Local sensitivity analysis of heating degree day and cooling degree day temperature derivatives prices

Abstract

We study the local sensitivity of heating degree day (HDD) and cooling degree day (CDD) temperature futures and option prices with respect to perturbations in the deseasonalized temperature or in one of its derivatives up to a certain order determined by the continuous-time autoregressive process modelling the deseasonalized temperature in the HDD and CDD indexes. We also consider an empirical case where a CAR process of autoregressive order 3 is fitted to New York temperatures and we perform a study of the local sensitivity of these financial contracts and a posterior analysis of the results.

1 Introduction

Weather related risks can be hedged by trading in weather derivatives. The Chicago Mercantile Exchange (CME) organizes trade in futures contracts written in weather indexes in several cities around the world. We focus on the temperature indexes HDD (heating-degree day) and CDD (cooling-degree day) which measure the aggregation of temperature below and above a threshold of F over a time period, respectively. The daily modelling of temperature is an approach that can be used to get the non-arbitrage price of temperature derivatives. A continuous-time function which consists of a deterministic term modelling the seasonal cycle of temperatures and a noise term modelling uncertainty is fitted to historical time series of daily average temperatures (DATs). Several empirical studies of temperature data, see Härdle and López Cabrera [6], Benth and Šaltytė Benth [3] and the references therein, have shown that continuous time autoregressive (CAR) models explain very well the statistical properties of the deseasonalized temperature dynamics. Although this approach requires a model for the instantaneous temperature, it has the advantage that the model can be used for all available contracts on the market on the same location. In Benth and Solanilla Blanco [2], HDD and CDD futures prices based on CAR temperature dynamics and option on these futures are derived theoretically. An approximative model for the HDD and CDD futures is suggested in order to derive a closed formula for the call option price. The (approximative) formulas for HDD and CDD futures and option prices depend on the deseasonalized temperature and its derivatives up to , where refers to the autoregressive order of the CAR process which models the deseasonalized temperature dynamics of these indexes.

The objective of this paper is to study the local sensitivity of the (approximative) HDD and CDD futures and option prices derived in Benth and Solanilla Blanco [2] with respect to perturbations in the deseasonalized temperature or in one of its derivatives up to order . To do so, we consider the partial derivatives of such financial contracts with respect to these variables evaluated at a fixed point. Local sensitivity measures parameter importance by considering infinitesimal variations in a specific variable.

Sensitivity analysis is widely used in mathematical modelling to determine the influence of parameter values on response variables. The local sensitivity analysis with partial derivatives is a first step to study the response of a model to changes in their inputs variables. In mathematical finance there is extensive literature of Greeks, which are quantities representing the sensitivity of derivatives prices to a change in underlying parameters. The sensitivity analysis focused on HDD and CDD futures and option prices where the temperature dynamics follows a CAR process has not been considered yet. Our contribution is a first analysis of the local sensitivities of such financial contracts with respect to a perturbation in the deseasonalized temperature or in one of its derivatives.

The paper is structured as follows: in the next section we review results concerning the arbitrage-free pricing of temperature HDD and CDD futures with measurement over a period and call options written on these. We also derive some results to study the sensitivity of these financial contracts to perturbations in the deseasonalized temperature or in one of its derivatives up to order , with being the order of the CAR process used to model the deseasonalized temperature in these indexes. In Section 3 we adapt all the results in Section 2 for the case where the measurement time is a day instead. In Section 4 we consider a previous empirical study of New York temperatures where the deseasonalized temperature dynamics follows a CAR(3)-process and we study local sensitivity of HDD and CDD futures and option prices with a measurement day. In Section 5 we include an empirical analysis of the sensitivity of the HDD and CDD futures prices with measurement over a period. Finally, in Section 6 we present a conclusion of the results.

2 Sensitivity of CDD and HDD derivatives prices with measurement period

In this Section we review results concerning pricing futures written on the temperature indexes CDD and HDD defined over a measurement period and call options on these temperature futures. These results are the baseline to develop a study of the sensitivity of these financial contracts with respect to changes in the components of the vector function involved in the definition of the indexes.

Let be a complete probability space, the CDD and HDD indexes over a time period , are defined respectively as

and

where is the daily average temperature in the location at time and the threshold is F (or C). The temperature is modelled as by means of a seasonal function and a CAR()-process defined as the first component of a multivariate Orstein-Uhlenbeck process with dynamics

| (2.1) |

We use the notation to denote the transpose of a vector (or matrix) . The matrix , which has a particular representation, contains the different speeds of mean reversion. We assume the condition of having different eigenvalues with strictly negative real part in order to have a stationary model. The function is the time-dependent volatility of the process. The arbitrage-free futures price written on a CDD index at time with measurement period is defined as

| (2.2) |

where the conditional expectation is taken under some probability . Analogously it can be considered for HDD indexes. We choose to work with the probability measure considered in Benth and Solanilla Blanco [2] given by a Girsanov transform which involves the parameter function referred as the market price of risk and the the stochastic process modeling the volatility. For a better understanding of this setting we refer Benth and Solanilla Blanco [2], where it is possible to find also all the results that we present next about futures and call options prices. We recall the CDD and HDD futures prices formulas provided in Proposition. 2.1 and Proposition. 2.3 respectively. For our convenience in this setting we restrict , so that

| (2.3) |

and

| (2.4) |

Note that , with being the cumulative standard normal distribution function and for

If we consider the initial condition , then as defined in (2.2) is a random variable for with all the stochasticity contained in the term . In our setting we loose this condition when for we fix with . In such a case the CDD futures price can be explained as a deterministic function. Denote by , for the th component of . Note that . We find that the term in the CDD and HDD future prices can be rewritten as follows

| (2.5) |

where for

that is as a linear combination of the components of . From now on, we focus on CDD futures prices and call options written on these. Similar results can be obtained considering the HDD index. The new notation in (2.5) let us to rewrite the CDD future price formula in (2.3) as follows:

| (2.6) |

To answer the question to what extent an infinitesimal change in a component of is affecting the behavior of the CDD futures price, we need to consider partial derivatives of this with respect to the components of say to avoid misunderstandings in the notation. In the next proposition we consider the partial derivatives of the CDD futures price with respect to the components of .

Proposition 2.1.

Let , then for it holds that

Proof.

The proof follows by first exchanging the derivative and the integral and afterwards applying the chain-rule on the integrand. In this last step consider that and take into account that can be rewritten as a linear combination of the components of

so that

CDD futures prices depend nonlinearly on the vector which is included in the function . This fact makes difficult to derive analytic formulas for plain vanilla options (call options) which are traded at the CME. To this aim, we recall some useful linearized formulas that allow to approximate the CDD futures prices. Let , setting in (2.6) reduces to

| (2.7) |

where

We can consider the first order Taylor approximation instead, then (2.6) reduces to

| (2.8) |

where

We introduce a new notation that encompasses both approximated formulas for the CDD futures price. To this end let , then

| (2.9) |

where and are generic notations for and or and . The next proposition provides the partial derivatives of the approximate CDD futures prices with respect to the components of

Proposition 2.2.

Let , then it holds that

| (2.10) |

for where is the generic notation for and .

Proof.

Rewrite (2.9) in terms of the components of as

and differentiate with respect to the components for .

Observe that (2.10) does not depend on .

We consider now CDD and HDD futures prices as the underlying to price call options. The arbitrage-free price for a call option with strike at exercise time , written on a CDD futures with measurement period , with and for times is defined as

| (2.11) |

where is the risk-free interest rate. All the stochasticity in the call option price is in the term which is contained in the CDD futures price at exercise time and more specifically in . For ,

| (2.12) |

is a solution of the stochastic differential equation in (2.1). Therefore reduces to

| (2.13) | ||||

where the dependence on is explicited in . We can use the same argument as for the CDD futures price to rewritte the call option price as follows

| (2.14) |

To study the sensitivity of the call option price with respcect to infinitesimal changes in the components of we have to consider also partial derivatives which is not an easy task, if possible. To avoid differentiating the payoff , it is known the density approach which moves the dependency of from the payoff to the required density function to compute the conditional expectation, see Broadie and Glasserman [4]. Next, we see that this method fails here because the payoff function is path-dependent on from to . Indeed, the payoff function contains the term in which depends on as we have seen in (2.13). This fact makes not possible to perform the study of the sensitivity in call options written on CDD futures prices over a measurement period with respect to infinitesimal changes in . The linearized CDD futures price as defined in (2.9) makes possible to get an approximate call option price formula which is analytically treatable in the sense that approximation methods like Monte Carlo are not required. This problem is thoroughly tackled by setting in (2.14) the linearized CDD futures prices defined in (2.9), see Benth and Solanilla Blanco [2] for a detailed explanation. The approximate formula for the call option price then reduces to

| (2.15) | ||||

with

and

Observe that the approximate call option becomes explicitly dependent on the approximate futures price. The next proposition provides the partial derivatives of the approximate call option price with respect to the components of .

