Algorithmic Collusion and Price Discrimination: The Over-Usage of Data

Abstract

As firms’ pricing strategies increasingly rely on algorithms, two concerns have received much attention: algorithmic tacit collusion and price discrimination. This paper investigates the interaction between these two issues through simulations. In each period, a new buyer arrives with independently and identically distributed willingness to pay (WTP), and each firm, observing private signals about WTP, adopts Q-learning algorithms to set prices. We document two novel mechanisms that lead to collusive outcomes. Under asymmetric information, the algorithm with information advantage adopts a Bait-and-Restrained-Exploit strategy, surrendering profits on some signals by setting higher prices, while exploiting limited profits on the remaining signals by setting much lower prices. Under a symmetric information structure, competition on some signals facilitates convergence to supra-competitive prices on the remaining signals. Algorithms tend to collude more on signals with higher expected WTP. Both uncertainty and the lack of correlated signals exacerbate the degree of collusion, thereby reducing both consumer surplus and social welfare. A key implication is that the over-usage of data, both payoff-relevant and non-relevant, by AIs in competitive contexts will reduce the degree of collusion and consequently lead to a decline in industry profits.

1 Introduction

The digitization of the economy has led to the development of algorithms and machine learning to process massive amounts of data and make decisions. As a result, important firm decisions, such as pricing and production levels, are determined autonomously by artificial intelligence. The growing reliance on artificial intelligence in market activities poses new challenges for market regulations. Two important issues that have raised great concern are algorithmic price discrimination and algorithmic tacit collusion. According to Gautier et al. (2020), price discrimination involves charging different prices for the same or similar products, while algorithmic tacit collusion implies that algorithms can sustain collusive outcomes without human pricing intervention. These two issues have been analyzed separately in the literature. It has been documented, both through simulation and empirical studies, that self-interested and autonomous algorithms can adapt to supra-competitive prices or collusive strategies. However, previous literature has studied the impact of price discrimination on collusion by assuming forward-looking and fully rational individuals. They examine how price discrimination limits collusive behavior to exclude off-equilibrium deviation. Our paper is, to the best of our knowledge, the first to investigate the interaction between these two issues. Our objective is to study collusive behavior of artificial intelligence in data-driven price discrimination towards consumers and provide potential explanations.

To achieve price discrimination, firms need to gather big data on consumers’ characteristics to train their models in predicting consumers’ types. Note that firms may adopt different training data set with possibly overlapping parts. Additionally, they may employ different algorithms to train their models and different customer tagging systems. Their predictions on customers’ types may therefore be different but correlated. The algorithms’ pricing strategies based on these different but correlated predictions echo with a fundamental topic in game theory, i.e. coordination and correlation. Coordination involves jointly choosing strategies, while correlation entails independently choosing strategies based on correlated signals. In this paper, we shift our focus from rational human being to artificial intelligence and investigate how autonomous and independent artificial intelligence adapt to coordinate on correlated signals.

We first study the static game to establish the competitive benchmark. A fixed number of firms produce perfectly substitutable goods with the same cost. A single consumer with an unknown willingness to pay (WTP) needs to purchase a single unit of the good. The firms set prices and engage in Bertrand competition upon observing noisy and correlated signals of the consumer’s WTP, subject to a given information structure. The consumer is expected to purchase the good from the firm that offers the lowest price. If multiple firms offer the same lowest price, the consumer will randomly choose one. We prove that, under any information structure, each firm earns exactly zero profit in every Bayesian Nash equilibrium.

We then construct AI pricing agents with Q-learning algorithms and allow them to interact with each other repeatedly in computer-simulated marketplaces. At each period, a single consumer with identically and independently distributed WTP entered the market. Imperfect and correlated signals regarding the consumer’s WTP were observed by each agent. Similar to previous literature without memory, these AI agents have adapted to supra-competitive prices. This is attributed to the failure of learning competitive strategies when facing a non-stationary environment. However, two novel mechanisms leading to collusive outcomes are documented. In asymmetric information structures, the more informed AI adopts a Bait-and-Restrained-Exploit strategy to “teach” less informed AI to collude. To bait the less informed AI into setting a high price, the more informed AI may set higher prices on certain signals while sacrificing profits. Conversely, to prevent less informed AI from lowering prices, more informed AI may set much lower prices on the remaining signals while accepting limited profits. In symmetric information structures, competition on certain signals can impede algorithms from learning competitive strategies on the remaining signals, which can facilitate collusion on those signals, and vise versa. Conversely, having more signals can lead to lower collusion levels in the mechanism. As demonstrated in our accompanying note (also included in the Appendix D), achieving the Bertrand Nash price level depends heavily on the process of sequential and alternating downward search. This process may be disrupted when low prices cannot be sustained. Competition on certain signals reduces the current stage payoff and, as a result, the Q values associated with these signals. If a low price is selected on one of the rest signals and it transits to one of the signals with competition, the corresponding Q value for this low price will decrease, making it less likely to sustain in the future. This can interrupt the process of sequential and alternating downward search on the rest signals, resulting in being stranded at a collusive outcome. Therefore, the degree of collusion is negatively correlated across signals. Then, on which signals are AI agents more likely to compete or collude? Our experiment shows that AI algorithms coordinate to collude more on signals with higher WTP in expectation.

Finally, a welfare analysis is conducted. In scenarios with symmetric information structures, we observed an inverted U-shaped trend in industry profits as information precision varied from Shannon Entropy (4,4) to (0,0). Initially, industry profits increased due to enhanced transaction efficiency and reduced collusion with more precise information. However, as the information became too precise, the diminishing returns from reduced collusion outweighed the benefits of enhanced efficiency, leading to decreased profits. Furthermore, algorithms that engage in precise price discrimination instead of pretending to be unaware of information may lead to lower profits for firms, indicating an over-usage of data. Moreover, in asymmetric scenarios, increased information generally leads to lower industry profits. In contrast, a more symmetric information structure often results in even lower profits. Conversely, the impact of AI information precision on consumer surplus and social welfare contradicted its effect on industry profits.

Our primary findings suggest that in competitive markets, the overuse of data by AIs for price discrimination weakens collusion, leading to lower industry profits. This aligns with earlier literature that did not consider algorithmic pricing (Miklós-Thal and Tucker 2019; Thisse and Vives 1988; Shaffer and Zhang 1995). Therefore, firms aiming to boost profits through AI adoption should take note of this drawback of artificial intelligence, in addition to the insights presented by Calvano et al. (2023b) and Bonelli (2022).

Furthermore, the study suggests that competition and algorithmic collusion could worsen price discrimination, resulting in increased collusion rates for consumers with a high WTP when information structure is symmetric.

The final implication is that permitting firms to leverage data may lead to reduced collusion and increased social welfare under algorithmic pricing. Even if only a single AI is allowed to engage in price discrimination, collusion levels can decrease, as it needs to set extremely low prices at certain signals to manipulate the competitor.

Related Literature. Our work is related to the emerging literature on algorithmic pricing and the possibility for algorithms to sustain supra-competitive outcomes. Calvano et al. (2020, 2021, 2023a) show that Q-learning can sustain a collusive outcome via collusive strategies with a finite phase of punishment followed by a gradual return to cooperation. Abada and Lambin (2023); Epivent and Lambin (2022) show that the seeming collusion may be due to imperfect exploration rather than excessive algorithmic sophistication. Asker et al. (2022, 2023) show that asynchronous updating can lead to pricing close to monopoly levels, while synchronous updating leads to competitive pricing. Banchio and Mantegazza (2023) show that a novel collusive channel relies on an endogenous statistical linkage in the algorithms’ estimates called spontaneous coupling. Banchio and Skrzypacz (2022) study auction design with Q-learning and find that first-price auctions without additional feedback lead to tacit collusive outcomes, while second-price auctions do not. They show that the difference is driven by the incentive in first-price auctions to outbid opponents by only one bid increment. Colliard et al. (2022) show that algorithmic market makers (AMs) charge a markup over the competitive price because the uncertainty of the environment may reduce the learning capacity of AMs. Dou et al. (2023) show that the collusion can be sustained through price-triggering strategies and learning biases. Other research also finds algorithmic collusion in different settings (Klein 2021; Johnson et al. 2023; Waltman and Kaymak 2007, 2008; Wu et al. 2023). In our work, we propose two new distinct mechanisms for securing collusion. We show that not only the uncertainty of the environment would affect the coordination of AIs, but also the number of signals can have a significant impact on the coordination. And the latter effect can sometimes be dominant.

This study is situated within the broader literature on price discrimination and collusion (Miklós-Thal and Tucker 2019). However, it is distinctly different in that it incorporates algorithmic pricing into its considerations. In addition, our work is consistent with the information structure literature (Aumann 1987; Bergemann and Morris 2016; Forges 1993; Harsanyi 1968), as we systematically consider the information structure of AIs. Furthermore, the study builds on the literature on Q-learning (Dearden et al. 1998; Watkins and Dayan 1992).

The rest of the paper is organized as follows. Section 2 presents the game model and its Bayesian Nash equilibrium. Section 3 describes the details of the setup. Section 4 and Section 5 report our experimental results in the symmetric and asymmetric cases, respectively. In Section 6, we performed a welfare analysis to summarize the economic implications of our results. Section 8 concludes. The proof of Proposition 1, the details of Q-learning, and the note on the channel underlying AI collusion can be found in the Appendix.

2 The Model

Consider firms with equal marginal costs, where for all . These firms sell homogeneous goods and compete by setting prices.

At any time , a buyer enters the market with a willingness to pay (WTP) . In each period, the buyer’s WTP is drawn according to a distribution and is independent across periods. If a firm sets a price such that , and is the minimum among the quoted prices of all firms, i.e., , then the demand for product is realized as , with ties being resolved randomly. If these conditions are not satisfied, . The payoff per period for firm is given by .

The information structure is captured by the 2-tuple , where represents the signal space and is a joint distribution for all and . Upon realization of , each firm receives a signal with probability , where .

The timing is as follows: Nature selects , and according to the information structure, signals are communicated to each seller. Armed with this information, sellers strategically set prices to maximize their revenue. In the static game, Proposition 1 describes the properties of the equilibrium.

Proposition 1.

If the action space is and the distribution of the WTP and the information structure are the common knowledge:

-

1.

There exists a Bayesian Nash equilibrium (BNE) characterized by every player quoting under every signal. Furthermore, in every BNE, every player receives profit.

-

2.

In the two-player case, the BNE characterized in (1) is the unique BNE.

-

3.

In the monopoly case, the optimal pricing strategy for a player is given by under any signal.

The proof of Proposition 1 is by contradiction. Suppose there exists a state in which a transaction with a strictly positive price is executed with strictly positive probability, and let be the state with the largest transaction price . Then there exist a pair of firms and , and a pair of signals and , such that these signals can be received by the corresponding players in state , and player chooses exactly at signal . Then it is strictly advantageous for player to deviate to at signal if is small enough. Therefore, the original strategy profile is not a Bayesian Nash equilibrium.

Proposition 1 establishes the competitive and monopoly outcomes, respectively, which serve as the extremes of the collusion level. These two outcomes are necessary for evaluating the collusion level of the experimental results in the following sections.

3 Simulation Design

Q-learning is a model-free optimal algorithm that is widely used in economic activities such as pricing. See details of Q-learning in Appendix B. We have constructed Q-learning algorithms and let them interact in a repeated Bertrand oligopoly setting with incomplete information. For each information structure, an “experiment” consists of 1000 sessions. In each session, agents play against the same opponents until convergence, as defined below.

3.1 Information Structure

In the simulation we define the state space as with states. Each state is randomly drawn at each period, i.e., . In the baseline setting, we focus on the simplest and most commonly used information structure, which is interval partitioning. We sequentially divide the set of states into divisions, each corresponding to a signal, where is a factor of to ensure an equal number of states per signal within the same structure. We use the reciprocal of the signal number to denote the information precision (abbreviated as ) of the agent. An agent has if it can receive different signals. For example, for an agent with , it will receive signal when is realized, and signal when occurs, and so on.

