Optimal Portfolio Choice with Cross-Impact Propagators

Abstract

We consider a class of optimal portfolio choice problems in continuous time where the agent’s transactions create both transient cross-impact driven by a matrix-valued Volterra propagator, as well as temporary price impact. We formulate this problem as the maximization of a revenue-risk functional, where the agent also exploits available information on a progressively measurable price predicting signal. We solve the maximization problem explicitly in terms of operator resolvents, by reducing the corresponding first order condition to a coupled system of stochastic Fredholm equations of the second kind and deriving its solution. We then give sufficient conditions on the matrix-valued propagator so that the model does not permit price manipulation. We also provide an implementation of the solutions to the optimal portfolio choice problem and to the associated optimal execution problem. Our solutions yield financial insights on the influence of cross-impact on the optimal strategies and its interplay with alpha decays.

- Mathematics Subject Classification (2010):

-

93E20, 60H30, 91G80

- JEL Classification:

-

C02, C61, G11

- Keywords:

-

optimal portfolio choice, price impact, cross-impact, propagator models, predictive signals, Volterra stochastic control

1 Introduction

Optimal portfolio choice has been a core problem in quantitative finance. In this class of problems investors dynamically select their portfolio while taking into account expected returns, risk factors, transaction and price impact costs, and trading signals. The seminal papers of Gârleanu and Pedersen [13, 14] provided a tractable framework for formulating and explicitly solving these problems under the assumptions of quadratic trading costs and exponential decay of the price impact, among others. Their work was further generalized in various directions (see e.g. [12, 18, 28]). Despite its phenomenal impact, the main drawback of Gârleanu and Pedersen’s framework is that it relies on the assumption that the price impact and the cross-impact decay at an exponential rate.

Price impact refers to the empirical fact that the execution of a large order affects a risky asset’s price in an adverse and persistent manner leading to less favourable prices. Propagator models are a central tool in describing these phenomena mathematically. They express price moves in terms of the influence of past trades, and therefore capture the decay of the price impact after each trade [6, 15]. Cross-impact models provide an additional explanation for the price dynamics of a risky asset in terms of the influence of past trades of other assets in the market. The price distortion due to both effects is quantified by the -dimensional process,

| (1.1) |

where describes the amount of shares in each of the assets in the portfolio at time . Here is a matrix of Volterra kernel functions, so that self-impact is captured by its diagonal entries and cross-impact is captured by its off-diagonal entries. The components of are often referred to as propagators (see e.g. [5, 6, 20, 23, 25, 26]). Throughout this paper we will adopt the convention introduced in Section 14.5.3 of [6] and refer to price impact (or equivalently price distortion) as the aggregated effects of self-impact and cross-impact.

Gârleanu and Pedersen along with follow-up papers assumed that the price distortion decays exponentially with time. On the other hand, Bouchaud et al. [6] (see Chapter 14.5.3) report on two main empirical observations reagarding price impact: (i) diagonal and off-diagonal elements of the propagator matrix decay as a power-law of the lag, i.e. , with . (ii) most of the cross-correlations between price moves (, depending on the time scale), are mediated by trades themselves, i.e. through a cross-impact mechanism, rather than through the cross-correlation of noise terms, which are not directly related to trading. See also [5] for further details. Mastromatteo et al. [23] show that neglecting cross-impact effects leads to an incorrect estimation of the liquidity and to suboptimal execution strategies. In particular, they demonstrate the importance of synchronizing the trades of correlated assets and comment on the characteristics of optimal portfolio trading strategies. Le Coz et al. [20] perform an empirical analysis using data of 500 US assets from 2017 to 2022. They conclude that price formation occurs endogenously within highly liquid assets first, and then trades in these assets influence the prices of their less liquid correlated products, with an impact speed constrained by their minimum trading frequency.

While power-law behaviour of cross-impact has strong evidence coming from market data, results on the corresponding optimal portfolio choice problem have been scarce for two main reasons: (i) power-law type or any more general propagator matrices which do not have an exponential decay turn the optimal portfolio choice problem into non-Markovian and often time inconsistent, hence standard tools of stochastic control such as dynamic programming or FBSDEs do not apply in this case. (ii) cross-impact may cause various problems from the financial point of view, such as round trips or transaction-triggered price manipulations (see [3, 19, 25] for some pathological examples). Some recent progress has been made in [1, 2] for the single asset version of this problem in the context of optimal execution with signals. However the solution for the single asset problem clearly does not take into account the aforementioned cross-impact effects.

The main theoretical contribution in this non-Markovian portfolio choice setting was derived by Alfonsi et al. [3], who proposed a discrete-time model for portfolio liquidation in presence of linear transient cross-impact using convolution type decay kernels . They characterized conditions on which guarantee that the model admits well-behaved optimal execution strategies by ensuring that price manipulation in the sense of Huberman and Stanzl [19] is excluded. This means that a portfolio starting and terminating with zero inventory cannot create any profit, or equivalently negative trading costs, due to the induced price distortion in (1.1). This condition translates into the following inequality,

| (1.2) |

where the time grid is discrete in [3], so that the integral is written as a sum. Alfonsi et al. [3] concluded that must be a matrix-valued nonnegative definite function in order for the model to satisfy condition (1.2) and thus preclude price manipulation. A sufficient condition for (1.2) in which is nonincreasing, nonnegative, convex, symmetric and commuting was given in [3], as well as a characterization of matrix-valued nonnegative definite functions. Alfonsi et al. also derived a first order condition for the optimal strategy of the execution problem and obtained an explicit solution for the case where the propagator matrix is given by for a symmetric nonnegative definite matrix . Note that in the framework of [3], not only the model is discrete in time, but also the alpha signals and the risk terms, which are central features of portfolio choice problems, are not incorporated. These simplifying assumptions turn the resulting stochastic control problem into a completely deterministic one. Moreover, explicit solutions in [3] are only given for the special case of an exponential propagator matrix.

Our contribution:

In this work we extend the results of Gârleanu and Pedersen [14] and Alfonsi et al. [3] in a few crucial directions which are of relevance to recent empirical studies on cross-impact and also of theoretical interest. Our results provide financial insights on the influence of cross-impact on optimal trading strategies and the interplay between cross-impact and alpha decays.

-

(i)

Derivation of explicit solutions: we formulate and solve the optimal portfolio choice problem in continuous time, allowing for a general Volterra propagator matrix of nonnegative definite type as well as for general progressively measurable signals. Our optimal strategy is derived explicitly in Theorem 2.8 in terms of resolvents of the operators involved, and it is implemented in Section 3. Theorem 2.8 extends the results of [14], as it allows to solve the problem for a general propagator matrix, which includes the exponential decay kernels used in [14], as well as the power-law kernels from [5, 23] as specific examples. We also allow for general progressively measurable signals, which substantially generalize the mean-reverting signals used in [14] and the diffusion signals used in follow-up papers. Theorem 2.8 also generalizes the results of [3] in various directions. First we solve the problem in continuous time, which is compatible with the high-frequency trading timescale. We also include stochastic signals and risk factors, which are crucial for general portfolio choice problems, and turn them from being matrix-valued and deterministic as in [3], into being operator-valued and stochastic. Moreover, we allow for a general Volterra propagator matrix instead of a convolution propagator matrix as used in [3, 14], and provide explicit solutions in the general case, in contrast to the special case with an exponential propagator matrix, which was solved in [3]. As mentioned earlier, due to the generality of the propagator matrix, the portfolio choice problem that we solve is non-Markovian and time inconsistent, hence we introduce new tools, in the form of stochastic forward-backward systems of Fredholm equations of the second kind (see Section 4), in order to solve the corresponding first order conditions.

