Also at ]Swarma Research, Beijing, 100085, China

Dynamical Reversibility and A New Theory of Causal Emergence

Abstract

The theory of causal emergence based on effective information suggests that complex systems may exhibit a phenomenon called causal emergence, where the macro-dynamics demonstrate a stronger causal effect than the micro-dynamics. However, a challenge in this theory is the dependence on the method used to coarse-grain the system. In this letter, we propose a novel notion of dynamical reversibility and build a coarse-graining method independent theory of causal emergence based on that. We not only found an approximately asymptotic logarithmic relation between dynamical reversibility and effective information for measuring causal effect, but also propose a new definition and quantification of causal emergence that captures the intrinsic properties of the Markov dynamics. Additionally, we also introduce a simpler method for coarse-graining large Markov chains based on the dynamical reversibility.

We live in a world surrounded by a multitude of complex systems. These systems function in a nonlinear fashion and are subject to time-irreversible stochastic dynamics[1, 2]. Consequently, the generation of entropy and the accumulation of disorder are inevitable. Nevertheless, there is a belief among people that underlying the disorder in complex systems are deeper patterns and regularities[3]. Hence, they strive to extract causal laws from these dynamic systems at a macro-level, while appropriately disregarding detailed information at the micro-level[4, 5, 6]. Ultimately, this pursuit aims to attain an effective theory or model capable of describing the causality of complex systems on a macro-level.

Recently, Hoel et al. have proposed a theoretical framework known as causal emergence to capture this idea[5, 6, 7]. This framework builds upon a novel information-theoretic measure called Effective Information (EI)[8], which quantifies the causal influence between states in different time steps within a Markov dynamical system. Through illustrative examples, they demonstrate that a coarse-grained Markov dynamics, when measured by EI at the macro-level, can exhibit stronger causal power than at the micro-level. Nevertheless, this theory is still in its developmental stage. One of the foremost challenges is that the manifestation of causal emergence relies on the specific manner in which we coarse-grain the system. Different coarse-graining methods may yield entirely disparate outcomes for causal emergence. While this issue can be mitigated by maximizing EI[5, 9, 10] or employing other indicators of causal emergence that are independent of coarse-graining[11], the computational complexity and the question of solution uniqueness remain open challenges[10, 7]. Is it possible to construct a more robust theory of causal emergence that is independent of the chosen coarse-graining method?

This letter endeavors to construct a theory based on an intriguing and slightly different concept: the reversibility of dynamics. In fact, there is deep connection between causality and the reversibility[12, 13, 14, 15, 16, 17, 13]. When we say that event A causes event B, we mean that not only does B occur when A occurs, but also when A does not occur, B must not occur (contractual). The former condition is necessary, while the latter is sufficient [18]. This implies that we can not only infer B from A, but also infer the occurrence of A based on the occurrence of B. Consequently, the underlying dynamical process that determines how A causally affects B is reversible [12]. This point is further supported by examples found in references[5, 6], where EI, as a measure of causality, is maximized when the underlying Markov dynamics are approximately reversible. Therefore, we can re-frame the theory of causal emergence as an endeavor to obtain a reversible macro-level dynamics by appropriately disregarding micro-level information.

This letter begins by introducing an indicator to quantify the reversibility of dynamics, which is based on the singular values of the transitional probability matrix (TPM) for Markov chains defined on discrete time and state space. Subsequently, a multitude of numerical simulations are conducted, and formal mathematical theorems are presented to establish the equivalence between EI and dynamical reversibility. Furthermore, a concise and coarse-graining method independent definition for causal emergence is introduced. Lastly, a simpler and more powerful coarse-graining method for general Markov chains, based on the singular value decomposition (SVD) of the TPM, is proposed.

First, we will briefly introduce Hoel et al’s theory of causal emergence. This theory is based on an important information theoretic measure called effective information(EI) [5]. For a given Markov chain with a discrete state space and TPM , is defined as:

| (1) |

where represent the state variables defined on at time step and , respectively. The do-operator, denoted as , represents Pearl’s intervention [19] that enforces to follow a uniform (maximum entropy) distribution on . Since , the do-operator indirectly intervenes on as well. Thus, the measures the mutual information between and after this intervention, quantifying the strength of the causal influence exerted by on .

An important aspect of this definition is that solely reflects the properties of the underlying probability distribution and remains independent of the distribution of [7]. This point can be more clear by showing another equivalent form of :

| (2) |

where is the row vector of , is the KL-divergence between two probability distributions, and is the average vector of all the row vectors of the TPM. Thus, measures the average KL-divergence between any and their average .

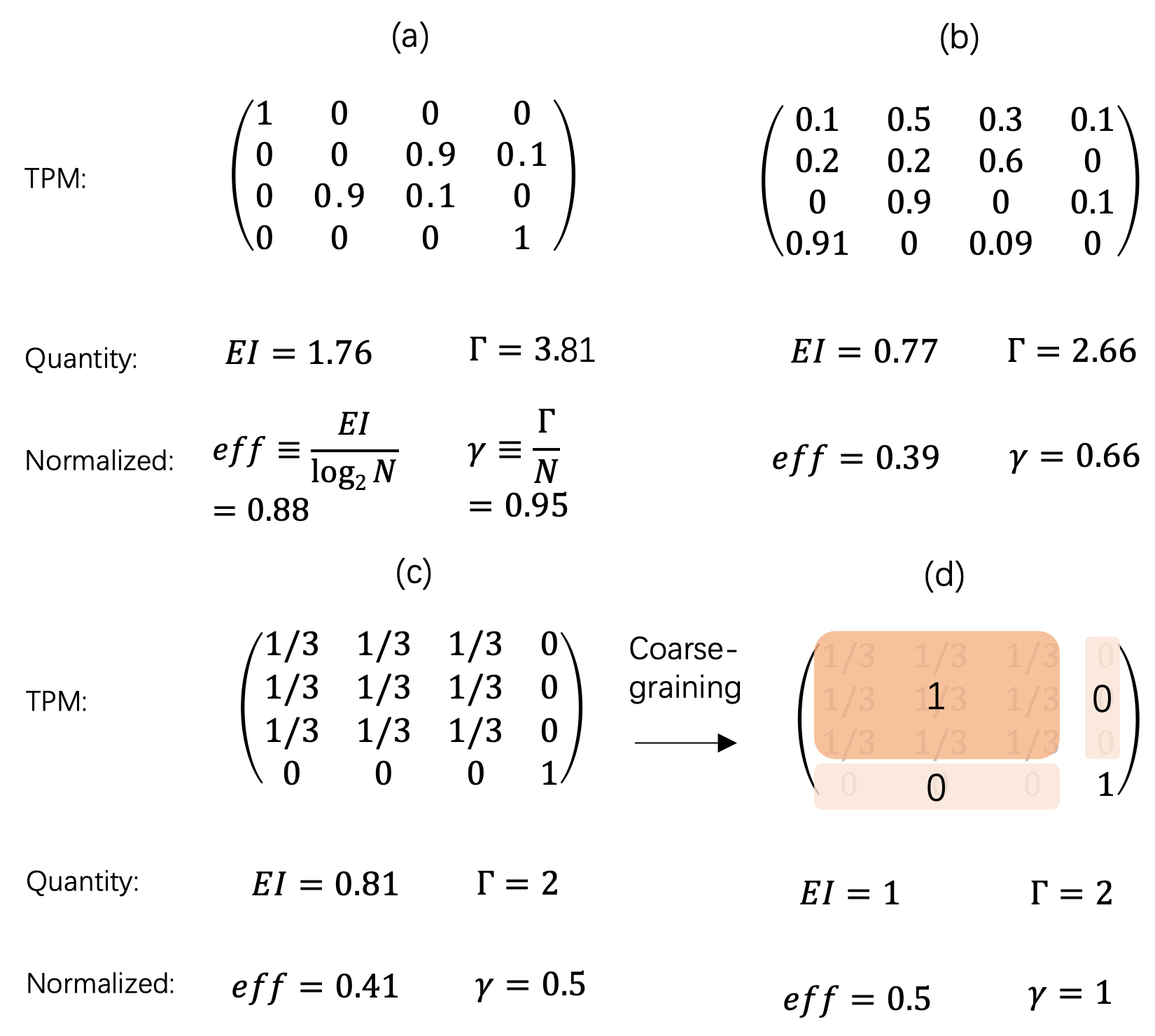

As the four cases of TPMs shown in Figure 1, the values and their normalized forms are also demonstrated below. As the TPM is closed to a permutation matrix, is larger. Actually, can reach its maximum when is reversible (that is is a permutation matrix according to Theorem 2 and 3 presented in Appendix E.1. In this case, , and ). The example in Figure 1(d) is the coarse-grained TPM of example in Figure 1(c) by collapsing the first three rows and columns into one macro-state. (or ) in (d) is clearly larger than (or ) in (c), which manifests that the strength of cause-effect in macro-level (coarse-grained TPM in (d)) is larger than the micro-level (c), thus, causal emergence occurs.

Second, we will introduce a quantitative indicator to measure the reversibility of dynamics for a Markov chain.

Firstly, it is important to clarify that in this context, a dynamically reversible Markov chain refers to a chain where its is reversible, and its inverse also serves as an effective TPM [16]. This definition differs from the commonly used term “time reversible” Markov chain [20], as dynamical reversibility necessitates the ability of to be reversibly applied to each individual state, whereas the latter focuses on the reversibility of state space distributions. Actually, we can prove that the former implies the latter (Theorem 4 in Appendix E).

