The Boosted Difference of Convex Functions Algorithm for Value-at-Risk Constrained Portfolio Optimization

Abstract

A highly relevant problem of modern finance is the design of Value-at-Risk (VaR) optimal portfolios. Due to contemporary financial regulations, banks and other financial institutions are tied to use the risk measure to control their credit, market, and operational risks. For a portfolio with a discrete return distribution and finitely many scenarios, a Difference of Convex (DC) functions representation of the VaR can be derived. Wozabal (2012) showed that this yields a solution to a VaR constrained Markowitz style portfolio selection problem using the Difference of Convex Functions Algorithm (DCA). A recent algorithmic extension is the so-called Boosted Difference of Convex Functions Algorithm (BDCA) which accelerates the convergence due to an additional line search step. It has been shown that the BDCA converges linearly for solving non-smooth quadratic problems with linear inequality constraints. In this paper, we prove that the linear rate of convergence is also guaranteed for a piecewise linear objective function with linear equality and inequality constraints using the Kurdyka– Łojasiewicz property. An extended case study under consideration of best practices for comparing optimization algorithms demonstrates the superiority of the BDCA over the DCA for real-world financial market data. We are able to show that the results of the BDCA are significantly closer to the efficient frontier compared to the DCA. Due to the open availability of all data sets and code, this paper further provides a practical guide for transparent and easily reproducible comparisons of VaR constrained portfolio selection problems in Python.

Keywords: Boosted Difference of Convex Functions Algorithm; Difference of Convex Functions Algorithm; Kurdyka– Łojasiewicz Property; Value-At-Risk; Conditional Value-at-Risk; Portfolio Selection

1. Introduction

“There’s a way to do it better …find it.”111Thomas A. Edison. True to this motto, for more than 70 years practitioners and theoreticians around the world have aimed to improve the basic Mean-Variance (MV) model introduced by Markowitz (1952) for solving the portfolio selection problem. Over the years two main streams of research on modern portfolio theory have emerged: (i) the incorporation of different risk measures, and (ii) the introduction of further criteria and constraints into the mathematical framework (cf. Anagnostopoulos and Mamanis (2010), p. 1285, and Righi and Borenstein (2018), p. 105.). However, each adaptation also comes at the cost of higher complexity. Current research is consequently caught between practical applicability, and accurate modelling of specific requirements of complex and unpredictable financial markets.

In the basic framework of the MV portfolio, an investor aims to distribute their money among available assets, under the assumption that no risk-free alternatives are available. The initial budget has to be allocated in such a way that the obtained portfolio is efficient with respect to the expected return and risk. In other words, if a portfolio is efficient, then there is no other way to invest the money to achieve a higher expected return with a fixed level of risk, and vice-versa. On a more technical level, the previously described objective can be expressed by defining the returns of an individual asset with as a random variable . The mean corresponds to the expected return of this investment and its standard deviation is equated with the expected risk. By introducing asset weights with and , the overall portfolio mean and variance can be respectively written as

| (1) | ||||

with being the vector containing the distinct asset returns, and being the weighted sum of individual returns (cf. Wozabal (2012), p. 861–863). The weight accordingly represents the share of money that the investor allocates to asset . Due to the covariance between individual random variables and with and , the portfolio can have a lower risk level and a higher expected return compared to investing all available money into the option with least risk. This general framework then can be reformulated into a constrained stochastic optimization problem of the form

| (2) | ||||

where the rational investor aims to find the portfolio weights in such a way that for a given risk level , the expected return is maximized. Note that equivalently, one can also minimize the expected risk for a given return level to obtain an efficient portfolio.

With the model formulation in Equation (2), Markowitz (1952) has only described a basic concept for the optimal portfolio selection. In several literature reviews on modern portfolio theory, among others Gunjan and Bhattacharyya (2022), Xidonas et al. (2020), Sun et al. (2019), Zhang et al. (2018), Rather et al. (2017), Mansini et al. (2014), and Roman and Mitra (2009), disadvantages of the original idea are listed and alternative approaches by other researchers are referenced. Some of the main points of criticism are the underlying planning horizon (single- vs. multi-period), objective function (single- vs. multi-objective), risk attitude of the investor (risk-neutral vs. risk-averse), distribution of returns (normal vs. non-normal), the neglected constraints for transaction costs or sparsity, and the chosen risk measure. Whereas most of the drawbacks can be allocated to the first stream of research, i.e. introducing additional real features, the risk measure defines its own stream.

Among others, Rather et al. (2017), Gambrah and Pirvu (2014), and Hoe et al. (2010) state that one major downside of using variance to measure risk arises from the fact that it is not desirable to minimize the risk on both sides of the return distribution. In other words, for reducing high volatility in general, very high returns and very high losses have to be avoided. This seems to be in contradiction with the overall objective - the maximization of the portfolio profit. Sun et al. (2019) provides a review of portfolio risk measures and concludes that the Value-at-Risk (VaR)is a prominent alternative that only focuses on one tail of the distribution. Intuitively, the with can be interpreted as the maximum loss of a financial portfolio during the next -days with probability and assuming that all settings remain unchanged. Accordingly, many publications, e.g. Liu et al. (2021), Mohammadi and Nazemi (2020), Babazadeh and Esfahanipour (2019), Lwin et al. (2017) Branda (2016), Feng et al. (2015), Gambrah and Pirvu (2014), Cui et al. (2013), Wozabal (2012), Wozabal et al. (2010), Benati and Rizzi (2007), Gaivoronski and Pflug (2005), Larsen et al. (2002), and Campbell et al. (2001), can be found that concentrate on actively managing the VaR of portfolios instead of the variance using a similar setup as shown in Equation (2).

Another important aspect of the risk measure occurs from a practical point of view. Due to contemporary financial regulations, banks and other financial institutions must maintain minimum levels of capital. These reserves must ensure that the financial institution remains solvent even if very high losses arise from their exposure to market, credit, or operational risks. In this framework, Basel II and Solvency II regulations require that the amount of regulatory capital must be determined depending on the VaR of the major business branches (cf. Wozabal (2012), p. 863, Cuoco and Liu (2006), p. 362-363, and Santos et al. (2012), p. 1928). This makes it desirable to actively monitor and manage the VaR of portfolios from a risk management perspective.

For most statistical distributions, the VaR is a non-convex function which makes it difficult to include in convex optimization frameworks. Wozabal et al. (2010), therefore, derived a Difference of Convex (DC)formulation of VaR by using the relationship to the Conditional Value-at-Risk (CVaR) for discrete distributions with finitely many scenarios of the underlying random variables. Intuitively, the can be interpreted as the average loss of a financial portfolio during the next -days considering only the worst % of cases, given that all settings remain unchanged. The CVaR, therefore, is a concave function w.r.t. the portfolio weights and a lower bound of the VaR. Wozabal et al. (2010) accordingly exploits the latter relationship to derive a DC functions formulation. In Wozabal (2012) the Difference of Convex Functions Algorithm (DCA)is then applied to solve a Markowitz type portfolio selection problem with a VaR constraint. The main idea of the DCA is to replace the concave part of the DC functions with a linear approximation and then subsequently to construct a strongly convex subproblem with a unique solution. In the analysis of Wozabal (2012) the DCA yields results close to the efficient frontier in acceptable time for moderately sized data sets. The author, therefore, concludes that the algorithm is attractive to financial institutions that want to actively manage the VaR of their portfolios due to easy implementation and nice convergence properties.

Although the DCA provides a computationally tractable solution, Wozabal (2012) also notes that the obtained solution is not necessarily globally optimal. Furthermore, the time required for computation becomes prohibitive for very large data sets. Aragón-Artacho et al. (2018), and Aragón-Artacho and Vuong (2020), therefore, show in a more general framework that results of the DCA can be improved by introducing the Boosted Difference of Convex Functions Algorithm (BDCA)for smooth and non-smooth DC functions. The main innovation is a line search step using an Armijo type rule and a backtracking procedure which are performed at each iteration based on the output of the DCA. This extrapolation step leads to a provable longer step size and subsequently a larger reduction of the objective function value per iteration, thereby accelerating convergence. Besides the reduction in computation time, the line search procedure also increases the capability to escape from local optima. In the experiments of Aragón-Artacho et al. (2018), and Aragón-Artacho and Vuong (2020), the BDCA consequently is faster and provides better solutions, especially in higher dimensional settings. Whereas Aragón-Artacho et al. (2018) tested the algorithm for solving a DC functions problem in biochemistry, Aragón-Artacho and Vuong (2020) applied the BDCA to solve the minimum sum-of-squares clustering as well as the multidimensional scaling problem.

The BDCA extension for linearly constrained problems is provided by Aragón-Artacho et al. (2022). This paper derives the convergence properties of the algorithm for a non-smooth objective function with linear inequality constraints. The authors emphasize that the BDCA can still be applied if the second part of the DC functions program are non-smooth. This is an additional relaxation compared to the results of Aragón-Artacho and Vuong (2020). However, the proof only holds if the first part of the DC functions formulation can be decomposed into a sum of a smooth convex function and an indicator function of a polyhedral set. Aragón-Artacho et al. (2022) subsequently showed that the BDCA linearly converges for solving quadratic problems with linear inequality constraints. To illustrate the superiority of the BDCA from a practical point of view, the authors additionally performed numerical experiments based on artificially generated data sets.

