Strategically-Robust Learning Algorithms for Bidding in First-Price Auctions

Abstract

Learning to bid in repeated first-price auctions is a fundamental problem at the interface of game theory and machine learning, which has seen a recent surge in interest due to the transition of display advertising to first-price auctions. In this work, we propose a novel concave formulation for pure-strategy bidding in first-price auctions, and use it to analyze natural Gradient-Ascent-based algorithms for this problem. Importantly, our analysis goes beyond regret, which was the typical focus of past work, and also accounts for the strategic backdrop of online-advertising markets where bidding algorithms are deployed—we prove that our algorithms cannot be exploited by a strategic seller and that they incentivize truth-telling for the buyer.

Concretely, we show that our algorithms achieve regret when the highest competing bids are generated adversarially, and show that no online algorithm can do better. We further prove that the regret improves to when the competition is stationary and stochastic. Moving beyond regret, we show that a strategic seller cannot exploit our algorithms to extract more revenue on average than is possible under the optimal mechanism, i.e., the seller cannot do much better than posting the monopoly reserve price in each auction. Finally, we prove that our algorithm is also incentive compatible—it is a (nearly) dominant strategy for the buyer to report her values truthfully to the algorithm as a whole.

1 Introduction

Advertising is an indispensable part of the internet economy. It allows online platforms (like Google and Meta) to monetize their services by charging advertisers for the opportunity to display their ads to users. This is operationally achieved through a online market/exchange where advertising opportunity is sold to interested advertisers. The mechanism of choice for these online advertising markets is real-time auctions: anytime a user visits the platform, an auction is run to determine the advertiser who will get to display their ad to that user, and the payment to be charged for that opportunity. Each of these auctions runs in less than a few milliseconds and advertisers typically participate in millions of such auctions as part of their advertising campaign. Given the speed and scale of these auction markets, all bidding in done programmatically—each advertiser employs an automated bidding algorithm, which is often provided as a service by the platform itself or a third-party demand-side platform (DSP). This algorithm takes an input high-level objectives like value-per-click, targeting criteria etc., and then bids on behalf of the advertiser in each of the auctions with the goal of maximizing her utility.

Until a few years ago, the second-price auction and its generalizations were the dominant auction formats in the online advertising, but that is no longer the case with the transition of the display-advertising industry111Display advertising refers to graphic advertising through banners, text, images, video, and audio. from second-price auctions to first-price auctions (Wong, 2021). Unlike second-price auctions, where truthful bidding is optimal, bidding in first-price auctions is highly non-trivial and presents the need for non-trivial bidding algorithms. Combined with the colossal scale of online advertising markets and the accompanying abundance of data, this transition has created a need for online algorithms for bidding in repeated first-price auctions that can learn from data.

Thus motivated, a recent line of work (Balseiro et al., 2022; Han et al., 2020b, a; Zhang et al., 2022; Wang et al., 2023; Badanidiyuru et al., 2023) has proposed algorithms for a variety of input models (adversarial, stochastic etc.) and feedback structures (bandit, partial, full etc.). These works analyze the problem of bidding in repeated first-price auctions through the lens of online learning, and consequently focus on minimizing regret against the best fixed bidding strategy in hindsight. However, although regret is an important aspect of any learning algorithm, it completely ignores the strategic nature of the markets in which these algorithms are deployed—both the buyer (advertiser) and the seller (platform) can attempt to manipulate the algorithm in order to obtain better revenue/utility. Consequently, bidding algorithms with strong regret guarantees can perform very poorly when deployed in markets with strategic agents. Braverman et al. (2018) showed that this is true of all mean-based algorithms, which includes bidding algorithms based on popular paradigms like Exponential Weights/Hedge (Freund and Schapire, 1997), EXP3 (Auer et al., 2002), Follow-the-Regularized-Leader (FTRL) etc., and importantly includes most algorithms proposed in recent works (see Subsection 1.2). In particular, Braverman et al. (2018) showed that any mean-based algorithm is susceptible to manipulation on either side of the market:

-

•

A seller who knows that the buyer is employing a mean-based algorithm can extract more revenue on average than is possible under the optimal single-shot mechanism (posting the monopoly reserve price). Moreover, she can do so by simply posting a sequence of decreasing reserve prices.

-

•

A buyer can improve her utility by misreporting her values to any automated bidding algorithm that is mean based.

| Regret | Strategic | Incentive | Complexity per Iteration | |||

| Adversarial | Stochastic | Robustness | Compatibility | Time | Space | |

| Mean-Based | ||||||

| BMSW’18 | ||||||

| Algorithm 1 | ||||||

| Algorithm 2 | ||||||

Braverman et al. (2018) go on to show the existence of an algorithm that attains sub-linear regret while being resistant to manipulation by the seller and incentivizing truthful reporting by the buyer. However, it is engineered to achieve this strategic robustness and is not very natural, in addition to being computationally expensive and suffering from sub-optimal regret scaling (see Table 1).222Braverman et al. (2018) study a model with possible values and provide guarantees in terms of . Here we use as the discretization because it optimally trades off regret and strategic robustness in their guarantees. In light of the vulnerability of all natural mean-based algorithms to strategic manipulation, one might be tempted to conclude that it is necessary to engineer algorithms for strategic robustness and bear the associated cost in regret/computation. However, such a conclusion would ignore perhaps the most important/popular data-driven optimization algorithm in existence: (Online) Gradient Descent/Ascent, which is not a mean-based algorithm. In fact, the literature on bidding in first-price auctions, including Braverman et al. (2018), is marked by a conspicuous lack of results for Gradient Ascent. The current paper aims to end that streak and provide a comprehensive analysis of Online Gradient Ascent, covering both regret and strategic robustness.

1.1 Major Contributions

We study the problem of designing algorithms for a buyer who participates in sequential first-price auctions with a continuum of values and discrete bids. We assume that the value of the buyer is drawn independently from some distribution (with bounded density) in each auction and she observes this value before bidding. Moreover, motivated by practice, we assume full feedback—the maximum of the highest competing bid and the reserve price is revealed after each auction. The performance of algorithms is measured using regret against the best fixed bidding strategy (map from values to bids) in hindsight. Below, we provide a brief overview of our results, and summarize them in Table 1.

Concave Formulation. The bedrock of our algorithms and analysis is a novel concave formulation for pure-strategy bidding in first-price auctions (Theorem 1). In particular, we propose a change-of-variables transformation that maps each (monotonic) pure bidding strategy to the probability distribution over bids induced by that strategy and the randomness in the buyer’s value. Importantly, while utility is not concave as a function of the bidding strategy (which itself is an infinite-dimensional object), we show that it is concave as a function of the induced probability distribution over bids. As the set of possible bids is finite (e.g. discretized to cents), we are able to transform the problem of finding the optimal bidding strategy in first-price auctions from an infinite dimensional non-concave problem to a finite-dimensional concave one. Notably, this transformation does not impose any regularity conditions on the value distribution , as is often the case with such transformations in other contexts (like Bulow and Roberts 1989 and Kinnear et al. 2022). To the best of our knowledge, this is the first unconditional concave formulation for pure-strategy bidding in first-price auctions, and may be of independent interest. In this work, we leverage it to propose two algorithms: Algorithm 1 requires knowledge of the value distribution and simply implements Online Gradient Ascent for the online concave maximization problem implied by our formulation; Algorithm 2 does not require knowledge of the value distribution and instead implements Online Gradient Ascent for utility functions corresponding to the uniform value distribution.

Regret Guarantees. Algorithm 1 directly inherits the -regret guarantee enjoyed by Online Gradient Ascent under adversarial input (Proposition 1). Using a potential-function argument, we also establish a -regret guarantee for Algorithm 2 against adversarial highest competing bids (Theorem 3). Moreover, we show that our guarantees are tight—no algorithm can achieve -regret against adversarial competition (Proposition 2). When the competition is stochastic, i.e., the maximum of the highest competing bid and the reserve price is i.i.d. from the some distribution, our concave reformulation yields a strongly-concave optimization problem; which allows us to prove that Algorithm 1 achieves regret (Theorem 7).

