Equitable Pricing in Auctions111This material is based upon work supported by the National Science Foundation under Grant No. DMS-1928930 and by the Alfred P. Sloan Foundation under grant G-2021-16778, while Simon Finster and Bary Pradelski were in residence at the Simons Laufer Mathematical Sciences Institute (formerly MSRI) in Berkeley, California, during the Fall 2023 semester. Simon Mauras received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation program (grant agreement No. 866132), as a postdoctoral fellow at Tel Aviv University.

Abstract

We study how pricing affects the division of surplus among buyers in auctions for multiple units. Our equity objective may be important, e.g., for competition concerns in downstream markets, complementing the long-standing debate on revenue and efficiency. We study a canonical model of auctions for multiple indivisible units with unit demand buyers and valuations with a private and a common component and consider all pricing rules that are a mixture (i.e., a convex combination) of pay-as-bid and uniform pricing. We propose the winners’ empirical variance (WEV), the expected empirical variance of surplus among the winners, as a metric for surplus equity. We show that, for a range of private-common value proportions, a strictly interior mix of pay-as-bid and uniform pricing minimizes WEV. From an equity perspective, auctions with a higher private value component benefit from more price discrimination, whereas only auctions with a sufficiently high common value justify a more uniform pricing rule. We provide a criterion under which strictly mixed pricing dominates uniform pricing, a partial ranking of different mixed pricing formats, and bounds on the WEV-minimizing pricing under the assumption of log-concave signal distributions. In numerical experiments, we further illustrate the WEV-minimal pricing as a function of the private-common-value mix.

1 Introduction

Multi-unit auctions are ubiquitous, finding applications across diverse domains such as treasury auctions, electricity markets, carbon emission trading, and beyond, more recently in the sale of fractionalized art and collectibles. The study of pricing rules, their impact on efficiency and revenue, and the inherent trade-offs involved have a long-standing tradition in both the theoretical and applied economic literature (Wilson (1979), Back & Zender (1993), Ausubel et al. (2014)). Perhaps the most prominent pricing rules studied are pay-as-bid pricing, where each winner pays their submitted bid price, and uniform pricing, where a single clearing price is paid by all winners. While revenue and welfare assessments typically focus on the distribution of auction surplus between buyers and sellers, the question of how this surplus is distributed among buyers (or sellers) has garnered limited attention.

In practice, the allocation of surplus among buyers may be of significant importance, as inequity may influence the stability and competitiveness of the downstream market after an auction, or it may enter the auctioneer’s welfare considerations. For example, major financial institutions, acting as primary dealers in high-stake treasury bond auctions, play an intermediary role between governments and retail consumers.777OECD (2021) finds in a survey that both pay-as-bid and uniform pricing are used: 25 out of 36 countries use pay-as-bid pricing and 21 out of 36 countries use uniform pricing (some use both). The government may prefer an equitable distribution of surplus between the primary dealers so they compete more effectively in the retail market. Similarly, electricity wholesale companies engage in spot and forward markets for power generation. Emission certificates, vital inputs for production, are routinely distributed through auctions, impacting the producing companies’ competitiveness in the downstream market. Welfare considerations may be relevant to market platforms selling their goods and services in auctions, as they may wish to create an attractive market for a wide range of traders. When the seller is a public entity, welfare considerations naturally enter the picture. We here aim to initiate the theoretical study of surplus considerations among buyers in auctions by developing novel insights into how pricing rules affect the distribution of buyer surplus.

We consider multi-unit auctions for the sale of goods with a composition of private and common values: part of the goods’ value is private to a buyer and information about it is only known to them, while another part of the goods’ value is common to all buyers. For example, an emission certificate may be necessary for a company to complete their production process, and the company derives a certain, privately known value from it. However, the emission certificate can also be resold after the auction, and its resale value is common to all potential buyers in the market. Our main finding is that if the good sold in the auction has a higher private value component, higher price discrimination, i.e., moving towards pay-as-bid pricing, distributes the auction surplus more equitably among buyers. Conversely, if the good has a higher common value component, steering towards a uniform market clearing price distributes surplus more equitably.

Our results are derived in the canonical model of auctions for indivisible goods: we consider standard auctions for the supply of finitely many identical units and bidders with single-unit demand, a well-studied model of auctions that, analytically, resembles the single-unit setting (e.g., Ortega-Reichert (1968), Krishna (2009), Anderson & Holmberg (2021)). We choose this model as it sharpens the focus of our analysis: All considered auctions, under classical assumptions, achieve the same expected revenue and allocate items efficiently to the highest-value buyers; we can thus study the distribution of surplus without having to consider potential trade-offs with revenue and efficiency. Thus, in our comparison of surplus equity between different pricing formats we may choose a surplus distribution measure without compromising other performance indicators. Our value model linearly interpolates between the extremes of pure private values and pure common values. The common value is defined as the average of the private values of all bidders, representing an approximate valuation of resale opportunities that is common to all bidders.888This model has been used in previous work by, e.g., Bikhchandani & Riley (1991), Krishna & Morgan (1997), Klemperer (1998) , Bulow & Klemperer (2002), Goeree & Offerman (2003). We call the interpolation parameter modulating between the private value and the common value the private-common-value mix, or simply the common value component.

On one extreme of pricing rules, we consider the common uniform pricing rule, where all winners pay the first rejected bid (FRB) in the auction. On the other extreme of pricing rules, we consider pay-as-bid (or discriminatory) pricing, under which all winners pay their own bid. We also consider convex combinations of uniform and pay-as-bid pricing and call this -mixed pricing (where corresponds to uniform pricing and corresponds to discriminatory pricing). In all auctions, losers are assumed to pay nothing.999Identical and closely related versions of mixed pricing have been considered, e.g., by Wang & Zender (2002), Viswanathan & Wang (2002), Armantier & Sbaï (2009), Ruddell et al. (2017), Woodward (2021).

Our analysis relies on the assumption of bidder symmetry as well as increasing and symmetric strategies. Empirical evidence suggests that the symmetric model is relevant in practice: for example, Armantier & Lafhel (2009) find that information between participants in auctions by the Bank of Canada is nearly symmetric, and Hortaçsu et al. (2018) conclude that in U.S. Treasury auctions for short-term securities bidders are close to symmetric. Hattori & Takahashi (2022) also find that symmetry between bidder also largely holds in Japanese treasury auctions. On the contrary, for example in French auctions for government bonds, bidders are more asymmetric (Armantier & Sbaï 2006, 2009) and similarly in Mexico’s treasury auctions (Cole et al. 2022). While bidder asymmetry may be an important characteristic for some markets, the analysis of surplus distribution remains, for now, intractable.101010With bidder asymmetries in size or downstream output (and hence value distribution functions), it is not clear that surplus equity in absolute terms is desirable; instead, a measure of proportionality may be relevant.

To study surplus equity in symmetric markets, we need to define an appropriate metric. The literature has proposed several prominent measures of inequality in wealth or income (Lorenz (1905), Gini (1912), Gini (1921), Pigou (1912), Dalton (1920), Atkinson (1970), Sen & Foster (1973)). Our choice for measuring equity is the expected empirical variance of surplus among the winners of an item. We call this metric winners’ empirical variance, or WEV. We choose this metric for two reasons:

First, WEV fulfills two foundational axioms of surplus inequality measures (see, e.g., Patty & Penn (2019)): (i) the Pigou-Dalton transfer principle, requiring that any transfer of surplus from a poorer to a better-off agent must increase the inequality metric, and (ii) symmetry, requiring that any reassignment of surplus among agents would result in the same inequality metric.111111Note that mean independence and replication invariance are not relevant in our setting, as only equal-size bidding environment with identical value distributions are ranked. Furthermore, WEV is closely linked to the Gini-coefficient; in particular, all the rankings of pricing rules with respect to surplus equity in terms of WEV, implied by the assumptions made, also hold for the Gini coefficient.

