Model-Free Local Recalibration of Neural Networks

Abstract

Artificial neural networks (ANNs) are highly flexible predictive models. However, reliably quantifying uncertainty for their predictions is a continuing challenge. There has been much recent work on “recalibration" of predictive distributions for ANNs, so that forecast probabilities for events of interest are consistent with certain frequency evaluations of them. Uncalibrated probabilistic forecasts are of limited use for many important decision-making tasks. To address this issue, we propose a localized recalibration of ANN predictive distributions using the dimension-reduced representation of the input provided by the ANN hidden layers. Our novel method draws inspiration from recalibration techniques used in the literature on approximate Bayesian computation and likelihood-free inference methods. Most existing calibration methods for ANNs can be thought of as calibrating either on the input layer, which is difficult when the input is high-dimensional, or the output layer, which may not be sufficiently flexible. Through a simulation study, we demonstrate that our method has good performance compared to alternative approaches, and explore the benefits that can be achieved by localizing the calibration based on different layers of the network. Finally, we apply our proposed method to a diamond price prediction problem, demonstrating the potential of our approach to improve prediction and uncertainty quantification in real-world applications.

Keywords: Calibration; Uncertainty assessment; Confidence interval; Coverage.

1 Introduction

Artificial neural networks (ANNs) are a highly effective class of predictive models which are widely used in many classification and regression tasks. Modern neural networks with higher representation capacity possess the flexibility to capture diverse nonlinear relationships within the modeled system. However, improvements in prediction have been associated with poor uncertainty quantification compared to earlier versions of these models (Guo et al., 2017; Kuleshov and Deshpande, 2022; Xiong et al., 2023; Dheur and Taieb, 2023). A possible exception to this phenomenon occurs in recent state-of-the-art non-convolutional architectures for image classification (Minderer et al., 2021).

Our work is concerned with probabilistic forecasts obtained from neural networks; that is, forecasts obtained from ANNs which take the form of probability distributions. For a sequence of probabilistic forecasts to be useful, it is desirable that they should be “calibrated". There are different kinds of calibration, but the common idea is that the forecast probabilities should agree with some frequency evaluations of them based on the observations. For example, one commonly used type of calibration would imply that for a sequence of events with forecast probability , half of them should occur in the limit of an increasing number of forecasts. Gneiting et al. (2007) suggest that probabilistic forecasting should aim to achieve sharpness of predictions (low uncertainty) subject to calibration, and discuss three different types of calibration – probabilistic, marginal, and exceedance calibration. Other notions of calibration have appeared more recently in the literature on uncertainty quantification methods for ANNs (discussed below). Calibrated uncertainty quantification is important in many high stakes applications of neural network models, for which quantifying the risk of undesirable outcomes may play an important role in decision making.

Our paper makes three main contributions. First, we consider a new approach to the recalibration of ANN predictive distributions, which localizes the calibration based on the representation of the input given by the ANN hidden layers. Existing methods of recalibration can be thought of as recalibrating based on the output layer, which may not be flexible enough, or on the input layer, which is difficult when the input is high-dimensional. The approach we describe is inspired by Rodrigues et al. (2018), in which the authors calibrate approximate posterior distributions in the context of likelihood-free inference methods. Our second contribution is to give an efficient computational implementation of this new approach. We suggest using fast approximate K-Nearest Neighbours (KNN) search algorithms (Arya et al., 1998) in the assignment of weights to observations in the recalibration process. Our third contribution is to demonstrate the good performance of our proposed approach in some real and simulated examples.

There is a large existing literature on recalibration methods for ANNs. For classification problems, ANNs give predictive distributions in the form of a vector of probabilities for a finite number of possible classes for the response. In contrast, for regression applications in which the response is continuous, probabilistic forecasts take the form of a continuous distribution parametrized in some way by the ANN outputs.

Recalibration methods for classification problems have the more extensive literature, and in this context Guo et al. (2017) observed that increased model capacity and lack of regularization are closely related to miscalibration. To alleviate this problem, they proposed a post-processing technique called temperature scaling, derived from Platt scaling (Platt et al., 1999). Temperature scaling involves dividing the network’s logit by a scalar value, , before applying a softmax transformation, which can improve calibration without compromising accuracy. Kumar et al. (2019) highlighted that widely used methods such as Platt scaling and temperature scaling may not be as well calibrated as reported. They introduced the scaling-binning calibrator, which bins the values of a parametric fitted function to reduce variance and promote calibration. Additionally, Mukhoti et al. (2020) observed that an increase in the confidence of a network about incorrectly classified test samples is a key indicator of miscalibration. They suggested using focal loss instead of cross-entropy loss to achieve better calibrated models. More recently, Xiong et al. (2023) argued that existing calibration algorithms commonly neglect the problem of proximity bias, which refers to the tendency of models to exhibit greater overconfidence in low proximity data (i.e. located in low-density regions of the data distribution) compared to high proximity samples. Their new method, coined ProCal, showed excellent results compared to existing alternative approaches. For a detailed overview of the area of classifier calibration, see Silva Filho et al. (2023).

Less attention has been paid to recalibration methods in regression problems where forecasts are in the form of a probability distribution for a continuous outcome. Kuleshov et al. (2018) considered a method for achieving quantile calibration, which is a sample version of probability calibration (Gneiting et al., 2007, Section 3.1), by using isotonic regression to learn a transformation for adjusting the quantiles of model predictive distributions. See also Menéndez et al. (2014). The method of Kuleshov et al. (2018) achieves uniformity of probability integral transform (PIT) values, which have long been used for forecast evaluation (Dawid, 1984). Utpala and Rai (2020) suggest achieving calibration implicitly by including a penalty term in the training loss to encourage uniformity of the PIT values. Building on this approach, Dheur and Taieb (2023) introduce a new regularization objective which uses kernel density estimation (KDE) and an approximation of the indicator function which makes the PIT distribution function differentiable. They also explore links between quantile calibration and conformal prediction.

The adjustment approaches discussed above are global in nature, and make the implicit assumption that the biases of the model remain consistent across the entire covariate space. In contrast, Song et al. (2019) consider the notion of distribution calibration. It requires equality between the forecast distribution for some given input, and the true conditional distribution of the outcome when we consider the input as a random variable and condition on this random input leading to the same forecast distribution as the given input. They propose a method for post-hoc distribution recalibration which involves learning a Beta calibration map (Kull et al., 2017a, b), which varies in the parametrization of the predictive distribution. The calibration map is learnt using a multioutput Gaussian process model and a complex approximate variational inference scheme to estimate multiple parameters, including kernel parameters, variational parameters, and link parameters.

Recently, Kuleshov and Deshpande (2022) proposed a post-hoc recalibration method for regression models which is considered to be at the forefront of current techniques. Their approach involves fitting a quantile function regression model (Si et al., 2021) taking a low-dimensional feature set derived from the predictive distribution as an input. Typically this input is based on the output layer of the original network, which is expanded by adding a feature . The recalibration model then provides a direct estimate of the -th quantile of the distribution of the response, and parameters of the recalibration model are learned using a training criterion which employs a quantile check loss. The key insight is that while fitting the regression model over the parametrization used for the predictive distributions is generally efficient, it is not as straightforward when applied directly to the possibly high-dimensional neural network input. Hence, the original model serves to reduce the original input into a set of summary statistics which are subsequently fed into the calibration model.

The approaches built on the definition of distribution calibration are capable of operating locally. However, the notion of localization is viewed with respect to the ANN’s output space. This is in contrast to a number of recalibration methods that aim to correct the model’s local biases in the actual input space (Prangle et al., 2014; Rodrigues et al., 2018; Tran et al., 2020). We demonstrate that an intermediate layer (or the input layer) may provide a richer space for diagnosing local biases while still operating on a low-dimensional space that avoids the curse of dimensionality.

This document is organized as follows. In Section 2 we give further background about existing definitions of calibration and recalibration methods based on them. Section 3 then presents our new recalibration method. In Sections 4.1 and 4.2, we apply the proposed method to a non-linear Gaussian model and a Gamma model, respectively, and discuss its impact on performance. In Section 4.3, we run a simulation study to evaluate how the proposed method fares in a variety of scenarios, including different recalibration configurations and network models. In Section 4.4 we test our method with a real data set example. Lastly, we summarise the results in Section 5.

2 Background

We are interested in estimating the conditional distribution of a continuous target random variable given an input , , from a training set consisting of independent identically distributed (i.i.d.) samples from the joint distribution of . A probabilistic ANN defines a function that maps an input vector to a predictive cumulative distribution within the space of probability distributions over . This study specifically focuses on this setting. It will be assumed that is continuous and strictly increasing for each , and we write for its inverse. Where convenient we will write and for and respectively. We now give some background on the notions of quantile and distribution calibration.

Quantile calibration: Kuleshov et al. (2018) suggest the following definition of calibration for which they introduced the term quantile calibration. Given as above, a neural network is said to be quantile-calibrated if

| (1) |

as , where denotes the indicator function which equals 1 if is true and 0 otherwise. (Gneiting et al., 2007, Theorem 2) consider this as a sample version of ‘probability calibration’, and establish an equivalence between quantile and probability calibration for ‘*-mixing’ sequences of random variables (Blum et al., 1963), where the convergence in (1) is almost convergence. Probability calibration requries that converges to for every almost surely.

Quantile calibration guarantees that observations fall below the -quantile of the forecast distributions with relative frequency . Sections 4.1 and 4.2 demonstrate that this notion of calibration is too weak for some purposes; for the models considered there, although approximately 95% of the test samples fall within 95% prediction intervals after calibration, this calibration does not hold after selecting data according to features of the predictive distribution or the input.

Under the assumption of a continuous and strictly increasing predictive distribution function, quantile calibration is equivalent to requiring uniformity of the limiting empirical distribution of probability integral transform (PIT) values . Empirical comparison of the PIT values to a uniform distribution has been widely used for forecast evaluation (Dawid, 1984). If forecasts are ideal in the sense that the forecast distribution always coincides with the distribution of the observations, then for all . Formal tests for uniformity of the PIT values and descriptive measures of their departure from uniformity based on the Wasserstein distance and the Cramér-von Mises distance have been suggested (Dheur and Taieb, 2023).

Kuleshov et al. (2018) proposed learning a distribution function that estimates the CDF of the PITs, , so that forecasts are nearly calibrated; if , then uniformity of the PIT values follows, since

The authors suggest approximating by fitting an isotonic regression over a recalibration set

where is the PIT value computed over the sample , and

denotes an empirical estimate of . The recalibration data may not correspond to the training data .

Distribution calibration: A more strict definition of calibration is introduced in Song et al. (2019). Suppose that the random vector is defined on a probability space . Let and denote the distribution function of the random variable as . Then the collection of distributions are distribution calibrated if

| (2) |

This definition requires that when considering the input as a random variable, when conditioning on obtaining the same predictions as the fixed input , the distribution of the outcome is equal to the forecast distribution for . This gives a notion of calibration that is local in the output space. Distribution calibration implies quantile calibration but the reverse implication does not hold. If is a parametric distribution indexed by , which we write as , then often the values of are given by the components of the neural network’s output layer, and the condition in the definition of reduces to .

3 Methods

Inspired by this definition, we introduce a novel algorithm that attempts to achieve uniformity of the PIT values locally. Algorithm 1 introduces our new post-processing method for recalibrating the predictive distributions of a probabilistic ANN regression model. We assume an -layers ANN has been previously fitted, with the predictive distribution defined according to the network’s loss function. For example, if the Mean Squared Error (MSE) was adopted as the loss function, the neural network provides Maximum Likelihood Estimates (MLE) for the mean of a conditional homoscedastic Gaussian distribution. Other approaches, including the non-parametric use of dropout layers for estimating the predictive distributions, are discussed in Section 4.2.

-

•

Recalibration set, , and new set, .

-

•

A neural network and its associated predictive distribution, .

-

•

A positive integer defining the network’s layer where the samples are to be compared.

-

•

Neural network’s outputs of the -th layer on the recalibration set, .

-

•

A smoothing kernel with scale parameter , which may be defined indirectly from a positive integer that represents the number of observations to be used for recalibration.

Our recalibration method is composed of two stages: calculating the predictive cumulative probability, , for each sample in the recalibration set, , and then performing the recalibration for each observation in the new set, (a collection of samples for which the inputs are known and for which we want to predict the respective responses). Throughout this work, we use the validation set (used for tuning the hyperparameters of the neural network) as the recalibration set.

For each new input , we compute , where denotes the network’s mapping to the -th layer. Here, is ideally a nearly sufficient low-dimensional representation (summary statistic) of the raw data implicitly learned by the network during training. We then use the approximate KNN search method (Chen et al., 2021) to identify the indices, , corresponding to the observations in the recalibration set for which the distances are within the -smallest values. Lastly, for each , we set and assign it a weight .

Larger weights are therefore given to samples for which, according to the metric , and are similar. This reflects the principle that closer observations are usually more informative of the model’s predictive capabilities (at that particular location of the space induced by the network’s -layer). The number of observations considered in the recalibration, , plays a critical role in the recalibration performance – the smaller it is, the better the local bias is captured, at the cost of an increased approximation error associated with the smaller number of weighted samples from the recalibrated distribution. If one wishes to recalibrate a model globally, without considering local biases, it can be achieved by setting and choosing a constant weighting function in Step 10 of Algorithm 1.

The task of identifying the nearest neighbours of in the recalibration set (Step 8, Algorithm 1) is very important for algorithm efficiency. Due to the curse of dimensionality, it becomes increasingly difficult to find an efficient solution to this problem as the sample size and dimensionality of increases. Given a set of points in , a -dimensional space, and a single query point, a naive approach to the problem of finding the closest point in to (through linear search) takes time. It is possible to use a GPU for calculating the distances to speed up the process. Trying to find the -closest points of to query set is much more costly. An efficient alternative for large data sets is approximate KNN search methods. Arya et al. (1998), shows that, given , the -approximate nearest neighbors of can be computed in time. Recent work on identifying approximate nearest neighbors Chen et al. (2021) can compute a solution with billion-scale data sets twice as fast as previous state-of-the-art search algorithms. We explore the influence of the approximation parameter in recalibration, along with other parameters, in Section 4.3.

Let be a vector of cumulative probabilities, as defined in Step 4. The -th recalibrated predicted value, , can then be obtained by taking the weighted average of the recalibrated predictive distribution’s samples,

| (3) |

where (see Step 10). Interval predictions and estimates of other features of the recalibrated predictive distributions (e.g. variance) can be similarly calculated.

A major advantage of the proposed method is that it can be used in any layer of a neural network. Let denote the index of the network layers; with and indicating that the recalibration is performed in the input and output layers, respectively. As previously discussed, current state-of-the-art methods, such as Song et al. (2019) and Kuleshov and Deshpande (2022), implicitly recalibrate on . In Section 4.3 we investigate the effect of calibrating on different layers.

If performed on the input space () and is high-dimensional, recalibration can be statistically and computationally challenging. At the other end of the spectrum, recalibrating on the output layer does not guarantee that the selected observations are, in fact, close, since only features of the predictive distribution are taken into account: two samples far apart in the input space can lead to similar predictions. Recalibrating on an intermediate layer may, therefore, provide two related benefits. First, the dimensionality can be easily controlled when setting the ANN’s architecture. Second, the distances are evaluated over a convenient representation of the original data.