The aim of this paper is two-folded. On the one hand, for the first time the convergence properties of the BDCA for a piecewise linear objective function with linear equality and inequality constraints will be derived. More precisely, it will be shown that the optimization framework fulfills the Kurdyka-Łojasiewicz (KL) property with an exponent of that implies that the sequence generated by the BDCA converges to a critical point with a linear rate. In comparison to Aragón-Artacho et al. (2022), we will replace Slater’s condition with the Linear Independence Constraint Qualification (LICQ) to obtain the result for a more general framework. Under the assumption of a discrete return distribution with finitely many scenarios, we will also provide the proof that the Markowitz (1952) type portfolio selection problem with a VaR constraint belongs to this class of objective functions. On the other hand, for the first time the BDCA is applied to a Markowitz (1952) type portfolio selection problem in practice. In this context, we contribute with an extended case study designed based on best practices by Beiranvand et al. (2017) for comparing optimization algorithms that will subsequently compare the DCA and BDCA from a practical point of view. In the numerical experiments, both algorithms will be applied to real-world financial data sets consisting of weekly returns of stocks belonging to four major indices. Ultimately, all code implementations will be made available via GitHub, such that the contents of this publication are transparent and easily reproducible. This paper, therefore, also provides a practical guide for VaR constrained portfolio selection problems using the DCA and BDCA in Python that will help to boost the numerical work in portfolio optimization.

The rest of this paper is structured as follows. In Section 2, the DC functions representation of the VaR based on the CVaR is derived. Section 3 then redefines the original MV model by replacing the variance with the VaR in the form of DC functions. The methodology part of the paper introduces the DCA and BDCA. For the latter, the linear rate of convergence for piecewise linear objective functions is also derived. The convergence analysis is followed by the practical application that compares both algorithms based on four real-world data sets and two different experimental settings. The last section summarizes all results.

2. Value-at-Risk as Difference of Convex Functions

The regulatory part in the introduction outlined the importance of VaR in modern finance. It was originally introduced by the global financial services company J.P. Morgan Chase & Co and is a risk measure that focuses on the tail of statistical distributions (cf. Wozabal (2012), p. 862). On a more technical level, the of a random return variable can be defined as the smallest quantile for which the corresponding Cumulative Distribution Function (CDF) is equal to or larger than . Formally, this can be expressed as

| (3) | ||||

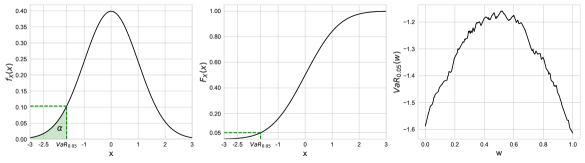

where denotes the Probability Density Function (PDF), the CDF, and the inverse CDF of . The latter is also called the quantile function. Graphical illustrations of the two former statistical functions using the standard normal distribution are shown in Figure 1. On the left side the green dashed lines indicate the based on the PDF () and in the middle using the CDF ().

The panel on the right side shows the depending on asset weight of an arbitrary portfolio consisting of two normally distributed random variables. These variables are associated with the returns of two assets, i.e. . The irregular fluctuations of the function plot illustrate that for most statistical distributions the is a non-convex and non-concave function with respect to .

Definition 2.1.

Recall, a function with is said to be convex if

holds for all choices of and . In contrast, the function is said to be concave if is convex.

The non-convexity, therefore, makes it difficult to include the as constraint in a convex optimization problem. Besides this technical drawback, the non-concavity further leads to a substantial disadvantage with respect to the axiomatic theory of risk measures introduced by Artzner et al. (1999), which contains properties of risk measures that ensure effective regulation or control of risks. Given that the random variables and are associated with the future returns of two financial positions, the might penalize diversification, i.e.

| (4) |

which contradicts financial common sense (cf. Wozabal (2012), p. 862). It also means that the does not fulfill the criteria of Artzner et al. (1999) for being a coherent risk measure as the subadditivity property is violated. This might lead to incorrect economic decisions in certain situations. Note that formal mathematical definitions of convex and coherent risk measures reviewed from an optimization point of view can be found in Lüthi and Doege (2005).

A prominent coherent alternative to the , and, therefore, frequently used to replace it, is the so-called Conditional Value-at-Risk (CVaR) which is sometimes also referred to as Average VaR or Expected Shortfall (ES) (cf. Wozabal (2012), p. 863.). On a more technical level, the of the random return variable can be defined as the integral over its quantile function, divided by . The relationship between and , therefore, can be formally expressed as

| (5) |

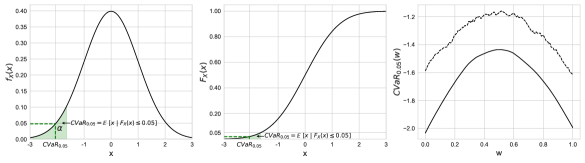

where all functions are defined as before. Graphical illustrations for the using the standard normal distribution are shown in Figure 2. On the left side the green dashed lines indicate the based on the PDF () and in the middle using the CDF ().

The panel on the right side shows the dependent upon asset weight of the same arbitrary portfolio consisting of two random variables. In comparison to the function plot (dashed line), it can be easily seen that the is concave with respect to . By recalling the relationship between convex and concave functions, it is evident why the coherent alternative can be solved as a convex program. The figure also illustrates that the is a lower bound for the , and thus portfolios that are constructed under the coherent alternative will also not violate the corresponding constraint.

In the academic literature, therefore, many researchers entirely replace the with the to circumvent all aforementioned problems. The publications Krokhmal et al. (2002), Lim et al. (2011), and Norton et al. (2021) can be seen as examples. However, from a practical point of view, it is not reasonable to completely rely on the concave alternative by recalling the regulatory framework from the introduction. Basel II and Solvency II regulations explicitly require active monitoring and management of the of portfolios (cf. Wozabal (2012), p. 863, Cuoco and Liu (2006), p. 362-363, and Santos et al. (2012), p. 1928). Using a lower bound, therefore, might lead to a competitive disadvantage compared to other banks or financial institutions (cf. Wozabal (2012), p. 863.). Nevertheless, the previously derived connection between the two risk measures still can be used to express the as a difference of two , assuming that the returns of a financial portfolio can be described based on a discrete distribution with finitely many realizations. This representation facilitates the inclusion of the in a optimization framework which will be shown later.

Given that the random returns of a portfolio follow a discrete distribution with finitely many scenarios with , the corresponding probability distribution function can be written as a list of possible realizations with together with their probability of occurrence with and . The CDF of , therefore, simplifies to a weighted sum of the ordered outcomes with their probabilities. This can be used to rewrite the from Equation (5) as

| (6) |

where is the set of ordered realizations of and are the corresponding probabilities of occurrence. The additional components and are determined based on the last outcome for which the cumulative sum of the ’s is smaller than , i.e.

| (7) | ||||

The realization , therefore, is also referred to as the boundary scenario and corresponds to the discrete version of the . In this context, it becomes clear that for all the following functions

| (8) | ||||

and

| (9) | ||||

can be used to define the boundary realization as the difference of two concave functions

| (10) |

This will be the basis for constructing the DC functions program as the negative accordingly can be written as the difference of two convex functions. Note that for the case , the maximum of the empty set is defined as zero and, therefore, in this particular situation and (cf. Wozabal (2012), p. 865–867).

3. Value-at-Risk constrained Portfolio Optimization

The previous section has shown that the can be expressed as the difference of and . This can be used to replace the variance in the basic MV portfolio model introduced by Markowitz (1952). The optimization framework of Equation (2), therefore, firstly has to be redefined as

| (11) | ||||

where , , and all other previous function and variable definitions remain unchanged. Note that the expectation of Equation (2) has been replaced by the corresponding empirical formula for discrete distributions. By expressing the as the difference of and , the previous formulation can be further adjusted to

| (12) | ||||

where is defined as given in Section 2.

To transform the difference of concave into a DC functions constraint the maximization problem is then transformed into the minimization form defined as

| (13) | ||||

where again all previous function and variable definitions are unchanged.

Afterwards, the constraint can be pulled into the objective function by using the results on exact penalization for DC functions programs by An et al. (1999) as

| (14) | ||||

with being the penalty parameter.

Note that the maximum in the objective function of Equation (14) can be written as

| (15) | ||||

because the pointwise maximum of finitely many DC functions can be expressed as

| (16) |

with . By introducing the two convex functions and and defining them as the functions

| (17) | ||||

and

| (18) | ||||

the problem finally can be written in the form

| (19) | ||||

which corresponds to the general setup of linearly constrained DC functions programs.

4. Methodology

In the previous part, the VaR constrained portfolio selection problem is reformulated as a linearly constrained DC functions program. Wozabal (2012) demonstrated that this optimization problem can be solved by using a hybrid version of the DCA. Aragón-Artacho et al. (2022) showed that the BDCA also can be applied in constrained frameworks. For quadratic problems with linear inequality constraints, the authors then proved that the BDCA has a linear rate of convergence. However, the portfolio selection problem from Equation (19) does not correspond to a quadratic problem and also has an equality constraint. Consequently, the derivation of the rate of convergence for this specific optimization setup remains an open question, that we address in this section.

4.1. Preliminary Mathematical Background

In this first subsection, some preliminaries and basic results are recalled that will be used later to explain the algorithms and to perform the convergence analysis. For more details on these concepts and relevant properties, interested readers are referred to Li and Pong (2018).

Definition 4.1.

The indicator function of a set is denoted as

where is convex if and only if is so.

