Randomized Control in Performance Analysis and Empirical Asset Pricing

Abstract

The present article explores the application of randomized control techniques in empirical asset pricing and performance evaluation. It introduces geometric random walks, a class of Markov chain Monte Carlo methods, to construct flexible control groups in the form of random portfolios adhering to investor constraints. The sampling-based methods enable an exploration of the relationship between academically studied factor premia and performance in a practical setting. In an empirical application, the study assesses the potential to capture premias associated with size, value, quality, and momentum within a strongly constrained setup, exemplified by the investor guidelines of the MSCI Diversified Multifactor index. Additionally, the article highlights issues with the more traditional use case of random portfolios for drawing inferences in performance evaluation, showcasing challenges related to the intricacies of high-dimensional geometry.

1 Introduction

This paper examines the use of randomized control techniques in empirical asset pricing and performance evaluation from various perspectives, including economic, mathematical, and computational considerations. The investigation addresses the role of controlled chance as a tool for performance evaluation and emphasizes the substantial influence of design on inference. A novel approach to both, the design and application of randomized controls is presented. This new methodology serves to evaluate the performance and risk drivers of systematic investment strategies, i.e., portfolios that exhibit certain quantifiable characteristics by construction. Examples of such inherent characteristics include exposures towards classical factors such as size111Stocks with lower market capitalization tend to outperform stocks with a higher market capitalization in the future. [9], value222Stocks that have a low price relative to their fundamental value, commonly tracked via accounting ratios like price to book or price to earnings outperform high-value stocks. [109], momentum333Stocks that have outperformed in the past tend to exhibit strong returns going forward. [60] or quality444Stocks which have low debt, stable earnings, consistent asset growth, and strong corporate governance, commonly identified using metrics like return to equity, debt to equity, and earnings variability. [6].

We introduce a way to construct random controls that account for investor constraints, including but not limited to upper bounds, short-selling restrictions, risk limits, and tolerances on factor exposures, which allows to analyze the relationship between portfolio characteristic and portfolio performance within stringent investment guidelines. The suggested approach roots in geometric random walks, a special class of (continuous) Markov Chain Monte Carlo (MCMC) methods. Further, a geometric perspective will help to categorize random controls into one of three groups based on the type of constraints that are to be mapped and on the notion of randomness. Given the portfolio context, a randomized control group is hereafter referred to as a random portfolio (RP).

RPs are commonly utilized within the domain of performance evaluation, an area closely aligned with the intended application scope we are proposing. In the ensuing discourse, we shall integrate this domain. However, it will become apparent that employing RPs for purposes of performance comparisons is fraught with complexities. From our perspective, insufficient attention has been directed toward these challenges in the past. Conversely, RPs prove valuable for examining the relation between systematic portfolio features and performance within real-world scenarios. In particular, the suggested RP framework based on geometric random walk enables an examination of factor effects within a constrained setup and has the capacity to unveil non-linear and asymmetric relations, if such exist, not only between characteristics and returns but also between characteristics and risks. As such, RPs constitute a novel technique for exploring asset pricing puzzles that is more versatile than classical sorting-based approaches going back to (at least) [42]. Further, RPs can be designed to closely resemble a strategy of interest in all aspects, except for one particular characteristic in question, which enables an isolated analysis of the implication of that specific characteristic.

Formally, a RP is a real-valued random vector, denoted , having a probability density function (pdf) with bounded support . is shaped by investor-imposed constraints and geometrically forms a convex body (which we will explore in detail later on). The components of represent the proportions of potential monetary allocations to investable assets, i.e., the random portfolio weights.

Our primary interest is on statistics derived from the random weights, i.e., the RP’s risk, return and characteristic, where the latter typically comes in the form of a factor score. Performance statistics and characteristics are functions of the random weights and of the coefficients obtained from market observations.

Consider the following example. Let be the vector of performance parameters, the mean and standard deviation of a RP; both are (scalar) random variables. At any point in time , we may estimate the parameters as , where is the vector of sample mean returns and , where is the sample covariance matrix of securities’ returns measured at over a specific period of stock market history.

The distribution of , estimated at a given point in time , serves as a representation of the potential outcomes in terms of the specified performance measures, that could have been achieved over a preceding period, considering a pre-defined universe of investable assets and constraints imposed by investors. This set of counterfactual results and the corresponding probability measure provides a basis for two kinds of inferences.

An option is to employ the performance distribution of the RP as a benchmark for comparing and statistically testing performance. It has been put forward as the null distribution of performance outcomes under the assumption of no skill, thereby framing performance evaluation as a hypothesis testing problem. This is the typical use case endorsed in the literature, see e.g., [121], [87], [70]. In the sequel, we demonstrate that this case subsumes the bootstrap approach of Efron [40], which appears frequently in the context of performance analysis, as a particular instance of a RP. The advantage of a general RP-based analysis over simple resampling procedures is that the former offers the possibility to incorporate investor constraints. This addresses limitations associated with classical benchmark or peer group comparisons which have faced criticism for their susceptibility to biases, such as the inclusion of investment styles that do not align with the strategy of interest or for constituting portfolios that fall outside the investor’s specified constraints (see e.g., [121]).

The narrative supporting the RP-based performance evaluation approach primarily relies on the following two conjectures: (i) A RP forms an obvious choice of control for performance analysis as, by design, it incorporates no penchant to any investment strategy; any portfolio structure is just as likely to occur as any other, and (ii) For (i) to hold, random weights need to follow a uniform distribution over the domain of feasible allocations. Both claims are flawed; even though they are intuitively appealing and despite their many appearances in the literature (we refer the reader to the literature review in Section 1.2). First, the idea that a RP is ”analogous to an enumeration of all feasible portfolios” [70] is misleading. Although the domain is defined such as to enclose all feasible portfolios, the probability measure over the domain strongly concentrates over a thin shell of typical allocations (the high-volume area of the domain) under a uniform distribution. This concentration phenomenon arises from the intricacies of high-dimensional geometry, which we will discuss in more details in the sequel. Second, the idea that a RP “by construction incorporates no investment strategy, bias or skill” [36] is subject to interpretation and depends on whether one views the capitalization-weighted or the equal-weighted portfolio as the unbiased and unskilled reference (see the discussion in Section 2.1).

These two drawbacks lead us to conclude that the use of RP-based statistical significance tests to evaluate the (over- or under-) performance of a particular investment strategy is not appropriate. As a purely descriptive tool, however, we consider RP-based analysis to be valuable, as exemplified in the subsequent Section.

The second use case, a novel concept in our understanding, pertains to exploit a RP for detecting and assessing asset pricing anomalies within real-world scenarios. Specifically, this entails exploring the interplay between factor exposure and the performance of portfolios that adhere to investor guidelines. At a time , the factor exposure of the RP is given by , where represents a cross-sectional vector of factor exposures of the firms in the investment universe. These asset-level exposures are (standardized) regression coefficients obtained by regressing the firm’s return series on the series of a factor where the factor is a long-short portfolio formed by sorting stocks according to attribute . Alternative to regression coefficients, company-specific characteristics could be used, e.g., fundamentals like a firm’s market capitalization or it’s balance sheet ratios. In accordance with the procedure of the index provider MSCI555https://www.msci.com/, which serves as the basis for our practical application presented in the empirical part (Section 5), we will sometimes employ the term (factor) score to be generic. Ultimately, we are interested in estimating the conditional distribution of , which elucidates the interrelation between portfolio score and performance.

Factor scores can also form part of the constraints which define the RP, especially those not integral to the investigated investment style of interest. This grants the researcher complete control over the management and assessment of potentially confounding variables. In Section 5, we will employ this approach to examine the persistence of well-studied factor premia in a practical setting.

We would like to stress that our suggested use of RPs is not intended to establish causal relationships. Instead, it aims to identify statistical associations between variables and to evaluate the performance of different investment strategies under various conditions. We therefore pay attention not to confuse between causation and association. The latter is a statistical relationship between two variables, a conditional probability , while the former means that the exposure produces the effect. Our approach thus distinguishes from the typical application of randomized control in experimental designs like, for instance, pharmaceutical studies, which aim to isolate causal effects by splitting subjects into treatment and control groups.666As stressed in [37], illuminating the causal nature of things requires more than just an experimental setup for testing but begins with a theory that outlines the causal mechanism(s) which are experimentally falsifiable. In Section 5, we emphasize that our use of a randomized control is not to compare treated and non-treated groups, but rather to differentiate portfolios with and without a specific characteristic.

Also, it is not our intention to advocate RPs as a panacea to solve asset pricing puzzles. Rather, we view them as a valuable addition to the arsenal of statistical tools for performance related questions in financial economics. However, it is important to acknowledge the complexities involved in generating RPs that accurately reflect real-world constraints. In a first instance, RPs are theoretical constructs, and the key question is whether one can effectively determine the distribution of performance measures or portfolio characteristics for inferential purposes. In most cases of practical relevance, analytical solutions are not feasible, and we must resort to numerical techniques to obtain the desired results.

