∎

22email: youngsun@pknu.ac.kr 33institutetext: Tae-Kyung Kim 44institutetext: Department of Management Information Systems, Chungbuk National University, 1, Chungdae-ro, Seowon-gu, Cheongju-si, Chungcheongbuk-do, South Korea

Empirical Analysis of Quantum Approximate Optimization Algorithm for Knapsack-based Financial Portfolio Optimization

Abstract

Portfolio optimization is a primary component of the decision-making process in finance, aiming to tactfully allocate assets to achieve optimal returns while considering various constraints. Herein, we proposed a method that uses the knapsack-based portfolio optimization problem and incorporates the quantum computing capabilities of the quantum walk mixer with the quantum approximate optimization algorithm (QAOA) to address the challenges presented by the NP-hard problem. Additionally, we present the sequential procedure of our suggested approach and demonstrate empirical proof to illustrate the effectiveness of the proposed method in finding the optimal asset allocations across various constraints and asset choices. Moreover, we discuss the effectiveness of the QAOA components in relation to our proposed method. Consequently, our study successfully achieves the approximate ratio of the portfolio optimization technique using a circuit layer of , compared to the classical best-known solution of the knapsack problem. Our proposed methods potentially contribute to the growing field of quantum finance by offering insights into the potential benefits of employing quantum algorithms for complex optimization tasks in financial portfolio management.

Keywords:

best-known solution, empirical analysis, knapsack-based financial portfolio optimization, quantum approximate optimization algorithm1 Introduction

The financial industry plays a remarkable role in the economic health and growth of a country. In the constantly evolving world of financial markets, technological advancements are shaping traditional portfolio optimization methods, presenting new opportunities and challenges; this process involves enlarging assets to reduce risk by offsetting individual risk profiles crucial to the investment process (Speidell et al. 1989). Although there are many portfolio optimization models, they possibly have limitations. For example, the mean–variance model, which provides solutions as percentages of the total budget, can result in fractional allocations of nonfeasible assets (Vaezi et al. 2019). In the constant pursuit of optimization, some studies have explored extensions to portfolio optimization (Loke et al. 2023). Among these, a technique that reformulates portfolio optimization as a knapsack problem has been proposed (Martello and Toth. 1987; Mansini et al. 2015).

In (Vaezi et al. 2019), the knapsack problem was adapted for portfolio optimization by treating all assets included in the portfolio as items. The value or profit of each asset is represented by its expected return, usually estimated using historical data or forecasting techniques. The weight or volume of each item corresponds to a risky asset, typically measured by its standard deviation or the variance–covariance matrix of the assets. The knapsack capacity corresponds to the budget or available capital that can be invested in the portfolio. By reformulating the problem as a knapsack, the primary objective is to maximize the total value or profit of the portfolio while satisfying the capacity constraint and potentially other constraints, such as a target return or a minimum number of assets. However, similar to (Chu and Beasley. 1998), the knapsack problem is considered NP-hard even with polynomial-bounded weights and values. Therefore, exploring new paradigms for optimization owing to computational complexity of solving this problem is crucial (Honggang et al. 2009).

Similarly, the paradigm of quantum computing, leveraging the properties of quantum mechanics, has been developed to solve complex problems intractable for classical computers (Herman et al. 2023). The financial domain is a primary aspect of quantum computing, with applications spanning price derivation, risk modeling, portfolio optimization, and fraud detection (Saxena et al. 2023). As technology redefines problem-solving in finance, the quantum approximate optimization algorithm (QAOA), rooted in quantum computing, offers the promise of efficiently finding approximate solutions for computationally demanding problems within the polynomial-bounded NP optimization complexity class. In (Dam et al. 2021; Kea et al. 2023), the application of QAOA to the knapsack problem is explored for optimization purposes.

Herein, we present an approach that harnesses the efficacy of QAOA in addressing the complex problem of portfolio optimization by reformulating it as a knapsack problem. Although additional research is required, our findings offer valuable insights into the following areas.

-

•

Our proposed model for portfolio selection formulates the problem as a knapsack concern by incorporating the expected return from the Markowitz model and setting the capacity according to the knapsack framework.

-

•

Our study presents a QAOA algorithm using a quantum walk mixer for the knapsack problem while incorporating a shallow circuit layer to decrease computational complexity and improve solution quality.

-

•

Our extensive empirical analysis reveals a consistent enhancement in identifying optimal solutions for the knapsack problem, providing an impressive approximation ratio ranging from 100% to 98%, with 2–5 stock selection cases. We also underscore the potential of quantum algorithms as robust, forward-looking solutions for complex financial optimization.

The paper is organized as follows: Section 2 provides an overview of the relevant background work. Section 3 explores the research concerning the proposed method. Section 4 details our proposed method, including the functionality of each step. Section 5 demonstrates the meticulous design and execution of the experiment to obtain the desired results. Finally, Section 6 dissects the findings of the proposed method, underscoring its achievements and limitations while presenting a comprehensive conclusion, key takeaways, and potential future directions.

2 Background

2.1 Portfolio Optimization

Portfolio optimization is a mathematical framework that maximizes returns while minimizing risks through strategically selecting assets within an investment portfolio (Anagnostopoulos and Mamanis. 2010). This is typically achieved by strategically allocating the proportion of each asset in the portfolio to optimize the risk–return tradeoff by considering the specified risk tolerance. The process involves four steps: i) identifying suitable assets, ii) projecting anticipated yields based on historical data for future forecasts, iii) quantifying the risk by assessing the uncertainty of each asset, and iv) selecting the optimal portfolio that maximizes the expected yield for a given risk level (Gunjan and Bhattacharyya. 2023). One of the various models used in this study was Markowitz model, developed by Harry Markowitz in 1952 (Markowitz. 1976). This analysis is in conjunction with the variance of the rate of return, providing a significant assessment of portfolio risk under a rational framework of assumptions. The Markowitz model represented the maximum expected yield by allocating funds into stocks as follows (Anton Abdulbasah Kamil and Kok. 2006):

| (1) |

where indicates the anticipated return at time per stock invested in, and is the rate at which return in the security where time is discounted back to the presents. The standard deviation—the variance of return—is a statistical measure used as an indicator of the uncertainty or risk linked to return. These statistical indicators effectively measure the extent to which returns deviate unpredictably from the average value over a specific period. The variance represents the degree of variation exhibited by the return concerning the expected return , as illustrated by the following equation:

| (2) |

The covariance of returns measures the relative riskiness of a security within a portfolio of securities. For two securities, denoted as and , the covariance of their returns is defined as

| (3) |

Furthermore, covariance can be measured depending on the variability of the two individual return series:

| (4) |

where is the correlation coefficient of returns, and and are the standard deviation of and . As previously stated, an efficient portfolio is characterized by selecting individual assets within the portfolio and weighting each asset. Therefore, the portfolio return is calculated as a weighted average of the returns of the individual investments within the portfolio. Next, denoted as the weight and applied to each return of the portfolio takes form as follows:

| (5) |

where is independent of . The simplified version of the variance of a portfolio can be written as

| (6) |

where is the variance of the portfolio, is the percentage of the investor’s assets that are allocated to the asset, and the represents the variance of the asset and the covariance between the returns for assets and denoted as . Reportedly, traditional asset allocation methods, such as the Markowitz theorem, provide solutions in percentages, potentially suggesting the allocation of half of a market share, making it impractical (Vaezi et al. 2019). Therefore, proposing a method for determining the number of shares for each asset is crucial; this involves the conversion of expected returns, prices, and budget into interval values and determines the priority and importance of each share by framing it within a knapsack-based model.

