| (2) |

Finally, denote the optimal reaching probability to a state as . Notice that rewards and transitions are independent, so reward information does not affect the optimal reaching probability and it is sufficient to look at Markovian policies. Moreover, after reaching a state , an agent could always deterministically choose an action , so . Similarly, we define the optimal conditional reaching probability as , and as the for non-conditional occupancy measures, we have that .

3 Competitiveness Versus Full Lookahead Agents

Before analyzing the CR for the full range of lookahead values, we start by studying the full lookahead case, where all rewards are observed before the interaction starts. This regime is applicable, for example, in goal-oriented problems, where goals are given to the agent before an episode starts (Andrychowicz et al., 2017). Notably, we show a link between the CR for the worst-case reward expectations, , and existing complexity measures in offline RL and reward-free exploration. While the results of this section will later be covered by the more general multi-step lookahead, this case gives valuable insights on the worst-case distributions. Moreover, much of the proof techniques presented in this section will later be used to prove the results for the multi-step lookahead.

When all rewards are observed before the interaction starts, each instantiation of the reward is equivalent to an RL problem with known deterministic rewards. In particular, the optimal policy given the reward is Markovian, and using the value formulation in \Crefeq: value as occupancy, we have

| (3) |

At first glance, this bound seems extremely crude – the agent optimally navigates to each state and collects its expected reward. Yet, at a second glance, it gives a clear intuition on the worst-case distribution; a situation where only one reward is realized in every episode, and a full lookahead agent could optimally navigate to collect it. While we cannot fully enforce a single reward realization (due to the independence of rewards in different timesteps), we can approximate this behavior by focusing on long-shot distributions (Hill and Kertz, 1981).

Definition 3.1.

Rewards have long-shot distributions with parameter and expectation if

independently for all . We also use the notation .

Notice that for any given , long-shot distributions are bounded; thus, long-shot rewards could always be scaled to be supported by without affecting the CR. Moreover, when , with high probability, at most a single reward will be realized, and the bound in \Crefeq: full info value upper bound is achieved in equality as . Formally, the CR versus a full lookahead agent is characterized as follows:

Theorem 3.2.

theorem]theorem:fullInfoCR[CR versus Full Lookahead Agents]

-

1.

Worst-case distributions:

-

2.

Worst-case reward expectations:

-

3.

Worst-case environments: For all environments, . Also, for any there exist stationary environments with rewards over s.t. if for , then , and if , then .

Proof Sketch (see \Crefappendix: proofs full lookahead for the full proof).

Part I.

Recalling \Crefremark:CR for worst-case distribution and \Crefeq: value as occupancy, to prove the first part of the proposition, one only needs to calculate the full lookahead value for the worst-case distribution. An upper bound for this value is already given in \Crefeq: full info value upper bound; we directly calculate the value for long-shot distributions and show that this bound is achieved at the limit of .

Part II.

The proof of the second part of the theorem utilizes the previously calculated to optimize for the worst-case expectations. This is done using the minimax theorem, exchanging the reward minimization and the policy maximization. To make the internal maximization problem concave, we move from the space of Markovian policies to the set of occupancy measures induced by Markovian policies, which is convex (Altman, 2021). To make the reward minimization convex, we show that the denominator can be converted to the constraint . Then, the minimax theorem can be applied, and we explicitly solve the resulting optimization problem. The formal application of the minimax theorem and its solution is done in \Creflemma: minmax for CR in the appendix.

Part III.

The proof of the final statement is further divided into two parts.

Lower bounding . The lower bound is inductively achieved from the dynamic programming equations for both the no-lookahead and full lookahead values. The bound is obtained by choosing a specific policy and substituting in : the Markovian policy whose occupancy is , where is a policy that maximizes the reaching probability to .

Upper bounding – designing a worst-case environment. We show that a modified tree graph achieves a near-worst-case competitive ratio. In tree-based MDPs, each state represents a node in a tree, with the initial state as its root, and actions take the agent downwards through the tree. In our example, rewards are long-shots located at the leaves of such trees. However, this structure, by itself, does not lead to the worst-case bound. Intuitively, a standard RL agent would navigate to the leaf with the maximal expected reward, while an agent with a full lookahead would navigate to the leaf with the highest reward realization. Since there are at most leaves with actions in each, this would lead to . This is improved by a simple modification: at the root of the tree, we allocate one action to ‘delay’ the entrance to the tree and stay in the root (as illustrated in \Creffigure:lower-bound-tree-mdp in the appendix). While agents without lookahead have no incentive to use this action, a full lookahead agent could predict when a reward will be realized and enter the tree at a timing that allows its collection. When is large enough (compared to the tree depth), this allows the full lookahead agent to have approximately attempts to collect a reward and lead to the additional -factor (up to log factors). The proof could be extended to any value of by allowing the tree to be incomplete – we refer the readers to the remark at the end of \Crefprop: worst case env example in the appendix for more details. \jmlrQED

Surprisingly, the CR for the worst-case reward expectation is the inverse of a concentrability coefficient that appears in many different RL settings, called the coverability coefficient. In particular, it affects the learning complexity in both online and offline RL settings, where agents must learn to act optimally either based on logged date or interaction with the environment (Xie et al., 2022).444A subtle difference between the coefficients is whether the outer maximum is over all valid Markovian occupancy measures or all possible state-action distributions; see (Al-Marjani et al., 2023, Section 2.3) for further discussion. It also has a central role in reward-free exploration, where agents aim to learn the environment so that they can perform well for any given reward function (Al-Marjani et al., 2023). We emphasize that the lookahead setting is fundamentally different – we assume that all agents have exact information on both the dynamics and reward distributions and ask about the multiplicative performance improvement due to additional knowledge on reward realization. In contrast, in learning settings, the main complexity is usually in learning the dynamics, and the rewards are oftentimes assumed to be deterministic. Moreover, the analyzed quantities are either regret measures or sample complexity, which cannot be directly linked to the competitive ratio.

The last part of \Creftheorem:fullInfoCR shows that tree-like environments with a delaying action at their root exhibit worst-case CR. Similar delay mechanisms were previously used to prove regret and PAC lower bounds for nonstationary MDPs (Domingues et al., 2021; Tirinzoni et al., 2022), though with a major difference – in previous works, a nonstationary reward distribution is used to force the agent to learn when to traverse the tree and where to navigate, and the reward is time-extended (obtained for rounds). In contrast, our formulation is fully stationary and a reward can only be collected once. Still, the lookahead agent can use the delay to linearly increase the reward-collection probability, without any need to create time-extended rewards.