Definition 4.2.

A function is said to be strongly convex with modulus if

holds for all choices of and .

Definition 4.3.

Let be a proper extended real-valued convex function with effective domain . The one-sided directional derivative of at with respect to the direction is denoted by

Definition 4.4.

For the distance from to a (nonempty) closed set is denoted by .

Definition 4.5.

A proper closed function has the KL property at if there exist a neighborhood of and a continuous concave function with such that

-

1.

is continuously differentiable on with over ;

-

2.

for all with , one has

Definition 4.6.

Definition 4.7.

For a proper closed function satisfying the KL property at , if the corresponding function can be chosen as for some and , i.e. there exist and such that

whenever and , then we say that has the KL property at with an exponent of . If is a KL function and has the same exponent at any , then we say that is a KL function with an exponent of .

Definition 4.8.

A function is piecewise linear if it can be expressed as

for some and .

Definition 4.9.

For a proper extended real-valued convex function with effective domain the subdifferential of at is expressed as

where if is differentiable at and denotes the gradient of at .

4.2. Algorithms

In Section 3 the general setup for a DC functions program with linear constraints has been derived for the piecewise linear constrained portfolio selection problem. Equation (19), therefore, has the form of the general DC functions problem defined as

| () | ||||

where , are proper, closed, and convex functions, , , and for and . Further, represents an inner product. By adding the term with to both functions and , the DC functions formulation with strongly convex components can be obtained.

Note that the problem () also can be rewritten as an unconstrained non-smooth DC functions optimization problem of the form

| () |

where is the feasible set. This formulation then can be solved by applying the classical Difference of Convex Functions Algorithm (DCA), which is a powerful method to tackle non-convex optimization problems. It originally was developed by Tao and Souad (1988) more than 30 years ago. Since then researchers like Geremew et al. (2018), Wozabal (2012), and An and Tao (2005) have applied the algorithm to a variety of practical applications, for example portfolio optimization, supply chain management, or telecommunications. The main idea of the methodology is to replace the concave part of the objective function with a linear approximation at the current iteration point. For this strongly convex approximation of () a unique solution can be derived.

| () | ||||

The general procedure of the DCA for a linearly constrained non-smooth objective function is shown in Algorithm 1. At each iteration the current solution of the strongly convex subproblem is used to construct a linear approximation of based on an element of the subgradient . The algorithm then continues iterating as long as the new unique solution deviates from the old one . With this procedure, the classical DCA aims to find a critical point of (). A critical point has been found if . For the constrained problem () this point is a Karush–Kuhn–Tucker (KKT) point if there exist Lagrange multipliers and such that the following conditions are fulfilled:

| (20) |

Even though the DCA provides a useful way to solve non-convex problems, among others Wozabal (2012), Aragón-Artacho et al. (2018), Aragón-Artacho and Vuong (2020), and Aragón-Artacho et al. (2022) conclude that the obtained solution is not necessarily globally optimal. In the framework of numerical experiments, all authors show that the algorithm tends to get stuck at local minima - especially for higher dimensional data sets. Another drawback arises from the computation time which becomes prohibitively long in these settings. For application to larger data the DCA, therefore, is not suitable.

To improve this undesirable property, Aragón-Artacho et al. (2018), and Aragón-Artacho and Vuong (2020) firstly introduced the Boosted Difference of Convex Functions Algorithm (BDCA)for smooth and non-smooth objective functions. The main innovation is the added line search step after each DCA iteration that uses an Armijo type condition in combination with a backtracking procedure. This adaptation makes the algorithm more robust against local minima and boosts the convergence. The corresponding extension for linearly constrained programming problems is provided by Aragón-Artacho et al. (2022) and is described in Algorithm 2. Until Line 5, the procedure is identical to the DCA. However, after solving the approximated problem (), a descent direction is calculated. For this direction the set of active inequality constraints, i.e.

| (21) |

is used afterwards to test if the vector is pointing into a feasible area. The linesearch step is then only performed if this condition is fulfilled. Further, must be differentiable at the current . Otherwise, Aragón-Artacho and Vuong (2020) showed based on the unconstrained case that it is not guaranteed that points into a descent direction. Line 8 subsequently checks if is part of the feasible set . If not, is scaled down by until the requirement is fulfilled. This is followed by the Armijo type condition in Line 10 that attempts to decrease the objective function further along the descent direction. If the shown inequality cannot be rejected, the backtracking procedure again scales down the current by . Note that the condition will always be violated as soon as is small enough.

As an alternative to the fixed as the starting point of each line search procedure, Algorithm 3 shows an adaptive way to select distinct initializations. At each iteration the parameter is determined such that the backtracking begins on the boundary of the feasible set. Afterwards, the values are scaled down based on in the same way. This eliminates the problem of selecting and justifying a suitable fixed value. From the computational point of view, the adaptive version also has the benefit that the while loop in lines 8 and 9 of Algorithm 2 is no longer required which can save computation time.

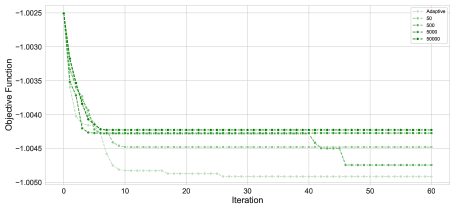

Figure 3 shows a comparison between fixed and adaptive . In the example, four different fixed values and the adaptive version have been tested for solving a VaR constrained portfolio selection problem from Section 3 with the BDCA. In comparison, the algorithm performs better if the line search always starts on the boundary of the feasible set. The line plot shows that, in this setting, the objective function is scaled down much faster when compared to the results of the four fixed ’s. After 60 iterations the adaptive version subsequently found the best end result. Due to this observation, the numerical experiments performed later in this paper will always use the boundary of the feasible set to determine .

4.3. Linear Convergence for Piecewise Linear Objective Functions

After recalling all preliminaries and the basic methodology of the algorithms, the last subsection proves that the BDCA has a linear rate of convergence for a piecewise linear objective function with linear equality and inequality constraints. For this purpose, this section firstly derives the convergence properties for a general piecewise linear objective function and then shows that the portfolio selection problem with Equation (19) belongs to this class.

Assumption 1.

Both functions and are strongly convex with the same modulus .

Assumption 2.

The function is subdifferentiable at every point in , i.e. for all and

Assumption 3.

All feasible points fulfill the LICQ, this means that the gradients of all active inequality constraints and the gradients of all equality constraints are linear independent.

Remark.

For the portfolio selection problem (19) both functions and are convex, and can be transformed into strongly convex functions by adding the term to each function. Hence Assumption 1 is fulfilled. In addition, the function is subdifferentiable at every point in .

Finally, all feasible points of the portfolio selection problem (19) fulfill the LICQ. Indeed, the gradient of the equality constraint is the vector . The gradients of the inequality constraints are the standard basis of , i.e. which are all linear independent. Because not all weights can be equal to zero, at most inequality constraints can be active at the same time. It then can be shown that the set of vectors including and vector from is linear independent and therefore another basis of .

Proposition 1.

Under Assumptions 1-3, and that for a given iteration the function is continuously differentiable with respect to contained in dom , the following properties of the line search procedure can be derived:

-

1.

;

-

2.

;

- 3.

Proof.

The proof of (1.) is similar to that of Proposition 3 shown in Aragón-Artacho et al. (2018). In Aragón-Artacho and Vuong (2020), it was proved that (2.) holds when is differentiable, but a careful review indicates that the proof is valid when is only differentiable at . Then (2.) can be proved in a similar way as shown in Aragón-Artacho et al. (2022). First we pick any and observe that for the one-sided directional derivative the following relationship holds

| (22) |

due to the convexity of . Second, we can write down the KKT conditions of the problem () as

| (23) |

Third, we observe that is strongly monotone with parameter , because is strongly convex with constant . Since and , we therefore have

| (24) |

It remains to combine the expressions (22), (23) and (24) with the fact that . Based on these components we can derive

| (25) | ||||

and by combining the last inequality with (22) the result follows. Lastly, (3.) was shown in Aragón-Artacho and Vuong (2020). ∎

The convergent properties of BDCA are collected in the following Theorem.

Theorem 1.

Under Assumptions 1-3, and that the function is differentiable at with , for any feasible starting point , either BDCA returns a KKT point of () or it generates an infinite sequence such that the following statements hold:

-

1.

is monotonically decreasing and hence convergent to some .

-

2.

Suppose that and are bounded, then any limit point of is a KKT point of ().

-

3.

We have . Moreover, if there is some such that for all , then .

Proof.

Algorithm 2 terminates when . This means that . Based on (20) and (23), it then becomes clear that is a KKT point of (). Otherwise, due to Proposition 1 and Line 14 of Algorithm 2, we obtain

| (26) |

with . As the sequence is monotonically decreasing and bounded from below due to Assumption 2, it converges to some . Consequently, we have

| (27) |

By also taking into account (26), we therefore can derive .

Now, assume that is a limit point of , then there must be a subsequence also converging to . We therefore have as . In combination with (23), we then obtain

| (28) |

Due to continuity of , we know that holds. Further, we can assume that , because the sequence is bounded by assumption. In this context, the sequences of Lagrange multipliers and also must be bounded. To prove this, let us introduce which is a vector that contains all Lagrange multipliers. Assume that . Without loss of generality we can assume that with and .

