Abstract.

Here, we examine a fully-discrete Semi-Lagrangian scheme for a

mean-field game price formation model.

We show that the discretization is monotone as a multivalued operator and prove the uniqueness of the discretized solution.

Moreover, we show that the limit of the discretization converges to the weak solution of the continuous price formation mean-field game using monotonicity methods.

This scheme performs substantially better than standard methods by giving reliable results within a few iterations, as several

numerical simulations and comparisons at the end of the paper illustrate.

King Abdullah University of Science and Technology (KAUST), CEMSE Division, Thuwal 23955-6900. Saudi Arabia. e-mail: yuri.ashrafyan@kaust.edu.sa

King Abdullah University of Science and Technology (KAUST), CEMSE Division, Thuwal 23955-6900. Saudi Arabia.

e-mail: diogo.gomes@kaust.edu.sa

The authors were partially supported by King Abdullah University of Science and Technology (KAUST) baseline funds and KAUST OSR-CRG2021-4674.

1. Introduction

This paper investigates first-order price formation mean field games (MFGs), modeling interactions within large populations of agents.

Mean field game theory, pioneered by [18, 19] and [17, 16], extends classical optimal control problems to scenarios involving large populations of interacting agents. The price formation problem draws on both optimal control principles [11]

and mean-field game techniques to model how individual decisions and market-wide dynamics influence each other.

Price formation MFGs hold the potential to revolutionize how we understand and predict market behavior. By capturing the interactions of many agents, these models can contribute to more efficient resource allocation, improved market stability, and better-informed decision-making for individuals and policymakers. Here, we develop a numerical method for approximating solutions of price formation MFGs using Semi-Lagrangian (SL) schemes.

We consider the following price formation problem.

Problem 1.

Given initial distribution ,

where is the space of probability measures on ,

terminal cost , and supply , and a uniformly convex Hamiltonian, .

Find functions wwith , and , satisfying

|

|

|

(1.1) |

subject to initial-terminal conditions

|

|

|

(1.2) |

In Problem 1, is a partial derivative of with respect to the second variable.

The unknown is the triplet , where the value function, , solves the first equation in the viscosity sense, and the probability distribution of the agents, , solves the second equation in the distributional sense. Finally,

the price, , is determined by the balance condition, the third equation in (1.1), which guarantees that supply meets demand exactly.

A typical agent’s state, represented by , denotes their assets.

At time , the distribution of assets is encoded in the probability measure .

Every agent trades assets at a price given by the time-dependent function .

Section 2 briefly recalls the preceding problem’s derivation and motivation.

Under the assumptions discussed in Section 3, in [11], the authors proved the existence and uniqueness of a solution to Problem 1.

This model assumes deterministic supply, a simplification which aids analysis but limits applicability in scenarios with uncertain supply. Nonetheless, deterministic models offer a foundation for understanding more complex markets and can

be directly useful when accurate forecasts are available.

The complexity of these models often renders analytical solutions infeasible. Numerical methods allow for the analysis of richer market dynamics, providing insights into previously unsolvable problems and informing decision-making in practical applications.

A significant challenge is the forward-backward nature of traditional MFGs, compounded by the additional balance condition.

Researchers have suggested various numerical techniques for solving standard MFG systems; for example,

finite difference schemes and Newton-based approaches were presented in [1] and [2], respectively, for standard MFGs without balance conditions.

For the specific model considered here, in [5],

the authors introduced a potential function that transforms the price formation MFG into a convex variational problem. Using this variational structure, this problem is solved numerically by minimizing a suitable functional discretized with finite differences.

Price problems with a stochastic supply and price were introduced in [14] and [15], respectively.

Substantial effort was made to address the issue of common noise with machine learning (ML) techniques.

In [13], an ML approach employing dual recurrent neural networks and adversarial training to address the price formation MFG model with common noise is given.

An ML training process was developed based on a min-max characterization of control and price variables in [12].

Using the potential transformation, [4] solved the price problem with common noise using a recurrent neural network.

These methods are suitable for common noise problems where standard numerical methods fail.

However, these methods can be slow for deterministic cases. This was, in fact, one of the original motivations for our work.

