Periodicity in Hedge-myopic system and an asymmetric NE-solving paradigm for two-player zero-sum games

Abstract

In this paper, we consider the two-payer zero-sum repeated game in which one player (player X) employs the popular Hedge (also called multiplicative weights update) learning algorithm while the other player (player Y) adopts the myopic best response. We investigate the dynamics of such Hedge-myopic system by defining a metric , which measures the distance between the stage strategy and Nash Equilibrium (NE) strategy of player X. We analyze the trend of and prove that it is bounded and can only take finite values on the evolutionary path when the payoff matrix is rational and the game has an interior NE. Based on this, we prove that the stage strategy sequence of both players are periodic after finite stages and the time-averaged strategy of player Y within one period is an exact NE strategy. Accordingly, we propose an asymmetric paradigm for solving two-player zero-sum games. For the special game with rational payoff matrix and an interior NE, the paradigm can output the precise NE strategy; for any general games we prove that the time-averaged strategy can converge to an approximate NE. In comparison to the NE-solving method via Hedge self-play, this HBR paradigm exhibits faster computation/convergence,better stability and can attain precise NE convergence in most real cases.

Keywords: Repeated game, Equilibrium solving, Hedge algorithm, Myopic best response, Evolutionary dynamical analysis

1 Introduction

Game theory is widely used to model interactions and competitions among self-interested and rational agents in the real world [15, 30, 33]. In such situations, the utility of each agent is determined by the actions of all the other agents, leading to the solution concept of equilibrium, in which Nash equilibrium (NE) is a central one. This makes the NE-solving one of the most significant problems in game theory, which however is very hard for general games.

The notion of NE [31, 32] aims to describe a stable state where each participant makes the optimal choice considering the strategies of others and thus has no incentive to change the strategy unilaterally. Due to the mutual influence of participants in the game and the existence of possible multiple equilibrium points in different scenarios, NE-solving is a difficult problem, which has been proven to be PPAD-hard [10, 11, 36]. For the special two-player zero-sum games, linear programming [21, 46] provides a powerful method to solve NE in polynomial time [45]. However, in practical scenarios, because of large scalability issues, imperfect information and the complexity of multiple-stage dynamics, two-player zero-sum game is still a subject of ongoing investigation and attracts attentions from researchers in different fields [26, 12, 38, 37]. Especially, participants are often not perfectly rational, leading to research which aimed at approximating NE from a learning perspective [14].

Concerning learning in games, there has been a long history and plentiful literature, where a lot of learning algorithms have been proposed according to different settings. Under the Fictitious Play algorithm [14], the empirical distribution of actions taken by each player converges to NE if the stage game has generic payoffs and is [41] or zero-sum game [27] or potential game [28]. When each player employs the no-regret algorithm [9, 8] to determine their stage strategy in repeated games, their time-averaged strategy profile converges to the coarse correlated equilibrium in general-sum games [18] and to NE in two-player zero-sum games. In imperfect-information extensive-form games, Zinkevich et al. [47] proposed the counterfactual regret minimization (CFR) algorithm and proved its convergence to NE in the two-player zero-sum setting. Based on these methods, lots of variants were proposed and widely used in solving equilibrium in complicated games [4, 5, 6, 22, 29, 43]. Note that in all these works, every player in the game adopts the same learning algorithm and the convergence results are based on the term of time-averaged strategy.

However, further investigation on the learning dynamics shows that even in simple game models, basic learning algorithms can lead to highly complex behavior and may not converge [35, 39, 42, 40, 19]. Palaiopanos et al. [34] discovered specific instances of potential games where the behavior of multiplicative weights update (MWU) algorithm exhibits bifurcation at the critical value of its step size. Bailey and Piliouras [2] showed that in two-player zero-sum games, when both players adopt the MWU algorithm, the system dynamics deviate from equilibrium and converge towards boundary. Mertikopoulos et al. [26] studied the regularized learning algorithms in two-player zero-sum games and proved the Poincaré recurrence of the system behavior, implying the impossibility of convergence to NE from any initial strategy profile. Perolat et al. [37] extended the results of Poincaré recurrence from normal-form games to two-player zero-sum imperfect-information games and built an algorithm to approximate NE by solving a series of regularized game with unique NE. Generally speaking, there is no systematic framework for analyzing the limiting behavior of these repeated games [20, 44].

For the asymmetric case, as emphasized in [7], the limiting behavior of dynamic processes where players adhere to different update rules is an open question, even for potential games. Therefore, related theoretical analysis of such system is extremely rare. Our previous work [16, 17] studied such dynamical system where one player employs the Hedge algorithm and the other player takes the globally or locally optimal strategy in finitely repeated two-player zero-sum games and proved its periodicity when the game is . As a byproduct, our investigation reveals that the detailed understanding about the dynamics can facilitate the design of novel algorithms with special properties, thereby suggesting a promising avenue for advancing learning algorithms.

This paper will consider the general zero-sum stage game and investigate the dynamics of repeated game under asymmetric updating rules. To be specific, we will study the dynamics of the repeated game where one player (player X) employs the Hedge algorithm to update his stage strategy and the other player (player Y) adopts the according myopic best response to the stage strategy of player X. The main contributions of this paper can be summarized as follows.

-

(1)

This paper considers the Hedge-myopic system and investigates its dynamic by analyzing the trend of a quantity called based on the Kullback-Leibler divergence, which measures the distance between the stage strategy x and the NE strategy of player X. For the game with rational payoff matrix and an interior NE, we prove that along the strategy sequence the Q-sequence is bounded and can only take finite values on the evolutionary path. This implies that the strategy sequence of player X will not converge to the NE strategy and justifies the finding in the literature.

-

(2)

Using the dynamic property, this paper theoretically proves that the stage strategy sequences of both players are periodic after finite stages for the game with rational payoff matrix and an interior NE. Additionally, the time-averaged strategy of player Y within one period is an exact NE strategy.

-

(3)

Based on the theoretical results, this paper proposes an asymmetric paradigm called HBR for solving NE in two-player zero-sum games. For the special game with rational payoff matrix and an interior NE, the paradigm can output the precise NE strategy; for any general games we prove that the time-averaged strategy can converge to an approximate NE. In comparison to the NE-solving method via Hedge self-play, this HBR paradigm exhibits faster computation/convergence, better stability and can attain precise NE convergence in most real cases.

2 Preliminary and Problem Formulation

2.1 Online Learning and Hedge Algorithm

Hedge algorithm is a popular no-regret learning algorithm proposed by Freund and Schapire, based on the context of boost learning [13]. Hedge algorithm is also known as weighted majority [24] or exponential weighted average prediction [8], or multiplicative weights update [1].

Consider the online learning framework known as learning with expert advice [8]. In this framework, the decision maker is a forecaster whose goal is to predict an unknown sequence , where belongs to an outcome space . The prediction of the forecaster at time , denoted by , is assumed to belong to a convex subset of . At each time , the forecaster receives a finite set of expert advice , then the forecaster computes his own guess based on . Subsequently the true outcome is revealed. Predictions of the forecaster and experts are scored using a non-negative loss function and the cumulative regret is introduced to measure how much better the forecaster could have done compared to how he did in hindsight, which is defined to be

By the Hedge algorithm, the prediction at time is taken as the weighted average of the predictions from the experts, i.e., , where

Then, the prediction sequence has the following regret bound.

Theorem 2.1 (Theorem 2.2 of [8]).

Assume that the loss function is convex in its first argument and takes values in . For any and , and for all , the regret for the Hedge algorithm satisfies

In particular, for , the upper bound becomes .

2.2 Normal-form zero-sum Game

Consider a two-player zero-sum normal-form game . The players are called player X and player Y. Suppose there are feasible actions for each player. We denote the action set of player X by and the action set of player Y by . For each action profile , the payoff obtained by player Y is and thus the payoff obtained by player X is since the game is zero-sum. Naturally, the payoff of the game is shown by a matrix . The matrix is called the payoff matrix for player Y and the loss matrix for player X. A mixed strategy of a player is a probability distribution over his action set. Denote the mixed strategy of player X and player Y by and respectively. The bold font is used to emphasize that x and y are both vectors. Given the mixed strategy profile , the payoff of player Y is and the payoff of player X is .

Write the NE strategy profile of the game as . Then the value of the game is

| (1) |

Denote the support of by and the support of by . A NE is said to be interior if and .

A strategy profile is called a Nash equilibrium (NE) if for all and , we have

Given a strategy profile , the exploitability [25] of strategy x is defined as the potential gain for player Y if she switches to the best response of strategy x suppose that x is fixed, i.e.,

Similarly, the exploitability of the strategy y is defined to be

Intuitively, if a strategy has low exploitability, it is difficult for the opponent to take advantage of it, while a strategy with high exploitability can be effectively exploited by the opponent. Given a strategy profile , a common metric to measure its distance to NE, called Nash Distance () [25], is

Since the game is zero-sum, .

If the game admits an interior NE strategy of player X, we denote the cross entropy between strategy x and by function , i.e.,

| (2) |

where for all . It is easy to see that for all x.

In the following, we will focus on infinitely repeated game, that is to say, let the game be repeated for infinite times. We denote , the stage strategy of player X and player Y at time respectively. Then, the instantaneous expected payoff of player Y is . Different stage strategy updating rules would lead to different stage strategy sequences of player X and Y, which form different game dynamic systems. Below we will study the dynamic characteristics of the repeated games driven by the Hedge algorithm and the myopic best response.

2.3 Problem Formulation

First, let player X update his stage strategy according to the Hedge algorithm. Specifically, the strategy of player X at time is updated by

| (3) |

where is called the learning rate, which is a constant parameter. In this paper, we assume that is sufficiently small and determined by the payoff matrix .

From formula (3), is fully determined by , , …, . Further, we can compute from and and get

| (4) |

Then, let player Y only consider maximizing her instantaneous expected payoff and take myopic best response to at each time . In most cases, the myopic best response is unique and is pure strategy. When the best response is not unique, we stipulate that player Y chooses the pure strategy with the smallest subscript in , i.e.,

| (5) |

and is a pure-strategy vector with only the -th element is 1 and all the other elements are 0. Then, the strategy of player Y at each stage is well-defined and is pure strategy. Apparently is totally determined by . Combined with (4), we know that is fully determined by , with no randomness involved.

Given the action rule of player X and Y as above, the infinitely repeated game is intrinsically determined and the system is called the Hedge-myopic system. In this paper, we will study the dynamic characteristics of such a dynamical system and try to answer the questions like: Is the system periodic? Does the system converge?

3 Main Results

3.1 Rational Games with an Interior Equilibrium

In this session, we prove that for the game with rational payoff matrix and an interior NE, the dynamics of the Hedge-myopic system is periodic after finite stages.

We state some assumptions below:

Assumption 1: The payoff matrix is rational and the game has an unique interior NE, denoted by ;

Assumption 2: The matrices are all non-singular for where is defined as

| (6) |

We note here that the uniqueness of equilibrium here is actually not a necessary condition. Through experiments, we found that as long as the game has interior equilibrium, even if it is not unique, the game system can still generate cycles. The assumption of uniqueness is a requirement in theoretical proofs.

