latexText page

Tail risk forecasting with semi-parametric regression models by incorporating overnight information

This research incorporates realized volatility and overnight information into risk models, wherein the overnight return often contributes significantly to the total return volatility. Extending a semi-parametric regression model based on asymmetric Laplace distribution, we propose a family of RES-CAViaR-oc models by adding overnight return and realized measures as a nowcasting technique for simultaneously forecasting Value-at-Risk (VaR) and expected shortfall (ES). We utilize Bayesian methods to estimate unknown parameters and forecast VaR and ES jointly for the proposed model family. We also conduct extensive backtests based on joint elicitability of the pair of VaR and ES during the out-of-sample period. Our empirical study on four international stock indices confirms that overnight return and realized volatility are vital in tail risk forecasting.

Keywords: Nowcasting, Markov chain Monte Carlo method, Value-at-Risk, Expected shortfall, CAViaR model, Realized measures, Overnight return.

JEL Classification: C11 C22 C51 C53 C58

1 Introduction

Value-at-Risk (VaR) is one of the most common measurements to quantify the risk of potential losses for a firm or an investment. It presents how much money one can lose from a portfolio or stock market during a specified period. While VaR only provides the maximum loss at a certain confidence level, it says nothing about what could happen beyond that point. In contrast, expected shortfall (ES, Artzner et al. 1999) measures the average loss in the worst-case scenarios beyond the VaR cutoff point. This feature makes ES a more comprehensive risk measure, as it better captures tail risk, which refers to the risk of extreme events. The ES of the return given at the level is:

| (1) |

where is a daily return at time , is some information set available at time , and is the conditional VaR of given at probability level . ES is a coherent risk measure, whereas VaR is not due to the lack of subadditivity. Furthermore, ES is preferred by regulators. For example, the Basel III framework recommends using both VaR and ES for market risk measurement. In practice, both measures are often used together to get a more comprehensive understanding of risk and to develop a more robust risk management strategy. This study focuses on forecasting VaR and ES jointly during the out-of-sample period, because doing so offers a better, more efficient, and more consistent understanding of risk, assisting with decision-making processes and helping to meet regulatory demands.

With the popularity of high-frequency data, observations on intra-day returns are now more widely available. Many studies explore intra-day return during trading hours given the availability of high-frequency data, whereby volatility can be predicted more precisely via, for example, realized variance (Andersen and Bollerslev 1998; Andersen et al. 2003), realized range (Martens and van Dijk 2007; Christensen and Podolskij 2007), and realized kernel (Barndorff-Nielsen et al. 2008). Some contemporary works incorporate the realized volatility component into parametric models to forecast VaR and ES (Chen and Watanabe 2019; Chen et al. 2021, 2022). Lazar and Xue (2020) and Chen et al. (2023) integrate realized volatility into the generalized autoregressive score (GAS) and the RES-CAViaR model within a semi-parametric framework. Gerlach and Wang (2020) and Wang et al. (2023) present semi-parametric models that include realized volatility measures.

Information flow in modern financial markets is continuous, but major stock exchanges are typically only open during regular trading hours (Ahoniemi & Lanne 2013). One day’s opening price usually differs from the previous day’s closing price, with the corresponding overnight return often accounting for a significant portion of the total daily return. This study integrates overnight information by defining the difference between today’s opening price and yesterday’s closing price. Consequently, we forecast VaR and ES immediately after today’s market opening. In this context, the cut-off line is the market opening time, with any information beyond this time remaining unknown. This concept relates to nowcasting through overnight information.

CAViaR (Conditional Autoregressive Value at Risk) first appears in Engle and Manganelli (2004) and is a significant development in the realm of financial econometrics as it models and predicts VaR directly. The CAViaR model is designed to forecast VaR and does not provide an estimate for ES, which is considered a more comprehensive risk measure. Taylor (2019) proposes a joint model that estimates conditional VaR and ES simultaneously and shows its superior performance to various existing models. We refer to this joint model as ES-CAViaR in this paper.

Motivated by the superior performance of the ES-CAViaR model in Taylor (2019), we propose to combine it with realized volatility and the concept of nowcasting through overnight information. We name this newly developed model as RES-VAViaR-oc. The contribution of this proposed model is to forecast VaR and ES by adding trading information, including close-to-close return, realized volatility, and overnight news simultaneously. Overnight information is critical in stock markets, mainly due to the uncertainty it introduces. Key announcements or events often happen during non-trading hours. This could include earnings reports, geopolitical events, or policy changes. These developments can lead to a significant difference in the perceived value of a stock as well as to a gap up or down at the next market opening. Since these announcements are unpredictable, they add an element of uncertainty that we must consider when forecasting the tail risks.

From a risk management perspective, the overnight return often contributes to a significant portion of total return volatility. This additional volatility introduces further uncertainty, making it essential for us to measure and manage its exposure to overnight risks. Moreover, in a globally interconnected world nowadays, developments in foreign markets can impact domestic markets; e.g., the impacts of the COVID-19 pandemic or the conflict between Ukraine and Russia. Overnight news or economic data from other countries affect investors’ sentiment and expectations, causing a price adjustment when the market opens. As different countries operate in different time zones, the unpredictability of these foreign market influences adds uncertainty.

The proposed model herein is more flexible, because it includes ES-CAViaR of Taylor (2019) and RES-CAViaR of Chen et al. (2023) as special cases. With the relevance of the asymmetric Laplace (AL) distribution and the quantile regression, we estimate all unknown parameters and forecast tail risks jointly via the Bayesian methods. This approach has various advantages. First, it is a more efficient and flexible way to estimate all parameters for complex models. Second, the parameter restrictions are established on the prior distribution. Third, it estimates the unknown parameters and tail risk simultaneously.

To compare the forecasting abilities among competing models, we use the violation rate (VRate) and three standard backtests. These backtests include the unconditional coverage (UC) test described by Kupiec (1995), the conditional coverage (CC) test by Christoffersen (1998), and the Dynamic Quantile (DQ) test of Engle and Manganelli (2004). We use these tests to evaluate VaR performance. The VRate measures the average number of instances when the return falls below the VaR forecast, and experts widely use it to assess the accuracy of the target models. The closer VRate is to the given level , the better is the model’s performance in forecasting VaR. In addition to these traditional backtesting techniques, we use the quantile score (Giacomini and Komunjer 2005) for the comparative backtest of VaR.

