Deep Horseshoe Gaussian Processes

Supplementary material to ‘Deep horseshoe Gaussian processes’

Abstract

Deep Gaussian processes have recently been proposed as natural objects to fit, similarly to deep neural networks, possibly complex features present in modern data samples, such as compositional structures. Adopting a Bayesian nonparametric approach, it is natural to use deep Gaussian processes as prior distributions, and use the corresponding posterior distributions for statistical inference. We introduce the deep Horseshoe Gaussian process Deep–HGP, a new simple prior based on deep Gaussian processes with a squared-exponential kernel, that in particular enables data-driven choices of the key lengthscale parameters. For nonparametric regression with random design, we show that the associated tempered posterior distribution recovers the unknown true regression curve optimally in terms of quadratic loss, up to a logarithmic factor, in an adaptive way. The convergence rates are simultaneously adaptive to both the smoothness of the regression function and to its structure in terms of compositions. The dependence of the rates in terms of dimension are explicit, allowing in particular for input spaces of dimension increasing with the number of observations.

keywords:

[class=MSC]keywords:

, and

1 Introduction

Gaussian processes (henceforth GPs) are among the most used machine learning methods, with applications ranging from inference in regression models to classification, see e.g. [36] for an overview. Due to their flexibility, in recent years GPs have been used as tools for geometric inference and deep learning. Before turning to deep Gaussian processes, and since our results are also relevant for standard GPs, we start with a brief overview of recent results for Gaussian processes.

A particularly natural field of application where there now exists at least partial theory to explain and validate practical successes of GPs is that of Bayesian nonparametrics: the posterior distribution corresponding to taking a GP as prior distribution on functions can be used for function estimation as well as for the practically essential task of uncertainty quantification. In a regression setting, when putting a GP prior distribution on the unknown regression function, the corresponding posterior distribution can often be efficiently implemented [36] and come with theoretical convergence guarantees: the works [9, 51, 53] indeed show that the posterior contraction rate in terms of relevant loss functions (e.g. –loss for regression) is completely determined (both upper and lower bounds) by the behaviour of its concentration function. Shortly thereafter, van der Vaart and van Zanten also showed that statistical adaptation to smoothness was possible with GPs with optimal minimax contraction rates by simply drawing at random its scaling parameter [54] in fixed design regression; see [34, 52] for extensions to random design regression and [45] to inverse problems. Results on uncertainty quantification include [44], [55] in nonparametric models and [10, 13] in semiparametric settings.

Let us mention a few applications of posterior distributions arising from GPs that illustrate their flexibility and are related to the setting considered below.

GPs flexibility: geometric settings. In modern statistical models, it is frequent that data naturally sit on a geometric object such as a compact manifold (one can think of a sphere, a swissroll etc.). It is tempting to use GPs in this setting as well, although some care is needed in their construction. For instance, the celebrated GP with squared–exponential kernel (thereafter SqExp) has no immediate analog in a manifold setting, as replacing the euclidian metric in the exponential defining SqExp by the geodesic distance does not form a covariance kernel. This can be remediated by using a kernel coming from heat equation solutions on the manifold [11], and this kernel can be shown to be a natural geometric analog of SqExp. Alternatively, one may put a prior directly on the ambient space equipped with the standard euclidean metric: the authors in [56] obtain a posterior rate that under some (smoothness) conditions adapts to the unknown dimension of the manifold with a rescaled SqExp exponential GP, when the loss function is the quadratic loss but restricted to sit on the manifold.

GPs flexibility: adaptation to anisotropy and variable selection. By drawing independent lengthscale parameters along different dimensions, [6] shows that posteriors arising from SqExp GPs contract at near-optimal minimax anisotropic rates. A related problem is that of variable selection in (possibly high-dimensional) regression. The unknown regression function may indeed depend only on a few coordinates (although these are not known in advance). By considering variable selection type priors and then drawing lengthscale parameters of SqExp GPs, [57] and [26] provide theory for this setting and respectively investigate optimal rates and variable selection properties for the corresponding posterior distributions.

Recent years have seen a number of remarkable applications of deep learning methods, where ‘deep’ typically refers to a certain (often compositional) structure in terms of a number of layers. For instance, deep neural networks are now routinely trained for image or speech processing, giving excellent empirical performance. Theoretical understanding in terms of convergence of statistical procedures is recent and includes [27, 42] for results on empirical risk minimisers for classes of deep neural networks with ReLU activation function in regression settings. A Bayesian counterpart of the results in [42] with theoretical guarantees is considered in [37], where spike-and-slab priors are placed on network coefficients. Sampling directly from the corresponding posterior can be costly due to the combinatorial nature of the search of nonzero network coefficients; the works [5, 16] consider theory and implementation for mean-field variational Bayes versions thereof. Among similarities between GPs and neural networks, it has been shown in [32, 25, 18] that both deep and shallow Bayesian neural networks with random parameters (appropriately rescaled to avoid degeneracy) and with all layers of width growing to infinity asymptotically behave like GPs, with covariance kernel depending on the network structure. The Bayesian approach we describe in the next paragraphs avoids the use of large networks using activation functions by modelling layers directly through independent Gaussian processes.

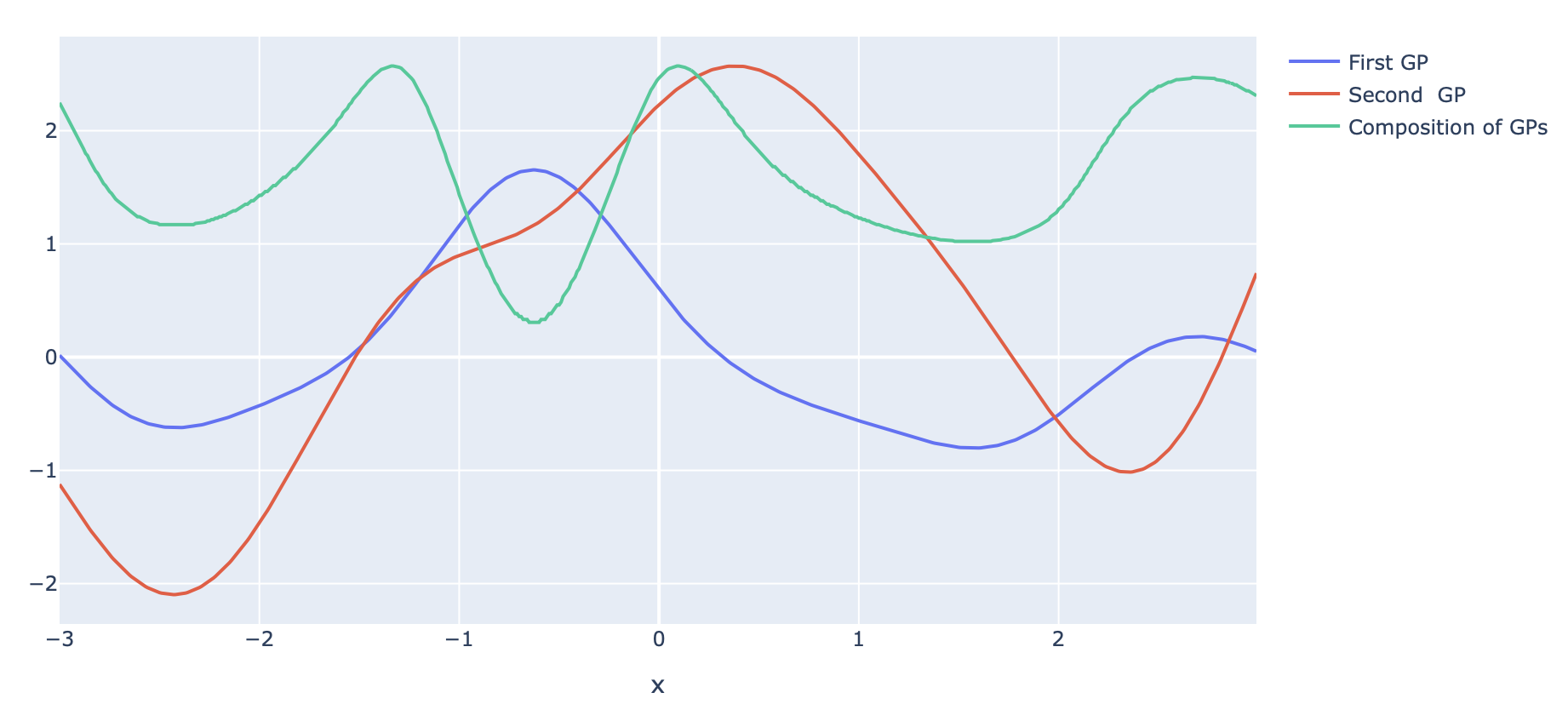

Deep Gaussian processes [17] (henceforth DeepGPs) correspond to iterated compositions of Gaussian processes and broadly speaking can be seen as a possible Bayesian analogue of deep neural networks. Figure 1 depicts the sample path of a simple DeepGP obtained from two independent GPs with squared-exponential kernels. The random paths resulting from DeepGPs have greater modelling flexibility compared to single Gaussian processes, enabling for instance to capture different spatial behaviours; [24] shows that single GPs cannot reach optimal rates for compositional structures, see also [1]. While the infinite-width limits of deep Bayesian neural networks behave like GPs, forcing instead some layers of the network to be of fixed width while letting others grow leads to a deepGP (see Section 7 of [20]). We indeed obtain in the limit the composition of the limiting GPs in-between the fixed layers. There is a lot of recent activity for providing efficient sampling methods for deepGPs [19, 38, 39]. Yet, theory is just starting to emerge.