1.1 Contributions

Our contributions within this article are fourfold. First, we clarify the inherent challenges associated with the conventional practice of utilizing RPs for performance assessment (Section 2). Second, we introduce an alternative use case focused on examining asset pricing anomalies within constrained scenarios. This use case is demonstrated in Sections 2 and 4. Third, we provide an extensive exposition of technical methodologies for generating RPs, covering both exact and approximate sampling-based solutions within a common geometric framework (Sections 3 and 5). Specifically, we introduce geometric random walks, a class of continuous MCMC methods tailored for high-dimensional constrained scenarios from computational geometry, as an instrument to create a randomized control which is useful to evaluate asset pricing anomalies within constrained setups. We survey all existing random walks, examining the algorithms from both theoretical and practical perspectives, and include complexity results. Lastly, we present an efficient open-source implementation in C++ with an interface in R (Sections 5 and 5.2), facilitating performance analysis via RPs with ease. With this software, assuming the reader has access to the Wharton Research Data Services (WRDS), our empirical research is fully reproducible.

1.2 Previous work

Ever since the claim of the economist Burton Malkiel [95] that “a blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by experts” the concept of a RP has been used to probe investment skill. Most prominently, the Wall Street Journal’s Dartboard Contest, a monthly column published by the business newspaper between 1988 and 2002, put Malkiel’s claim to the test by letting their staffers (acting as the allegoric monkeys) literally throw darts at a stock table, while investment experts picked their own stocks, always for a holding period of six months777Prior to January 1990, the holding period was for one month. The extension to six months was made to alleviate a possible bias from the price pressure resulting from the announcement effect.. If nothing else, the game added another animal symbolism to the jargon at Wall Street, emblematic in the ongoing debate on active versus passive management and the underlying hypothesis on market efficiency. While the results of the game are not informative, the experimental design, or rather, its deficiencies contain meaningful learnings about the use of a randomized control for research in finance. Several academic studies have examined the game pointing out biases like expert’s tilt towards high risk stocks [101], low dividend888Performances were computed on price series rather than on total return series, thus ignoring the effect of dividends and arguably incentivizing professionals to pick stocks with high growth opportunities. yield stocks [85] and high momentum stocks [108].

From a procedural aspect, the dartboard game forms an educative example of what we call a naive RP (a formal definition follows in Section 3.1) and sampling from it boils down to a bootstrap exercise in the spirit of [40]. Such bootstrap-like use of RPs is very common in the financial literature. One of the earliest reports we could find is [31] who used a bootstrap-type of RP in the analysis of mutual fund performances.

Dedicated articles to the topic of RP-based performance analysis are [120], [121], [36], [16], [87], [13], [119], [70] and [79]. All articles advocate the benefits of RP-based performance evaluations over traditional approaches and implicitely or explicitely promote the idea to view performance evaluation as a hypothesis test. In [121] they argue that traditional performance evaluation methods used by the finance community, namely peer group and benchmark comparisons, suffer from inevitable biases and should be replaced by Monte Carlo approaches. In [70] they point towards inefficiencies of simulation-based methods and propose a closed-form expression for the probability distribution of the Sharpe ratio of a uniformly distributed RP. Another analytical procedure based on a geometric algorithm was suggested in [19] and applied in [18] and [21], again imposing a uniform distribution for a otherwise unconstrained long-only RP. To our knowledge, there is currently no prior literature offering guidance on the creation of a RP with a well-defined distribution within a constrained domain.

Concerning geometric random walk methods, which we posit fill the identified gap, their origin traces to a substantial body of literature which has explored sampling methods for generating randomized approximations to the volumes of polytopes and other convex bodies [39, 88, 89, 35]. Geometric random walk methods possess a distinct lineage compared to the more conventional MCMC methods widely employed in finance, particularly within Bayesian frameworks for approximating posterior distributions. The uniqueness of geometric random walk methods lies in their specialization for approximating distributions characterized by a bounded support.

Geometric random walks have numerous application, including computational biology and medical statistics, where they play an important role in metabolic network studies [122, 107, 53]. Additionally, geometric random walks prove useful in solving convex programs [11, 64] and mixed integer convex programs [57]. Financial texts that use geometric random walk routines are sparse. In [29] they use a geometric random walk algorithm to optimize portfolios under qualitative input. To the best of our knowledge, the only text to use geometric random walk for performance analysis is [8].

The progress towards algorithms for volume computation, random sampling, and integration has developed deep connections between high-dimensional geometry and the efficiency of algorithms and shaped our understanding of convex geometry. Literature on those aspects include

[127],

[35],

[131],

[97]. Further important work on geometric random walk sampling include

[117],

[88],

[89],

[65] and

[92].

References to the source literature of existing geometric random walk routines are given in Section 4.

The remainder of this article is structured as follows. Section 2 contextualizes random portfolios within the realm of performance analysis and factor analysis. In Section 3, we delve into the problem of RP generation from a geometric perspective. Following that, Section 4 explores geometric random walk methods for constructing RPs tailored to address complex real-world scenarios. This Section provides an overview of possible algorithms, accompanied by descriptions of their properties and complexity, with a focus on their programmatic implementation. Subsequently, Section 5 presents empirical experiments using a geometric random walk-based RP to investigate the relationship between factor tilts and performance within the framework of the MSCI Diversified Multifactor index, which we consider representative of a typical setup. Finally, Section 5.4 concludes.

2 Use and abuse of Random Portfolios

2.1 A (brief) review of performance analysis

To characterize RP’s in a performance evaluation and asset pricing context, we briefly review some classical performance analysis methods.

Performance evaluation is inherently relative. The capitalization-weighted benchmark-relative perspective, arguably predominant in both industry and academia, has deep roots in economic theory, e.g., [115], [86], [102], and forms the blueprint for classical performance analysis. In this context, the available tools try to identify sources of excess returns and to attribute them to active bets undertaken by the portfolio manager.

Holdings-based or transaction-based performance attribution tools in the line of [14] (but applied to equity-only portfolios), building upon the work of [38] and [1], are widely employed in the industry. This is so because of their explanatory power to simultaneously outline the difference in the allocation structure between a portfolio and a benchmark by grouping stocks into easily interpretable categories like countries, sectors or currencies, and to quantify the individual contributions to overall performance coming from the allocation differences among and within the pre-defined categories. The determinants of portfolio performance [15] are however not to be understood in an etiological sense. Unless the categories, according to which the attribution is done, effectively correspond to deliberate bets undertaken by the portfolio manager which characterize the strategy, allocation and selection effects do not cause over- or underperformance. They can be seen as residuals, meaning that the strategy may generate these effects while pursuing other objectives. They can only identify what we may refer to as the ”causa proxima”, the immediate cause, while the ”causa remota”, the remote and perhaps indirect cause, which is encoded in the strategy and ultimately leads to the performance delta, remains unexplored. For instance, the underperformance of a minimum variance strategy following the 2022 energy crisis might be attributed to the strategy’s underweighting of the energy sector. However, it is not an inherent characteristic of minimum variance strategies to avoid investments in the energy sector. Rather, the strategy may not have selected energy-related firms due to the high volatility of stocks in that industry in response to the external shock. Thus, the cause of the performance difference is only superficially due to the sector performance but roots in the underlying variance minimizing mechanism that leads to the tendency of avoiding high-volatility assets regardless of their origin or sector.

Another school of performance evaluation, initiated by [44], subsumed under the term return- or factor-based models, uses regressions to break down observed portfolio returns into a part resulting from a manager’s ability to pick the best securities at a given level of risk and a part which is attributable to the dynamics of the overall market as well as to that of further risk factors which are recognized to explain security returns and are associated with a positive premium. This allows for an assessment as to whether the active performance is attributable to a particular investment style.

While the Brinson-type of performance attribution is purely descriptive, the regression setup goes beyond simple performance measurement as it allows for statistical inference in terms of significance testing of the out- or underperformance (alpha) and the loadings on other return drivers (betas) and therefore provides a basis for normative conclusions (assuming that the usual assumptions for linear regression are met). A skilled manager should be able to beat the market (factor) in a statistically significant manner after controlling for alternative betas. In this sense, skill is reserved to the active manager who is able to harvest a positive return premium not explained by known factors. Any benchmark replicating strategy, since it involves no active deviation from the capitalization-weighted allocation structure in a market, is therefore called passive and comes with performance expectations which should match the performance of a market index rather than trying to outperform it.

This view, that the average investor possesses no skill, conflicts (at least semantically) with the concept of a naive RP as the null of no skill. This is because a naive RP averages on the equal-weighted portfolio which forms a natural alternative benchmark. From a portfolio selection perspective the equal-weighted portfolio is rightly called the naive benchmark since the strategy implies no views on market developments. It results as the optimal solution in a Markowitz framework when expectations on returns, variances and correlations are considered constant cross-sectionally. Yet, from an asset pricing perspective, equal weighting provides exposure to systematic investment styles, foremost to the low-size factor, and is thus not so naive after all. The lack of consideration of the different points of view has led to unnecessary misinterpretations in the past. Unnecessary because, as we will show, RPs can easily be constructed to reflect either reference points in expectation, the naive investor who bets on all companies in a universe equally, or the average investor who accounts for the the number of shares a company has issued999For the computation of total market value one may want to restrict calculations to shares that are free-floating, i.e., available to public trading, giving rise to a free-float adjusted market capitalization versus a non-adjusted capitalization considering all shares outstanding, i.e., also those that are held by company insiders and which are restricted to trade. and the price they are traded for, i.e., firm capitalization (or actually any other reference point that could be relevant to an investor). In the forthcoming, we use the terms naive RP and basic RP to refer to either cases. A formal definition of the two concepts is given in Section 3 and a first educative example follows shortly.