4 Competitiveness Versus Multi-Step Lookahead Agents

We now generalize the results of \Crefsection:full lookahead and analyze the competitive ratio compared to -lookahead agents, for any possible lookahead range . We also give special attention to the case of one-step lookahead, where the immediate rewards are revealed before taking an action.

Inspired by the full lookahead case, we focus on long-shot rewards. For such rewards, an agent would expect to see no more than a single reward during an episode, which would only be discovered -steps in advance. As such, a reasonable strategy would play a Markovian policy that maintains a ‘favorable’ state distribution, such that whenever and wherever a future reward is realized, the agent could optimally navigate to it. Letting be the time step where the -step rewards are revealed to an -lookahead agent, this corresponds with the following worst-case value:

Proposition 4.1

For any , let . Then, it holds that

The proof can be found at \Crefappendix: proofs multi-step. It is comprised of calculating the value of long-shot rewards at the limit when and then showing that the same quantity also serves as an upper bound of the value for all reward distributions.

For full lookahead, we have , and becomes the initial state distribution . This leads to the same value as in \Crefeq: full info value upper bound. The second extremity is when and . Then, the conditional occupancy is and we get the simplified expression

| (4) |

Notably, this is the value of an agent that collects the rewards of all the actions in visited states (regardless of the action it actually played) but has no lookahead information.

Recalling \Crefremark:CR for worst-case distribution, one could use \Crefprop: multi-step value to directly calculate . This, in turn, allows analyzing the worst-case reward expectations and environment, as stated in the following:

Theorem 4.2.

theorem]theorem:multistepCR[CR versus Multi-Step Lookahead Agents]

For any , let . Then, it holds that

-

1.

Worst-case distributions:

-

2.

Worst-case reward expectations:

-

3.

Worst-case environments: For all environments, . Also, for any there exist stationary environments with rewards over s.t. if for , then , and if , then .

Proof Sketch (see \Crefappendix: proofs multi-step for the full proof). The first part of the theorem is a direct result of \Crefprop: multi-step value and \Crefremark:CR for worst-case distribution. For the second part, we first rewrite

and as in the full lookahead case, we apply the minimax theorem using \Creflemma: minmax for CR. However, direct application would require calculating the infimum over , and not a minimum. Thus, compared to the full lookahead, we also need to prove that the minimum is obtained in this set. We do so in \Creflemma: min-inf for CR, relying on the set of occupancy measures being a convex compact polytope.

In the last part, we use the same tree example to upper bound . The lower bound is proven using a reduction from the full lookahead bound. In particular, the bound of trivially holds from the full lookahead case. For the second lower bound, we devise a Markovian policy such that for the appropriate choice of reward functions , we prove that

Each of the terms is the competitive ratio versus a full lookahead agent with horizon that starts acting at . Hence, by \Creftheorem:fullInfoCR, all terms are bounded by . To elaborate, the reward limits the reward only to the new timesteps the lookahead agent gets to observe when it reaches step . The policy is a mixture (in the occupancy space) of policies that start by playing the Markovian policy that maximizes the value of \Crefprop: multi-step value, up to timestep , and then maximizes . \jmlrQED \Creftheorem:multistepCR extends the full lookahead results of \Creftheorem:fullInfoCR and tightly characterizes the CR for the full spectrum of lookaheads, both as a function of the environment and for the worst-case environments. Notice that even though lookahead policies are highly non-Markovian, all bounds are expressed using Markovian policies.

One-step lookahead.

In the case where the immediate reward is observed before acting, \Creftheorem:multistepCR proves that even for the worst-case environment, , namely, independent of the size of the state-space. Moreover, for any transition kernel , the CR is given by

| (5) |

While the coverability coefficient of requires a policy to cover all states simultaneously in proportion to their optimal reaching probability, provides a weaker coverability notion; it requires being able to cover any pre-known state-distribution induced by a Markov policy . We emphasize that must cover this distribution using all actions, so imitating the behavior of might be challenging – with a ratio of as the worst case.

Thus, could be seen as an intermediate point between the coverability coefficient and single-policy coverability (Xie et al., 2022), defined by the ratio between the state-action occupancy of the optimal policy and a single data distribution. Yet, Xie et al. (2022) argue that this notion is too weak to allow any guarantees. It is of interest to investigate whether our refined notion, which requires covering all valid state distributions, mitigates the issues they present and allows deriving meaningful results in offline and online RL.

In general, one could interpret the ratios as a class of decreasing555The sequence is decreasing by definition because increasing the lookahead only extends the policy class. (inverse) concentrability coefficients, starting from the coverability of all pre-known state distributions () and ending with the coverability coefficient (). Thus, it is intriguing to further study the connection of these values to other domains in which concentrability naturally arises.

5 Examples

We now present several MDP structures and analyze their competitive ratio for various lookaheads.

Disguised contextual bandit (Al-Marjani et al., 2023).

Maybe the most basic scenario is when actions do not affect the transitions, i.e., for all possible . Specifically, the state distribution is independent of the played policy – there exists an occupancy measure such that for all policies, . Thus, it also holds that , and

The last equality holds since . Using the same arguments, one could also obtain this CR for one-step lookahead, so by the monotonicity of the CR in the lookahead, for all . This is to be expected – without control over the dynamics, the best lookahead agents could do is to maximize immediate rewards, and any additional lookahead information is useless. Then, in each state, knowing the realization can only increase the reward by a factor of .

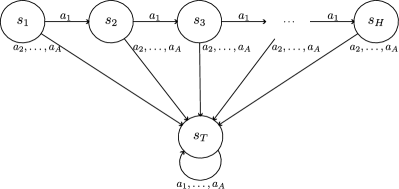

Delayed trees.

This is the example described in the proofs of the main results, also detailed in \Crefprop: worst case env example and depicted in \Creffigure:lower-bound-tree-mdp. In such environments, we get a worst-case CR of . These trees are an extreme case where lookahead information is not only used to collect immediate rewards but rather to navigate to long-term rewards.

Chain MDPs.

We go back to a bandit-like scenario and add limited control on the dynamics, in the form of a chain. The agent starts at the head of the chain (), and at each node of the chain, it could choose to advance to the next node by taking the action or to move to an absorbing terminal state by taking any other action. The environment is depicted in \Creffigure:chain MDP.

figure:examples

\subfigure[Chain MDP: agents start at the head of a chain and can either move forward in the chain or transition to an absorbing terminal state.] \subfigure[Grid MDP: agents start at the bottom-left corner of an grid and can move either up or right, until ending at the top-right corner after steps.]