However, in the case of a general TPM, it is not inherently reversible. Hence, an indicator that can quantify the degree to which a TPM deviates from being reversible is required.

Definition 1.

Suppose the transitional probability matrix (TPM) is for a markov chain , and its singular values are , then the measure of dynamical reversibility is:

| (3) |

In literateurs [21, 22, 23], is called nuclear norm or -Schatten norm with , and it is always treated as the continuous relaxation of the rank of matrix .

The reason why can quantify the reversibility of is clear if we make an SVD decomposition on :

| (4) |

where, and are two orthogonal and normalized matrices with dimension , and is a diagonal matrix which contains all the ordered singular values. To be noticed that and are all reversible operators(matrices), therefore, the reversibility of is solely determined by . If there are zero singular values in , then in irreversible. If all the singular values are much larger than zero, is more reversible.

We actually can prove strictly that 1) achieves its maximal value when is reversible (Theorem 5 and Theorem 3, see Appendix E.2); and 2)If is closed to be reversible (a permutation matrix), then also approaches its maximal value in the same time (Theorem 7, see Appendix E.2).

In the four examples of Figure 1, varies from 2 to 3.81, and it is dependent on the system size . To compare the reversibility measures across different sizes, we normalize by dividing to obtain , it varies from 0.5(case c) to 1(case d) in Figure 1. It is clear that is larger if the TPM is closed to a permutation matrix(reversible matrix).

Next, we will compare and on similarities and differences.

First, and can reach their maximal values and , respectively, when is reversible (permutation matrix) according to Theorem 2 and Theorem 5 (See Appendix E.2). They also achieve their minimal values ( and ) according to Theorem 1 and Theorem 6, see Appendix E.1) when . However, we can prove that is not the unique minimum solution of , any TPM with for any can make . Therefore, is not a convex function but is (see Theorem 6 and Corollary 1, Appendix E.2), as a result, the latter is more suitable for optimization.

Secondly, both and are correlated with the auto-correlation matrix . As expressed in Equation 1, actually is the “de-similarity” between each and their average , measured by KL-divergence. While, any entry in is the similarity between and but measured by inner product. On the other side, all squared singular values of are the eigenvalues of , and is the trace of and it also decreases when all s are similar(see Theorem 5 in Appendix E.1).

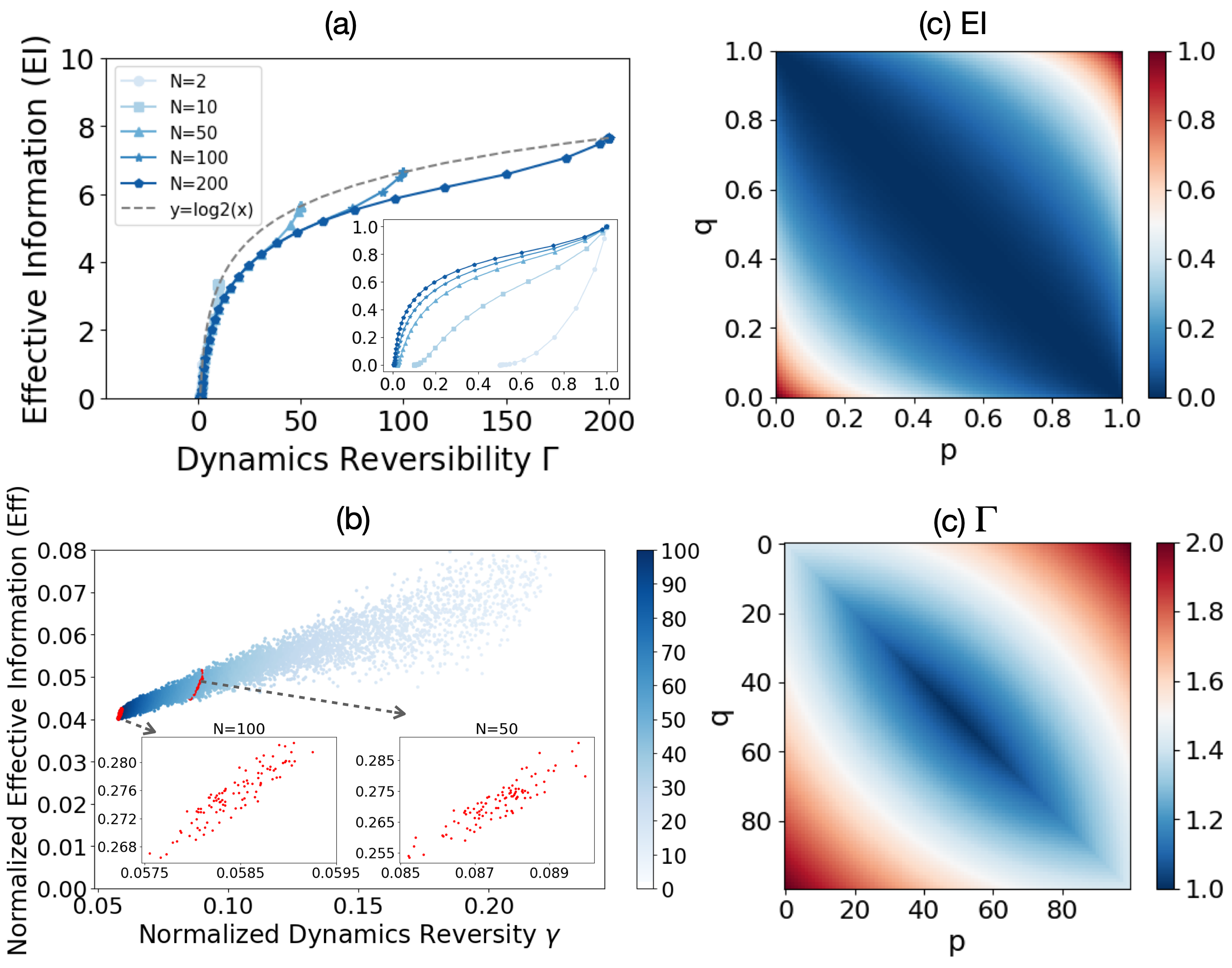

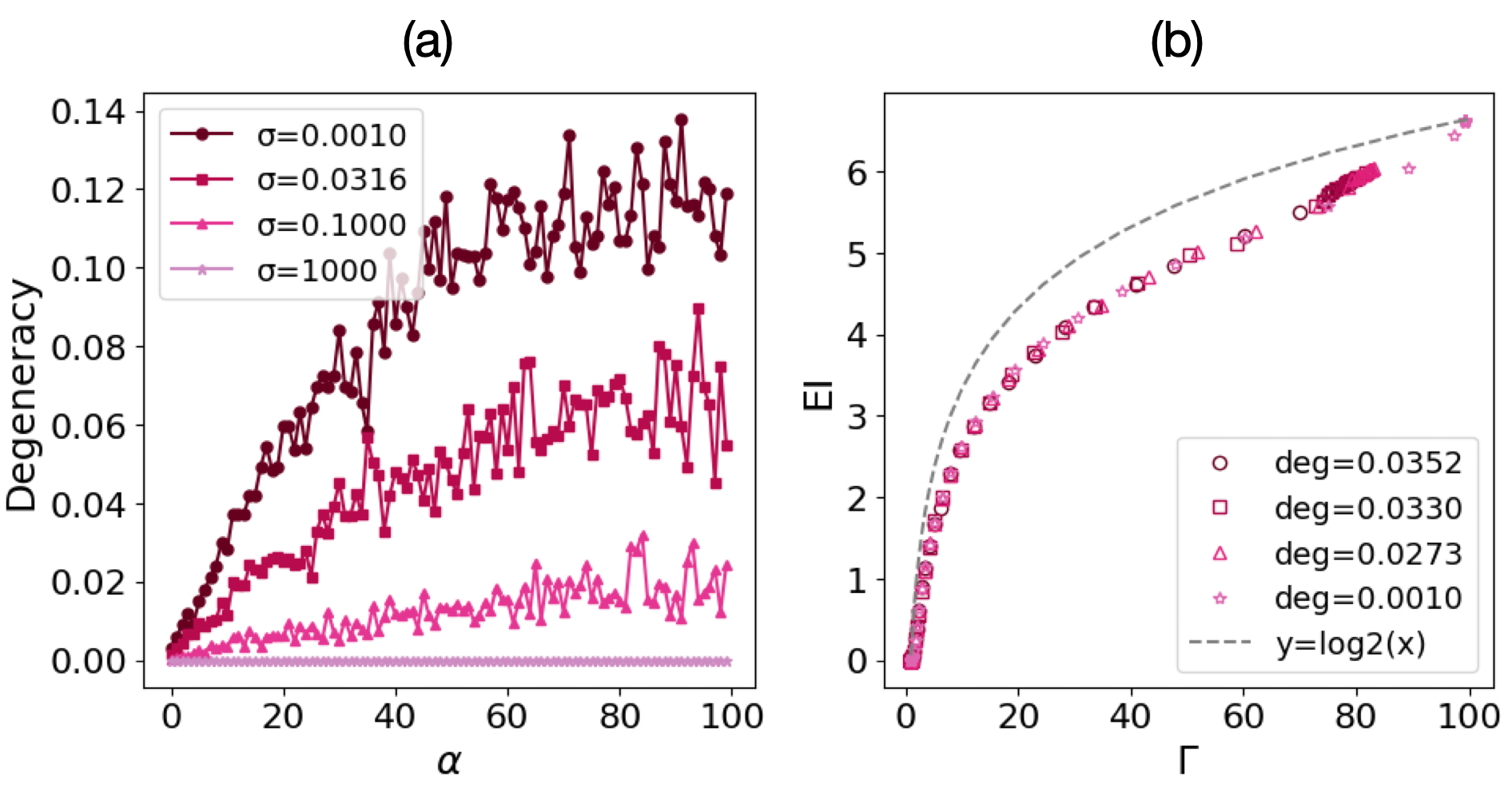

We further compare and on a variety of TPMs generated by a random perturbation on a randomly selected permutation matrix with size or composed by random normalized row vectors (the details are in Appendix A). As shown in Figure 2(a) and (b), a positive correlation is observed on all these examples, and an approximately asymptotic relationship is conjectured for large :

| (5) |

This relation is obviously observed in Figure 2(a), but degenerates to a nearly linear relation in Figure 2(b) since limited value region of is covered. However, the logarithm relation of Equation 5 can also be observed in another set experiments by controlling the degeneracy of the TPM (see Appendix A.3).