A third and more direct approach of performance analysis comes in the form of hypothesis tests for the difference in performance measures of two strategies; typically, the portfolio in question and a benchmark. For instance, Sharpe ratio tests building upon the work of [63], the correction of [100] and the extension of [78] accounting for stylized facts of asset returns. However, at least since [67] it is known that these tests suffer from low power, that is, they are unlikely to identify superior performance in the data even if there is one.

A randomized procedure for performance analysis replaces the reference point with a reference set (equipped with the empirical probability measure). Using a RP is intuitively appealing as it is a model-free method. In principle, it eliminates the need for parameter estimation, thereby avoiding dependencies on extensive time series data and assumptions about the data generating process. Moreover, it offers flexibility in evaluating different performance measures while considering transaction costs and investment constraints. However, it relies on the assumption that the distribution of no-skill performance, crucial for hypothesis system evaluation, can be objectively approximated through sampling. We contend that such is not unequivocally feasible.

2.2 RP-based performance evaluation - An example

Let us illustrate the challenges of performance evaluation and the use as well as the potential for misuse of RP-based inference through a somewhat absurd, yet genuine, example. Imagine a portfolio manager who constructs a portfolio based on the number of times the letter ’Z’ appears in the company names of constituents within the S&P 500 index. Intuitively, this approach appears dubious and common sense would advise against entrusting this manager with our savings. However, when comparing a backtest of the manager’s strategy over a 22-year period (from 2000-01-01 to 2022-12-31) to the capitalization-weighted parent index (i.e., the S&P 500), the results show an annualized outperformance of % (based on daily geometric returns) and the Sharpe ratio test of Ledoit and Wolf ([78])101010The test accounts for time series structures in the data by employing heteroscedasticity and autocorrelation consistent (HAC) estimates of standard error. rejects the null hypothesis of equal Sharpe ratios at the 5% tolerance level. What is going on? Is there anything special about the letter Z? Of course not. In fact, it happens to be the case that we could have chosen any letter of the alphabet and the simulated out-of-sample111111Our backtesting procedure ensures that at every point in time, only stocks that have been in the index at that point in time enter the portfolio selection (i.e., there is no look-ahead bias). The allocation is then held for three months, letting the weights float with total return (i.e., dividends are assumed to be reinvested) developments of the underlying stocks, until the portfolios are rebalanced. backtest would have shown an outperformance. We could even take the nonsense to the extreme and invert the strategies by investing in all assets except those with a particular letter in the company name. Again, all backtests outperform the benchmark. How should we make sense of this?

Our absurd example is similar to the seemingly paradoxical results presented in [5] who find that the arguably nonsensical inverses of sensible investment strategies, i.e., strategies built from well-founded investment beliefs, which outperform the capitalization weighted benchmark, outperform even more. The cause is readily identified by the authors by a tilt towards the size and value factors meaning that both, sensible and senseless strategies outperform for the same (unintended) reasons. In particular, even randomly generated strategies, i.e., strategies generated from a Monte Carlo simulation (i.e., a RP approach), lead to outperformances for the same causes. All these findings enforce the authors to conclude that “value and size arise naturally in non-price-weighted strategies and constitute the main source of their return advantage” and that, therefore, “a simple performance measure becomes an unreliable gauge of skill”.

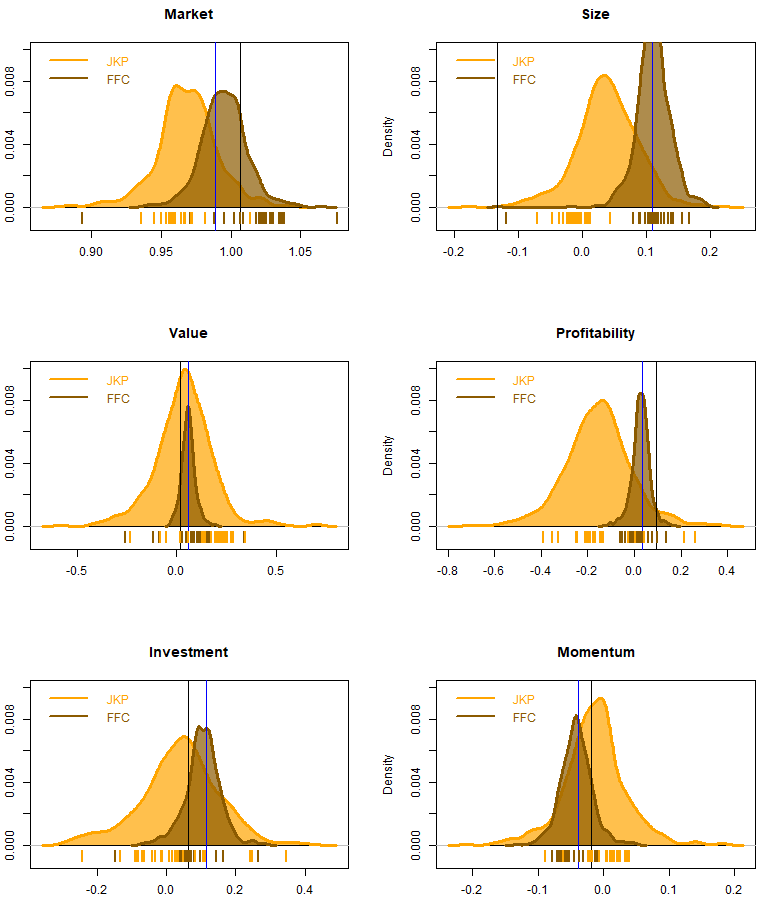

Also our inane letter strategies can be rationalized by their exposures to priced factors. For instance, when analyzed through the lens of the Fama-French-Carhart (FFC) 6-Factor model ([43], [20]) one finds that the majority of factor loadings are statistically significant. Coefficients are predominantely positive for size and value as well as for the two quality-related factors –profitability and investment– while all coefficients for momentum are negative. Market betas are, for the most part, below one and as low as for strategy Z (and when not controlling for other factors). However, alphas remain positive and significant for all strategies (at the 5% level) except for strategy Q. This finding appears robust to the choice of factors, as evidenced by the qualitative consistency of alphas obtained from a regression on the factor themes suggested by Jensen, Kelly, and Pedersen (JKP) [61]. Conversely, betas can differ substantially between the two models. Such discrepancies are to be expected, given the methodological disparities between the FFC and JKP models in constructing factors, utilizing underlying data, and selecting control factors.121212We found it interesting to study the (cross-sectional) correlation between FFC loadings and JKP loadings as they turn out to be surprisingly low. Over the analyzed period and for constituents of the S&P 500, the average correlation among exposures under the two models are for SMB and size, for WML and momentum, merely for HML and value and are even negative RMW and profitability and for CMA and investment (the correlations are computed cross-sectionally and the average is taken over time). Nevertheless, the observed inferential disparity can be confusing, as in various instances, one model attributes outperformance to a positive exposure to a specific factor, while the other attributes the opposite, both with compelling statistical significance131313Naturally, the regression setups should undergo thorough statistical analysis beyond a simplistic reliance on p-values, but unfortunately, such rigor is seldom practiced in reality. (especially for profitability, investment, and momentum). To arrive at a conclusive understanding, it might be necessary to forsake the convenience of the regression approach and engage in a more intricate analysis of the fundamental data related to the stocks within the letter portfolios141414For example, strategy J shows a clearly negative portfolio size score when calculated directly on the basis of company characteristics (we used the logarithm of market captitalization, standardized cross-sectionally to have mean zero), while the size exposure is positive under both FFC and JKP. For a long-only portfolio to have an exposure to a long-short factor does not necessarily mean that this translates to the portfolio having the corresponding characteristic (a portfolio with strong size exposure may nevertheless contain very large companies)..