Shannon entropy was proposed by Shannon (1948) to measure uncertainty or randomness in a system. If is a discrete random variable with possible outcomes and a probability mass function , then the Shannon entropy is defined as

| (1) |

The entropy value increases as the uncertainty in the system increases, and we use the Shannon entropy of the signal to symbolize the uncertainty of its corresponding information structure, denoted by with a slight abuse of notation.111We can think of the signal as a random variable, with equal probabilities of realizing each contained state. In our context, the information precision corresponds to Shannon entropy values of , respectively, continuously increasing by .

3.2 Action Space

Since Q-learning requires a finite action space, we need to discretize the model. Here are two criteria for discretizing the continuous action space: the first ensures that in each signal Q has the same number of actions to choose from, and the second ensures that there is a unique Nash equilibrium. Let be the value of the maximum state in signal . We define the set of feasible prices as follows:

| (2) |

where . Under this discretized setting, the unique Bertrand-Nash price is for . Moreover, the monopoly price is exactly in this set, and we allow a price slightly higher than the monopoly price. We discretize the action space relative to the largest state in the support of the posterior conditional on the signal. This practice ensures that the collusion index is nearly the same in each state partition/signal. Therefore, when analyzing different collusion indexes across signals, we can exclude the effect of how we partition the state space.222Figure 18 in the Appendix C provides evidence for this view.

3.3 Multi-Agent Q-Learning

In each episode a buyer with enters the market. After receiving , agent chooses action according to the rule described in the following paragraph. After Q receives the immediate payoff and the next signal , it updates the corresponding Q value using the standard Q learning update rule:

| (3) |

To ensure that Q-learning sufficiently explores all states and actions, in this paper we use the -greedy strategy with a time-declining exploration rate. Specifically, we set , where is the exploration parameter. In episode , with probability , Q chooses the action that is optimal according to the current Q-matrix, and it randomizes uniformly over all actions with probability . It is obvious that the exploration decreases faster as increases.

3.4 Collusion Index

To quantify the extent of collusion, we introduce a collusion index (CI), which is a normalized measure inspired by Calvano et al. (2020):

| (4) |

where is the total profit at convergence, is the total profit in the static Bertrand-Nash equilibrium, and is the profit under monopoly. In asymmetric cases, denotes the profit under monopoly for the information-advantaged player.333In analogy to the principle of coordination, where agents make decisions and share information simultaneously, monopoly profit-or the peak of collusion profit-is defined as the maximum aggregate profit achievable by using all available market information. Moreover, the validity of our results holds under this definition of monopoly profit, ensuring that they remain applicable under any variation of weighted monopoly profit, which is conceptualized as the weighted sum of the monopoly profits of two firms. For more details on this claim, see footnote 8. The CI reflects the percentage of supra-competitive profits achieved upon convergence. We compute the CI for each simulation and report the average CI over 1000 simulations.444Due to the fact that is close to zero, the average CI can be approximated by substituting the average profit at convergence into the equation used to compute the CI.

Extending this concept further, we also define a CI specific to each signal (or state ):

| (5) |

where each parameter is adjusted based on the results corresponding to each signal (or state).555In asymmetric information structure scenarios, the signal in question belongs to the less informed party, and corresponds to the highest profits achievable under that particular signal .

3.5 Baseline Setting

In the baseline simulation, the Q-learning algorithms are memoryless (see Calvano et al. (2020) for the memory setting). We focus on a baseline setting consisting of symmetric duopoly (), where the state and information structure follow the above specifications with and , as in Calvano et al. (2020). To find reasonable values for , it is useful to relate to the expected number of times a cell would be visited by pure random exploration over an infinite time horizon, denoted by . In our model, we have

| (6) |

For our base scenario, we set , which corresponds to in the information structure .666In the information structure , . In the following simulations, unless otherwise noted, the parameters are set according to the baseline scenario.

3.6 Convergence

For strategic games played by Q-learning algorithms there are no general convergence results. To verify convergence, we use the following piratical criterion: convergence is said to be achieved if, for each player, either the action chosen in each signal does not change for 100000 consecutive periods, which is slightly different from the criterion in Calvano et al. (2020).777In Calvano et al. (2020), convergence means that the optimal action does not change for 100000 consecutive periods. In our setting, we also ensure that the decay of the exploration is sufficient. We stop the algorithms if they do not converge after 1 billion periods.

4 Asymmetric Information Structure

In this section, we study the scenario where firms have different capabilities to discriminate prices. Firms train their models to predict consumers’ WTP with a dataset of past transactions, either collected by themselves or purchased from data intermediaries. On the one hand, the different capabilities result from different training datasets. Large firms and especially large platforms have conducted large volumes of transactions with different consumers in the past. The generated data can then be transformed as part of the training dataset, leading to the data advantage of large firms. On the other hand, the different price discrimination capabilities may also be due to different training algorithms used. In order to process the large volume of transactional data, the efficiency of the algorithms and the computational power of the firms are crucial in determining the accuracy of the trained predictive model. Large firms can not only hire more computer scientists to improve their algorithms, but also purchase or rent more hardware to improve their computational power, which in turn leads to the data advantage of large firms. Accordingly, we focus on the case where one firm has a strict data advantage over the other firm. In other words, the information structure of one firm is strictly more informative in Blackwell order than that of the other firm. The main results in this section show that the collusive outcome can be sustained by the adoption of a Bait-and-Restrained-Exploit strategy by the firm possessing an information advantage.

Without loss of generality, we assume in the following simulation results that Firm 1 has more accurate information than Firm 2. Specifically, Firm 1 can effectively distinguish between different consumer segments, whereas Firm 2 may not have this ability.

Observation 1.

The results under asymmetric information structure are summarized as follows,

-

1.

Collusive strategy: Under some signals, the more informed firm sets prices strictly higher than those of the less informed firm (bait). Under other signals, the more informed firm sets prices much lower than the minimum of the consumer’s WTP and the less informed firm’s prices (restrained exploit).

-

2.

Market division: The less informed firm tends to capture markets with higher expected WTP, while the firm with information advantage tends to capture markets with lower expected WTP.

-

3.

Profit: The less informed firm achieves almost the same average profit as the more informed firm, and sometimes even a strictly higher profit.

-

4.

Collusion degree: The collusion index increases as the information asymmetry increases.888 If we characterize the monopoly profit as the weighted sum of the individual monopoly profits of two firms, i.e, , where is the monopoly profit of the more informed firm and is that of the less informed firm, our results remain robust. This robustness stems from the fact that as information asymmetry increases, the denominator in the new CI equation decreases when . This event actually strengthens our result, given that the denominator is constant in the CI definition we use.

-

5.

Collusion degree within and across signals: The collusion index decreases with WTP under the same signal of the less informed firm, but increases with WTP across signals of the less informed firm.

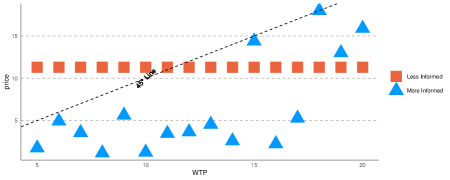

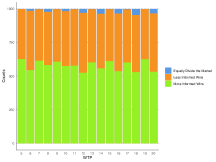

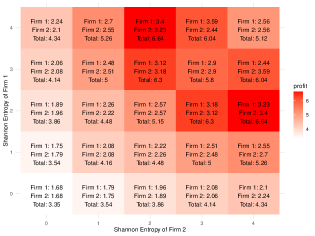

Figure 1 illustrates the Bait-and-Restrained-Exploit strategy in a representative sample with Shannon entropy . The less informed AI offers a single price to all consumers, while the more informed AI can fully discriminate between consumers with different WTP. We can observe that for consumers whose WTP is 15, 18, 19, and 20, the more informed AI offers a strictly higher price. In other words, the more informed AI, although equipped with the full ability to discriminate prices, gives up the profits made in these segmented markets. Surrendering profits seems to be an irrational behavior, and given the strategy of the less informed AI, the more informed AI should adapt to lower its prices and thus capture profits in these markets. However, in an interactive context, this strategy component, called bait, entices the less informed AI to set a relatively high price at the cost of giving up profits in these markets. In turn, the more informed AI wins the remaining markets by setting a lower price. However, the price it offers is much lower than the minimum of consumers’ WTP and the price offered by the less informed AI. Again, leaving excess profit room seems irrational, and given the strategy of the less informed AI, the more informed AI should adapt to setting prices slightly lower than its opponent’s price or just exactly the same as consumers’ WTP (if its opponent’s price is well above consumers’ WTP). However, in a competitive environment, this strategy component, called restrained exploit, can exclude the less informed AI from downward deviations. If the AI with information disadvantage explores locally with lower prices, it not only loses profit margin in the markets where it already occupies the market share, but also fails to conquer more markets because its offer prices are still higher than its opponent’s prices. Therefore, the less informed AI is reinforced to maintain this high price level.

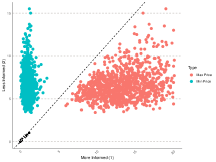

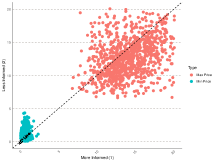

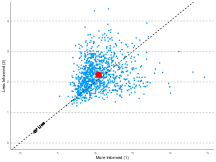

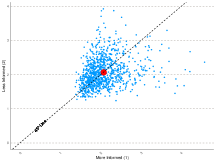

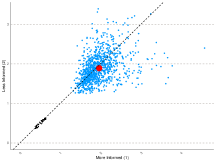

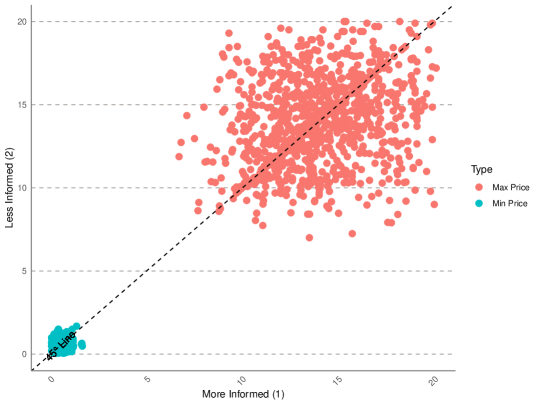

To demonstrate that the first part of Observation 1 is a general phenomenon, we plot the distribution of maximum and minimum prices offered by both AI agents in Figure 2.

The left figure 2(a) shows the scenario where one AI agent has full price discrimination capability, while the other AI agent can only offer a uniform price to consumers, i.e. with entropy level . The mass of red dots, well below the 45-degree line, indicates that the information-advantaged AI consistently sets the maximum price strictly higher than that of the information-disadvantaged AI. Thus, the more informed AI is giving up profits in some markets. The mass of green dots, well above the 45 degree line with strictly positive gap, implies that the minimum prices set by the more informed AI are strictly lower than those set by the less informed AI. Therefore, the well-informed AI captures the remaining markets with restrained exploitation. The remaining three graphs document the pattern of maximum and minimum prices as information asymmetries decrease. The mass of red and green dots both moving towards the 45 degree line indicates that the gaps between the maximum prices of these two agents and between the minimum prices are both shrinking. This implicitly implies that the tendency to adopt the Bait-and-Restrained-Exploit strategy, a way to manipulate less informed AIs into colluding, is reduced as the information advantage of more informed AIs diminishes. 999When Shannon entropy is (0,0), two firms set prices that are statistically symmetric. See Figure 18 in Appendix C.

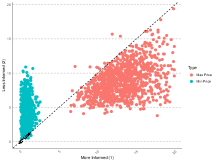

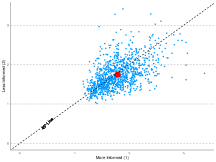

The Figure 3 illustrates the market division scheme for various degrees of information asymmetry. The left figure 3(a) shows the situation with the greatest information asymmetry, i.e. with an entropy level of . The more informed AI dominates the market, which consists of consumers with low WTP. The AI with information advantage captures almost the whole market of consumers with WTP 5 and 6. As consumers’ WTP increases, this dominance in market shares weakens. In markets where consumers’ WTP exceeds 15, the more informed AI has only about 50 percent of the market share. In the remaining graphs of Figure 3, within the same partition of signals for the less informed AI, its market share of segmented markets increases as the value of the segmented markets increases. Thus, it shows that the AI with information advantage is more likely to forgo profits in high-value markets while exploiting profits in low-value markets. The rationale behind this phenomenon is that more informed AI must refrain from over-exploiting profits, i.e., there is a strictly positive gap between the consumer’s WTP and the price offered by more informed AI. Therefore, more informed AI is almost indifferent between high and low valued markets. Thus, its profit is primarily determined by the number of “markets” it can capture. If it gives up high-value signals/markets, it may only need to surrender a small number of markets to successfully trick the less informed AI into setting high prices.