Here, in the deterministic case, we

develop efficient and accurate methods for deterministic price models. We build on previous work on

SL schemes for MFGs.

Both semi-discrete and fully discrete SL schemes have been employed for first and second-order MFGs [7], [9], and [8].

In the Hamilton-Jacobi equation, we use a fully discrete SL scheme, and

for the transport equation, we use the adjoint of the linearization of the Hamilton-Jacobi equation.

For the balance condition, we use a simple numerical quadrature.

This discretization and the algorithm to solve it are detailed in Section 4.

Properties and estimates related to the discretization are presented in Section 5.

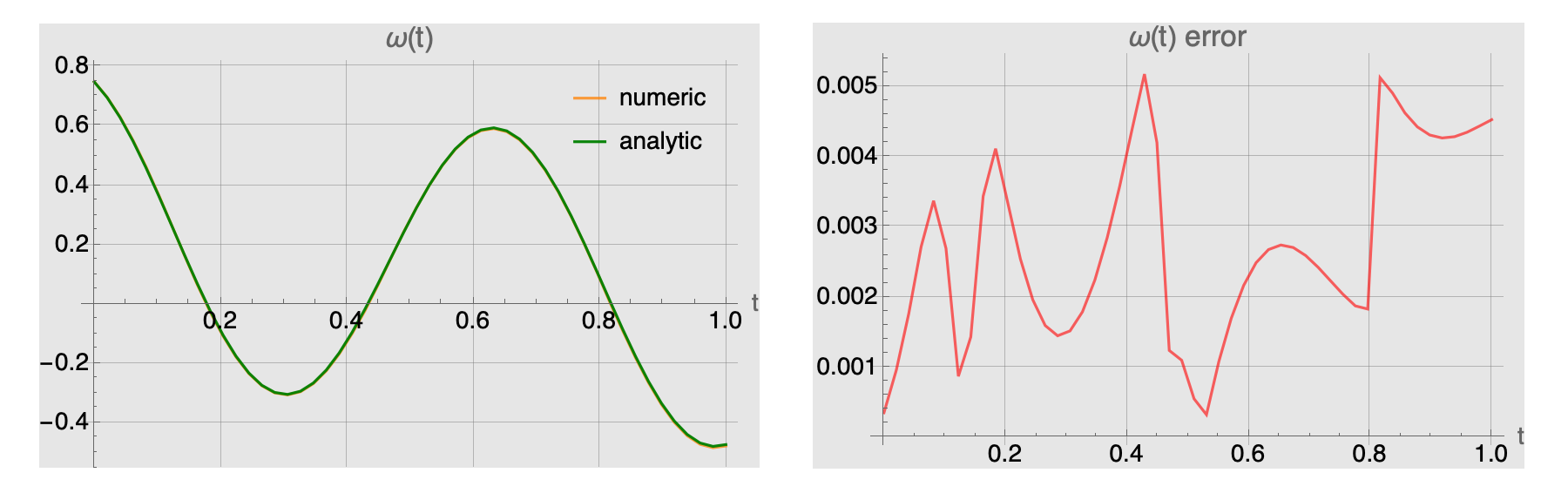

Our approach addresses several key gaps in existing numerical methods for price formation MFG: challenges with computational efficiency, accuracy in nonlinear scenarios, and suitability for large-scale validation of machine learning results. Our SL-based scheme offers advancements in all of these areas: it provides improved computational speed, robust handling of complex market dynamics, and the precision necessary for benchmarking ML models. These advantages are crucial for iterative analysis, policy testing, real-time applications, and the development of reliable, data-driven market insights.