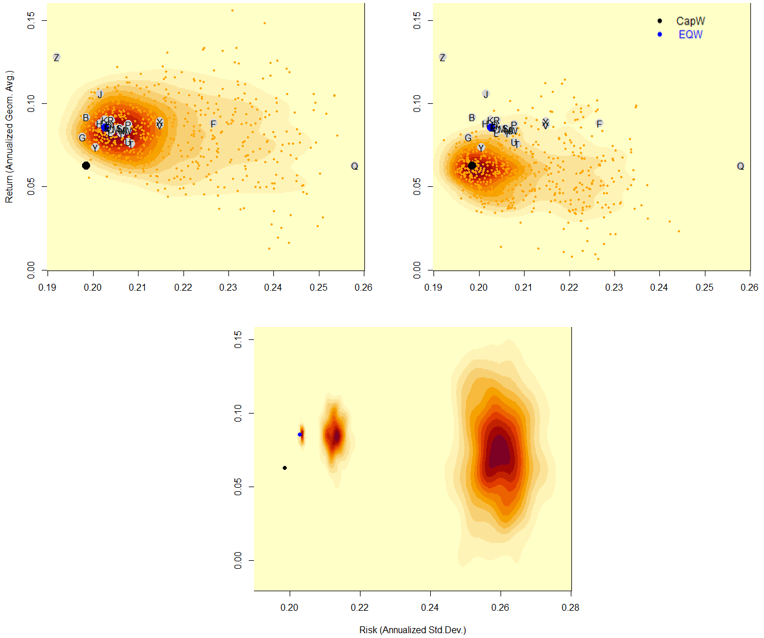

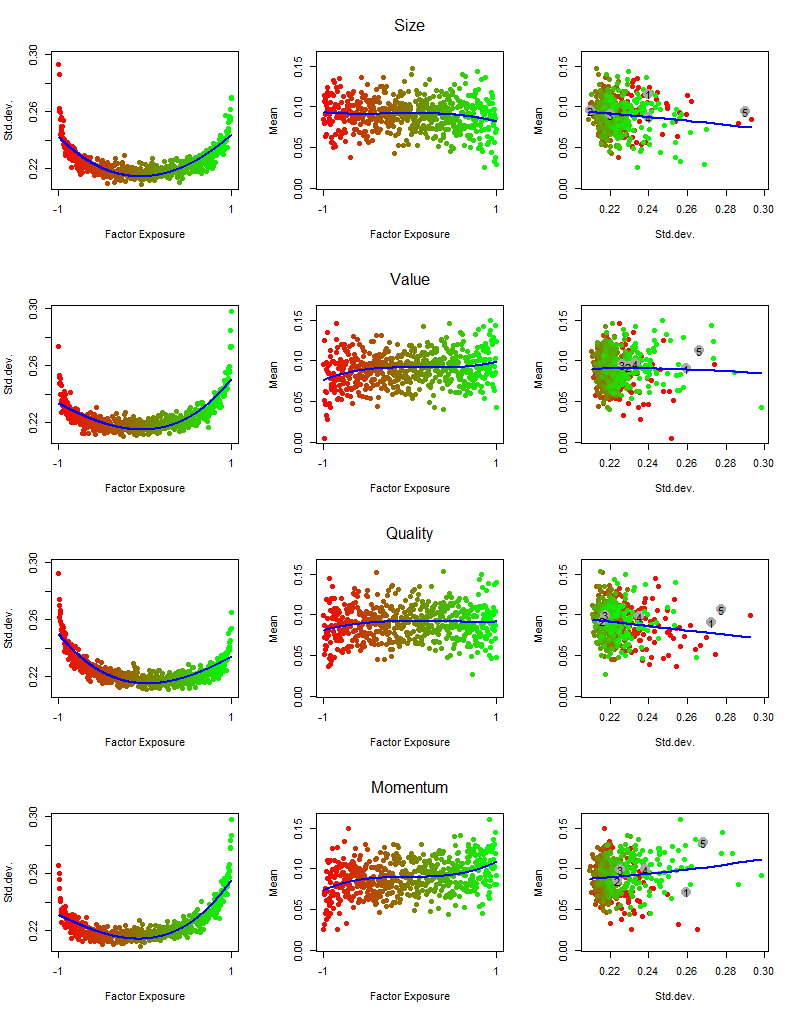

Instead, let us explore whether an RP-based approach can provide clarity. The top left chart in Figure 1 shows the bivariate risk-return distribution of a RP (red to yellow level sets) together with the corresponding statistics for the 26 letter strategies (grey dots), realizations of the RP (yellow small dots), the capitalization-weighted benchmark given by the S&P 500 index (black dot) and the equal-weighted portfolio of the index constituents, rebalanced monthly (blue dot).

Two immediate observations arise: Firstly, the performances of the letter strategies fall within the high-mass area of the RPs pdf, with Z and Q being outliers. Secondly, most of the mass of the RP return distribution is at levels above the return of the capitalization-weighted benchmark. The first observation suggests that any apparent performance or skill is consistent with chance and that the letter strategies could very well be instances of the RP. Analyzing the factor composition of the RP samples further reinforces this intuition. Figure 2 shows the distributions of factor scores of RP samples under the FFC and the JKP models. The marks above the x-axis display the corresponding exposures of the letter strategies. While the divergence of the two models poses some concern, the consistency of the letter strategy scores with the RP distribution under either model individually paints a rather clear picture, which is that the outperformance of the letter strategies may be attributed to factor exposures that happen to be prevalent in the market. By contrast, the factor structure of the capitalization-weighted benchmark can be far-off the bulk of the RP’s exposure distributions (this is evident for size where the benchmark must have a negative exposure by construction).

Unlike the letter-based performances, which mostly align with the outcomes of the RP, the capitalization-weighted benchmark exhibits a notable deviation. Here is where one has to be cautious not to jump to conclusions. If we were to statistically test the benchmark return based on the RP return distribution we would conclude that the average investor is rather unskilled since most investment decisions based on chance outperformed the market. This result would be in line with the findings of [5] as well as [30] who locate the return of the capitalization-weighted benchmark far out in the left tail of a RP return distribution over a years (1964 - 2012) and years (1968 - 2011) period respectively. However, one should recall Sharpe’s arithmetic of active management [116] that for every outperforming strategy there needs to be an underperforming one (relative to the capitalization-weighted benchmark). The fact that the RP outperforms the benchmark does not imply that any strategy, or even most strategies, outperform the benchmark. The outcome depends on the way the RP is constructed, circling back to the two previously mentioned issues in the RP narrative regarding the no-skill reference point and the misunderstanding that an RP covers the entirety of outcomes.

Without delving too deeply into the subject of RP construction (a concise description follows in Sections 3 and 4), some qualitative aspects need addressing here. The RP depicted in the top left chart of Figure 1 is not constructed as having a uniform distribution over the set of feasible assets. Such an approach would yield an inadequate representation of attainable performance, as it would consist solely of homogeneous and biased portfolios. Instead, it is crafted by convolving individual RPs, each centered on an equally-weighted portfolio while considering the number of assets in the specific letter portfolio at a given rebalancing date.

As the number of assets considered decreases, the risk-return distribution of the RP widens, and the distribution’s center shifts right, as depicted in the bottom chart of Figure 1. The chart displays three RP densities, constructed using a method commonly found in the literature. The procedure involves repeatedly sampling stocks uniformly from the set of investable stocks (here, with a set cardinality of ) and forming equally-weighted portfolios. This process essentially constitutes an -out-of- bootstrap. In the chart, we have used from left to right.

In the first case where all assets in the index are used, the density merely provides a measure of the uncertainty in the performance of the equal-weighted strategy151515It can be understood as an estimate of the sampling distribution of the equal-weighted portfolio’s performance statistics, or, if one would sample the asset space uniformly, as the posterior density of the risk-return parameters of the equal-weighted portfolio.. This is because sampled portfolios are all very close to the equally weighed portfolio (in terms of the weights). In higher dimensions, sampling according to a uniform distribution does not mean that each possible portfolio will be sampled with equal probability. Quite the contrary. With overwhelming probability, samples will be drawn from the high-volume area of the sampling space, which forms a thin shell (the region between two concentric higher dimensional spheres of differing radii)161616It can be shown that and that therefore, with denoting the equal-weighted portfolio, , which tends to zero with increasing .. Sparse or highly concentrated portfolios (such as the capitalization-weighted benchmark) are thus extremely unlikely to be sampled.

In cases where , as exemplified by and , chosen to align with the selections made by [5] and in the dartboard game, respectively, the imposed sparsity leads to a broader dispersion of portfolio weights. This translates to a more extensive distribution of performance statistics. However, the resulting distributions remain relatively compact, covering only a small area of the space of feasible solutions, refecting the homogeneity of sampled portfolios. Therefore, such RPs do not form acceptable control groups. Utilizing these distributions for significance testing would likely result in overly optimistic rejections of the Null hypothesis.

Adapting the RP mechanism to center on the capitalization-weighted allocation leads to the risk-return distribution in the top right chart of Figure 1. This distribution is more consistent with Sharpe’s arithmetic, having mode close to the performance of the market index. In contrast, the profile of the naive index significantly deviates from the center of mass. We could have further expanded or contracted the risk-return distribution by adjusting the variance in the weights, essentially reverse-engineering the random control to achieve a desired statistical test result. A dangerous game. We therefore conclude that a RP, as we have presented it so far, does not provide a statistically acceptable experimental design to probe skill (or lack thereof). Nevertheless, we would argue that, with some care in the construction of the RP, it can serve as a visual aid to characterize the dispersion of performance for non-elaborate strategies (such as letter-based investing). Hopefully, the geometric perspective which we advocate in the subsequent discussion offers some transparency in this context.

The utility of employing an RP lies in the ability to analyze the relationship between portfolio performance and portfolio characteristics. Let’s consider the frequency of a letter in a company’s name as a stock characteristic and examine whether there is a correlation between the returns of portfolios drawn from the RP and the characteristics of those portfolios171717For each occurrence of a specific letter in the company name, a score of one is assigned (i.e., a company having letter ’A’ appearing three times in it’s name gets a score of three). The portfolio characteristics are computed as the weighted sum of stock-level characteristic-scores times the portfolio weights.. If exposure to a particular letter, let’s say ’Z’, were a rewarded characteristic, this relationship should be reflected in the cross-section of RP samples as a correlation (or more broadly, a relation) between the loading on ’Z’ and performance. This (cor-) relation should be present in both RPs used above, the one centered on the equal-weighted and the one centered on the capitalization-weighted benchmark. While there are simpler ways to dismiss letter-based weighting as a viable method for portfolio construction, our point with current example is that the RP approach lends itself to an analysis of the performance impact of any systematic portfolio formation approach. In Section 5, we build on this approach to investigate recognized factors and their impact on performance. The analysis aims to detect genuine anomalies and reveal whether certain characteristics are still rewarded in the market when accounting for constraints that many investors need to adhere to.