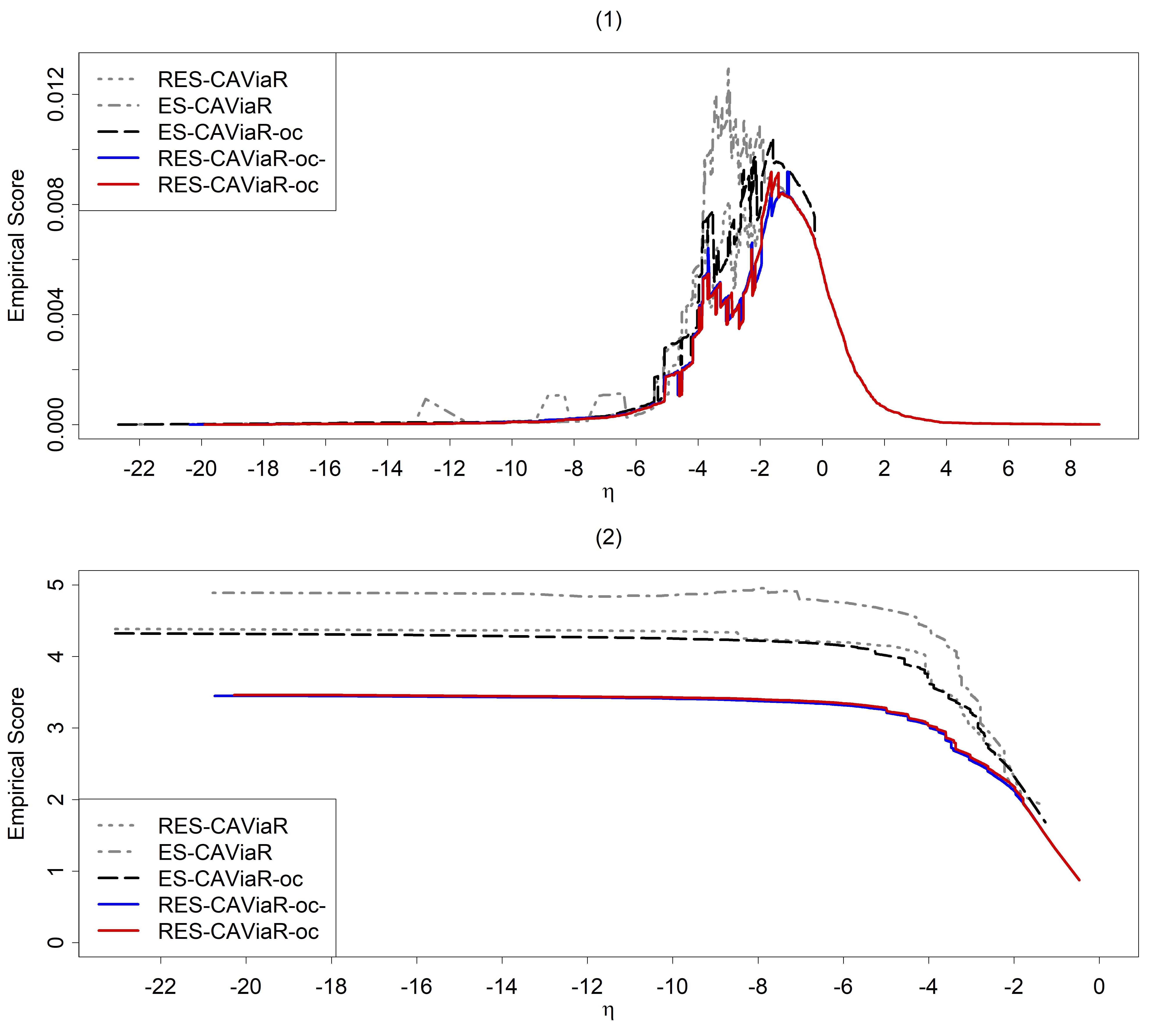

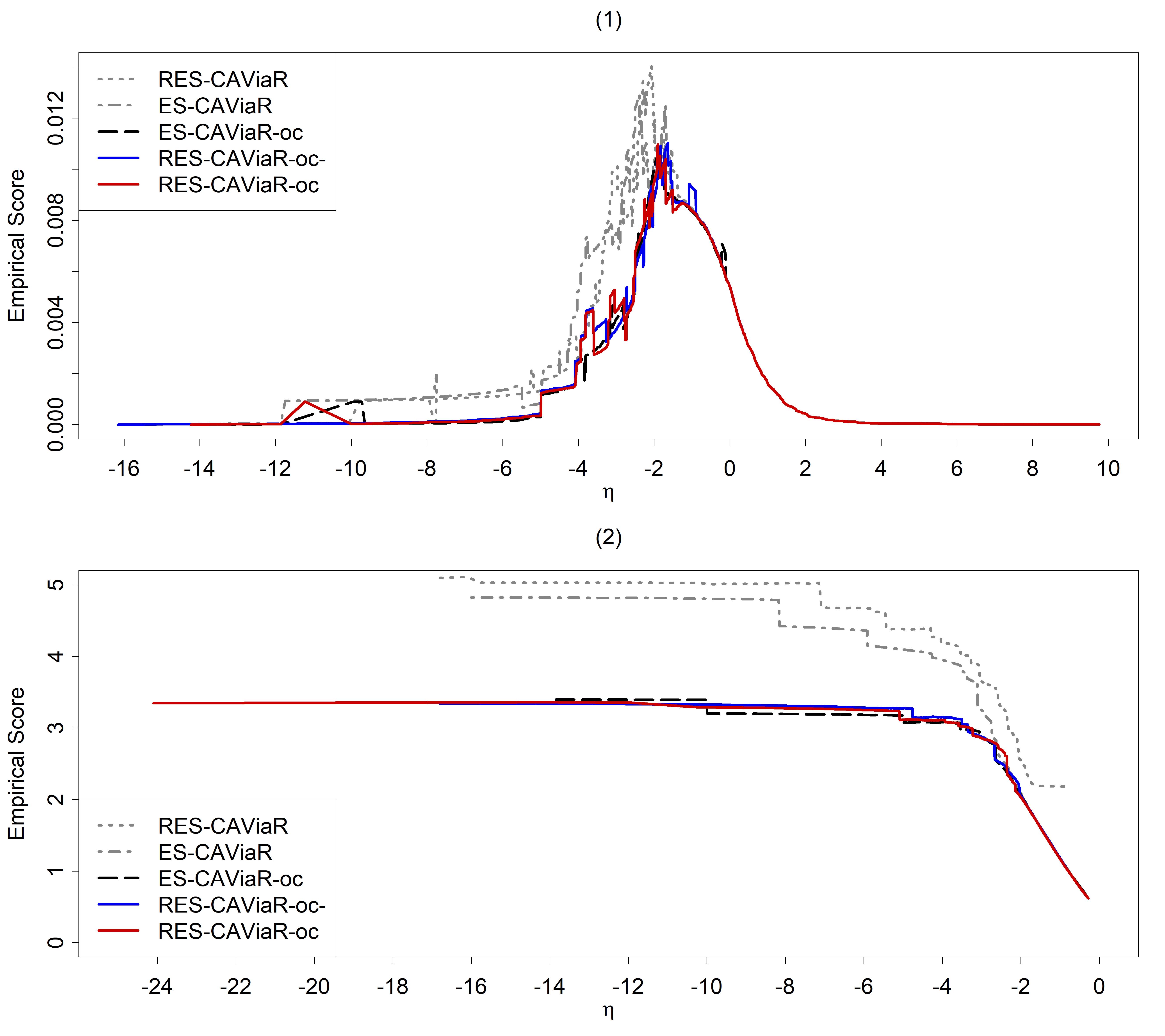

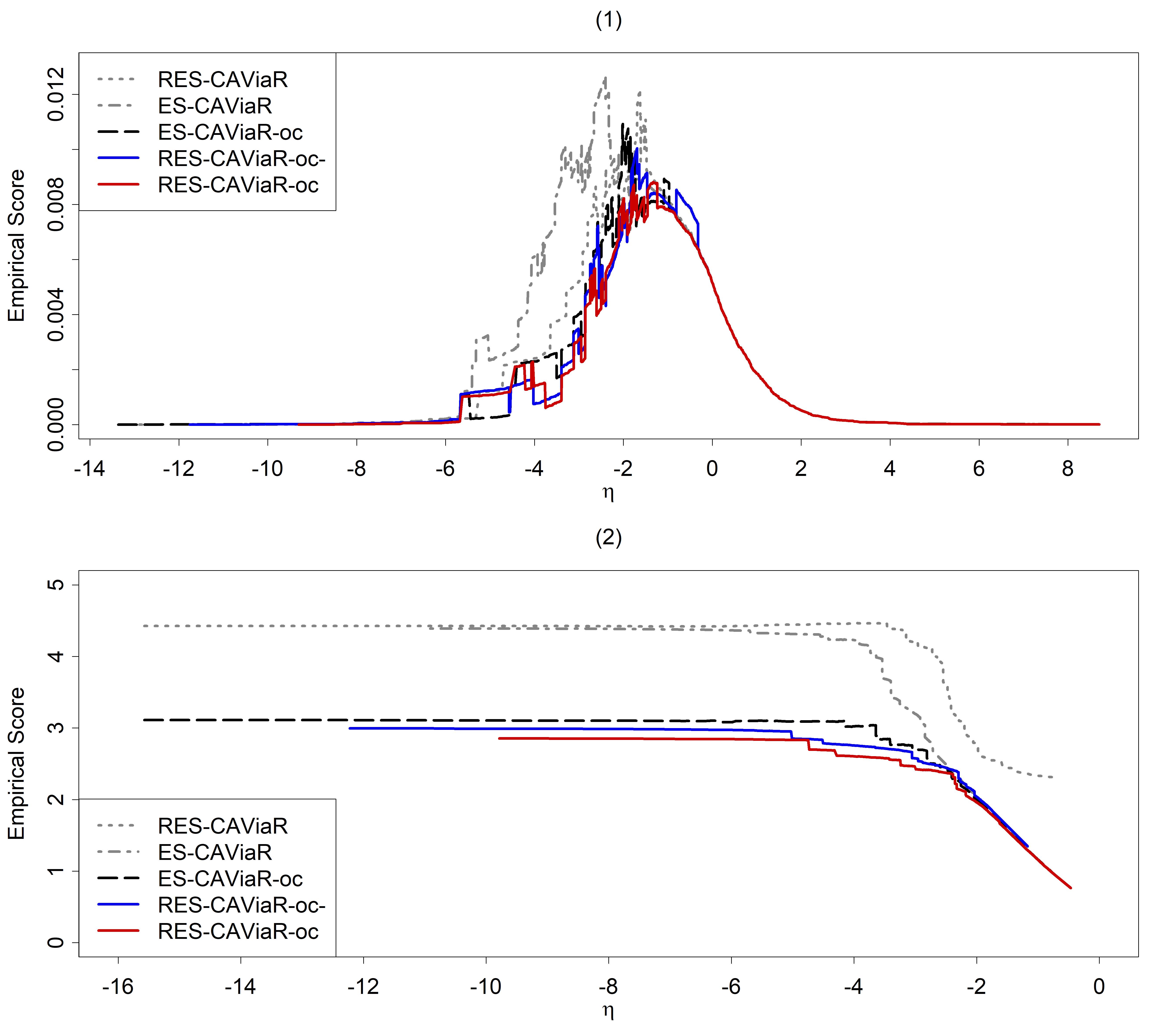

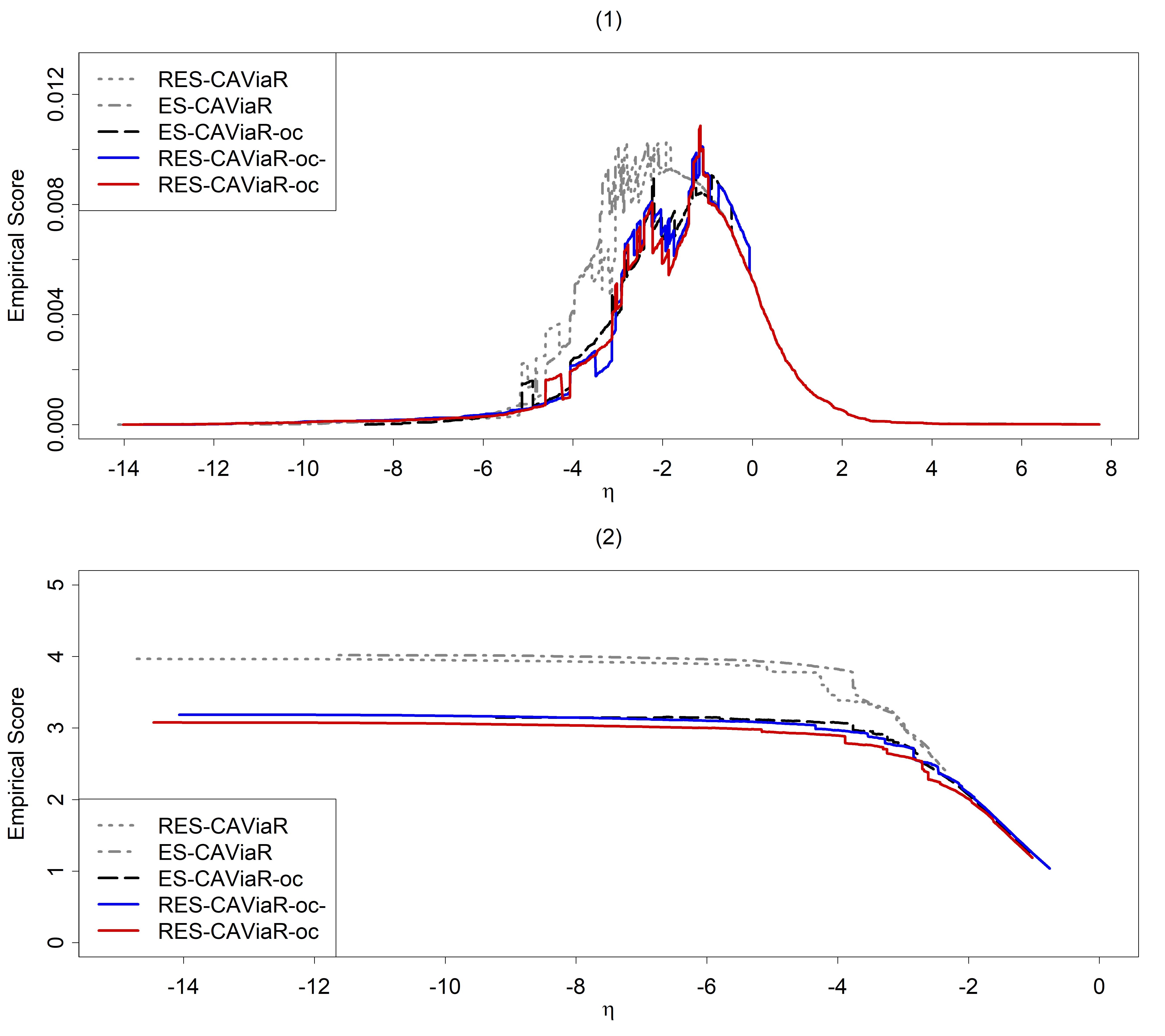

Regarding the ES evaluation, we first conduct the measurement of Embrechts, Kaufmann, and Patie (2005), which has the benefit of directly connecting ES to VaR and to the tail of the loss distribution. In addition, we apply the regression-based backtest proposed by Bayer and Dimitriadis (2022) for solely backtesting ES. For the pair assessment of VaR and ES, we consider the AL log score (Taylor 2019), which integrates the AL distribution and the class of scoring functions derived by Fissler and Ziegel (2016). Note that the latter two methods depend on the choice of the scoring function, for which the ranking of competing forecasts may change under a different scoring function (Patton 2020). Due to this concern, we provide the Murphy diagram of Ehm et al. (2016) and Ziegel et al. (2020), which is a powerful tool in assessing the quality of probabilistic forecasts of VaR or ES via visual inspection. The key advantages of using Murphy Diagrams for VaR or ES include (1) robustness: provides a robust forecasting evaluation against the choice of the scoring function; (2) comprehensive comparison: allows for performance assessment for a relevant class of scoring functions; (3) visual interpretation: facilitates clear graphical representation of model performance; and (4) versatility: applicable to various types of risk models. We also conduct a formal hypothesis test for forecast dominance (Ziegel et al. 2020), which is a strong concept showing that one forecast is superior to another under a relevant class of scoring functions.

The Basel Committee on Banking Supervision (2016) recommends a shift in risk metrics from VaR to ES and a reduction in the confidence level from 99% to 97.5%. This change heightens the focus on tail risk, thereby enabling banks to better understand their risk exposure through the examination of a more extensive set of worst-case scenarios and ensuring they have adequate capital to absorb potential losses. In alignment with these suggestions, we evaluate tail forecasts, VaR and ES, at the 1% and 2.5% levels for four international stock markets: NASDAQ in the U.S., DAX in Germany, HSI in Hong Kong, and Nikkei 225 in Japan. We consider five competing risk models, three related to our proposed models with overnight information, as well as ES-CAViaR of Taylor (2019) and RES-CAViaR with realized volatility of Chen et al. (2023).

The above-mentioned backtests and Murphy diagrams confirm that CAViaR-type models with overnight return and realized volatility are more efficient in forecasting tail risk than models without incorporating overnight information. In particular, our Murphy diagrams and related hypothesis tests indicate a strong relation of forecast dominance (Ziegel et al. 2020) between models with and without incorporating overnight information, which demonstrates the improvement of tail risk forecasting by nowcasting independently of the choice of the scoring function. Finally, by comparing standardized score differences, we observe that the improvement of incorporating overnight information is typically more significant in RES-CAViaR compared with ES-CAViaR, and in the two Asian markets in Japan and Hong Kong compared with those in U.S. and Germany.

The rest of the paper runs as follows. Section 2 presents the RES-CAViaR-type models. Section 3 explains the Bayesian Markov Chain Monte Carlo (MCMC) method for estimating unknown parameters, and describes our forecast evaluation methods. Section 4 shows the empirical analysis, which adopts four market indices to ensure the performance of our proposed models. Section 5 concludes the study.

2 Realized volatility CAViaR-type models

An asset’s opening price is usually not identical to its previous day’s closing price, because essential information related to the listed companies might be released after the financial market closes. The difference is that after-hours trading changes investor valuations or expectations for assets. Aside from news about companies, the development of after-hours trading has significantly influenced the difference between the previous closing price and the opening price. After-hours trading can also reflect volatility of a stock price.

When incorporating the idea of nowcasting, we take information on the difference between the opening price and the previous day’s closing price into our risk model. We calculate today’s tail risk once the market opens. For a given stock of interest, and respectively denote its opening price and closing price at time . The overnight return at time is . In the framework of nowcasting, the information set is generated by the union of all closing prices up to time and those of opening prices until time . For a given level, the conditional VaR and ES of given are and , respectively. Based on market reaction, we propose to use different coefficients in response to positive and negative . We now describe the first proposed model as follows.

ES-CAViaR-oc:

| (2) | |||

| (4) |

The stationarity condition in Eq. (2) is to ensure the stability of the time series. If the market perceives overnight information as negative, investors might become more risk-averse the following day. Additionally, if overnight information suggests that assets were previously overvalued, their prices might drop, leading to a higher VaR the next day. For these reasons, we expect to be a negative coefficient.

Realized volatility is an important factor to forecast tail risk as confirmed by many papers in the literature. Therefore, we further include the realized volatility series into Eq. (2).

RES-CAViaR-oc:

| (5) | |||

| (7) |

Here, , and we expect .

When a stock price falls in the opening market compared to the previous closing price, it creates market volatility to which traders and investors are sensitive. Hence, we only consider a negative effect of in the model.

RES-CAViaR-oc-:

| (8) | |||

| (10) |

Here, , and we expect . Note that the setting in (5) reduces to (2), and the setting in (5) gives (8). Therefore, ES-CAViaR-oc in Eq. (2) and RES-CAViaR-oc- in Eq. (8) are special cases of RES-CAViaR-oc in Eq. (5). For this reason, we describe our analysis for the most general RES-CAViaR-oc model (5) in the next section. We use the parsimonious models (2) and (8) to study the effects of the dropped explanatory variables in Section 4.

3 Estimation and forecast evaluations

3.1 Bayesian MCMC approach

This section describes the Bayesian approach and MCMC sampling procedures employed in estimating unknown parameters of the proposed model and for conducting the tail risk forecasting. For brevity, we present the procedures only for the RES-CAViaR-oc model.

Let in the RES-CAViaR-oc model, where and . Fundamentally, the MCMC method requires a posterior distribution of , which is the product of a prior distribution and a likelihood function , where , , and . We adopt the AL distribution as the log-likelihood function:

| (11) |

As in Taylor (2019), we assume throughout the paper that for every .

With flat priors on and , the prior specifications go as follows.

| (12) |

where , and . We impose and to guarantee the stability of the time series. In addition, the downside effects of realized volatility and negative overnight return to the tail risk are incorporated into the conditions . Finally, the constraints assure that for every .

The conditional posterior distribution is expressed by the likelihood function and prior distribution as follows:

| (13) |

where is the likelihood function for the proposed model in the description, and represents the vector without component .

In order to estimate the nonstandard posterior distribution for the proposed model, we employ an adaptive MCMC algorithm of Chen and So (2006), which integrates the random walk Metropolis algorithm (Metropolis et al. 1953) and independent kernel Metropolis-Hastings (MH) algorithm (Hastings 1970). The parameter groups of and are updated based on an adaptive MCMC method separately. The simulation study in Gerlach et al. (2011) employs Bayesian methods for the general quantile regression problem using the asymmetric-Laplace distribution. Their approach is designed for parameter estimation of the CAViaR model family via an adaptive MCMC sampling scheme. The study demonstrates favorable estimation performance regarding precision and efficiency compared to numerical optimization of the standard quantile criterion function. Although the model proposed in Gerlach et al. (2011) does not factor in realized volatility and overnight information, we believe the results still attest to the effectiveness of the adaptive MCMC methods for parameter estimation.

To forecast VaR and ES in the out-of-sample period for the RES-CAViaR-oc model, we choose a one-step-ahead approach with rolling window and compute them by all unknown parameters estimated in the MCMC procedure. Let be the number of total iterations of the MCMC run and be the burn-in period. The procedure based on the MCMC algorithm goes as follows.

-

Step 1: Initialize .

-

Step 2: For the th iteration, draw from the conditional posteriors:

by the random walk Metropolis if and independent kernel MH if .

-

Step 3: Collect , and based on:

-

Step 4: When , we calculate:

where and are obtained from Step 3.

3.2 Evaluation of VaR and ES forecasting

It is critical that financial regulators evaluate the accuracy of the proposed models in forecasting VaR and ES since both tail risks are unobservable. We employ various tests to evaluate the forecast performance of the proposed models, which include traditional backtests and recent comparative backtests based on loss (scoring) functions.

First, we identify the model’s forecasting accuracy equal to the nominal level by computing the violation rate (VRate) for quantile forecasting:

| (14) |

where is the in-sample period, is the out-of-sample period, and stands for VaR in the models. The closer VRate is to , the better the performance of the model is to forecast VaR. For a conservative evaluation of risk, we prefer VRate to be overestimated than underestimated.