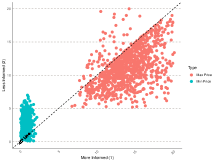

Figure 4 illustrates the third part of Observation 1. We can see that when the Shannon entropy of the information structure for the less informed AI is , , and , the profit pair is located around the 45 degree line, implying that their profits are roughly equal. This argument can be further verified since the average profit pair is almost on the 45 degree line. However, when the Shannon entropy of the information structure for the less informed AI is , i.e., when the information asymmetry reaches its extreme, the less informed AI can actually achieve a strictly higher expected profit. This observation contradicts the conventional wisdom that data advantage translates into competitive advantage in the marketplace. One possible reason is that less informed AI, which can only offer a single price to all consumers, is more difficult to collude with because it has to give up low-value markets by raising its offered prices. In order to achieve collusion, the more informed AI must, on the one hand, give up more high-value markets and, on the other hand, lower its prices and thus limit its exploitation in low-value markets. Thus, competitive advantage is sacrificed in exchange for collusion.

Figure 5 illustrates the fourth part of the Observation 1, where we fix the Shannon entropy of Firm 1’s information structure at 0 and vary the Shannon entropy of Firm 2’s information structure from 0 to 4. As the informativeness of Firm 2’s information structure decreases, the CI increases.

As the Shannon Entropy of the less informed AI increases, the average CI also increases from to . Thus, information asymmetry leads to a higher degree of collusion. One possible explanation is that higher information asymmetry makes it easier for the more informed AI to manipulate the less informed AI and thus “teach” the less informed AI to collude.

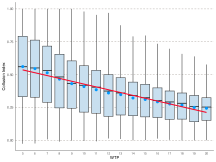

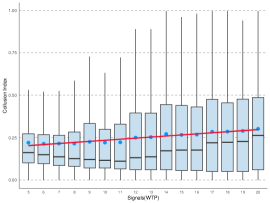

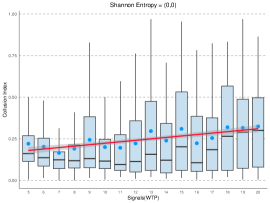

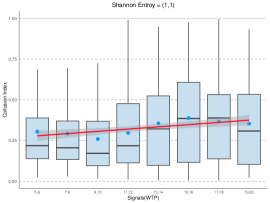

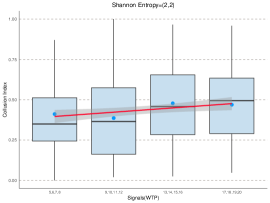

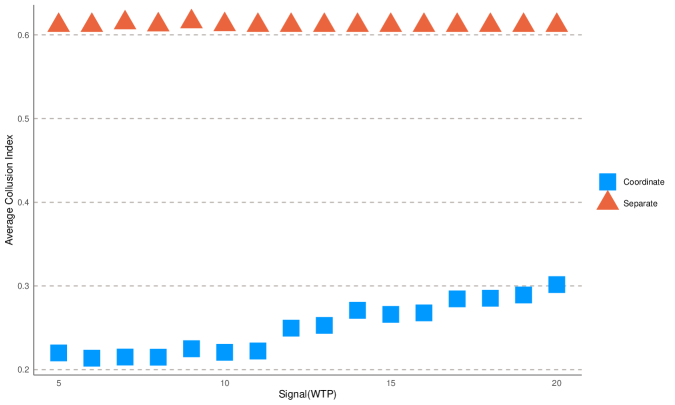

Finally, we draw the Figure 6 to show the last part of the Observation 1. In Figure 6, we plot a box plot of CI for each WTP under different pairs of Shannon entropies. We can see that within a single signal of the less informed AI, as WTP increases, the box goes lower and the regression line has a downward slope. Across the signals of the less informed AI, as WTP increases, the CI increases as WTP increases. In short, the trend of the CI shows a decrease within signals and an increase between signals.

Within a given signal scenario, the less informed firm can only offer a uniform pricing strategy. For those segments of WTP that are captured by the less informed firm, CI tends to decrease as WTP increases. Conversely, in segments where the more informed firm has a competitive advantage, although the price may increase as WTP increases, the increase is relatively modest and not proportional to the increase in WTP. This is due to the need for the price offered by the more informed firm to maintain a mark-up below the less informed firm’s uniform price in order to remain collusive. As a result, in these segments dominated by the more informed firm, CIs also show a downward trend.

In certain scenarios, such as when the less informed firm is completely unaware of the buyer’s WTP, it may strategically choose not to engage with buyers exhibiting low WTP in a monopolistic setting. This strategic choice implies that competition is inherently lower for segments with lower WTP than for those with higher WTP.

The observation that CI increases across signals serves as an extension of the Observation 4 noted in symmetric cases. The underlying rationale for this trend remains consistent in both scenarios. This pattern and its causes will be analyzed in detail in the next section.

5 Symmetric Information Structure

In this section, we consider the case where the two firms have a symmetric information structure. In reality, firms may buy data from the same third-party or even use the same third-party prediction. Sometimes competitors are forced to use the same consumer dataset. For example, when firms compete for a single advertising slot in Wechat moment, the Tencent increasingly relies on the first-price auction to allocate this slot. The Tencent will provide its own data to help companies evaluate the degree of match between the slot and their own products. Sometimes, the Tencent will close the interface to get access to firms’ own data. We find that strengthening price discrimination mitigates the collusion degree.

5.1 The Effect of Information Precision

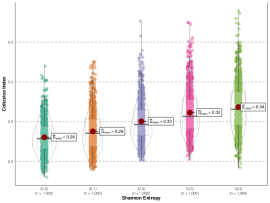

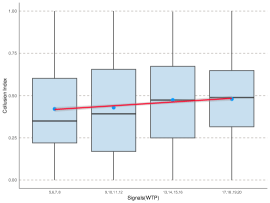

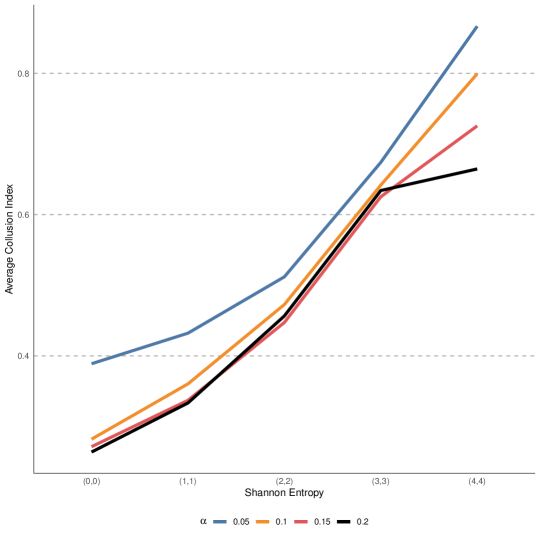

We first examine how the degree of collusion varies with different levels of information precision, as indicated by Shannon entropy. Based on the evidence in Figure 9, we draw Observation 2.

Observation 2.

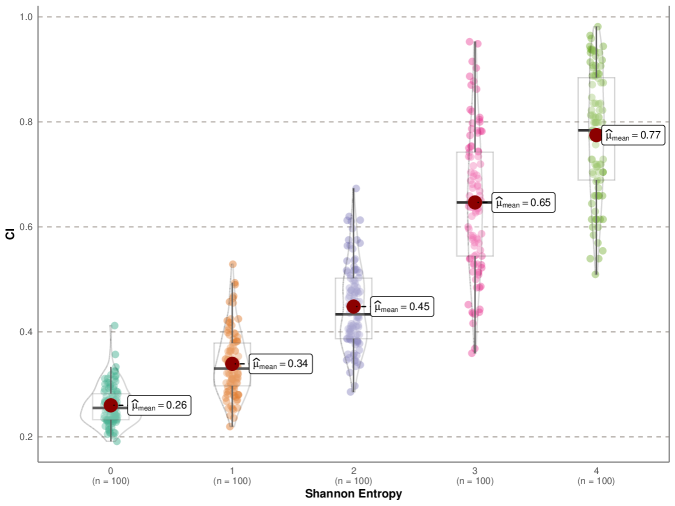

Collusion Index is increasing with respect to Shannon Entropy of the information structures.

Figure 9 shows that as the Shannon entropy of the information structure increases, the average CI increases from to . In addition, higher Shannon entropy also leads to higher variance in the CI. Intuitively, coarser information about consumers’ WTP introduces additional randomness into the system, and therefore the convergence outcome varies significantly if it is strictly above the Bertrand-Nash equilibrium.

This observation echoes with two classic arguments in industrial organization. First, in a static market game, more information increases competition and thus reduces firms’ profits, which is in the same spirit as the prisoner’s dilemma (see Thisse and Vives (1988); Shaffer and Zhang (1995)). However, this argument does not fit our setup perfectly, since it crucially relies on the assumptions of full rationality and a Bayesian decision maker. Moreover, Proposition 1 already implies that Bertrand competition is so fierce that any collusive outcome cannot be sustained by the equilibrium under any information structure. Second, in a repeated market game with more precise good signals, there should be stricter constraints on collusive behavior in the equilibrium path to preclude off-equilibrium deviations (see Miklós-Thal and Tucker (2019)). Again, this argument does NOT fit our framework, since Q-learning algorithms are not forward-looking, where they are programmed to make decisions based on what they have learned in the past. Moreover, the inactivation of one-step memory even precludes the possibility of making decisions depending on the opponent’s past behavior, a necessary assumption underlying the grim-trigger or carrot-stick strategy in repeated games.