The recent seminal work by Finocchio and Schmidt–Hieber [20] on deepGPs shows that using a model selection prior to select active variables in the successive Gaussian processes, and conditioning individual GP sample paths to verify certain smoothness constraints, the induced posterior distributions contract nearly optimally and adaptively in quadratic loss for compositional structures in regression, for a variety of kernel choices. Focusing on compositions of constrained GPs (with bounded sample paths and derivatives), the paper [4] uses an adapted concentration function for deepGPs and derives near-optimal contraction rates in density estimation and classification. In [1], the authors investigate the use of deepGPs for a class of nonlinear inverse problems.

This work follows the footsteps of [20] and aims at answering the following two questions. The first concerns the possibility to obtain theory and optimality results for a deepGP construction as simple as possible that comes closer to current implementations of deepGPs in practice. The second concerns the possibility to allow for a high-dimensional ambient space as well as a smaller intrinsic dimension.

-

1.

Can deepGP priors avoid an explicit model selection step?

While the deepGP prior construction in [20] is completely natural and ‘canonical’ from the theoretical perspective, both the conditioning step (to match smoothness constraints) and the model selection prior (for which the posterior on submodels is often expensive to compute) make posterior sampling involved in view of practical implementation. One main objective here is to try to simplify the construction of the prior as much as possible while keeping optimality properties, and thereby come closer to the practically used deepGPs, for which lengthscale parameters are often kept free and then adjusted in an empirical Bayes [17] or hierarchical Bayes [41] fashion. In view of this last observation, we propose a prior with a ‘soft’ model selection based on a prior on lengthscales instead of the previous ‘hard’ model selection prior. -

2.

How do deepGPs scale with respect to ‘dimension’?

Below we shall allow in some results the input space dimension to grow with . Even though any method must then face a ‘curse of dimensionality’, if the effective ‘intrinsic’ dimension of the problem remains fixed or very slowly grows with , it is conceivable that rates of convergence can still be obtained. While recent work on deep methods has shown that convergence rates only depending on intrinsic dimension(s) can be derived [42], most results are quite generous in the dependence on dimension of the constant factor in the rate. In particular, we are not aware of works allowing for input and ‘intrinsic’ dimensions to possibly grow with ([33] considers an example of Bayesian deep ReLU network with growing but fixed intrinsic dimension). We demonstrate below that our construction can adapt to the intrinsic dimension even for a high-dimensional ambient space (with sublinear in ). This requires a careful tracking of the dependence on dimension, in particular revisiting earlier results in the GP literature to make the dependence on precise.

The main contributions of the paper are as follows:

-

1.

we introduce a new idea of freezing–of–paths for multi-bandwidth Gaussian processes. The benefit of random lengthscales of a stationary kernel for adaptation to smoothness has been established for a while [6, 34, 52, 54]. Such an adaptation to the regularity of the underlying truth is made possible by letting the lengthscales grow polynomially with in a suitable way with sufficient probability under the prior. In the present paper, we show that letting lengthscales appropriately vanish (instead of diverge) enables adaptation to structure (instead of smoothness) or in other words to perform variable selection, by ‘freezing’ irrelevant dimensions through the corresponding (tempered) posterior distributions. Intuitively, sample paths become almost constant in the directions with vanishing lengthscales, performing effectively a form of ‘soft’ model selection.

-

2.

we show that the previous two effects of lengthscale parameters, namely adaptation to smoothness and to structure (by using respectively diverging and vanishing lengthscales), can be obtained using a single prior for lengthscales: the horseshoe distribution [8], that both puts a lot of mass near zero and at the tails, is shown to lead to optimal contraction rates with near-optimal scaling in terms of dimension. Our results also include exponential prior distributions on lengthscales as in earlier contributions on Gaussian processes (e.g. [54]), although dependence on dimension may not be optimal in ‘large ’ regimes.

-

3.

we study high-dimensional variable selection for standard smoothness classes and for compositional structures; in particular we allow the input dimension to grow polynomially with and the number of actually relevant variables to grow slowly with . A main technical contribution of the paper consists in deriving dimension-dependent analogues of the inequalities that are at the heart of GP regression theory with a squared-exponential kernel. Namely, we give precise dependence on ambient and intrinsic dimensions of the metric entropy of the unit ball of the RKHS of the covariance kernel, of the small ball probability of the GP and on quantities measuring approximation properties of this RKHS.

We note that the results are not only relevant for deep learning applications, but also already for shallow (standard) Gaussian processes, for which the freezing-of-paths effect described above is shown to lead to effective variable selection. Also, from the technical perspective, in order to leverage the smaller intrinsic dimensionality of the problem, a key new ingredient in the proofs consists in replacing the prior by a ‘low-dimensional’ oracle GP defined on the relevant coordinates. We also note that the results obtained in this paper are for tempered posterior distributions, where the tempering parameter can take any fixed value smaller than ; we refer to the discussion in Section 4 for more elements on this point and the currently open question of extending this to the standard posterior distribution (corresponding to a tempering parameter equal to ).

The paper is organised as follows: Section 2 introduces the statistical model and deep Gaussian process priors. We recall the main elements of a frequentist theoretical analysis of GP regression in Section 2.2. The main results are presented in Section 3: Theorem 2 deals with variable selection, possibly in high dimensions, for multibandwidth GPs. The case of adaptation to compositional structures via deep horseshoe GPs is considered in Theorems 3 and 4. A discussion follows in Section 4. Proofs are provided in Section 5. A key result underlying the proofs and bounding the GPs’ concentration function is presented in Section 6. Auxiliary lemmas and their proofs can be found in the appendix [12].

Notation. For two real numbers , we let , . We denote by the density of a standard normal random variable. The -covering number of a semimetric space equipped with a semimetric is the minimal number of balls of radius needed to cover . For a vector , denote

and for . For integrable on , let denote its Fourier transform, with the euclidean inner product. In the following, denote absolute constants whose value may change from line to line.

2 The deep horseshoe GP prior

Consider a nonparametric regression model with random design, where one observes , with independent identically distributed design points sampled from a probability measure on for an interval of chosen for simplicity to be in the sequel and

| (1) |

for an unknown regression function and independent errors, with assumed known for simplicity. We consider estimation of with respect to the integrated quadratic loss

For a given regression function , let denote the distribution of one observation under model (1), which has density

with respect to , for the Lebesgue measure on .

For a real , the largest integer strictly smaller than and an integer, let denote the classical Hölder space equipped with the norm . It consists of functions whose norm defined as

| (2) |

is finite, with the multi-index notation , and . We note that functions with finite Hölder norm are bounded, for any .

2.1 Structural assumptions for multivariate regression

In order to assess the performance of machine learning methods, a popular benchmark is the regression setting (1) equipped with some ‘ structural’ assumptions. In the unconstrained case where only a smoothness condition is assumed on , rates for –Hölder smooth functions are typically of the form , and so are prone to the curse of dimensionality (the rate becomes extremely slow for large ). A common approach is to assume that the multivariate regression function admits a certain unknown ‘structure’, of ‘effective dimension ’ possibly much smaller than . For instance, in the simplest setting considered below, may only depend on a small but unknown number of coordinates. The goal is then to find algorithms that are able to achieve optimal risk bounds that adapt to the unknown underlying structure, and that therefore scale with instead of .

A first basic setting: shallow variable selection. Let us first consider the simple setting where only depends on variables, that is

| (3) |

for some and . The subset of indices is unknown to the statistician and the target convergence rate in quadratic loss is .

Define, for and two integers, and recalling that ,

| (4) | ||||

As in recent works in deep learning and similar to [20], we assume that an upper-bound is known for the true function and without loss of generality we assume .

Compositional structure. Following [42], suppose that can be written as a composition

| (5) |

with , for a sequence of integers such that and . Since takes values in , one may write , where for are its –dimensional coordinate functions.

The compositional class . Let us further assume that ’s as above only depend on a subset of at most variables, and restricted to the variables belongs to . For , and , let

| (6) |

Minimax optimal rate. The minimax rate of estimation in quadratic loss over this class

for ranging over the set of estimators of , is, up to logarithmic factors,

| (7) |

under the mild condition , see [42].

2.2 Key ingredients

Posterior distributions and frequentist analysis. Given a prior distribution on regression functions, the posterior mass of a measurable set is given by Bayes’ formula: this is the next display for . More generally, one may set, for any ,

When this is the usual conditional probability that belongs to given the data. If , this quantity is called –posterior (or tempered posterior). Its use is very much widespread in machine learning, in particular in PAC–Bayesian settings [14, 58]. We use the tempered posterior in our main result, and discuss in more details the links with the case in Section 4.

Gaussian process (–) posteriors: theory. For any centered Gaussian process on the Banach space of continuous functions on equipped with the norm, the probability measure of any ball is lower bounded by a quantity depending on the mass of the centered ball of radius and on how well can be approximated by elements of the RKHS of the covariance kernel of the process. More precisely, according to Proposition 11.19 of [22], for any ,

| (8) |

The function in (2.2) is called the concentration function of the Gaussian process and plays a key role in the study of contraction rates for GPs [53]. It is the sum of two terms: the first term with the infimum is the approximation term whereas the second term is called the small ball term (the probability within the log is the small ball probability of the process ).

