Shrinkage for Extreme Partial Least-Squares

(2) Aix Marseille Univ, CNRS, I2M, Marseille, France.

⋆ Corresponding author, stephane.girard@inria.fr )

Abstract

This work focuses on dimension-reduction techniques for modelling conditional extreme values. Specifically, we investigate the idea that extreme values of a response variable can be explained by nonlinear functions derived from linear projections of an input random vector. In this context, the estimation of projection directions is examined, as approached by the Extreme Partial Least Squares (EPLS) method–an adaptation of the original Partial Least Squares (PLS) method tailored to the extreme-value framework.

Further, a novel interpretation of EPLS directions as maximum likelihood estimators is introduced, utilizing the von Mises–Fisher distribution applied to hyperballs. The dimension reduction process is enhanced through the Bayesian paradigm, enabling the incorporation of prior information into the projection direction estimation. The maximum a posteriori estimator is derived in two specific cases, elucidating it as a regularization or shrinkage of the EPLS estimator. We also establish its asymptotic behavior as the sample size approaches infinity.

A simulation data study is conducted in order to assess the practical utility of our proposed method. This clearly demonstrates its effectiveness even in moderate data problems within high-dimensional settings.

Furthermore, we provide an illustrative example of the method’s applicability using French farm income data, highlighting its efficacy in real-world scenarios.

Keywords: Extreme-value analysis, Dimension reduction, Shrinkage, Non-linear inverse regression, Partial Least Squares.

MSC 2020 subject classification: 62G32, 62H25, 62H12, 62E20.

1 Introduction

Partial Least Squares (PLS).

In modern statistical regression situations, one has to deal with problems where the dimension of the covariates is large, and where the size of the dataset is insufficient to provide reliable estimations. Using standard (parametric or nonparametric) regression techniques in such situations may yield overfitting and therefore unstable estimations. This curse of dimensionality (Geenens,, 2011) may be mitigated by identifying a low-dimensional subspace of the covariates that maintains a strong link between the projected covariates and the response variable . As an example, Partial Least Squares (PLS) regression (Wold,, 1975) aims at estimating linear combinations of coordinates having a high covariance with . Even though PLS has been initially developed within the chemometrics field (Martens and Næs,, 1992), it has also received considerable attention in the statistical literature, see for instance Naik and Tsai, (2000). Sliced Inverse Regression (SIR, Li,, 1991) is an alternative method to estimate a so-called central dimension reduction subspace based on an inverse regression model, i.e. when is written as a function of . Several extensions have been developed for PLS and SIR, see Cook et al., (2013); Li et al., (2007) and Chiancone et al., (2017); Coudret et al., (2014); Portier, (2016) among others or Girard et al., (2022) for a review. While the above-mentioned methods adopt the frequentist point of view, there also exist a number of works in the literature based on Bayesian approaches. In Reich et al., (2011), the authors model the response variable in terms of the predictors using a mixture model whose parameters are estimated with a Markov chain Monte Carlo (MCMC) procedure. The converse point of view is adopted in Mao et al., (2010): is modelled as a function of thanks to an inverse mixture model, the estimation also requiring an MCMC method. A similar approach is proposed in Cai et al., (2021) using a Bayesian inverse regression through Gaussian processes and MCMC procedures.

Extreme Partial Least Squares (EPLS).

The curse of dimensionality is exacerbated when modelling conditional extremes since tail events are rare by nature. Nonparametric estimators of extreme conditional features (Daouia et al.,, 2013, 2023; Girard et al.,, 2021) are thus impacted both by the scarcity of extremes and the high dimensional setting. Recently, some works have introduced dimension-reduction tools dedicated to conditional extremes. One can mention Aghbalou et al., (2024); Gardes, (2018) who propose extreme analogues of the central dimension reduction subspace. In Xu et al., (2022), a semi-parametric approach is introduced for the estimation of extreme conditional quantiles based on a tail single-index model. The dimension reduction direction is estimated by fitting a misspecified linear quantile regression model. Extreme Partial Least Squares (EPLS, Bousebata et al.,, 2023) is a dimension reduction method relying on PLS principles for estimating the linear combinations of that best explain the extreme values of . See also Girard and Pakzad, (2024) for an adaptation of EPLS to functional covariates.

Shrinkage EPLS, contributions, and outline.

In this work, we develop two shrinkage versions of the EPLS method for high-dimensional settings under the common acronym SEPaLS. The starting point consists of recognizing the EPLS estimator as a maximum likelihood estimator associated with a von Mises–Fisher likelihood (Section 2). The latter distribution, which naturally arises for modelling directional data distributed on the unit sphere (Mardia and Jupp,, 1999), is here adapted to hyperballs. Two prior distributions are introduced on the dimension reduction direction in Section 3: a conjugate one based on the von Mises–Fisher distribution and a second one using the Laplace distribution (both defined on the unit sphere) to enforce sparsity. Proposition 4 and Proposition 6 show that the maximum a posteriori (MAP) estimator is available in closed form. Its computation does not require MCMC methods and can be interpreted as a shrinkage version of the initial EPLS estimator. See Figure 1 for a summary of the different PLS adaptations.

Convergence results are also established when the sample size tends to infinity, in Proposition 2, Proposition 5, and Proposition 7. The behavior of the two proposed estimators is illustrated on simulated data in Section 4, while an application on French farm income data is described in Section 5 to assess the influence of various parameters on field-grown carrot production. The functions to compute Shrinkage Extreme Partial Least Squares estimators are available in the R package SEPaLS111https://github.com/hlorenzo/SEPaLS/ (Lorenzo et al.,, 2023), while the R code replicating the figures can be found online222https://github.com/hlorenzo/SEPaLS_simus/. A discussion is provided in Section 6 and proofs are postponed to Appendix A.

2 Extreme Partial Least Squares without shrinkage

Throughout, is the Euclidean scalar product on , is the corresponding quadratic norm and is the associated unit sphere. Moreover, for any set , denotes the vector . Plus, two sequences of random variables and (where is almost surely non-zero) are equivalent in probability if which is denoted by . Also, we write if .