We also obtain the analytic solution for and on the simplest parameterized TPM with size (see Appendix B), and we show the landscape how and are dependent on the parameters and . It is clear that both and obtain their maximum values on the anti-diagonal regions ( or , in this case, is a permutation matrix). The differences between Figure 2(c) and (d) are apparent: 1) has a peak value when but has not; 2) a broader region with is observed, while the region with is much smaller; 3)an asymptotic transition from 0 to maximal is observed for , but not for .

Therefore, we conclude and are highly correlated on various TPMs. This implies we may use to replace to build a new theory of causal emergence.

We have witness the power of singular values to characterize the property of the Markov dynamics in previous sections, therefore, we will build such a theory based on singular values. First, we will give two definitions for causal emergence.

Definition 2.

For a given markov chain with TPM , if then clear causal emergence occurs in this system. And the degree of causal emergence is

| (6) |

This definition is independent of any coarse-graining method or external parameters. As a result, it represents an intrinsic and objective property of Markov dynamics.

Definition 3.

For a given markov chain with TPM , suppose its singular values are . For a given small real value , if there is an integer , such that , then there is vague causal emergence with the level of vagueness occured in the system. And the degree of causal emergence is:

| (7) |

This definition applies when there is no distinct cutoff in the singular value spectrum, necessitating the manual selection of a threshold .