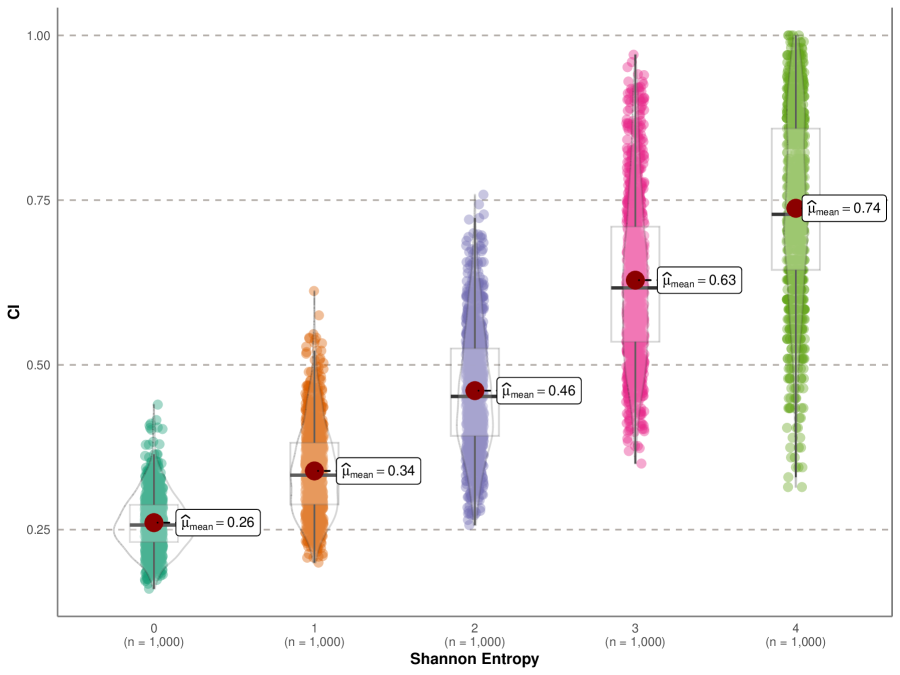

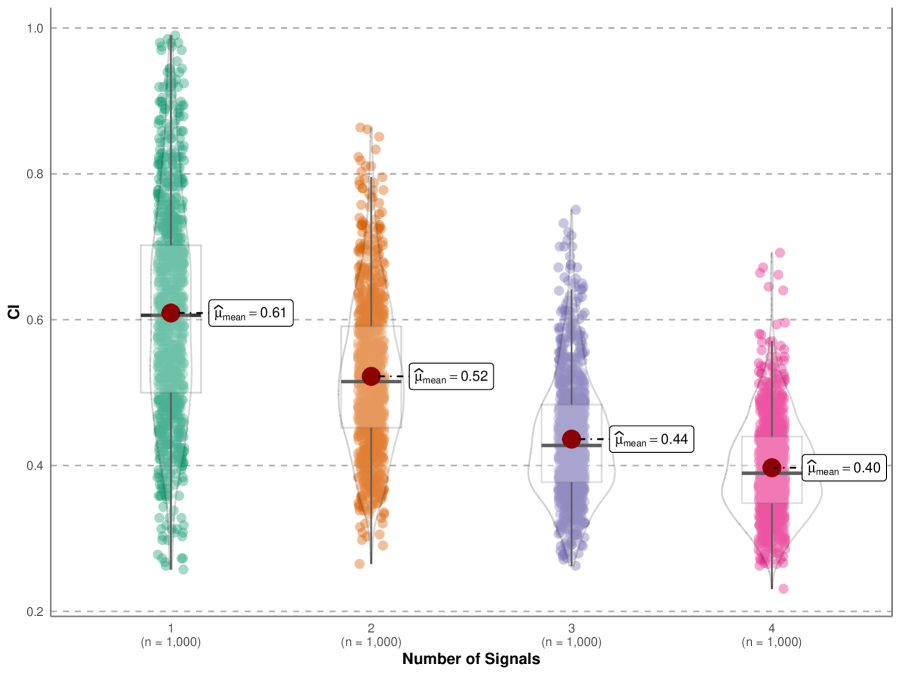

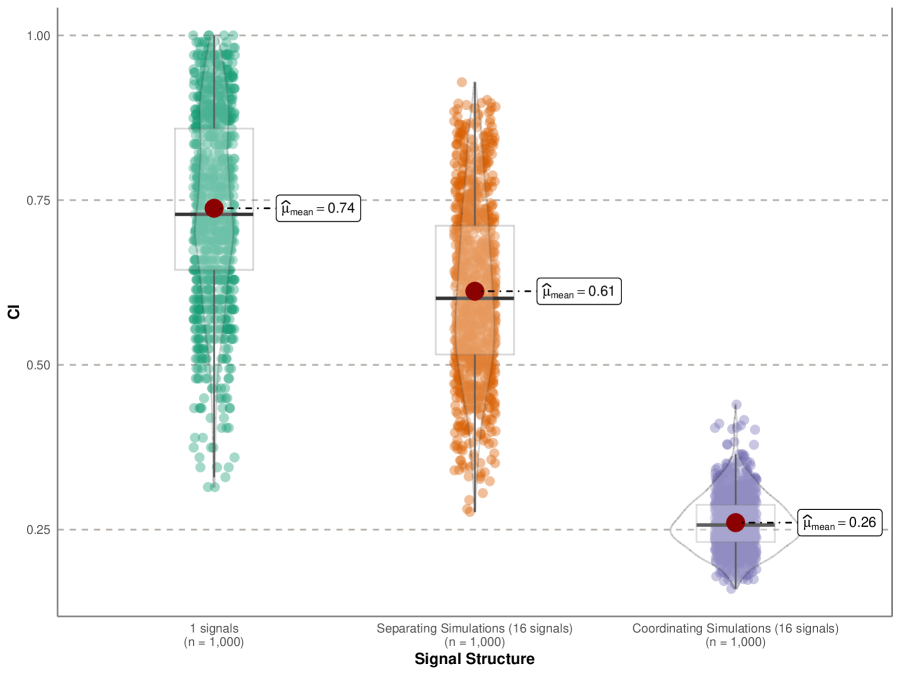

This argument is also related to a recent paper Colliard et al. (2022), which shows that decreasing the uncertainty of the underlying state makes it easier for AI agents to learn competitive strategies and thus reduces the degree of collusion. However, the information structure in their paper is fixed, since AI agents always receive a single signal. Their framework cannot accommodate our setting where the information structure varies but the prior state distribution is fixed. To show that these three arguments cannot fully explain our results, we run the auxiliary experiments where the underlying state is certain and fixed at 10 (the expected WTP in the original experiments), and AI agents receive different numbers of payoff-irrelevant signals. The results are shown in Figure 9. Even in the absence of uncertainty, as the number of payoff-irrelevant signals increases from to , the collusion index decreases from to . This observation implies that, in addition to reducing uncertainty and enabling effective price discrimination, the information structure as a correlating device also plays a role in mitigating collusion. Before discussing how the correlating device works, we first compare the significance level of these two roles in mitigating collusion. Figure 9 compares the (average) collusion level under three scenarios: there are 16 uniformly distributed states with a single observed signal, there is only a single state, and there are 16 uniformly distributed states and 16 corresponding perfect-revealing signals. Compared to the first scenario, only the uncertainty is removed in the second scenario. Accordingly, the CI only decreases from 0.74 to 0.61. Compared to the second scenario, the third scenario includes a correlating device, but also removes uncertainty. The collusion index drops sharply from 0.61 to 0.26. Thus, in the original experiment, when the Shannon entropy is reduced from 4 to 0, the removal of uncertainty or the strengthening of price discrimination accounts for only 27.1 percent of the reduction in collusion, while the correlating device accounts for 72.9 percent of the reduction in collusion.101010The differences of average Collusion Index for each signal when Shannon Entropy is (0,0) can be found in Figure 18 in Appendix. Thus, the Observation 2 should be attributed more to the presence of the correlating device than to the removal of uncertainty or the reinforcement of price discrimination.

5.2 Potential Reasons

To address how the information structure affects the degree of collusion through the correlating device, we first answer how AI agents achieve collusive outcome under a single signal. Basically, similar to Colliard et al. (2022); Abada and Lambin (2023), we attribute the supra-competitive price to the failure to learn competitive prices. Suppose it starts with a price pair where player 2 wins the market. For any chosen price, as long as player 1 loses the market, his Q-value of that price decreases, forcing him to change his pricing strategy until he finds a lower price. Then it is player 2’s turn to search downward. We call this process sequential and alternating downward search. Ideally, as long as this process continues, the price level should converge to the Bertrand Nash equilibrium. However, this process can be interrupted because low prices cannot be maintained even if he wins the market and takes all the profit, because the Q-value of this low price is overestimated for some reason. If this process is interrupted, then both AI agents will search for other pricing strategies, and if by chance both agents choose the same relatively high pricing strategy at the same time, then they may converge at this supra-competitive price. For more details, see our accompanying note Xu et al. (2024), also attached in the Appendix D.

Then we move on to the multi-signal scenario. On the one hand, suppose that the AI agents are in fierce competition under certain signals . The competition under these signals lowers their payoffs in the stage game and thus the Q-values of these signals. Under the remaining signals , as the process of sequential and alternating downward search proceeds, suppose an AI agent has just found a lower price that can be sustained by the Q-value at signals . Then it is the turn of the other AI agent to search downwards. During this process, if signals transition to signals with fierce competition, then the low Q-value at signal will significantly reduce the Q-value of price at signal . This forces the AI agent to stop choosing at signal and to search for an appropriate price together with agent , resulting in an interruption of the process of sequential and alternating downward search. Correspondingly, competition under certain signals increases the probability of interruption of the process of sequential and alternating downward search, thus increasing both the probability and the intensity of the collusive outcome under the remaining signals. And vice versa.

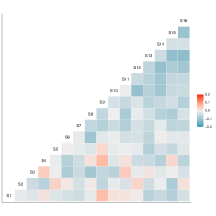

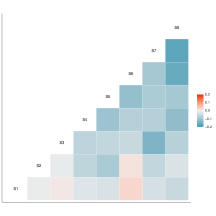

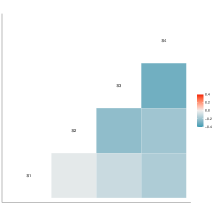

To support this reasoning, we further study the collusion degree among different signals by fixing the information structures. First, we study the empirical correlations between collusion levels among different signals. Pearson Correlation Coefficient is one of the classical correlation coefficients used to measure the strength and direction of the linear relationship between two continuous variables. The expression of Pearson Correlation Coefficient for CIs between signal and is

| (7) |

where is the number of samples, is the Collusion Index of the session under signal , is the sample average of . The correlation coefficients among collusion degree under various signals is plotted in Figure 10. Based on this figure, we then make Observation 3.

Observation 3.

Fixing information structure, collusion index among different signals are negatively correlated.

Figure 10 shows the correlation coefficients of CIs between different signals at different levels of information precision. The graph is almost stacked with blue blocks, indicating negative correlations in collusion levels between signals. In other words, if both agents are in fierce competition on some signals, they are more likely to collude on the other signals. And vice versa.

It is argued that competition under certain signals facilitates collusive outcomes under the remaining signals. Then, under which signals are they more likely to compete or collude?

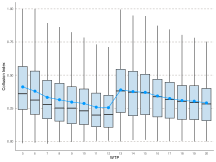

Observation 4.

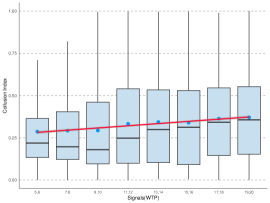

The Collusion Index is higher in markets consisting of consumers with higher expected WTP.

The Figure 11 plots the CI across signals for information structures with Shannon entropy , , and , respectively. It shows that these AI agents seem to adapt to collude more in high-value markets, while competing fiercely in low-value markets. One possible explanation is that, given significant differences in WTP, a higher level of collusion in high-value markets generates a much higher level of Q-value compared to the Q-value in low-value markets. These higher levels of Q in high-value markets then stabilize the process of sequential and alternating downward search in low-value markets, facilitating the learning of competitive strategies. And vice versa. Therefore, it is more likely that AI agents will be more staggered in collusion outcomes. This observation is in stark contrast to the one in asymmetric information structure, where high-value markets in the same state partition end up with low collusion levels. This result again demonstrates that information structure also plays a key role in determining coordination among multi-agent reinforcement learning.

6 Welfare Analysis and Economic Implications

6.1 Welfare Analysis

AI’s use of data for price discrimination has profound implications for industry profits and consumer surplus. The critical questions revolve around the extent to which designers should provide data to AI to maximize the firm’s profit, and how to protect consumer surplus through data control measures.

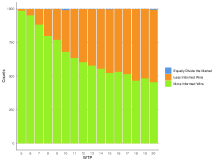

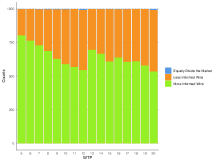

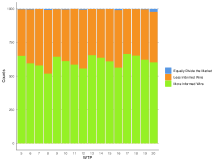

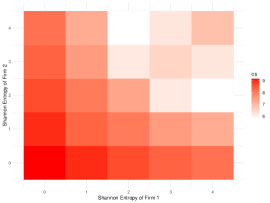

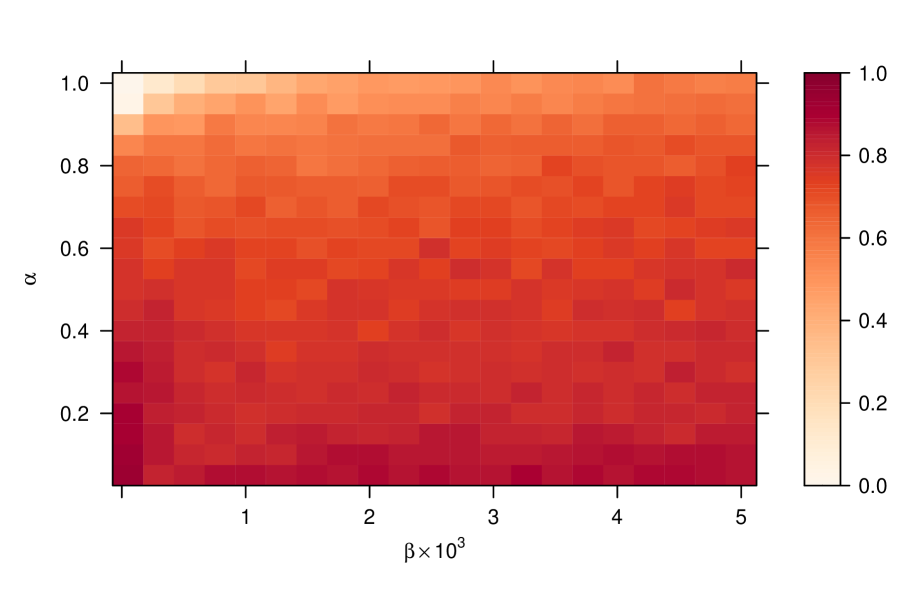

We focus first on the impact of AI information precision on industry profits, as shown in Figure 12.