4 Illustrations

4.1 Heteroscedastic Gaussian Model

Consider samples from the following Gaussian heteroscedastic quadratic model

| (4) |

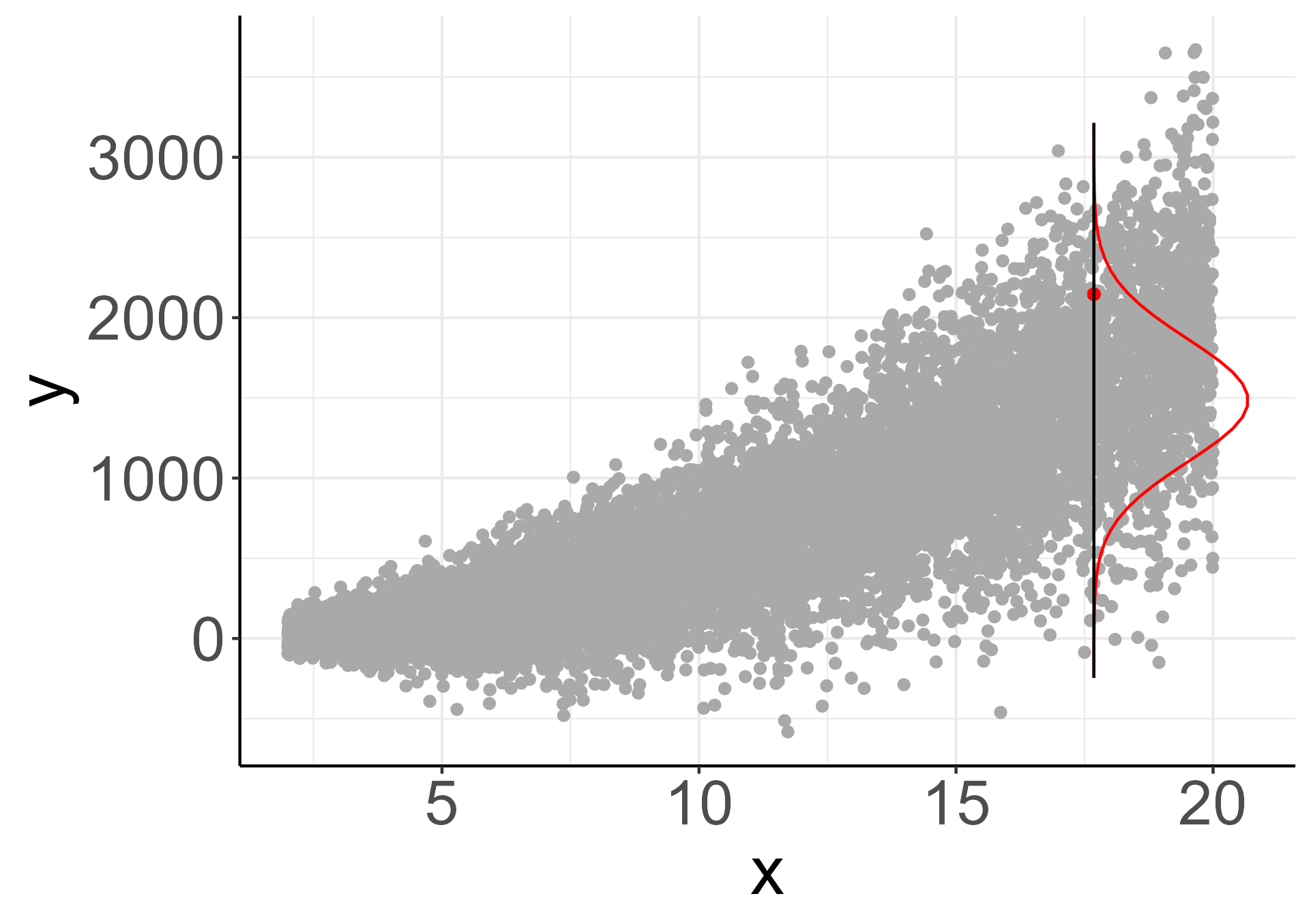

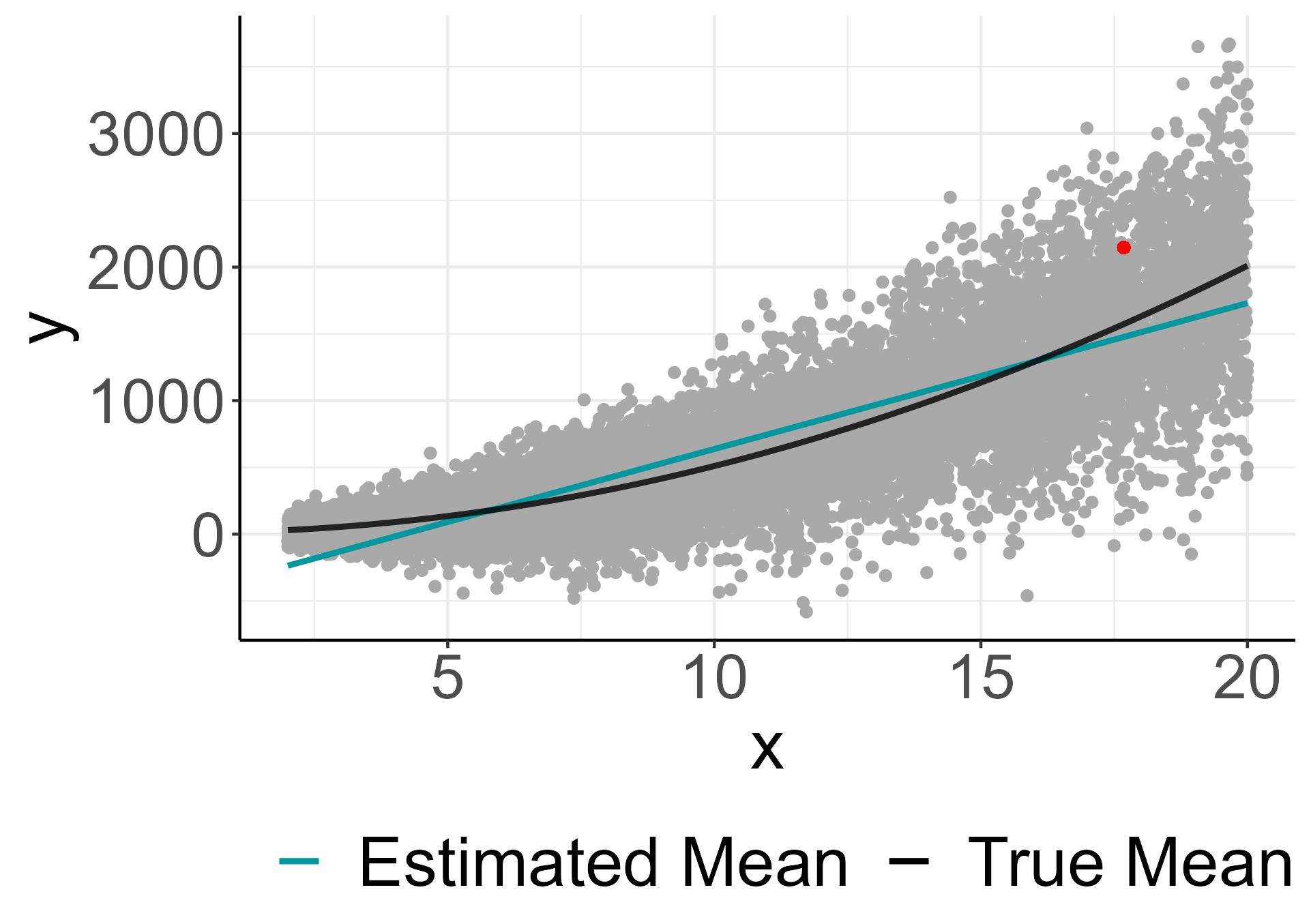

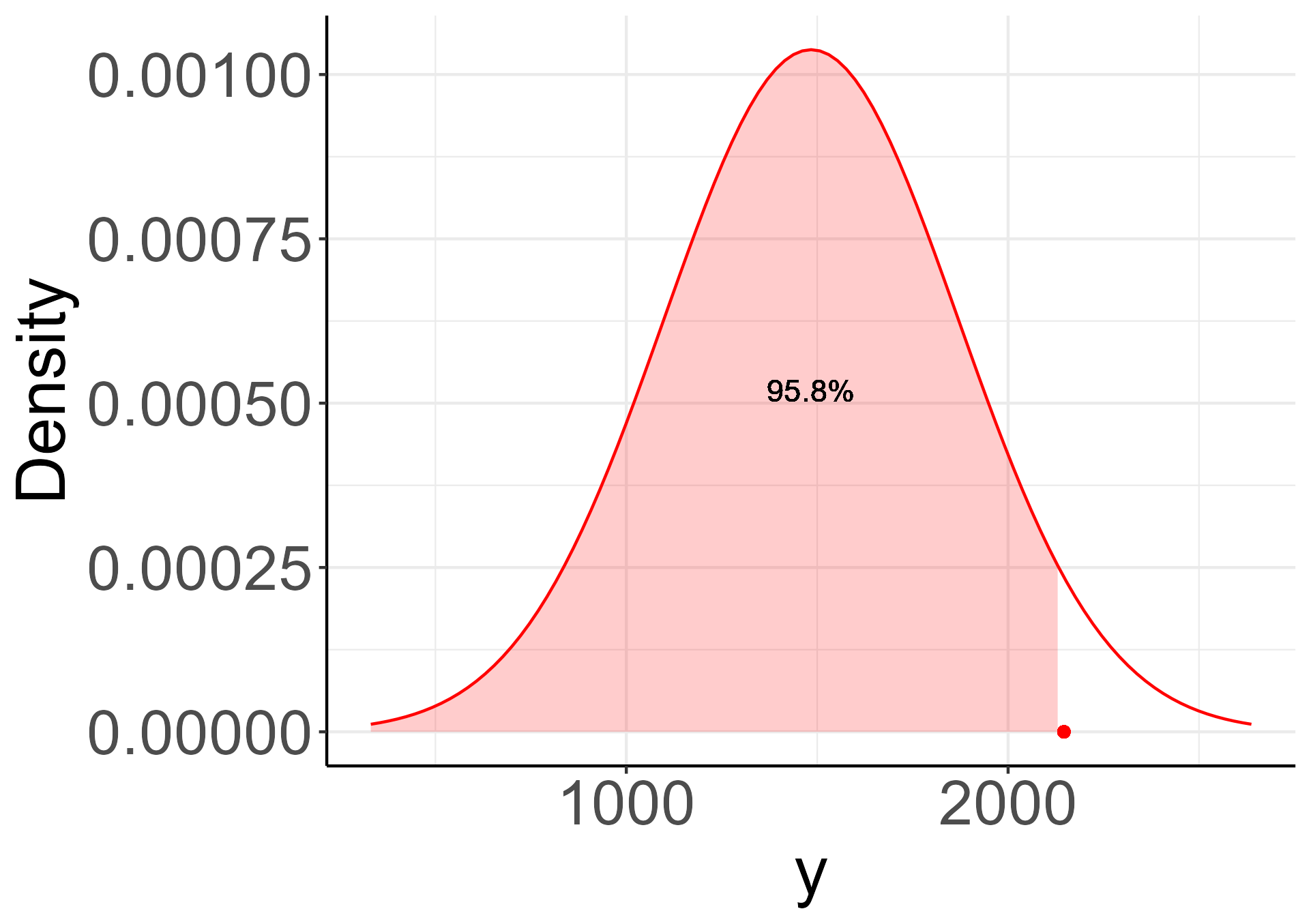

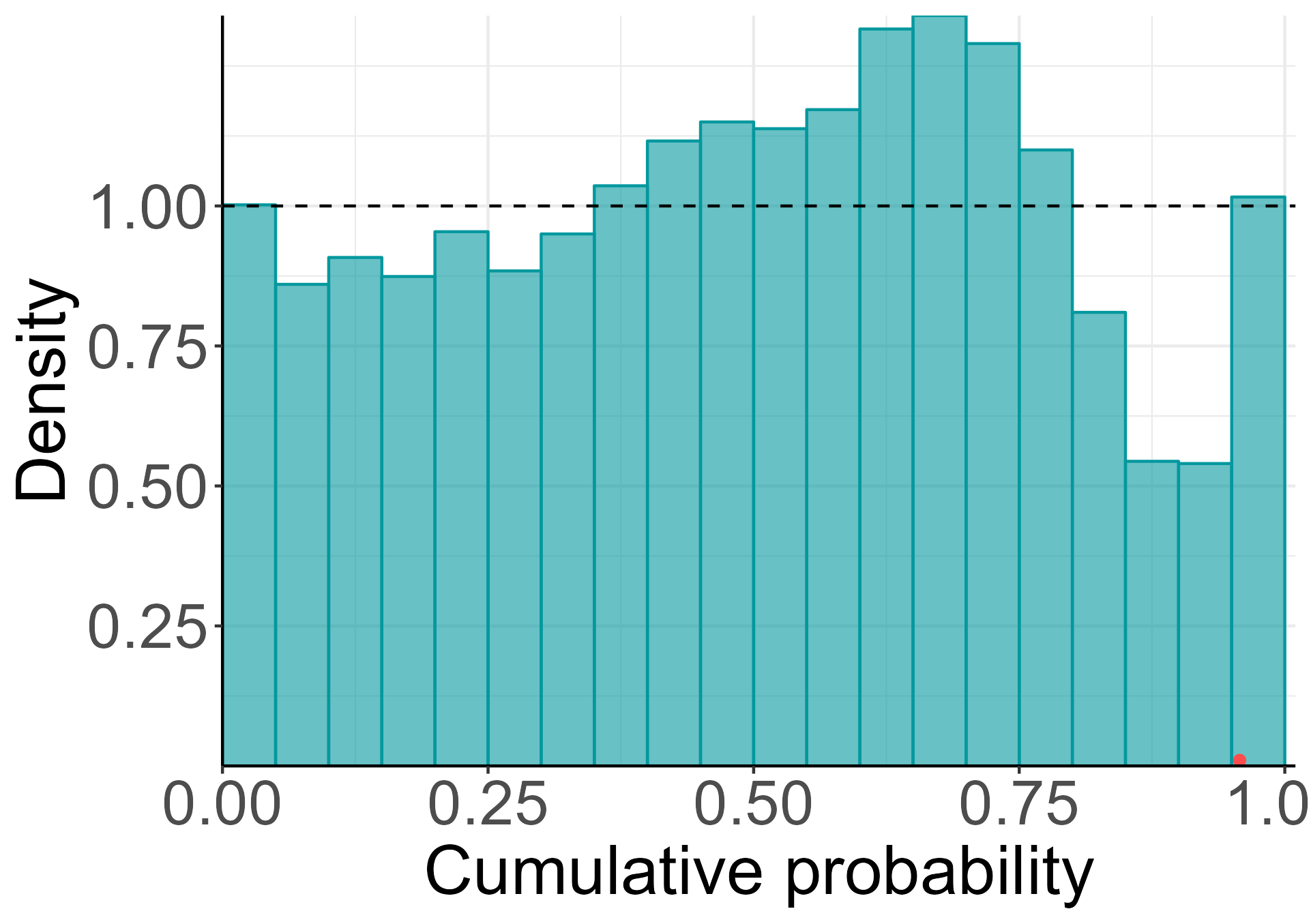

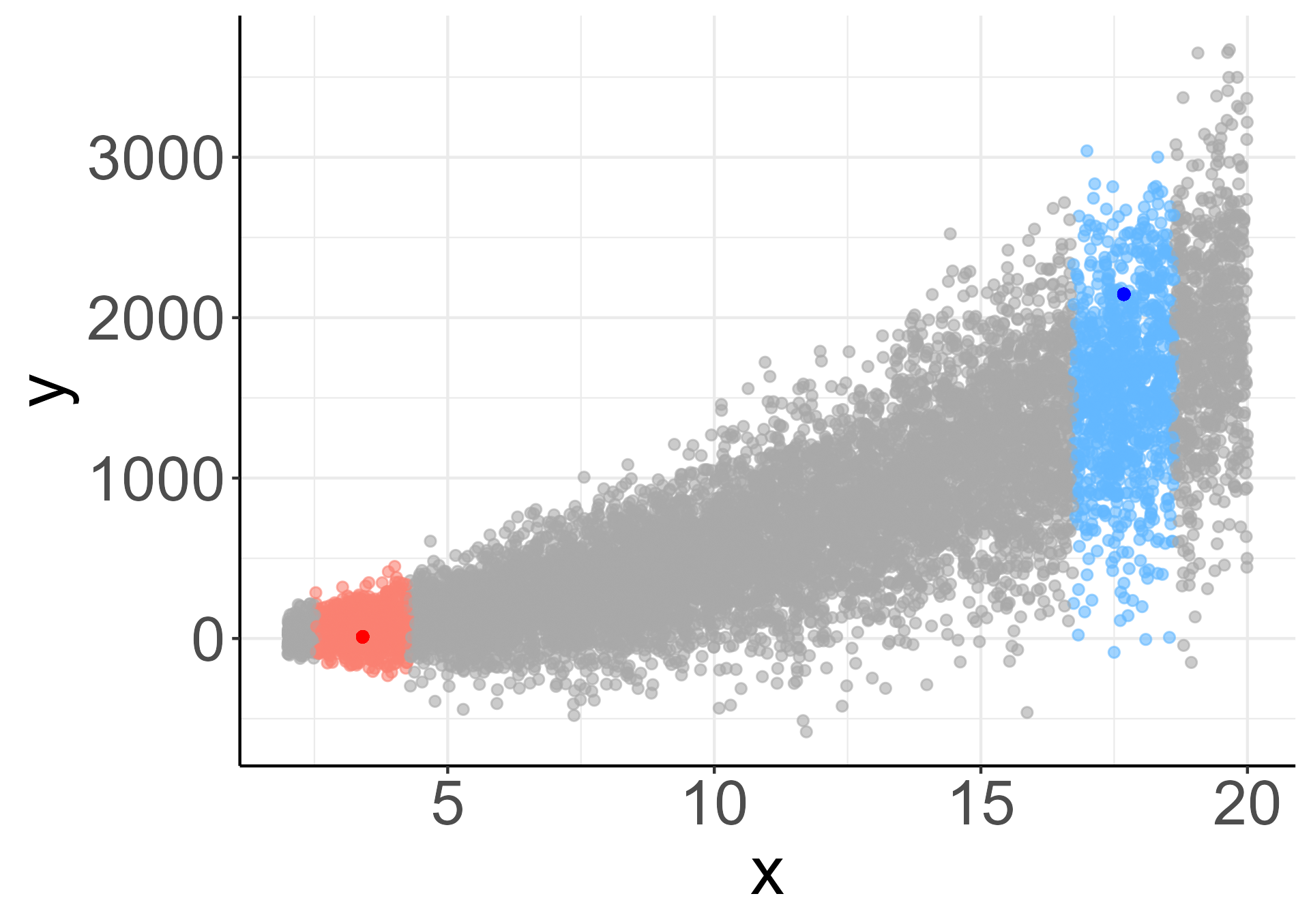

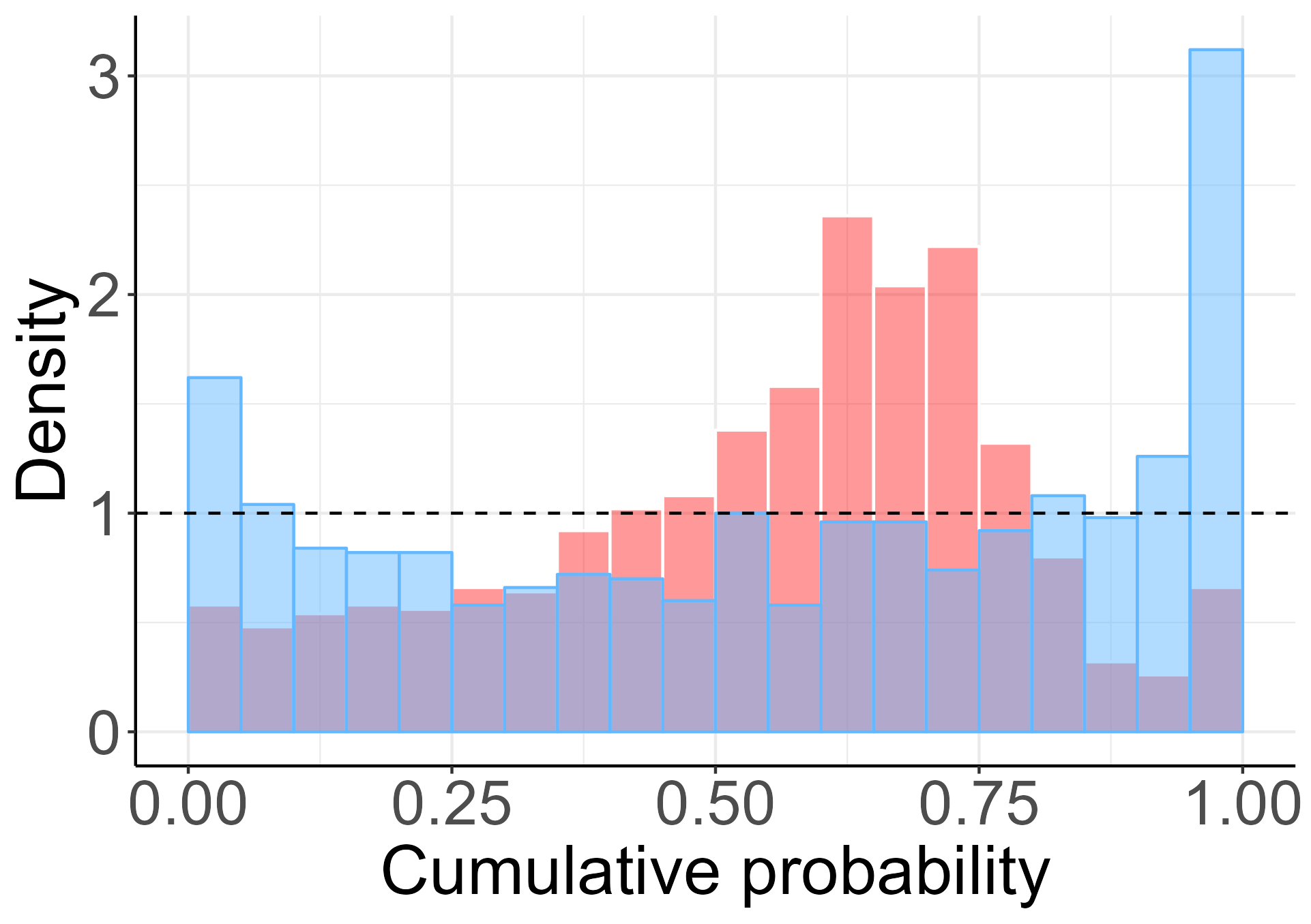

where (Figure 1(a)) and . In this study, the samples are split into training (), validation () and test sets (). The validation set is also adopted as the recalibration set. We fit the misspecified linear homoscedastic model over the training data. Figure 1(b) shows the fitted linear regression line in contrast with the actual mean curve. The red curve shows the plug-in normal predictive distribution for the observation which has mean and standard deviation and , respectively. Figure 1(c) shows that, for a random variable with distribution , the highlighted observation has an associated cumulative probability of . The non-uniform cumulative probability histogram of all observations in Figure 1(d) hints at the global bias of the predictions of this model.

