Adaptive Ridge Approach to Heteroscedastic Regression

Abstract.

We propose an adaptive ridge (AR) based estimation scheme for a heteroscedastic linear model equipped with log-linear errors. We simultaneously estimate the mean and variance parameters and show new asymptotic distributional and tightness properties in a sparse setting. We also show that estimates for zero parameters shrink with more iterations under suitable assumptions for tuning parameters. We observe possible generalizations of this paper’s results through simulations and will apply the estimation method in forecasting electricity consumption.

Key words and phrases:

Heteroscedastic Regression, Adaptive Ridge, Asymptotic Theory, Regularized Estimation1. Introduction

Consider the following location-scale regression model

| (1.1) |

for one-dimensional responses , covariates and with log-linear errors. The model can also be written as

| (1.2) |

where and are the design matrices, is the response, is the error and . The covariates and may have common components.

The seminal work [8] introduced ridge estimators to tackle multicollinearity, an issue that made the ordinary least squares estimator unreliable. Taking advantage of the availability of the explicit form of ridge estimators, we propose an adaptive ridge estimator to estimate the unknown parameter for bounded domains and . We introduce a computationally efficient estimator that does not require numerical optimization. We also carefully consider variable selection without fully committing to a sparse regularization, which is known to be fragile if true parameters are small but non-zero.

The model under (1.1) was first studied in 1976 by [7] using an approach utilizing the least squares regression and then the likelihood analysis for normal errors. We will not restrict to normal errors in this paper, as we discuss conditions required for asymptotics to hold. In particular, we show asymptotic results for the scale parameter that were absent in [7] and subsequent works studying this model.

Results for penalized estimators are widely studied, as in [6]. A similar iterative approach is the Broken Adaptive Ridge (BAR) estimator for the parameter , under a setting without including exponentially-scaled errors [2]. Our adaptive ridge (AR) estimator is an iterative procedure that estimates and in alternation. We empirically show that our estimators can strike a balance between computational ease and stability for small non-zero parameters, see for instance [6] and [10]. Altogether, we take a practical standpoint and simultaneously tackle multiple statistical settings such as multiplicative heteroscedasticity, and sparsity.

We organize the paper as follows. We introduce notation and the setup of the AR procedure in Section 2. In Section 3, we first state the assumptions, and then prove asymptotic distributional results for the initial and iterated estimators of and in 3.5 and 3.6, respectively. Then, we justify the reason to perform more iterations in 3.9. Simulation results are given in Section 4 and we compare the performance of AR with other well-known regularized estimators using electricity consumption data in Section 5. We discuss unresolved issues in Section 6 with concluding remarks and defer our proofs to the Appendix.

2. Constructing the Adaptive Ridge Estimators

We begin by describing the AR procedure, defining the estimators, and introducing the required notation. We will denote the transpose of matrices and vectors by and , respectively. Furthermore, we will take exponentials, logarithms, and powers of vectors component-wise. Throughout this paper, unless otherwise specified, stands for the Euclidean norm for vectors and the spectral norm of matrices, so that for any square matrix , is the square root of the largest eigenvalue of . We denote positive definite matrices by and positive semi-definite matrices by . For a diagonal matrix, this is equivalent to having positive and non-negative entries. We will use for convergence in law and for convergence in probability. We write and for the minimum and maximum eigenvalues of a matrix . Finally, we will use the notation to mean for some universal constant , for every large enough .

Define the diagonal tuning parameter matrix . The initial ridge estimator corresponding to is:

| (2.1) |

We aim to construct a ridge estimator for by plugging in our estimator of . If we write

then

| (2.2) |

Assuming (see 3.3), (2.2) is well defined almost surely. Then, by subtracting the unknown expectation on both sides, we get

which allows us to consider a ridge-type estimator for the zero-mean errors . Denote

and ,

where denotes a column of 1’s. We define the initial ridge estimator of to be

| (2.3) |

where is the diagonal tuning parameter matrix associated with . We will show the asymptotic normality of and depending on the strictness of conditions placed on , tightness or asymptotic normality of before further deducing the asymptotic results of subsequent estimators.

Remark 2.1.

We assume the matrix does not contain a column of ’s, which is crucial as we wish to estimate , so an additional intercept term poses an identifiability issue. If a column of 1’s is present, we lose consistency when estimating the intercept term of , as there will be bias contributed by the term . We avoid this inconvenience by imposing this assumption, but results for the AR procedure for other components do not depend on this assumption.

Using this estimate for , we can define an adaptive weighted ridge estimator for . By letting

we can define for

| (2.4) |

We then repeat a process similar to (2.3) upon obtaining an updated estimator for with adjusted weights in the ridge penalty. Namely, by setting

for we define an updated estimator of as follows:

| (2.5) |

Remark 2.2.

Note that since the initial ridge estimators and and their subsequent iterations are non-zero almost surely, and are well defined.

In our proposed method, we will have to divide by very small, non-zero values in the matrix when the estimates of are small, in turn causing arithmetic overflow [2]. One solution given in [5] to circumvent this issue is by introducing a small perturbation by defining and for some small constants , which improves numerical stability at the cost of introducing some bias and fitting two extra hyperparameters.

3. Main results

3.1. Assumptions

Assumption 3.1.

There exist positive definite matrices , , , and such that

| (3.1) |

as . Furthermore, there exist constants , , and for which

| (3.2) |

Assumption 3.2.

Assumption 3.3.

The random errors are i.i.d. with , . Furthermore, for all .

Assumption 3.4.

For each , there exists some and such that

3.1, 3.2 and the mean and variance conditions of 3.3 are standard to make. The rest are regularity conditions tailored to proving asymptotic results of . The negative moments conditions of 3.3 and 3.4 can be verified by considering densities when they exist [9], which we will further explain after stating 3.5. Note that the logarithmic moments and also exist under 3.3.

3.2. Asymptotic results of and

We provide an asymptotic result for our initial estimators. As we construct an iterative scheme, the following convergences will play a vital role in asymptotic results for subsequent estimators. The following result for is well known and is present in literature such as [6]. The asymptotic results for are first proved here to the authors’ understanding.

Theorem 3.5.

Although we have stated a general result for , we will focus on for the rest of this paper. Moreover [9] provides a link between negative moments and the density function (when it exists), which will help understand the negative moments condition needed for (3.5), as well as 3.3 and 3.4. To summarize, [9] showed that if possesses a density function , then

-

(1)

If is bounded near then for all .