Second, we employ three traditional VaR backtest procedures to properly evaluate the accuracy of the VaR forecast: UC test, CC test, and DQ test. Both CC and DQ are joint tests where the null hypothesis consists of the independence property of the VaR violation, equivalently correct conditional violation rate for a given model, and combined with a correct UC rate.

Third, we assess whether the ES forecast is specified correctly based on various measurements. Embrechts, Kaufmann, and Patie (2005) consider the measure , where is the sample mean of over the time points in when (estimated) VaR violation occurs, and is the sample mean of over the time points when with being the empirical -quantile of . We prefer the smallest value of for ES in the comparisons. We also examine the regression-based ES backtest proposed by Bayer and Dimitriadis (2022) for ES backtesting. We carry out three versions of the ES regression (ESR) backtests: Strict ESR, Auxiliary ESR, and Strict Intercept, using the R package esback (Bayer and Dimitriadis 2019).

Under the framework of a comparative backtest (Nolde and Ziegel 2017), a possibly vector-valued risk measure forecast is said to (empirically) dominate another with respect to a scoring function if:

We take function to be strictly consistent in the sense that the risk measure of interest is the unique minimizer of the expectation of with respect to the return. If such a function exists, then the risk measure is called elicitable. It is known that VaR is elicitable, and that the pair of risk measures , , is (jointly) elicitable (Fissler and Ziegel 2016). Therefore, we evaluate the forecasting accuracy of the series and the pair of series under certain choices of strictly consistent scoring functions. Among others, we use the quantile score (Giacomini and Komunjer 2005) for the comparative backtest of VaR:

| (15) |

For the pair of VaR and ES, we consider the AL log score (Taylor 2019), which integrates the AL distribution and the class of scoring functions derived by Fissler and Ziegel (2016). Under the assumption that , the AL log score is:

| (16) |

The AL log score is the negative logarithm of the AL distribution, and this interpretation connects the comparative backtest based on this score with the (quasi) maximum likelihood and Bayesian quantile regression frameworks.

A potential criticism of the above backtesting framework is that the scoring functions (15) and (16) are just a few of innumerable strictly consistent scoring functions of and , respectively. To address this issue, we also provide Murphy diagrams, which enable us to check whether one forecast dominates another under a relevant class of scoring functions. Ehm et al. (2016) propose the Murphy diagram for VaR, which plots the empirical elementary scores:

against . For ES, Ziegel et al. (2020) propose to plot:

against to evaluate the forecasting accuracy of ES.

We refer the reader to Ehm et al. (2016) and Ziegel et al. (2020) for more details, such as the range of the -axis of the diagram. These Murphy diagrams provide graphical ways to check forecast dominance, where a forecast , or , dominates others, independently of the choice of scoring functions, if its curve of empirical elementary scores against is lower than those of others on the entire line. The forecast dominance undergoes formal examination using the test proposed by Ziegel et al. (2020), which is based on the stationary bootstrap (Politis and Romano 1994).

4 Empirical study

This study utilizes data of daily (opening and closing) prices, as well as realized volatility data. We collect four market indices: Nasdaq Composite (U.S.), DAX (Germany), Hang Seng Index (HSI, Hong Kong), and Nikkei 225 (Japan). From Oxford-Man Institute of Quantitative Finance by Heber et al. (2009), we download the daily returns , where is defined as closing price on day , close-to-open returns , where is defined as opening price on day , and the square root of median realized volatility is .

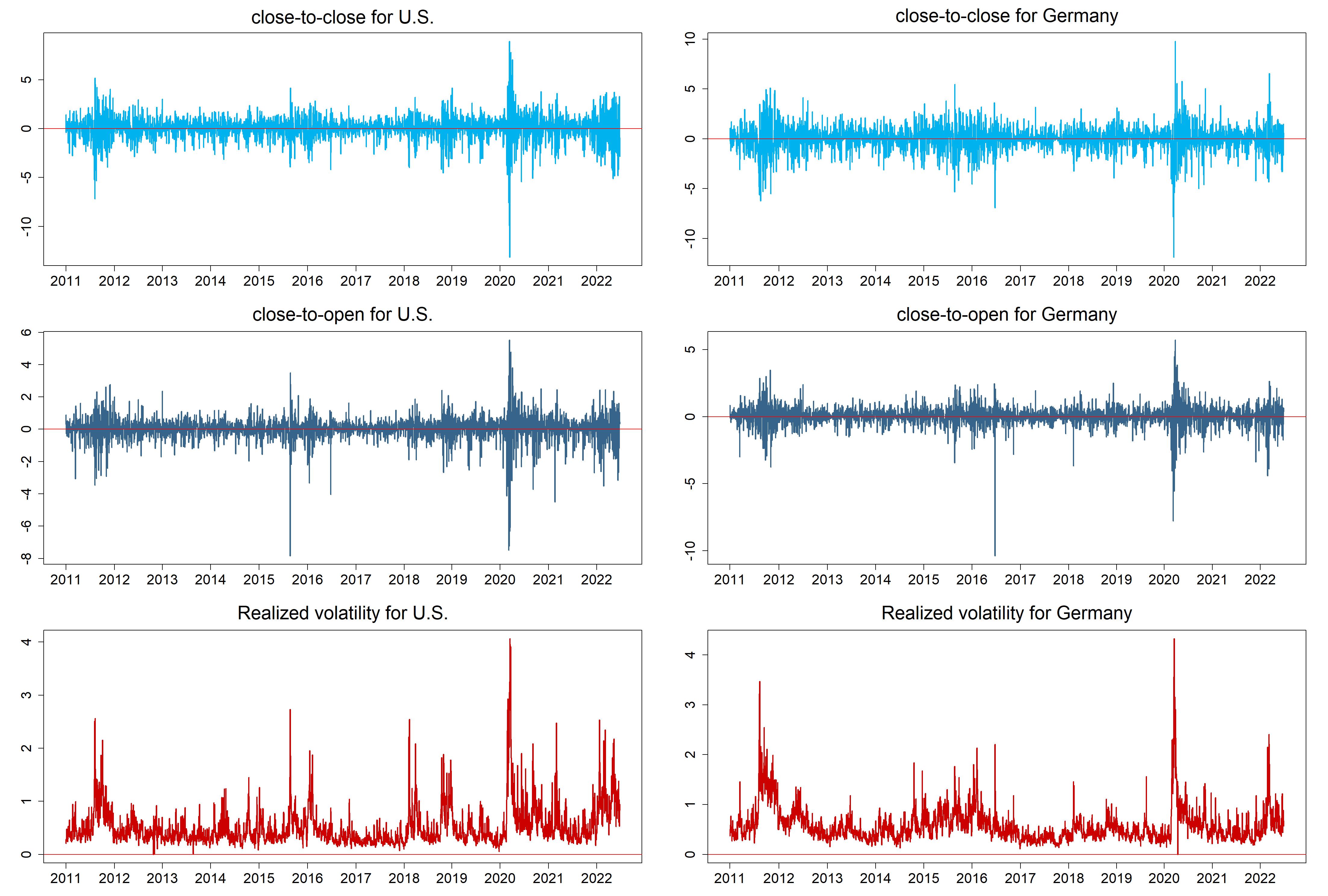

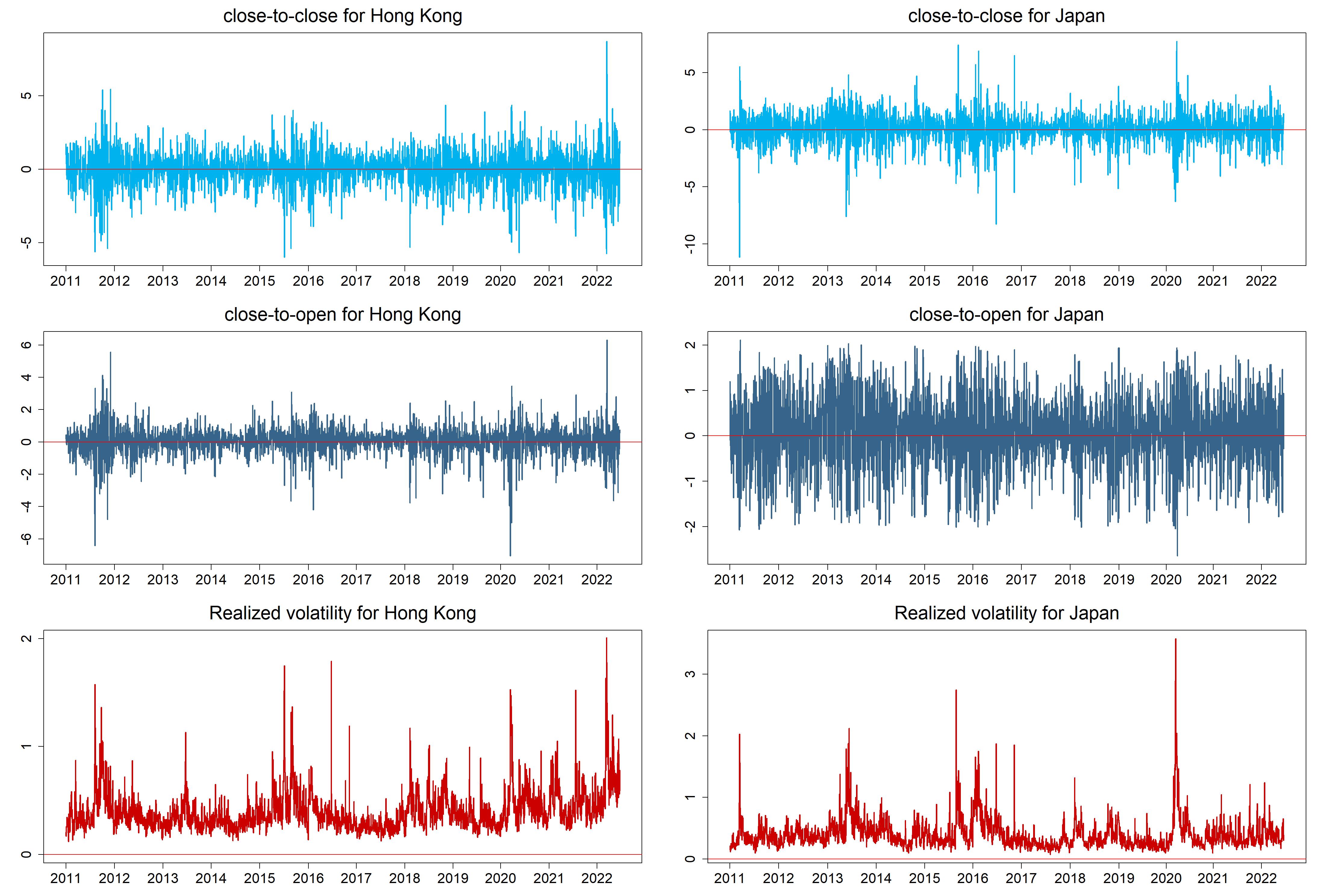

We divide the dataset into two parts: one is the in-sample period from January 3, 2011 to December 31, 2017, and the other is the out-of-sample period from January 2, 2018 to June 28, 2022. The out-of-sample period covers the COVID-19 pandemic period and the circuit breakers in the U.S. stock market in March 2020. Table 1 exhibits the summary statistics for the series of , , and . The series of and exhibit left skewness, while shows right skewness in all of the markets. The series is much more skewed than the series in the out-of-sample period for all markets. Figures 1 and 2 are the time plots of , , and for each market.

| Market | Period | Mean | Std | Skewness | Excess | Min | Max |

|---|---|---|---|---|---|---|---|

| kurtosis | |||||||

| U.S. | In-sample | ||||||

| 0.0543 | 1.0219 | -0.4916 | 4.0615 | -7.1685 | 5.1919 | ||

| 0.0321 | 0.6213 | -1.5929 | 19.3854 | -7.8300 | 3.4956 | ||

| 0.4417 | 0.2704 | 2.6949 | 12.1243 | 0.0000 | 2.7297 | ||

| Out-of-sample | |||||||

| 0.0430 | 1.5964 | -0.8308 | 7.8033 | -13.1409 | 8.9264 | ||

| 0.0429 | 0.9676 | -1.4884 | 11.4856 | -7.4754 | 5.5183 | ||

| 0.6504 | 0.4814 | 2.5585 | 10.0379 | 0.0529 | 4.0618 | ||

| Germany | In-sample | ||||||

| 0.0352 | 1.2463 | -0.3188 | 2.8239 | -6.9250 | 5.4459 | ||

| 0.0375 | 0.6961 | -2.0460 | 30.3964 | -10.3707 | 3.4814 | ||

| 0.6002 | 0.3483 | 2.2364 | 8.5089 | 0.1118 | 3.4666 | ||

| Out-of-sample | |||||||

| 0.0021 | 1.3476 | -0.6325 | 10.2397 | -11.8631 | 9.7634 | ||

| 0.0218 | 0.9035 | -0.9364 | 11.9028 | -7.7812 | 5.7059 | ||

| 0.5679 | 0.3766 | 4.1954 | 27.6662 | 0.0000 | 4.3226 | ||

| Hong Kong | In-sample | ||||||

| 0.0152 | 1.1409 | -0.2975 | 2.7641 | -5.9799 | 5.4535 | ||

| 0.0553 | 0.8072 | -0.4703 | 7.0448 | -6.4188 | 5.5614 | ||

| 0.3654 | 0.1662 | 2.7188 | 12.9573 | 0.1176 | 1.7931 | ||

| Out-of-sample | |||||||

| -0.0295 | 1.3688 | -0.0630 | 3.1543 | -5.7351 | 8.7072 | ||

| 0.0448 | 0.9502 | -0.7125 | 6.4850 | -7.0391 | 6.3041 | ||

| 0.4643 | 0.2088 | 2.1383 | 7.8327 | 0.1592 | 2.0100 | ||

| Japan | In-sample | ||||||

| 0.0466 | 1.3680 | -0.5936 | 6.1547 | -11.1534 | 7.4262 | ||

| 0.0592 | 0.8115 | -0.1524 | -0.1471 | -2.0717 | 2.1097 | ||

| 0.4151 | 0.2451 | 2.7385 | 12.9574 | 0.0740 | 2.7455 | ||

| Out-of-sample | |||||||

| 0.0160 | 1.2765 | -0.1262 | 3.6175 | -6.2736 | 7.7314 | ||

| 0.0245 | 0.7656 | -0.2236 | 0.0276 | -2.6409 | 1.9427 | ||

| 0.3798 | 0.2542 | 4.6227 | 38.1402 | 0.0941 | 3.5747 |

We consider five competing risk models. Three of them are proposed in this study: (1) ES-CAViaR-oc with overnight information in Eq. (2); (2) RES-CAViaR-oc with overnight information and realized volatility in Eq. (5); and (3) RES-CAViaR-oc- with negative overnight information and realized volatility in Eq. (8). The other two we consider for comparison are: (4) ES-CAViaR of Taylor (2019) and (5) RES-CAViaR with realized volatility of Chen et al. (2023). The latter two appear as follows.