2.2 Knapsack Problem

Herein, a given set of items with known sizes is selected and packed into a knapsack with a fixed capacity (Kleywegt and Papastavrou. 1998). This problem is one of the simpler NP-hard problems in combinatorial optimization because it focuses on maximizing an objective function while adhering to a single resource constraint. To find the exact solutions, some techniques have been employed, such as relaxations, bounds, reductions, and other algorithmic approaches (Du and Pardalos. 1998). These techniques include genetic algorithms (Pradhan et al. 2014), dynamic programming (Schäfer et al. 2021), simulated annealing (Delahaye et al. 2019), Tabu search (Lai et al. 2019), and greedy algorithm (Abidin. 2017). These classical approaches are instrumental in providing optimal solutions. Although these conventional approaches are successful and valuable, they are limitations in computation in the classical domain. Furthermore, the new paradigm of quantum computing introduces optimization techniques, including QAOA, to tackle problems such as the knapsack problem, yielding better solutions than classical computation techniques (de la Grand’rive and Hullo. 2019).

2.3 Quantum Approximate Optimization Algorithm (QAOA)

In combinatorial optimization, QAOA excels as solutions tailored for quantum computing while leveraging the strengths of the classical computing (Farhi et al. 2014; Chen et al. 2023). QAOA, a hybrid quantum-classical algorithm, has demonstrated remarkable effectiveness in addressing recent NP-hard problems, including Max-Cut (Crooks. 2018), traveling salesman problem (Zawalska and Rycerz. 2023), and quadratic unconstrained binary optimization (QUBO) (Borle et al. 2021). Given a combonitorial optimization problem involving an N-bit binary string represented as , with a classical objective function to be maximized (Ausiello et al. 1999). The goal is to find a solution that satisfies an approximation condition as follows:

| (7) |

where , and is a desired approximation ratio. Accordingly, the QAOA algorithm tackles this problem by encoding, which involves mapping the classical objective function into the phase Hamiltonian in order to find the optimal eigenvalues:

| (8) |

Furthermore, operates diagonally on the computational basis states of dimensional Hilbert space (-qubit space). Ideally, the performance of the -level QAOA improves with increasing . For the -level QAOA, the state is initialized, while the and a mixing Hamiltonian:

| (9) |

are applied alternately with controlled durations, generating a wave function:

| (10) |

This variational wave function is parameterized by variational parameters, and . The expected value of in this variational state is determined through repeated measurements on a computational basis:

| (11) |

Furthermore, a classical computer is used to search for the optimal parameters and maximize the averaged output :

| (12) |

Next, the approximate ratio showing the QAOA performance is

| (13) |

Moreover, searching for the approximate ratio is typically performed by starting a random initial estimate of parameter and performing gradient-based optimization (Zhou et al. 2020).

3 Related Work

Our study builds upon several key pieces of research that delve into the application of QAOA to the knapsack problem concerning portfolio optimization. QAOA has been employed as an optimization method for portfolio optimization. Herein, the portfolio optimization problem is transformed into a binary version. Accordingly, the weight vector is discretized, with the element taking values of either 0 or 1. In (Awasthi et al. 2023), a comprehensive study of quantum computing approaches for multiknapsack problems is proposed by investigating some of the most prominent and state-of-the-art quantum algorithms using different quantum software and hardware tools. Consequently, quantum computing offers the potential for good and fast solutions to multiknapsack optimization problems in various fields, such as logistics (allocating goods to containers), resource allocation in computing (distributing tasks among different servers), and financial portfolio optimization (allocating assets among different investment opportunities).

In (Brandhofer et al. 2022), the Markowitz models of portfolio optimization were converted into binary knapsacks. A hard constraint model was employed by incorporating hard constraints into the quantum algorithm, involving designing mixing operators based on the constraint conditions. Additionally, a combination of - and -mixers was used to encode the constraints in the quantum circuit. -mixers were used to mix the quantum state and generate a superposition of feasible solutions, whereas -mixers were used to enforce the hard constraints. Moreover, using a hard constraint model ensured that the quantum state evolved between feasible solutions satisfying the constraints while allowing for a high degree of flexibility in opting parameters.

Another intriguing study highlights the strengths of the quantum walk optimization algorithm (QWOA) (Marsh and Wang. 2019) compared to other quantum optimization algorithms while highlighting the challenges posed by the complex and large solution space associated with its lattice structure. Moreover, the quantum mix optimization algorithm (QMOA) was introduced as an extension of QWOA. QMOA enhanced the efficiency of quantum optimization algorithms for portfolio optimization by reducing the number of iterations required for computations (Shunza et al. 2023).

4 Knapsack-based Portfolio Optimization

4.1 Overall Architecture

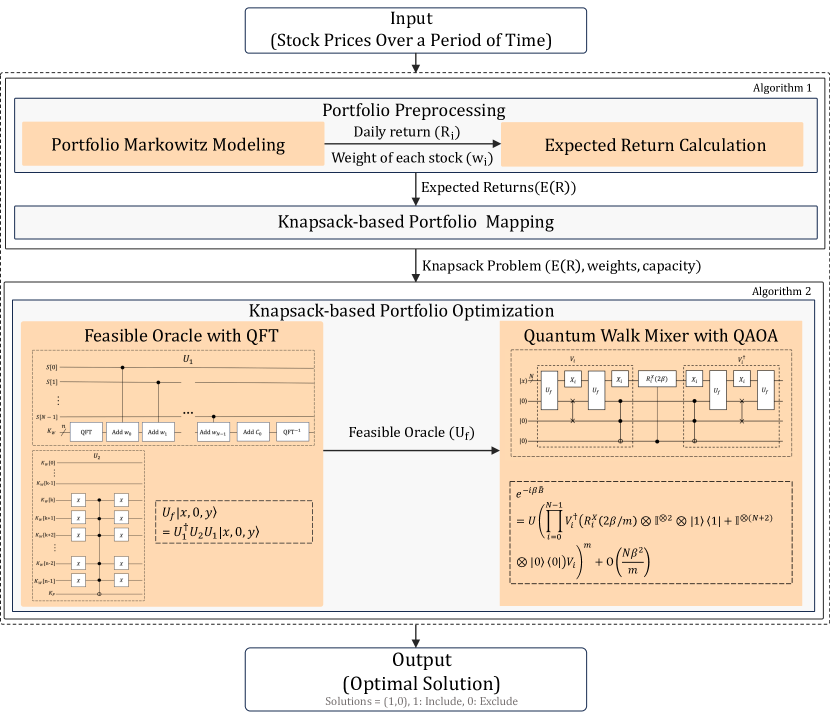

This section explains how our method processes everything from stock selection to finding the optimal solution. Figure 1 shows that our structured workflow employs a quantum computing approach to portfolio optimization. Initiating with historical stock price data over time, Algorithm 1 calculates the expected returns of the portfolio using the Markowitz portfolio optimization model. These expected returns are crucial in constructing the portfolio as a binary knapsack problem, incorporating computed mean returns, asset weights, and the portfolio’s capacity constraints. This problem is optimized using Algorithm 2, where the approach for optimizing the knapsack-based portfolio optimization problem is employed. At this stage, we prepared the feasible oracle with quantum Fourier transform (QFT) (Weinstein et al. 2001) for conditional checking of the feasibility of our proposed solution to the knapsack problem before constructing QWM, as discussed in (Marsh and Wang. 2019) with QAOA (QWM–QAOA). The result is a bit string revealing which stocks are chosen or omitted from the portfolio. For example, a solution of (1,0) in the portfolio optimization for Stocks A and B means that Stock A is included and Stock B is excluded, thus outlining the final investment strategy.