-

(2)

is sufficient for .

-

(3)

If for some , for some , then exists for all .

Referring to these conditions, it is straightforward to see that most errors, including normal errors, satisfy the condition needed for for all in 3.3, but fail to possess an inverse first moment, which is why (3.4) and (3.5) are presented separately. Still, there are families of distribution that satisfy the condition in (3), for instance, one can show that the log-normal distribution (reflected about and standardized) is a class of errors that satisfy the stricter conditions.

3.3. Notation Under Sparsity

We are mainly interested in the asymptotic behavior of estimators under a sparse model, so for clarity we introduce additional notation for subsequent parts. Suppose exactly and components from and are non-zero. We will denote using the () and () subscripts for the non-zero and zero components respectively. Upon permuting the components, and . We will therefore write and in the same manner, despite and being unknown. Moreover, the symmetric by matrices such as

and

will be written in the form of

| (3.6) |

where the top left block will have dimension , corresponding to the nonzero entries of ; this is a generic notation for block decomposition. Similar subscripts will be adopted for by matrices such as , with the top left block being size . Diagonal matrices such as and will also be written as

| (3.7) |

with the top left block having dimensions by and by respectively. We further introduce the functions

corresponding to the zero and non-zero entries of and respectively.

3.4. Asymptotic Results of and

The next theorem provides insight into the asymptotic behavior of estimators after a fixed number of iterations . In particular, we will see how there is reduced asymptotic covariance compared to the initial estimators of 3.5. In the remainder of the paper we will denote and .

Theorem 3.6.

Assume for some constant matrix . Under Assumptions 3.1, 3.2 and 3.3, for each integer ,

| (3.8) |

where .

Moreover, if 3.4 holds and , then for all and ,

| (3.9) |

Further, if for some , and for some constant matrix , then

| (3.10) |

where .

Remark 3.7.

Remark 3.8.

In 3.6, we have not identified the weak limits of and . Yet, the matrices and are non-negative definite, which implies

and

Therefore, we can infer that the AR estimators are -tight and gain reduced covariance by penalization. However, 3.6 alone is insufficient in describing all the benefits of AR as it does not justify the motivation to perform extra iterations. Since the changes in distributions from extra iterations depend solely on and , understanding the behaviour of sparse estimates is crucial, which motivated us to give the next result.

Theorem 3.9.

Under 3.1, if and then for any ,

| (3.12) |

If for some and , then for any ,

| (3.13) |

If in particular for some , then we can replace above by .

4. Simulation

This section aims to illustrate the theoretical results presented in Section 3 and provide numerical evidence to generalize them further.

4.1. Model 1 Setup

We simulate data under true parameters and , where apart from the first three components, the rest of and are generated as independent and respectively. The main goal of the numerical experiment is to observe the theoretical results of individual non-zero and zero components through simulation, and we focus only on the first three components of and as they are representative of our findings and display the same type of behaviour regardless of what the remaining components are. Further, the reason to generate and to have higher dimensions than needed is to show the stability of the AR under finite sample settings, hence its practicality. We generate the entries of the design matrices and using independent normal random variables with mean 0 and standard deviation 1 and 0.3 respectively and will be kept the same throughout the simulation. The errors ’s are also independent in this model, so that

where denotes the digamma function [7]. Therefore, . The tuning parameters are chosen to be for all and for simplicity. While methods such as cross-validation (CV) can be implemented for better performance they come at a further computational cost. As our focus here is only on observing theoretical properties, we will keep the tuning parameters simple.

We set the number of samples and performed 1000 independent trials. We will compare the performances of our proposed AR estimators when the number of iterations is 0, 2, 5, and 10.