ES-CAViaR:

| (17) | |||

| (19) |

RES-CAViaR:

| (20) | |||

| (22) |

Here, in (17) and in (20) are the stationarity conditions, respectively. For all the CAViaR models, the initial values are set to be negative. In our experiment, the results are robust when we vary the initial values.

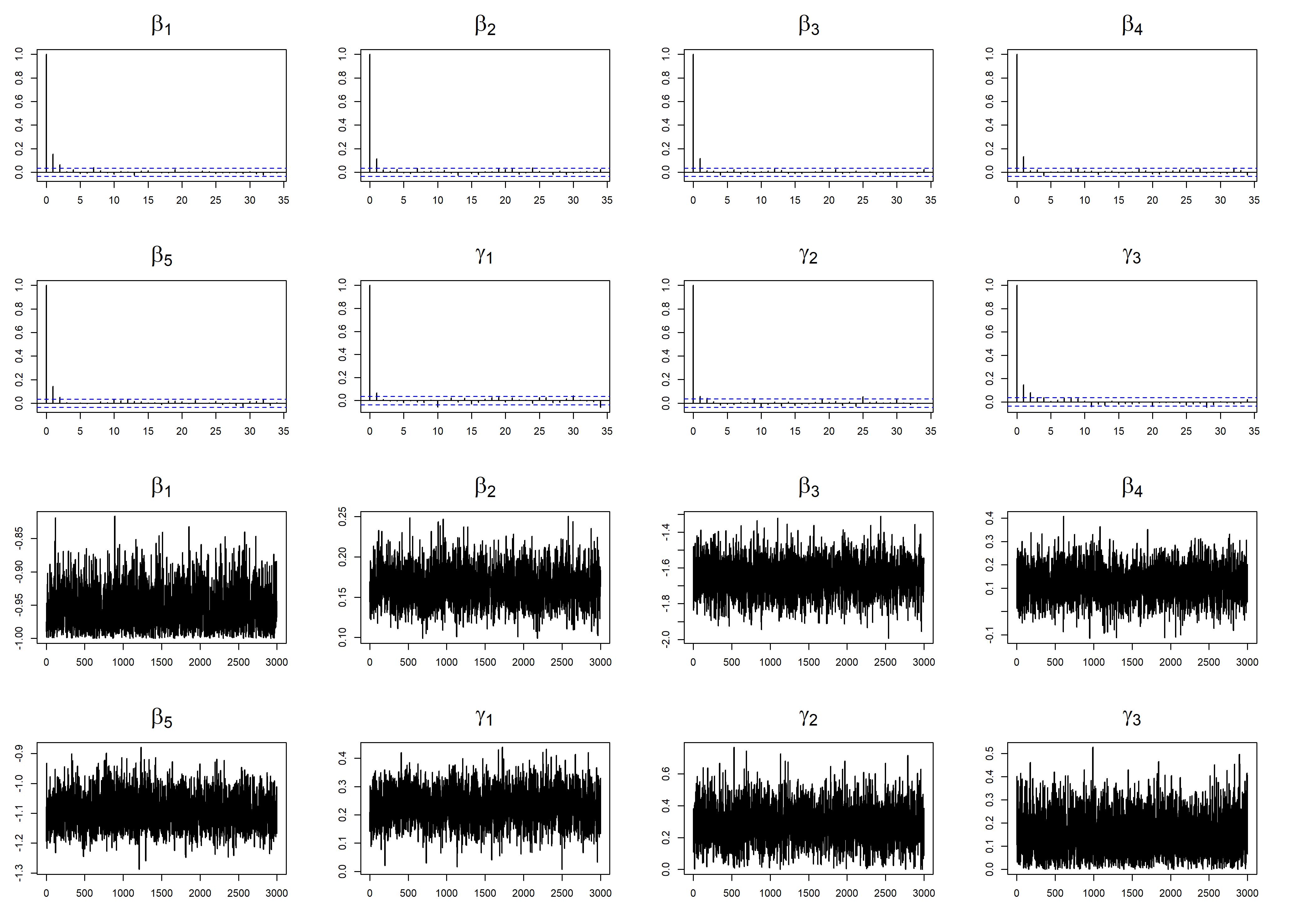

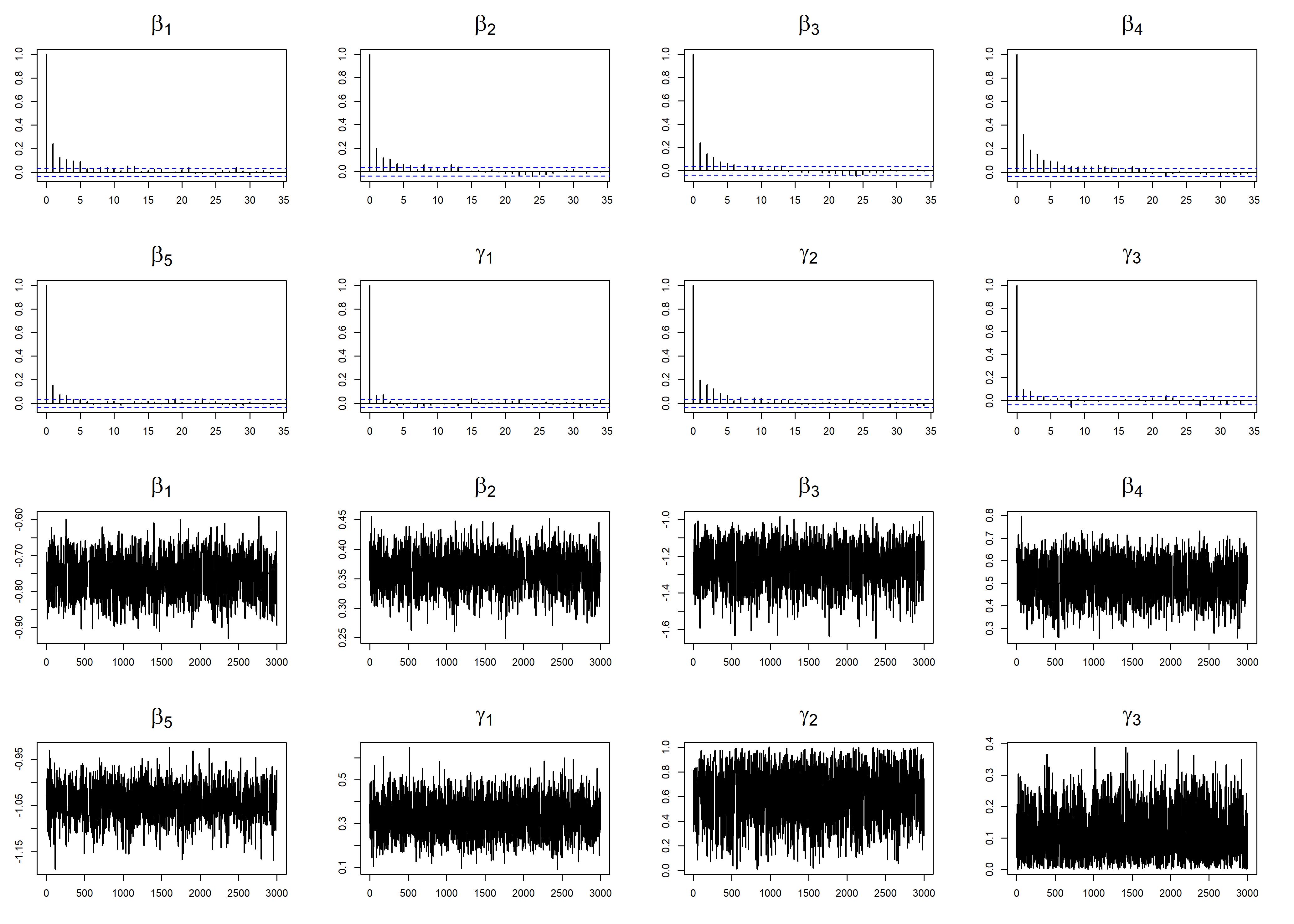

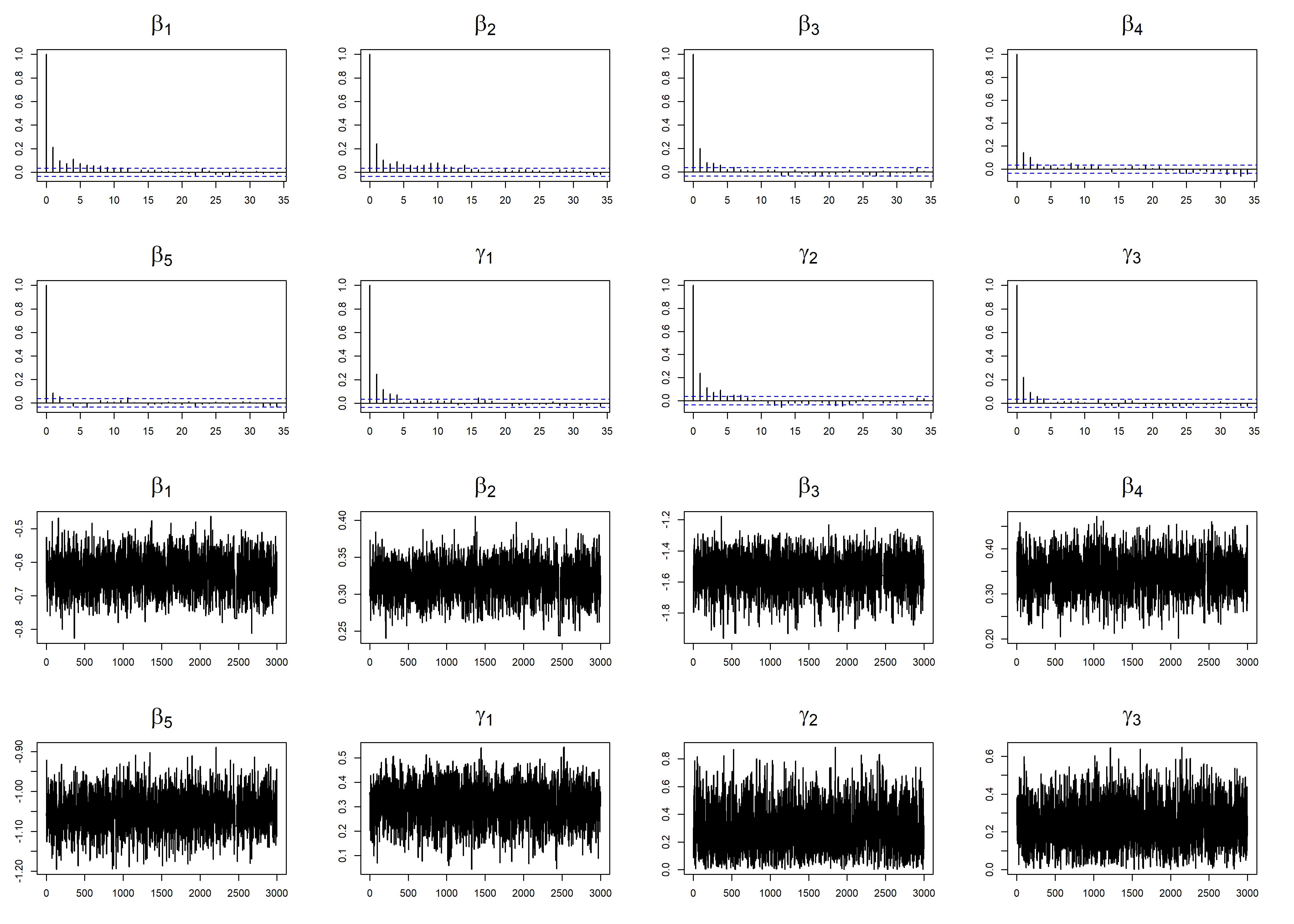

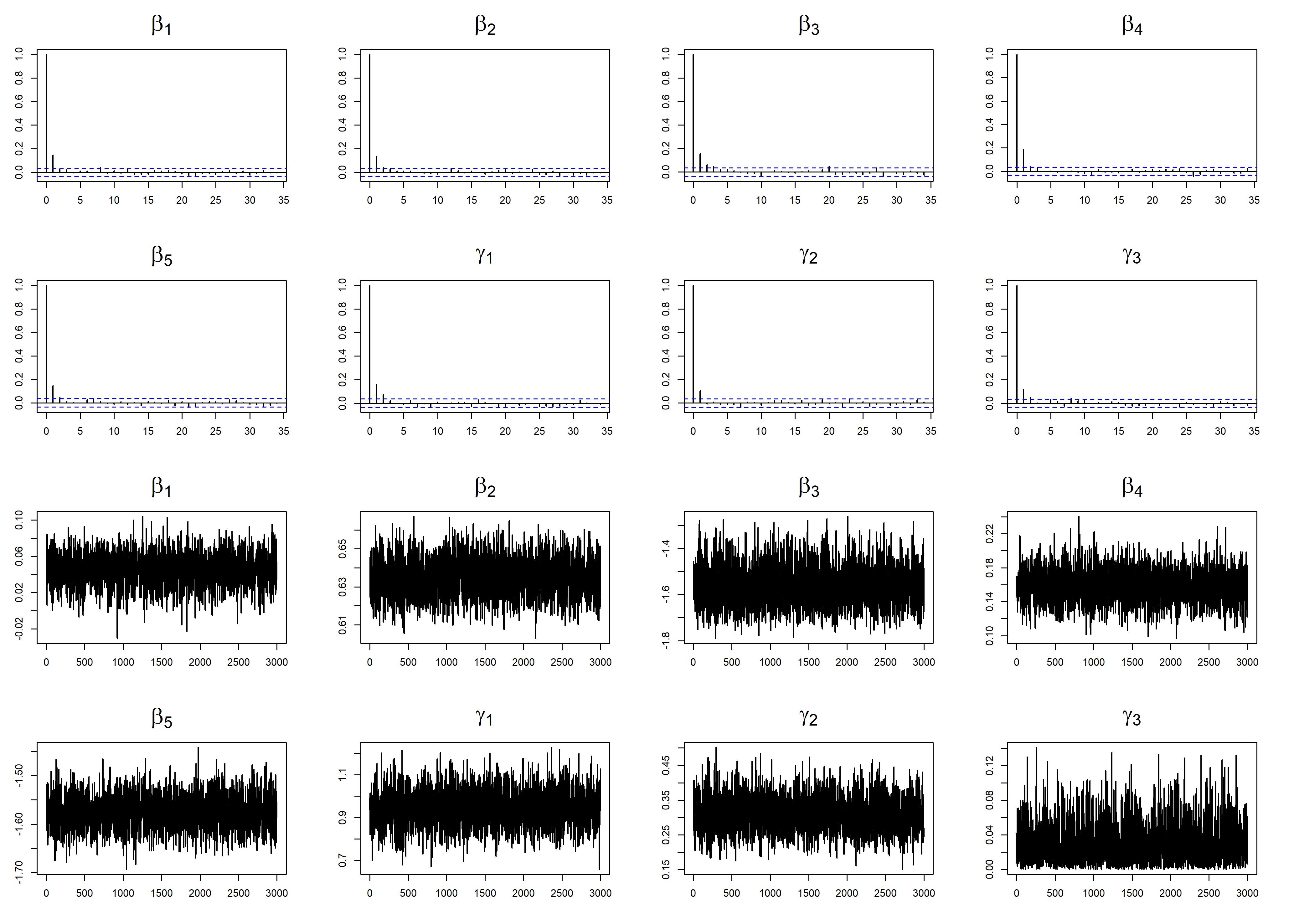

The adaptive MCMC method consists of two steps. We carry out 20,000 MCMC iterations, discard the first 8,000 iterations as the burn-in period, and include only every fourth iteration in the sample period for inference. Gelman et al. (1996) demonstrate that the acceptance rate should be between 25% to 50% in the MCMC procedure. To ensure rapid convergence and an optimal mix of adaptive MCMC, the trace plot and autocorrelation function (ACF) plot reflect the convergence conditions. Convergence diagnostic plots are in Supplementary Materials. We discover that the ACF plots decay quickly and that the trace plots are a good mix, denoting that the MCMC iterations reach convergence from these plots.

