Stochastic gradient descent for streaming linear and rectified linear systems with Massart noise

Abstract

We propose SGD-exp, a stochastic gradient descent approach for linear and ReLU regressions under Massart noise (adversarial semi-random corruption model) for the fully streaming setting. We show novel nearly linear convergence guarantees of SGD-exp to the true parameter with up to Massart corruption rate, and with any corruption rate in the case of symmetric oblivious corruptions. This is the first convergence guarantee result for robust ReLU regression in the streaming setting, and it shows the improved convergence rate over previous robust methods for linear regression due to a choice of an exponentially decaying step size, known for its efficiency in practice. Our analysis is based on the drift analysis of a discrete stochastic process, which could also be interesting on its own.

1 Introduction

Robust regression aims to develop regression methods that provide a proper fit of the data, even in the presence of outliers. Such outliers can arise, for example, from labeling mistakes during the data-gathering process [5], incorrect measurements in tomography [27], transmission errors [13], or adversarial attacks [4, 35] in distributed machine learning. On the other hand, the high-dimensionality and just sheer volume of modern datasets pose significant challenges in machine learning. Stochastic algorithms such as stochastic gradient descent (SGD) are standard approaches to address this high dimensionality, as they utilize only a part of the dataset at a time [14, 36, 7]. Moreover, in many modern applications, data is streamed, meaning that methods cannot retain past data and are only allowed to work with a given small portion of data at a time in such scenarios. In the fully streaming setting, an algorithm typically processes one data point at a time and cannot revisit past data points [18, 31]. Such constraints arise from limited memory, the immediacy of real-time processing, or just the vast volume of the data. These challenges have naturally led to the development of robust regression methods suited for the streaming setting.

1.1 Robust linear and ReLU regression

Robust regression has a long history and has played an important role in both statistics and machine learning. Its goal is to learn the fitting parameters, even when the observations are contaminated by a constant fraction of adversarial outliers [37, 20, 6, 24, 9, 28]. In particular, fitting generalized linear models is a fundamental subject in statistics [22, 21]. One important case arises when the nonlinear function is the ReLU activation function. Recently, ReLU regression has garnered a lot of attention due to its relevance to neural networks [33, 42, 23, 10].

In the non-streaming setting, robust linear regression can be formulated in the following way. For a system of linear equations , suppose that a certain fraction of entries in are replaced with arbitrary values so that we have for some error vector instead. Recently, Haddock et al. [16] have proposed two methods based on the quantile estimate of residual of the current iterate, one is based on the randomized Kaczmarz algorithm, and the other is based on the loss function which is known to be robust to outliers in general [19, 25]. Although these methods are effective in solving corrupted systems of linear equations, they may not be suitable for the time-sensitive streaming setting, due to the possible computational burden in estimating quantiles. Possible ways to alleviate these time/memory requirements for estimation include using a sliding window [16], approximate quantile estimation [15], and in more general SGD context, choosing the data point with the lowest loss value after observing a sufficiently large number of data points per iteration [32]. However, none of these methods would apply to the fully streaming scenario, where accessing any past data is not possible. At the same time, the corruption model considered in these works might be too strong for the streaming setting. Essentially, it implies that in the worst case a presumed adversary can examine all past equations to choose the worst possible placement of corrupted measurements. Here, we consider a semi-random Massart noise model as described below.

1.2 On corruption models

Let us recall several main models of adversarial corruption here. By adversarial corruption model we imply that the corruptions do not stem from a particular distribution but can be added in arbitrary way. Thus we do not assume an existence of an actual adversary (although it might be a convenient to describe a model and in some of the applications) but rather that the proposed methods are expected to work in the worst case.

In the fully adversarial corruption model, as in QuantileSGD and QuantileRK methods in [16], before we run the methods, the adversary can select any measurements and replace them with any values (so it can depend on the true parameter and measurement vectors) as long as the corruption fraction is . This effectively makes the setting non-streaming for the adversary. For this noise model, the question about how much of the corruption fraction can be tolerated by SGD-exp or any reasonable streaming learning method appears to be still open. Even stronger adversarial models such as those considered in [7], allow for the adversarial to modify the measurement vectors as well.

In the Massart noise model (this work, also [11]), the adversary cannot choose which measurements to corrupt. Instead, the measurement is randomly selected for corruption with probability . Then, the adversary replaces it with any values (so again, it can depend on the true parameter and the associated parameter vectors). For example, in the streaming setting, with probability , an adversary can inspect a data point at each time and replace the associated label with any incorrect label to confuse the receiver as much as possible. This includes the sign-flip corruption.

Lastly, in the oblivious response corruption model (e.g., [11, 31]), there is essentially no adversary. Each measurement is randomly selected with a probability of and then corrupted by additive random noise that is independent with the associated measurement vector and the true parameter. This is the weakest corruption model used in works such as [31]. This excludes noise types such as sign-flip noise, which is covered in our outlier model, the Massart noise model.

1.3 Contribution summary

Here, we propose the SGD-exp method to solve the minimization problem efficiently in the streaming setting. Since in our streaming setting each data point arrives one at a time, the most generic yet natural corruption model is the Massart noise as described above. As such, we do not require the observations to be obliviously corrupted nor that the magnitude or moments of corruption to be bounded. This is an informal version of our theoretical results, Theorems 3 and Theorem 4:

Theorem 1.

Let be an unknown vector, let for represent streaming measurements of . Here, is the Massart noise with corruption probability , the measurement vectors satisfy Gaussian-like assumptions and can be an identity or a ReLU function. There exists a constant such that for any , if we take and run iterations of -SGD

| (1) |

where is a subgradient of for iterations, then, with high probability, we have

The proof of main theorems relies on type of analysis that is, to the best of our knowledge, new in the robust regression literature. It is based on drift analysis of the stochastic process after we have transformed the residual equation of SGD, and can be interesting on its own.