\subfigure[Grid MDP: agents start at the bottom-left corner of an grid and can move either up or right, until ending at the top-right corner after steps.]

One special problem that falls into this structure is the prophet inequality problem. In particular, assume that reward can only be obtained when moving from the chain to the terminal state (). Thus, at each node of the chain, the agent chooses whether to collect a reward and effectively end the interaction or discard it and move forward in the chain. In other words, the problem becomes an optimal-stopping problem. As such, it is reasonable to allow the agent to see the instantaneous rewards before deciding whether to stop, leading to one-step lookahead agents. This problem has numerous applications, especially in the context of posted-price mechanisms (Correa et al., 2017, 2019a). A classical result is that the CR between one-step lookahead and full lookahead agents is always bounded by (Hill and Kertz, 1981).

Assuming this reward structure with the worst-case reward distribution, the full lookahead agent could reach all rewards and collect them, thus collecting (as in \Crefeq: full info value upper bound). Similarly, a one-step lookahead agent could move forward in the chain using the policy while effectively collecting all rewards and achieving the same value (see \Crefeq: one-step value). In contrast, a no-lookahead agent would have to choose a single reward to collect, obtaining a value of . The resulting CR for this reward structure would be

where the inequality is since there are only rewarding actions, and equality is achieved when all expected rewards are equal. Notably, the reward structure in the prophet problem is near-worst-case; one could verify that for chain MDPs, it holds that . This is due to the second part of \Creftheorem:fullInfoCR, using the following policy: for all chain states , move forward w.p. and play any other action w.p. . At the absorbing state , play uniformly . This simple example provides two important insights.

-

1.

Hardness versus one-step lookahead: chain MDPs exhibit the worst-case CR versus one-step lookahead agents. A central reason is that to move towards rewarding states (forward in the chain), agents must take non-rewarding actions () – there is a tradeoff between gathering instantaneous rewards and moving to future rewarding states.

-

2.

Easiness versus full lookahead: as previously mentioned, the CR between one-step and full lookahead agents is the well-known prophet inequality and is at least ; In other words, for chain MDPs, the information-gain from one-step-to full lookahead is marginal compared to the value of one-step versus no-lookahead. This is mainly because navigating to rewarding states is especially easy in chain MDPs – the agent only has to move forward. In contrast, in environments where navigating to rewarding states is difficult (e.g., the tree environment described in the main results), there is a substantial gain to the full lookahead.

These insights motivate two natural assumptions that reduce the CR.

Dense rewards.

Assume that in all states with non-zero rewards, it holds that . Then, agents could navigate to rewarding future states and still collect rewards, mitigating the issue observed in the chain MDPs. Letting , we have

where is since . Thus, dense rewards remove the horizon dependence in the CR, and for small , we get a similar CR as in the disguised contextual bandit problem.

Ergodic MDPs.

One way to make the navigation task easier is to limit the control of the agent on the state. In (Al-Marjani et al., 2023), the authors suggest looking at MDPs whose transition kernels are near-uniform. Formally, for , they defined the family of transitions

and assumed that for all . As goes to zero, the transition distribution becomes uniform, while at the limit of , this becomes the set of all possible transition kernels. Under this assumption, they prove that the coverability coefficient is bounded by (see the end of the proof of Lemma 38 of Al-Marjani et al. 2023), which implies that . In particular, if for all , , then : independent of the size of the state-space. Finally, in their proof, Al-Marjani et al. 2023 show that for all policies and timesteps. Substituting to \Crefeq: CR one step (and using the uniform policy for ) directly leads to , potentially improving the worst-case environment when .

Grid MDPs

We end this section by analyzing a navigation example, where an agent navigates from one corner of an grid to the opposite corner ("Navigating in Manhattan", also illustrated in \Creffigure:grid-mdp). Due to space limits, we briefly describe the results while fully proving them in \Crefappendix: grid-mdp. This example directly generalizes the chain example with added navigation difficulty; by enforcing zero rewards for all states above the bottom row, we effectively get a chain MDP of horizon . As a direct result, we immediately get that and . Surprisingly, this bound is tight – adding one additional dimension to the problem is just as difficult as a chain. Like chains, some of the difficulty comes from sparsity in the reward, but even when all rewards have unit expectations, we show that . This implies that the problem has additional hardness due to the need for navigation, which is the same order of magnitude as the one due to sparse reward. As a final remark, we show that the ratio between one-step lookahead and full lookahead in grid MDPs is at most . This might be counter-intuitive at first, as the worst-case CR versus either of them is . In fact, this is possible since the worst-case environments are different; when competing with one-step lookahead agent, the hardness comes from reward sparsity, while versus full lookahead, it is also due to navigation issues. The one-step lookahead agent cannot use its information to navigate, so it has the same CR of as the no-lookahead.

6 Conclusions and Future Work

We studied the value of future reward lookahead information in tabular reinforcement learning through the lens of competitive analysis. We characterized the CR for the worst-case distributions, reward expectations and transition kernels for the full range of possible lookahead. We also showed the connection between the resulting CR and concentrability coefficients from the literature of offline and reward-free RL. We find the appearance of the same coefficients in seemingly completely different RL problems intriguing and warrants further study.

While we took the first step in analyzing competitiveness in RL, various other competitive measures could be studied. One natural alternative would be to study transition lookahead, where agents observe future transition realizations. We believe that the results would greatly differ from ours; indeed, even with one-step lookahead, the CR can be exponentially small (as we prove in \Crefappendix: transition lookahead). Another relevant competitivity measure is to compare an agent with predictions of the future rewards to agents with exact lookahead information. This models the realistic scenario where agents get approximate information on future rewards and want to utilize it to improve performance. Finally, as in the prophet problem, one could analyze the CR between multi-step lookahead to full lookahead agents. We leave all these directions for future work.

Finally, we focus on the CR for the worst-case distribution, which allows us to derive the exact value of lookahead agents. However, planning with lookahead for general reward distribution can be challenging. For full lookahead, one can perform standard planning using reward realization, making planning tractable. With one-step lookahead, it is possible to write Bellman equations for the value, but each calculation depends on the full distribution of the reward, making it hard to calculate. For multi-step lookahead, there is no clear way to perform planning without incorporating the future rewards into the state, rendering the planning exponential. While exact planning might be intractable, it could be possible to devise methods for approximate planning, but we leave this for future work.

We thank Simon Mauras and Jose Correa for the helpful discussions. This project has received funding from the European Union’s Horizon 2020 research and innovation programme under the Marie Skłodowska-Curie grant agreement No 101034255. Dorian Baudry thanks the support of ANR-19-CHIA-02 SCAI.