Proposition 2.3.

Let , then it holds that

for

Proof.

In the next section we simplify our setting to perform the study of sensitivity and consider futures prices with a measurement day and call options written on these.

3 Sensitivity of CDD and HDD derivatives prices with a measurement day

In this Section we perform a complete study of the sensitivity of CDD and HDD futures prices with a measurement day and call options written on these to infinitesimal changes on the components of .

The Fubini-Tonelli theorem, see e.g. Folland [5] connects futures prices setting over a time period and futures prices with a delivery day running over a time period as follows

| (3.1) |

for . We see that is expressed as the CDD futures price at time with a measurement day , denoted , running over the time period Consequently, we deduce from (2.3) and (2.4) respectively that

and

where, for

Recall that , with being the cumulative standard normal distribution function. The same notation introduced in (2.6) can be used in this context, then

The term included in and rewritten as in (2.5) contains all the stochasticity of the futures prices and provides information about its evolution. Note that when the time to measurement , the function tends to zero for since the real parts of the eigenvalues of the matrix are all strictly negative for having a stationary model. Hence, at the long end we can say that the behavior of the future prices is not affected by this term. But, if is approaching to zero, the term is influenced for all the components of the . Finally, for , only the first component of takes part on the evolution of the futures prices. These arguments determine the evolution of futures prices at time when time to delivery is a day , . In the case of futures prices with measurement period as presented in Section 2, we have to take into account that is running over a measurement period. In the next proposition we consider the partial derivatives of the CDD futures price with respect to the components of .

Proposition 3.1.

Let , it holds that

for .

Proof.

The proof follows by applying the chain-rule. Consider that and also take into account that can be written as a linear combination of the components of as follows

so that

Next, we also adapt the linearized formulas for CDD futures prices presented before to our setting. To this end let , formulas (2.7) and (2.8) reduce respectively to

| (3.2) |

where

and

| (3.3) |

where

We provide also the new notation that encompasses both approximate CDD futures prices formulas. To this end let , then

| (3.4) |

where and are generic notations for and or and . The next proposition provides the partial derivatives of the approximate CDD futures prices with respect to the components of .

Proposition 3.2.

Let , then it holds that

| (3.5) |

for , where is the generic notation for and .

Proof.

Rewrite (3.4) in terms of the components of as

and differentiate with respect to the components for .

Observe that unlike the result in Proposition. 3.1, here we loose the dependency on .

The arbitrage-free price for a call option with strike at exercise time , written on a CDD futures with measurement day , for a time with is defined as

| (3.6) |

where is the risk-free interest rate. For our purposes and making use of the same argument as in Section 2 we can rewritte (3.6) as

| (3.7) |

Next, we see that the density approach here works well as the payoff function of the call option price is not path-dependent on over a time period. In the next Proposition we present then the partial derivatives of the call option price with respect to the components of .

Proposition 3.3.

Let , then it holds that

for , where for

is a normally distributed random variable and

are the mean and the variance of conditioned on , respectively.

Proof.

The random variable included in is normally distributed and

and

are the mean and the variance of , respectively, conditioned on The probability density function of is then

We see that we have moved the dependency of contained in from the payoff function to the required density function to compute the the conditional expectation as follows

Next, we adapt to our setting the approximate call option price formula in (2.15) which reduces to

| (3.8) | ||||

with

and

We end up this Section with a result for the partial derivatives of the approximate call option price with respect to the components of .

Proposition 3.4.

Let , then it holds that

for

4 Empirics

Consider the stationary CAR()-process obtained to model the temperature data from New York in Benth and Solanilla Blanco [2] which is defined with the following mean reverting matrix ,

and a constant volatility, . The function which defines the CDD and HDD futures price now reduces to

Furthermore we choose to work with and fix the measurement day as August 1st, 2011. We focus our empirical study on CDD futures prices with a measurement day being August 1st, 2011 and call options written on these. We include also a final section with some empirics on CDD futures prices with a delivery period being August 2011. We choose to work with delivery in August 2011, whether it is a particular day or all the month, as it was proved in Benth and Solanilla Blanco [2] that the approximative formula for the CDD futures price worked well in this time period.

To analyze the sensitivity of CDD futures prices with measurement as August 1st 2011 we consider Proposition. 3.1 and Proposition. 3.2 in Section 3. In this context, the random variable which makes the difference between the result provided in Proposition 3.1 and Proposition 3.2 can be rewritten as where

| (4.1) |

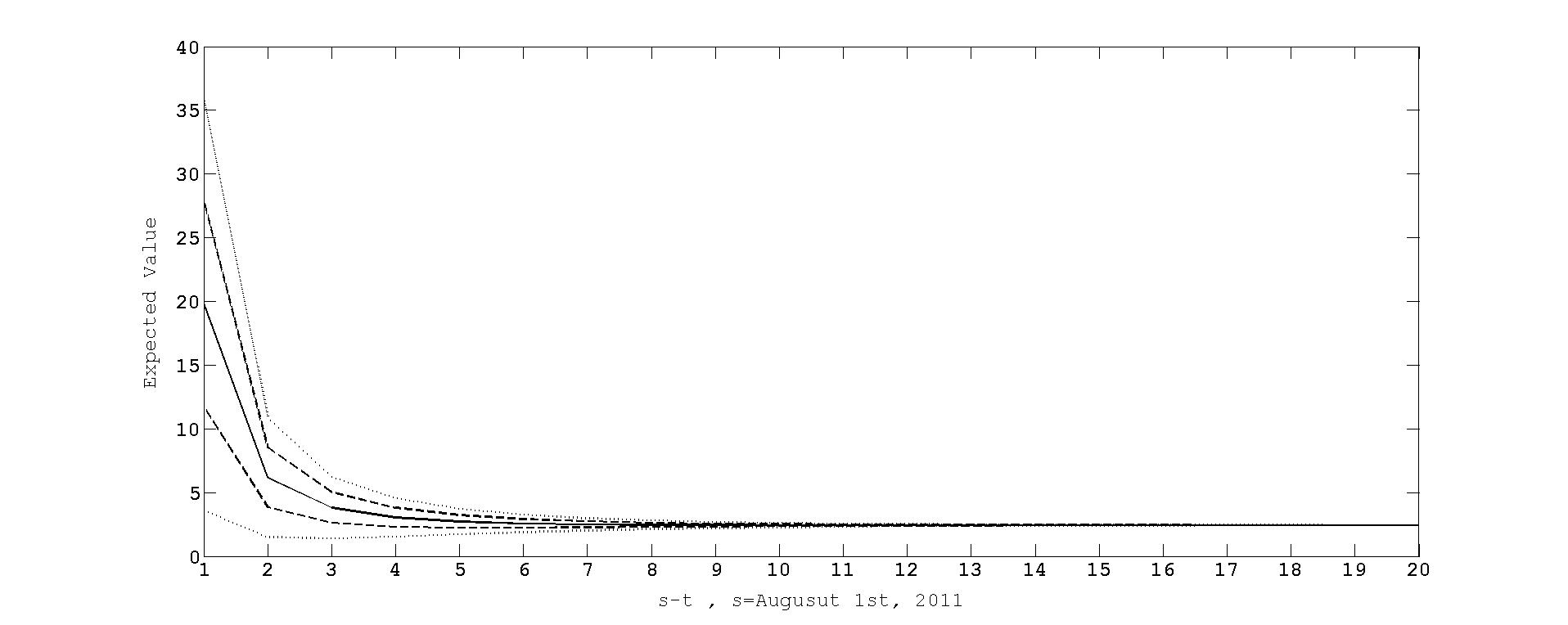

and is the time to maturity. In Benth and Solanilla Blanco [2], a more general study with being a time dependent function concludes that when the expected value of tends to and the variance . Such a case indicates too much dispersion. On the other hand, when , the variance of tends to zero, then . Figure. 1 shows the tendency when the measurement day is August 1st, 2011.