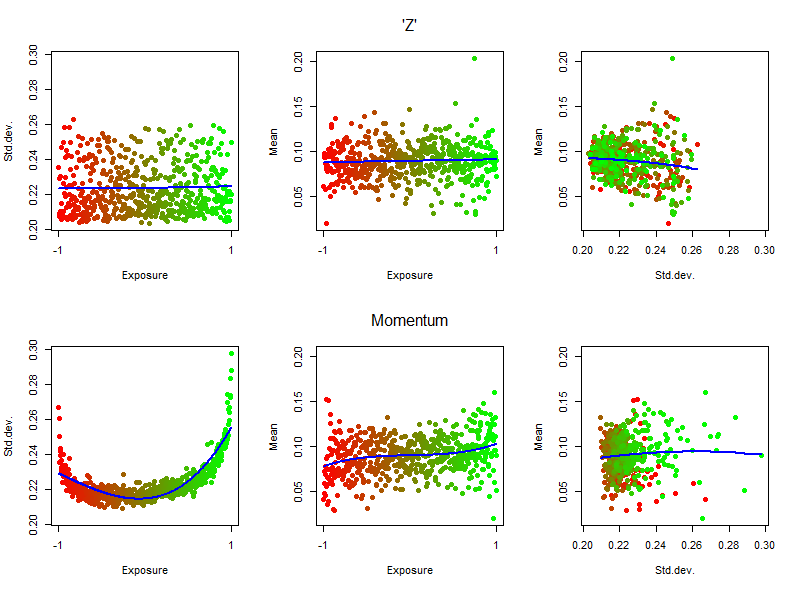

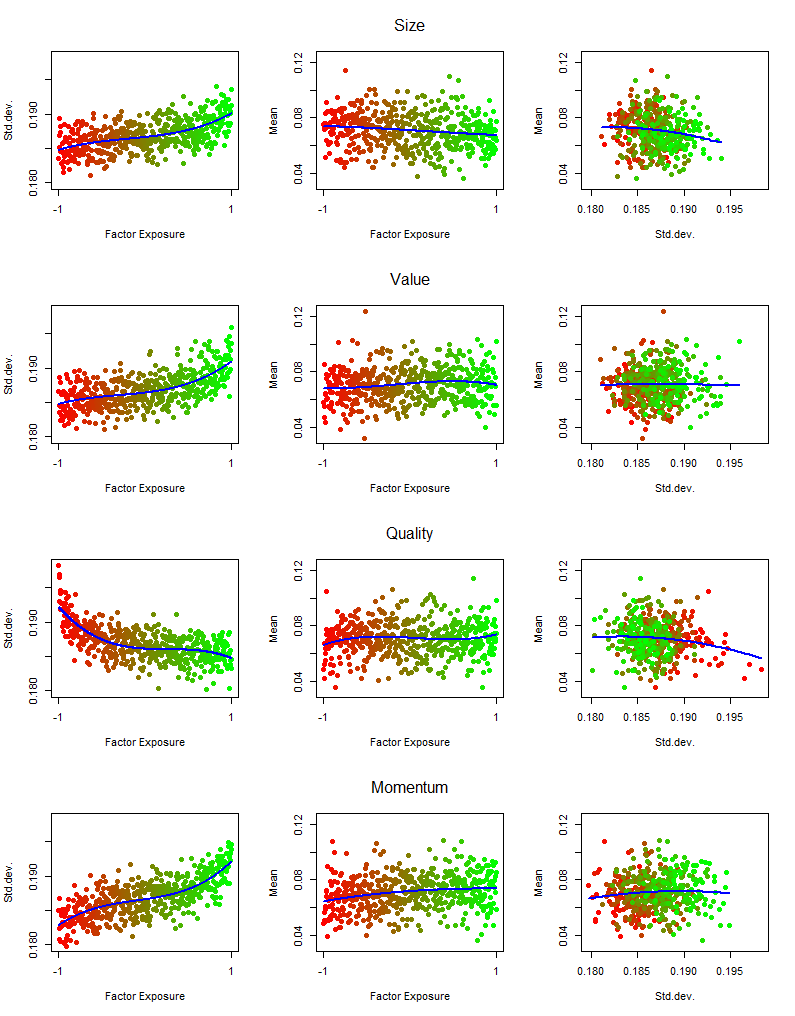

To finalize our example, Figure 3 shows the scatter plot of performance versus characteristics of samples from the RP visualized in the left plot of 1. Unsurprisingly, there is no observable correlation for characteristic ’Z’, neither between return and characteristic nor between risk and characteristic. In contrast, the right panel of Figure 3 illustrates the existence of a fairly strong relationship between momentum181818we measure momentum by the cumulative return of the portfolio over the last 12 months, omitting the last month. and performance at the portfolio level. The chart shows a non-linear (almost quadratic) pattern between risk and momentum. This implies that both, portfolios with the lowest and portfolios with the highest momentum scores exhibit high ex-post volatility, while volatility is low for intermediate-scoring portfolios. The correlation between portfolio’s returns and momentum scores is positive (0.31) overall, with steeper segments at the low- and high-exposure endpoints, while the middle part appears to be relatively flat. The graph prompts us to contemplate whether the momentum anomaly would endure in a constrained setting where extreme exposures are no longer feasible due to constraints on asset weights and/or on additional factor exposures. This question is the focus of Section 5. Additionally, the Section will provide a detailed description of the backtesting methodology, which we have also applied here. For completeness, the two charts in the third row of Figure 3 shows the risk-return patter for the RP samples. The color-coding from red (low exposure) to green (high exposure) helps to identify the unstructured and the partially structured nature of the Z-characteristic versus the momentum characteristic, respectively.

3 Random Portfolio Generation

In this Section, we explore the design and construction of a RP. We propose a categorization of RPs into three groups of increasing complexity: naive, basic, and regularized. Among the regularized RPs, we distinguish between simply regularized (where sampling is easy) and generally regularized (where sampling is difficult). The primary objective is to gain insights into the distribution of function values of a RP, such as its return. In certain cases, these distributions have an analytic expression. However, in general, analytic solutions do not exist and sampling-based approximations are necessary.

3.1 Naive Random Portfolios

The arguably most intuitive case is to consider non-negative portfolio weights that sum up to one; these are the two defining properties of long-only portfolios. The geometric object which characterizes the space of long-only portfolios is the canonical simplex

| (1) |

In practice, mutual funds frequently encounter legal constraints mandating full investment while prohibiting short selling. Consequently, the simplex constraint embodies a legal requirement to which they must adhere. Given its prevalence within the industry, our analysis will concentrate on this typical scenario, presuming the asset space to be defined by the standard simplex or a subset thereof, which arises when additional constraints are imposed. However, the geometric random walk routines which we propose in the sequel are by no means limited to the simplex case but readily extend to accommodate long-short applications.

As for the definition of randomness, we begin with the (arguably) most intuitive case of a uniformly distributed RP, i.e., we focus on the uniform measure over the simplex. Hence, a naive RP may be given by , which we parametrize it through a flat191919Flat means that the elements of the parameter vector of the Dirichlet distribution, , are all equal to one. Dirichlet model; i.e., , where is a vector of ones. The Dirichlet pdf is given by

| (2) |

This particular setup allows for an exact characterization of the distribution of linear statistics associated with a RP. For instance, the cumulative distribution function (cdf) of the return of a RP, denoted by , has an expression as a ratio of volumes. I.e.,

| (3) |

for some scalar , where denotes the volume operator and is the half-space induced by a hyperplane with normal that is the empirical mean vector of the asset return distribution (see [7]).

The volume in the numerator of Eq. (3) has a closed form expression, e.g., [77]. However, it has been observed that the evaluation of this expression is numerically unstable when the dimension is not small, , e.g., [19, 18]. To overcome this obstacle Chalkis et al [19, 18] suggest the use of an efficient and exact geometric algorithm, due to Varsi, see [126] and [3], for the evaluation of the volume(s). This is the preferable implementation strategy of naive RP applications. For the sake of convenience, we include the pseudocode for Varsi’s algorithm in Appendix A.1.

Another form of a naive RP is given by the mechanism underlying the dartboard game. Dart throwing monkeys are easily digitalized by drawing counts from a Multinomial distribution with trials where, with uniform probabilities , , which is exactly the setup underlying the classical bootstrap of [40]. Normalizing each count produces (RP) weights . Unlike the Dirichlet model, the weight space is no longer given by the canonical simplex but consists of a discrete grid over the canonical simplex. As a result, the bootstrap distribution of any derived RP statistic is discrete. The grid node at the centroid of the simplex represents the equal-weighted portfolio and vertices represent single-asset portfolios. Grid nodes located on the boundary of the simplex form sparse portfolios, i.e., allocations where one or more position is exactly zero.