Second, WEV is, as we demonstrate, a combined measure of within-bidder variation and across-bidder correlation of surpluses (Lemma 1). In particular, surplus may vary due to variation in a bidder’s own signal and their competitors’ signals, and the surplus derived by one bidder may affect the surplus (through a price-setting bid) of another bidder.

The within-bidder variation of surplus is measured by the bidder’s ex-ante variance of surplus, and thus relates to risk attitudes. Focusing on a single bidder, the ex-ante variance was used to compare the variation of surplus across different auction formats in early work by Vickrey (1961). When multiple items are sold, however, multiple bidders may earn a positive surplus, opening up the question of surplus distribution across participating bidders.

In our bidding environment, for a given realization of signals, surplus only varies among the winners because all considered auctions are efficient, i.e., items are assigned to the highest value bidders. Thus, a difference in variation of surpluses between auction formats may only stem from the winning bidders. Consequently, our primary concern is the distribution of surplus among the winners. More generally, in settings where the number of winners may vary, or where bidders are asymmetric, surplus equity among all bidders may also be of interest.

Our main results consider how the winners’ empirical variance (WEV) varies with the choice of auction. This crucially depends on the private-common-value mix. We also introduce monotone ex-post utility, a sufficient condition for some of our results. A bidding equilibrium satisfies monotone ex-post utility if, in the pairwise comparison of any two signals, the higher signal results in a higher realized utility.

-

1.

For a range of private-common-value mixes, , there exist -mixed auctions that have lower WEV than pay-as-bid and uniform auctions (cf., Theorem 1).

-

2.

Given an -mixed auction, if the equilibrium bid functions are not ‘too steep’, then it has lower WEV than the uniform-price auction (cf., Theorem 2).

-

3.

Given a private-common-value mix , if the equilibrium satisfies monotone ex-post utility, then WEV is monotonically decreasing in (cf., Theorem 3).

-

4.

For log-concave signal distributions, given a private-common-value mix , the WEV-minimal mixed-pricing is bounded from below by , and any -mixed auction with has lower WEV than the uniform-price auction (cf., Theorem 4).

It is a straightforward observation that, with pure common values, there is no variation in bidder surplus, that is, uniform pricing is optimal in terms of WEV. When the private value portion increases, the results are more nuanced: our sufficient conditions show that, for a large class of signal distributions and associated bidding functions, inequality measured by WEV is lower in the pay-as-bid auction compared to the uniform-price auction. In general, for any distributions, it holds that the larger the common value component in item valuations the less steep the bid functions are allowed to be. We also provide a counterexample to prove that there indeed exist (rather extreme) equilibrium bid functions which result in counter-intuitive phenomena: in such cases, the uniform-price auction results in lower WEV even for pure private values.

While our main results prove existence of some WEV-minimal -mixed auctions and bounds on the WEV-minimal value of , we also provide numerical experiments. For a variety of signal distributions and given private-common value mixes, the landscape of WEV-minimal -pricing designs are computed, which can be seen to be unique.

1.1 Related literature

The analysis of within-agent variation of surplus goes back to Vickrey (1961), who showed that the ex-ante variance of surplus is lower in a single-unit first-price than in a single-unit second-price auction for uniform distributions of private values. More generally, the distribution of equilibrium prices in a second-price auction is a mean-preserving spread of the distribution of equilibrium prices in a first-price auction (Krishna 2009), which implies that the variance of bidder surplus is greater in the second-price than in the first-price auction for any private-value distribution. While the within-agent variation relates to risk attitudes, the study of equity concerns must take into account across-bidder variation of surplus, the subject of our analysis. Crucially, we study how the proportion of common value affects the distribution of surplus.

The study of common values in auctions started with Wilson (1969, 1977) and was further pioneered by Wilson (1979), who showed that share auctions may result in significantly lower revenue, regardless of uniform or discriminatory pricing, than an auction for an indivisible unit. Milgrom & Weber (1982) consider the statistical correlation between bidders’ signals and provide revenue comparisons in a more general framework of private, common, and correlated values for single-unit auctions. Klemperer (1998) show that even in ascending common-value auctions with just two players, multiple (potentially asymmetric) equilibria may exist. Under revenue considerations, a first-price auction may be the better choice for common-value and almost common-value goods. We add the new dimension of surplus equity to these considerations, making a case for uniform pricing in auctions for predominantly common-value goods.

Our multi-unit auction model with unit demand bidders is based on the work of Ortega-Reichert (1968) and Krishna (2009). Slightly generalizing their results, we derive explicit formulas for bid functions in the -auction with private and common values. Our model of private and common values resembles the one used in Goeree & Offerman (2003) in the context of a single-unit auction. The focus of their study is on uncertainty about the common value component, demonstrating that higher uncertainty results in greater expected inefficiency in the auction. Interestingly, Goeree & Offerman (2003) assume log-concave signal distributions for all their results, as we do for some of ours. While we prove that log-concavity ensures monotone ex-post utility, they require log-concavity to show that, for each bidder, the private and the common part of the signal are positively correlated in expectation.121212We (and the authors themselves) note that their definition of surplus only encompasses the private information available to a bidder, in contrast to our standard definition of surplus.

A convenient simplification in our model is the assumption of unit demand, which allows us to focus on the distribution of surplus across bidders as the auctions we consider are then efficient and revenue equivalence holds. A series of articles analyzes strategic bidding in multi-unit auctions with multi-unit demand, in which supply is assumed to be continuous and stochastic. For example, Ausubel et al. (2014) show that bids for the marginal unit can influence the price of inframarginal units and incentivize bidders to shade their bids for different units differently and to reduce their demand. Most generally, this may result in ambiguous efficiency and revenue rankings between uniform and pay-as-bid pricing, also depending on equilibrium selection. As Pycia & Woodward (2018) show, revenue equivalence does hold in the truthful-bidding equilibrium of an optimally designed uniform-price auction and the optimally designed pay-as-bid auction, and both equilibria are efficient.131313Their design parameters for revenue optimality are reserve prices and supply uncertainty Bidding strategies are derived for the case where bidders’ signals are fixed and values symmetric, i.e., common values. Similarly, Woodward (2021) analyze mixed-price auctions for a divisible supply, where bidders have a pure common signal. They focus on equilibrium characterization and revenue comparisons.141414Woodward (2021) show that, with linear marginal values, the unique equilibrium of the pay-as-bid auction yields higher revenue than any equilibrium of the uniform-price auction. In contrast with this strand of the literature, our model allows for explicit equilibrium bid functions for mixed private-common values assuming a fixed, indivisible supply. We consider our model, in which revenue and efficiency equivalence holds across the considered pricing formats, more apt to develop results on equity concerns that are unaffected by potential revenue and efficiency trade-offs.

Redistributive concerns in markets are also studied from a mechanism-design perspective. E.g., Akbarpour et al. (2024) consider ‘non-market’ mechanisms which allocate goods at below-market-clearing prices. They characterize when non-market mechanisms are optimal for a designer to allocate a fixed supply of goods of different qualities. Individuals’ characteristics are partially private, and, contrasting our analysis of equilibrium behavior, the authors exploit the statistical correlation between those characteristics to characterize the optimal incentive-compatible and individually rational mechanism. Reuter & Groh (2020) study the allocation of a number of goods to unit demand agents. The agents are heterogeneous in their marginal utilities for money and, additionally, the designer has an ex-ante budget constraint. They contrast the utilitarian optimal allocation with the ex-post efficient allocation and consider ‘within-agent’ and ‘between-agents’ redistributive motives, reminiscent of the within-bidder variation and across-bidder variation of surplus in our work. In a similar vein, Dworczak et al. (2021) characterize a mechanism that yields the optimal trade-off between efficiency and redistribution in a buyer-seller market. Considering a market without money, Pycia & Ünver (2017) characterize the class of group strategy-proof and efficient mechanisms for the allocation of a multi-unit supply of a resource to unit demand agents, and assess equality in outcomes across all top-trading-cycle mechanisms.

