remarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim \headersThe Price of Information S. Jaimungal, and X. Shi

The Price of Information ††thanks: February 17, 2024\fundingSJ would like to acknowledge support from the Natural Sciences and Engineering Research Council of Canada (RGPIN-2018-05705).

Abstract

When an investor is faced with the option to purchase additional information regarding an asset price, how much should she pay? To address this question, we solve for the indifference price of information in a setting where a trader maximizes her expected utility of terminal wealth over a finite time horizon. If she does not purchase the information, then she solves a partial information stochastic control problem, while, if she does purchase the information, then she pays a cost and receives partial information about the asset’s trajectory. We further demonstrate that when the investor can purchase the information at any stopping time prior to the end of the trading horizon, she chooses to do so at a deterministic time.

keywords:

Price of Information, Portfolio Maximization with Partial Information60G15, 91B24, 91B70, 93E11, 93E20

1 Introduction

When stock returns are predictable, the trading signal and the anticipation of future signals affect investor’s trading strategies [15, 19]. Without access to the trading signal, rational investors may still trade strategically by filtering the trading signal [1, 4, 10, 11] – i.e., treat the optimization problem as a partial information control problem. As an investor with full information always has higher utility than those without the full information [5, 11, 12], possessing information about the trading signal has a strictly positive value. The investor, therefore, has a maximum price that she is willing to pay to acquire this additional information.

Further, consider a group of informed traders who have access to partial information regarding the trading signal. Often there are regulatory constraints that prevent them from legally participating in the market. They can, however, form an information agency (IA) to “sell” some aspect of the trading signal that they possess to other investors. The maximum price an investor is willing to pay for this information may be viewed as the maximum price that the IA can sell the information to the investor.

In this article, we refer to this maximum price as the “indifference price”. In particular, the indifference price is the price that the investor is willing to pay such that their expected utility from optimally investing and filtering the trading signal (i.e., in the absence of the information) equals the expected utility from paying the indifference price, receiving the information, and then optimally trading with the information (i.e., in the presence of full information). Naturally, the investor will accept any price below the indifference price and will reject any price above the indifference price.

Our main goal is to address the question: how does an investor quantify the price of the trading signal? We show that, on a fixed trading horizon , an investor with constant absolute risk aversion (CARA) has two parameters that affect their indifference price: (i) the investor’s risk aversion coefficient and (ii) the signal-to-noise ratio (or more specifically, the signal-to-volatility ratio). Further, we investigate the question of timing: when should the investor subscribe to the trading signal (until the end of the time horizon)? We show that if the investor is allowed to choose a stopping time at which to subscribe to the trading signal (and keep her subscription to the terminal time ), then, somewhat surprisingly, the optimal stopping time is a deterministic stopping time.

The remainder of the paper is organized as follows. In Section 2, we develop a single-period model, derive the participating investor’s optimal informed and uninformed trading strategy, and obtain the closed form expression for the indifference price. In Section 3, we develop the continuous time analogue of the model, and once again determine the indifference price in closed form and derive a limiting subscription rate for subscribing to the information when the time horizon is large. Finally, we consider the optimal subscription time problem in Section 4. All proofs are found in Appendix A.

Throughout, we fix a filtered probability space supporting two independent standard Brownian motions, and , and being the trading horizon. We use to denote the collection of all processes adapted to the filtration generated by the process .

2 A Single-Period Model

We introduce the essential ideas in a single-period model.

2.1 Single-Period Model Setup

Suppose interest rates are zero, the initial price of a risky asset price is , and at time the risky asset’s price is

| (1) |

The investor knows the values of and they are constants. The increment of the stock price therefore consists of three parts: (i) a (deterministic) growth rate , (ii) a trading signal which the investor cannot observe, and (iii) a completely random part .

The investor begins with some initial wealth , and wishes to determine how much to invest in the risky asset. The investor can purchase the information from an IA that charges to provide her with the value of before the investor makes decisions. To be more precise, at time , the investor pays to the IA, and the investor chooses . That is is the investors decision variable corresponding to acquiring the information about or not. Conditional on the information the investor has, she chooses the position in the risky asset to maximize her exponential utility of the terminal wealth , i.e., she finds the maximizer of

| (2) |

where the initial and terminal wealth are

| (3) |

and the strategy is -measurable. When , the investor determines her strategy knowing , hence is -measurable. When , we have , which renders the -algebra trivial, the investor makes decisions without any information and her strategy is now .