Figure 12 shows that in symmetric scenarios, industry profits tend to decrease with increased data usage for discrimination, except in the extreme case of no data usage. Recall that in Observation 2, the CI is higher when the Shannon entropy is than when the Shannon entropy is . However, the industry profits when the Shannon entropy is are lower than when the Shannon entropy is . The main reason is that monopolistic profits are higher when the Shannon entropy is than when it is . Moreover, one can see that from the Shannon entropy of to , the industry profits first go up and then go down. This kind of inverted U-shaped trend is in line with certain theoretical results (e.g. Chen et al. (2001)). Moving from the Shannon entropy of to , more precise information simultaneously increases transaction efficiency and reduces collusion. Once information precision exceeds a relatively modest benchmark of (the corresponding Shannon entropy is ), the adverse effects of reducing collusion begin to offset the gains in transaction efficiency, culminating in reduced profits.

In asymmetric situations, where the price discrimination ability of the more informed AI remains constant, the industry profits decrease as the less informed AI uses more data. Furthermore, we find that industry profits peak when the Shannon entropy pairs are either or , and are lowest when both entities can perform first-order price discrimination. It is also apparent that blocks along the symmetry line appear more white than other nearby regions, indicating that the more symmetric information would tend to induce higher consumer surplus and lower industry profits.

For all situations, the numbers in Figure 12 illustrate the distribution of profits among firms by placing them in the context of a standard static game. The Nash equilibria of this game are at points or . If firms choose their prediction precision in a manner similar to human competition, they will choose a precision level of (corresponding to a Shannon entropy of 2) or no prediction precision (Shannon entropy of 4) in the equilibria, even if they have the ability to fully differentiate between different consumers. However, if firms provide accurate consumer WTP information to the pricing algorithms, Q-learning cannot pretend not to know these accurate predictions, resulting in a market outcome where the Shannon entropy is . We think the most likely reason is that Q-learning is incapable of learning such sophisticated strategies. We refer to the behavior of Q-learning always using the most accurate signals as the pricing algorithm’s over-usage of data.

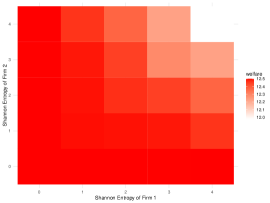

If we look at consumer surplus and social welfare in Figure 13, we see that the effect of AI information accuracy is opposite to that of industry profit.

We observe that consumers generally benefit from firms’ data-driven discrimination, maximizing surplus when firms have the most accurate consumer information. This trend also holds for social welfare. For consumer surplus, blocks along the symmetry line appear more red than other nearby regions, indicating that more symmetric information would tend to induce higher consumer surplus and lower industry profits.

The reason for the effects of information precision is the same as we mentioned in the section on industry profits. On the one hand, as Shannon entropy decreases, firms gain more precise information about consumers, allowing flexible pricing strategies and increasing social welfare. On the other hand, lower entropy limits the ability of firms to collude effectively. Consumers benefit from both of the above channels, so that consumer surplus strictly increases as Shannon entropy decreases.

6.2 Economic Implication

The over-usage of data, which we propose in our analysis of industry profits, suggests that it may not always be beneficial for firms to incorporate extensive consumer data into their price discrimination systems. Therefore, for firms aiming to increase profits through big data and AI, this is one of the drawbacks of artificial intelligence, along with Calvano et al. (2023b); Bonelli (2022). Thus, firms aiming for high profits through algorithmic pricing should carefully choose the optimal information precision for algorithms, instead of providing the most precise data and letting the algorithm filter it.

It is important to note, however, that the reasoning behind our results is very different from human competition. In human competition, collecting more consumer data typically leads to higher profits, resembling a prisoner’s dilemma (Thisse and Vives 1988): regardless of opponents’ data holdings, acquiring more data is advantageous, even if it is detrimental to all parties if data collection increases across the board. However, in scenarios where AI replaces human participants, learning failures lead to collusive outcomes. In such situations, the accumulation of more data is always detrimental. Despite this, AI fails to recognize the detrimental effects and continues to engage in price discrimination, perpetuating the overuse of data.

Price discrimination can be exacerbated by competition, and algorithmic collusion is the second implication. Price discrimination involves setting different prices for different groups of consumers. According to Proposition 1, the Bayesian Nash equilibrium in human pricing involves both firms setting the lowest available action for each consumer. However, as shown in Observation 4, when firms use Q-learning to set prices, they tend to achieve higher collusion levels in markets with high WTP, resulting in generally higher prices for consumers with high WTP. As a result, algorithmic collusion could exacerbate price discrimination and raise fairness concerns.

The final implication underscores that allowing firms to exploit data is not necessarily detrimental to consumers, regardless of factors such as algorithmic recommendations that directly increase consumer utility. A primary concern regarding the use of data is that firms may use consumer data to maximize profits at the expense of consumer surplus. However, our results suggest that in scenarios involving data-driven price discrimination, firms’ use of data can increase consumer surplus and social welfare. Moreover, even if only a single AI is allowed to engage in data-driven price discrimination, collusion may be reduced because the AI must set exceptionally low prices at certain signals to manipulate competitors, thereby benefiting consumers.

7 Robustness

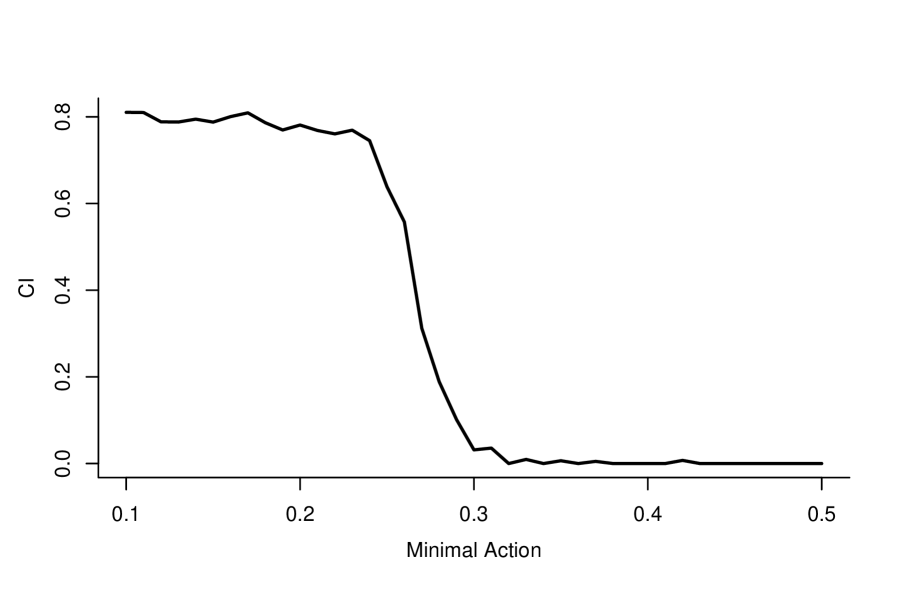

In this preliminary vision, we focus on assessing the robustness of our baseline results to variations in specific parameters. In the future, we plan to conduct a more comprehensive evaluation of the stability of our results across different economic environments. All “experiments” in this section consists of 100 simulations.

Initially, we assumed a uniform value of in each information structure in our baseline simulations. This approach results in different frequencies of random exploration within each cell of the Q-matrix across different information structures. To address this, we aim to standardize the number of random exploration instances in each cell of the Q-matrix across all information structures to ensure uniformity. Specifically, we set as a constant number of random exploration instances for each cell. The corresponding values are then derived using the formula presented in Equation 6.

The results of our robustness evaluations are meticulously illustrated in Figure 15 and Figure 16. The CIs for each information structure are closely aligned with those observed in our baseline scenario. As a result, the Observation 2 remains valid. In addition, Figure 16 shows that, in general, the CI for each signal continues to show an upward trend along with the expected WTP.

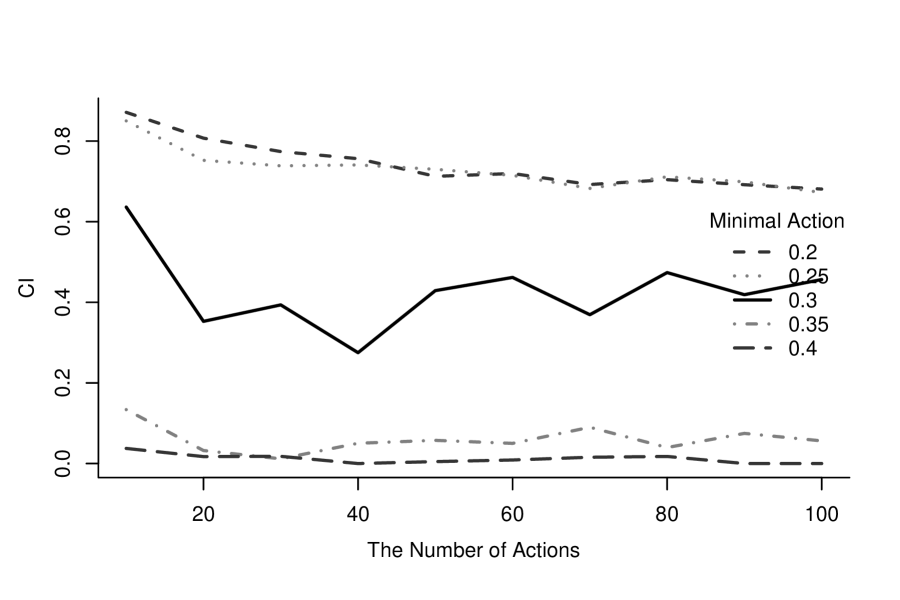

Then, we explore the robustness of our results with respect to the learning rate, . Effective learning requires persistence, suggesting that should be set to a relatively low value to ensure gradual integration of new information. In computer science, a commonly used value is 0.1, as highlighted in Calvano et al. (2020). To further validate the stability of our results, we examine the robustness of our findings across three additional values of , . Figure 15 shows that regardless of the learning rate, the CI consistently increases with respect to the Shannon entropy of the information structures.

8 Concluding Remarks

We study Q-learning driven algorithmic collusion under different information structures in an uncertain environment, and identify two novel mechanisms that sustain collusion. Under asymmetric information structure, the AI with an information advantage employs a Bait-and-Restrained-Exploit strategy to lure the less informed AI into setting high prices. Under symmetric information, AIs compete in low-value markets to ensure the sustainability of collusion in high-value markets.

Furthermore, we observe that uncertainty, the absence of correlated signals, and information asymmetry intensify collusion, leading to a reduction in both consumer surplus and social welfare.

The implications of this article are threefold: First, the excessive use of data by AIs for price discrimination weakens collusion in competitive markets, highlighting an important drawback for firms to consider when adopting AI strategies. Second, competition and algorithmic collusion can exacerbate price discrimination, undermining fairness in the market. Furthermore, regardless of factors such as algorithmic recommendations that directly increase consumer utility, the results of this study suggest that firms using data do not necessarily harm consumers. Thus, a more nuanced perspective on companies that collect and use data is advisable.

For future research, three key areas merit attention. First, a more general theoretical exploration of algorithmic collusion is crucial to better understand its underlying mechanisms. Second, the study of market segmentation adds an interesting dimension to this work. Finally, providing empirical evidence on algorithmic collusion is essential to gain a deeper understanding of its dynamics.

