longtable \setkeysGinwidth=\Gin@nat@width,height=\Gin@nat@height,keepaspectratio

Spatial Data Analysis

Abstract

This handbook chapter provides an essential introduction to the field of spatial econometrics, offering a comprehensive overview of techniques and methodologies for analysing spatial data in the social sciences. Spatial econometrics addresses the unique challenges posed by spatially dependent observations, where spatial relationships among data points can significantly impact statistical analyses. The chapter begins by exploring the fundamental concepts of spatial dependence and spatial autocorrelation, and highlighting their implications for traditional econometric models. It then introduces a range of spatial econometric models, particularly spatial lag, spatial error, and spatial lag of X models, illustrating how these models accommodate spatial relationships and yield accurate and insightful results about the underlying spatial processes. The chapter provides an intuitive understanding of these models compare to each other. A practical example on London house prices demonstrates the application of spatial econometrics, emphasising its relevance in uncovering hidden spatial patterns, addressing endogeneity, and providing robust estimates in the presence of spatial dependence.

Keywords: Spatial Econometrics, Spatial Data Analysis, Spatial Dependence, Spatial Spillovers, London House Prices, Handbook

1 Introduction

The availability of spatial data for social sciences has rapidly increased over the past decade. Various spatial packages have been implemented in standard statistical software and have steadily been updated (Bivand 2022) in addition to already existing software in Geo-Information Systems (GIS) such as ArcGIS or QGIS. At the same time, many empirical social science papers investigate research questions with an explicit spatial focus. Examples of spatial topics in the social sciences include labour market dynamics (Martén et al. 2019, Nisic 2017, Zoch 2021), processes of residential segregation (Roberto 2018, Tóth et al. 2021) and gentrification (Fransham 2020, Zapatka & Beck 2021), the spatial distribution of environmental goods or bads (Boillat et al. 2022, Jünger 2022, Rüttenauer 2018), the consequences of extreme weather events (Ogunbode et al. 2019, Hoffmann et al. 2022, Rüttenauer 2023) or the access to infrastructural conditions (Moreno-Monroy et al. 2018, Liao et al. 2020, Wiedner et al. 2022).

In general, spatial data is structured like conventional data (e.g. a dataset with variables), but has one additional dimension: every observation is linked to some geo-spatial information. Most common types of spatial information are points, lines, or polygons (vector data) or raster data. Similar to the time dimension in panel data, this adds an additional layer of information and connectivity between units. As with panel data, we could thus proceed as if we had conventional data and ignore the spatial dimension. This comes however with two distinct problems. First, we waste potentially interesting information, that may help us to understand the underlying social processes. Second, we will end up with biased inferential statistics and biased point estimates in some cases if we ignore the underlying spatial dependence.

There are various techniques to model spatial dependence and spatial processes (LeSage & Pace 2009). Here, we will cover the most common spatial econometric models. Generally, spatial regression models make some assumptions about the source of spatial dependence observed in the data and then account for this dependence in the specified model. What makes spatial regression models more complicated than panel models is the ambiguous direction and circular nature of the dependence. I may influence my neighbour, but my neighbour may also influence me (interdependence). Moreover, if someone influences a third neighbour, they may be neighbours of my neighbour – 2nd order neighbour of me – which will then influence me as well (diffusion). However, we may also not influence each other at all but just be affected by the same exogenous shock, thus making our observed values more similar (common confounding).

The chapter proceeds as follows. First, we will briefly introduce the concept of spatial connectivity and spatial dependence and clarify why conventional regression techniques may fail with spatial dependence. We will then provide an overview of the most common spatial regression models. In a further step, we will demonstrate how to interpret summary measures of the coefficients of these models, which becomes more complicated in the case of spatial interdependence. Lastly, we use the relation between neighbourhood characteristics and house prices in London as an applied example.

2 Spatial weights

Given the geographical information of spatial data (i.e. the location of each unit), we can form relationships between units: which units are closer or further away from each other. Similar to network analysis, we have to set up a measure that defines which units are connected to each other and how they are connected (e.g. the magnitude of connectivity). There are some obvious measures that can be used to define these relations with spatial data: adjacency and proximity.

The connectivity between units is usually represented in a matrix denoted . The spatial weights matrix is an dimensional matrix, where each element of this matrix specifies the relation or connectivity between each pair of units and .

| (1) |

In the example above, describes the relationship between unit 3 and unit 1, while describes how unit 2 and unit are connected. The diagonal elements of are always zero: no unit is a neighbour of itself. This is not true for spatial multiplier matrices (as we will see later). Contiguity weights are a very common type of spatial weights. This is a binary specification, taking the value 1 for neighbouring units (queens: sharing a common edge; rook: sharing a common border), and 0 otherwise. See for instance Pebesma & Bivand (2023) for more detailed information about spatial relations.

Contiguity weights matrices are usually sparse matrices and keep relations relatively simple and easy to interpret. However, they often create island, i.e. units without any neighbours, which can be problematic for spatial regression models. Another common type of connectivity measures is distance based weights. For instance, inverse distance weights assign higher weights to more proximate units , where distance is usually discounted by a spatial decay factor . Often is it recommended to specify a distance threshold (e.g. 100km) to get rid of very small non-zero weights for very distant units. There is an ongoing debate about the importance of spatial weights for spatial econometrics and about the right way of specifying weights matrices (LeSage & Pace 2014, Neumayer & Plümper 2016).

2.1 Normalization

Normalizing ensures that the parameter space of the spatial multiplier in regression models is restricted to , and the multiplier matrix is non-singular (more on this later). The important message is: normalizing the weights matrix is always a good idea. Otherwise, the spatial parameters may blow up – if they can be estimated at all. Normalising also ensures an easy interpretation of spillover effects (as we see later). Again, how to normalize a weights matrix is subject of debate (LeSage & Pace 2014, Neumayer & Plümper 2016).

Row-normalization divides each non-zero weight by the sum of all weights of unit , which is the sum of the row : . With contiguity weights and row-normalisation, spatially lagged variables contain the mean of the respective variable among the neighbours of . However, proportions between units such as distances get lost due to row-normalisation, which can be bad if one is theoretically interested in using inverse-distance based weights. It also induces asymmetries, as different units have different numb of neighbours: .

Another common way of standardization is maximum eigenvalues normalization. Maximum eigenvalues normalization divides each non-zero weight by the overall maximum eigenvalue of the entire matrix : . Each element of is divided by the same scalar value, which preserves the relations. It keeps proportions of connectivity strengths across rows, which is relevant for distance based . I thus recommend maximum eigenvalues normalization for distance based neighbours weights. However, interpretation may become more complicated.

2.2 Spatial dependence

‘Everything is related to everything else, but near things are more related than distant things’ (Tobler 1970). Tobler’s first law of geography has been used extensively (11,584 citation in 2023-06) to describe spatial dependence. In practical term, this means that close observations are more likely to exhibit similar values on some of their characteristics, and we cannot handle observations as if they were independent.