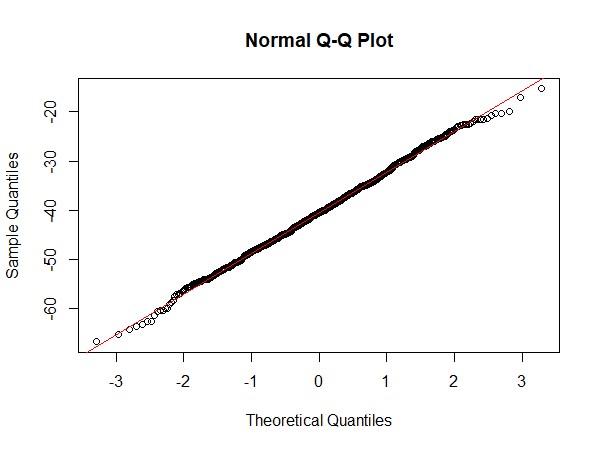

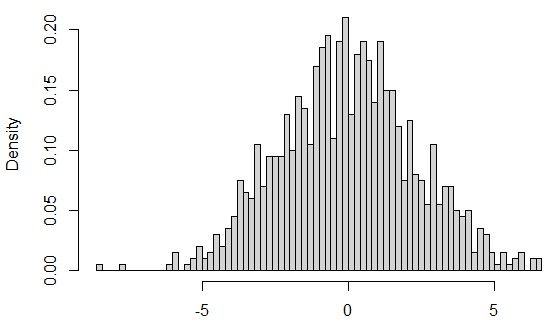

4.2. Normality of

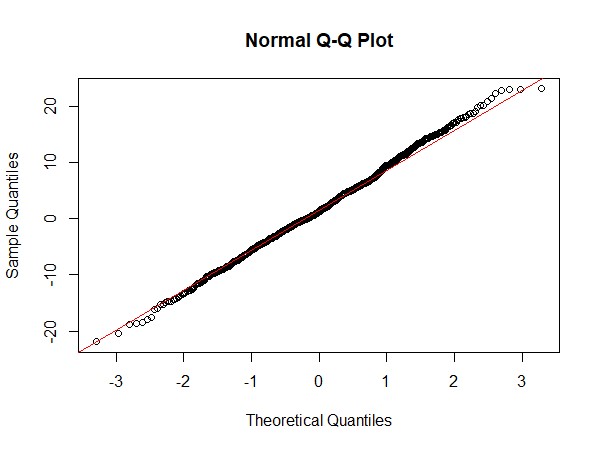

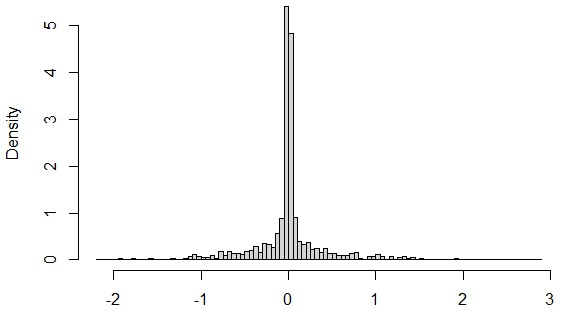

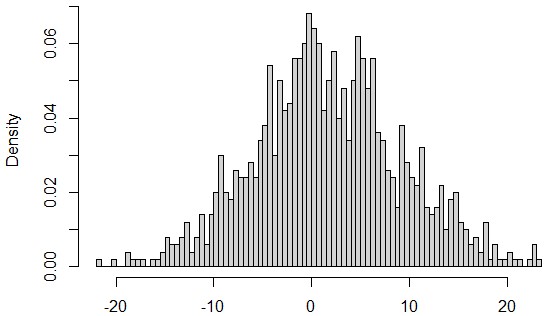

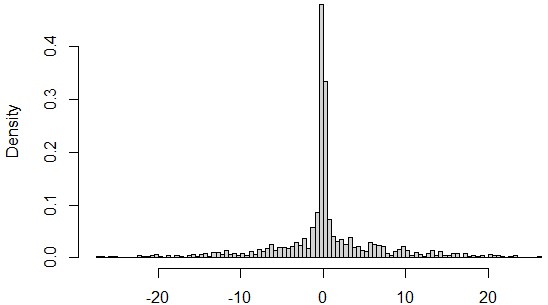

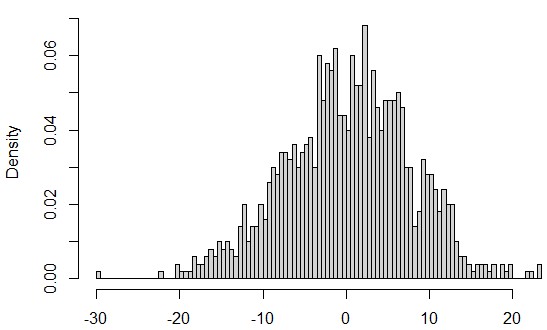

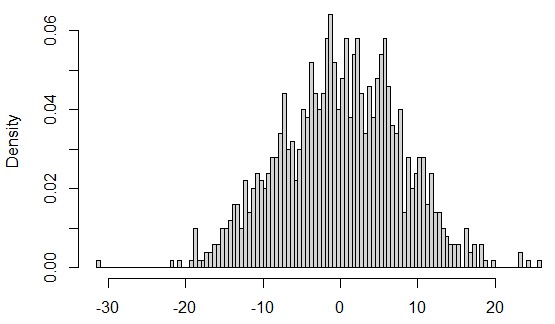

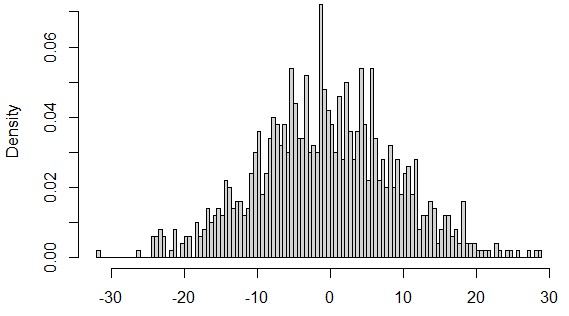

The asymptotic normality result for in 3.5 is proved only under stronger conditions on , namely for some . While providing theoretical guarantees, the assumption is restrictive and excludes commonly considered errors including normally distributed . In the hopes of generalizing and incorporating a wider class of noise distributions, we lift the condition on and empirically obtain (3.5) in Figure 1, where we obtain strong numerical evidence of asymptotic normality of for . For further evidence of normality for , we may also refer to Figure 2, where the green line on the right plots the sample density of .

4.3. Effect of iterations

Sparse and non-sparse parameters behave very differently under the AR scheme. Non-zero parameters are not expected to see apparent improvements in performance with added iterations, while estimates for the zero components will shrink as discussed in 3.9. As such, we present the numerical results separately below.

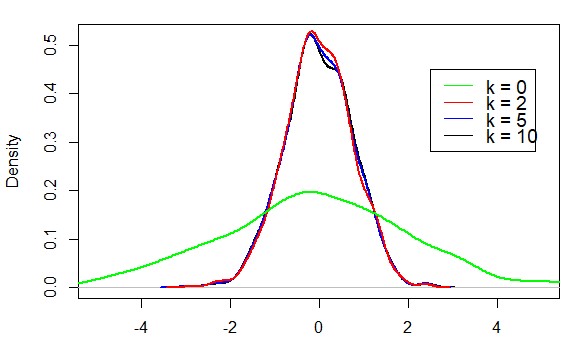

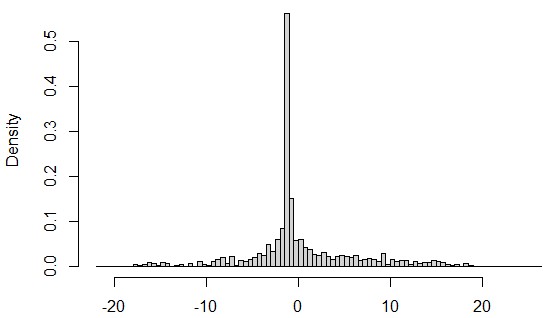

Sample densities of the 1000 independent estimates of are shown on the left of Figure 2. The green line provides evidence of a normal density of the initial estimator, in line with 3.5. The three other lines for mostly overlap as there is no visible improvement in performance under more iterations. The empirical mean squared error (eMSE) of the initial estimator was whereas the eMSE for for were reduced approximately , which is a result of re-weighting for non-homogeneous errors.