-

(ii)

Preventing price manipulation: in Theorem 2.14 we give sufficient conditions for a convolution propagator matrix to be nonnegative definite, which means that the expected costs caused by transient price impact are nonnegative for any trading strategy, so that in particular price manipulation in the sense of Huberman and Stanzl [19] is prevented (see (1.2)). Specifically, we show that if is nonincreasing, convex, nonnegative and symmetric, then is nonnegative definite, and price manipulations are excluded. Our result generalizes Theorem 2 of [3] from discrete to continuous time domains, and is of independent interest to the theory of nonnegative definite Volterra kernels. In Corollary 2.17 we address a popular example from the econophysics literature (see e.g. [23]). Namely, we prove that if the convolution propagator matrix is factorized as , where is a symmetric nonnegative definite matrix and the function is nonnegative, nonincreasing and convex on , then is nonnegative definite, hence price manipulations are excluded.

-

(iii)

Insights on the influence of cross-impact: our numerical study in Section 3 explores the influence of transient cross-impact on the optimal liquidation of Asset 1, with an initial inventory of 0 in Asset 2. The conclusions can be summarized as follows:

-

(a)

In the absence of signals, cross-impact induces a ‘transaction-triggered’ round trip in Asset 2, prompting more aggressive trading in both assets. The strategy is particularly aggressive for the exponential propagator matrix compared to the more persistent fractional one (see Figure 2).

-

(b)

In the presence of positive alpha signals on both assets, cross-impact leverages the different alpha decays. The optimal strategy may involve selling or shorting the asset with the fastest alpha decay to leverage the cross-impact effect that decreases the price of the other asset with the slowest alpha decay. This allows profiting from both the more persistent signal on the second asset as well as the cross-impact effect (see Figures 3 and 4).

-

(a)

Organization of the paper:

In Section 2 we present our main results regarding the solution to the portfolio choice problem and the prevention of price manipulation. Section 3 is dedicated to numerical illustrations of our main results. In Section 4 we derive explicit solutions to a class of systems of stochastic Fredholm equations arising from the first order condition in the proof of Theorem 2.8. Finally, Sections 5–7 are dedicated to the proofs of our main results.

2 Model Setup and Main Results

2.1 Model setup

Motivated by [14], we introduce in the following a variant of the optimal portfolio choice problem with transient price impact driven by a Volterra propagator matrix and in the presence of general alpha signals.

Let be a filtered probability space satisfying the usual conditions of right-continuity and completeness and let be a deterministic finite time horizon. We consider risky assets whose unaffected price is given by an -dimensional semimartingale with a canonical decomposition

| (2.1) |

Here is a predictable finite-variation process with

and is a continuous martingale such that

| (2.2) |

where is a symmetric nonnegative definite covariance matrix and denotes the Euclidean norm.

We consider an investor whose initial portfolio is given by , where the amounts of shares held in each of the risky assets are given by

| (2.3) |

Here denotes the trading speed chosen by the investor from the set of admissible strategies

| (2.4) |

We assume that the investor’s trading activity causes linear temporary impact on the assets’ execution prices given by

| (2.5) |

where is a positive definite (not necessarily symmetric) matrix, i.e. for all . Note that the diagonal entries of capture the temporary self-impact while the off-diagonal entries introduce temporary cross-impact on the price of asset caused by trading one share of asset per unit of time.

Remark 2.1.

Note that empirical findings in Capponi and Cont [8], Le Coz et al. [20] and Cont et al. [9] suggest that there is no significant temporary cross-impact of assets, i.e. that the off-diagonal entries of are zero. Incorporating these findings into our model would turn into a diagonal matrix with positive entries that capture the temporary self-impact of the assets à la Almgren and Chriss [4].

The investor’s trading activity also creates a price distortion which is given by

| (2.6) |

where is a matrix of Volterra kernels, i.e. each entry in the matrix satisfies for . The so-called propagator matrix captures linear transient self-impact in the diagonal terms along with linear cross-impact in the off-diagonal terms. That is, the value describes the impact at time on the -th asset’s price caused by trading at time one share of the -th asset per unit of time. We further say that is nonnegative definite, if it holds for every that

| (2.7) |

We define to be the space of Borel-measurable matrix-valued kernels satisfying

| (2.8) |

Here, denotes the Frobenius norm in consistency with our notation for the Euclidean norm. The set of admissible kernels is given by,

| (2.9) |

Example 2.2.

We present some typical examples for propagator matrices which arise from applications and can be incorporated into our model.

- (i)

-

(ii)

Power-law decay: Benzaquen et al. [5] and Mastromatteo et al. [23] use for their empirical studies the factorized power-law kernel

(2.12) where is symmetric nonnegative definite, and . If , our model also allows the factorized kernel

(2.13) with singular power-law decay as introduced by Gatheral [15].

-

(iii)

Permanent impact: The constant kernel

(2.14) for a symmetric nonnegative definite matrix incorporates permanent self- and cross-impact as discussed in Section 5 of Huberman and Stanzl [19], Section 3 of Schneider and Lillo [25] and Example 1 of Alfonsi et al. [3]. If is a diagonal matrix with nonnegative entries, represents permanent impact à la Almgren and Chriss [4].

-

(iv)

Constructed decay kernels: Motivated by Section 3.1 of [3], the general kernel

(2.15) for an invertible matrix and nonnegative, nonincreasing, convex kernel functions , is nonnegative definite.

-

(v)

Interest rate derivatives: The following non-convolution kernel is a straightforward generalization of the price impact for bonds trading model proposed in Section 3.1 of Brigo et al. [7], to a portfolio of bonds,

Here is a nonnegative, nonincreasing, convex function taking values in , such as the exponential or power-law kernels in the above examples and is a symmetric nonnegative definite matrix . The factor for is added in order to enforce a terminal condition on the bond price regarding its expiration at time .

Lemma 2.3.

All propagator matrices introduced in Example 2.2 belong to the class of admissible kernels .

The investor’s objective is the maximization of the following portfolio performance criterion over the time period ,

| (2.16) |

over all admissible trading strategies . The first two terms in the right-hand side of (2.16) describe the investor’s terminal wealth, in terms of her final cash position resulting from trading the assets in the presence of price impact as prescribed above, as well as her remaining final portfolio’s book value. The last term in (2.16) represents the portfolio’s risk in the sense of Markowitz [22] (see also Section 1 of [14]), where was defined in (2.2) and is a risk aversion parameter.

Remark 2.4.

One may consider to implement in (2.16) the final portfolio’s distorted value instead of its final book value . Recall the decomposition . Hence in this case if and are both differentiable with respect to , an application of integration by parts yields that maximizing is equivalent to maximizing the following cost functional,

| (2.17) |

which is a finite time horizon version of the objective functional in Gârleanu and Pedersen [14]. Note however that in this case might not be concave for general Volterra kernels , unlike for the exponential kernel case studied in [14].

2.2 Solution of the portfolio choice problem

Before we present our results regarding the solution to the portfolio choice problem we introduce some essential definitions and notation.

We denote the inner product on by , i.e.

| (2.18) |

and its induced norm by .

For any (recall (2.8)) define the linear integral operator on induced by as

| (2.19) |

Then is a bounded linear operator from into itself (see Theorem 9.2.4 and Proposition 9.2.7 (iii) in [17]). Moreover, we denote by the adjoint kernel of with respect to given by

| (2.20) |

and by the induced adjoint bounded linear operator on .