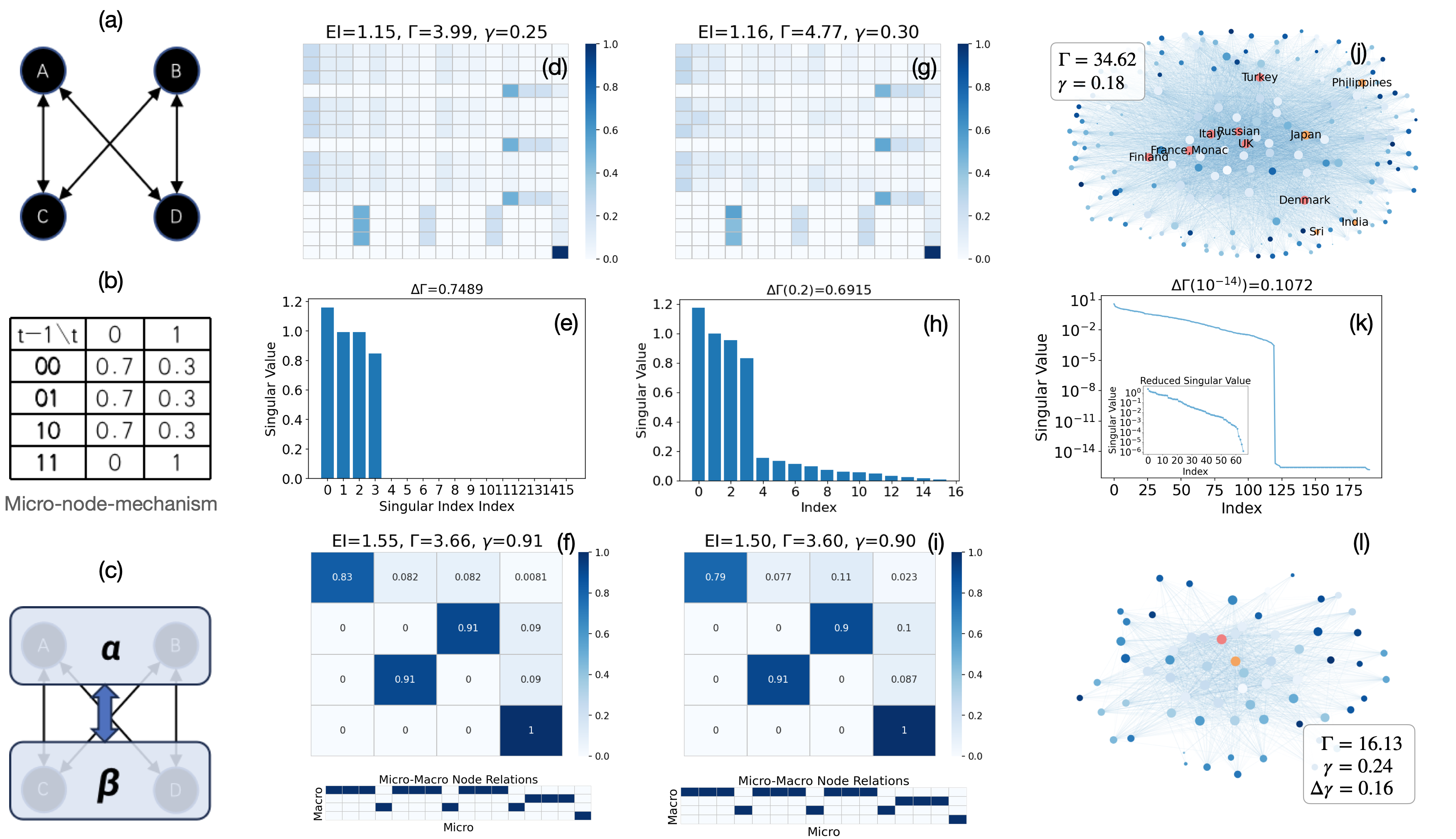

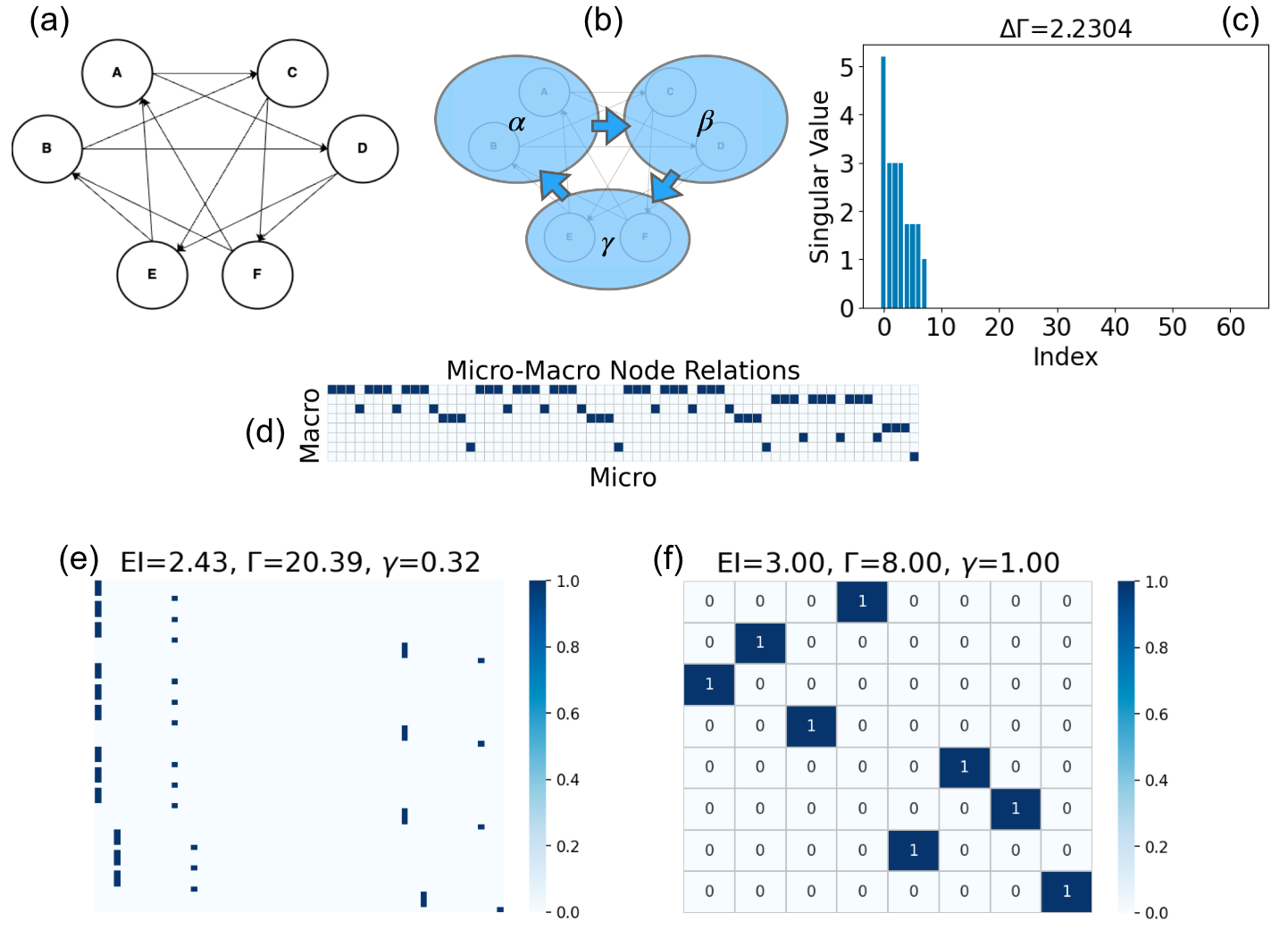

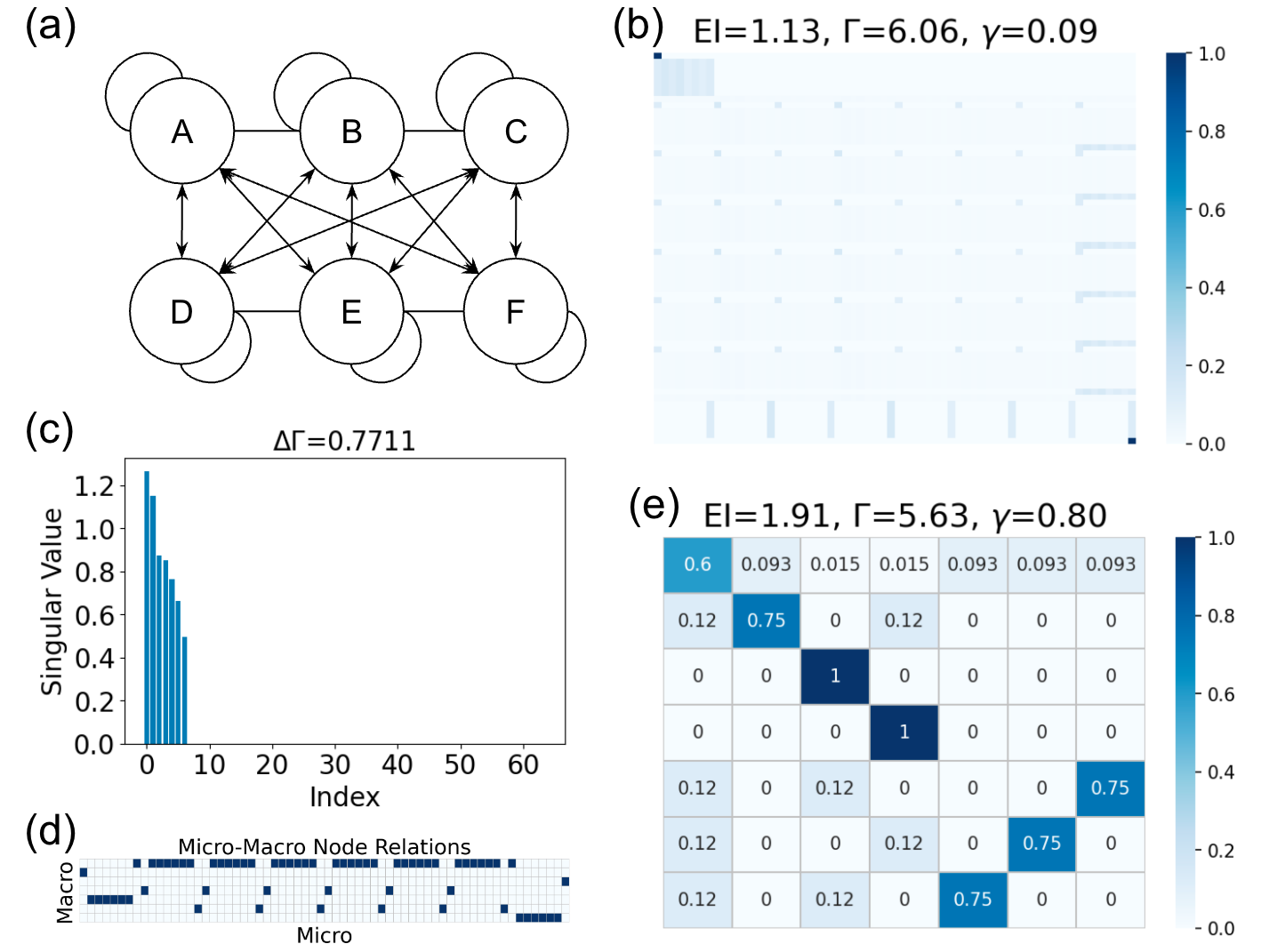

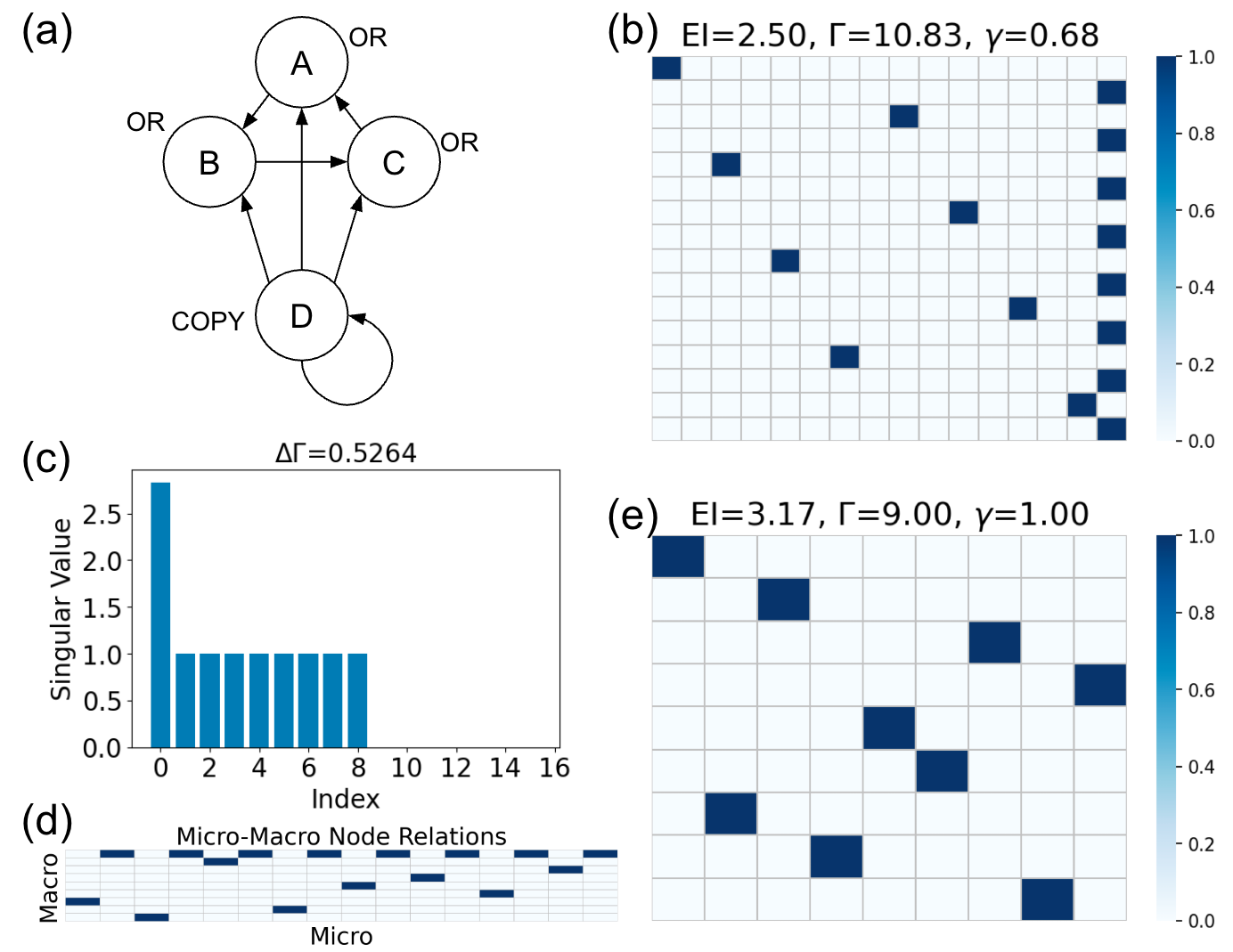

Two examples of TPMs for clear emergence and vague emergence are shown in Figure 3(a-i), respectively. The TPM in Figure 3(d) is derived from the boolean network and its node-mechanism in Figure 3(a) and (b) directly. Their singular value spectra are shown in Figure 3(e). There are only 4 non-zero singular values (Figure 3(e)) for the first example in (d), therefore, clear causal emergence occurs, and the degree of causal emergence is .

