Empirical business cycle studies using cross-country data usually cannot achieve causal relationships while within-country studies mostly focus on the bust period. We provide the first causal investigation into the boom period of the 1999-2010 U.S. cross-metropolitan business cycle. Using a novel research design, we show that credit expansion in private-label mortgages causes a differentially stronger boom (2000-2006) and bust (2007-2010) cycle in the house-related industries in the high net-export-growth areas. Most importantly, our unique research design enables us to perform the most comprehensive tests on theories (hypotheses) regarding the business cycle. We show that the following theories (hypotheses) cannot explain the cause of the 1999-2010 U.S. business cycle: the speculative euphoria hypothesis, the real business cycle theory, the collateral-driven credit cycle theory, the business uncertainty theory, and the extrapolative expectation theory.

Keywords: business cycle, financial crisis, credit supply, private-label mortgages

JEL Classification: E32, G01, G21

Testing Business Cycle Theories: Evidence

from the Great Recession

Empirical business cycle studies using cross-country data usually cannot achieve causal relationships while within-country studies mostly focus on the bust period. We provide the first causal investigation into the boom period of the 1999-2010 U.S. cross-metropolitan business cycle. Using a novel research design, we show that credit expansion in private-label mortgages causes a differentially stronger boom (2000-2006) and bust (2007-2010) cycle in the house-related industries in the high net-export-growth areas. Most importantly, our unique research design enables us to perform the most comprehensive tests on theories (hypotheses) regarding the business cycle. We show that the following theories (hypotheses) cannot explain the cause of the 1999-2010 U.S. business cycle: the speculative euphoria hypothesis, the real business cycle theory, the collateral-driven credit cycle theory, the business uncertainty theory, and the extrapolative expectation theory.

Keywords: business cycle, financial crisis, credit supply, private-label mortgages

JEL Classification: E32, G01, G21

tempdima tempdima “Crises do not occur randomly, and, as a result, an understanding of financial crises requires an investigation into the booms that precede them.”

– Amir Sufi and Alan M. Taylor, Financial Crises: A Survey, 2022

1 Introduction

Finding the cause of the 1999-2010 U.S. business cycle is vital because the U.S. ended up with the deepest recession since the Great Depression in the 1930s. In the bust period, the U.S. economy experienced widespread mortgage defaults (Mayer, Pence, and Sherlund, 2009; Keys, Mukherjee, Seru, and Vig, 2010), massive failures in the banking industry (Bernanke, 2023), large consumption drop (Mian, Rao, and Sufi, 2013; Kaplan, Mitman, and Violante, 2020), and huge unemployment rise (Hoynes, Miller, and Schaller, 2012; Mian and Sufi, 2014). Identifying the cause and its major mechanisms is crucial for understanding of the economic connections among credit, housing, banking, and employment. It is also helpful for the design of regulatory frameworks and macroeconomic policies that monitor the economy, avoid a similar recession, and intervene in an early stage to heal the whole economy.

In the literature, there are multiple theories (hypotheses) trying to explain the business cycle. Prevalent hypotheses include speculative euphoria hypothesis (Kindleberger, 1978; Minsky, 1986), real business cycle theory (Prescott, 1986), the collateral-driven credit cycle theory (Kiyotaki and Moore, 1997), the business uncertainty theory (Bloom, 2009), extrapolative expectation theory (Eusepi and Preston, 2011), and credit-drive household demand hypothesis (Mian and Sufi, 2009; Schularick and Taylor, 2012). Each theory (hypothesis) has found some pieces of supporting evidence. So far, however, we have not gathered enough micro-style causal evidence to distinguish which theory (hypothesis) captures the major origin of the business cycle. The empirical difficulties are twofold. First, cross-country empirical studies usually only achieve correlation because of large endogenous differences in economic development, institutions, and culture. Second, within-country studies mostly focus on the bust periods without digging into the boom period, partially because of the difficulty in finding long-term incentives that have persistent geographic divergence that potentially causes the divergence in credit expansion. Prevalent theories and ample empirical evidence, however, support geographic convergence within a country (Kim and Margo, 2004).

To preview, by combining insights from regional economics and international economics, we design a causal framework to locate the long-term incentive for credit that has persistent geographic divergence. Our research design enables us to find ample micro-style causal evidence for the “credit-driven housing-dominant view”. Specifically, induced by net export growth, credit expansion in private-label mortgages (non-jumbo) causes the 1999-2010 U.S. business cycle. This business cycle is much stronger in the high net-export-growth areas and housing-related industries experienced an amplified boom and bust cycle (“housing industry channel”). Most importantly, our unique research design empowers us to conduct the most comprehensive tests on the relevance of prevalent theories (hypotheses) regarding business cycles. We find that other hypotheses cannot explain the origin of this business cycle. We will describe our research design, then major findings, and lastly, our contribution.

Research Design Empirical studies of the business cycle by cross-country data face several challenges in identifying the cause and its primary channel. First, credit supply and household demand can be driven endogenously by institutional differences. For example, countries with higher prior economic growth, better legal protection of creditors, and a stronger regulatory system against financial fraud could have higher household demand that attracts international credit. Alternatively, these countries could attract more international funds that reduce interest rates and induce higher household demand. Second, we need to achieve a consistent measure of household debt so that such a measure can be comparable in the cross-section. For the largest part of household debt, mortgages (around 70% in the US), the average maturity is around 45 years in Sweden, 30 years in the USA, and 15 years in Germany (Bernstein and Koudijs, 2021). This fact means the same debt-to-income ratio due to the same amount of mortgage means relatively higher payback pressure for households in Germany but much lower payback pressure for households in Sweden. In a similar way, differences in the availability and level of social welfare programs also present difficulties in achieving a consistent measure of household leverage across countries. The above two difficulties prevent many empirical studies from accomplishing causal evidence by cross-country study (e.g., Mian, Sufi, and Verner (2017); Müller and Verner (2023)).

Within-country studies also face several challenges, though they can avoid the above difficulties faced by cross-country studies. First, any identification strategy requires cross-section differences in credit expansion, which in turn needs the treatment variable to capture the incentives to the credit supply.111To be precise, the ‘treatment variable’ here can refer to the instrumental variable in an IV strategy, the running variable in a regression discontinuity design, and the treatment variable in a difference-in-difference design. For example, Di Maggio and Kermani (2017) uses the interaction between anti-predatory lending laws and 2004 OCC preemption as the treatment variable in a difference-in-difference setting. This requirement means the treatment variable must have enough area coverage (US mainland), geographic variation, and time coverage (99-10). Second, the geographic variation must persist over the business boom period (1999-2005) since the credit supply expansion (in corporate debt or in home mortgages) is a long-term financial decision. In other words, the treatment variable must provide persistent incentives to induce stronger credit expansion in certain areas or certain industries than others throughout the entire boom period. Short-run shocks, such as weather (e.g., rain, extreme temperature, and wildfires), are inadequate. Third, beyond variable nature, shocks to the treatment variable are required to constitute a solid identification strategy. Fourth, the underlying economic theory (or story) shall explain why the treatment variable (incentive) can induce stronger credit expansion in the boom period rather than in other periods (such as the prior period). Such a theory (or story) requires a large framework consist of the incentives of different types of participants, the mortgage market structure, and the time-varying nature of them.

Our within-US research design addresses the above challenges in three parts. In the first part, we operationalize the key idea of “economic base theory” (Tiebout, 1962) and construct a treatment variable that captures the long-term incentive of credit expansion: metropolitan exposure to net export growth of manufacturing industries. The “economic base” (tradable sector) refers to the economic activities that a local area provides for the areas outside, thus bringing wealth to the local area. Most of the wealth will be reused locally via a money multiplier effect. By this theory, the tradable sector growth is the key driving force for local economic growth in the long term. Therefore, credit expansion in mortgages would be stronger in areas with stronger growth in tradable sector due to higher residual value of a mortgage given default.222Please see the model by Li (2024) for more details. Ideal measurement of the composite and growth of table sector requires census-style data consisting of the accounting data of all firms, which is unavailable in reality. Alternativly, following Li (2024), we proxy the composite (share) with manufacturing employment data at the industry-by-metropolitan level. In addition, we employ the substantial time series change (shift) in net export growth in the U.S. as a proxy for the relative growth at the industry level. Aggregating these two proxies (shift and share) can give us a good measure of the relative growth of the local tradable sector across metropolitan areas. By this construction, net export growth has enough area coverage (U.S. mainland) and enough time coverage (92-09). In addition, its geographic variation comes from the fact that the related manufacturing industries tend to cluster in just a few locations. Further, the persistence feature of net export growth comes from two dimensions. At the industry level, both increasing return to scales at the industry level and comparative advantages across nations make trade patterns persistent over time. At the individual level, job reallocation across different industries or locations is very costly.