References

- Al-Marjani et al. (2023) Aymen Al-Marjani, Andrea Tirinzoni, and Emilie Kaufmann. Active coverage for pac reinforcement learning. In Proceedings of Thirty Sixth Conference on Learning Theory, volume 195, pages 5044–5109. PMLR, 2023.

- Altman (2021) Eitan Altman. Constrained Markov decision processes. Routledge, 2021.

- Andrychowicz et al. (2017) Marcin Andrychowicz, Filip Wolski, Alex Ray, Jonas Schneider, Rachel Fong, Peter Welinder, Bob McGrew, Josh Tobin, OpenAI Pieter Abbeel, and Wojciech Zaremba. Hindsight experience replay. Advances in neural information processing systems, 30, 2017.

- Azar et al. (2017) Mohammad Gheshlaghi Azar, Ian Osband, and Rémi Munos. Minimax regret bounds for reinforcement learning. In International Conference on Machine Learning, pages 263–272. PMLR, 2017.

- Camacho et al. (2007) Eduardo F Camacho, Carlos Bordons, Eduardo F Camacho, and Carlos Bordons. Model predictive control. Springer, 2007.

- Correa et al. (2017) José Correa, Patricio Foncea, Ruben Hoeksma, Tim Oosterwijk, and Tjark Vredeveld. Posted price mechanisms for a random stream of customers. In Proceedings of the 2017 ACM Conference on Economics and Computation, pages 169–186, 2017.

- Correa et al. (2019a) José Correa, Paul Dütting, Felix Fischer, and Kevin Schewior. Prophet inequalities for iid random variables from an unknown distribution. In Proceedings of the 2019 ACM Conference on Economics and Computation, pages 3–17, 2019a.

- Correa et al. (2019b) Jose Correa, Patricio Foncea, Ruben Hoeksma, Tim Oosterwijk, and Tjark Vredeveld. Recent developments in prophet inequalities. ACM SIGecom Exchanges, 17(1):61–70, 2019b.

- Dann et al. (2019) Christoph Dann, Lihong Li, Wei Wei, and Emma Brunskill. Policy certificates: Towards accountable reinforcement learning. In International Conference on Machine Learning, pages 1507–1516, 2019.

- Domingues et al. (2021) Omar Darwiche Domingues, Pierre Ménard, Emilie Kaufmann, and Michal Valko. Episodic reinforcement learning in finite mdps: Minimax lower bounds revisited. In Algorithmic Learning Theory, pages 578–598. PMLR, 2021.

- Efroni et al. (2019a) Yonathan Efroni, Gal Dalal, Bruno Scherrer, and Shie Mannor. How to combine tree-search methods in reinforcement learning. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 3494–3501, 2019a.

- Efroni et al. (2019b) Yonathan Efroni, Nadav Merlis, Mohammad Ghavamzadeh, and Shie Mannor. Tight regret bounds for model-based reinforcement learning with greedy policies. In Advances in Neural Information Processing Systems, pages 12224–12234, 2019b.

- Efroni et al. (2020) Yonathan Efroni, Mohammad Ghavamzadeh, and Shie Mannor. Online planning with lookahead policies. Advances in Neural Information Processing Systems, 33:14024–14033, 2020.

- Garg et al. (2013) Vikas Garg, TS Jayram, and Balakrishnan Narayanaswamy. Online optimization with dynamic temporal uncertainty: Incorporating short term predictions for renewable integration in intelligent energy systems. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 27, pages 1291–1297, 2013.

- Hill and Kertz (1981) Theodore P Hill and Robert P Kertz. Ratio comparisons of supremum and stop rule expectations. Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete, 56:283–285, 1981.

- Jaksch et al. (2010) Thomas Jaksch, Ronald Ortner, and Peter Auer. Near-optimal regret bounds for reinforcement learning. Journal of Machine Learning Research, 11(Apr):1563–1600, 2010.

- Jia et al. (2023) Jianhao Jia, Hao Li, Kai Liu, Ziqi Liu, Jun Zhou, Nikolai Gravin, and Zhihao Gavin Tang. Online resource allocation in markov chains. In Proceedings of the ACM Web Conference 2023, pages 3498–3507, 2023.

- Jin et al. (2018) Chi Jin, Zeyuan Allen-Zhu, Sebastien Bubeck, and Michael I Jordan. Is q-learning provably efficient? Advances in neural information processing systems, 31, 2018.

- Schaul et al. (2015) Tom Schaul, Daniel Horgan, Karol Gregor, and David Silver. Universal value function approximators. In International conference on machine learning, pages 1312–1320. PMLR, 2015.

- Simchowitz and Jamieson (2019) Max Simchowitz and Kevin G Jamieson. Non-asymptotic gap-dependent regret bounds for tabular mdps. In Advances in Neural Information Processing Systems, pages 1153–1162, 2019.

- Sutton and Barto (2018) Richard S Sutton and Andrew G Barto. Reinforcement learning: An introduction. MIT press, 2018.

- Tamar et al. (2017) Aviv Tamar, Garrett Thomas, Tianhao Zhang, Sergey Levine, and Pieter Abbeel. Learning from the hindsight plan—episodic mpc improvement. In 2017 IEEE International Conference on Robotics and Automation (ICRA), pages 336–343. IEEE, 2017.

- Tirinzoni et al. (2022) Andrea Tirinzoni, Aymen Al Marjani, and Emilie Kaufmann. Near instance-optimal pac reinforcement learning for deterministic mdps. Advances in Neural Information Processing Systems, 35:8785–8798, 2022.

- Xie et al. (2022) Tengyang Xie, Dylan J Foster, Yu Bai, Nan Jiang, and Sham M Kakade. The role of coverage in online reinforcement learning. In The Eleventh International Conference on Learning Representations, 2022.

- Zanette and Brunskill (2019) Andrea Zanette and Emma Brunskill. Tighter problem-dependent regret bounds in reinforcement learning without domain knowledge using value function bounds. In International Conference on Machine Learning, pages 7304–7312. PMLR, 2019.

- Zhang et al. (2021) Zihan Zhang, Xiangyang Ji, and Simon Du. Is reinforcement learning more difficult than bandits? a near-optimal algorithm escaping the curse of horizon. In Conference on Learning Theory, pages 4528–4531. PMLR, 2021.

sectionappendix

Appendix A Proofs for Full Lookahead Agents

Theorem A.1 (CR versus Full Lookahead Agents).

-

1.

Worst-case distributions:

-

2.