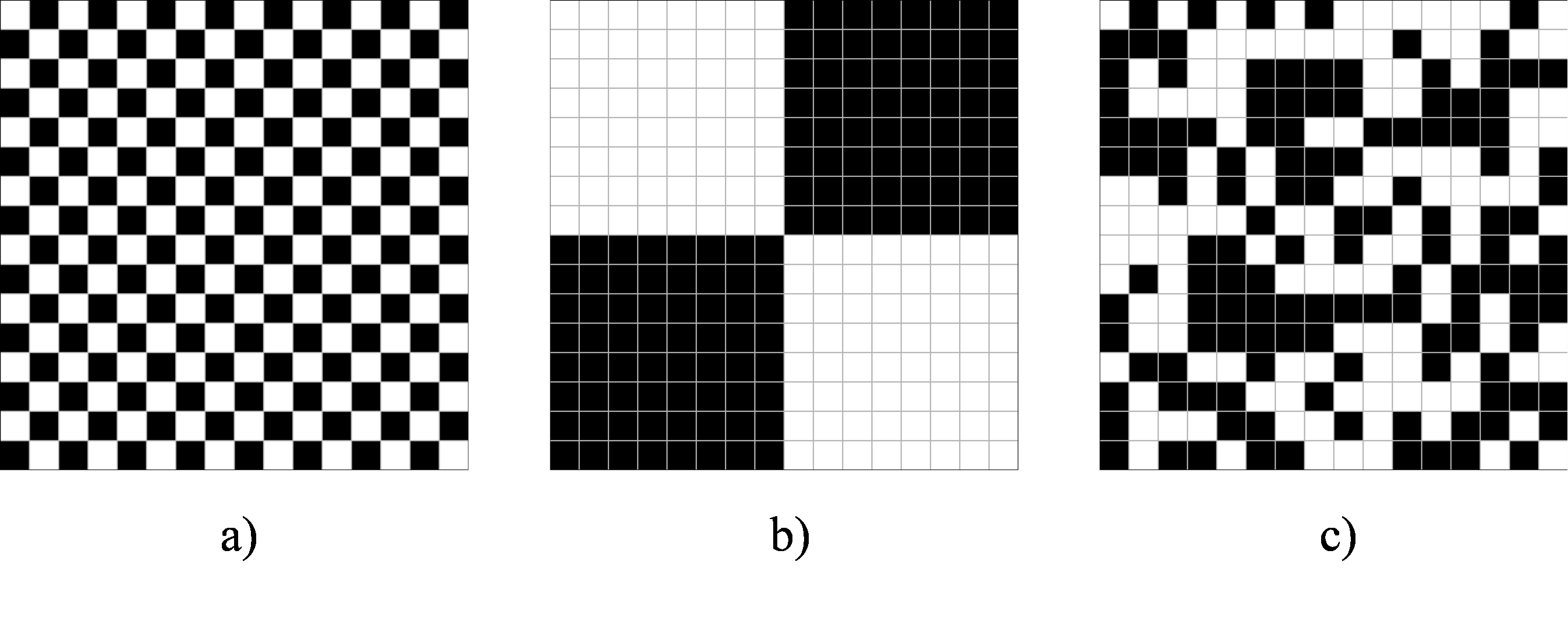

There is a very easy and intuitive way of detecting spatial autocorrelation: look at the map. Below we can see three distinct patterns. Figure Figure 1 a) has perfect negative auto-correlation. Every black unit is surrounded by white units, and every white unit is surrounded by black units. Figure Figure 1 b) has very strong positive autocorrelation. Most white units are surrounded only by white units, and most black units are surrounded by only black units. Figure Figure 1 c), by contrast, is generated by a random process, although even here one is inclined to observe some degree of clustering.

Would our interpretation be the same if we aggregate the data to four larger areas / districts using the average within each of the four districts? We would actually draw very different conclusions. It is thus important to keep in mind that spatial dependence is a also a result of spatial boundaries and potential higher-level processes generating an outcome (Wong 2009). If a variable was measured on the district level and we assign those district-level measures to the lower neighborhood level, we will artificially introduce spatial dependence / clustering in our data.

Given our spatial data, we can use various statistical measures to test whether there is spatial dependence. The most common statistic for spatial dependence or autocorrelation is Moran’s I, which goes back to Moran (1950) and Cliff & Ord (1972). For more extensive materials on Moran’s I see for instance Kelejian & Piras (2017), Chapter 11. We first define a neighbours weights matrix , and the Global Moran’s I test statistic is calculated as

| (2) |

In the case of row-standardized weights, . Moran’s measures the correlation between neighbouring values: how does my correlated with the average of my neighbours? Negative values indicate negative autocorrelation, values around zero (not zero exactly) indicate no autocorrelation, and positive values indicate positive autocorrelation. Moran’s can also be calculated for the residuals from an estimated model (e.g. non-spatial OLS), which allows to test for remaining autocorrelation after accounting for potential confounders.

3 Bias in non-spatial OLS

So, why should we care about spatial dependence? First, spatial dependence violates standard assumptions of common non-spatial estimators. Second, spatial dependence itself can provide important information about the social processes that generated the data we observe.

Let us start with a linear model in the non-spatial setting. Here, is the outcome or dependent variable (), are various exogenous covariates (), and () is the error term. We are usually interested in an estimate for the coefficient vector .

The work-horse for estimating in the social science is the OLS estimator (Wooldridge 2010), which is given by the form:

This OLS estimator hinges on a few assumptions, among them that the underlying sample observations are independent and identically distributed (i.i.d). This assumption is often violated with spatial data. Another (more important) assumptions is the absence of any omitted (residual) variables that are related to and : . This assumption is violated when our neighbours’ characteristics influence our covariates and our outcome.

So, does spatial dependence allways induce bias in non-spatial estimators? No, the best answer is: it depends (Betz et al. 2020, Cook et al. 2020, Pace & LeSage 2010, Rüttenauer 2022). The easiest way to think of it is analogous to the well-kown omitted variable bias (Betz et al. 2020, Cook et al. 2020):

where is some omit variable, and is the conditional effect of on . Now imagine that the neighbouring values of the dependent variable are autocorrelated to focal unit which we denote with , and that the covariance between the focal unit’s exogenous covariate and is not zero (my covariate correlates with my neighbours’ outcome). Then we will have an omitted variable bias due to spatial dependence:

4 Spatial Regression Models

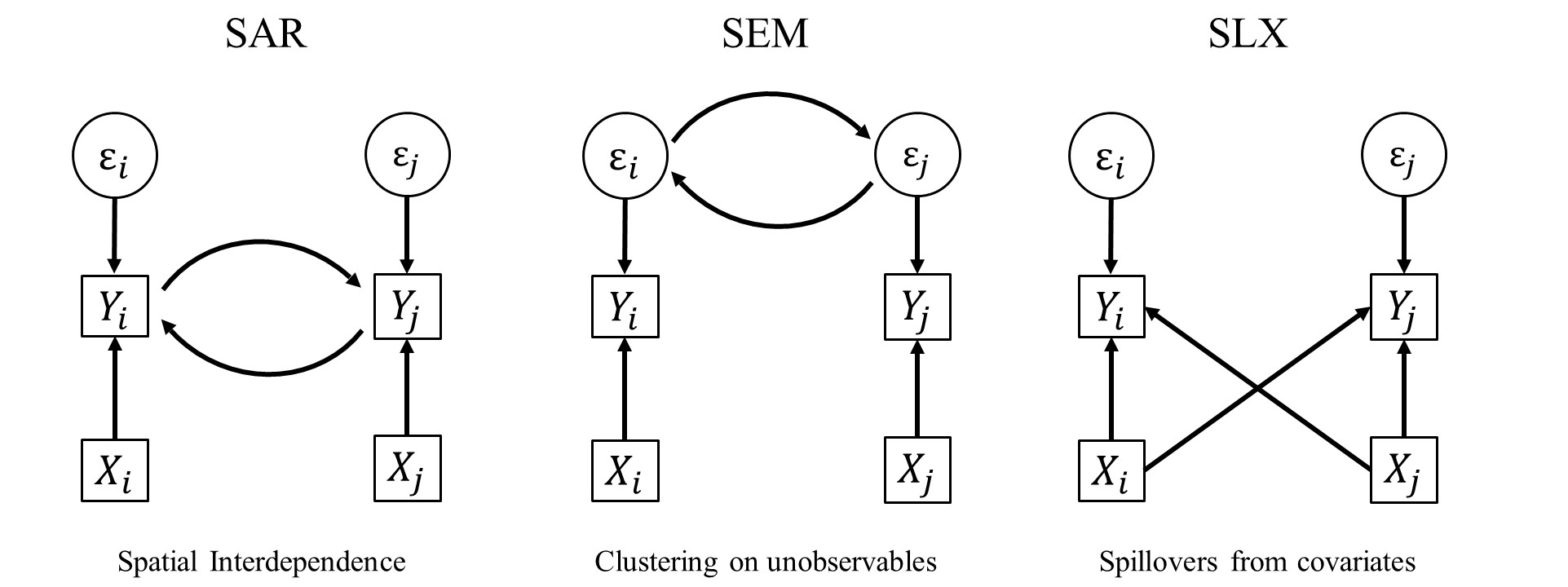

Spatial regression models do not only overcome the potential bias, they also help us to understand the spatial processes happening in the underlying data. Broadly, spatial dependence in some characteristics can be the result of three different processes: a) Spatial interdependence, b) Clustering in unobservables, and c) Spillovers from covariates. As shown in Figure Figure 2, there are three basic ways of incorporating spatial dependence: the Spatial Autoregressive Model (SAR) accounts for spatial interdependence, the Spatial Error Model (SEM) for clustering on unobservables, and the Spatially lagged X Model (SLX) for spillovers from covariates. Moreover, they can be further combined. As before, the spatial weights matrix defines the spatial relationship between units.