In nonparametric regression with fixed design, [54] proved that posterior contraction rates that are adaptive to the unknown smoothness of the regression function are achievable for stationary Gaussian process priors, with a dilatation parameter of the sample paths distributed as a Gamma variable. As a particular case, consider the squared exponential process SqExp defined as the zero-mean Gaussian process with covariance kernel (and the euclidean norm) on . Next, for , one sets

This construction induces a prior on the Banach space of continuous functions for which the posterior concentrates in the empirical norm at rate (up to a log factor) whenever has -Hölder regularity, .

Although this rate coincides with the minimax estimation rate over a ball in , it becomes very slow for large . However, if the fixed design is located on a -dimensional Riemannian manifold, , of the ambient space , we expect the faster rate to be attainable. The work [56] achieves it with a dilated Gaussian process as well, the dilatation factor being distributed as . One may note that this approach requires an estimate of to be applied and that posterior contraction rates are obtained for local distances on the manifold (such as the empirical -norm) only, but not on the ambient space.

When the regression function depends on a small number of variables only, a special case of the add-GP prior from [57] gives optimal posterior contraction rates without the need to estimate . This is achieved by the introduction of an additional layer in the prior, drawing via Bernoulli random variables in which direction the Gaussian sample paths have to be dilated (the sample paths being constant in the other directions). From a practical point-of-view, this ‘hard’ selection of variables adds a combinatorial complexity to posterior sampling.

Below, we introduce the Horseshoe Gaussian process prior to answer the question of variable selection and posterior contraction rates for the most natural global loss (in contrast to a loss e.g. restricted only on active directions) via a soft selection of dilated variables.

2.3 Deep Horseshoe Gaussian Process prior

We introduce a Gaussian process prior with independent inverse–lengthscales distributed following a half-horseshoe distribution. This distribution possesses two interesting properties for our goals. Its density has a pole at , which allows to ‘freeze’ irrelevant dimensions, drawing small inverse lengthscales with high probability. It also has heavy tails, so that it performs an adequate scaling on the ambient dimensions with sufficiently large probability.

The single-layer case. In the following, we use the real map

For a density function on , consider the following prior on regression functions

| (9) | ||||

where

for the squared exponential process SqExp. For a given value of , we call a multibandwidth Gaussian process.

Although the theory below can be applied to arbitrary scaling distributions , we consider two main examples in the sequel: an exponential and a horseshoe distribution. Let us define , , as the (half-) horseshoe density (introduced in [8]) i.e. the density of a random variable distributed as

with a standard half-Cauchy distribution and the half-normal distribution of , . We refer to [49] for posterior contraction results in the case of estimation of sparse vectors, with priors based on and discussions on the influence of .

When the horseshoe density on in (9), we call the above hierarchical prior the Horseshoe Gaussian Process prior and denote it .

The multi-layer case. In order to perform inference in more complex models, we introduce a deepGP-type prior, mixing ideas from [20] and the just introduced prior (9).

We first place discrete priors on the number of layers and on the successive ambient dimensions in the composition (5). We assume that and for any integers and .

Given , we define a random regression function where, for , the map is a multivariate Gaussian process indexed by and is applied element-wise. We assume that for , the coordinates are independently (accross and ) and identically (across ) distributed as a prior of the form (9). Constraining the sample paths between and ensures that the composition is well-defined.

The Deep Horseshoe Gaussian Process Deep–HGP is a special case of this construction where the prior on lengthscales is a horseshoe prior: it is defined as the hierarchical prior

| (10) |

for , . In the above, with , .

Some comments are in order. Here for full flexibility we draw first a prior on the number of compositions and ‘inner’ dimension parameters : at the –th level of the composition, there are coordinate functions distributed as the HGP process, each of these functions depending on parameters (and setting the output dimension). Note that on each layer , all variables are present simultaneously as input to each Gaussian process component, although the scalings (distributed as horseshoe random variables) calibrate the ‘strength’ (or ‘importance’) of these variables.

3 Main results: deep simultaneous adaptation to structure and smoothness

To gain intuition on our proposed procedure, we now build up progressively the results, starting from a standard smoothness condition in regression (no composition) where the regression function depends on an effective number of coordinates possibly smaller than the input dimension . Section 3.1 presents a simple oracle result while Section 3.2 considers more precise results allowing for adaptation and growing dimension. The ‘deep’ case of compositional structures is considered in Section 3.3. Recall that is the variance of the noise in (1) and set

| (11) |

3.1 “Freezing of paths" for variable selection: a new effect of scaling for Gaussian processes

The first result assumes that the true regression function depends on a number of coordinates only, and that for now the indices of the active variables are known.

Theorem 1 (freezing of paths).

Let be a fixed integer and for , set . Fix , let and suppose

with and some . Let be a multibandwidth prior

with a –dimensional SqExp Gaussian process with deterministic scaling parameters

| (12) |

Then, there exists such that the –posterior verifies

Theorem 1 shows that by taking GP lengthscale parameters that are very small, of order , for the coordinates such that in fact does not depend on , and taking lengthscales equal to the ‘standard nonparametric cut-off’ (for estimating –smooth functions in dimension ) on the other coordinates, leads to an optimal minimax contraction rate for the integrated squared loss up to a logarithmic factor for the –posterior distribution (the power in the log factor is improved in the next result). Inspection of the proof shows that for , one may take to be any value smaller than for some fixed .

The intuition behind the result is that taking a small lengthscale for coordinate ‘freezes’ the GP path along this coordinate, making it almost constant in that coordinate, which corresponds to the limiting case . Note that Theorem 1 is an ‘oracle’ result in that it assumes both and (and even the indices ) to be known. Adaptive versions are considered below. While the result is somewhat expected if one sets for (this would correspond to a ‘hard’ variable selection), the fact that the rate remains optimal for small but non-zero values of suggests that there may be room for a ‘soft’ variable selection procedure that would allow for small in a data-driven way: this is the purpose of our next Theorem.

3.2 Single layer setting: horseshoe GP

The next statement is our main result on variable selection for (non-deep) Gaussian processes. It is a non-asymptotic result that allows for dimensions varying with . It is stated for an arbitrary prior on lengthscales. We then particularise it over the next paragraphs by stating simpler asymptotic versions and giving examples of lengthscale priors that satisfy the conditions. We consider both the fixed dimensional case and the case where both and vary with .

Theorem 2 (Variable selection).

Theorem 2 gives a contraction of the –posterior distribution at rate around the true , provided is suitably large. A more explicit expression of is given in the next Corollary.

Corollary 1 (Optimal and posterior rate).

In the asymptotic regime , for taken equal to the right hand-side of (16), it follows that and , so that provided (13) holds, the posterior mass in the last display of Theorem 2 goes to , and the posterior contracts to at rate asymptotically. For reasonable (i.e. fixed or growing slowly with ) values of , the first term in (16) dominates and, again under (13), the resulting rate goes to with . Next we investigate a few examples of priors for which (13) holds with a resulting given by (16).

The proof of Theorem 2 is based on

considering an oracle process defined on the relevant dimensions. The rates can then carry over to the full prior thanks to Condition (13), which ensures that the lengthscale prior tunes down irrelevant dimensions, so that the difference between the processes is small with high probability. These deviations are controlled via new dimension–dependent estimates of characteristics of the squared-exponential Gaussian process (via its RKHS), see Theorem 5 and Lemmas 2–4, coupled with concentration of measures tools. This theorem is a main theoretical novelty of the paper: a lengthscale prior which puts large mass on small values allows to ‘freeze’ irrelevant directions, so that the overall prior behaves like a smaller-dimensional one.

Fixed dimensions. Let us now examine the case where the dimensions are fixed, independent of . We derive conditions on two natural priors: an exponential prior, as used e.g. in [53] for adaptation to smoothness, and a horseshoe prior.

Example 1 (Exponential prior with fixed scaling ).

Example 2 (Horseshoe prior with fixed parameter ).

To obtain (18), one simply uses that the horseshoe density is bounded from below by a constant on the integration interval; this is sensible for a fixed but can be significantly improved for small , as seen below.

Corollary 2 (Fixed dimensions).

In the setting of Theorem 2, suppose the input dimension is fixed (independent of ). Let be either the exponential prior or the horseshoe prior with fixed (independent of ) respective parameters and . Then for large enough (depending on only), as ,

where is given by . In particular, the posterior distribution achieves the minimax convergence rate up to a logarithmic factor.

An important consequence of Corollary 2 is that it is possible to derive a (near-)optimal rate adapting to the unknown number and coordinates of the active variables with continuous priors, that is, even without setting the scaling exactly to zero on certain coordinates (i.e. without performing a ‘hard model selection’). Even more surprisingly at first, such ‘soft model selection’ is possible (at least with tempered posteriors) using a prior not putting a particularly large amount of mass near , such as an exponential prior. In particular, simple priors on scalings such as exponentials or gamma distributions considered in [53] have prior mass permitting for ‘enough’ variable selection in order for their (tempered)–posterior distribution to contract at near optimal rate, without using oracle knowledge of which coordinates are active or not.

At this point it may seem as if variable selection can be achieved at no cost with just simple random scalings on coordinates. This is not (completely) so, the reason being that the dependence on the input dimension in the convergence rate that arises from e.g. putting exponential priors on scalings is far from optimal. This can be seen from (17), or similarly (18) for with fixed , as follows. Recall that (17)–(18) are non-asymptotic conditions, so one may let depend on . Suppose for instance for some and is fixed, say to fix ideas. Then (17) cannot hold with the lower bound in (16): indeed, the latter is up to a log-factor of order , so is a as soon as , which shows that in this setting the rate is suboptimal for large enough ’s.