2.2 Single-Period Indifference Price

We define the indifference price of the extra information as the price such that the investor’s expected utility is the same whether or not they purchase the information. To this end, we determine the investor’s optimal strategies and her value functions in both the uninformed (UI) and informed (I) cases, and report the indifference price in Theorem 2.1 – the proof may be found in Section A.1. That is, satisfies . Notice that is also the maximum price the investor is willing to pay for the information.

Theorem 2.1.

In the single-period model setting, the following statements hold:

-

1.

In the informed case, with purchasing information with price the optimal informed strategy is , and the optimal expected utility of the investor is

(4) -

2.

In the uninformed case, the optimal strategy is , and the optimal expected utility of the investor is

(5) -

3.

The indifferent price is

(6)

As long , then . The strict inequality stems from the trading signal being only one of the sources of randomness in the market, the other being . We can easily see that the indifference price is increasing in the signal-to-noise ratio . That is, the larger the variance of the trading signal compared to the variance of the stock price, the higher the value of the information. The other important parameter that appears in the indifference price is the investor’s risk aversion . To wit, the indifference price is proportional to the risk capacity – the reciprocal of the investor’s risk aversion .

3 A Tractable Continuous-Time Model

In the continuous-time version of the problem, the investor no longer naïvely chooses a static strategy at time , rather, she can filter the trading signal process based on the stock price. We next explicitly show how the information filtering is conducted, and develop an indifference price in the continuous-time setup.

3.1 Continuous-Time Model Setup

For the continuous-time analogue of (1), we consider the following hierarchical structure:

| (7) |

where the trading signal process satisfies the SDE

| (8) |

Here, the expected excess return , the volatility of the stock , and the volatility of the trading signal process are all treated as known constants to the public. There are two sources of randomness in the stock price dynamics: the Brownian motion that drives the price volatility, and the trading signal process , driven by an independent Brownian motion . The information regarding the value of the trading signal process is not publicly available, but can be purchased through an IA at time , and the charge is . Different from Kyle-type insider trading model [2, 3, 16], the IA only reveals the information of adaptively, i.e., at time , the IA only knows the historical value , but not any value of at times later than . Thus, we can view the IA as providing precision on the expected instantaneous return of the stock, rather than precision on the value of the stock at the end of the trading horizon.

As in the single-period model in Section 2, there is an investor who participates in the market but does not have access to the trading signal process . Starting with initial wealth at time 0, there are two options for the investor: (i) subscribe to the information from the IA regarding and make an informed decision (), or (ii) do not subscribe to the information and make decisions by filtering ().

If the investor purchases the information about , at each time , she can decide on a trading strategy based on the whole history of the stock price and the trading signal process . In this case, by setting , the admissible set of , denoted by , contains all processes adapted to the filtration generated by the stock price and the trading signal process. Contrastingly, if the investor chooses not to purchase the information on the process , at each time , she can only choose a trading strategy based only on the past information of the stock price . In this case, by setting , the admissible set of shrinks to , which contains processes adapted to the filtration generated by the stock price alone. In summary, based on the information she has, the investor maximizes her exponential utility of the terminal wealth , i.e., she aims to solve for the maximizer of

| (9) |

where the wealth process is

| (10) |

In this setting, our goal is to determine the indifference price of acquiring the information for the whole interval , which, similarly to the discrete-time problem in Section 2, requires solving the portfolio optimization problems in both the uninformed and informed cases.

3.2 Continuous-Time Indifference Price

Determining the price of information requires solving the portfolio optimization problem with partial information. The extant literature on the topic is vast, e.g., see [1, 4, 6, 8, 9, 10, 11, 21, 24, 22, 20], including numerical algorithms such as [17, 18, 25]. Closed form solutions, however, are limited.

In our setting, as the stock price and the factor process are jointly Gaussian, information filtering (see, e.g., [1, 5, 11, 13]) can be explicitly constructed. We summarize the key result in Lemma 3.1, and refer to Appendix A.2 for details.

Lemma 3.1.

Let denote the natural filtration generated by the stock price and denotes the filtered process, s.t., . Then

| (11) |

where is an -Brownian motion defined by

| (12) |

With the information filtering Lemma 3.1, particularly the explicit form of in (11), we can solve the informed and uninformed portfolio optimization problem (9) in closed form. The results are summarized in Theorem 3.2, and we refer to Appendix A.3 for its proof.

Theorem 3.2.

In the continuous-time setting in Section 3.1, the following statements hold:

-

1.

The optimal informed trading strategy is , and the optimal wealth follows (10) with . The investor’s value function is therefore

(13) -

2.

The optimal uninformed trading strategy (with filtering of the trading signal ) is , and the optimal wealth follows (10) with . The investor’s value function is therefore

(14) -

3.