In the second part, our research design employs the gravity model-based instrumental variable approach developed by Feenstra, Ma, and Xu (2019) as our identification strategy. Feenstra, Ma, and Xu (2019) develop their IVs from a general equilibrium model and their IVs can isolate the exogenous part of U.S. imports and exports. Conceptually, their IVs capture the exogenous parts of net export growth due to (1) increasing world demand reflected in US export growth, (2) increasing world supply reflected in US import growth, and (3) tariff changes. They also use high-dimensional fixed effects to remove the potentially endogenous parts: (1) US industry-by-year supply-side shocks in exports and (2) US industry-by-year demands-side shocks in imports, and (3) pre-determined bilateral distance between U.S. and partner countries. They construct IVs separately for exports and imports, and we combine them together as an IV for net export growth.

In the third part of our research design, we rely on the model by Li (2024) to explain (1) why our framework is consistent with the viewpoint that net export growth cannot induce credit expansion in the prior period (1991-1999) and (2) the intuition for the business cycle.

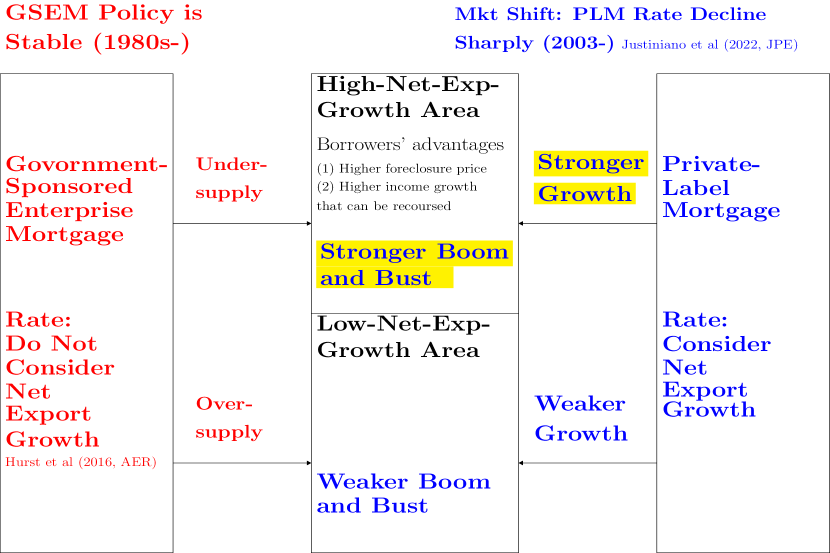

Intuition for the Business Cycle The basic intuition of the cross-metro differential business cycle story in this paper can be illustrated in the following Figure (1). Conceptually, U.S. metropolitan areas can be divided into high and low net-export growth areas. Higher net export growth leads to higher household income growth, higher employment growth, and higher population growth gradually in the high net-export-growth area than in the low net-export-growth area. These differences grant the mortgage borrowers in the high net-export-growth area two advantages: (1) higher foreclosure price of house given default 333In the empirical literature, there is ample evidence that household income growth, employment growth, and population growth (including migration) can push up housing demand and then housing price, especially in the long term (Olsen, 1987). and (2) higher income growth in the future that can be recoursed by lenders after default.

This paragraph explains why our framework is consistent with the viewpoint that net export growth cannot induce credit expansion in the prior period (1991-1999). A key legal requirement is that government-sponsored enterprise mortgages cannot consider regional economic conditions (growth) (Hurst, Keys, Seru, and Vavra, 2016) in setting up mortgage rates. But private-label mortgages can. Since securitization innovation (notably the Copula approach by Li (2000) (Salmon, 2012)), “global saving glut” (Bernanke, 2005; Bernanke et al., 2007), mortgage market deregulation (Di Maggio and Kermani, 2017; Lewis, 2023), and political push (Mian, Rao, and Sufi, 2013) all occurred after 1999, private-label mortgages maintained high mortgage rates between 1991 and 1999 and only had a small market share. On the contrary, government-sponsored enterprise mortgages dominated the mortgage market with low rates due to economies of scale and the government’s implicit guarantee.444Estimates show that the spread between government-sponsored enterprise mortgages and otherwise similar jumbo loans (purchased by private issuers) are, on average, between 15-40 basis points between 1996 and 2006 (see Sherlund (2008) and its summary of the literature). Therefore, Without aggregate credit expansion, even high net-export-growth areas cannot undergo a business cycle before 1999.

However, documented by Justiniano, Primiceri, and Tambalotti (2022), there is a huge credit expansion in the private-label mortgages that starts in 2003 summer.555Justiniano, Primiceri, and Tambalotti (2022) argues that this rate drop likely reflects mispricing, as shown in the subsequent increasing default rate. Using loan-level data and a regression model, they identify a sharp and persistent decline in the spread between private-label mortgages and 10-year treasury yield started in 2003 summer. Given such credit expansion, our story predicts that private-label mortgages choose to increase strongly in high net-export-growth areas because of the two above advantages in borrowers (higher foreclosure price and higher borrower income growth). This differentially stronger growth in private-label mortgages in high net-export-growth areas eventually results in a much stronger boom and bust cycle in the house-related employment.

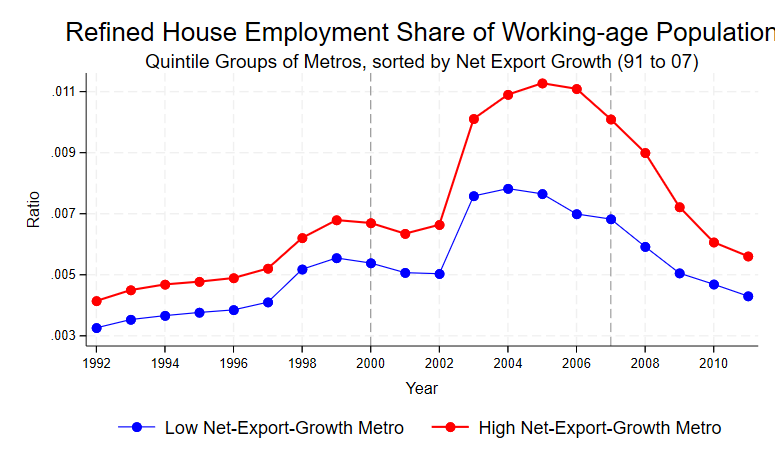

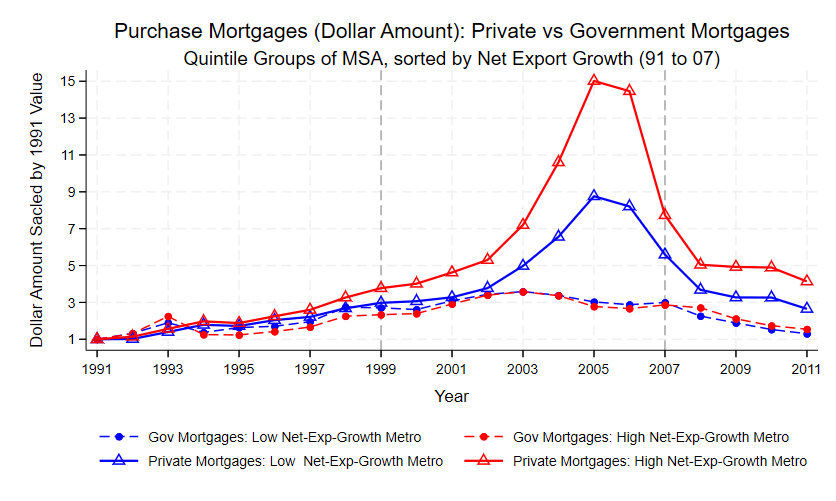

Findings We illustrate our major findings in four parts. In the first part, we document two new empirical facts. There is a much stronger business (employment) cycle for house-related industries in the high net-export-growth metropolitan areas (HNEG areas) than in the low net-export-growth areas (LNEG areas) between 1999-2010. Figure (2) shows this stronger local house-related employment cycle. In the prior period (1992-2000), there is no difference in the dynamics of house-related employment share in the working-age population between the HNEG areas and the LNEG areas. However, in the boom period (2000-2006) characterized by excess credit supply in private-label mortgages (Justiniano, Primiceri, and Tambalotti, 2022), the increase in house-related employment share is much stronger in the HNEG area (0.440%) than one in the LNEG area (0.161%). From 2007 to 2010, the drop is also stronger in the HNEG area (0.403%) than in the LNEG area (0.214%).

In contrast, the total employment share of working-age population only experiences a differentially higher boom (2000-2006) the high net-export-growth metropolitan areas (HNEG areas) (-0.077%) than in the low net-export-growth metropolitan areas (HNEG areas) (-2.184%). for total employment. No stronger bust (2007-2010) for total employment is found in these areas (-5.477% in the HNEG areas and -5.616% in the LNEG areas). Figure (3) shows these trends.