As a result, the proposed method SGD-exp (1) provides (nearly) linear convergence guarantees for any corruption probability less than , which is the best possible for the Massart noise model. Our analysis also reveals that SGD-exp tolerates any corruption probability less than when the corruption is symmetric oblivious noise111Actually, the only assumption we need is (the random outlier is positive) = (the random outlier is negative). for the streaming setting, answering a related question in [34].

To the best of our knowledge, our approach provides the first nearly linear convergence guarantees for both linear regression and ReLU regression under the adversarial Massart noise model (see discussion above and Assumption 1 below for the formal definition) in the fully streaming setting.

1.4 Related works

For the linear regression in the streaming environment with oblivious random corruption, Pesme and Flammarion [31] have proposed a method (which we will refer to as SGD-root due to the square-root decaying step size scheduling), which is based on the SGD for the loss, as well as SGD-exp. Compared to it, SGD-exp comes with a faster convergence rate under a less restricted corruption model. Specifically, running SGD-root for -iterations to recover -dimensional signals only provides recovery accuracy, whereas our method guarantees the recovery error of the order of . In [31], the outliers are generated by the random oblivious response corruption model, which excludes noise types such as sign-flip noise, which are covered in the Massart noise model that we consider. SGD-root also requires the corruption noise to have a finite first absolute moment, whereas we do not require any such condition.

Diakonikolas et al. study robust linear and ReLU regression under the Massart noise model in [11], but their approach is not designed for the streaming setting and does not provide an explicit convergence rate in terms of the number of iterations. In [8], Diakonikolas et al. study robust regression for generalized linear models. Although this work considers more general distributions and activation functions, it is not for the streaming setting, and the corruption model is the oblivious response corruption, weaker than the Massart noise.

In [7], the authors consider an even more general contamination model where the measurement vectors can also be modified by the adversary. Due to this general model assumption, the error does not decay below , where is the corruption probability, even if we increase the number of iterations. Moreover, without any distributional assumption on the measurement vectors, the recovery of the true parameter is information-theoretically impossible in general [11, 29]. The works [10, 41] aim to find a parameter to minimize the risk function, assuming that the covariates and contaminated responses are jointly random along with an additional condition on the size of contaminated responses. Neither of these conditions is required for our convergence guarantees.

1.5 SGD with exponential decay step size

The exponential step decay scheduling or its variants for SGD are commonly used as a default setting in many popular machine learning software packages, including TensorFlow [1] and PyTorch [30]. The last iterates of SGD with these types of step size scheduling have demonstrated excellent empirical performance, as observed in [12, 26, 40]. However, the first convergence results for exponential step decay scheduling have emerged only recently [26, 39]. These studies primarily focus on the problem from an optimization perspective and do not address robustness, thus failing to provide meaningful recovery in cases where measurements or stochastic gradients are contaminated by outliers like our setting. Our method, SGD-exp, employs this more practical step size scheduling to address robust linear and ReLU regression problems in a streaming setting.

1.6 Organization

In the next section, we formalize the streaming measurement model and the assumptions on the noise and on the measurements. Then, we define the method both in linear (4) and in ReLU cases (5) and state our main convergence theorems, Theorem 3 and Theorem 4. In Section 3, we provide necessary background on discrete drift analysis: we state and prove Theorem 5 – a convenient modification of [[17], Theorem 2.3] – which might be applicable more broadly. In Sections 4 and 5, we prove our main theorems, and provide empirical evidence in Section 6 to support our theory. We summarize our results and discuss future research directions in Section 7.

2 Main results

We formalize the models and state our main results in this section.

2.1 Model 1: Streaming linear system

Suppose we want to recover an unknown vector from random linear measurements with corruption probability . More precisely, we have observations arriving in a streaming fashion:

| (2) |

such that the noise satisfies Assumption 1 and measurement vectors satisfy Assumption 2:

Assumption 1 (Massart noise model).

The coordinates of an -dimensional noise vector satisfy , where are the indicator random variables taking value with probability and independent with all other variables, and are any variables, possibly random and dependent on measurement vectors or true signal.

Assumption 2 (Measurement model).

For any let be the -algebra generated by .

Let be the unit-norm measurement vectors independent with such that are i.i.d. mean-zero isotropic random vectors. For any measurable with respect to it holds that

for some constant that only depends on the distribution of .

Direct computation shows that the normalized random Gaussian vector, or equivalently, the random vectors drawn uniformly at random from , satisfy Assumption 2 with the constant . More generally, many other measurement models such as the normalized Bernoulli random vector satisfy the above assumption for moderately large dimension by the following lemma.

Lemma 2.

Let be independent random vectors whose entries are i.i.d., mean-zero, unit-variance, and sub-Gaussian with sub-Gaussian norm bounded by . Then the normalized vectors satisfy Assumption 2 with a constant with probability at least . Here, and are positive constants that depend on .

Proof.

Let be the -algebra generated by and be measurable with respect to as in Assumption 2. By the Khintchine inequality (see, e.g., Exercise 2.6.6 in [38]),

Also, by Bernstein’s inequality, for a given constant ,

for some constant that only depends on the sub-Gaussian norm of the entries of random vector . Hence,

where we have used that is measurable with respect to and is independent with . Setting and taking large enough such that proves the lemma.

Remark 1.

The analyses for some works including SGD-root [31] also assume a mean-zero Gaussian feature (measurement) which is more restricted than our measurement model in Assumption 2. Although they cover a non-identity covariance matrix for Gaussian vectors, we would like to point out that by multiplying by (where is the Cholesky Decomposition), the vectors can be standardized. Hence, we can easily extend our convergence analysis to the non-identity covariance (non-isotropic) Gaussian case. For simplicity, we have carried out our analysis for the isotropic case but under a broader class of random measurement models.