The definition of randomness of the weights depends on the type of resampling plan one chooses in the bootstrap procedure. For instance, the specifications of the dartboard game, i.e., how many darts, , are thrown at a list of how many company names, , and whether a name can be hit multiple times or not (i.e., sampling with or without replacement), define the structure of the corresponding grid. In practical applications, resampling plans often involve drawing fewer than samples (), corresponding to an out of bootstrap [12]. In this case, the induced grid is biased toward the boundaries of the simplex, resulting in a wider dispersion of the bootstrap distribution of the statistic in question compared to the classical bootstrap RP version. The continuous analogue of this approach involves using a concentration parameter in the Dirichlet distribution such that . By introducing a mapping , the standard errors of the linear statistic of interest become equivalent under both and (see [7]). Notice that the flat Dirichlet model also describes a form of bootstrap version, namely the Bayesian bootstrap of [111].

To summarize, a naive RP conforms to a classical or a Bayesian bootstrap scheme encompassing the -out-of- bootstrap, where can be smaller, larger, or equal to , and the case , in the Bayesian paradigm202020Notice that leads to a more concentrated distribution around the centroid of the simplex. On the other hand, pushes weights outwards towards the faces, edges and vertices of the simplex (that is compared to uniform density implied by the flat base case ).. We call it naive because, in expectation, it recovers the naive benchmark, i.e., , where denotes the equally-weighted portfolio.

3.2 Basic Random Portfolios

We call a RP basic if, like a naive RP, the geometric representation corresponds to a standard simplex. However, we also impose the condition that is not equal to the centroid, i.e., one cannot recover the (naive) equally-weighted portfolio in expectation. This occurs whenever some form of asymmetry is introduced in the parametrization of the Dirichlet or the Multinomial model which breaks the symmetry in the distribution of the weights. By that we mean that paremeter elements cannot all be equal. For instance, setting , where is the capitilization-weighted allocation, generates a distribution of weights which has center of mass at . Although the full distribution of a linear RP statistic is no longer available in exact form under the non-flat parametrization, the central moments of the distribution still are (see [7]).

3.3 Regularized Random Portfolios

The simplex condition is typically not the only constraint that asset managers need to adhere to. When there are additional constraint, it becomes quite challenging to obtain analytical results. These additional constraints often originate from regulatory requirements and are designed to limit the risk exposure to individual security issuers or groups of issuers212121A common example is the UCITS 5/10/40 rule, which restricts single asset representation to no more than 10% of the fund’s assets and limits holdings exceeding 5% to aggregate below 40% of the fund’s assets.. As a result, upper bounds are imposed on the asset weights, either individually or collectively. Geometrically, these linear restrictions correspond to halfspaces that intersect the simplex, resulting in a polytope

| (4) |

Furthermore, managers may impose additional constraints to prevent concentration, or to align with the benchmark allocations, e.g., by setting lower and upper bounds on country or sector exposures relative to the benchmark or in terms of variation of the return difference (tracking-error), to limit transaction costs, to control portfolio characteristics (e.g., factor exposure, sustainability criteria, risk metrics), or to satisfy other specific requirements. From a sampling perspective, the mathematical characterization of constraints plays a crucial role, distinguishing between linear, quadratic, convex, non-linear, and other types. Certain risk measures like Value-at-Risk (VaR) are non-convex, meaning that, if a RP is subject to a maximum VaR constraint, it’s domain can no longer be represented by a common convex geometric body, which makes sampling extremely hard. Other measures of risk like variance or tracking error are quadratic and geometrically form ellipsoids

| (5) |

Sampling from (the surface) of an ellipsoid is relatively straightforward. However, when the simplex condition must also be satisfied, sampling from the intersection of the simplex with an ellipsoidal surface becomes a non-trivial task (albeit possible, as demonstrated in [8]).

Under general constraints, the cdf of a RP statistic is not tractable analytically and one has to turn to numerical methods (see Section 4). The following special case forms an exception. Recently, [7] demonstrated that Varsi’s algorithm can also be applied in the context of a shadow Dirichlet distribution ([45]), which is defined on a linearly constrained simplex. The shadow Dirichlet model allows for the consideration of linear regularizations of the weights, making it highly relevant in practical applications. If and an left-stochastic matrix (i.e., each column sums to one) of full rank, then , where denotes the shadow Dirichlet model with pdf

The normalizing constant is the determinant of matrix times the normalizing constant of the standard Dirichlet distribution, i.e., the multinomial beta function , where is the gamma function.

Therefore, in cases where linear constraints can be expressed using the mapping , the distribution of linear functions of a random portfolio can be precisely obtained using Varsi’s algorithm under the uniform measure. These cases are referred to as simply regularized. For all other cases where linear constraints cannot be directly accommodated, sampling methods need to be employed.

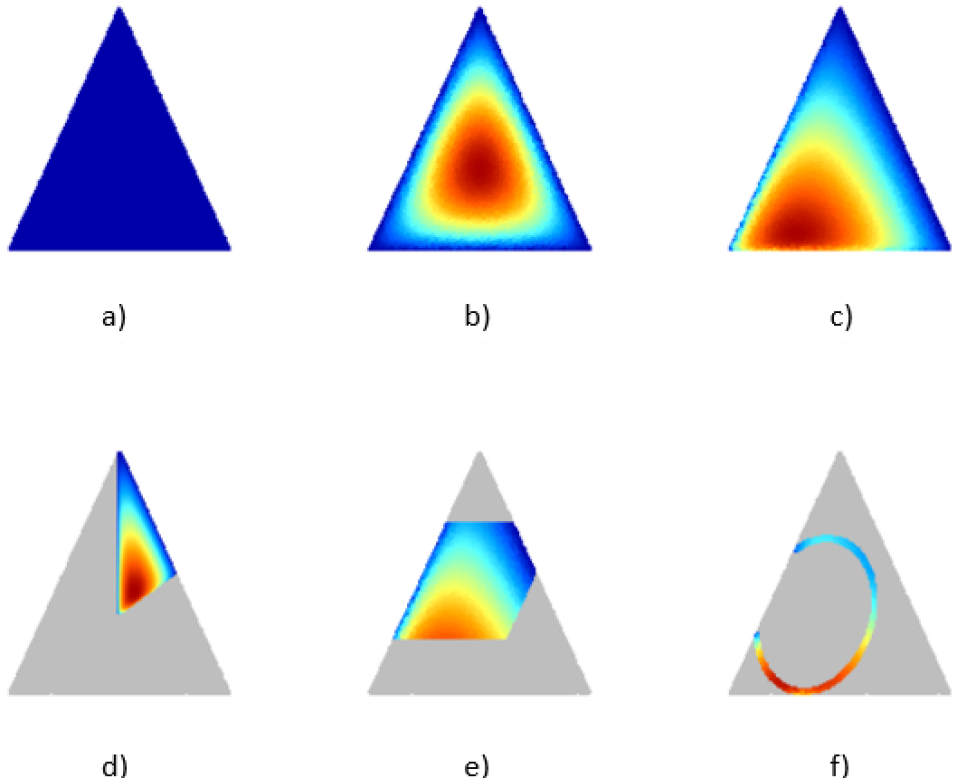

Figure 4 visualizes the different types of RPs for the case of assets. Subplot a) shows the uniform density of a naive RP defined over the unit simplex, i.e., . Subplot b) also shows another naive RP since, like a), it also centers on the naive portfolio. However, the distribution of the weights is not uniform but follows a concentrated Dirichlet model with ; , giving the distribution more mass around the center. If we would have chosen the concentration parameter , the density colors would be reverted (i.e., distributing more mass towards the boundaries of the simplex). Subplot c) shows a simple RP with ; . d) visualizes the shadow of the Dirichlet distribution in c), i.e., , restricted by a mononotic which has th column … . The so constrained weights satisfy the ordering . Subplots e) and f) show instances of generally regularized RPs defined by the intersection of the simplex with a polytope in the former case, and by the intersection of the simplex with the boundary of an ellipsoid in the latter case. In both cases, the distribution of the weights is a truncated version of the basic RP in c).

3.4 Sampling

The task of generating RP variates, i.e., the activity of obtaining realizations of a random composition having a specified distribution over a bounded domain, requires the implementation of a sampling engine. Ideally, the sampler is exact (results in random samples with exactly the desired distribution), efficient (in terms of storage space and execution222222Execution time has two components: Set-up time and marginal execution time. Set-up time is the time required to do some initial computing depending on the particular problem and marginal execution time is the incremental time required to generate each observation. time), robust (the algorithm is efficient for all parameter values), and not too complex (conceptually and also with respect to practical implementation). Whether these expectations can be met depends on the concrete problem specification, i.e., on the distributional assumption and the investment constraints which define the sampling space.

To sample from a naive, a basic or a simply regularized RP one just has to sample a Dirichlet distribution with parameter vector . To do so, it is enough to sample the marginals from a Gamma distribution with shape parameter and fixed rate parameter and then standardizing by the sum: . Recall that under the uniform measure, the naive as well as the simply regularized RP allow for an exact solution of the distribution function for linear statistics via Varsi’s algorithm. Therefore, sampling is actually not needed.