In the second part, using the instrumental variable by Feenstra, Ma, and Xu (2019), we provide the first causal evidence that the credit expansion in the private-label mortgages (PLMs), rather than the government-sponsored enterprise mortgages (GSEMs), causes the employment boom and bust across metropolitan areas between 1999 and 2010. Intuitively, the gravity model-based instrumental variable (GIV) captures the exogenous parts of net export growth due to (1) rising world demand (supply) reflected in export (import) growth and (2) tariff changes while controlling for US industry-by-year supply (demand) shocks and pre-determined transportation cost. With this IV, we show that credit supply expansion in the private-label mortgages (PLMs) causes a much stronger cycle in house-related employment in the high net-export-growth areas than in the low net-export-growth areas. We term this result as “housing industry channel”, which emphasizes the much stronger employment cycle in residential construction industry, other supporting industries, and the mortgage industry.

Please note that “causal evidence” means that we only find an incentive (net export growth) in the cross-section that induces credit expansion in private-label mortgages to be much stronger in the high net-export-growth areas. In contrast, We do not find the incentives that cause the aggregate credit expansion between 1999 and 2005. For the causes of the aggregate credit expansion, the literature have documented facts and evidence from financial innovation in securitization (notably the Copula formula by Li (2000) (Salmon, 2012)), international capital flow (“global saving glut” mainly 2003-2007 by Bernanke (2005); Bernanke et al. (2007)), mortgage market deregulation (2004 preemption of national banks from state anti-predatory lending laws by the Office of the Comptroller of the Currency (Di Maggio and Kermani, 2017), 2005 Bankruptcy Abuse Prevention and Consumer Protection Act (Lewis, 2023)), and political push (2002-2007 mortgage industry campaign contributions (Mian, Sufi, and Trebbi, 2013)). Thus, our choice of 1999-2005 as the boom period tries to include all major events documented above and our choice also matches the mortgage boom period commonly used in the literature (see Griffin, Kruger, and Maturana (2021) for a review).

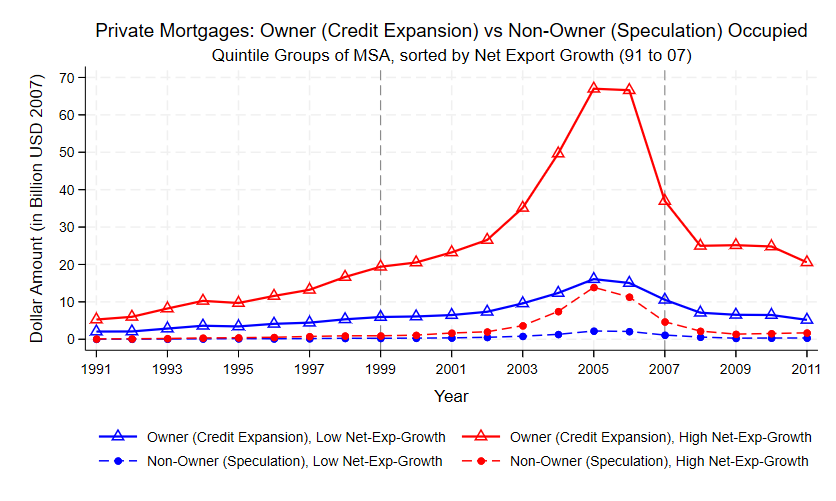

In the third part, we take advantage of empirical design and test alternative theories (hypotheses) regarding the business cycle. The first alternative one is the “speculative euphoria hypothesis” by Kindleberger (1978); Minsky (1986), which proposes that initial local economic growth can trigger bank to loose lending standard that fuels speculation by borrowers. The speculation eventually results in an unsustainable boom and ultimate crash. Due to the irrelevance of government-sponsored enterprise mortgages, we only distinguish speculation and credit expansion within the private-label mortgages (non-jumbo). we use the “non-owner-occupied” home purchase mortgages as a measure of speculation (Gao, Sockin, and Xiong, 2020) and “owner-occupied” ones as a measure of pure credit expansion. We use three tests to address the “speculative euphoria hypothesis”. Our first test shows that speculation (99-05) is largely caused by pure credit expansion. we use the residuals from the above regression as my measure of credit-independent speculation. Our second test shows that, compared to the dominant impact of pure credit expansion, credit-independent speculation only has a modest impact on the house employment cycle. Our third test shows that, without credit expansion, speculation does not respond to net export growth.

The second alternative theory is the famous “real business cycle theory” by Prescott (1986), which states that business boom and bust are mainly driven by shocks to the total productivity capacity of corporations. We provide three pieces of evidence against this theory. First, we show that net export growth causes a higher growth in the tradable employment in the high net-export-growth areas in both the boom and the bust periods, rather than only in the boom period. Second, commercial construction employment experiences neither a stronger boom nor a stronger bust in the high net-export-growth areas. Third, the debt (mainly home mortgages) in the household and nonprofit sector rather than the corporate sector experiences a boom and bust cycle.

We address two variants of the real business cycle theory: the “natural disaster hypothesis” and “technology shock hypothesis in construction sector”. The “natural disaster hypothesis” proposes that good whether conditions might drive the stronger boom and natural disaster might result in the stronger bust in the high net-export-growth areas. We present two pieces of opposing evidence. First, farm employment in the high net-export-growth areas experiences neither a stronger boom (00-06) nor a sharper bust (07-10). Second, manufacturing employment in these areas experiences a differentially stronger growth in both the boom (00-06) and the bust (07-10) periods. The “technology shock hypothesis in the construction sector” argues that the technology advancement reduces the construction cost and other sectors increase their building demand. then the mortgage supply only overreacts to this shock and causes the boom and bust. We employ three pieces of opposing evidence to address this hypothesis. First, unlike the residential construction employment, the commercial construction employment experiences neither a stronger boom nor a stronger bust in the high net-export-growth areas (HNEG areas). Second, contrary to the trend in private-label mortgages (non-jumbo), government-sponsored enterprise mortgages experience neither a stronger boom (99-05) nor a stronger bust (05-08) in the HNEG areas. In other words, credit-qualified households do not increase their demand to the “declining cost of housing” argued by this hypothesis. Third, We do not find a stronger boom (00-06) or a stronger bust (07-10) in manufacturing employment in the HNEG areas.

The third alternative theory is the “collateral-driven credit cycle theory” developed by Kiyotaki and Moore (1997). Their model highlights that a small shock to real estate can be amplified by a feedback loop via collateral and can ultimately result in large fluctuations. We offer two pieces of evidence against such a hypothesis. First, the “collateral channel hypothesis” predicts that the house (collateral) price increase (decrease) shall be followed by mortgage amount increase (decrease). However, we show that private-label mortgages (non-jumbo) increases at the same pace as the house price between 1999 and 2005 and decreases before the house price crash between 2005 and 2010. Second, the hypothesis predicts that the debt-to-GDP ratio by corporations shall experience a much stronger boom and bust than households. However, we show that debt (mainly home mortgages) by household and nonprofit sector experiences a strong boom and bust cycle while no cycle can be found in debt by the business sector.

The fourth alternative theory is the “The business uncertainty theory” Bloom (2009), which emphasizes the uncertainty (that might rise from government policies) can cause firms to pause investment and hiring. We present two pieces of opposing evidence. First, we find commercial construction employment does not experience a differentially stronger drop during the bust period (07-10) in the high net-export-growth areas (HNEG areas). Additionally, tradable sector employment continues to enjoy differentially stronger expansion in the bust period (07-10) in the HNEG areas.

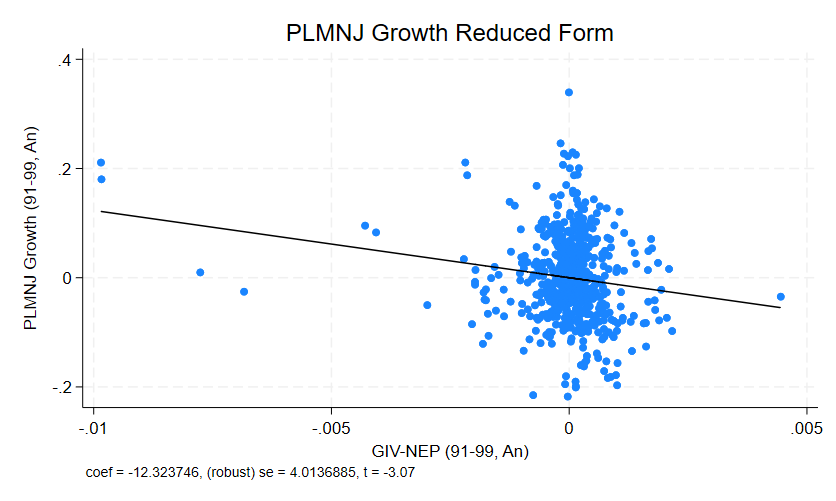

The fifth alternative theory, “extrapolative expectation theory” (Eusepi and Preston, 2011), states that local economic growth can drive extrapolation expectation in households that increases mortgage demand (and other consumption), which might overshoot and eventually lead to a stronger business cycle locally. Since government-sponsored enterprise mortgages (GSEMs) are still cheaper than non-jumbo private-label mortgages (PLMNJs) for credit-qualified households (Sherlund, 2008), the above theory would predict that both GSEMs and PLMNJs show stronger growth in the high net-export-growth metropolitan areas. However, we only see such a trend in PLMNJs rather than in GSEMs. In addition, we use the evidence supporting exclusion restriction to help address the above “extrapolative expectation theory”. We show that net export growth impacts house employment only via its impact on PLMNJs, rather than directly. Specifically, we show that in the prior period (91-99) without credit expansion net report growth did not increase house employment.