We then can divide the first equality in (28) by and let to obtain

| (29) |

Similarly, we can apply the same technique to the second equality in (28) such that we get

| (30) |

Based on the previous result we can derive that for all and therefore we obtain the following equality

| (31) |

Equation (29) therefore simplifies to

| (32) |

By Assumption 3 we deduce for all and for all . This result leads to , which is a contradiction with the fact that . We consequently can extract subsequences if necessary and can assume that

| (33) |

Due to the closedness of the graph of , we then can take the limit in (28) and obtain

| (34) |

which means that is a KKT point of (). The proof for (3.) is omitted, because it is similar to the one in Aragón-Artacho et al. (2018). ∎

Definition 4.10.

We say that the sequence with , converges linearly to if for sufficiently large

| (35) |

for some constants and .

To establish the linear convergence of the iterative sequence to a KKT point of (), we will require that the objective function in () satisfying the KL property with an exponent of .

Theorem 2.

Under Assumptions 1-3, suppose that the sequence generated by the BDCA has the limit point and that is locally Lipschitz continuous around . Suppose in addition that the objective function of () satisfying the KL property with an exponent of . Then the sequence converges linearly to .

Proof.

Since is a KL function with exponent , the function is also a KL function with exponent (Li and Pong, 2018, Section 5). Following the standard techniques developed in Attouch et al. (2010); Aragón-Artacho et al. (2018); Aragón-Artacho and Vuong (2020); Li and Pong (2018), it is a routine task to derive the linear convergence of . We skip the detailed proof for brevity. ∎

We are now in the position to derive the linear convergence of the BDCA when applying to the VaR optimization problem in (19). For this purpose, we will use the following result.

Lemma 1 (Li and Pong (2018), p. 1221).

Suppose that is a proper closed function of the form

where , are proper closed polyhedral functions for and is a proper closed convex function with an open domain, is strongly convex on any compact convex subset of dom and is twice continuously differentiable on dom . Suppose in addition that is continuous on dom . Then is a KL function with an exponent of .

The main mathematical contribution of this paper is stated in the following theorem.

Theorem 3.

Proof.

For discrete return distributions with finitely many scenarios the can be redefined as a sorting problem. For this purpose the realizations of the assets are stored in matrix . The portfolio profits accordingly can be calculated as where are the asset weights.

In the next step up to realizations have to be selected from smallest to largest. The sorting process can be performed by introducing matrix that only consists of 0s or 1s and has row and column sums less than or equal to one. In other words, if one realization was already selected, it cannot be chosen another time. The vector of selected realizations then is represented by . If only with realizations are chosen, all other entries at position with are zero. For all non-zero entries it must hold that for all . Due to all these requirements there are only possibilities to construct . Note that for the case of equal realizations this number increases but remains finite.

By additionally requiring , the can then be redefined as

where contains the scenario probabilities and is automatically determined as the smallest realization that was not selected by . Based on basic matrix calculus the problem then can be rewritten as

where and .

Finally, consider Corollary 1 with and such that . Then it is clear that any piecewise linear function is a KL function with exponent . Hence, the conclusion follows.

∎

Remark.

Even though in general could be non-smooth at for the VaR constrained portfolio selection problem shown in (19), the BDCA still can be applied. Indeed, the function is smooth almost everywhere except at the corner where two linear functions intersect. However, the probability that the solution of is exactly at one of these corners is zero.

Figure 4 empirically visualizes the previously derived rate of convergence. For this purpose, the BDCA ran a fixed number of iterations for an arbitrary data set five times, using different starting points. Afterwards, Definition 4.10 has been used to derive the convergence constant for each iteration and to plot the corresponding results.

Note that as the global solution is unknown, the last objective function value of the sequence has been taken to represent . In the figure it is observable that the constant mainly fluctuates between 0.8 and 1, empirically confirming the theoretical result. In the end the constant further decreases as the sequence gets closer to the last iteration value.

5. Practical Application & Numerical Experiments

After taking into account all theoretical aspects, the focus is on the practical application now. Due to the added line search procedure, the BDCA theoretically promises a faster convergence and a higher robustness against local minima compared to the DCA. So far no comparison for the portfolio selection problem described in Section 3 has been performed. This part of the paper consequently investigates the practical point of view based on a case study using four real-world data sets provided by Bruni et al. (2016).

The data sets were chosen as the authors have filtered and removed possible errors in the original sources and also have adjusted for dividends and stock splits. This allows more accurate experiments to be conducted. Further, any future comparison of the results will be easy to perform due to the open availability.

Table 1 gives a brief description of all data sets. Note that the names are abbreviations for the collection of individual stocks belonging to the following indices: Dow Jones Industrial Average (DowJones), National Association of Securities Dealers Automated Quotation 100 (NASDAQ100), Financial Times Stock Exchange 100 (FTSE100), and Fama & French 49 Industrial Portfolios (FF49).

Source: Cf. Bruni et al. (2016), p. 860.

| Data Set | Country | n | k | Interval | Time Period |

| DowJones | USA | 28 | 1,363 | Weekly | Feb 1990 - Apr 2016 |

| FF49 | USA | 49 | 2,325 | Weekly | Jul 1969 - Apr 2016 |

| FTSE100 | UK | 83 | 717 | Weekly | Jul 2002 - Apr 2016 |

| NASDAQ100 | USA | 82 | 596 | Weekly | Nov 2004 - Apr 2016 |

Summary statistics are provided in Table 2. The mean, variance, and have been calculated individually per stock, and the table shows the minimum and maximum as well as the first, second, and third quartile (Q25, Q50, Q75) of these distributions. More information about the data derivation can be found in Bruni et al. (2016).

The two upcoming experiments were designed using the best practices by Beiranvand et al. (2017) for fair and unbiased comparisons of optimization algorithms. The authors suggest to measure the performance based on three categories: efficiency, reliability, and quality of algorithmic output. In the case study, the first criterion is evaluated by tracking the CPU time. The reliability of algorithmic output is measured by using multiple starting points and then reporting the objective function value and the number of feasible solutions with 95% Confidence Intervals (CIs). The intervals are constructed by bootstrapping independent samples with replacement. The quality of the algorithmic output is normally measured by the distance to the optimal solution. However, as the solutions for the financial data sets are unknown, a common approach is to replace the optimum with the best known value.

| Stats | DowJones | FF49 | FTSE100 | NASDAQ100 | |

| Min | 1.00128 | 1.00275 | 0.99939 | 1.00012 | |

| Q25 | 1.00210 | 1.00369 | 1.00147 | 1.00188 | |

| Q50 | 1.00253 | 1.00390 | 1.00251 | 1.00306 | |

| Q75 | 1.00282 | 1.00436 | 1.00360 | 1.00475 | |

| Max | 1.00605 | 1.00544 | 1.00802 | 1.01030 | |

| Min | 0.00084 | 0.00034 | 0.00063 | 0.00065 | |

| Q25 | 0.00112 | 0.00079 | 0.00126 | 0.00155 | |

| Q50 | 0.00160 | 0.00089 | 0.00163 | 0.00217 | |

| Q75 | 0.00211 | 0.00114 | 0.00296 | 0.00295 | |

| Max | 0.00385 | 0.00303 | 0.00773 | 0.00704 | |

| Min | 0.90997 | 0.92400 | 0.89527 | 0.88142 | |

| Q25 | 0.93284 | 0.95443 | 0.92092 | 0.92053 | |

| Q50 | 0.94326 | 0.95712 | 0.93805 | 0.93096 | |

| Q75 | 0.95074 | 0.96137 | 0.94744 | 0.94173 | |

| Max | 0.95876 | 0.97628 | 0.96213 | 0.96338 |

The case study was performed under the following environmental factors. All numerical experiments were solved using the IRIDIS High Performance Computing Facility of the University of Southampton. One user can simultaneously use up to 32 nodes. Each of these available compute nodes contained 40 CPUs and 16GB RAM. 222For more information: https://www.southampton.ac.uk/isolutions/staff/iridis.page.

Both algorithms were implemented in Python 3.9.12 using the optimization framework of the SciPy package programmed by Virtanen et al. (2020). As the authors of this case study also want to contribute to an easily reproducible experimental setup, all codes have been uploaded into the following Git repository https://github.com/mlthormann/BDCA-For-Portfolio-Optimization/.