The previous comments naturally make one wonder if variable selection is still feasible with a better dependence on dimensions with continuous scaling. The next section investigates this, in a setting where can go to with .

High-dimensional variable selection. Let us now study the problem of variable selection if is possibly allowed to depend on . In the high-variable selection problem as in the first setting of Section 2.1, the work [57] derives up to constants the minimax rate of estimation for the squared loss which is up to a constant factor depending on , and ,

The first term corresponds to the rate of estimation of a low-dimensional function and the second is the rate for the variable selection problem. Under Condition (19) below, the first term dominates. Note however that, as the dependence of the constants in is not explicit in the last display, this result allows for and a fixed but not both going to infinity.

Let us consider the high-dimensional variable selection setting where can go to infinity; we also allow the effective dimension to slowly grow with : more precisely for some and suppose

| (19) |

One may hope to obtain a convergence rate that depends on the effective dimension only, not on . In Appendix E [12], Corollary 4, we derive a lower bound result that shows that under mild conditions on the design distribution, and if the radius of the considered Hölder ball is not too large, the minimax rate for the integrated quadratic risk is bounded below by , for constants independent of . We show below that this rate can be achieved by a well-chosen horseshoe GP in the regime (19), up to a slowly-varying term . To do so, one first determines a horseshoe scaling parameter for which condition (13) holds, and then we state the high-dimensional variable selection result as Corollary 3 (more details on optimality can be found below in Section E Corollary 4).

Example 3 (Horseshoe prior with vanishing parameter ).

Corollary 3 (High-dimensional horseshoe GP).

In the setting of Theorem 2, suppose verify Condition (19). Let be the multibandwidth prior (9) with horseshoe scaling density and , . Then, for , there exists such that

as where, for some constant that depends on only,

In particular, for , the rate is of order , up to a smaller order term at most of order .

The rate obtained in Corollary 3 is optimal in the minimax sense up to the smaller order term (up to a log factor). As mentioned above, as long as does not grow faster than this is a slower order term compared to the main term (in regime (19)) in the minimax lower bound from Corollary 4: in this case the rate is minimax optimal up to a slower order term . We also note that a growth in for the radius of the Hölder ball is typical for functions in Hölder spaces of dimension , see Appendix D [12], where this is checked for functions of product form.

The idea behind Corollary 3 is that for small values of the parameter , the horseshoe distribution becomes very ‘sparse’ in the sense that most nonzero values are very close to : this is reminiscent of the high-dimensional statistics literature for sparse models, see e.g. [50, 48], where near-optimal posterior rates for horseshoe posteriors are derived in sparse settings. We now turn to a deep learning setting, where the Gaussian process is allowed to have several compositional layers.

3.3 Multilayer setting: Deep Horseshoe GP

We go back for now to the fixed dimensional case, but we consider the additional problem of adaptation to an unknown compositional structure. The following result shows that, assuming the regression function can be expressed as a composition (5), such adaptation can be achieved with a prior mimicking this structure and organizing Gaussian processes in layers. In particular, in the Deep–HGP prior, the distribution on the scalings of the individual Gaussian processes allows for adaptation to the regularity as we have seen above, but also adaptation to a sparse network of compositions.

Theorem 3.

Let , , , and suppose . Let be the Deep–HGP prior (10) with fixed parameters . Then, for any , contracts to at the rate

in distance, where : for any

Theorem 3 shows that the fractional posterior attains the minimax rate of convergence of contraction (7) over the class up to the logarithmic factor , . For simplicity, we only considered the situation where inverse-bandwidths are distributed as horseshoe random variables. As above in the fixed setting with GPs, one can derive similar results for exponential priors on scalings. However, given the benefits of the horseshoe prior in high-dimensional settings (see also below), we focus on this choice.

Theorem 3 can be compared to Theorem 2 of [20], providing rates for a deepGP construction over a compositional functional class. The present result on the Deep–HGP prior now shows that adaptation to the structure can be achieved with –posteriors without imposing a hyperprior on all the parameters describing the structure. It is sufficient to specify a prior on the depth and width of the composition. As in our results of Section 3.2 on (single-layer) GPs, instead of imposing a ‘hard’ selection of relevant variables on each layer, a continuous distribution on the lengthscales, with sufficient mass on small values, is enough for simultaneous adaptation to smoothness and sparse compositional structure.

In view of Corollary 3, one naturally wonders if the Deep–HGP prior is able to perform adaptation to the structure and the regularity in a high-dimensional framework as well. More precisely, suppose belongs to with and possibly depending on . As in (19), we suppose verify, for some and ,

| (21) |

The next result shows that letting the horseshoe scale parameter of the first layer in the composition vanish in the Deep–HGP prior, while keeping the other scale parameters across the other layes, constant, is enough to still obtain a near-minimax rate of contraction for the fractional posterior. Choosing appropriately small (although independent of the true unknown ) allows one obtain sparsity on the first layer, mitigating the effect of the growing input dimension .

Theorem 4.

To the best of our knowledge, Theorem 4 is the first result on deep methods in high-dimensional regression where both the input dimension and first effective dimension are allowed to grow with . It combines both the ability of the horseshoe prior to select relevant dimensions in the input space and its ability to perform model selection in presence of a compositional parameter. It is particularly interesting given that these methods are most often applied to high-dimensional problems.

Compared to the condition on in Corollary 3, the preceding result requires a smaller . In the present setting, given the flexibility of the sample paths from deep Gaussian processes, it is necessary to ’stabilize’ each GP to avoid ’wild’ behavior. From a technical point of view, it translates into more restrictive prior mass conditions for these GPs and the need for more efficient variable selection. This is achieved with a horseshoe prior that is more peaked near , given the choice of the smaller parameter.

Remark 1.

In Theorem 4, we let the dimensions indexed by on the first layer of the composition to possibly grow with . Extending this result to a situation where can also grow with is not straightforward. Indeed, inspection of the proof of Theorems 3 and 4 shows that the rate involves a multiplicative factor whose dependence on the inner dimensions of the composition is linear and thus prevents polynomially growing ’s. As this factor does not involve , it still allows for as in (21).

4 Discussion and open questions

In this work, we provide theoretical guarantees for the convergence of fractional posterior distributions using deep Gaussian process priors. One key insight is in the role played by lengthscale parameters: not only do these enable adaptation to smoothness, but they can also at the same time perform variable selection by ‘freezing’ the Gaussian process paths in suitable directions, a point relevant also for standard (non-deep) Gaussian processes; this has not been recognised so far in the literature to the best of our knowledge. The fact that adaptation to smoothness and structure can be performed simultaneously is particularly appealing computationally in that there is no need to include a model selection part in the building of the prior (if that was the case, posterior sampling would require to have access to the posterior distribution over models, which is often costly to implement). The obtained deepGP prior is then simple enough so that it corresponds to recently proposed algorithms, see below for more on this. One possible (at least formal) limitation to our results is the fact that the results are valid for any fractional posterior () but that they do not apply to the standard posterior (). We argue below that this does not represent an essential limitation for statistical inference if one is willing to lose slightly in terms of constants in front of the convergence rates, which is generally considered acceptable for most nonparametric models. We also derive new results on deep methods for high-dimensional input space, and on the way obtain explicit dimension-dependent constants for the characteristics of the involved GPs.

The use of fractional posteriors. We obtain our main results for fractional posterior distributions, where the parameter can be taken to be any constant in . The main reason for this is of technical nature: in order for one to use the general theory of convergence of Bayesian posteriors in [21], one needs to build sieve sets, capturing most prior mass, whose entropy or ‘complexity’ is well controlled. However, especially in complex settings such as deep learning models, sieves can be difficult to construct, in particular since the probability of the complement of the sieve is required to have a form of exponentially fast decrease, with at the same time the requirement to control the entropy of the sieve set. This difficulty leads [20] to condition sample paths of Gaussian processes to verify certain smoothness constraints. This can be avoided using –posteriors, since convergence of these can be guaranteed under prior mass conditions only [7, 28, 30, 58], so we do not need to condition on boundedness of derivatives in our prior construction. This is an advantage also computationally, as adding more conditioning constraints may typically slow down MCMC samplers.

A natural question is whether the results for fractional posteriors obtained here also hold for the standard posterior (). It seems delicate to answer this using the current tools available for proving posterior convergence; given that construction of sieves (while keeping the prior simple) looks particularly difficult, it is conceivable that, at least in say regression settings, one may be able to state an adapted version of the generic theorem of [21]. Although beyond the scope of the present contribution, one may note that promising results are obtained in [3], where in regression with heavy-tailed priors both standard and fractional posteriors are shown to converge at the same rate up to constants, for a prior for which the construction of sieves seems also presently out of reach, which suggests that posterior convergence for under prior mass conditions only is not exceptional.

On the other hand, we argue that, at least for the set of applications of Bayesian (possibly tempered) posteriors considered here, one does not loose much, except slightly in the constants in the convergence rate: here as is fixed (and can be chosen e.g. to be ) we did not keep the dependence in in the constants, but it is shown in [30] that nonparametric rates arising from –fractional posteriors are typically the same as for the usual posterior but with effective sample size ; for the constant in terms of in the rate is not particularly large then, so is not a main concern. Also, regarding sampling algorithms in practice, most sampling methods such as MCMC are of similar difficulty with the fractional or the original likelihood, so this is not a main concern computationally (we discuss below sampling from deepGP fractional posteriors from Example 1). One loses, though, the interpretation of the posterior as a conditional distribution and possibly efficiency for –estimable parameters that comes with the Bernstein–von Mises theorem, which will not hold as such for –posteriors but again typically with a variance inflated by ; this can be remedied under some conditions though, as investigated in [30]. However, again, this is not a main concern here, as we are mainly interested in estimation rates up to constants.