We conduct various tests to show that our main conclusion is robust. First, we consider the difference between states with and without the anti-predatory lending law (APL). In January 2004, the Office of the Comptroller of the Currency (OCC) preempted national banks from state-level anti-predatory lending laws (Di Maggio and Kermani, 2017). We find that preempted states experience neither a stronger boom nor a stronger bust in house-related employment. After controlling the state difference in APL, our main conclusion holds for all states. Second, we consider state-level differences in recourse law (Ghent and Kudlyak, 2011). We do not find non-resource states experiencing a stronger boom or a stronger bust in house-related employment. After controlling for state-level differences in recourse law, our main conclusion is robust for all states. Third, I investigate state-level differences in the judicial requirement of foreclosure laws (Mian, Sufi, and Trebbi, 2015). Though non-judicial states experience a stronger boom and a stronger bust in house-related employment, our major conclusion still holds for all states. Fourth, our major conclusion still holds after controlling sand-state dummy. Fifth, our main conclusion is robust to the inclusion of state capital gain tax as a control.

Contribution We illustrate our contribution to the literature in four parts. First, we document two new empirical facts in the literature: (1) a stronger boom in total employment and (2) a stronger boom and a stronger bust in refined-house employment in the high net-export-growth metropolitan areas than in the low net-export-growth ones in the U.S. from 1999 to 2010.

In addition, our paper makes unique contributions to the literature on the causal impact of credit expansion on the U.S. 1999-2010 business cycle in five dimensions. First, our paper explains the differential business cycles across metropolitan areas (MSA) within the USA, a new dimension in the literature. In contrast, most papers on business cycle focus on the cross-country differences Mian, Sufi, and Verner (2017); Müller and Verner (2023) whereas some focus on differences across states (Di Maggio and Kermani, 2017; Choi, Hong, Kubik, and Thompson, 2016; Mian, Sufi, and Trebbi, 2015). Second, our unique method has three major advantages. The first advantage is that we capture the long-term incentive of credit expansion by building on the “economic base theory”. This theory states that the tradable sector (for which we proxy it by net export growth) determines the local economy in the long term. The second advantage is that we can take advantage of the state-of-art instrumental variable by Feenstra, Ma, and Xu (2019) from International Economics for causal inference. The third advantage is that the IV approach by Feenstra, Ma, and Xu (2019) can cover the entire period of credit boom period (99-05) consisting of most major events in mortgage expansion. These events consist 2003-2007 “global saving glut” by Bernanke (2005); Bernanke et al. (2007), financial innovation in securitization (particularly the Copula formula by Li (2000) (Salmon, 2012)), mortgage market deregulation (2004 preemption by the Office of the Comptroller of the Currency (Di Maggio and Kermani, 2017), the 2005 Bankruptcy Abuse Prevention and Consumer Protection Act (Lewis, 2023)), and political lobby (2002-2007 mortgage industry campaign contributions (Mian, Sufi, and Trebbi, 2013)). In contrast, other causal studies mostly focus on one single event (Di Maggio and Kermani, 2017; Lewis, 2023). The above three advantages enable us to delve into the boom period preceding the bust period. In contrast, many previous papers focus on the bust period only (Mian, Rao, and Sufi, 2013; Mian and Sufi, 2014). Third and most importantly, we apply our method to test the relevance of almost all major theories (hypotheses) on the business cycle, including the speculative euphoria hypothesis, the real business cycle theory, the collateral-driven credit cycle theory, the business uncertainty theory, and the extrapolative expectation theory. No other paper can test as many theories and hypotheses as us. Our extensive tests add knowledge to the cause and the mechanism of the Great Depression and can advise future regulatory designs aimed at preventing it from happening again. Fourth, we also take advantage of a key legal constraint to distinguish the role of government-sponsored enterprise mortgages and private-label mortgages. Most other papers do not distinguish these two mortgages.666The only two exceptions that separate the role of government-sponsored enterprise mortgages and private-label mortgages are Justiniano, Primiceri, and Tambalotti (2022); Mian and Sufi (2022), though they do not show the irrelevance of government-sponsored enterprise mortgages to the differential business cycle across metropolitan areas. Fifth, we show that housing-related employment is central to the business boom and bust cycle (the housing industry channel).

These five dimensions distinguish our paper from other papers in the literature. The most related paper is Di Maggio and Kermani (2017). They exploit the 2004 preemption of national banks (rather than state-chartered depository institutions and independent mortgage companies) from state antipredatory-lending laws (APL) by the Office of the Comptroller of the Currency (OCC). They find that, compared to non-APL states, preempted states experienced stronger growth in national banks’ credit expansion, house price, and nontradable employment in 2004-2006 but also stronger declines in these outcomes subsequently. Our paper differs from their paper in ******** angles. First, we explain the cross-metro differential business cycles while they explain the cross-state differential business cycles. Table (A.7) shows that our cross-metro results are still very strong after controlling for the anti-predatory lending laws at the state level. Second, our empirical design builds on the “economic base theory” so that net export growth captures the long-term incentives of credit expansion in mortgages. One important advantage of our IV is that it covers the boom period (1991-2005) with almost all major events related to the mortgage market. In comparison, Their paper captures a single and perhaps temporary legal change as the incentive, thus ignoring technology innovation in securitization (Salmon, 2012), 2005 Bankruptcy Abuse Prevention and Consumer Protection Act (Lewis, 2023), and other important changes happened or started before 2004 (such as the international capital inflow 2003-2007 termed as “global saving glut” by Bernanke (2005)). Third, they and we both provide causal evidence, but our IV strategy can do more. Specifically, our IV strategy can decompose the household speculation (non-owner-occupied private-label purchase mortgages) and show with three tests that credit expansion is a necessary condition for speculation. Fourth and most importantly, our research design and comprehensive data analyses allow us to go further and test the relevance of major alternative hypotheses. In contrast, their difference-in-difference research design can do little to test alternative hypotheses with data from different periods. Fifth, we take advantage of a key legal constraint to distinguish the roles of government-sponsored enterprise mortgages and private-label mortgages whereas they use the 2004 OCC’s preemption to separate national banks from other mortgage institutions.

In spirit, our paper is similar to Mian, Sufi, and Verner (2020), which studies the state-level differential deregulation in the banking sector in the late 1970s and 1980s in the United States. They provide causal evidence that credit expansions amplify the business cycle via the household demand channel: credit expansions cause a differential higher rise in nontradable employment and nontradable goods. Different from their period, our paper focus on 1999-2010 US business cycle. Two other papers focus on the business downturn (2007-2009 or 2006-2009) and attribute the cause to the deterioration of house prices in household balance sheets. Mian, Rao, and Sufi (2013) document that the deterioration of household balance sheets significantly predicts the sharp decline in U.S. consumption across areas between 2006 to 2009. Mian and Sufi (2014) show that deterioration in household balance sheets predicts the sharp decline in U.S. employment across areas between 2007-2009 mainly via the “household demand channel”. Favara and Imbs (2015) exploit the 1994-2005 state-level branching deregulation and show that early-deregulating states experience stronger growth in mortgage and house prices. However, their figure 4 shows that deregulation cannot explain well the house price growth from 2002 to 2005. Importantly, they do not study the period from 2005 to 2009.

Unlike our focus on the differential business cycle across metropolitan areas within a country, most empirical business cycle papers focus on cross-country differential business cycles. Schularick and Taylor (2012) use 14 countries over the years 1870-2008 and show that credit growth is a powerful predictor of the financial crisis. Mian, Sufi, and Verner (2017) use 30 countries from 1960 to 2012 and document that an increase in household debt predicts lower GDP growth and higher unemployment in the medium term. Greenwood, Hanson, Shleifer, and Sørensen (2022) employ 42 countries from 1950 through 2016 and document that combination of rapid credit and asset price growth in the past three years in either the nonfinancial business or household sector is significantly associated with financial crisis in the next four years. Müller and Verner (2023) use 117 countries between 1940 and 2014 to show that credit expansion to the nontradable sector is systematically associated with subsequent growth slowdown and financial crisis while credit expansion to the tradable sector can systematically predict sustainable output and productivity growth without a higher probability of financial crisis.