Recall formula (2) and (3), we denote

| (7) |

where is the value of the game. Thus is determined by , , …, and it can measures the “goodness” of . Call the Q-sequence.

actually is based on the Kullback-Leibler divergence (KL divergence), which measures the level of resemblance between the strategy and the NE strategy and defined as

| (8) |

Here, we omit the term for convenience and obviously

Hence, by studying the Q-sequence especially the difference between and , we can obtain the variation in the level of resemblance between the stage strategy and the NE strategy along the time.

By (7), we can calculate

| (9) |

Recall that if is small. Substitute this into the definition of , we obtain

| (10) |

On the other hand, since is the myopic best response of , i.e., , we have

| (11) |

by the Minimax theorem [46].

Substitute (11) to (10), we get

indicating that roughly speaking, the value of gradually decreases as time increases.

Inspired by this rough estimation, we can prove the below theorem.

Theorem 3.1.

There exists a positive number such that for all , i.e., the Q-sequence is bounded.

To prove Theorem 3.1, we need to study the sequence and in details. To this end, define

| (12) |

where with . Take , we have . Obviously, if , then ; if , then .

Depending on whether is positive, for the mixed strategy set , define

Easy to see that the NE strategy , hence .

To locate the regions and on , we need the following inequality in probability theory.

Lemma 3.1 (Lemma A.1 of [8]).

Let be a random variable with . Then, for any ,

Applying Lemma 3.1 , we can estimate as below.

where . Then, depending on whether is positive, we further split the set into another two regions and where

For the strategy , if , immediately we have , i.e., . Hence, we have the Claim 1 below:

Claim 1: and .

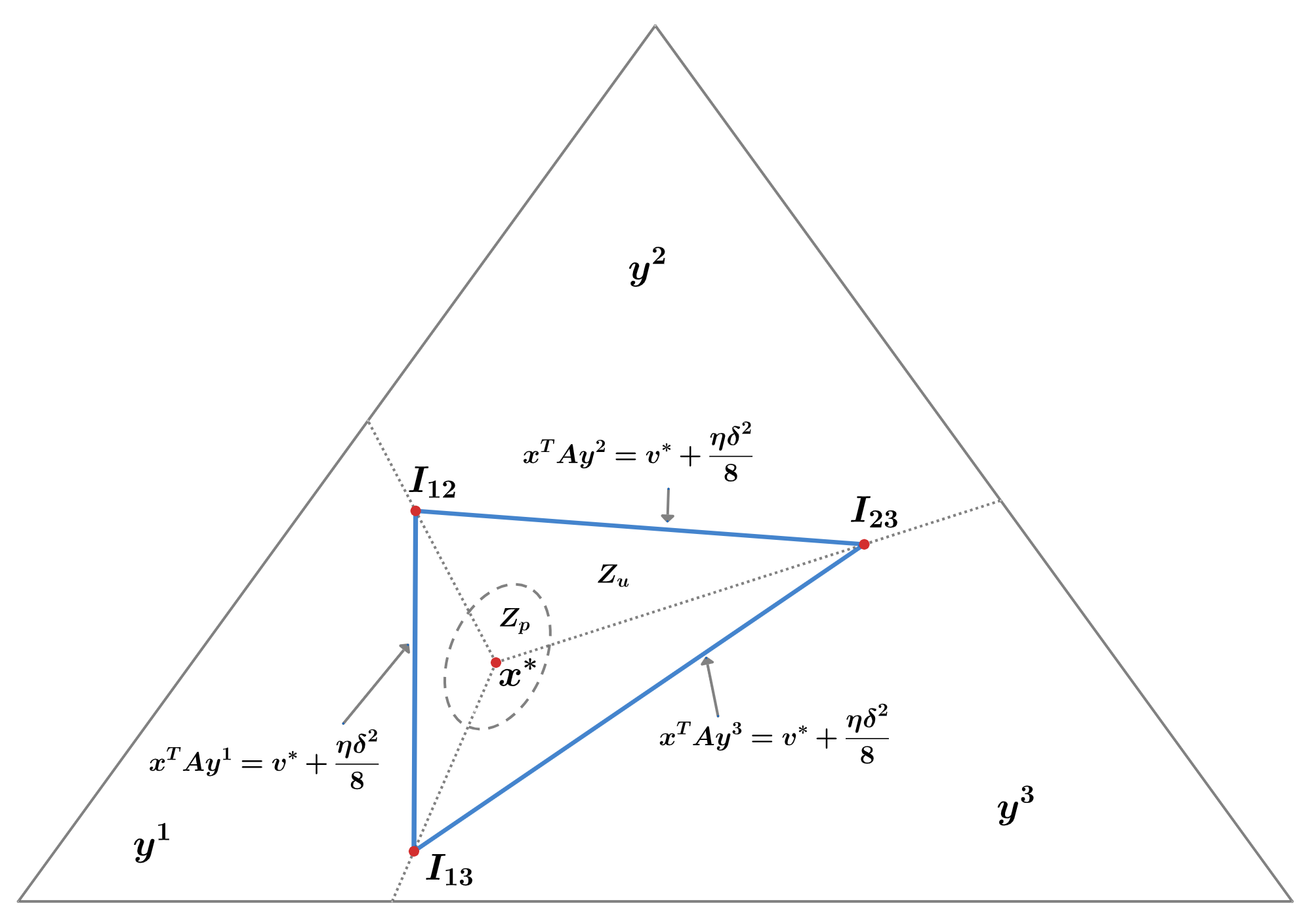

Figure 1 gives a graphical illustration about the region , , and interior NE strategy for a game. In this figure, the entire triangular region represents the simplex , and the red point in the center represents the NE strategy of player X; the gray dashed lines divide the triangular region into three areas, labeled , and respectively, which represents the best response action of player Y to the strategies in that area; the points on the blue solid line represent the strategy whereby the payoff of player Y is equal to when player Y adopts the corresponding best response, and the triangular region enclosed by the blue solid line is region ; within region , the elliptical region enclosed by the gray dashed line (the actual region may not necessarily be elliptical) is region , and the NE strategy is located in region .

For the region , we claim that:

Claim 2: The region can be further rewritten as , where . Thus, the region is a bounded polyhedron.

For the bounded polyhedron, we have the following result, which can be found in the Theorem 2.9 of [3].

Lemma 3.2 (Representation of Bounded Polyhedra).

A bounded polyhedron is the set of all convex combinations of its vertices.

In Figure 1, the points and are the vertices of polyhedron . Thus by Lemma 3.2, every point in can be written as a convex combination of these vertex points. Then, we can prove that the polyhedron must lie in the strict interior of .

Proposition 3.1.

If , then the elements of x are uniformly lower bounded. That is, for all , there exists such that for all .

(Proof in Appendix A)

Based on Proposition 3.1, we can obtain the following corollary.

Corollary 3.1.

In the Hedge-myopic system, if , then is upper bounded, i.e., there exists such that for all .

Proof.

Since , we immediately prove that is also upper bounded by in the region .

Corollary 3.1 indicates the boundness of over and , which is a property in a spatial sense. The subsequent proof of Theorem 3.1 demonstrates that the boundness in the spatial sense actually implies boundness in the temporal sense.

Proof of Theorem 3.1.

By Corollary 3.1, if , then .

Consider the sequence in the Hedge-myopic system. Suppose that for some time , . Then,

| (13) |

where

Now, we consider different cases for the behavior of the strategy sequence .

Case 1: if the strategy sequence never goes into the region , which implies that for all , then we have for all . By calculating, . Hence, for all .

Case 2: if the strategy sequence goes into the region at some time , then for the strategy before time , we have for all . For the strategy after time :

(1). if , then we have ;

(2). if , then we can find an integer such that and for .

Combining this with (13), we can obtain that since .

Take , then the Q-sequence is upper bounded by . ∎

From Definition (2), for strategy x, if some element is near zero, the value of is near infinity. Hence, by Theorem 3.1, the elements of the stage strategy cannot be too small since the Q-sequence is bounded. Based on this direct intuition, we can further prove the following theorem, which shrinks the range of possible values for to be a finite set.

Theorem 3.2.

In the Hedge-myopic system, for player X can only take finite values.

(Proof in Appendix B)

Remark 1.

From the proof of Theorem 3.2, it can be observed that when there are irrational number elements in the payoff matrix, Theorem 3.2 no longer holds except for the special case such as all elements are rational multiples of the same irrational number. This implies that the rationality of the payoff matrix is nearly an intrinsically necessary condition for periodicity.

By Theorem 3.2, in the Hedge-myopic system, player X can only adopt a finite number of mixed strategies. This directly leads to the periodicity of the dynamical system as stated below.

Theorem 3.3.

In the Hedge-myopic system with Assumption 1 and Assumption 2 satisfied, after finite steps,

-

(1)

the strategy sequence of player X and player Y enters a cycle (i.e., is periodic);

-

(2)

the time-averaged strategy of player Y in one period is a NE strategy.

In other words, there exists and such that for all , we have and , where is a NE strategy of player Y.

Below we give an example to illustrate Theorem 3.3.

Example 3.1.