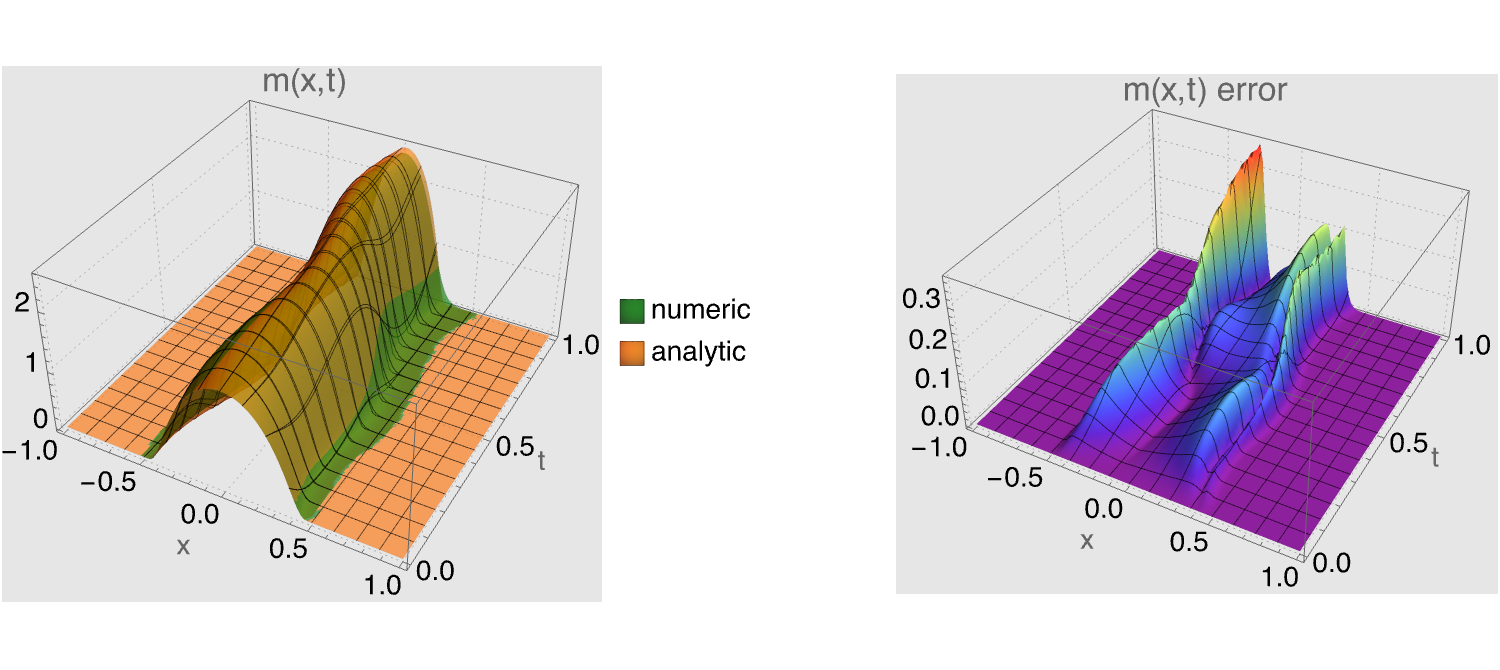

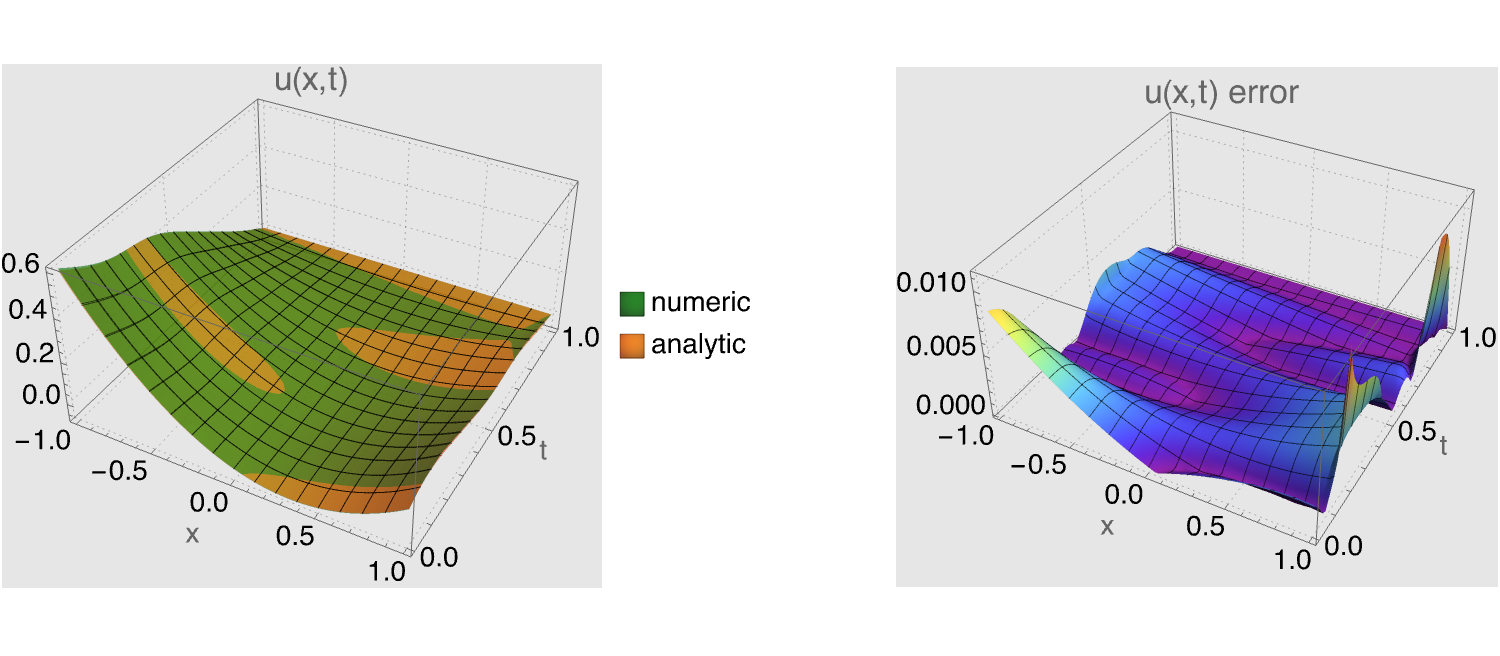

A detailed comparison between our fully discrete SL, potential minimization, and ML methods appears in Section 7.

2. Background

This section establishes the foundation for our price formation model.

The model examines how prices form within a market where numerous agents interact, each trading motivated by profit maximization (here formulated

as cost-minimization).

Employing optimal control theory, we analyze

how individual agents strategize to minimize costs associated

with holding an asset, market impact, storage costs, and risk preferences.

Additionally, using mean-field game theory, we track the overall distribution of agents, impacting supply and demand. These individual choices and their aggregate distribution together with a market clearing mechanism

form the core mechanism that ultimately drive price dynamics within this model.

Agents have a a state which corresponds to the assets they hold.

Let be the set of bounded, measurable real-valued functions on

the interval .

An admissible control is a function . Each agent

selects an admissible control which drives its trajectory

|

|

|

(2.1) |

where represents the agent’s state at the time .

The total cost for an agent is the sum of the terminal cost, , and the integral of the running cost, . Here , the market impact term,

represents costs like market impact or other trading expenses.

The preference potential,