Third, we show that house-related industries dominate the business cycle. Previous studies do not study the comprehensive list of housing-related industries as we do, including the residential construction, other supporting industries, and mortgage banker industries. Thus we emphasize the central role of housing in the credit-induced business cycle.

2 Research Design

In this section, we illustrate our empirical research design, which is similar to Li (2024), that can provide causal evidence for the business cycle. First, we measure the fundamental incentive for mortgage credit by operationalizing the central ideal of the “Economic Base theory” (Tiebout, 1962). Specifically, we use metropolitan exposure to net export growth of manufacturing industries (thereafter “net export growth”) as a proxy of the growth of local tradable sector, which by theory is the fundamental force of long-term economic growth. To overcome the endogeneity issue of OLS, we use an instrumental variable approach from International Economics by Feenstra, Ma, and Xu (2019) as our identification strategy.

2.1 Operationalize the “Economic Base Theory”

In this subsection, we operationalize the key idea of “economic base theory” by using metropolitan exposure to net export growth of manufacturing industries (thereafter “net export growth”) as a proxy of the growth of local tradable sector. This net export growth measure addresses the requirement of treatment variable in the introduction: enough area coverage (U.S. mainland), enough time coverage (91-09), enough geographic variation, and a feature of persistence.

Regional economics defines the “economic base sector” (tradable sector) as economic activities that a local area offers for the areas beyond its boundaries (Tiebout, 1962; Nijkamp, Rietveld, and Snickars, 1987). The tradable sector brings wealth into the local area and majority of the money will be circulated locally via a multiplier effect through nontradable sector. By this theory, the economic base is the most important driving force for local economic growth in the long term (Nijkamp, Rietveld, and Snickars, 1987; Thrall, 2002; Ling and Archer, 2017). Therefore, the tradable sector growth can predict demand-side factors that shape the long-term business growth, such as employment growth, household income growth, and population growth.777Olsen (1987) provides a survey on the demand factors of housing and business, including the three factors mentioned above. By the above theory, credit expansion would be stronger in areas with stronger tradable sector growth due to at least two reasons: (1) higher foreclosure price of house and (2) higher income growth that can be recoursed by lenders given default.

Perfect measurement of local tradable sector growth requires census-style data to include the accounting data of all firms in the tradable sector, which is not available. Instead, following Li (2024), we use the local employment composite as a proxy for the composite (share) of local tradable sector. Second, we use the time-series change in U.S. net export growth in manufacturing industries as a proxy for the relative growth (shift) at the industry level. Aggregating the above two proxies (share and shift) can achieve a good measure of the relative growth of the local treatable sector across metropolitan areas.888We acknowledge that the use of manufacturing does not include several other factors in the tradable sector: college town, retirement community, other tradable goods industries (e.g., natural resource), and tradable services (e.g., information technology and medical sector). To account for the work commuting within local areas, we aggregate net export growth at the metropolitan level.

We implement the above approach in two steps in data. First, in industry in year , net export measure is defined as , where , , and are US export, import and domestic production value in industry in year (or 1991), respectively. All terms are converted to 2007 US dollars. US domestic production in 1991 serves as the scaling factor. Year 1991 is chosen to avoid potential response of domestic production to trade in later periods.999The same choice of domestic production in 1991 as the denominator is taken by other papers like Barrot, Loualiche, Plosser, and Sauvagnat (2022). Second, we use local employment composite (share) to aggregate net export growth at the metropolitan level across period:

| (1) |

where and are the employment of industry and total employment, respectively, in metropolitan area in year . I choose to make sure the employment share is pre-determined to the trade measure so that all changes in net export growth () is driven by changes in trade measures instead of employment composite. Year to is the period of interest.

The above net export growth satisfies the requirements of treatment variable. First, the net export growth has enough area coverage (U.S. mainland) and enough time coverage (91-09). Second, its geographic variation arises from the fact that the local tradable sector tends to cluster within several related industries due to economies of scale. Internal economies of scale increase the size of local manufacturing firms (The World Bank, 2009) while external economies of scale attracts firms in the same and related industries to the clusters (Krugman, Obstfeld, and Melitz, 2018; The World Bank, 2009). Internal economies of scale include input purchase at a volume discount, fixed cost of plant operating, and learning in operation. External economies of scale consist specialization of suppliers, labor market pooling, and knowledge spillovers. Third, the long-term reduction in transportation costs and increased labor mobility in the last century strengthened the tradable sector clustering. Fourth, many global events in the 1980s and 1990s promoting international trade also added to the local industry clustering at the global level. These events include reforms and opening in large emerging countries, huge tariff reduction, the Dissolution of the Soviet Union in 1991, the establishment of North American Free Trade Agreement (NAFTA) in 1994, and the creation of World Trade Organization (WTO) in 1995. See World Trade Organization (2007) for a review. Fifth, the persistence feature of net export growth at the metropolitan level arises from three dimensions. At the industry level, both comparative advantages (due to technology level or natural endowment) and horizontal specialization (due to economies of scale) across nations make trade patterns persistent over time. At the local area level, clusters formation with huge costs is unlikely to change rapidly in a short period of time. At the individual level, human capital accumulation and job reallocation across industries are very difficult both locally and remotely.

2.2 OLS and Its Bias

In this subsection, we illustrate the potential bias from OLS regression specification. we begin with OLS specification that relates the employment growth to the growth of private-label mortgages (non-jumbo) (PLMNJ) at the county level:

| (2) |

Here, the dependent variable is the change of the total employment share in working-age population at county 00-06. The independent variable is the growth rate of the dollar amount (07USD) of private-label mortgage (non-jumbo) (PLMNJ) at county 99-05.

Omitted Variable Problems Potential omitted variables could bias . For example, the rapid net export growth and, hence, mortgage growth in 1999-2005 has been anticipated by employees in Silicon Valley so that house price and total employment grow before 1999 to reflect such expectation. In this case, could be biased downward because some of the effect of the mortgage shows up in total employment growth in earlier period, reducing the total employment growth 2000-2006.

2.3 Gravity Model-based Instrumental Variable

To overcome the endogenous concern regarding OLS specification, we use gravity model-based instrumental variable introduced by Feenstra, Ma, and Xu (2019) for net export growth. While they construct IV for exports and imports separately, we combine both as an IV for net exports. For illustration, we show the model of exports while leaving the model of imports in Appendix Section A.1.

To form an instrumental variable for US exports at the industry-year level, Feenstra, Ma, and Xu (2019) builds on the key idea that eight other high-income countries’ exports can instrument for the US exports since they both capture the world’s rising demand. In addition, they incorporate tariff changes, which are commonly believed to be exogenous to foreign firms. Further, this method corrects for the supply shocks in the home country by employing a fixed effect to remove them.

To predict US export, the gravity model-based IV starts from a symmetric constant-elasticity equation by Romalis (2007) for export:

| (3) |

In the formula above, is US export to country in industry in product variant in year . By the same notation, represents export from country to . and are the relative marginal cost of production in the industry in the US and country , respectively. and are the ad valorem import tariff imposed by country on exports from the US and country , respectively. and are the bilateral distance and other fixed trade costs from US to country and from country to country , respectively. Lastly, is the constant elasticity of substitution ().

The intuition of this gravity-style model is relatively straightforward. Competing with country , US exports to country are decreasing in the ratio of bilateral distance, in the ratio of relative marginal cost, and in the ratio of ad valorem total import tariff.

Assume that there are identical product varieties exported by country to the country in the industry and year , Feenstra, Ma, and Xu (2019) re-arranges this equation, multiply both sides with , and sum over countries :

As the above equation holds for any countries , one can choose a set of countries that have similar economic conditions (so that they are close competitors of US exports) to make the prediction more accurate. Feenstra, Ma, and Xu (2019) use the eight high-income countries used by Autor, Dorn, and Hanson (2013).

Again, one can multiple (number of variants of products in US exports) on both sides and denote the sectoral exports and , then one can get

With a few re-arrangements, one can get the formula for :

| (4) |

Note in the above formula, we multiply and divide by to prepare for the following regression setup. Now we can take logs of the above equation and get the regression-style formula:

|

|

(5) |

Now, We can see that US exports to the country in the industry year can be divided into six terms. “Term 0” represents the exports from eight other high-income countries to the country , which reflects the world demand. The second term , which represents the US supply shocks by industry and year, is potentially endogenous. We remove this term by the US industry-year fixed effects. The third term reflects the predetermined distance from the US to the destination market and all other industry- and year-invariant trade costs. We remove it by importing country fixed effects. “Term 1” is the tariffs on US exports imposed by destination country , which is out of control by US firms. I retain this term to capture the shocks from tariffs. “Term 2” is the weighted average tariffs on non-US exports charged by destination country , which is out of control of US firms. Intuitively, when this weighted average tariffs on non-US exports rise, country will import more from the US as substitutions. I retain this term to reflect this substitution effect. Lastly, the term is unobserved and remains in the regression error term.