Simulations. Although our main focus here is on theoretical guarantees, we note that sampling from the deep Gaussian process fractional posteriors with exponential priors on GP lengthscales (Example 1) is readily available using the R package deepgp [40]. The later provides MCMC samples for standard posteriors () using Vecchia approximation; one can similarly obtain MCMC samples from fractional posteriors with any using the following remark. Note that using a fractional likelihood with a given to form the fractional posterior in Gaussian regression with independent errors is equivalent to using the standard likelihood in the case the errors are misspecified as independent . Since posterior sampling is conditional on the observed values, and the deepgp package allows for specifying a given noise level, it suffices to specify it to the misspecified value (while data will truly be generated with errors of variance ). We refer to [41] for illustrations and details on the sampling schemes (we note that it should also be possible to modify the code, which presently allows for Gamma priors, to include horseshoe priors on lengthscales as in Examples 2–3).

For given lengthscale parameters, the prior considered in the present work coincides with that considered in the paper [17] introducing deepGPs, where the kernel is termed ARD (Automatic Relevance Determination) and the lengthscales are called weights. In [17], the weights/lengthscales are then calibrated using a variational approach. Many different posterior approximating schemes for deepGPs have been proposed over the last few years, using in particular variational approximations; we refer to [41] for an overview and discussion. Obtaining theoretical guarantees for these different approaches, in particular for the Deep HGP posteriors introduced here, is an interesting avenue for future work.

5 Proof of the main results

We denote by the spectral measure of the squared-exponential SqExp process. Let us recall that this process is stationary with covariance and that by Bochner’s theorem ; in particular it follows that has Lebesgue density .

Preliminaries: reducing the problem to a prior mass condition. Given a rate , Theorem 6 and Proposition 1 in Appendix F [12] ensure that if satisfies, for and ,

| (22) |

then the fractional posterior is such that, for the –Rényi divergence as in (66),

Let us now focus on the considered regression model. Assuming that the regression functions we consider are bounded, say , using and both for and the additivity of the Rényi divergence for densities of independent observations, it follows that

| (23) |

We note that under the regularity assumptions on and with the use of the ‘link’ function , the boundedness assumption is satisfied for both and a draw from the posterior in our different theorems. Consequently, in the following, the proofs consist in proving (22) for as in the different statements and for the different priors considered. This will imply

which suffices to conclude.

5.1 Proof of Theorem 1

5.2 Proof of Theorem 2

Given , let us denote by the concentration function of the Gaussian process as in (9) and its RKHS by . To derive the result, we prove below that (22) is satisfied, since any satisfies and by definition. Also, since , we bound this last quantity instead as it then implies (22) for .

Since we assume , we have for some . Let us set, for and ,

for as in the statement of the Theorem. For a given vector , let us introduce with for . For any ,

One may now split the contribution of ’s into subsets of indices as follows

In what follows we bound from below and above respectively the quantities, for ,

| (24) | ||||

| (25) |

In the bounds to follow, we use that the involved scaling parameters belong to the respective intervals defined above.

Starting with (24), denote . Conditionally on the ’s, the Gaussian process , interpreted as a process on variables indexed by only, has the same distribution as the Gaussian process on (they are both centered with same covariance kernel; in slight abuse of notation we denote also for the process in the –dimensional space). Since is independent of for , for ,

The term can then be bounded from below by

where we use Lemma 1 to bound from below the probability in the display.

We now use Theorem 5 applied to , a function with input dimension . We set to be chosen so that . Suppose,

| (26) | |||||

| (27) |

where are constants of the form as in the statement of Theorem 5. Up to making larger, one can always assume . Below we will also use that if verifying the last display exist, then . Indeed, the last term in the second inequality is bounded from below by . As one must have where , so that .

By Theorem 5 we have , uniformly for . One deduces

Let us now deal with the term in (25). First one notes that, given A,

is a centered Gaussian process. In order to bound it, one first computes

using for any and . Setting , , , ,

For , using again ,

For any , we have , using the inequalities and . Deduce

Combining the previous bounds one obtains, for any ,

On the other hand, using for any , we have

According to Lemma 9, since almost surely, we have

Writing , this quantity is upper bounded by

using for , which is the case here since (see also below). By a change of variable , the upper bound is, with ,

Integrating by parts, . For we have so that . Let us apply this to the previous bound, noting that , using the upper bound on obtained above and the definition of . One obtains, using that is increasing on , and that

Assuming , we obtain for some universal ,

One can now use Gaussian concentration to control the deviations of from its expectation. Suppose

| (28) |

Combining Lemma 8 and the above bound on gives

| (29) |

Recall that, for ,

which gives , so that the last but one display is bounded from above by , uniformly for in the corresponding interval . One deduces

Combining this with the obtained lower-bound on , one gets, using if , that , so that

| (30) |

where we used (13).

Let us now optimise in terms of verifying the conditions (26)–(27)–(28). Since

for , we have that (28) holds if, for some depending on ,

| (31) |

Now turning to , recalling and , it suffices to have, using and as noted earlier,

| (32) |

where and , with universal constants. We note that (32) implies (31) for large enough, using and (which implies ). This concludes the proof of Theorem 2, provided .

5.3 Proof of Theorem 3

The proof of Theorem 2 needs to be suitably generalized and modified: as we shall see below, the considered balls for the various layers of the composition need to have carefully chosen radii. To obtain the results, one needs to verify the prior mass condition (22) for as in the statement of the theorem. For any where , we now have

Let us now fix and , such that we focus on the marginal distribution of . Lemma 7 indeed ensures that for any , denoting ,

| (33) |

for . Since the are bounded by in supnorm, the factors in the above product are lower bounded by

If we can find such that the above quantity is lower bounded by , then we can verify that such that , for

is a posterior contraction rate thanks to (22). Having ensures that the remaining mass in Theorem 6 in Appendix F [12] is vanishing, so that is indeed a contraction rate. Indeed, up to the constant factor

independent of , we can derive (22) from the lower bound on the right-hand side of (33)

Indeed, as long as , we could replace with , , for such that . Since the left side of (22) increases when replacing with , (22) would be satisfied with . This is enough as we seek to express up to a large enough constant.

From here, we can continue as in the proof of Theorem 2. Since we assume , we have for some . Let us set, for , , and

the intervals

for . Let’s also consider an arbitrary vector such that for (in the following, we note for simplicity). If we can show , and, constants of the form , , as in the statement of Theorem 5,

| (34) | ||||

| (35) |

(counterparts of (26) and (27)) and, for some ,

| (36) | ||||

| (37) |

(the first is a counterpart of (28), the second ensures that an upper bound obtained as in (29) is further upper bounded by , as ). Under these conditions, we can conclude

in the same way we obtained (30).

From (37), which is satisfied by definition of , and , (36) is satisfied whenever

| (38) |

for some . Now turning to , recalling and , it suffices to have, using and as noted earlier,

| (39) |

where and , with universal constants. If , we note that (39) implies (38) for large enough, using , and (which implies ).

Optimising in (32), leads to setting

| (40) |

Condition (39) then becomes, for as in (40),

| (41) |

where , recalling , and are constants only depending on . For equal to the lower bound in (41), we indeed have and, for large enough, . Condition (37) is then satisfied by definition.

It now remains to prove that given the definition of and condition (40). Using the fact that , a straightforward modification of the proof of Lemma 17 gives that it is satisfied for a parameter satisfying

| (42) |

whenever . This last condition is satisfied for any fixed as and . Also, equation (42) is satisfied for large enough as the left-hand side has a polynomial growth and the right-hand side has a logarithmic growth in .

This concludes the proof of Theorem 3.

5.4 Proof of Theorem 4

We proceed as in the proof of Theorem 3 but with the new horseshoe prior with shrinking parameter on the lengthscales of the first layer, with special attention to that layer of GPs, , as may now go to infinity. As in Corollary 3, for , we now have

| (43) |

which as , under (21), is equal to , for depending on , and , . Also the condition on becomes

| (44) |

for as in (40) and depending and , via a slight modification of Lemma 18. As it is satisfied under the assumption of the theorem, this concludes the proof.

6 Dimension-dependent bounds for multibandwidth SqExp Gaussian processes

In order to prove posterior contraction rates for deep GPs, a key step is to derive an upper bound for the concentration function (2.2). The next Theorem enables us in particular to revisit Lemmas 4.2 and 4.3 from [6], with explicit multiplicative constants depending on the ambient dimension in the result. This is a novel contribution to the literature on squared-exponential GPs, to the best of our knowledge. Also, these results allow us to deploy the HGP and Deep–HGP priors in the high-dimensional setting. For simplicity we do not consider here the anisotropic case in which the function can have varying smoothness across coordinates, although this could be done as well, following the approach of [6]. We focus on the variable selection aspect of the problem, assuming the same regularity on the active directions of .

Theorem 5.

Let be a SqExp Gaussian process in dimension with deterministic vector of scalings with for and some . Let be the concentration function of . Suppose for some . There exist constants and depending only on and a universal such that, if

then

Moreover, for one can take for some constants that depend only on .