INPUT : start date of stock prices, : end date of stock prices, : list of stocks

OUTPUT : portfolio optimization as a knapsack problem

Algorithm 1 was initiated by extracting the historical returns of each stock within a specified time frame, ranging from the initiation to the termination dates. This retrieval of historical returns was achieved using the function. Subsequently, the algorithm applies the Markowitz model usin the function, to compute the expected returns denoted as based on the historical return prices. This variable provides valuable insights into the potential profitability of the selected stocks in the portfolio. In addition, it constructs a covariance matrix serving as an indicator of the correlation in movements between pairs of stocks. From lines , the calculated returns and covariance underwent a transformation to represent the values, weights, and constraints, which are essential components for formulating the knapsack problem. Herein, we set the values to the expected returns (), and the weights for each stock were uniformly set to 1, indicating an equal weight allocation. The algorithm also defined the constraints or capacity for the knapsack problem, with representing half the length of the expected return array ().

INPUT : knapsack problem , : layer of circuit, : Trotter step count for QAOA

OUTPUT : approximation ratio representing optimal choice selection

After formulating portfolio optimization into a knapsack problem, we optimized it in Algorithm 2. In this stage, we used QWM–QAOA to prepare the mixing Hamiltonian of QAOA. The steps in lines involve setting up quantum registers and other preparations necessary for QAOA using a function called . Line focuses on the preparation of the Mixing Hamiltonian using the QWM-QAOA approach; this is realized via the , which requires parameters, such as a predefined trotter step count , the number of quantum registers of choices, weights, and ancillaries. In line 14, we prepare the phase Hamiltonian , which is a vital component for constructing QAOA, using . The specifications of each method’s construction are presented in Subsection 4.3.

At each circuit layer , the algorithm computed the expectation value (line ), facilitating the determination of a new set of optimal parameter . These optimal parameters were identified using the SHGO method and implemented as in line . Finally, the algorithm measured probabilities (line ) through a measurement process. These probabilities were used to determine the optimal solution using the function to determine the best selection of items represented as in line .

4.2 Knapsack-based Portfolio Formulation

Our methodology is based on the fundamental principles of mean–variance optimization, focusing on the Markowitz model. This model historically maximizes the anticipated yield of a portfolio while considering a predetermined level of risk, quantified by the variance of portfolio returns. We denoted the expected return of stock by using the mean–variance calculation. Next, we transformed the expected return into a knapsack problem. Subsequently, we extended this model by reinterpreting the expected return as a component of a knapsack problem, thereby aligning portfolio optimization with knapsack problem dynamics; this adaptation involves redefining the expected return of each stock as a value optimized under the constraints of total portfolio risk. This mathematical transformation, which effectively converts portfolio optimization into a knapsack problem, is expressed as follows:

| (14) |

where the risk of including stock in the portfolio, denoted as , and the total risk tolerance, denoted by , serves as the knapsack capacity. The binary variable indicates whether to include stock in the portfolio, and represents its expected return values.

4.3 QAOA for the knapsack problem

4.3.1 Feasibility Oracle

The feasibility oracle is used as a hypothetical subroutine that instantly determines whether a proposed solution to the knapsack problem violates any constraints (Chawla et al. 2023). We can explore solutions within a well-defined space of bitstrings by representing our portfolio model as a binary knapsack problem. We defined as the set of all possible bitstrings of length representing potential portfolio choices.

Furthermore, at each possible choice of any of the items is represented by a bitstring . ). Thus, the subset feasible solution was denoted as for the knapsack problem, and the feasibility function was defined as

| (15) |

Considerably, the feasibility oracle to be unitary can be described as:

| (16) |

In portfolio optimization, a state symbolizes a specific stock allocation, which is deemed feasible (i.e., ) if the total weight does not exceed the capacity . This oracle toggles a flag qubit based on the feasibility of the state , representing a possible portfolio configuration.

Next, we allocated qubits for storage as follows: to record the formulated knapsack choices, to hold the weight of the item choice, and as the flag qubit indicating the feasibility of the state . Remarkably, the number of qubits required for , , and are deonted by , , and respectively. Upon that, the total number of qubits that are required is .

Furthermore, the total weight is calculated by adding the weight of each item to register , controlled by the corresponding bit in register . We also compare the computed weight to the capacity using an inequality check facilitated by a multiple-controlled NOT gate.

For suitable , the inequality can be verified using the following condition:

| (17) |

This condition ensures that the binary representation of has zeros in all positions beyond . The feasibility oracle employs two primary unitary operations- and . augments with a predetermined offset , facilitating the binary representation required for the feasibility check; is applied conditionally based on ’s outcome.

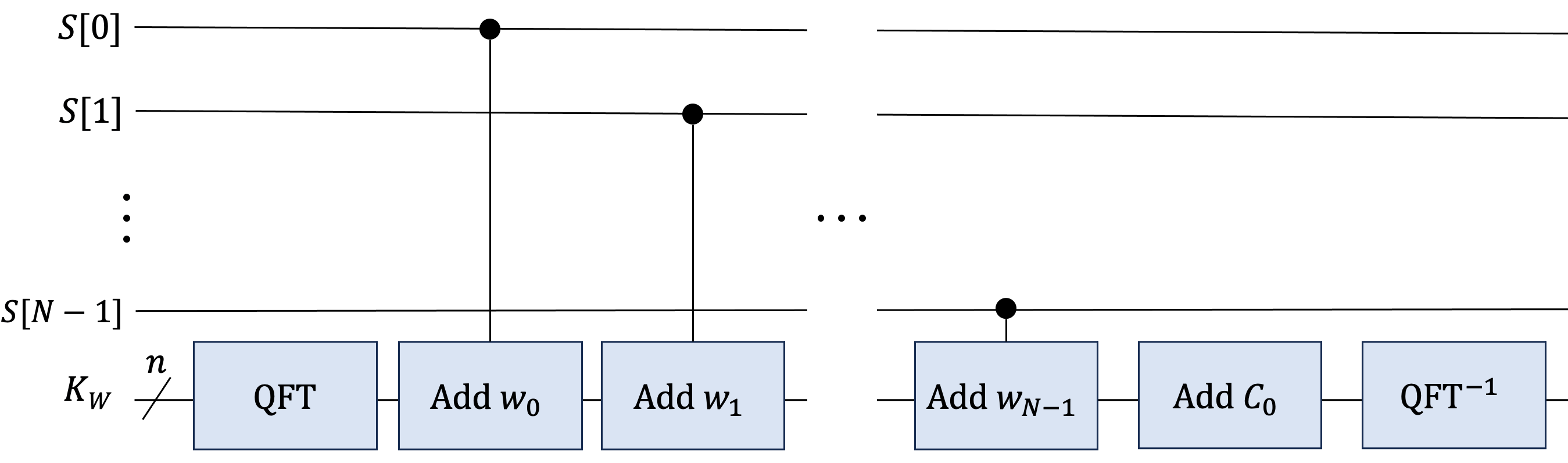

We begin by illustrating how is prepared. Quantum Fourier Transform (QFT) (Weinstein et al. 2001) is employed within the unitary operation to facilitate the process of the adding of weights in the knapsack problem.