After the above regression, we can construct predicted US exports that are isolated from supply shocks and the predetermined distance:

| (6) |

2.4 Data Implementation

There are four detailed steps when implementing the above procedures in data to get net export and its GIV at the metropolitan level across periods. First, we estimate Eq (5) at the 6-digit HS industry level (5673 industries) and derive predicted US export (isolated from supply shocks) by Eq (6). Second, we aggregate predicted US exports across importing countries and crosswalk the 6-digit HS code (5673 industries) to the 4-digit revised SIC system (392 manufacturing industries) by the crosswalk with weights by Acemoglu, Autor, Dorn, Hanson, and Price (2016). We end up with predicted US exports to the world at the industry year level. We perform this aggregation by . In a similar fashion, we get predicted US imports from the world . Third, we derive the gravity model-based instrumental variable for net export at the industry-year level

| (7) |

where is US domestic production in year 1991. Fourth, we use employment data from County Business Pattern to aggregate at the metropolitan level across periods.

| (8) |

where and are the employment counts of industry and total employment, respectively, in metropolitan area in year . Following Acemoglu, Autor, Dorn, Hanson, and Price (2016), we choose to prevent potential covariance due to data error between the dependent variable and the independent variable.

Relevance Condition Conceptually, the gravity model-based IV captures the exogenous part of net export growth due to (1) increasing world demand reflected in net export growth by other eight high-income counties and (2) tariff changes, after removing the US industry-year supply shocks. This relevance condition of this GIV is satisfied because it starts from the general equilibrium model by Romalis (2007) and is derived from specific decomposition by Feenstra, Ma, and Xu (2019). We will test this condition in data by robust F-statistics (Kleibergen and Paap, 2006) and efficient F-statistics Olea and Pflueger (2013).

Exclusion Restriction We have exclusion restrictions at two levels. The first level refers to the gravity model-based instruments by Feenstra, Ma, and Xu (2019). They have already removed supply-side shocks via industry fixed-effect in predicted US exports and demand-side shocks via industry fixed-effect in predicted US imports. Thus, exclusion restriction holds for the gravity model-based IV. The second level refers to our regression specification Eq (2), where the exclusion restriction means that net export growth can only affect house prices via private-label mortgages. Section 5.6.2 provides evidence supporting such claim.

As with all instrumental variable estimates, our 2SLS estimates capture the local average treatment effects on compilers (Imbens and Angrist, 1994). In our setting, compilers are metropolitan-by-year observations that experience more industry-by-year US net export to the world following increases in gravity model-based predicted US net export.

3 Data Sources

I combine several datasets to study how credit expansion in mortgages causes a stronger business boom and bust in the high-net-export-growth areas (HNEG areas). The International trade and tariff data are new to the literature on business cycles, enabling me to use the gravity model-based instrumental variable (Feenstra, Ma, and Xu, 2019) as my identification strategy.

3.1 Data for Net Export Growth

Trade Flow Data International trade flow data are from the UN Comtrade Database.101010The website of UN Comtrade Database is https://comtrade.un.org/data/. This database contains bilateral imports and exports data for detailed products recorded under the six-digit Harmonized Commodity Description and Coding System (HS code). To convert trade value to 2007 USD dollar, I apply the Personal Consumption Expenditures Chain-type Price Index by Federal Reserve in St. Louis.111111Federal Reserve in St. Louis provides Personal Consumption Expenditures Chain-type Price Index at https://fred.stlouisfed.org/series/PCEPI. To crosswalk these trade data from a six-digit HS system to a four-digit SIC system, I use the crosswalk file and revised SIC system (392 manufacturing industries) in Acemoglu, Autor, Dorn, Hanson, and Price (2016).121212This crosswalk file is also available from Prof. David Dorn’s website: https://www.ddorn.net/data.htm. The further refined SIC system (392 manufacturing industries) and crosswalk file are available from Acemoglu, Autor, Dorn, Hanson, and Price (2016). 131313To make sure my calculation is correct, I calculate China’s exports to the US and eight other high-income countries at the industry-year level from 1991 to 2007 and compare them to data provided by David Dorn’s website. The trade data is within the section [D] Industry Trade Exposure via his data page https://www.ddorn.net/data.htm. Correlations between my calculation and his corresponding data are 0.9983 for China’s export to the US and 0.9973 for China’s export to eight other high-income countries.

Tariff Data Bilateral tariff schedule data at five-digit SITC product level between 1984 to 2011 is from Feenstra and Romalis (2014).141414The original data are collected from the TRAINS, IDB databases, and various other resources, with multiple cleaning steps and filling in missing values by other resources. The data work is described in Appendix C in Feenstra and Romalis (2014). To crosswalk tariff data from a five-digit SITC system to a six-digit HS system, I follow the methods in Feenstra, Ma, and Xu (2019). Specifically, I first use crosswalk files from the Trade Statistics Branch (TSB) of the United Nations Statistics Division to convert the HS 2007 version to the HS 2002 version.151515The crosswalks files between different HS versions are available from the UN Comtrade database: https://unstats.un.org/unsd/trade/classifications/correspondence%2Dtables.asp. Then I use a crosswalk from Feenstra, Lipsey, Deng, Ma, and Mo (2005) to match each six-digit HS code to one five-digit SITC2. When one six-digit HS code is matched to multiple SITC2 codes, I follow Feenstra, Ma, and Xu (2019) and use the one with the highest value share.

Manufacturing Production Data I use the US 4-digit SIC manufacturing industry total domestic production (vship) in 1991 as the denominator to scale the trade value. Such data comes from NBER-Center for Economics Studies (NBER-CES) Manufacturing Industry Database. 1991 is the first year in analysis so production is unlikely to respond to trade change afterward.161616This choice of scaling is also used by Barrot, Loualiche, Plosser, and Sauvagnat (2018).

Manufacturing Employment Data Employment data across detailed manufacturing industries at the county-by-year level in the U.S. comes from County Business Patterns (CBP) Database by U.S. Census.171717County Business Patterns Database is available here: https://www.census.gov/programs-surveys/cbp/data/datasets.html. Following the method by Acemoglu, Autor, Dorn, Hanson, and Price (2016), I use manufacturing employment data to aggregate net export growth and its IV at the metropolitan areas across periods. Refer to Section 2.4 for implementation details.

3.2 Data for Mortgages and House Prices

Mortgage Data Detailed loan-level mortgage data are from the Home Mortgage Disclosure Act (HMDA) database.181818The Consumer Financial Protection Bureau (CFPB) provides 2007-2017 HMDA data” https://www.consumerfinance.gov/data%2Dresearch/hmda/historic%2Ddata/. The Federal Financial Institutions Examination Council (FFIEC) maintains 2017-2021 HMDA data at https://ffiec.cfpb.gov/data%2Dpublication/2021. CFPB offers links of 1990-2006 HMDA to the National Archives at https://github.com/cfpb/HMDA_Data_Science_Kit/blob/master/hmda_data_links.md. In 1975, Congress enacted HMDA to improve public reporting of mortgage loans. Any financial institution must report HMDA data to its regulator if it meets certain criteria, such as a threshold for assets and whether the institution has a home office or branch in a Metropolitan Statistical Area (MSA). This annual database contains information on loan applications, borrower demographics, lender identifiers, and loan specifics such as purpose, amount, and location. The HMDA database provides near-universal coverage of the mortgage market. Avery, Bhutta, Brevoort, Canner, Gibbs, et al. (2010) confirm that in 2008, commercial banks filing HMDA carried 93% of the total mortgage dollars outstanding on commercial bank portfolios.191919Although lenders with offices only in non-metropolitan areas are not required to file HMDA, 83.2% of the population lived in metropolitan areas in 2006 (Dell’Ariccia, Igan, and Laeven, 2012).

We use the following filtering criteria for HMDA data. First, we keep originated loans and delete applications that are denied, withdrawn, or not accepted. Second, for loan types, we keep conventional and Federal Housing Administration-insured (FHA-insured) loans and delete loans insured by the Veterans Administration, Farm Service Agency, or Rural Housing Service. Third, for loan purposes, we mainly use home purchase mortgages for most empirical tests and add refinancing mortgages in some robustness tests. Fourth, for occupancy types, we keep both non-owner-occupied and owner-occupied loans and treat “not applicable” as owner-occupied.202020Based on the HMDA manual (https://www.ffiec.gov/hmda/pdf/1998guide.pdf), this “not applicable” occupancy very likely refers to a multifamily dwelling where the borrower lives in. In terms of numbers, this “not applicable” occupancy is only around 3.5% of the number of non-owner-occupied loans and 0.59% of the number of owner-occupied loans as of 2007.