2.2 Model 2: Streaming ReLU regression

Suppose we observe a signal through nonlinear measurements given as

| (3) |

where the ReLU activation function , the noise satisfies Assumption 1 and measurement vectors satisfy Assumption 2 with the following additional condition on the distribution of :

Assumption 3.

For any and , for any we have

and

Remark 2.

Note that Assumption 3 holds for any symmetric distribution for ; the distribution of is identical to the distribution of . This includes common measurement models such as the Gaussian distribution or the symmetric Bernoulli distribution.

Remark 3.

At least some form of assumption on the distribution of is necessary for ReLU regression, otherwise recovering the unknown vector is information-theoretically impossible [11, 29]. The Assumption 3 is similar to the one in [41], but their work aims to minimize the risk with respect to the loss and is not about the true parameter recovery using the more robust loss as ours. Moreover, unlike our work, their corruption model and result do not allow arbitrary large corruptions.

2.3 SGD-exp method and main theorems

Consider the following version of stochastic gradient descent for the -loss, or least absolute deviation error. The same version was considered in QuantileSGD [16] in the non-streaming setting but with a different step size scheduling. Namely, in the linear case, we define SGD-exp method iteration as

| (4) |

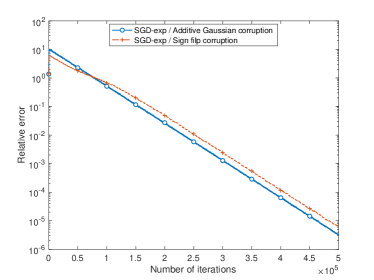

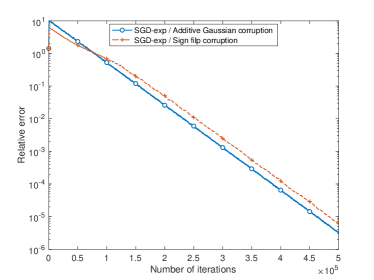

where is the step size in -th iteration and . The initial iterate is set to . Figure 1 (left) shows that the method empirically converges linearly in the number of iterations for .

Our main result is that

Theorem 3.

Suppose that is observed through the noisy streaming scheme (2) and the measurement vectors satisfy Assumption 2. Suppose that the dimension is sufficiently large enough to satisfy . Let a parameter be such that for

Let be the result of steps of SGD as per (4). Then, with probability the error is bounded by

where the positive constant is from Assumption 2 on the measurement and it only depends on the the sub-Gaussian norm .

Remark 4 (On the choice of ).

In the ReLU case, using the subdifferentials of the absolute function and the activation function , the corresponding SGD-exp iteration is given by

| (5) |

Figure 1 (right) shows that SGD-exp empirically converges linearly in the number of iterations for for the streaming with corrupted ReLU measurements.

The main theorem in the ReLU case is as follows:

Theorem 4.

Suppose is observed through the noisy ReLU streaming scheme (3) and the measurement vectors satisfy Assumptions 2 and 3. Suppose that the dimension is sufficiently large enough to satisfy . Let a parameter be such that for

Let be the result of steps of SGD-exp as per (5). Then, with probability

the error is bounded by

where the positive constant is from Assumption 2 on the measurement and it only depends on the sub-Gaussian norm .

Remark 5 (Addressing highly corrupted regime).

Theorem 3 implies that the iterates of the SGD-exp converge (almost) linearly up to logarithmic factors for the corruption probability . This is theoretically the best possible: suppose that . Then, any approach would not be able to determine whether the responses are generated from the signal with the sign-flip corruption with probability or they are generated from with the sign-flip corruption with probability . Prominently, in the case when the noise is symmetric and oblivious, our proof yields the result for all , see Remark 7 and Remark 8 for the details.

Remark 6 (Convergence rate is almost like in an uncorrupted setting).

Our effective convergence rate from Theorem 3 and Theorem 4 is

Notably, it is only logarithmically slower than compatible streaming algorithms on the uncorrupted setting. For example, in the streaming setting, the standard Kaczmarz convergence rate is for -dimensional Gaussian or Bernoulli measurement vectors. Then, in [26], an SGD with similar exponential step size schedule results in the loss decreases of order on the setting without contamination and under appropriate smoothness -Lipschitz conditions.

The idea of convergence analysis in both Theorem 3 and Theorem 4 is to show that a sequence of random variables is (almost) uniformly bounded with high probability, which in turn shows the residual error decreases (almost) geometrically since . To this end, we adapt for our case the result from Hajek [17] on the drift analysis of discrete stochastic processes, also used in several stochastic algorithm convergence analyses recently [2, 3].

3 Background on drift analysis

Consider a sequence of random variables measurable with respect to a filtration (that is, are -measurable). We follow the general convention that . Let be the first hitting time defined as

The goal is to obtain a high probability upper bound on the first hitting time defined above, given that the random process’s increments are bounded in expectation. The next theorem is a variant of Theorem 2.3 in [17], modified to suit our specific purpose.

Theorem 5.

Let be a discrete stochastic process adapted to the filtration , where is a trivial -algebra. Suppose that for some such that , , and , the process satisfies

-

(C0)

a.s.,

-

(C1)

a.s. for any ,

-

(C2)

a.s. for any .

Then, for the first hitting time it hold for any

| (6) |

Proof.

First, we note that is indeed a stopping time, namely, for any . Hence, we have a recursive estimate

| (7) |

where in the second step we have used that if and (C1), (C2) in the last step.

Now, since a.s. and is a trivial -algebra, (6) will immediately follow if we prove that for every

| (8) |

For , (8) holds trivially. Let’s employ induction: suppose (8) holds for some , then, using the tower property of conditional expectation we have for :

where we have used (3) with in the last step. This concludes the proof of (8) and of Theorem 5.