We first recall in Subsection 2.1 the derivation of the EPLS estimator from a statistical regression model and, in Subsection 2.2, the extreme-value assumptions necessary to establish its asymptotic properties. Subsection 2.3 is dedicated to the presentation of the von Mises–Fisher distribution on the sphere and to its adaptation to hyperballs. Based on these, we then reinterpret the EPLS direction as a maximum likelihood estimator and derive its asymptotic properties in Subsection 2.4.

2.1 EPLS model

The following single-index inverse regression model is introduced in Bousebata et al., (2023):

-

, where is the unknown direction which is the parameter of interest, and are -dimensional random vectors, is a real random variable, and is an unknown link function.

Model is referred to as an inverse regression model since the covariates are written as functions of the response variable , see Bernard-Michel et al., (2009); Cook, (2007) for similar inverse models in the SIR framework. Under model , if the distribution tail of is negligible compared to the one of , then for large values of , leading to the approximate single-index forward model . Finally, let us stress that no independence assumption is made on . Let be an sample with same distribution as .

Definition 1 (EPLS estimator of the unit direction , Bousebata et al.,, 2023).

The EPLS estimator of the unit direction is obtained by maximizing with respect to the empirical covariance between and conditionally on values of larger than :

| (1) |

where, for any threshold , is defined by

| (2) |

with, for all ,

the following first-order empirical moment

and the empirical survival function of .

The asymptotic properties of the EPLS estimator can be established under some assumptions on the distribution tails, described hereafter.

2.2 Extreme-value framework

Three assumptions on the link function and the distribution tail of and are considered. They rely on the notion of regularly-varying functions. Recall that is regularly-varying with index if and only if is positive and

for all . We refer to Bingham et al., (1987) for a detailed account of regular variations.

-

The density function of is regularly-varying of index , with .

-

The link function is regularly-varying of index and .

-

There exists such that .

Assumption implies that the survival function is regularly-varying with index , which in turn is equivalent to assuming that the distribution of is in the Fréchet maximum domain of attraction with positive tail-index , see Bingham et al., (1987, Theorem 1.5.8) and Haan and Ferreira, (2007, Theorem 1.2.1). This domain of attraction consists of heavy-tailed distributions, such as Pareto, Burr and Student distributions, see Beirlant et al., (2004) for further examples. The larger is, the heavier the tail. The restriction to ensures that the first-order moment exists for all . Assumption ensures that the link function ultimately behaves like a power function. Combined with , it implies that is heavy-tailed with tail-index . Finally, can be interpreted as an assumption on the tail of . It is satisfied, for instance, by distributions with exponential-like tails such as Gaussian, Gamma or Weibull distributions. More specifically, implies that the tail-index associated with is such that . Condition thus imposes that , meaning that has an heavier right tail than . Under model , the tail behaviors of and are thus driven by , i.e., , which is the desired property. Finally, condition implies the existence of var for all .

2.3 Two von Mises–Fisher distributions

The von Mises–Fisher distribution on the unit sphere , , is defined by its probability density function (Watson and Williams,, 1956):

where is a location parameter and is a concentration parameter. The normalizing constant is given by:

| (3) |

where is the modified Bessel function of the first kind and order defined on by

| (4) |

see Abramowitz and Stegun, (1965, Chapter 9), with the Gamma function. The von Mises–Fisher distribution on the unit sphere is widely used in the analysis of directional data and can be considered as a spherical analogue of the multivariate Gaussian distribution (Mardia,, 1975). Let us also recall that, for all , is the uniform distribution on the unit sphere (and thus, coincides with the inverse of the sphere surface) and that is the mode of the distribution for all . We propose the following adaptation of this distribution on balls:

Definition 2 (von Mises–Fisher distribution on the ball).

The von Mises–Fisher distribution on the -dimensional ball, , of radius is defined by its probability density function:

where is a location parameter and is a concentration parameter.

2.4 Maximum likelihood estimation

We first prove that the EPLS estimator, initially introduced by maximizing some empirical covariance, can also be interpreted as a maximum likelihood estimator. It is thus denoted by in the sequel.

Proposition 1 (EPLS estimator as a maximum likelihood estimator).

The EPLS estimator of Definition 1 is the maximum likelihood estimator of , denoted by , in the following model:

-

(i)

are independent and, for all , given is distributed, with location parameter , radius and concentration parameter , where is an arbitrary parameter.

-

(ii)

is distributed according to some arbitrary density on that does not depend on .

The next proposition provides a consistency result on the EPLS maximum likelihood estimator (Definition 1 and Proposition 1).

We refer to Bousebata et al., (2023) for a discussion of the assumptions on the sequence. Let us simply note that the associated rate of convergence is faster than . Even though the exact rate is not available there, this result will reveal sufficient for deriving the exact rates of convergence associated with the shrunk estimators, see Proposition 5 and Proposition 7 hereafter.

3 Shrinkage for Extreme Partial Least Squares

The result of item (i) in Proposition 1 opens the door to the construction of shrinkage estimators for based on the Bayesian paradigm, referred to as Shrinkage for Extreme Partial Least Squares (SEPaLS) estimators. A prior distribution is introduced on the direction parameter and the shrinkage effect of the maximum a posteriori (MAP) estimator is investigated. The posterior distribution is established in Subsection 3.1 and MAP estimators are derived for two particular cases of priors, a conjugate one based on the von Mises–Fisher distribution on the sphere in Subsection 3.2, and a sparse one based on the Laplace distribution in Subsection 3.3.

3.1 Posterior distribution

Combining Bayes’ rule with Proposition 1 makes it possible to derive the posterior distribution of . See Appendix A for a detailed proof.

Proposition 3 (SEPaLS posterior distribution).

The mode of the above posterior distribution is referred to as the SEPaLS estimator in the sequel. Its existence is ensured as soon as is continuous on , since a continuous function on a compact domain attains its maximum value within that domain. We focus on the computation of the SEPaLS estimator for two particular choices of described in the next two subsections.