Figure 1 shows the poor quality of the fit of the linear model due to its misspecification. Frosini’s test rejected the null hypothesis of uniformly distributed for all with a significance level. In the histogram of global cumulative probability estimates (Figure 1(d)), it is possible to see a combination of bias patterns indicating both model’s variance underestimation and overestimation in distinct regions of the covariate space (Figures 1(e) and 1(f)).

We generate samples from the recalibrated distribution using Algorithm 1, with (that is, we recalibrate in the input space), using Euclidean distance for , and the Epanechnikov smoothing kernel with scale parameter chosen so that .

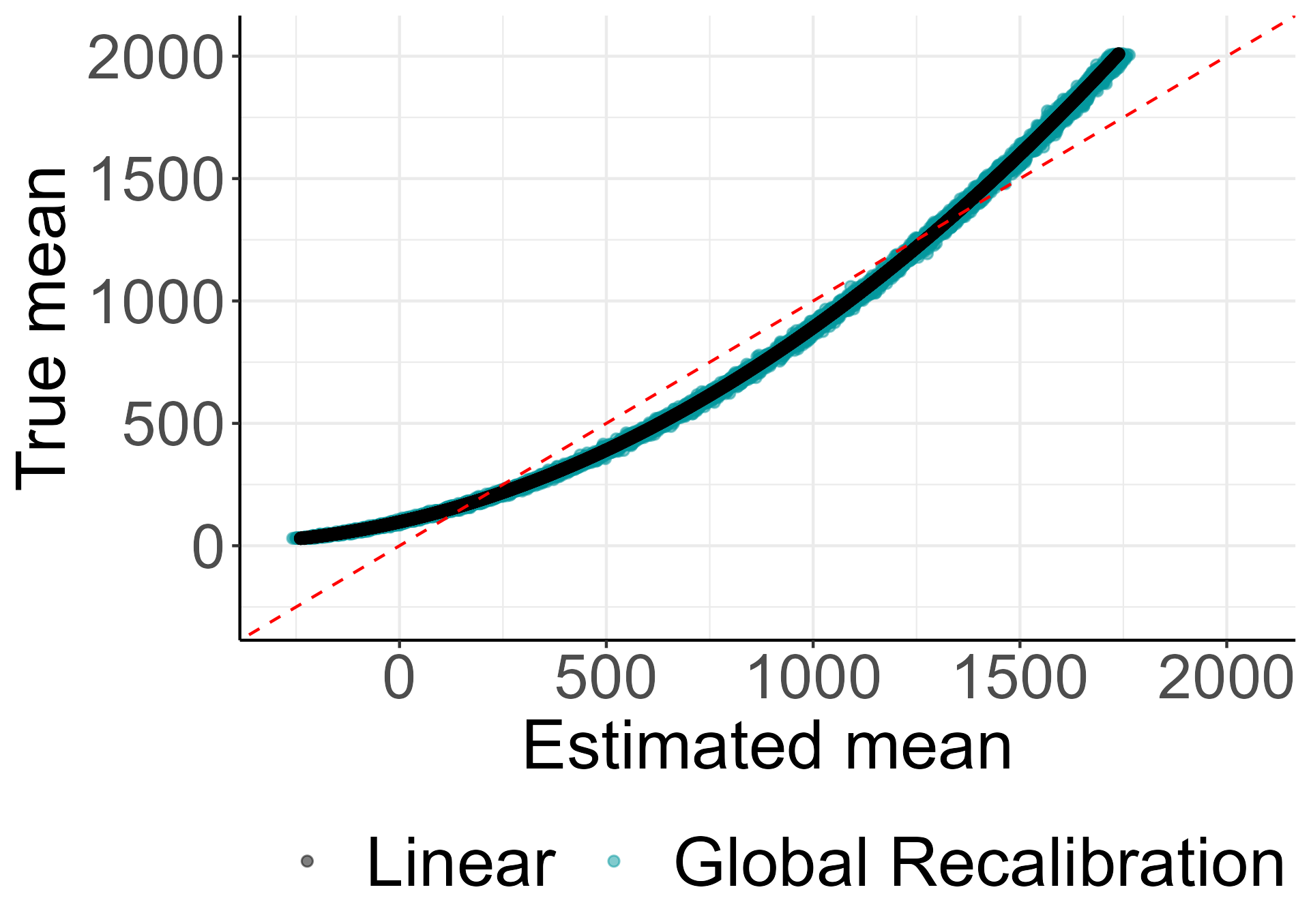

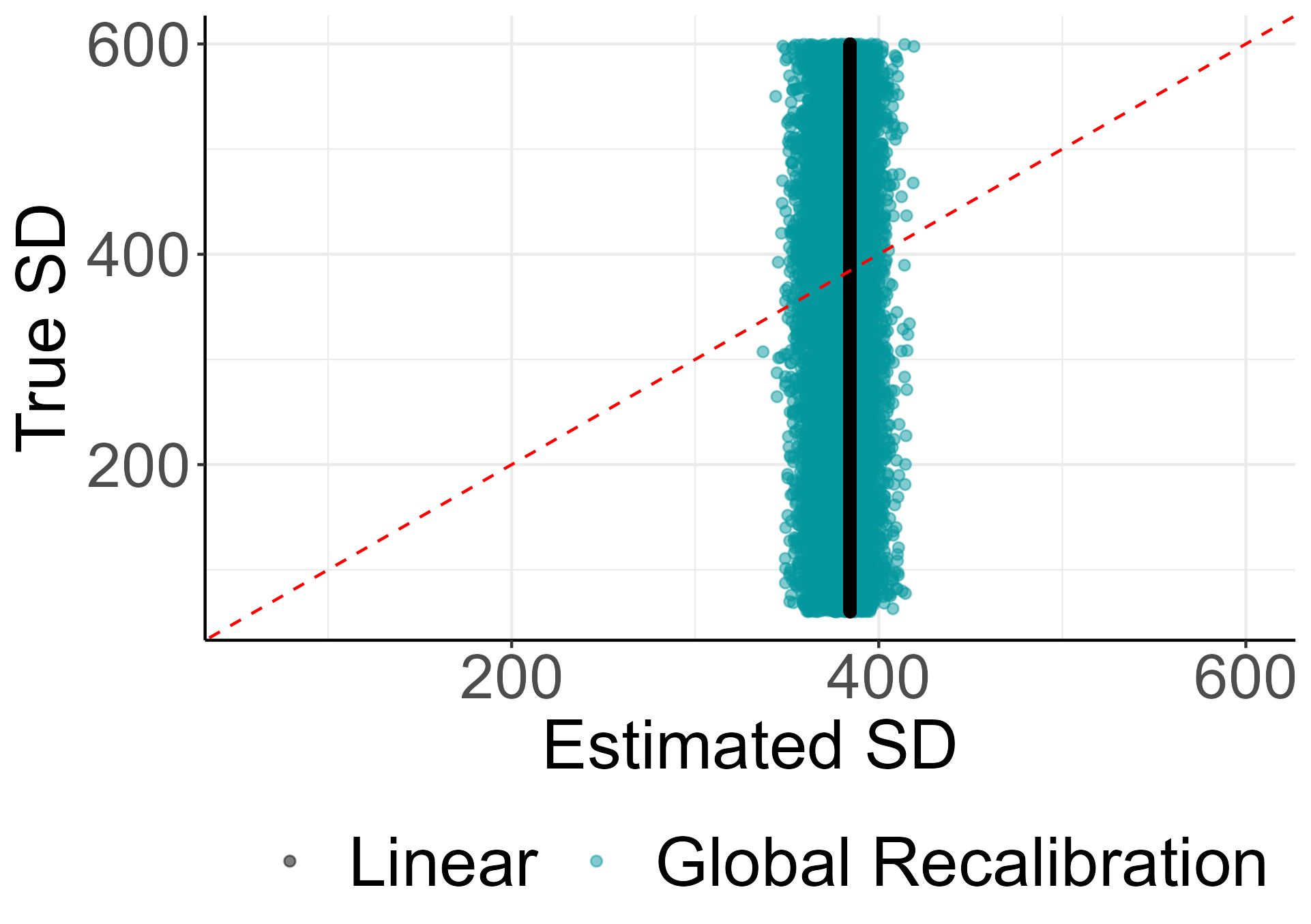

Figure 2 compares the effect of global and local recalibrations, in terms of how well each recalibrated model estimates the true means and standard deviations. Overall, the global recalibration offered no significant improvement over the linear model, as seen in Figures 2(a) and 2(b). However, the locally-recalibrated model improved both the mean (Figure 2(c)) and the variance estimations (Figure 2(d)).