, encodes the agent’s asset level preference and can account for things like storage cost. It can incorporate risk aversion, short-selling constraints, or storage costs.

Lastly, is the price that agents pay by trading units at a price .

The agent aims to minimize the following cost functional:

|

|

|

(2.2) |

by selecing appropriate admissible controls.

The value function, , is the infimum of the

cost functional

over all

|

|

|

(2.3) |

The associated Hamiltonian, , is the Legendre-Fenchel transform of ,

given by

|

|

|

(2.4) |

Viscosity solutions offer a framework to handle potential non-differentiability that arise in such problems [6].

In fact, is a viscosity solution to the Hamilton-Jacobi equation

|

|

|

The dynamic programming principle for (2.3) provides

a representation formula for the value function

|

|

|

(2.5) |

where solves (2.1). Furthermore, the optimal control is given in feedback form by

|

|

|

(2.6) |

at all points where is differentiable.

The transport equation is the adjoint to the linearized Hamilton-Jacobi

equation. This transport

equation tracks the evolution of the distribution of the states over time

and incorporates the initial distribution, , as initial condition:

|

|

|

More precisely, given , consider the trajectory

|

|

|

We have

|

|

|

Recall that push forward for a probability measure and a map , , is the probability measure defined by

|

|

|

for all bounded and continuous functions .