4.1 Spatial Autoregressive Model (SAR)

The Spatial Autoregressive Model (SAR) model is by far the most prominent spatial specification. It assumes spatial interdependence in the outcome and incorporates this interdependence in the model:

| (3) |

Here, denotes the strength of the spatial correlation in the dependent variable (spatial autocorrelation): your outcome influences my outcome (: positive spatial dependence, : negative spatial dependence, : traditional OLS model). Given that we have normalised the weights matrix, is defined in the range of .

4.2 Spatial Error Model (SEM)

A second, also very common spatial model is the Spatial Error Model (SEM). It assumes Clustering on unobservables, and thus models spatial interdependence in the error term:

| (4) |

In this case, denotes the strength of the spatial correlation in the errors of the model: your error influences my errors (: positive error dependence, : negative error dependence, : traditional OLS model). Again, is defined in the range of .

4.3 Spatially lagged X Model (SLX)

A third spatial model is called Spatially lagged X Model (SLX). It assumes spillovers in the covariates. It specifies a relationship between the covariate values of neighbours and the outcome of the focal unit:

| (5) |

In the SLX, denotes the strength of the spatial spillover effects from covariate(s) on the dependent variable: your covariates influence my outcome. In contrast to the previous two specifications, is defined like any other coefficient from a conventional covariate. It is thus not bound to any range, and its scale depends on the scale of the covariates in .

The dependence structure assumed in SAR and SEM has a circular element (see Figure Figure 2). In A SAR model, my outcome influences my neighbours’ outcome, which then again influences my outcome. In A SEM model, my error term influences my neighbours’ error term, which then again influences my error term. This also means that SAR and SEM models cannot be estimate by conventional OLS estimators, as they would suffer from simultaneity bias in the spatial autoregressive term:

| (6) |

with defined as the th element of the spatial lag operator . It can further be shown that the second part of the equation , which demonstrates that OLS would provide a biased estimate of (Franzese & Hays 2007, Sarrias 2023).

A potential way of estimating SAR-like models is an instrumental variable approach with 2SLS, where the autoregressive term is instrumented by spatial lags of (Kelejian & Prucha 1998). SEM-like models can be estimated using Generalized Method of Moments (Kelejian & Prucha 1999). However, given the improvements in computational power, it is now common to rely on Maximum Likelihood estimation of spatial models (Ord 1975, Anselin 1988). They start with some auxiliary regression to obtain initial estimates, and then update them in further steps. For more details see Bivand & Piras (2015), LeSage & Pace (2009), and Sarrias (2023). The package spatialreg (Bivand & Piras 2015, Bivand et al. 2021, Pebesma & Bivand 2023) provides a series of functions to calculate the ML estimators for all spatial models consider here.

Moreover, there are models combining two sets of the above specifications.

4.4 Spatial Durbin Model (SDM)

The spatial Spatial Durbin Model (SDM) integrates spatial interdependence in the outcome and spatial spillovers in covariates by combining SAR and SLX:

| (7) |

4.5 Spatial Durbin Error Model (SDEM)

The Spatial Durbin Error Model (SDEM) model integrates clustering on unobservables and spillovers in covariates by combining SEM and SLX:

| (8) |

4.6 Combined Spatial Autocorrelation Model (SAC)

The Combined Spatial Autocorrelation Model (SAC) assumes spatial interdependence in the outcome and clustering on unobservables to be present at the same time. It combines SAR and SEM:

| (9) |

The SAC specification has demonstrated a rather poor performance in Monte Carlo simulations (Rüttenauer 2022). Moreover, it has been argued that the SAC specification has severe theoretical drawbacks in applied research, and that its popularity (among econometricians) mainly stems from the fact that it constitutes an interesting estimation problem (LeSage 2014).

4.7 General Nesting Spatial Model (GNS)

Finally, the General Nesting Spatial Model (GNS) nests all three processes: spatial interdependence, clustering on unobservables, and spillovers in covariates. It can be written as a full combination of SAR, SEM, and SLX:

| (10) |

One could be inclined to think that the General Nesting Spatial Model is superior compared to the more restricted models with two or one source of spatial dependence. However, in practice the GNS is rather useless as an estimation model, as it is only weakly identifiable at best (Gibbons & Overman 2012). This is analogous to Manski’s reflection problem on neighbourhood effects (Manski 1993): if people in the same group behave similarly, this can be because a) imitating behaviour of the group (), b) members of the same group are exposed to the same external circumstances (), and c) exogenous characteristics of the group members () influence the behaviour. We just cannot separate those in observational data.

All of the models above assume different data generating processes (DGP) leading to the observed spatial pattern. Although there are specifications tests, it is generally not possible to let the data decide which one is the true underlying DGP (Cook et al. 2020, Rüttenauer 2022). There may however be theoretical reasons to guide the model specification (Cook et al. 2020). SAR is the most commonly used model, but it is definitely not the best choice in many applications. Various studies (Halleck Vega & Elhorst 2015, Rüttenauer 2022, Wimpy et al. 2021) highlight the advantages of the relative simple SLX model. Moreover, this specification can be incorporated in any other statistical method, such as non-linear estimators or machine learning algorithms.

Note that missing values create a problem in spatial data analysis. For instance, in a local spillover model with an average of 10 neighbours, two initial missing values will lead to 20 missing values in the spatially lagged variable. For global spillover models, one initial missing will diffuse through the neighbourhood system until the cut-off point (and create an excess amount of missings). Depending on the data, units with missings can either be dropped and omitted from the initial weights creation, or we need to impute the data first, e.g. using interpolation or Kriging. Similarly, islands (i.e units without neighbours) create problems in the estimation procedure. If this is a very small number of observations, they can be dropped. Otherwise, distance or k-nearest neighbours may be alternative options for that circumvent this problem.

5 Spatial Impacts

As shown in Figure Figure 2, models withe a SAR-like process have a feedback loop in the outcome: if my influences my , this change in my will influence my neighbour’s , which will influence their neighbours’ and also my own again (I am second order neighbour of my neighbour). We thus cannot interpret coefficients as marginal or partial effects in SAR, SAC, and SDM (Anselin 2003, LeSage & Pace 2009, Kelejian & Piras 2017). This is similar to auto-regressive time-series models where we have a long-term effects due a one unit change in . We thus differentiate between the effects in SAR-like models and those in models without an auto-regressive (endogenous) outcome term: while SAR, SAC, and SDM assume global spatial dependence, SLX and SDEM assume local spatial dependence (Anselin 2003, Halleck Vega & Elhorst 2015, LeSage & Pace 2009).111Note that SEM assumes no spatial effects, as all the spatial dependences comes from nuisance Consequently, also interpretation of the coefficients differs between models with endogenous feedback loops and those with only local spillovers.