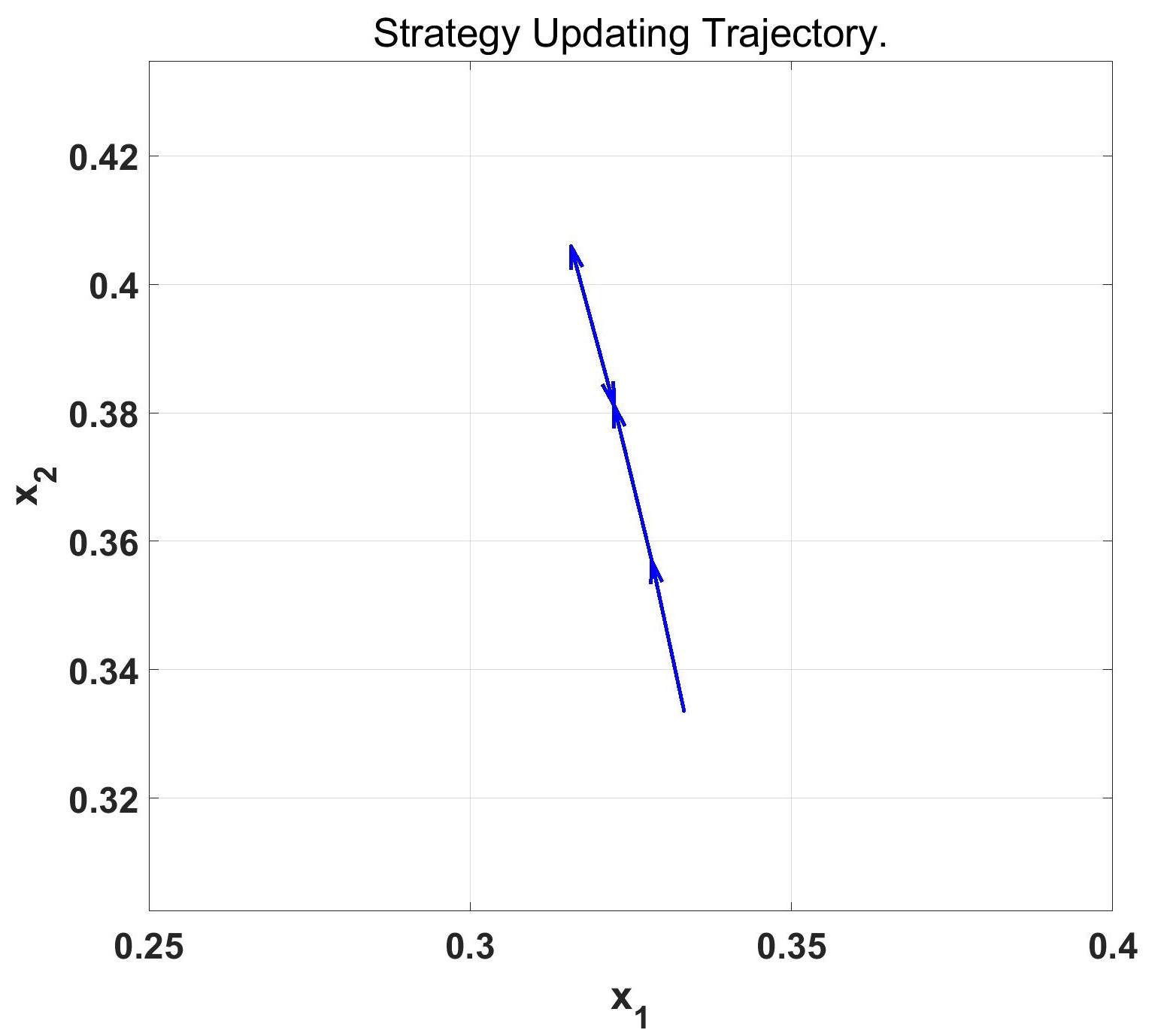

Consider a zero-sum game and the payoff matrix is taken as

and . In the Hedge-myopic system for this game, the evolution of is shown in Figure 2. The X-axis represents the first element , and the Y-axis represents the second element .

From Figure 2, we can observe that basically gradually approaches the NE strategy of player X. However, after reaching a certain range, enters a cycle. In Figure 2, we mark a point such that two red arrows both point to it, meaning that a cycle is formed. Additionally, we can see that does not converge to his NE strategy, no matter how long the game is repeated.

Before proving Theorem 3.3, we give Lemma 3.3 below by which we only need to prove the periodicity of in order to prove the periodicity of the system.

Lemma 3.3.

If enters a cycle, then also enters a cycle and her time-averaged strategy in a single cycle is a NE strategy.

(Proof in appendix C)

Now, we can prove Theorem 3.3.

Proof of Theorem 3.3.

By Lemma 3.2, can only take finite values. Then, using the pigeonhole principle, we can obtain that there must exist two stages, , such that because the game is repeated for infinite times. Since is fully determined by , we have , which implies that is periodic from time . Combining Lemma 3.3, we can prove Theorem 3.3. ∎

Remark 2.

The time required to enter a cycle depends on the parameter . Due to the complexity of the problem, it is difficult to provide an explicit expression for it. We have studied it for games in [17] where the time needed for the strategy sequences of both players to enter a cycle is .

Remark 3.

In addition to periodicity, it is worth noting that the time-averaged strategy of player Y in a single cycle is a precise NE strategy! Compared with this, when both players adopt the no-regret learning algorithm in two-player zero-sum games, their time-averaged strategy profile converges to a NE when the time horizon goes to infinity, that is to say, only an approximate NE can be obtained. Moreover, in the Hedge-myopic system, not only can we obtain a precise NE, but we also only need to compute the time-averaged strategy in a single cycle whose length is far shorter than the whole time horizon.

3.2 Non-periodicity Examples without Rational Interior NE

In this section, we study the dynamic of the Hedge-myopic system for general games by examples. These games may have an unique irrational interior equilibrium, or have more than one interior equilibria, or have an unique non-interior equilibrium. We will see that the dynamics of the Hedge-myopic systems can vary significantly for different games, preventing a consistent result.

First, we give Example 3.2 to show that when the NE of the game is irrational, the periodicity of the strategy sequence no longer holds.

Example 3.2.