Remark 2.5.

Note that if then it holds that

| (2.21) |

Moreover, recalling (2.7), the following three statements are equivalent:

-

(i)

The integral operator is nonnegative definite,

-

(ii)

The integral operator is nonnegative definite,

-

(iii)

The integral operator is nonnegative definite,

Definition 2.6.

Let denote a matrix-valued function in one variable and be a linear operator from into itself. Then we define the column-wise application of to as

| (2.22) |

where

| (2.23) |

is given by the -th column of for .

Definition 2.7.

For a Volterra kernel and a fixed define

| (2.24) |

and let denote the induced integral operator on .

Notation.

Recall that was defined in (2.5). We denote by

| (2.25) |

the symmetric part of , which is a positive definite matrix again.

Recall that and were introduced in (2.16). For a Volterra kernel as before, we introduce the following Volterra kernels :

| (2.26) |

We denote by the conditional expectation with respect to .

Finally, we define the following linear operator,

| (2.27) |

where is the identity operator on , and the stochastic process

| (2.28) |

where is given in (2.3).

Recall that the class of admissible propagator matrices was defined in (2.9). In the following theorem we derive the unique maximizer of the portfolio’s revenue-risk functional (2.16) in terms of resolvents. Recall that the resolvent of a Volterra operator is given by .

Theorem 2.8.

In the following corollary we derive the maximizer of (2.16) for the case of a deterministic signal in (2.1). This assumption considerably simplifies the optimal portfolio choice and is of relevance for practical applications.

Corollary 2.9.

In the following remarks we give additional details regarding the contribution and implementation of our results.

Remark 2.10.

If the investor’s objective is to optimally liquidate the portfolio, an additional terminal penalty on the remaining inventory can be added to (2.16). Specifically, we define the revenue-risk functional as follows:

| (2.35) |

where in the last term of , is a positive constant and is a symmetric nonnegative definite matrix. In this case the result of Theorem 2.8 applies with a slight modification by setting:

| (2.36) |

and

| (2.37) |

Remark 2.11.

Remark 2.12.

Theorem 2.8 extends the results of Proposition 2 in [14], as it allows to solve the problem for general propagator matrices as in (2.9), which include the exponential decay kernels used in [14], as well as the power-law kernels from [5, 23] and other specific examples outlined earlier in this section. We also allow for general semimartingale signals, which substantially generalize the integrated Ornstein-Uhlenbeck signals used in [14]. Theorem 2.8 also generalizes the results of [3] in the following directions: First, we solve the problem in continuous time, which is compatible with the high-frequency trading timescale. We also include stochastic signals and risk factors in the objective functional (2.16), which are crucial for portfolio choice problems. This turns the portfolio choice problem from being matrix-valued and deterministic as in [3] into an operator-valued stochastic control problem. We also allow for a general Volterra propagator matrix instead of the convolution propagator matrix in [3], and provide explicit solutions, in contrast to the first order condition derived in Theorem 3 of [3], which is solely solved for exponential propagator matrices (see Example 2 therein). In particular, in the proof of Theorem 2.8, we characterize the first order condition corresponding to the objective functional (2.16) in terms of a system of coupled stochastic Fredholm equations of the second kind with both forward and backward components. In Section 4 we develop a method for solving this system explicitly, which is a central ingredient for the proof of Theorem 2.8.

Remark 2.13.

In the single asset case where , Theorem 2.8 generalizes the main results of both [1] and [2] to a larger class of admissible kernels . Indeed, the proof of Theorem 2.8 relies heavily on the theory of kernels of type and their resolvents. See in particular the proofs of Proposition 4.1 and Lemma 4.8. The method of the proof allows us to extend the class of admissible kernels such that only square-integrabilty of the kernels is needed (see (2.9) and (2.8)), instead of the more restrictive assumption that

| (2.38) |

which was assumed by Abi Jaber and Neuman [1] and Abi Jaber et al. [2] who studied the single asset case. In particular our new approach can be applied to prove Proposition 4.5 and Lemma 7.1 in [1] as well as Proposition 5.1 and Lemma 5.5 in [2] under the more general integrability assumption on the admissible kernels in given by

| (2.39) |

2.3 Results on price manipulations

In this section we address the following question:

How to choose the propagator matrix in order to prevent price manipulation?

We recall that for a kernel the expected costs caused by transient impact induced by a strategy are given by

| (2.40) |

Note that (2.40) can be obtained by considering strategies with fuel constraints (i.e. ), setting the risk aversion term and temporary price impact matrix in (2.16) to and by choosing a martingale unaffected price process which prevents arbitrage opportunities (see Section 2.1 of [21] for the derivation). Hence the condition that a propagator matrix satisfies (2.7) rules out the possibility of price manipulations in the sense of [19]. This means that a portfolio starting and terminating with zero inventory cannot create any profit, or equivalently negative trading costs, so we must have

Put differently, a price manipulation in this context is a round trip strategy with positive expected profit, which in the absence of trading signals, is only possible if (2.40) is negative. We refer to Section 2 of Alfonsi et al. [3] for the price impact manipulation condition in discrete time portfolio choice problems. Interestingly enough, assumption (2.7) is also needed in order to prove that the objective functional (2.16) is concave (see Lemma 5.1), hence it is essential for the proof of Theorem 2.8.

Note that condition (2.7) is not straightforward to verify. The main result of this section derives sufficient conditions for a large class of convolution kernels to satisfy (2.7). We recall that in the single asset case, convolution kernels of the form are nonnegative definite kernels whenever the real function on is nonnegative, nonincreasing and convex (see Example 2.7 in [16]). However in the multi-asset case deriving a characterization for nonnegative definite kernels is substantially more involved. Recall that the class of admissible Volterra kernels was defined in (2.9).

Theorem 2.14.

Let be a convolution kernel so that the associated Volterra kernel is in . Assume that satisfies the following assumptions:

-

•

nonincreasing, i.e. the function is nonincreasing on for every ,

-

•

convex, i.e. the function is convex on for every ,

-

•

nonnegative, i.e. the matrix is nonnegative definite for any ,

-

•

symmetric, i.e. the matrix is symmetric for any .

Then is nonnegative definite and is in the class of admissible kernels , i.e.

| (2.41) |

Remark 2.15.

Remark 2.16.

Theorem 2.14 generalizes the result of Theorem 2 of [3] from discrete time grids to a continuous domain, which is of independent interest to the theory of nonnegative definite Volterra kernels. One of the main ingredients of the proof is Proposition 6.3, which states that a matrix-valued Volterra kernel which is nonnegative definite in the discrete sense (see (6.3)) is also nonnegative definite on a continuous domain, i.e. it satisfies assumption (2.7).

The following corollary rules out the possibility of price manipulation in the sense of [19] for a specific class of factorized convolution propagator matrices introduced by Benzaquen et al. [5], Mastromatteo et al. [23].

Corollary 2.17.

Let be a symmetric nonnegative definite matrix and be nonnegative, nonincreasing and convex on . Then the convolution kernel

| (2.42) |

is nonnegative definite and thus its associated Volterra kernel is in .

Remark 2.18.

From Corollary 2.17 it follows that our model accommodates the factorized model introduced in [5, 23], where empirical evidence for the explanatory relevance of cross-impact for the cross-correlation of US stocks was given. The authors found that as a good and efficient approximation the price impact kernel can be written as for a symmetric nonnegative definite matrix and a power-law function

| (2.43) |

where and are estimated model parameters. The main conclusions of their papers are also briefly summarized in Section 14.5.3 of [6].