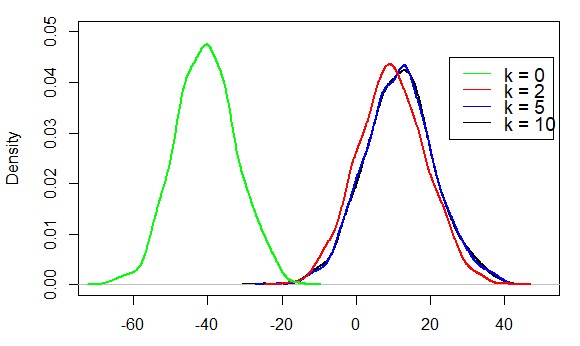

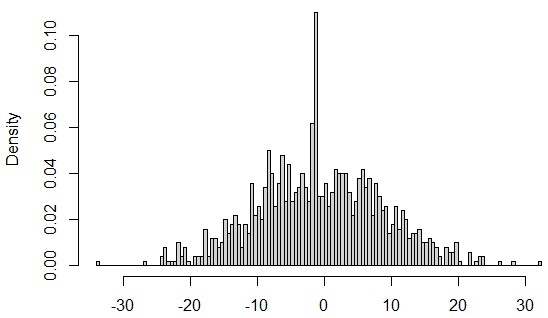

The initial estimator shows significant bias as seen in Figure 2 when estimating . Upon iterating, bias is reduced due to more accurate plug-in estimators for (2.5). As in the case for , there is no major difference in performance between the cases . The eMSE for was 3.41, and 0.354, 0.451 and 0.455 for , and respectively.

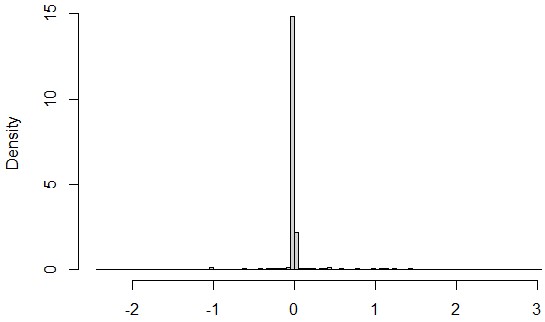

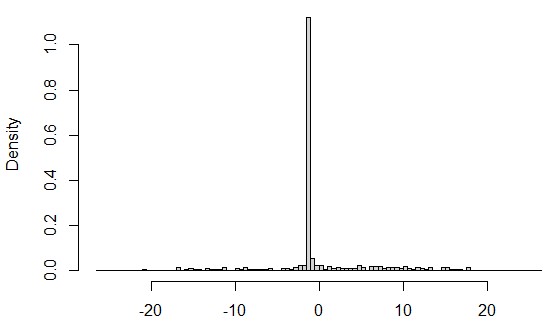

Next, we show the merits described by 3.6 and 3.9 when estimating sparse signals by numerically showing the shrinking effect to and discussed in 3.9. In Table 1, we tabulated the medians of the absolute value of our 1000 estimates to show a central tendency towards . The medians decrease as we perform more iterations, indicating that the estimates shrink, with the most notable drops being from to for all four estimators. We note that due to computational limitations, if more than half of the estimators are numerically 0, as in the cases of and , then their medians will also be 0 even if their real values are non-zero.

Remark 4.1.

As we are considering large finite sample behaviour, it is possible that a few estimates for 0 components do not converge, but instead are much further away from than the rest. In such cases, if the mean was used to evaluate the extent of shrinkage, such outliers would prevent any meaningful comparison. Instead, by using the median, we do not need to worry about the discussed issue.

| 0.068 | 0.077 | 0.22 | 0.21 | |

| 0.049 | 0.052 | |||

| 0 | 0 |

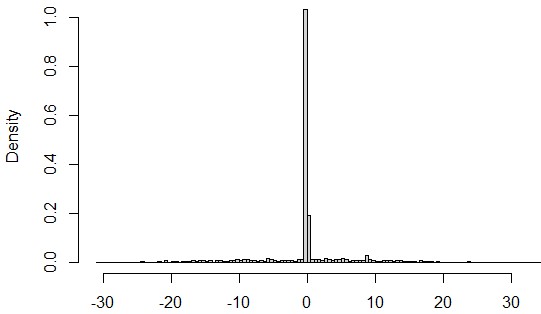

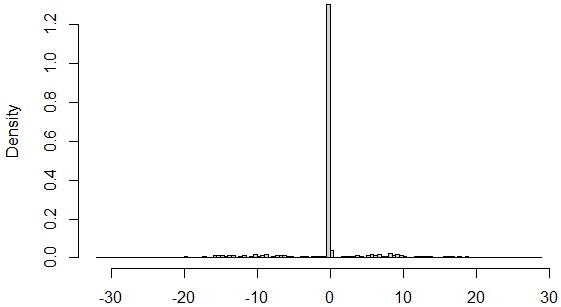

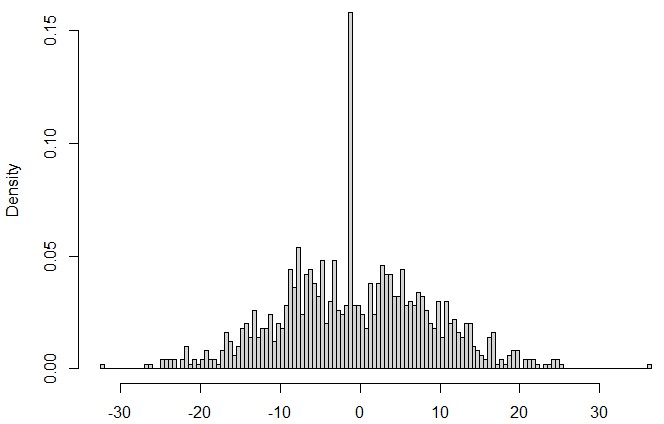

We also provide histograms of estimates for and () for a better picture of the shrinkage process in Figure 3 and Figure 4. We can also refer to the top-left () histograms for another observation of normality, which does not hold when . The histograms in Figure 3 and Figure 4 provide another perspective to shrinkage induced by the iteration scheme. Furthermore, we may refer to the top-left () histograms for extra empirical evidence of asymptotic normality under normal errors, which does not hold when .

4.4. Model 2: Setup

The next model is used for discussing the effect small parameters have on AR estimators. In this section, we adopt a similar setup as Section 4.1. We change the true parameters to and , where the remaining components of and are generated as and , and entries of and are generated as and independent random variables as before. In this section, we let and and change the values of and accordingly. We also change the distribution of to a -distribution with degrees of freedom 2.5, whose main purpose is to incorporate a wider family of errors and suggest the possibility of weakening current assumptions on . The result shows that our procedure continues to work under errors with heavier tails.