We will use the result about the drift through the following key corollary that is a modification of Proposition 2.5 in [17]:

Corollary 6.

Suppose satisfy following two conditions (C1) and (C2) in Theorem 5 for some and , and . Now, let be a given nonnegative integer. Then, we have

for any with .

Proof.

The proof follows from Markov’s inequality applied to the result of Theorem 5:

The last inequality holds since is positive as and .

4 SGD-exp convergence analysis for linear problem

Now, we give the estimates of the type (C1) and (C2) as per Theorem 5 for the process

where are the iterates of SGD, is the solution and defines the step size as per (4) .

4.1 Initial reductions

First, let us compute explicitly. By definition of measurements (2) and linearity of the inner product, we have

Multiplying to both sides we have

and

| (9) |

since is positive, so . Next, we take the squared Euclidean norm on both sides above to get

| (10) |

where we have used the fact that .

4.2 SGD drift estimates

Lemma 7.

Let the random process defined as per (10), where are i.i.d. random vectors in satisfying Assumption 1 with some constant and the corruption noise is non-zero with probability . Let be the -algebra generated by . Then for any step size decay parameter that satisfies

| (11) |

for and

we have

Proof.

Note that each is measurable with respect to by (9), so is adapted to . From Taylor’s series expansion, with ,

| (12) |

First, we estimate the linear term:

| (13) |

where the inequality follows from independence of with and being -measurable, and also . The inequality follows from the worst case that flips the , which happens if all the flips when outlier occurs. Lastly, the inequality follows from Assumption 2 for the measurement vector and .

Now, for the second term in (12), we have for

and, choosing ,

Then, if we choose small enough so that , and using that by assumption, the geometric sum can be further upper-bounded as

Using this estimate together with (4.2) in the initial Taylor expansion (12), we have

The condition essentially ensures that the first term dominates in .

This quadratic polynomial in is minimized by

| (14) |

using the estimates on (11) to show the inequalities, which in turn yields

To conclude the proof of Lemma 7, note that is indeed small enough to make . This follows by a direct check using that and the conditions on (11).

Lemma 8.

Let the random process be defined as per (10), where are i.i.d. random vectors in satisfying Assumption 1 with some constant and the corruption noise is non-zero with probability . Let be the -algebra generated by . Then for any step size decay parameter that satisfies

for

we have

Proof.

Using the event and that , we estimate

where the last line is from the choice of and .

4.3 Proof of Theorem 3

We are ready to give the proof of our main result in the linear case.

Proof of Theorem 3.

Recall that So, with probability we have and

where the last inequality is from the inequality for .

Remark 7.

(Random symmetric oblivious corruption) Lemma 7 applies to the more restricted corruption model, the random symmetric oblivious noise with corruption probability . Recall that in this case, the corruption noise is a symmetric random variable with probability and 0 otherwise. In addition, the noise is also independent with and , where . One can easily check that the same argument applies except we have a sharper inequality in in the proof of Lemma 7.

For the Massart noise , since it can access and , we have to consider the worst case, which happens if all the flips or is different with .

In contrast, for the random symmetric oblivious noise, suppose that the -th response is selected for corruption. Since is independent with (also as well since it only depends on ) and is symmetric with respect to , the probability that the sign of differs from the sign of is at most . Thus, the sign of differs the sign of with probability at most . Since the probability of -th response being selected for corruption is , the overall probability that is . Hence, in this case, the inequality in the proof of Lemma 7 is refined to

Now, the rest of the proof of the lemma and the main theorem remain the same, except we have the factor instead of in Theorem 3. This allows the recovery of the signal for SGD-exp for any corruption probability under the random symmetric oblivious corruption model, answering a related question in [34] for the streaming setting.

5 SGD-exp analysis on streaming ReLU

In this section, we show that our approach SGD-exp can be naturally generalized to the robust ReLU regression problem.

5.1 Initial reductions

Directly from SGD-exp iteration (5), we have

where is the -th residual vector. Similarly to the linear case, we get

| (15) |

Then, we take the squared Euclidean norm on both sides above to get for that

| (16) |

where we have used the fact that and on the event . The following lemma shows how the expression further simplifies on the event (no corruption event)

Lemma 9.

As long as , we have

Proof.

First, we note that conditioned on the event that ,

Indeed, if then both expressions under the sign are negative, and if then both expressions are the same. We have the statement of the lemma by the law of total probability.

5.2 SGD drift estimates and proof of convergence theorem for ReLU regression

We have the following result similar to Lemma 7:

Lemma 10.

Proof.

Here, the step (i) requires the assumption on the size of and Lemma 9 , the step (ii) requires Assumption 3, and finally we use Assumption 2 in the last step. Note the similarity with equation (4.2). We proceed in parallel with the proof of Lemma 7 to get using Taylor expansion

From the condition we can take

This gives

With the proof directly following the proof of Lemma 8, we also get:

Lemma 11.

Let the random process be defined as per (10), where are i.i.d. random vectors in satisfying Assumption 1 with some constant and the corruption noise is non-zero with probability . Let be the -algebra generated by . Then, for any step size decay parameter that satisfies

for

we have

Proof of Theorem 4.

Remark 8.

(Random symmetric oblivious corruption for ReLU regression) For the random symmetric oblivious noise, suppose that the -th response is selected for corruption. The probability that the sign of differs from the sign of is at most . Thus, the sign of differs from the sign of with probability at most . Since the probability of -th response being selected for corruption is , the overall probability that is . Hence, in this case, the inequality in the proof of Lemma 10 is refined to

Now, the rest of the proof of Lemma 10 and Theorem 4 remain the same, except we have the factor instead of in Theorem 3. This allows the recovery of the signal for SGD-exp for any corruption probability under the random symmetric oblivious corruption model for ReLU regression, same as in the linear case.