3 Numerical Illustrations

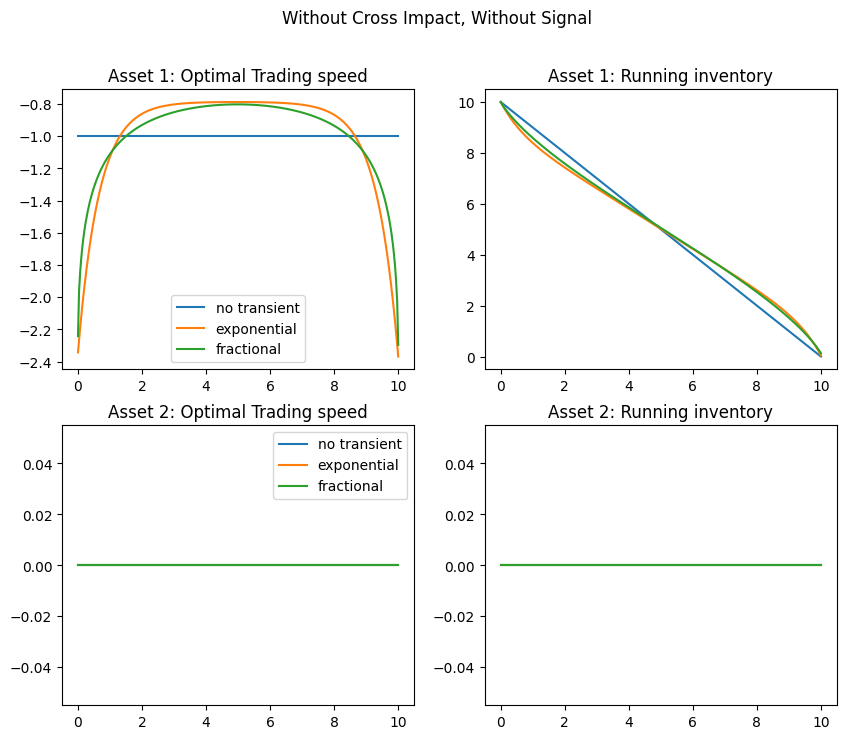

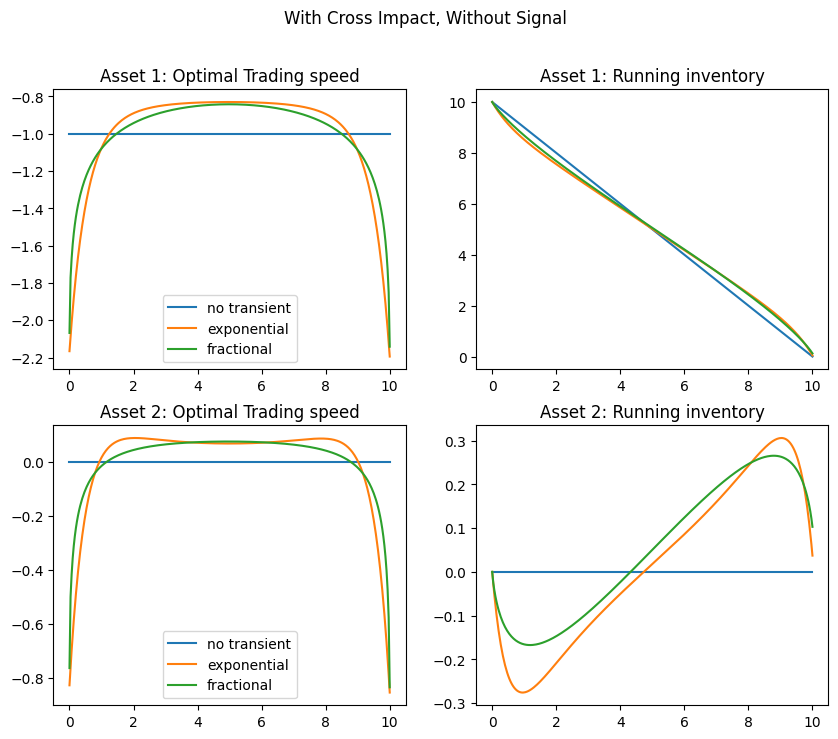

3.1 Optimal liquidation: what is the influence of cross-impact?

In this section, we explore the influence of transient cross-impact for two assets in a liquidation problem with time horizon , where Asset 1 has shares initial inventory and Asset 2 starts from zero inventory, i.e. . Our objective is to elucidate the influence of cross-impact on optimal trading speeds and inventories and its interplay with trading signals (also called alphas). To isolate these effects, we consider a penalty on terminal inventory using the parameters of the form

| (3.1) |

and we set , removing the risk component in the objective functional in Remark 2.10 originating from the covariance matrix between the assets.

We consider temporary self-impact but no temporary cross-impact through the -matrix :

| (3.2) |

The transient price impact is given by the parsimonious propagator from [5, 23] (see Corollary 2.17) of the form

| (3.3) |

with a deterministic symmetric -matrix that will be taken to be either diagonal or non-diagonal to study the impact of cross-impact (see (3.4)-(3.5) below), and a scalar convolution kernel which will be either set to , exponential with or fractional with .

We analyze four figures to illustrate our findings:

Our conclusions are summarized as follows:

-

1.

In the absence of trading signals (see Figures 1 and 2), cross-impact induces:

-

•

a ‘transaction-triggered’ round trip in Asset 2 on the bottom panels of Figure 2 which was absent from Figure 1. Initiating fast liquidation of Asset 1 at time triggers a drop in Asset 2’s price due to , prompting a ‘transaction-triggered’ shorting signal’ on Asset 2. Therefore, the optimal strategy starts by shorting Asset 2. After a while, as the selling speed of Asset 1 slows down, the strategy starts buying Asset 2 at a steady rate. This strategic move aims at increasing the price of Asset 1 undergoing liquidation, using the positive cross-impact term . This steady buying even results in a long position in Asset 2 which is then liquidated quickly near the maturity. The strategy is more aggressive for the exponential kernel compared to the fractional one.

- •

-

•

-

2.