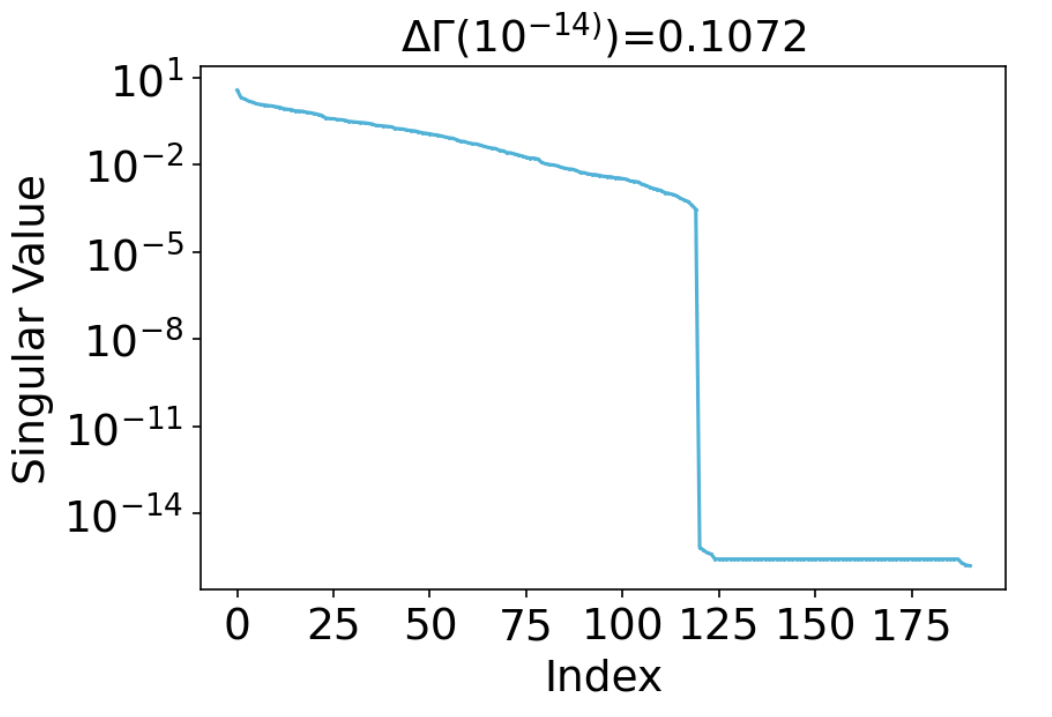

Vague causal emergence can be shown on the TPM in Figure 3(g), which is derived from (d) by adding random Gaussian noise with strength () on the TPM in (d). As a result, the singular spectrum is obtained as shown in Figure 3(h). We select as the threshold such that only 4 large singular values are left. The degree of causal emergence is .

Therefore, the occurrences of both clear and vague causal emergence, as well as the extent of such emergence, can be objectively quantified without dependence on any specific coarse-graining method.

Finally, our theory can also provide a concise coarse-graining method based on the singular value decomposition of to obtain a macro-level reduced TPM. The basic idea is to project the row vectors in onto the sub-spaces spanned by the eigenvectors of such that the major information of is conserved, as well as is kept unchanged. The coarse-graining method contains five steps: 1). SVD decomposition for the TPM according to Equation 4; 2) selecting an as the threshold to cut off the singular value spectrum, and to obtain as the number of retained states; 3)dimensionality reduction for all in by calculating , where only the first eigenvectors are retained; 4)clustering all row vectos in into groups to obtain a projection matrix ; and 5) obtain a new TPM by using and such that the total stationary flux is kept unchanged. If there is clear cut off of the singular value spectrum of the reduced network, then repeat the steps from 1) to 5). The detailed information about this method and why it does work can be referred in Appendix C.

We test our method on the two examples shown in Figure 3(d) and (g), and the coarse TPMs are shown in (f) and (i). The macro-level boolean network model(3 (c)) can be read out from the TPMs and the projection matrix . To be noticed, s in the coarse TPMs are almost identical to the original ones, which means our method is conservative. We further test the examples of causal emergence in the references [5, 6], and almost identical coarse TPMs can be obtained.

Finally, to illustrate one of the potential applications, we employ our method on the world trade network in 2000(Figure 3(j)) to obtain a coarse-grained network, as depicted in Figure 3(l). In which, fewer than half the original nodes and only about one-seventh of the edges are retained, while the measure is halved. Interestingly, the degree of causal emergence, as assessed by the normalized measure , actually rises. Consequently, a smaller and more tightly connected core network is identified, which facilitates the major trade flows.

In summary, we have discovered that the nuclear norm, which is the sum of all singular values of a TPM, can be utilized to quantify the reversibility of the Markov dynamics. Both theoretical findings and empirical experiments provide support for the existence of positive correlation, where the is approximately and asymptotically proportional to the logarithm of the measure . Building upon this measure, we have developed a new theory of causal emergence that provides a clearer definition, reflecting the intrinsic properties of the system and independent of any specific coarse-graining method. Additionally, through the SVD decomposition of a TPM, we have identified a more concise approach to coarse-grain the system.

Further, this work establishes a potential link between thermodynamics and causal emergence. The emergence of causation corresponds to the emergence of dynamical reversibility, which in turn implies a reduction in entropy. Therefore, the interest in emergent behaviors can be explained by the desire to achieve macro-dynamics with a lower rate of entropy production. However, this is contingent upon the entropy production during the process of coarse-graining. Hence, the balance between the rates of entropy productions in macro-dynamics and coarse-graining deserves further attention.

Nevertheless, there are limitations in this work. Firstly, all the aforementioned discussions have been centered around the state space, whereas an extension to the variable space would be more practical. However, it should be noted that the size of the state space grows exponentially with the number of variables, which poses a challenge. Secondly, while is a convex function that aids in optimization, it cannot be decomposed into determinism and degeneracy like [5], thereby reducing its interpretability. As a result, further research is warranted to address these issues.

Acknowledgements.

We wish to acknowledge all the members who participated in the ”Causal Emergence Reading Group” organized by the Swarma Research and the ”Swarma - Kaifeng” Workshop.References

- Prigogine and Stengers [1997] I. Prigogine and I. Stengers, The end of certainty (Simon and Schuster, 1997).

- Waldrop [1993] M. M. Waldrop, Complexity: The emerging science at the edge of order and chaos (Simon and Schuster, 1993).

- West [2018] G. West, Scale: The universal laws of life, growth, and death in organisms, cities, and companies (Penguin, 2018).

- Landau and Lifshitz [1980] L. D. Landau and E. M. Lifshitz, Statistical Physics, Vol. 5 (Elsevier, 1980).

- Hoel et al. [2013] E. P. Hoel, L. Albantakis, and G. Tononi, Quantifying causal emergence shows that macro can beat micro, Proceedings of the National Academy of Sciences of the United States of America 110, 19790 (2013).

- Hoel [2017] E. P. Hoel, When the map is better than the territory, Entropy 19, 10.3390/e19050188 (2017).

- Yuan et al. [2024] B. Yuan, J. Zhang, A. Lyu, J. Wu, Z. Wang, M. Yang, K. Liu, M. Mou, and P. Cui, Emergence and causality in complex systems: A survey of causal emergence and related quantitative studies, Entropy 26, 108 (2024).

- Tononi and Sporns [2003] G. Tononi and O. Sporns, Measuring information integration, BMC neuroscience 4, 1 (2003).

- Zhang and Liu [2023] J. Zhang and K. Liu, Neural Information Squeezer for Causal Emergence, Entropy 25, 1 (2023), 2201.10154 .

- Mingzhe et al. [2023] Y. Mingzhe, W. Zhipeng, L. Kaiwei, R. Yingqi, Y. Bing, and Z. Jiang, Finding emergence in data by maximizing effective information (2023).

- Rosas et al. [2020] F. E. Rosas, P. A. Mediano, H. J. Jensen, A. K. Seth, A. B. Barrett, R. L. Carhart-Harris, and D. Bor, Reconciling emergences: An information-theoretic approach to identify causal emergence in multivariate data, PLoS computational biology 16, e1008289 (2020).

- Faye [1997] J. Faye, Causation, reversibility and the direction of time, in Perspectives on time (Springer, 1997) pp. 237–266.

- Bernardo et al. [2023] M. Bernardo, I. Lanese, A. Marin, C. A. Mezzina, S. Rossi, and C. Sacerdoti Coen, Causal reversibility implies time reversibility, in International Conference on Quantitative Evaluation of Systems (Springer, 2023) pp. 270–287.

- Bernardo and Mezzina [2022] M. Bernardo and C. A. Mezzina, Bridging causal consistent and time reversibility: A stochastic process algebraic approach, arXiv preprint arXiv:2205.01420 (2022).

- Farr [2020] M. Farr, Causation and time reversal, The British Journal for the Philosophy of Science (2020).

- Bernardo and Mezzina [2023] M. Bernardo and C. A. Mezzina, Bridging causal reversibility and time reversibility: A stochastic process algebraic approach, Logical Methods in Computer Science 19 (2023).

- Kathpalia and Nagaraj [2021] A. Kathpalia and N. Nagaraj, Time-reversibility, causality and compression-complexity, Entropy 23, 327 (2021).

- Comolatti and Hoel [2022] R. Comolatti and E. Hoel, Causal emergence is widespread across measures of causation, arXiv preprint arXiv:2202.01854 (2022).

- Pearl and Mackenzie [2018] J. Pearl and D. Mackenzie, The book of why: the new science of cause and effect (Basic books, 2018).

- Stroock [2013] D. W. Stroock, An introduction to Markov processes, Vol. 230 (Springer Science & Business Media, 2013).

- Recht et al. [2010] B. Recht, M. Fazel, and P. A. Parrilo, Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization, SIAM review 52, 471 (2010).

- Chi et al. [2019] Y. Chi, Y. M. Lu, and Y. Chen, Nonconvex optimization meets low-rank matrix factorization: An overview, IEEE Transactions on Signal Processing 67, 5239 (2019).

- Cui et al. [2020] S. Cui, S. Wang, J. Zhuo, L. Li, Q. Huang, and Q. Tian, Towards discriminability and diversity: Batch nuclear-norm maximization under label insufficient situations, in Proceedings of the IEEE/CVF conference on computer vision and pattern recognition (2020) pp. 3941–3950.

- Ding and He [2004] C. Ding and X. He, K-means clustering via principal component analysis, in Proceedings of the twenty-first international conference on Machine learning (2004) p. 29.