We obtain the density function from the initial measure by push

forward of the flow :

|

|

|

Note that for every , we have

|

|

|

that is

|

|

|

(2.7) |

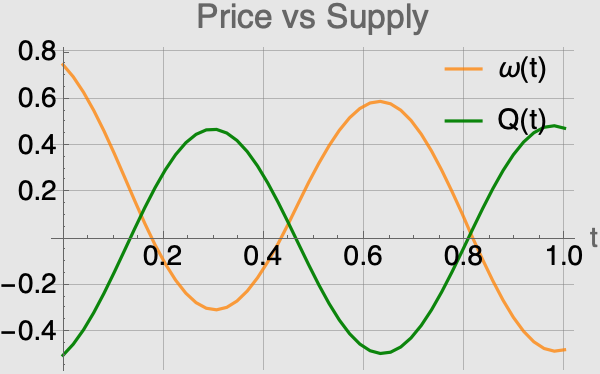

Our model presupposes a predefined supply function, denoted by .

The model imposes the equality between supply and demand:

|

|

|

(2.8) |

This condition, expressed using the Hamiltonian, becomes

|

|

|

(2.9) |

3. Main assumptions

Throughout this paper, we work under the following assumptions as in [11] and ensure that the model is well-posed.

Assumption 1.

Hamiltonian, , is the Legendre-Fenchel transform of a uniformly convex Lagrangian,

|

|

|

(3.1) |

where the market impact term, , is uniformly convex with a convexity constant ; that is, , and the preference potential is bounded from below.

The assumption that the market impact is independent of the agent’s current state aligns well with price models, where these costs are typically distinct from preference costs .

The convexity of , which penalizes oscillating trading strategies, is fundamental to the stability and uniqueness of the MFG system’s solutions.

Without it, the Hamiltonian becomes singular as in (3.1) the supremum could be if .

Assumption 2.

There exist constants and , such that

|

|

|

for all .

The uniform convexity of yields the strict convexity of with respect to the second variable and gives an upper bound for ; that is,

Assumption 2 implies .

The boundedness of the Hamiltonian’s derivatives is essential for the existence of solutions.

Assumption 3.

The potential , the terminal cost , and the initial density belong to .

Furthermore, there exists a constant such that

|

|

|

Assumption 4.

and are globally Lipschitz and convex.

The convexity of and give regularity and uniqueness of solutions, see [11].

Assumption 5.

The supply function, , belongs to .

The compactness assumption on initial distribution corresponds to

the case agent’s assets are bounded for the whole population.

Assumption 6.

The initial distribution function, , is compactly supported in , for some positive number .

Under assumptions 1-5, from [11], we have existence and uniqueness of solution , where is bounded, is Lipschitz, semiconcave, and differentiable in .

Moreover, from [3], is Lipschitz continuous.

Finally, assumption 6

ensures compact support of the

density function up to the terminal time .