5.1 Global spillovers

To see the meaning of marginal effects in SAR-like models, we have to consider its reduced form:

| (11) |

where is an diagonal matrix (diagonal elements equal 1, 0 otherwise). If interpreting regression results, we are usually interested in marginal or partial effects (the association between a unit change in and ). We obtain these effects by looking at the first derivative. When taking the first derivative of the explanatory variable from the reduced form in (11) to interpret the partial effect of a unit change in variable on , we receive

for each covariate . The partial derivative with respect to produces an matrix, thereby representing the partial effect of each unit onto the focal unit itself and all other units . The dimensional term is also called spatial multiplier matrix. Intuitively, this multiplier matrix equals as a power series:222A power series of converges to if the maximum absolute eigenvalue of , which is ensured by standardizing .

| (12) |

where the identity matrix contains the direct effects and the sum represents the first and higher order indirect effects, including the feedback loops. It implies that a change in one unit does not only affect the direct neighbours but passes through the whole system towards higher-order neighbours, where the impact declines with distance within the neighbouring system. Global indirect impacts thus are ‘multiplied’ by influencing a) direct neighbours as specified in and b) indirect neighbours not connected according to , with c) additional feedback loops between those neighbours.

Consider a minimal example with 5 observations, and assume the weights matrix and its row-normalised version look as follows:

| (13) |

Assume that we have relatively strong spatial interdependence with . If we want to get the total effect of on , we need to combine the direct effects on the diagonal and the indirect effects on the off-diagonal.

| (14) |

Finally, we take the inverse and calculate the spatial multiplier matrix

| (15) |

The multiplier matrix has diagonal elements : these include direct effects and also feedback loops, which amplify the direct impact: my influences my directly, but my then influences my neighbour’s , which then influences my again (and other neighbour’s s). The influence of my on my includes a spatial multiplier effect. To get the partial effect of a change in , we need to multiply the coefficient estimate from the SAR model model with the spatial multiplier matrix. Assume we have , then the partial effect is given by matrix

| (16) |

The partial effects matrix contains the effect of each unit on itself on the diagonal (including feedback loops) and the effect on each other unit on the off-diagonal. In theory, tells us that a one-unit change of in observation 1 correlates with a unit change in the outcome of observation 3. The th row of the matrix represent the impacts on individual observation , whereas the th column contains the impacts from an individual observation (Anselin 2003, LeSage & Pace 2009, LeSage 2014). However, the variation across these individual effects depends foremost on the weights matrix . They are not individual estimates, and it is advisable to not interpret these individual effects, but rather refer to their summary measures (see below).

Substantively Interpreting these global spillover effects can be a bit tricky. The global spillover effects can be understood as a diffusion process. For example, an exogenous event may increase the house prices in one district of a city, thus leading to an adaptation of house prices in neighbouring districts, which then leads to further adaptations in other units (the neighbours of the neighbours), thereby globally diffusing the effect of the exogenous event due to the endogenous lag of term. Yet, those processes happen over time. In a cross-sectional framework, Anselin (2003) proposes an interpretation as an equilibrium outcome, where the partial impact represents an estimate of how this long-run equilibrium would change due to a change in (LeSage 2014).

5.2 Local spillovers

In contrast, the the spatial spillover effects of SLX and SDEM are local spillover effects. They can be interpreted as the effect of a one unit change of in the spatially weighted neighbouring observations on the dependent variable of the focal unit. It is the effect of the weighted average value among neighbours. When using a row-normalised contiguity weights matrix, is the simple mean of in the neighbouring units.

Assume we have covariates, then

| (17) |

Only direct neighbours – as defined in – contribute to those local spillover effects. The coefficients only estimate how my direct neighbour’s values influence my own outcome . There are no higher order neighbours involved as long as we do not explicitly specify such higher order processes, nor are there any feedback loops due to interdependence.

In consequence, local and global spillover effects represent two distinct kinds of spatial spillover effects (LeSage 2014). The interpretation of local spillover effects is straightforward: it is the effect of a change in among local neighbours on the outcome of the focal unit . Global spillover effects are a bit more complicated: it is the effect that a change in one unit has on the entire system of neighbours, bringing on a new equilibrium outcome.

5.3 Summary measures

Marginal or partial effects in SAR-like models are given by an matrix of effects. However, since reporting the individual partial effects is usually not of interest, LeSage & Pace (2009) proposed to average over these effect matrices. While the average diagonal elements of the effects matrix represent the so called direct impacts of variable , the average column-sums of the off-diagonal elements represent the so called indirect impacts (or spatial spillover effects).

| Model | Direct Impacts | Indirect Impacts | type |

|---|---|---|---|

| OLS/SEM | – | – | |

| SAR/SAC | Diagonal elements of | Off-diagonal elements of | global |

| SLX/SDEM | local | ||

| SDM | Diagonal elements of | Off-diagonal elements of | global |

Note that impacts in SAR and SAC are bound to a common ratio between direct and indirect impacts. SAR and SAC models only estimate one single spatial multiplier coefficient. Thus direct and indirect impacts are bound to a common ratio, say , across all covariates: if , then , . For specifications including a lagged version of , in contrast, we estimate a local spatial effect for each unique covariate, plus an additional spatial multiplier in case of an SDM. SLX-like specification are thus much more flexible. Usually, impact measures come with simulation based inferential statistics (Bivand & Piras 2015).

6 Model selection

Various spatial model specifications can be used to account for the spatial structure of the data. Selecting the correct model specification remains a crucial task in applied research. There are two empirical strategies for model selection: a specific-to-general or a general-to-specific approach (Florax et al. 2003, Mur & Angulo 2009). However, both come with severe drawbacks.

The specific-to-general approach is more common in spatial econometrics. This approach starts with the most basic non-spatial model and tests for possible misspecification due to omitted autocorrelation in the error term or the dependent variable. Anselin et al. (1996) has proposed to use robust Lagrange multiplier (LM) tests for the hypotheses : and : , which are robust against the alternative source of spatial dependence. The specific-to-general approach based on the robust LM test offers a good performance in distinguishing between SAR, SEM, and non-spatial OLS (Florax et al. 2003). Still, the test disregard the presence of spatial dependence from local spillover effects ( is assumed to be zero), as resulting from an SLX-like process. Cook et al. (2020) show theoretically that an SLX-like dependence structure leads to the rejection of both hypotheses : and : , though no autocorrelation is present (Elhorst & Halleck Vega 2017, Rüttenauer 2022).

The general-to-specific approach follows the opposite direction. It starts with the most general model and stepwise imposes restrictions on the parameters of this general model. In theory, we would 1) start with a GNS specification and 2) subsequently restrict the model to simplified specifications based on the significance of parameters in the GNS (Halleck Vega & Elhorst 2015). The problem with this strategy is that the GNS is only weakly identified and, thus, is of little help in selecting the correct restrictions (Burridge et al. 2016). The most intuitive alternative would be to start with one of the two-source models SDM, SDEM, or SAC. This, however, bears the risk of imposing the wrong restriction in the first place (Cook et al. 2020). Furthermore, Cook et al. (2020) show that more complicated restrictions are necessary to derive all single-source models from SDEM or SAC specifications.

Some argue that the best way of choosing the appropriate model specification is to exclude one or more sources of spatial dependence – autocorrelation in the dependent variable, autocorrelation in the disturbances, or spatial spillover effects of the covariates – by design (Gibbons & Overman 2012, Gibbons et al. (2015)). Natural experiments would be the best way of making one or more sources of spatial dependence unlikely, thereby restricting the model alternatives to a subset of all available models. However, the opportunities to use natural experiments are restricted in social sciences, making it a favourable but often impractical way of model selection. Cook et al. (2020) and Rüttenauer (2022) argue that theoretical considerations should guide the model selection. 1) Rule out some sources of spatial dependence by theory, and thus restrict the specifications to a subset, and 2) theoretical mechanisms may guide the choice of either global or local spillover effects.

A recent simulation study (Rüttenauer 2022) has shown that SLX, SDM, and SDEM are preferable if all sources of dependence may be present. Besides that, the SLX is the most simple specification, as it can easily be estimated by OLS. Given that is just another variable, SLX can easily be combined with non-linear models or other more complicated model specifications, such as panel estimators or machine learning algorithms. Similar conclusions are supported by Wimpy et al. (2021), and also Jeffrey Wooldridge argued for SLX as the only reasonable spatial specification in a Tweet from 2021 called “I will use spatial lags of X, not spatial lags of Y” 333Tweet on using SLX by J. Wooldridge on Twitter: https://twitter.com/jmwooldridge/status/1369460526770753537.