References

- Abada and Lambin (2023) Abada, I. and X. Lambin (2023, September). Artificial Intelligence: Can Seemingly Collusive Outcomes Be Avoided? Management Science 69(9), 5042–5065.

- Asker et al. (2022) Asker, J., C. Fershtman, and A. Pakes (2022). Artificial intelligence, algorithm design, and pricing. In AEA Papers and Proceedings, Volume 112, pp. 452–56.

- Asker et al. (2023) Asker, J., C. Fershtman, and A. Pakes (2023). The impact of artificial intelligence design on pricing. Journal of Economics & Management Strategy.

- Aumann (1987) Aumann, R. J. (1987). Correlated equilibrium as an expression of bayesian rationality. Econometrica, 1–18.

- Banchio and Mantegazza (2023) Banchio, M. and G. Mantegazza (2023). Adaptive algorithms and collusion via coupling. In Proceedings of the 24th ACM Conference on Economics and Computation, EC ’23, New York, NY, USA, pp. 208. Association for Computing Machinery.

- Banchio and Skrzypacz (2022) Banchio, M. and A. Skrzypacz (2022). Artificial intelligence and auction design. In Proceedings of the 23rd ACM Conference on Economics and Computation, EC ’22, New York, NY, USA, pp. 30–31. Association for Computing Machinery.

- Bergemann and Morris (2016) Bergemann, D. and S. Morris (2016). Bayes correlated equilibrium and the comparison of information structures in games. Theoretical Economics 11(2), 487–522.

- Bonelli (2022) Bonelli, M. (2022, November). Data-driven Investors.

- Calvano et al. (2020) Calvano, E., G. Calzolari, V. Denicolò, and S. Pastorello (2020, October). Artificial Intelligence, Algorithmic Pricing, and Collusion. American Economic Review 110(10), 3267–3297.

- Calvano et al. (2023a) Calvano, E., G. Calzolari, V. Denicolò, and S. Pastorello (2023a, September). Algorithmic collusion: Genuine or spurious? The 49th Annual Conference of the European Association for Research in Industrial Economics, Vienna, 2022 90, 102973.

- Calvano et al. (2023b) Calvano, E., G. Calzolari, V. Denicolò, and S. Pastorello (2023b). Artificial Intelligence, Algorithmic Recommendations and Competition. Algorithmic Recommendations and Competition (May 14, 2023).

- Calvano et al. (2021) Calvano, E., G. Calzolari, V. Denicoló, and S. Pastorello (2021, December). Algorithmic collusion with imperfect monitoring. International Journal of Industrial Organization 79, 102712.

- Chen et al. (2001) Chen, Y., C. Narasimhan, and Z. J. Zhang (2001). Individual marketing with imperfect targetability. Marketing Science 20(1), 23–41.

- Colliard et al. (2022) Colliard, J.-E., T. Foucault, and S. Lovo (2022). Algorithmic pricing and liquidity in securities markets. HEC Paris Research Paper.

- Dearden et al. (1998) Dearden, R., N. Friedman, and S. Russell (1998). Bayesian q-learning. Aaai/iaai 1998, 761–768.

- Dou et al. (2023) Dou, W. W., I. Goldstein, and Y. Ji (2023). Ai-powered trading, algorithmic collusion, and price efficiency. Available at SSRN 4452704.

- Epivent and Lambin (2022) Epivent, A. and X. Lambin (2022, August). On Algorithmic Collusion and Reward-Punishment Schemes.

- Forges (1993) Forges, F. (1993). Five legitimate definitions of correlated equilibrium in games with incomplete information. Theory and Decision 35, 277–310.

- Gautier et al. (2020) Gautier, A., A. Ittoo, and P. Van Cleynenbreugel (2020). Ai algorithms, price discrimination and collusion: A technological, economic and legal perspective. European Journal of Law and Economics 50(3), 405–435.

- Harsanyi (1968) Harsanyi, J. C. (1968). Games with incomplete information played by “bayesian” players part ii. bayesian equilibrium points. Management Science 14(5), 320–334.

- Johnson et al. (2023) Johnson, J. P., A. Rhodes, and M. Wildenbeest (2023). Platform design when sellers use pricing algorithms. Econometrica 91(5), 1841–1879.

- Klein (2021) Klein, T. (2021). Autonomous algorithmic collusion: Q-learning under sequential pricing. The RAND Journal of Economics 52(3), 538–558.

- Miklós-Thal and Tucker (2019) Miklós-Thal, J. and C. Tucker (2019). Collusion by algorithm: Does better demand prediction facilitate coordination between sellers? Management Science 65(4), 1552–1561.

- Mitchell (1997) Mitchell, T. M. (1997). Machine Learning.

- Shaffer and Zhang (1995) Shaffer, G. and Z. J. Zhang (1995). Competitive coupon targeting. Marketing Science 14(4), 395–416.

- Shannon (1948) Shannon, C. E. (1948). A mathematical theory of communication. The Bell System Technical Journal 27(3), 379–423.

- Thisse and Vives (1988) Thisse, J.-F. and X. Vives (1988). On the strategic choice of spatial price policy. American Economic Review 78(1), 122–137.

- Waltman and Kaymak (2007) Waltman, L. and U. Kaymak (2007). A theoretical analysis of cooperative behavior in multi-agent q-learning. In 2007 IEEE International Symposium on Approximate Dynamic Programming and Reinforcement Learning, pp. 84–91. IEEE.

- Waltman and Kaymak (2008) Waltman, L. and U. Kaymak (2008). Q-learning agents in a cournot oligopoly model. Journal of Economic Dynamics and Control 32(10), 3275–3293.

- Watkins and Dayan (1992) Watkins, C. J. and P. Dayan (1992). Q-Learning. Machine Learning 8, 279–292.

- Watkins (1989) Watkins, C. J. C. H. (1989). Learning from Delayed Rewards.

- Wu et al. (2023) Wu, J. X., Y. Wu, K.-Y. Chen, and L. Hua (2023). Building socially intelligent ai systems: Evidence from the trust game using artificial agents with deep learning. Management Science 69(12), 7236–7252.

- Xu et al. (2024) Xu, Z., M. Zhang, and W. Zhao (2024). Channel underlying ai collusion. Working Paper.

Appendix A Proof of Proposition 1

It is straightforward that any player quoting is a BNE, and proving (3) is trivial.

(1) Let denote the equilibrium transaction price distribution in state for . We define as the maximum price in state with positive transaction probability, where is the maximum of over all states in . The corresponding state is denoted by .121212This is due to the discrete setting of signal and state.

Suppose a player earns a positive profit, which implies the existence of a signal for player with and , with a positive probability of market participation under state . So there must also exist for player with and . Therefore, player optimally lowers the price quote on signal to , where is small enough, since quoting the original price will at most share the market with others in any state. Consequently, in any equilibrium, degenerates to a constant for all .

(2) Without loss of generality, suppose that player offers under signal . According to (1), there exists a signal such that and have a positive probability of occurring together, and player quotes under signal . However, player has an incentive to bid higher on signal in order to make a positive profit.

Appendix B The Introduction of Q-Learning

B.1 Signal-Agent Q-Learning

Q-learning is a fundamental concept in reinforcement learning, a branch of machine learning where an agent learns to make decisions by interacting with an environment. At its core, Q-learning is a model-free, off-policy reinforcement learning algorithm used to find the optimal action-selection policy for a given finite Markov decision process.

In a stationary Markov decision process, in each period an agent observes a state variable131313In this context, “state” does not refer to the “state” or WTP, but rather to the “signal” discussed in the main section. To be consistent with the traditional literature, and with a slight abuse of notation, we use the notation to represent “state” here, while it denotes the “signal” in the main body of the discussion. and then chooses an action . For any and , the agent obtains a reward , and the system moves to the next state , according to a time-invariant (and possibly degenerate) probability distribution . The goal of the agent is to find an optimal strategy for choosing actions. A strategy is optimal if in each state it selects an action that maximizes the agent’s cumulative payoff, which is the sum of its immediate payoff and its future payoffs.

Q-learning was proposed by Watkins (1989) to find an optimal strategy with no prior knowledge of the underlying model, i.e., the distribution . The algorithm works by iteratively updating an action-value function , which estimates the expected cumulative reward of taking action in state . The key idea behind Q-learning is the Bellman optimal equation, which states that the optimal action-value function satisfies the equation:

| (8) |

where denotes the discount factor. If the values of the function are known, an optimal strategy is given by

| (9) |

Q-learning algorithm estimate the values iteratively. Starting from an arbitrary initial matrix , after choosing action in state , the algorithm observes immediate payoff and next state and updates the estimated -values, denoted by using the update rule:

| (10) |

where is called the learning rate. Note that only for the cell visited, the corresponding -value is updated. It is proven in Watkins and Dayan (1992) that values estimated will converge with probability to the optimal ones if each action is executed in each state an infinite number of times and is decayed appropriately. In deterministic Markov decision process convergence of values can also be proven if a fixed value is used for (Mitchell, 1997).

B.2 Exploration Policy

Exploration and exploitation are two fundamental concepts in reinforcement learning and decision-making processes. To have a chance to approximate the true function starting from an arbitrary , all actions must be tried in all states. Exploration allows the agent to discover the environment and learn about unknown states and actions. Exploitation, on the other hand, involves leveraging the information the agent already has to maximize immediate rewards. It entails choosing actions that are known to be rewarding based on past experiences or learned knowledge. Balancing exploration and exploitation is crucial for achieving optimal long-term performance in reinforcement learning tasks, as too much exploration may lead to inefficiency, while too much exploitation may cause the agent to miss out on potentially better actions or opportunities for learning. Strategies such as -greedy, Boltzmann exploration and upper confidence bound are commonly used in various reinforcement learning algorithms and decision-making contexts.

Appendix C Additional Figures

Appendix D Note: Channel Underlying AI Collusion

In this note, we will explain why AIs cannot learn Nash equilibrium in most cases, even if there is no memory.

D.1 Q-Learning

Q-learning was proposed by Watkins (1989) to find an optimal strategy with no prior knowledge of the underlying model. Starting from an arbitrary initial matrix , after choosing action in state , the algorithm observes immediate payoff and next state and updates the one element of the Q-matrix corresponding to to be

| (11) |

where is called the learning rate and denotes the discount factor.

To ensure that Q-learning sufficiently explores all states and actions, in this paper, we use the -greedy strategy. With probability , it chooses the action that is optimal according to the current Q-matrix and to randomize uniformly across all actions with probability . For a more detailed introduction to Q-learning, please see Appendix B.

In the special case that the environment is a Markov decision process that has only one state, this canonical Q-learning has a reduced form. Since the action taken in the current period does not affect the payoffs received in future periods, it follows that, in theory, maximizing the cumulative payoff is tantamount to maximizing the immediate payoff.141414the action executed influence future payoffs only through influencing the future states. Hence, the update rule reduces to

| (12) |

This signal-state Q-learning is a special case of the canonical Q-learning with the discount factor set to . In the single-agent problems, if the environment has only one state, it is without loss of generality to use the reduced Q-learning algorithm. However, in multi-agent Q-learning framework, the discount factor is a crucial parameter that determines the game’s converging outcome, even if there is only one state. In the following context, “reduced Q-learning” refers to signal-state Q-learning, while “Q-learning” denotes the canonical Q-learning.

D.2 Experiment Design

We have constructed Q-learning algorithms and let them interact in a repeated Bertrand oligopoly setting. For each set of parameters, an “experiement” consists of 100 sessions. In each session, agent play against the same opponents until convergence as defined below.

Here we describe the economic environment in which the algorithms operate, discrete action space and other aspects of the numerical simulations.

D.2.1 Economic Environment

We take as our stage game the standard Bertrand pricing game. Consider firm with marginal cost . Firms sell homogeneous goods and compete by setting prices. The buyer’s reservation value for the good is denoted by . In each period, a unit continuum of buyers enters the market. If there is no price lower than , the buyers will leave the market without making a purchase. Otherwise, each buyer will randomly choose a firm with the lowest price to buy from. We denote the lowest price as . The set of firms with the lowest price (lower than ) is denoted by . We parameterize the model such that demand faced by firm is151515For a set , in this paper represents the size of the set .

| (13) |

The per-period reward accruing to firm is then . In the symmetric setting, the unique Bertrand-Nash price is and the monopoly price is when the action space is continuous.