[Acknowledgments] The authors would like to thank François Bachoc, Agnès Lagnoux, Johannes Schmidt-Hieber and Aad van der Vaart for insightful comments. {funding} This work is co-funded by ANR GAP project (ANR-21-CE40-0007) and the European Union (ERC, BigBayesUQ, project number: 101041064).

References

- [1] {bmisc}[author] \bauthor\bsnmAbraham, \bfnmKweku\binitsK. and \bauthor\bsnmDeo, \bfnmNeil\binitsN. (\byear2023). \btitleDeep Gaussian Process Priors for Bayesian Inference in Nonlinear Inverse Problems. \bnoteArxiv preprint 2312.14294. \endbibitem

- [2] {bbook}[author] \beditor\bsnmAbramowitz, \bfnmMilton\binitsM. and \beditor\bsnmStegun, \bfnmIrene A.\binitsI. A., eds. (\byear1992). \btitleHandbook of mathematical functions with formulas, graphs, and mathematical tables. \bpublisherDover Publications, Inc., New York \bnoteReprint of the 1972 edition. \bmrnumber1225604 \endbibitem

- [3] {barticle}[author] \bauthor\bsnmAgapiou, \bfnmSergios\binitsS. and \bauthor\bsnmCastillo, \bfnmIsmaël\binitsI. (\byear2023). \btitleHeavy-tailed Bayesian nonparametric adaptation. \bnotearXiv e-print 2308.04916. \endbibitem

- [4] {barticle}[author] \bauthor\bsnmBachoc, \bfnmFrançois\binitsF. and \bauthor\bsnmLagnoux, \bfnmAgnès\binitsA. (\byear2021). \btitlePosterior contraction rates for constrained deep Gaussian processes in density estimation and classification. \bnoteArxiv preprint 2112.07280. \bdoi10.48550/ARXIV.2112.07280 \endbibitem

- [5] {binproceedings}[author] \bauthor\bsnmBai, \bfnmJincheng\binitsJ., \bauthor\bsnmSong, \bfnmQifan\binitsQ. and \bauthor\bsnmCheng, \bfnmGuang\binitsG. (\byear2020). \btitleEfficient Variational Inference for Sparse Deep Learning with Theoretical Guarantee. In \bbooktitleAdvances in Neural Information Processing Systems \bvolume33 \bpages466–476. \endbibitem

- [6] {barticle}[author] \bauthor\bsnmBhattacharya, \bfnmAnirban\binitsA., \bauthor\bsnmPati, \bfnmDebdeep\binitsD. and \bauthor\bsnmDunson, \bfnmDavid\binitsD. (\byear2014). \btitleAnisotropic function estimation using multi-bandwidth Gaussian processes. \bjournalThe Annals of Statistics \bvolume42 \bpages352–381. \endbibitem

- [7] {barticle}[author] \bauthor\bsnmBhattacharya, \bfnmAnirban\binitsA., \bauthor\bsnmPati, \bfnmDebdeep\binitsD. and \bauthor\bsnmYang, \bfnmYun\binitsY. (\byear2019). \btitleBayesian fractional posteriors. \bjournalThe Annals of Statistics \bvolume47 \bpages39 – 66. \bdoi10.1214/18-AOS1712 \endbibitem

- [8] {barticle}[author] \bauthor\bsnmCarvalho, \bfnmCarlos M.\binitsC. M., \bauthor\bsnmPolson, \bfnmNicholas G.\binitsN. G. and \bauthor\bsnmScott, \bfnmJames G.\binitsJ. G. (\byear2010). \btitleThe horseshoe estimator for sparse signals. \bjournalBiometrika \bvolume97 \bpages465-480. \bdoi10.1093/biomet/asq017 \endbibitem

- [9] {barticle}[author] \bauthor\bsnmCastillo, \bfnmIsmaël\binitsI. (\byear2008). \btitleLower bounds for posterior rates with Gaussian process priors. \bjournalElectron. J. Stat. \bvolume2 \bpages1281–1299. \bdoi10.1214/08-EJS273 \bmrnumber2471287 \endbibitem

- [10] {barticle}[author] \bauthor\bsnmCastillo, \bfnmIsmaël\binitsI. (\byear2012). \btitleA semiparametric Bernstein-von Mises theorem for Gaussian process priors. \bjournalProbability Theory and Related Fields \bvolume152 \bpages53–99. \bmrnumber2875753 \endbibitem

- [11] {barticle}[author] \bauthor\bsnmCastillo, \bfnmIsmaël\binitsI., \bauthor\bsnmKerkyacharian, \bfnmGérard\binitsG. and \bauthor\bsnmPicard, \bfnmDominique\binitsD. (\byear2014). \btitleThomas Bayes’ walk on manifolds. \bjournalProbab. Theory Related Fields \bvolume158 \bpages665–710. \bdoi10.1007/s00440-013-0493-0 \bmrnumber3176362 \endbibitem

- [12] {barticle}[author] \bauthor\bsnmCastillo, \bfnmI.\binitsI. and \bauthor\bsnmRandrianarisoa, \bfnmT.\binitsT. (\byear2024). \btitleSupplementary material to ’Deep Horseshoe Gaussian Processes’. \endbibitem

- [13] {barticle}[author] \bauthor\bsnmCastillo, \bfnmIsmaël\binitsI. and \bauthor\bsnmRousseau, \bfnmJudith\binitsJ. (\byear2015). \btitleA Bernstein–von Mises theorem for smooth functionals in semiparametric models. \bjournalAnn. Statist. \bvolume43 \bpages2353–2383. \bdoi10.1214/15-AOS1336 \bmrnumber3405597 \endbibitem

- [14] {bbook}[author] \bauthor\bsnmCatoni, \bfnmOlivier\binitsO. (\byear2004). \btitleStatistical learning theory and stochastic optimization. \bseriesLecture Notes in Mathematics \bvolume1851. \bpublisherSpringer-Verlag, Berlin \bnoteLecture notes from the 31st Summer School on Probability Theory held in Saint-Flour, July 8–25, 2001. \bdoi10.1007/b99352 \bmrnumber2163920 \endbibitem

- [15] {barticle}[author] \bauthor\bsnmChang, \bfnmAlan\binitsA. (\byear2017). \btitleThe Whitney extension theorem in high dimensions. \bjournalRev. Mat. Iberoam. \bvolume33 \bpages623–632. \bdoi10.4171/RMI/952 \bmrnumber3651018 \endbibitem

- [16] {binproceedings}[author] \bauthor\bsnmChérief-Abdellatif, \bfnmBadr-Eddine\binitsB. (\byear2020). \btitleConvergence Rates of Variational Inference in Sparse Deep Learning. In \bbooktitleProceedings of the 37th International Conference on Machine Learning, ICML 2020. \bseriesProceedings of Machine Learning Research \bvolume119 \bpages1831–1842. \endbibitem

- [17] {binproceedings}[author] \bauthor\bsnmDamianou, \bfnmAndreas\binitsA. and \bauthor\bsnmLawrence, \bfnmNeil D.\binitsN. D. (\byear2013). \btitleDeep Gaussian Processes. In \bbooktitleProceedings of the Sixteenth International Conference on Artificial Intelligence and Statistics. \bseriesProceedings of Machine Learning Research \bvolume31 \bpages207–215. \endbibitem

- [18] {binproceedings}[author] \bauthor\bparticlede \bsnmG. Matthews, \bfnmAlexander G.\binitsA. G., \bauthor\bsnmHron, \bfnmJiri\binitsJ., \bauthor\bsnmRowland, \bfnmMark\binitsM., \bauthor\bsnmTurner, \bfnmRichard E.\binitsR. E. and \bauthor\bsnmGhahramani, \bfnmZoubin\binitsZ. (\byear2018). \btitleGaussian Process Behaviour in Wide Deep Neural Networks. In \bbooktitleInternational Conference on Learning Representations. \endbibitem

- [19] {barticle}[author] \bauthor\bsnmDutordoir, \bfnmVincent\binitsV., \bauthor\bsnmSalimbeni, \bfnmHugh\binitsH., \bauthor\bsnmHambro, \bfnmEric\binitsE., \bauthor\bsnmMcLeod, \bfnmJohn\binitsJ., \bauthor\bsnmLeibfried, \bfnmFelix\binitsF., \bauthor\bsnmArtemev, \bfnmArtem\binitsA., \bauthor\bsnmvan der Wilk, \bfnmMark\binitsM., \bauthor\bsnmHensman, \bfnmJames\binitsJ., \bauthor\bsnmDeisenroth, \bfnmMarc P.\binitsM. P. and \bauthor\bsnmJohn, \bfnmST\binitsS. (\byear2021). \btitleGPflux: A Library for Deep Gaussian Processes. \bjournalarXiv e-prints \bpagesarXiv:2104.05674. \bdoi10.48550/arXiv.2104.05674 \endbibitem

- [20] {barticle}[author] \bauthor\bsnmFinocchio, \bfnmGianluca\binitsG. and \bauthor\bsnmSchmidt-Hieber, \bfnmJohannes\binitsJ. (\byear2023). \btitlePosterior contraction for deep Gaussian process priors. \bjournalJournal of Machine Learning Research \bvolume24 \bpages1–49. \endbibitem