7 House prices in London

As an example to compare the different spatial model specifications, we estimate the effect of local characteristics such as green space and public transport connectivity on the median house price. The relation between environmental characteristics and housing choice and prices has been investigated in several studies (Anselin & Lozano-Gracia 2008, Kley & Dovbishchuk 2021, Liebe et al. 2023). The data for the current example was retrieved from the London Datastore444For house prices, see: https://data.london.gov.uk/dataset/average-house-prices. For London accessibility scores see: https://data.london.gov.uk/dataset/public-transport-accessibility-levels, the 2011 Census555For UK demographics, see: https://www.nomisweb.co.uk/sources/census_2011 and OpenStreetMaps and combined at the Middle Layer Super Output Areas (MSOA). There are 983 MSOAs in London with an average population size of around 8,000 residents. The script for compiling and preparing the data can be found in the Supplementary Materials. All data preparation and analysis were performed with the statistical software R. For a comprehensive overview of spatial software see Bivand et al. (2021) or Pebesma & Bivand (2023).

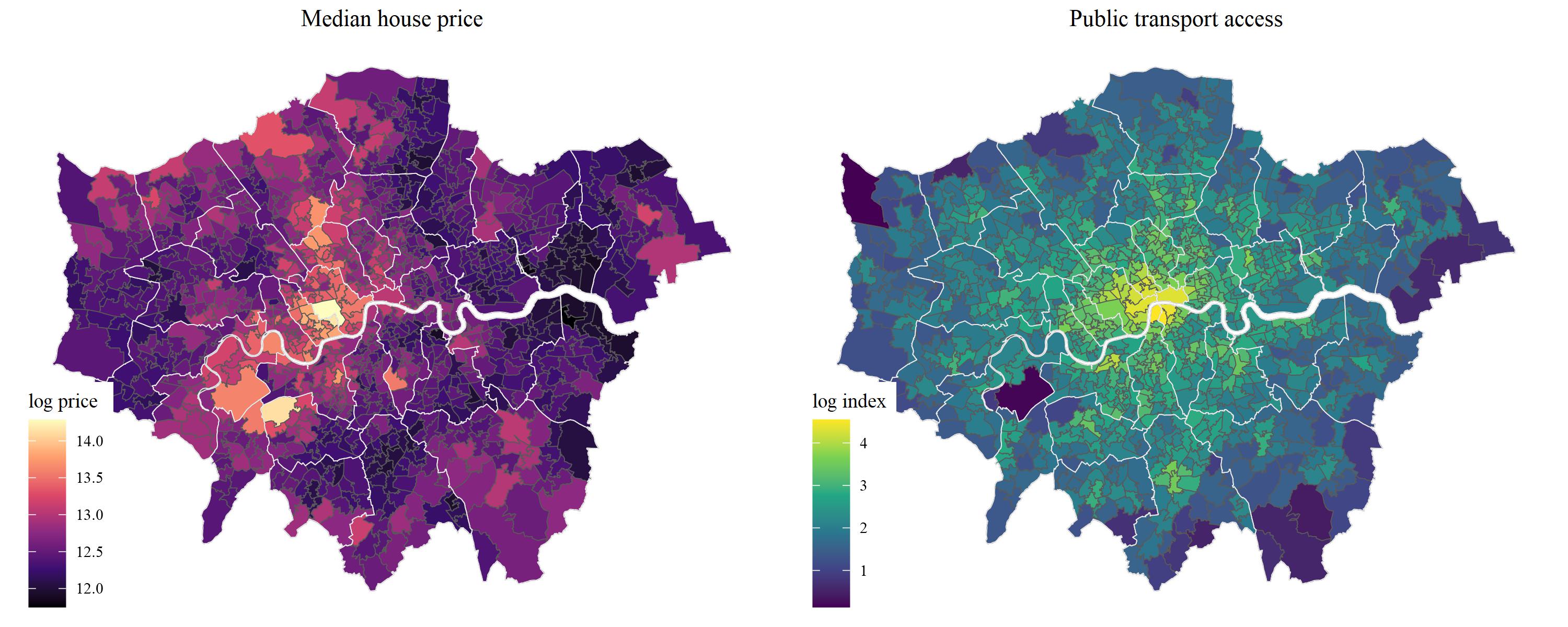

Figure Figure 3 shows an unclassified choropleth map of house prices and public transport access across London, both log-scaled for mapping. As we would expect, both indicators follow a relatively strong spatial of positive autocorrelation: house prices first decrease with increasing distance to the centre, and then seem to increase again in suburban areas. Moreover, there seems to be a pattern of higher prices towards the west and particularly high prices around Hyde Park. Public transport accessibility steadily decreases with distance to the city centre. Spatial regression models thus seem to be important here for two reasons: a) observations are not independent of each other but follow clear spatial patterns, and b) surrounding / adjacent urban characteristics likely play a role for housing demand and prices in the focal unit as well.

In Table 1, we regress the median house price in 2011 on the area (in km^2) covered by green space according to OpenStreetMaps, an index of public transport access (ranging from 0-low accessibility to 100-high accessibility), and several population characteristics from the 2011 census such as population density, the percent of non-UK residents and the percent of social housing. Reported are results form (1) non-spatial OLS, (2) Spatial Autoregressive (SAR), (3) Spatial Error Model (SEM), (4) Spatial Lag of X (SLX), (5) Spatial Durbin Model (SDM), (6) and Spatial Durbin Error Model (SDEM). All variables were standardized before estimation, and we thus interpret coefficients in standard deviations. Note that we do not estimate results for Spatial Autoregressive Combined (SAC) models because of its severe drawbacks for applied research (LeSage 2014).

| OLS | SAR | SEM | SLX | SDM | SDEM | |

| (Intercept) | ||||||

| Green space | ||||||

| Public transport access | ||||||

| Population density | ||||||

| Percent non-UK | ||||||

| Percent social housing | ||||||

| W Green space | ||||||

| W Public transport access | ||||||

| W Population density | ||||||

| W Percent non-UK | ||||||

| W Percent social housing | ||||||

| Num. obs. | ||||||

| R2 | ||||||

| Adj. R2 | ||||||

| LR test: statistic | ||||||

| LR test: p-value | ||||||

| AIC | ||||||

| ; ; | ||||||

Compared to results from conventional non-spatial models, Table 1 comes with several additions: First, variables starting with a “W” (or “lag”) indicate the spatially lagged variable or in the case of row-normalized weights matrices the average value of the respective variable across the local neighbours. Moreover, there are two auto-regressive parameters: “rho” for the estimated auto-correlation in the dependent variable and “lambda” for the estimated auto-correlation in the error term. In case of the SAR, a highly significant coefficient of 0.786 indicates strong positive spatial auto-correlation in the median house price: the house price in adjacent areas positively impacts the focal house prices. A of 0.89 in the SEM however indicates that there is very strong spatial auto-correlation among the (remaining) error variance. The likelihood ratio test in the goodness-of-fit statistics are highly significant in both cases, rejecting the NULL of no spatial auto-autocorrelation.