Outline

The remainder of the article is organized as follows. Section 2 introduces the model and Section 2.1 shows that in our model, revenue equivalence and efficiency hold. In Section 3 we introduce our measure of surplus equity, the winners’ empirical variance. Section 4 derives equilibrium bidding strategies and a series of monotonicity properties. Section 5 contains our main results. In Section 6 we present numerical experiments illustrating our findings. Finally, Section 7 provides a discussion.

2 Model

There are bidders competing for a fixed supply of identical items , where . Each bidder only demands one item and receives a private signal , which is drawn independently for each bidder at random from the interval , , and distributed according to some probability distribution absolutely continuous with respect to the Lebesgue measure with density . We call , i.e., all signals so that , the open support of , and we assume that over . We also assume that the signals have finite second moment .

For , a collection of iid signals distributed according to some distribution with density , we denote by the -th highest value of the collection , i.e., is the maximum and is the minimum, and by its distribution with corresponding density . Functions and are given by Fisz (1965) as

and

| (1) |

Equivalently, we can write

Private and common values.

Bidder ’s value for an item is given by the valuation function , where (the value of is symmetric in other agents’ signals).

Assumption 1 (Bidder values).

We assume the following functional form for the bidder’s values , where is the common value parameter.

Our model interpolates between common values and private values, where the common value parameter encodes to what extent the signal of the other bidders influence the value for any bidder. In particular, is the pure common value case and is the pure private value case. We consider auction mechanisms in which each bidder makes a single bid . The price for bidder in an auction is given by , which is symmetric across buyers.151515Symmetric means that for some pricing function . Bidder’s utility are quasi-linear, i.e., when winning an item of value and paying price the utility (or surplus) is given by . We only consider symmetric and monotonically increasing bidding strategies , and auctions where the highest bids win. Thus, the utilities are only a function of signals:

We will denote equilibrium bidding strategies by .

In an alternative model, the common value might be distributed according to some prior distribution, and the bidders’ private signals are drawn conditional on the realization of this common value. As Goeree & Offerman (2003) point out, the model where the common value component is the average of all bidders’ signals and the alternative model have identical qualitative characteristics: (i) the items are valued equally by all bidders in the common value component, and (ii) the winner’s curse is present, i.e., winning an item is ‘bad news’, in that the winner’s expectation of the item’s value was likely too optimistic.

Pricing formats.

We consider standard auctions with the following pricing formats: For given each winning bidder pays . For a given , we call this -mixed pricing. At one boundary, for , this resolves to first-rejected-bid uniform pricing or short uniform pricing, where each winning bidder pays the -st highest bid . At the other boundary, for , this resolves to pay-as-bid pricing, where each winning bidder pays their bid . Finally, if we say that the auction (or the pricing) is strictly mixed.

Expected values.

Given a buyer with signal , recall that we denote by the -th highest signal among the other signals, with probability distribution , and density . We define the expected value given and as follows:

Observe that because is continuous and non-decreasing, is continuous and non-decreasing in and .161616In fact, in our model it is strictly increasing in . We define .

Auction properties.

We say that an auction is standard if the highest bids win the items.171717Cf. Krishna (2009). An auction is a winners pay auction if only winners pay and no more than their bid. An auction is efficient if, in equilibrium, the bidders with the highest values are allocated the items.

2.1 Revenue equivalence and efficiency

We next recall results from Krishna (2009) that show that the auctions we consider exhibit revenue equivalence and (allocative) efficiency. In the following, we allow value functions more general than 1. We only assume that is symmetric in , continuous in each signal and monotone in the sense that for any and (if all signals are larger, the value is larger)181818In particular, this implies that is differentiable almost everywhere..

Proposition (Revenue equivalence, Krishna (2009)).

Assuming iid signals, any standard auction, under any symmetric and increasing equilibrium with an expected payment of zero at value zero, yields the same expected revenue to the seller.

We note that the crucial assumption for revenue equivalence is the independence of signals. In settings where signals are correlated, revenue equivalence fails (Krishna 2009, Chapter 6.5). It can be further shown that a bidder with signal has an expected surplus

A value function satisfies the single crossing condition if for all and for all , . Naturally, the value function as given in 1 is single-crossing.

Proposition (Efficiency, Krishna (2009)).

Any standard auction, under any symmetric and increasing equilibrium and values satisfying the single-crossing condition, is efficient.

Given the prior propositions, we can focus on the question of surplus distribution among buyers more succinctly without considering potential trade-offs.

3 Measuring surplus equity

Our metric to assess surplus equity is the expected empirical variance of surplus among the winners of an item; recall its discussion in Section 1. We call this metric winners’ empirical variance, or short WEV. Note that while all our results actually hold ex-post, we choose to define our metric in expectation. This ensures that the metric gives rise to a total ranking over all auctions and does not depend on the realizations of signals, which would result in competing rankings. In expectation, equilibrium surplus varies due to different factors: a bidder’s own and their competitors’ signals, and surplus between winners may be correlated.

Definition 1 (Winners’ empirical variance (WEV)).

By simple algebra, an equivalent expression for WEV is given by

We also define the empirical variance among all bidders (thus including losers) in the auction, given by , which can also be expressed as a sum of squared differences. The ex-ante variance of a winner is . Using symmetry between bidders, an alternative expression is given by , and analogous definitions hold when not conditioning on winning an item.191919Note that the notions which concern only winning bidders can only be sensibly defined for winners pay auctions.

Recall that our metric fulfills two of the basic axioms of surplus inequality measures (e.g., Patty & Penn (2019)), namely the Pigou-Dalton transfer property, as well as symmetry. Mean independence and replication invariance are not relevant in our model, because we consider an equal-size bidding environment with identical value distributions. We argue in Section 7.3 that our metric is also closely linked to the Gini coefficient.

As we consider efficient auctions, surplus only varies among the winners in the auctions. Among those winners, WEV measures variation and correlation of surplus, i.e., it measures surplus dispersion across bidders. In contrast, the ex-ante variance measures only surplus variation within a given bidder. The ex-ante variance can be interpreted as follows: let a bidder participate in many repeated auctions, keeping all model parameters are fixed across repetitions, redrawing in every auction. The variation in surplus the bidder experiences between different auctions is due to different realizations of signals.

Lemma 1.

The empirical variance can be written as , and the winners’ empirical variance as .

Lemma 1 reveals that the empirical variance has a component that measures only variation within bidder and a component that measures the correlation between surpluses. A related expression involves the second moment of surplus and is given in the full proof in Section A.1. Finally, we note that a ranking of auction formats in terms of ex-ante variance or winners’ ex-ante variance is identical. A ranking with respect to the empirical variance, however, may differ depending on if only winners are considered, or all bidders. This observation holds in our model only in the case of pure private values, when ex-post individual rationality is given.

Lemma 2.

Assuming that the auction is a winners pay auction, the empirical variance and the ex-ante variance can be decomposed, respectively, as and .

Recall that does not depend on the auction format (by revenue equivalence), while does. The full proof is given in Section A.1.

The focus of our main results will be the WEV metric.

4 Equilibrium bidding

We start by deriving the Bayes-Nash equilibrium in symmetric and increasing bid function. This Bayes-Nash equilibrium is the center of our analysis of surplus equity. All proofs are given in Section A.2.

Proposition 1 (Krishna (2009)).

The equilibrium bidding strategy in the uniform pricing auction, i.e., the case , is given by .

We note that the equilibrium is unique in the class of symmetric and increasing strategies. With pure private values the strategy is weakly dominant (see also Krishna (2009)).

Proposition 2.

The unique symmetric equilibrium bidding strategy in the -mixed-price auction, for , is given by

| (2) |

An alternative representation is given by

| (3) |

Our analysis makes use of the alternative representation as well as the following monotonicity properties of the equilibrium strategy, with proofs given in Section A.2.