3.2 Conjugate prior

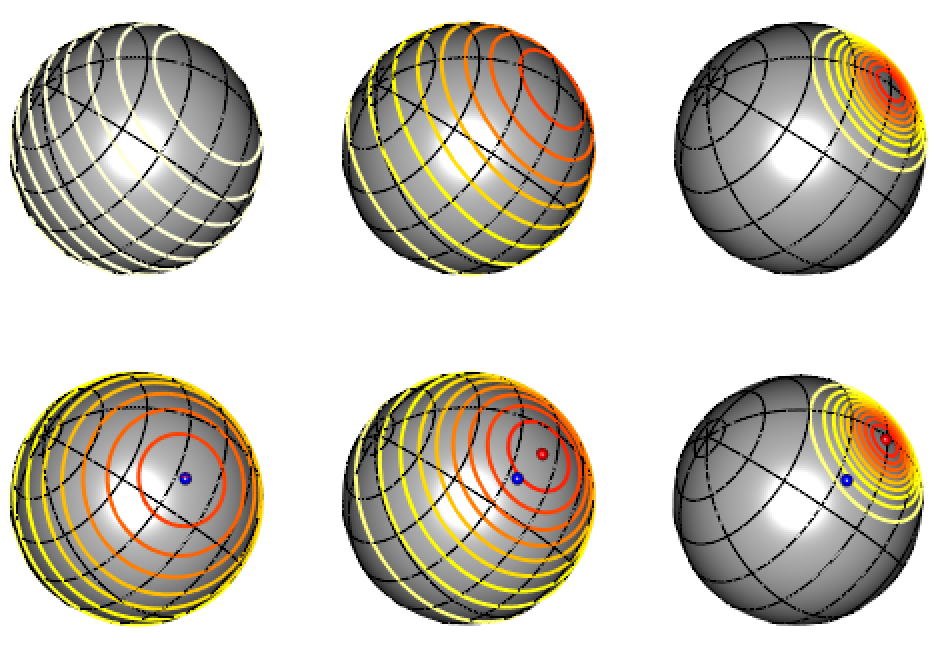

We first assume a prior distribution for the direction , with location parameter and concentration parameter . The unit vector can be interpreted as a prior on while is the confidence level on this prior. A graphical representation in dimension of the density isocontours associated with this distribution is provided on the top of Figure 2(a) for and . On the leftmost panel, the density is uniform on the unit sphere, and it becomes more peaked around as increases. Proposition 3 entails that the posterior distribution is written for any as:

which is still a distribution. As expected, since the von Mises–Fisher distribution belongs to the exponential family, considering the associated conjugate prior for yields a posterior distribution of the same type (Nunez-Antonio and Gutiérrez-Pena,, 2005; Taghia et al.,, 2014). The following proposition is easily derived.

Proposition 4 (MAP with conjugate prior).

In this conjugate framework, the computation of the MAP estimator is straightforward since the mode of the distribution coincides with the location parameter: is a linear combination of the prior direction with the EPLS estimator . Letting yields , the EPLS estimator is shrunk towards the prior direction. In contrast, setting amounts to assuming a uniform prior distribution for the direction and we thus recover the EPLS framework. This behavior is illustrated on the bottom panel of Figure 2(a) with and .

We show in the next proposition that a similar situation arises when (where ) and the rate of convergence of to is provided.

Proposition 5 (MAP consistency under conjugate prior).

Under the assumptions of Proposition 2, let and

as , then,

where denotes the projection of on the hyperplane orthogonal to .

It appears that converges to at the rate which is the classical convergence rate of most of extreme-value estimators since is the effective number of tail observations involved in the estimator. The MAP estimator can however reach a faster convergence rate when i.e. when , meaning that the prior distribution is centred on the true (unknown) direction.

3.3 Sparse Laplace prior

The EPLS method can be adapted to take into account the information that only a few covariates in are useful to explain the extreme values of the response variable . To this end, consider a Laplace distribution on the unit sphere:

| (5) |

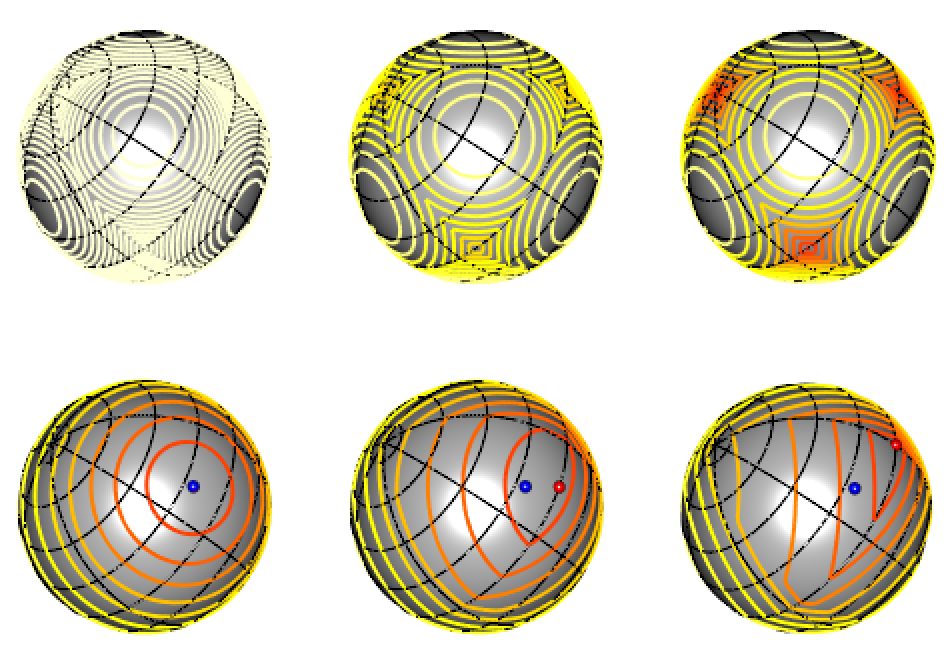

as a prior for , where is a concentration parameter. We refer to Tibshirani, (1996) for the introduction of the Laplace prior in the regression context and to Chun and Keleş, (2010); Vidaurre et al., (2013) for sparse versions of PLS in a non-extreme context. A graphical representation of the density isocontours of the Laplace distribution in dimension is provided on the top of Figure 2(b) for . On the leftmost panel, the density is nearly uniform on the unit sphere, and it becomes more peaked around the three vertices , and as increases.