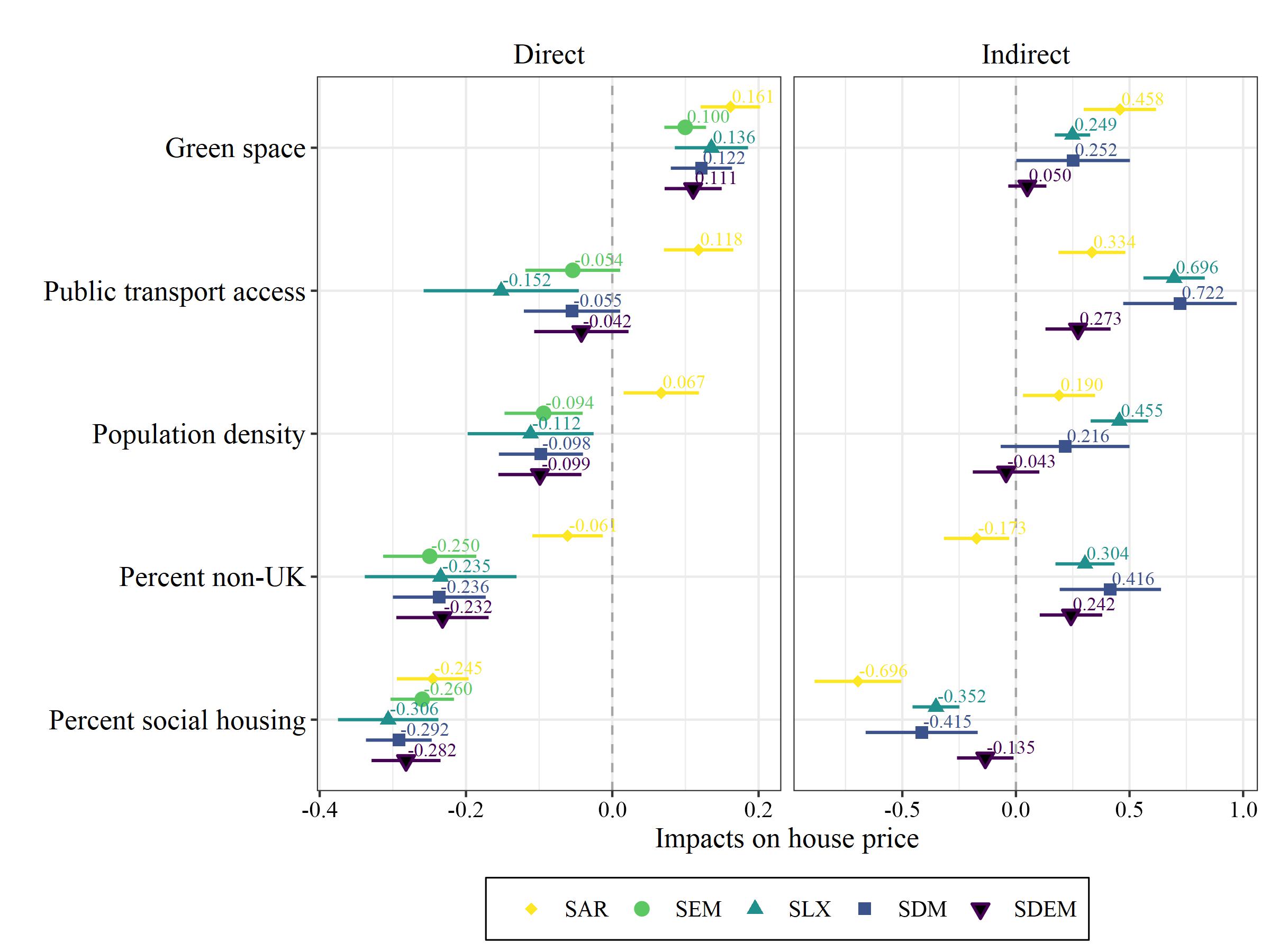

Given the strong positive auto-correlation in the dependent variable in SAR and SDM, we cannot directly interpret the coefficients as marginal effects. Similar to auto-regressive temporal models, we need to account for the spatial multiplier effect. For SEM, SLX and SDEM, we could directly interpret the coefficients of Table 1. However, we plot the impacts of all five models in Figure Figure 4 for reasons of comparison. Note that SEM only has direct and no indirect impacts.

We start with the results of the SAR model in Figure Figure 4. A one standard-deviation increase of green space in the focal unit is associated with a 0.161 standard deviation increase in house prices within the same spatial unit. However, there are also highly significant diffusion processes. This increase in green space in the focal unit will also increase house prices in neighbouring units and the neighbours of these neighbours. This indirect impact will add up to a 0.458 standard deviation increase in house prices across neighbouring units connected through the spatial weights system. Similarly, an increase in public transport accessibility is associated with a 0.118 standard-deviation higher median house price in the unit itself and an additional 0.458 deviation increase diffusing though the neighbouring regions. Note that direct and indirect effects are bound to a common ration, as SAR only estimates one single spatial parameter . In our case, every indirect impact equals approximately 2.83 times the direct impact. This is a very restrictive conditions and a severe drawback of the SAR model.

The SLX - similar to SAR - estimates a positive impact of green space in the focal but also in adjacent neighbourhoods on house prices in the focal unit. A one standard deviation in the focal unit is associated with 0.136 standard-deviations higher house price in the focal unit. If green spaces in adjacent neighbourhoods increase on average by one standard deviation, this would increase house prices in the focal unit by 0.249 standard deviations. Note that the SLX tells a different story about the effect of public transport access than SAR: there is a negative direct and a very strong and positive indirect effect. A one standard deviation increase in public transport access in the focal unit is associated with -0.152 standard deviations lower house prices. In contrast, more public transport in the local surrounding (the average neighbours) is associated with 0.696 standard deviations higher prices. This is in line with the idea that public transport facilities are usually not particularly attractive: it is good to have them close but not too close. The same is true for population density: it is good to live in a broader area with high population density as indicated by the indirect impacts (probability indicating high centrality), but the local neighbourhood should have a low population density as indicated by the negative direct impact.

We could go further with the other models. However, interpretation in SDM follows the same logic as SAR, and interpretation in SDEM aligns to SLX. Interpretation in SEM is analogous to non-spatial OLS, as there are no indirect impacts. Moreover, it is important to keep in mind that the indirect impacts are summary measures which sum over all impacts from or onto neighbouring regions. The indirect public transport effect of 0.696 in SLX would occur if the average public transport access across neighbours would increase by one standard deviation. This only occurs if all neighbours would simultaneously increase public transport access by one standard deviation.

8 Conclusions

Interest in spatial research topics has witnessed a surge within the social sciences, largely due to the increasing availability of geo-referenced data. This growing availability carries immense potential for delving into the analysis of spatial phenomena, such as spillovers and diffusions. However, it also presents challenges for statistical estimators. Notably, utilizing non-spatial techniques with spatial data results in the loss of valuable information. In this chapter, we’ve offered an extensive overview of common spatial econometrics models that permit the explicit testing of spatial relationships. For those keen on exploring spatial panel data, consider the works of Elhorst (2014) and Cook et al. (2023). Meanwhile, those intrigued by non-linear spatial models should delve into LeSage & Pace (2009) and Franzese et al. (2016).

In framework of this chapter, spatial dependence can be integrated as three distinct processes: a) Spatial interdependence in the outcome, b) Clustering of unobservable factors, and c) Spillovers originating from covariates. In any practical application, it is crucial to first contemplate potential theoretical underpinnings for spatial dependence. In the case outlined above, it is plausible to anticipate dependence in the outcome, as house prices in adjacent neighbourhoods directly influence prices in the focal units, given that agents or home-owners rely on price information from surrounding areas. Clustering of unobservable factors is also evident; attributes like distance to the city centre or housing age are spatially clustered and likely exert influence on house prices and other covariates, potentially causing an omitted variable bias. Moreover, there are likely spillover effects from the covariates, where factors like parks, population density, and public transport access in surrounding neighbourhoods have a direct impact across neighbourhood borders. Thus, all the models discussed here are theoretical plausible.

The choice of the correct model specification is often arbitrary, especially in cases like house price modelling. It is advisable to steer clear of the Spatial Autoregressive (SAR) and Autoregressive Conditional (SAC) models, as they come with drawbacks in applied research as highlighted by LeSage (2014) and Rüttenauer (2022). Models with only one estimated spatial parameter across all covariates, like SAR and SAC, impose heavy restrictions on indirect impacts, potentially leading to biased estimates when multiple covariates are involved. Consequently, it is generally sensible to consider more flexible specifications such as SLX, Spatial Durbin Model (SDM), and Spatial Durbin Error Model (SDEM). In our example above, the conclusions derived from SLX, SDM, and SDEM are fairly consistent, with SDEM being the most conservative regarding indirect spatial impacts. This aligns with the model’s accounting for spatial clustering among errors, which encompasses potential confounders. For instance, the indirect impact of population density diminishes significantly when controlling for the distance to the city center, explaining why the indirect positive effect of population density vanishes in SDEM—it is largely confounded by distance to the city center.