This process starts with the initialization of the ancillary weight register to . Next, QFT is applied to to prepare the register for quantum addition, even though the QFT does not change the state for state . This step is necessary for nonzero initial states . Poststate transformation of from the computational basis to the Fourier basis, the weight representation was distributed across the amplitude of the quantum state:

| (18) |

where we use the notaion , and is the binary representation of . Furthermore, weights were added to using controlled operations applying phase rotations. These operations are conditioned on the on the bits of the bitstring indicating the selection of items. Each bit in determines whether the corresponding weight should be added to . The addition in the Fourier space was related to phase rotation and implemented by a sequence of controlled phase gates. The magnitude of the rotation was determined by wi and the position of the bit controlling the operation. The implementation of controlled additions can be described as follows: for each selected item (where the corresponding bit in is , a controlled phase rotation is applied to . Additionally, the phase added to each computational basis state within is proportional to :

| (19) |

This phase rotation effectively encodes the addition of into the quantum state. After completing this process, the step transformed the register back to the computational basis required, where

| (20) |

The inverse QFT decodes the phase information back into a computational state representing the total weight of the selected items. If QFT encodes the weight as a superposition of phases, the inverse QFT converts these phases back into a binary number—the sum of the weights. The final state of the register after applying was the binary representation of the total weight of the items:

| (21) |

Figure 2 shows how is implemented using an algorithm based on QFT.

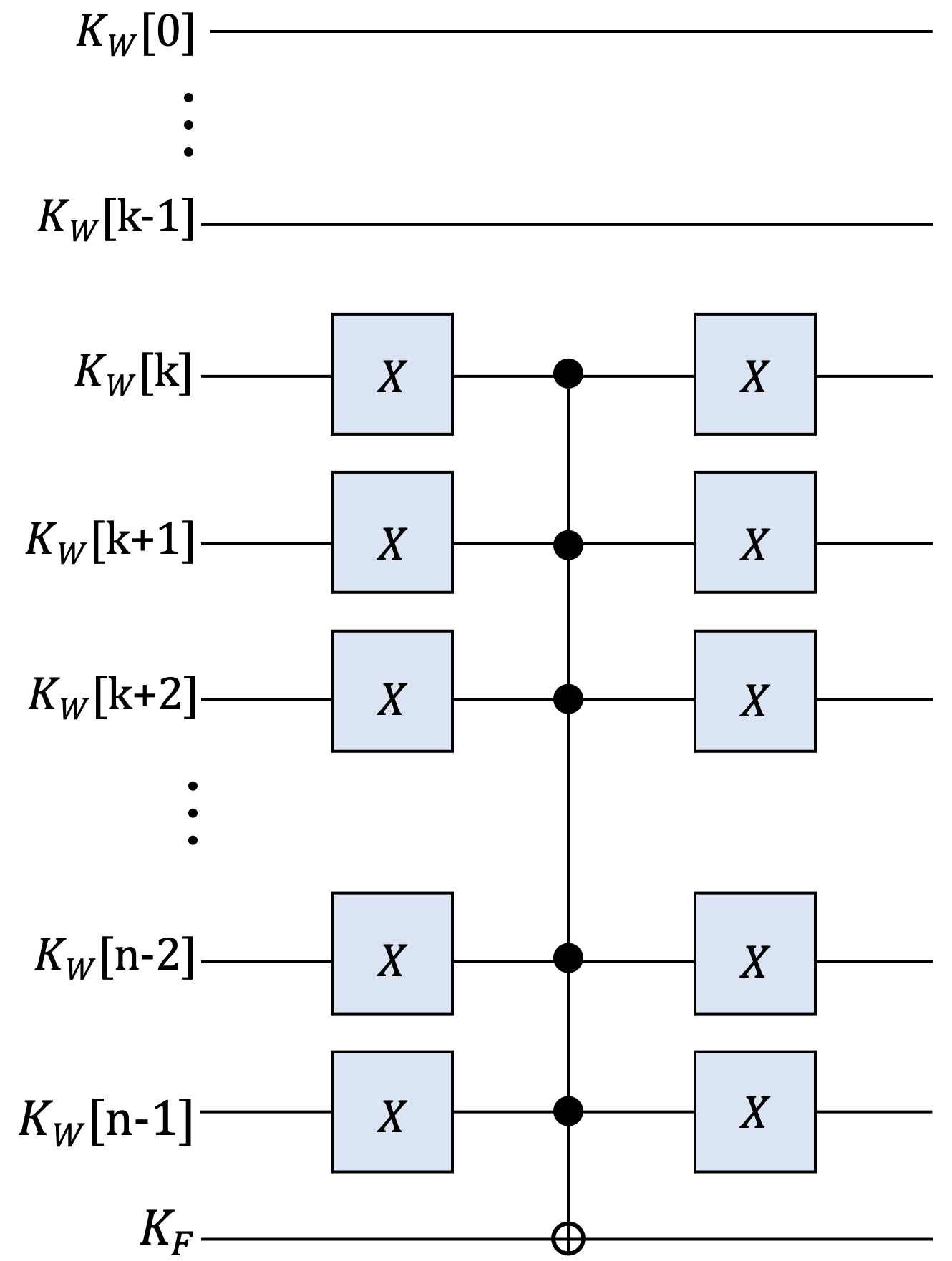

Following the implementation of the unitary operation , is described, which comprises a quantum circuit that conditionally modifies the state of an ancillary qubit in concerning the sum of weights represented in the register . Referring to Equation 17, the ancillary qubit underwent a state flip to signal a valid configuration when the total weight , augmented by a constant offset is less than the predefined threshold . This transformation was executed through several multicontrolled NOT gates, where each gate was influenced by a qubit distinct from the weight register. The successful transition of the ancillary qubit’s state post signified a feasible solution, adhering to the knapsack’s capacity, which effectively segregates the solution space into permissible and impermissible weights.

4.3.2 Quantum Walk Mixer for Enforcing Constraints

This process relies on the mixing operator generated by mixing Hamiltonian from Equation 9 as follows:

| (22) |

Alternatively, by leveraging the feasible function in Equation 15 and neighboring states for exploring the solution space, can be described as

| (23) |

where is the neighbor of ( with bit flliped). Using this alternative representation, it is easy to observe that .