- [21] {barticle}[author] \bauthor\bsnmGhosal, \bfnmSubhashis\binitsS., \bauthor\bsnmGhosh, \bfnmJayanta K.\binitsJ. K. and \bauthor\bparticlevan der \bsnmVaart, \bfnmAad W.\binitsA. W. (\byear2000). \btitleConvergence rates of posterior distributions. \bjournalAnn. Statist. \bvolume28 \bpages500–531. \bdoi10.1214/aos/1016218228 \bmrnumber1790007 \endbibitem

- [22] {bbook}[author] \bauthor\bsnmGhosal, \bfnmSubhashis\binitsS. and \bauthor\bparticlevan der \bsnmVaart, \bfnmAad\binitsA. (\byear2017). \btitleFundamentals of nonparametric Bayesian inference. \bseriesCambridge Series in Statistical and Probabilistic Mathematics \bvolume44. \bpublisherCambridge University Press, Cambridge. \bdoi10.1017/9781139029834 \bmrnumber3587782 \endbibitem

- [23] {bbook}[author] \bauthor\bsnmGiné, \bfnmEvarist\binitsE. and \bauthor\bsnmNickl, \bfnmRichard\binitsR. (\byear2016). \btitleMathematical foundations of infinite-dimensional statistical models. \bseriesCambridge Series in Statistical and Probabilistic Mathematics, [40]. \bpublisherCambridge University Press, New York. \bdoi10.1017/CBO9781107337862 \bmrnumber3588285 \endbibitem

- [24] {binproceedings}[author] \bauthor\bsnmGiordano, \bfnmMatteo\binitsM., \bauthor\bsnmRay, \bfnmKolyan\binitsK. and \bauthor\bsnmSchmidt-Hieber, \bfnmJohannes\binitsJ. (\byear2022). \btitleOn the inability of Gaussian process regression to optimally learn compositional functions. In \bbooktitleAdvances in Neural Information Processing Systems \bvolume35 \bpages22341–22353. \endbibitem

- [25] {barticle}[author] \bauthor\bsnmHazan, \bfnmTamir\binitsT. and \bauthor\bsnmJaakkola, \bfnmTommi\binitsT. (\byear2015). \btitleSteps toward deep kernel methods from infinite neural networks. \bjournalarXiv preprint arXiv:1508.05133. \endbibitem

- [26] {barticle}[author] \bauthor\bsnmJiang, \bfnmSheng\binitsS. and \bauthor\bsnmTokdar, \bfnmSurya T.\binitsS. T. (\byear2021). \btitleVariable selection consistency of Gaussian process regression. \bjournalAnn. Statist. \bvolume49 \bpages2491–2505. \bdoi10.1214/20-aos2043 \bmrnumber4338372 \endbibitem

- [27] {barticle}[author] \bauthor\bsnmKohler, \bfnmMichael\binitsM. and \bauthor\bsnmLanger, \bfnmSophie\binitsS. (\byear2021). \btitleOn the rate of convergence of fully connected deep neural network regression estimates. \bjournalAnn. Statist. \bvolume49 \bpages2231–2249. \bdoi10.1214/20-aos2034 \bmrnumber4319248 \endbibitem

- [28] {bincollection}[author] \bauthor\bsnmKruijer, \bfnmWillem\binitsW. and \bauthor\bparticlevan der \bsnmVaart, \bfnmAad\binitsA. (\byear2013). \btitleAnalyzing posteriors by the information inequality. In \bbooktitleFrom probability to statistics and back: high-dimensional models and processes. \bseriesInst. Math. Stat. (IMS) Collect. \bvolume9 \bpages227–240. \bpublisherInst. Math. Statist., Beachwood, OH. \bdoi10.1214/12-IMSCOLL916 \bmrnumber3202636 \endbibitem

- [29] {barticle}[author] \bauthor\bsnmKuelbs, \bfnmJames\binitsJ. and \bauthor\bsnmLi, \bfnmWenbo V.\binitsW. V. (\byear1993). \btitleMetric entropy and the small ball problem for Gaussian measures. \bjournalJ. Funct. Anal. \bvolume116 \bpages133–157. \bdoi10.1006/jfan.1993.1107 \bmrnumber1237989 \endbibitem

- [30] {barticle}[author] \bauthor\bsnmL’Huillier, \bfnmAlice\binitsA., \bauthor\bsnmTravis, \bfnmLuke\binitsL., \bauthor\bsnmCastillo, \bfnmIsmaël\binitsI. and \bauthor\bsnmRay, \bfnmKolyan\binitsK. (\byear2023). \btitleSemiparametric Inference Using Fractional Posteriors. \bjournalJournal of Machine Learning Research \bvolume24 \bpages1–61. \endbibitem

- [31] {barticle}[author] \bauthor\bsnmLi, \bfnmWenbo V.\binitsW. V. and \bauthor\bsnmLinde, \bfnmWerner\binitsW. (\byear1999). \btitleApproximation, metric entropy and small ball estimates for Gaussian measures. \bjournalAnn. Probab. \bvolume27 \bpages1556–1578. \bdoi10.1214/aop/1022677459 \bmrnumber1733160 \endbibitem

- [32] {bbook}[author] \bauthor\bsnmNeal, \bfnmRadford M\binitsR. M. (\byear2012). \btitleBayesian learning for neural networks \bvolume118. \bpublisherSpringer Science & Business Media. \endbibitem

- [33] {bmisc}[author] \bauthor\bsnmOhn, \bfnmIlsang\binitsI. and \bauthor\bsnmLin, \bfnmLizhen\binitsL. (\byear2022). \btitleAdaptive variational Bayes: Optimality, computation and applications. \bnoteeprint Arxiv 2109.03204. \endbibitem

- [34] {barticle}[author] \bauthor\bsnmPati, \bfnmDebdeep\binitsD., \bauthor\bsnmBhattacharya, \bfnmAnirban\binitsA. and \bauthor\bsnmCheng, \bfnmGuang\binitsG. (\byear2015). \btitleOptimal Bayesian estimation in random covariate design with a rescaled Gaussian process prior. \bjournalJ. Mach. Learn. Res. \bvolume16 \bpages2837–2851. \bmrnumber3450525 \endbibitem

- [35] {bbook}[author] \bauthor\bsnmPisier, \bfnmGilles\binitsG. (\byear1989). \btitleThe volume of convex bodies and Banach space geometry. \bseriesCambridge Tracts in Mathematics \bvolume94. \bpublisherCambridge University Press, Cambridge. \bdoi10.1017/CBO9780511662454 \bmrnumber1036275 \endbibitem

- [36] {bbook}[author] \bauthor\bsnmRasmussen, \bfnmCarl Edward\binitsC. E. and \bauthor\bsnmWilliams, \bfnmChristopher K. I.\binitsC. K. I. (\byear2006). \btitleGaussian processes for machine learning. \bseriesAdaptive Computation and Machine Learning. \bpublisherMIT Press, Cambridge, MA. \bmrnumber2514435 \endbibitem

- [37] {binproceedings}[author] \bauthor\bsnmRocková, \bfnmVeronika\binitsV. and \bauthor\bsnmPolson, \bfnmNicholas\binitsN. (\byear2018). \btitlePosterior Concentration for Sparse Deep Learning. In \bbooktitleAnnual Conference on Neural Information Processing Systems 2018, NeurIPS 2018 \bpages938–949. \endbibitem

- [38] {binproceedings}[author] \bauthor\bsnmSalimbeni, \bfnmHugh\binitsH. and \bauthor\bsnmDeisenroth, \bfnmMarc\binitsM. (\byear2017). \btitleDoubly Stochastic Variational Inference for Deep Gaussian Processes. In \bbooktitleAdvances in Neural Information Processing Systems \bvolume30. \endbibitem

- [39] {binproceedings}[author] \bauthor\bsnmSalimbeni, \bfnmHugh\binitsH., \bauthor\bsnmDutordoir, \bfnmVincent\binitsV., \bauthor\bsnmHensman, \bfnmJames\binitsJ. and \bauthor\bsnmDeisenroth, \bfnmMarc\binitsM. (\byear2019). \btitleDeep Gaussian Processes with Importance-Weighted Variational Inference. In \bbooktitleProceedings of the 36th International Conference on Machine Learning. \bseriesProceedings of Machine Learning Research \bvolume97 \bpages5589–5598. \endbibitem

- [40] {bmanual}[author] \bauthor\bsnmSauer, \bfnmAnnie\binitsA. (\byear2022). \btitledeepgp: Deep Gaussian Processes using MCMC \bnoteR package version 1.1.1. \endbibitem

- [41] {barticle}[author] \bauthor\bsnmSauer, \bfnmAnnie\binitsA., \bauthor\bsnmCooper, \bfnmAndrew\binitsA. and \bauthor\bsnmGramacy, \bfnmRobert B.\binitsR. B. (\byear2023). \btitleVecchia-Approximated Deep Gaussian Processes for Computer Experiments. \bjournalJournal of Computational and Graphical Statistics \bvolume32 \bpages824-837. \bdoi10.1080/10618600.2022.2129662 \endbibitem

- [42] {barticle}[author] \bauthor\bsnmSchmidt-Hieber, \bfnmJohannes\binitsJ. (\byear2020). \btitleNonparametric regression using deep neural networks with ReLU activation function. \bjournalAnn. Statist. \bvolume48 \bpages1875–1897. \bdoi10.1214/19-AOS1875 \bmrnumber4134774 \endbibitem