5.1. Experiment 1

The starting point can have a huge impact on the overall output of the optimization. It has to be defined by the user and in the most extreme case an adverse initialization can lead to a complete failure because no feasible solution can be found. In the first numerical experiment, therefore, random initialization weights are drawn from a Dirichlet distribution to evaluate the dependency of algorithmic output on good starting values. The algorithms are tested based on two different settings. In one framework the DCA and BDCA start with nearly equal weights for all assets. In the other one the values are more extreme so that only few decision variables have initialization not equal to zero. This increases the chance for a bad starting point. The latter consequently has been selected to stress test the performance. Both settings are then repeated 100 times. Five random draws for six assets are shown in Table 3.

| Setting | Rep | ||||||

| 1 | 1 | 0.17493 | 0.16305 | 0.16348 | 0.16067 | 0.17559 | 0.16228 |

| 2 | 0.16894 | 0.17088 | 0.16166 | 0.16667 | 0.16552 | 0.16631 | |

| 3 | 0.17525 | 0.16799 | 0.16425 | 0.16384 | 0.16547 | 0.16321 | |

| 4 | 0.16845 | 0.17085 | 0.16294 | 0.17190 | 0.16597 | 0.15989 | |

| 5 | 0.16823 | 0.16418 | 0.17899 | 0.16459 | 0.16118 | 0.16282 | |

| 2 | 1 | 0.37573 | 0.00000 | 0.00001 | 0.00012 | 0.22837 | 0.39577 |

| 2 | 0.02160 | 0.21907 | 0.01499 | 0.00001 | 0.00051 | 0.74382 | |

| 3 | 0.00791 | 0.00001 | 0.99208 | 0.00000 | 0.00000 | 0.00000 | |

| 4 | 0.39894 | 0.47972 | 0.00978 | 0.00000 | 0.02959 | 0.08197 | |

| 5 | 0.00000 | 0.00000 | 0.01100 | 0.98892 | 0.00008 | 0.00000 |

Note that besides the variation in the initialization weights, the values of the penalty parameter and the constraint are also altered. For the latter in total six different lower levels are defined - from easily solvable to numerically more challenging. The confidence level of the has been set to which is commonly used in practice. The effect of the penalty parameter is tested based on three different values associated with soft, medium, or strong penalization. An overview with all parameters used in the experiment is shown in Table 4. It also reports the additional BDCA parameters and . For each parameter three different values have been selected. This leads to combinations where the search procedure scales down slowly, moderately, or quickly from a line with shallower or steeper slope.

| Experiment | Parameter | Values |

| 1 | 0.958, 0.960, 0.962, | |

| 0.964, 0.965, 0.966 | ||

| 10, 50, 90 | ||

| 0.0001, 0.001, 0.01 | ||

| 0.3, 0.5, 0.7 |

Beiranvand et al. (2017) highlight that stopping conditions also play an important role in the comparison of algorithms. They can drastically change the quality of algorithmic output. To avoid an unfair comparison, different stopping criteria must be tested before the performance of both algorithms is ultimately compared. The first two options are based on the change in the solution vector. They are defined as

where elementwise differences are calculated for all . The algorithm consequently stops when all values are below a certain tolerance . It indicates that the sequence has converged to a stationary point.

Likewise the change in the objective function can be used to terminate the optimization process. If the sequence has converged to a stationary point, the same should also hold for . The two equivalent stopping conditions are defined as

where the algorithm again stops when a certain tolerance is reached.

Another practicable option is defined as

i.e. let the algorithm run for a certain number of iterations . This criterion generally does not measure how close the solution of a certain iteration is to a stationary point. However, it might be helpful to overcome stationary points that are not critical points. For example, Figure 3 shows that the improvement sometimes stagnates over a few rounds. Afterwards a bigger step downside can be observed. A fixed number of iterations, therefore, can be beneficial to benchmark the other criteria. The maximum number of iterations has been set to for this stopping condition by considering the approximated computation time for all data sets. All other criteria run based on a tolerance equal to . To ensure that the algorithms terminate in an acceptable time, the maximum number of iterations is limited to .

The procedure of the first numerical experiment then can be divided into two steps. Firstly, the additional parameters of the BDCA and the best stopping criterion for both algorithms has to be determined. For this purpose a grid search combines all possible parameters and repeats each combinations 100 times per Dirichlet setting. This leads to 18,000 observations for the DCA and 162,000 instances for the BDCA. To ensure that both algorithms are compared based on the same amout of observations, the additional BDCA parameters are evaluated first. The comparison of the stopping criteria, therefore, only shows the results of the best and combination. In the second part, the experiments are repeated another 400 times using the best stopping criterion. Both algorithms were then trained on 500 different initialization weights per parameter setting and the outputted results serve as basis for the comparison.

The performance of the additional BDCA parameters and is summarized in Table 5. It reports the share of infeasible solutions as well as the median expected return and CPU time in minutes of all feasible solutions including 95% bootstrap CIs. The best values per column and data set are highlighted in bold font. Overall, the effect of the chosen parameters does not significantly change the algorithmic output across data sets. For nearly all performance measures the CIs of different and combinations are highly overlapping even without a correction of the significance level for simultaneous testing. With the adjustment, the intervals would have been even wider and consequently no correction was performed.

| BDCA Parameter | Share Infeasible | Expected Return | CPU Time | ||||||||

| Data Set | Lower | Q50 | Upper | Lower | Q50 | Upper | L | Q50 | U | ||

| DowJones | 0.0001 | 0.3 | 0.2110 | 0.2170 | 0.2230 | 1.003043 | 1.003057 | 1.003068 | 0.8 | 0.8 | 0.9 |

| 0.5 | 0.2065 | 0.2125 | 0.2186 | 1.003036 | 1.003046 | 1.003057 | 0.8 | 0.9 | 0.9 | ||

| 0.7 | 0.2147 | 0.2207 | 0.2267 | 1.003041 | 1.003055 | 1.003066 | 0.9 | 0.9 | 1.0 | ||

| 0.0010 | 0.3 | 0.2113 | 0.2173 | 0.2234 | 1.003042 | 1.003054 | 1.003066 | 0.8 | 0.8 | 0.9 | |

| 0.5 | 0.2067 | 0.2127 | 0.2187 | 1.003035 | 1.003045 | 1.003055 | 0.8 | 0.9 | 0.9 | ||

| 0.7 | 0.2148 | 0.2208 | 0.2269 | 1.003043 | 1.003056 | 1.003066 | 0.9 | 0.9 | 1.0 | ||

| 0.0100 | 0.3 | 0.2104 | 0.2164 | 0.2224 | 1.003037 | 1.003049 | 1.003061 | 0.8 | 0.8 | 0.9 | |

| 0.5 | 0.2051 | 0.2110 | 0.2170 | 1.003030 | 1.003041 | 1.003051 | 0.8 | 0.9 | 0.9 | ||

| 0.7 | 0.2128 | 0.2188 | 0.2249 | 1.003037 | 1.003049 | 1.003061 | 0.9 | 0.9 | 1.0 | ||

| FF49 | 0.0001 | 0.3 | 0.0716 | 0.0754 | 0.0793 | 1.004112 | 1.004117 | 1.004120 | 0.7 | 0.8 | 0.9 |

| 0.5 | 0.0711 | 0.0749 | 0.0788 | 1.004119 | 1.004123 | 1.004127 | 0.8 | 0.8 | 0.9 | ||

| 0.7 | 0.0710 | 0.0748 | 0.0787 | 1.004120 | 1.004123 | 1.004127 | 0.8 | 0.9 | 1.0 | ||

| 0.0010 | 0.3 | 0.0717 | 0.0756 | 0.0794 | 1.004113 | 1.004117 | 1.004120 | 0.7 | 0.8 | 0.9 | |

| 0.5 | 0.0712 | 0.0750 | 0.0789 | 1.004119 | 1.004123 | 1.004126 | 0.8 | 0.8 | 0.9 | ||

| 0.7 | 0.0711 | 0.0749 | 0.0788 | 1.004120 | 1.004123 | 1.004127 | 0.8 | 0.9 | 0.9 | ||

| 0.0100 | 0.3 | 0.0716 | 0.0754 | 0.0793 | 1.004113 | 1.004117 | 1.004120 | 0.8 | 0.8 | 0.9 | |

| 0.5 | 0.0707 | 0.0745 | 0.0783 | 1.004119 | 1.004122 | 1.004126 | 0.8 | 0.8 | 0.9 | ||

| 0.7 | 0.0706 | 0.0743 | 0.0782 | 1.004119 | 1.004122 | 1.004125 | 0.8 | 0.9 | 0.9 | ||

| FTSE100 | 0.0001 | 0.3 | 0.1693 | 0.1748 | 0.1804 | 1.003162 | 1.003176 | 1.003188 | 13.9 | 14.5 | 15.0 |

| 0.5 | 0.1689 | 0.1744 | 0.1800 | 1.003158 | 1.003172 | 1.003189 | 15.1 | 15.6 | 16.2 | ||

| 0.7 | 0.1786 | 0.1843 | 0.1899 | 1.003160 | 1.003178 | 1.003190 | 16.4 | 17.0 | 17.7 | ||

| 0.0010 | 0.3 | 0.1699 | 0.1755 | 0.1811 | 1.003162 | 1.003176 | 1.003188 | 13.9 | 14.4 | 14.9 | |

| 0.5 | 0.1682 | 0.1738 | 0.1793 | 1.003159 | 1.003173 | 1.003191 | 15.0 | 15.5 | 16.1 | ||

| 0.7 | 0.1790 | 0.1847 | 0.1904 | 1.003159 | 1.003176 | 1.003190 | 16.3 | 17.0 | 17.6 | ||

| 0.0100 | 0.3 | 0.1717 | 0.1773 | 0.1829 | 1.003162 | 1.003176 | 1.003189 | 14.0 | 14.5 | 15.0 | |

| 0.5 | 0.1706 | 0.1761 | 0.1817 | 1.003158 | 1.003172 | 1.003190 | 15.1 | 15.6 | 16.1 | ||

| 0.7 | 0.1778 | 0.1834 | 0.1891 | 1.003161 | 1.003178 | 1.003190 | 16.4 | 17.0 | 17.5 | ||

| NASDAQ100 | 0.0001 | 0.3 | 0.4408 | 0.4481 | 0.4553 | 1.004563 | 1.004581 | 1.004599 | 25.4 | 27.0 | 28.6 |

| 0.5 | 0.4351 | 0.4423 | 0.4496 | 1.004567 | 1.004582 | 1.004603 | 26.1 | 27.2 | 28.8 | ||

| 0.7 | 0.4482 | 0.4556 | 0.4628 | 1.004597 | 1.004612 | 1.004632 | 27.5 | 29.4 | 31.1 | ||

| 0.0010 | 0.3 | 0.4413 | 0.4486 | 0.4558 | 1.004561 | 1.004580 | 1.004597 | 25.4 | 26.8 | 28.5 | |

| 0.5 | 0.4346 | 0.4419 | 0.4492 | 1.004566 | 1.004581 | 1.004602 | 26.0 | 27.2 | 28.8 | ||

| 0.7 | 0.4484 | 0.4557 | 0.4630 | 1.004598 | 1.004614 | 1.004634 | 27.4 | 29.3 | 31.0 | ||

| 0.0100 | 0.3 | 0.4401 | 0.4473 | 0.4546 | 1.004559 | 1.004576 | 1.004593 | 25.3 | 26.6 | 28.3 | |

| 0.5 | 0.4373 | 0.4446 | 0.4518 | 1.004561 | 1.004575 | 1.004596 | 26.3 | 27.6 | 29.0 | ||

| 0.7 | 0.4477 | 0.4550 | 0.4623 | 1.004594 | 1.004610 | 1.004628 | 27.0 | 28.7 | 30.7 | ||