| (24) |

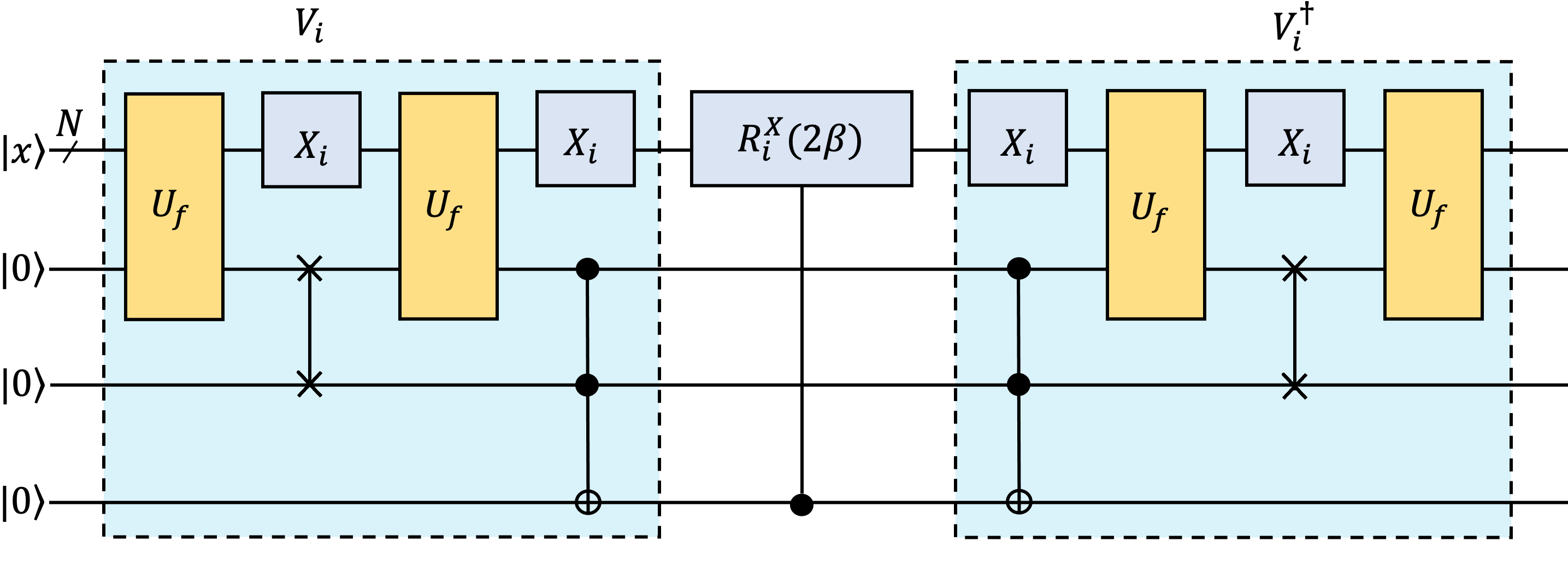

where Ham represents the Hamming distance between two binary strings and , which is the count of positions where the corresponding bits differ. The exact implementation of the desired mixing operator presents challenges due to its Hamiltonian, requiring additional resources and noncommuting elements. To address this, we employ an alternative operator , closely resembling . This operator is constructed from , and the inverse for encoding feasibility information of neighboring states into auxiliary qubits that enable the controlled state manipulation. Additionally, the operator includes single-qubit gates for creating neighboring state exploration. Moreover, —the feasible oracle—is included to determine the feasibility of states by ensuring that only valid states are mixed. Finally, aids in adjusting the amplitudes of states based on feasibility and further refining the mixing process, whereas auxiliary qubits are employed to store feasibility information.

As shown in Figure 4, the process starts from:

| (25) |

which implies that the behavior of when acting on a state is to transform it into a new state with additional information encoded in the auxiliary qubits, dependent on the feasibility function and its value at neighboring points. Therefore, the state of can be described as

| (26) |

Next, neighboring state mapping is performed using to determine whether the original and neighboring states have the same feasibility. Thus, Equation 25 can be written as

| (27) |

Then, the bit flip of the qubit acts as:

| (28) |

Therefore, we can describe the encoded feasibility information after applying and based on Equation 26 as follows:

| (29) |

Next,

| (30) |

Thus, for a given operator, which approximates the original operator, we have

| (31) |

Moreover, implements given three ancillary qubits, or more precisely, it is represents as:

| (32) |

It follows that

| (33) |

where is used to generate . Moreover, is not commute and should use three ancilla qubits. Therefore, the approximate implementation of needs to use the trotter product formula. Meanwhile, using the identity , the state representing the rest of the circuit in Figure 4 is given by

| (34) |

where . Furthermore, we optimized with the trotter product formula as

| (35) |

Moreover, to maintain the validity of the approximation within the new parameter range, the range needs to be adjusted accordingly to .

As an objective function, we use the value function . Therefore, the corresponding phase separation can be described as follows:

| (36) |

4.3.3 Number of Qubit Requirements

The presented illustration implies that using a feasibility oracle with nf ancilla qubits requires qubits. In contrast, there is an exigency for an additional three qubits, specifically for generating the unitary (Equation 33).

5 Evaluation

This section presents the numerical results by evaluating the effectiveness of the proposed algorithm across different asset numbers along with the impact of parameter configuration.

5.1 Experimental Setup

Initially, we implemented the proposed method using the Qiskit library (Aleksandrowicz et al. 2019), a widely used open-source quantum computing framework. We run the algorithms on the QASM simulator, a tool provided by Qiskit for simulating quantum circuits, which helped us gain insights into the behavior and performance of the algorithms before moving on to the real quantum device. While using the real device, we used IBM Cairo, a 27-qubit quantum device, for quantum computations, which offers the opportunity to test the algorithms in a real-world quantum computing environment. The experimental phase involves conducting several tests in which we select varying stocks from well-known companies, such as Apple Inc. (AAPL), Amazon.com Inc. (AMZN), Alphabet Inc. (GOOGL), Microsoft Corporation (MSFT), NVIDIA Corporation (NVDA), and Tesla, Inc. (TSLA). Notably, the selection of these stocks was based on different scenarios, including cases with two, three, four, and five stocks. Postselection, we proceeded with the experimental setup of the proposed method. During the optimization process, we focused on optimizing QAOA, which was achieved by optimizing the angle parameters, i.e., and , using the classical optimizer SHGO (Endres et al. 2018). Additionally, we integrated quantum walk to boost optimization by leveraging its benefits for refining the process and achieving superior results. To evaluate the performance of the proposed method, we defined the problem of our algorithm based on the number of assets to be optimized (Table 1). First, we selected 2–5 subsets of stocks using the capabilities of PyPortfoliopt (Martin. 2021). The values in Table 1 represent the expected return of stocks counting from January 1, 2018, to January 1, 2023. This step clarifies the problem and enables us to tailor our algorithm accordingly. We aimed to evaluate the effectiveness of the QAOA optimization technique concerning portfolio optimization. To achieve this, we specifically evaluated the performance of the algorithm using the best-known solution (BKS), a result of using a classical algorithm (Martello et al. 1999), where signifies selection and denotes exclusion. This technique compared the results obtained from our algorithm with those of the classical solution, providing a benchmark for assessing its performance and effectiveness. By undertaking this evaluation, we can gain valuable insights into the capabilities and limitations of the QAOA optimization technique in portfolio optimization.

| # Stocks | Type | Values | Capacity | BKS | Qubits | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2 |