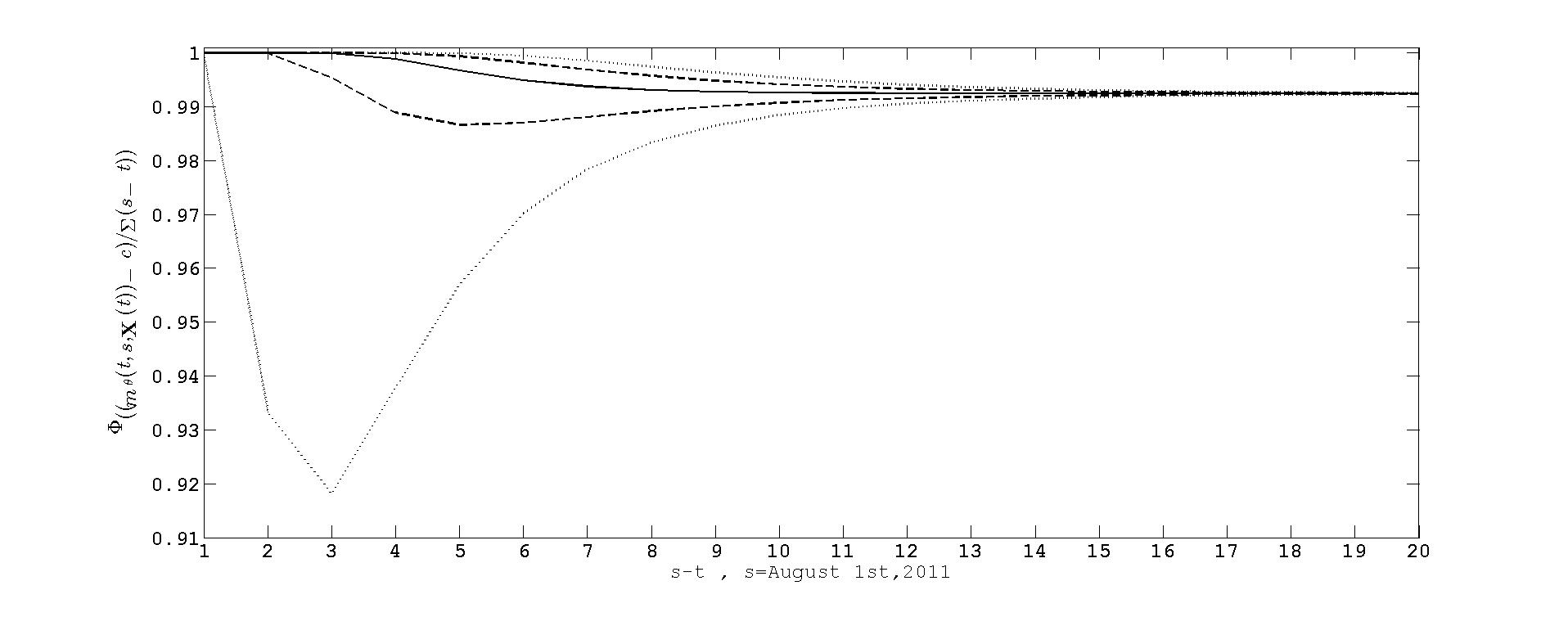

Figure. 2 is the result of applying the function to the plot in Figure. 1. We see that for . From to there is a small decay and finally stabilizes at 0.9924 for . The values between the dashed lines are more probable than the ones in between the dotted lines. We deduce that

for , i.e., the approximate CDD futures prices are more sensitive to changes in the components of than the CDD futures prices.

Recall from Benth and Solanilla Blanco [1] that contains the deseasonalized temperature and its derivatives up to order . In our setting then, reduces to

| (4.2) |

where and are respectively the slope and the curvature of , respectively.