4.5. Presence of small parameters

While many sparse estimators usually provide desirable asymptotic results, their performances under finite samples can sometimes be overlooked. It is known that penalized schemes can suffer from inconsistency issues when small coefficients are present outside the asymptotic setting. See [13] for detailed analyses where they revealed weaknesses of the penalized estimator in a moving parameter setting by allowing the real parameter to perturb around at an order of . One of the strengths of the AR scheme is its flexibility in such scenarios. As both the magnitude of tuning parameters and the number of iterations can be adjusted, the degree of shrinkage can also be more properly and continuously controlled than most existing schemes.

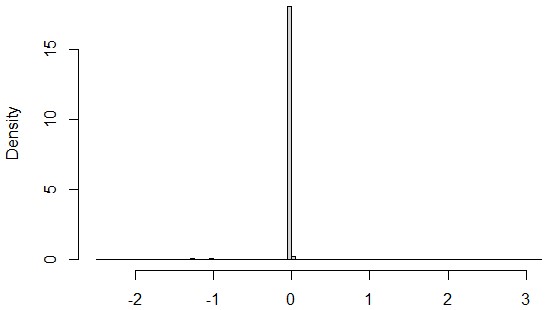

The spikes away from 0 in Figure 5 correspond to estimates incorrectly shrunk towards 0. As the number of iterations increases, so does the frequency of this phenomenon. Away from the spike, the histograms are non-sparse, which is a reassuring sign of robustness against small parameters. Yet, the results are unsatisfactory especially for and , as almost all estimates incorrectly interpreted a non-zero parameter as zero.

One approach to tackle this issue is to use smaller tuning parameters, which makes the scheme more sensitive to small parameters but reduces shrinkage. We show the results in Figure 6 reducing from 1 to 0.1 and from 1 to 0.001, where we also increase the number of iterations in return. In doing so, the frequency of incorrect shrinkage is drastically reduced, and the distribution for non-zero parameters is recovered even when is large. In particular, allowing for a trade-off of performance and computation efficiency is one of the merits of using the AR.

5. Electricity Consumption Data Analysis

We analyze electricity consumption data obtained from Tokyo Electric Power Company Holdings, Incorporated (TEPCO) for 2018 to 2021 as a real-data example. The data is available on TEPCO’s official website (”https://www4.tepco.co.jp/en/forecast/html/download-e.html”) and contains records of the highest hourly consumption, contributing to a total of entries. We have split the data into training (2018 and 2019, ) and testing (2020 and 2021, ) sets.

and contain 64 features, including the day of the week (: Tuesday to Sunday), hour of day () and temperature (), public holidays (), weekend public holidays () and interaction terms (, , , ), where . The design matrices have been standardized so that each column has mean 0 and unit variance, whereas the consumption data has been centralized to have mean 0 for ease of calculations.

We compare the estimates of for AR estimators for with the LASSO [14] and Elastic Net [15] with elastic net mixing parameter 0.5. The LASSO and Elastic Net were both implemented using the R package glmnet [4] and were optimized using 10-fold CV over 100 values of tuning parameters. To reduce complexity, we let the tuning parameters be identical, so that and . We performed simultaneously five-fold cross validation for and , trialing 25 points from for and , and was optimal. We will also show the AR estimates of . Finally, the threshold to round small estimates to 0 is set to be .