| U.S. | Germany | |||||||||

| Mean | Median | Std | 2.5 | 97.5 | Mean | Median | Std | 2.5 | 97.5 | |

| -0.7478 | -0.7492 | 0.0335 | -0.8113 | -0.6799 | -0.7199 | -0.7161 | 0.0582 | -0.8349 | -0.6101 | |

| 0.2496 | 0.2496 | 0.0267 | 0.1981 | 0.3011 | 0.3636 | 0.3631 | 0.0262 | 0.3118 | 0.4147 | |

| -1.6094 | -1.6045 | 0.1007 | -1.8128 | -1.4347 | -1.2814 | -1.2792 | 0.0907 | -1.4914 | -1.1087 | |

| 0.0760 | 0.0779 | 0.0707 | -0.0698 | 0.2174 | 0.4841 | 0.4866 | 0.0845 | 0.3350 | 0.6455 | |

| -1.1728 | -1.1766 | 0.0638 | -1.2867 | -1.0407 | -1.0442 | -1.0446 | 0.0263 | -1.0982 | -0.9910 | |

| 0.2652 | 0.2658 | 0.0611 | 0.1420 | 0.3851 | 0.2807 | 0.2857 | 0.0723 | 0.1309 | 0.4154 | |

| 0.2561 | 0.2528 | 0.1061 | 0.0576 | 0.4669 | 0.7706 | 0.7845 | 0.1384 | 0.4547 | 0.9860 | |

| 0.1208 | 0.1009 | 0.0933 | 0.0044 | 0.3511 | 0.1384 | 0.1215 | 0.0993 | 0.0063 | 0.3648 | |

| Hong Kong | Japan | |||||||||

| -0.7128 | -0.7117 | 0.0587 | -0.8367 | -0.6082 | 0.0356 | 0.0390 | 0.0264 | -0.0200 | 0.0831 | |

| 0.2901 | 0.2931 | 0.0334 | 0.2117 | 0.3467 | 0.6361 | 0.6364 | 0.0111 | 0.6132 | 0.6572 | |

| -1.5477 | -1.5436 | 0.1223 | -1.8302 | -1.3341 | -1.5112 | -1.5192 | 0.1277 | -1.7167 | -1.2271 | |

| 0.3820 | 0.3835 | 0.0443 | 0.2912 | 0.4624 | 0.1516 | 0.1511 | 0.0233 | 0.1110 | 0.2002 | |

| -1.0172 | -1.0170 | 0.0541 | -1.1266 | -0.9139 | -1.5864 | -1.5857 | 0.0393 | -1.6636 | -1.5133 | |

| 0.2564 | 0.2558 | 0.0836 | 0.0958 | 0.4143 | 0.9718 | 0.9713 | 0.0853 | 0.8105 | 1.1345 | |

| 0.3547 | 0.3487 | 0.1760 | 0.0476 | 0.7084 | 0.3043 | 0.3004 | 0.0546 | 0.2014 | 0.4169 | |

| 0.3396 | 0.3408 | 0.1228 | 0.0957 | 0.5781 | 0.0296 | 0.0210 | 0.0288 | 0.0008 | 0.1092 | |

For the initial value, we select and , where represents the number of parameters for in the proposed model. Tables 2 and 3 present the Bayesian estimates for the two oc-type models across the four stock markets. These estimates include posterior means, medians, standard deviations, and 95% credible intervals for the unknown parameters. For the RES-CAViaR-oc model, we note that the estimates for the U.S. market and for the Japan market are insignificant, as their 95% credible intervals include zero. Similarly, for the RES-CAViaR-oc- model, for the Japan market is not significant. Since all the other estimated coefficients are significant, we conclude that both realized volatility and positive overnight return explain the variation in tail risk.

| U.S. | Germany | |||||||||

| Mean | Median | Std | 2.5 | 97.5 | Mean | Median | Std | 2.5 | 97.5 | |

| -0.6282 | -0.6298 | 0.0582 | -0.7364 | -0.5038 | -0.7643 | -0.7669 | 0.0443 | -0.8427 | -0.6740 | |

| 0.2616 | 0.2638 | 0.0316 | 0.1965 | 0.3209 | 0.1669 | 0.1642 | 0.0324 | 0.1081 | 0.2370 | |

| -1.8802 | -1.8839 | 0.1033 | -2.0887 | -1.6766 | -1.9311 | -1.9346 | 0.1240 | -2.1701 | -1.6422 | |

| -1.2534 | -1.2574 | 0.0743 | -1.3953 | -1.1151 | -1.1340 | -1.1336 | 0.0613 | -1.2489 | -1.0324 | |

| 0.2978 | 0.2974 | 0.0623 | 0.1725 | 0.4248 | 0.2499 | 0.2515 | 0.0593 | 0.1297 | 0.3613 | |

| 0.1703 | 0.1640 | 0.0944 | 0.0135 | 0.3751 | 0.7842 | 0.7954 | 0.1268 | 0.5125 | 0.9849 | |

| 0.1211 | 0.1053 | 0.0877 | 0.0041 | 0.3254 | 0.0765 | 0.0633 | 0.0590 | 0.0030 | 0.2159 | |

| Hong Kong | Japan | |||||||||

| -0.5649 | -0.5678 | 0.0401 | -0.6325 | -0.4819 | 0.0023 | 0.0045 | 0.0346 | -0.0754 | 0.0741 | |

| 0.3055 | 0.3038 | 0.0248 | 0.2620 | 0.3571 | 0.7346 | 0.7354 | 0.0163 | 0.6990 | 0.7661 | |

| -1.3807 | -1.3800 | 0.0895 | -1.5656 | -1.2155 | -1.0280 | -1.0258 | 0.1253 | -1.2884 | -0.7893 | |

| -1.2980 | -1.2973 | 0.0387 | -1.3835 | -1.2223 | -0.9925 | -0.9954 | 0.0623 | -1.1095 | -0.8728 | |

| 0.2369 | 0.2299 | 0.1038 | 0.0529 | 0.4489 | 0.9872 | 0.9883 | 0.0804 | 0.8327 | 1.1430 | |

| 0.5217 | 0.5302 | 0.1680 | 0.1760 | 0.8435 | 0.1726 | 0.1716 | 0.0502 | 0.0732 | 0.2693 | |

| 0.2908 | 0.2944 | 0.1357 | 0.0362 | 0.5493 | 0.0448 | 0.0342 | 0.0395 | 0.0013 | 0.1449 | |

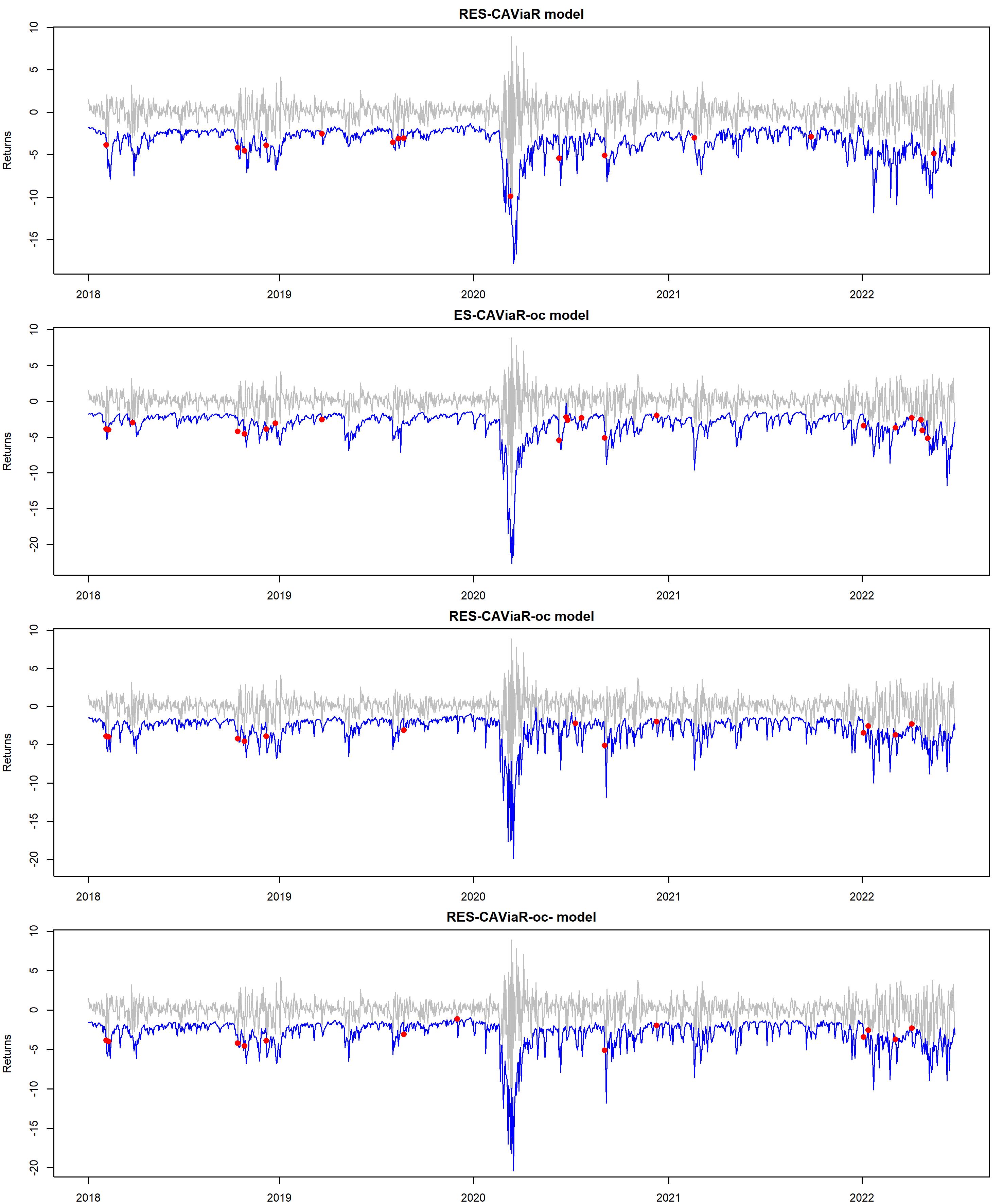

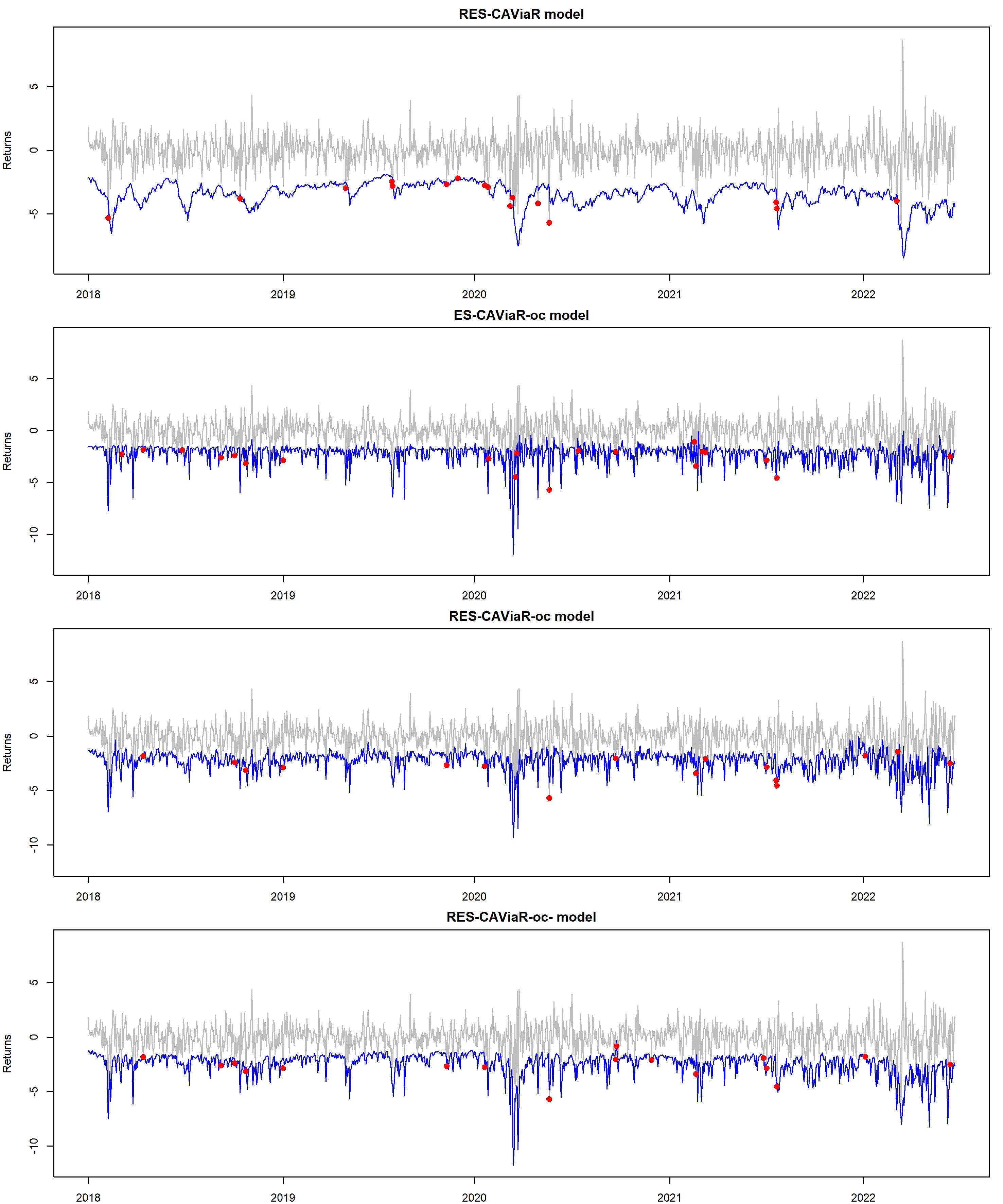

Due to space limits, we only provide two violation plots for U.S. and Hong Kong in Figures 3 and 4, respectively, which illustrate the VaR violation plots at the 1% level based on the ES-CAViaR-oc, RES-CAViaR, RES-CAViaR-oc, and RES-CAViaR-oc- models. We examine the performance of forecasting by observing the violation during the circuit breakers in the U.S. stock market in March 2020. In this study, all four markets are successfully able to capture the extreme negative return for forecasting in the RES-CAViaR-oc and RES-CAViaR-oc- models.