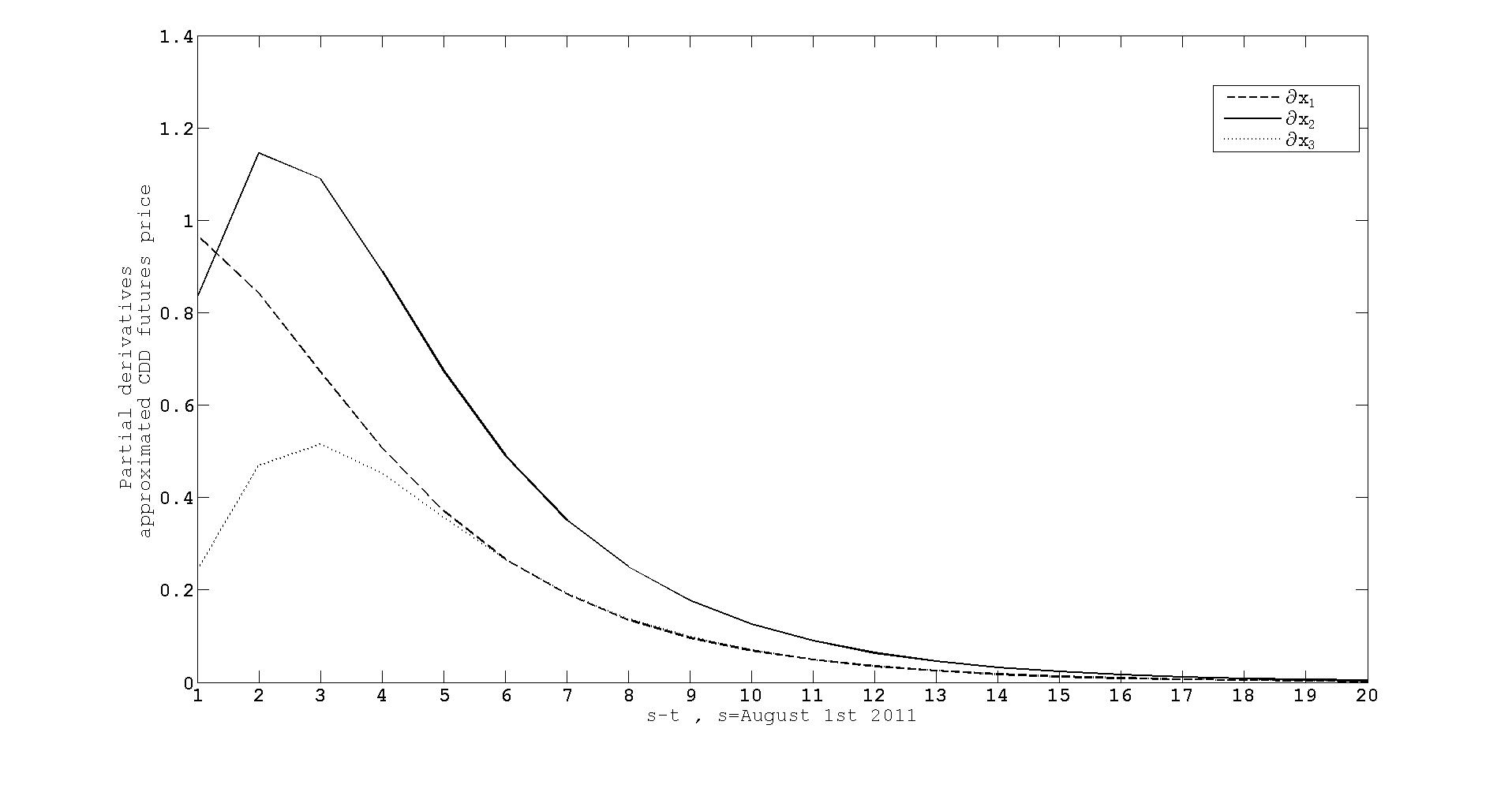

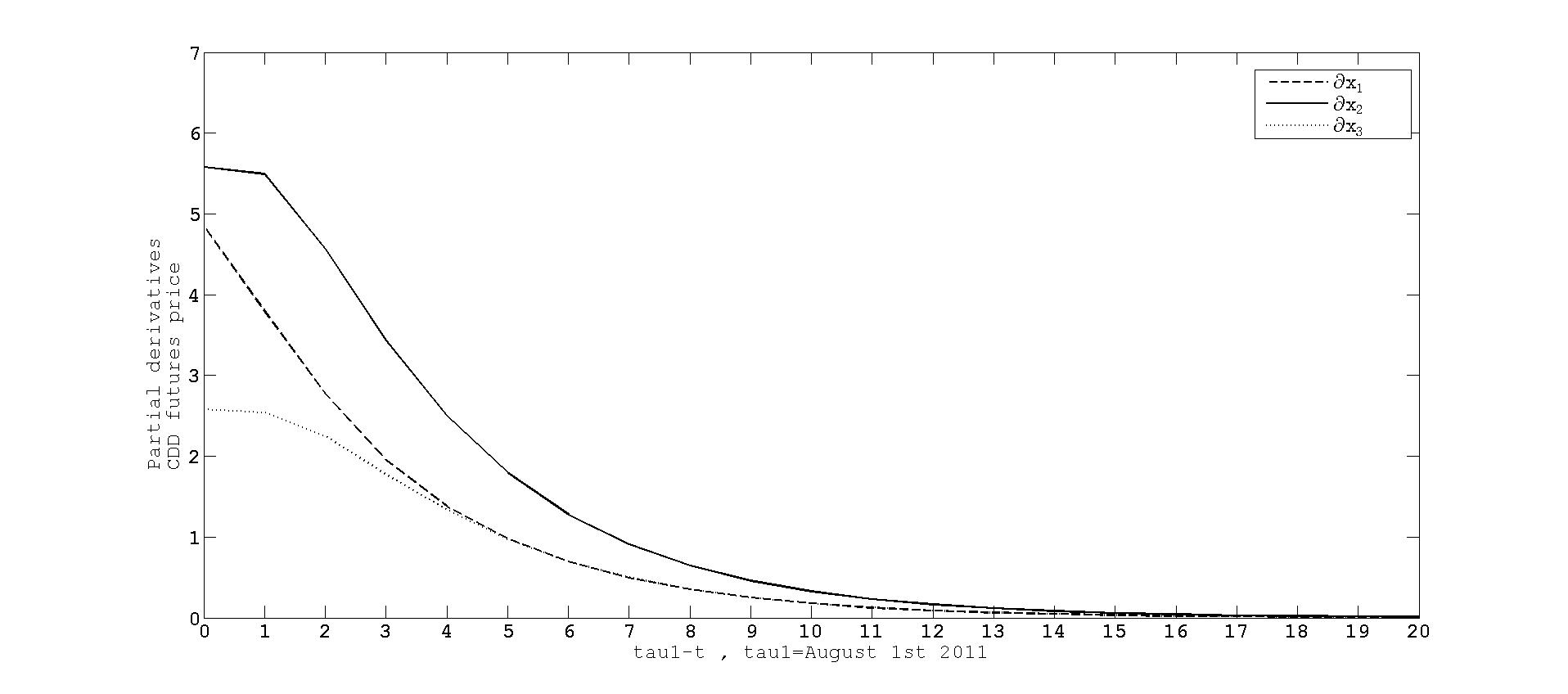

Figure. 3 shows the partial derivatives of the approximate CDD futures price with respect the coordinates of as presented in Proposition. 3.2. The x-axis considers the time to maturity, , where the measurement day is August 1st, 2011. The y-axis shows the different partial derivatives. Firstly, we observe that the partial derivatives of the approximate CDD futures price are positive. We see that at time to maturity any perturbation in the component affects the tendency of the approximate CDD futures price more than in the components and . However, when time to maturity increases the contribution of decreases gradually. From to the contribution of increases to the extent that at time to maturity perturbations in dominate the evolution of the approximate CDD futures price. From the contribution of decreases gradually but it remains always above . The contribution of increases from to . For bigger times to maturity it decreases gradually. We point out that variations in always contribute less than variations in or . At the long end, small variations in any component hardly affect the tendency of the approximate CDD futures price. This fact makes sense as the term , which is dependent on the coordinates of , tends to zero at the long end. The partial derivatives of the CDD futures price with respect the coordinates of , as presented in Proposition. 3.1, depend on . The first component corresponds to the deseasonalized temperature. We approximate the derivatives of with backward finite differences. Hence is approximated by the difference between the deseasonalized temperature at times and . is approximated by a linear combination of the deseasonalized temperatures at times and the two prior times and . Finally, we get the following relation between the temperature and the seasonal function:

| (4.3) |

Observe that given a fixed with , the temperature at time is approximately degrees above the seasonal mean function and one and tho days prior to , it is approximately and degrees above the seasonal mean function, respectively.

Consider where is the null vector in . The partial derivatives of the CDD futures price are completely deterministic. By the relation between the temperature and the seasonal function established in (4), for this particular case the temperature for the time and the two prior times and is approximately the seasonal mean function.