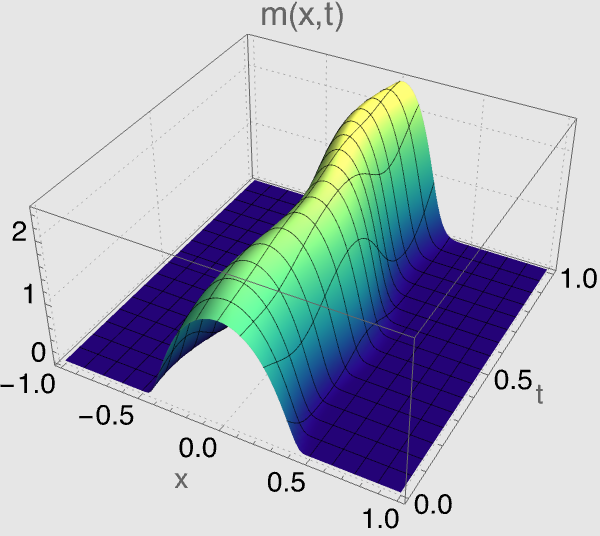

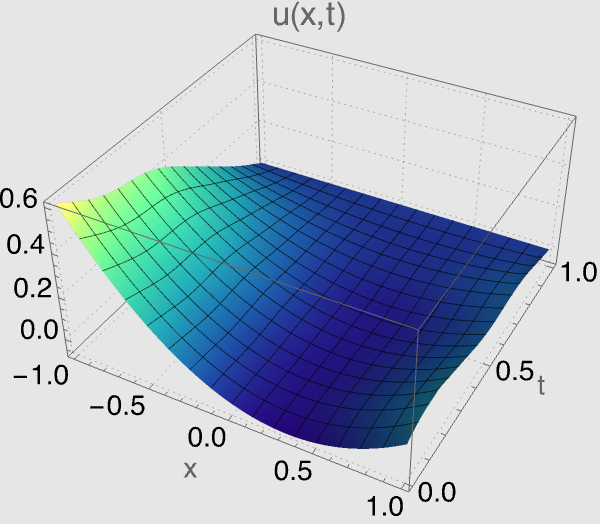

4. Discretization

In this section, we construct a discretized version of Problem 1. We use the dynamic programming principle and a fully discrete SL scheme to discretize the value function ; for the density function m, we use trajectories of the dynamics (2.1); finally, we discretize the balance condition to get an update rule for the price function .

The section concludes by presenting an algorithm

to solve the discretized system.

In a Semi-Lagrangian scheme, solutions of partial differential equations are approximated by following characteristics. For hyperbolic conservation laws and Hamilton-Jacobi equations, SL schemes are known for their stability and ability to handle sharp gradients or nonsmooth solutions.

To construct the discretization,

we introduce the following notations and definitions.

Let be an interval and a finite time.

For given positive numbers and , consider a grid

|

|

|

such that .

Consider a set of basis functions

that consist of compactly supported and infinitely differentiable functions , each compactly supported in , for , and , where is the Kronecker delta.

Furthermore,

|

|

|

(4.1) |

for all , and positive constants , depending only on .

Given values at the nodes , we define the interpolation function as

|

|

|

(4.2) |

This interpolation function is crucial for the Semi-Lagrangian discretization scheme, as it allows for the approximation of a function outside the grid .

Moreover our choice of the functions as a smooth partition of unity, ensures

that this approximation is smooth.

A well-known estimate (see, e.g., [10, 20]) states that for every bounded Lipschitz function , the following holds:

|

|

|

Finally, for clarity, we adopt the following notations: for any function and all indices , and , we denote the value of a function at the node by , and the vector by , and for any time-dependent function ,

.

For any function we denote its approximation function by .

Because our numerical algorithm is iterative,

is the approximation of at -th iteration.

4.1. Hamilton-Jacobi equation

We approximate by a function by replacing the right-hand side of (2.5)

with the following Semi-Lagrangian discretization

|

|

|

(4.3) |

where is the discretization of .

For and for the discrete Hamilton-Jacobi equation is

|

|

|

(4.4) |

where

|

|

|

(4.5) |

We note that the minimizer in (4.5) may not be unique. This matter can be addressed in one of two ways. Either by the conditions

in Lemma 5.3, which ensure the uniqueness of a minimizer,

or through the interpretation of the discretized system as a

multivalued monotone operator. This last approach is addressed in Section 6.

Here, in the remaining of this section, we suppose that is unique.

4.2. Continuity equation

The discretization of the Hamilton-Jacobi equation offers a method to approximate the value function.

Now, we consider the continuity equation, which complements this, approximating the time evolution of density functions.

Substituting by

in equation (2.7) , we get

|

|

|

Taking into account that ,

the preceding expression suggests

the discretization formula for

|

|

|

(4.6) |

for and , where we use the discretized flow given by

|

|

|

4.3. Balance condition

Here, we address the discretization of the last term in (1.1),

the balance condition. This discretization yelds an implicit formula for the price function:

|

|

|

(4.7) |

Notice that, since Hamiltonian is separable; therefore, is a function of alone.

From the feedback formula (2.6) and the definition of (4.5), we have

|

|

|

Substituting into the discretization of the balance condition (4.8), we get an implicit update rule for price, for each iteration ,

|

|

|

(4.8) |

for .

According to the prior discussion, the discretization

of the MFG system (1.1)-(1.2)

is represented by the system of equations (4.4), (4.6), and (4.8).

We employ an iterative algorithm outlined below to effectively solve this discretized system.

4.4. Algorithm

-

0)

Initialize , select an initial guess for the price, , and fix a tolerance parameter, .