- Marin and Rossi [2014] A. Marin and S. Rossi, On the relations between lumpability and reversibility, in 2014 IEEE 22nd International Symposium on Modelling, Analysis & Simulation of Computer and Telecommunication Systems (IEEE, 2014) pp. 427–432.

- Barreto and Fragoso [2011] A. M. Barreto and M. D. Fragoso, Lumping the states of a finite markov chain through stochastic factorization, IFAC Proceedings Volumes 44, 4206 (2011).

- Klein and Hoel [2020] B. Klein and E. Hoel, The emergence of informative higher scales in complex networks, Complexity 2020, 1 (2020).

- Seabrook and Wiskott [2023] E. Seabrook and L. Wiskott, A tutorial on the spectral theory of markov chains, Neural Computation 35, 1713 (2023).

- [29] https://en.wikipedia.org/wiki/matrix_norm.

- Hoheisel and Paquette [2023] T. Hoheisel and E. Paquette, Uniqueness in nuclear norm minimization: Flatness of the nuclear norm sphere and simultaneous polarization, Journal of Optimization Theory and Applications 197, 252 (2023).

Appendix A Experiments on testing the correlation between and

In this section of the appendix, we will introduce the details of our experiments on the relationship between dynamical reversibility and on various generated TPMs. The generative model of TPMs have three classes: perturbation on permutation matrix, random normalized, and perturbation on controlled degenerative TPMs.

A.1 Perturbation on Permutation Matrix

In this series experiments, we will find out what the relationships between and are on a variety of TPMs with different deviations from the reversible TPMs (permutation matrix) and different sizes.

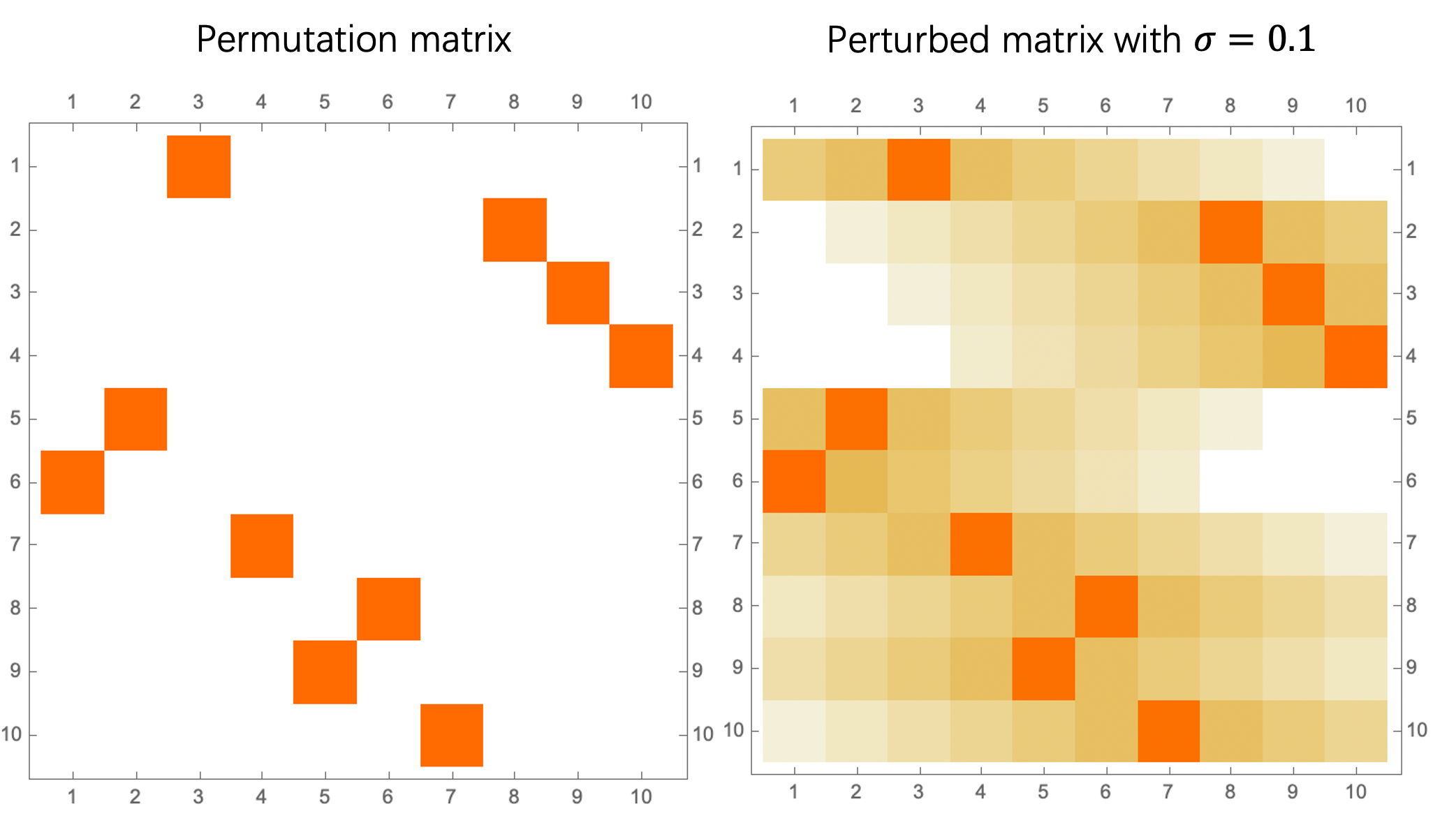

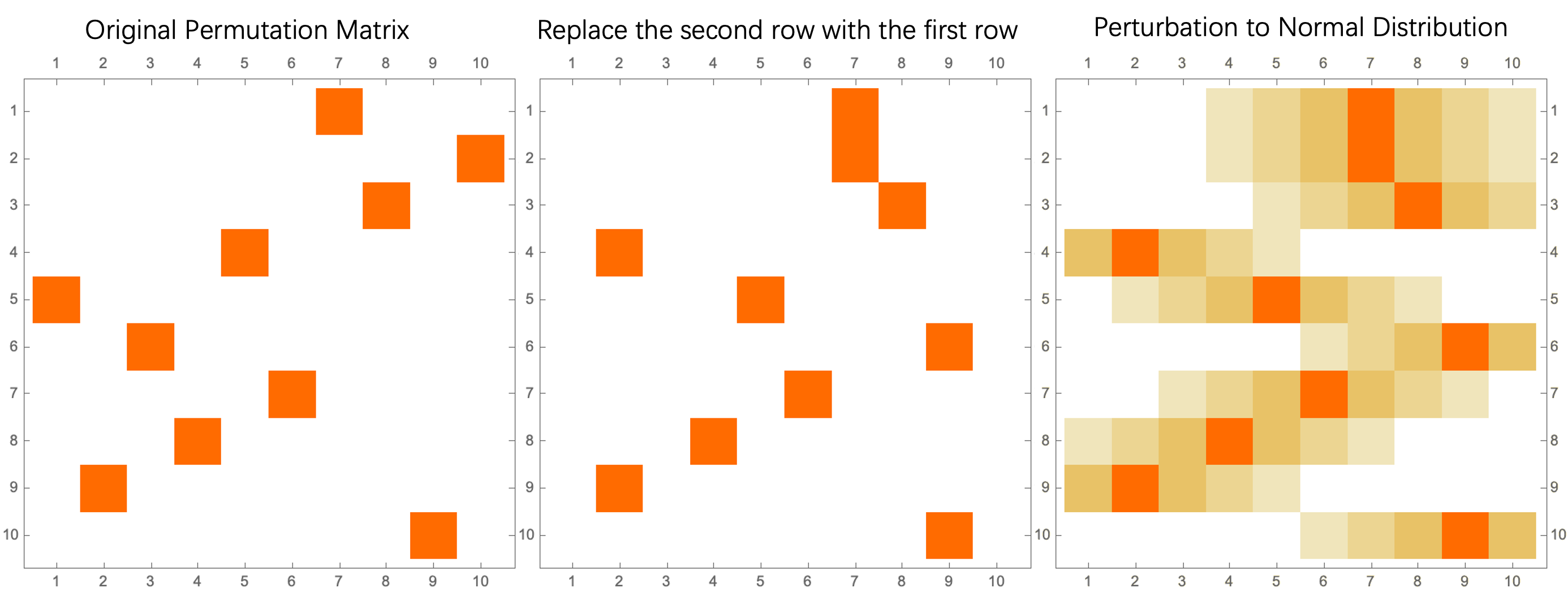

For given size , The TPM is generated by three steps: 1). Randomly sample a permutation matrix with dimension ; 2). For each row vector in , and suppose the position of the sole 1 element is , fill out all entries of with the probabilities of a Gaussion distribution center at , that is, , where, is the position where the sole 1 element locates in , and is a free parameter; 3). Normalize this new row vector by dividing , such that the modified matrix is also a TPM.

In this model, the unique parameter can control the degree of deviations from the original TPM. When , we recover the original TPM. And when increases to very large value, then the row vectors converge to the vector . Figure S1 shows the TPMs before and after the update on , where the colors represent the probabilities.

A.2 Random Normalization

In this model, only two step can generate a TPM: 1). Sample a row random vector, 2) normalize this row vector such that the generated matrix is a TPM.

A.3 Perturbation on Controlled Degeneracy

The third model is very similar to the first one, however, the original matrix is not a permutation matrix, but a degenerated permutation matrix. Here, a TPM is degenerative means that there are some row vectors are identical, and the number of identical row vectors is denoted as which is the controlled variable. By tuning , we can control the degeneracy [5] of the as Figure S2 shows.