Worst-case reward expectations: For non-stationary reward expectations,

If the reward expectations are stationary (), then

-

3.

Worst-case environments: For all environments, . Also, for any there exist stationary environments with rewards over s.t. if for , then , and if , then .

Proof A.2.

Worst-case distribution:

We already saw in \Crefeq: full info value upper bound that for all reward distributions

We now show that for any , there exists a distribution such that

This would imply that

and conclude this part of the proof (by \Crefremark:CR for worst-case distribution and \Crefeq: value as occupancy).

Let and assume long-shot reward distribution . For any , define the event that a positive reward was realized just in :

Under any of these events, the value of the optimal full lookahead agent is

Now, notice that each of these mutually exclusive events occur w.p. , and that the value is non-negative when none of them occur. Hence, for this reward distribution,

| (6) |

Setting leads to the desired bound and concludes this part of the proof.

Worst-case reward expectations:

Before proving the results, we remark on the choice to limit reward expectations to . The main motivation for doing so is the ubiquity of this boundedness assumption in the literature of RL, but in fact, it is only a matter of convention and has no real impact. Indeed, since CR is invariant to scaling, the same result would directly hold for any bounded interval . Furthermore, as explained in \Crefremark: unbounded expected rewards, the result would also hold under the less restrictive assumptions that reward expectations are just non-negative.

We proof both results using \Creflemma: minmax for CR. As a first step, we highlight that the only dependence of the optimization problem in the Markovian policy is through the occupancy measure . Therefore, denoting the set of all occupancy measures induced by a Markovian policy with transition kernel by , the problem can be reformulated as

| (7) |

The set of the possible occupancy measures is convex and compact in (Altman, 2021), so we can apply \Creflemma: minmax for CR with , and , resulting with

where we again used the equivalence between optimizing over Markovian policies and their occupancy measures.

For stationary rewards, where for all , we rewrite \Crefeq: CR worst-expectation full info as

Now, another application of \Creflemma: minmax for CR with , and yields

which is the desired result for stationary environments.

Worst-case environment – lower bound:

We now derive the lower bound . We prove it for nonstationary environments, so in particular, it also holds for stationary ones.

Recall that by definition, for any , is the occupancy measure of a Markovian policy that maximizes the visitation probability in , and let be a Markovian policy that achieves this occupancy. Since the set of occupancy measures induced by Markovian policies is convex (Altman, 2021), there exists a Markovian policy such that its occupancy measure is the average of all these occupancies, namely, for all ,

Using the previous part of the theorem, for all environments , it holds that

In , we discard all the (non-negative) terms in the summation where , while in the following equalities, we use the definition of and the fact that . As this inequality holds for all environments, it also implies that .

To prove that , we take a different approach and go back to the Bellman equations. Denote by , the optimal value of a full lookahead policy, starting from timestep and state , and given reward realization . Therefore, the value of the full lookahead agent is given by . Similarly, denote the standard value with no lookahead information starting from timestep and state by . As previously explained, given reward realizations, the optimal full lookahead policy is Markovian, so both values can be calculated using the following Bellman equations for all and :

We prove by backward induction that for all and , . Specifically, using this relation for and taking the expectation over the initial state distribution would imply that , regardless of the environment, and thus .

As the base of the induction, see that the claim trivially holds for , where all values are . Next, for any and , given that the claim holds for all states in step , we have

where throughout the derivation, we use the fact that all rewards (and thus the values) are non-negative and is due to the induction hypothesis. This concludes the proof of the lower bound in the statement, namely, that for all dynamics and rewards, it holds that .

Worst-case environment – upper bound:

see \Crefprop: worst case env example, where we present a tree-like stationary environment for which the aforementioned bounds are near-tight.

Appendix B Proofs for Multi-Step Lookahead Agents

See 4.1

Proof B.1.

We start by lower-bounding the optimal value in the presence of long-shot rewards. Then, we prove a matching upper value for all rewards and -step lookahead policies

Lower bound on the value of long-shots.

Let and assume that , namely, that for any , a reward of is generated with probability ; otherwise, the reward would be zero. Let be any Markovian policy that does not observe future rewards and let be a policy that plays if all the -step future rewards are zero and otherwise optimally navigates to one strictly positive reward (ties broken arbitrarily). In particular, if only one long-shot reward is realized at , this policy would play until timestep and then maximize the reaching probability from to . If the agent successfully reaches , it will play and collect the reward.

The value of can be lower-bounded by the value that at most one long-shot is realized; Denoting

the event that a reward was realized only in , we bound

In , we use the facts that the events are disjoint and the rewards are non-negative. Next, in , we decompose to steps until , where we play , and steps from to , where we try to maximize reaching probability to at timestep . Notice that the reward is independent of the transition, so the optimal reaching policy is Markovian. Relation replaces the probability notation to conditional occupancy measure and substitutes the probability of the events. Maximizing over and taking the limit of small , we get a lower bound of

Upper bound on the value of all reward distributions.

For any fixed lookahead policy and any reward distribution, we bound

Relation holds since the state dynamics are independent of the rewards realization and the maximal reaching probability is . Relation holds because we reach the state at timestep just before seeing ; therefore, the two variables are independent. Finally, relation holds since we can rewrite the value as

This expression is equivalent to the optimal value of a no-lookahead agent whose expected reward at any is , so there exists a Markovian policy that maximizes this value.

Theorem B.2.

theorem]theorem:multistepCRExtended[CR versus Multi-Step Lookahead Agents] For any , let . Then, it holds that

-

1.

Worst-case distributions:

-

2.

Worst-case reward expectations:

If the reward expectations are stationary (), then

-

3.

Worst-case environments: For all environments, . Also, for any there exist stationary environments with rewards over s.t. if for , then , and if , then .

Proof B.3.

Worst-case distribution:

This part of the theorem is a directly corollary of \Crefprop: multi-step value, applied with \Crefremark:CR for worst-case distribution and \Crefeq: value as occupancy. We remark that we assume w.l.o.g. that for at least one reachable (i.e., ). Otherwise, both values in the numerator and denominator equal zero and the ratio is defined as .