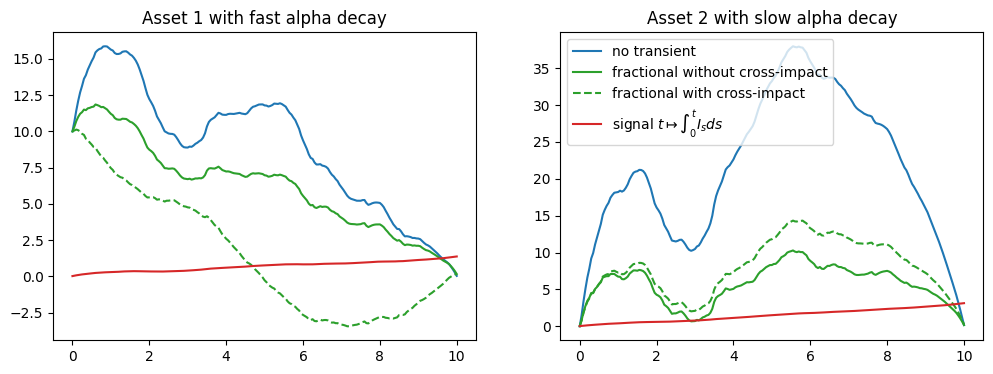

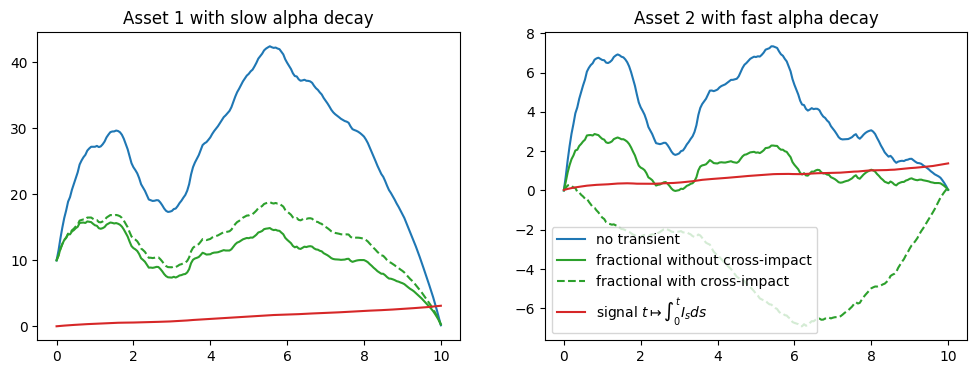

In the presence of positive trading signals on both assets with different alpha decays (see Figures 3 and 4):

-

•

Without cross-impact (solid lines): in both figures, the positive signal for Asset 1 prompts from the start a purchasing of Asset 1 even in the presence of transient impact. The ‘buy’ strategy is more aggressive in the absence of transient impact. Similarly, the positive signal of Asset 2 triggers a ‘buy round trip’ on Asset 2.

-

•

With cross-impact (dashed lines): in Figure 3 with in (3.8) we observe that in contrary to the no cross-impact case, there is almost no buying of Asset 1 at , even in the presence of the positive signal for Asset 1. Indeed, since the ‘buy’ signal for Asset 1 decays more rapidly compared to that of Asset 2, recall the mean-reversion coefficients in (3.8), the optimal strategy starts selling Asset 1 quickly (and even shorts it) in order to leverage the cross-impact that will decrease the price of Asset 2 that has a more persistent positive signal. Hence, this strategy allows profiting from both the persistent signal on Asset 2 and from the cross-impact effect. More of Asset 2 is bought compared with the case without cross-impact.

-

•

3.2 Optimal trading with frictions

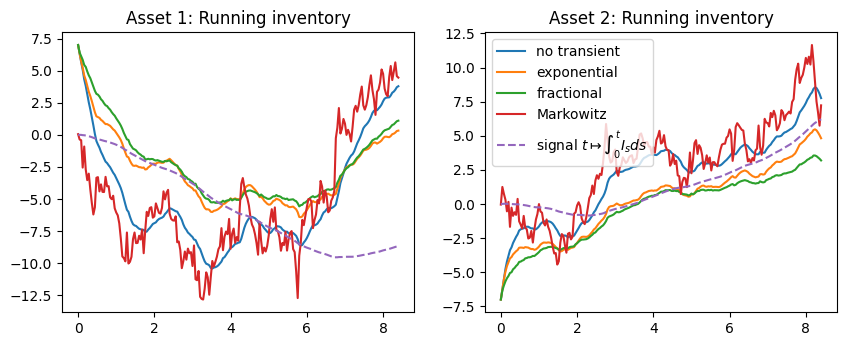

In this section, we illustrate the influence of transient impact on an portfolio choice example with two independent assets. Here we set as in the objective functional (2.16) (i.e. no penalty on terminal inventory) and we set the risk aversion coefficient to . We look at the time evolution of holdings in each asset in comparison with the Markowitz portfolio, i.e. the zero temporary and transient price impact case. This experiment has already appeared in [14] for the exponential kernel.

We set , with two independent assets with a -covariance matrix given by

and a stochastic trading signal of the form (3.6)-(3.7) with

The temporary impact is given by (3.2) and the transient impact is given by (3.3), where we do not consider cross-impact, i.e. is given by (3.5) and is chosen as in the previous section.

We make precise the notion of the Markowitz portfolio in this context.

Remark 3.1.

In the absence of any market frictions, i.e. , for an un-affected price of the form

with a martingale, the optimal position is given by the celebrated Markowitz portfolio

| (3.9) |

To see this it suffices to set in the functional in (2.16) and apply an integration by parts to get:

which would then yield the functional

| (3.10) |

and the optimality the Markowitz portfolio (3.9).

The optimal positions in Assets 1 and 2 without cross-impact are illustrated in Figure 5. The Markowitz portfolio is just a reference portfolio that describes the weights of the optimal portfolio derived from the optimal trade-off between risk and expected excess return scaled by . We make the following observations:

-

•

Similarly to Gârleanu and Pedersen [14], we observe that if one chooses any initial starting portfolio , all optimal positions in the presence of frictions try to follow and get closer to the Markowitz portfolio in a smooth way.

-

•

The ‘speed of convergence’ towards the Markowitz portfolio seems to depend on the type of the frictions, being faster for the no-transient kernel than for the the exponential kernel, and slowest for the more persistent fractional case.

3.3 Numerical scheme

A major advantage of the operator formulas appearing in Theorem 2.8 is their ease of implementation. One possibility is the use of the so-called Nyström method to discretize the operators, and the method described in Section 5.1 of [1] for the single asset case can be readily adapted to our multi-asset setting.

For completeness, we briefly describe the numerical implementation for deterministic signals as in Corollary 2.9.

Fix assets, and a partition of as well as a propagator matrix in the form (3.3). We set .

Step 1. Specify the signal for a deterministic function and compute the -vector,

using the expression of in (2.37). (Note that .) Second, specify the scalar convolution kernel that appears in (3.3) and set and . Define the following lower and upper triangular -matrices and where the nonzero elements are given by:

| (3.11) | |||||

| (3.12) | |||||

| (3.13) | |||||

| (3.14) | |||||

| (3.15) | |||||

| (3.16) |

For instance, for the three particular kernels in the previous subsection, and admit explicit expressions collected in Table 1.

| for | for | ||

|---|---|---|---|

| No-transient | 0 | 0 | 0 |

| Exponential | |||

| Fractional |

Step 2. Construct the -matrix using

where is the Kronecker product.

Step 3. Recover the -vector for the optimal control path

and note that the first components are the first trading values for all assets, the next components are the second trading values for all assets etc.

4 Systems of Stochastic Fredholm Equations

In this section we derive solutions to a class of coupled stochastic Fredholm equations of the second kind with both forward and backward components, which arise from the first order condition in the proof of Theorem 2.8 in Section 5. The main result of this section is given in the following proposition. Recall that the class of admissible propagator matrices was defined in (2.9) and that the operation was defined in Definition 2.6. We also recall for any kernel , the kernel is the truncation of from Definition 2.7 and that is the operator induced by the kernel .

Proposition 4.1.

Let be Volterra kernels in , let be a symmetric positive definite matrix, and let be an -dimensional progressively measurable process with . Then the following coupled system of stochastic Fredholm equations

| (4.1) |

admits a unique progressively measurable solution in given by

| (4.2) |

where

| (4.3) |

| (4.4) |

| (4.5) |

Here is the identity operator on and is the integral operator induced by the kernel .

Remark 4.2.