6 Experiments

In this section, we report on numerical experiments designed to validate our theoretical findings and demonstrate the performance of SGD-exp.

6.1 Experiments on random systems

In each trial of experiments in Section 6.1, we generate the measurement vectors and in randomly according to the -dimensional standard Gaussian random distribution. The effectiveness of the tested methods is evaluated by measuring the relative L2 error, in the number of iterations or data point access. We will further refer to it as relative error.

6.1.1 SGD-exp vs SGD-root

The semilog plots in Figure 2 imply that SGD-exp converges linearly for a smaller step size decay rate , whereas SGD-root only provides a sublinear convergence. Here, the measurement vectors are the -dimensional normalized Gaussian vectors, and the relative errors are averaged over trials.

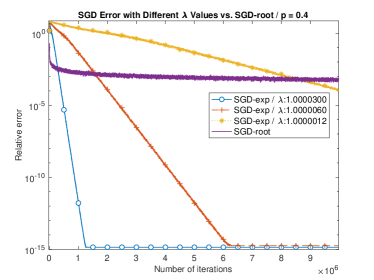

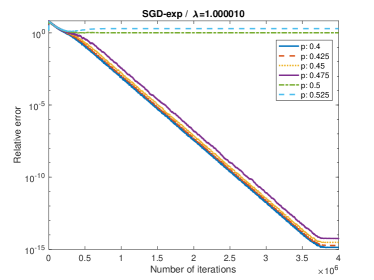

6.1.2 SGD-exp with various values of and step sizes for sign-flip corruption

Figure 3 displays the relative error plots of SGD-exp for robust linear regression with various choices of step sizes and different corruption probabilities . The measurement vectors are the -dimensional normalized Gaussian vectors.

The corruption model is the sign corruption, in other words, the -th measurement is replaced with with probability . This is a typical example of the Massart noise since it requires the knowledge of the sign of . We have selected this model because, in random symmetric oblivious corruption models that involve adding large random errors, SGD-exp still converges to the true parameter even when as predicted by our theory and demonstrated by the experiments in the following subsection.

The plots in Figure 3 indicate that as the step size decay factor gets close to , SGD-exp converges for higher values of the corruption probability at the expense of the convergence rates. The right plot confirms our theory that SGD-exp still converges when the corruption probability is close to for the Massart noise type corruption.

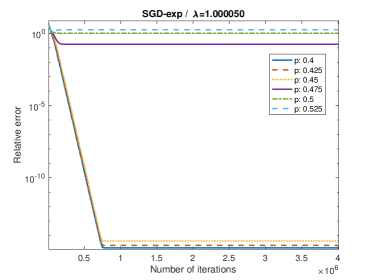

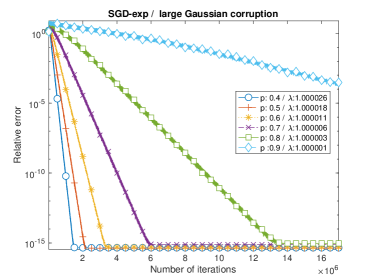

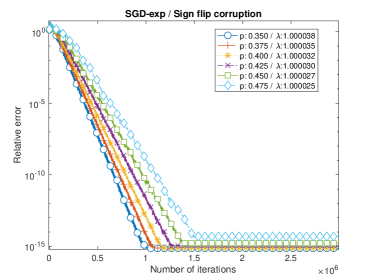

6.1.3 SGD-exp with various values of with recommended step size for the symmetric oblivious corruption and the sign-flip corruption

Figure 4 illustrates the error plots of SGD-exp for robust linear regression with several corruption probability and associated step size parameter . Here, the measurement vectors are the -dimensional rescaled standard normal Gaussian vectors. The response is corrupted by the random symmetric oblivious additive Gaussian noise with variance . Following the guideline about the dependence of the parameter on , and as stated in Theorem 3, we set for various values of the corruption probability .

The error plot on the left in Figure 4 supports our theory that SGD-exp still converges to the solution for any corruption probability under the random symmetric oblivious corruption model. Similarly, the relative error plot on the right in Figure 4 validates our theory that SGD-exp still converges to the solution for any corruption probability under the Massart corruption noise.

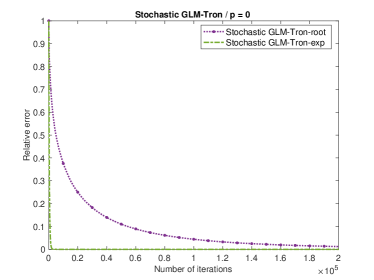

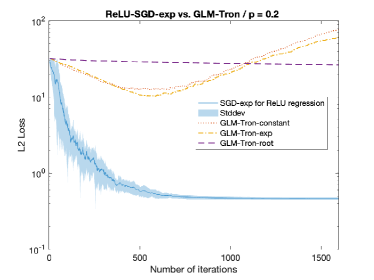

6.1.4 SGD-exp for robust ReLU regression

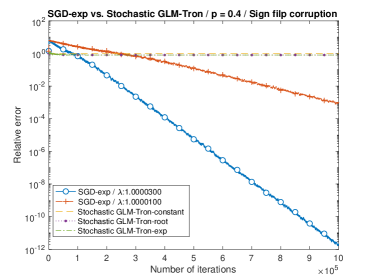

In this subsection, we illustrate the effectiveness of SGD-exp for robust ReLU regression. Our findings suggest that SGD-exp outperforms GLM-Tron [21, 23, 41], the popular ReLU regression method. GLM-Tron is essentially a (stochastic) iterative method for ReLU regression based on the loss. Although works such as [41] have provided some robustness property of GLM-Tron, our findings indicate that it is not robust with respect to the Massart noise, which is our corruption model. In particular, as shown in Figure 5, SGD-exp provides (nearly) linear convergence for robust ReLU regression under Massart noise, while stochastic GLM-Tron with constant, polynomial and exponential step size decays (which we denote for brevity as GLM-Tron-constant, GLM-Tron-root and GLM-Tron-exp and define precisely in the caption of Figure 5) all fail to converge. We note that on the same data without corruptions (when ) the same GLM-Tron-exp and GLM-Tron-root methods converge successfully, achieving relative error of and respectively in iteration steps.