Table 4 displays the 1% level forecasting performance for each model. The fourth column shows the VRate at , with values closer to 1% indicating superior models. For instance, between 0.9% and 1.1% VRate, 0.9% is preferable as it forecasts more conservatively. The boldface values in this column highlight the models that are closest to the desired 1% rate. The fifth column lists the rejection counts for the UC, CC, and DQ tests in out-of-sample forecasts. If the p-value is below 5%, we count the number of rejections. Notably, both RES-CAViaR-oc and RES-CAViaR-oc- pass the backtests across all markets. The final column employs the ES evaluation method (Embrechts, Kaufmann, and Patie 2005), where smaller values are favored.

In the U.S. and Germany markets, RES-CAViaR-oc- stands out as the best-performing model. In the Hong Kong market, three models have the same violation rate which is the closest to 1%. However, RES-CAViaR-oc- is favored when considering the ES evaluation method. For Japan, the simple ES-CAViaR model has the violation rate closest to 1% and the smallest ES value, making it the most favored model for this market. Finally, the last column represents the number of rejections from three ES regression (ESR) backtesting methods (Bayer and Dimitriadis 2019, 2022): Strict ESR, Auxiliary ESR, and Strict Intercept. All tests are two-sided, and decisions are based on the 10% significance level. The results suggest that RES-CAViaR and ES-CAViaR do not forecast the ES effectively for the Germany market, aligning with the findings from the ES evaluation method.

Table 5 presents the forecasting performance of each model at the 2.5% level. According to the VRate column, at the level the RES-CAViaR model is most appropriate for the U.S. market, while RES-CAViaR-oc- is the most suitable choice for the Germany market. For Japan, RES-CAViaR-oc is selected based on its superior forecasting accuracy. Using the ES evaluation method, the U.S. and Germany markets prefer the RES-CAViaR-oc- model, while the Hong Kong market opts for the ES-CAViaR-oc model. The ESR backtests reveal that the RES-CAViaR model for Hong Kong and the models incorporating overnight returns in Japan do not provide precise ES forecasts. These findings align with the results of the ES evaluation method presented in the sixth column. On the whole, the ES-CAViaR model is effective for Japan, whereas the RES-CAViaR-oc- model seems to be a fitting choice for the other markets.

[t] Market Model Violation Violation Count of rejection ES Count of rejection number rate % VaR backtestsa evaluationb ESR backtestsc U.S. RES-CAViaR 14 1.25 0 0.1989 0 ES-CAViaR 22 1.96 3 0.3585 0 ES-CAViaR-oc 20 1.78 3 0.2069 0 RES-CAViaR-oc- 13 1.16 0 0.0175 0 RES-CAViaR-oc 13 1.16 0 0.0709 0 Germany RES-CAViaR 26 2.30 3 0.7876 1 ES-CAViaR 20 1.77 3 0.6831 1 ES-CAViaR-oc 8 0.71 0 0.1639 0 RES-CAViaR-oc- 13 1.15 0 0.0853 0 RES-CAViaR-oc 14 1.24 0 0.1374 0 Hong Kong RES-CAViaR 16 1.47 2 0.3547 0 ES-CAViaR 16 1.47 0 0.2954 0 ES-CAViaR-oc 20 1.83 3 0.1291 0 RES-CAViaR-oc- 17 1.56 0 0.0825 0 RES-CAViaR-oc 16 1.47 0 0.0913 0 Japan RES-CAViaR 15 1.39 0 0.0700 0 ES-CAViaR 11 1.02 0 0.0137 0 ES-CAViaR-oc 10 0.93 0 0.4621 0 RES-CAViaR-oc- 11 1.02 0 0.3034 0 RES-CAViaR-oc 12 1.11 0 0.2094 0 aNumber of rejections of UC, CC, and DQ tests are based on the 5% significance level. b The ES evaluation method by Embrechts, Kaufmann, and Patie (2005). The boldface highlights the most favored model. c The three ES regression (ESR) backtesting methods—Strict ESR, Auxiliary ESR, and Strict Intercept, cited in (Bayer and Dimitriadis 2019, 2022)—determine the number of rejections at the 10% significance level. All tests are two-sided.

[t] Market Model Violation Violation Count of rejection ES Count of rejection number rate % VaR backtestsa evaluationb ESR backtestsc U.S. RES-CAViaR 29 2.58% 0 0.2000 0 ES-CAViaR 43 3.83% 2 0.2234 0 ES-CAViaR-oc 42 3.74% 3 0.1117 0 RES-CAViaR-oc- 36 3.21% 0 0.0505 0 RES-CAViaR-oc 33 2.94% 0 0.0827 0 Germany RES-CAViaR 43 3.81% 3 0.4345 0 ES-CAViaR 37 3.28% 0 0.2255 0 ES-CAViaR-oc 36 3.19% 0 0.3141 0 RES-CAViaR-oc- 30 2.66% 0 0.0394 0 RES-CAViaR-oc 33 2.92% 0 0.2110 0 Hong Kong RES-CAViaR 37 3.39% 2 0.2782 2 ES-CAViaR 41 3.75% 2 0.1722 0 ES-CAViaR-oc 45 4.12% 3 0.1350 0 RES-CAViaR-oc- 30 2.75% 0 0.3566 0 RES-CAViaR-oc 37 3.39% 1 0.2727 0 Japan RES-CAViaR 31 2.88% 0 0.0523 0 ES-CAViaR 23 2.13% 0 0.0453 0 ES-CAViaR-oc 26 2.41% 0 0.3581 1 RES-CAViaR-oc- 30 2.78% 0 0.3629 2 RES-CAViaR-oc 27 2.50% 0 0.1981 2 aNumber of rejections of UC, CC, and DQ tests are based on the 5% significance level. b The ES evaluation method by Embrechts, Kaufmann, and Patie (2005). The boldface highlights the most favored model. c The three ES regression (ESR) backtesting methods—Strict ESR, Auxiliary ESR, and Strict Intercept, cited in (Bayer and Dimitriadis 2019, 2022)—determine the number of rejections at the 10% significance level. All tests are two-sided.

| Level | Market | RES-CAViaR | ES-CAViaR | ES-CAViaR-oc | RES-CAViaR-oc- | RES-CAViaR-oc |

|---|---|---|---|---|---|---|

| U.S. | 49.1663 | 54.8570 | 48.4814 | 38.6955 | 38.8420 | |

| Germany | 57.5574 | 54.4840 | 38.8935 | 37.7599 | 37.7904 | |

| 1% | Hong Kong | 48.3234 | 47.9249 | 33.8620 | 32.6990 | 31.1612 |

| Japan | 42.7430 | 43.3155 | 33.8938 | 34.3394 | 32.8257 | |

| Avg lossa | 49.4475 | 50.1453 | 38.7827 | 35.8734 | 35.1548 | |

| U.S. | 105.6847 | 111.0860 | 98.2114 | 85.0127 | 84.5575 | |

| Germany | 109.5971 | 104.0882 | 86.3762 | 95.8727 | 77.3612 | |

| 2.5% | Hong Kong | 101.0733 | 103.9773 | 70.3721 | 72.1480 | 72.3486 |

| Japan | 90.5812 | 92.4619 | 69.4997 | 63.0793 | 63.5964 | |

| Avg lossa | 101.7341 | 102.9034 | 81.1148 | 79.0282 | 74.4659 |

-

•

aAvg loss is the average loss of the four stock markets in every model.

-

•

∗Boldface number represents the best model in each market.

Table 6 illustrates the quantile score for VaR at two different levels: 1% and 2.5%, for five models, in which the most accurate model should minimize the scoring functions. For each of the two VaR levels, the lowest quantile score (boldface number) in each market indicates the best-performing model for that market, as a lower score indicates a better fit to the data. At the 1% VaR level, the RES-CAViaR-oc- model performs best in the U.S. and Germany markets, while the RES-CAViaR-oc model outperforms in the Hong Kong and Japan markets. At the 2.5% VaR level, the RES-CAViaR-oc model provides the best performance in the U.S. and Germany markets, whereas the RES-CAViaR-oc- model is superior in the Hong Kong and Japan markets.

The AL log score, as per Taylor (2019), is a measure used to evaluate the goodness of fit of these models. Lower AL log scores indicate a better fit of the model to the data. Table 7 presents the scoring function by the AL distribution at the 1% and 2.5% levels, evaluating VaR and ES jointly. At the 1% level, as the scoring function is smallest, RES-CAViaR-oc- is outstanding in the U.S. and Germany markets; otherwise, RES-CAViaR-oc is the best in the Hong Kong and Japan markets. The last row demonstrates RES-CAViaR-oc is most appropriate by average loss. As for the 2.5% level, RES-CAViaR-oc- has the best performance in the U.S., Hong Kong, and Japan markets, and RES-CAViaR-oc has the best performance in the Germany market. Finally, the RES-CAViaR-oc is more outstanding for both functions than the others.

| Level | Market | RES-CAViaR | ES-CAViaR | ES-CAViaR-oc | RES-CAViaR-oc- | RES-CAViaR-oc |

|---|---|---|---|---|---|---|

| U.S. | 2685.305 | 2984.366 | 2822.656 | 2423.667 | 2457.262 | |

| Germany | 2942.582 | 2877.914 | 2524.169 | 2487.010 | 2500.123 | |

| 1% | Hong Kong | 2740.954 | 2735.130 | 2378.305 | 2305.682 | 2248.653 |

| Japan | 2532.623 | 2565.484 | 2325.988 | 2360.695 | 2240.589 | |

| Avg lossa | 2725.366 | 2790.724 | 2512.780 | 2394.264 | 2361.657 | |

| U.S. | 2511.184 | 2690.685 | 2492.153 | 2301.253 | 2318.049 | |

| Germany | 2613.412 | 2568.101 | 2885.410 | 2855.559 | 2320.561 | |

| 2.5% | Hong Kong | 2529.315 | 2565.263 | 2190.503 | 2166.356 | 2168.694 |

| Japan | 2374.241 | 2399.931 | 2112.757 | 1998.683 | 2009.564 | |

| Avg lossa | 2507.038 | 2555.995 | 2420.206 | 2330.463 | 2204.217 |

-

•

aAvg loss is the average loss of the four stock markets in each model.

-

•

∗Boldface number represents the best model in each market.