We use the HMDA database to construct loan volume (number and dollar amount) at the county-by-year level for government-sponsored enterprise mortgages (GSEM) and private-label mortgages (PLM). Based on the HMDA examination procedures, an institution is required to report the type of entities that purchase the loans that are originated (or purchased) and then sold in the same calendar year.212121See “Home Mortgage Disclosure Act Examination Procedures” at https://www.federalreserve.gov/boarddocs/caletters/2009/0910/09%2D10_attachment.pdf. These procedures imply that the HMDA can potentially under-estimate the mortgages that are sold as GSEM and PLM since the mortgages originated near the end of the calendar year need some time to be sold. Nonetheless, this potential underestimation can only bias my results to zero. I follow the classification of PLMs and GSEMs by Mian and Sufi (2022).222222Mian and Sufi (2022) group five categories as PLMs when a mortgage is sold: (1) to a commercial bank, savings bank, or savings affiliation affiliate, (2) into private securitization, (3) to an affiliate institution, (4) to a life insurance company, credit union, mortgage bank, or finance company, and (5) to other types of purchasers.

Conforming Loan Limits Data I obtain conforming loan limits by year and county from Federal Housing Finance Agency.232323Before and in 2007, conforming loan limits are set only at the national level: https://www.fhfa.gov/AboutUs/Policies/Documents/Conforming%2DLoan%2DLimits/loanlimitshistory07.pdf. From 2008 onward, conforming loan limits are set by year and by county: https://www.fhfa.gov/DataTools/Downloads/Pages/Conforming%2DLoan%2DLimit.aspx. Conforming loan limits are, in general, different for 1-unit, 2-unit, 3-unit, and 4-unit dwellings in each year (and county). Since the HMDA data does not include information on the number of units in a home between 1991 and 2009, We use the 1-unit conforming loan limit for all mortgages. Thus, our conservative measure of non-jumbo mortgages can help avoid a potentially upward bias in results.

Consistent Counties Covered by HMDA Following the suggestion by Avery, Brevoort, and Canner (2007), we infer counties that are consistently covered by HMDA based on the scope of metropolitan areas defined and updated by the U.S. Office of Management and Budget. Detailed steps are the same in Li (2024). Consequently, We get 800 “HMDA consistent counties after 1996” and 712 “HMDA consistent counties after 1990”.

U.S. House Price Data We obtain the U.S. house price index data based on repeated sales at the county and ZIP levels from the Federal Housing Finance Agency.242424The data are available at https://www.fhfa.gov/DataTools/Downloads.FHFA working paper Bogin, Doerner, and Larson (2019) describes the construction of the index and tests its accuracy via various methods.

Merge House Price and Mortgage Data For both figure and regression analysis regarding house prices, I require that the counties are covered by both house price data and mortgage data. The merged data set contains fewer counties compared to mortgage data since house price data covers fewer counties.

3.3 Data for Employment and Business

Aggregate Debts for Sectors I obtain annual debt data for households, business (corporate and non-corporate), and government (federal and local) from the Federal Reserve.252525The debt data is available here: https://www.federalreserve.gov/releases/z1/dataviz/z1/nonfinancial_debt/table/. Such data also contains subcategories for household debt: mortgages, consumer credit, and other liability.

BEA Employment Data I obtain annual employment data at the county level from the U.S. Bureau of Economic Analysis (BEA) for analysis on total employment because such data include both (1) wage and salary employment and (2) proprietor employment (self-employment).262626The BEA employment data is available at https://apps.bea.gov/regional/downloadzip.cfm. In the category “Personal Income (State and Local)”, ”CAEMP25S” contains data from 1969 to 2000, while ”CAEMP25N” contains data from 2001 and onward. This coverage is better than County Business Pattern employment data, which does not contain self-employment not working in commercial establishments.

CBP Employment Data I get employment data in house-related and other industries from the County Business Pattern (CBP) database in the U.S. Census.272727County Business Patterns Database is available at: https://www.census.gov/programs-surveys/cbp/data/datasets.html. To derive the accurate number from ranges reported in CBP, I obtain the carefully imputed CBP data from Eckert, Fort, Schott, and Yang (2020).282828Eckert, Fort, Schott, and Yang (2020) provide final data, code, and detailed documentation of their methodology in imputing CBP data at https://fpeckert.me/cbp/. For industry classification, I follow Goukasian and Majbouri (2010) and Mian and Sufi (2014). Please see detailed information in Table (1).

New Residential Unit Permits I get county-by-year new residential unit permit data from the U.S. Census.292929New residential unit permits data is available at: https://www.census.gov/construction/bps/index.html. To avoid reduced sample size due to missing observations because of non-survey years for some counties, I use the Census-imputed permit data.

3.4 Local Economic Conditions

IRS Household Income Data I obtain household income data at the county-by-year level from the U.S. Internal Revenue Service (IRS).303030For 1989 to 2018, the data is available at https://www.irs.gov/statistics/soi%2Dtax%2Dstats%2Dcounty%2Ddata. The average household income at the county level is the adjusted gross income divided by the number of returns (households). The income is adjusted to the 2007 USD by the Personal Consumption Expenditures Chain-type Price Index (PCEPI) from the Federal Reserve Bank of St. Louis.

Local Control Variables I obtain Control variables at county and ZIP code levels from U.S. Decennial Census Summary Files. Control variables in 1989 at the county level are from 1990 (March) Census Summary File 1C and 3C, whereas control variables at the ZIP level are from Summary File 3B.313131The 1990 U.S. Census Summary File 1 is available at https://www.census.gov/data/datasets/1990/dec/summary-file-1.html and Summary File 3 is available at https://www.census.gov/data/datasets/1990/dec/summary-file-3.html. Control variables in 1999 at the county level and the ZIP level are from both 2000 (March) Census Summary File 1 and 3.323232The 2000 U.S. Census Files are available at: https://www.census.gov/programs-surveys/decennial-census/guidance/2000.html

3.5 Counties Severely Affected by 2005 Hurricanes

Following Li (2024), we delete twelve “deeply affected counties by 2005 Hurricanes” since they experienced unusual growth in mortgages due to hurricane damage and subsequent government subsidies.333333I try my best to present the most robust results. Since outliers only largely affect results in regression but not the illustration in figures, I include these twelve counties in the figures but remove them from regressions and summary statistics. In 2005, three Category 5 hurricanes (Katrina, Rita, and Wilma) caused enormous fatalities and damage (estimated $125 billion).343434These “deeply affected counties” include Monroe County (FL, 12087), Cameron Parish (LA, 22023), Jefferson Parish (LA, 22051), Orleans Parish (LA, 22071), Plaquemines Parish (LA, 22075), St. Bernard Parish (LA, 22087), St. Tammany Parish (LA, 22103), Vermilion Parish (LA, 22113), Hancock County (MS, 28045), Harrison County (MS, 28047), Jackson County (MS, 28059), Stone County (MS, 28131).

3.6 Summary Statistics and Figures

Summary statistics of key variables are reported in Table (2) and (3), separated into different periods. In the prior period, starting with 712 “HMDA consistent counties after 1990”, we remove seven counties due to heavy impact of the 2005 hurricanes described in section (3.5), ending up with 705 counties. Due to data availability, we have less number of observations for refined house employment and housing supply elasticity. In the boom period and bust period, beginning with 800 “HMDA consistent counties after 1996”, we remove eight counties due to heavy impact of the 2005 hurricanes, resulting in 792 counties. Again, due to data availability, we have less number of observations for many variables of employment growth and housing supply elasticity.

First, we can see that the total employment and refined house employment share experienced a clear boom and bust cycle. For example, while the mean of annualized change across counties is only 0.029% in the prior period (1992-2000), it is 0.042% in the boom period (1999-2005) and -0.089% in the bust period (2007-2009).

Second, the government-sponsored enterprise mortgages (GSEM) play an less important role in the boom period: its mean annualzed growth rate across counties is 14.950% in the prior period but only 4.378% in the boom period.

Third, for the private-label mortgages (non-jumbo) (PLMNJ), it is interesting that the mean of growth rates across counties is similar between the prior period (17.072%) and boom period (16.978%). The similar mean values result from the use of different base values.353535Specifically, the 1991 PLMNJ dollar amount is used for the growth rate between 1991 and 1999 while the 1999 PLMNJ dollar mount is used for the growth rate between 1999 and 2005. The similar mean growth rates disguise the much larger increase in absolute dollar amount in private-label mortgages in the boom period . Figure (8) shows the differential huge increase in dollar amount in PLMNJ in the boom period, because time series values are scaled by 1991 dollar value only. Figure (8) and (7) hint that the impact of private-label mortgages (non-jumbo) shall be much larger than the government-sponsored enterprise mortgages in the boom and bust cycle of refined house employment since the former ones do show a differentially stronger increase in the high-net-export metropolitan areas.

Fourth, the net export growth rates have negative mean in the boom period (with a mean of -0.218% and standard deviation of 0.20%) and in the prior period (with a mean of -0.18% and standard deviation of 0.17%). This pattern is also present in the gravity model-based net export growth rates.