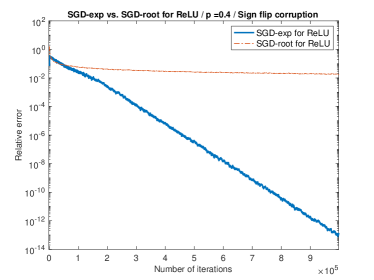

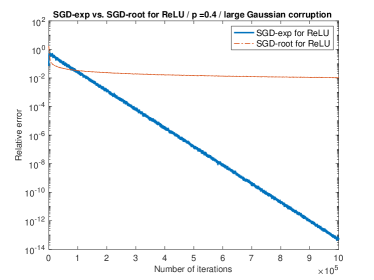

One might also try different step size scheduling such as the square-root decay step size instead of the exponentially decaying step size in the iteration equation (5) of SGD-exp for robust ReLU regression. In fact, the iteration equation (5) with square-root decay step size can be viewed as an extension of SGD-root [31] to ReLU regression. However, our findings suggest that this extension of SGD-root does not converge to the true parameter as shown in Figure 6 for sign-flip/large Gaussian corruption, whereas SGD-exp provides linear convergence for both types of corruption. This indicates that the exponential decaying step size in SGD-exp is a correct choice for robust ReLU regression under the Massart noise model.

6.2 SGD-exp on real datasets

In this section, we demonstrate the effectiveness of SGD-exp for linear and ReLU regression using real datasets with corrupted data. We apply our methods on two datasets, Red Wind Quality Data and Lending Club Loan Data and record the average loss values over trials.

6.2.1 Red Wine Quality Data

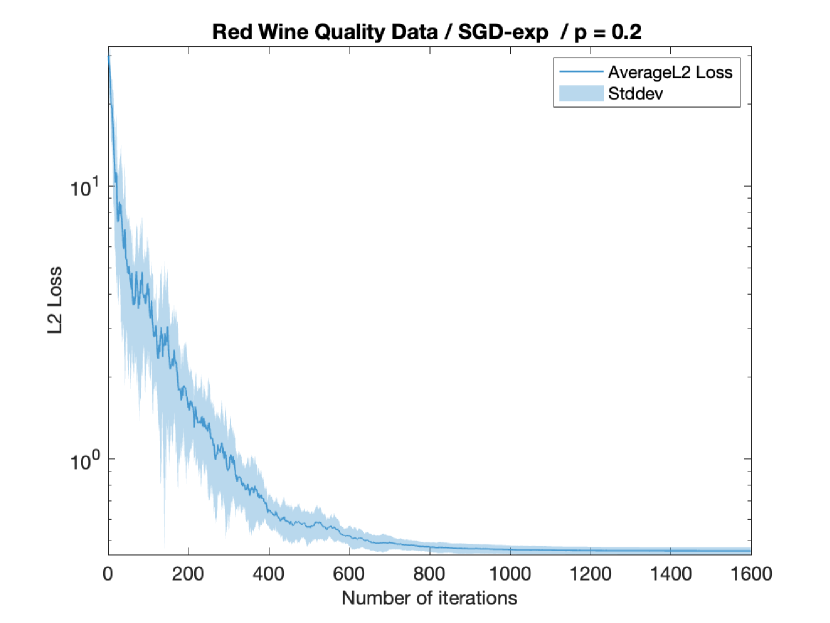

We use Red Wine Quality, a popular dataset for linear regression. The dataset consists of 1599 samples with physicochemical covariates and sensory response variable. Among the covariate variables, we only use 10 numerical ones for simplicity. The features are fixedAcidity, volatileAcidity, citricAcid, residualSugar, chlorides, freeSulfurDioxide, density, pH, sulphates, alcohol. We centralize/normalize these features and corrupt the response variable by adding large random Gaussian noise drawn from with probability . The parameter . A similar corruption model with real dataset has been used in [16].

To simulate the i.i.d. samples, we randomly select one of the data point from the dataset at each iteration of SGD-exp. Because typically there is no such reasonable ground truth vector for the real datasets, we measure the performance of methods using the loss function associated uncorrupted dataset instead. In Figure 7, we record the loss of the uncorrupted dataset, , where is the corresponding uncorrupted response vector.

The loss value after one pass of the corrupted dataset using SGD-exp for linear regression is about 0.463. For smaller scale of noise, drawn from , a similar plot to that in Figure 7 is obtained, which is omitted here, where we have obtained the loss value 0.450. These values are close to the optimal value 0.4220 which can be obtained by running the conventional linear regression on the uncorrupted dataset. If we run the linear regression on the corrupted dataset, the loss value is over 32.11, much higher than the one associated with the uncorrupted dataset.

As for robust ReLU regression, we obtain a similar plot for SGD-exp for ReLU regression, whereas GLM-Tron suffers from the corruption as shown in Figure 8.