| Model | MSE | KL Divergence | Coverage (%) | sMIS |

|---|---|---|---|---|

| Linear | 14546.25 | 0.8455 | 93.78 | 2.7475 |

| Globally Recalibrated Linear | 14763.29 | 0.7353 | 94.65 | 2.7391 |

| Locally Recalibrated Linear | 303.93 | 0.1097 | 94.96 | 2.0947 |

Table 1 shows performance indicators for all the models considered. The observed coverage represents the percentage of confidence intervals that captured the respective observed value in the test data set. The standard Mean Interval Score (sMIS) (Gneiting and Raftery, 2007) is given by

| (5) |

where , and are the upper and lower interval quantiles, standardized by the validation set mean absolute values. sMIS directly compares prediction intervals by penalizing observations missed and rewarding narrower intervals. It can be seen that local recalibration performed best in all measures compared to the other models.

4.2 Non-Linear Gamma Model

Here we utilize synthetic data to estimate the Rosenbrock function, which is widely used as a test function for optimization algorithms. For fixed constants and , the function is given by

We take the Rosenbrock function with and as the conditional mean () of a Gamma distributed random variable with shape parameter and scale parameter given by . Assuming that and , we generate i.i.d. samples of from this model. The data is split into training (), validation () and test () data sets. The validation set is also adopted as the recalibration set.

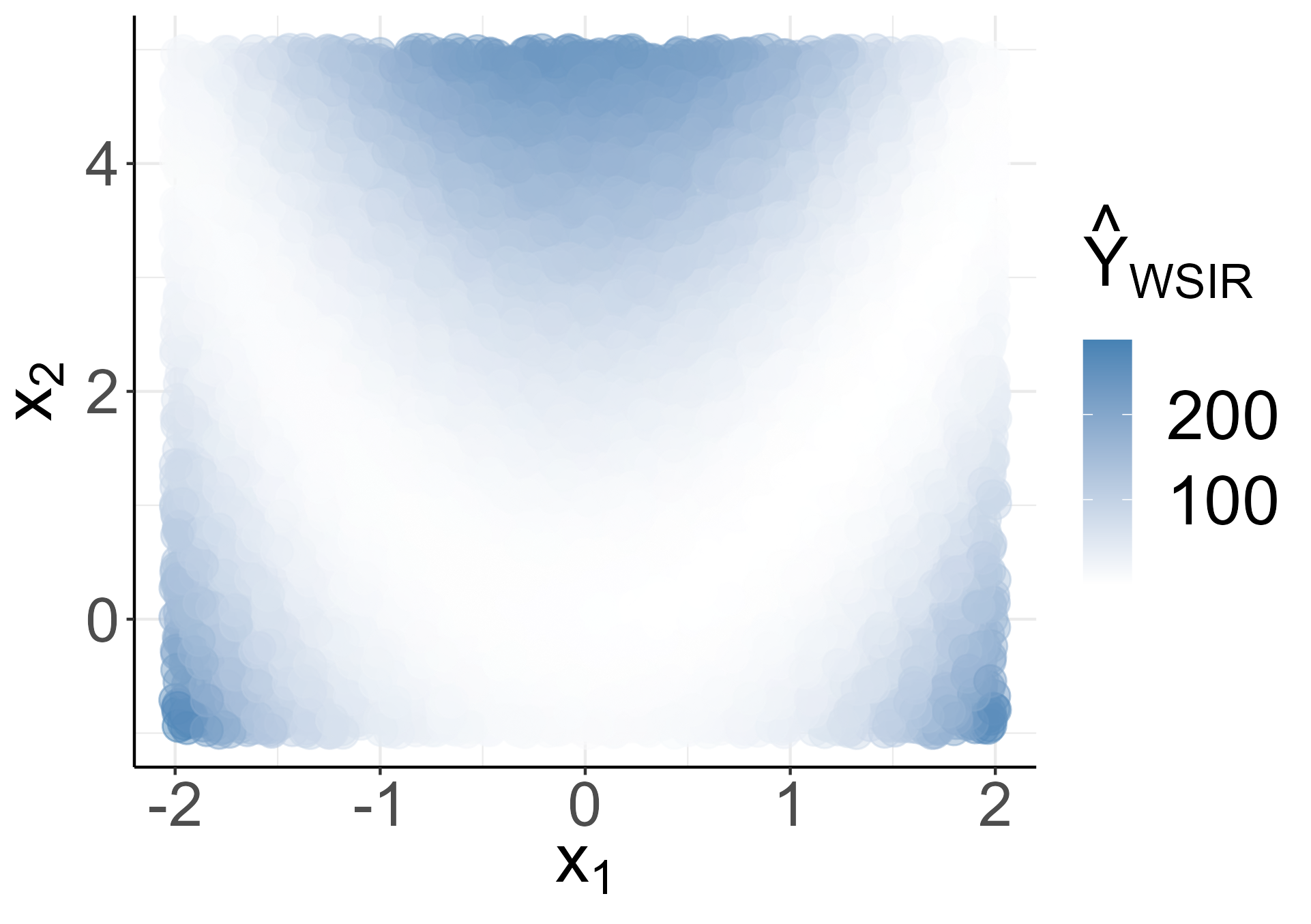

Figure 3(a) shows the generated test data and the mean surface in three dimensions, where it can be seen that the farther the observations are from the valley, the greater the variability around the mean. The variability of the test data can also be seen in Figure 3(b).

To estimate the mean function from the data, we fit a neural network model to , comprising four hidden dense layers (, , , neurons) with ReLU activation function and an output linear layer with a single neuron. We also added batch normalization layers and dropout layers with probability between every hidden layer. The network was trained for epochs with a learning rate of , using an ADAM optimizer, MSE loss function and batches of size .

The use of dropout layers opens up two possibilities to estimate the network’s uncertainty. The first approach consists of using the weight scaling inference rule (WSIR) to make a single prediction for every data point in the test set, assuming normality in the logarithmic scale of . The second approach consists of using the dropout’s randomly generated masks to obtain a sample of the network’s predictions for every data point in the test set, following the methodology proposed by Gal and Ghahramani (2016) (Monte Carlo Dropout), without parametric assumptions on the predictive distribution.

The logarithmic transformation takes the response variable from the interval to . Since the weight scaling inference rule averages the output of all dropout masks, in the first approach we can assume the network outputs the mean of a Normal distribution with variance equal to the validation set MSE. For every prediction, we generated a sample of size from the predictive distribution on the log-scale, then applied the exponential transformation, , to take the samples back to the interval . By doing so, we obtain a Monte Carlo sample from the predictive distribution for every observation in the test set on its original scale.

The Monte Carlo Dropout (MC Dropout) approach uses the randomness intrinsic to the dropout technique to get samples of the network’s predictions for each data point. At every iteration, each dropout layer generates a random mask that turns off some of the neurons according to the chosen dropout probability. We activated the dropout layers during the inference stage and generated samples of size for each observation in the test set (on the original scale). In both methods, the point estimates are the mean taken from the samples generated from the predictive distributions.

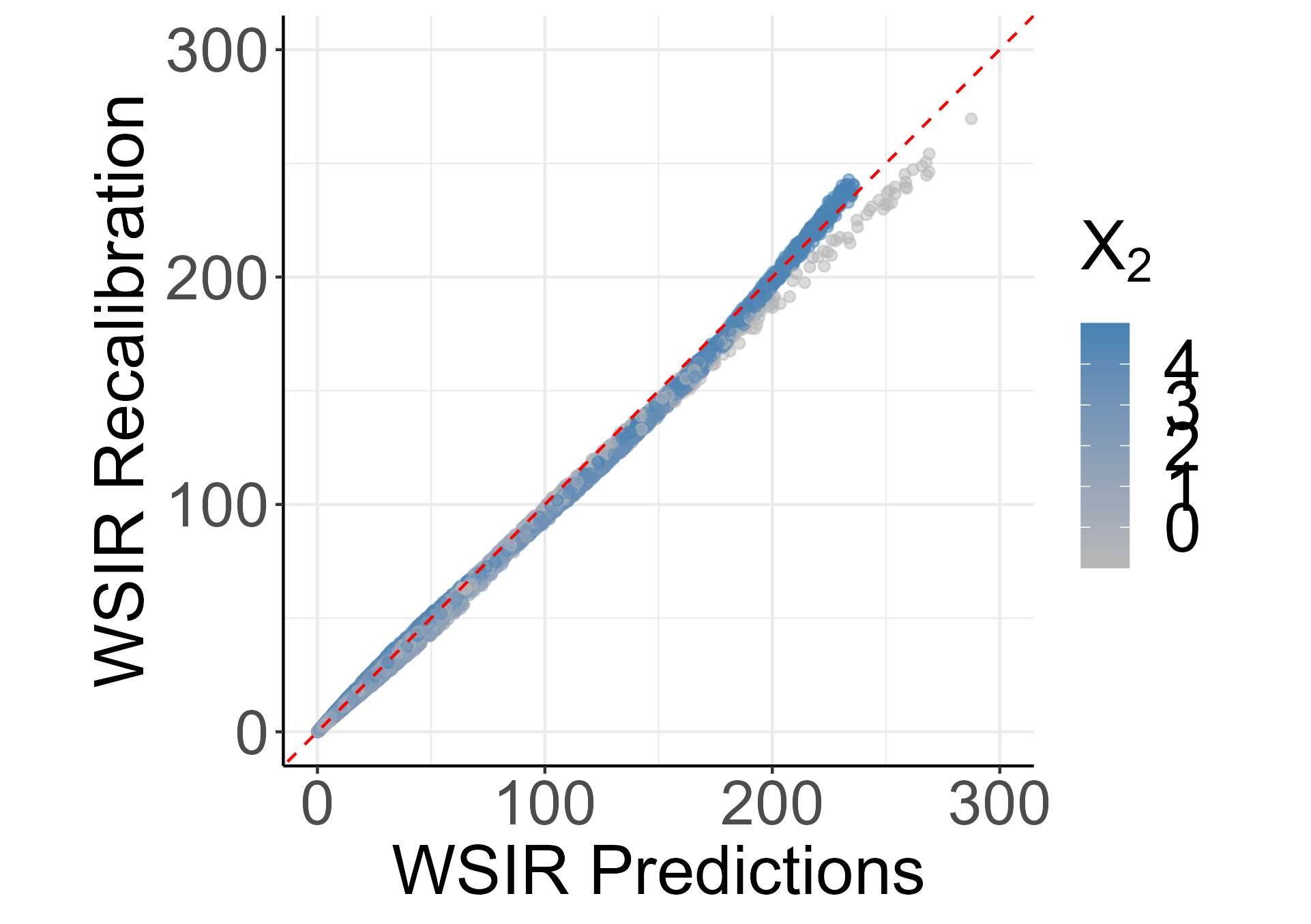

Since we have very high dimensionality in the network’s layers weight space, we recalibrated both methods locating the nearest neighborhood of each observation in the input space. In this analysis, if we fix the number () of neighbors, the observations on the edge of the mean function’s region will have a much greater neighborhood area than the ones in the center. To avoid that, for each observation in the test set, we selected the closest observations in the validation set based on a fixed maximum distance (equal to ). Due to the non-parametric nature of the samples generated by the MC Dropout method, to directly compare both method’s estimates, we calculate the cumulative probabilities empirically from the Monte Carlo samples obtained from each method and generated unweighted samples of the recalibrated predictive distributions according to the weights defined by the Epanechnikov kernel.

Figure 3(c) shows WSIR predictions in the covariate space. One of the major effects of recalibration on both ANN models was decreased prediction values for lower values of , previously overestimated, as illustrated with the WSIR method in 3(d).