| LASSO | Elastic Net | AR () | AR () | AR () | |

| ph | -33.0235 | -36.2142 | -62.3015 | -45.0963 | -50.0355 |

| Tues | 1.5724 | -0.4790 | -0.2587 | 0 | 0 |

| Wed | 7.7628 | 7.0601 | -0.3479 | 0 | 0 |

| Thurs | 14.5631 | 9.4511 | 1.7723 | 0.0889 | 0 |

| Fri | 13.4204 | 14.5521 | -3.2292 | -4.1425 | -0.0094 |

| Sat | -89.3486 | -89.4677 | -105.9261 | -83.6348 | -61.0291 |

| Sun | -138.9144 | -127.5361 | -94.2650 | -115.6102 | -94.6262 |

| -653.5430 | -515.4238 | -610.9382 | -881.6154 | -898.8703 | |

| 0 | -348.0740 | 1.0840 | 0 | 0 | |

| 788.1030 | 1108.7086 | 93.6917 | 1870.6414 | 1822.3644 | |

| 0 | -83.7872 | 746.4624 | -956.4272 | -900.4149 | |

| 168.6433 | 265.2008 | 404.5176 | -141.2085 | -821.3668 | |

| … | … | … | … | … | … |

| Fri | -24.2677 | -29.0486 | 0 | 0 | 0 |

| Fri | 0 | 0 | 0.0012 | 0 | 0 |

| Fri | 0 | 0 | 0.2434 | 0 | 0 |

| Fri | 31.5986 | 34.4185 | 13.4298 | 18.9116 | 20.4004 |

| Sat | 5.7711 | 28.2225 | 0 | 0 | 0 |

| Sat | -3.9340 | -38.7760 | 0.0230 | 0 | 0 |

| Sat | 0 | 0 | 0.1239 | 0 | 0 |

| Sat | 0 | 14.2698 | 0.6059 | 0 | 0 |

| Sun | 0 | -32.9260 | -94.0100 | 1.0281 | 0 |

| Sun | 19.7139 | 0 | 28.6261 | -3.6234 | 0 |

| Sun | 0 | 114.2071 | 7.6010 | -6.7407 | -9.6121 |

| Sun | -39.6542 | -112.9375 | -0.0340 | 0 | 0 |

| Selected Predictors | 40 | 57 | 60 | 36 | 26 |

| MSPE | 74425.05 | 73281.74 | 93358.09 | 78277.78 | 74487.11 |

| Intercept | 9.9408 | 9.5954 | 9.4546 |

|---|---|---|---|

| ph | -0.2105 | -0.1197 | -0.0017 |

| Tues | -0.0075 | 0 | 0 |

| Wed | -0.0131 | -0.0002 | 0 |

| Thurs | 0 | 0 | 0 |

| Fri | -0.1403 | -0.0423 | -0.0984 |

| Sat | -0.2844 | -0.1511 | 0 |

| Sun | -0.3449 | -0.1677 | 0 |

| 0.6288 | -0.0123 | 0 | |

| -2.2129 | -2.3932 | -3.8494 | |

| Sat | 0 | 0 | 0 |

| Sat | 0 | 0 | 0 |

| Sat | 0 | 0 | 0 |

| Sat | -0.0151 | -0.0008 | 0 |

| Sun | 0.0382 | 0 | 0 |

| Sun | 0.1866 | 0.0752 | 0.0868 |

| Sun | -0.0798 | 0 | 0 |

| Sun | 0 | 0 | 0 |

| Selected Predictors | 57 | 36 | 20 |

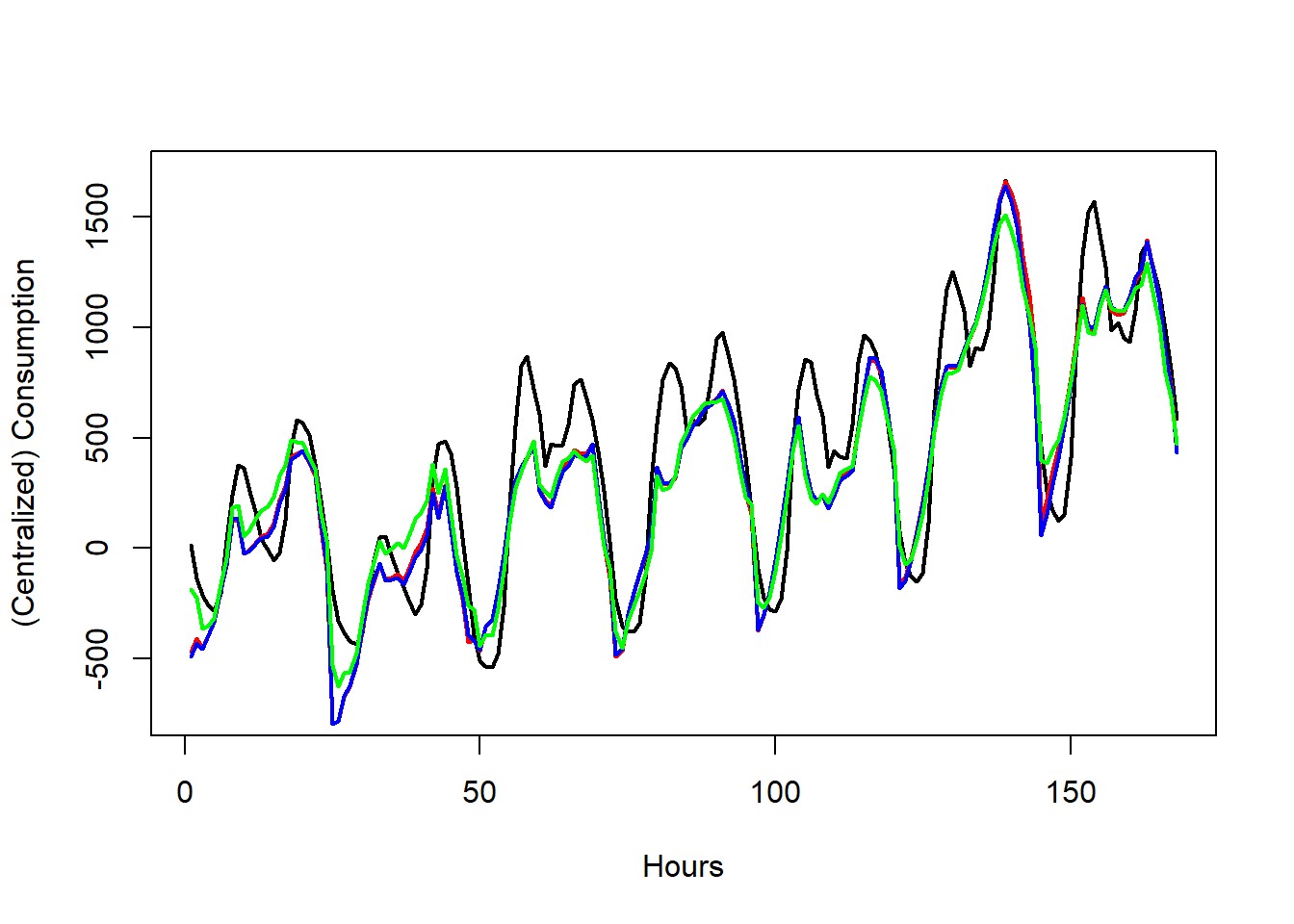

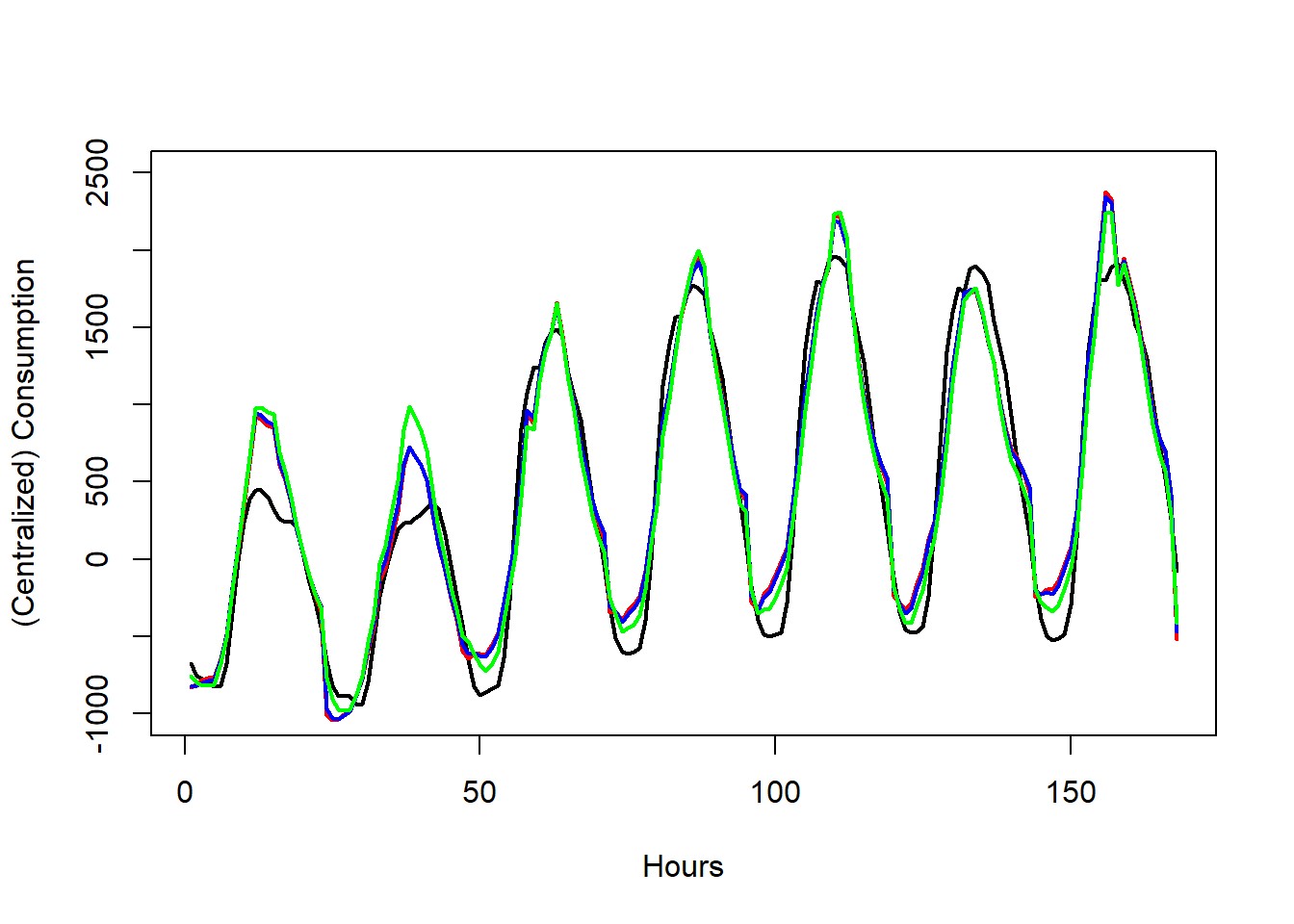

Some of the estimated coefficients of are shown in Table 2. Among the AR estimators, (AR10) selects the fewest number of predictors and has minimal MSPE. The AR10 also shares similar performances to well-established and optimized schemes like the LASSO and Elastic Net. We refer to Figure 7 to visualize the fit of each of the estimators.

As shown in Table 2, the AR becomes increasingly sparse (post-threshold), as the number of selected predictors decreases with the number of iterations, as described in 3.9. Another feature to be noted is how the AR scheme preserves very small coefficients even for . For instance, estimates such as are still preserved, as in the case of for .

On the other hand, Table 3 shows the estimates for . Results indicate the model might not be purely homogeneous, and the estimators have identified relevant features. Shrinkage is also observed here as the number of selected predictors drops with the number of iterations.

6. Discussion and Concluding Remarks

One area for future work is on extending the tuning matrices and to general positive definite matrices. We believe similar results should arise by generic eigenvalue arguments. On this avenue, improvement can also be made in the selection of tuning parameters.

Motivated by the numerical success in Section 4, it is likely that the assumptions on can be weakened so that asymptotic distributional results for hold under a wider class of errors. Further, to strengthen the result given in 3.6, one can attempt to construct approximate confidence sets for the iterated estimators of .

Finally, with the success of ordinary ridge estimators in high-dimensional settings, it will be interesting to see the AR as an extension of high-dimensional ridge regression. Alternatively, motivated by the success in modeling electricity consumption data, we are optimistic that the estimator can be generalized to other frameworks such as time series or stochastic differential equations.

Acknowledgement