|

|

1 | (1,0) | 7 | ||||||||||

| 3 |

|

|

1 | (1,0,0) | 8 | ||||||||||

| 4 |

|

|

2 | (1,1,0,0) | 10 | ||||||||||

| 5 |

|

|

2 | (0,1,0,0,1) | 11 |

5.2 Performance Evaluation

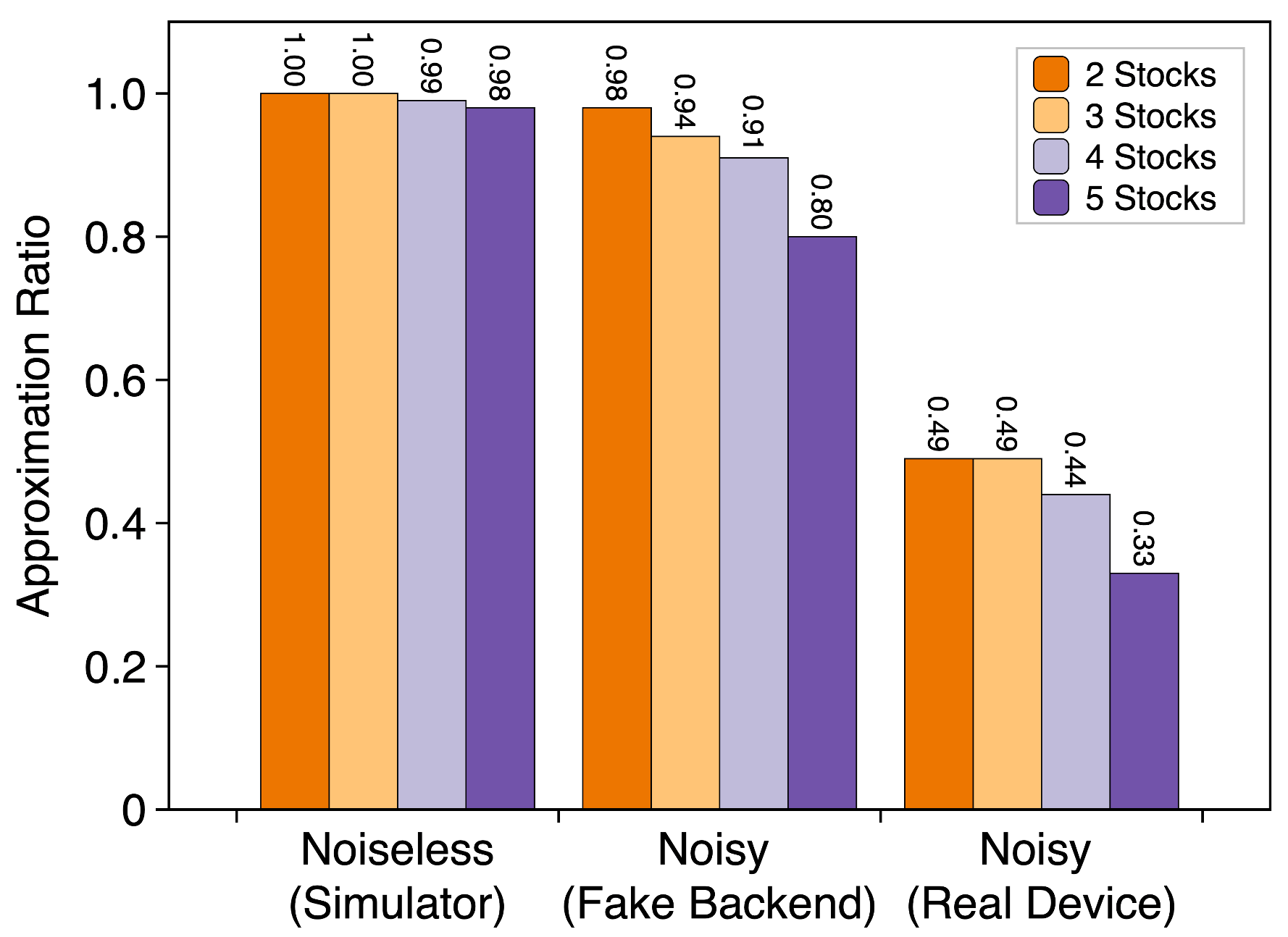

By meticulously exploring the variable settings within the QWM-QAOA, we identified a circuit layer of and a trotter step value of as the optimal configuration for achieving superior results. Contextually, we explore the probability distributions arising for each stock in the portfolio. Figure 5 shows the experimental results, which are the optimal results of each scenario of the number of stocks. The obtained results reveal the probability distribution results for all possible cases of stock selection. Additionally, we employed the BKS method to evaluate the obtained results and ensured its expected behavior (Table 1).

Within the circuit layer of , the approximation ratio varied based on the number of stocks in the portfolio. The obtained results ranged from 100% to 98% in a noiseless environment, from 98% to 80% when the fake backend was used, and from 49% to 33% when the real device was employed. When we extended our study to real-world conditions by implementing the experiment on the IBM Cairo device, the approximation ratio decreased to approximately 50% because of gate errors and decoherence affecting the fidelity of quantum states (Johnstun and Van Huele. 2021). Addressing these challenges will require additional efforts, such as error mitigation, which is beyond the scope of this study (Alam et al. 2019; Gaur et al. 2023).

5.2.1 Sensitivity Analysis

We conducted a comprehensive sensitivity analysis of key parameters using the QWM–QAOA algorithm. Our empirical exploration encompassed crucial elements, such as the circuit layer and the number of trotter steps . These parameters are crucial for shaping the effectiveness of the proposed algorithm, and variation comprehension of their sensitivity is crucial for optimizing the performance of the algorithm. Through a methodical examination and evaluation, we present details of the relationship between these parameters and how much they influence the overall efficiency and resilience of QAOA.