Worst-case reward expectations:

As in the proof of \Creftheorem:fullInfoCRExtended, we start by rewriting the maximization problems in the competitive ratio using, the set of occupancy measures induced by the transition kernel and all Markovian policies:

| (8) |

Continuing following the proof of \Creftheorem:fullInfoCRExtended, we use the convexity and compactness of the set of occupancy measures to apply \Creflemma: minmax for CR on the two internal problems, this time with . Doing so results with

At this point, we deviate from the previous proof and analyze the external optimization problem. In particular, we want to show that the minimum is obtained in the set of Markovian policies. We prove it using \Creflemma: min-inf for CR. For its application, notice that is a convex and compact polytope, and therefore so does its linear transformation , so the conditions of the lemma hold: the infimum is obtained at a minimizer in the set. Substituting it back into and using the equivalence between occupancy measures and policies leads to the desired result:

| (\Creflemma: min-inf for CR) | ||||

For stationary rewards, where , we rewrite \Crefeq: CR worst-expectation multistep as

We can now reapply \Creflemma: minmax for CR with the appropriate , followed by applying \Creflemma: min-inf for CR, to get

| (\Creflemma: minmax for CR ) | ||||

| (\Creflemma: min-inf for CR) |

Worst-case environment – lower bound:

First notice that by definition, any -step lookahead policy is also a full lookahead policy. In particular, for all environments, , and the reverse relation would hold for the CR. Thus, from \Creftheorem:fullInfoCR, we directly get the lower bound . We further proof that using a reduction to the full lookahead case.

To this end, we start by decomposing the no-lookahead value of any as follows

In the last inequality, we decompose the summation into two terms depending on whether or . For brevity, let be such that for all ,

Using this notation, one could rewrite the value as

| (9) |

Notice that are the expected rewards of timesteps observed by the lookahead agent at step . We now define the following set of policies

-

•

A Markovian policy that maximizes the -lookahead value is denoted by

-

•

For any , let be a Markovian policy that plays until reaching some state and then continues by a policy that maximizes the reward function for the following timesteps:

For , the state would be the initial state, generated from the initial state distribution. Notice that starting for the timestep, is an optimal policy given rewards in the standard MDP model, so there exists an optimal Markovian policy that maximizes its value simultaneously for all . By ignoring all but the term in \Crefeq: standard value decomp to lookahead, one could clearly see that

-

•

All aforementioned policies are Markovian, so by the convexity of the occupancies induced by Markovian policies (Altman, 2021), there exists such that for all ,

Since values are linear in the occupancy measure, we can bound the optimal no-lookahead value by

| (10) |

Moving forwards, we use a similar decomposition to the -lookahead value using \Crefprop: multi-step value:

| (11) |

To conclude the reduction, recall the inequality , which holds for all values of s.t. , due to the quasiconcavity of the ratio of linear functions (given the convention that ). Applying this on the CR with the coefficients and using \Crefeq: no-lookahead value multistep decomp,eq: L-lookahead value multistep decomp, we get for all environments that

The last inequality is the reduction to the full lookahead: each of the terms is exactly the CR versus a full lookahead agent with horizon and reward expectations (see \Creftheorem:fullInfoCR, part 1). Thus, each of the terms is lower-bounded by the bound for the worst-case environment given horizon (see \Creftheorem:fullInfoCR, part 3) – by .

Worst-case environment – upper bound:

as in \Creftheorem:multistepCR, this part of the proof is covered in \Crefprop: worst case env example, where we present a tree-like stationary environment with the stated behavior.

Appendix C Analyzing the Competitive Ratio of Specific Environments

C.1 Upper-Bounds for Reward Lookahead – Delayed Trees

Proposition C.1.

For any and any , there exist stationary environments with rewards over s.t. if for , then , and if , then . Moreover, if and , there exists an environment s.t.

Proof C.2.

Assume that for some . We divide the proof into different cases, depending on the values of and .

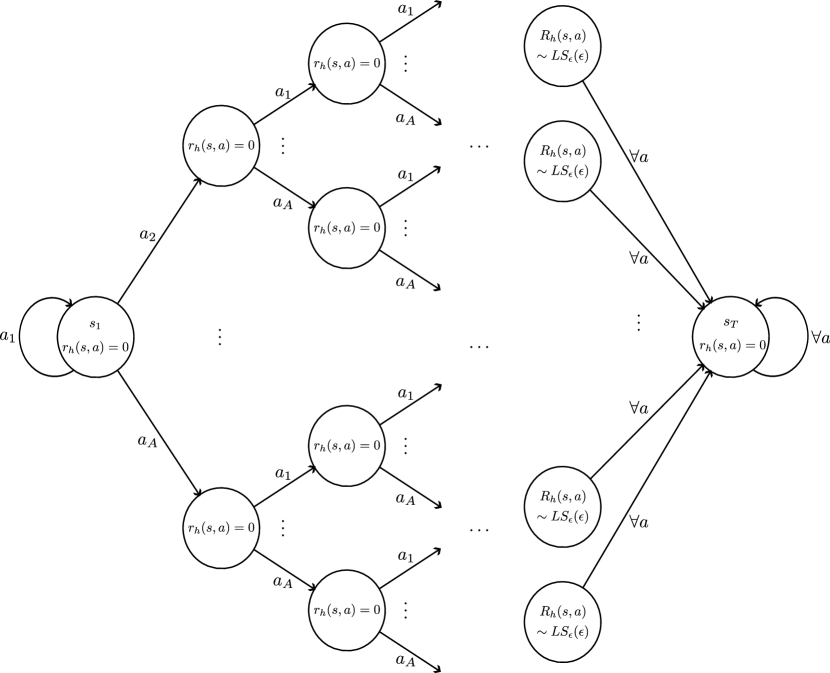

figure:lower-bound-tree-mdp

Case 1:

and . To prove this bound, we design a tree MDP with an additional option to decide when to traverse it, as illustrated in \Creffigure:lower-bound-tree-mdp. In particular, assume that the fixed initial state is the root of a tree of depth such that the root has descendants and all other nodes have descendants. Thus, the number of nodes in this tree is

and the number of leaves is . Assuming that after traversing the tree, the environment moves to a terminal state , this environment could indeed be represented using states. We denote the dynamics of this tree by .

For the dynamics, we allocate one action in the root of the tree that keeps the agent at the root, while the rest of the actions allow traversing through the tree. At the leaves, all actions transition to a terminal state . We emphasize that once an agent has decided to start traversing the tree, it has to continue all the way until the leaves (and terminal state), so the decision when to traverse the tree is taken at its root. Finally, the reward of any action at any leaf is a long-shot , namely Bernoulli-distributed with probability . In particular, this distribution is bounded in .

In this example, any agent with no lookahead information will perform at most one action at a single leaf, independently of the reward realization, thus collecting in expectation no more than the expected reward of a single leaf .

On the other hand, an -lookahead agent could start traversing the tree only when a reward will be realized upon its arrival to the leaf. To reach a leaf at timestep , the agent has to start traversing the tree at timestep . Thus, this agent will wait at the root to see whether a reward is realized in any leaf at timesteps , and only if so, will traverse it.