The performance of all methods was measured from samples obtained from their estimated predictive distributions and compared against samples taken from the true model’s distribution (Table 2). While the predictions taken from the WSIR presented smaller MSE value than the ones taken from the MC Dropout, the recalibrated methods resulted in the predictions closest to the true samples by a large margin, indicating recalibrated predictions were much closer to the original test data on average. In regards to prediction interval estimation, the closest to nominal coverage and largest interval score were attained by the MC Dropout method, with the latter suggesting this method generated too wide prediction intervals. The recalibrated methods had coverage and score metrics very close to those of the true model.

| Model | MSE | Coverage (%) | sMIS |

|---|---|---|---|

| WSIR ANN | 71.25 | 95.5 | 0.569 |

| MC Dropout ANN | 75.06 | 99.0 | 0.874 |

| Recalibrated WSIR ANN | 60.52 | 94.3 | 0.500 |

| Recalibrated MC Dropout | 60.44 | 94.7 | 0.499 |

| True model | 59.64 | 94.6 | 0.477 |

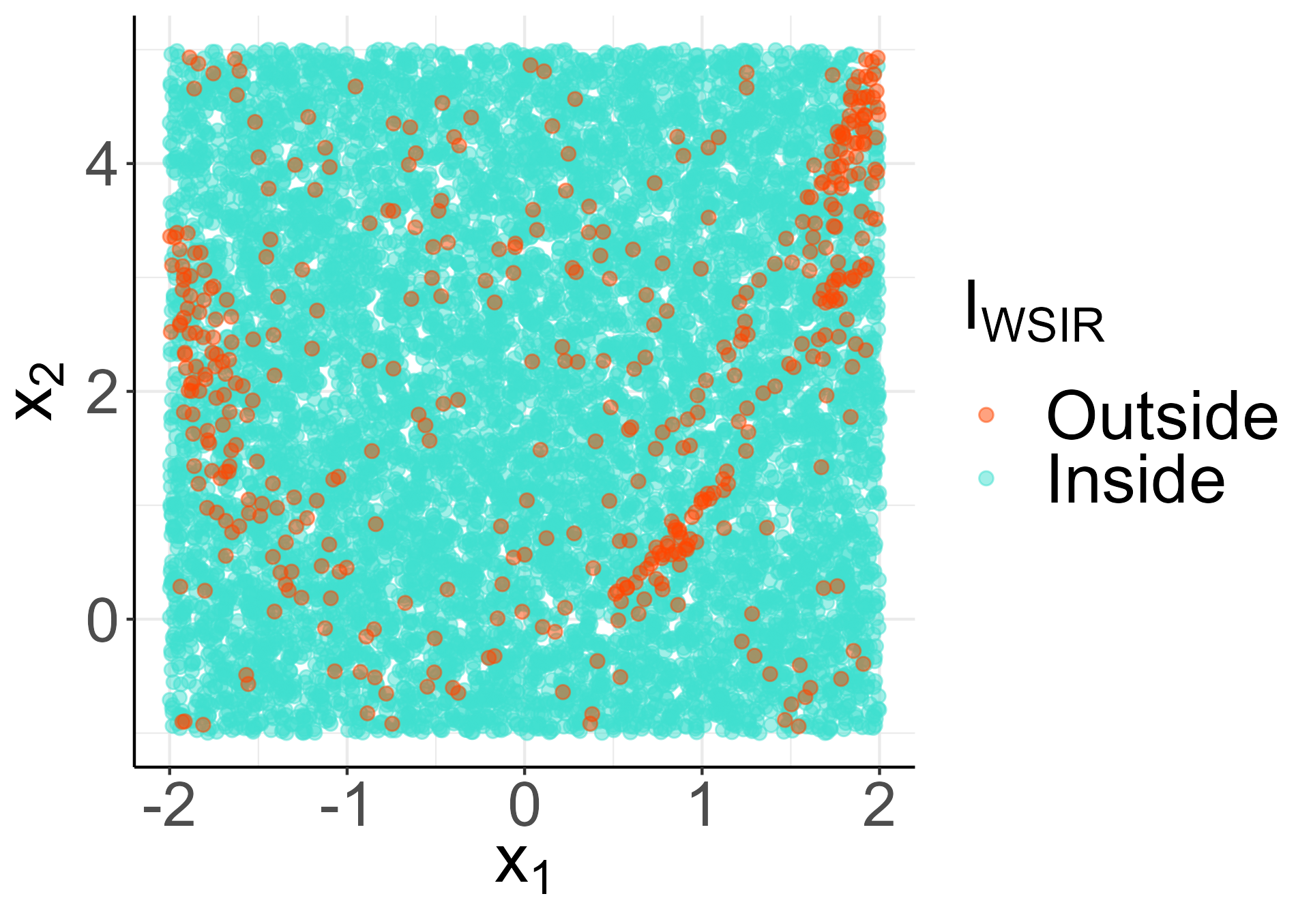

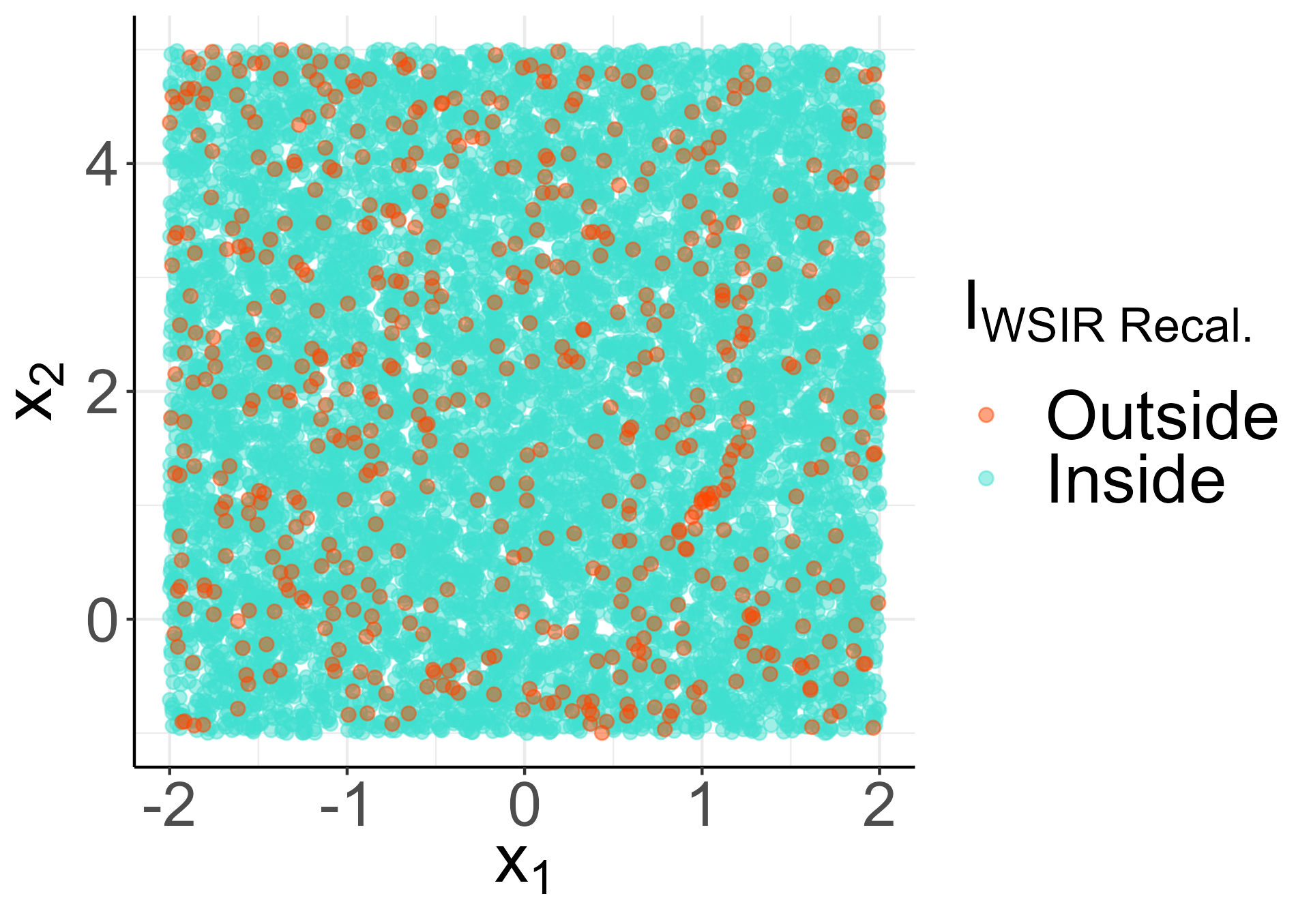

The coverage of the WSIR methods (with and without recalibration) is shown in Figures 3(e) and 3(f), where light red points represent observations not captured by the prediction intervals. It can be seen that ANN predictions, despite getting close to the nominal coverage level presented a very clear pattern, missing observations in specific areas. On the other hand, recalibration appears to have largely reduced local biases. That is, after the recalibration, the coverage showed a much more evenly spread pattern throughout the covariate space, an indication that these models are well-calibrated.

4.3 Simulation Study

In this analysis, we run a simulation study to investigate and quantify the effect of our recalibration procedure on neural network models under various conditions. We revisit the analysis in Tran et al. (2020) and consider the highly nonlinear model given by

| (6) |

where . We generate the variables , from which are non-informative to the model, from a multivariate normal distribution with mean vector , , and covariance matrix , . Data from this process are simulated in sets of sizes , , and . Then, in each scenario, we randomly split the data into a training set, a validation set and a test set using , and , respectively. We propose to fit and recalibrate two neural network models as well as compare recalibration performance with a K-Nearest Neighbor (KNN) regression model, due to methodological similarities, and two well-known post-hoc recalibration methods, isotonic regression recalibration (Kuleshov et al., 2018) and density estimation recalibration (Kuleshov and Deshpande, 2022). The simulation study is run multiple times, each with a different seed.

Because this section compares the models’ performances for each configuration under study, all recalibration models and the KNN regression model are fit with the validation set and evaluated with the test set, it not being necessary to optimize KNN regression parameter values.

Apart from the number of neurons, the two neural networks considered are identical in architecture, both being composed of a neurons input layer, followed by four hidden layers with ReLU activation function, then a linear output layer with a single neuron. The "small" network’s hidden layers are all composed of neurons, while the "big" network’s first three hidden layers have neurons and its last hidden layer has neurons. The neural networks are trained with the Adam optimizer and mean squared error loss function with the early stop callback. Due to computational and time constraints, both neural network model’s learning rates were optimized in advance for every scenario considered in the simulation, with values ranging from to .

The neural network models are recalibrated assuming normally distributed predictive distributions and considering Epanechnikov’s kernel function to weight the recalibrated samples. To evaluate the effects of recalibration, both networks are recalibrated on the input layer, the fourth layer, the fifth layer and the output layer.

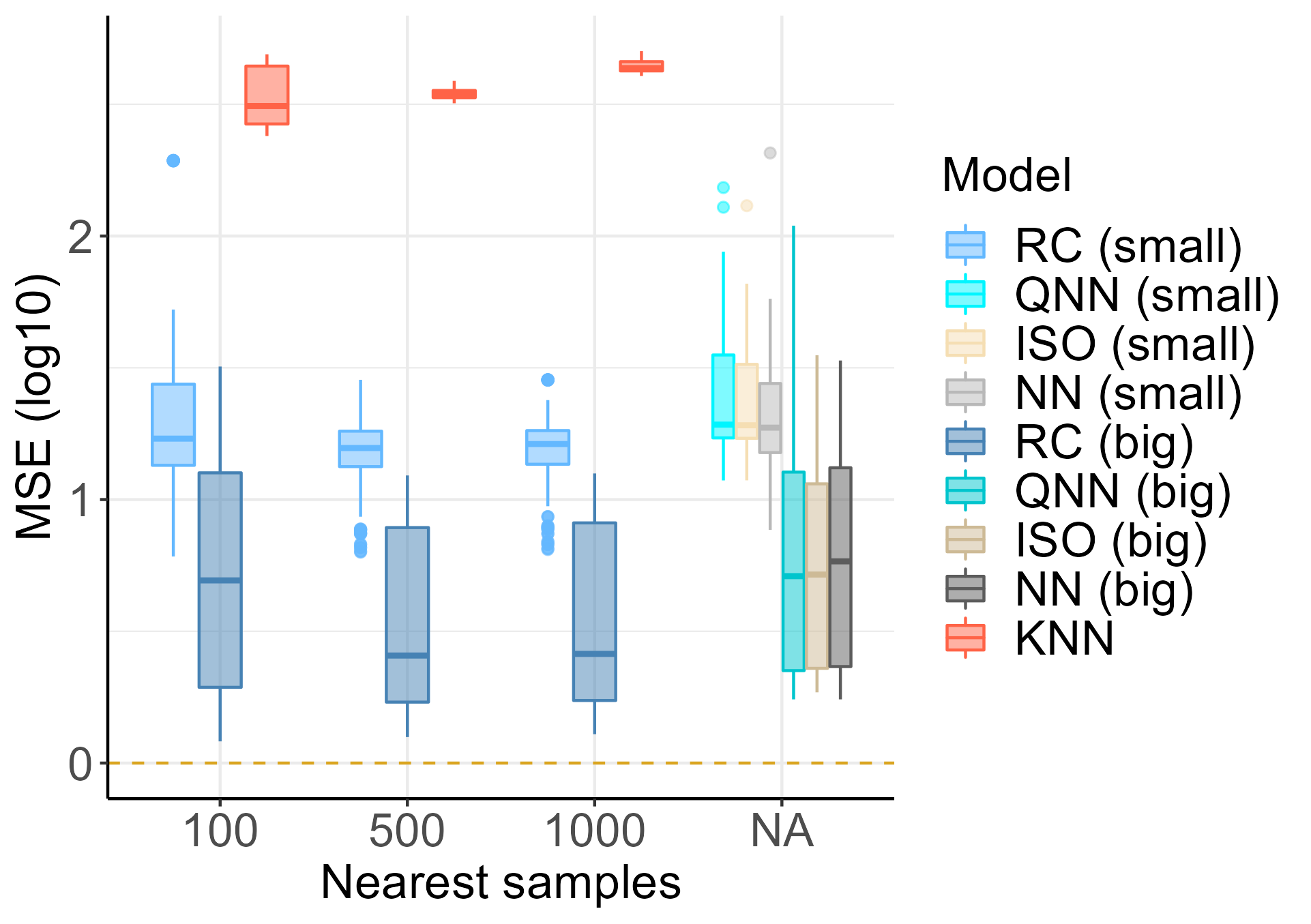

The networks are recalibrated with the , and nearest neighbors. The nearest neighbor search is conducted with three degrees of approximation: (exact search), and , where is the KNN search approximation parameter.

For the density estimation models, we replicate the same quantile neural network architecture in the experiments described by Kuleshov and Deshpande (2022). The models are trained with of the original validation set and validated with the last . Predictions and metrics are taken from the test set, as with the other models used in this simulation.