-

•

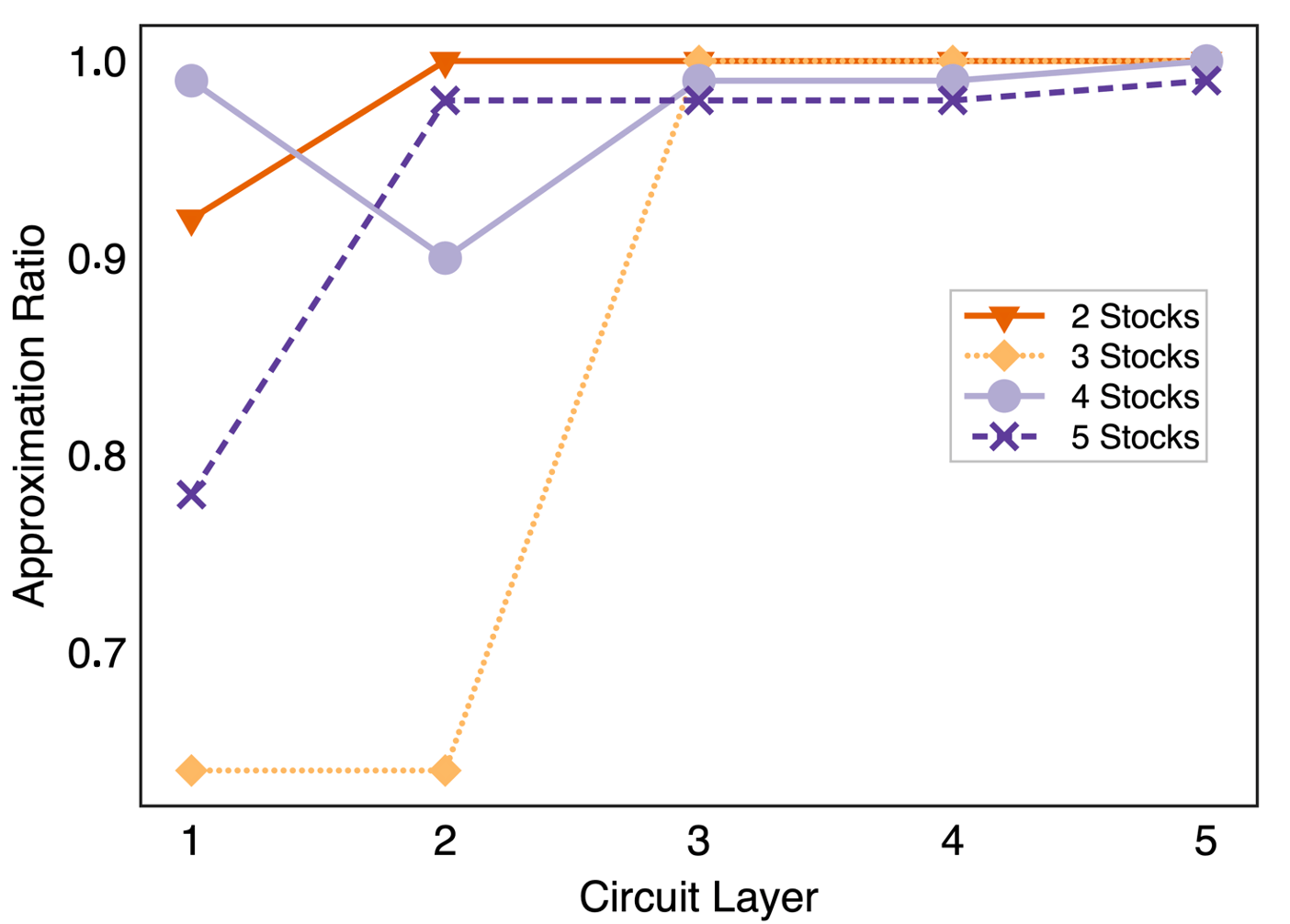

Circuit layer: Figure 6 shows that as the circuit layer increases beyond the initial value of , the approximation ratio of the diverse portfolio optimization result consistently reaches an impressive result ranging from from 100% to 98%, categorically based on the setup cases of portfolio optimization. This empirical evidence emphatically establishes that our performance consistently produces an efficient result even at some circuit layers.

Figure 6: Approximation ratio of the circuit layer is – across all problems. Remarkably, when the, the approximation ratio reaches 100%, indicating that the proposed method is efficient even at the lower circuit layer.

-

•

Trotter step count in QWM-QAOA: We aimed to find the parameter , representing the trotter step counts in the QWM–QAOA algorithm while maintaining a constant circuit layer of and optimize , for the resulting circuit of –. Table 2 shows that the approximation ratio for various stock selections increasingly exhibits a better result starting from , ranging from 99% to 97%. Finally, when , we obtained an efficient optimization results from our proposed method ranging from 100% to 98%.

Table 2: Number of trotters step of QWM–QAOA from to , followed by the corresponding approximation ratio; results emphasize the importance of careful consideration when selecting the trotter step count, as it can significantly impact the approximation ratio. # Stocks =1 =2 =3 =4 =5 2 1 1 0.99 1 1 3 0.99 0.61 0.99 0.99 1 4 0.99 0.99 0.99 0.99 0.99 5 0.80 0.97 0.97 0.98 0.98

6 Discussion and Conclusion

We empirically investigate the effectiveness of quantum computing techniques in portfolio optimization. We transform the portfolio optimization problem into a knapsack-based portfolio optimization and employ QWM–QAOA as the optimization method. Table 1 summarizes the data, including the number of stocks and required qubits, and outlines the direct relationship between stock count and qubit requirements. Furthermore, we compared our results with those of conventional optimization BKS to ensure the accuracy of our optimal solution. Optimization was performed under three different scenarios (Figure 5). Our proposed method achieves efficient results in noiseless and fake device settings, ranging from100% to 98% and 98% to 80%. However, in noisy real device conditions, the fidelity notably drops to approximately 50%, ranging from 50%, due to errors, indicating the potential for further research in error mitigation techniques. Moreover, we investigated the effectiveness of the proposed method using circuit layer analysis (Figure 6). The proposed method yields a result of 100% to 98% with from various portfolio optimization scenarios and – stocks. Table 2 emphasizes the critical role of selecting the number of trotter set counts in QWM–QAOA optimization. Consequently, with , our approximation ratio reaches an impressive value between 100% and 98%.

Finally, by extending the experimentation to larger stock configurations of – in the case of knapsack-based portfolio optimization using the QWM–QAOA technique, we aim to contribute valuable insights into the applicability and efficiency of the proposed approach across a broader spectrum of portfolio sizes. This research augments our understanding of the capacity of quantum computing. In particular, our proposed method improves portfolio optimization, especially concerning the knapsack-based problem and financial domain. In the future, we intend to extend the proposed method using large data by designing an error mitigation technique to enhance the potential of our current work.

Acknowledgements.

This work was supported by a Research Grant of Pukyong National University(2023).References

- Abidin (2017) Abidin S (2017) Greedy approach for optimizing 0-1 knapsack problem. Communications 7:1–3, https://doi.org/10.5120/CAE2017652675

- Alam et al (2019) Alam M, Ash-Saki A, Ghosh S (2019) Analysis of quantum approximate optimization algorithm under realistic noise in superconducting qubits. arXiv: Quantum Physics https://doi.org/10.48550/arXiv.1907.09631

- Aleksandrowicz et al (2019) Aleksandrowicz G, Alexander T, Barkoutsos P, Bello L, Ben-Haim Y, Bucher D, Cabrera-Hernández FJ, Carballo-Franquis J, Chen A, Chen CF, et al (2019) Qiskit: An open-source framework for quantum computing. Accessed on: Mar 16, https://doi.org/10.5281/ZENODO.2562111

- Anagnostopoulos and Mamanis (2010) Anagnostopoulos KP, Mamanis G (2010) A portfolio optimization model with three objectives and discrete variables. Computers & Operations Research 37(7):1285–1297, https://doi.org/10.1016/j.cor.2009.09.009

- Anton Abdulbasah Kamil and Kok (2006) Anton Abdulbasah Kamil CYF, Kok LK (2006) Portfolio analysis based on markowitz model. Journal of Statistics and Management Systems 9(3):519–536, https://doi.org/10.1080/09720510.2006.10701221

- Ausiello et al (1999) Ausiello G, Crescenzi P, Gambosi G, Kann V, Marchetti-Spaccamela A, Protasi M (1999) Combinatorial optimization problems and their approximability properties. Complexity and Approximation Springer-Verlag https://doi.org/10.1007/978-3-642-58412-1

- Awasthi et al (2023) Awasthi A, Bär F, Doetsch J, Ehm H, Erdmann M, Hess M, Klepsch J, Limacher PA, Luckow A, Niedermeier C, et al (2023) Quantum computing techniques for multi-knapsack problems. arXiv preprint arXiv:230105750 https://doi.org/10.48550/arXiv.2301.05750

- Borle et al (2021) Borle A, Elfving VE, Lomonaco SJ (2021) Quantum approximate optimization for hard problems in linear algebra. SciPost Phys Core 4:031, https://doi.org/10.21468/SciPostPhysCore.4.4.031

- Brandhofer et al (2022) Brandhofer S, Braun D, Dehn V, Hellstern G, Hüls M, Ji Y, Polian I, Bhatia AS, Wellens T (2022) Benchmarking the performance of portfolio optimization with qaoa. Quantum Information Processing 22(1):25, https://doi.org/10.1007/s11128-022-03766-5

- Chawla et al (2023) Chawla P, Singh S, Agarwal A, Srinivasan S, Chandrashekar C (2023) Multi-qubit quantum computing using discrete-time quantum walks on closed graphs. Scientific Reports 13(1):12078, https://doi.org/10.1038/s41598-023-39061-1

- Chen et al (2023) Chen B, Wu H, Yuan H, Wu L, Li X (2023) Quantum portfolio optimization: Binary encoding of discrete variables for qaoa with hard constraint. arXiv preprint arXiv:230406915 https://doi.org/10.48550/arXiv.2304.06915

- Chu and Beasley (1998) Chu PC, Beasley JE (1998) A genetic algorithm for the multidimensional knapsack problem. Journal of heuristics 4:63–86, https://doi.org/10.1023/A:1009642405419