Consider a zero-sum game with the payoff matrix for player Y being

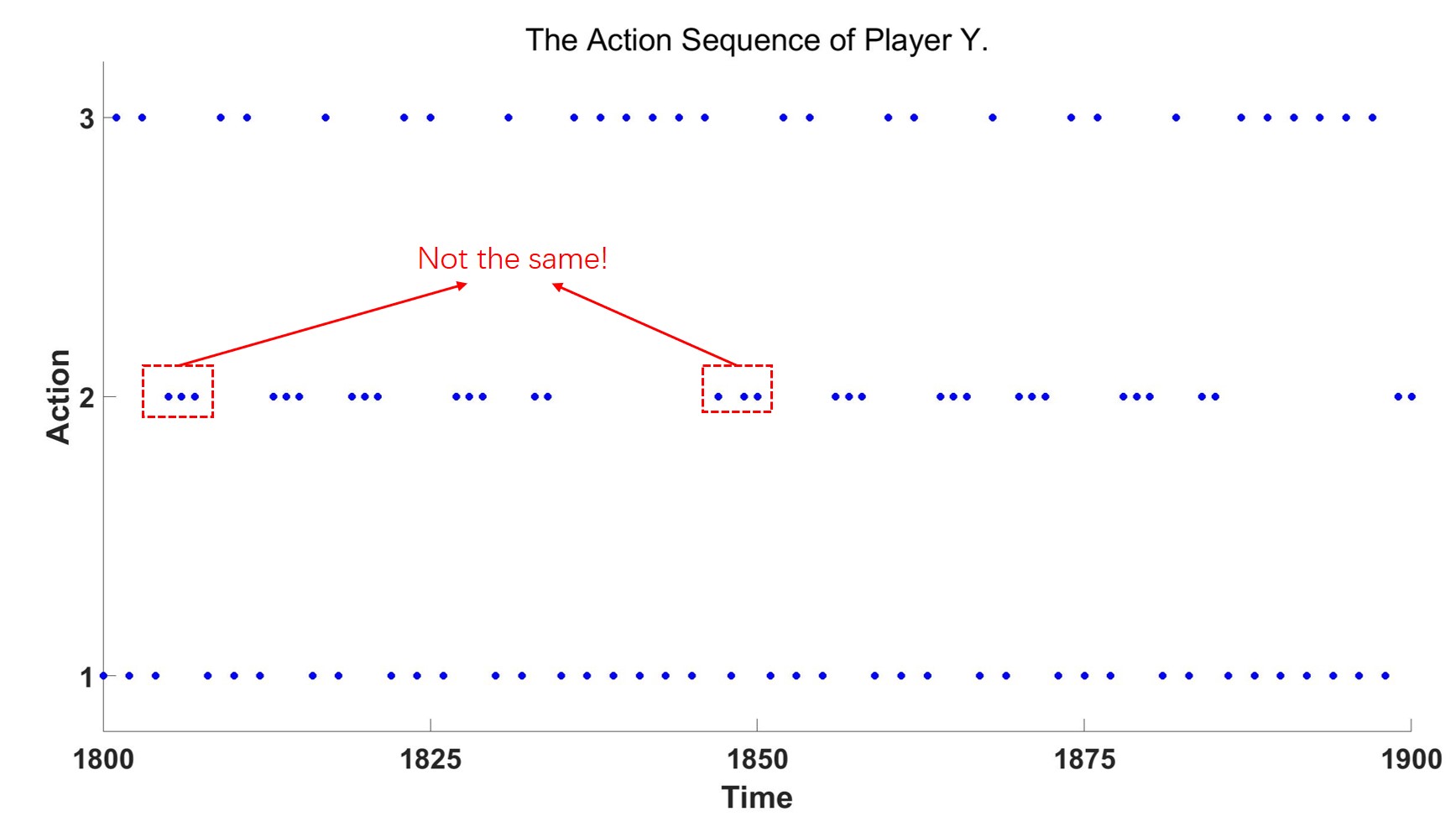

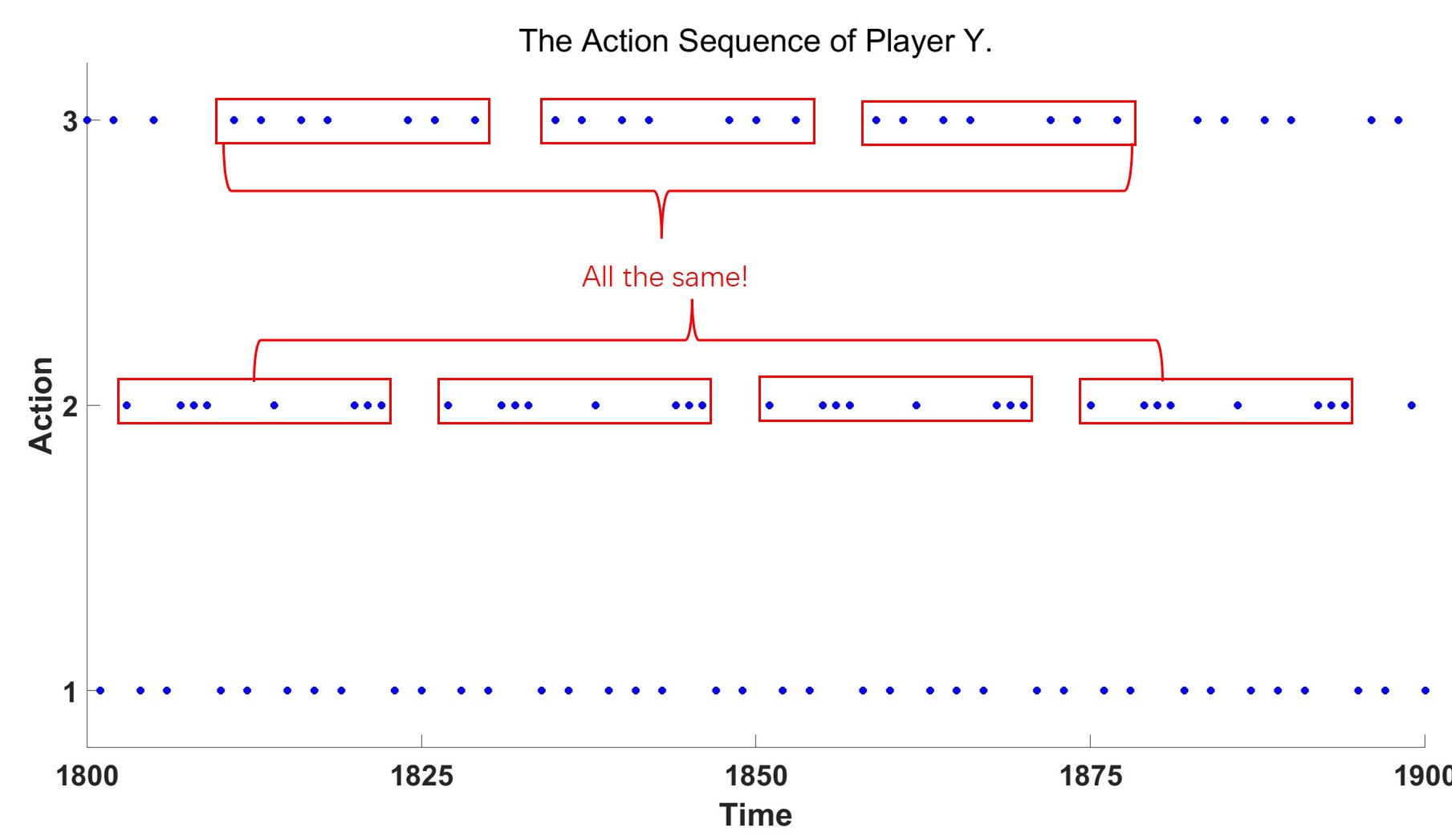

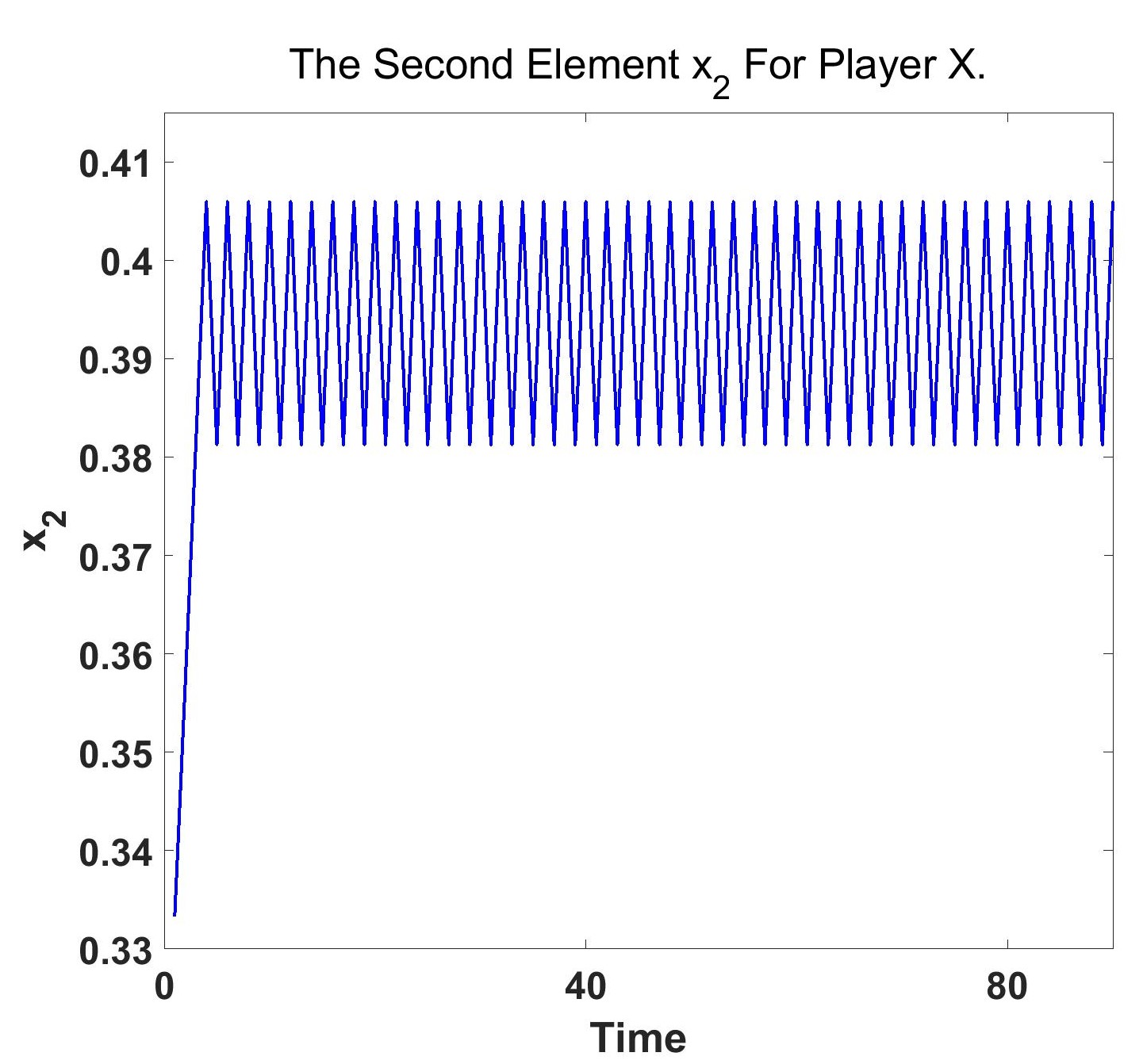

in which there is an irrational number . For this game, in the Hedge-myopic system, the action sequence is shown by Figure 3(a). We only present the part that lies between stage 1800 and 1900.

For comparison, we also show the action sequence for the game in Example 3.1 by Figure 3(b). Comparing these two figures, we can observe that the action sequence is periodic when the elements of payoff matrix are all rational numbers, while the action sequence is not periodic when there are irrational numbers in the elements of payoff matrix.

In the Hedge-myopic system, since player Y can only take pure strategies, the averaged strategy has only rational elements, so it is impossible for the averaged strategy to be a NE strategy when there are irrational numbers in the NE strategy. This explains why the periodicity no longer holds.

Below we present Example 3.3 and Example 3.4 to illustrate that when the game does not admit interior equilibrium, the periodicity of system dynamics also no longer holds, and periodicity only exists in special games.

Example 3.3 (No interior equilibrium and no cycle).

Consider a zero-sum game and let the payoff matrix of player Y be

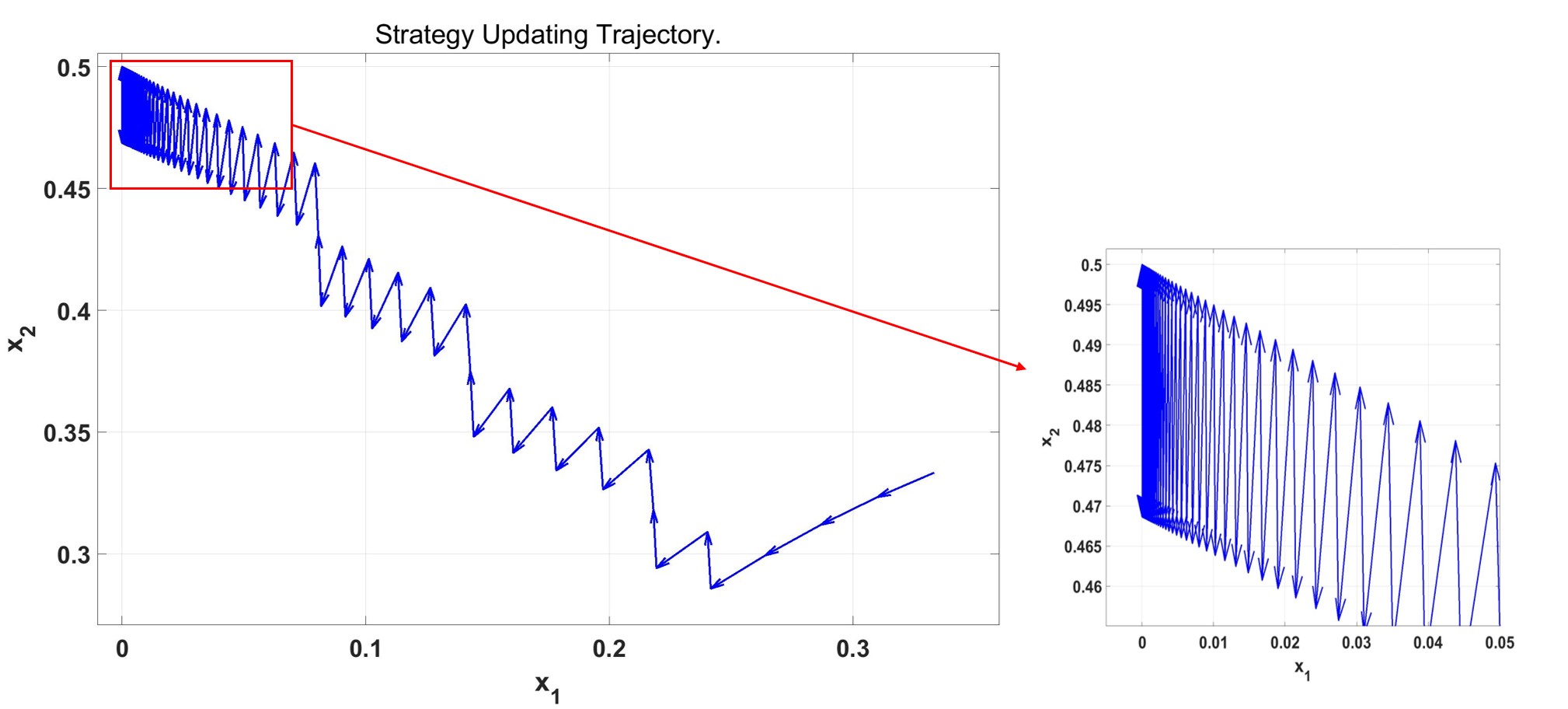

The NE strategy for player X is , which is non-interior, and the equilibrium strategy for player Y is not unique. The evolving path of is shown by Figure 4, from which we can see that the first element continually decreases and the repeated game does not enter a cycle.

Example 3.4 (No interior equilibrium but with a special cycle).

Generally, for all the two-player games, we can approximate the NE no matter whether the Hedge-myopic system enters a cycle or not. We state it in Theorem 3.4 below, whose proof can also be found in [23].