Proposition 3.

The equilibrium bid functions satisfy the following monotonicity properties:

-

1.

is strictly increasing in , for all fixed .

-

2.

is strictly decreasing in , for all fixed .

-

3.

the derivative is strictly increasing in , for all fixed .

-

4.

the derivative is strictly increasing in , for all fixed .

Proposition 4.

The equilibrium bid function satisfies the following continuity properties:

-

1.

is jointly continuous over .

-

2.

is jointly continuously differentiable over and .

We further define a crucial monotonicity property of the bidders’ realized utilities.

Definition 2 (Monotone ex-post utility).

The ex-post utility of a winner is monotonically increasing iff . We say that an equilibrium satisfies monotone ex-post utility if for any two winning signals , monotone ex-post utility holds.

Furthermore, we can relate this property to the derivative of the bid functions by the following lemma. The proof is given in Section A.2.

Lemma 3.

An equilibrium satisfies monotone ex-post utility iff for all signals .

5 Main results: surplus equity

We now turn to our main objective and analyze how to design an auction that minimizes the winners’ empirical variance, i.e., is WEV-minimal. As it turns out this depends crucially on the extent of the common value, .

5.1 WEV-minimality of strictly mixed pricing auctions

To gather intuition, consider one of the boundary cases: with pure common values (), the ex-post utilities among winners are equalized if everyone pays the same price, leading to zero winners’ empirical variance. Once the private value component enters the value function with a non-zero weight (), chosing an auction that minimizes WEV is much less obvious. Our first step is to show that, without any further assumptions, strictly interior -mixed pricing minimizes WEV for a range of private-common value mixes. We formalize this in Theorem 1.

Theorem 1.

For any signal distribution:

-

1.

For a pure common value auction, i.e., , the uniform-price auction () minimizes WEV, in particular, .

-

2.

For a non-pure common value auction, i.e., , the uniform-price auction does not minimize WEV among all -auctions.

-

3.

There exists such that for any , the pay-as-bid auction () does not minimize WEV, in particular it has a higher WEV than the uniform auction.

Thus, for the WEV-minimal auction is neither the pay-as-bid nor the uniform-price auction, but strictly mixed.

Proof.

To prove (1), note that for , the realized value is identical for all bidders as . In a uniform-price auction each bidder pays the same, so all bidders have identical surplus, leading to an empirical variance of surplus among winners of zero. For any , the payment differs across winners with strictly positive probability and hence the winners’ empirical variance is strictly greater than zero.

For (2) we only present a proof sketch and the full proof is given in Lemma 6. We take the derivative of with respect to . The term inside the expectation can be dominated by an integrable random variable by the assumption that has a finite second moment, which allows us to use dominated convergence and exchange derivative and expectation. Finally, the limit of and of as goes to are, respectively, and . This yields , which is strictly negative as is strictly increasing.

Finally, we prove (3). Note that WEV is continuous and at it is strictly lower for uniform pricing ( than for pay-as-bid pricing () by (1). Thus, by the mean value theorem, there exists an open interval , , such that, for any , WEV remains strictly lower under uniform pricing than pay-as-bid pricing. ∎

5.2 Ranking -mixed-price auctions

Having established the importance of strictly mixed pricing, i.e., pricing between pay-as-bid and uniform pricing, we characterize how surplus equity changes as a function of the design parameter , that is, the extent of pay-as-bid versus uniform pricing, for any given private-common-value mix . A sufficient condition, demanding that bid functions be not too steep, allows us to compare the WEV of any -mixed auction with the uniform-price auction (Theorem 2). With the slightly stronger condition of monotone ex-post utility (cf., Definition 2), we establish a partial ranking of -mixed auctions in terms of WEV (Theorem 3). Furthermore, with another condition on bid functions, using a generalized mean value theorem, we are able to compare any two -mixed auctions. This is formally stated in Theorem 5 in Section A.2. Our sufficient conditions are relatively weak as they allow a large class of bid functions (see also Lemma 3), but strong in the sense that they are requirements on equilibrium outcomes. Of course, monotone ex-post utility and its relaxations need not always hold, and as we will see in Section 5.4, the failure thereof may indeed cause the theorems to break down.

Theorem 2.

For a given common value component , consider any -mixed auction, , and suppose the equilibrium bidding function satisfies for all signals . Then, WEV is lower for -mixed pricing than uniform pricing.

Proof.

Let denote bidder ’s utility in the -mixed auction, and let denote bidder ’s utility in the uniform-price auction. Now let be two winning bidders. As above, (resp. ) denotes the symmetric equilibrium bid function in the -mixed (resp. uniform-price) auction. Let denote the first rejected bid. Then, canceling out , we have

where . It also holds that

We will now show that is a non-expansive mapping. Note that can be increasing or decreasing, so we need to show that . We have . As is increasing in , holds whenever . Therefore

| (4) |

Taking the square of Eq. 4 we obtain the result point-wise, for each pair of winning signals and and, taking the expectation, the theorem follows. ∎

Theorem 3.

For a given common value component and for some , if the equilibrium satisfies monotone ex-post utility, then WEV is monotonically decreasing over .

Proof.

First, we prove that WEV is locally decreasing in . Let and and with denote the signals of two winning bidders and . We define as done previously. Note that because of Proposition 3 (3), monotone ex-post utility holds for all . For all , , we have

| (5) | ||||

| (6) | ||||

| (7) |

For the final equivalence, observe that monotone ex-post utility together with Proposition 3 (1) implies that is non-expansive, allowing to remove the absolute value in Eq. 6. Proposition 3 (4) guarantees that Eq. 7 holds. As the ex-post difference in utilities (Eq. 5) is decreasing in , so is its expectation. To establish global monotonicty on , note that if then it also holds for any by Proposition 3 (3), concluding the proof. ∎

To summarize, an -mixed-price auction is better than all auctions with less discriminatory pricing, if monotone ex-post utility holds for a given common value component (Theorem 3). Our Theorem 2 proves that for a large class of signal distributions and associated bidding functions, namely those satisfying a relaxation of monotone ex-post utility, uniform pricing is not optimal in terms of surplus equity. Moreover, by Theorem 3 if monotone ex-post utility holds, i.e., the slope of the equilibrium bid function is sufficiently flat, moving closer to uniform pricing will not improve surplus equity. Note that, by inspection of Lemma 3, the higher the common value component, the more stringent the sufficient conditions from Theorems 2 and 3 become.

5.3 Log-concave signal distributions

Monotone ex-post utility and its relaxations are imposed on equilibrium outcomes rather than primitives. In this section, we derive more succinct characterizations and bounds restricting our attention to the large class of log-concave signal distributions.

Definition 3.

We say that a real-valued function is log-concave if is concave.

In the following, we denote by a minimizer in of WEV.

Theorem 4.

Assume signals are drawn from a log-concave distribution. Then, for a given common value component , (i) the WEV-minimal mixed pricing is bounded from below by , and (ii) any mixed-price auction with , has lower WEV than the uniform-price auction ().

Theorem 4 provides a simple yet powerful bound on the WEV-minimal pricing rule and we prove it below. In Section 6, we show numerically that this bound is indeed a good heuristic, especially for high values of . For low values of , the heuristic even coincides with . If signal or value distributions are unknown, an exact calculation of the WEV-minimal pricing rule may be difficult in practice. Our bound, however, is robust for a large class of distributions. The following corollaries provide further characterizations.

Corollary 1.

Assuming log-concave signal distributions and , the pay-as-bid auction () yields lower WEV than the uniform-price auction.

The proof is immediate by setting in Theorem 2. Our numerical experiments in Section 6 indicate that, for , pay-as-bid pricing may often even be WEV-minimal.

Corollary 2.

Assuming log-concave signal distributions and pure private values (), the pay-as-bid auction () is WEV-minimal among all -mixed auctions.

The proof is immediate by setting in Theorem 3.