The experimental results are as follows. First, we will justify if degeneracy of the TPM can be controlled by . We work with a matrix, progressively adjusting from 0 to 99, corresponding to the process of increasing degeneracy. We also introducing disturbance noise as another control parameter, here we test from to . Figure. S3(a) shows the degeneracy of different disturbance change as . Figure S3(b) shows EI versus for different degeneracy.

Appendix B Analytic solutions on the parameterized 2*2 TPM

We compare and on a simplest example, the TPM is as:

| (1) |

where and are all free parameters in the range of . With this TPM, we can explicitly write down the expression for :

| (2) | ||||

Appendix C The coarse graining method based on SVD decomposition

We will first give the detailed introduction of the coarse-graining method based on SVD, and then we give an explanation why this simple method can work in practice.

C.1 The method

Intuitively, the basic idea of our method is to treat all row vectors in as data vectors with dimensionality of , then we first take dimensionality reduction for these row vectors, second to cluster them into clusters where is selected according to the threshold for singular value spectrum. With the clusters, we can reduce the original TPM according to the principle that all the stationary flows are conservative.

Concretely, the coarse-graining method contains five steps:

1) We first make SVD decomposition for (suppose is irreducible and recurrent such that stationary distribution exist):

| (4) |

where, and are two orthogonal and normalized matrices with dimension , and is a diagonal matrix which contains all the ordered singular values.

2) Selecting a threshold and the corresponding if there is a clear cut off on the singular value spectrum;

3) Reducing the dimensionality of row vectors in from to by calculating the following Equation:

| (5) |

where .

4) Clustering all row vectors in into groups by K-means algorithm to obtain a projection matrix , which is defined as:

| (6) |

for .

5) Obtain the reduced TPM according to and .

To illustrate how we can obtain the reduced TPM, we will first define a matrix called stationary flow matrix as follows:

| (7) |

where is the stationary distribution of which satisfies . In the example of trade network in the main text, is actually proportional to the trade flow matrix of the whole network.

Secondly, we will derive the reduced flow matrix according to and :

| (8) |

where, is the reduced stationary flow matrix. The trade flow network in Figure 3(l) is obtained by and multiplying the total trade volume of each country. Finally, the reduced TPM can be derived directly by the following formula:

| (9) |

Finally, is the coarse-grained TPM.

If there is still apparently cut-off in the singular value spectrum of , then repeat step 2) to 5). The reduced flow network in the example of trade network is obtained by running 1) to 5) twice.

C.2 Explanation

We will explain why this coarse-graining strategy outlined in the previous sub-section works here.

In the first step, the reason why we SVD decompose the matrix is that the singular values of actually are the squared roots of the eigenvalues of because:

| (10) |

thus, we will try our best to utilize the corresponding eigenvectors in to reduce , because they may contain more important information of .

Actually, the eigenvectors with the largest eigenvalues are the major axes to explain the auto-correlation matrix . Therefore we can use PCA method to reduce the dimensionality of s, it is equivalent to projecting onto the subspace spanned by the first eigenvectors.

In the fourth step, we cluster all the row vectors into groups according to the new feature vectors of . Actually, according to the previous studies [24], these major eigenvectors can be treated as the centroids of the clusters obtained by K-means algorithm for the row vectors . Therefore, we cluster all row vectors in by K-means algorithm, and the row vectors in one group should aggregate around the corresponding eigenvectors.

The final step is to obtain the reduced TPM according to the clustering result or in the previous step. This is a classic problem of lumping a Markov chain [25, 26]. There are many lumping methods, and we adopt the one in [27].

The basic idea of this method is to keep the stationary distribution and the total stationary flux unchanged during lumping process because they can be understood as a conservative quantity such as trade volume. As a result, we derive the method mentioned in the previous sub-section.

Appendix D Applying our coarse-graining method on more examples

D.1 Examples of boolean networks in Hoel(2003)

To compare our method and EI maximization method, we apply our method to the examples of causal emergence in Hoel et al’s original papers [5] and [6]. All the examples show clear causal emergence. And almost identical reduced TPMs are obtained for all the examples.

In Figure S4, we present the results for the same example Hoel mentioned, which uses a directed Boolean network of 6 nodes. Our findings align perfectly with Hoel’s, proving that the equivalence of the two theoretic frameworks.

Figures S5 and S6 show additional examples from the SI, where our model predicts a higher macro EI compared to Hoel’s findings. The main difference lies in our approach: Hoel groups variables to form a new macro network and then calculates EI for the TPM. We, on the other hand, group states directly, which might result in a TPM that doesn’t fully represent the original Boolean network in terms of variables. Therefore, the extension of our method to variable-based coarse-graining method is deserve future studies.

D.2 Example of trade flow network in 2000

To show one of the potential applications of our coarse-graining method, we apply the method on international trade network. The dataset is downloaded from the NBER-United Nations trade data (http://cid.econ.ucdavis.edu/nberus.html), and it covers the details of world trade flow from 1962 to 2000, and SITC4 (4-digit Standard International Trade Classification,Revision 4) standard [23] is used to organize hundreds types of products in the dataset. We select the network at year 2000 and ignore the products and aggregate the trade flows for all products. The network contains 190 nodes(countries) and 7,074 edges(trade relations) with weights representing trade flows.

Suppose the trade flow matrix is , where each entry represents the trade flow from country to , then the TPM is calculated as:

| (11) |

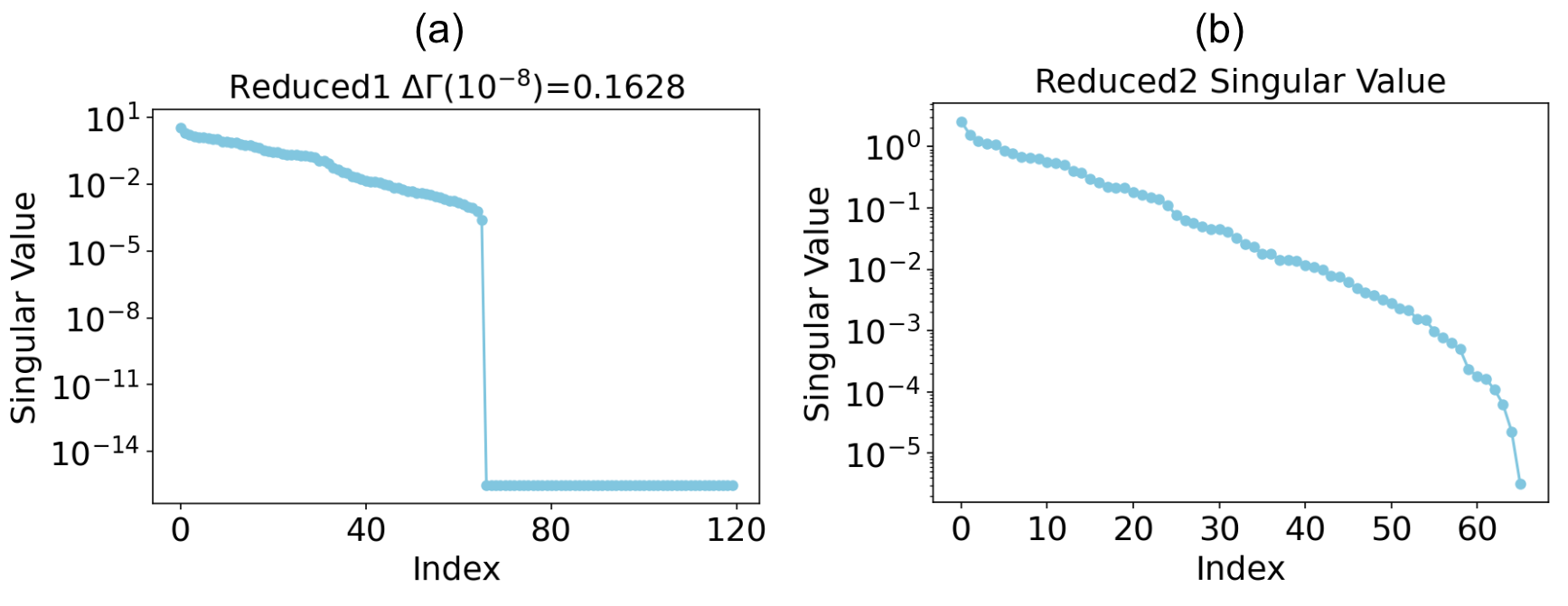

We plot the spectrum of singular values of as shown in Figure S7.

And there is an apparent cut off, thus we implement the coarse-graining method mentioned in section C on this network to obtain a reduced network. The threshold is set as , and the corresponding .

Next, we further plot the singular value spectrum as shown in Figure S8(a).

And there still is an apparent cut off, thus we run the coarse-graining method on this reduced network. The threshold is set , and the corresponding number of retained nodes to obtain the final reduced network as shown in Figure 3(l), and the spectrum of this final network is as shown in Figure S8(b).

Appendix E Theorems and Proves

E.1 Theorems and proves for

We will layout the theorems about and give the proves for them in this sub-section.

Theorem 1.

The can reach its minimum at if and only if the row vectors of the probability transition matrix are identical.

Proof.

The can be expressed as:

| (12) |

where, is the th row vector in , and is the logarithm function with base . By taking derivative, and using the normalization condition of probability distribution for , we obtain that:

| (13) |

for and , where for . Therefore, Equation 13 is equal to 0 if and only if:

| (14) |

for any . That is to say, all the row vectors are identical: for any . And the corresponding value of is:

| (15) |

∎

Therefore, can reach its minimum value when all the row vectors are identical. For the special matrix , also equals 0, however, it is not the unique minimum point. Actually, all the matrix with identical normalized probability vector can make .