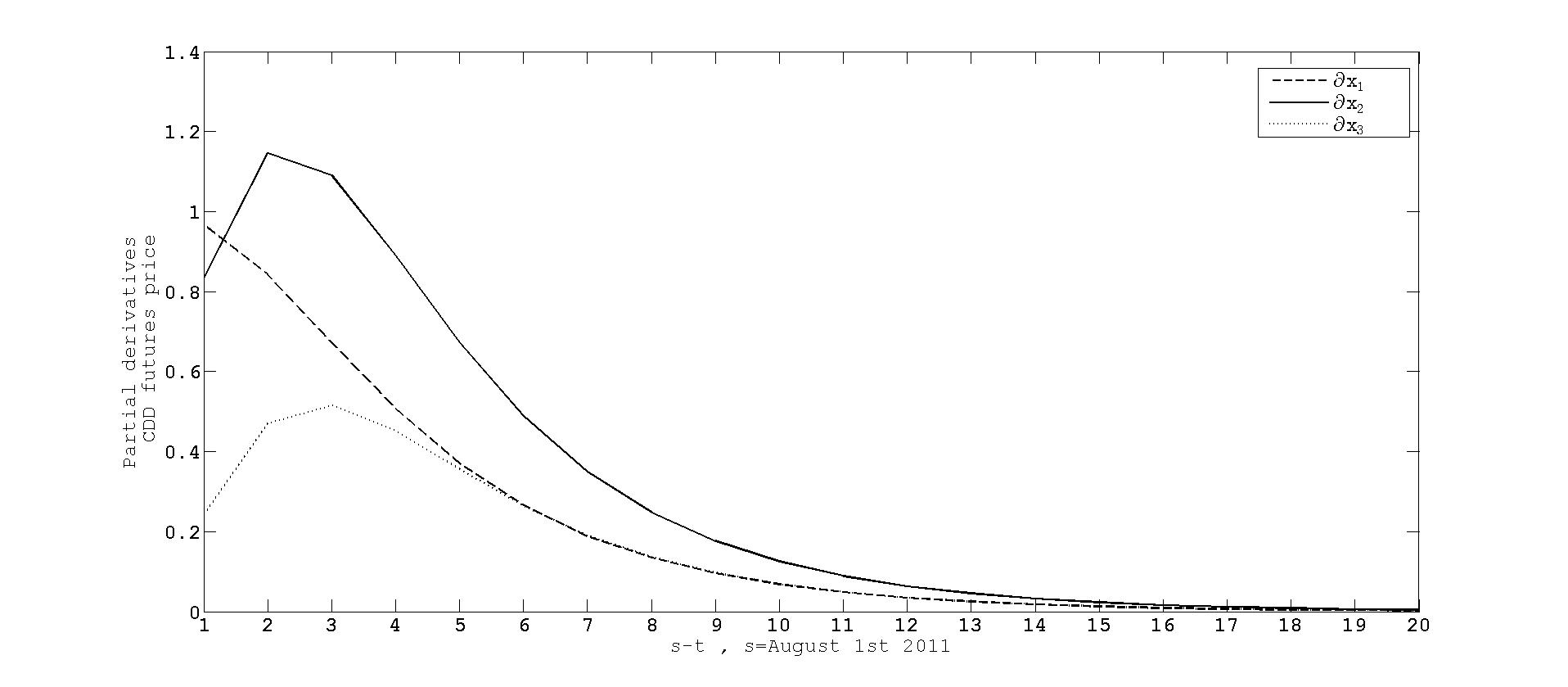

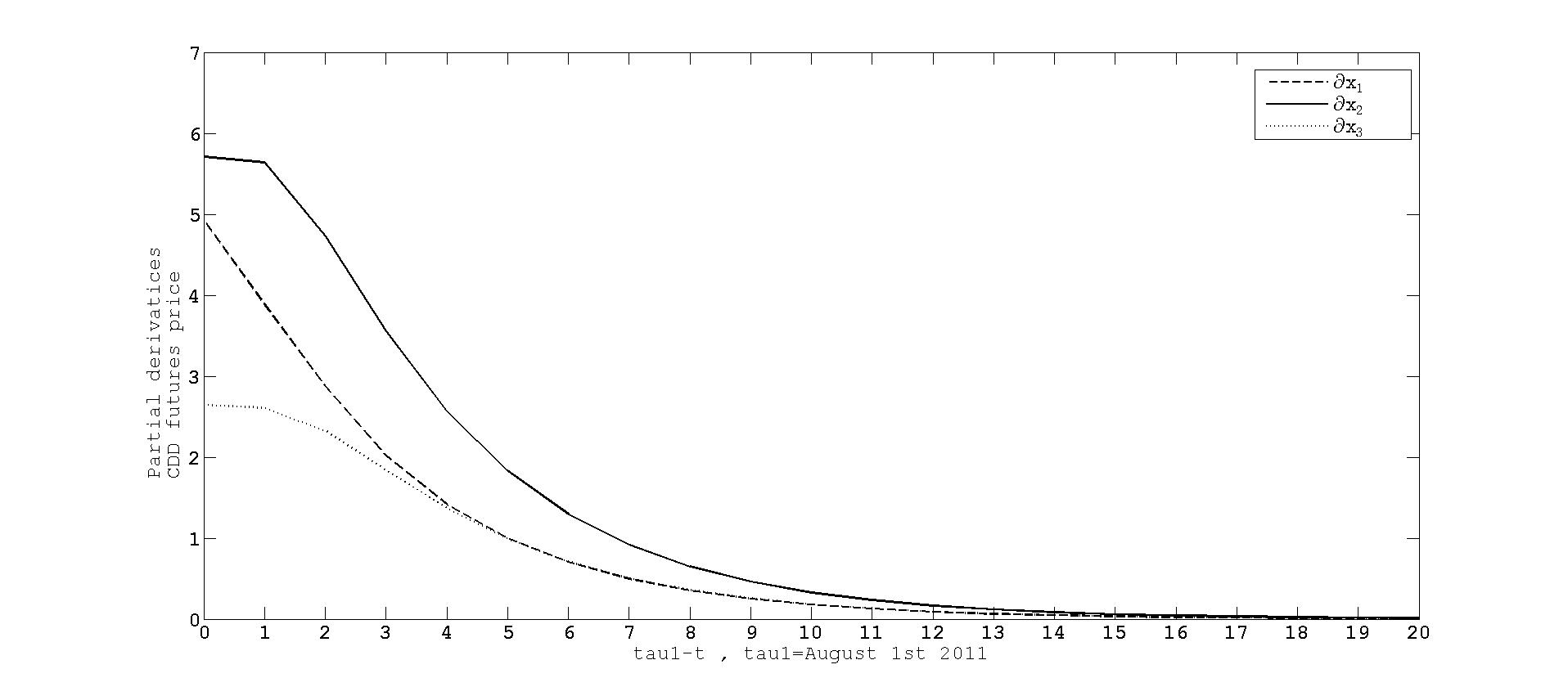

Figure. 4 shows the partial derivatives of the CDD futures price with respect the coordinates of derived in Proposition 3.1. The x-axis considers the time to maturity, , where the measurement day is August 1st, 2011. The y-axis shows the different partial derivatives.

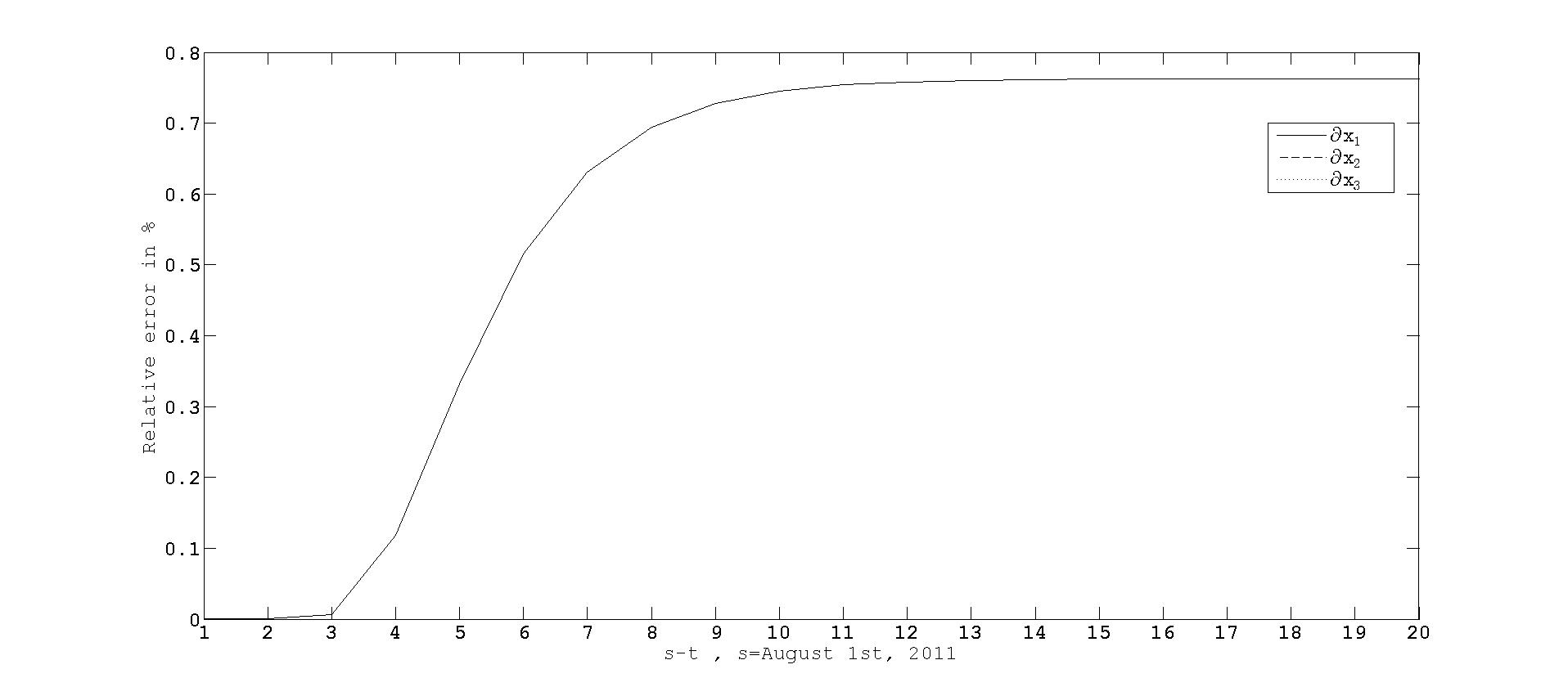

Observe that at first sight Figure. 3 and Figure. 4 seem to coincide. Indeed, Figure. 5 below shows that the relative error between them is less than 1 entirely.