Theorem 3.4.

In a repeated two-player zero-sum game with stages, suppose player X employs the Hedge algorithm to update his stage strategy with parameter set to be , where is the number of his feasible actions, and suppose player Y takes the myopic best response to the stage strategy of player X, then the time-averaged strategy profile converges to the NE.

Proof.

By Theorem 2.1, we know that the upper regret bound for the Hedge algorithm with is . Then, we have

where . Thus, for all ,

| (14) |

4 A Novel NE-solving Algorithm and Experiments

4.1 HBR: an Asymmetric Equilibrium-solving Paradigm

Based on Theorem 3.3 and Theorem 3.4, we can propose an asymmetric Nash-equilibrium solving paradigm for two-player zero-sum games. Given the time horizon and the payoff matrix , let one player employ the Hedge algorithm to update his stage strategy, and let the other player know all the information and take the myopic best response. The paradigm is called the HBR paradigm in which H stands for the Hedge algorithm of one player and BR stands for the best response of the other player.

As we know from Theorem 3.3, we can compute exact NE fast if there is a cycle. So we exert additional efforts to identify whether the strategy sequences enter a cycle. If a cycle is detected, the computation can be terminated, and by Theorem 3.3, an exact NE strategy for the player using the myopic best response can be obtained. If the strategy sequences never enter a cycle, we can output the time-averaged strategy over the entire time horizon. By Theorem 3.4, this converges to an approximate NE as the time horizon T increases. By exchanging the updating rules of the players, an exact or approximate NE for the other player can also be obtained.