Proposition 4.1 is a generalization of Proposition 5.1 in [2] from the class of one-dimensional stochastic Fredholm equations to –dimensional coupled systems. Note that in the one-dimensional case is just a positive scalar, so that the integral operators and are nonnegative definite and therefore the operator invertible, which is an important ingredient in the derivation of the solution. However, since the composition of two general nonnegative definite linear operators on a Hilbert space is not necessarily nonnegative definite, even if they are self-adjoint, this argument does not go through in the –dimensional case. Thus, the positive definite operator is inverted as part of the solution, and appears as part of the terms and .

As a preparation for the the proof, we introduce the concept of kernels of type following the terminology of Definition 9.2.2 in [17].

Definition 4.3.

A Borel-measurable function is called a kernel of type if it satisfies

| (4.6) |

where the supremum is taken over all real-valued functions with norm bounded by and denotes the Frobenius norm (following the convention introduced after (2.8)).

Every kernel in is also a kernel of type (see Proposition 9.2.7 (iii) in [17]). However, the converse does not hold in general as the following counterexample shows.

Example 4.4.

Define the kernel by , where

| (4.7) |

Then for every and therefore . Now let such that . Then applications of Hölder’s inequality and Young’s convolution inequality imply,

and therefore that . Here, denotes the convolution of and . This example can be generalized to the case where is -valued.

The following auxiliary lemmas are essential ingredients for the proof of Proposition 4.1.

Lemma 4.5.

For any fixed , the integral operator is nonnegative definite.

Proof.

Lemma 4.6.

Let be a symmetric positive definite matrix. Then, the linear operator on is self-adjoint and satisfies

| (4.8) |

where denotes the smallest eigenvalue of . In particular, is positive definite.

Proof.

Since is symmetric positive definite, it can be decomposed as

| (4.9) |

where is an orthogonal matrix whose columns are orthonormal eigenvectors of and is a diagonal matrix whose entries are the positive eigenvalues of . Let and define , which in particular implies that as is orthogonal. We get,

| (4.10) |

Let . Then from (4.10) it follows that

| (4.11) |

∎

Notation.

Let be a linear operator between two normed real vector spaces and . Then the operator norm of is denoted as,

| (4.12) |

Lemma 4.7.

Let be a bounded linear operator from a real Hilbert space into itself. Suppose that there exists a constant such that for all . Then is invertible and .

Proof.

See [27], Chapter 10, Problem 165. ∎

Now we are ready to prove Proposition 4.1.

Proof of Proposition 4.1.

For every define the auxiliary process

| (4.13) |

Taking the conditional expectation on both sides of (4.1), then multiplying by and using the tower property we get

| (4.14) | ||||

where

| (4.15) |

The bounded linear operator is nonnegative definite by Lemma 4.5. Thus, due to Lemma 4.6 and Lemma 4.7, the operator is invertible with,

| (4.16) |

where denotes the operator norm as introduced in (4.12) and denotes the smallest eigenvalue of . It follows from (4.14) that

| (4.17) |

By plugging in (4.17) into (4.1) we get

| (4.18) |

Using (4.15) we rewrite the third term on the right-hand side of (4.18) as follows:

| (4.19) | ||||

where denotes the column-wise application of the operator to the function for fixed (see Definition 2.6). The above equality holds because of Fubini’s theorem and the fact that the operator , multiplication by , and integration are all linear operations. From (4.18) and (4.19) it follows that

| (4.20) |

where and are given in the statement of Proposition 4.1.

We introduce the following auxiliary lemma, which will be proved at the end of this section.

Lemma 4.8.

Note that by Corollary 9.3.16 of [17] and Lemma 4.8(ii), the deterministic Volterra kernel has a resolvent of type (recall Definition 4.3), which is the kernel corresponding to this operator,

| (4.21) |

Therefore, by Theorem 9.3.6 of [17] the integral equation (4.20) admits a unique solution for any fixed for which , i.e. for -a.e. by Lemma 4.8(i). This solution is given by a variation of constants formula in terms of the resolvent , namely

| (4.22) |

It follows that any solution to the coupled system of stochastic Fredholm equations must be of the form

| (4.23) |

which yields the uniqueness of up to modifications. For the existence, let be defined as in (4.23). It follows that satisfies (4.22) and thus (4.20). Therefore, it also satisfies (4.18) and consequently (4.1) due to (4.17), as desired. Thanks to Lemma 4.8(iii) it is ensured that . ∎

Proof of Lemma 4.8.

(i) Recall that

| (4.24) |

Since by the hypothesis of the lemma, it suffices to show that

| (4.25) |

To see this, note that from (4.16), from the conditional Jensen inequality and the tower property we get

| (4.26) | ||||

Moreover, recall that by assumption and thus

see (2.9). The submultiplicativity of the Frobenius norm, Hölder’s inequality and (4.26) yield

| (4.27) | ||||

which verifies (4.25).

5 Proofs of Theorem 2.8 and Corollary 2.9

In order to prove Theorem 2.8 and Corollary 2.9, we introduce the following essential lemmas. We first prove that the objective functional in (2.16) is strictly concave in .

Lemma 5.1.

For any fixed the map is strictly concave in .

Proof.

We prove the result be showing that each of the components of is concave and at least one of them is strictly concave. We first notice that the term

| (5.1) |

is affine in .

Recall that is a positive definite matrix, hence the quadratic form is strictly convex in , which implies that

| (5.2) |

is strictly concave in due to the linearity and monotonicity of the integral. Thus by (2.16) is strictly concave if the term

| (5.3) |

is concave in . Without loss of generality, we assume that , as terms in involving are affine in . In order to show the concavity of (5.3), we adopt the approach from Gatheral et al. (see Proposition 2.9 in [16]). Since and is nonnegative definite, it follows from (2.6) and (2.7) that for all . Next, define the cross functionals

| (5.4) |

From (5.3) and (5.4) it follows that

| (5.5) |

and since , we get that

| (5.6) |

The concavity of for , follows from (5.6) and the fact that the map

| (5.7) |

is continuous in . We therefore obtain the concavity of the left-hand side of (5.3) and hence of . ∎

From Lemma 5.1 it follows that the objective functional in (2.16) admits a unique maximizer characterized by the critical point at which its Gâteaux derivative

| (5.8) |

vanishes for any (see Propositions 1.2 and 2.1 in Chapter 2 of [11]). In the following lemma we calculate .

Lemma 5.2.

For any , the Gâteaux derivative of is given by

| (5.9) |

Proof.

Let and let . Recall that the objective functional is given by

| (5.10) |

A direct computation using (2.3) and (2.6) yields

| (5.11) | |||

| (5.12) | |||

| (5.13) | |||

| (5.14) | |||

| (5.15) |

where we used the symmetry of and applied Fubini’s theorem in the last equality. Recalling (2.25), dividing by and taking the limit as yields the result. ∎

Next, we derive from Lemma 5.2 a system of stochastic Fredholm equations which is satisfied by the unique maximizer of the objective functional in (2.16).

Lemma 5.3.

Proof.

The unique maximizer of is characterized by the critical point at which the Gâteaux derivative is equal to 0 for any . It follows from Lemma 5.9 that this is equivalent to

| (5.17) |

Next, by an application of Fubini’s theorem and recalling that was defined in (2.26),

| (5.18) | ||||

where . Plugging (LABEL:eq:inventory) into (5.17), conditioning on and using the tower property of conditional expectation we get the following first order condition,

| (5.19) | ||||

Recalling the definition of in (2.26) and in (2.28), equation (LABEL:eq:foc) simplifies to

| (5.20) |

which is equivalent to (5.16), since is a Volterra kernel. ∎

In order to prove Theorem 2.8 and Corollary 2.9, the following lemma is needed, which in combination with Remark 2.5 shows that the Volterra kernel defined in is in .