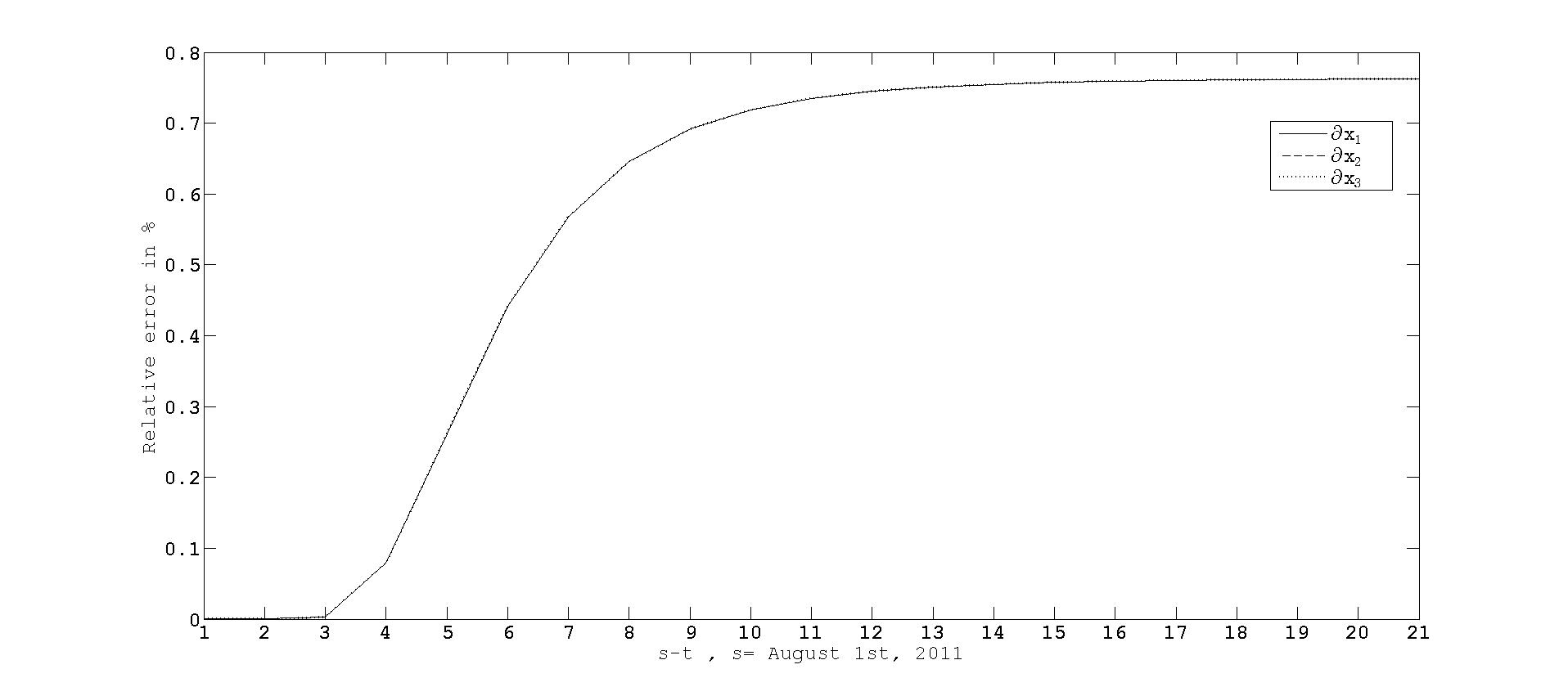

Consider also the case where is the th canonical basis vector in for . For the temperature at the present time and at the two consecutive prior times to , say and , is approximately one degree above the seasonal mean function. For , the temperature is close to the seasonal mean at present time and it is approximately one and two degrees below the seasonal mean at times and , respectively. Finally for the temperature is close to the seasonal mean at present time and one prior time, but two days prior to it is nearly one degree above its seasonal mean. The partial derivatives of the CDD futures price evaluated at the canonical basis vectors in also behave in a similar way to the partial derivatives on the approximate CDD futures price. Figure. 6 below shows that, for the case , the relative error between the partial derivatives of the approximate CDD futures price and the CDD futures price is also less than 1% entirely.

We proceed now with the analysis of call option prices written on CDD futures prices and call option prices written on the approximate CDD futures prices. To do so, we consider the results in Propositons 3.3 and 3.4. Observe that in both results there is dependency on . We focus on an at-the-money call option prices. In view of Figure. 7 we fix the strike price being .

For the study of the sensitivity of call option prices, we restrict our attention to the cases and . Next, we show the plots with the partial derivatives of the (approximate) call option prices with respect to the coordinates of derived in Proposition. 3.3 and Proposition. 3.4.