As a consequence of Proposition 3, the posterior distribution can be written as

| (6) |

for any . Although this posterior distribution does not correspond to a classical distribution on the unit sphere, the MAP can be computed in closed form:

Proposition 6 (MAP with sparse prior).

The MAP is obtained by shrinking the coordinates of associated with the EPLS estimator towards zero. See Theorem 3 of Chun and Keleş, (2010) for a similar result in a non-extreme framework. The zero coordinates in correspond to covariates in that have no impact on the extreme values of . Note that when the concentration parameter is set to , we recover the EPLS method. The behavior of the estimator is illustrated on the bottom panel of Figure 2(b) with and . When is small, both estimates and are superimposed. When increases, gets closer and closer to the vertex .

Similarly to the conjugate case, when (where ), the rate of convergence of to can be established.

Proposition 7 (MAP consistency under sparse prior).

Under the assumptions of Proposition 2, let and

as , then, for all such that ,

Otherwise, if , then with probability tending to 1.

It appears that the null coordinates of are recovered with large probability thanks to the Laplace prior. Similarly to the conjugate case, the MAP estimator converges to at the usual rate. The convergence rate is higher when the non-zero coordinates of all coincide: for all such that .

4 Illustration on simulated data

4.1 Experimental design

The behavior of the SEPaLS estimators and is illustrated on the regression model with power link function: , . The output variable is distributed from a Pareto distribution with survival function , and with tail-index . Each margin , of the error is simulated as the absolute value of a random variable and depending on using the Clayton copula, an Archimedean copula (Nelsen,, 2007, Section 4), defined for all by

where is a parameter tuning the dependence between the margins. Equivalently, the joint cumulative distribution function of is given for all by the one-factor model (Krupskii and Joe,, 2013):

where denotes the cumulative distribution function of the standard Gaussian distribution. Note that represents the independence copula while, as , which represents the co-monotonicity copula. The dependence between the margins is assessed using Kendall’s tau and is thus limited to positive values. We shall also consider the associated rotated copula defined by whose Kendall’s tau is negative and given by , for all . Here, leads to four possible values of the Kendall’s tau: .

The standard deviation is selected such that the signal-to-noise ratio, defined as , is equal to 10. Note that represents the approximate maximum value of on a -sample from the distribution with associated survival function .

The sample size is fixed to and two dimensions are considered: . The true direction is for both dimensions.

The location parameter of the prior distribution (conjugate case) is set either to , which corresponds to a perfect prior, or to , which is far from the true one, see Subsection 3.2. Four values of the concentration parameter are investigated: . In the case of the Laplace prior (sparse case), we let . In both situations, we set since this parameter is irrelevant to the inference.

4.2 Performance assessment

Let us define a similarity measure between the theoretical vector and its MAP estimator computed on replications as follows:

| (7) |

where denotes the MAP estimate on the replication under either the conjugate or the sparse prior. Clearly and the closer is to 1, the larger the proximity is. In practice, is computed as a function of the number of exceedances , where denotes the largest observation from the sample .