For a generally regularized RP, sampling is the only option. Under the uniform measure, the sampling problem forms an instance of the fundamental problem addressed in the seminal paper [117]: Given a bounded -dimensional body , where , find a way to efficiently sample pseudo-random points such that with denoting the -dimensional content of . While [117] considered the general case of sampling from a generic surface, here, we restrict analysis to sampling from a which is either a polytope , the interior of an ellipsoid or their intersection. Exact uniformity can only be obtained under specific circumstances which require either the applicability of transformation, composition or acceptance-rejection methods.

The transformation technique maps uniformly distributed points from a hypercube with a smooth deterministic function onto where has to preserve uniformity. A necessary and sufficient condition for this is that the Jacobian of is constant over all [117]. In principle, this is a highly efficient method since there exist very efficient pseudo-random number generator to sample from . The problem is just that is known only for a very limited class of regions like spheres or simplices, not so though for general polytopes. Theoretically, one could partition any bounded polytope into a finite union of simplices, and then apply the transformation from the hypercube to each simplex yielding the composite technique. Although conceptually sound, the complexity of identifying the simplices is generally such that the approach is not tractable computationally.

The idea behind the acceptance-rejection technique is to first find an enclosing set for which efficient sampling algorithms exist, take samples from and either accept them if they lie within or reject them, otherwise. Accepted points will be uniformly distributed in because if a point is uniformly distributed within , then it is conditionally uniformly distributed in given it lies in . The problem here is that even when is chosen based on certain optimality conditions, like the smallest enclosing sphere, the number of trial points in needed to get a point in grows, as Smith ([117]) calls it ’explosively’232323As an example, [117] shows that when is a hypercube and is a circumscribed sphere the expected number of points generated in needed to find one in grows from 1.5 for to for ..

As the dimension grows, the (only viable) solution is to sample with geometric random walks. The next Section provides a survey of existing walks that we can use to sample from a RP and, ultimately, to address the finance problems of performance and factor analysis.

4 Geometric Random Walks

Geometric random walk algorithms are a specific type of Markov chains that initiate from an interior point within a convex body . At each step, they transition to a neighboring point selected from a distribution dependent solely on the current position. The fundamental concept behind all geometric random walks is to generate a lengthy sequence of points, randomizing their order to render the sequence independent and identically distributed (i.i.d.) over . The complexity of the algorithms depends on its mixing time, i.e., the number of steps required to bound the distance between the current and the stationary distribution, and on the complexity of the basic geometric operations performed at each step of the walk; the latter is termed per-step complexity.

The problem of sampling from a bounded convex body is closely related to the problem of approximating the volume of . The first celebrated result is given in [39] where they sample approximately from the uniform distribution using a grid walk in . Since then a great effort has been devoted to geometric random walks; to mention a few seminal papers, in [117] they introduced the Hit-and-Run (HaR) algorithm, in [65] they crucially improve rounding and sampling results using Ball walk (BaW) and in [93] they show fast mixing for HaR even when the random walk starts from a corner point in . Over the last 35 years various walks have been presented, each possessing distinct advantages and drawbacks. Some routines confine the sampling space to a polytope, while others are more generic, though often, there is a trade-off between flexibility and efficiency. Further, some walks are restricted to uniform sampling while others accommodate more general distributions, although they may need some pre-processing steps where uniform samples are required. The discriminating aspect among the various routines lies in their approach to take the next Markov step, i.e., in the choice of the direction, the step-length, the curvature of the trajectory and behavior when a boundary is hit.

Figure 5 illustrates the mechanisms of four geometric random walks which are at the basis of various descendent methods. For HaR, the logic is as follows: Start with an arbitrary point inside the convex body. Then, generate a random direction vector with each component sampled independently from a standard normal distribution. Compute the intersections between the line defined by the point and the direction vector and the boundary of . Finally, choose a random point on the segment defined by the two computed boundary points and repeat the process. The choice of the random distribution on the segment needs to be chosen with respect to the target distribution (for instance, uniformly, if the target is to sample uniformly distributed points). Billiard Walk (BiW) [51] operates similarly to HaR, but it exclusively moves in the direction of and reflects the ray upon encountering the boundary whereby the exit angle matches the entry angle. Both methods work on general , but BiW is limited to sampling from the uniform distribution. Dikin walk [103] (and other ellipsoidal procedures like Vaidya and John walk) choose their steps by sampling uniformly from an ellipsoid centered at the current point whose shape and size are determined by the shape of and the proximity of the current point to the boundary. Those algorithms are very efficient even in high-dimensional cases but only allow for uniform sampling from polytopes. Hamiltonian Monte Carlo (HMC) [105] is a sophisticated technique that employs Hamiltonian dynamics to enhance sampling efficiency. It picks a random velocity according to a local distribution and then walks on a Hamiltonian trajectory, i.e., a trajectory which is given by the Hamiltonian dynamics, to obtain the next Markov point. So generated proposals exhibit less of a random-walk behavior, resulting in more effective and less correlated samples. Various versions of HMC exist, all allowing sampling from general log-concave distributions, though some versions (Riemannian HMC [72]) are limited to polytopes.

In the following we discuss important aspects that are common to all routines before moving to a detailed description of the individual procedures. We provide a survey of all existing routines. Readers seeking more in-depth understanding of the technicalities are encouraged to consult the source literature for a more comprehensive exploration.

Distribution support.

We assume that the support of the target distribution is either a full dimensional convex polytope given by a set of linear inequalities as Eq. (4) or the intersection between a polytope and an ellipsoid (see Eq. (5)). In either case we may refer to the support as a convex body. In the case where the portfolio domain is given also by an additional set of equalities –which is always the case in our examples since we require portfolios to be fully invested (simplex condition)– we transform it using an isometric transformation to obtain a full dimensional polytope and ellipsoid. In particular, let, for example, the set be defined by the corresponding additional equality constraints. Then, we compute an orthonormal basis of the null space of the matrix and we project the polytope and the ellipsoid onto the null space to obtain a full dimensional polytope and ellipsoid in the form of and respectively. Let us demonstrate an example using the Dirichlet model in Eq. 2 truncated in the intersection between a convex polytope and an ellipsoid, i.e.,

| (6) |

Notice that in this case . Consider the transformation , where is the matrix that generates the null space of and a feasible point in the support of . When we apply the transformation on both and its support we obtain the density,

| (7) |

since . By replacing in the constraint equations one could also obtain the support of the transformed density . Finally, we sample from the full dimensional body in the null space and we apply the inverse transformation to obtain the sampled portfolios in the initial space.

In the sequel, we consider the case of sampling from a full dimensional convex set given by the intersection between a convex polytope and an ellipsoid,

| (8) |

Computational oracles.

Each geometric random walk uses certain sub-routines called oracles. An oracle is an algorithm that answers a certain question that is needed for the implementation of a random walk. The oracle that every geometric random walk needs is the membership oracle that answers if a given point belongs or not in . The simplest implementation of this oracle is to check the validity of the Eq. (4, 5).

Another useful sub-routine is the boundary oracle that computes the intersection between the boundary of , denoted , and a ray that starts from a point in the interior of , let . To compute the intersection with we have to solve one linear equations per facet and keep the smallest positive root. We have,

| (9) |

where is the number of facets and are the normal vectors defining the support hyperplane of each facet. The computations in Eq. (9) costs operations242424Here and in the remainder of the text we use Bachmann-Landau symbols to express computational complexity (in terms of oracle evaluations and arithmetic operations) as a function of the dimension of the geometric object. Additionally, the notation means that we are ignoring polylogarithmic factors.. To compute the intersection with we have to solve the following equation and keep the smallest positive root,

| (10) |

That is a second order polynomial equation for which we have a closed form to compute its roots. The computations in Eq. (10) costs operations. Clearly, in the case of the body we solve both Eq. (9, 10) and keep the smallest positive root . Then, is the intersection point.

Some random walks, like e.g., BiW, use a sub-routine called reflection oracle. This oracle computes the reflection of a ray when the later hits the boundary of so that the reflected ray continues in . Typically, this oracle is called after the boundary oracle which computes the boundary point of ray intersecting . Let the normal vector defining the tangent hyperplane at and the direction vector of the ray until it hits . Then, the update rule to obtain the direction vector of the reflected ray is the following,

| (11) |

Thus, the reflected direction can be computed after operations, given the normal vector . When hits a facet of the vector is equal to the normal vector of that facet, i.e., equal to the normalized row of the matrix that corresponds to that facet. When hits the vector is equal to , where is the boundary point.

Last, certain random walks need to sample uniformly from special sets, namely from the boundary and/or the interior of the unit ball and the interior of a given ellipsoid. To sample from the boundary of the unit ball we sample numbers from the standard Gaussian distribution and then the vector is uniformly distributed on the boundary of . Moreover, the point , where is uniformly distributed in , is uniformly distributed in . Last, the point , where is uniformly distributed in the boundary of and , is uniformly distributed in the ellipsoid .

Computing an interior point.