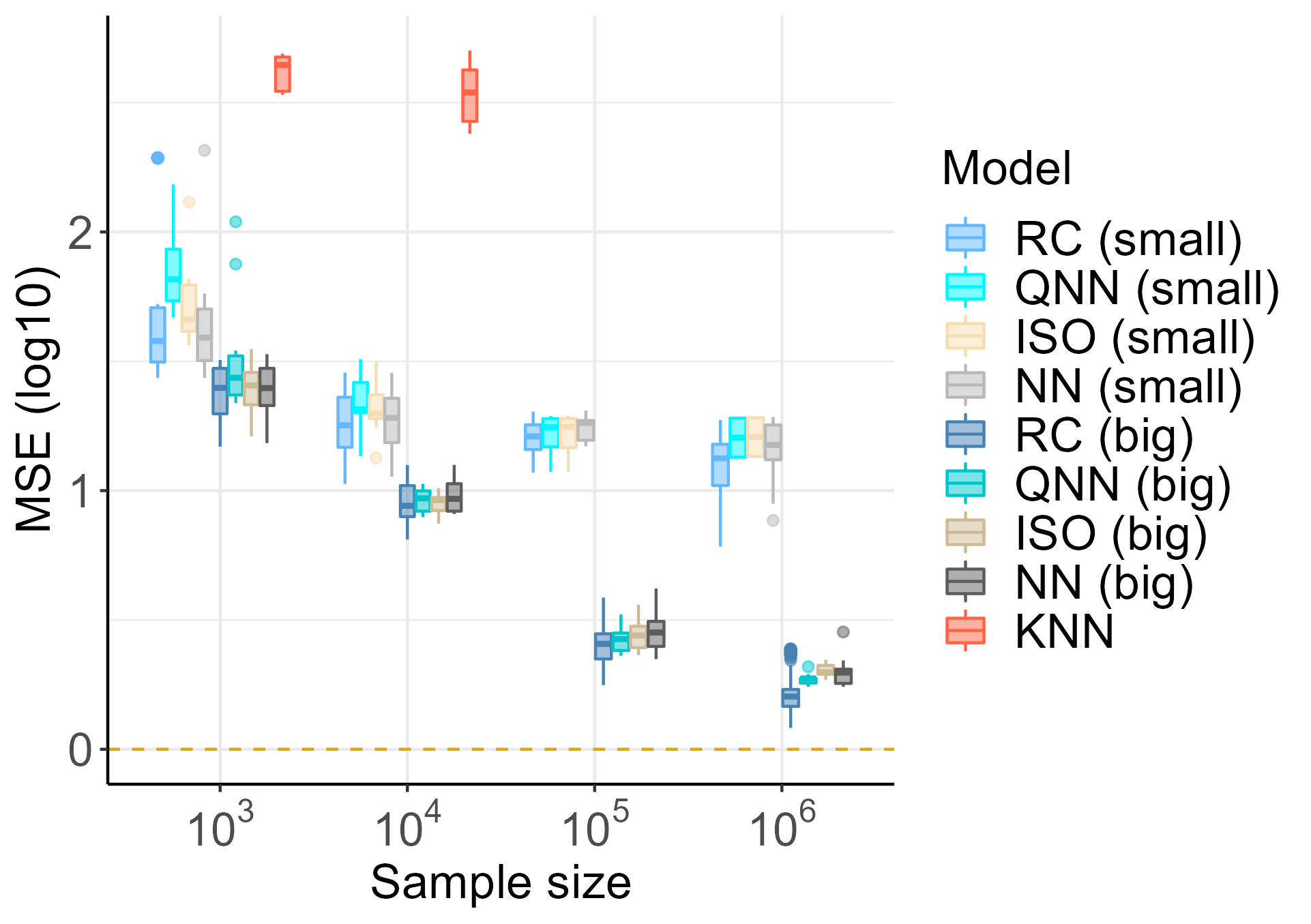

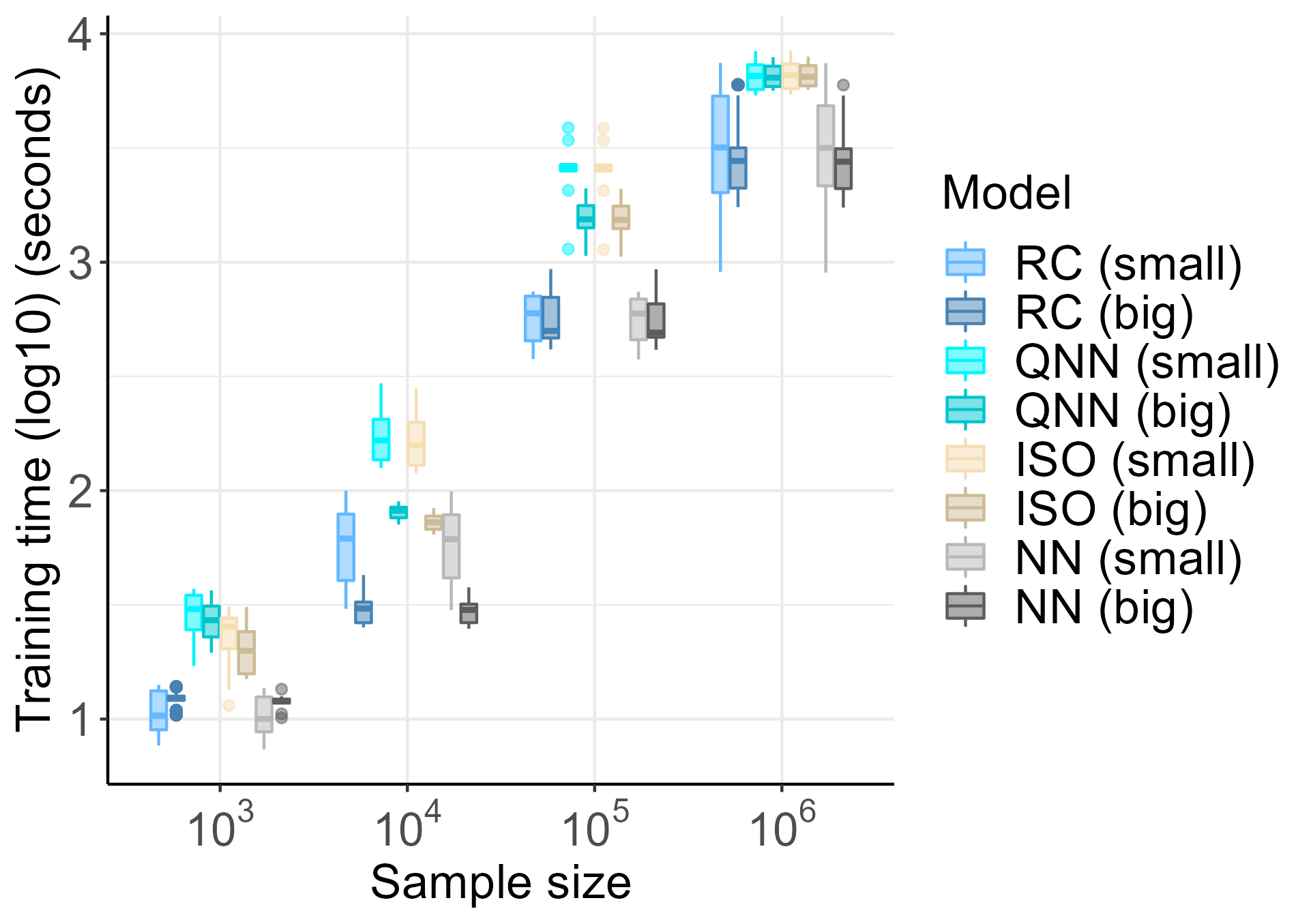

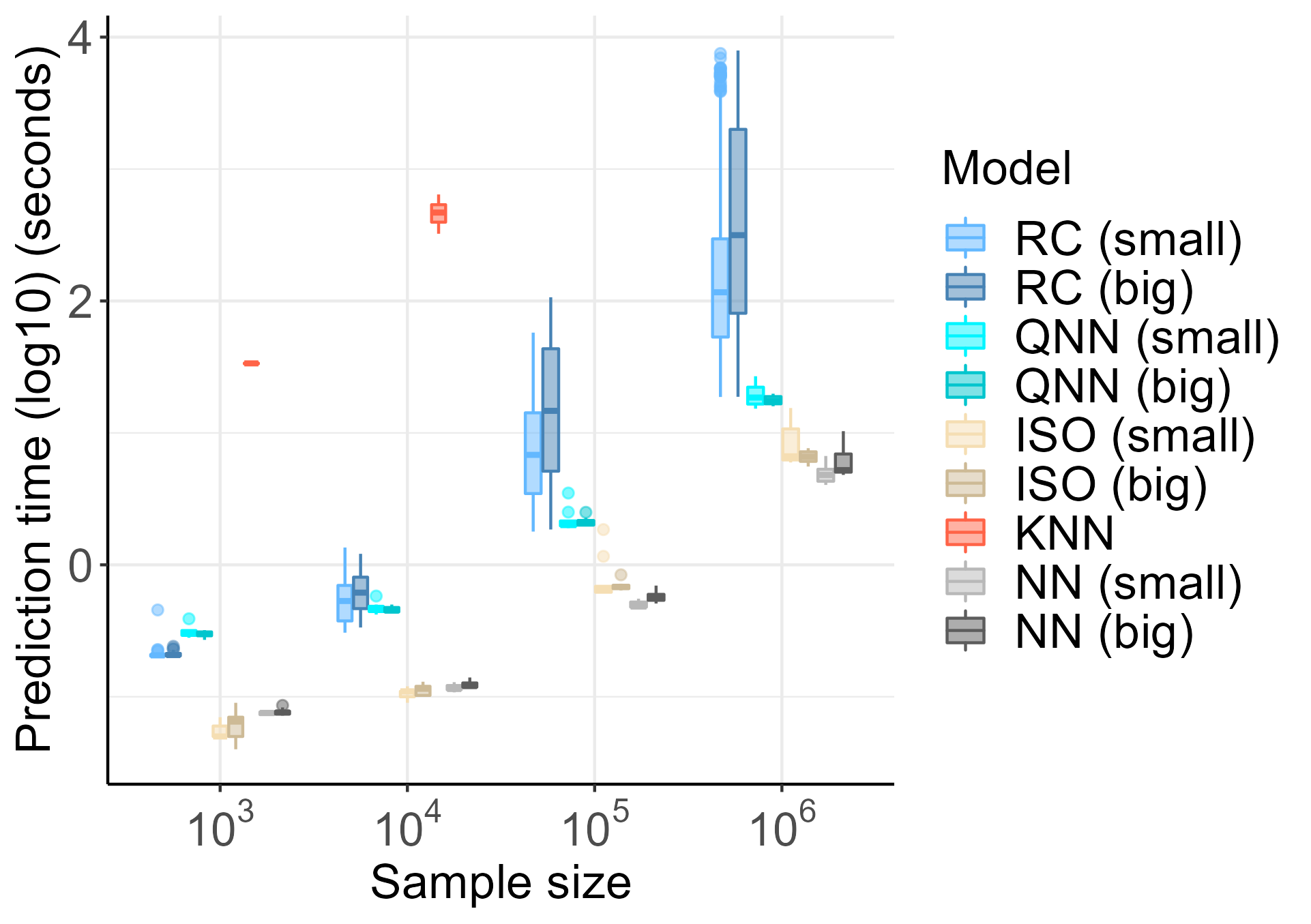

An algorithm directly comparable to the proposed recalibration method is the KNN regression, which we also apply considering the Epanechnikov’s kernel function, the same KNN approximate search algorithm and the same set of values of the (nearest samples) and parameters, for direct comparison. Due to memory and computational time constraints, all recalibrated models and KNN regression were fit in batches according to test set size, KNN regression being applied only to the first two scenarios of and . In the last two scenarios, KNN regression computational cost was simply too high to be carried over, taking alone up to two-thirds of the total simulation time, on average. As shown in Figure 4 though, it is clear that, while KNN regression is comparable to the recalibration in terms of methodology, it does not compare in terms of computational efficiency and model performance.