We now turn to the proof of Theorem 4. We first derive a proposition that relies on a series of lemmas given in Section A.2.

Proposition 5.

If the signal density is log-concave, then for all signals .

Proof sketch.

The core argument has three parts as detailed in Lemma 9. First, by differentiating twice , we can see that its log-concavity is equivalent to . Second, using closure properties of product and integration of log-concave distributions, the log-concavity of follows from the log-concavity of . Third, since order statistics conditioned on other order statistics behave just like order statistics of a truncation of the original distribution, a more tractable expression of the expected valuation can be derived for the pure common value case, , and similar log-concavity arguments imply that for all signals . As is a linear combination of a bidder’s private signal and in the pure common value case, extends to all . Inspection of given yields the conclusion. ∎

Note that this bound on the derivative implies that, in the private value setting, the ex-post utility is non-decreasing for log-concave signal distributions. Indeed, for , we have that .

We can now prove Theorem 4:

Proof of Theorem 4.

Using Proposition 5, we apply Theorems 2 and 3 to derive bounds on . Indeed, Theorem 2 always holds if . Thus, given any with , the -auction has lower WEV than the uniform-price auction. Similarly, Theorem 3 always holds if . Hence, given any with , WEV is decreasing in , and thus . ∎

Remark 1.

Note that, while we gave simple general conditions to obtain bounds on , better bounds can be obtained by considering specific signal distributions. Indeed, while can be difficult to compute analytically even for simple distributions, it is sometimes possible to compute . For example, for the uniform distribution we have , which yields . Similarly, for the exponential distribution and thus (with being constant).

5.4 Non-monotone ex-post utility

Theorems 2, 3 and 4 show that, generally, provided that the common value component is not too large, a certain degree of price discrimination is beneficial to achieve an equitable surplus distribution. However, these results are crucially based on monotone ex-post utility and its relaxations, which itself relies on well-behaved equilibrium bid functions, whose slope cannot be too steep. In the following, we give an example of a ‘non-well-behaved’ bid function and prove that uniform pricing may be preferred to pay-as-bid pricing in terms of WEV, even with pure private values. However, the signal distributions needed for this result are quite extreme.

Example 1.

Consider an auction with bidders and items. We consider a value model where signals are distributed uniformly on and the (pure private) value is given by a function , where

and we fix .

The following remark shows that choosing a continuous function would yield a value model exactly equivalent to ours. However, for simplicity, we choose a function , which is not continuous and is not strictly increasing. We analyze the example ignoring these concerns, as all the properties we use can be obtained by approximation with continuous and monotone functions.202020This is, generally, not admissible for revenue equivalence and for the equilibrium bid with uniform pricing. However, the non-continuous function may be perturbed by a small noise that ensures continuity, sufficiently small to not affect our results in the limit.

Remark 2.

If is continuous and strictly increasing, there is a bijection mapping between this value model with uniform signals and our original model with arbitrary signal distributions: is simply given by in the original model, the inverse of the cdf of signals. The slight change of model allows us to present the example more succinctly.

For signal , the bid functions for and are given by

Rewriting the WEV as

and using the distribution of above, we can bound the WEV in the uniform-price auction and the pay-as-bid auction. For large , it holds that and , thus showing that uniform-pricing has lower WEV than pay-as-bid pricing. The computational details are given in Section A.4.

6 Numerical experiments

We further illustrate the effect of the private-common value mix on surplus equity by presenting several numerical examples. We compute the WEV-minimal pricing (in terms of ) for any given private-common value mix (parameterized by ). We note that the computation of equilibrium bid functions is computationally very expensive. Our experiments rely on theoretical simplifications, such as Lemma 9 (Section A.2) and Lemma 10 (Section A.3).

The simulations are performed through numerical integration of our analytical formulae. The efficiency and accuracy of the code rely on various techniques. Most importantly, we rewrite all multi-dimensional expectations as nested one-dimensional integrals (with variable bounds) which we compute by integrating polynomial interpolations. Second, the code makes sure that each quantity is computed at most once, using memorization. Finally, some quantities (such as bidding functions) have multiple analytical expression, among which we choose the best, depending on the value of the signal (e.g., Equation 3 can be integrated more efficiently than Equation 2, but is less accurate for small signals). Our code is available on github.

Example 2.

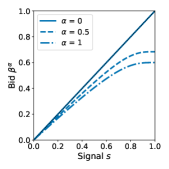

There are bidders competing for items. The signals are sampled uniformly from . For this signal distribution, one can easily compute , and accordingly . Note that is only linear because of the uniform signals; for more complex distributions it is not straightforward to compute . Fig. 1 illustrates the bid functions for four different values of .

(a) *

(b) *

(b) *

font=footnotesize,margin=0.5cm,0.5cm

font=footnotesize,margin=0.5cm,0.5cm

(c) *

font=footnotesize,margin=0.5cm,0.5cm

(c) *

font=footnotesize,margin=0.5cm,0.5cm

(d) *

(d) *

Note that increasing the common value component shifts the optimal bids for low signal realizations above the 45-degree line. A bidder with a low signal has an expectation of the average signal that is higher than their bid. Equally, for high signals, the ‘truthful’ bid in the uniform-price auction shifts below the 45-degree line. A bidder with a high signal knows that the average signal is lower than their own. The truthful bid in the uniform-price auction is given by the expected value for any signal . This effect is a consequence of the winner’s curse with common values, which bidders, in equilibrium, are attempting to salvage, but cannot escape. We note that, with pure common value, i.e., , and uniform signals, ex-post utilities are decreasing in signals (by analogy with Definition 2).

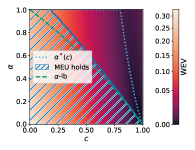

We show the winners’ empirical variance corresponding to these equilibria in Fig. 3. In line with Theorem 4 — noting that the uniform distribution is log-concave —, the figure illustrates that with a high private value component (low ), pay-as-bid pricing () minimizes WEV; with higher common value components (high ), strictly mixed pricing for some minimizes WEV (cf., Theorem 1); and with pure common values (), uniform pricing () minimizes WEV (cf., Theorem 1).

![[Uncaptioned image]](/html/2403.07799/assets/x5.png) Figure 2: WEV as a function of for uniform signals

Figure 2: WEV as a function of for uniform signals

![[Uncaptioned image]](/html/2403.07799/assets/x6.png) Figure 3: WEV-minimizing design , monotone ex-post utility (MEU), and a lower bound on (-lb) for uniform signals

Figure 3: WEV-minimizing design , monotone ex-post utility (MEU), and a lower bound on (-lb) for uniform signals

Indeed, we can compute the optimal design parameter for every given private-common-value mix . We illustrate this in Fig. 3, which presents the WEV as a function of and . We also illustrate the parameter combinations for which monotone ex-post utility holds and the lower bound for for the uniform distribution, which is given by (cf., Theorem 4 and Remark 1). Note that for small common value parameter (), monotone ex-post utility holds for any and thus pay-as-bid pricing () is WEV-minimal (cf., Theorem 3). Eventually, for larger , the WEV-minimal pricing is strictly mixed () and for the uniform auction is WEV-minimal (cf., Theorem 1). Notice also that the WEV at the minimal decreases in . Naturally, with a higher common value share in the overall value, bidders’ values given different signal realizations, as well their bids, move closer together, thus explaining smaller differences in utilities ex-post as well as in expectation.