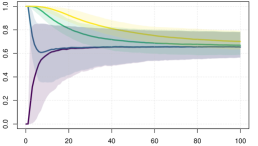

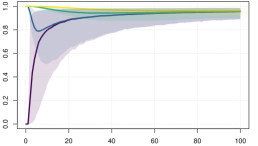

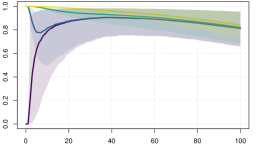

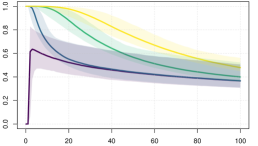

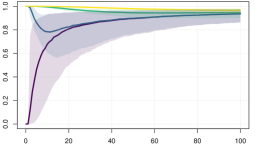

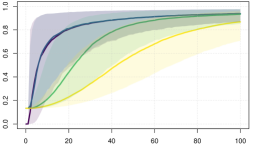

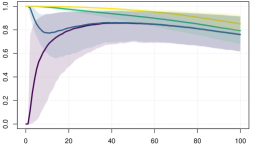

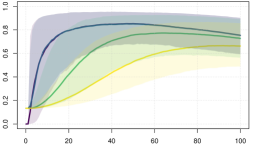

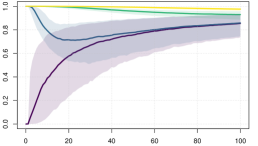

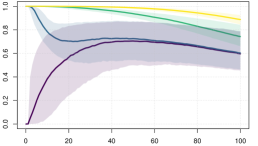

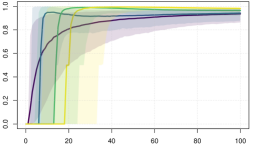

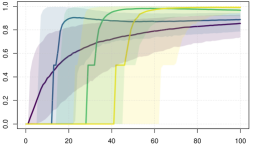

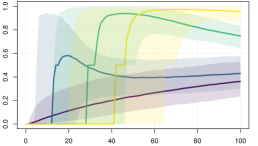

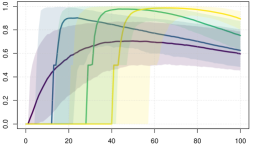

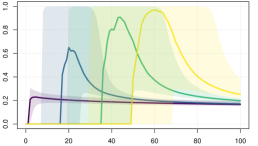

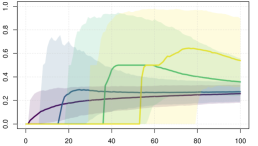

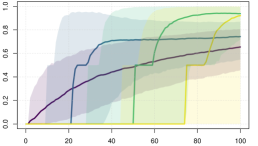

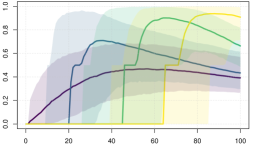

| Conjugate prior and link function with . | ||

|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4.3 Results

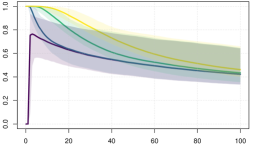

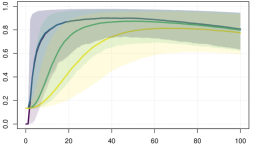

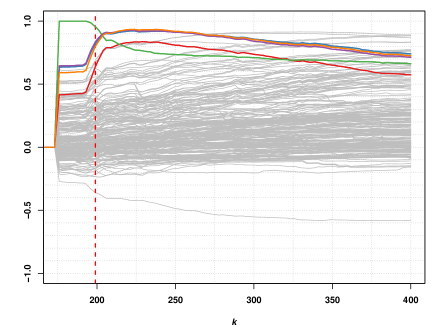

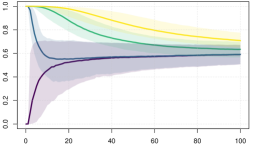

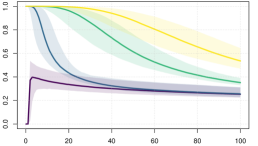

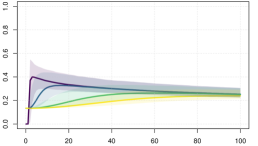

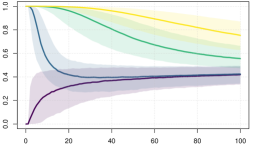

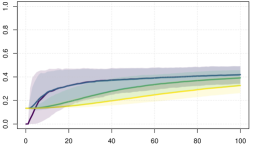

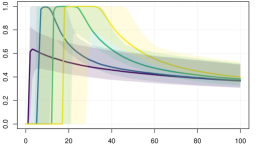

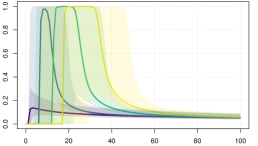

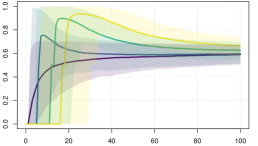

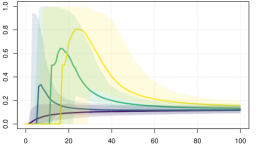

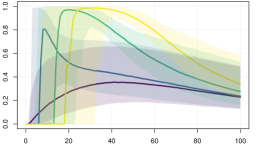

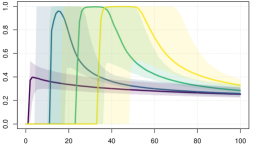

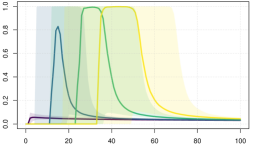

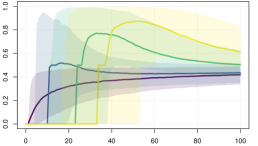

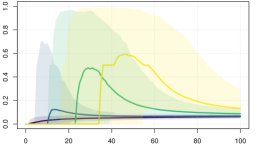

Conjugate prior. The similarity measure between and is represented as a function of on Figure 3 for the choice of parameter . See Figure 6 and Figure 7 in Appendix B for the cases . Each of these figures considers 32 configurations in dimension : , , and , see Subsection 4.1 for details. Unsurprisingly, when i.e. when the prior direction points towards the true one, the shrinkage improves the results of the original EPLS estimator (obtained when ). Moreover, it reduces the sensitivity with respect to the number of exceedances , the dependence degree , and the exponent of the link function. In all situations, one can obtain with . In contrast, when , the prior direction is ill-adapted since and too large values of deteriorate the EPLS estimator. As expected, the choice of is of primary importance in the conjugate prior.

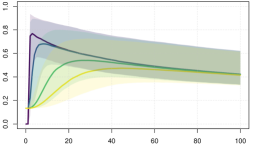

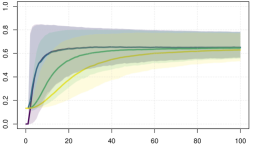

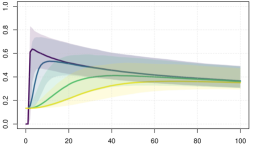

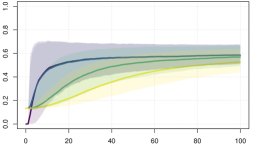

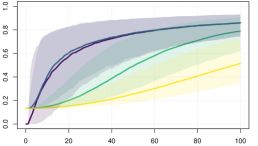

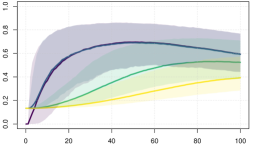

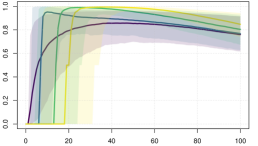

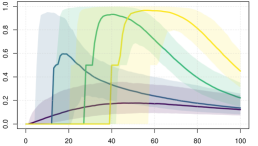

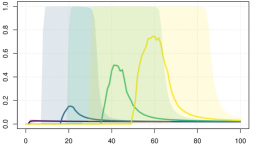

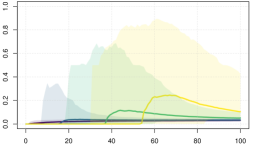

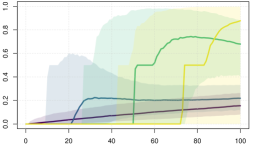

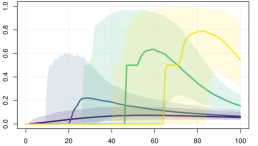

Sparse prior. Similarly, the similarity measure between and is represented as a function of on Figures 8–10 in Appendix B for the cases . Each of these figures considers 32 configurations: , , and . Here, the shrinkage always improves the results of the original EPLS estimator (obtained when ) since the true direction is rather sparse, it only has two non-zero coordinates. Enforcing sparsity allows to obtain (resp. ) in dimension (resp. ) with exponents . The case of small exponents appears to be more complicated, the maximum value of depending on the dimension and on the dependence degree .

5 Application to real data

The SEPaLS method is illustrated on data extracted from the Farm Accountancy Data Network (FADN)333Available in French at:

https://agreste.agriculture.gouv.fr/agreste-web/servicon/I.2/listeTypeServicon/..

This dataset targets French farms described by numerous qualitative and quantitative variables over the period 2000–2015.