D.2.2 Action Space

Since Q-learning requires a finite action space, we need discretize the model. Similar to Calvano et al. (2020), we take the set of the feasible prices to be given by equally spaced points in the interval , where . The rationale behind setting the lowest price as the Bertrand-Nash price plus twice the spacing is to ensure uniqueness of the Bertrand-Nash equilibrium in this discrete framework. Additionally, monopoly price is exactly in this set and we allow one price slightly higher than the monopoly price.

D.2.3 Other Settings

The following settings are the same as that in Calvano et al. (2020). Regarding the exploration mode, we also use the -greedy model with a time-declining exploration rate. Specifically, we set , where is a parameter. As for the initial matrix , our baseline choice is to set the Q-values at at the discounted payoff that would accrue to player if opponents randomized uniformly.

D.3 Baseline Outcomes

In the baseline simulation, the Q-learning algorithms are memoryless (see Calvano et al. (2020) for the setting of memory). We focus on a baseline economic environment that consists of symmetric duopoly () with , , , . In the baseline simulation setup, we fix . To establish reasonable values for , it is useful to relate to the expected number of times a cell would be visited purely through random exploration over an infinite time horizon, denoted by . In the single-state without memory case, we have:

| (14) |

For our baseline scenario, we set , which corresponds to when .

For strategic games played by Q-learning algorithms there are no general convergence results. To verify convergence, we use the following piratical criterion: convergence is deemed to be achieved if for each player either the action chosen in each state does not change for consecutive periods161616If a state has not been visited for consecutive periods, we maintain that the chosen action in this state remains unchanged for the consecutive periods. which is a little different with the criterion in Calvano et al. (2020). We stop the algorithms if they do not converge after 1 billion periods.

To quantify the degree of collusion, we introduce a collusion index (CI), which is a normalized measure inspired by Calvano et al. (2020):

| (15) |

where is the average total profit upon convergence, is the total profit in the Bertrand-Nash static equilibrium, and is the profit under monopoly. In our setting, is the lowest price in the discrete action space, ans is equal to buyer’s reservation value, .

D.3.1 Collusion Index under Standard Q-Learning and Single-State Q-Learning

To compare the outcomes of the game played by standard Q agents and single-state Q agents, we focus on our baseline environment and explore the entire grid of the points by varying in the range and in . Here, the lower and upper bounds of correspond to and respectively.

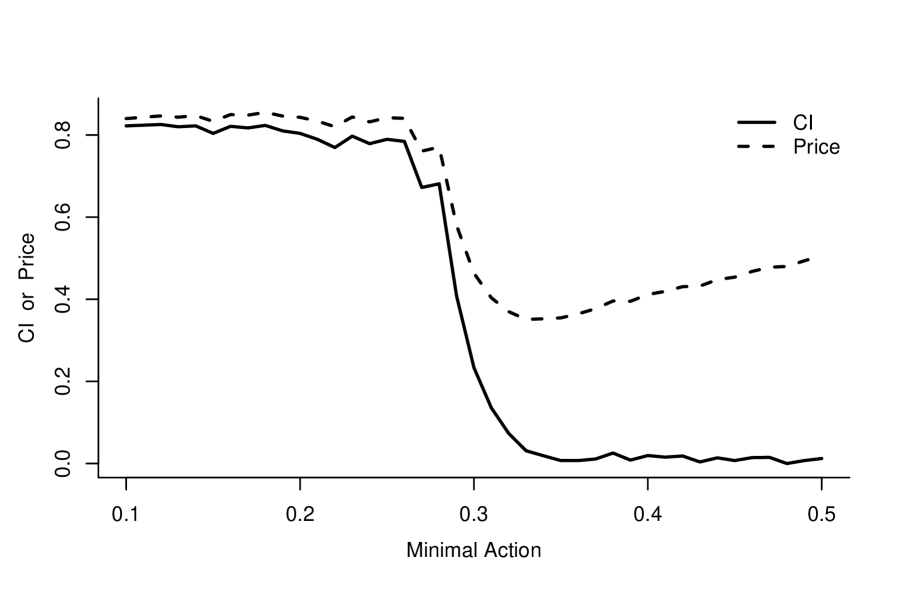

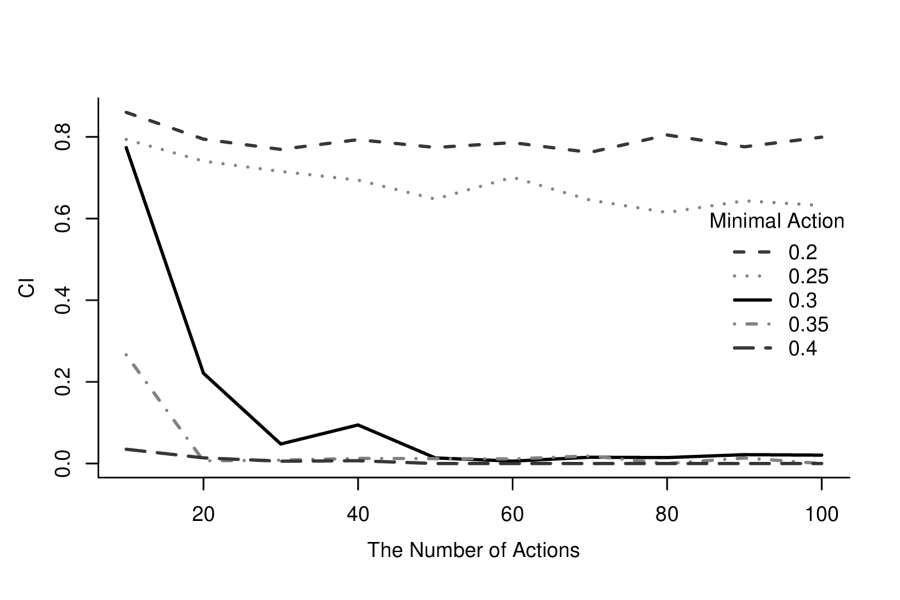

Figure 20 and Figure 20 illustrate CI for grid values of and in standard and single-state settings, respectively. It is evident that under standard Q with , except for the region where approaches and approaches , the degree of collusion remains notably high. When , even the lowest CI exceeds . In contrast, under single-state Q, the CI is near across the grid, with the highest CI being occurring at .

The first finding of the paper indicates that in a multi-agent game scenario, despite having only one state, standard Q agents and single-state Q agents exhibit notably distinct behaviors. Focusing solely on single-state Q agents within a one-state environment entails a loss of generality. Moreover, considering the uncertainty inherent in real economic environments or the prevalence and practicality of adding memory about past actions in algorithms, employing standard Q-learning to analyze single-state environments is more reasonable for a comprehensive depiction of reality.

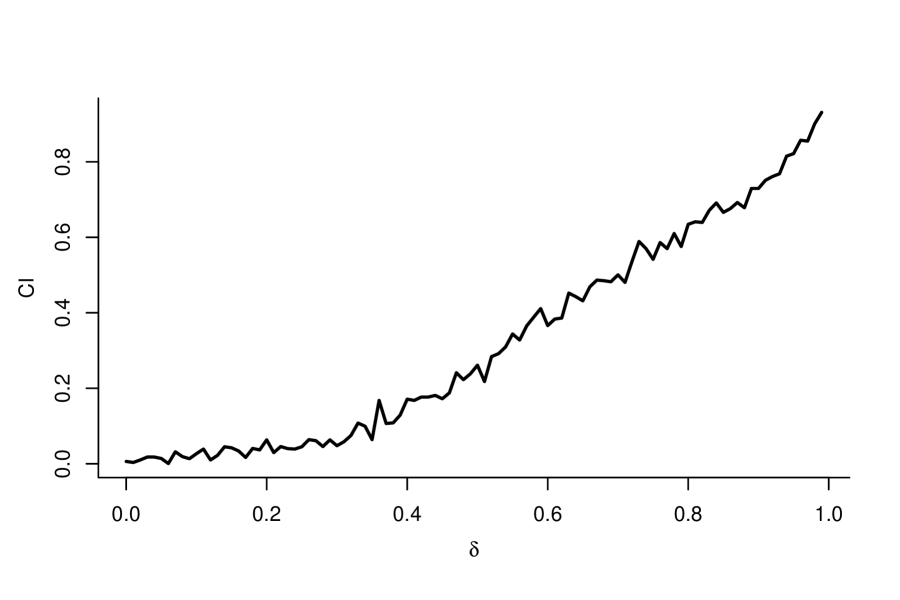

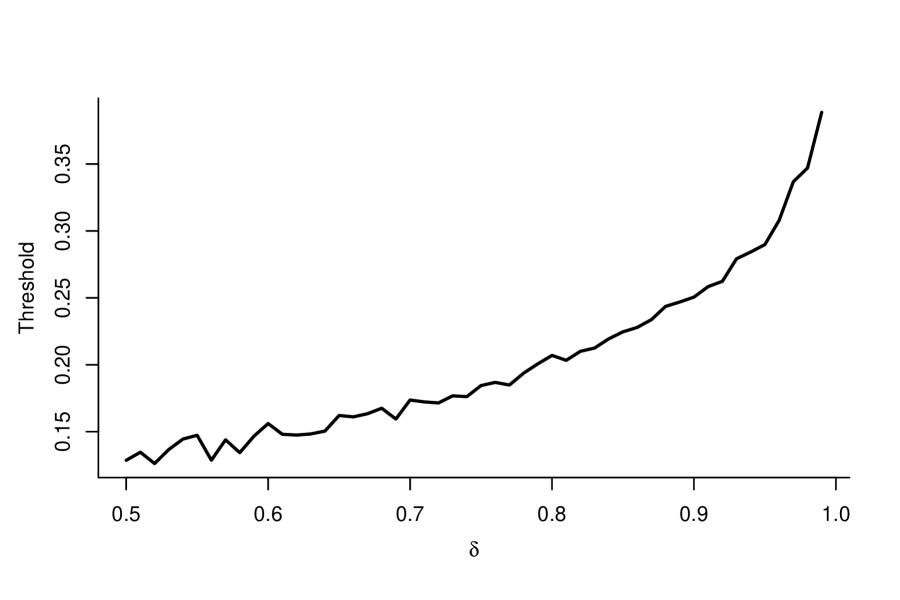

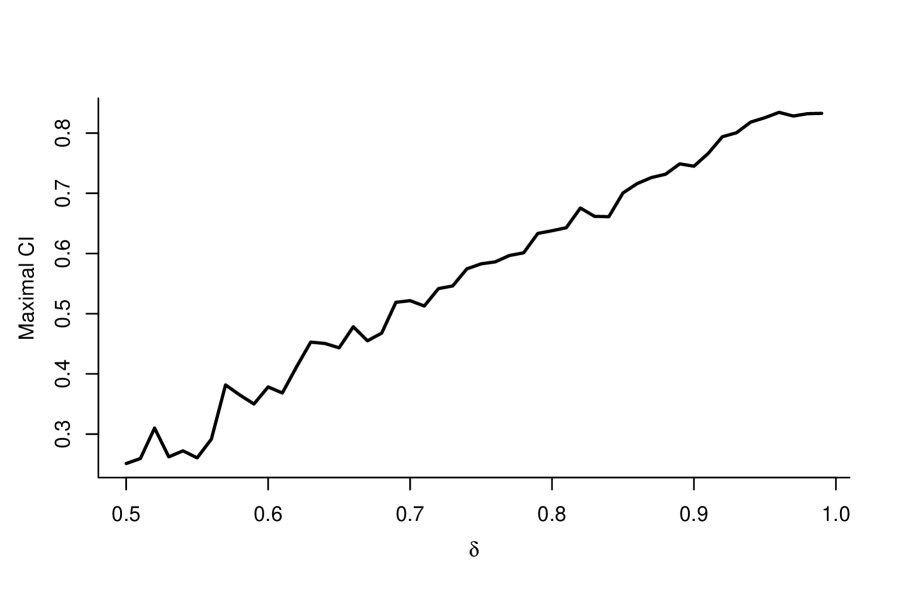

Note that single-state Q-learning is merely a special case of standard Q-learning with . The disparity in behavioral outcomes between the single-state Q agents and the standard Q agents in the game essentially stems from the variance in . To delve deeper into the influence of the discount factor on collusive behavior among AI agents, Figure 22 demonstrates how CI fluctuates with variations in in the baseline environment. The trend indicates that with the increasing value of , the degree of collusion tends to rise. This observation aligns with findings from Calvano et al. (2020), where Q-learning with memory was employed. When , which is not overly stringent, CI surpasses , indicating a significant level of collusion that cannot be ignored.