- Crooks (2018) Crooks GE (2018) Performance of the quantum approximate optimization algorithm on the maximum cut problem. arXiv preprint arXiv:181108419 https://doi.org/10.48550/arXiv.1811.08419

- Dam et al (2021) Dam Wv, Eldefrawy K, Genise N, Parham N (2021) Quantum optimization heuristics with an application to knapsack problems. In: 2021 IEEE International Conference on Quantum Computing and Engineering (QCE), pp 160–170, https://doi.org/10.1109/QCE52317.2021.00033

- Delahaye et al (2019) Delahaye D, Chaimatanan S, Mongeau M (2019) Simulated annealing: From basics to applications. Handbook of metaheuristics pp 1–35, https://doi.org/10.1007/978-3-319-91086-4_1

- Du and Pardalos (1998) Du D, Pardalos PM (1998) Handbook of combinatorial optimization, vol 4. Springer Science & Business Media

- Endres et al (2018) Endres SC, Sandrock C, Focke WW (2018) A simplicial homology algorithm for lipschitz optimisation. Journal of Global Optimization 72:181–217, https://doi.org/10.1007/s10898-018-0645-y

- Farhi et al (2014) Farhi E, Goldstone J, Gutmann S (2014) A quantum approximate optimization algorithm. arXiv preprint arXiv:14114028 https://doi.org/10.48550/arXiv.1411.4028

- Gaur et al (2023) Gaur B, Humble T, Thapliyal H (2023) Noise-resilient and reduced depth approximate adders for nisq quantum computing. https://doi.org/10.1145/3583781.3590315

- de la Grand’rive and Hullo (2019) de la Grand’rive PD, Hullo JF (2019) Knapsack problem variants of qaoa for battery revenue optimisation. arXiv preprint arXiv:190802210 https://doi.org/10.48550/arXiv.1908.02210

- Gunjan and Bhattacharyya (2023) Gunjan A, Bhattacharyya S (2023) A brief review of portfolio optimization techniques. Artificial Intelligence Review 56(5):3847–3886, https://doi.org/10.1007/s10462-022-10273-7

- Herman et al (2023) Herman D, Googin C, Liu X, Sun Y, Galda A, Safro I, Pistoia M, Alexeev Y (2023) Quantum computing for finance. Nature Reviews Physics 5(8):450–465, https://doi.org/10.1038/s42254-023-00603-1

- Honggang et al (2009) Honggang W, Liang M, Huizhen Z, Gaoya L (2009) Quantum-inspired ant algorithm for knapsack problems. Journal of Systems Engineering and Electronics 20(5):1012–1016

- Johnstun and Van Huele (2021) Johnstun S, Van Huele JF (2021) Understanding and compensating for noise on IBM quantum computers. American Journal of Physics 89(10):935–942, https://doi.org/10.1119/10.0006204

- Kea et al (2023) Kea K, Huot C, Han Y (2023) Leveraging knapsack qaoa approach for optimal electric vehicle charging. IEEE Access 11:109964–109973, https://doi.org/10.1109/ACCESS.2023.3320800

- Kleywegt and Papastavrou (1998) Kleywegt AJ, Papastavrou JD (1998) The dynamic and stochastic knapsack problem. Operations research 46(1):17–35, https://doi.org/10.1287/opre.46.1.17

- Lai et al (2019) Lai X, Hao JK, Yue D (2019) Two-stage solution-based tabu search for the multidemand multidimensional knapsack problem. European Journal of Operational Research 274(1):35–48, https://doi.org/10.1016/j.ejor.2018.10.001

- Loke et al (2023) Loke ZX, Goh SL, Kendall G, Abdullah S, Sabar NR (2023) Portfolio optimization problem: A taxonomic review of solution methodologies. IEEE Access 11:33100–33120, https://doi.org/10.1109/ACCESS.2023.3263198

- Mansini et al (2015) Mansini R, ‚odzimierz Ogryczak W, Speranza MG, of European Operational Research Societies ETA (2015) Linear and mixed integer programming for portfolio optimization

- Markowitz (1976) Markowitz HM (1976) Markowitz revisited. Financial Analysts Journal 32(5):47–52, https://doi.org/10.2469/faj.v32.n5.47

- Marsh and Wang (2019) Marsh S, Wang J (2019) A quantum walk-assisted approximate algorithm for bounded np optimisation problems. Quantum Information Processing 18:1–18, https://doi.org/10.1007/s11128-019-2171-3

- Martello and Toth (1987) Martello S, Toth P (1987) Algorithms for knapsack problems. North-Holland Mathematics Studies 132:213–257, https://doi.org/10.1016/S0304-0208(08)73237-7

- Martello et al (1999) Martello S, Pisinger D, Toth P (1999) Dynamic programming and strong bounds for the 0-1 knapsack problem. Management Science 45(3):414–424, https://doi.org/10.1287/mnsc.45.3.414

- Martin (2021) Martin RA (2021) Pyportfolioopt: portfolio optimization in python. Journal of Open Source Software 6(61):3066, https://doi.org/10.21105/joss.03066, https://doi.org/10.21105/joss.03066

- Pradhan et al (2014) Pradhan T, Israni A, Sharma M (2014) Solving the 0–1 knapsack problem using genetic algorithm and rough set theory. In: 2014 IEEE International Conference on Advanced Communications, Control and Computing Technologies, pp 1120–1125, https://doi.org/10.1109/ICACCCT.2014.7019272

- Saxena et al (2023) Saxena A, Mancilla J, Montalban I, Pere C (2023) Financial Modeling Using Quantum Computing: Design and manage quantum machine learning solutions for financial analysis and decision making. Packt Publishing Ltd

- Schäfer et al (2021) Schäfer LE, Dietz T, Barbati M, Figueira JR, Greco S, Ruzika S (2021) The binary knapsack problem with qualitative levels. European Journal of Operational Research 289(2):508–514, https://doi.org/10.1016/j.ejor.2020.07.040

- Shunza et al (2023) Shunza J, Akinyemi M, Yinka-Banjo C (2023) Application of quantum computing in discrete portfolio optimization. Journal of Management Science and Engineering https://doi.org/10.1016/j.jmse.2023.02.001

- Speidell et al (1989) Speidell LS, Miller DH, Ullman JR (1989) Portfolio optimization: A primer. Financial Analysts Journal 45(1):22–30, https://doi.org/10.2469/faj.v45.n1.22

- Vaezi et al (2019) Vaezi F, Sadjadi SJ, Makui A (2019) A portfolio selection model based on the knapsack problem under uncertainty. PLOS ONE 14:1–19, https://doi.org/10.1371/journal.pone.0213652

- Weinstein et al (2001) Weinstein YS, Pravia MA, Fortunato EM, Lloyd S, Cory DG (2001) Implementation of the quantum fourier transform. Phys Rev Lett 86:1889–1891, https://doi.org/10.1103/PhysRevLett.86.1889

- Zawalska and Rycerz (2023) Zawalska J, Rycerz K (2023) Solving the traveling salesman problem with a hybrid quantum-classical feedforward neural network. In: Wyrzykowski R, Dongarra J, Deelman E, Karczewski K (eds) Parallel Processing and Applied Mathematics, Springer International Publishing, Cham, pp 199–208

- Zhou et al (2020) Zhou L, Wang ST, Choi S, Pichler H, Lukin MD (2020) Quantum approximate optimization algorithm: Performance, mechanism, and implementation on near-term devices. Phys Rev X 10:021067, https://doi.org/10.1103/PhysRevX.10.021067