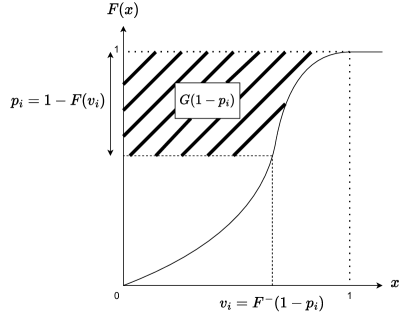

Strategic Robustness. If a buyer employs either of our algorithms for bidding, we prove that the seller cannot extract more revenue than from her in total, where is the optimal revenue obtainable under any single-shot mechanism for value distribution , i.e, is the revenue obtained by posting the monopoly reserve price. Put another way, the seller cannot exploit our algorithms to extract (substantially) more revenue than on average (Theorem 2 and Theorem 4). In particular, the seller does not gain by dynamically changing the reserve price and is best off just posting the monopoly reserve price in each auction. This robustness to strategic manipulation is critical in practice because platforms often have detailed knowledge of the bidding algorithms of the advertisers (they might even design them!). Our algorithms also lead to more stability by removing the incentive for the seller to manipulate the bidding algorithm through dynamic reserve prices. On the theoretical front, this strategic robustness of Online Gradient Ascent is very surprising when contrasted with the strategic vulnerability of FTRL with the Euclidean regularizer (which is a mean-based algorithm), because the only difference between the two is that the projection is agile in the former and lazy in the latter (see Hazan (2016) for definitions). Moreover, unlike the proof of Braverman et al. (2018), our proof proceeds directly through a simple potential-function argument and does not require establishing incentive-compatibility first, which may be of independent interest. Finally, Algorithm 2 is also strategically robust in the multi-buyer setting where all of the buyers simultaneously use it to bid. In that setting, it limits the seller revenue to , where is the revenue of the optimal mechanism for buyers with as the prior. Once again, this implies that the seller cannot extract more average revenue than is possible under the optimal single-shot mechanism (Theorem 6).

Incentive Compatibility. Bidding algorithms are deployed as automated agents that bid on behalf of the buyers (advertisers) in the auctions. The buyers provide high-level information about their value for winning these auctions by specifying their value per click/conversion/impression and targeting criteria, which is then used by the automated bidding algorithm to optimize utility. As the high-level information is private to the buyer, one cannot simply assume that she will reveal it truthfully to the algorithm. If the algorithm incentivizes misreporting of values by the buyer, it hurts the seller because she does not obtain reliable data about the values of the buyer (which is very valuable for experimentation), and it hurts the buyer because it imposes the burden of computing the best misreporting strategy. Algorithm 2 does not suffer from these shortcomings and incentivizes truthful reporting of values by the buyer. Formally, we show that the excess utility over truthful reporting earned through any misreport of values is no more than (Theorem 5). In other words, the online algorithm itself is (approximately) incentive compatible with respect to its input. Once again, this is surprising because FTRL with the Euclidean regularizer is not incentive compatible, which reinforces the importance of lazy versus agile projections for robustness to manipulation by strategic agents.

1.2 Additional Related Work

The first-price auction is arguably the most popular auction format in human history. It has been studied extensively in the economics literature, where the primary focus has been on the analysis of equilibria. Since our focus is on developing data-driven bidding algorithms, we do not discuss the work on equilibrium analysis here, and refer the reader to standard texts on auction theory like Krishna (2009) and Milgrom (2004). Similarly, we omit the work on equilibrium analysis in computer science and operations research, and refer to recent works of Chen and Peng (2023) and Balseiro et al. (2023) for an overview. Finally, extensive work has been done at the intersection of auctions and data-driven optimization, the vast majority of which has focused on the mechanism-design problem faced by the seller. We refer to the survey by Nedelec et al. (2022) for a detailed discussion of learning algorithms for buyers and sellers in repeated auctions, and focus here exclusively on relevant work on bidding algorithms for first-price auctions and strategic aspects of learning.

Motivated by the change of auction format in the Display Advertising industry, Balseiro et al. (2022) analyze bidding algorithms for first-price auctions. They assume that the buyer only observes binary feedback, i.e., whether or not she won the auction, and model it as a contextual bandit problem with potential cross-learning between contexts. When the highest competing bids are stochastic, they propose a UCB-based algorithm which achieves regret, whereas when the highest competing bids are adversarially generated, they propose an EXP3-based algorithm which achieves regret (this was later improved to regret by Schneider and Zimmert (2024)). Han et al. (2020b) also study a model where the highest competing bids are stochastic, albeit under a different partial-feedback model where only the winning bid is revealed at the end of each auction. They propose algorithms that achieve regret and allow for infinitely many possible bids. Han et al. (2020a) study a model where both the values and the highest competing bids are adversarial, but restrict the space of benchmark strategies to be Lipschitz. They propose an algorithm that runs the Exponential Weights Algorithm over a suitable cover of the space of all Lipschitz bidding strategies, and prove a -regret guarantee for it. Moreover, they show that a computationally-expensive version of their algorithm attains -regret when the benchmark strategies are monotonic instead of Lipschitz. Zhang et al. (2022) extend the algorithm and analysis of Han et al. (2020a) to incorporate hints about the highest competing bids.

Badanidiyuru et al. (2023) study a contextual model of first-price auctions in which the highest competing bids are the sum of a linear function of the contexts and a log-concave stochastic noise term. They propose algorithms that attain regret under different feedback and informational assumptions. Wang et al. (2023) analyze repeated first-price auctions with a global budget constraint. When the highest competing bids are stochastically generated, they propose dual-based algorithms which achieve regret under both full and partial feedback. Importantly, all of these aforementioned algorithms are mean-based, and consequently they are neither strategically robust nor incentive compatible (Braverman et al., 2018). Feng et al. (2018) and Cesa-Bianchi et al. (2023) investigate bidding in repeated auctions when the buyer does not know her own value, and propose algorithms that compete against the best static bid in hindsight. We assume that the buyer observes her value before bidding and use the best strategy in hindsight as the benchmark, and therefore our results are not directly comparable. Kinnear et al. (2022) study the different but related problem of procuring advertising opportunity for contract fulfilment. They analyze the full-information optimization problem against stochastic competition, and reformulate it as a convex optimization problem in the space of winning probabilities. Unlike our unconditional concave formulation, their convex formulation for first-price auctions requires the competing bid distribution to have full support and satisfy a log-concavity-like assumption.

Finally, our paper is closely connected to a growing body of literature on strategizing against no-regret learning algorithms in games. This area of work is concerned with the two questions of: 1. how should you best-respond if you know other players in a repeated game choose their actions according to a learning algorithm? and 2. what learning algorithm should you choose to be robust to the strategic behavior of other players? Braverman et al. (2018) was one of the first works to investigate these questions, specifically for the setting of non-truthful auctions – their work was later generalized to the prior-free setting Deng et al. (2019b), the setting of multiple buyers Cai et al. (2023), and the setting of selecting parameters for bidding algorithms Kolumbus and Nisan (2022a, b). Since then, these questions have also been studied in the settings of general games Deng et al. (2019a); Brown et al. (2023), Bayesian games Mansour et al. (2022), contract design Guruganesh et al. (2024) and Bayesian persuasion Chen and Lin (2023). Interestingly, all previous-known algorithms achieving this sense of strategic robustness required some form of swap-regret minimization algorithm (with Deng et al. (2019a); Mansour et al. (2022) even showing that low swap regret is a necessary property for a learning algorithm to be generically strategically-robust across all games): our work is the first to our knowledge to achieve these properties without explicitly minimizing some form of swap regret.