Lemma 5.4.

The following inequality holds,

| (5.21) |

Proof.

First, observe that for all we have

| (5.22) |

Thus for any we get that

| (5.23) | |||

| (5.24) | |||

| (5.25) | |||

| (5.26) |

since is nonnegative definite and . ∎

Proof of Theorem 2.8.

Let . Recall that , and are defined in (2.25), (2.26) and (2.28), respectively. It follows from Lemma 5.4 and Remark 2.5 that and thus as well. Moreover, is progressively measurable and satisfies

| (5.27) |

because is progressively measurable and satisfies by assumption.

Now by Lemmas 5.1 and 5.3, the objective functional in (2.16) admits a unique maximizer in , and this maximizer satisfies (5.16). An application of Proposition 4.1 with and yields that (5.16) admits a unique progressively measurable solution given by

| (5.28) |

with and defined as in Theorem 2.8. It follows that in (5.28) must be the unique maximizer of , which finishes the proof. ∎

Proof of Corollary 2.9.

Let and assume that in (2.1) is deterministic. Then, in (2.28) is a deterministic function in given by

| (5.29) |

It follows that the unique maximizer of the objective functional from Theorem 2.8, which satisfies (5.16), is deterministic and satisfies the simplified equation

| (5.30) |

Now (5.30) admits the deterministic solution

| (5.31) |

where the bounded linear operator

| (5.32) |

defined in (2.26) and (2.27) is invertible because of the following. Since by assumption, due to Lemma 5.4 and Remark 2.5, and there exists a real number such that satisfies

| (5.33) |

due to Lemma 4.6. It follows that the operator is positive definite with

| (5.34) |

Therefore, Lemma 4.7 implies that is invertible.

6 Proofs of Theorem 2.14 and Corollary 2.17

This section is dedicated to the proofs of of Theorem 2.14 and Corollary 2.17, which concern convolution kernels. However, one of the main ingredients for these proofs is Proposition 6.3, which gives a new sufficient condition for the nonnegative definite property for a more general class of Volterra kernels. Since this result could be of independent interest for the theory of Volterra equations we assume in the first part of this section that the kernel is a Volterra kernel.

6.1 Volterra kernels

Definition 6.1.

Let be a Volterra kernel. Then the associated mirrored kernel is defined as

| (6.1) |

Remark 6.2.

It holds for any Volterra kernel that

| (6.2) |

and therefore that for every . This observation will be crucial for the proof of Proposition 6.3.

The following proposition provides a sufficient condition (6.3) for the nonnegative definite property of Volterra kernels. Note that (6.3) below is similar to Definition 2 in [3], which was used in order to define nonnegative definite convolution kernels.

Proposition 6.3.

Let be a matrix-valued Volterra kernel such that its mirrored kernel is continuous and satisfies

| (6.3) |

for any , and . Then for any function the following holds,

| (6.4) |

In order to prove Proposition 6.3 we will need the following auxiliary lemma.

Lemma 6.4.

Let be a map satisfying for all . Then it holds that

| (6.5) |

if and only if

| (6.6) |

Proof.

Proof of Proposition 6.3.

The main idea of the proof is to apply a generalized version of Mercer’s theorem for matrix-valued kernels (see [10]). In order to apply this result, first notice that is a separable metric space with respect to the Euclidean distance and that the Lebesgue measure defined on is finite. Next, by assumption, the mirrored kernel associated with is continuous and satisfies condition (6.3). Therefore by Lemma 6.4 it also satisfies (6.6). Moreover, since is compact and is continuous, it holds that

| (6.12) |

where Tr denotes the trace of a matrix in . Note that must be nonnegative on the diagonal, this can be seen for example from the expansion (6.14) used later. Next, define the linear integral operator

| (6.13) |

which is well-defined and bounded (see Theorem 9.2.4 in [17]), and denote by its kernel. Since (6.6) and (6.12) hold, we can apply a generalized version of Mercer’s theorem for matrix-valued kernels (see Theorem 4.1 in [10]), which, in combination with the auxiliary Theorem A.1 in [10], implies that there exists a countable orthonormal basis of of continuous eigenfunctions of with a corresponding family of positive eigenvalues such that

| (6.14) |

where the series converges uniformly on . Let . From (6.14) it follows that

| (6.15) | ||||

where is the counting measure on the countable index set of the eigenfunctions . In particular, is -finite.

Next, we would like to switch the order of integration on the right-hand side of (6.15) using Fubini’s theorem. In order to do that, we show that the following integral is finite, by using Young’s inequality, (6.12) and (6.14),

Let denote the matrix of ones in all entries, which is nonnegative definite as its eigenvalues are with multiplicity and with multiplicity . Moreover, for every we define

| (6.16) |

which is the Hadamard product of and . Then (6.15) and Fubini’s theorem imply

| (6.17) | ||||

This finishes the proof. ∎

Remark 6.5.

In the proof of Proposition 6.3, we use Fubini’s theorem and the counting measure to justify interchanging integration and summation, since the uniform convergence of

| (6.18) |

on does not imply the uniform convergence of

| (6.19) |

on for any as may be unbounded.

6.2 Convolution kernels

For the remainder of this section we restrict our discussion to convolution kernels of the form as in Theorem 2.14.

Proof of Theorem 2.14.

Without loss of generality, we can assume that

| (6.20) |

where the limit always exists, since is continuous, nonincreasing, nonnegative and symmetric on by assumption.

Case 1: We assume that be bounded. Then we can also assume without loss of generality that

| (6.21) |

where the limit exists by a similar argument. Now we continuously extend to by defining

| (6.22) |

Then is continuous, symmetric, nonnegative, nonincreasing and convex on . Thus, it follows from Theorem 2 in [3] that the mirrored kernel associated with the Volterra kernel on satisfies (6.6). Therefore, the continuous mirrored kernel associated with satisfies (6.6) as well. This allows us to apply Proposition 6.3 to conclude that for every ,

| (6.23) |

Case 2: We consider the case where is unbounded. Then it follows from the assumptions of the theorem that must have a singularity at , i.e. the limit of as decreases to does not exist in . Let denote the extension of to as in (6.22). Then it follows that is nonincreasing, continuous, convex, nonnegative and symmetric on . Define the sequence of convolution kernels by

| (6.24) |

and notice that it converges pointwise to on , as is continuous on . Furthermore, for every , is nonincreasing, convex, nonnegative, symmetric, continuous and thus bounded on , so that the proof of Case 1 applies to them.

In order to proceed we notice that if is symmetric nonnegative definite matrix, then all of its diagonal entries are nonnegative and we have

| (6.25) |

where we have used the fact that for and the symmetry of . This implies the second inequality of the following,

| (6.26) |

where the first inequality follows from the definition of the Frobenius norm.

Let . Using, in order of appearance below, the submultiplicativity of the Frobenius norm, Definition (6.24) and Young’s inequality, the right-hand side of (6.26), the facts that the diagonal set has -Lebesgue measure zero and that the diagonal entries of are nonincreasing on , it holds for all ,

| (6.27) | ||||

where we have used the left-hand side of (6.26), the fact that for , and finally that is in in the last three inequalities.

Now the sequence of functions

| (6.28) |

defined on converges pointwise on and thus almost everywhere to

| (6.29) |

Therefore, it follows from (LABEL:fe1) that dominated convergence can be applied to get,

| (6.30) |

which completes the proof. ∎

Proof of Corollary 2.17.