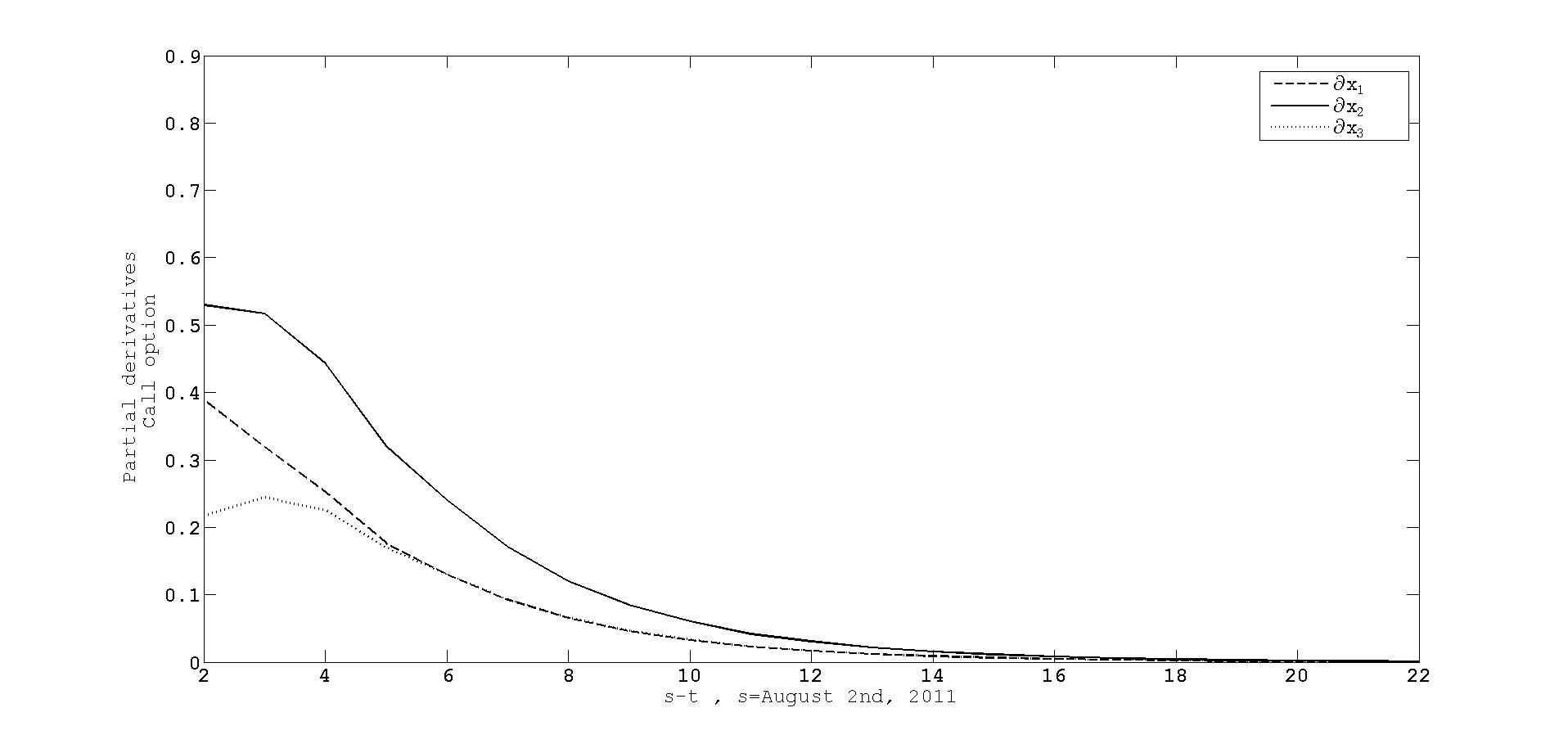

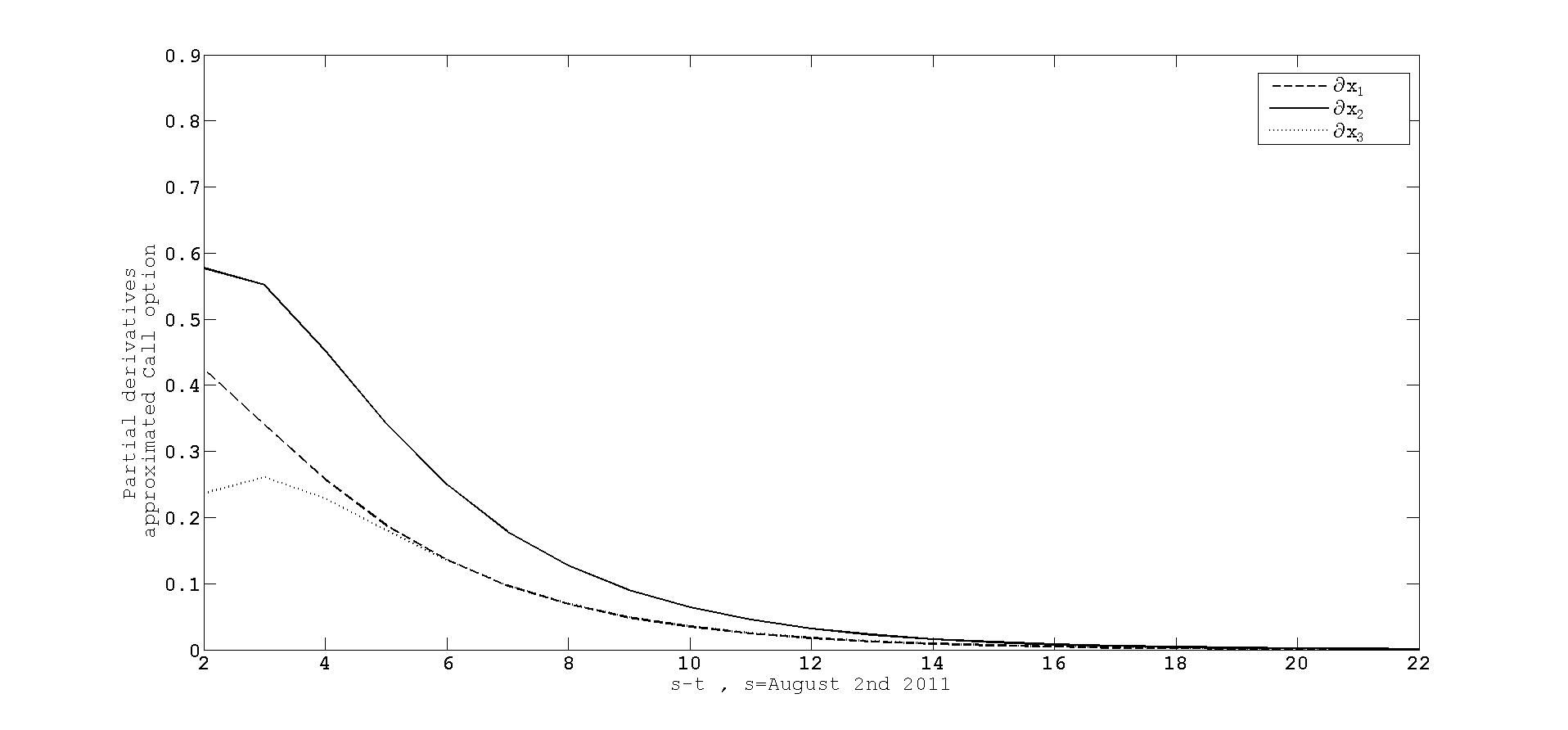

The x-axis considers the time to maturity, , where is August 2nd, 2011. We have fixed the exercise time being August 1st, 2011. The y-axis shows the different partial derivatives of the call option price when . Firstly, we observe that all the partial derivatives of the call option are positive. We see that for all times to maturity the call option price is more sensitive to any infinitesimal change in the component , followed by and . This tendency follows as time to maturity increases. At the long end, small variations in any component hardly affect the tendency of the call option prices.

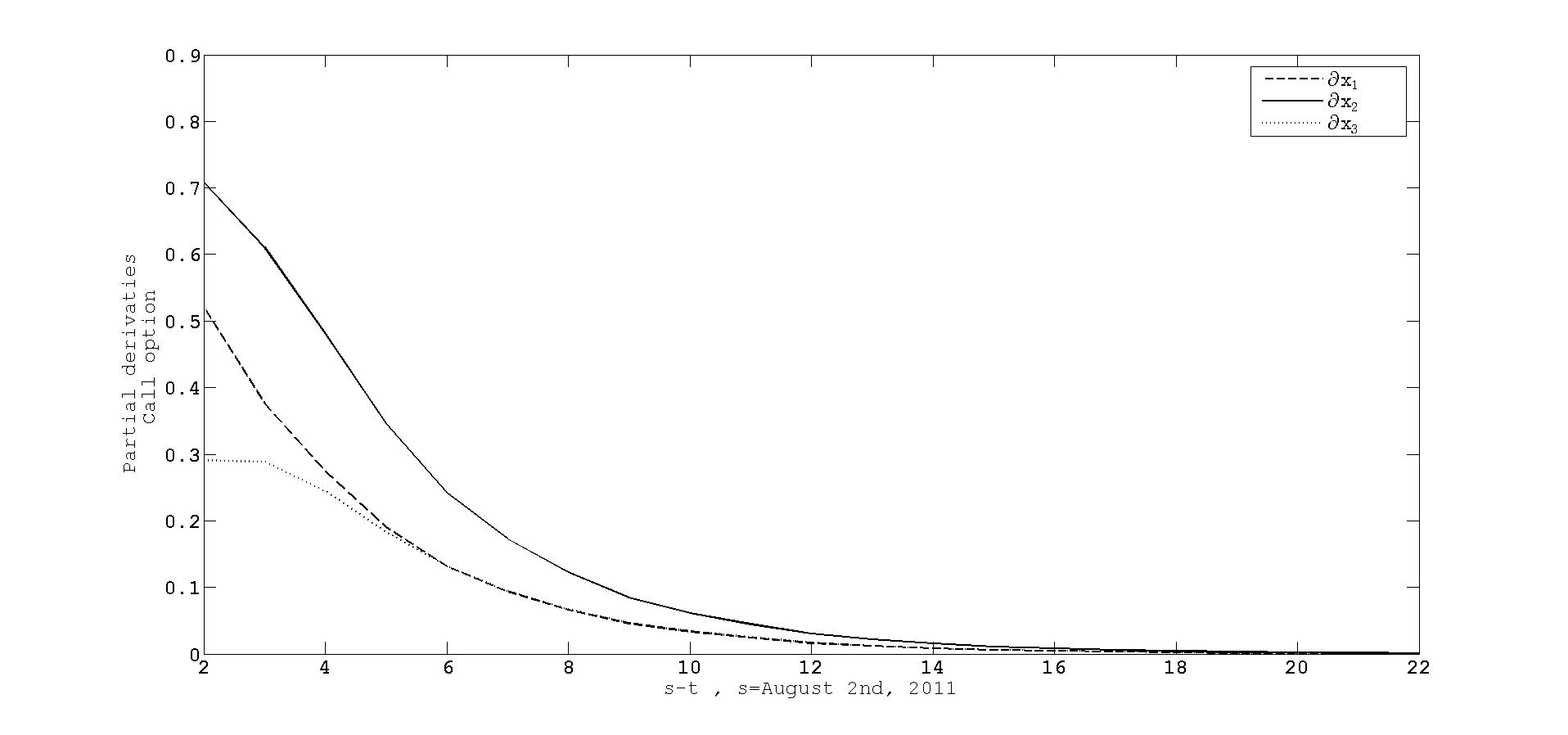

Figure. 9 shows the partial derivatives of the approximate call option prices with respect to the coordinates of derived in Proposition. 3.4 when . We observe that the partial derivatives in Figure. 8 and Figure. 9 show a close habavior. We also see that for small times to maturity the partial derivatives of the approximate call option price are bigger than the partial derivatives of the call option price.

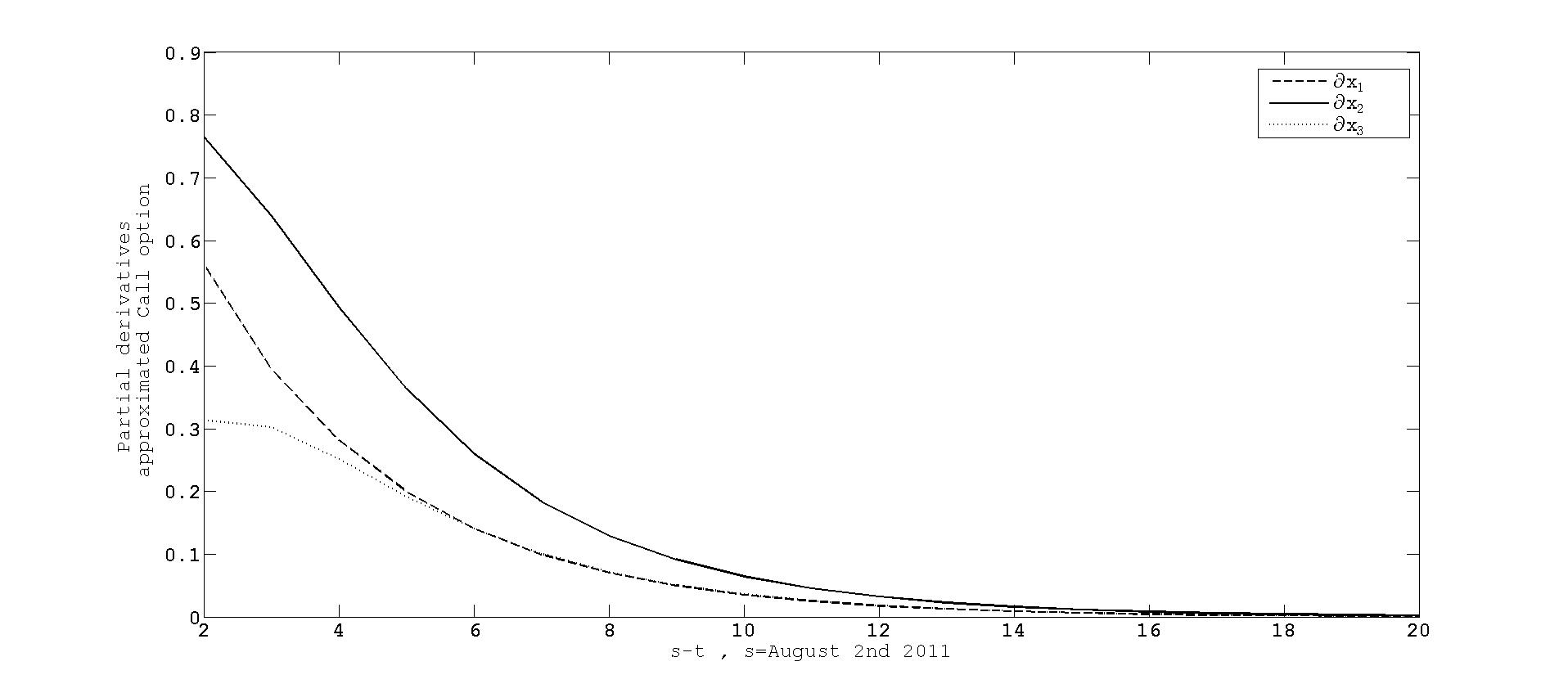

We end our analysis with the results for the case .