2 Model

Notation.

denotes the set of non-negative reals. We use boldface for vectors. If a vector is indexed by time, like , then its -th component is denoted by . Throughout the paper, represents the Euclidean norm, i.e., .

Consider a buyer who participates in sequential first-price auctions. In each auction , her value for the item is drawn independently from a distribution with CDF , and bounded density such that . In line with practice, we will assume that the set of possible bids is finite and equally spaced (e.g., multiples of cents): there are possible bids , where for some . We use to denote the minimum bid needed to win at time , i.e., is the maximum of the highest competing bid and the reserve price. To simplify terminology, we will treat the reserve price as an additional bid submitted by the seller and often refer to simply as the highest competing bid.

In auction , the following sequence of events takes place:

-

•

The buyer observes her value and places a bid .

-

•

The buyer wins the item and pays if . If , she does not win the item and does not make any payment.

-

•

The buyer observes the highest competing bid .333Many platforms reveal the minimum bid needed to win in practice to help advertisers bid more efficiently, e.g., see https://support.google.com/authorizedbuyers/answer/12798257?hl=en.

As the value can lie anywhere in , the buyer effectively specifies a bidding strategy at each time , where is the bid in auction if her value is . When the buyer employs the strategy and the highest competing bid is , her expected utility is given by

An online bidding algorithm for the buyer is a (potentially randomized) procedure which specifies a bidding strategy at each time , based only on the information observed till time and the value . We will measure the learning rate of an online algorithm by its (pseudo) regret compared to the best static bidding strategy . For the sequence of highest competing bids , we define the regret of algorithm as

Note that the space of bidding strategies is infinite dimensional and the map is non-convex, which makes online optimization over the set of bidding strategies unwieldy. As our first step, we circumvent this hurdle and show that the problem of utility maximization in first-price auctions over pure strategies can be formulated as a finite-dimensional concave maximization problem in the space of bidding probabilities. This reformulation forms the cornerstone of all our algorithms and results.

3 Concave Formulation

Consider a buyer who participates in a single-shot first-price auction where the set of possible bids are . As before, assume that her value for the item is drawn from an absolutely continuous distribution with CDF and density . Moreover, assume that the highest competing bid is drawn from , and that this draw is independent of the value . Independence of the value and the highest competing bid is a common assumption in the literature (for example, Han et al. 2020b; Balseiro et al. 2022; Wang et al. 2023) on first-price auctions, and holds in practice for thick markets.

Let be a bidding strategy of the buyer, i.e., she bids when her value is . For this strategy and highest competing bid distribution , the expected utility of the buyer is given by

We first simplify the space of strategies by showing that it is sufficient to restrict attention to non-decreasing and left-continuous strategies that never overbid. In particular, the optimal strategy that optimizes the utility at each value always satisfies these properties (if ties are broken appropriately).

Lemma 1.

For each , define to be the bid which maximizes the quantity , breaking ties in favor of smaller bids. Then . Moreover, is non-decreasing, left continuous, and satisfies .

In the rest of this section, we will assume that the bidding strategy is non-decreasing, left-continuous and satisfies for all . Then, if we set for all , we get and for all . In other words, we can alternately parameterize the bidding strategy in terms of the value thresholds such that the bid is constant between any two consecutive thresholds. In particular, note that because for all . Now, we can rewrite the utility function in terms of value thresholds as follows:

| (1) |

Note that this transformation allows use to reduce the infinite-dimensional optimization problem to a finite-dimensional one , which is a considerable simplification. However, since can be arbitrary, may not be convex, we are still left with a non-convex problem. Getting rid of this non-convexity requires yet another change of variables, which we outline next.

To motivate our approach, we first rewrite in terms of the generalized inverse of , defined as . To do so, we use the fact that, if is the uniform random variable over , then is distributed according to the CDF . Therefore,

where the third equality follows from part (5) of Proposition 1 of Embrechts and Hofert (2013). This allows us to simplify (3) further and write

| (2) |

Now, observe that since is non-decreasing, the function is concave. Formally, for and , we have

where the inequality follows from the fact that is non-decreasing. As is continuous, the above inequality implies that is concave.

This observation motivates our final change of variables. Let denote the probability that the buyer submits a bid greater than or equal to , i.e., set for all (define for convenience). Then, , and we can rewrite (2) in the form

| (3) |

As is concave, the function is a positive linear combination of concave functions and purely linear terms, and therefore itself is concave. Thus we have derived a concave formulation for the utility maximization problem, and (surprisingly) done so without relying on randomized bidding strategies. We summarize this result in the following theorem, which delineates the transformation between the space of bidding strategies and the space of bidding probabilities .

Theorem 1.

The following statements hold for all value distributions and competing bid distributions :

-

1.

is concave.

-

2.

Let be a non-decreasing left-continuous bidding strategy with for all , and set for all . Then, and .

-

3.

Let and define bidding strategy as

and . Then, .

Having formulated the problem of bidding in first-price auctions as a concave maximization problem, we can now exploit the powerful machinery of Online Convex Optimization (Shalev-Shwartz 2012; Hazan 2016) in order to develop learning algorithms for bidding in first-price auctions. First, in Section 4, we propose and analyze a natural Online Gradient Ascent algorithm based on our concave formulation. We prove that, in addition to attaining the optimal regret scaling of , it is robust to strategic reserve pricing by the seller. However, the direct application of Online Gradient Ascent to the concave formulation requires knowledge of the value distribution , which may not always be available. In Section 5, we propose another Gradient-Ascent-based algorithm which does not require the knowledge of the value distribution . It also attains -regret while being robust to strategic reserve pricing by the seller, and is additionally incentive compatible as an autobidding algorithm for the buyer.

4 Gradient Ascent for Known Value Distributions

In this section, we will assume that the value distribution is known to the buyer ahead of time (before the first auction). Leveraging the concave formulation of Theorem 1, we propose an algorithm (Algorithm 1) that runs Gradient Ascent in the space of bidding probabilities with reward functions . To determine the bid in each auction, it translates the iterates of Gradient Ascent to bidding strategies by using the change-of-variables equivalence established in Theorem 1.

| (4) |

Before diving into the analysis of Algorithm 1, we take a deeper look at its updates to build intuition. First observe that, for highest competing bid , we can rewrite the expected utility as

| (5) |

In particular, this implies that the gradient is given by

Ignoring the projection step, i.e., assuming , we can see that Algorithm 1 updates to

-

•

increase the probability of bidding because for all ,

-

•

decrease the probability of bidding or higher for all .

This is intuitive because is the optimal bid against the highest competing bid of , and bidding strictly higher only increases the payment without increasing the chance of winning the item. Although the projection step is important and significantly complicates the analysis, we will largely ignore it here to build intuition. Importantly, as we show in Appendix B, it is possible to execute the projection step in time. In fact, we give a (quasi) closed-form expression for in terms of in Lemma 2.

The gradient also has an economic interpretation, wherein the -th component is simply the change in utility from bidding instead of :

-

•

If , there is no change in utility from bidding instead.

-

•

When , bidding increases the utility by when compared to the losing bid of .

-

•

If , bidding increases the payment by in comparison to . Since both and result in a win, this reduces the utility by .

4.1 Regret Guarantees

We now investigate the regret guarantees of Algorithm 1. Since Algorithm 1 is a variant of Online Gradient Ascent, it inherits the low-regret bounds enjoyed by that family of algorithms. In particular, it inherits the regret bound of Online Gradient Descent (e.g., see Shalev-Shwartz 2012 or Hazan 2016), which we formally bound in the following proposition.

Proposition 1.

Proposition 1 shows that Algorithm 1 achieves regret. The next result shows that this is the best that can be achieved by any online bidding algorithm.

Proposition 2.

Let be any online algorithm for bidding in repeated first-price auctions, then

This is true even when there is just one non-zero bid ().