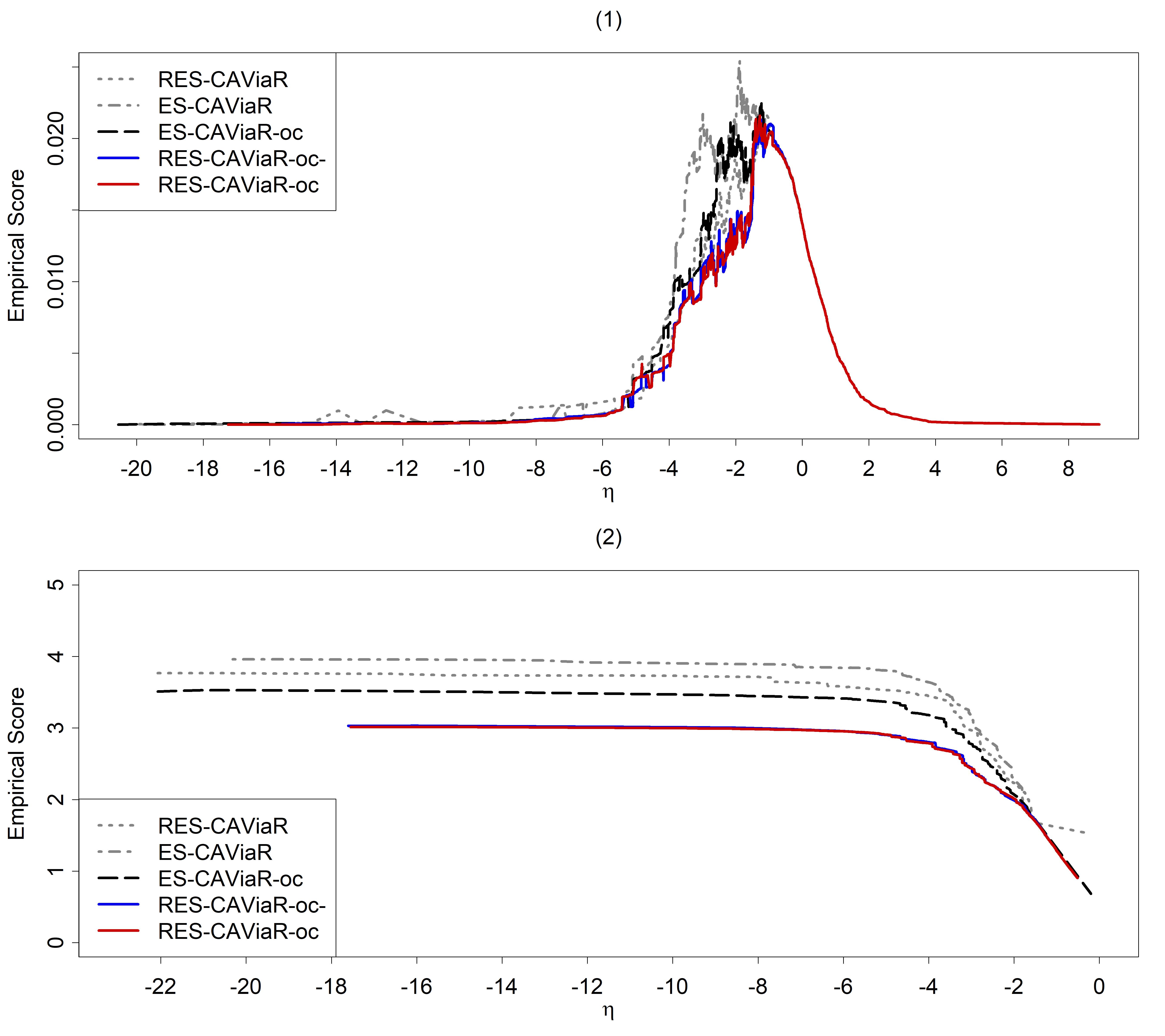

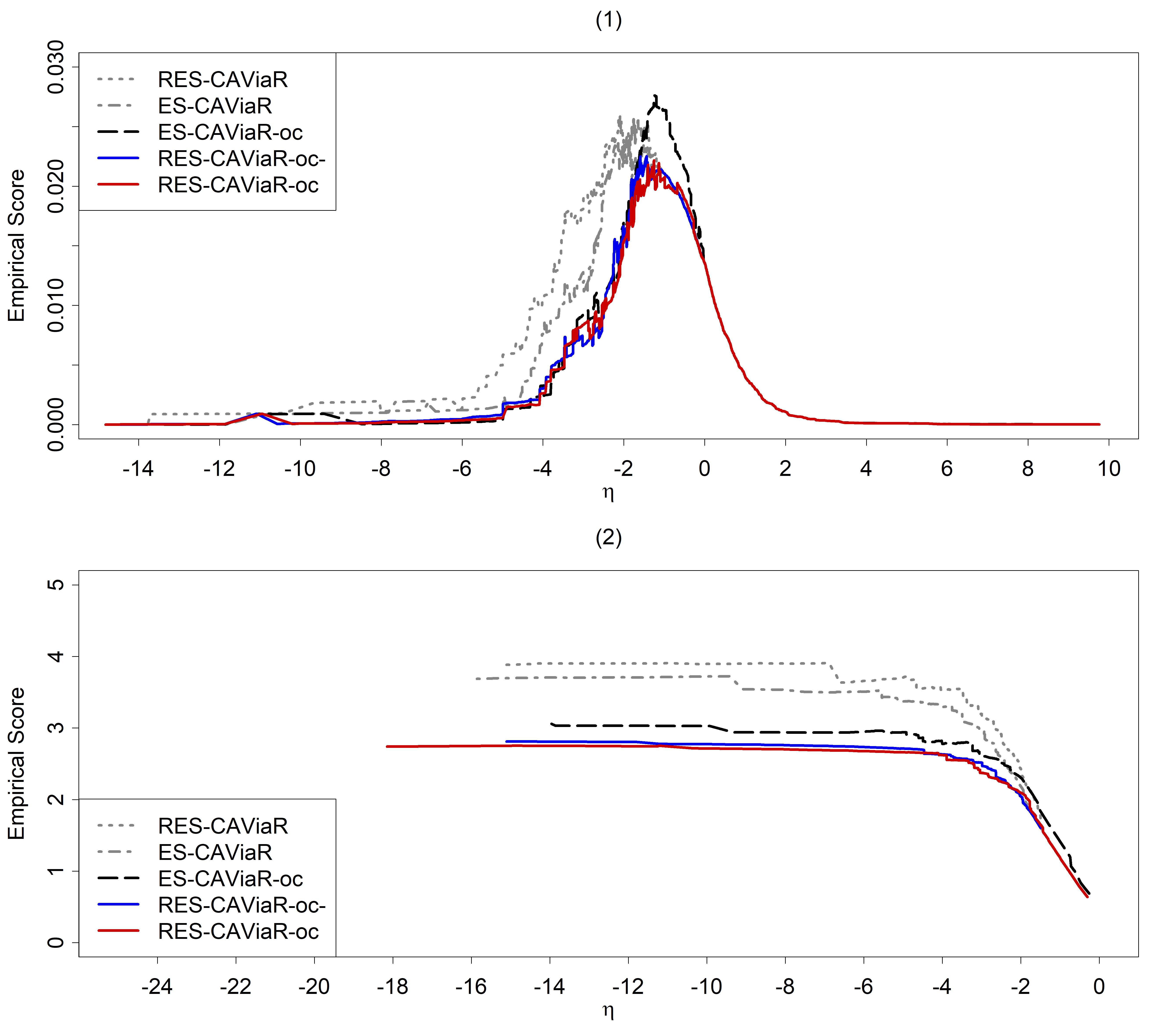

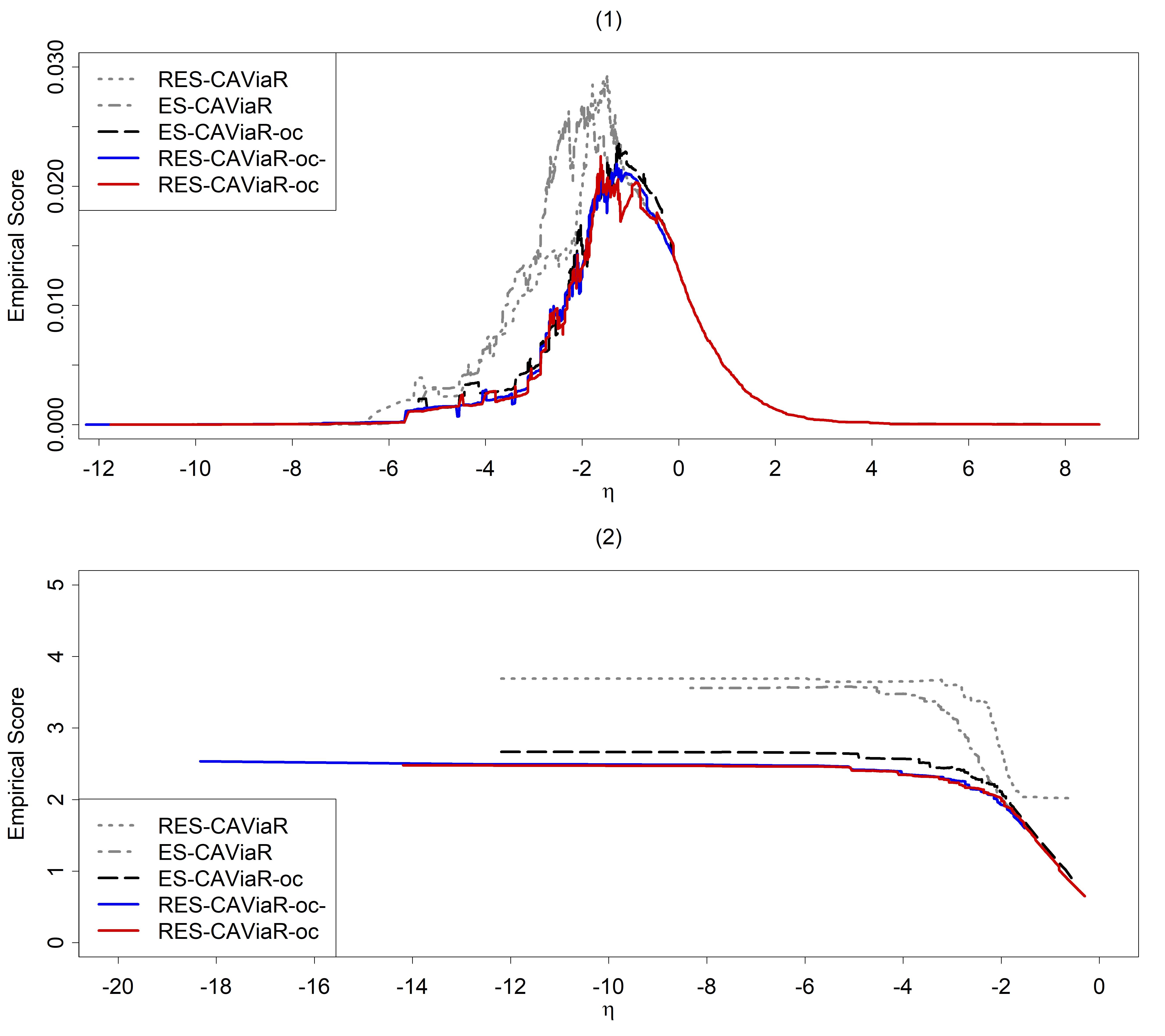

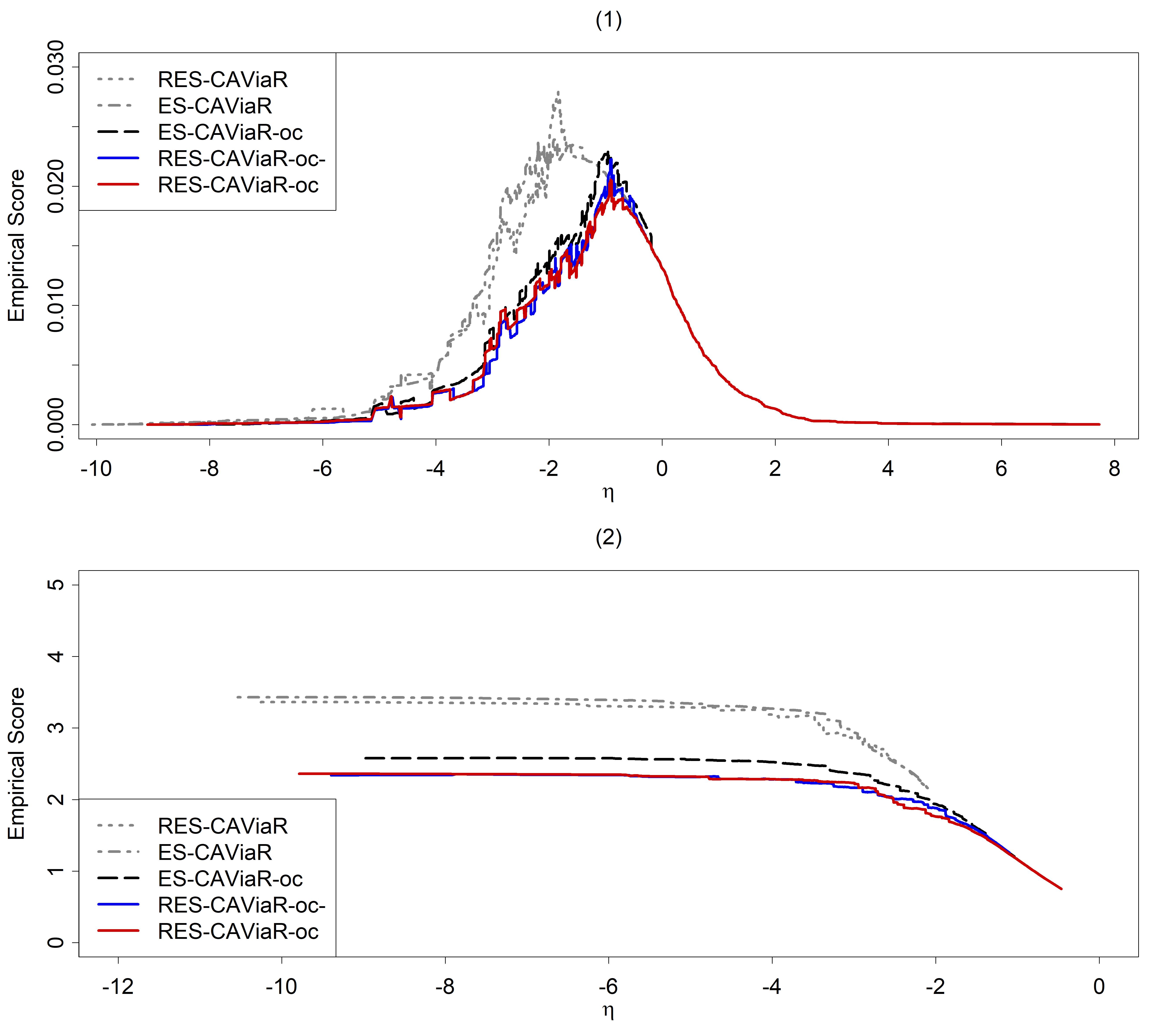

Figures 5–8 display the Murphy diagrams for the 1% VaR and ES. From these figures, it is evident that the proposed RES-CAViaR-oc type models outperform other models, regardless of the scoring functions applied. We choose to include the Murphy diagrams for the 2.5% VaR and ES in the Supplementary Materials, as they exhibit the same patterns as those mentioned above. We also formally test the forecast dominance of the proposed RES-CAViaR-oc model over other models through the test proposed by Ziegel et al. (2020). Specifically, for each competing forecast of VaR or ES in comparison with RES-CAViaR-oc, we establish a null hypothesis: RES-CAViaR-oc outperforms the other model across the set of elementary scoring functions. If this test is rejected, then the proposed RES-CAViaR-oc model provides less accurate forecasts than its competitor, when accuracy is gauged using an elementary scoring function. Notably, for each competing forecast in comparison to RES-CAViaR-oc and for each market, the p-value is so close to that we opt not to report the findings. As a result, the hypothesis remains unchallenged even at a significance level of .

These results formally corroborate the insights gained from the Murphy diagrams, suggesting that the proposed model outperforms others, irrespective of the scoring functions chosen. Given the extent of this dominance, as described in Ehm et al. (2016) and Nolde and Ziegel (2017), we believe these findings strongly support the choice of the AL log score and highlight the benefits of nowcasting based on overnight information.

Tables 8 and 9 present summaries of model comparisons, which are ranked by five criteria at the 1% and 2.5% levels, respectively. The top-performing model is assigned a rank of 1, and the ranking continues in ascending order. In case of a tie, the models share the same rank, and the next rank is skipped. The last row in each market’s table represents the sum of the previous four rank rows, which are ordered according to VRate, the ES method, quantile score, AL log score, and ESR backtest.

At the 1% level, Table 8 showcases the performance of five different models based on five criteria across four stock markets. Across the board, RES-CAViaR-oc- appears to be the most consistently high-performing model, particularly in the U.S. and Germany markets. The RES-CAViaR-oc model exhibits solid performance across multiple markets, particularly in the U.S., Germany, and Japan markets (Table 9). In reference to the last row in Tables 8 and 9, the RES-CAViaR-oc- and RES-CAViaR-oc models are the most appropriate, as indicated by the smallest rank sum at the 1% and 2.5% levels, respectively. In conclusion, the ES-CAViaR model, which incorporates realized volatility and overnight return, along with RES-CAViaR-oc- and RES-CAViaR-oc, demonstrates strong performance in the model comparison process.