Figure. 10 and Figure.11 show the partial derivatives for the (approximate) call option prices, respectively. We see also here that both prices are more sensitive to changes in the second component of in all the domain. Furthermore, the sensitivity to this component decreases as time to maturity increases.

5 Sensitivity of CDD futures prices with measurement over a period

The sensitivity analysis of CDD future prices with measurement over a period with respect to infinitesimal changes in the components of can be performed by means of the partial derivatives provided in Proposition.2.1 and Proposition. 2.2. We proceed analogously as in the previous section for CDD futures prices with a measurement day.

The random variable with in (4.1) makes here also the difference between the results provided in both Propositions. The same reasoning followed for CDD future prices with a measurement day is valid to conclude that

| (5.1) |

Hence, the approximate CDD futures price becomes more sensitive to any infinitesimal change in the coordinates of than the CDD futures price.

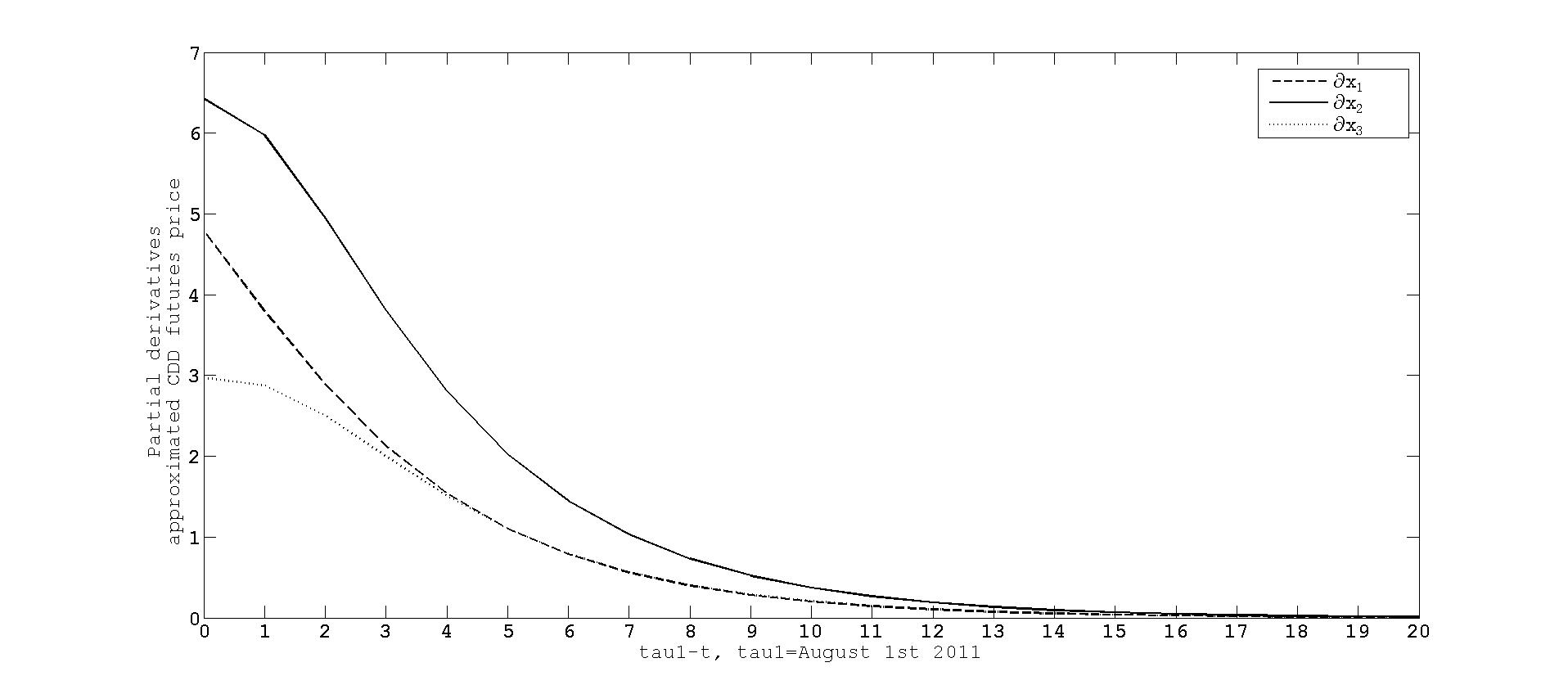

Figure.12 shows the partial derivatives of the approximate CDD futures price with respect the coordinates of derived in Proposition. 2.2.

The x-axis considers the time to maturity, , where is August 1st, 2011 and the measurement period is August 2011. The y-axis shows the different partial derivatives of the approximate CDD futures price. Firstly, we observe that the values here of the partial derivatives are greater than those corresponding to the partial derivatives of the approximate CDD futures price with a measurement day, with more emphasis on times which are close to . Indeed, the partial derivatives of the approximate CDD futures prices can be understood as the partial derivatives of the approximate CDD futures prices with measurement day which runs over as shown as follows

Recall that Figure. 3 shows that the derivatives of the approximate CDD futures price with a measurement day are positive and when time to maturity increases tend to zero. This fact together with the relation in (5.1) let us to justify why the derivatives of the approximate CDD futures prices with measurement over a period behave in this way. We also observe that any infinitesimal change in dominates more the behaviour of the approximate CDD futures price, followed by any change in and . This was exactly the same tendency followed by the partial derivatives of the approximate CDD futures price with a measurement day, see Figure. 3, for times to maturity greater than 2.

For the study of the sensitivity of the partial derivatives of the CDD futures price with measurement over a period derived in Proposition. 2.1 we consider the cases and .

6 Conclusions

In this paper we have studied the local sensitivity of the (approximate) CDD and HDD futures and options prices with respect to a perturbation in the deseasonalized temperature or in one of its derivatives up to a certain order, determined by the CAR process modelling the deseasonalized temperature. We have considered the partial derivatives of these financial contracts with respect to these variables (deseasonalized temperature and its derivatives). The HDD and CDD futures and call option prices and their approximate formulas were derived in Benth and Solanilla Blanco [2]. We have considered and empirical analysis where we have taken the same CAR(3)-process fitted to the time series of New York temperatures in Benth and Solanilla Blanco [2]. The sensitivity study of these financial contracts with a fixed measurement day shows first that the approximate futures prices are more sensitive to any perturbation in one of these variables than the theoretical futures prices. Nevertheless, the relative error between both partial derivatives is rather small. We also observe that one time prior to the considered measurement day the behaviour of the (approximate) futures prices is more affected by a perturbation in the deseasonalized temperature. As time to maturity increases then a perturbation in the slope of the deseasonalized temperature dominates the behaviour of both futures prices. At the long end any perturbation of these variables hardly affect their behaviour. For the call option prices we also observe that the approximate model is more sensitive to any pertubation in one of the previous variables than the theoretical model. We emphasize that unlike futures prices, any perturbation in the slope of the deseasonalized temperature, dominates the behaviour of the call option prices. We have also extended the analysis of sensitivity to futures prices with measurement over a fixed month. We have seen that in this case the slope of the deseasonalized temperature dominates the bahaviour in all the domain.

References

- [1] F. E. Benth and S. A Solanilla Blanco. Forward prices in markets driven by continuous-time autoregressive processes. In Recent Advances in Financial Engineering: Proceedings of the International Workshop on Finance 2012, pages 1–24, Singapore, 30–31 October 2012 2014. World Scientific.

- [2] F. E. Benth and S. A Solanilla Blanco. Approximation of the price dynamics of heating degree day and cooling degree day temperature futures. The Journal of Energy Markets., 8:69–92, 2015.

- [3] F. E. Benth and J Šaltytė Benth. Modeling and Pricing in Financial Markets for Weather Derivatives, volume 17 of Advanced series on statistical science & applied probability. World Scientific, Singapore, 2012.

- [4] M. Broadie and P Glasserman. Estimating security price derivatives using simulation. Management Science., 42:269–285, 1996.

- [5] G.B Folland. Real Analysis: Modern Techniques and Their Applications. Advanced series on statistical science & applied probability. Wiley, Chicheter, 1984.

- [6] W. Härdle and B López Cabrera. The implied market price of weather risk. Appl. Math. Finance., 19:59–95, 2012.