Here, we focus on the farms producing field-grown carrots.

The response variable is the production of carrots (in quintals) and the covariate is made of continuous variables

including meteorological and economic measurements.

Our goal is to investigate, among the 259 collected factors, which ones may influence

the upper tail of , i.e. are linked to large productions of carrots.

A similar study could be achieved on the small productions of carrots by focusing on the upper tail of .

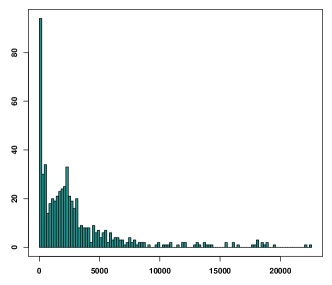

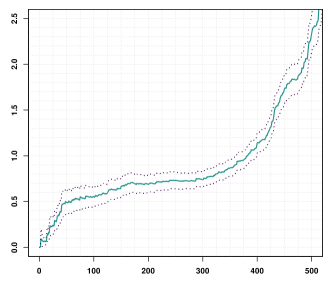

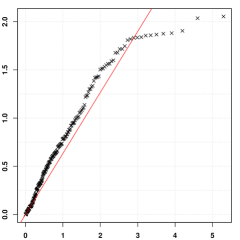

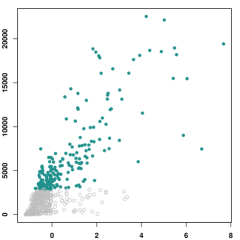

Three visual checks are first carried out in Figure 4 to verify whether the heavy-tail hypothesis on is realistic. The histogram of the on the top left panel is skewed to the right and has a heavy right tail. Besides, the Hill estimator (Hill,, 1975)

of the tail-index is drawn on the top right panel as a function of . The resulting graph is stable on the range and points towards . Finally, selecting (this choice is discussed below), the associated quantile-quantile plot of the log-excesses against the quantiles of the unit exponential distribution, , exhibits a linear trend (bottom panel) which is further empirical evidence that the heavy-tail assumption is appropriate, see Beirlant et al., (2004, pp.109–110).

|

Frequency |

|

|

|

|

|

|

|

|

In the following, we focus on the sparse estimator since the use of would require an initial guess for which is not obvious in this application context. The next two conditional tail correlation measures are introduced to interpret the results obtained with :

| (8) | ||||

| (9) |

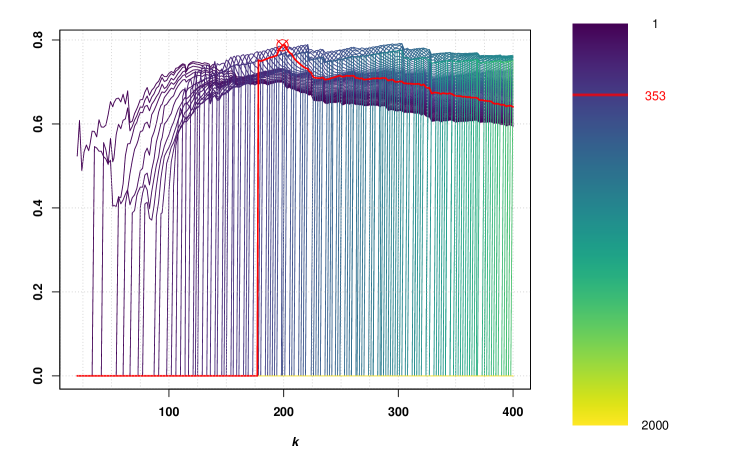

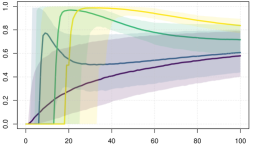

with . The role of the tail correlation measure (8) is to assess the correlation in the tail between the response variable and the summary of the predictors built by the SEPaLS method. It is computed at the threshold and plotted on Figure 5(a) as a function of the number of exceedances for several levels of shrinkage . Note that, when is small, the correlation vanishes for a wide range of values since, in this case, the prior weight is too large compared to the likelihood one. The global maximum is located at which corresponds to a stable region of the Hill estimator according to Figure 4. The maximum correlation () is reached at .

|

|

|

|

|

The role of the tail correlation measure (9) is to assess the correlation in the tail between the summary of the predictors built by the SEPaLS method and the initial ones , . It is computed at the threshold and plotted on Figure 5(b) as a function of the number of exceedances for . All correlation curves feature nice stability with respect to , especially in the neighbourhood of .

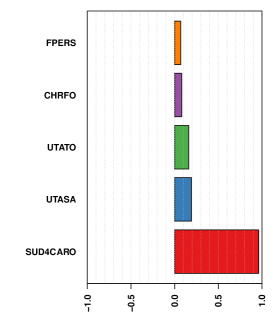

In the sequel, we thus select and . With these choices, only 5 coordinates of out of 259 are estimated to non-zero values, see Figure 5(c) for an illustration and Table 1 for a description of the selected variables. Meteorological variables are discarded since large productions of carrots do not seem to depend on weather conditions. Remarking on Figure 4 that the summary variable is positively correlated with the high values of , one can conclude that, unsurprisingly, large productions are associated with large cultivated areas (SUD4CARO), large amounts of work both in terms of time (UTASA, UTATO) and remuneration charges (FPERS), and large investments in supplies (CHRFO).

| Selected variables | Description | Units | |

|---|---|---|---|

| SUD4CARO | Area cultivated with field-grown carrots | hectares | 0.978 |

| UTASA | Salaried work | UTA(⋆) | 0.158 |

| UTATO | Salaried and not salaried work | UTA(⋆) | 0.124 |

| CHRFO | Actual cost of stored supplies | euros | 0.038 |

| FPERS | Remuneration charges | euros | 0.026 |

(⋆) UTA: amount of work associated with one full-time working person during one year.