On an individual parameter level, provides a good trade-off between efficiency and reliability of algorithmic output. Smaller values decrease the computation time as the line search procedure requires fewer iterations, but the objective function is also evaluated at fewer points. This leads to lower median expected returns and a slightly higher share of infeasible solutions. Based on a similar trade-off, has been selected as the second parameter.

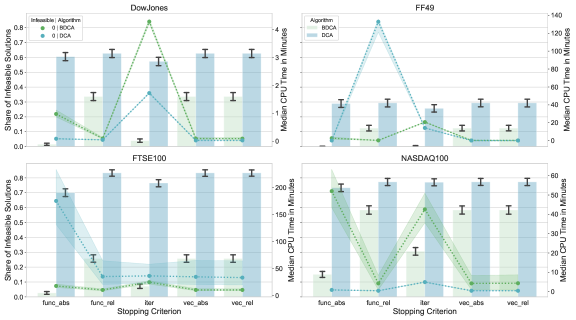

Figure 5 illustrates the performance of the distinct stopping criteria per data set and algorithm. The left y-axis shows the share of infeasible solutions in form of bar plots including 95% CIs. Note that the significance level of all upcoming intervals has been corrected using the Bonferroni method proposed by Dunn (1961). It is one commonly used approach to ensure that the family wise error rate stays at . In the first experiment in total 80 CIs are constructed simultaneously per data set. The confidence level consequently was corrected to .

Across data sets and stopping conditions, the BDCA outputs significantly fewer infeasible solutions than the DCA. Whereas for func_rel, vec_abs, and vec_rel the difference is mostly between 15 and 40 percentage points, the gap further increases up to 70 percentage points for func_abs and iter. At this point the benefit of the line search procedure comes to light. Within the optimization it is possible that the convex subproblem can only be solved with an infeasible solution. In other words, the constraint is not fulfilled or the weights are not included in the simplex. Especially the former problem occurred many times for the DCA because the constraint was pulled into the objective function. It, therefore, can only be ensured indirectly via a stronger penalty parameter. However, in our experiments we observed that with even higher values for the tendency for ill-conditioning also increased. This especially happened in unfavorable parameter settings. In these constellations, the line search assisted in resolving the issue.

Overall, the iter or func_abs produce significantly fewer infeasible solutions independent of data sets and algorithms. The only exception occurs for the FF49 data set where the performance of func_abs is very similar to the other stopping conditions of the DCA. Table 2 shows that the underlying data contains fewer high risk assets. This leads to a portfolio selection problem that is easier to solve for the given constraints. The distinct criteria, therefore, do not make a huge difference.

In constellations with fewer decision variables (DowJones and FF49), the DCA has the highest share of feasible outcomes if a fixed number of iterations is chosen. In contrast, for data sets consisting of many assets (FTSE100 and NASDAQ100), the func_abs performs better. This result mirrors the downside of the fixed number of iterations. In settings with many decision variables the algorithm more often requires over 100 iterations to find a stationary point. As the stopping condition does not take this into account, it becomes too inflexible. Nevertheless, the CIs of the DCA are highly overlapping for most criteria and data sets. Only in a few cases one mechanism performs significantly better than all other options.

For the BDCA slightly different conclusions can be made. Across all data sets the func_abs delivers the highest number of feasible solutions. In settings with many decision variables the difference is also statistically significant compared to all other options. In case of an unfavorable initialization or a stricter constraint, the algorithm requires more than 100 iterations to output a feasible solution. In comparison to the iter criterion - which also performed well - the algorithm has more flexibility.

The right y-axis of Figure 5 shows the median CPU time in minutes for all feasible solutions. The DCA generally shows one profile. The fixed number of iterations require the highest median CPU time and between the other stopping conditions no bigger differences can be observed. However, two exceptions from this pattern occur for the FF49 and FTSE100 data set. Here the func_rel and func_abs condition have the by far highest median CPU time. For this data the DCA required many more iterations several times. While for the FTSE100 stricter constraint values caused the problem, the opposite was true for the FF49 data set. Table 2 again helps to explain these results. The FTSE100 data contains more risky assets, this makes it difficult to solve the portfolio selection problem for higher constraints. In contrast, the FF49 has the least risky data structure. For low constraint values the DCA can further slowly improve the objective function value such that the criterion is not triggered.

The results of the BDCA show the same profile as described for the baseline. One anomaly shows up for the NASDAQ100 data set where func_abs has the highest median CPU time. Here stricter constraints and challenging parameter settings caused the algorithm to run for more than 100 iterations. Compared to the DCA, the BDCA many times is significantly slower. Only for the FTSE100 data set the baseline requires more CPU time for all stopping criteria. However, it has to be noted that for data sets with more decision variables, the DCA has drastically fewer feasible data points. By taking a closer look at the results, it is evident that, especially for very high constraints, only a few feasible points are available. The median CPU time, therefore, is dominated by easily solvable settings. This distorts the comparison. Final conclusions should be made after repeating the settings another 400 times for the best stopping condition. From the statistical viewpoint, this will ensure that sufficient observations are available. The results subsequently can be evaluated by differentiating between different parameter settings.

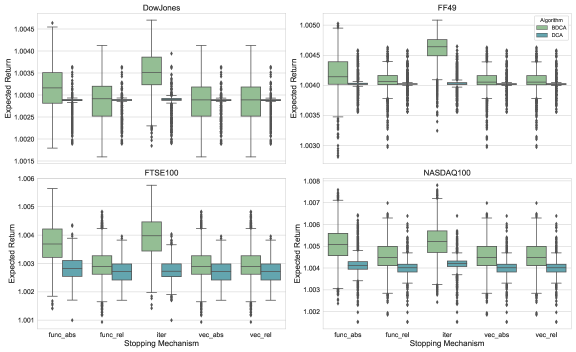

Figure 6 shows the expected returns for all feasible solutions per stopping criterion and data set in the form of boxplots. Overall, the conclusions of the first performance evaluation can be confirmed. The stopping criteria func_abs and iter achieve better results for all data sets compared to the other options. Whereas the outputs of the DCA are less sensitive to the stopping criteria, the results of the BDCA can significantly be improved if iter or func_abs is used. Several times the Interquartile Range (IQR) for these mechanisms is non-overlapping with the IQR of the other options. For the DCA, one should keep in mind that fewer data points are available. A direct comparison with respect to the volatility of the expected returns consequently should not be made. By focusing on the median values, the added line search step definitely helps to escape from local minima. Across data sets the median expected return of the BDCA is clearly above the value of the DCA for most stopping criteria.

For all upcoming analyses the func_abs has been selected as stopping criterion. In the first part of the experiment it provided the best trade-off between share of feasible solutions, computation time, and expected return. In comparison to the iter, it also indicates that the sequence has converged to a stationary point. All parameter settings are accordingly tested based on another 400 starting values per Dirichlet setting. In total the 500 repetitions per initialization and parameter combination then lead to 18,000 observations for each algorithm.

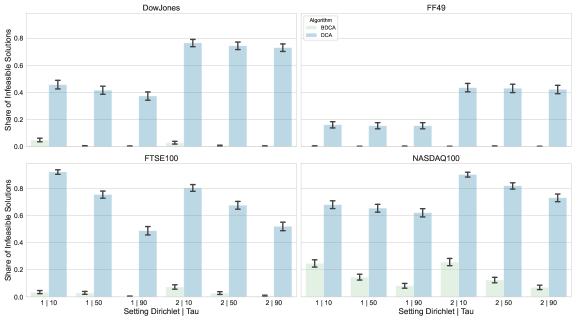

Figure 7 illustrates the share of infeasible solutions per Dirichlet setting, penalty parameter , and data set in form of bar plots. The highest number of feasible solutions can be unsurprisingly achieved if the strongest penalty parameter and nearly equal starting values are chosen independent of the algorithm. Nevertheless, the reliability of the algorithmic output can be drastically increased if a line search step is performed. While the results of the BDCA only slightly vary between settings, confirmed by overlapping CIs, the share of feasible solutions of the DCA significantly changes for distinct parameter combinations. Extreme initialization weights are especially challenging for the baseline. This confirms once again that the line search procedure significantly improves the capability to recover from an unfavorable initialization.