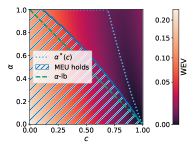

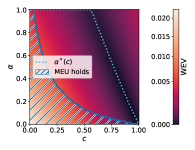

We further illustrate the optimal design for three other signal distributions in Fig. 4. The truncated exponential and the normal distribution are log-concave. Note that for the truncated exponential, we show the lower bound (cf., Remark 1) on , and for the normal distribution we show the lower bound (cf., Theorem 4). In addition, we show for which combinations of and the condition of monotone ex-post utility holds. Note that the Beta distribution with shape parameters is not log-concave. Thus, we are not able to provide a theoretical lower bound on the WEV-minimal design . However, the region where monotone ex-post utility holds can be found numerically, and its ‘frontier’ provides a lower bound for the WEV-minimal design . Notice that the region where monotone ex-post utility holds is much smaller for the Beta distribution, i.e., for many - combinations, our theorems cannot speak to the monotonicity of WEV. However, monotonicity in seems to hold even in this example (for any given ), up to . Indeed, monotone ex-post utility is sufficient, but not necessary for the monotonicity of WEV.

0ptTruncated exponential

0ptTruncated normal

0ptBeta

7 Discussion

Our results center around the winners’ empirical variance and some require regularity assumptions. We now discuss how our results relate to within-agent variation and the empirical variance among all bidders, how the regularity assumptions imposed are necessary for our lines of argument, and finally offer possible extensions with respect to other measures of equity and multi-unit demand.

7.1 Equity and risk aversion

As previously noted, surplus equity and distributional concerns are distinct from questions of within-agent variation and associated risk preferences, e.g., risk aversion. An appropriate measure to assess the latter is, e.g., the ex-ante variance. While the two notions are distinct, the measures are linked through Lemmas 1 and 2. In addition, for the pure private value setting, we derive the following result:

Proposition 6.

In the pure private value setting (), the pay-as-bid auction minimizes the ex-ante variance of surplus among all standard auctions with increasing bid functions.

The proof is given in Section A.4. Because of revenue equivalence, note that the previous proposition also implies that the second moment of the surplus is minimal in the pay-as-bid auction among standard auctions. The second moment of surplus links the winners’ empirical variance and the empirical variance among all bidders, as shown in Lemma 2. Hence, using Theorem 2 for the pure private value case and Lemma 2, we have the following corollary:

Corollary 3.

In the pure private value setting (), consider any -mixed auction, , and suppose the equilibrium bidding function satisfies for all signals . Then, the empirical variance (among all bidders) is lower for -mixed pricing than uniform pricing.

This illustrates that some of the results we derived for the winners’ empirical variance also translate to the empirical variance among all bidders. However, in general this may not be the case, as the second moment of surplus may have a significant effect. To study surplus distribution in efficient auctions, the WEV appears to be the natural and unconfounded metric.

7.2 Assumptions on signal distributions and bid functions

Consider the pay-as-bid and the uniform-price auction for simplicity. The crucial ingredient for Theorem 4 is that the derivative of the equilibrium bid function is bounded by , which holds for log-concave distributions by Proposition 5. In particular, the density of the first rejected signal must be log-concave. Log-concavity is equivalent to concavity (a generalization of convexity, see Anderson et al. (2007)), and is thus equivalent to concavity of . One idea to extend our results could then be to consider other generalizations of convexity. Considering Theorem 2, one might attempt to bound the slope of the bid functions by . It holds that is equivalent to concavity of the same function where is the harmonic mean. But contrary to concave functions, there are no simple group closure properties that allows for the concavity of to always imply that of . Thus, this route of inquiry does not carry fruits.

We also note that conditions on the slope of bid functions such that uniform pricing yields lower WEV than pay-as-bid pricing, are much more difficult to attain. Why is that? If we follow the same main ideas of the proof of Theorem 2, a similar condition using the mean value theorem would be that, for all , is an expansive mapping, translating into . As is strictly positive, it must hold that . For signal distributions with bounded density, is close to zero near (this follows from the definition of order statistics), and therefore is close to zero for a non-zero interval of signals, and thus cannot hold for all signals on the support. Thus, our proof technique does not readily extend to yield conditions for uniform pricing to have lower WEV than pay-as-bid pricing.

7.3 Possible extensions

Most of our results stem from comparisons of ex-post utility. Therefore, all our rankings of pricing rules with respect to WEV also hold for other equity measures that build on the pairwise comparison of surplus. A prominent measure among those is the Gini coefficient, a version of which may be adapted to our setting as the ‘expected Gini coefficient among winners’ . The only technical difference is a normalization by the expected surplus and absolute values of pairwise differences instead of squares. Similarly, employing the range of surpluses as an equity metric would yield the same rankings of pricing formats as our results. Beyond those measures involving pairwise comparisons, it may be an interesting direction for future research to show robustness with respect to other common inequality metrics.

An important consideration in our work is the restriction to efficient and revenue-equivalent auctions. While this allows to focus on a single design objective, surplus equity, the trade-offs between efficiency, revenue, and equity may be interesting in itself. An interesting setting to consider may be multi-unit auctions with multi-unit demand, where items may be allocated inefficiently Ausubel et al. (2014), and efficiency and revenue comparisons become relevant.

References

- (1)

- Akbarpour et al. (2024) Akbarpour, M., Dworczak, P. & Kominers, S. D. (2024), ‘Redistributive allocation mechanisms’, Journal of Political Economy Forthcoming.

- Anderson & Holmberg (2021) Anderson, E. & Holmberg, P. (2021), Multi-unit auctions with uncertain supply and single-unit demand, Ifn working paper no. 1460, 2023, https://www.ifn.se/media/cssdutm1/wp1460.pdf.

- Anderson et al. (2007) Anderson, G. D., Vamanamurthy, M. & Vuorinen, M. (2007), ‘Generalized convexity and inequalities’, Journal of Mathematical Analysis and Applications 335, 1294–1308.

- Armantier & Lafhel (2009) Armantier, O. & Lafhel, N. (2009), Comparison of auction formats in Canadian government auctions, Technical report, Bank of Canada Working Paper, https://www.bankofcanada.ca/2009/01/working-paper-2009-5/.

- Armantier & Sbaï (2006) Armantier, O. & Sbaï, E. (2006), ‘Estimation and comparison of treasury auction formats when bidders are asymmetric’, Journal of Applied Econometrics 21(6), 745–779.

- Armantier & Sbaï (2009) Armantier, O. & Sbaï, E. (2009), ‘Comparison of alternative payment mechanisms for french treasury auctions’, Annals of Economics and Statistics/Annales d’Économie et de Statistique pp. 135–160.

- Arnold et al. (2008) Arnold, B. C., Balakrishnan, N. & Nagaraja, H. N. (2008), A first course in order statistics (classics in applied mathematics).

- Atkinson (1970) Atkinson, A. B. (1970), ‘On the measurement of inequality’, Journal of Economic Theory 2(3), 244–263.

- Ausubel et al. (2014) Ausubel, L. M., Cramton, P., Pycia, M., Rostek, M. & Weretka, M. (2014), ‘Demand Reduction and Inefficiency in Multi-Unit Auctions’, Review of Economic Studies 81, 1366–1400.

- Back & Zender (1993) Back, K. & Zender, J. F. (1993), ‘Auctions of divisible goods: On the rationale for the treasury experiment’, The Review of Financial Studies 6(4), 733–764.

- Bagnoli & Bergstrom (2005) Bagnoli, M. & Bergstrom, T. (2005), ‘Log-concave probability and its applications’, Economic Theory 26(2), 445–469.

- Bikhchandani & Riley (1991) Bikhchandani, S. & Riley, J. G. (1991), ‘Equilibria in open common value auctions’, Journal of Economic Theory 53(1), 101–130.

- Bulow & Klemperer (2002) Bulow, J. & Klemperer, P. (2002), ‘Prices and the winner’s curse’, The RAND Journal of Economics 33(1), 1–21.

- Cole et al. (2022) Cole, H., Neuhann, D. & Ordoñez, G. (2022), ‘Asymmetric information and sovereign debt: Theory meets mexican data’, Journal of Political Economy 130(8), 2055–2109.

- Dalton (1920) Dalton, H. (1920), ‘The measurement of the inequality of incomes’, The Economic Journal 30(119), 348–361.