The first author (KH) would like to thank JGMI of Kyushu University for their support. Also, this work was partially supported by JST CREST Grant Number JPMJCR2115 and JSPS KAKENHI Grant Number 22H01139, Japan (HM).

Appendix A Proof of 3.5

We begin by stating the matrix inversion formula (also known as the first-order resolvent formula or Sherman-Morrison-Woodbury formula), used as in [2]:

| (A.1) |

Using (A.1), we write

| (A.2) |

Let us first consider term , where we can apply the Lindeberg Central Limit Theorem. By writing

the mean is computed as, where denotes the -dimensional -vector. Also, the covariance

under 3.1. Finally, to check for Lindeberg’s condition, we let and note that by 3.2. Thus for any ,

where the final limit follows from and applying Lebesgue’s Dominated Convergence Theorem on the sequence . Thus the first term of (A.2) converges in law:

| (A.3) |

As for the other term of the sum in (A.2), we rewrite it as

which we further evaluate as a sum of two terms. By (A.3) and (), it follows that

and

Combining these results with (A.3) show asymptotic normality as stated in (3.3):

We now proceed to the asymptotics of . First note that

We denote and , so that for ,

| (A.4) |

By (A.1), the first term of the sum vanishes as for under :

Then, if we write and use the Lindeberg Central limit theorem analogously, we obtain under 3.1 and that

| (A.5) |

which also proves that the second term of (A.4) is if .

We will first prove (3.4), and to this end, we are going to show the tightness of the third term of :

By 3.1, it is sufficient to show

We denote , , and . Let denote the indicator function of the event . Then,

| (A.6) |

We first treat . Since for all and , there exists some constant so that

Using this with we get by 3.2

| (A.7) |

The following Lemma is required next.

Lemma A.1.

There exists some such that for all ,

Proof.

We will now estimate the upper bound in (A.7) using the Markov and Hölder inequalities: under Assumptions 3.2 and 3.3, for any positive constant :

| (A.8) |

as by A.1, provided that we choose and such that and . Therefore,

| (A.9) |

We now turn our attention to . Taking expectations, we have

where we chose the exponents independently of that in (A.8). We bound similar to (A.8). For any there is some constant such that

| (A.10) |

By choosing and so that and , we get consistent results with (A.9). Finally,

for any . The last inequality follows from choosing a sufficiently small using the following bound: For all real , there exists some constant such that for all

Taking expectation and supremum over and , the first, third, and fourth terms are all finite under Assumptions 3.2 and 3.3. Finally for sufficiently large , by 3.4 we have

| (A.11) |

Along with (A.10), we obtain

| (A.12) |

Combining the results of (A.9) and (A.12) proves (3.4). If there exists such that , then in (A.8) we can instead allow and to get in (A.9) and in (A.10) let to obtain , which show in (A.4). Finally, we deduce (3.5) using (A.5).

Appendix B Proof of 3.6

First, we write

where we denote . We will first prove and then simplify the expression of .

Firstly, if no entries are exactly 0 then follows from the consistency of , and the matrix inversion formula, which is similar to what we have proved in 3.5. Otherwise, suppose are non-zero (The case where is similar to the result below without needing to consider block matrices), in which case we let

The Schur complement of is given by

and the inverse of is [12]

| (B.1) |

Here, the matrices are written without the subscript for brevity. Next, we rewrite as follows:

| (B.2) |

We will proceed to evaluate the limits of the rows

and

separately. For the upper part (), note that , so by (B.1) we get

| (B.3) |

Moreover by (A.1), since ,

| (B.4) |

Finally by 3.1, is bounded for large enough , and since , is bounded for all large enough . Also, so is also bounded for all sufficiently large , which jointly imply

Therefore,

and thus

| (B.5) |

For the second row (), we get

| (B.6) |

Therefore,

| (B.7) |

Substituting (B.5) and (B.7) into (B.2) gives

as required.