The indifferent price is

(15)

As in the single-period setting in Section 2.2, the indifference price is proportional to the reciprocal of the investor’s risk aversion , and is monotonically increasing with respect to the signal-to-noise ratio . Moreover, if the trading horizon is large compared to the ratio , then the indifference price is approximately linear in . We term the ratio of the lhs to as the limiting subscription rate and denote it by ,i.e.,

| (16) |

We also note that, as long as , we have the inequality . This suggests that the IA charges the “noise ratio” , i.e. how large the volatility of the factor process is compared with the volatility of the stock price .

4 Best Time to Subscribe

The limiting subscription rate introduced in (16) is the rate the investor is willing to pay starting at time zero until the the end of the trading horizon – specifically, the decision is made once at the beginning of the trading horizon such that she is indifferent between purchasing the information or filtering the information. The investor may, however, wish to wait and purchase the information only at a later point in time. To this end, let denote the subscription rate set by the IA for receiving information at time . The relationship of the subscription rate and the one-time price in Section 3 is given by . Notably, this rate is assumed to be deterministic and does not depend on the stock price or the trading signal – if it did depend, e.g., on , then the rate itself reveals and hence the investor would not purchase the information and instead simply query the price of the information.

With given subscription rate , the investor’s optimization problem is to find the optimal time at which to purchase the information, and the admissible trading strategy , where the process is defined as . That is, (i) for all , the investor filters and optimal trades based on the filtered process; (ii) for all , she is subscribed to the information feed, and receives information about , and thus has no need to filter it. To define the optimization problem, let denote the collection of all -stopping times, the investor aims to find the maximizer of

| (17) |

where the wealth follows

| (18) |

Next, we prove that the optimal time to subscribe is not necessarily unique and that when it is unique, the optimal time is deterministic. When it is not unique, any time in the interval satisfying , where and are deterministic, is equally optimal. The deterministic time is defined111Here, if there is no that satisfies the strict inequality in (19), without loss of generality we set . as

| (19) |

where is the constant subscription rate induced by the indifference price in Theorem 3.2 and given by (16) and . Further, the deterministic time is defined as

| (20) |

We then have the following Proposition 4.1, and refer to Appendix A.4 for its proof.

Proposition 4.1.

The following statements hold:

-

1.

Suppose the IA charges the rate , then the optimal time for the investor to start the subscription is any such that . If the IA charges the constant limiting subscription rate given by (16), then , and the optimal time is unique.

-

2.

The indifference subscription rate with is

(21)

5 Example

In this section, we provide an illustrative example of the ideas that we develop. To do so, we make the following model parameter assumptions:

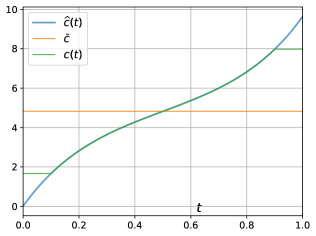

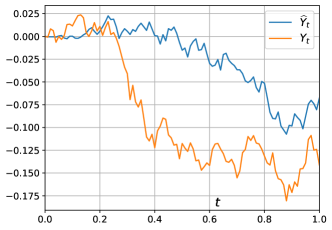

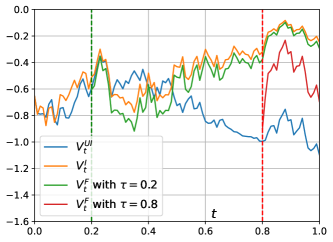

Using these parameters we obtain the indifference subscription rate shown in Figure 3. We further include the limiting subscription rate and introduce a prescribed subscription rate shown in green in the figure. As the prescribed subscription rate lies above the indifference rate prior to , it is never optimal for the investor to subscribe early than . Similarly, as the prescribed subscription rate lies below the indifference price after , it is optimal for the investor to susbcribe no later than . The investor can subscribe at any time between and with equal value. In Figure 2, we show a sample path of the true and filtered signals and , respectively. In tandem, Figure 3 shows the corresponding sample paths of the value functions without subscribing and with subscribing at different times.

Acknowledgments

We would like to acknowledge fruitful discussions with Paolo Guasoni, Mike Ludkovski, and Zhi Li.

References

- [1] A. Al-Aradi and S. Jaimungal, Outperformance and tracking: Dynamic asset allocation for active and passive portfolio management, Applied Mathematical Finance, 25 (2018), pp. 268–294.

- [2] J. Amendinger, P. Imkeller, and M. Schweizer, Additional logarithmic utility of an insider, Stochastic processes and their applications, 75 (1998), pp. 263–286.