So how can we identify a cycle? This can be done through . To be specific, we can record all values of , and once , then the strategy sequence forms a cycle. By the proof of Lemma 3.3 and (3), the vector is the other object to detect, where the operator means subtracting each element of a vector by its -th element. Then it can be observed that the detection of a cycle implies that player Y has an interior equilibrium strategy.

The pseudocode for this paradigm is shown in Algorithm 1.

4.2 Experimental Results

We conduct several experiments to show the effectiveness of the HBR paradigm. First, we consider the game whose payoff matrix is set to be

The equilibrium of this game is an interior equilibrium, which is . An existing NE solving paradigm via learning is by the self-play of no-regret algorithm, such as Hedge, abbreviated to HSP. Now, we compare the performance of HBR and HSP paradigm.

-

(1).

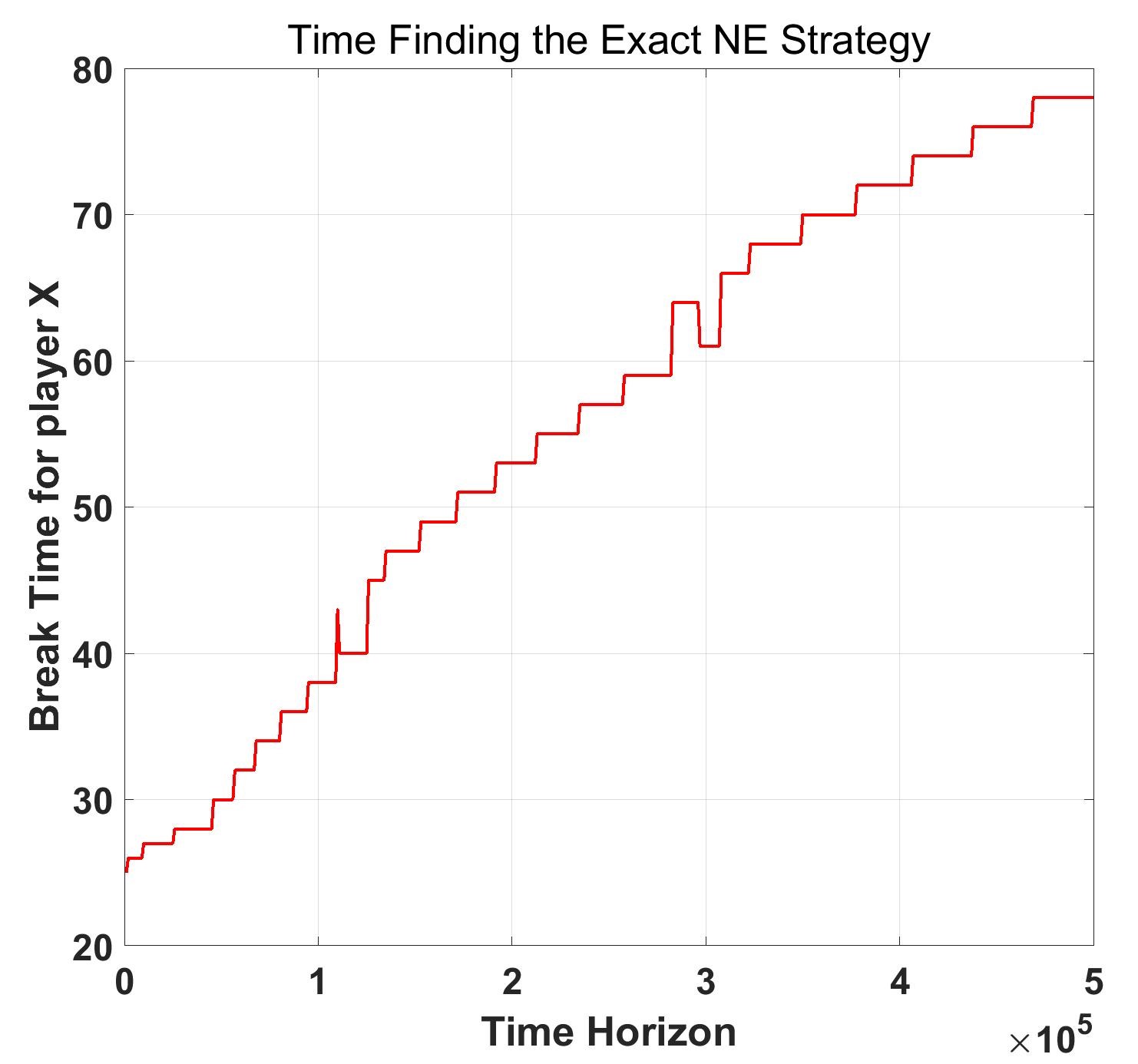

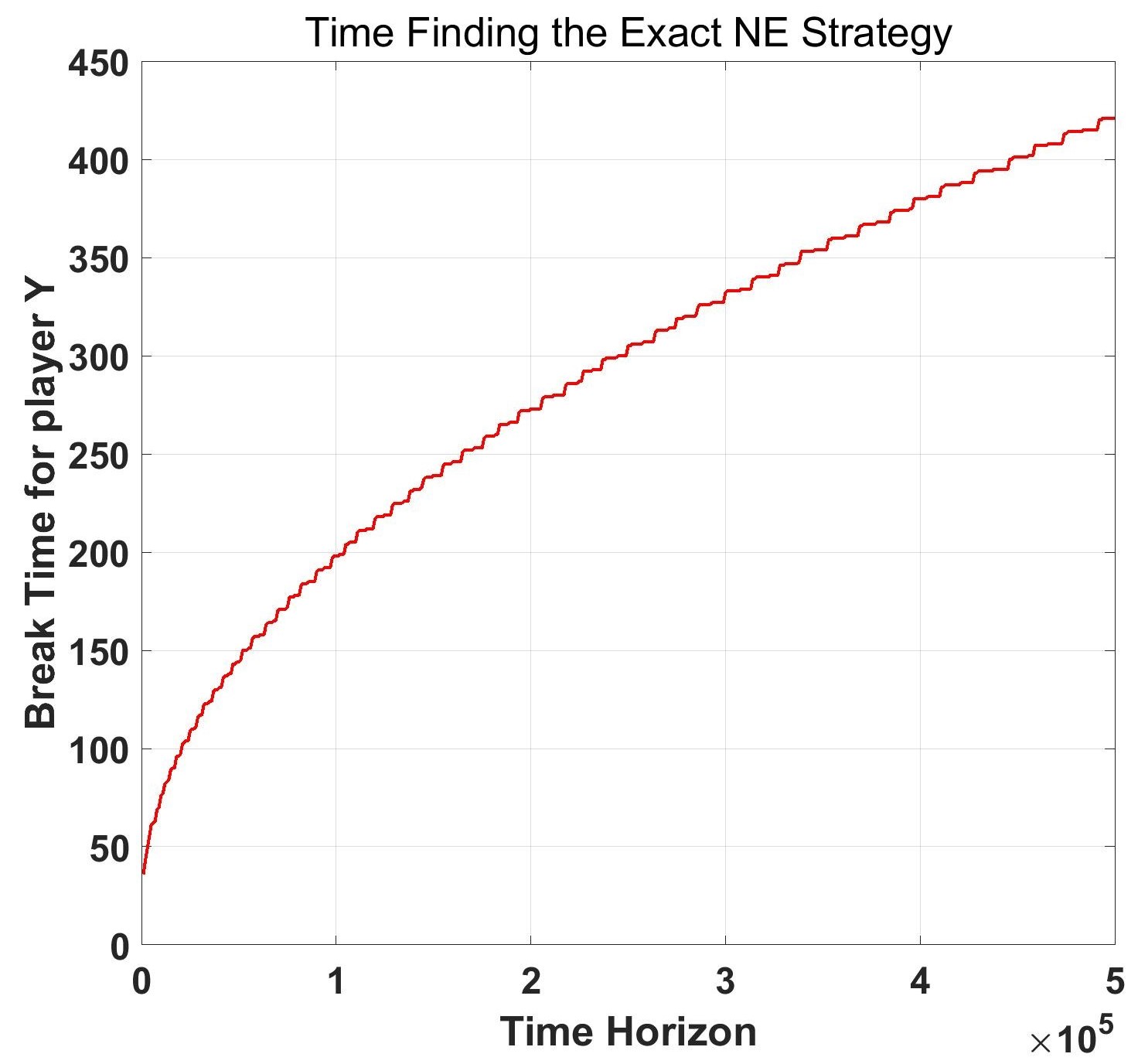

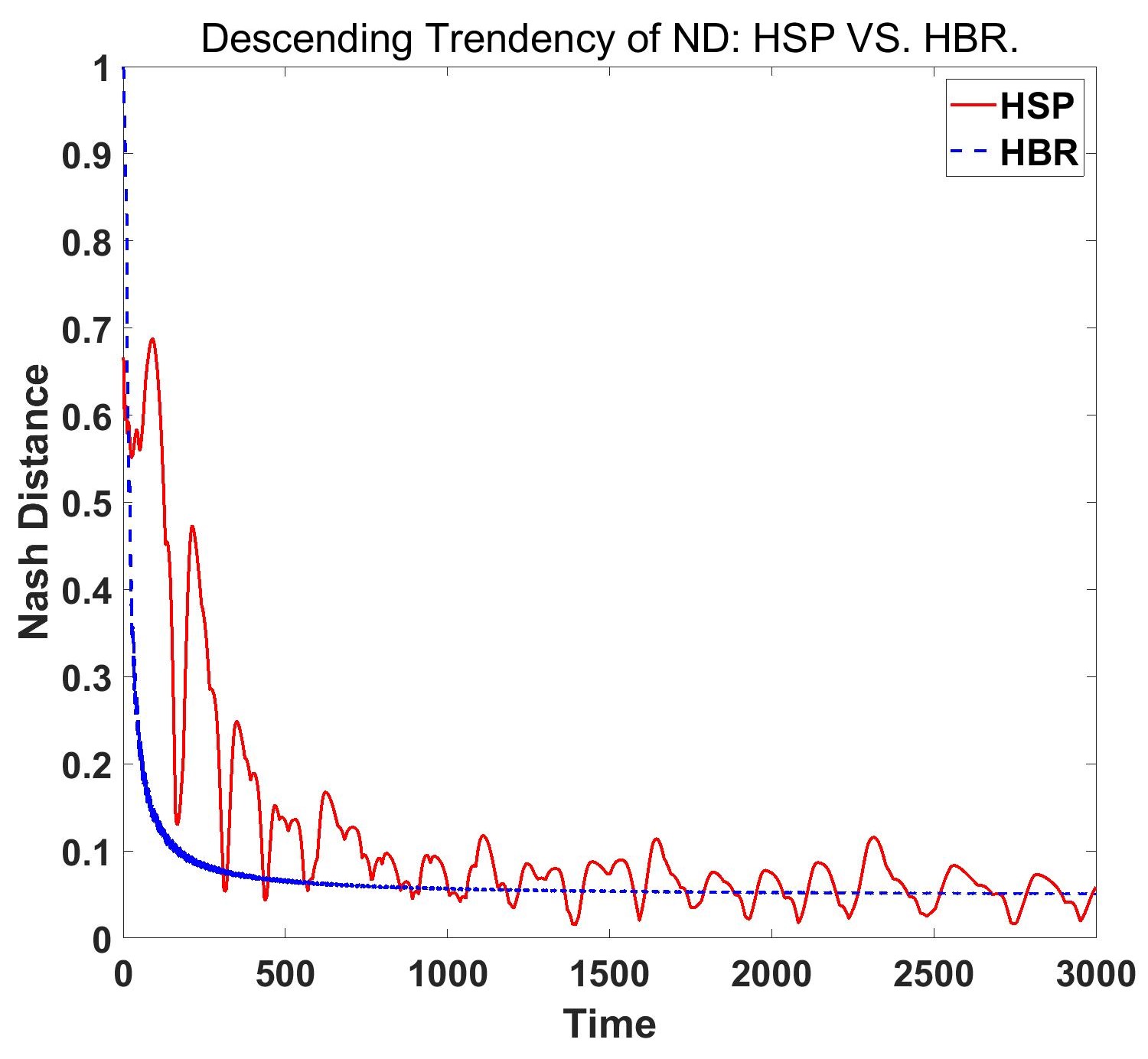

For different time horizons , let . Figure 6 gives the time needed to get the NE for player X and Y by the HBR paradigm. From Figure 6, we can see that the HBR paradigm actually enters a cycle very quickly. For this special game, time needed to calculate the NE strategy for player X and Y is different. Basically, needed steps to enter a cycle increases with .

For example, when , calculating the NE strategy for player Y terminates prematurely at time , while calculating the NE strategy for player X terminates prematurely at time . Basically, we can save a substantial amount of computation.

Why is the termination time so different for player X and Y? The reason lies in their NE strategies. For player X, it is , while for player Y, it is , which is more balanced among the elements. It is natural that it needs shorter time to enter a cycle corresponding to .

-

(2).

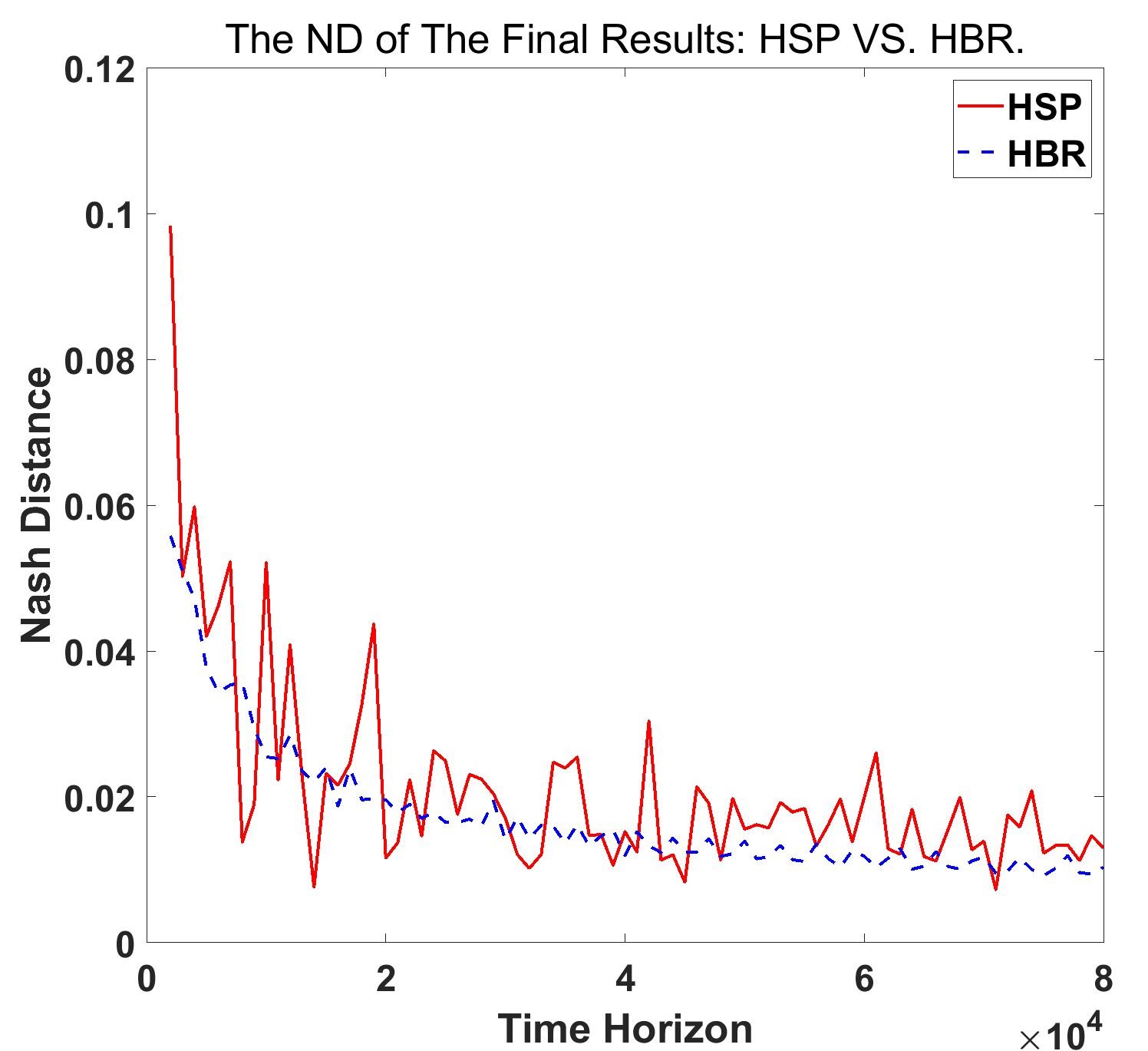

For different time horizons , let . We calculate the of the time-averaged strategy profile and the results are in Figure 7(a). This figure illustrates that, 1) as increases, the of the time-averaged strategy profile obtained by HBR roughly decreases, indicating that the calculated results approach the NE more closely; 2) compared to HSP, the volatility of the performance of HBR is lower.

We set and present the of the time-averaged strategy at each time in Figure 7(b). We can see that compared to HSP, the ND of the averaged strategy of HBR decreases faster and fluctuates lighter once it stabilizes.