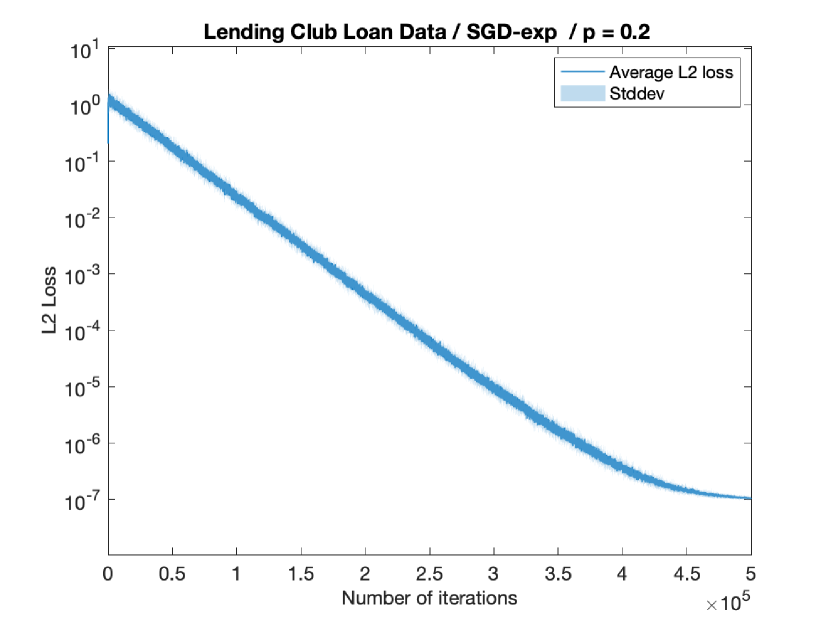

6.2.2 Lending Club Loan Data

Lending Club Loan dataset comprises samples with loan data from to issued by Lending Club, a lending company in the US. There are several features in the data such as interest rates, loan amounts, balances, and so on. We use the first features in the dataset and the response variable is paid_total. We normalize the feature/response vectors in the dataset, which is the typical preprocessing step for many machine learning algorithms.

As before, the data points are randomly drawn from the dataset at each iteration of SGD-exp.

Under the random corruption model with probability by adding Gaussian noise drawn from to the response variable and setting , we record the loss of SGD-exp in Figure 7.

The loss value after iterations of SGD-exp is 1.0116e-06, which is the optimal value by running the linear regression on the uncorrupted dataset. On the other hand, the loss of linear regression on the corrupted dataset that is obtained by a direct solver is 0.0017. This demonstrates the effectiveness of our method, SGD-exp, in handling random corruption.

7 Conclusion

In this paper, we have introduced Stochastic Gradient Descent with Exponential Decay (SGD-exp) for linear and ReLU regression in streaming settings under the presence of semi-random adversarial corruptions. Through theoretical analysis and numerical experiments, we have established that SGD-exp offers near-linear convergence rates for corruption probabilities less than for the Massart model and for the symmetric oblivious corruption model, optimal for both cases. Future research avenues include exploring SGD-exp’s application to other robust optimization problems, further refining the convergence analysis under different noise models, and extending the framework to accommodate additional forms of non-linearity and constraints.

References

- [1] Martín Abadi, Ashish Agarwal, Paul Barham, Eugene Brevdo, Zhifeng Chen, Craig Citro, Greg S Corrado, Andy Davis, Jeffrey Dean, Matthieu Devin, et al. Tensorflow: Large-scale machine learning on heterogeneous distributed systems. arXiv preprint arXiv:1603.04467, 2016.

- [2] Youhei Akimoto, Anne Auger, Tobias Glasmachers, and Daiki Morinaga. Global linear convergence of evolution strategies on more than smooth strongly convex functions. SIAM Journal on Optimization, 32(2):1402–1429, 2022.

- [3] Nikhil Bansal and Joel H Spencer. On-line balancing of random inputs. Random Structures & Algorithms, 57(4):879–891, 2020.

- [4] Battista Biggio, Blaine Nelson, and Pavel Laskov. Poisoning attacks against support vector machines. arXiv preprint arXiv:1206.6389, 2012.

- [5] Carla E Brodley and Mark A Friedl. Identifying mislabeled training data. Journal of artificial intelligence research, 11:131–167, 1999.

- [6] Yudong Chen, Constantine Caramanis, and Shie Mannor. Robust sparse regression under adversarial corruption. In International conference on machine learning, pages 774–782. PMLR, 2013.

- [7] Ilias Diakonikolas, Daniel M Kane, Ankit Pensia, and Thanasis Pittas. Streaming algorithms for high-dimensional robust statistics. In International Conference on Machine Learning, pages 5061–5117. PMLR, 2022.

- [8] Ilias Diakonikolas, Sushrut Karmalkar, Jong Ho Park, and Christos Tzamos. Distribution-independent regression for generalized linear models with oblivious corruptions. In The Thirty Sixth Annual Conference on Learning Theory, pages 5453–5475. PMLR, 2023.

- [9] Ilias Diakonikolas, Weihao Kong, and Alistair Stewart. Efficient algorithms and lower bounds for robust linear regression. In Proceedings of the Thirtieth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 2745–2754. SIAM, 2019.

- [10] Ilias Diakonikolas, Vasilis Kontonis, Christos Tzamos, and Nikos Zarifis. Learning a single neuron with adversarial label noise via gradient descent. In Conference on Learning Theory, pages 4313–4361. PMLR, 2022.

- [11] Ilias Diakonikolas, Jong Ho Park, and Christos Tzamos. ReLU regression with Massart noise. Advances in Neural Information Processing Systems, 34:25891–25903, 2021.

- [12] Rong Ge, Sham M Kakade, Rahul Kidambi, and Praneeth Netrapalli. The step decay schedule: A near optimal, geometrically decaying learning rate procedure for least squares. Advances in Neural Information Processing Systems, 32, 2019.

- [13] Prasanta Gogoi, Dhruba K Bhattacharyya, Bhogeswar Borah, and Jugal K Kalita. A survey of outlier detection methods in network anomaly identification. The Computer Journal, 54(4):570–588, 2011.