The proof of Proposition 2 uses an argument similar to the one used for establishing -regret in Online Convex Optimization (e.g., see Theorem 3.5.1 of Hazan 2016), which leverages the anti-concentration property of sums of i.i.d. binomial random variables.

Proposition 1 highlights the power of our concave formulation (Theorem 1): it allows us to directly leverage the powerful theory of Online Convex Optimization to get the optimal regret rate. Moreover, unlike previous algorithms, our Algorithm 1 uses pure strategies which are monotonic. This ensures that having a higher values never leads to lower bids, a property that algorithms based on randomized strategies (like the ones proposed in Balseiro et al. 2022) lack. Having characterized the regret of Algorithm 1, we next establish its strategic-robustness guarantee.

4.2 Strategic Robustness

Although -regret is a desirable property, a variety of other algorithms proposed in previous work also achieve regret. However, as we discussed in the introduction, regret is not the end-all-be-all performance metric, and other properties of algorithms turn out to be equally important in real-world auction markets. Specifically, the strategic nature of online advertising markets implies that resistance to manipulation by the seller is of paramount importance. In the remainder of this section, we will demonstrate the strategic robustness of Algorithm 1 by proving that it limits the seller’s average revenue to that attained under the optimal mechanism (posting the monopoly reserve), i.e., the seller cannot exploit their knowledge of the buyer’s algorithm to extract more average revenue from her than is possible under the optimal single-shot mechanism.

Before proceeding with the formal statement and proof of strategic robustness of Algorithm 1, we introduce some notation. When the buyer uses the bidding strategy , the revenue that the seller extracts from her under the reserve-price/highest-competing-bid is given by

Moreover, let denote the revenue obtained by the optimal mechanism, i.e.,

The following theorem demonstrates the strategic robustness of Algorithm 1. It states that the maximum average revenue that can be extracted from a buyer using Algorithm 1 is bounded above by . In other words, if the buyer uses Algorithm 1 to bid and the seller wants to maximize the revenue that is extracted from her, she cannot do much better than posting the monopoly reserve price at each time step . This is despite the fact that the seller has complete knowledge of the exact algorithm being used by the buyer and her value distribution. Importantly, none of the mean-based algorithms satisfy this property (Braverman et al., 2018); we provide a concrete example demonstrating their lack of strategic robustness in Subsection 5.2.

Theorem 2.

With step size and initial iterate , Algorithm 1 satisfies

Remark 1.

In fact, our proof yields a stronger instance-dependent upper bound. For for all , we get:

Note that is simply the revenue attained from the posted-price mechanism that sells the item with probability exactly , which is the probability that the algorithm wins the item in auction . Therefore, is the total revenue attained from selling the items separately to a strategic buyer, with the price for item being . Under this mechanism, the probability of selling item is equal to , which is the probability with which item is sold to Algorithm 1, thereby yielding a more fine-grained instance-dependent bound.

The proof of Theorem 2 is based on a potential-function argument that couples the revenue of the seller in each auction with the change in the potential caused by the update of Algorithm 1. The intuition of this argument is best conveyed using the continuous-time approximation of Gradient Ascent, and that is what we present here. The full proof is more involved because it has to deal with discrete updates and the projection onto , and it can be found in Appendix B.

Let be the bidding probabilities of the buyer. Define the potential to be the squared Euclidean norm of scaled down by , i.e.,

When , note that the revenue obtained from the bidding strategy corresponding to bidding probabilities (Theorem 1) is given by

Moreover, the continuous-time approximation of the update step of Algorithm 1 is given by

We start by showing that the excess revenue over accrued by the seller can be charged against the change in potential and . To see this, observe that the change in potential is given by

Therefore, we have

where the last inequality follows from for . As the reserve price was arbitrary, we have argued that the excess revenue over can be charged against the change in potential, i.e.,

Integrating over time and using to denote the total revenue of the seller yields

As for any , we get that the total revenue extracted from the buyer is at most a constant larger than . The analysis of the continuous-time approximation is not exact, and going from continuous time to discrete time introduces the additional error that appears in the guarantee of Theorem 2. The simplicity of the aforementioned potential function argument is worth emphasizing; one rarely comes across a potential function simpler than the Euclidean norm. Importantly, it directly establishes strategic robustness, without first proving incentive compatibility like Braverman et al. (2018), and the proof may be of independent interest.

In this section, we assumed that the value distribution was known to the algorithm designer. Since this may not always be the case in practice, we relax this assumption in the next section, and develop an algorithm that does not require knowledge of .

5 Value-Threshold-Based Algorithm for Unknown Distributions

| (6) |

In this section, we no longer assume that the value distribution is known to the algorithm-designer, and instead only assume knowledge of an upper bound on the density. The knowledge of is not crucial to our results: we use it solely for tuning the step size , and setting yields the same dependence on even in its absence. Now, as the utility function and its gradient depend on the value distribution , we can no longer directly implement Gradient Ascent to our concave formulation. However, it turns out that the design principles of Algorithm 1 continue to work well even in this setting, and we use them to construct Algorithm 2. In particular, Algorithm 2 maintains feasible value-thresholds , where

and bids in auction whenever . It updates the value-thresholds iteratively with the same directional changes as Algorithm 1: upon encountering the highest competing bid for some , it decreases the probability of bidding strictly greater than by increasing the thresholds for all , and it increases the probability of bidding by decreasing the threshold ; leaving all other thresholds unchanged. Even though Algorithm 1 and Algorithm 2 may seem very different at first sight, the following proposition demonstrates their intimate connection: Algorithm 2 is simply Algorithm 1 run under the assumption that the values are uniformly distributed.

Proposition 3.

5.1 Regret Guarantee

Algorithm 2 is motivated by Proposition 3—it is not possible to run Algorithm 1 without knowledge of the value distribution , so we pretend that the value distribution is the uniform distribution over and deploy Algorithm 1 with the uniform distribution. However, this mismatch between the true value distribution and the uniform distribution means that we cannot directly use the Proposition 1, or extend its proof to establish regret bounds for Algorithm 2. In fact, the utility of the buyer as a function of the value thresholds may not even be a concave function. Despite this apparent lack of structure, Algorithm 2 performs well and attains -regret.

Theorem 3.

The proof of Theorem 3 is based on a novel potential function argument which does not use any of the machinery from Online Convex Optimization, and can be found in Appendix C. Here we present a proof-sketch for the special case where , i.e., there is only 1 possible non-zero bid, namely . Once again, the intuition behind the proof is best conveyed with a continuous-time argument that allows us to ignore the tedious edge cases.

Fix the benchmark policy against which we want low regret (assume no overbidding). Moreover, also fix a value ; we will prove the no-regret property for each value separately. Let denote the threshold such that the buyer bids when the value and bids otherwise. Define the following potential function:

We will show that the regret corresponding to value can be charged against the change in the potential for any possible highest competing bid . First, observe that the continuous-time update of Algorithm 2 is given by

Note that the algorithm only accumulates regret when it bids something different from the benchmark . Moreover, it also has zero regret when : the algorithm always bids for value because , which is the same as the benchmark . Therefore, assume . Thus, for the highest competing bid , it only accumulates non-zero regret in the following cases,

-

•

and : In this case, the algorithm bids for value , whereas the benchmark bids . As , both bids result in a win, but the benchmark pays less than the algorithm, thereby incurring regret. On the other hand, in this case we have .

-

•

and : In this case, the algorithm bids for value , whereas the benchmark bids . As , the algorithm does not win, but the benchmark does, resulting in a regret of . On the other hand, in this case we have .

-

•

and : In this case, the algorithm bids for value , whereas the benchmark bids . As , the algorithm wins and the benchmark loses, resulting in a negative regret of . On the other hand, in this case we have .

-

•

and : In this case, the algorithm bids for value , whereas the benchmark bids . As , both bids result in a win, but the benchmark overpays by , resulting in a negative regret of . On the other hand, in this case we have .