- [43] {bbook}[author] \bauthor\bsnmStein, \bfnmElias M.\binitsE. M. (\byear1971). \btitleSingular Integrals and Differentiability Properties of Functions (PMS-30), Volume 30. \bpublisherPrinceton University Press, \baddressPrinceton. \bdoidoi:10.1515/9781400883882 \endbibitem

- [44] {barticle}[author] \bauthor\bsnmSzabó, \bfnmBotond\binitsB., \bauthor\bparticlevan der \bsnmVaart, \bfnmAad W.\binitsA. W. and \bauthor\bparticlevan \bsnmZanten, \bfnmHarry\binitsH. (\byear2015). \btitleFrequentist coverage of adaptive nonparametric Bayesian credible sets. \bjournalAnn. Statist. \bvolume43 \bpages1391–1428. \bnote(with discussion). \endbibitem

- [45] {barticle}[author] \bauthor\bsnmTeckentrup, \bfnmAretha L.\binitsA. L. (\byear2020). \btitleConvergence of Gaussian process regression with estimated hyper-parameters and applications in Bayesian inverse problems. \bjournalSIAM/ASA J. Uncertain. Quantif. \bvolume8 \bpages1310–1337. \bdoi10.1137/19M1284816 \bmrnumber4164077 \endbibitem

- [46] {barticle}[author] \bauthor\bsnmTomczak-Jaegermann, \bfnmNicole\binitsN. (\byear1987). \btitleDualité des nombres d’entropie pour des opérateurs à valeurs dans un espace de Hilbert. \bjournalC. R. Acad. Sci. Paris Sér. I Math. \bvolume305 \bpages299–301. \bmrnumber910364 \endbibitem

- [47] {bbook}[author] \bauthor\bsnmTsybakov, \bfnmAlexandre B.\binitsA. B. (\byear2009). \btitleIntroduction to nonparametric estimation. \bseriesSpringer Series in Statistics. \bpublisherSpringer, New York \bnoteRevised and extended from the 2004 French original, Translated by Vladimir Zaiats. \bdoi10.1007/b13794 \bmrnumber2724359 \endbibitem

- [48] {barticle}[author] \bauthor\bparticlevan der \bsnmPas, \bfnmStéphanie\binitsS., \bauthor\bsnmSzabó, \bfnmBotond\binitsB. and \bauthor\bparticlevan der \bsnmVaart, \bfnmAad\binitsA. (\byear2017). \btitleUncertainty quantification for the horseshoe (with discussion). \bjournalBayesian Anal. \bvolume12 \bpages1221–1274. \bnoteWith a rejoinder by the authors. \bdoi10.1214/17-BA1065 \bmrnumber3724985 \endbibitem

- [49] {barticle}[author] \bauthor\bparticlevan der \bsnmPas, \bfnmS. L.\binitsS. L., \bauthor\bsnmKleijn, \bfnmB. J. K.\binitsB. J. K. and \bauthor\bparticlevan der \bsnmVaart, \bfnmA. W.\binitsA. W. (\byear2014). \btitleThe horseshoe estimator: Posterior concentration around nearly black vectors. \bjournalElectronic Journal of Statistics \bvolume8 \bpages2585 – 2618. \bdoi10.1214/14-EJS962 \endbibitem

- [50] {barticle}[author] \bauthor\bparticlevan der \bsnmPas, \bfnmS. L.\binitsS. L., \bauthor\bsnmKleijn, \bfnmB. J. K.\binitsB. J. K. and \bauthor\bparticlevan der \bsnmVaart, \bfnmA. W.\binitsA. W. (\byear2014). \btitleThe horseshoe estimator: posterior concentration around nearly black vectors. \bjournalElectron. J. Stat. \bvolume8 \bpages2585–2618. \bdoi10.1214/14-EJS962 \bmrnumber3285877 \endbibitem

- [51] {barticle}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmAad\binitsA. and \bauthor\bparticlevan \bsnmZanten, \bfnmHarry\binitsH. (\byear2007). \btitleBayesian inference with rescaled Gaussian process priors. \bjournalElectron. J. Stat. \bvolume1 \bpages433–448. \bdoi10.1214/07-EJS098 \bmrnumber2357712 \endbibitem

- [52] {barticle}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmAad\binitsA. and \bauthor\bparticlevan \bsnmZanten, \bfnmHarry\binitsH. (\byear2011). \btitleInformation rates of nonparametric Gaussian process methods. \bjournalJ. Mach. Learn. Res. \bvolume12 \bpages2095–2119. \bmrnumber2819028 \endbibitem

- [53] {barticle}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmA. W.\binitsA. W. and \bauthor\bparticlevan \bsnmZanten, \bfnmJ. H.\binitsJ. H. (\byear2008). \btitleRates of contraction of posterior distributions based on Gaussian process priors. \bjournalAnn. Statist. \bvolume36 \bpages1435–1463. \bdoi10.1214/009053607000000613 \bmrnumber2418663 \endbibitem

- [54] {barticle}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmA. W.\binitsA. W. and \bauthor\bparticlevan \bsnmZanten, \bfnmJ. H.\binitsJ. H. (\byear2009). \btitleAdaptive Bayesian estimation using a Gaussian random field with inverse gamma bandwidth. \bjournalAnn. Statist. \bvolume37 \bpages2655–2675. \bdoi10.1214/08-AOS678 \bmrnumber2541442 \endbibitem

- [55] {barticle}[author] \bauthor\bsnmYang, \bfnmYun\binitsY., \bauthor\bsnmBhattacharya, \bfnmAnirban\binitsA. and \bauthor\bsnmPati, \bfnmDebdeep\binitsD. (\byear2017). \btitleFrequentist coverage and sup-norm convergence rate in Gaussian process regression. \bjournalarXiv e-prints \bpagesarXiv:1708.04753. \bdoi10.48550/arXiv.1708.04753 \endbibitem

- [56] {barticle}[author] \bauthor\bsnmYang, \bfnmYun\binitsY. and \bauthor\bsnmDunson, \bfnmDavid B.\binitsD. B. (\byear2016). \btitleBayesian manifold regression. \bjournalThe Annals of Statistics \bvolume44 \bpages876 – 905. \bdoi10.1214/15-AOS1390 \endbibitem

- [57] {barticle}[author] \bauthor\bsnmYang, \bfnmYun\binitsY. and \bauthor\bsnmTokdar, \bfnmSurya T.\binitsS. T. (\byear2015). \btitleMinimax-optimal nonparametric regression in high dimensions. \bjournalAnn. Statist. \bvolume43 \bpages652–674. \bdoi10.1214/14-AOS1289 \bmrnumber3319139 \endbibitem

- [58] {barticle}[author] \bauthor\bsnmZhang, \bfnmTong\binitsT. (\byear2006). \btitleFrom -entropy to KL-entropy: analysis of minimum information complexity density estimation. \bjournalAnn. Statist. \bvolume34 \bpages2180–2210. \bdoi10.1214/009053606000000704 \bmrnumber2291497 \endbibitem

This supplementary material contains the proof of Theorem 5 as well as the proofs of a number of technical lemmas. It also contains results on Hölder spaces in increasing dimensions (Appendices D and E), including a lower bound for the minimax rate in regression in this setting. Appendix F is concerned with fractional posteriors, while Appendix G verifies the conditions for different priors on scalings.

Appendix A Proof of Theorem 5

In order to prove Theorem 5, we need to bound from above the concentration function of the SqExp Gaussian process .

Recall that the concentration function of the Gaussian process with RKHS is

The form of the RKHS for the SqExp Gaussian process is recalled in Section A.1. Then, in Lemma 2 and 3, we bound successively the two parts of the in the last display for in terms of , the scale parameters and the smoothness of . Combining the conclusions of the two Lemmas, one obtains Theorem 5. ∎

A.1 RKHS of multi-bandwidth SqExp Gaussian process

The RKHS of the SqExp process with bandwidth sequence has been characterised in [54], Lemma 4.1, in case of a common bandwidth , result extended in [6], Lemma 4.1, to the case of different bandwidths.

The space is the set of real parts of functions

| (45) |

where the spectral measure admits a density with respect to Lebesgue measure, and runs over the complex Hilbert space . We recall that in the case of the SqExp process is given by .

Also, the results of [54, 6] show, since has an interior point, that the squared-RKHS norm of the element of in the last display is

| (46) |

The key role played by the RKHS in the characterization of posterior contraction rates for Gaussian processes priors is explained by the following lemma.

A.2 Dimension-dependent upper bounds on the concentration function

Dimension-dependent bound on the approximation term. Let us denote for and an integer,

| (47) |

The following lemma deals with the "approximation" part of the concentration function.

Lemma 2.

Suppose as in (47) for some and an integer. Let be such that for and . Then, there exist positive constants and that depend only on such that

Moreover, for one can take for some constants that depend only on .

Proof.

We revisit the proof of Lemma 4.2 from [6], making the dependence in dimension explicit. Let be a complex-valued function such that , ,

and its Fourier transform is compactly supported (all integrals being over ).

Define by and

By Lemma 12, we extend to a function with . Next we set , where is a –function, equal to on , to outside of and with (from Lemma 11, it suffices to build such a function, say , for the case , and to set ), where only depend on . By construction, the function equals on , has compact support within , and by Leibniz’s rule and the same argument as in the proof of Lemma 11

where only depends on .

Additionally, is the set of real parts of functions for the measure with Lebesgue density and (see Appendix A.1). The corresponding RKHS norm is also equal to the –norm of . The convolution is then an element of since for any