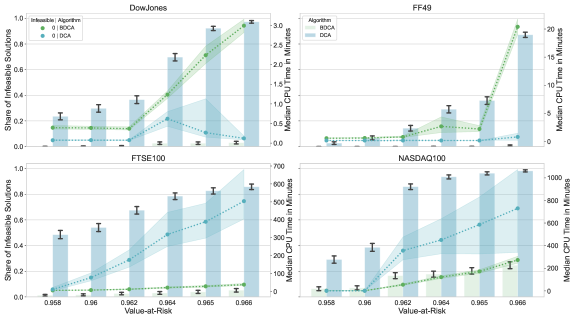

A similar analysis with respect to the distinct constraints is shown in Figure 8. Overall, for both algorithms the share of infeasible solutions rises for stricter constraints as expected. The data sets with more decision variables are also more challenging. This can be explained by the underlying data structure. The summary statistics shown in Table 2 indicate that the FTSE100 and NASDAQ100 include assets with greater risk. This leads to fewer possible asset combinations fulfilling the given constraints and consequently the portfolio selection problem is harder to solve. Independent of the requirements, the BDCA produces significantly fewer infeasible solutions. For stricter constraint settings the gap increases up to 85 percentage points. This validates the conclusions of the previous paragraph.

The y-axis on the right side of Figure 8 shows the median CPU time of all feasible solutions in the form of line plots including 95% CIs. Across data sets both algorithms require more time for stricter constraints. Whereas the DCA is faster for data sets with fewer decision variables, the BDCA evidently wins the race for the FTSE100 and NASDAQ100 data sets. The CIs are only overlapping for the two easiest constraints of the NASDAQ100 results. Other than that, the line search procedure significantly boosts the convergence. In settings with many decision variables the BDCA is subsequently up to 10 times faster than the DCA.

The last part of the first experiment is illustrated in Figure 9. The right y-axis shows the median expected return per constraint in the form of line plots including 95% CIs. Additionally, the best feasible solution per algorithm and constraint is illustrated. As expected, for both algorithms the maximum expected return globally decreases as the constraint becomes stricter. The only notable exception occurs for the DCA. The algorithm has grave problems to find a continuously declining sequence for the FTSE100 data set. Independent of the number of decision variables and constraints, the BDCA outputs higher expected returns. The DCA accordingly got stuck in local optima and did not find an efficient frontier.

Slightly different conclusions can be made for the median expected returns. Although the BDCA produced significantly higher results, both algorithms show some irregular patterns in the curves themselves. Especially for the NASDAQ100 data set the median returns are significantly rising and falling along the x-axis even though the constraint increases. This contradicts the requirements of the efficient frontier. For a given expected return level there should be no other asset combination that has lower risk.

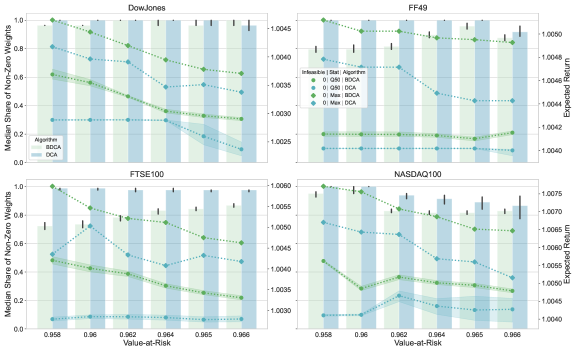

The problems of the BDCA may be explained by the change in the portfolio composition. The left y-axis of Figure 9 shows the median share of non-zero weights for all feasible solutions per constraint. Generally for stricter constraints a slight increase in diversification is observable. However, at two points this process is interrupted by a significant drop in the median share of non-zero weights. The first exception occurs for the FF49 data set between the constraints and and the second one from to for the NASDAQ100 data set. Exactly at these points the continuously decreasing sequence of median expected returns is also violated. Figure 8 further shows that at these points the share of feasible solutions changes. Stricter constraints, therefore, might have led to an exclusion of more unfavorable starting points and parameter settings that lead to many non-zero weights. For easier constraints these points were still good enough to output a feasible solution, but the algorithm likely got stuck into a bad local minimum. The results, therefore, adversely influence the median expected return.

For the DCA this pattern of diversification generally does not come to light. Independent of the constraint, the median values mainly fluctuate around 90-100% non-zero weights. The violations of the continuously decreasing sequence of median expected returns also only coincides a few times with a significant change in the portfolio composition or in the share of feasible solutions. However, Figure 7 illustrates that the DCA has more infeasible solutions for extreme starting points. This fact, in combination with the tendency to get stuck into local minima, might explain the output. The median non-zero weights are generally dominated by feasible solutions of the first Dirichlet setting where the optimization terminated too early. In these cases more extreme weights could not unfold over the iterations.

In comparison to the BDCA, the DCA chooses significantly more assets to construct the portfolios for most data sets. As the line search procedure always starts on the boundary of the feasible set, it is easier to find weight combinations including zero values. Nevertheless, even for the BDCA, the median share of non-zero weights is never below . From a practical point of view, therefore, it might be reasonable to extend the optimization framework with a sparsity term to better control for the number of chosen assets.

5.2. Experiment 2

The first numerical experiment confirmed that the reliability of the DCA highly depends on the chosen initialization weights and the selected penalty parameter. In comparison to the BDCA, the algorithm delivered worse results in this respect, measured by the share of feasible solutions. The final assessment of the efficiency was more difficult. Although the DCA had a smaller median run time for lower dimensional data sets, it required much more time in settings with many decision variables. By taking the quality of algorithmic output into account, the faster run time also came at the cost of worse median expected returns. For all data sets the Q50 of the BDCA was significantly closer to the efficient frontier.

To cope with performance differences, the second numerical experiment is conducted based on a fixed cost approach. This simplifies a fair comparison between efficiency and quality of algorithmic output. In the experiments the CPU time is tracked until a fixed budget is reached or until the algorithm finds the best possible objective function value - if the optimum is known. Otherwise, the best known solution can be used to substitute the unknown target.

Unfortunately, for the available data sets the optimal solutions are unknown. The best known solution, therefore, is represented by the objective function value that the BDCA achieves after iterations. The CPU time of the DCA is subsequently tracked until it finds at least the same value or until iterations are reached. The set up is then repeated for 500 different starting points using the first Dirichlet setting and the strongest penalty parameter introduced in Subsection 5.1. Under these circumstances both algorithms were able to find the highest share of feasible solutions across data sets. The additional BDCA parameters are again chosen as and . An overview with all parameters is provided by Table 6.

| Experiment | Parameter | Values |

| 2 | 0.958, 0.960, 0.961, 0.962, 0.963 | |

| 0.964, 0.965, 0.966, 0.967, 0.968 | ||

| 90 | ||

| 0.001 | ||

| 0.5 |

Table 7 summarizes the results of the fixed cost experiment. The left part of the table shows ratios between the results of the DCA and BDCA. For the number of iterations, the CPU time, and the objective function value , the median result of the DCA has been divided by the median result of the BDCA to visually simplify the numbers. Infeasible solutions have not been excluded from the evaluation.

| Iter | CPU Time | Infeasible | Max | |||||||||

| Data Set | a | Q50 | L | Q50 | U | Lower | Q50 | Upper | D | B | DCA | BDCA |

| DowJones | 0.958 | 10.0 | 5.0 | 5.1 | 5.1 | 0.9985 | 0.9985 | 0.9985 | 0 | 5 | 1.003052 | 1.004786 |

| 0.959 | 10.0 | 5.0 | 5.1 | 5.1 | 0.9986 | 0.9986 | 0.9986 | 0 | 5 | 1.003052 | 1.004686 | |

| 0.960 | 10.0 | 5.0 | 5.1 | 5.1 | 0.9987 | 0.9987 | 0.9987 | 0 | 4 | 1.003052 | 1.004602 | |

| 0.961 | 10.0 | 5.0 | 5.1 | 5.1 | 0.9988 | 0.9988 | 0.9988 | 0 | 7 | 1.003052 | 1.004469 | |

| 0.962 | 10.0 | 5.1 | 5.1 | 5.2 | 0.9989 | 0.9989 | 0.9989 | 0 | 4 | 1.003052 | 1.004369 | |

| 0.963 | 10.0 | 5.1 | 5.1 | 5.2 | 0.9990 | 0.9990 | 0.9991 | 0 | 1 | 1.003027 | 1.004153 | |

| 0.964 | 10.0 | 5.0 | 5.0 | 5.1 | 0.9991 | 0.9992 | 0.9992 | 86 | 15 | 1.003003 | 1.004076 | |

| 0.965 | 10.0 | 4.9 | 5.0 | 5.1 | 0.9943 | 0.9989 | 0.9991 | 287 | 12 | 1.003038 | 1.003909 | |

| 0.966 | 10.0 | 4.9 | 5.0 | 5.1 | 0.9112 | 0.9187 | 0.9259 | 489 | 8 | 1.003007 | 1.003791 | |

| 0.967 | 10.0 | 4.8 | 4.9 | 5.0 | 0.8190 | 0.8277 | 0.8342 | 498 | 11 | 1.002892 | 1.003624 | |

| 0.968 | 10.0 | 4.6 | 4.7 | 4.8 | 0.7302 | 0.7402 | 0.7482 | 500 | 15 | - | 1.003562 | |