- [3] S. Banerjee and B. Breon-Drish, Strategic trading and unobservable information acquisition, Journal of Financial Economics, 138 (2020), pp. 458–482.

- [4] V. E. Beneš and I. Karatzas, Estimation and control for linear, partially observable systems with non-gaussian initial distribution, Stochastic Processes and their Applications, 14 (1983), pp. 233–248.

- [5] S. Brendle, Portfolio selection under incomplete information, Stochastic processes and their Applications, 116 (2006), pp. 701–723.

- [6] P. Casgrain and S. Jaimungal, Trading algorithms with learning in latent alpha models, Mathematical Finance, 29 (2019), pp. 735–772.

- [7] C. Chicone, Ordinary differential equations with applications, vol. 34, Springer Science & Business Media, 2006.

- [8] J. Cvitanić, A. Lazrak, L. Martellini, and F. Zapatero, Dynamic portfolio choice with parameter uncertainty and the economic value of analysts’ recommendations, The Review of Financial Studies, 19 (2006), pp. 1113–1156.

- [9] J. B. Detemple, Asset pricing in a production economy with incomplete information, The Journal of Finance, 41 (1986), pp. 383–391.

- [10] J.-P. Fouque, A. Papanicolaou, and R. Sircar, Filtering and portfolio optimization with stochastic unobserved drift in asset returns, Communications in Mathematical Sciences, 13 (2015), pp. 935–953.

- [11] P. Guasoni, Asymmetric information in fads models, Finance and Stochastics, 10 (2006), pp. 159–177.

- [12] P. Guasoni, A. Tolomeo, and G. Wang, Should commodity investors follow commodities’ prices?, SIAM Journal on Financial Mathematics, 10 (2019), pp. 466–490.

- [13] M. Hitsuda, Representation of Gaussian processes equivalent to Wiener process, Osaka J. Math., (1968).

- [14] I. Karatzas and S. Shreve, Brownian motion and stochastic calculus, vol. 113, Springer Science & Business Media, 2012.

- [15] T. S. Kim and E. Omberg, Dynamic nonmyopic portfolio behavior, The Review of Financial Studies, 9 (1996), pp. 141–161.

- [16] A. S. Kyle, Continuous auctions and insider trading, Econometrica, 53 (1985), pp. 1315–1335.

- [17] M. Ludkovski, A simulation approach to optimal stopping under partial information, Stochastic processes and their applications, 119 (2009), pp. 4061–4087.

- [18] M. Ludkovski and S. O. Sezer, Finite horizon decision timing with partially observable poisson processes, Stochastic Models, 28 (2012), pp. 207–247.

- [19] R. C. Merton, Optimum consumption and portfolio rules in a continuous-time model, in Stochastic optimization models in finance, Elsevier, 1975, pp. 621–661.

- [20] A. Papanicolaou, Backward sdes for control with partial information, Mathematical Finance, 29 (2019), pp. 208–248.

- [21] I. Pikovsky and I. Karatzas, Anticipative portfolio optimization, Advances in Applied Probability, 28 (1996), pp. 1095–1122.

- [22] U. Rieder and N. Bäuerle, Portfolio optimization with unobservable markov-modulated drift process, Journal of Applied Probability, 42 (2005), pp. 362–378.

- [23] L. A. Shepp, Radon-nikodym derivatives of gaussian measures, The Annals of Mathematical Statistics, (1966), pp. 321–354.

- [24] Y. Xia, Learning about predictability: The effects of parameter uncertainty on dynamic asset allocation, The Journal of Finance, 56 (2001), pp. 205–246.

- [25] J. Yang, L. Zhang, N. Chen, R. Gao, and M. Hu, Decision-making with side information: A causal transport robust approach.

Appendix A Proofs

To ease notation, we define and recall that .

A.1 Proof of Theorem 2.1

Proof A.1.

We solve the optimization problem with and without purchasing the information.

Informed case

In the informed case, the investor chooses to purchase the information, hence over -measurable , she optimizes , which yields and by the characteristic function of , we have (4).

Uninformed case

In the uninformed case, the investor does not purchase the information, and hence over deterministic she maximizes . Therefore, the (deterministic) optimal strategy is and we have (5).

The investor is indifferent to the two options whenever and solving for provides us with (6).

A.2 Proof of Lemma 3.1

Proof A.2.