The Spatial Lag Model (SLX) stands out for several reasons: 1) It is straightforward in its simplicity; 2) Estimation can be performed using least squares; 3) It can be seamlessly integrated into panel data methods, non-linear models, and machine learning techniques, treating as just another set of covariate; 4) SLX can be globalised by incorporating higher-order neighbours such as and so forth, allowing for a broader assessment of spatial impacts.

A topic deserving more attention is the necessity for spatial econometric models when working with individual-level survey data merged with geographic context information. Do we need to account for spatial structure when adding neighbourhood information to survey data? A common approach involves multi-level models, which address error dependence. However, this approach assumes that units living very close to each other but separated by an arbitrary spatial border are independent —- a strong assumption. An alternative approach is a spatial error model, which accommodates spatially clustered errors. For instance, Diekmann et al. (2023) presents a compelling example in the field of environmental inequality, where error models seem more plausible since it is unlikely that randomly sampled survey respondents directly influence each other (as assumed in SLX and SAR), but very likely that neighbouring respondents are exposed to similar unobservable factors. Nevertheless, one may still wish to investigate the influence of context effects and their spatial patterns. In such cases, SLX-like specifications for the context appear reasonable, as demonstrated by Haußmann & Rüttenauer (2023), who employed spatial SLX specifications to explore the impact of regional deprivation on right-wing votes at various spatial scales.

For further exploration in spatial data analysis, I recommend Pebesma & Bivand (2023) as an open-science book on Spatial Data Science, offering a comprehensive overview of handling and processing spatial data. LeSage & Pace (2009) and Kelejian & Piras (2017) provide comprehensive introductions to spatial econometrics, complete with the necessary mathematical foundations. Ward & Gleditsch (2008) offers an intuitive introduction to spatial regression models, while Elhorst (2012), Halleck Vega & Elhorst (2015), LeSage (2014), and Rüttenauer (2022) present article-length introductions to spatial econometrics.

References

- (1)

- Anselin (1988) Anselin, L. (1988), Spatial Econometrics: Methods and Models, Studies in Operational Regional Science, Kluwer, Dordrecht.

- Anselin (2003) Anselin, L. (2003), ‘Spatial Externalities, Spatial Multipliers, and Spatial Econometrics’, International Regional Science Review 26(2), 153–166.

- Anselin et al. (1996) Anselin, L., Bera, A. K., Florax, R. & Yoon, M. J. (1996), ‘Simple Diagnostic Tests for Spatial Dependence’, Regional Science and Urban Economics 26(1), 77–104.

- Anselin & Lozano-Gracia (2008) Anselin, L. & Lozano-Gracia, N. (2008), ‘Errors in Variables and Spatial Effects in Hedonic House Price Models of Ambient Air Quality’, Empirical Economics 34(1), 5–34.

- Betz et al. (2020) Betz, T., Cook, S. J. & Hollenbach, F. M. (2020), ‘Spatial interdependence and instrumental variable models’, Political Science Research and Methods 8(4), 646–661.

- Bivand (2022) Bivand, R. (2022), ‘R Packages for Analyzing Spatial Data: A Comparative Case Study with Areal Data’, Geographical Analysis 54(3), 488–518.

- Bivand et al. (2021) Bivand, R., Millo, G. & Piras, G. (2021), ‘A Review of Software for Spatial Econometrics in R’, Mathematics 9(11), 1276.

- Bivand & Piras (2015) Bivand, R. & Piras, G. (2015), ‘Comparing Implementations of Estimation Methods for Spatial Econometrics’, Journal of Statistical Software 63(18), 1–36.

- Boillat et al. (2022) Boillat, S., Ceddia, M. G. & Bottazzi, P. (2022), ‘The role of protected areas and land tenure regimes on forest loss in Bolivia: Accounting for spatial spillovers’, Global Environmental Change 76, 102571.

- Burridge et al. (2016) Burridge, P., Elhorst, J. P. & Zigova, K. (2016), Group Interaction in Research and the Use of General Nesting Spatial Models, in B. H. Baltagi, J. P. LeSage & R. K. Pace, eds, ‘Spatial Econometrics: Qualitative and Limited Dependent Variables’, Vol. 37 of Advances in Econometrics, Emerald Group Publishing Limited, pp. 223–258.

- Cliff & Ord (1972) Cliff, A. & Ord, K. (1972), ‘Testing for Spatial Autocorrelation Among Regression Residuals’, Geographical Analysis 4(3), 267–284.

- Cook et al. (2020) Cook, S. J., Hays, J. C. & Franzese, R. J. (2020), Model Specification and Spatial Interdependence, in L. Curini & R. Franzese, eds, ‘The Sage Handbook of Research Methods in Political Science and International Relations’, 1st ed edn, SAGE Inc, Thousand Oaks, pp. 730–747.

- Cook et al. (2023) Cook, S. J., Hays, J. C. & Franzese, R. J. (2023), ‘STADL Up! The Spatiotemporal Autoregressive Distributed Lag Model for TSCS Data Analysis’, American Political Science Review 117(1), 59–79.

- Diekmann et al. (2023) Diekmann, A., Bruderer Enzler, H., Hartmann, J., Kurz, K., Liebe, U. & Preisendörfer, P. (2023), ‘Environmental Inequality in Four European Cities: A Study Combining Household Survey and Geo-Referenced Data’, European Sociological Review 39(1), 44–66.

- Elhorst (2012) Elhorst, J. P. (2012), ‘Dynamic spatial panels: Models, methods, and inferences’, Journal of Geographical Systems 14(1), 5–28.

- Elhorst (2014) Elhorst, J. P. (2014), Spatial Econometrics: From Cross-Sectional Data to Spatial Panels, SpringerBriefs in Regional Science, Springer, Berlin and Heidelberg.

- Elhorst & Halleck Vega (2017) Elhorst, J. P. & Halleck Vega, S. (2017), ‘The SLX Model: Extensions and the Sensitivity of Spatial Spillovers to W’, Papeles de Economía Española 152, 34–50.

- Florax et al. (2003) Florax, R., Folmer, H. & Rey, S. J. (2003), ‘Specification Searches in Spatial Econometrics: The Relevance of Hendry’s Methodology’, Regional Science and Urban Economics 33(5), 557–579.

- Fransham (2020) Fransham, M. (2020), ‘Neighbourhood gentrification, displacement, and poverty dynamics in post–recession England’, Population, Space and Place 26(5), 255.

- Franzese & Hays (2007) Franzese, R. J. & Hays, J. C. (2007), ‘Spatial Econometric Models of Cross-Sectional Interdependence in Political Science Panel and Time-Series-Cross-Section Data’, Political Analysis 15(2), 140–164.

- Franzese et al. (2016) Franzese, R. J., Hays, J. C. & Cook, S. J. (2016), ‘Spatial- and Spatiotemporal-Autoregressive Probit Models of Interdependent Binary Outcomes’, Political Science Research and Methods 4(01), 151–173.

- Gibbons & Overman (2012) Gibbons, S. & Overman, H. G. (2012), ‘Mostly Pointless Spatial Econometrics?’, Journal of Regional Science 52(2), 172–191.

- Gibbons et al. (2015) Gibbons, S., Overman, H. G. & Patacchini, E. (2015), Spatial Methods, in G. Duranton, J. V. Henderson & W. C. Strange, eds, ‘Handbook of Regional and Urban Economics’, Vol. 5, Elsevier, Amsterdam, pp. 115–168.

- Halleck Vega & Elhorst (2015) Halleck Vega, S. & Elhorst, J. P. (2015), ‘The SLX Model’, Journal of Regional Science 55(3), 339–363.

- Haußmann & Rüttenauer (2023) Haußmann, C. & Rüttenauer, T. (2023), ‘Material deprivation and the Brexit referendum: A spatial multilevel analysis of the interplay between individual and regional deprivation’, European Sociological Review p. jcad057.