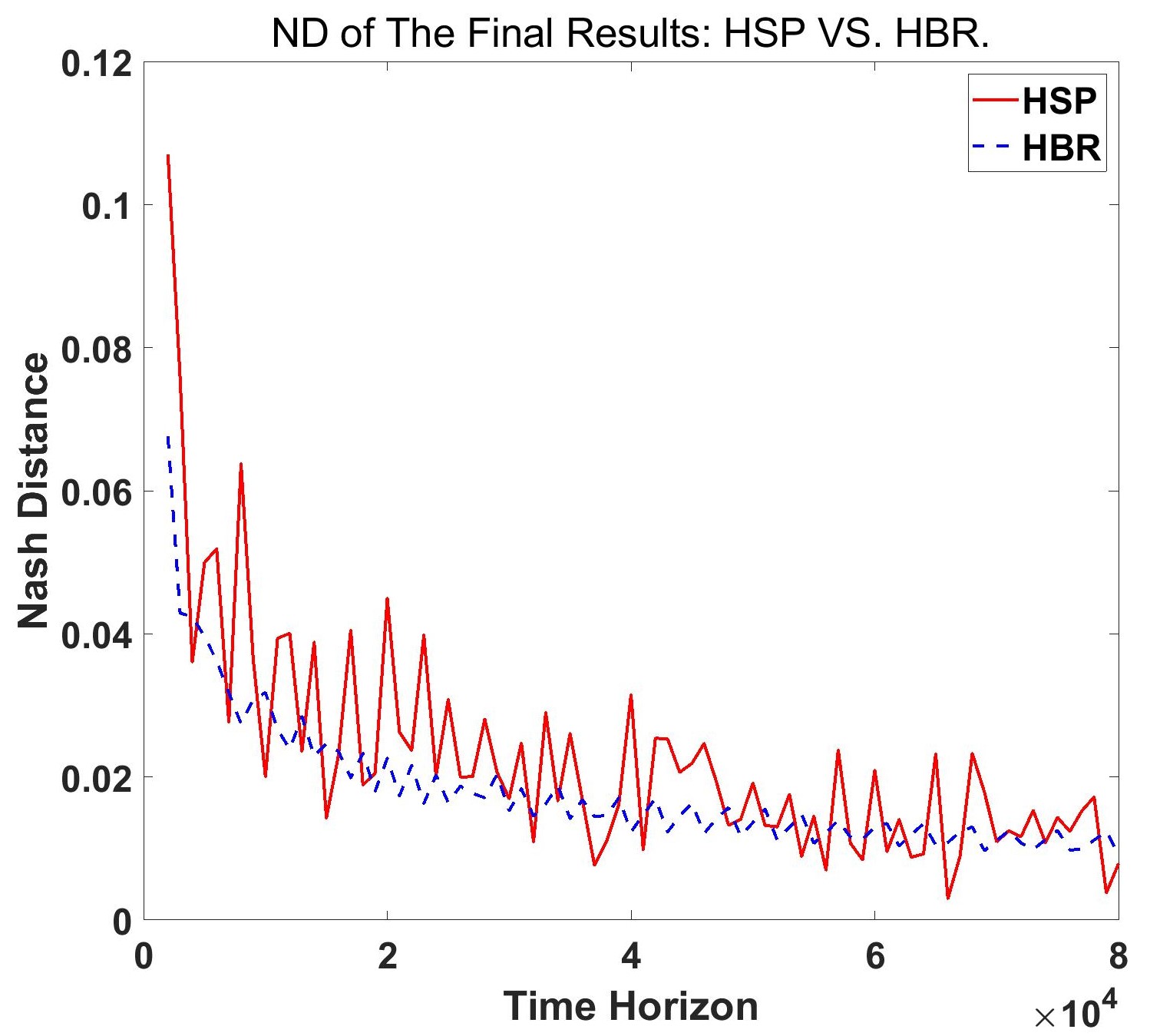

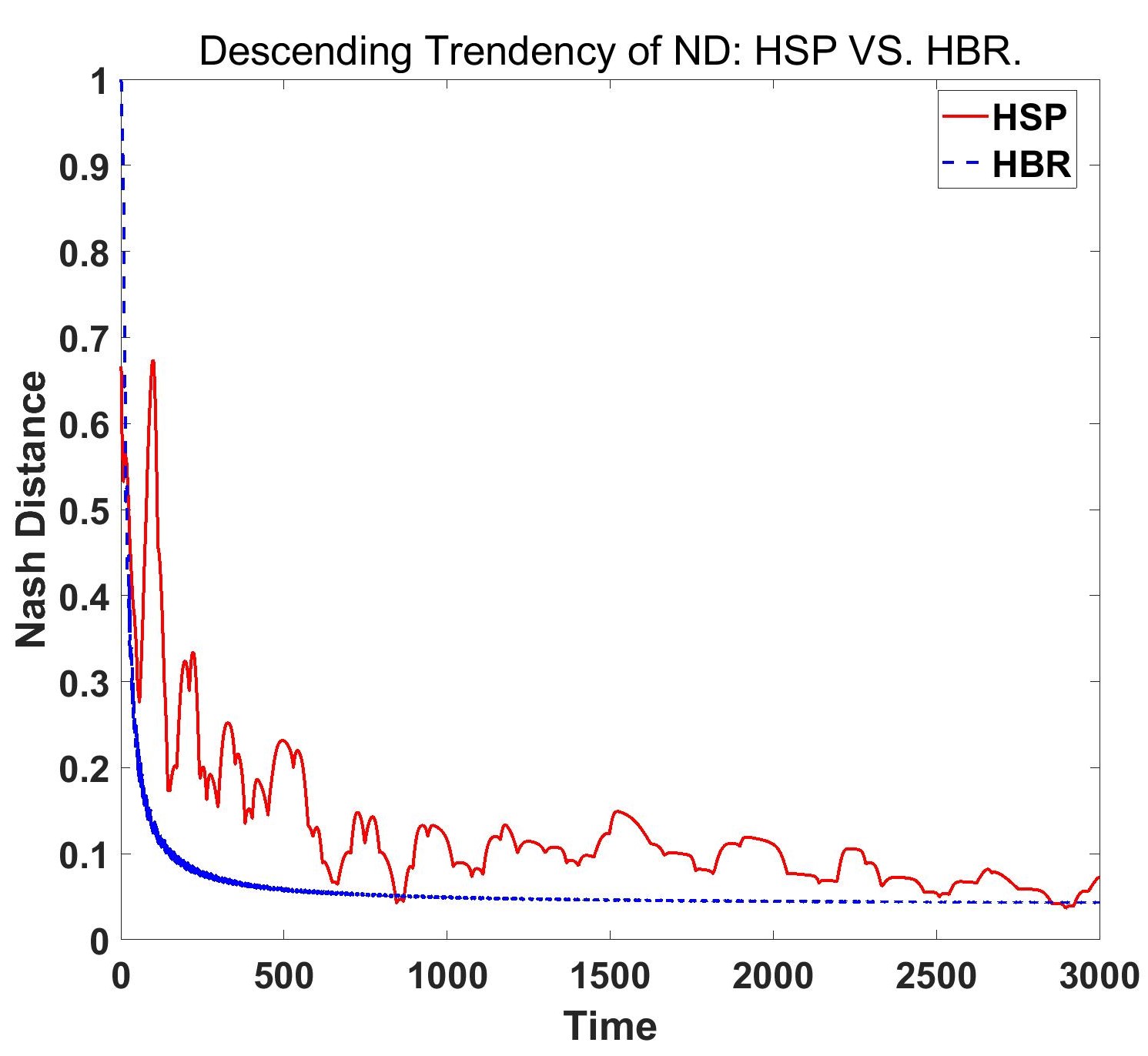

Furthermore, we consider another game matrix

whose equilibrium is not rational interior. The of the time-averaged strategy profile and the convergence rate are shown in Figure 8(a) and 8(b) respectively. In this case, the HBR paradigm still performs better than HSP in the perspective of stability and convergence rate.

5 Conclusion and Future Work

In this paper, we study the repeated game between one player using the Hedge algorithm and the other using the myopic best response. We prove that within this framework, when the payoff matrix is rational and the game has an interior NE, the dynamical game system enters a cycle after finite time. Moreover, within each period, the time-averaged strategy of the player using the myopic best response is an exact NE strategy. For the game with no cycle, the time-averaged strategy over the entire time horizon converges to the approximate NE. Based on these results, we propose the novel asymmetric HBR paradigm for NE-solving, which can save a substantial amount of computation costs and exhibit fast convergence rate and better stability.

In the future, we can explore the Hedge-myopic system for general games which have complex structures of NE. On the other hand, the periodicity of the Hedge-myopic system actually rules out the possibility of stage strategies converging to NE. Therefore, it is significant to consider how to modify the HBR paradigm so that the stage strategy can converge to NE strategy, i.e., the last-iterate property. We leave this also as future work.

6 Acknowledgement

This work was supported by the National Key Research and Development Program of China under grant No.2022YFA1004600, the Natural Science Foundation of China under Grant T2293770, the Major Project on New Generation of Artificial Intelligence from the Ministry of Science and Technology (MOST) of China under Grant No. 2018AAA0101002, the Strategic Priority Research Program of Chinese Academy of Sciences under Grant No. XDA27000000.

References

- Arora et al. [2012] Sanjeev Arora, Elad Hazan, and Satyen Kale. The multiplicative weights update method: a meta-algorithm and applications. Theory of computing, 8(1):121–164, 2012.

- Bailey and Piliouras [2018] James P Bailey and Georgios Piliouras. Multiplicative weights update in zero-sum games. In Proceedings of the 2018 ACM Conference on Economics and Computation, pages 321–338, 2018.

- Bertsimas and Tsitsiklis [1997] Dimitris Bertsimas and John N Tsitsiklis. Introduction to linear optimization, volume 6. Athena scientific Belmont, MA, 1997.

- Brown and Sandholm [2018] Noam Brown and Tuomas Sandholm. Superhuman ai for heads-up no-limit poker: Libratus beats top professionals. Science, 359(6374):418–424, 2018.

- Brown and Sandholm [2019] Noam Brown and Tuomas Sandholm. Solving imperfect-information games via discounted regret minimization. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 1829–1836, 2019.

- Brown et al. [2019] Noam Brown, Adam Lerer, Sam Gross, and Tuomas Sandholm. Deep counterfactual regret minimization. In International conference on machine learning, pages 793–802. PMLR, 2019.

- Candogan et al. [2013] Ozan Candogan, Asuman Ozdaglar, and Pablo A Parrilo. Dynamics in near-potential games. Games and Economic Behavior, 82:66–90, 2013.

- Cesa-Bianchi and Lugosi [2006] Nicolo Cesa-Bianchi and Gábor Lugosi. Prediction, learning, and games. Cambridge university press, 2006.

- Cesa-Bianchi et al. [1997] Nicolo Cesa-Bianchi, Yoav Freund, David Haussler, David P Helmbold, Robert E Schapire, and Manfred K Warmuth. How to use expert advice. Journal of the ACM (JACM), 44(3):427–485, 1997.

- Chen and Deng [2006] Xi Chen and Xiaotie Deng. Settling the complexity of two-player nash equilibrium. In FOCS, volume 6, pages 261–272, 2006.

- Daskalakis et al. [2009] Constantinos Daskalakis, Paul W Goldberg, and Christos H Papadimitriou. The complexity of computing a nash equilibrium. Communications of the ACM, 52(2):89–97, 2009.

- Daskalakis et al. [2011] Constantinos Daskalakis, Alan Deckelbaum, and Anthony Kim. Near-optimal no-regret algorithms for zero-sum games. In Proceedings of the twenty-second annual ACM-SIAM symposium on Discrete Algorithms, pages 235–254. SIAM, 2011.

- Freund and Schapire [1997] Yoav Freund and Robert E Schapire. A decision-theoretic generalization of on-line learning and an application to boosting. Journal of computer and system sciences, 55(1):119–139, 1997.

- Fudenberg and Levine [1998] Drew Fudenberg and David K Levine. The theory of learning in games, volume 2. MIT press, 1998.

- Fudenberg and Tirole [1991] Drew Fudenberg and Jean Tirole. Game theory. MIT press, 1991.

- Guo and Mu [2023a] Xinxiang Guo and Yifen Mu. The optimal strategy against hedge algorithm in repeated games. arXiv preprint arXiv:2312.09472, 2023a.

- Guo and Mu [2023b] Xinxiang Guo and Yifen Mu. Taking myopic best response against the hedge algorithm. In 2023 42nd Chinese Control Conference (CCC), pages 8154–8158. IEEE, 2023b.

- Hart and Mas-Colell [2000] Sergiu Hart and Andreu Mas-Colell. A simple adaptive procedure leading to correlated equilibrium. Econometrica, 68(5):1127–1150, 2000.

- Hofbauer [1996] Josef Hofbauer. Evolutionary dynamics for bimatrix games: A hamiltonian system? Journal of mathematical biology, 34:675–688, 1996.

- Jordan [1993] James S Jordan. Three problems in learning mixed-strategy nash equilibria. Games and Economic Behavior, 5(3):368–386, 1993.

- Karmarkar [1984] Narendra Karmarkar. A new polynomial-time algorithm for linear programming. In Proceedings of the sixteenth annual ACM symposium on Theory of computing, pages 302–311, 1984.

- Lanctot et al. [2009] Marc Lanctot, Kevin Waugh, Martin Zinkevich, and Michael Bowling. Monte carlo sampling for regret minimization in extensive games. Advances in neural information processing systems, 22, 2009.

- Li et al. [2023] Kai Li, Wenhan Huang, Chenchen Li, and Xiaotie Deng. Exploiting a no-regret opponent in repeated zero-sum games. J. Shanghai Jiatong Univ., June 2023.

- Littlestone and Warmuth [1994] Nick Littlestone and Manfred K Warmuth. The weighted majority algorithm. Information and computation, 108(2):212–261, 1994.

- Lockhart et al. [2019] Edward Lockhart, Marc Lanctot, Julien Pérolat, Jean-Baptiste Lespiau, Dustin Morrill, Finbarr Timbers, and Karl Tuyls. Computing approximate equilibria in sequential adversarial games by exploitability descent. arXiv preprint arXiv:1903.05614, 2019.

- Mertikopoulos et al. [2018] Panayotis Mertikopoulos, Christos Papadimitriou, and Georgios Piliouras. Cycles in adversarial regularized learning. In Proceedings of the twenty-ninth annual ACM-SIAM symposium on discrete algorithms, pages 2703–2717. SIAM, 2018.

- Miyasawa [1961] Koichi Miyasawa. On the convergence of the learning process in a 2 x 2 non-zero-sum two-person game. Princeton University Princeton, 1961.

- Monderer and Shapley [1996] Dov Monderer and Lloyd S Shapley. Fictitious play property for games with identical interests. J. Econ. Theory, 68:258–265, January 1996.

- Moravčík et al. [2017] Matej Moravčík, Martin Schmid, Neil Burch, Viliam Lisỳ, Dustin Morrill, Nolan Bard, Trevor Davis, Kevin Waugh, Michael Johanson, and Michael Bowling. Deepstack: Expert-level artificial intelligence in heads-up no-limit poker. Science, 356(6337):508–513, 2017.

- Narahari [2014] Yadati Narahari. Game theory and mechanism design, volume 4. World Scientific, 2014.

- Nash [1950] John F. Nash. Equilibrium points in n-person games. Proceedings of the national academy of sciences, 36(1):48–49, 1950.