-

1)

For and , find

|

|

|

and compute the value function, , using the discretization of the Hamilton-Jacobi equation:

|

|

|

-

2)

For and , compute the distribution function, , using the discretization of the Fokker-Planck equation:

|

|

|

-

3)

For , update the price, , from the following implicit equation

|

|

|

-

4)

If

|

|

|

stop, otherwise, set , and repeat steps .

Observe that the price function is defined up to the time step, since there is no optimization occurs at the terminal time.

To avoid notational clutter, subsequent sections omit the explicit dependence on for symbols representing approximation functions when the context is clear.

5. Some properties and estimates

This section establishes the theoretical foundation for our discretization scheme. Specifically, we establish several properties crucial to its well-definedness, consistency, and computational behavior. First, we demonstrate the existence and uniqueness of minimizers within the scheme. Next, we derive crucial bounds for the discretized variables, followed by proving that compactly supported initial distributions remains compactly supported.

Let the right-hand side of the value function discretization in (4.4) be denoted by

|

|

|

A well-defined numerical scheme must produce unique outputs and remain computationally tractable. We addresse this in the subsequent lemmas, establishing conditions for the existence of a unique minimizer and providing explicit bounds on this minimizer.

Lemma 5.1.

Under Assumption 1, enjoys the following properties:

-

i.

[Well-defined]

For bounded below function , there exists , at which the right-hand side attains its infimum.

-

ii.

[Monotone] For a fixed price , the discretization is monotone, i.e. if , we have

|

|

|

-

iii.

[Consistent] Let , as and grid points converge to , then for every , then

|

|

|

-

iv.

[Translation Invariance] For all

|

|

|

Proof.

-

i.

Let be a minimizing sequence, then

|

|

|

since is uniformly convex in , by Assumption 1.

-

ii.

Let and be minimizers for and , respectively.

Since ,

we have

|

|

|

|

|

|

|

|

-

iii.

Recall that is the Legendre-Fenchel transform of given by (3.1):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note that in the above identities, we can switch the limit with the infimum because

and by the coercivity of , we can restrict

to a compact set.

-

iv.

is linear and for any constant , .∎

The next lemma shows that the distribution function is a probability measure, and gives uniform estimates on value function and price, which are only dependent on the data of the problem, but not on a grid.

Lemma 5.2.

Suppose Assumptions 1, 3, 4 and 5 hold.

Let be the solution to the discretized system (4.4), (4.6), and (4.8).

Then the triplet satisfies the following properties:

-

i.

, for all ,

-

ii.

and for all ,

-

iii.

.

Proof.

-

i.

Using the density function discretization (4.6) and property (4.1), we get

|

|

|

|

|

|

|

|

To finish the proof, note that for

|

|

|

-

ii.

The bound follows from of Lemma 5.1, which gives us a lower bound, and from the discretization for the value function (4.4), we can get an upper bound taking :

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The Lipschitz estimate is obtained by using the discretization for the value function (4.4), and Assumption 4.

At point , we have

|

|

|

|

|

|

|

|

|

|

|

|

Because the preceding estimate is symmetric with respect to and , we get

|

|

|

Applying iteratively the same procedure for , yields:

|

|

|

|

|

|

|

|

-

iii.

This estimate follows from combining the results of and , and the discretization for balance condition (4.7). ∎

Next, we prove the uniqueness and boundedness of minimizer in (4.5).

Lemma 5.3.

Suppose Assumptions 1 and 3 hold.

Then, there exists a positive constant that depends only on the problem data, such that, if

|

|

|

then, has a unique minimizer . Moreover, there exists a positive constant , such that

|

|

|

for all .

Proof.

To prove the minimizer uniqueness, it suffices to show that the function

|

|

|

is strictly convex.

We need the second derivative of to be strictly positive

|

|

|

|

|

|

|

|

For strict positivity, we require

|

|

|

Now, we show the boundedness of minimizer.

Because is a minimizer of , we have

|

|

|

which gives a bound for :

|

|

|

By Assumption 1, the function is uniformly convex, so is monotone strictly increasing function. Thus, it can be bounded provided that is also bounded.