Therefore, in all cases, we have shown that the regret for value can be charged against the change in potential, i.e.,

where is the regret for value associated with bidding according to the threshold instead of the benchmark , when the highest competing bid is . Integrating over time and using to denote the total regret for value yields

As for all , we get that is at most 2 for each value . Finally, the total regret of the algorithm is simply the expected total regret for each value with . Therefore, the total regret of the algorithm is 2. This analysis of the continuous-time approximation is inexact and simplified. The proof becomes much more intricate when one goes to discrete time and considers the general case of , and it introduces the additional error that appears in the guarantee of Theorem 3.

5.2 Strategic Robustness

Having established a -regret guarantee for Algorithm 2, we now turn our attention to its strategic robustness. In the known-distribution setting, the allure of Algorithm 1 over previously proposed algorithms stems from its ability to limit the average revenue extracted from the buyer to . The next theorem shows that Algorithm 2 is also robust to strategic manipulation by the seller, without requiring knowledge of the value distribution (aside from a bound on ).

Theorem 4.

With step size for some constant and initial iterate , Algorithm 2 satisfies

The proof of Theorem 4 is based on yet another potential function argument. It has some similarities to the one used used for Theorem 2, but uses a novel potential function. We omit the proof here and instead discuss a concrete example in which mean-based algorithms yield a revenue higher than , but our Algorithm 2 does not.

Example.

Consider a single buyer whose value distribution is a smoothly-truncated equi-revenue distribution starting at 1/8, i.e.,

for some small constant . The possible bids are , and . It is straightforward to check that posting a price of either or leads to a revenue of . In fact, 1/8 is the maximum revenue that can be achieved by any price because

Therefore, we have .

Consider the sequence of decreasing reserve prices such that for and for , i.e., the seller posts a reserve price of for the first half of the auctions and then reduces it to for the second half. We start by showing that this simple sequence of reserve prices is sufficient to exploit mean-based algorithms and extract more revenue than . Informally speaking, an algorithm is mean-based if it plays historically sub-optimal actions with a small probability (see Braverman et al. 2018 for a formal definition). In other words, they almost always play actions that yield the highest historical cumulative utility. Many popular algorithms like Exponential Weights, EXP3 and FTRL are mean based, and consequently most of the recently proposed algorithms for bidding in first-price auctions are also mean based (see Subsection 1.2 for a discussion).

First note that, in the first auctions, bidding for values is the optimal strategy for the past, i.e., maximizes the historical cumulative utility in auctions 1 through . Therefore, in the first auctions, every mean-based algorithm bids for values and bids arbitrarily for the other values. Importantly, even after the shift to reserve price (auctions ), the bid with the highest historical cumulative utility remains for values . For values , the bid with the highest historical cumulative utility transitions from to at some time . Lastly, for values , the bid with the highest historical utility is . Therefore, in the last auctions, every mean-based algorithm continues to bid for values , transitions to bidding for values , and bids for values . Crucially, this implies that the total payment made by any mean-based algorithm is at least

On the other hand, except for an initial transition period of length , Algorithm 2 bids for all values in the first auctions. Moreover, except for a transition period of length after the change of reserve price from to , Algorithm 2 bids for all values in the last auctions. Therefore, the total payment of Algorithm 2 is bounded above by

The above decomposition and comparison of total payment precisely highlights a weakness of mean-based algorithms: they are not agile and put too much weight on the distant past. In particular, they fail to learn the new optimal bid for values sufficiently fast after the change in reserve price from to , and this results in unnecessarily high payments for those values. In contrast, Algorithm 2 is based on Gradient Ascent and quickly switches to the optimal bid of after the transition. The lack of agility on the part of mean-based algorithm not only results in higher revenue for the seller, but also lower utility for the buyer. We will use this fact to demonstrate the lack of incentive compatibility in mean-based algorithms when we continue this example in the next subsection.

5.3 Incentive Compatibility

In the previous subsection, we showed that Algorithm 2 is resistant to manipulation by the seller. However, thus far we have paid very little attention to manipulation by the buyer. In particular, bidding algorithms of the type developed in this paper are deployed as automated bidding algorithms (or autobidders for short) on internet platforms. These autobidders take as input the high-level objectives of the advertiser and attempt to maximize total utility according to those objectives. One of the main inputs provided by each advertiser is her value-per-click and targeting criteria, which is used to compute her value for winning each auction. Therefore, even though buyers cannot directly choose their bids in each auctions, they can misreport their values in an attempt to gain higher utility. In particular, a strategic buyer can misreport their high-level objectives to the autobidder in a way that causes it to believe that her value is whenever her true value is .

This misreporting of values is detrimental to both the buyer and the seller. The buyer has to spend effort and incur costs in order to find beneficial misreports. This in turn makes the system unpredictable for the seller and she loses the ability to measure the true value of the buyer, which is very valuable for experimentation. Thus it is practically desirable to employ algorithms which are resistant to manipulation by a strategic buyer who has the power to misreport her values. Formally, we want algorithms that are ex-post incentive compatible: the buyer should not regret truthfully reporting her values in hindsight. Like strategic robustness, mean-based algorithms fail to hit the mark here too and are not incentive compatible. In contrast, as the next theorem establishes, Algorithm 2 is ex-post incentive compatible.

Theorem 5.

For any misreport map and initial iterate , Algorithm 2 with step-size satisfies

The proof of Theorem 5 is also based on a potential function argument. It is analogous to the proof of Theorem 3, but uses a new potential function. We refer the reader to Appendix C for the full proof, and instead continue with our discussion of the concrete example we introduced in the previous subsection. In particular, we show that the same example demonstrates the lack of incentive compatibility in mean-based algorithms.

Example (Continued from Subsection 5.2).

Recall that any mean-based algorithm bids for all values in all auctions . On the other hand, for the values close to (i.e., ), it bids nearly optimally: in the first auctions and in the last auctions, except for a short transition period when the reserve price changes from to . As a consequence, the buyer would receive higher expected utility by misreporting her value to be (close to) whenever her true value is larger than , i.e., mean-based algorithms incentivize the buyer to misreport her value in this example.

In contrast, recall that Algorithm 2 bids for values in the first half of the auctions, and bids for values in the last half (ignoring the transition periods of length ). Therefore, every value bids nearly optimally in all auctions, and consequently the buyer does not gain anything from misreporting her values.

Intuitively, the lack of incentive compatibility of mean-based algorithms stems from their inability to learn effectively across values: even though they learn to bid optimally for values close to , they are not able to leverage it for larger values . Algorithm 2 does not suffer from this issue. It uses the threshold structure of the bidding strategies to learn the optimal bid for all values after the change in reserve price from to . In particular, the threshold increases to 1 within auctions of the change in reserve price, and Algorithm 2 only bids for values , which results in optimal bids for all values.

It is worth noting that this lack of incentive compatibility arises naturally. A strategic seller who wants to maximize revenue from a mean-based algorithm is incentivized to post decreasing reserve prices. And it is precisely for that sequence of reserve prices that the buyer can gain for misreporting her value to the mean-based algorithm. In other words, the sequences of reserve prices that help the seller maximize her revenue are exactly the ones which render the mean-based algorithm non-incentive-compatible.

5.4 Multi-Buyer Strategic Robustness

In this subsection, we show that the strategic robustness of Algorithm 2 continues to hold in the multi-agent setting where all of the buyers simultaneously employ it. Consider a setting with buyers who participate in sequential second price auctions. We will use to denote the value distribution of buyer (and assume that is an upper bound on the density of all of the ). Let denote the maximum revenue that can be extracted from these buyers in a single-shot incentive-compatible mechanism. We will assume that ties are broken based on some random ranking of the buyers. In particular, this includes the uniform tie breaking rule (uniformly random ranking) and the lexicographic tie-breaking rule (fixed ranking). Random-ranking-based tie-breaking rules allow us to maintain our convention that a buyer wins if her bid is equal to the (effective) highest competing bid: if other bidders are tied for the highest competing bid , then the effective highest competing bid is if all them have a rank lower than the buyer under consideration, and otherwise.