- Dworczak et al. (2021) Dworczak, P., Kominers, S. D. & Akbarpour, M. (2021), ‘Redistribution through markets’, Econometrica 89(4), 1665–1698.

- Fisz (1965) Fisz, M. (1965), Probability Theory and Mathematical Statistics, Wiley, New York, 3rd edition.

- Gini (1912) Gini, C. (1912), Variabilità e mutabilità: contributo allo studio delle distribuzioni e delle relazioni statistiche. [Fasc. I.], Studi economico-giuridici pubblicati per cura della facoltà di Giurisprudenza della R. Università di Cagliari, Tipogr. di P. Cuppini.

- Gini (1921) Gini, C. (1921), ‘Measurement of inequality of incomes’, The Economic Journal 31(121), 124–126.

- Goeree & Offerman (2003) Goeree, J. K. & Offerman, T. (2003), ‘Competitive bidding in auctions with private and common values’, The Economic Journal 113(489), 598–613.

- Hattori & Takahashi (2022) Hattori, T. & Takahashi, S. (2022), Discriminatory versus uniform auctions under non-competitive auction: Evidence from japan, Technical report, Available at SSRN.

- Hortaçsu et al. (2018) Hortaçsu, A., Kastl, J. & Zhang, A. (2018), ‘Bid shading and bidder surplus in the us treasury auction system’, The American Economic Review 108(1), 147–169.

- Klemperer (1998) Klemperer, P. (1998), ‘Auctions with almost common values: The ‘wallet game’ and its applications’, European Economic Review 42(3), 757–769.

- Krishna (2009) Krishna, V. (2009), Auction theory, Academic press.

- Krishna & Morgan (1997) Krishna, V. & Morgan, J. (1997), (Anti-) Competitive Effects of Joint Bidding and Bidder Restrictions, Discussion paper in economics. Woodrow Wilson school of public and international affairs, Woodrow Wilson School, Princeton University.

- Kruse & Deely (1969) Kruse, R. L. & Deely, J. J. (1969), ‘Joint continuity of monotonic functions’, The American Mathematical Monthly 76(1), 74–76.

- Lorenz (1905) Lorenz, M. O. (1905), ‘Methods of measuring the concentration of wealth’, Publications of the American Statistical Association 9(70), 209–219.

- Milgrom & Weber (1982) Milgrom, P. R. & Weber, R. J. (1982), ‘A theory of auctions and competitive bidding’, Econometrica: Journal of the Econometric Society pp. 1089–1122.

- OECD (2021) OECD (2021), OECD Sovereign Borrowing Outlook 2021.

- Ortega-Reichert (1968) Ortega-Reichert, A. (1968), Models for competitive bidding under uncertainty, PhD thesis.

- Patty & Penn (2019) Patty, J. W. & Penn, E. M. (2019), ‘Measuring fairness, inequality, and big data: Social choice since arrow’, Annual Review of Political Science 22(1), 435–460.

- Pigou (1912) Pigou, A. C. (1912), Wealth and welfare, London: Macmillan and Company, limited.

- Pycia & Ünver (2017) Pycia, M. & Ünver, U. (2017), ‘Incentive compatible allocation and exchange of discrete resources’, Theoretical Economics 12(1), 287–329.

- Pycia & Woodward (2018) Pycia, M. & Woodward, K. (2018), A case for pay-as-bid auctions, Working paper, https://sites.econ.uzh.ch/pycia/pycia-woodward-paba.pdf.

- Reuter & Groh (2020) Reuter, M. & Groh, C.-C. (2020), Mechanism design for unequal societies, Working paper, https://ssrn.com/abstract=3688376.

- Ruddell et al. (2017) Ruddell, K., Philpott, A. & Downward, A. (2017), ‘Supply function equilibrium with taxed benefits’, Operations Research 65(1), 1–18.

- Sen & Foster (1973) Sen, A. & Foster, J. (1973), On Economic Inequality, Oxford University Press.

- Vickrey (1961) Vickrey, W. (1961), ‘Counterspeculation, Auctions, and Competitive Sealed Tenders’, The Journal of Finance 16(1), 8–37.

- Viswanathan & Wang (2002) Viswanathan, S. & Wang, J. J. D. (2002), ‘Market architecture: limit-order books versus dealership markets’, Journal of Financial Markets 5(2), 127–167.

- Wang & Zender (2002) Wang, J. J. D. & Zender, J. F. (2002), ‘Auctioning divisible goods’, Economic Theory 19(4), 673–705.

- Wilson (1969) Wilson, R. (1969), ‘Competitive bidding with disparate information’, Management Science 15(7), 446–448.

- Wilson (1977) Wilson, R. (1977), ‘A bidding model of perfect competition’, The Review of Economic Studies 44(3), 511–518.

- Wilson (1979) Wilson, R. (1979), ‘Auctions of shares’, The Quarterly Journal of Economics 93(4), 675–689.

- Woodward (2021) Woodward, K. (2021), Mixed-price auctions for divisible goods, Working paper, https://kylewoodward.com/ research/auto/woodward-2021a.pdf.

Appendix A Omitted proofs

A.1 Measuring surplus equity

Proof of Lemma 1. The empirical variance of surplus can be transformed as follows.

Similarly, the empirical variance conditioned on winning can be written as

Proof of Lemma 2. We first note that

For the ex-ante variance, we write:

For the empirical variance, we write:

A.2 Main results

Proof of Proposition 1. Consider bidder and let all bidders follow the bidding strategy . First, observe that is continuous and increasing. Then bidder ’s expected payoff when their signal is and bidding is given by

Because is increasing in , it holds for all that , and for all that . Therefore, choosing maximizes bidder ’ expected payoff .

Proof of Proposition 2. First, observe that is continuous. We verify that it is also monotone: writing , , and , an alternative expression for is given by

| (8) |

In particular, it is differentiable almost everywhere and we can compute its derivative.

| (9) |

which it positive almost everywhere. Next, assume that all bidders follow the bidding strategy , and let be bidder ’s bid, whose expected utility is given by

The derivative of is

In equilibrium, the first order condition requires . Solving this differential equation yields the stated form for . Using as the integrating factor, we obtain

Using equations (8) and (9), and the fact that is increasing in , we obtain that is positive when and negative when . Therefore, choosing maximizes ’s expected payoff .

Writing and , observe that the derivative of is . Using integration by parts and a change of variable, we obtain

Dividing by gives the result.

Lemma 4.

For any continuous function , and for all , we have

where and .

Proof.

Fix , and let be a continuous function, such that when . Using the change of variable , we have that

Observe that for all fixed , and taking , the first (resp. second) integrand converges towards (resp., ). We define the constant , we bound the first integrand by (resp.the second integrand by ), and we use the theorem of dominated convergence, which gives

To prove the lemma, observe that with the change of variable , we have

where we define

Finally, it remains to prove that when . First, observe that is bounded on . Second, observe that we have

where . Because is positive and integrable in , we have that is bounded. Therefore, the overall limit when is equal to , which concludes the proof. ∎

Lemma 5.

The following derivate formulas can be derived:

Proof.

In order to derive the value of these functions at points where they are not directly, defined, we will use the dominated convergence theorem multiple times.

(1) Let . We first look at . Let be the function under the integral. Clearly because is increasing, for we have that . Hence is dominated by , and , hence by dominated convergence when , and the function is separately continuous over .

(2) We now consider the derivative of with respect to . Let . There exists and such that . We focus on the derivative of the integral part:

where the is finite as is continuous. Because is integrable, we can use dominated convergence. Using Leibniz integral rule yields the formula. The formula as goes to can be computed with Lemma 4.

(3) Le us now compute the derivative of with respect to . Note that we do a careful derivation as we are also interested in the value of this derivative at . Let . We have

The first part is again dominated by which is integrable, we focus on the second part: define for the function . Note that implies that for and , we have as is increasing and takes values in over by definition. Fix , and take the derivative with respect to : we obtain that which is positive as long as and negative otherwise. The maximum of for is at and . This shows that the second part is smaller that which is also integrable. Overall by dominated convergence we can invert derivative and integral: . Using that we can conclude by that

Using the same upper bound on , we can show that the integrand of is smaller than which allows for domination both in small and small . By dominated convergence once more, we obtain that the limit of as either or go to is .