We observe that nowcasting enhances forecasting accuracy. Our next inquiry is to determine if and how this improvement varies across different models and markets. To investigate this, we examine the sample mean, denoted by , of the score difference over the out-of-sample period , where presents the score of a forecast from the ES-CAViaR-oc (or RES-CAViaR-oc) model at time and is that of the ES-CAViaR (or RES-CAViaR) model, which does not incorporate overnight information. We choose the quantile score for VaR and AL log score for ES. To compare this average difference across countries, we compute the -statistics where is an autocorrelation-consistent estimator of the standard deviation as computed in Ziegel et al. (2020). The results appear in Tables 10 and 11. The larger the reported standardized score difference is, the more nowcasting enhances forecasting accuracy. We note that both models, especially RES-CAViaR, benefit from incorporating overnight information. Furthermore, the two Asian markets, Japan and Hong Kong, show more significant nowcasting improvement than do the U.S. and Germany. This implication suggests that Asian markets might be more influenced by other markets that are trading live while they are closed.

| Market | Rule | RES-CAViaR | ES-CAViaR | ES-CAViaR-oc | RES-CAViaR-oc- | RES-CAViaR-oc |

| U.S. | VRate | 3 | 5 | 4 | 1 | 1 |

| ES method | 3 | 5 | 4 | 1 | 2 | |

| Quantile score | 4 | 5 | 3 | 1 | 2 | |

| AL log score | 3 | 5 | 4 | 1 | 2 | |

| ESR backtest | 1 | 1 | 1 | 1 | 1 | |

| Suma | 14 | 21 | 16 | 5 | 8 | |

| Germany | VRate | 5 | 4 | 3 | 1 | 2 |

| ES method | 5 | 4 | 3 | 1 | 2 | |

| Quantile score | 5 | 4 | 3 | 1 | 2 | |

| AL log score | 5 | 4 | 3 | 1 | 2 | |

| ESR backtest | 4 | 4 | 1 | 1 | 1 | |

| Sum | 24 | 20 | 13 | 5 | 9 | |

| Hong Kong | VRate | 4 | 1 | 5 | 3 | 1 |

| ES method | 5 | 4 | 3 | 1 | 2 | |

| Quantile score | 5 | 4 | 3 | 2 | 1 | |

| AL log score | 5 | 4 | 3 | 2 | 1 | |

| ESR backtest | 1 | 1 | 1 | 1 | 1 | |

| Sum | 20 | 14 | 15 | 9 | 6 | |

| Japan | VRate | 5 | 1 | 3 | 1 | 4 |

| ES method | 2 | 1 | 5 | 4 | 3 | |

| Quantile score | 4 | 5 | 2 | 3 | 1 | |

| AL log score | 4 | 5 | 2 | 3 | 1 | |

| ESR backtest | 1 | 1 | 1 | 1 | 1 | |

| Sum | 16 | 13 | 13 | 12 | 10 | |

| Totalb | 74 | 68 | 57 | 31 | 33 |

-

•

aSum is the summation of five criteria.

-

•

bTotal is the total ranking of the four stock markets in each model.

-

•

∗Boldface number represents the best model in each market.

| Market | Rule | RES-CAViaR | ES-CAViaR | ES-CAViaR-oc | RES-CAViaR-oc- | RES-CAViaR-oc |

| U.S. | VRate | 1 | 4 | 5 | 3 | 2 |

| ES method | 4 | 5 | 3 | 1 | 2 | |

| Quantile score | 4 | 5 | 3 | 2 | 1 | |

| AL log score | 4 | 5 | 3 | 1 | 2 | |

| ESR backtest | 1 | 1 | 1 | 1 | 1 | |

| Suma | 14 | 20 | 15 | 8 | 8 | |

| Germany | VRate | 5 | 4 | 3 | 1 | 2 |

| ES method | 5 | 3 | 4 | 1 | 2 | |

| Quantile score | 5 | 4 | 2 | 3 | 1 | |

| AL log score | 3 | 2 | 5 | 4 | 1 | |

| ESR backtest | 1 | 1 | 1 | 1 | 1 | |

| Sum | 19 | 14 | 15 | 10 | 7 | |

| Hong Kong | VRate | 3 | 4 | 5 | 1 | 2 |

| ES method | 4 | 2 | 1 | 5 | 3 | |

| Quantile score | 4 | 5 | 1 | 2 | 3 | |

| AL log score | 4 | 5 | 3 | 1 | 2 | |

| ESR backtest | 5 | 1 | 1 | 1 | 1 | |

| Sum | 20 | 17 | 11 | 10 | 11 | |

| Japan | VRate | 5 | 4 | 2 | 3 | 1 |

| ES method | 2 | 1 | 4 | 5 | 3 | |

| Quantile score | 4 | 5 | 3 | 1 | 2 | |

| AL log score | 4 | 5 | 3 | 1 | 2 | |

| ESR backtest | 1 | 1 | 3 | 4 | 4 | |

| Sum | 16 | 16 | 15 | 14 | 12 | |

| Totalb | 69 | 67 | 56 | 42 | 38 |

-

•

aSum is the summation of five criteria.

-

•

bTotal is the total ranking of four stock markets in each model.

-

•

∗Boldface number represents the best model in each market.

| VaR | ES | |||

|---|---|---|---|---|

| Market | ES-CaViaR | RES-CaViaR | ES-CaViaR | RES-CaViaR |

| U.S. | 1.34 | 3.87 | 0.75 | 3.19 |

| Germany | 2.85 | 2.55 | 2.50 | 2.30 |

| Hong Kong | 2.83 | 5.14 | 2.30 | 4.59 |

| Japan | 3.78 | 4.13 | 2.85 | 4.06 |

| VaR | ES | |||

|---|---|---|---|---|

| Market | ES-CaViaR | RES-CaViaR | ES-CaViaR | RES-CaViaR |

| U.S. | 2.04 | 4.49 | 1.67 | 3.91 |

| Germany | 2.06 | 3.16 | -0.82 | 2.71 |

| Hong Kong | 3.93 | 5.03 | 0.89 | 3.20 |

| Japan | 6.37 | 5.66 | 5.80 | 5.60 |

5 Conclusion

This study offers a combination of the semi-parametric model with realized volatility and the concept of nowcasting through overnight information for forecasting VaR and ES simultaneously. We extend a semi-parametric regression model based on asymmetric Laplace distribution and offer a family of RES-CAViaR-oc models by adding overnight return and realized measures as a nowcasting method. We further employ the adaptive MCMC method in Bayesian inference for parameter estimation and tail forecasting due to the advantage of estimating complex models. We also see optimal convergence for every parameter. In addition, we conduct comprehensive backtests to ensure forecasting capability of the proposed models in the out-of-sample period.

The empirical study finds that both the RES-CAViaR-oc and RES-CAViaR-oc- models are more favorable than the original ES-CAViaR, ES-CAViaR-oc and RES-CAViaR models in terms of the quantile and AL log scores. This suggests that realized volatility and overnight information are two important factors that are useful for predicting tail risk. Murphy diagrams also confirm that CAViaR-type models with realized volatility and overnight returns are more efficient in forecasting tail risk than other models. The results help financial institutions raise capital allocation efficiency, allowing them more profit maximization opportunities.

Acknowledgement

We extend our gratitude to the editor, the associate editor, and the anonymous referees for their invaluable time and insightful comments on our paper. Cathy W.S. Chen’s research is funded by the National Science and Technology Council, Taiwan (NSTC109-2118-M-035-005-MY3 and NSTC112-2118-M-035-001-MY3). Takaaki Koike is supported by Japan Society for the Promotion of Science (JSPS KAKENHI Grant Number JP21K13275).

References

- Ahoniemi & Lanne (2013) Ahoniemi, K. & Lanne, M. (2013). Overnight stock returns and realized volatility. International Journal of Forecasting, 29, 592–604.

- Andersen and Bollerslev (1998) Andersen, T.G. & Bollerslev, T. (1998). Answering the skeptics: Yes, standard volatility models do provide accurate forecasts. International Economic Review, 39, 885–905.

- Andersen et al. (2003) Andersen, T.G., Bollerslev, T., Diebold, F.X., & Labys, P. (2003). Modeling and forecasting realized volatility. Econometrica, 71, 579–625.

- Artzner et al. (1999) Artzner, P., Delbaen, F., Eber, J.M., & Heath, D. (1999). Coherent measures of risk. Mathematical Finance, 9, 203–228.

- Barndorff-Nielsen et al. (2008) Barndorff-Nielsen, O.E., Hansen, P.R., Lunde, A., & Shephard, N. (2008). Designing realised kernels to measure the ex-post variation of equity prices in the presence of noise. Econometrica, 76, 1481–1536.

- Basel Committee on Banking Supervision (2016) Basel Committee on Banking Supervision Minimum capital requirements for market risk BIS, Basel, Switzerland (2016) http://www.bis.org/bcbs/publ/d352.pdf

- Bayer and Dimitriadis (2019) Bayer, S., & Dimitriadis, T. (2019). esback: Expected Shortfall Backtesting. R package version 0.3.0. Available at https://CRAN.R-project.org/package=esback.

- Bayer and Dimitriadis (2022) Bayer, S., & Dimitriadis, T. (2022). Regression-based expected shortfall backtesting. Journal of Financial Econometrics, 20, 437–471.

- Chen et al. (2023) Chen, C.W.S., Hsu, H.Y., & Watanabe T. (2023). Tail risk forecasting of realized volatility CAViaR models. Finance Research Letters, 51, 103326.

- Chen et al. (2022) Chen, C.W.S., Lin, E.M.H., & Huang, T.F.J. (2022). Bayesian quantile forecasting via the realized hysteretic GARCH model. Journal of Forecasting, 41, 1317–1337.

- Chen and So (2006) Chen, C.W.S. & So, M.K. (2006). On a threshold heteroscedastic model. International Journal of Forecasting, 22, 73–89.

- Chen and Watanabe (2019) Chen, C.W.S. & Watanabe, T. (2019). Bayesian modeling and forecasting of Value-at-Risk via threshold realized volatility. Applied Stochastic Models in Business and Industry, 35, 747–765.

- Chen et al. (2021) Chen, C.W.S., Watanabe, T., & Lin, E.M.H. (2023). Bayesian estimation of realized GARCH-type models with application to financial tail risk management. Econometrics and Statistics, 28, 30–46.

- Christoffersen (1998) Christoffersen, P.F. (1998). Evaluating interval forecasts. International Economic Review, 39, 841–862.

- Christensen and Podolskij (2007) Christensen, K. & Podolskij, M. (2007). Realized range-based estimation of integrated variance. Journal of Econometrics, 141, 323–349.

- Ehm et al. (2016) Ehm, W., Gneiting, T., Jordan, A., & Krüger, F. (2016). Of quantiles and expectiles: Consistent scoring functions, choquet representations and forecast rankings. Journal of the Royal Statistical Society Series B: Statistical Methodology, 78, 505–562.

- Embrechts, Kaufmann, and Patie (2005) Embrechts, P., Kaufmann, R., & Patie, P. (2005). Strategic long-term financial risks : Single risk factors. Computational Optimization and Applications, 32, 61–90.

- Engle and Manganelli (2004) Engle, R.F. & Manganelli, S. (2004). CAViaR: conditional autoregressive value at risk by regression quantiles. Journal of Business and Economic Statistics, 22, 367–381.

- Fissler and Ziegel (2016) Fissler, T. & Ziegel, J.F. (2016). Higher order elicitability and Osband’s principle. The Annals of Statistics, 44, 1680–1707.

- Gerlach et al. (2011) Gerlach, R., Chen, C.W.S., & Chan, N.Y. (2011). Bayesian time-varying quantile forecasting for value-at-risk in financial markets. Journal of Business and Economic Statistics, 29, 481–492.

- Gerlach and Wang (2020) Gerlach, R., Wang, C. (2020). Semi-parametric dynamic asymmetric Laplace models for tail risk forecasting, incorporating realized measures. International Journal of Forecasting, 36, 489–506.

- Gelman et al. (1996) Gelman, A., Roberts, G.O., & Gilks, W.R. (1996). Efficient metropolis jumping rules. Bayesian Statistics, 5, 599–608.

- Giacomini and Komunjer (2005) Giacomini, R. and Komunjer, I. (2005). Evaluation and combination of conditional quantile forecasts. Journal of Business and Economic Statistics, 23, 416–431.

- Hastings (1970) Hastings, W.K. (1970). Monte Carlo sampling methods using Markov chains and their applications. Biometrika, 57, 97–109.

- Heber et al. (2009) Heber, G., Lunde, A., Shephard, N., & Sheppard, K. (2009). Oxford-Man Institute’s realized library, Oxford-Man Institute, University of Oxford. Library Version: 0.3.

- Kupiec (1995) Kupiec, P.H. (1995). Techniques for verifying the accuracy of risk measurement models. Journal of Derivatives, 3, 73–84.

- Lazar and Xue (2020) Lazar, E. & Xue, X. (2020). Forecasting risk measures using intraday data in a generalized autoregressive score framework. International Journal of Forecasting, 36, 1057–1072.

- Martens and van Dijk (2007) Martens, M. & van Dijk, D. (2007). Measuring volatility with the realized range. Journal of Econometrics, 138, 181–207.

- Metropolis et al. (1953) Metropolis, N., Rosenbluth, A.W., Rosenbluth, M.N., Teller, A.H., & Teller, E. (1953). Equation of state calculations by fast computing machines. The Journal of Chemical Physics, 21, 1087–1092.

- Nolde and Ziegel (2017) Nolde, N. and Ziegel, J.F. (2017). Elicitability and backtesting: Perspectives for banking regulation. The annals of Applied Statistics, 11, 1833–1874.

- Patton (2020) Patton, A. J. (2020). Comparing possibly misspecified forecasts. Journal of Business & Economic Statistics, 38, 796–809.

- Politis and Romano (1994) Politis, D. N. and Romano, J. P. (1994). The stationary bootstrap. Journal of the American Statistical association, 89(428), 1303–1313.

- Taylor (2019) Taylor, J.W. (2019). Forecasting value at risk and expected shortfall using a semiparametric approach based on the asymmetric Laplace distribution. Journal of Business and Economic Statistics, 37, 121–133.

- Wang et al. (2023) Wang, C., Gerlach, R., Chen Q. (2023). A semi-parametric conditional autoregressive joint value-at-risk and expected shortfall modeling framework incorporating realized measures. Quantitative Finance, 23, 309–333.

- Ziegel et al. (2020) Ziegel, J.F., Krüger, F., Jordan, A., & Fasciati, F. (2020). Robust Forecast Evaluation of Expected Shortfall. Journal of Financial Econometrics, 18, 95–120.

Supplement to

“Tail risk forecasting with semi-parametric regression models by incorporating overnight information”

To monitor the convergence and stability of MCMC iterates for the stock markets of the U.S., Germany, Hong Kong, and Japan, Figures S9 to S12 present ACF plots and trace plots for each parameter based on the RES-CAViaR-oc- model, while Figures S13 to S16 focus on the RES-CAViaR-oc model. We carry out MCMC iterations, discard the first as the burn-in period, and include only every fourth iteration in the sample period for inference.

Figures S17 through S20 display Murphy diagrams for (1) VaR and (2) ES at the 2.5% level for the stock markets of the U.S., Germany, Hong Kong, and Japan.