Theorem 6.

If all buyers employ Algorithm 2 with , then the total expected revenue satisfies

Remark 2.

An analogue of Theorem 6 continues to hold even if the buyers use different step sizes. In particular, as long as each buyer uses a step size satisfying , our analysis guarantees .

The proof of Theorem 6 follows from the incentive compatibility guarantees we proved as part of Theorem 5. In particular, we show that the expected allocation and payment rules resulting from all bidders running Algorithm 2 form a mechanism that is close to an ex-ante truthful mechanism, which allows us to upper bound its expected revenue by the revenue of the optimal mechanism.

6 Logarithmic Regret for Stochastic Environments

Thus far we have focused our attention on the worst-case setting where the highest competing bids are generated adversarially. In this section, we consider a more well-behaved environment and assume that the highest competing bid is drawn from an unknown distribution . Moreover, we relax our assumption that for all and allow the set of possible bids to be arbitrary. This allows us to discard highest-competing bids with zero probability of occurring and posit the existence of a positive lower bound . Furthermore, we assume that such a lower bound is known to the algorithm designer. In this setting, our concave formulation (Theorem 1) yields a strongly-concave reward function, thereby allowing us to attain a regret guarantee.

Proposition 4.

The utility function is -strongly concave for .

7 Acknowledgements

The authors would like to thank Santiago Balseiro and Christian Kroer for helpful discussions, and providing valuable feedback on a preliminary version of this paper.

References

- Auer et al. (2002) Peter Auer, Nicolo Cesa-Bianchi, Yoav Freund, and Robert E Schapire. The nonstochastic multiarmed bandit problem. SIAM journal on computing, 32(1):48–77, 2002.

- Badanidiyuru et al. (2023) Ashwinkumar Badanidiyuru, Zhe Feng, and Guru Guruganesh. Learning to bid in contextual first price auctions. In Proceedings of the ACM Web Conference 2023, pages 3489–3497, 2023.

- Balseiro et al. (2022) Santiago Balseiro, Negin Golrezaei, Mohammad Mahdian, Vahab Mirrokni, and Jon Schneider. Contextual bandits with cross-learning. Mathematics of Operations Research, 2022.

- Balseiro et al. (2023) Santiago Balseiro, Christian Kroer, and Rachitesh Kumar. Contextual standard auctions with budgets: Revenue equivalence and efficiency guarantees. Management Science, 2023.

- Braverman et al. (2018) Mark Braverman, Jieming Mao, Jon Schneider, and Matt Weinberg. Selling to a no-regret buyer. In Proceedings of the 2018 ACM Conference on Economics and Computation, pages 523–538, 2018.

- Brown et al. (2023) William Brown, Jon Schneider, and Kiran Vodrahalli. Is learning in games good for the learners? In Thirty-seventh Conference on Neural Information Processing Systems, 2023. URL https://openreview.net/forum?id=jR2FkqW6GB.

- Bulow and Roberts (1989) Jeremy Bulow and John Roberts. The simple economics of optimal auctions. Journal of political economy, 97(5):1060–1090, 1989.

- Cai et al. (2023) Linda Cai, S Matthew Weinberg, Evan Wildenhain, and Shirley Zhang. Selling to multiple no-regret buyers. In International Conference on Web and Internet Economics, pages 113–129. Springer, 2023.

- Cesa-Bianchi et al. (2023) Nicolò Cesa-Bianchi, Tommaso Cesari, Roberto Colomboni, Federico Fusco, and Stefano Leonardi. The role of transparency in repeated first-price auctions with unknown valuations. arXiv preprint arXiv:2307.09478, 2023.

- Chen and Peng (2023) Xi Chen and Binghui Peng. Complexity of equilibria in first-price auctions under general tie-breaking rules. In Proceedings of the 55th Annual ACM Symposium on Theory of Computing, STOC 2023, page 698–709, New York, NY, USA, 2023. Association for Computing Machinery. ISBN 9781450399135. doi: 10.1145/3564246.3585195. URL https://doi.org/10.1145/3564246.3585195.

- Chen and Lin (2023) Yiling Chen and Tao Lin. Persuading a behavioral agent: Approximately best responding and learning. arXiv preprint arXiv:2302.03719, 2023.

- Deng et al. (2019a) Yuan Deng, Jon Schneider, and Balasubramanian Sivan. Strategizing against no-regret learners. Advances in Neural Information Processing Systems, 32, 2019a.

- Deng et al. (2019b) Yuan Deng, Jon Schneider, and Balasubramanian Sivan. Prior-free dynamic auctions with low regret buyers. Advances in Neural Information Processing Systems, 32, 2019b.

- Embrechts and Hofert (2013) Paul Embrechts and Marius Hofert. A note on generalized inverses. Mathematical Methods of Operations Research, 77:423–432, 2013.

- Feng et al. (2018) Zhe Feng, Chara Podimata, and Vasilis Syrgkanis. Learning to bid without knowing your value. In Proceedings of the 2018 ACM Conference on Economics and Computation, pages 505–522, 2018.

- Freund and Schapire (1997) Yoav Freund and Robert E Schapire. A decision-theoretic generalization of on-line learning and an application to boosting. Journal of computer and system sciences, 55(1):119–139, 1997.

- Guruganesh et al. (2024) Guru Guruganesh, Yoav Kolumbus, Jon Schneider, Inbal Talgam-Cohen, Emmanouil-Vasileios Vlatakis-Gkaragkounis, Joshua R Wang, and S Matthew Weinberg. Contracting with a learning agent. arXiv preprint arXiv:2401.16198, 2024.

- Han et al. (2020a) Yanjun Han, Zhengyuan Zhou, Aaron Flores, Erik Ordentlich, and Tsachy Weissman. Learning to bid optimally and efficiently in adversarial first-price auctions. arXiv preprint arXiv:2007.04568, 2020a.

- Han et al. (2020b) Yanjun Han, Zhengyuan Zhou, and Tsachy Weissman. Optimal no-regret learning in repeated first-price auctions. arXiv preprint arXiv:2003.09795, 2020b.

- Hazan (2016) Elad Hazan. Introduction to online convex optimization. Foundations and Trends® in Optimization, 2(3-4):157–325, 2016.

- Hazan et al. (2006) Elad Hazan, Adam Kalai, Satyen Kale, and Amit Agarwal. Logarithmic regret algorithms for online convex optimization. In International Conference on Computational Learning Theory, pages 499–513. Springer, 2006.

- Kinnear et al. (2022) Ryan J Kinnear, Ravi R Mazumdar, and Peter Marbach. Convexity and duality in optimum real-time bidding and related problems. arXiv preprint arXiv:2206.12408, 2022.

- Kolumbus and Nisan (2022a) Yoav Kolumbus and Noam Nisan. How and why to manipulate your own agent: On the incentives of users of learning agents. Advances in Neural Information Processing Systems, 35:28080–28094, 2022a.

- Kolumbus and Nisan (2022b) Yoav Kolumbus and Noam Nisan. Auctions between regret-minimizing agents. In Proceedings of the ACM Web Conference 2022, pages 100–111, 2022b.

- Krishna (2009) Vijay Krishna. Auction theory. Academic press, 2009.

- Mansour et al. (2022) Yishay Mansour, Mehryar Mohri, Jon Schneider, and Balasubramanian Sivan. Strategizing against learners in bayesian games. In Conference on Learning Theory, pages 5221–5252. PMLR, 2022.

- Milgrom (2004) Paul Robert Milgrom. Putting auction theory to work. Cambridge University Press, 2004.

- Nedelec et al. (2022) Thomas Nedelec, Clément Calauzènes, Noureddine El Karoui, Vianney Perchet, et al. Learning in repeated auctions. Foundations and Trends® in Machine Learning, 15(3):176–334, 2022.