By further taking the second order derivative of , we can prove that is not a convex function.

Corollary 1.

The second order derivative of with respect to the distribution with and is:

| (16) |

and the is not a convex function.

Proof.

By further taking the derivative of Equation 13 with respect to the distribution with and , we obtain Equation 16.

When and , the second order derivative of is:

| (17) | ||||

but when ,

| (18) |

holds no matter if or not. Therefore, the Hessian matrix is not positive-definite, is not a convex function. ∎

We will further discuss the condition and the properties of the maximum point of .

Theorem 2.

The effective information measure can reach its maximum if and only if is a permutation matrix.

Proof.

By noticing that

| (19) | ||||

where is the Shannon entropy of the average distribution . Thus, the can also be separated as:

| (20) | ||||

Where is the Shannon entropy of the distribution . Furthermore, we have:

| (21) |

the equality holds when is a one hot vector, and we also have:

| (22) |

and the equality holds when . By combining these two inequality together, we can obtain:

| (23) |

The condition that make the equality in Equation 21 and the equality in Equation 22 hold simantanously is that all row vectors in are one-hot vectors, and they are all different such that

| (24) |

Therefore, we reach the statement claimed by this theorem that must be a permutation matrix.

∎

E.2 Theorems and proves for dynamical reversibility and

E.2.1 Dynamical Reversibility and Time Reversibility

Theorem 3.

For a given markov chain and the corresponding TPM , if simoutanously satisfy: 1. is reversible, that is, there is a matrix , such that ; and 2. is also a TPM of another markov chain , then must be a permutation matrix.

Proof.

Because is reversible, therefore,

| (25) |

where, are the eigenvalues of , and their modulus are less than or equal to 1:

| (26) |

these inequality holds because is a TPM of a Markov chain according to [28].

Thus, the inverse of can be expressed by:

| (27) |

and:

| (28) |

However, this conflicts with the conclusion that the modulus of all the eigenvalues of a TPM must be less or equals to 1 if the inequality holds strictly. Thus, we have:

| (29) |

Therefore, the eigenvalues are the complex solutions for the equation of , thus is a permutation matrix. ∎

Next, we will prove dynamical reversibility implies time reversibility for Markov chains.

Theorem 4.

For a recurrent discrete Markov chain , suppose its TPM is on the space of states and its stationary distribution is , if is dynamically reversible, then also satisfies time reversibility.

Proof.

Suppose ’s time reversed Markov chain is , and its TPM , where and are the states at time steps and , respectively. Then should satisfy the detailed balance condition:

| (30) |

By using Bayesian formulation,

| (31) |

and let such that , Equation 31 can be written as:

| (32) |

If is time reversible, then , therefore:

| (33) |

Equation 33 is the sufficient and necessary condition for being time reversible.

If is dynamically reversible, then is a permutation matrix, and satisfies , then the corresponding stationary distribution must be such that any permutation on elements in is the same vector. Therefore, by taking all these special values into Equation 33, we have

| (34) |

Therefore, the dynamical reversibility of implies its time reversibility. But its reverse is not, apparently.

∎

E.2.2 The Measure of Dynamical Reversibility

We will present the theorems and the proves about the measure of dynamical reversibility in this sub-section. Before the theorems are presented, we will prove the lemma related with the theorem that will be used in the following parts.

Lemma 1.

For a TPM , where is the -th row vector, then:

| (35) |

Proof.

Because is a probability distribution, therefore, it should satisfy normalization condition which can be expressed as:

| (36) |

where, is 1-norm for vector, which is defined as the summation of the absolute values of all elements. Thus:

| (37) |

∎

Lemma 2.

For a given TPM , suppose its singular values are , we have:

| (38) |

Proof.

Because are the eigenvalues of , thus, can be written:

| (39) |

where is a orthonormal matrix with size , . Thus,

| (40) | ||||

The last inequality holds because of Lemma 1. And the equality hold if and only if:

| (41) |

∎

Lemma 3.

For a TPM , we can write it in the following way:

| (42) |

where is the -th row vector. And suppose ’s singular values are . Thus, if

| (43) |

then the singular values of satisfy:

| (44) |

and

| (45) |

where is the rank of the matrix .

Proof.

If , then , that means is a unit vector with modulus 1. While, for all , so must be a one hot vector which means only one element is 1 and others are zeros.

Therefore, there are two cases for : 1. There are , such that ; 2. For any , .

Case 1: If and because both of them are one-hot vectors, therefore and due to the symmetry of inner product. Therefore, both the element at the th row and th column and the element at the th row and th column are ones, and others are zeros. Notice that, holds in the same time according to the condition, thus, the matrix of has the following form:

| (46) |

in which, all the elements are 0 except the diagonal entries and the elements at and .

From the Equation 46, we know that the th row is identical to the th row. Thus, the minimum eigenvalue of which is also the last singular value of must be 0.

If there are multiple (say ) pairs of and which satisfies , then the last singular values are all zeros. And the rank of is . Therefore:

Case 2: If holds only for , then the non-zero elements all locate on the diagonal of , thus, . In this case , and must be a permutation matrix, and all singular values are 1. This is also in accordance with the Lemma.

∎

We want to prove that it is reasonable that the proposed measure to characterize the dynamical reversibility. First, we will prove that is upper bounded by the system size , and it can reach the maximum value if and only if is reversible.

Theorem 5.

For a given TPM , the measure of dynamical reversibility is less than or equal to the size of the system . And when is reversible, the upper bound can be achieved.

Proof.

Suppose any entry of the matrix is . It is easy to prove that for any since all the eigenvalues of (the singular values of ) are non-negative. We will prove that .

According to the definition of , the relations between the entries of the matrix and are:

| (49) |

where is the th row vector of , thus, according to Lemma 1, we have:

| (50) |

The inequality holds because of Lemma 1. Therefore, for the diagonal elements:

| (51) |

thus, . Finally,

| (52) |

The condition for that makes the equality holds is for all .

Therefore, according to Lemma 3, there are two cases need to be discussed separately.

Case 1: If there are two rows of are identical: for some , then the rank of is . Then, according to Lemma 3 the first singular values satisfy:

| (53) |

and for any .

Suppose there are singular values strictly larger than 1, then for those , thus:

| (54) |

And for , the singular values are either 0 or 1, and therefore . Finally, we have:

| (55) |

Case 2: If for any , and for , then according to Lemma 3, if and only if all the singular values are , which implies is reversible. ∎

Corollary 2.

If in is one hot vector for , and is degenerative, then the following equation holds:

| (56) |

Proof.

Because are all one hot vectors, thus, for all . According to Lemma 3, there are two cases. And because is degenerative, which means there are two rows of are identical: for some . This is exactly the first case in the proof of Theorem 5. Thus, we have:

| (57) |

∎

This theorem implies is a better indicator for dynamical inversibility than although both of them can achieve the maximized value when is reversible. However, if is degenerative, is also , but is not.

Theorem 6.

For a given TPM , can reach its global minimum 1 if and only if for , and this is the unique minimum for .

Proof.

When for ,

| (58) |

therefore, it has a sole eigenvalue . And this leads to that there is a solely one singular value for , which is also 1. Therefore,

| (59) |

On the other hand, the minimum value is also , this can be achieved when for .

Because the minimum value of is zero, and , thus can be minimized if the number of zero singular values is maximized. Notice that number of non-zero singular values of is the same as the rank of . Thus, the minimized value of can be reached when all the row vectors of are linearly dependent. In such case, there is only one non-zero singular value because is not zero, and all other row vectors can be expressed by the first vector .

Thus, according to Lemma 2:

| (60) |

However, because is a probability distribution which satisfies , thus, can be minimized when all the elements are equal. Thus,

| (61) |

For any other vector , because it is linearly dependent on , thus

| (62) |

with . However, because , thus must be zero. Therefore, .

Furthermore, because is the nuclear norm of the matrix (Schatten norm for ), thus, is a convex function[29]. Therefore, the minimum is the global minimum. It is also the unique minimum according to [30].

∎

Thus, the module of probability vector has lower bound of .

Next, to illustrate why the dynamics reversibility measure increases as the probability matrix asymptotically converges to a permutation matrix, or reversible, we have the following lemmas and theorem.

Lemma 4.

The reversibility measure is lower bounded by , and increases as the probability vectors are close to one hot vectors.

Proof.

Because the singular values are non-negative, so:

| (63) |

The last equality holds because of Lemma 2. Therefore:

| (64) |

∎

As can achieve its maximum when it is a one-hot vector, therefore the lower bound of increases as approaches a matrix with one-hot row vectors. However, may not be a permutation matrix because some row vectors may be similar, which means for all are not orthogonal each other but they collapse to one direction. Thus, we need to further prove a theorem to exclude this case.

Finally, we can conclude the following theorem by combining the conclusions of Lemma 4 and Theorem LABEL:thm:upperbound_gamma.

Theorem 7.

The reversibility measure is increased when the row vectors in converges to one-hot vectors, and they are orthogonal each other.

Proof.

Because for all , therefore and the equality holds if and only if is a one-hot vector. According to Lemma 4, we know that

| (65) |

Thus, as each row vector converges to a one-hot vector, increases. However, to reach the maximum value of , these one-hot vectors are not identical. According to Theorem 5, when is reversible, the reversibility measure can reach the maximum value . This implies that is a permutation matrix, and all row vectors are orthogonal each other. ∎