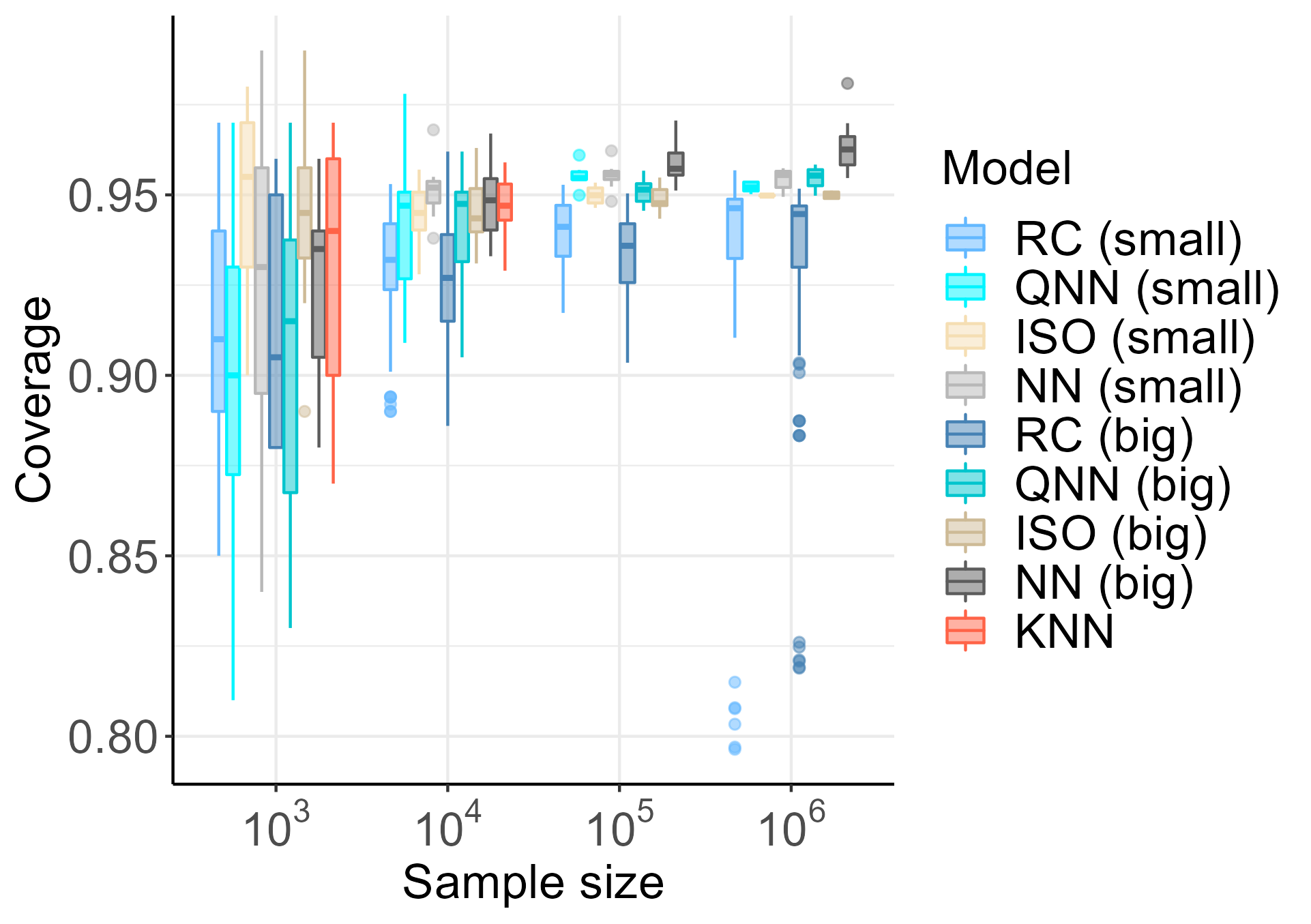

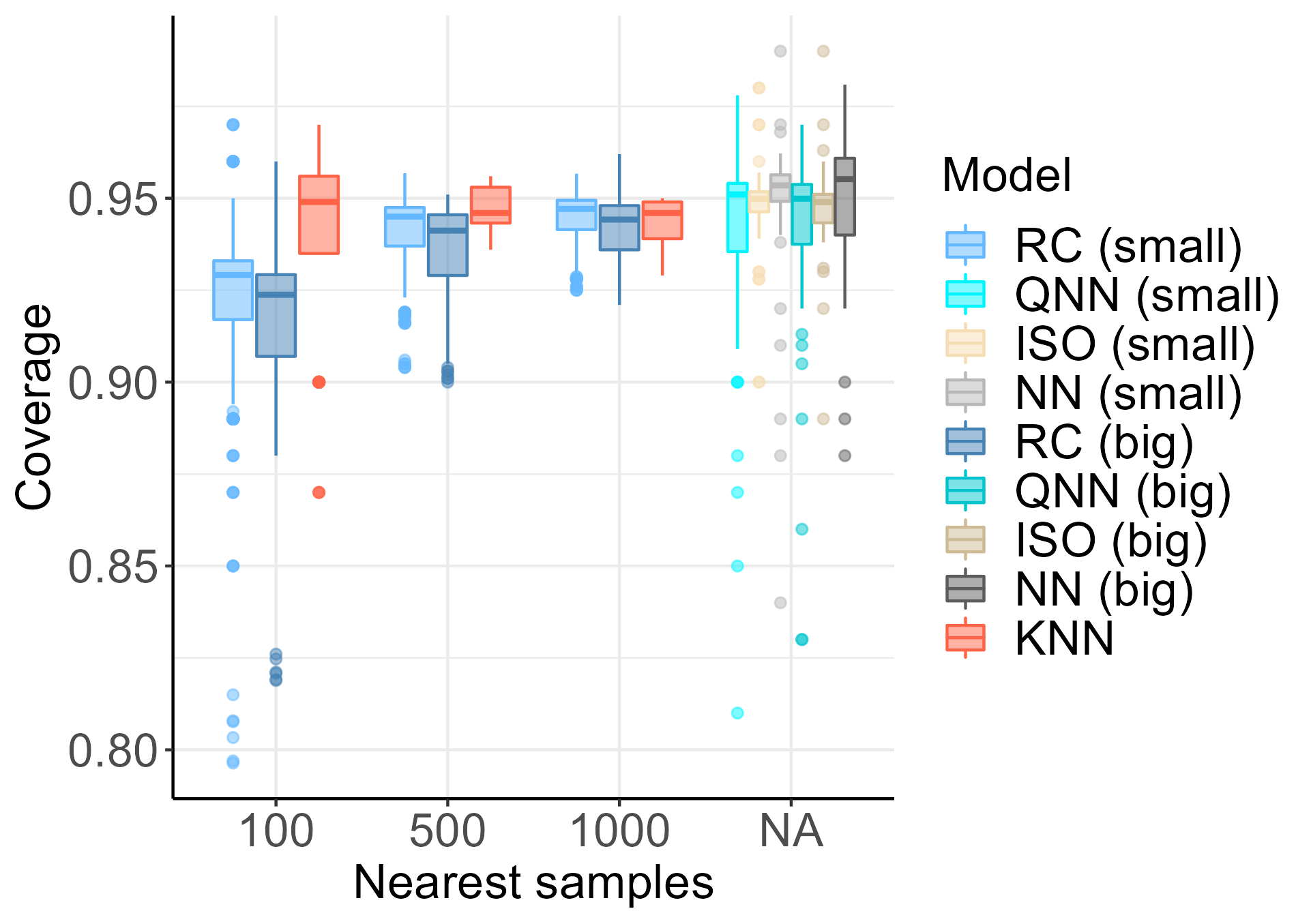

Figure 4(a) shows the models’ MSE as sample size increases, with the true model MSE (equal to 1) represented by the golden dashed line. Overall, recalibration improved MSE over the network models and other recalibration methods, with larger impact on the smaller neural network, benefiting the most when there is plenty of data. It can be observed that even with more data provided, the smaller neural network’s low capacity prevents it from improving model MSE further. Even in this case, recalibration was able to improve performance, on average. In Figure 4(b), increasing the nearest samples size improved the biggest recalibrated model’s MSE on average with diminishing effects as nearest samples size increases, meaning that increasing the proportion of nearest data will not add much information to the model predictions when there is already enough information, in terms of model capacity. The target layer and the approximation level also did not influence much the prediction accuracy (figure not shown). Figures 4(c) and 4(d) show the observed coverage of confidence intervals for different settings. Unsurprisingly, all models become more reliable as the sample size increases, and our recalibration method (RC), in particular, becomes more consistent for higher values of the parameter .

Figure 4(e) shows that the proposed recalibration algorithm does not significantly affect model training time as the sample sizes increase. However, Figure 4(f) confirms that our proposal significantly affects prediction time. This is partially mitigated by the search level of approximation, with the exact search taking longer than a higher approximation level (figure not show). Recalibration prediction memory size grows in , proportional to , where is the number of test observations, is the number of nearest samples, is the number of neurons in the target layer and is the size of the network’s output.

4.4 Diamonds Price Prediction

We explore the data from diamonds from the dataset "diamonds" available in the ggplot2 R package (Wickham, 2016). This data set lists several diamond characteristics including price in US dollars, carat weight, cut quality, colour, clarity, length (in mm), width (mm), depth (mm), and table width (width of the top of the diamond relative to the widest point).

Interest is in modelling diamond prices conditional on their physical attributes. We specify the response variable as Gamma distributed, , with the conditional mean and the shape parameter. The data were randomly assigned to the training set (70%), validation/recalibration set (20%), and test set (10%). We consider two models – a generalized linear Gamma model (GLM) with logarithmic link function, and a neural network model with negative Gamma log-likelihood loss function.

The architecture of the neural network model was selected by minimizing the loss function in the validation set within a predefined search space. The final network architecture is composed of an input layer, a hidden layer with neurons and ReLu activation function, two hidden layers with neurons and ReLu activation function, and a forked output with two exponential layers, one for estimating the mean, , and the other with zero-constrained weights for estimating the shape parameter, , which is the same for all observations.

In this application, we recalibrate both the Generalized Linear Model and the Neural Network by employing the three distinct methods considered in the simulation study presented in Section 4.2: Isotonic Regression Recalibration (Kuleshov et al., 2018), Density Estimation Recalibration (Kuleshov and Deshpande, 2022), and our Quantile Recalibration approach. Inspired by findings from the simulation study and considering our low-dimensional feature vector, we execute the Quantile Recalibration locally, directly within the input space (), using nearest neighbors.

Table 3 illustrates the impact of recalibration on prediction accuracy, measured by the Root-mean-square deviation, and the observed coverage for confidence intervals at , , and . Quantile Recalibration stands out as the sole method that effectively decreased the Root Mean Square Error (RMSE) of the Neural Network. Additionally, both Isotonic Regression Recalibration and Quantile Recalibration demonstrated remarkable performance in achieving observed coverage close to their respective nominal levels.