- Nash [1951] John F. Nash. Non-cooperative games. Annals of mathematics, 54(2):286–295, 1951.

- Osborne and Rubinstein [1994] Martin J Osborne and Ariel Rubinstein. A course in game theory. MIT press, 1994.

- Palaiopanos et al. [2017] Gerasimos Palaiopanos, Ioannis Panageas, and Georgios Piliouras. Multiplicative weights update with constant step-size in congestion games: Convergence, limit cycles and chaos. Advances in Neural Information Processing Systems, 30, 2017.

- Papadimitriou and Piliouras [2016] Christos Papadimitriou and Georgios Piliouras. From nash equilibria to chain recurrent sets: Solution concepts and topology. In Proceedings of the 2016 ACM Conference on Innovations in Theoretical Computer Science, pages 227–235, 2016.

- Papadimitriou [1994] Christos H Papadimitriou. On the complexity of the parity argument and other inefficient proofs of existence. Journal of Computer and system Sciences, 48(3):498–532, 1994.

- Perolat et al. [2021] Julien Perolat, Remi Munos, Jean-Baptiste Lespiau, Shayegan Omidshafiei, Mark Rowland, Pedro Ortega, Neil Burch, Thomas Anthony, David Balduzzi, Bart De Vylder, et al. From poincaré recurrence to convergence in imperfect information games: Finding equilibrium via regularization. In International Conference on Machine Learning, pages 8525–8535. PMLR, 2021.

- Perolat et al. [2022] Julien Perolat, Bart De Vylder, Daniel Hennes, Eugene Tarassov, Florian Strub, Vincent de Boer, Paul Muller, Jerome T Connor, Neil Burch, Thomas Anthony, et al. Mastering the game of stratego with model-free multiagent reinforcement learning. Science, 378(6623):990–996, 2022.

- Piliouras and Shamma [2014] Georgios Piliouras and Jeff S Shamma. Optimization despite chaos: Convex relaxations to complex limit sets via poincaré recurrence. In Proceedings of the twenty-fifth annual ACM-SIAM symposium on Discrete algorithms, pages 861–873. SIAM, 2014.

- Piliouras et al. [2014] Georgios Piliouras, Carlos Nieto-Granda, Henrik I Christensen, and Jeff S Shamma. Persistent patterns: multi-agent learning beyond equilibrium and utility. In AAMAS, pages 181–188, 2014.

- Robinson [1951] Julia Robinson. An iterative method of solving a game. Annals of mathematics, pages 296–301, 1951.

- Sato et al. [2002] Yuzuru Sato, Eizo Akiyama, and J Doyne Farmer. Chaos in learning a simple two-person game. Proceedings of the National Academy of Sciences, 99(7):4748–4751, 2002.

- Sayin et al. [2022] Muhammed O Sayin, Francesca Parise, and Asuman Ozdaglar. Fictitious play in zero-sum stochastic games. SIAM Journal on Control and Optimization, 60(4):2095–2114, 2022.

- Shapley [1964] Lloyd Shapley. Some topics in two-person games. Advances in game theory, 52:1–29, 1964.

- van den Brand [2020] Jan van den Brand. A deterministic linear program solver in current matrix multiplication time. In Proceedings of the Fourteenth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 259–278. SIAM, 2020.

- Von Neumann and Morgenstern [2007] John Von Neumann and Oskar Morgenstern. Theory of games and economic behavior (60th Anniversary Commemorative Edition). Princeton university press, 2007.

- Zinkevich et al. [2007] Martin Zinkevich, Michael Johanson, Michael Bowling, and Carmelo Piccione. Regret minimization in games with incomplete information. Advances in neural information processing systems, 20, 2007.

Appendix A Proof of Proposition 3.1

Proof.

First, we claim that there does not exist such that the payoffs obtained by the pure strategies of player Y are all greater than the game value , i.e., for all , we have

If not, suppose that for , for all . Then, for the NE strategy of player Y, since the equilibrium is interior, to play with of player Y, the loss of player X will be the same (which actually equals ) no matter which pure strategy is taken by player X. Then we have

which leads to contradiction.

Next, we investigate the vertices of the region .

Note that the point corresponding to the NE strategy of player X is the unique solution of the systems of linear equations: , where the coefficient matrix is

| (17) |

and , whose first components are and the -th component is .

Now, consider the equation system , where , whose first components are and the -th component is . By Assumption 2, is non-singular, the equation system admits an unique solution, denoted by .

Firstly, we prove that belongs to the region and is a vertex of . Since the strategy is the solution to the linear equation system , i.e., , thus for . By the arguments at the beginning of this proof, we have . Combining these equations and inequality, we have , where b is the vector defined in Claim 2. That proves . On the other hand, by the equations, lies on the facets of the polyhedron , thus is a vertex of .

Secondly, we prove that is an interior strategy for all . Since is the solution of the linear equation system , it follows that and thus,

where . is finite since is non-singular for all . Since is an interior strategy and is small enough, we know that for any , is also an interior point, i.e., , s.t.

Lastly, let By Lemma 3.2, for all , there exists , satisfying and , such that . Then, for all , we have

which completes the proof. ∎

Appendix B Proof of Theorem 3.2

Proof.

First, define the set

| (18) |

For , denote the index such that to be . The index might not be unique, but it does not affect the following discussion.

Note that for , has a lower bound since

where the first inequality holds because for all .

By Lemma 3.1, we know that the Q-sequence is bounded, i.e., for all . By the definition of , given , there must exist such that for all and .

Recall the formula (7) saying For , let and let . Then, the formula (3) can be written as

| (19) |

implying that for a given vector , only one strategy can be obtained. Denote the mapping from to by . Since for all and , the range of the mapping is .

Now consider the inverse mapping of , i.e.,

By the equation (19), we have

| (20) |

For , we also have

| (21) |

since the game is zero-sum and is the NE strategy of player X. Combining the equation (20) and (21), we obtain that

| (22) |

which means that for a given vector , only one regret vector can be obtained.

Note that for all , we have for all and . Hence, we have

for all and , which means that the possible values of in the Hedge-myopic system are in the range

On the other hand, by the definition, , in which refers to one of the elements of the matrix , and is the game value, which is a fixed rational number. Hence, is also rational and can only take values that are integer multiples of a fraction, rather than being able to take all rational numbers. Combing with the boundness of , we can infer that can only take finite possible values. This implies that can only take finite values and thus can only take finite values, which completes the proof. ∎

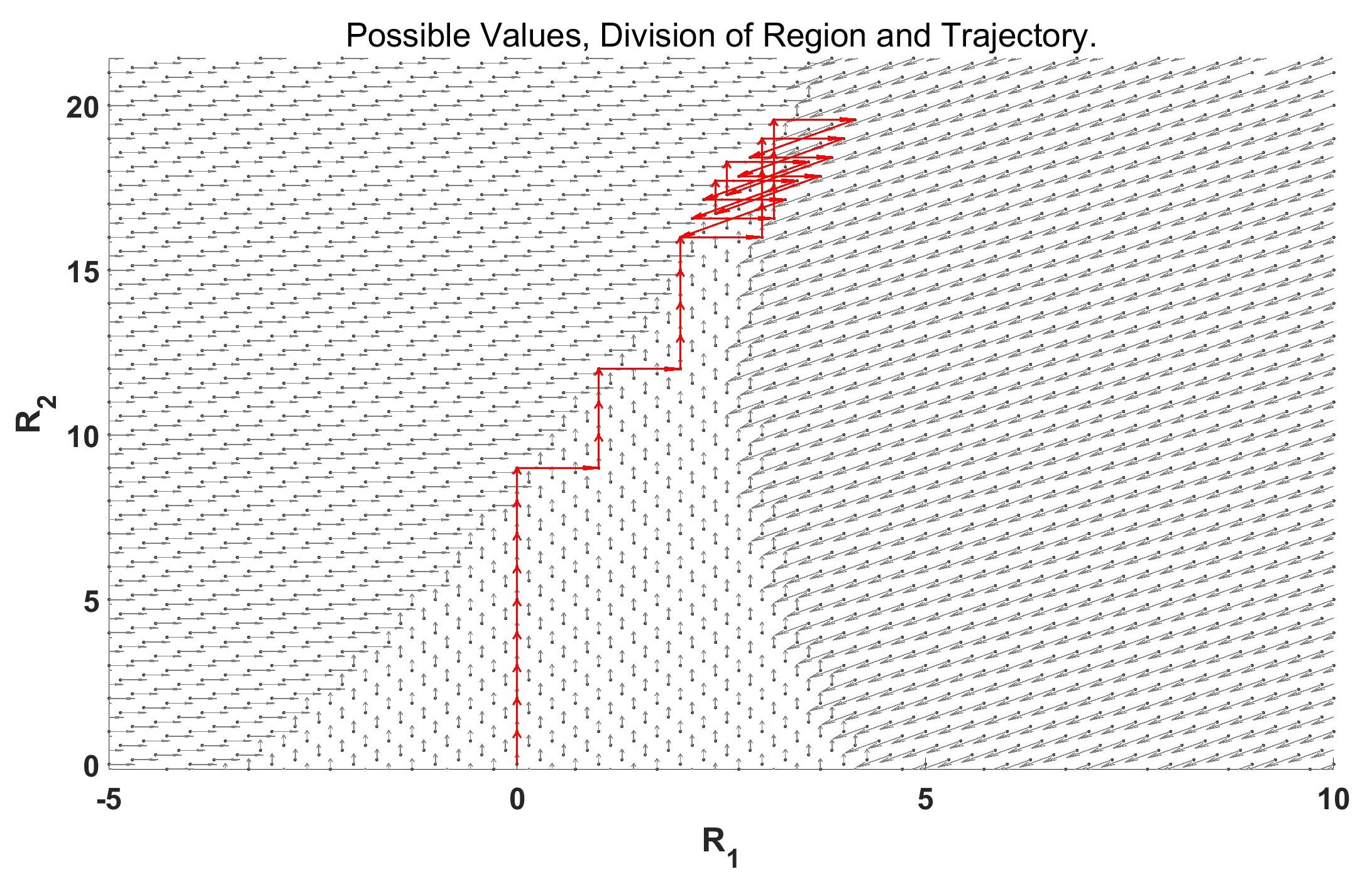

The evolutionary direction of in the Hedge-myopic system for a special game(Example 3.1) is shown in Figure 9. In this figure, each point represents a possible value of , and has an arrow pointing to another point, indicating the best response action of player Y when player X adopts the strategy corresponding to that point. The entire range of possible values for is divided into three regions: below, left, and upper right. In each region, the update direction of is opposite to the relative location of that region. For example, the points in the lower region point upwards. The red line represents the actual evolutionary path of the Hedge-myopic system.

Appendix C Proof of Lemma 3.3

Proof.

By the updating rule of , we know that is fully determined by the value of . Thus, it is natural that if the sequence is periodic, then the corresponding sequence of is also periodic.

Suppose for some , By the formula (3), each element of is strictly positive, i.e., . Then, for , we have

Since the game admits an unique rational interior equilibrium, the above equations implies that is the NE strategy of player Y, i.e. . ∎