In this proof 222There are multiple ways to obtain the representation. Here we just present one relatively easy way. , we use to denote the separable Hilbert spaces of real-valued, square-integrable functions; two functions are considered equal if they coincide almost everywhere. Using Fokker–Planck equation, we can verify that are jointly Gaussian processes. In particular, is a mean zero Gaussian process with covariance function , . By checking the conditions in [23, Theorem 1], and by [13, Proposition 2], there exists a unique Brownian motion and a unique kernel such that

| (22) |

Here, the kernel satisfies the following integral equation:

and following similar arguments as in [11, Section 5], can be calculated explicitly as

| (23) |

Recall that for the filtration generated by the stock price, we define the projection Hence, by the uniqueness of supported by , comparison of the dynamic of from (7) and (22) yields (11) and (12) in Lemma 3.1.

A.3 Proof of Theorem 3.2

Proof A.3.

We solve the optimization problem in both the informed and uninformed cases.

Informed Case

In the informed case, at time 0, the investor pays to acquire the full information of on the trading interval and, hence, has admissible strategies . The investor’s wealth at time is thus given by (10), and her goal is to choose to maximize (9) with . The corresponding value function is defined as . Standard arguments suggest that satisfies the HJB equation:

| (24) |

with terminal condition . Point-wise optimization yields the optimal controls in feedback form . Making the ansatz that , and substituting into the HJB equation (24), we find satisfies the following ODEs:

with terminal conditions . Solving this system of ODEs, we obtain that

Accordingly, , and the value function is (1). By Corollary 5.14 in[14, Chapter 3], the value function is a true martingale.

Uninformed Case

Now let’s assume the investor does not purchase the full information but filters it from . By Lemma 3.1, using the filtered signal process from (11) and the Brownian motion from (12) under the restricted filtration , we can re-write the stock price dynamic as . As before, for wealth follows (10) with , the value function associated with the problem (9) is defined as From standard analysis, satisfies the HJB equation (where we write instead of ):

| (25) |

subject to the terminal condition . Point-wise optimization provides the optimal controls in feedback form: . Making a similar ansatz as before , and substituting into the HJB equation above, we find satisfies the following ODEs:

subject to . Solving the ODEs yields

| (26) | ||||

| (27) |

and the value function in the uninformed case is therefore (2), with the optimal (filtering) strategy given by the expression stated in Theorem 3.2. By Corollary 5.14 in [14, Chapter 3], the value function is a true martingale.

A.4 Proof of Proposition 4.1

Proof A.4.

First we investigate the value function once information has been purchased. If the investor purchases the information at time , then from the wealth dynamic (18) and a similar procedure to derive the informed value function (1), we have

The expectation of the informed value function just prior to acquiring the information is

| (28) |

where . The second equality follows from using the value function in (2) and the deterministic function in (27).

Next, we show that in (19) is an upper bound on the time at which the investor is indifferent to purchasing the information feed. To this end, if the investor purchases information at , then she uses an uninformed strategy on (with filtering to obtain ) and uses an informed strategy on (with knowledge of ). As is a true -martingale (by (2)), we have

| (29) |

The investor will not purchase the information later than if , . Comparing (28) and (29) and plugging in the expression for from (27), this means

| (30) |

Thus, with defined in (16), we introduce the ‘latest subscription time’ of a subscription rate in (19). If , suppose the investor decides to purchase the information at time , where is a stopping time in , we can infer the strict inequality (30) holds if . Therefore, if , then , the investor will immediately purchase the information at . By the definition of , there exists such that

which makes given in (20) well defined.

As we have demonstrated that is an upper bound on the optimal stopping time, we focus now on the shortened interval . Let denote the investor’s value function who can choose the purchasing time on for the information. In the continuation region, satisfies

Point-wise optimization yields the optimal controls in feedback form in the continuation region Standard arguments imply that satisfies the quasi-variational inequality on :

| (31) |

When , it is optimal for the investor to purchase the information. We make the ansatz , where is given by (26). Substituting this ansatz into the quasi-variational inequality (31), we obtain a quasi-variational inequality for on :

With and given by (26) and (21), respectively, using a comparison argument (cf., e.g., [7]), the unique solution to this variational ODE is

| (32) |

It is optimal for the investor to make the purchase at time whenever . Using the above expression and the form of and , is deterministic

| (33) |

There may be multiple satisfying (33), i.e., at which the investor is indifferent in entering into the subscription. Among them, the earliest time is given by (20).

We turn to two special cases that demonstrate that and are not necessarily equal.

Special case with by (16)

In this case, as is strictly positive on and strictly negative on , we have that

Notice that for , . Hence for the limiting subscription rate in (16), the investor purchases the information subscription at time .

Special case with by (21)

In this case, the term under the integral in the expression for is identically zero, hence . By definition, we have . Moreover, on we have that

and, therefore, the investor is indifferent between purchasing the information subscription or trading with the information of the stock over the whole time period, hence the earliest time to make the purchase is therefore .