6 Discussion

We proposed a Bayesian interpretation of the EPLS model to introduce prior information on the direction of dimension reduction for extreme values. Two examples of shrinkage priors are provided: a conjugate von Mises–Fisher prior allowing to consider an initial guess on the direction, and a Laplace prior enforcing sparsity on the estimated direction. Finite sample experiments demonstrate that the proposed method is effective in high dimension ( on simulated data and on real data) with moderate sample sizes ( on simulated data and on real data). Here, we limited ourselves to the estimation of one single direction, but the SEPaLS method can easily be adapted to the estimation of multiple directions using the iterative procedure described in Bousebata et al., (2023, Section 4). We also focused on prior distributions yielding explicit shrinkage estimators. It would be of interest to investigate the use of other priors: either uninformative priors such as Jeffreys’ one (Harold,, 1946) or other shrinkage priors (van Erp et al.,, 2019) can be considered. The computation of the posterior mode estimate would rely on an MCMC procedure.

Acknowledgements

This work is partially supported by the French National Research Agency (ANR) in the framework of the Investissements d’Avenir Program (ANR-15-IDEX-02). J. Arbel acknowledges the support of ANR-21-JSTM-0001 grant. S. Girard acknowledges the support of the Chair “Stress Test, Risk Management and Financial Steering”, led by the French Ecole Polytechnique and its Foundation and sponsored by BNP Paribas.

References

- Abramowitz and Stegun, (1965) Abramowitz, M. and Stegun, I. A. (1965). Handbook of Mathematical Functions: With Formulas, Graphs, and Mathematical Tables. Dover Publications.

- Aghbalou et al., (2024) Aghbalou, A., Portier, F., Sabourin, A., and Zhou, C. (2024). Tail inverse regression: Dimension reduction for prediction of extremes. Bernoulli, 30(1):503–533.

- Beirlant et al., (2004) Beirlant, J., Goegebeur, Y., Teugels, J., and Segers, J. (2004). Statistics of Extremes: Theory and Applications. Wiley, Chichester, England, UK.

- Bernard-Michel et al., (2009) Bernard-Michel, C., Gardes, L., and Girard, S. (2009). Gaussian Regularized Sliced Inverse Regression. Statistics and Computing, 19(1):85–98.

- Bingham et al., (1987) Bingham, N. H., Goldie, C. M., and Teugels, J. L. (1987). Regular Variation. Encyclopedia of Mathematics and its Applications. Cambridge University Press.

- Bousebata et al., (2023) Bousebata, M., Enjolras, G., and Girard, S. (2023). Extreme Partial Least-Squares. Journal of Multivariate Analysis, 194:105101.

- Cai et al., (2021) Cai, X., Lin, G., and Li, J. (2021). Bayesian inverse regression for supervised dimension reduction with small datasets. Journal of Statistical Computation and Simulation, 91(14):2817–2832.

- Chiancone et al., (2017) Chiancone, A., Forbes, F., and Girard, S. (2017). Student Sliced Inverse Regression. Computational Statistics & Data Analysis, 113:441–456.

- Chun and Keleş, (2010) Chun, H. and Keleş, S. (2010). Sparse Partial Least Squares Regression for Simultaneous Dimension Reduction and Variable Selection. Journal of the Royal Statistical Society: Series B, 72(1):3–25.

- Cook, (2007) Cook, R. D. (2007). Fisher Lecture: Dimension Reduction in Regression. Statistical Science, 22(1):1–26.

- Cook et al., (2013) Cook, R. D., Helland, I. S., and Su, Z. (2013). Envelopes and Partial Least Squares Regression. Journal of the Royal Statistical Society: Series B, 75(5):851–877.

- Coudret et al., (2014) Coudret, R., Girard, S., and Saracco, J. (2014). A new sliced inverse regression method for multivariate response. Computational Statistics & Data Analysis, 77:285–299.

- Daouia et al., (2013) Daouia, A., Gardes, L., and Girard, S. (2013). On kernel smoothing for extremal quantile regression. Bernoulli, 19(5B):2557–2589.

- Daouia et al., (2023) Daouia, A., Stupfler, G., and Usseglio-Carleve, A. (2023). Inference for extremal regression with dependent heavy-tailed data. The Annals of Statistics, 51(5):2040–2066.

- Gardes, (2018) Gardes, L. (2018). Tail dimension reduction for extreme quantile estimation. Extremes, 21(1):57–95.

- Geenens, (2011) Geenens, G. (2011). Curse of dimensionality and related issues in nonparametric functional regression. Statistics Surveys, 5:30–43.

- Girard et al., (2022) Girard, S., Lorenzo, H., and Saracco, J. (2022). Advanced topics in Sliced Inverse Regression. Journal of Multivariate Analysis, 188:104852.

- Girard and Pakzad, (2024) Girard, S. and Pakzad, C. (2024). Functional Extreme Partial Least-Squares. hal-04488561.

- Girard et al., (2021) Girard, S., Stupfler, G., and Usseglio-Carleve, A. (2021). Extreme conditional expectile estimation in heavy-tailed heteroscedastic regression models. The Annals of Statistics, 49(6):3358–3382.

- Haan and Ferreira, (2007) Haan, L. and Ferreira, A. (2007). Extreme Value Theory. Springer, New York, NY, USA.

- Harold, (1946) Harold, J. (1946). An invariant form for the prior probability in estimation problems. Proceedings of the Royal Society of London: Series A, 186(1007):453–461.

- Hill, (1975) Hill, B. M. (1975). A Simple General Approach to Inference About the Tail of a Distribution. The Annals of Statistics, 3(5):1163–1174.

- Krupskii and Joe, (2013) Krupskii, P. and Joe, H. (2013). Factor copula models for multivariate data. Journal of Multivariate Analysis, 120:85–101.

- Li, (1991) Li, K.-C. (1991). Sliced Inverse Regression for Dimension Reduction. Journal of the American Statistical Association, 86(414):316–327.

- Li et al., (2007) Li, L., Cook, R. D., and Tsai, C.-L. (2007). Partial inverse regression. Biometrika, 94(3):615–625.

- Lorenzo et al., (2023) Lorenzo, H., Girard, S., and Arbel, J. (2023). SEPaLS: Shrinkage for Extreme Partial Least-Squares in R. R package.

- Mao et al., (2010) Mao, K., Liang, F., and Mukherjee, S. (2010). Supervised Dimension Reduction Using Bayesian Mixture Modeling. In Proceedings of the Thirteenth International Conference on Artificial Intelligence and Statistics, pages 501–508.