We include control variables only in the starting year in each period in the county , which avoids any impact from net export growth during that period. Control variables are employed to neutralize factors that may affect credit expansion. Our basic controls include average household income, the number of households, and the fraction of the labor force in the county . Our housing controls include the number of house units, house vacancy rate, housing supply elasticity (Saiz, 2010), and fraction of renters in the occupied house units. Our demographic controls include the percentage of the white population, the fraction of population holding a Bachelor’s degree and above, and the count of immigrants entering the U.S. between 1990 and 1999. We do not control local industry employment share, which is partially and jointly determined by my left-hand-side industry-level employment. The joint determinant relationship means that local industry employment shares are very likely “bad controls”.

4 Empirical Results: Supporting Credit Expansion

Our main empirical tests provide direct evidence that credit expansion in private-label mortgages (PLMs) instead of government-sponsored enterprise mortgages (GSEMs) cause the 1999-2010 boom and bust in the business boom and bust. To compare these two categories of mortgages under the same criteria, we use the conforming loan limits to get the non-jumbo category of private-label mortgage (PLMNJ) and remove the jumbo ones. we will focus on the comparison between private-label mortgages (non-jumbo) (PLMNJs) and the government-sponsored enterprise mortgages (GSEMs).363636First, jumbo loan borrowers are usually not low-income households so credit expansion study shall focus on non-jumbo loans. Second, the jumbo category of private-label mortgages is much smaller in number when compared to non-jumbo ones. Third, including jumbo ones only strengthens my results on private-label mortgages.

Based on the intuition described in the instruction, we predict that when the funding cost declines private-label mortgages (non-jumbo) expand more in the high net-export-growth areas in response to higher net export growth.

4.1 Total Employment Boom (00-06) and Bust (07-10)

Total Employment Boom (00-06)

Let us first focus on my main hypothesis: total employment boom (00-06) as a result of credit expansion in response to net export growth across metropolitan areas. First, I expect private-label mortgages (non-jumbo) would experience stronger growth (99-05) in the high-net-export-growth metropolitan areas. Consequently, the above credit expansion causes total employment to grow stronger in the high-net-export-growth metropolitan areas.

Hypothesis 1 In cross-section, growth in private-label mortgages (non-jumbo) (PLMNJs) in the boom period (1999-2005) causes the total employment boom (2000-2006).

To test the total employment boom, I perform the following regression.

| (9) |

The left-hand-side dependent variable is the change of the total employment share in working-age population at county 2000-2006, and the key independent variable is the growth rate of the dollar amount of private-label mortgage (non-jumbo) (PLMNJ) at county 1999-2005. indicates control variables at county in 1999. I use the gravity model-based instrument variable for net export growth .

Since employment growth is usually lagged, we choose the period for employment growth (00-06) to be a year later than the period for credit expansion (99-05). To prevent excessive influence from outliers, total employment share is winsorized at 0.5% and 99.5% level. Each regression uses analytical weight as the natural logarithm of the number of house units in the starting year 1999. Logarithm instead of the absolute number of house units is chosen to guard results from being dominated by a few super-populous counties. To take into account that households might commute to work across counties within a metropolitan area, I measure net export growth in the metropolitan area.373737According to US Census, “the general concept of a metropolitan statistical area is that of a core area containing a substantial population nucleus, together with adjacent communities having a high degree of economic and social integration with that core.” (https://www.census.gov/programs-surveys/metro-micro/about.html) Furthermore, I cluster standard errors at the metropolitan area (CBSA 2003 code) level.

Table (5) reports OLS, reduced-form, second-stage, and first-stage results in panel A, B, C, and D, respectively. First, panel A shows the impact of PLMNJ growth (99-05, annualized) on total employment growth (00-06, annualized) are positive but insignificant. This result is consistent with our prediction that some of the growth of PLMNJ is expected. Reduced-form estimates in panel B show a significant and positive effect, since the gravity model-based instrument captures the exogenous and unexpected part of net export growth. The first-stage estimates in panel D are positive and significant at 1% level. For the specification with full controls, clustered Kleibergen-Paap F-statistic (Kleibergen and Paap, 2006) is 10.48, and the Montiel Olea-Pflueger Efficient F-Statistic (Olea and Pflueger, 2013) is 10.47, both of which are larger than 10. Thus, my estimates are very unlikely biased by a weak instrumental variable. Panel C reports 2SLS estimates for equation (9). Like reduced-form estimates, the 2SLS estimates are statistically significant and quite stable across various specifications.

Let us turn our attention to economic meaning in 2SLS with full controls in Table (8). According to column (5) with all controls, one standard deviation in cross-sectional difference in annualized PLMNJ growth (99-05) results in difference in annualized total employment share growth (00-06) across metropolitan areas, translating into difference from 2000 to 2006. One standard deviation in cross-section difference in annualized total employment share growth (00-06) is , translating into from 2000 to 2006. The two results mean that, one standard deviation in PLMNJ growth (99-05) can explain of one standard deviation in total employment share growth (00-06).

The literature has shown that housing supply elasticity (Saiz, 2010) is a very important determinant of mortgage growth. Our first-stage regression in Table (8) verifies the above finding with coefficient being and significant at 1% level. However, the insignificant 2SLS estimate shows that housing supply elasticity does not impact the total employment growth directly after controlling for private-label mortgages. We provide a potential explanation for this result. Recall that lower elasticity in the local housing market means insufficient land supply for new buildings, thus attracting mortgage growth given the higher expected housing price in the near future. But lower elasticity also means that insufficient building supply cannot provide enough cheap establishment buildings for business expansion. Thus the total effect of housing supply elasticity on the total employment growth could be near zero after controlling for private-label mortgages.

We also show that the employment boom is robust to the alternative measures of total employment. In Appendix Table (A.2), we report OLS, reduced-form, first stage, and second stage results for three measures of alternative total employment in our context: wage and salary, nonfarm, and nonfarm private employment. Wage and salary employees are likely more impacted by business cycle than self-employed workers. Nonfarm employees are likely more influenced by business cycle than farm employees. Nonfarm private employee are nonfarm and non-government employees who are more vulnerable to business cycle than nonfarm government workers. Again, to guard results from excessive influence by outliers, alternative measures are all winsorized at 0.5% and 99.5% level. The reduced-form and 2SLS estimates together show that the employment boom results are very strong for the above three alternative measures, with significant levels all at 1%. Specifically, the 2SLS coefficients (, , and ) are also very close to the the coefficient () for the total employment share growth.

Total Employment Bust (07-10) The employment bust (07-10) is quite different from the employment boom (00-06) and is not stronger in the high net-export-growth metropolitan areas. Conceptually, this happens because, in the boom period, the high net-export-growth areas experience higher growth in tradable sector, housing-related sector, and nontradable sector. However, in the bust period, the high net-export-growth areas experience higher growth in tradable sector but higher drop in housing-related sector and nontradable sector. Thus, we do not find the total employment bust to have a differential trend in the high net-export-growth areas. The results in the rest of paper will make the above claim clear.

4.2 The Housing Industry Channel

Since the credit expansion in mortgages seem to dominant the 1999-2010 U.S. business cycle, I propose a “housing industry channel”, which states that the credit expansion in mortgages results in employment boom and bust primarily through the house-related industries. I will show causal evidence for this channel in this section. In this subsection 4.2, to make regression coefficient more visible with digit, I multiple the employment share by 100 for all dependent variables.

4.2.1 House-Related Employment

This section provides causal evidence that growth in private-label mortgages (non-jumbo) 1999-2005 causes the house-related industries employment boom (2000-2006) and bust (2007-2010). For house-related industries, I use the definition by Goukasian and Majbouri (2010). The complete definition of all sub categories and finer SIC industries are provided in Table (1). I use crosswalk files from US census to crosswalk these 1987 SIC codes to 2007 NAICS codes. Then I process house employment data from the computed county business pattern data by Eckert, Fort, Schott, and Yang (2020).383838Fabian Eckert provides their computed county business pattern data at https://fpeckert.me/cbp/.

Since the primary driving force is the private-label residential mortgages, not all house-related industries experience the same boom and bust pattern. In particular, commercial construction employment is likely not impacted as significantly as residential construction employment. In addition, real estate brokerage and management may not be impacted significantly because the mortgage boom may only trigger a shift of renters to homeowners while the entire real estate brokerage and management demand do not change. Due to these reasons, I define “refined house-related industries” that include residential construction, supporting industries, and mortgage banks and brokers. I expect the boom and bust trend is stronger for “refined house-related industries” but may be weaker for other house-related industries defined by Goukasian and Majbouri (2010).

Refined House-Related Employment Boom (00-06) and Bust (07-10) I test the refined house-related employment boom and bust in the following single regression

|

|

(10) |

Controls, weight, and standard errors are the same as Eq(9).