Moving onto , the consistency of and (3.2) imply

and

Writing then gives

| (B.8) |

We can use the Lindeberg CLT analogously as we did for (A.3) to obtain

Further, by noting and , we may appeal to (A.1) and to conclude

Returning to (B.8), we obtain

| (B.9) |

which proves (3.8).

We now move on to prove the corresponding results for by first writing

where

.

The term can be shown to be in the exact same way we did for , swapping out for ; for ; for and for . Then under 3.3, we denote and use the Lindeberg CLT to show

which also implies .

Finally, under B.1 (stated below), we can follow the proof of 3.5 to show that for all by bounding the term , which gives (3.9). Further, with the stronger condition of for some , we can proceed as in (B.9) to get

which gives (3.10). The statement for general follows inductively.

We state a similar Lemma as A.1 to prove corresponding results for .

Lemma B.1.

For each , there exists some such that for all ,

Proof.

We only consider as the general case follows the same proof. We write as before, and we will bound the moments of each of the two terms.

Using the same notation as in (B.2), we may write as follows and bound the upper and lower parts separately:

| (B.10) |

First, we look at . As we previously expanded in (B.3), for

By the matrix inversion formula (A.1), we also have

Using the eigenvalue bound of in 3.1, we can also bound the moments of and for sufficiently large . Then, rewriting

we will consider conditioning on the event

for a fixed constant , so that

Since for , is bounded on for sufficiently large , which in turn ensures that for some . As is bounded,

where the latter inequality follows from Markov’s inequality. By choosing , along with A.1, we can conclude

Finally, by uniformly bounding the norms of and as we did in the proof of 3.6, we also get

Next, we turn to . Once again, it suffices to show that

By the second line of (B.6), we can rewrite the expression as

which can be handled analogously to . We conclude that .

We next need to show that Recall that

and by 3.1

Therefore, it suffices to show

Let . Using the Sobolev inequality, as is a bounded convex domain in , for any , we have

where is a constant independent of , and is the partial derivative of with respect to . We can then write and , where both and are non-random and satisfy that for large enough because and are both bounded by 3.2. Finally, the Burkholder inequality gives

where the final inequality follows from by 3.3. The result corresponding to follows analogously. ∎

Appendix C Proof of 3.9

We only show the result for , the general case can be obtained similarly. Denoting , we write

Multiplying both sides by yields

which can be rearranged to

namely

| (C.1) |

As and , the right-hand side of (C.1) is . For ease of reading, we now let for the remainder of the proof. Then, focusing on the lower components of (C.1) gives

| (C.2) |

We then proceed similarly as in Lemma 1 of [2] by first considering the order of the second term on the left-hand side of (C.2):

where follows from 3.1 as we also note and . Hence,

| (C.3) |

Using the triangle inequality, we estimate the left-hand side of (C.3) as follows:

Below, we will bound the norm of from below and the norm of from above in (C.4) and (C.5), respectively.

As is symmetric positive definite, it is diagonalizable by orthonormal eigenvectors. With probability tending to one, has a spectral decomposition for eigenvalues and orthonormal eigenvectors by 3.1. Using the spectral decomposition, we obtain

Now denoting

with probability tending to 1, we have

| (C.4) |

Moving on to , we have

| (C.5) |

Combining (C.4) and (C.5) and writing we obtain

Recall from (C.3) that and note that . Then for sufficiently large , we can estimate as follows:

as . Finally, for sufficiently large ,

The proof above relied only on the fact that . For we repeat the proof and obtain

as claimed in (3.12). To show (3.13), we first observe

which can be rewritten as

We may bound similarly as before, but as it is not proven that , we can only appeal to for , thus requiring the slightly stronger condition:

| (C.6) |

for some . The final step is identical to the case of so (3.13) is proved. In the case where , is -tight for , which means the proof follows if .

References

- [1] B. V. Bahr. On the Convergence of Moments in the Central Limit Theorem. The Annals of Mathematical Statistics, 36(3):808 – 818, 1965.

- [2] L. Dai, K. Chen, Z. Sun, Z. Liu, and G. Li. Broken adaptive ridge regression and its asymptotic properties. Journal of Multivariate Analysis, 168(C):334–351, 2018.

- [3] A. DasGupta. Moment Convergence and Uniform Integrability, pages 83–89. Springer New York, New York, NY, 2008.

- [4] J. H. Friedman, T. Hastie, and R. Tibshirani. Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software, 33(1):1–22, 2010.

- [5] F. Frommlet and G. Nuel. An adaptive ridge procedure for l0 regularization. PloS one, 11(2):e0148620, 2016.

- [6] W. Fu and K. Knight. Asymptotics for lasso-type estimators. The Annals of Statistics, 28(5):1356 – 1378, 2000.

- [7] A. C. Harvey. Estimating regression models with multiplicative heteroscedasticity. Econometrica, 44(3):461–465, 1976.

- [8] A. E. Hoerl and R. W. Kennard. Ridge regression: Biased estimation for nonorthogonal problems. Technometrics, 12(1):55–67, 1970.

- [9] A. Khuri and G. Casella. The existence of the first negative moment revisited. The American Statistician, 56(1):44–47, 2002.

- [10] H. Leeb and B. M. Pötscher. Sparse estimators and the oracle property, or the return of hodges’ estimator. Journal of Econometrics, 142(1):201–211, 2008.

- [11] Z. Liu and G. Li. Efficient regularized regression with l0 penalty for variable selection and network construction. Computational and Mathematical Methods in Medicine, 2016:1–11, 10 2016.

- [12] T.-T. Lu and S.-H. Shiou. Inverses of 2 × 2 block matrices. Computers & Mathematics with Applications, 43(1):119–129, 2002.

- [13] B. M. Pötscher and H. Leeb. On the distribution of penalized maximum likelihood estimators: The lasso, scad, and thresholding. Journal of Multivariate Analysis, 100(9):2065–2082, 2009.

- [14] R. Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), 58(1):267–288, 1996.

- [15] H. Zou and T. Hastie. Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 67(2):301–320, 2005.