- Hoffmann et al. (2022) Hoffmann, R., Muttarak, R., Peisker, J. & Stanig, P. (2022), ‘Climate change experiences raise environmental concerns and promote Green voting’, Nature Climate Change 12(2), 148–155.

- Jünger (2022) Jünger, S. (2022), ‘Land use disadvantages in Germany: A matter of ethnic income inequalities?’, Urban Studies 59(9), 1819–1836.

- Kelejian & Piras (2017) Kelejian, H. H. & Piras, G. (2017), Spatial Econometrics, Elsevier.

- Kelejian & Prucha (1998) Kelejian, H. H. & Prucha, I. R. (1998), ‘A Generalized Spatial Two-Stage Least Squares Procedure for Estimating a Spatial Autoregressive Model with Autoregressive Disturbances’, The Journal of Real Estate Finance and Economics 17(1), 99–121.

- Kelejian & Prucha (1999) Kelejian, H. H. & Prucha, I. R. (1999), ‘A Generalized Moments Estimator for the Autoregressive Parameter in a Spatial Model’, International Economic Review 40(2), 509–533.

- Kley & Dovbishchuk (2021) Kley, S. & Dovbishchuk, T. (2021), ‘How a Lack of Green in the Residential Environment Lowers the Life Satisfaction of City Dwellers and Increases Their Willingness to Relocate’, Sustainability 13(7), 3984.

- LeSage (2014) LeSage, J. P. (2014), ‘What Regional Scientists Need to Know about Spatial Econometrics’, The Review of Regional Studies 44(1), 13–32.

- LeSage & Pace (2009) LeSage, J. P. & Pace, R. K. (2009), Introduction to Spatial Econometrics, Statistics, Textbooks and Monographs, CRC Press, Boca Raton.

- LeSage & Pace (2014) LeSage, J. P. & Pace, R. K. (2014), ‘The Biggest Myth in Spatial Econometrics’, Econometrics 2(4), 217–249.

- Liao et al. (2020) Liao, Y., Gil, J., Pereira, R. H. M., Yeh, S. & Verendel, V. (2020), ‘Disparities in travel times between car and transit: Spatiotemporal patterns in cities’, Scientific Reports 10(1), 4056.

- Liebe et al. (2023) Liebe, U., van Cranenburgh, S. & Chorus, C. (2023), ‘Maximizing Utility or Avoiding Losses? Uncovering Decision Rule-Heterogeneity in Sociological Research with an Application to Neighbourhood Choice’, Sociological Methods & Research p. 00491241231186657.

- Manski (1993) Manski, C. F. (1993), ‘Identification of endogenous social effects: The reflection problem’, The Review of Economic Studies 60(3), 531–542.

- Martén et al. (2019) Martén, L., Hainmueller, J. & Hangartner, D. (2019), ‘Ethnic Networks Can Foster the Economic Integration of Refugees’, Proceedings of the National Academy of Sciences of the United States of America 116(33), 16280–16285.

- Moran (1950) Moran, P. A. P. (1950), ‘Notes on Continuous Stochastic Phenomena’, Biometrika 37(1/2), 17.

- Moreno-Monroy et al. (2018) Moreno-Monroy, A. I., Lovelace, R. & Ramos, F. R. (2018), ‘Public transport and school location impacts on educational inequalities: Insights from São Paulo’, Journal of Transport Geography 67, 110–118.

- Mur & Angulo (2009) Mur, J. & Angulo, A. (2009), ‘Model Selection Strategies in a Spatial Setting: Some Additional Results’, Regional Science and Urban Economics 39(2), 200–213.

- Neumayer & Plümper (2016) Neumayer, E. & Plümper, T. (2016), ‘W’, Political Science Research and Methods 4(01), 175–193.

- Nisic (2017) Nisic, N. (2017), ‘Smaller Differences in Bigger Cities? Assessing the Regional Dimension of the Gender Wage Gap’, European Sociological Review 33(2), 292–3044.

- Ogunbode et al. (2019) Ogunbode, C. A., Demski, C., Capstick, S. B. & Sposato, R. G. (2019), ‘Attribution matters: Revisiting the link between extreme weather experience and climate change mitigation responses’, Global Environmental Change 54, 31–39.

- Ord (1975) Ord, J. K. (1975), ‘Estimation Methods for Models of Spatial Interaction’, Journal of the American Statistical Association 70(349), 120–126.

- Pace & LeSage (2010) Pace, R. K. & LeSage, J. P. (2010), Omitted Variable Biases of OLS and Spatial Lag Models, in A. Páez, J. Gallo, R. N. Buliung & S. Dall’erba, eds, ‘Progress in Spatial Analysis’, Springer, Berlin and Heidelberg, pp. 17–28.

- Pebesma & Bivand (2023) Pebesma, E. & Bivand, R. (2023), Spatial Data Science: With Applications in R, first edn, Chapman and Hall/CRC, Boca Raton.

- Roberto (2018) Roberto, E. (2018), ‘The Spatial Proximity and Connectivity Method for Measuring and Analyzing Residential Segregation’, Sociological Methodology 48(1), 182–224.

- Rüttenauer (2018) Rüttenauer, T. (2018), ‘Neighbours Matter: A Nation-wide Small-area Assessment of Environmental Inequality in Germany’, Social Science Research 70, 198–211.

- Rüttenauer (2022) Rüttenauer, T. (2022), ‘Spatial Regression Models: A Systematic Comparison of Different Model Specifications Using Monte Carlo Experiments’, Sociological Methods & Research 51(2), 728–759.

- Rüttenauer (2023) Rüttenauer, T. (2023), ‘More Talk, No Action? The Effect of Exposure to Extreme Weather Events on Climate Change Concern and Pro-Environmental Behaviour’, European Societies Forthcoming.

- Sarrias (2023) Sarrias, M. (2023), Intermediate Spatial Econometrics with Applications in R.

- Tobler (1970) Tobler, W. R. (1970), ‘A Computer Movie Simulating Urban Growth in the Detroit Region’, Economic Geography 46, 234–240.

- Tóth et al. (2021) Tóth, G., Wachs, J., Di Clemente, R., Jakobi, Á., Ságvári, B., Kertész, J. & Lengyel, B. (2021), ‘Inequality is rising where social network segregation interacts with urban topology’, Nature communications 12(1), 1143.

- Ward & Gleditsch (2008) Ward, M. D. & Gleditsch, K. S. (2008), Spatial Regression Models, Vol. 155 of Quantitative Applications in the Social Sciences, Sage, Thousand Oaks.

- Wiedner et al. (2022) Wiedner, J., Schaeffer, M. & Carol, S. (2022), ‘Ethno-religious neighbourhood infrastructures and the life satisfaction of immigrants and their descendants in Germany’, Urban Studies p. 004209802110664.

- Wimpy et al. (2021) Wimpy, C., Whitten, G. D. & Williams, L. K. (2021), ‘X Marks the Spot: Unlocking the Treasure of Spatial-X Models’, The Journal of Politics 83(2), 722–739.

- Wong (2009) Wong, D. (2009), The Modifiable Areal Unit Problem (MAUP), in A. S. Fotheringham & P. Rogerson, eds, ‘The Sage Handbook of Spatial Analysis’, Sage, Los Angeles and London, pp. 105–124.

- Wooldridge (2010) Wooldridge, J. M. (2010), Econometric Analysis of Cross Section and Panel Data, MIT Press, Cambridge, Mass.

- Zapatka & Beck (2021) Zapatka, K. & Beck, B. (2021), ‘Does demand lead supply? Gentrifiers and developers in the sequence of gentrification, New York City 2009–2016’, Urban Studies 58(11), 2348–2368.

- Zoch (2021) Zoch, G. (2021), ‘Thirty Years after the Fall of the Berlin Wall—Do East and West Germans Still Differ in Their Attitudes to Female Employment and the Division of Housework?’, European Sociological Review 37(5), 731–750.