First, note that the function given by

| (6.31) |

is the convolution of the integrable function and the constant function . It follows that the convolution is integrable again (see Theorem 2.2.2 (i) in [17]), i.e.

| (6.32) |

Therefore the Volterra kernel is in for as in (2.42). Next, for any we have that . This implies that the function

| (6.33) |

is nonincreasing and convex on because is nonincreasing and convex on by assumption. Finally, the matrix

| (6.34) |

is symmetric nonnegative definite for every , since is nonnegative and is symmetric nonnegative definite. Thus, the conditions of Theorem 2.14 are satisfied. ∎

7 Proof of Lemma 2.3

Proof of Lemma 2.3.

Note that all propagator matrices from Example 2.2 except for the singular power-law kernel in Example 2.2(ii) and the non-convolution kernel in Example 2.2(v) are of the general form

| (7.1) |

for an invertible matrix and nonnegative, nonincreasing, convex functions . For the matrix exponential kernel, this follows from Example 2 in [3]. For the other kernels, an eigendecomposition of the corresponding symmetric nonnegative definite matrix yields the desired representation. Next, in order to see that , we proceed by verifying the conditions of Theorem 2.14 for the kernel . Let and . Then it follows that

| (7.2) |

is nonnegative, nonincreasing and convex on . Moreover is symmetric for any . Therefore, Theorem 2.14 applies, since is bounded and thus in .

The singular power-law kernel in Example 2.2(ii) given by

| (7.3) |

for and nonnegative definite is in due to Corollary 2.17.

For the non-convolution kernel in Example 2.2(v) we follow similar lines as in the proof of Lemma 5.4, using the fact that is nonnegative definite (see Example 2.7 in [16]) to get

Hence is a product of a nonnegative, nonincreasing, convex function taking values in and a nonnegative definite matrix , so the result follows from the argument used for examples (i)–(iv) above. ∎

References

- Abi Jaber and Neuman [2022] E. Abi Jaber and E. Neuman. Optimal liquidation with signals: the general propagator case. arXiv preprint arXiv:2211.00447, 2022.

- Abi Jaber et al. [2023] E. Abi Jaber, E. Neuman, and M. Voß. Equilibrium in functional stochastic games with mean-field interaction. arXiv preprint arXiv:2306.05433, 2023.

- Alfonsi et al. [2016] A. Alfonsi, F. Klöck, and A. Schied. Multivariate transient price impact and matrix-valued positive definite functions. Mathematics of Operations Research, 41(3):914–934, 2016. ISSN 0364765X, 15265471. URL http://www.jstor.org/stable/24736389.

- Almgren and Chriss [2001] R. Almgren and N. Chriss. Optimal execution of portfolio transactions. Journal of Risk, 3:5–40, 2001.

- Benzaquen et al. [2017] M. Benzaquen, I. Mastromatteo, Z. Eisler, and J.-P. Bouchaud. Dissecting cross-impact on stock markets: An empirical analysis. Journal of Statistical Mechanics: Theory and Experiment, 2017(2):023406, 2017.

- Bouchaud et al. [2018] J.-P. Bouchaud, J. Bonart, J. Donier, and M. Gould. Trades, Quotes and Prices: Financial Markets Under the Microscope. Cambridge University Press, 2018. doi: 10.1017/9781316659335.

- Brigo et al. [2022] D. Brigo, F. Graceffa, and E. Neuman. Price impact on term structure. Quantitative Finance, 22(1):171–195, 2022.

- Capponi and Cont [2020] F. Capponi and R. Cont. Multi-asset market impact and order flow commonality. Available at SSRN 3706390, 2020.

- Cont et al. [2023] R. Cont, M. Cucuringu, and C. Zhang. Cross-impact of order flow imbalance in equity markets. Quantitative Finance, 23(10):1373–1393, 2023.

- De Vito et al. [2013] E. De Vito, V. Umanità, and S. Villa. An extension of mercer theorem to matrix-valued measurable kernels. Applied and Computational Harmonic Analysis, 34(3):339–351, 2013.

- Ekeland and Temam [1999] I. Ekeland and R. Temam. Convex analysis and variational problems. SIAM, 1999.

- Ekren and Muhle-Karbe [2019] I. Ekren and J. Muhle-Karbe. Portfolio choice with small temporary and transient price impact. Mathematical Finance, 29(4):1066–1115, 2019.

- Gârleanu and Pedersen [2013] N. Gârleanu and L. H. Pedersen. Dynamic trading with predictable returns and transaction costs. The Journal of Finance, 68(6):2309–2340, 2013. doi: https://doi.org/10.1111/jofi.12080. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/jofi.12080.

- Gârleanu and Pedersen [2016] N. Gârleanu and L. H. Pedersen. Dynamic portfolio choice with frictions. Journal of Economic Theory, 165:487–516, 2016.

- Gatheral [2010] J. Gatheral. No-dynamic-arbitrage and market impact. Quant. Finance, 10:749–759, 2010.

- Gatheral et al. [2012] J. Gatheral, A. Schied, and A. Slynko. Transient linear price impact and Fredholm integral equations. Math. Finance, 22:445–474, 2012.

- Gripenberg et al. [1990] G. Gripenberg, S.-O. Londen, and O. Staffans. Volterra integral and functional equations. Encyclopedia of mathematics and its applications 34. Cambridge University Press, 1990.

- Horst and Xia [2019] U. Horst and X. Xia. Multi-dimensional optimal trade execution under stochastic resilience. Finance and Stochastics, 23:889–923, 2019.

- Huberman and Stanzl [2004] G. Huberman and W. Stanzl. Price manipulation and quasi-arbitrage. Econometrica, 72(4):1247–1275, 2004.

- Le Coz et al. [2023] V. Le Coz, I. Mastromatteo, D. Challet, and M. Benzaquen. When is cross impact relevant? arXiv preprint arXiv:2305.16915, 2023.

- Lehalle and Neuman [2019] C.-A. Lehalle and E. Neuman. Incorporating signals into optimal trading. Finance and Stochastics, 23:275–311, 2019.

- Markowitz [1952] H. Markowitz. Portfolio selection. The Journal of Finance, 7(1):77–91, 2024/02/28/ 1952. doi: 10.2307/2975974. URL http://www.jstor.org/stable/2975974.

- Mastromatteo et al. [2017] I. Mastromatteo, M. Benzaquen, Z. Eisler, and J.-P. Bouchaud. Trading lightly: Cross-impact and optimal portfolio execution. arXiv preprint arXiv:1702.03838, 2017.

- Obizhaeva and Wang [2013] A. A. Obizhaeva and J. Wang. Optimal trading strategy and supply/demand dynamics. Journal of Financial markets, 16(1):1–32, 2013.

- Schneider and Lillo [2019] M. Schneider and F. Lillo. Cross-impact and no-dynamic-arbitrage. Quantitative Finance, 19(1):137–154, 2019. doi: 10.1080/14697688.2018.1467033.

- Tomas et al. [2022] M. Tomas, I. Mastromatteo, and M. Benzaquen. How to build a cross-impact model from first principles: Theoretical requirements and empirical results. Quantitative Finance, 22(6):1017–1036, 2022.

- Torchinsky [2015] A. Torchinsky. Problems in real and functional analysis, volume 166. American Mathematical Soc., 2015.

- Tsoukalas et al. [2019] G. Tsoukalas, J. Wang, and K. Giesecke. Dynamic portfolio execution. Management Science, 65(5):2015–2040, 2019.