- [14] Mert Gurbuzbalaban, Umut Simsekli, and Lingjiong Zhu. The heavy-tail phenomenon in SGD. In International Conference on Machine Learning, pages 3964–3975. PMLR, 2021.

- [15] Jamie Haddock, Anna Ma, and Elizaveta Rebrova. On subsampled quantile randomized Kaczmarz. In 2023 59th Annual Allerton Conference on Communication, Control, and Computing (Allerton), pages 1–8. IEEE, 2023.

- [16] Jamie Haddock, Deanna Needell, Elizaveta Rebrova, and William Swartworth. Quantile-based iterative methods for corrupted systems of linear equations. SIAM Journal on Matrix Analysis and Applications, 43(2):605–637, 2022.

- [17] Bruce Hajek. Hitting-time and occupation-time bounds implied by drift analysis with applications. Advances in Applied probability, 14(3):502–525, 1982.

- [18] Cullen Haselby, Mark A Iwen, Deanna Needell, Elizaveta Rebrova, and William Swartworth. Fast and low-memory compressive sensing algorithms for low Tucker-rank tensor approximation from streamed measurements. arXiv preprint arXiv:2308.13709, 2023.

- [19] Peter J Huber. The place of the L1-norm in robust estimation. Computational statistics & data Analysis, 5(4):255–262, 1987.

- [20] Peter J Huber. Robust estimation of a location parameter. In Breakthroughs in statistics: Methodology and distribution, pages 492–518. Springer, 1992.

- [21] Sham M Kakade, Varun Kanade, Ohad Shamir, and Adam Kalai. Efficient learning of generalized linear and single index models with isotonic regression. Advances in Neural Information Processing Systems, 24, 2011.

- [22] Adam Tauman Kalai and Ravi Sastry. The isotron algorithm: High-dimensional isotonic regression. In COLT, 2009.

- [23] Sayar Karmakar and Anirbit Mukherjee. Provable training of a ReLU gate with an iterative non-gradient algorithm. Neural Networks, 151:264–275, 2022.

- [24] Adam Klivans, Pravesh K Kothari, and Raghu Meka. Efficient algorithms for outlier-robust regression. In Conference On Learning Theory, pages 1420–1430. PMLR, 2018.

- [25] Roger Koenker and Gilbert Bassett Jr. Regression quantiles. Econometrica: journal of the Econometric Society, pages 33–50, 1978.

- [26] Xiaoyu Li, Zhenxun Zhuang, and Francesco Orabona. A second look at exponential and cosine step sizes: Simplicity, adaptivity, and performance. In International Conference on Machine Learning, pages 6553–6564. PMLR, 2021.

- [27] Qingyang Lin, SJ Neethling, Katherine J Dobson, L Courtois, and Peter D Lee. Quantifying and minimising systematic and random errors in x-ray micro-tomography based volume measurements. Computers & Geosciences, 77:1–7, 2015.

- [28] Liu Liu, Yanyao Shen, Tianyang Li, and Constantine Caramanis. High dimensional robust sparse regression. In International Conference on Artificial Intelligence and Statistics, pages 411–421. PMLR, 2020.

- [29] Pasin Manurangsi and Daniel Reichman. The computational complexity of training ReLUs. arXiv preprint arXiv:1810.04207, 2018.

- [30] Adam Paszke, Sam Gross, Francisco Massa, Adam Lerer, James Bradbury, Gregory Chanan, Trevor Killeen, Zeming Lin, Natalia Gimelshein, Luca Antiga, et al. Pytorch: An imperative style, high-performance deep learning library. Advances in Neural Information Processing Systems, 32, 2019.

- [31] Scott Pesme and Nicolas Flammarion. Online robust regression via SGD on the L1 loss. Advances in Neural Information Processing Systems, 33:2540–2552, 2020.

- [32] Vatsal Shah, Xiaoxia Wu, and Sujay Sanghavi. Choosing the sample with lowest loss makes SGD robust. In International Conference on Artificial Intelligence and Statistics, pages 2120–2130. PMLR, 2020.

- [33] Mahdi Soltanolkotabi. Learning ReLUs via gradient descent. Advances in neural information processing systems, 30, 2017.

- [34] Stefan Steinerberger. Quantile-based random Kaczmarz for corrupted linear systems of equations. Information and Inference: A Journal of the IMA, 12(1):448–465, 2023.

- [35] Jacob Steinhardt, Pang Wei W Koh, and Percy S Liang. Certified defenses for data poisoning attacks. Advances in neural information processing systems, 30, 2017.

- [36] Che-Ping Tsai, Adarsh Prasad, Sivaraman Balakrishnan, and Pradeep Ravikumar. Heavy-tailed streaming statistical estimation. In International Conference on Artificial Intelligence and Statistics, pages 1251–1282. PMLR, 2022.

- [37] John Wilder Tukey. A survey of sampling from contaminated distributions. Contributions to probability and statistics, pages 448–485, 1960.

- [38] Roman Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- [39] Xiaoyu Wang, Sindri Magnússon, and Mikael Johansson. On the convergence of step decay step-size for stochastic optimization. Advances in Neural Information Processing Systems, 34:14226–14238, 2021.

- [40] Xiaoyu Wang and Ya-xiang Yuan. On the convergence of stochastic gradient descent with bandwidth-based step size. Journal of Machine Learning Research, 24(48):1–49, 2023.

- [41] Jingfeng Wu, Difan Zou, Zixiang Chen, Vladimir Braverman, Quanquan Gu, and Sham M Kakade. Finite-sample analysis of learning high-dimensional single ReLU neuron. In International Conference on Machine Learning, pages 37919–37951. PMLR, 2023.

- [42] Gilad Yehudai and Shamir Ohad. Learning a single neuron with gradient methods. In Conference on Learning Theory, pages 3756–3786. PMLR, 2020.