| FF49 | 0.958 | 10.0 | 6.5 | 6.5 | 6.5 | 0.9989 | 0.9989 | 0.9989 | 0 | 0 | 1.004051 | 1.005272 |

| 0.959 | 10.0 | 6.4 | 6.5 | 6.5 | 0.9989 | 0.9989 | 0.9989 | 0 | 0 | 1.004051 | 1.005270 | |

| 0.960 | 10.0 | 6.4 | 6.4 | 6.5 | 0.9989 | 0.9989 | 0.9989 | 0 | 0 | 1.004051 | 1.005232 | |

| 0.961 | 10.0 | 6.4 | 6.5 | 6.5 | 0.9989 | 0.9989 | 0.9990 | 0 | 0 | 1.004051 | 1.005248 | |

| 0.962 | 10.0 | 6.5 | 6.5 | 6.5 | 0.9990 | 0.9990 | 0.9990 | 0 | 0 | 1.004051 | 1.005194 | |

| 0.963 | 10.0 | 6.4 | 6.5 | 6.5 | 0.9990 | 0.9990 | 0.9990 | 0 | 0 | 1.004051 | 1.005143 | |

| 0.964 | 10.0 | 6.5 | 6.5 | 6.5 | 0.9991 | 0.9991 | 0.9991 | 0 | 0 | 1.004051 | 1.005099 | |

| 0.965 | 10.0 | 6.5 | 6.6 | 6.6 | 0.9991 | 0.9991 | 0.9991 | 0 | 0 | 1.004051 | 1.005085 | |

| 0.966 | 10.0 | 6.0 | 6.1 | 6.2 | 0.9991 | 0.9992 | 0.9992 | 140 | 2 | 1.004064 | 1.005032 | |

| 0.967 | 10.0 | 5.9 | 6.0 | 6.2 | 0.9829 | 0.9887 | 0.9941 | 379 | 2 | 1.004034 | 1.004986 | |

| 0.968 | 10.0 | 5.7 | 5.9 | 6.1 | 0.9174 | 0.9239 | 0.9345 | 489 | 3 | 1.004220 | 1.004913 | |

| FTSE100 | 0.958 | 10.0 | 6.4 | 6.6 | 6.7 | 0.9984 | 0.9984 | 0.9985 | 183 | 46 | 1.004644 | 1.005938 |

| 0.959 | 10.0 | 6.8 | 7.2 | 8.0 | 0.9985 | 0.9986 | 0.9986 | 177 | 38 | 1.004504 | 1.005765 | |

| 0.960 | 10.0 | 7.1 | 7.9 | 9.4 | 0.9985 | 0.9986 | 0.9987 | 191 | 54 | 1.004193 | 1.005729 | |

| 0.961 | 10.0 | 8.5 | 9.5 | 10.7 | 0.9986 | 0.9987 | 0.9987 | 179 | 41 | 1.004247 | 1.005456 | |

| 0.962 | 10.0 | 9.5 | 10.8 | 12.0 | 0.9986 | 0.9987 | 0.9988 | 201 | 44 | 1.004446 | 1.005495 | |

| 0.963 | 10.0 | 9.7 | 11.2 | 12.3 | 0.9987 | 0.9988 | 0.9989 | 224 | 41 | 1.004306 | 1.005316 | |

| 0.964 | 10.0 | 9.5 | 10.6 | 12.0 | 0.9988 | 0.9989 | 0.9990 | 212 | 56 | 1.004285 | 1.005005 | |

| 0.965 | 10.0 | 9.4 | 10.8 | 12.1 | 0.9988 | 0.9988 | 0.9989 | 233 | 44 | 1.004111 | 1.004939 | |

| 0.966 | 10.0 | 10.6 | 12.2 | 14.0 | 0.9988 | 0.9989 | 0.9990 | 260 | 60 | 1.003995 | 1.004958 | |

| 0.967 | 10.0 | 10.1 | 11.6 | 13.2 | 0.9987 | 0.9989 | 0.9990 | 286 | 64 | 1.003829 | 1.004692 | |

| 0.968 | 10.0 | 8.0 | 9.8 | 11.8 | 0.9987 | 0.9989 | 0.9991 | 291 | 70 | 1.003854 | 1.004721 | |

| NASDAQ100 | 0.958 | 10.0 | 6.0 | 6.0 | 6.0 | 0.9991 | 0.9992 | 0.9993 | 88 | 89 | 1.006652 | 1.007838 |

| 0.959 | 10.0 | 6.0 | 6.0 | 6.1 | 0.9994 | 0.9995 | 0.9996 | 99 | 124 | 1.006518 | 1.007626 | |

| 0.960 | 10.0 | 6.0 | 6.1 | 6.1 | 0.9997 | 0.9998 | 0.9999 | 146 | 130 | 1.006449 | 1.007477 | |

| 0.961 | 10.0 | 6.1 | 6.2 | 6.2 | 0.9996 | 0.9998 | 0.9999 | 212 | 168 | 1.006689 | 1.007417 | |

| 0.962 | 10.0 | 7.6 | 8.8 | 10.5 | 0.9991 | 0.9994 | 0.9998 | 238 | 148 | 1.006376 | 1.007216 | |

| 0.963 | 10.0 | 6.8 | 8.1 | 9.7 | 0.9986 | 0.9989 | 0.9992 | 293 | 121 | 1.006190 | 1.007033 | |

| 0.964 | 10.0 | 6.1 | 7.3 | 8.7 | 0.9789 | 0.9981 | 0.9986 | 336 | 97 | 1.006261 | 1.006896 | |

| 0.965 | 10.0 | 6.5 | 7.7 | 9.4 | 0.9747 | 0.9977 | 0.9984 | 347 | 118 | 1.005642 | 1.006712 | |

| 0.966 | 10.0 | 5.0 | 6.8 | 8.2 | 0.8625 | 0.9084 | 0.9550 | 399 | 126 | 1.005547 | 1.006675 | |

| 0.967 | 10.0 | 4.8 | 5.6 | 7.0 | 0.6737 | 0.7889 | 0.8686 | 441 | 154 | 1.005255 | 1.006332 | |

| 0.968 | 10.0 | 2.6 | 3.3 | 4.2 | 0.5121 | 0.5982 | 0.6883 | 472 | 220 | 1.005491 | 1.006261 | |

To mirror the uncertainty of the estimates, 95% bootstrap CIs have also been added. As per data set 33 intervals are constructed simultaneously, the level again has been adjusted to using the Bonferroni method. For the iterations the CIs are not shown in Table 7 because the upper and lower values always coincide with the result of the median. In most of the experimental setups, the DCA, therefore, never reached the objective function value of the BDCA. This leads to a termination as soon as no more iterations remain in the budget.

The right part of Table 7 shows the number of infeasible solutions and the best feasible solution Max per algorithm and constraint.

The results for the data sets with fewer decision variables (DowJones and FF49) are very similar. Independent of the constraint, the DCA nearly always needs 10 times as many iterations and around 5 to 6.5 times more CPU time compared to the BDCA.

Whereas for the FF49 data set the highest difference in the objective function is around 8%, the gap increases up to 26% for the DowJones data as the constraint becomes stricter. As mentioned in Subsection 5.1, the FF49 index generally has a less risky composition of stocks which makes it easier to solve the portfolio selection problem for the given constraints . This is formally confirmed by the number of infeasible solutions, independent of the algorithm.

The BDCA never produces more than 15 infeasible solutions per 500 repetitions, while the baseline has great difficulties with stricter settings. The number of infeasible solutions increases up to 480-500 cases.

By considering the best solution Max , another drawback of the DCA comes to light. Whereas for both data sets the values of the BDCA are a strictly decreasing sequence as the constraint becomes stricter, the sequence of the DCA shows either no difference, or irregular fluctuations. Additionally, the expected returns of the DCA are always lower than the best solution of the BDCA. The outputs of the baseline, therefore, violate the requirements for an efficient frontier.

The lower part of Table 7 shows the results for data sets with more decision variables (FTSE100 and NASDAQ100). Independent of the constraint, the DCA always needs 10 times as many iterations and up to 12 times more CPU time compared to the BDCA. This again shows that in most cases the baseline ran until the fixed budget was exhausted.

The ratio between the objective function values remains negligible for the FTSE100 data set. Only for the NASDAQ100 data does the difference increases up to 40% for stricter settings. The latter mentioned data set consists of slightly riskier assets. This leads to a portfolio selection problem that is more difficult to solve. It is formally confirmed by the number of infeasible solutions independent of the algorithm. In the direct comparison between approaches, it is again observable that the DCA produces fewer feasible solutions compared to the BDCA. This again confirms a higher robustness of the challenger with respect to the starting points.

Independent of the data set, the best solution for each shows some irregular fluctuations for the DCA as the constraint becomes stricter. For the FTSE100 data the sequence of the BDCA is also not strictly decreasing. Nevertheless, the violations are relatively small compared to the ones from the baseline. Further, the challenger always finds higher expected returns compared to the DCA, independent of the data set. It, therefore, can be confirmed that the results of the BDCA are closer to the efficient frontier.

6. Conclusion

For over 70 years the MV portfolio selection problem has been a topic of great interest in financial academic literature. Although many extensions - modelling the specific requirements of financial markets more accurate - have been proposed, the accompanying increase in complexity often leads to non-convex optimization problems being much harder to handle. As a result, many common algorithms reach the limits of their capabilities when applied to big data.