(4) Finally, let us compute the cross derivative. The integrand of is , which derivative with respect to alpha is . Because this function is continuous on the open set , we can as done previously apply dominated convergence to show that derivation and integral can be inverted. Therefore

∎

Lemma 6.

Consider a function , such that

-

•

is continuous over for all fixed ,

-

•

is continuous over for all fixed ,

-

•

either all ’s are monotone or all ’s are monotone,

then is jointly continuous in and .

Proof.

The proof on the open set is written in Kruse & Deely (1969), and directly generalizes to and given that is separately continuous in those points. ∎

Proof of Proposition 3. Monotonicity follow from the derivatives computed in Lemma 5.

Proof of Proposition 4. We first show that (1) the function is jointly continuous over and . Thanks to Lemma 5, it is separately continuous and increasing in for every , thus we can apply Lemma 6.

Next, we show that (2) the function is jointly continuously differentiable over and . The partial derivative is separately continuous, and is monotone in for every fixed (using the cross derivative), hence it is jointly continuous. The same argument applies to the second partial derivative . Therefore, the differential is jointly continuous.

Proof of Theorem 1. We detail here the complete proof for (2). Using the formula of , we can focus only on the squared difference of winners’ utility. Moreover for , we have (refer to Theorem 2 for a more detailed derivation). We want to compute . We have that

As done in Lemma 5, we can bound by . We also have that , which implies . Overall we can upper bound the absolute value of the above derivative by sum of products like , , or . We have that has finite second moment, and thus so does as a combination of order statistics of . By Cauchy-Schwartz we get the integrability of all the above products, as and . This also implies the integrability conditionally on winning as . All in all, the derivative inside the expectation is dominated by an integrable function, we thus apply dominated convergence to intervert expectation and derivative.

Finally, using Lemma 5, we take the limit of , , and , as goes to . We have that and . The product is negative, as is increasing, and this concludes the proof.

Theorem 5.

For a given common value component , consider two -mixed auctions for and suppose the equilibrium bidding functions satisfies for all signals . Then, WEV is lower for the -mixed auction than for the one.

Proof.

Let . We have . Let . By the generalized Cauchy mean value Theorem, we have that there exists such that

Hence if then we have lower for the mixed auction. We have the following chain of equivalences:

where the third equations comes from the monotonicity of in from Proposition 3. ∎

Lemma 7.

Assuming private values (), for any , iff is log-concave.

Proof.

Let us compute the second derivative of the logarithm of :

Notice that the left-hand fraction is always positive. Hence log-concavity of is equivalent to being negative. The latter is equivalent to

∎

Lemma 8.

If the density of signals is log-concave, then so is .

Proof.

To prove Lemma 8, we will use properties of log-concave distributions from Bagnoli & Bergstrom (2005). Namely their Theorems and state together that log-concavity of a density implies log-concavity of the corresponding cdf and of the complementary cdf , and that log-concavity of or imply log-concavity of respectively or , where is the upper limit of the support of (either a constant or ). Additionally, we also have that the product of two log-concave functions is log-concave also. Using the above properties, we have that and are log-concave. Moreover, the order statistics density , given by Eq. 1, is a product of , , and . Thus, as well as the corresponding cdf are also log-concave. Furthermore, is log-concave because . Finally, we remark that is right-continuous non-decreasing by composition with , which is continuous non-decreasing, and , as well as (if , the equality is understood as a limit). Therefore is a cdf, and applying one last time Bagnoli & Bergstrom (2005), we obtain that is log-concave. ∎

Lemma 9.

Assuming common values (), is differentiable on , and can be expressed as

Moreover, if the signal density is log-concave, then for all signals .

Proof.

We first rewrite for in terms of all the order-statistics of .

| (Ordering the signals) | ||||

Note that the previous decomposition is similar the equilibrium bid in an English auction given that bidders have dropped out in Goeree & Offerman (2003). However, we offer a careful derivation in the multi-unit setting of our model. We now use Theorem and Theorem from Arnold et al. (2008) on the conditional distribution of order statistics. They state that, for , the distribution of given is the same as the distribution of the -th order statistic of independent samples of the original distribution left-truncated at , and we denote a random variable drawn according to this distribution. Hence, for , . Similarly for we have that the distribution of given is the same as the distribution of the -th order statistic of independent samples of the original distribution right-truncated at , and we denote by a random variable drawn according to this distribution. Hence, for , . Notice that summing all order statistics drawn from some samples recovers exactly the sum of original samples. Thus we obtain

The same can be done for the . Finally, the are iid and thus have identical conditional expectations. We obtain

| (10) | ||||

| (11) |

which readily yields a formula for . Clearly, the above function is well defined and differentiable on the open support of .

We now examine the derivative of and prove that . First, we consider the derivatives of the two ratios with an integral in the numerator in Eq. 11. First, by integration by parts, we have

and using that for positive random variables , which guarantees convergence of the integral, we have that

Now, taking derivatives, we have

By a similar argument as in the proof of Lemma 7, using log-concavity of , the above derivative is bounded by . Taking the derivative of the second ratio, we have

| (12) |

To derivative of :

| (13) |

Eq. 13 is negative iff . This means that the log-concavity of is equivalent to Eq. 12 being smaller than . As the log-concavity of follows from the log-concavity of and (Bagnoli & Bergstrom 2005, Theorem 3), is implied. Finally, using the above derivatives it is clear that , and

∎

Proof of Proposition 5. First, we recall the expression of the derivative of the bid function for any :

| (14) |

is clearly positive. Note that for any , is a linear combination of and in the case of a pure common value. The derivative of the latter is bounded by by Lemma 9. Hence for any , . Moreover, because of Lemma 8, we know that is log-concave, and we can therefore apply Lemma 7. Hence using the above results,

| (15) |

Proof of details in Example 1. For convenience, we define the following order statistics.

For uniform pricing (), the bidding function is

Given , the bidding function in -mixed auction is given by when , and

For any -mixed auction, recall that the WEV is given by

where we define . We can then write

We next compute these quantities for uniform and discriminatory pricing. For uniform pricing () we have that . We derive

and finally

For discriminatory pricing () we have that . We will use the following bounds:

Next, we write

and

Next, we will use the upper bound , which is nearly tight as is increasing, and has the limit when .

Finally, we obtain

A.3 Numerical experiments

Lemma 10.

Suppose an auction is a winners pay auction. Then we can write , , and .

Proof.

Observe that we have

| (16) | ||||

| (17) |

∎

A.4 Discussion

Proof of Proposition 6. We define the probability that wins . Recall that denotes the equilibrium bid in the pay-as-bid auction. Consider any standard auction, characterised by a payment rule . Revenue equivalence implies that

| (18) |

In particular, note that if is chosen to be the uniform pricing rule, this formula can be used to compute . Now define the ex-post surplus . We write

| (19) |

Now, observe that by revenue equivalence we have for all . We write

| (20) | ||||

| (21) |

To show that the extra terms are non-negative, notice that , and that

| (22) |

Therefore, putting everything together, we obtain

| (23) | ||||

| (24) | ||||

| (25) |

Finally, observe that an auction which minimize the interim variance also minimize the ex-ante variance. Denoting by the utility of a bidder in the pay-as-bid auction, the law of total variance states

| (26) |

By the revenue equivalence theorem, we know that is the same for all standard auctions, hence is also the same for all standard auctions (it only depends on the distribution of the signals).

The interim variance is minimal point-wise (in ) for all standard auctions, hence is also minimal in expectation. Therefore, the ex-ante variance is minimal in the pay-as-bid auction among standard auctions.