- Schneider and Zimmert (2024) Jon Schneider and Julian Zimmert. Optimal cross-learning for contextual bandits with unknown context distributions. arXiv preprint arXiv:2401.01857, 2024.

- Shalev-Shwartz (2012) Shai Shalev-Shwartz. Online learning and online convex optimization. Foundations and Trends® in Machine Learning, 4(2):107–194, 2012.

- Wang et al. (2023) Qian Wang, Zongjun Yang, Xiaotie Deng, and Yuqing Kong. Learning to bid in repeated first-price auctions with budgets. ICML’23. JMLR.org, 2023.

- Wong (2021) Matt Wong. Moving adsense to a first-price auction. https://blog.google/products/adsense/our-move-to-a-first-price-auction/, 2021. Accessed: 2024-01-22.

- Zhang et al. (2022) Wei Zhang, Yanjun Han, Zhengyuan Zhou, Aaron Flores, and Tsachy Weissman. Leveraging the hints: Adaptive bidding in repeated first-price auctions. Advances in Neural Information Processing Systems, 35:21329–21341, 2022.

Electronic Companion:

Strategically-Robust Learning Algorithms for Bidding in First-Price Auctions

Rachitesh Kumar, Jon Schneider, Balasubramanian Sivan

March 5, 2024

Appendix A Proofs for Section 3

A.1 Proof of Lemma 1

Proof.

and follow directly from the definition of . Consider two values , and let , . For contradiction, assume (or equivalently, ). Then, the definition of implies that

respectively. The former is a strict inequality because ties are broken in favor of smaller bids. Adding the two inequalities together and cancelling the terms and yields

which is a contradiction because , and for all . Therefore, is non-decreasing.

Next, we establish the left-continuity of . Consider any sequence of increasing values such that . Since is non-decreasing, there exists a such that . Since there are only finitely many bids, there exists an such that for all . Therefore, for any , we have

for all . Taking the limit on both sides yields

Therefore, . Combining this with yields , thereby establishing the left-continuity of . ∎

A.2 Proof of Theorem 1

Proof.

We have already established (1) and (2) in Section 3, and only need to prove (3). First, observe that is absolutely continuous with and . Consequently, the Intermediate Value Theorem implies . Therefore, part (4) of Proposition 1 of Embrechts and Hofert (2013) implies for all . Consequently,

Hence, and part (2) applies. Consequently, . ∎

Appendix B Proofs for Section 4

The following lemma characterizes the update step of Algorithm 1. It plays a vital role in our analysis of Algorithm 1. Intuitively, projecting onto involves a modification of isotonic-regression which ensures the ‘no over-bidding’ condition by ensuring . Someone versed in the Pool Adjacent Violators Algorithm (PAVA) for isotonic regression will find the characterization of the projection and the analysis familiar.

Lemma 2.

Fix bidding probabilities , step size , and highest competing bid . Define

Moreover, let and

Then, we have

| (B-7) |

where . Moreover, for all .

Proof.

For the purposes of the proof, define using (B-7). To establish the lemma, we need to show that is a solution to the following optimization problem:

| (B-8) | |||||

| s.t. | |||||

By the KKT optimality conditions, it suffices to show that , which is the gradient of the objective function at , lies in the cone formed by the coefficient vectors of the tight constraints. We establish this fact in two mutually exclusive and exhaustive cases based on the value of .

-

•

CASE I: Assume . In this case, satisfies

i.e., the constraints for and for are tight at . Define dual variables as follows:

The condition implies

(B-9) Therefore, we can write

To establish the KKT conditions for the current case, all that remains to be shown is . This is trivially true for because and the definition of implies that for all . To prove it for , note that the definition of implies , which in turn implies

Therefore, . Since for all , we get that for all , and consequently . Finally, note that (B-9) implies

thereby establishing for all .

-

•

CASE II: Assume . In this case, satisfies

i.e., the constraints for , for and are tight at . Define dual variables as follows:

The definition of implies for all , i.e, for all . Moreover, the definition of along with the condition implies . As before, we have for all because for all by definition of . To establish the KKT conditions, note that

In both cases, we have shown that lies in the cone formed by the coefficient vectors of the tight constraints. Therefore, by KKT Theorem, is an optimal solution for the quadratic optimization problem (B-8). Moreover, in both cases we established that for all , thereby concluding the proof. ∎

B.1 Proof of Proposition 1

B.2 Proof of Proposition 2

Proof.

Let the value distribution be the uniform distribution on the interval . Moreover, let the set of possible bids be and . In each auction , suppose the highest competing bid is set equal to 0 and with equal probability, i.e., , and assume that these highest competing bids are independent across auctions and independent of the values .

For any auction and a bidding strategy that does not depend on the realization of , it is clear that

where the last inequality follows from the fact that, when is selected uniformly at random from , bidding 1/4 yields higher utility than bidding for all . This is because for all . Therefore, we get an upper bound on the expected performance of every online algorithm

| (B-13) |

On the other hand, note that the anti-concentration of sums of independent Bernoulli random variables implies the existence of a constant such that

B.3 Proof of Theorem 2

Proof.

We will use a potential function argument: we define a function such that for all auctions , the difference between the revenue of the seller and can be charged against the change in for all possible values of . To this end, define the potential function as

Note that for all .

We start by showing that, to establish the theorem, it suffices to prove the following statement for all and :

| (B-15) |

where

-

•

is the change in potential caused by a single update-step of Algorithm 1,

-

•

for the bidding strategy corresponding to bidding-probability vector , which sets for .

This is because applying (B-15) to iterate of Algorithm 1 and highest competing bid yields

Summing over all times steps and noting that , we get

and the theorem statement follows. To complete the proof, we next establish (B-15).

Fix some and highest competing bid for some . First, observe that for for , we have

| () |

Appendix C Proofs for Section 5

C.1 Proof of Proposition 3

Proof.

We will prove the proposition using induction on . The base case follows from our assumption that . Assume that the induction hypothesis holds for some , i.e., . Suppose the -th highest competing bid is equal to for some . Observe that

Therefore we have . Next, note that implies

| (Setting ) | ||||

Finally, combining and , we get

This completes the induction step. ∎

As a direct consequence of Proposition 3 and Lemma 2, we get the following corollary characterizing the update step of Algorithm 2. We will use it repeatedly in our proofs for Algorithm 2.

Corollary 1.

Fix thresholds , step size , and highest competing bid . Define

Moreover, let and

Then, we have

| (C-16) |

where . Moreover, for all .

C.2 Proof of Theorem 3

Proof.

Consider a benchmark bidding strategy and a value . Assume for all , and let be the bid for value under . Define the potential function as

We start by showing that, to prove the theorem, it suffices to prove the following statement for all thresholds , values , and highest competing bids :

| (C-17) |

where

- •

-

•

is the regret associated with bidding according to instead of the benchmark strategy for a buyer with value . Here is the bidding strategy corresponding to thresholds , i.e., if .

Suppose (C-17) holds for all thresholds , values , and highest competing bids . Then, we can apply it to and to get

Taking an expectation over yields

where the first implication follows from the definition of and the union bound, and the second implication follows from (here is an upper bound on the density of ).

Summing over yields:

Since the benchmark strategy was an arbitrary strategy that did not overbid, we have shown that (C-17) is a sufficient condition for the theorem to hold, and we focus on establishing (C-17) in the remainder of the proof.

Fix a benchmark strategy with for all , a value , a highest competing bid and thresholds . First assume that . In particular, this implies that if (respectively ), then (respectively ), i.e., the thresholds don’t cross during the update . Let be the bid under strategy for value , let be the bid under strategy for value (i.e., ), and let be the highest competing bid. Since the thresholds don’t cross during the update , we have

We establish (C-17) by separately analyzing the following mutually exclusive and exhaustive cases on the ordering of the algorithm’s bid , the benchmark bid , and the highest other bid . Throughout these cases, we extensively use our characterization in Corollary 1 of the form of the update .