∎

Finally, we show that under the compactness assumption on initial distribution function, , there is a space and time discretization relation ensuring that agent’s assets remain bounded.

Lemma 5.4.

Suppose Assumption 6 holds, for some , and

|

|

|

for some positive constant .

Then, is compactly supported, that is there exists a positive constant , such that

, for all .

Proof.

By the definition of in (4.6), we have

|

|

|

Recall that are compactly supported in , the initial distribution function, , is compactly supported in , and from Lemma 5.3, , for some constant .

These yield that for to have non-zero values the following relations must hold:

|

|

|

Which means that may have non-zero values only for , where

|

|

|

Applying iteratively the same reasoning for , gives that is compactly supported in , where

|

|

|

Setting completes the proof.

∎

6. Monotonicity

In this section, we discuss the interpretation of the discretization (4.4), (4.6) and (4.8) as a multivalued map.

Then, we show that this map is monotone, which provides uniqueness of the discretized price.

Moreover, we show that the limit of the discretization is a weak solution to Problem 1.

In the continuous case, under the convexity condition of the map , the operator

|

|

|

associated with Problem 1 is monotone; that is, it satisfies

|

|

|

(6.1) |

where and are arbitrary elements from a proper domain, see [11].

The triplet is called a weak solution induced by monotonicity to Problem 1, if

|

|

|

(6.2) |

for every .

6.1. Multivalued map

A multivalued map from a set to a set is a map such that for each , there exists a non-empty subset , the value of at , denoted as

; that is,

|

|

|

where denotes the power set of .

Let be the set of all controls that minimize the discrete cost functional in (4.4), at the point , for a given price , that is,

|

|

|

In general, may contain multiple values .

Thus, the transport equation discretization depends on the particular choice of . However,

the value is uniquely defined.

Thus, it is natural to regard the discretization (4.4), (4.6) and (4.8) as a multivalued map that takes into account all possible choices of optimal controls.

For every , we define a multivalued map that returns a set of Hamilton-Jacobi, transport, and balance equations, as

|

|

|

The third component of corresponds to the balance condition written in

terms of , as in (2.8). The corresponding discretization, for , becomes

|

|

|

(6.3) |

Note that the factor in the third line does not change the solutions, but it is needed to make the operator monotone.

We define a multivalued operator as

|

|

|

(6.4) |

The subsequent discussion proves is monotone.

Lemma 6.1.

Under Assumption 1, the operator in (6.4) is monotone.

Proof.

Let , and let be a minimizer for

|

|

|

The following relations between the Lagrangians and hold true:

|

|

|

|

|

|

Further, we observe the following identity

|

|

|

|

|

|

|

|

Now, we show that satisfies the monotonicity condition,

(6.1).

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

This is nonnegative, because and are minimizers for and , respectively.

∎

6.2. Uniqueness

Here, we show the uniqueness of the solution for the discretized operator .

Proposition 6.2.

Suppose Assumptions 1 and 3 hold.

Let and be two solutions for the operator , that is, , and the condition in Lemma 5.3 is satisfied.

Then .

Proof.

From the proof of Lemma 6.1, we have

|

|

|

This yields that is also a minimizer for .

Similarly, is also a minimizer for .

Thus, , by Lemma 5.3.

Moreover, we get by the definition of .

Now, take in both and , and recall that :

|

|

|

|

|

|

|

|

For a given price , the map in the functional is injective.

This implies , which also means .

Applying this reasoning iteratively for , we get and , for every .

∎

6.3. Convergence

Here, we prove that the limit of a solution of is a weak solution to Problem 1.

Proposition 6.3.

Suppose Assumptions 1, 3–5 hold.

For , let , , and be a solution of operator .

By denote a step function that has values on the domain .

Then there exist subsequences in , in and in , as .

Moreover is a weak solution to Problem 1.

Proof.

From the Lemma 5.2, and are uniformly bounded, and is a probability measure on by its definition, that is, , for all .

Therefore, there exist , and , such that in , in and in ,

taking subsequences as needed, as .

Now, fix smooth functions and , such that and .

Define , and , and denote and .

Because , from the Lemma 6.1 we have:

|

|

|

|

|

|

|

|

Then, passing to the limit, when in this expression, concludes the proof.

∎