- Mardia, (1975) Mardia, K. V. (1975). Distribution Theory for the Von Mises-Fisher Distribution and Its Application. In A Modern Course on Statistical Distributions in Scientific Work, pages 113–130. Springer Netherlands, Dordrecht.

- Mardia and Jupp, (1999) Mardia, K. V. and Jupp, P. E. (1999). Directional Statistics. John Wiley & Sons, Chichester, England, UK.

- Martens and Næs, (1992) Martens, H. and Næs, T. (1992). Multivariate Calibration. Wiley, Hoboken, NJ, USA.

- Naik and Tsai, (2000) Naik, P. and Tsai, C.-L. (2000). Partial Least Squares Estimator for Single-Index Models. Journal of the Royal Statistical Society: Series B, 62(4):763–771.

- Nelsen, (2007) Nelsen, R. B. (2007). An Introduction to Copulas. Springer, New York, NY, USA.

- Nunez-Antonio and Gutiérrez-Pena, (2005) Nunez-Antonio, G. and Gutiérrez-Pena, E. (2005). A Bayesian analysis of directional data using the von Mises-Fisher distribution. Communications in Statistics-Simulation and Computation, 34(4):989–999.

- Portier, (2016) Portier, F. (2016). An Empirical Process View of Inverse Regression. Scandinavian Journal of Statistics, 43(3):827–844.

- Reich et al., (2011) Reich, B. J., Bondell, H. D., and Li, L. (2011). Sufficient Dimension Reduction via Bayesian Mixture Modeling. Biometrics, 67(3):886–895.

- Taghia et al., (2014) Taghia, J., Ma, Z., and Leijon, A. (2014). Bayesian estimation of the von-Mises Fisher mixture model with variational inference. IEEE Transactions on Pattern Analysis and Machine Intelligence, 36(9):1701–1715.

- Tibshirani, (1996) Tibshirani, R. (1996). Regression Shrinkage and Selection via the Lasso. Journal of the Royal Statistical Society: Series B, 58(1):267–288.

- van Erp et al., (2019) van Erp, S., Oberski, D. L., and Mulder, J. (2019). Shrinkage priors for Bayesian penalized regression. Journal of Mathematical Psychology, 89:31–50.

- Vidaurre et al., (2013) Vidaurre, D., van Gerven, M. A. J., Bielza, C., Larrañaga, P., and Heskes, T. (2013). Bayesian Sparse Partial Least Squares. Neural Computation, 25(12):3318–3339.

- Watson and Williams, (1956) Watson, G. S. and Williams, E. J. (1956). On the Construction of Significance Tests on the Circle and the Sphere. Biometrika, 43(3):344–352.

- Wold, (1975) Wold, H. (1975). Soft Modelling by Latent Variables: The Non-Linear Iterative Partial Least Squares (NIPALS) Approach. Journal of Applied Probability, 12:117–142.

- Xu et al., (2022) Xu, W., Wang, H. J., and Li, D. (2022). Extreme Quantile Estimation Based on the Tail Single-index Model. Statistica Sinica, 32(2):893–914.

Appendix A Appendix: Proofs

This first lemma establishes that is a proper density function integrating to one.

Lemma 1.

Proof of Lemma 1.

The change of variable leads to

and switching to polar coordinates yields

From the definition of the modified Bessel function (4) as a power series with infinite radius of convergence, one has:

Taking account of , it follows

leading to

which concludes the proof. ∎

Proof of Proposition 1.

For any , in view of (2), the optimization problem (1) can be rewritten as:

| (10) |

Under model , the triangle inequality yields and thus, conditionally on , belongs to the ball centred at 0 with radius . The optimization problem (10) can be rewritten in terms of densities associated with the distribution as

It appears that can be interpreted as the estimator maximizing the likelihood conditionally on . Since the density of does not depend on , one also has

and thus can also be viewed as the unconditional maximum likelihood estimator of . ∎

The next lemma will reveal useful in the proof of Proposition 2 below.

Lemma 2.

Let and be positive real sequences with as . Let be a random vector in , a non-random vector, and a sequence of random vectors in such that

Then,

where denotes the projection of on the hyperplane orthogonal to .

Proof of Lemma 2.

Let . From the assumption of convergence in distribution, we have that converges in distribution to a Dirac mass at 0. Clearly,

and inverting the latter equality yields

Replacing in the expression of , we obtain

and therefore

which is the desired result. ∎

Proof of Proposition 2.

Proof of Proposition 3.

In view of Bayes’ rule, the posterior distribution of is given by

Since does not depend on , the posterior distribution can be simplified as

and the result is proved. ∎

Proof of Proposition 5.

Proof of Proposition 6.

In view of (6), the MAP estimator is given by:

Introducing and so that , the above optimization problem can be rewritten as

Clearly, the solution w.r.t. is given by for all and therefore

where

Let us introduce the two sets of indices

such that where

The minimum of the non-negative term is reached for , . The negative term corresponding to negative values of remains and the problem can be rewritten as

One can recognise a problem of minimization of projection on the vector of negative terms which is solved for positive terms defined by

One can notice that , and therefore

The result is thus proved.

∎

Proof of Proposition 7.

Let us recall the notation introduced in the proof of Proposition 5: . Combining Proposition 6 and Proposition 2, it follows that with, for all :

where . Two cases arise:

-

•

If then, clearly, with probability tending to one, since and as .

-

•

If , then and entail as and, therefore, with probability tending to one,

(11)

As a consequence, one has, with probability tending to one,

since . It follows that

with probability tending to one, leading to

Combining with (11), one has, for all such that ,

or equivalently,

and proves the result. ∎

Appendix B Appendix: Additional figures

We provide below additional figures corresponding to the illustration on simulated data presented in Section 4. They correspond to the use of the conjugate prior with parameter (while the case can be found in the main text), and the sparse prior with parameter .

| Conjugate prior and link function with . | ||

|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Conjugate prior and link function with . | ||

|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Sparse Laplace prior and link function with . | ||

|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Sparse Laplace prior and link function with . | ||

|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Sparse Laplace prior and link function with . | ||

|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|