-

1.

: The utility under is and the utility under is . Therefore, the regret . On the other hand, since for all , we get .

-

2.

: The utility under is and the utility under is . Therefore, the regret . On the other hand, since for all , we get .

-

3.

: The utility under is and the utility under is because . Hence we have . On the other hand, because for all and thresholds cannot cross during the update .

-

4.

: The utility under is and the utility under is because . Hence we have . On the other hand, because for all .

-

5.

: The utility under is because , and the utility under is . Therefore, the regret . On the other hand, for and for . Moreover, the definition of implies , and the definition of implies . Thus, we get .

-

6.

: The utility under is and the utility under is because . Therefore, the regret . On the other hand, for all and for all . The definition of , the fact that , and the assumption that the thresholds don’t cross implies . As a consequence, we get . Moreover, the definition of implies . Thus, we have .

In all of the six cases, we have established the desired bound .

To complete the proof of (C-17), we now relax our assumption that and consider the setting where . First, observe that Corollary 1 implies

which in turn implies . Next, observe that the following functions are 1-Lipschitz:

As a consequence, we get for all . On the other hand, for all . Combining the two, we get the desired bound in the case when . This establishes (C-17) and completes the proof. ∎

C.3 Proof of Theorem 4

Proof.

We will use a potential-function argument with the potential function defined as

Note that for all .

We start by showing that, to establish the theorem, it suffices to prove the following statement for all thresholds and highest competing bids :

| (C-18) |

where

- •

-

•

for the bidding strategy corresponding to thresholds , which sets for .

This is because applying (C-18) to iterate of Algorithm 2 and highest competing bid yields

Summing over all times steps and noting that , we get

and the theorem statement follows. To complete the proof, we next establish (C-18).

Fix some and highest competing bid for some . First, observe that

| () |

Next, using the terminology and the result from Corollary 1, we can write

| () |

where the first inequality follows from the fact that for a decreasing function and , the third inequality follows from the definition of (as defined in Lemma 2), and the final inequality follows from the fact that and for all . Moreover, we have repeatedly used the fact that for all .

C.4 Proof of Theorem 5

Proof.

Fix a misreport map . Consider a value and define the potential function as follows:

We start by showing that, to prove the theorem, it suffices to prove the following statement for all thresholds , value , and highest competing bid :

| (C-19) |

where

- •

-

•

is the regret associated with reporting the true value in lieu of misreporting . Here is the bidding strategy corresponding to thresholds , i.e., if .

Suppose (C-19) holds for all thresholds , values , and highest competing bids . Then, we can apply it to and to get

Taking an expectation over yields

where the first implication follows from the definition of and the union bound, and the second implication follows from (here is an upper bound on the density of ).

Summing over and using the linearity of expectations yields:

Therefore, we have shown that (C-19) is a sufficient condition for the theorem—we focus on establishing (C-19) in the remainder.

Fix a value , highest competing bid and thresholds . First assume that . In particular, this implies that if (respectively ), then (respectively ), i.e., the thresholds don’t cross during the update . Let be the bid under strategy for value (i.e., ), let be the bid under strategy for value (i.e., ), and let be the highest competing bid. Since the thresholds don’t cross during the update , we have

where the last inequality follows from the fact that and have the same sign for all possible values of .

We establish (C-19) by separately analyzing the following mutually exclusive and exhaustive cases. These cases (and their analysis) is fairly similar to the cases in the proof of Theorem 3. The main difference is in the case where (the misreporting benchmark wins the item, but the algorithm doesn’t), which we split into two cases depending on whether or not .

-

1.

: The utility obtained by misreporting with is and the utility under is . Therefore, the regret . On the other hand, since for all , we get .

-

2.

: The utility obtained by misreporting with is and the utility under is . Therefore, the regret . On the other hand, since for all , we get .

-

3.

: The utility obtained by misreporting with is and the utility under is because . Hence . On the other hand, because and for all . Here, follows from the fact that thresholds cannot cross during the update .

-

4.

: The utility obtained by misreporting with is and the utility under is because . Hence we have . On the other hand, because for all .

-

5.

: The utility obtained by misreporting with is because , and the utility under is . Therefore, the regret . On the other hand, for and for . The definition of implies . Moreover, the definition of implies . Thus, we get .

-

6.

and : The utility obtained by misreporting with is and the utility under is because . Therefore, the regret . On the other hand, for all and for all . The definition of , the assumption that , and the assumption that the thresholds don’t cross implies . As a consequence, we get . Moreover, the definition of implies . Thus, we have .

-

7.

and : The utility obtained by misreporting with is and the utility under is because . Therefore, the regret . On the other hand, for all and for all . Thus, we have .

In all of the seven cases, we have established the desired bound .

To complete the proof of (C-19), we now relax our assumption that , and consider the setting where . First, observe that Corollary 1 implies

which in turn implies . Next, observe that the following function is 1-Lipschitz:

As a consequence, we get for all . On the other hand, for all . Combining the two, we get the desired bound in the case when . This establishes (C-19) and completes the proof. ∎

C.5 Proof of Theorem 6

Proof.

Let be the iterates of Algorithm 2 when all of the buyers simultaneously use Algorithm 2 with to bid, the seller sets (potentially random and adaptive) reserve prices and the ties are broken using (random) ranking-based rules . Note that is a random variable that depends on the realized values , (where denotes the value of buyer in auction ), the reserve prices and the tie-breaking rankings. Let denote all of the tuples of random variables that determine the run of an algorithm. Consider the first-price auction in which buyer bids according to thresholds (i.e., using the strategy ), the seller sets the reserve and ties are broken using the ranking . For a value tuple , define to be 1 if buyer wins this auction and 0 otherwise. Moreover, let be the effective highest competing bid faced by buyer in this auction, i.e., if and only if buyer bids greater than or equal to .

Define the following direct revelation mechanism for buyers and a single item:

-

1.

Ask all buyers to report their values. Let denote the value reported by buyer .

-

2.

Define the allocation function as follows:

and the payment rule as

Note that the definition of implies that is the total expected revenue generated when all buyers simultaneously employ Algorithm 2.

We will use and to denote the interim allocation rule of , i.e.,

| and |

It is easy to see that is monotonic for all buyers because the allocation function is monotonic in the -th component. Define to be the expected utility when buyer has value but reports . For a function , these definitions along with Fubini’s Theorem imply

Define the optimal misreport function for buyer as . Moreover, define the regret for not misreporting value to be as

Now, note that Theorem 5 implies

| (C-20) |

Next, observe that the definition of implies

In other words, is the interim utility for value in incentive compatible mechanism with allocation rule and payment rule . Therefore Equation (5.7) of Krishna (2009) applies, and we get

Since for all , we have , and as a consequence

Next, note that Revenue Equivalence (Proposition 5.2 of Krishna 2009) implies that is simply the interim expected payment of buyer with value under the incentive-compatible mechanism with allocation rule . Therefore, we have

where the last inequality follows from (C.5). Finally, the theorem follows from the fact that . ∎

Appendix D Proofs for Section 6

For completeness, we formally state the time-varying step-size variant of Algorithm 1 here:

D.1 Proof of Proposition 4

Proof.

Recall the definition of the utility function under highest-competing-bid distribution as given in (3):

We start by showing the function defined below is -strongly concave:

To see this, observe that , and for we have

where we have used the fact that for . This allows us to establish the -strongly concavity of using the first-order condition:

Next, observe that the function defined as

is -strongly convex because

As is the sum of and a linear function of , we get the proposition. ∎

D.2 Proof of Theorem 7

Proof.

First, observe that Algorithm 1 implements Stochastic Gradient Ascent for the reward function :

Moreover note that is an upper bound on the gradient samples.

Now, we can apply the -regret guarantee described in Hazan et al. (2006) for Stochastic Gradient Descent with step size to get

Finally, Theorem 1 implies that for all and , which completes the proof. ∎