D.4 Channel Underlying AI Collusion

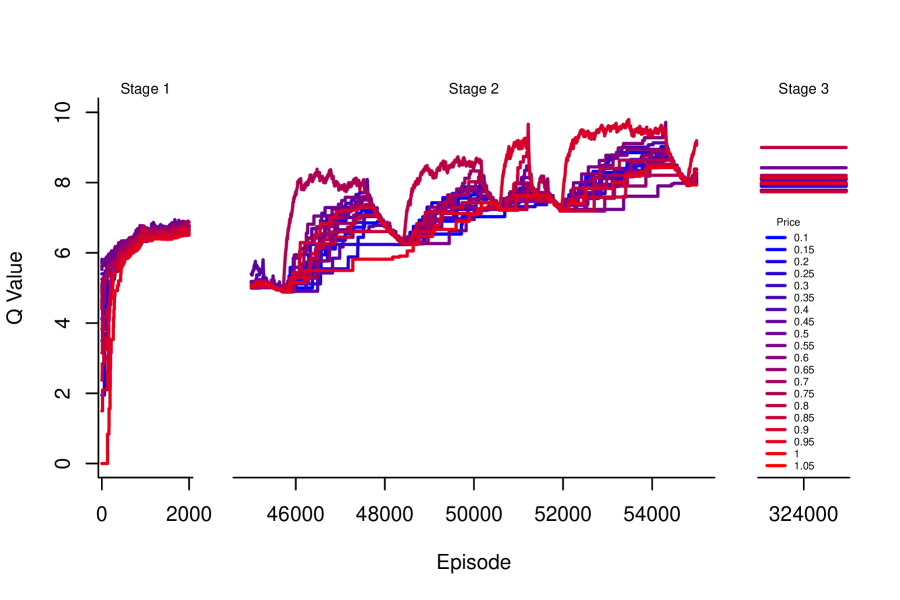

To unveil the channels underlying AI collusion, we initially delve into the entire process of a single simulation. Figure 22 illustrates the series of Q-matrix values throughout the simulation. In the initial phase, the Q-values converge to nearly identical values, resulting in a Q-value “bubble”. Subsequently, agents sequentially and alternately downward search for lower prices to capture market share from their opponents. However, once their prices dip below a certain threshold, they rebound to the higher price and maintain it for an extended period. After numerous iterations of this process, in the third phase, they settle into a high collusion state as the exploration rate decays to zero.

To facilitate analysis, let us introduce some key concepts.

D.4.1 Sustainable Line and Stationary Line

We define a price as sustainable if, upon selection and monopolizing the entire market, its corresponding Q value will not decrease. Initially, we introduce the concept of a sustainable line, which represents the minimal price capable of sustaining the current chosen Q value. In our framework, the sustainable line is delineated by

| (16) |

Should the selected price fall below the sustainable line, it fails to maintain its Q value. Even if it constitutes the best response to the opponent’s chosen price, the player will abandon this price in the subsequent period.

For a price profile , if it can sustain under Q-matrix indefinitely without exploration, we designate as the stationary price profile under . Notably, if is a stationary price profile, then . To simplify, we denote as a stationary price under if represents the stationary price profile under .

While a high price is sustainable, it may not persist as the stationary price. In the stationary price scenario, both agents choose the same price, resulting in each agent receiving half of the price as immediate profit. We introduce the stationary line as

| (17) |

If the price falls below the stationary line, it cannot remain as a stationary state under current Q-matrix. The stationary line is exactly twice the value of the sustainable line, allowing Q to search lower prices but preventing it from stabilizing at a low price.

D.4.2 Bubble

Due to the high exploration in the initial periods, the Q-values of each price converge to the same value, typically ranging from to , regardless of the different initial values. 171717If prices are chosen randomly, the average transition price can be calculated as follows: resulting in a corresponding Q-value of . This process injects a “bubble” into the Q-value, wherein it overestimates the discounted profit of lower prices. This bubble induces that prices lower than cannot be sustainable, and prices lower than cannot be stationary.

The crucial aspect of stabilizing at the lowest price lies in eliminating the bubble. However, accomplishing this debubbling process is highly challenging. Once they establish collusion at a high price, continuous exploration aimed at destabilizing the high price collusion will also inflate the bubble in the Q-value of lower prices. During the sequential and alternating downward search (as detailed in the next subsection), the bubble diminishes. However, when rebounding to a high price and stabilizing, efforts to debubble become futile.

D.4.3 Sequential and Alternating Downward Search

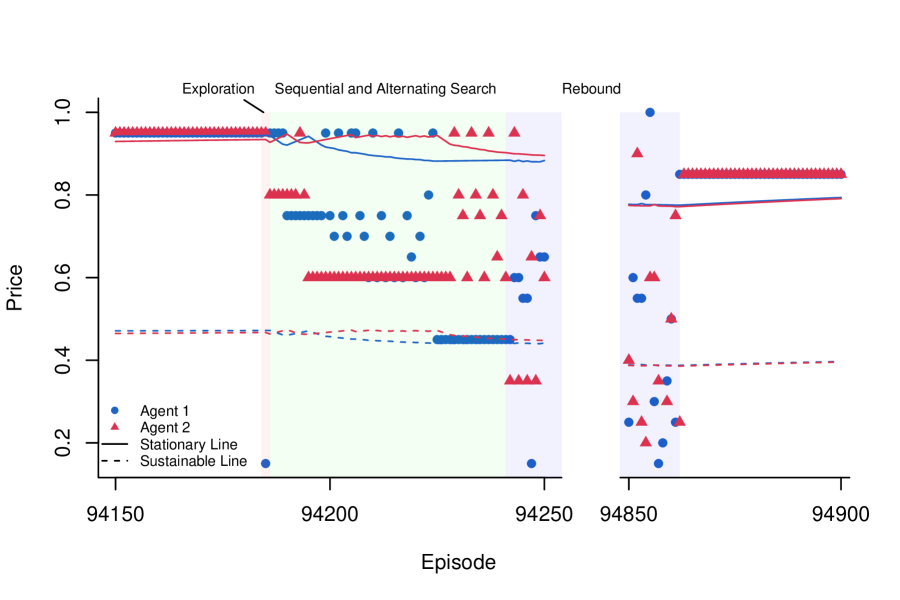

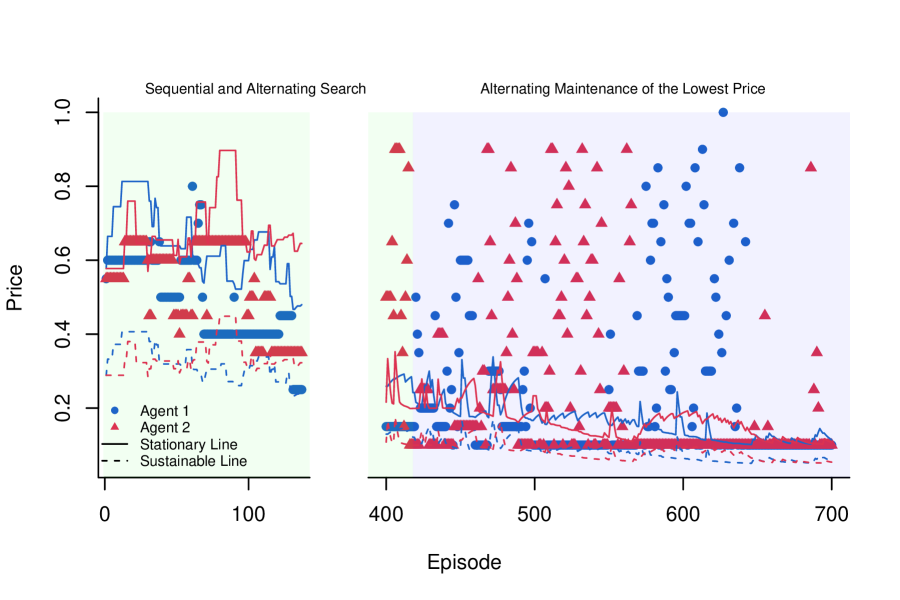

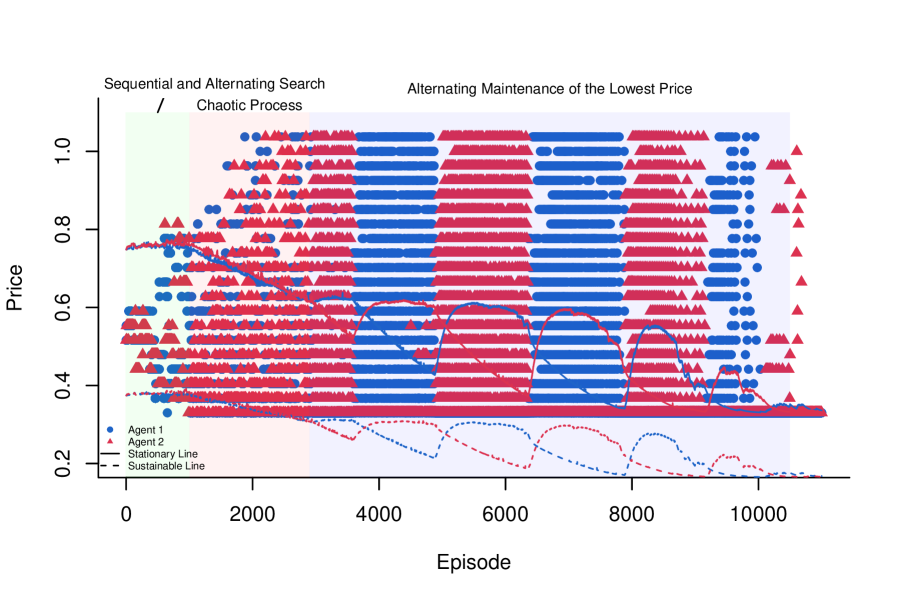

Figure 24, illustrating the descending phase within the second stage of Figure 22, depicts a mechanism leading towards the lowest value. This mechanism is commonly observed in 1000 simulations and is named sequential and alternating downward search. “Sequential” denotes the sequential decrease in price, while “alternating” signifies that agents lower their prices alternately.

Initially, starting from a high collusion point, after sufficient exploration (the last exploration being when agent [blue] explores to the lowest price, marked by a red background), agent (red) first learns to adjust its price downwards to maximize its profit. However, agent does not immediately respond due to the persistence of a high Q-value associated with the higher price. This delayed reaction leads to a rise in agent ’s Q-value corresponding to this new price. Subsequently, as agent begins to search for a more competitive price (i.e., a lower price), agent maintains its price at a constant level. This aspect can be viewed as a stationary learning process for agent , enabling him to discover a lower price.

After the sequential and alternating downward search, agent first quotes a price below the sustainable line, indicating that the immediate payoff is insufficient to sustain its corresponding Q-value. Subsequently, agent abandons this price and explores other options. However, since agent ’s price is almost at the sustainable line, agent struggles to find a price that yields positive profit and is sustainable. As a result, agent occasionally revisits this price below the sustainable line. This situation hinders agent from maintaining their price, leading both agents to continually select prices in a chaotic manner.

D.4.4 Rebound

In this chaotic process, the Q-value gradually decreases, with the speed of decrease being slow and dependent on the learning rate . A higher leads to a quicker decrease in the Q-value, reflecting a general decrease in the collusion index with an increase in . However, as the Q-value decreases, agents have a higher probability of sustaining at a high price, halting the Q-value decrease and transitioning to an increase.