Since there are leaves with actions each, the probability that no reward is realized in any leaf at these timesteps is , and the optimal lookahead agent would collect an expected reward of at least

where the last inequality is since .

Combining both inequalities, for this environment we have that

In particular, for any , we could fix small enough such that

where we used the relation .

Case 2:

and . This is the case of . We separate it for the clarity of presentation, but the example remains the same: the first state is the initial state and the second is a terminal non-rewarding state. When in , a single action does not change the state but yields no reward, while all other actions transition the environment to state , giving a long-shot reward . As in the first case, without any lookahead information, the agent could collect a reward at most once and obtain in expectation at most .

On the other hand, any lookahead agent would move from to only when a reward is realized. Since there are rewarding actions and opportunities to collect rewards, a lookahead agent could collect at least

where the last inequality is again due to the inequality .

Combining both bounds, we now get

Thus, for any , there exist small enough such that

Case 3:

and . We use the same example as in the first case and , ignoring all extra states. Direct substitution to that bound results with

Case 4:

Finally, if and , we discard the loop at the root and just build a full tree of depth , leading to leaves (with actions each). From the root, the full lookahead agent can reach any leaf with a realized reward, which exists with probability . Following the exact same analysis would now yield for any , concluding the proof.

Modification when :

In this case, we cannot build a complete tree of depth . Instead, we start from the complete tree of depth and use any extra states to create additional leaves of depth . The number of leaves for was . Therefore, of these leaves will have descendants in the new tree, increasing the number of leaves by each, while one additional ‘old’ leaf will take the rest of the states. For this reason, the total number of leaves would be

Recalling that in each leaf, we have possible actions, so rewards could be realized in locations, and increasing the depth by (so that the lookahead agent has one less attempt), we can follow the exact same analysis and get a more general bound of

for any .

C.2 Analysis of Grid MDPs

appendix]appendix: grid-mdp In the grid MDP, an agent starts at the bottom-left corner of an grid and can either move up or right until getting to the top-right corner (‘Manhattan navigation’, see \Creffigure:grid-mdp). After taking one last action, the interaction ends. We denote the states on the column (starting from the left) by (with as the bottom state) and the states on the row (starting from the bottom) by (with as the leftmost state). At the top edge of the grid, the agent must move right, and at the right edge, it must move up. The size of the state space is , the action space is of size (at most) and the horizon is .

This MDP generalizes the chain MDP with , analyzed in \Crefsection: examples; indeed, by setting the reward to be non-zero only when going up from the bottom row (), we effectively get a chain of length and a corresponding CR of . In particular, the reduction immediately leads to an upper bound of for (and ), where the bound for one-step is almost worst-case, since . Interestingly, this is a near-worst-case reward placement also versus full lookahead for the grid-MDP, as we now prove.

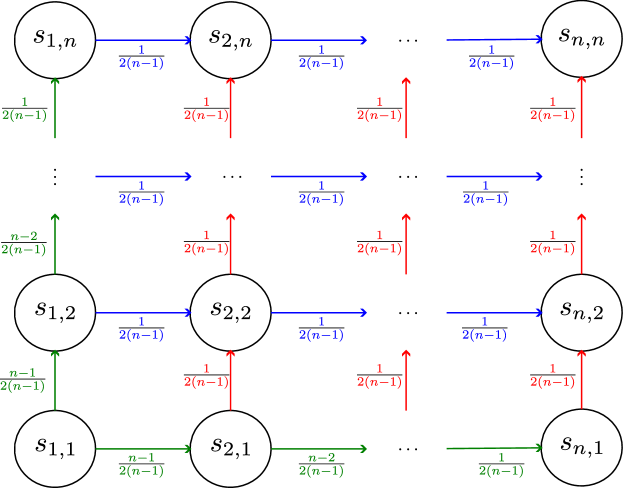

figure:grid-mdp flow

One way to prove this is to analyze a flow on the grid graph, which is equivalent to occupancy in deterministic MDPs. The value of the full lookahead agent corresponds with the maximal possible flow through any edge in the graph, which is the unit flow (). Hence, the goal of the no-lookahead agent is to make sure that there is a minimal flow in all the edges of the graph, and this minimum would be the CR. This could be achieved by distributing a flow on the bottom and leftmost states and sending it in straight lines to the other side of the grid, as explained in \Creffigure:grid-mdp flow. The resulting flow ensures a minimal flow of through all the edges. Even more, looking at the flow description, we could explicitly write the stochastic policy that achieves this flow by looking at the ratio of the flow in each direction:

For this policy, it is easy to prove that the minimal occupancy is lower-bounded by by directly verifying on the edges of the grid (starting from the bottom and left edges and then continuing to the top and right ones), and then proving with a simple induction that strictly inside the grid, . This implies that

In particular, for the grid MDP, the worst-case CR for full lookahead is at most worse by a factor of compared to the CR versus one-step lookahead, similar to the chain MDP. However, in contrast to chains, where the prophet inequality ensures a constant ratio between one-step and full lookahead, in grids, this ratio could depend on . For example, assume long-shot rewards for arbitrarily small . As we already calculated the value for long-shot rewards, we know that one-step lookahead agents effectively collect all expected rewards along their trajectory (\Crefeq: one-step value) – at most rewards – while the full lookahead agents collect all reachable rewards (\Crefeq: full lookahead longshots) – a total of rewards. At first glance, it might be seen as a contradiction, following a logic that

but the careful reader would notice that the CRs are derived for very different reward expectations; one CR is calculated for sparse chain-like rewards while the other is calculated for dense rewards where all expectations are equal.

Dense rewards.

We end this example by analyzing the CR when rewards are dense – all rewards are of unit expectation. Since all reward expectations are equal to , regardless of the policy, the value of all no-lookahead agents would trivially be . For the value of -lookahead agents we use \Crefprop: multi-step value and rewrite the value by decomposing to different values of as follows:

Since the environment is deterministic, all occupancies are binary: one if a state is reachable and zero otherwise. From the initial state, there are reachable states so the first term is equal to . For the second term, we bound the number of reachable states after exactly steps by (all the possible number of ’up’ moves between and ). This yields the bound

and result with a CR of .

This bound is near-tight, again using \Crefprop: multi-step value. For the proof, we focus on a policy that iterates between moving up and right. As previously explained, the number of reachable states when looking steps forward is if we could perform all combinations of moving up and right. In particular, this is the case as long as we are not too close to the top-right border of the grid. By iterating the movements upwards and rightwards, for any , we arrive to a state such that , which ensures we are a distance of at least from the border. Therefore, we can bound

where the last relation is immediately obtained by looking at either or . Thus, we also have that , and we can conclude that .