| Model | RMSE | Observed Coverage | ||

|---|---|---|---|---|

| 90% | 95% | 99% | ||

| GLM | 798.9 | 0.955 | 0.982 | 0.997 |

| Isotonic GLM RC | 789.3 | 0.894 | 0.949 | 0.991 |

| Density Estimation GLM RC | 796.0 | 0.956 | 0.982 | 0.997 |

| Quantile GLM RC | 751.2 | 0.898 | 0.946 | 0.986 |

| NN | 557.8 | 0.933 | 0.966 | 0.987 |

| Isotonic NN RC | 557.8 | 0.898 | 0.947 | 0.988 |

| Density Estimation NN RC | 558.0 | 0.934 | 0.965 | 0.987 |

| Quantile NN RC | 542.8 | 0.896 | 0.944 | 0.986 |

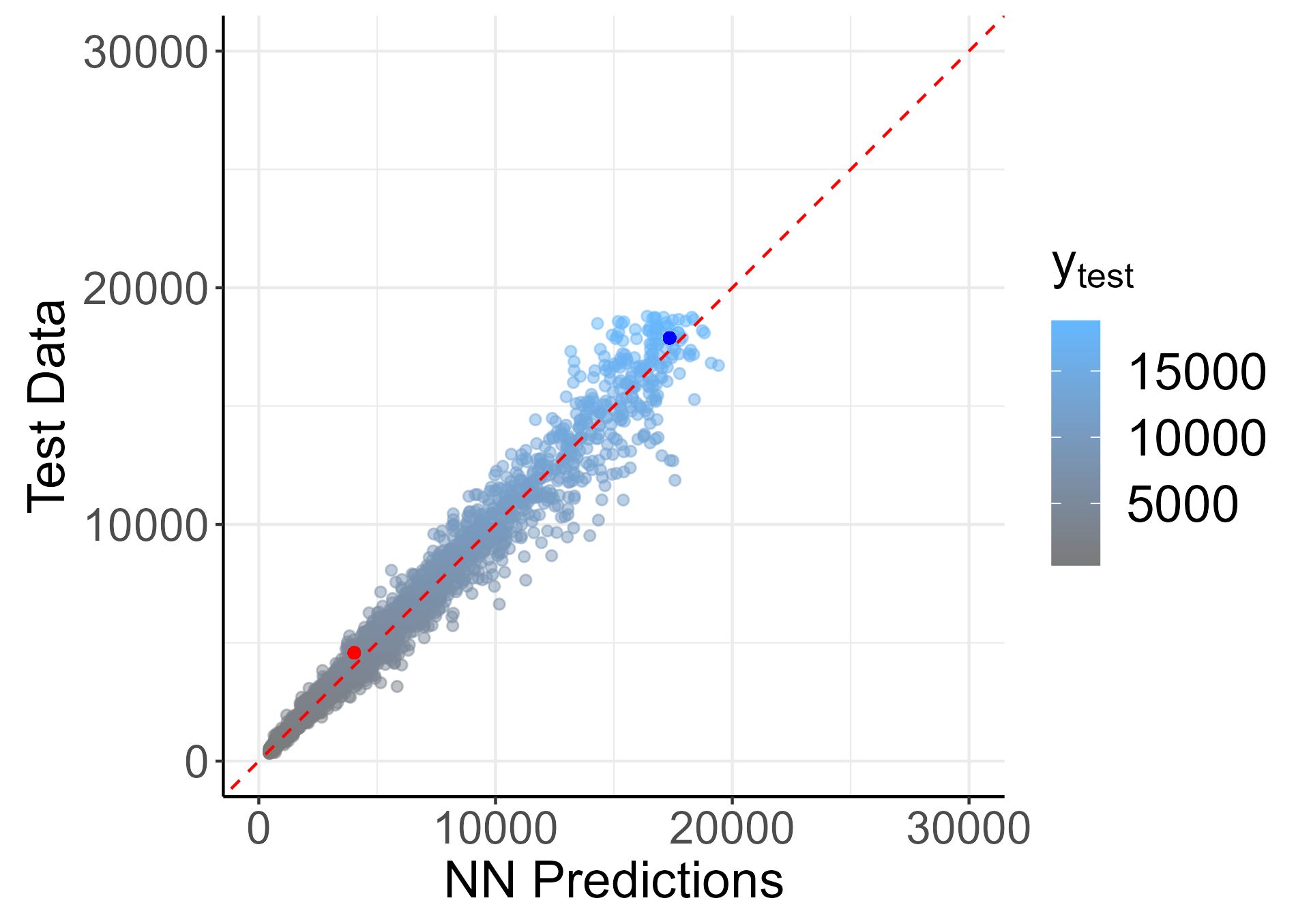

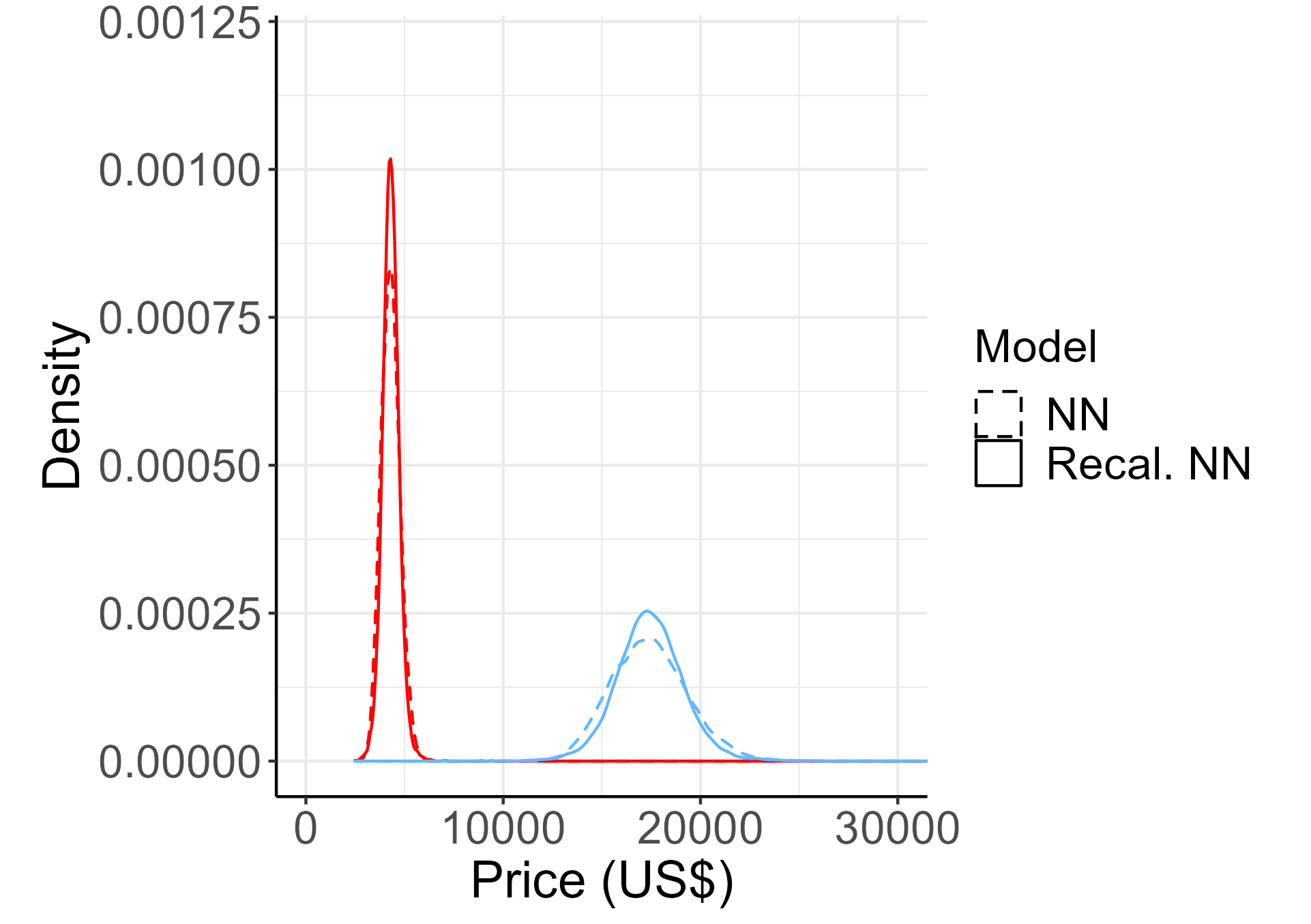

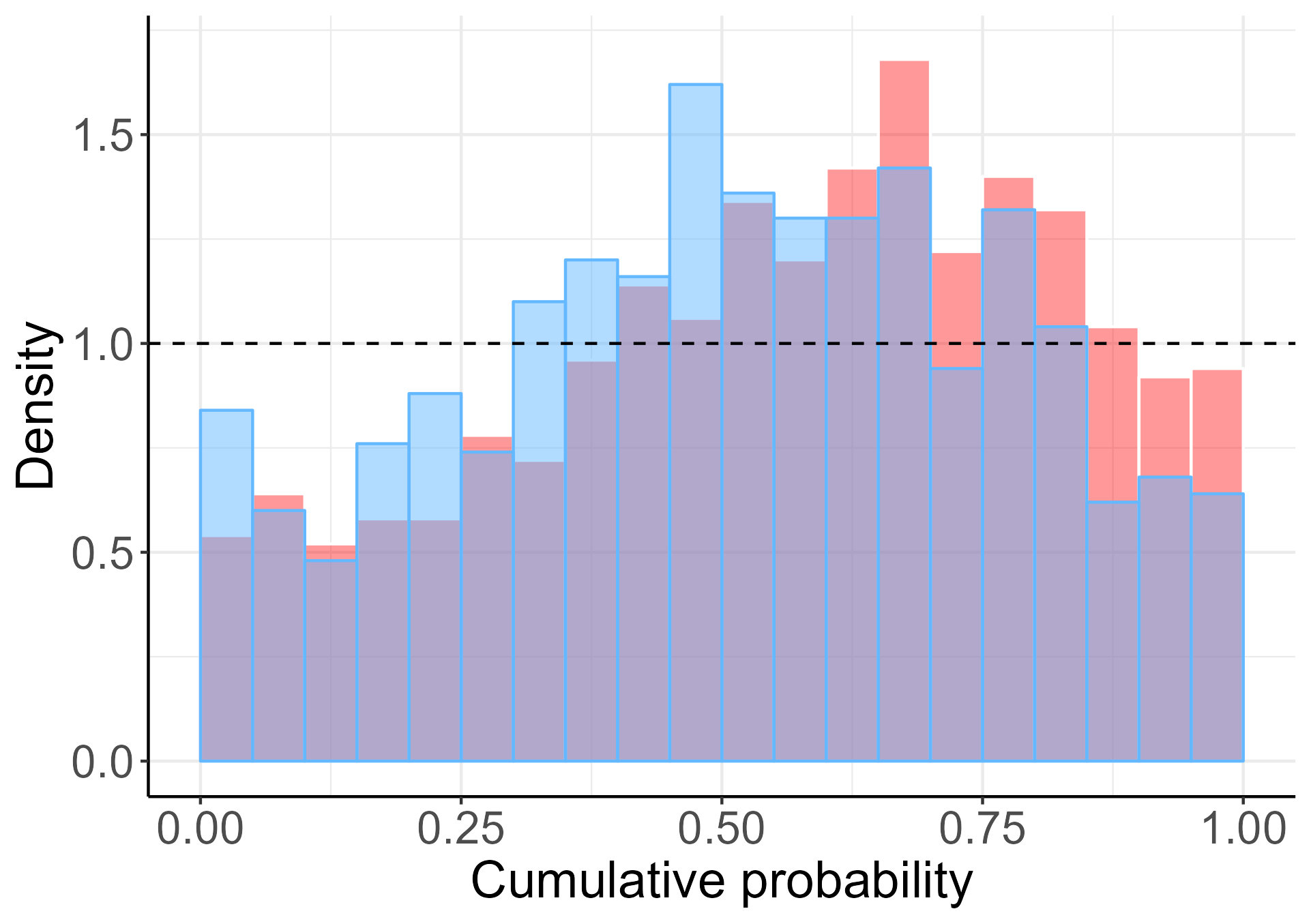

Figure 5 further explores the impact of our recalibration strategy on the base Neural Network model across different regions of the dependent variable space. Specifically, Figures 5(a) compares predictions made by the base model with observed diamond prices in the test set. There is an increased prediction dispersion for higher values of , underscoring the necessity for a heteroscedastic model. To illustrate local patterns, two points, (red) and (blue), are highlighted. Figure 5(b) overlays the predictive distributions of the base and recalibrated models for each highlighted point, showcasing that recalibration has not only decreased the variance but also adjusted the distribution mean and shape in each case.

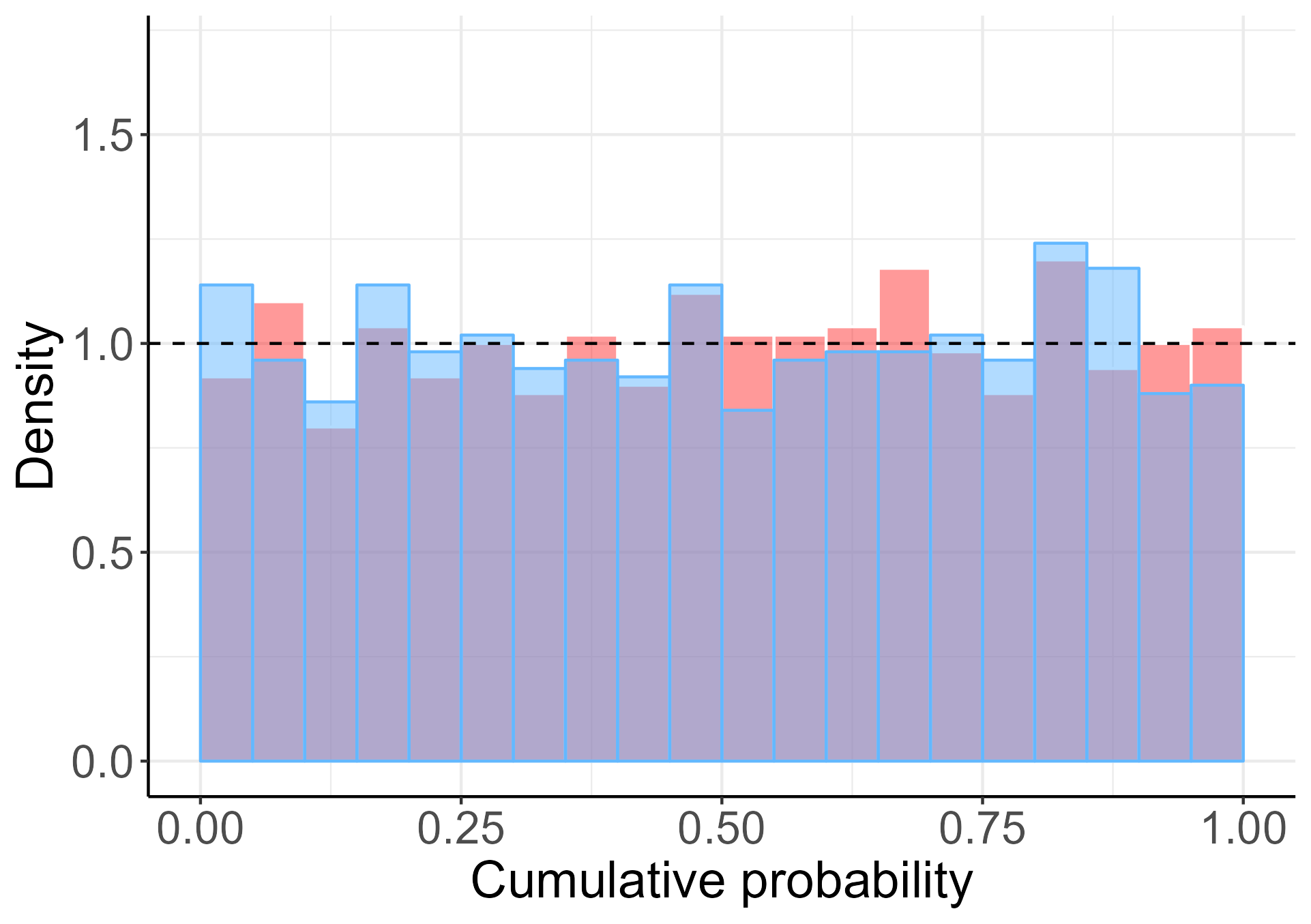

The cumulative probability histograms in Figure 5(c) reveal the deviation from uniformity for the base model in the proximity of the highlighted points. In contrast, the histogram of the recalibrated model (Figure 5(d)) exhibits a more uniform distribution, emphasizing that the recalibrated model provides a more accurate probabilistic representation of the conditional distributions.

5 Conclusion

This work introduces a novel method for recalibrating neural networks based on the observed cumulative probabilities of their predictive distributions. Unlike previous approaches that only consider the network’s outputs, this method addresses region-specific bias patterns by recalibrating the networks locally within a space learned by the neural network itself. Two different methods are considered when creating the initial probabilistic neural networks. The first involves assuming a probabilistic model through the selection of an appropriate loss function, while the second employs an empirical predictive distribution obtained via Monte Carlo Dropout.

The results of simulations using simple examples demonstrate the positive impact of the proposed method on various performance metrics. Recalibrated models exhibit improved Mean Squared Error, confidence intervals coverage, and interval scores compared to uncalibrated models. These improvements indicate better prediction accuracy and closer approximation to the true distribution. Furthermore, the recalibrated models demonstrate evenly distributed interval coverage while reducing interval width, effectively correcting local prediction bias and improving variance estimation.

Through a simulation study we explored the effects of different recalibration parameter configurations and compared the performance of our procedure with alternative recalibration approaches (Kuleshov et al., 2018; Kuleshov and Deshpande, 2022). The study revealed that training time is primarily influenced by the number of observations in the training set, while prediction time increases with nearest samples size, , and decreases with target layer dimensionality (number of neurons in the recalibration layer). Importantly, recalibration consistently yields superior MSE and interval metrics. Moreover, recalibrated neural networks prove to be more efficient than the simple application of KNN regression under the same conditions.

When tested against real data, recalibration demonstrates positive effects on prediction precision and confidence interval metrics. Sections 4.1, 4.2 and 4.4 demonstrate that recalibration can offer advantages even when the observed coverage closely matches the nominal level. This is particularly pertinent because the model may be locally uncalibrated, potentially leading to a misleading characterization of the underlying system. Additionally, it’s important to note that recalibration methods are not explicitly designed to minimize Mean Squared Error (MSE) or another specific metric. Instead, their primary goal is to offer a more comprehensive and accurate probabilistic description of the data-generative process.

Although our approach successfully improves the quality of predictive distributions, it is important to acknowledge that the prediction time can be a potential drawback. As a result, this method may not be suitable for scenarios where fast predictions are of utmost importance.

References

- Arya et al. (1998) Arya, S., Mount, D. M., Netanyahu, N. S., Silverman, R., and Wu, A. Y. (1998), “An optimal algorithm for approximate nearest neighbor searching fixed dimensions,” Journal of the ACM (JACM), 45, 891–923.

- Blum et al. (1963) Blum, J. R., Hanson, D. L., and Koopmans, L. H. (1963), “On the strong law of large numbers for a class of stochastic processes,” Zeitschrift für Wahrscheinlichkeitstheorie und Verwandte Gebiete, 2, 1–11.

- Chen et al. (2021) Chen, Q., Zhao, B., Wang, H., Li, M., Liu, C., Li, Z., Yang, M., and Wang, J. (2021), “Spann: Highly-efficient billion-scale approximate nearest neighborhood search,” Advances in Neural Information Processing Systems, 34, 5199–5212.

- Dawid (1984) Dawid, A. P. (1984), “Present Position and Potential Developments: Some Personal Views: Statistical Theory: The Prequential Approach,” Journal of the Royal Statistical Society. Series A (General), 147, 278–292.

- Dheur and Taieb (2023) Dheur, V., and Taieb, S. B. (2023), “A Large-Scale Study of Probabilistic Calibration in Neural Network Regression,” .

- Gal and Ghahramani (2016) Gal, Y., and Ghahramani, Z. (2016), “Dropout as a bayesian approximation: Representing model uncertainty in deep learning,” in international conference on machine learning, PMLR, pp. 1050–1059.

- Gneiting et al. (2007) Gneiting, T., Balabdaoui, F., and Raftery, A. E. (2007), “Probabilistic Forecasts, Calibration and Sharpness,” Journal of the Royal Statistical Society Series B: Statistical Methodology, 69, 243–268.

- Gneiting and Raftery (2007) Gneiting, T.— (2007), “Strictly Proper Scoring Rules, Prediction, and Estimation,” Journal of the American Statistical Association, 102, 359–378.

- Guo et al. (2017) Guo, C., Pleiss, G., Sun, Y., and Weinberger, K. Q. (2017), “On calibration of modern neural networks,” in International conference on machine learning, PMLR, pp. 1321–1330.

- Kuleshov and Deshpande (2022) Kuleshov, V., and Deshpande, S. (2022), “Calibrated and sharp uncertainties in deep learning via density estimation,” in International Conference on Machine Learning, PMLR, pp. 11683–11693.

- Kuleshov et al. (2018) Kuleshov, V., Fenner, N., and Ermon, S. (2018), “Accurate uncertainties for deep learning using calibrated regression,” in International conference on machine learning, PMLR, pp. 2796–2804.

- Kull et al. (2017a) Kull, M., Filho, T. S., and Flach, P. (2017a), “Beta calibration: a well-founded and easily implemented improvement on logistic calibration for binary classifiers,” PMLR, vol. 54 of Proceedings of Machine Learning Research, pp. 623–631.

- Kull et al. (2017b) Kull, M., Silva Filho, T.— (2017b), “Beyond Sigmoids: How to obtain well-calibrated probabilities from binary classifiers with beta calibration,” Electronic Journal of Statistics, 11, 5052–5080.

- Kumar et al. (2019) Kumar, A., Liang, P. S., and Ma, T. (2019), “Verified uncertainty calibration,” Advances in Neural Information Processing Systems, 32.

- Menéndez et al. (2014) Menéndez, P., Fan, Y., Garthwaite, P., and Sisson, S. (2014), “Simultaneous adjustment of bias and coverage probabilities for confidence intervals,” Computational Statistics and Data Analysis, 70, 35–50.

- Minderer et al. (2021) Minderer, M., Djolonga, J., Romijnders, R., Hubis, F., Zhai, X., Houlsby, N., Tran, D., and Lucic, M. (2021), “Revisiting the calibration of modern neural networks,” Advances in Neural Information Processing Systems, 34, 15682–15694.

- Mukhoti et al. (2020) Mukhoti, J., Kulharia, V., Sanyal, A., Golodetz, S., Torr, P., and Dokania, P. (2020), “Calibrating deep neural networks using focal loss,” Advances in Neural Information Processing Systems, 33, 15288–15299.

- Platt et al. (1999) Platt, J. et al. (1999), “Probabilistic outputs for support vector machines and comparisons to regularized likelihood methods,” Advances in large margin classifiers, 10, 61–74.

- Prangle et al. (2014) Prangle, D., Blum, M. G., Popovic, G., and Sisson, S. (2014), “Diagnostic tools for approximate Bayesian computation using the coverage property,” Australian & New Zealand Journal of Statistics, 56, 309–329.

- Rodrigues et al. (2018) Rodrigues, G., Prangle, D., and Sisson, S. A. (2018), “Recalibration: A post-processing method for approximate Bayesian computation,” Computational Statistics & Data Analysis, 126, 53–66.

- Si et al. (2021) Si, P., Bishop, A., and Kuleshov, V. (2021), “Autoregressive Quantile Flows for Predictive Uncertainty Estimation,” arXiv preprint arXiv:2112.04643.

- Silva Filho et al. (2023) Silva Filho, T., Song, H., Perello-Nieto, M., Santos-Rodriguez, R., Kull, M., and Flach, P. (2023), “Classifier calibration: a survey on how to assess and improve predicted class probabilities,” Machine Learning, 1–50.

- Song et al. (2019) Song, H., Diethe, T., Kull, M.— (2019), in Proceedings of the 36th International Conference on Machine Learning, eds. Chaudhuri, K., and Salakhutdinov, R., PMLR, vol. 97 of Proceedings of Machine Learning Research, pp. 5897–5906.

- Tran et al. (2020) Tran, M.-N., Nguyen, N., Nott, D., and Kohn, R. (2020), “Bayesian deep net GLM and GLMM,” Journal of Computational and Graphical Statistics, 29, 97–113.

- Utpala and Rai (2020) Utpala, S., and Rai, P. (2020), “Quantile regularization: towards implicit calibration of regression models,” arXiv preprint arXiv:2002.12860.

- Wickham (2016) Wickham, H. (2016), ggplot2: Elegant Graphics for Data Analysis, Use R!, Springer International Publishing.

- Xiong et al. (2023) Xiong, M., Deng, A., Koh, P. W., Wu, J., Li, S., Xu, J., and Hooi, B. (2023), “Proximity-Informed Calibration for Deep Neural Networks,” .