To run a geometric random walk it is necessary to compute a point in the interior of the convex body we want to sample from. When the convex body is the convex polytope in Eq. (4) one could compute the largest ball inside , called Chebychev ball. Then, by definition, the center of the ball lies inside . To compute the Chebychev ball we have to solve the following linear program,

| (12) |

where are the rows of the matrix in Eq. (4). When the convex body is the intersection between a polytope and an ellipsoid, , one could apply on the transformation that maps the ellipsoid to the unit ball and consider the intersection of the transformed polytope with . Then, the largest ball inside the latter body can be computed by solving the following Second-Order Cone Program (SOCP),

| (13) |

where the pairs define the facets of the transformed polytope. We can obtain a point in by applying the inverse transformation on the computed center in Eq. (13).

Empirical convergence to the target distribution.

In order to evaluate the quality of a sample as an accurate approximation of the target distribution, several convergence diagnostics [110] are available like potential scale reduction factor (PSRF) [48], maximum mean discrepancy (MMD) [50] and the uniform tests [33]. For a dependent sample, a powerful diagnostic is the effective sample size (ESS). It is the number of effectively independent draws from the target distribution that the Markov chain is equivalent to. In our empirical applications, we ensure that PSRF and ESS , where reflects the dimensionality of the problem (i.e., in general the number of assets minus the number of equality constraints).

Starting point.

A crucial aspect for the efficiency of a random walk is its starting point, which needs to be a point in the interior of the convex body. When the starting point comes from a distribution close to the target distribution, then it is called a warm start. The mixing time analysis in the literature usually requires a warm start to bound the rate of convergence. When the starting point is a fixed or a corner point it is called a cold start. Regarding uniform sampling, in [94] they give an algorithm that computes a warm start after calls to the membership oracle of the input convex body.

In practical implementations the starting point usually is a ”central” point as the Chebychev or the analytical center of the polytope [35, 22, 72]. A common practice is to allow for a user defined positive integer that corresponds to the number of Markov points to be ignored before the implementation starts to store the generated points. Several practical methods have been developed to compute a good starting point [41, 27, 28, 35].

Roundness of the distribution.

Another key aspect affecting the performance of a random walk is the roundness of the target distribution, that is how close the covariance of the target distribution is to the identity matrix. Regarding uniform sampling, this is translated to body’s roundness, measured by the ratio [65, 93]. and are the radii of the largest and smallest ball centered at the origin that contains, and is contained, in , respectively; i.e., . Hence, before the actual sampling process is started, it is crucial to reduce , i.e., to put in a well-rounded position, where . This is particularly relevant for financial applications like the one we suggest in our empirical study in Section 5 because lower and upper bounds on asset weights are typically tight, inducing a skinny polytope.

A powerful approach to obtain well roundness is to put in isotropic position. In general, is in isotropic position if the uniform distribution over is in isotropic position, that is and , where is the identity matrix. Thus, to put into isotropic position one has to generate a set of uniform points in its interior and apply to the transformation that maps the point-set to isotropic position; then iterate this procedure until is in -isotropic position [35, 93]. In [112] they prove that iterations and uniformly distributed points per iteration suffice to achieve isotropic position. There are several algorithms based on this routine [65, 94, 62]. In [62] they build upon [129] to provide the best algorithm so far that puts a convex body in isotropic position after membership oracle calls. The practical method in [27] brings a convex body in near-isotropic position by using BiW with multiple starting points for uniform sampling in each phase. It successfully rounds convex polytopes in a few thousand dimensions.

An alternative notion of well roundness is the John position. A convex body in John position has a sandwiching ratio of which is worse than that of isotropic position. To put the body in John position one needs to compute the maximum volume ellipsoid (MVE) in it and apply to the body the transformation that maps the ellipsoid to the unit ball. To our knowledge there are specialized results only for the case of a convex polytope . In [106, 4] they independently give an algorithm that computes the John ellipsoid of in operations. Interestingly, in [69] they provide a linear time transformation of the MVE problem by computing a minimum volume enclosing ellipsoid (MVEE) of a set of points. Thus, the algorithms in [74, 123] that solve the MVEE problem can be used to compute the John ellipsoid after operations. The practical method in [134] to compute the MVE has been used in [53] to bring convex polytopes of thousands of dimensions in John position. However, the practical method in [27] obtains, in almost the same runtime, both a better sandwiching ratio than [134] –as it brings the polytope to a near isotropic position– and a uniformly distributed sample in . Last, in [32, 118] they provide algorithms to compute the John ellipsoid in the special case of a centrally symmetric convex polytope achieving near optimal performance. However, those algorithms can not be used for the purpose of rounding any convex polytope. For an overview in rounding a convex body we refer to Table 1.

| Year & Authors | Type of rounding | Total cost | Polytope | Convex body |

| 1997 [65] | Isotropic position | memb. calls | ✓ | ✓ |

| 1999 [106, 4] | John position | operations | ✓ | ✗ |

| 2003 [134, 53] | ∗John position | ?? | ✓ | ✗ |

| 2005 [74, 123] | John position | operations | ✓ | ✗ |

| 2006 [94] | Isotropic position | memb. calls | ✓ | ✓ |

| 2016 [35] | ∗Isotropic position | ?? | ✓ | ✓ |

| 2021 [62] | Isotropic position | memb. calls | ✓ | ✓ |

| 2021 [27] | ∗Isotropic position | ?? | ✓ | ✓ |

∗Practical methods.

To round a log-concave distribution with density function , is chosen to bound the expected squared distance of the random variable from the centroid of , i.e., , where is the centroid. We say that a log-concave density function is well-rounded if , where is the radius of the ball contained in a level set of of constant probability.

In [91] they provided the first algorithm to round a log-concave distribution after membership oracle calls, where is a convex function. They introduce an iterative algorithm that brings to isotropic position a certain level set of the density function, showing that it suffices to bring it to a near isotropic position. The algorithm can use either HaR or BaW. In [92] they give an algorithm that uses HaR and rounds a log-concave distribution after membership oracle calls; they generalize the algorithm in [64] that is specialized for the exponential distribution. Moreover, if a near-optimal point of is given they provide a multi-phase algorithm that rounds after membership oracle calls. The main idea in [64, 92] is to consider the density function,

| (14) |

where the parameter controls the variance of . They introduce a new multi-phase algorithm where in each phase they set a different value of ; the last phase sets and samples from . Initially, the algorithm invokes the rounding algorithm outlined in [94] to obtain a warm start for the uniform distribution over . In the initial phase, it samples for , representing the uniform distribution. As the algorithm progresses to the -th phase, the parameter incrementally increases to ensure that a sampled point from serves as a warm start for in accordance with the norm on density functions. Furthermore, the sample generated in the -th phase is utilized to estimate the covariance matrix for the subsequent phase. Upon reaching , the algorithm concludes by applying a linear transformation to both and , converting the ellipsoid defined by the approximated covariance into the unit ball. Consequently, the resulting density function is well-rounded. Lastly, it is important to state that these rounding results on constrained, log-concave density functions, highlight the importance of HaR since it can mix starting from warm starts or even from cold start, which can be exploited to reduce the number of phases we need to round .

| Year & Authors | Random walk | Mixing time | Cost per step in | Cost per step in |

| 2006 [93] | Hit-and-Run | |||

| 2014 [51] | Billiard walk | ?? | ||

| 2016 [82] | Geodesic walk | – | ||

| 2016 [103] | Generic Dikin Walk | |||

| 2017 [130] | Vaidya walk | – | ||

| 2018 [131] | Approximate John walk | – | ||

| 2018 [52] | John’s Walk | – | ||

| 2018 [83] | Uniform Riemannian HMC | – | ||

| 2019 [65] | Ball walk | |||

| 2020 [75] | Dikin walk | – | ||

| 2020 [75] | Weighted Dikin Walk | – | ||

| 2021 [27] | Multiphase Billiard walk | ?? | ||

| 2021 [84, 97, 129] | †Ball walk | |||

| 2022 [133] | †Hit-and-Run | |||

| 2022 [72, 73] | Riemannian HMC | – | ||

| 2023 [76] | Coordinate Hit-and-Run |

† For a convex body in isotropic position; for Ball walk in the case of an isotropic convex polytope the (amortized) cost per step is when an -warm start in the interior of the polytope is given.

Best mixing times.

Regarding uniform sampling from a general convex body, best mixing time is achieved by HaR and Ball walk (BaW, see Section 4.1, that is steps for a body in general position with sandwiching ratio equal to . However, one could bring the body to a near isotropic position, as a preprocessing step, after membership oracle calls. Then, both HaR and BaW can generate an almost uniformly distributed point after steps. Then, the efficiency per almost unifromly distributed point depends on which oracle is cheaper (i.e., the membership or the boundary oracle). In the case of sampling uniformly from a bounded convex polytope , we have that the number facets to guarantee boundness. Therefore, for a convex polytope in a general position, the best mixing time is given between Weighted Dikin walk [75] and Riemannian HMC [83] while their mixing times do not depend on . Since they have the same cost per step, which is the most efficient random walk depends on the number of facets . Let where . For the most efficient random walk is Riemannian HMC and for Weighted Dikin walk achieves a smaller mixing time. However, if one brings to a near isotropic position, the most efficient option is BaW since its mixing time is (same with HaR and Weighted Dikin walk) and its cost per step is the smallest among all uniform samplers, i.e., steps.