C.3 Upper-Bound for Transition Lookahead

appendix]appendix: transition lookahead In this appendix, we analyze the competitive ratio versus one-step transition lookahead agents. Formally, at each timestep and state , such agents observe what the next state would be upon playing any of the actions . We assume that this is the only information available to the agent (namely, the agent has no reward lookahead). We also assume that transitions are generated independently at different timesteps and are independent of the rewards. Notably, even with one-step information, the CR is exponentially small, as stated in the following proposition:

Proposition C.3.

For any , and , there exists an environment such that the CR versus one-step transition lookahead agents is .

Proof C.4.

The environment we build is a complete tree of depth (to be determined), where each node has descendants. The agent always starts at the root of the tree. At each node, the agent can play to stay at the same node, while the rest of the actions move the agent to one of the descendants of the node uniformly at random. Only one leaf has a deterministic unit reward of for all actions, while all other leaves yield no reward. After traversing the tree, the agent moves to a terminal non-rewarding state . The total number of states required to create this environment is

and the number of leaves in the tree is . A no-lookahead agent could not do better than randomly traversing the tree and would obtain an expected reward of at most .

On the other hand, one-step transition lookahead agents could choose the following policy: if an action leads in the direction of the rewarding leaf, take it; otherwise, wait in the current node. To obtain the reward, there have to be at least timesteps where an action leads in the right direction, over the span of attempts (one additional round is required to collect the reward. Letting be the probability that such an action exists at a certain node (‘success’), the value of the one-step lookahead agent would be at least the probability that a binomial distribution has at least successes. Setting , so that , we use Hoeffding’s inequality to get

Therefore, the competitive ratio is upper-bounded for

We remark that the constraint allows building such a tree, while ensures a depth of at least .

Appendix D Auxiliary Lemmas

Lemma D.1.

lemma]lemma: minmax for CR Let and . Also, let be a convex compact nonempty set. Then,

where we define all ratios to be if the denominator equals zero.

Proof D.2.

We first remark that if for all , then by the definition of the division by zero, both sides are trivially equal to , and the result holds. Thus, from this point onwards, we assume w.l.o.g. that for some , it holds that .

Step I:

We start from analyzing the l.h.s. problem and showing that

Notice that choosing leads to a bounded value of , so the value is finite – there cannot be a solution such that (and the value is ), and we can w.l.o.g add the constraint . We further remark that both the numerator and denominator are always non-negative, so the infimum is bounded from below by . Given that, the internal problem is always well-defined, and the maximizer is given by .

We next show that the constraints can be replaced by the constraints . First, for any s.t. , define , for which and

Thus, we have the inequality

On the other hand, for any s.t. , define (which is well defined due to the constraints). For this choice, we get that and . In particular, one can write , which implies that

Therefore, we also have the other inequality

which implies equality

Step II:

Applying the minimax theorem.

The objective is linear in (and thus convex and concave in the variables, respectively), and the set is convex and compact. The constraint on is also convex, though not compact, but this is easily fixable; notice that for all such that , does not affect the constraint. On the other hand, setting can only increase the objective since . Indeed, for any s.t. , letting , we have and . Hence, w.l.o.g., we can always add the constraint that for all with . With this additional constraint, the set is convex and compact, so the infimum is actually a minimum and we can apply the minimax theorem to obtain

Step III:

Solving the internal problem for fixed values of .

At this point, we note that components where do not affect either the value or the solution. Therefore, from this point onwards, we assume w.l.o.g that for all ; we will then apply our results only on the subset of components with . Given that, we also assume w.l.o.g. that for all – otherwise, the constraint could be met by letting for components with , which would lead to the optimal value of (we verify this case at the end of the proof).

Thus, we focus on solving the following problem: for any fixed s.t. for all , solve

Due to the linearity of both the objective and constraints (in ), KKT conditions are both necessary and sufficient for the solution of this problem. Letting and be the dual variables for the constraints and , respectively, the KKT requires that for all ,

| (stationarity) | |||

| (complementary slackness) | |||

| (feasibility 1) | |||

| (feasibility 2) |

For the stationarity to hold with the non-negativity of , we must have that . Moreover, if this is a strict inequality, all are strictly positive, which leads to the infeasible zero-reward vector (due to the complementary slackness). Therefore, we can conclude that , and so only in coordinates where this minimal ratio in achieved. By complementary slackness, for the rest of the coordinates.

Substituting in the equality constraint, we get

Explicitly, is by the constraint and is since when . Reorganizing, we get that the value of the internal problem is

We end by remarking that when for some , the value becomes so that the result also holds in this case.

Summary:

Combining all parts of the proof, we got

If we define the internal value to be when , we can further write

which concludes the proof.

Remark D.3.

Following almost identical proof, we could similarly prove that

The only change would be in the first step; using the same rescaling idea (), one could prove that

while the reverse inequality trivially holds since . The rest of the proof follows without any change.

Notably, since this lemma is used in all our proofs to calculate the CR for the worst-case reward expectations, it implies that we would get the same results were we to define the CR as .

Lemma D.4.

lemma]lemma: min-inf for CR Let . Also, let be a convex compact set and be a convex compact polytope, both assumed to be nonempty. Then

where we define all ratios to be if the denominator equals zero.

Proof D.5.

We assume w.l.o.g. that , since the infimum over a singleton is always equal to the minimum (in this case, both equal ), and the result trivially holds.

Next, for all , define . Notice that for any s.t. , there exists such that , and so

where the last inequality follows from the compactness of . In particular, since and is nonempty, such exists, and thus , so the value at the optimization problem in the l.h.s. is finite.

We next prove that is quasi-concave over , namely

First, if and (or the opposite), for any we have that

where we used the non-negativity of and the convention that . Next, assume that both . Also, let such that

and similarly define . Such must exist, since we could always write

The maximum over a finite number of linear functions is continuous and the set is compact, so a maximizer in is always attainable. Using these definitions, we have,

| ( is convex) | ||||

Relation is due to the inequality for , and one could easily verify that the inequality is still valid when either or .

Finally, recall that is a compact convex polytope; in particular, each interior point could be represented as a convex combination of one of its finite extreme points . Then, by the quasi-concavity, the value of each interior point is lower-bounded by the value of at least one of these extreme points so that

This proves that the infimum is attainable by a point in , thus concluding the proof.